Introduction

Private capital will play a pivotal role in decarbonization of the global economy, filling the multitrillion-dollar financing gap between what governments provide and what is needed to transform global industrial and energy systems.Footnote 1 Capital markets drive innovations in green technology by incentivizing new ventures and lowering barriers to entry, and advance existing clean energy solutions towards broader deployment.Footnote 2 Yet it is not clear if capital can drive “brown-to-green” transitions, where carbon-intensive incumbents in the fossil fuel sector switch towards decarbonized business models. Given the outsize footprint of this sector in driving climate changeFootnote 3 and in obstructing climate policy,Footnote 4 it is important to understand whether capital markets can advance the clean energy transition in polluting firms.

Existing work emphasizes the role of shareholders and investor advocacy groups in pressuring oil, gas, and coal firms to address their negative climate effects.Footnote 5 Much of this pressure comes from advocates and investors with long time horizons, who see value and diminished risk in pro-climate strategies that avoid asset stranding.Footnote 6 There is mixed evidence on the effectiveness of investor pressure, however, as some see investors successfully driving firms away from fossil assetsFootnote 7 while others find that climate outcomes are worse in firms facing the greatest investor pressure.Footnote 8 A separate literature views firms as strategic actors in using pro-climate behavior to gain advantage over competitors in accessing capital and growing market share or to preempt regulation by policymakers, thereby minimizing the role of stakeholder pressure altogether.Footnote 9

Building on theories of firm behavior from economics and theories of climate politics, we propose that companies operating in contexts where climate commitments are voluntary and climate regulations are weak—such as the U.S.—are unlikely to make meaningful changes to their climate strategies, even when facing increased pressure from shareholders. In doing so, we apply the political science concept of the three faces of power to conceptualize different types of shareholder pressure, with a focus on the shareholder resolution process as a manifestation of agenda-setting power.Footnote 10 This view is based on three key assumptions: (1) in contrast to pressure to act on climate from investors with long time horizons, firms prioritize short-term profits to maximize shareholder value for investors with short horizons; (2) the costs and uncertainties of shifting to climate-friendly business models are high—particularly in carbon-intensive sectors; and (3) without mandatory regulations, firms can use symbolic actions to appear responsive to climate concerns without making real operational changes. As a result, we expect that investor pressure will be unlikely to change the climate strategy of fossil fuel firms.

In testing our argument, we aim to overcome two challenges that may explain the inconsistency in existing work on the role of investor pressure. The first is measurement: existing measures of firm behavior on climate are limited in scope, focusing either on lobbying as a proxy for firm preferences for climate policy or on emissions reporting as a proxy for the climate vulnerability of firms. The second is the threat to precise identification because of selection bias: climate activists and other stakeholders target firms based on their climate performance. Some investors select on firms that perform better on climate outcomes and divest from those that perform poorly, while others target the worst offenders with the goal of transformational change.

We approach the measurement challenge by drawing on an overlooked source of data in political science using novel techniques in analyzing corporate text. We analyze the annual filings (Form 10-K) of 530 publicly-traded oil and gas companies in the U.S. over a 22-year period from 2000 to 2021.Footnote 11 These forms can substantially impact the market’s perception of a company, prompting investors, regulators, and other stakeholders to carefully examine their content to assess a company’s annual financial results and its strategy going forward. Compared to the “colorful, glossy annual reports” that companies are also required to share with investors, 10-K forms are much more heavily regulated and follow a standard structure and format, making “cheap talk” costly and subject to litigation.Footnote 12 We then fine-tune a natural language processing (NLP) model to classify text in 10-K forms to measure the climate strategies of firms based on existing measures of climate risk adopted by the Taskforce on Climate-related Financial Disclosures (TCFD).

We overcome the selection problem in identifying the effect of shareholder pressure by examining an exogenous shock whereby investors with long time horizons became better positioned relative to short-horizon investors to exert shareholder pressure over firms. In September 2020, the Securities and Exchange Commission (SEC) amended Rule 14a-8 of the Exchange Act of 1934 to raise the bar for filing shareholder resolutions—proposals for changes in corporate governance that are voted on at annual meetings—from shareholders that held $2,000 of stock for at least one year to shareholders that have held $2,000 of stock for at least three years or $25,000 for at least one year. This change meant that short-horizon investors (e.g. high-frequency traders) were no longer eligible to file shareholder proposals. This made long-horizon investors (e.g., institutional investors and pension funds) relatively more empowered in pressuring firms because they maintained the ability to file shareholder resolutions. As a result, the SEC rule change created a sudden shift in potential exposure for increased pressure from long-horizon investors, who will see greater value in climate strategy, relative to short-horizon investors.

Using a difference-in-differences approach, we find that while the rule change did lead to more empowerment in terms of the number of proposed shareholder resolutions on climate, there are limited effects on firm climate strategies of increased exposure to this pressure. For all but one measure of climate strategy, there is no distinguishable difference in climate strategies between firms that were and were not exposed to the change in shareholder power resulting from the SEC’s amendments to Rule 14a-8. Where we find positive effects are in firms’ announcements of net zero goals. We view this as a relatively weak signal of climate strategy when compared to governance reforms and detailed transition timelines and targets. A case study of the largest firm in our sample, ExxonMobil, shows that despite shareholder pressure through direct communication, filed resolutions, and media campaigns, climate-motivated investors are unable to overcome internal stakeholder resistance.

By conceptualizing firms’ climate behavior as a strategic response, our study provides new contributions to the literature on the politics of environmental governance in the context of strategic variation in firm behavior.Footnote 13 We show that, because of the power of resistant internal stakeholders, shareholder pressure by itself is not a sufficient condition for improved corporate responsibility. This is in line with regulatory theory that solving asymmetries between firms and governments in the context of complex information requires regulations and enforcement of voluntary behavior through monitoring and litigation.Footnote 14 Ultimately, in contexts such as the U.S. where climate regulation is minimal and firms are not subject to mandatory disclosure requirements, policy will have to play an important role for “brown-to-green” transitions to occur.

Theory

What is climate strategy?

We first define climate strategy as a firm’s plan to identify and manage the risks stemming from climate change. These risks can be physical—e.g., asset damage from extreme weather events—or they can be “transitional” risks, which encompass how policies related to climate mitigation are likely to materially impact a firm’s businesses, operations, or financial condition.Footnote 15 The latter depends on a firm’s emissions footprint as well as its ability to generate revenue in a carbon-constrained market. The more that a company is doing to mitigate both kinds of risks—through detailed adaptation plans and a viable transition away from fossil fuels—the stronger will be its climate strategy.

As climate strategy includes a broad range of firm activities, we use global standards developed by the TCFD and the SEC, which gauge a firm’s climate strategy through its disclosure of climate-related information. This includes, but is not limited to, the disclosure of climate-related risks, detailed data on emissions, how a firm responds to climate risks and climate impacts, the adoption of a transition plan, progress towards climate-related targets, and the role of management in overseeing these efforts. We provide more information on measurement below and in Appendix A and Table A2.

A theory of limited shareholder pressure on firm climate strategy

How shareholders exert pressure

We theorize that fossil fuel firms operating under conditions of voluntary climate commitments and weak regulations will show limited meaningful operational change in their climate strategy, even when subject to increased shareholder pressure on climate. The theory rests on three core assumptions: the short-term profit-maximizing behavior of firms, the high and uncertain costs of substantive change, and the availability of strategic tools that allow firms to respond symbolically via distinct disclosure strategies. First, firms are rational business actors seeking to maximize shareholder value, which, in the U.S. context, is interpreted through short-term financial allowances.Footnote 16 Second, the short-term costs of changing business models to meet long-term climate goals are high, uncertain, and politically contentious in carbon-intensive industries.Footnote 17 Third, in the absence of binding mandates, firms possess strategic tools to respond to shareholder demands without incurring economic or operational costs.Footnote 18 While the geographic focus of our theory is centered in the U.S., in the conclusion we consider how the theory would apply in other contexts.

We begin by considering the sources of shareholder pressure. The most likely to exert pressure on firms to adopt climate strategies, and thus the primary source of climate-related pressure, are investors with relatively long time horizons, who see future value creation in mitigating physical and transitional climate risks to the firm and possibly maximizing gains created by the firm’s early positions on pro-climate business models.Footnote 19 Shareholders with long time horizons will demand more climate strategy, and will “pay” for this information by maintaining their investment or interest in the company (i.e., not divesting or boycotting its products). Such payment also takes the form of stakeholders amplifying signals that the firm is worthy of engagement by other investors, suppliers, and consumers.Footnote 20

Conditional on these sources of pressure, how does shareholder pressure manifest in practice? Investors attempt to pressure firms through a range of tools, including voting on proposals, submitting resolutions, and engaging in private negotiations. This body of research has largely focused on tactical mechanisms of engagement.Footnote 21 While the effectiveness of these tools has been studied and found to vary, we contend that broader conceptualization of shareholder pressure has been missing, and that less visible types of targeting areas such as disclosure have therefore been overlooked.Footnote 22 These include efforts to shape what climate issues appear on the corporate agenda, how climate risks are perceived, how expectations about disclosure are normalized in financial markets, and what firms eventually do in response.

Building on recent work seeking to conceptualize the impacts of business-related pressure on climate reform,Footnote 23 we believe that political science can provide a broader conceptualization of shareholder power to help distill how pressure can be exercised, resisted, or even neutralized beyond formal engagement. To elucidate shareholder power, we apply the well-established concept of the three faces of power—direct control, agenda setting, and preference shapingFootnote 24 —to theorize shareholder influence and extend corporate governance research beyond the study of tactics alone. Applying this framework allows us to focus attention on both how investors influence and where that influence is targeted.

Shareholders that seek direct control essentially aim to challenge managerial authority, often through changing the composition of board leadership; here, the target of influence is ultimately the highest levels of internal decision-making. Shareholders may also engage in agenda setting by pushing both internal and external stakeholders for the persistent elevation of climate risks within corporate discourse, whether through repeated proposals, resolutions, or informal engagements or signaling. Finally, investors who are keen on driving deeper changes within corporate discourse may engage in preference shaping by integrating climate risk into investment logic to influence firms’ strategy or reinforcing the idea that climate responsibility aligns with long-term shareholder value, similar to the legacy of socially responsible investing and philanthropy.

Yet we expect that these dimensions of power, while potentially targeting core business interests, will not yield substantive responses from firms. In a voluntary disclosure regime where institutions reward the appearance of compliance, firms may appear responsive while preserving the status quo. Meaningful change would require disrupting the deeper institutional and procedural mechanismsFootnote 25 through which contestation is suppressed and prevailing norms are kept intact, such as the use of “no-action” letters.Footnote 26 With that in mind, why and how should we expect shareholder pressure to produce any change in firm behavior at all?

Firms may respond to pressure due to both financial and social motivations.Footnote 27 On the one hand, institutional investors view climate risks as financially material and demand more climate resilience to protect long-term value. On the other hand, firms may comply with pressure to align with broader social norms, particularly when those norms are diffused by influential investors or strong institutional environments such as the E.U.Footnote 28 ; exiting such an environment can weaken firms’ incentives to maintain responsible climate strategy.Footnote 29 In addition, U.S.-based firms operate within a regulatory environment where external pressure is visible and reputational risk is high, yet concrete regulatory climate-related requirements remain weak.

The climate disclosure market, while offering some economic returns, remains marginal. Nonetheless, it can still create strategic and economic incentives for some industries to engage in climate disclosure, not to radically reinvent business models but to manage risksFootnote 30 or to gain reputational benefits through signaling.Footnote 31 Such reputational benefits can be considerable, and at times large enough to persuade a firm to deviate from its industry norms or from status quo behavior by other firms.Footnote 32 There are also global market pressures, such as emissions-based trade policies and carbon border adjustments, which create differing economic incentives for multinational U.S-based firms.Footnote 33

How firms respond to shareholder pressure

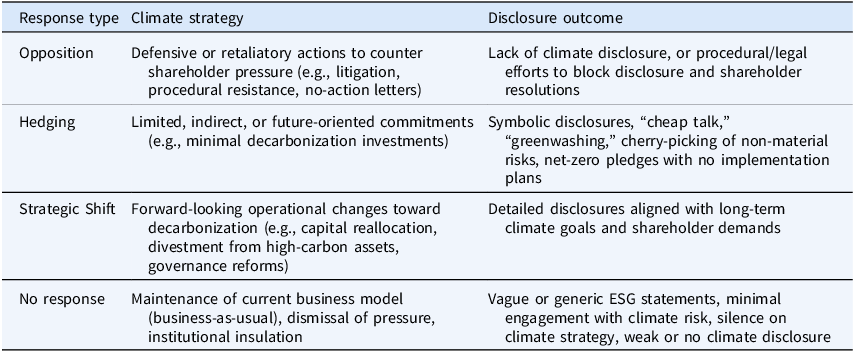

We outline a typology of potential firm behaviors in order to understand corporate responses to shareholder pressure. Here, we build on Meckling’s (Reference Meckling2015) typology of opposition, hedging, support, and nonparticipation. We modify this framework to categorize firm reactions to shareholder pressure into four broad types: (1) defensive or retaliatory responses to directly counter pressure; (2) reallocation of resources or subtle diversion away from pressure points, which may range from overt to low-level repositioning for internalizing shallow decarbonization within the business model, such as through large-scale investments in carbon capture technology; (3) strategic changes indicating meaningful shifts to deep decarbonization, such as mergers, acquisitions, or large-scale investments; and (4) business as usual (BAU), including non-response or minimal symbolic actions to signal compliance.Footnote 34

In Table 1, we map these four types of responses onto distinct climate strategies and associated disclosure outcomes—the ways firms use disclosure to either communicate or obscure their reactions to shareholder pressure. We anticipate that opposition as a climate strategy will likely include lack of climate disclosure overall, in addition to inclusion of legal and procedural strategies to exclude climate-related proposals through no-action letters, such as the case of ExxonMobil v. Arjuna.Footnote 35

Typology of firm climate strategies and disclosure patterns

We anticipate future-oriented limited commitments and some capital reallocations to map onto a form of hedging, in which firms may acknowledge climate concerns while committing only limited or indirect resources. These disclosures may refer to obscure net-zero pledges without detailed implementation plans; symbolic or low-risk investments; or internal restructuring without operational shifts.Footnote 36

We expect strategic changes correspond to a supportive disclosure strategy, in which firms communicate alignment with shareholder demands. These disclosures are typically detailed and forward-looking, indicating meaningful shifts toward deep decarbonization, mergers or acquisitions, or governance reforms that reflect with long-term climate goals. We do not expect to find these disclosures in our corpora.

Finally, BAU responses are likely to include minimal engagement with pressure in public disclosure and almost no change in addressing climate risks. These firms rely on vague and generic statements that repeat industry-standard Environmental, Social, and Governance (ESG) language. This language can overlap with hedging.

While external pressure can—and, as evidence shows—does create palpable shifts in firm behavior, such as ESG policy adoption or increased Corporate Social Responsibility performance, these changes tend to be declarative and do not necessarily translate into substantive strategic shifts when measured at the rigorous level of corporate behavior.Footnote 37 Consider, for example, a firm’s inclusion in an ESG index or the adoption of sustainability policy may signal responsiveness to investor demands, yet these symbolic acts differ fundamentally from the operational and financial realities captured in corporate earnings calls or legally binding disclosures as 10-K filings.Footnote 38 In short, these documents are more accurate in revealing core business priorities and risk assessments. They have the potential to shed light on a gap between performative compliance and implemented climate strategy.

This divergence between rhetoric and action suggests both a measurement problem and a strategic gap between perceived shareholder influence and corporate behavior, as shown in the typology of disclosure patterns (Table 1). Organizational-level response, such as a net-zero pledges, may create the appearance of alignment with climate goals on the surface, but fail to translate into material strategic corporate shifts in decarbonization strategy.

While stakeholder power and applied pressure are becoming more visible—amplified by increases in resolutions and campaigns—we expect stakeholders’ pressure to remain structurally limited in its capacity to disrupt entrenched business models. Shareholder proposals, for example, may raise awareness or apply reputational pressure, but they rarely overcome management resistance.Footnote 39 Because of this limitation, we view shareholder pressure as a contingent and often symbolic form of corporate governance in the context of a voluntary disclosure regime. This idea lies at the core of our theoretical argument: shareholder pressure is more often absorbed as symbolic compliance than converted into substantive climate strategy, leading to hedging and/or business-as-usual.

How oil firms stymie shareholder pressure

We now turn to the specific means through which firms in the oil and gas industry in the U.S. respond to shareholder pressure through climate strategy. We identify three means through which firms absorb or resist shareholder pressure: (1) managerial control over value-maximization, (2) managerial short-termism and emphasis of climate risks’ uncertainty, and (3) procedural suppression of shareholder influence.

Managerial control over value-maximization. While management is often seen as responding to pressure, the substance and scope of its responses remain inconsistent. Management might develop “genuine” preferences for environmental regulation when they see benefits but still adopt opposition or business-as-usual strategies due to coalition standing and peer pressure.Footnote 40 In theory, firms should respond to pressure when the demanded change maximizes profits and shareholder returns.Footnote 41 In that regard, shareholder value maximization should direct a firm’s management in fulfilling its fiduciary duty to act in shareholders’ interests, be it major changes like board takeovers or more risk-averse hedging activities.Footnote 42 This varies across markets, with the United States presenting a prime example of prioritizing immediate investor interests, given the default favorable position of investors relative to management. As a result, resistance to long-term shareholder pressure is expected to take precedence over long-term climate considerations.

Managerial short-termism and climate risks’ uncertainty. As oil and gas firms are increasingly exposed to climate change and climate policies, shareholders seek greater disclosure of these risks. Yet internal stakeholders have pushed back on the scale of these risks, as these are perceived to be too far into the future and highly uncertain.Footnote 43 Evidence from internal fossil fuel industry strategy documents points to this being the case: management does not have long enough time horizons to consider climate risks a serious threat to their business-as-usual operations.Footnote 44 Public-facing energy models from the oil majors continue to see a large role for hydrocarbons in the world’s future energy mix,Footnote 45 in stark contrast to models that incorporate long-term climate policy environments showing little room for investments in oil and gas projects beyond 2030.Footnote 46 As a result, firms are more likely to engage in political hedging—“performing” symbolic decarbonization efforts rather than implementing business decisions to transition away from fossil fuels.

Procedural suppression of shareholder influence. Beyond strategic communication shaped by management’s short-termism, firms rely on procedural tools to limit shareholder influence. A central mechanism is the use of SEC Rule 14a-8 “no-action” letters to exclude resolutions from appearing on proxy ballots.

Since firms have a strategic tool to absorb, deflect, or hedge external demands without changing their core business model, the power of pressure does not lead to increased operational changes. So simply increasing the power of pressure does not lead to increased operational changes, as firms continue to avoid substantive shifts in their climate strategy. Because response is itself not procedurally required—nearly all shareholder resolutions are non-binding—the absence of regulatory mandated disclosure allows firms to signal responsiveness through non-enforceable, forward-looking commitments such as net-zero pledges.

The role of time horizons in firm responses

These mechanisms explain how pressure is absorbed or blocked; however, they do not explain which firms shift, hedge, or resist. Our theory suggests firms in the oil and gas sector operationalize these response strategies in practice through distinct disclosure strategies. Building on the typology outlined in Table 1, we explore how investor pressures shape firms’ choices along this response range.

In theorizing shareholder preferences, we build on the literature on time horizons and climate action.Footnote 47 Long-horizon investors, such as pension funds and family-owned or family-controlled firms concerned with legacy, are more likely to press for meaningful, forward-looking climate action that reduces long-term risks to firm value. In contrast, short-horizon investors, such as hedge funds and traders, apply pressure focused on near-term financial returns, which can discourage substantive changes that might carry short-term costs. Decarbonization is risky for short-term gains, so firms face divergent pressures and respond in accordance with their ownership composition.

If pressure threatens direct control of management, for example through board replacement, firms are more likely to “oppose,” even if management itself has long time horizons and shares investor perceptions of the seriousness of climate risks. Such threats challenge management’s autonomy and internal stakeholder power, and firms will respond with unequivocal resistance to a loss of power.

For pressure that manifests as agenda-setting, response types depend on shareholder horizons. From the perspective of the expectation of fiduciary duty,Footnote 48 firms should respond to pressure by an investor with actions that would benefit the broader composition of shareholders. For firms dominated by short-horizon investors, management seeks to satisfy those whose interests the firm perceives as its primary obligation.Footnote 49 Such a firm will be unlikely to shift its strategy, maintaining “business-as-usual” (BAU). Firms predominantly owned by long-horizon investors should in theory act on their interests and adopt meaningful shifts in strategy in response to pressure. In practice, firms would only adopt this shift if their own preferences are internalized towards decarbonization, which would result from shareholder pressure that manifests as preference-shaping. Firms with a mix of long- and short-horizon investors face the challenge of placating both camps, and will likely respond to pressure by “hedging.”

These mechanisms—the balance of long-term versus short-term investor horizons, coupled with whether management perceives a threat to its control—help explain heterogeneity in firm responses to shareholder pressure: why some firms shift, some hedge, and others resist or ignore pressure altogether. While we speculate on these mechanisms across all responses, we limit our empirical tests of the mechanism to the “opposition” response through a case study of ExxonMobil in section “Internal stakeholder resistance: The case of ExxonMobil,” where initial governance changes in response to shareholder pressure were later followed by strategic opposition through litigation.

Theoretical expectations

Here we return to our conceptualization of shareholder power. In principle, the three faces—direct control, agenda-setting, and preference-shaping—can alter corporate climate strategy. However, our argument is that these forms of pressure are, in effect, “filtered” through firms’ internal power structures and time horizons. Direct control (e.g., replacing board members) triggers managerial resistance, irrespective of time horizons.Footnote 50 Agenda-setting power (e.g., filing resolutions) is neutralized through no-action letters filed by firms, selective transparency leading to symbolic disclosure, or maintaining BAU. Preference-shaping, the deepest and most material form of influence—where firms internalize and act upon shareholder demands—has yet to be seen in the oil industry.Footnote 51

Importantly, even when pressure originates from long-horizon investors, we expect firms in the oil and gas sector to see their overall investor base as either short-term oriented or mixed in horizons. In combination with high management resistance to disrupt entrenched business models, we therefore derive the following expectation: firms exposed to increased pressure are more likely to respond by hedging or maintaining business-as-usual than to report material changes in business strategy or operations. When management does not perceive a direct threat to control, increased shareholder pressure interacts with the firm’s management climate risks perceptions: overall, firms are more likely to absorb or deflect pressure than to shift strategy, leading to anti-climate behavior through means we describe in section “How oil firms stymie shareholder pressure.”

In Figure 1, we summarize firms’ responses as a function of various types of pressure: Hedging and BAU responses are likely to originate from agenda-setting pressure; Opposition will follow any attempts to directly control management; and Strategic shift will follow from preference-shaping pressure.

Hypothetical firm responses to shareholder pressure conceptualized using the three faces of power on climate strategy. The diagram illustrates pathways toward four types of firm response—opposition, business-as-usual, hedging, and strategic shift. Arrows illustrate the anticipated firm response to shareholder pressure. Dashed arrows between responses illustrate the coarse and overlapping nature of firms’ responses; note that firms may pursue multiple strategies simultaneously.

Measuring climate strategy using investor-facing reports

Indicators of climate strategy

To evaluate this argument, we focus on the climate-related disclosures of oil and gas firms publicly traded on U.S. market. We source our data from the SEC’s EDGAR system, specifically focusing on companies in the oil and gas sector identified by the Standard Industrial Classification (SIC) code 1311 and 2911. The dataset consists of annual 10-K forms submitted by U.S.-based firms for fiscal years from 2000 to 2021.

We use three benchmarks to evaluate the climate strategy of firms. First, we use TCFD recommendations structured around Governance, Strategy, Risk Management, and Metrics & Targets. Second, we use the March 2024 ruling by the SEC on climate-related disclosure, which are informed by the TCFD guidelines and the Greenhouse Gas Protocol.Footnote 52 SEC standards include disclosures such as exposure to physical and transition climate risks, management oversight, climate-related targets, transition plans’ progress, cost, and time horizons. Third, we use a component based on whether firms have announced net zero and emissions reduction targets.Footnote 53

Measuring climate disclosure using NLP tools

While the general transformer-based Bidirectional Encoder Representations from Transformers (BERT) modelFootnote 54 has been used on downstream text classification tasks, research from the NLP literature has shown that general-purpose models do not perform well on niche financial lexicon and climate-related texts.Footnote 55 Recently, a growing number of pre-trained models and analysis, such as ClimateBERT and ESGBERT, have emerged specifically for tackling corporate climate-related tasks and broadly across political texts.Footnote 56 We use two existing models to measure the four TCFD indicators and the two components of net-zero and emissions-reduction disclosures.

To locate firms’ climate strategy based on the SEC’s disclosure ruling, we develop an original downstream task transformer-based language model “EGAPE/secdisclosure-28l” that classifies paragraphs into distinct categories of climate-related risk.Footnote 57 Considering its broad application, we use the ClimateBERT language model given its high performance on downstream tasks and relevance to our niche corporate text.Footnote 58 We apply ClimateBERT to our labeled dataset to identify whether firms report specific voluntary climate-related information that describes climate risks, the financial impacts of these risks, and how firms plan to address and mitigate these risks and more. To our knowledge, this is the first attempt to obtain non-financial climate disclosure measures for a sample of U.S. fossil fuel firms, specifically based on the SEC’s proposed 2024 regulations. We provide more information on the ClimateBERT application in Appendix A.

Our approach builds on but extends earlier efforts to quantify corporate climate disclosure. Prior work used coarse measures of report content such as the percentage of numeric content in ESG reportsFootnote 59 or aggregate climate risk scores based on the length and specificity of climate-related language in 10-K filings available from Ceres/CookESG.Footnote 60 These approaches capture certain aspects of disclosure complexity, but they do not distinguish between types or components of climate strategy.

Description of the dataset used to fine-tune ClimateBERT

Investor-facing documents in the oil and gas industry contain specialized language, which existing NLP tools are unable to parse with precision. For the purpose of fine-tuning ClimateBERT, we assembled a human-coded dataset with paragraphs from 10-Ks filed by a select training set of oil and gas firms. These paragraphs were labeled in accordance with climate disclosure indicators derived from the SEC benchmark described above.Footnote 61 Overall, this dataset is composed of paragraphs labeled according to whether they relate to one of the 28 indicators we trained our model for. We use multi-label classification, which assumes that indicators can be tagged with multiple labels.Footnote 62 Our final resampled training dataset consists of 2,856 paragraphs, of which 102 are related to each label (see Appendix A for more detail).

Methodology and text classification performance

The original ClimateBERT returns a parameter for each paragraph indicating the probability that the paragraph is “climate-related.” Our goal is to get probability parameters according to the SEC categories for all paragraphs extracted from each 10-K form. Table A2 in the Appendix shows the names of each of the categories used in the model’s training.Footnote 63 Overall, our metrics suggest that the model performs well in distinguishing between classes.

Once we run the 10-K forms through our EGAPE/secdisclosure-28l model, each paragraph is individually assigned a probability score. As a result, we calculate and report maximum probabilities for each label for each firm-year observation. This is an important nuance: rather than calculating an aggregate accuracy score for an entire document or a batch of paragraphs, we assessed the accuracy of the model’s predictions at the paragraph level. Each paragraph’s probability score represents how confidently the model was able to classify it according to the predefined climate disclosure indicators. In practical terms, a high probability score for a paragraph indicates that the model is highly confident that it has been correctly labeled, falling in line with human-coded labels. Conversely, a lower score would suggest that the model is less sure about classification. Scores for each indicator are scaled to continuously range between 0 (no information about a given climate-related risk) to 1 (full information about a given climate-related risk).

Measurement model for latent climate strategy

We map the combined indicator scores using measurement models to estimate a firm-level, latent measure of climate strategy. We start with a set of firms indexed

$i = 1, \ldots, n$

(

$i = 1, \ldots, n$

(

$N = 530$

), with each providing a value for a set of climate risk indicators indexed

$N = 530$

), with each providing a value for a set of climate risk indicators indexed

$j = 1, \ldots, p$

. The likelihood of the

$j = 1, \ldots, p$

. The likelihood of the

$i$

th firm providing information related to the

$i$

th firm providing information related to the

$j$

th indicator depends on their positioning on the latent climate strategy

$j$

th indicator depends on their positioning on the latent climate strategy

${\xi _i}$

. Given the continuous nature of each indicator, we specify the latent indicator based on the standard factor analysis model (Jackman, Reference Jackman2009, 438):

${\xi _i}$

. Given the continuous nature of each indicator, we specify the latent indicator based on the standard factor analysis model (Jackman, Reference Jackman2009, 438):

$${y_{itj}}\sim {\cal N}\left( {{\xi _{it}}{\delta _j} - {\alpha _j},{\rm{\Psi }}} \right)$$

$${y_{itj}}\sim {\cal N}\left( {{\xi _{it}}{\delta _j} - {\alpha _j},{\rm{\Psi }}} \right)$$

where

${y_{itj}}$

are observed values for climate-risk indicators

${y_{itj}}$

are observed values for climate-risk indicators

$j$

for each firm

$j$

for each firm

$i$

in year

$i$

in year

$t$

, with the relationship between each indicator and the single latent variable

$t$

, with the relationship between each indicator and the single latent variable

${\xi _{it}}$

represented in terms of

${\xi _{it}}$

represented in terms of

${\delta _j}$

(discrimination) and

${\delta _j}$

(discrimination) and

${\alpha _j}$

(difficulty) parameters for each indicator

${\alpha _j}$

(difficulty) parameters for each indicator

$j$

.Footnote

64

$j$

.Footnote

64

${\rm{\Psi }}$

is a matrix of variance parameters.

${\rm{\Psi }}$

is a matrix of variance parameters.

The resulting measure for each firm over the entire time frame is shown in Figure 2. While some firms do not consistently mention climate in their disclosures every consecutive year (as reflected in the sharp valleys of some lines), on average firms are adopting relatively greater climate strategy over time. However, it is notable that no firm exhibits high climate strategy: the maximum observed value in the sample is 1.2, whereas the theoretical maximum is 2, which would indicate a firm that is aligned with all climate-related indicators. More details on specification and our estimation procedure can be found in Appendix C.

Climate strategy of oil and gas firms, 2000–2021. Each line corresponds to the latent measure of climate strategy (which ranges from −2 to +2) for each firm in the sample, with a solid black line showing the average climate strategy for each year.

Climate strategy and firm time horizons

Before turning to the analysis of how firms respond to increased exposure from shareholders with long time horizons, we first examine the correlation between shareholder time horizons and firm climate strategy. Here we rely on a proxy for investor time horizons, using a measure for average turnover: the frequency with which an investor trades shares in a given year. Investors with short time horizons will buy and sell shares with high frequency, which corresponds to high turnover. Investors with long time horizons will exhibit low frequency in trading, which corresponds to low turnover; at the extreme, such investors retain shares for decades at a time. We also use investor type as a measure of time horizons, where we categorize day-traders and hedge funds as short-horizon investors, versus pensions and institutional investors as long-horizon investors.

Using our measure of firm climate strategy and investors’ average turnover at the market level (Appendix Figure A5), we find that firms comprised of investors with shorter time horizons have lower climate strategy scores, consistent with a firm response of business-as-usual; firms comprised of mixed-horizon investors have slightly higher climate strategy scores consistent with a firm response of hedging. Given the challenges of measuring time horizons with average turnover at the firm level (see Appendix F for a discussion), we also use investor type as a proxy to find that firms with more short-horizon investors tend to have lower climate strategy scores (Appendix Table A9).

While these findings align with our theoretical expectations, the relationship between external stakeholder pressure and climate strategy is rife with endogeneity. Investors deliberately select on climate issues when deciding to invest or divest from firms. Firms with poor performance on climate are more likely to be targeted by investor activism; by contrast, some climate-conscientious shareholders reward pro-climate firms with increased investment. For these reasons, we turn to a research design in which we exploit an exogenous shock from a ruling by the SEC in 2020 that limited the power of shareholders in some firms but not others to improve our ability to infer a causal effect of shareholder pressure on climate strategies.

SEC Rule 14a-8 and the limited power of shareholder resolutions

Background

On November 5, 2019, the SEC proposed an amendment to Exchange Act Rule 14a-8 on the matter of shareholder engagement with firms through the shareholder proposal process.Footnote 65 These shareholder proposals—typically referred to as shareholder resolutions—are an essential tool for owners of a firm to request information, propose changes to company leadership, and call for changes in a company’s overall strategy. From the perspective of our theory above, we conceptualize resolutions as a form of agenda-setting power. Resolutions allow shareholders to place climate issues on the corporate docket, require a formal response from management, and thus should be treated as an observable signal of investor demands.

Proposed resolutions are then voted on by all eligible shareholders, with firms varying widely in how and whether they adopt changes based on vote results. We do not evaluate the effectiveness of passed vs. unpassed resolutions here, as we are more interested in the question of agenda-setting power that leads to these resolutions in the first place. Such resolutions have become an important battleground on climate strategy in particular, where investor activism has used resolutions to demand greenhouse gas emissions reporting and reductions as well as replacements of boards of directors.Footnote 66

The SEC’s amended rule raised the bar for which shareholders could file resolutions.Footnote 67 Prior to the amendment, any shareholder who held at least $2,000 worth of the company’s shares for at least 1 year in duration could file a resolution. After the amendment the threshold was raised and split into three tiers, summarized in Table 2. Because of the requirement to have held these values of a firm’s shares for at least 1 year (and upwards of 3 years), investors could not quickly “game the system” by buying or selling enough shares to meet the SEC’s new thresholds.

Summary of changes for shareholder eligibility to file resolutions from rule 14a-8 amendments

The rule change effectively elevated the shareholder power of large, long horizon shareholders such as institutional investors and pension funds, while restricting the power of small individual investors and high-frequency traders. As a result, it created a differential in the potential for shareholder pressure. Given that institutional investors with long time horizons are recognized as key drivers in affecting companies to decrease carbon emissions and move towards a low-carbon economy,Footnote 68 we see this shock as a test of whether increased agenda-setting power among these actors translates into changes in shareholder resolution behavior. Our analysis below confirms that the change led to an increase in proposed resolutions, though with little effect on filed resolutions (see section “SEC Rule 14a-8 led to increased resolution activity, but not successfully-filed resolutions”).

In altering who can decide what issues are open for contestation, Rule 14a-8 transformed the population of filers, effectively consolidating the capacity to initiate resolutions among long-term investors.Footnote 69 Procedurally, this shift meant a transfer of agenda-setting power away from small and short-term investors.Footnote 70 However, this reallocation was interpreted differently and contested by some stakeholders. On one side, regulators and large corporate incumbents cheered this reform as one that “would facilitate constructive engagement by long-term shareholders,”Footnote 71 who meet the SEC’s threshold for demonstrating a “meaningful ‘economic stake or investment interest’ in a company.”Footnote 72 On the other side, advocates for small shareholders criticized the change as “the most significant SEC attempt to limit shareholder rights since the commission was created,” arguing that “raising ownership filing thresholds” will restrict “the voice of small shareholders.”Footnote 73

Empirically, the rule change resulted in fewer resolutions filed by short-term investors. Using the previously-discussed measure of investor turnover, the proportion of resolutions filed by short-term investors declined from 28% in 2020 to 22% in 2021.Footnote 74 However, the number of resolutions filed by long-term shareholders only increased modestly. This confirms critiques of the rule change as taking power away from short-term investors, but also shows that the empowerment of long-term investors was therefore relative rather than absolute.

Analysis

To evaluate the effect of the rule change on decisions about climate strategy at the firm level, we assess whether there was a change in the proportion of investors who could file resolutions before and after the rule. This allows for a direct comparison between firms whose long-horizon shareholders were empowered by the 14a-8 amendment and firms whose shareholder power was unaffected by the amendment based on their pre-existing investor composition.

This enables a difference-in-differences analysis where we compare the climate strategies of firms by change in exposure to shareholder pressure. The treatment here is whether there is a difference between the proportion of shareholders who could file a resolution under the amended 14a-8 rule and the proportion who could have filed a resolution had the rule not been enacted. This is calculated at the investor level, where we first assess if an investor’s holdings in a firm throughout a given year qualify that investor to file resolutions under the prior rule and the amended rule. We then aggregate this at the firm level, based on the size of investor holdings, to estimate the percentage of a firm’s shares that are held by investors eligible to file resolutions. The amended rule was proposed in late 2019 and finalized in September 2020, so we consider 2020 and prior as the pre-treatment period and 2021 the post-treatment period. As we are examining 10-K forms, this would refer to filings made to the SEC in 2022 for the Fiscal Year ending in 2021.

Consider a firm like Unit Corp, a Tulsa-based drilling company. Looking at 2021, under the new rule investors holding 12.1% of the firm’s shares could file resolutions compared to 13.4% who could have filed resolutions had the prior rules still been in place. In this case, the amended rule created a negative 1.3 percentage-point difference—which amounts to $5 million worth of shares given the firm’s market cap in 2021—in the proportion of investors able to file resolutions. Unit Corp experienced a change in exposure to shareholder pressure, with the remaining shareholders who could file resolutions being those who have held shares at higher amounts and for a longer period of time.

More than half of the difference-in-difference sample (70 firms) experienced a negative change in exposure to shareholder pressure, with less than half (63 firms) experiencing no change in exposure to pressure. This makes the difference in exposure a one-directional measure: the rule change either had no effect or led to a decrease in the number of shareholders who could file resolutions.

To clarify how the change in exposure manifests in practice, we assess how exposure compares to time horizons. The latter is measured using an indicator for investors’ average stock turnover: a score of 1 indicates firms whose investors do not trade their shares in a given year (e.g., trusts and pensions), while 3 indicates firms whose investors never hold the same share over the course of a year (e.g., daily traders).Footnote 75 Consider Amplify Energy Corp, whose investors on average bought or sold their shares frequently (turnover = 2.3) and were ineligible to file resolutions even under the prior rule. But some of Amplify’s investors’ eligibility characteristics were near the SEC rule change cutoff: prior to the rule change, they could file a resolution but after the rule change they could not. As a result, Amplify would be in the treated group (D = 1) given its exposure to resolution-eligible firms declined because of the rule change.

In the year after the rule change, firms which experienced a change in exposure on average had investors with shorter time horizons (i.e., higher turnover), despite having a higher proportion of investors eligible to file resolutions under the rule change (Table 3).Footnote 76 In other words, the treatment here is not a direct measure of investor time horizons (which would be captured instead by turnover), nor is it a measure of exposure to long-term investors (which would be captured by filing eligibility). Rather, the treatment is a binary measure of change in exposure to long-term investors if the SEC rule change did not take place versus exposure to long-term investors under the rule change.

Exposure vs. investor composition in 2021. Change in exposure indicates whether the proportion of a firm’s investors who file a resolution was changed by reforms to SEC Rule 14a-8, categorized as either unchanged (control group) or changed (treatment group). Filing eligibility refers to the level of the proportion of investors that could file resolutions after changes to SEC Rule 14a-8. Turnover refers to a proxy measure for investor time horizons, ranging from 1 (low turnover = long time horizons) to 3 (high turnover = short time horizons)

Note:

${{\rm{\;}}^{\rm{*}}}p \lt 0.1{;\; ^{{\rm{**}}}}p \lt 0.05{;\; ^{{\rm{***}}}}p \lt 0.01$

.

${{\rm{\;}}^{\rm{*}}}p \lt 0.1{;\; ^{{\rm{**}}}}p \lt 0.05{;\; ^{{\rm{***}}}}p \lt 0.01$

.

Because we consider the difference in exposure to be exogenous to firms’ climate strategies—and the composition of qualified investors given the inability to game the rule because of duration requirements for shares held—we assume here that the treatment is as-if randomly assigned. This allows for unbiased estimation using the standard two-way fixed effects estimator, which is robust in these situations to heterogeneous effects.Footnote 77 Our research design also allows us to hold constant any potential period effects, such as the COVID-19 pandemic and its resulting shocks on shareholders and firm strategies.

With this framework in mind, we specify an estimator as follows:

$${Y_{it}} = {\beta _0} + {\beta _1}{D_{it}} + {\beta _2}{T_{it}} + {\beta _3}{D_{it}} \times {T_{it}} + {\alpha _i} + {\lambda _t} + {\varepsilon _{it}}$$

$${Y_{it}} = {\beta _0} + {\beta _1}{D_{it}} + {\beta _2}{T_{it}} + {\beta _3}{D_{it}} \times {T_{it}} + {\alpha _i} + {\lambda _t} + {\varepsilon _{it}}$$

where

${\beta _3}$

estimates the average treatment effect on firm climate strategies (

${\beta _3}$

estimates the average treatment effect on firm climate strategies (

${Y_{it}}$

) from a change in exposure to shareholder pressure (

${Y_{it}}$

) from a change in exposure to shareholder pressure (

${D_{it}}$

) as a result of the SEC amendments to Rule 14a-8 before and after 2020 (

${D_{it}}$

) as a result of the SEC amendments to Rule 14a-8 before and after 2020 (

${T_{it}}$

), along with firm (

${T_{it}}$

), along with firm (

${\alpha _i}$

) and year (

${\alpha _i}$

) and year (

${\lambda _t}$

) fixed effects. In our main specification,

${\lambda _t}$

) fixed effects. In our main specification,

${D_{it}}$

is a binary indicator equal to 1 if the SEC amendment led to a change in exposure to shareholder pressure, and 0 otherwise.Footnote

78

${D_{it}}$

is a binary indicator equal to 1 if the SEC amendment led to a change in exposure to shareholder pressure, and 0 otherwise.Footnote

78

Results

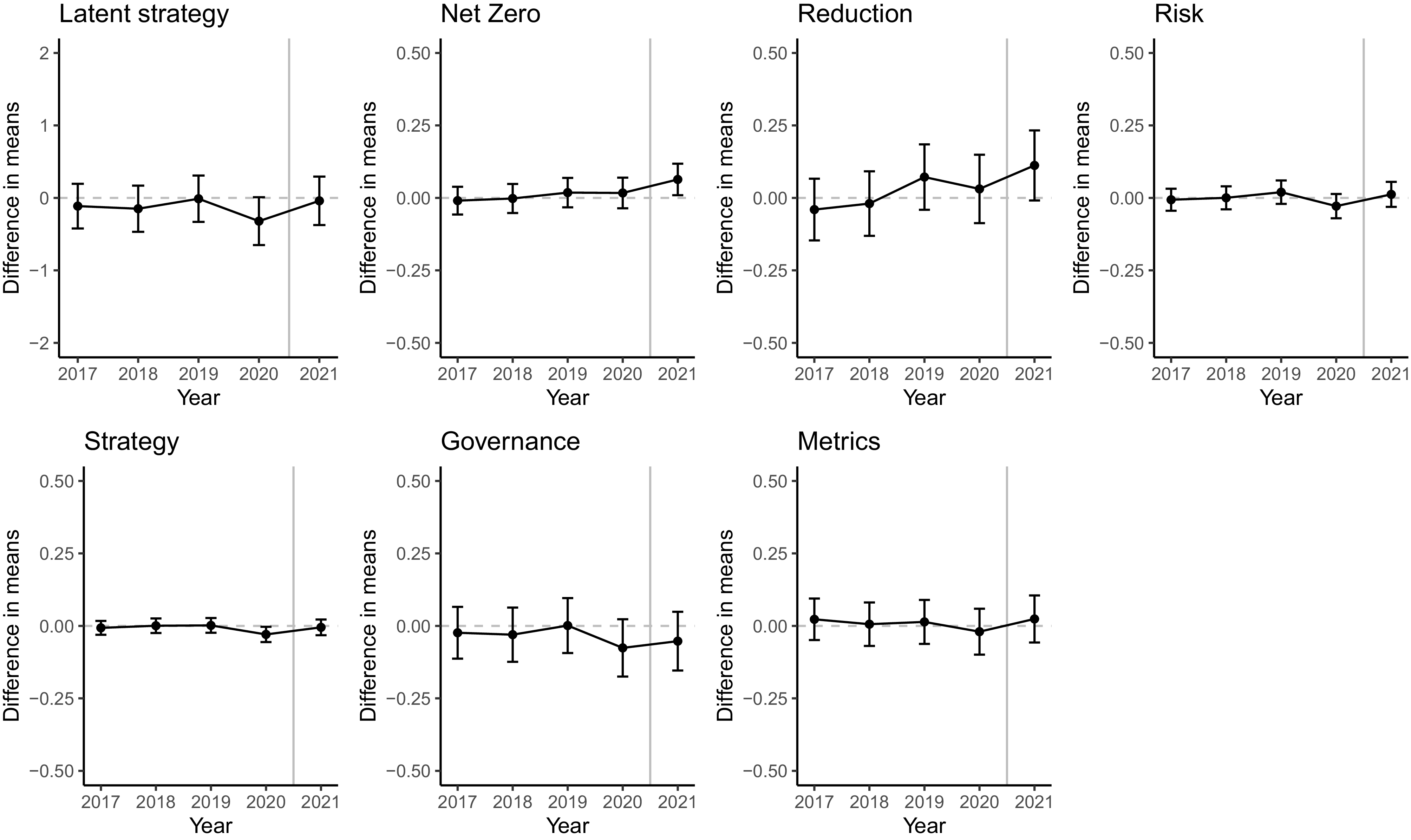

Figure 3 visualizes the results from OLS regression on the DiD estimator for the latent climate measure, the four TCFD categories, and two net-zero measures of climate strategy (tabular results are shown in Appendix Table A4). For five of the seven measures we find clear null effects, one that is significant at the 10% level, and only one of the seven distinguishable from zero at conventional levels. These largely null findings are in line with our theoretical expectation: there is no statistically distinguishable difference in climate strategies between firms that were and were not exposed to the change in shareholder power resulting from the SEC’s amendments to Rule 14a-8.

Difference-in-difference estimates from OLS regression across seven measures of climate strategy for treated and control firms based on change in exposure to shareholder pressure resulting from the 2020 amendments to SEC Rule 14a-8. Refer to Appendix Table A4 for tabular results.

The magnitude of these six null effects are relatively small. Consider the model results in panel 4, where the outcome is the NLP-coded score for whether a firm discloses how it manages climate-related risks (TCFD’s Risk category), ranging from 0 to 1. The estimated average treatment effect is

$0.01$

, corresponding to a one percentage-point increase in probability of a firm disclosing how it manages climate risks, which is roughly one-tenth the standard deviation of the Risk score.

$0.01$

, corresponding to a one percentage-point increase in probability of a firm disclosing how it manages climate risks, which is roughly one-tenth the standard deviation of the Risk score.

We do find a positive effect of a change in exposure to shareholder pressure for the Net Zero measure in panel 2. Here the effect corresponds to a seven percentage-point increase in a firm’s willingness to declare a net zero target. This is a modest increase relative to the distribution of this score, with a standard deviation of 0.13. But the result is not robust to applying firm-level fixed effects: the coefficient drops in magnitude to a five percentage-point increase and no longer significantly different from zero (Appendix Table A5). Substantively, however, an announcement of a net zero target—without any details or timelines on how the firm will achieve that target—is a low bar for a firm’s climate strategy. This corresponds to the hedging climate strategy in our typology, which results in shallow or selective transparency.

To account for any potential differences between firms that were and were not exposed to a change in investor shareholder empowerment as a result of the amendments to Rule 14a-8, we apply entropy balancing.Footnote 79 This is based on firm size, employment, asset base, profitability, and investor turnover (Appendix Table A7). After balancing the data, we see null results across the board for all seven indicators.

Finally, we expand the treatment to a continuous measure of the percentage-point difference in shareholders eligible to file resolutions because of the 14a-8 rule change. Here again the results show null results for all seven measures, further reflecting the limited impact of shareholder pressure on firm climate strategies (see Appendix Table A8).

Resolution-filing power and the case of ExxonMobil

Why does investor pressure from empowered long-horizon shareholders not result in a change to a firm’s climate strategy? That we do not find evidence of a shift in climate strategies suggests at least two possibilities: either (1) the empowerment of these shareholders did not lead to more pressure, or (2) that any new pressure that emerged—e.g., through increased shareholder resolutions—was ineffective in changing firm behavior.

SEC Rule 14a-8 led to increased resolution activity, but not successfully-filed resolutions

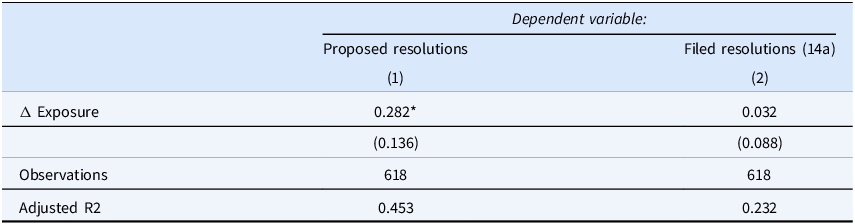

We address the first possibility using the exogeneity of the SEC Rule 14a-8 amendments to analyze whether firms impacted by the rule change experienced greater pressure from shareholders on any and all matters, whether related to climate issues or not. Applying the same DiD framework, we estimate whether treated firms had more resolutions filed by shareholders than non-treated firms.

Here we rely on two measures of shareholder resolutions: the number of resolutions disclosed by firms on their 14a filings, and the number of resolutions filed at the firm overall as tracked by third-party advocacy groups. The former is based on parsing 14a documents from the SEC, while the latter is based on totals from SEC filings plus resolutions that were filed but later withdrawn or excluded from voting at annual meetings.

The results in Table 4 indicate that the amended rule led to more resolutions proposed by shareholders (column 1), but no difference in the number of resolutions successfully filed and voted on at annual meetings (column 2). This implies that the rule change did lead to more pressure from shareholders—who were now more empowered to file resolutions of any kind—but that the pressure was limited in manifesting into resolutions that were ultimately voted on at annual meetings.Footnote 80

Difference-in-difference estimates from OLS regression across proposed (col. 1) and successfully filed (col. 2) shareholder resolutions for treated and control firms based on change in exposure to shareholder pressure resulting from the 2020 amendments to SEC Rule 14a-8

Note: *p

$\lt $

0.05; **p

$\lt $

0.05; **p

$ \lt $

0.01; ***p

$ \lt $

0.01; ***p

$\lt$

0.001.

$\lt$

0.001.

Internal stakeholder resistance: The case of ExxonMobil

We next look outside the context of the SEC rule change to examine how shareholders use resolutions, the proxy fight process, and other tools of investor engagement to effect a change in climate strategy. Examining declassified documents on correspondence between ExxonMobil and its external stakeholders, we find that shareholders applied considerable pressure on the firm, but that firm behavior on climate strategy was largely unchanged. Advocates first applied pressure to increase Exxon’s disclosures on climate-related risks; when this failed to achieve adequate transparency, stakeholders then attempted to replace internal stakeholders with more future-oriented leaders. Still, the firm sufficiently pushed back against climate-related shifts in strategy by changing its governance structure to align with the pre-existing positions of its internal stakeholders.

In September 2013, an advocacy group on behalf of 72 institutional investors with nearly $3 trillion in assets submitted a letter to Exxon management and prepared a shareholder resolution requesting information on what assets might become stranded as a result of future societal and policy constraints on carbon.Footnote 81 After several rounds of negotiations, Exxon in March 2014 published a comprehensive analysis of the company’s climate positions in exchange for shareholders agreeing to withdraw their resolution.Footnote 82 Exxon stated up front in the report that “we are confident that none of our hydrocarbon reserves are now or will become ‘stranded’.”Footnote 83 However, in internal conversations Exxon managers “discussed the desire to downplay assertions of impairment and carbon asset risk” when preparing the report.Footnote 84 It took less than three years for the company to backtrack on its public claim, when Exxon wrote off 19% of its total oil reserves, including 3.5 billion barrels of carbon-intensive tar sands in Canada.Footnote 85

This spurred an escalation by shareholders to go beyond filing resolutions and instead to target the company’s board of directors. After failed attempts in 2018 and 2019, activist shareholders succeeded in 2021 in seating three new members of the board with a vision to improve transparency and steer Exxon towards a low-carbon transition.Footnote 86 Yet in the years since, Exxon has failed to disclose detailed emissions data, eschewed substantial investments in clean energy, and expanded its commitments to oil.Footnote 87

Existing legal institutions have also proven insufficient in supporting external pressure for a shift in the company’s climate strategy. Exxon’s 2014 report formed part of the basis of a lawsuit by the New York Office of the Attorney General alleging that “Exxon provided false and misleading assurances that it is effectively managing the economic risks posed to its business” by climate change.Footnote 88 But the case was ultimately thrown out by a New York judge, finding that the State “failed to prove by a preponderance of evidence that ExxonMobil made any material misrepresentations.”Footnote 89

Given its sheer size and historical position in the industry, Exxon could be uniquely impervious to change.Footnote 90 But its experience in resisting shareholder and judicial pressure spotlights the limited ability of external stakeholders to improve climate strategy among fossil fuel firms absent a change in the position of internal stakeholders.

Corporate counter-strategies against shareholder resolutions

The ExxonMobil case points to a broader phenomenon in how firms stall the progress of shareholder resolutions once a proposal is filed. We lay out two strategies in particular: seeking SEC exclusion and canvassing other shareholders.

Firms can apply to the SEC through “no-action” letters to exclude proposals that focus on strategic, operational, or day-to-day management issues, or issues deemed improper under state law. Across industries, the exclusion rate in 2024 remains close to the 69% average from the 2017 to 2020 administration at 68%, but the increase in “no-action” requests resulted in 139 proposals being excluded in 2024, up from only 76 in 2023.Footnote 91 Many of these exclusions targeted climate-focused proposals, which were dismissed as attempts to micromanage company operations. Applicants argued that these disclosures would reveal critical gaps in companies’ climate transition strategies, yet the SEC consistently ruled that such granular demands overstepped shareholders’ role and went too invasively into day-to-day management, thus warranting their exclusion.

For resolutions that will be voted on at annual meetings, one form of firm contestation is the use of strategic recommendations in proxy statements to actively shape shareholder opinion. In this approach, corporate managers may recommend voting “against” specific resolutions, particularly those that challenge existing business practices or push for significant changes in areas like climate. By issuing statements in proxy materials or during shareholder meetings that draw attention to potential negative impacts of the resolutions—such as increased costs, a conflicting nature of proposals, risks to business strategy, or operational disruptions—management can shape the perception of shareholders.Footnote 92 Leveraging internal communications, investor relations campaigns, and persuasive narratives that align with shareholders’ financial interests, management builds a consensus against the proposed resolutions.Footnote 93

For example, in 2022, Activision Blizzard’s management campaigned against a resolution that would have required the company to release a workplace harassment report.Footnote 94 In the weeks leading up to the vote, the board on several occasions attempted to sway shareholders’ votes in favor of management’s position.Footnote 95 The company released an internal review that there was no widespread harassment and argued in its proxy statement that the proposal could potentially distract from ongoing reforms. Ultimately, shareholders voted in favor of the proposal.Footnote 96

Conclusion

While capital markets can in theory drive clean energy transitions in fossil fuel firms, we show that in practice this is not the case for a range of tools used by shareholders. For oil and gas firms listed in U.S. markets, we find that investor pressure through filing resolutions is not sufficient, moving the needle on surface-level announcements but not affecting a meaningful shift in corporate climate strategy. An analysis of the largest firm in our sample, ExxonMobil, shows that other forms of pressure such as voting on board members, direct communication with management, and support for climate-related litigation are similarly met with internal resistance. The result is the same: external pressure has limited impacts on decarbonizing polluting firms.

Our findings suggest that existing regulations and judicial levers in the U.S. grant considerable power to firms in resisting shareholder pressure. While few firms directly oppose shareholders via so-called Strategic Lawsuit Against Public Participation (SLAPP) litigation, firms face little regulatory cost for responding to shareholder pressure by simply maintaining business-as-usual or by hedging via soft commitments to future action. In addition, firms have undertaken legal action to strike down regulations that elevate climate disclosures in investor-facing materials, such as ExxonMobil’s 2025 lawsuit against the State of California for its mandatory disclosure rules.Footnote 97 Firms in the U.S. can also directly engage with regulators to exclude proposals that are deemed to be oversteps of investor roles. Taken together, this leaves no regulatory benefit for deep strategic shifts away from the traditional model of oil and gas operations, or even for more gradual changes that would be TCFD-aligned. As a result, we see such activities—e.g., the use of “no-action” letters and strategic litigation—as understudied areas of state-business relations worthy of future research.

This is in contrast to firms subject to regulations such as the U.K. Sustainability Reporting Standards or the E.U. Corporate Sustainability Reporting Directive, which serve as a floor for disclosure of climate risks and opportunities that firms face. These differing regulatory frameworks likely explain the divergence in climate strategies of major oil and gas firms based in the U.S. versus Europe cited in prior work,Footnote 98 for which we find continued support even for smaller firms listed in U.S. markets. This suggests institutional design mediates corporate power and shapes the boundaries of “permissible” shareholder engagement and mandated firm disclosures, including the purview of how firms respond to shareholder demands.

While these differences are endogenous to corporate power—for example, E.U. companies are less ideologically resistant to market regulations than U.S. companies—in practice, E.U.-based fossil fuel firms still contest stakeholder pressure despite more stringent pro-climate regulatory environments. The case of Shell, for instance, illustrates that contention over shareholder climate demands persists even under stronger disclosure regimes. When a coalition of institutional investors (Climate Action 100+) filed one of the first resolutions to align Shell’s targets with the Paris Agreement, management at first urged investors to vote against it, but later negotiated with the filers to avoid the vote and released its “Net Carbon Footprint” targets in an attempt to preempt potentially more ambitious goals.Footnote 99 In 2024, when investor-activist group Follow This filed a new resolution, Shell changed its strategy and released its own “Energy Transition Plan” designed to circumvent the resolution. Shareholders voted 78% in favor of Shell’s watered-down strategy, compared to 18.6% for the proposal from Follow This.Footnote 100

In showing the limited ability of shareholders to directly control, set the agenda for, or shape preferences of firms in the U.S., our study contributes to the literature on the faces of power by illustrating how regulations and the judiciary insulate firms from investor pressure.Footnote 101 In different institutional settings, shareholders and other stakeholders can wield these faces of power more effectively to enact change on corporate climate strategies, while U.S.-based firms remain protected from stakeholder demands.Footnote 102 Specifically, the absence of “no action” letters in the U.K. or E.U. removes a procedural barrier that U.S. firms often rely on to exclude before the proposals reach a vote. Without this avenue for dismissal, investors must build stronger cases for each proposal given higher eligibility requirements in these jurisdictions. At the same time, because investors are required to assemble a bigger coalition (5% ownership in the U.K.), engagement often takes place before the resolution is submitted. We see this as example of institutionally-mediated contestation.

Our findings also contribute to the study of state-business relationships, reaffirming the privileged position of management as insulated from collective pressures, often at the expense of shareholder influence.Footnote 103 This insulation reproduces the asymmetry between economic and political power: firms limit stakeholder influence and maintain business autonomy. In this sense, we also contribute to the study of institutionalized constraints on internal contestation in the area of corporate political power—business enjoys an advantaged position in markets and in politics—one that extends to the internal governance of firms themselves. Through contestation, firms can retain direct control over decision-making; through hedging, firms can effectively maintain agenda-setting power and shape preferences of general shareholders.

In addition, we see our measure of climate strategy as contributing to the study of corporate behavior in climate politics.Footnote 104 In particular, our measurement approach offers a new avenue through which scholars can test theories of “greenwashing” in future research. By systematically estimating how firms communicate regarding climate change across a wide range of topics, our measure of climate strategy can be compared to firms’ operations and activities to assess whether firms are “walking the talk” or instead misleading or deceiving the public about their climate efforts.Footnote 105 In addition to testing claims regarding corporate behavior outside the U.S., future research can also use our measure to conduct additional case studies beyond ExxonMobil to trace the process of how firms comprised of investors with medium or long horizons react to increased shareholder pressure.

Period effects experienced by all firms, such as the COVID-19 pandemic, have implications for the external validity of our findings. The sharp reduction in oil demand in the first year of the pandemic—due to travel restrictions and the rise in remote work—sparked a fundamental rethinking on the need for transportation fuels in the global economy.Footnote 106 From a market-response perspective, this would have reduced the cost for oil firms in 2021 to strategically shift to decarbonization. That we find limited effects of pro-climate shareholder pressure in this period suggests that these results would hold in other periods when transition costs for oil firms would be higher. However, future research could evaluate these claims as the costs to decarbonization continue to decline.

It is important to note that our findings do not rule out the necessary role for shareholder engagement. While we do not find that shareholder engagement by itself is enough to influence corporate climate behavior, more research is needed to evaluate whether shareholder engagement in concert with other financial levers can drive deeper decarbonization. Sustainability-linked loans or results-based financing, for example, may be more effective as “carrots” to decarbonize firms when coordinated with shareholder resolutions.Footnote 107 Shareholder engagement that arrives on the heels of “sticks” such as successful climate litigation may also prove to be more potent. Alternatively, future research would be needed to explore whether certain categories of shareholder pressure are more effective than others, such as resolutions that garner wide support at annual meetings.

Supplementary material

The supplementary material for this article can be found at https://doi.org/10.1017/bap.2025.10021. Replication material can be found at https://doi.org/10.7910/DVN/T5DJ9L.

Acknowledgements

We are very grateful for constructive comments and suggestions from participants at the American Political Science Association Annual Meetings, the Environmental Politics and Governance Workshop, the Environmental Politics Workshop at UCSB, the SAIS Political Economy Series Seminar, and the Columbia University International Politics Seminar. We acknowledge computational support from the UCSB Center for Scientific Computing at CNSI.

Competing interests

The authors report no competing interest.

Open access

Open access