How do foreign firms respond to electoral cycles in host economies? Investment, whether foreign-sourced or domestic, boosts economic growth and employment opportunities; incumbent politicians therefore work to attract investment to curry favor with voters who reward politicians who preside over growing economies. Foreign direct investment (FDI), in particular, is associated with higher wages and increased exports.Footnote 1 , Footnote 2 Multinational enterprises (MNEs), who expand into host economies through FDI, are also more resilient than domestic counterparts to economic downturns.Footnote 3 For these reasons, political leaders may endeavor to attract FDI to their districts, states, and countries to reap the electoral benefits of a strong economy. This political investment cycle dynamic predicts investments increase before elections, while an uncertainty and delay hypothesis anticipates investment declines in advance of elections. While elected officials may prioritize investment attraction, particularly in advance of elections, firms are likely to view elections as a source of uncertainty.Footnote 4 After all, the regulatory environment might change drastically if voters elect a new representative.Footnote 5 For this reason, firms might be hesitant to invest in districts where electoral uncertainty is high.

We adjudicate these competing expectations to contribute to international political economy theory on whether, when, and to what extent do electoral dynamics influence FDI decisions. While there is substantial theory and evidence that electoral uncertainty creates investment delay for foreign portfolio and sovereign debt investment, the literature is less settled on whether FDI follows similar patterns. We expect that firms attempt to minimize policy uncertainty and therefore will be more likely to announce investment plans in election years in congressional districts deemed uncompetitive—which we call clear-winner elections—than in districts with close elections (close-call elections). When probing causal mechanisms, we anticipate three additional observable implications of our theory. First, that districts with clear-winner elections are better able to secure federal funding, which in turn positively influences FDI announcements. Second, that sensitivity to regulatory uncertainty varies with capital intensity and so firms in industries characterized by high fixed capital expenditures will be more sensitive to the electoral cycle than firms in industries that require little fixed capital. Finally, that an uncompetitive election provides maximal certainty when an incumbent is running, and so increases in election-year investment announcements in clear-winner districts will only hold when incumbents are running for re-election.

Our theoretical expectations could apply to elections at various levels of government. To date, scholars have primarily examined the effects of elections on FDI at the state or local executive level.Footnote 6 In contrast, we analyze congressional elections. Like executives, legislators also work to secure investment projects for their districts, are evaluated by voters by local economic performance, and can be powerful regulatory advocates or foes of investors depending on their policy positions and voting records on an array of issues such as trade, taxation, and various labor and environmental regulations. Members of Congress can fulfill important facilitation roles to coordinate regulators across multiple jurisdictions, secure federal funding for necessary infrastructure, and generally champion complex projects when they run into regulatory or financial challenges.Footnote 7 Additionally, the immediate economic impact of a new investment project is more localized than the state level but, due to commuting zones, covers a larger area than one municipality. Therefore, congressional districts are sized in a way that better matches the geographic reach of investment effects.Footnote 8 Focusing on congressional races also has practical benefits because our dataset matches investment locations to congressional district and, unlike local races, we can obtain reliable data on the competitive status of congressional races.

Our empirical analysis provides substantial support for our hypotheses—foreign investors are significantly more likely to announce FDI projects in U.S. congressional districts where election outcomes are predictable. Using panel data from 2003 to 2017 and a conditional logit framework, we show that districts with clear-winner elections attract more FDI announcements than those with close-call elections or no elections. This pattern holds across multiple operationalizations, including investment volume and job creation, and is robust to alternative definitions of electoral competitiveness. We also show that this effect is concentrated in capital-intensive and new investments and is especially pronounced when the expected winner is a Republican incumbent—further supporting the argument that firms prioritize political continuity and ideological alignment when making location decisions. Supplemental mediation analysis finds that increased federal appropriations—a lever local congresspeople can influence—partly explain this pattern. Jointly, these findings reveal a political bias in global capital allocation: politically monopolistic districts attract more investment, while vibrant electoral competition deters it—raising fundamental concerns about the interplay between democracy and money.

Our analysis has important implications for both IPE theory and those interested in the relationship between democratic institutions and economic performance. First, these findings offer an important qualification to a growing body of research on investment incentives.Footnote 9 While electoral considerations may increase the offering of investment incentives—which are generally inefficient, unnecessarily reduce the tax base, and transfer fiscal burden from corporate forms to workers and consumers—electoral competitiveness likely reduces the acceptance of these incentive offers, at least in the run up to elections. Second, these findings offer concerning implications for the relationship between institutions of democratic governance and economic performance. If foreign investment is an important component of localized economic growth and employment, our findings suggest that congressional districts with the most vibrant forms of electoral contestation are disadvantaged to capture the economic benefits of such investments. Our analysis also complicates the broad consensus that MNEs prefer to invest in democracies and suggests that foreign firms equate electoral competition with policy uncertainty. Reconciling the chilling effect of elections on investment with the importance of contestation and representative governance remains an important task, particularly in an era of economic populism.

Foreign investors and electoral uncertainty

Scholars frequently highlight the effect of electoral uncertainty on firms’ investment decisions, identifying elections as periods of heightened uncertainty.Footnote 10 Elections introduce the possibility of substantial shifts in policy and regulatory frameworks. New officeholders may propose novel regulations, repeal existing ones, or alter enforcement strategies, particularly in sectors such as energy, labor, and environmental protection. They may hold divergent views on fiscal policy, monetary stability, or public investment priorities,Footnote 11 affecting the broader macroeconomic environment in which foreign firms operate. Studies show that differences in political party positions on economic management frequently influence firms’ timing and scale of investment decisions.Footnote 12

Most crucial for our argument, however, elections can disrupt the local political relationships and institutional access points that foreign firms rely on to navigate complex political systems. While national-level elections may shift macroeconomic expectations, the replacement of a long-standing representative can create localized uncertainty—particularly when that politician has played a consistent facilitative role in guiding firms through the intricacies of overlapping political jurisdictions. Newly elected representatives may differ in policy preferences, possess less institutional seniority, or lack the established networks necessary to assist firms in coordinating across local, state, and federal levels. In such cases, firms face not only a potential change in advocacy but a disruption in the procedural and informational continuity that supports effective project planning.

To date, much of the empirical evidence on the effect of electoral uncertainty comes from portfolio equity markets. Studies demonstrate that elections are associated with heightened volatility,Footnote 13 increased risk premia,Footnote 14 and movements in sovereign bond yields.Footnote 15 Stock market research similarly finds increased volatility and risk pricing around election periods.Footnote 16 These market dynamics underscore the real and immediate consequences of political uncertainty for financial actors.

Political economy scholars have routinely established the importance of democracy, or political institutions closely associated with democracy, as important for attracting foreign investment, even if this relationship is complex and attenuated by local context.Footnote 17 However, relatively little research has explored the effects of domestic legislative elections on FDI. Notable exceptions include studies that examine how election-driven policy uncertainty influences FDI patterns across countries. Chen and coauthors analyze FDI trends in 126 countries from 1996 to 2015, using the timing of national elections as a proxy for policy uncertainty.Footnote 18 Their findings indicate a significant drop in FDI during election years, suggesting that increased policy uncertainty deters foreign investment. Similarly, Julio and Yook investigate the effects of political uncertainty on cross-border capital flows by analyzing U.S. investors’ direct investment in 43 countries between 1994 and 2010.Footnote 19 They find that FDI flows from U.S. companies decrease notably in the period leading up to elections, only to rise again once electoral uncertainty is resolved.

Both studies provide valuable insights but rely on broad cross-country samples, raising questions about unobserved country-specific factors that could influence the results. This limitation highlights the need for a more controlled, single-country analysis to better isolate the effects of elections on FDI. By focusing on a specific country and analyzing the cross-district variation, we can better apply ceteris paribus conditions, controlling for contextual variables that differ across countries.

While much of the existing literature assumes that any election introduces uncertainty, the degree of uncertainty varies substantially across elections. We differentiate between two types of elections: close-call elections and clear-winner elections. Some contests are highly competitive, making it difficult to predict the winner in advance. These close-call elections create significant ambiguity for foreign firms, which must anticipate how a potential change in political leadership might affect their access to public goods, regulatory stability, or policy advocacy. In contrast, other elections feature a clear frontrunner whose victory is all but assured. These clear-winner elections provide firms with a greater sense of political continuity, reducing the perceived risk associated with electoral cycles.

Why do foreign investors prefer clear-winner districts?

Investors favor clear-winner districts because they value political stability and continuity. Foreign firms, in particular, are often deterred by the uncertainties associated with closely contested elections, preferring to invest in regions where electoral outcomes—and by extension, political representation—are more predictable. Clear-winner districts reduce the likelihood of frequent turnover, offering a more reliable forecast of legislative continuity. For firms planning large-scale, long-term investments such as manufacturing facilities, the selection process often unfolds over multiple years. As such, investment decisions are unlikely to hinge on the outcome of a single election. This long-horizon perspective makes electoral predictability a key criterion in reducing exposure to political disruptions. In addition to turnover risk, firms must also account for the possibility of ideological shifts when incumbents are replaced. Newly elected representatives may hold markedly different positions on labor laws, tax incentives, or environmental regulations—issues that can materially affect firms in highly regulated sectors such as energy, chemicals, or transportation. While national politics set the broader policy framework, changes in district-level representation can shape how rules are implemented and how effectively firms can access political support when navigating regulatory bureaucracies.

Political continuity at the district level also matters because it sustains access to established relationships and institutional knowledge. As noted above, investors benefit from having a consistent point of contact who can help them interpret the bureaucratic environment, coordinate across government levels, and facilitate engagement with federal programs. Long-serving legislators can act as durable access points within the political system. Their tenure often translates into stronger committee positions, deeper agency networks, and accumulated procedural knowledge—all of which can help reduce transaction costs and uncertainty for firms. In this sense, clear-winner districts are attractive not because their representatives guarantee policy outcomes but because they minimize the risk of disruption to these informal but valuable access relationships.

This dynamic is especially salient for foreign investors, which often lack the alternative political ties available to domestic actors.Footnote 20 Most countries restrict political contributions from foreign sources, and multinational enterprises headquartered abroad generally avoid taking on prominent lobbying roles in host countries. As a result, foreign investors have limited means of influencing political processes and must rely more heavily on cultivating relationships with politicians in the localities where they invest. Without access to established networks or multiple political entry points, foreign firms have a heightened interest in securing partnerships with politicians who are likely to remain in office and who can help them navigate the complexities of the bureaucracy. This vulnerability to political turnover makes electoral predictability especially valuable. For foreign MNEs undertaking capital-intensive projects with high sunk costs, the stakes are particularly high—uncertainty about future representation or regulatory support poses a direct risk to the viability of long-term investments. Clear-winner districts, by contrast, offer a more reliable foundation for forecasting political and policy stability.

Why do investors not simply delay until after the election?

One may argue that if elections generate uncertainty, firms could simply delay their investment decisions until the election has concluded. From this perspective, rational investors would wait until the political environment stabilizes, allowing them to proceed with greater confidence in future policy trajectories and political representation.Footnote 21

However, we contend that there are compelling reasons why some firms—particularly foreign investors—may still choose to announce FDI projects before an election, especially in districts where the incumbent is highly likely to retain their seat. In such “clear winner” districts, political continuity is predictable, and the expected risk of representation-related disruption is low. When investors can anticipate this outcome with reasonable certainty, the perceived cost of investing before the election diminishes significantly. Moreover, early announcements can confer distinct strategic advantages that are less about extracting tangible “goodies” and more about shaping expectations and building institutional relationships.

First, firms may seek to gain a first-mover advantage in the competition for limited bureaucratic attention and political engagement. While legislators do not unilaterally allocate governmental resources, they do play a central role in helping firms access funding streams and navigate regulatory complexity. These forms of assistance operate less through formal control and more through informal advocacy, constituent service, and procedural guidance. Since the pool of governmental resources and agency bandwidth is finite, multiple firms within a district may effectively compete for assistance. Early investment signals not only help firms demonstrate commitment to the district but also allow them to position themselves as credible stakeholders and partners. As Crepaz, Hanegraaff, and JunkFootnote 22 note, early lobbying and engagement can shape downstream access to policymaking processes. Similarly, Jung, Owen, and ShimFootnote 23 highlight that early positioning enhances firms’ ability to influence outcomes and secure institutional support—even in complex or contested environments.

Second, early investment announcements can be used as a strategic signal to policymakers, reinforcing firms’ commitment to a particular location and increasing the credibility of subsequent requests for assistance. During an election campaign, incumbents are likely to publicly affirm support for major investment projects in their district. While firms might gain bargaining leverage from electoral timing in general, incumbents who are highly likely to win can make more credible commitments. Their electoral security enhances the likelihood that any informal assurances given during the campaign will be honored in the post-election period. In contrast, candidates in competitive districts may offer campaign promises with limited follow-through capacity, simply because the electoral outcome remains uncertain. Thus, early engagement in stable districts does not rest on the assumption that legislators are decisive actors, but rather on the expectation that their continued presence offers institutional continuity that reduces political transaction costs and enhances policy reliability.

In this way, firms’ decision to move before an election—particularly in clear-winner districts—should be understood as a strategic response to both national-level and district-level dynamics. While federal policy is shaped largely at the national level, local political continuity still matters for how policies are interpreted, accessed, and implemented at the ground level. Delaying investment until after the election may minimize some risks, but it can also mean forfeiting early access to valuable institutional relationships that facilitate long-term project success.

Expectations

In sum, we argue that the electoral process introduces uncertainty for foreign investors and that the strength of this treatment varies by how competitive the election is. In districts where elections produce a clear winner, the political environment is relatively predictable, providing investors with high confidence about who will represent the district in the national legislature. Conversely, in districts with closely contested elections, the political outlook remains uncertain until the final results, creating heightened risks for investors who prioritize consistent representation and policy continuity. Therefore, we hypothesize that:

Hypothesis 1. In comparing electoral districts, those with clear-winner elections will exhibit an increase in FDI announcements in election years relative to previous non-election years, while those with close-call elections do not experience such an increase.

Testing predictions using U.S. Congressional elections

The theoretical framework we develop above could generally apply across various levels of political representation. We focus on U.S. congressional races. We believe this choice is both a hard test of our theory—extant scholarship on FDI attraction focuses either at the national executive level or on state and local officials—and justified. There is evidence that foreign firms closely monitor congressional elections and actively pursue relationships with U.S. Members of Congress (MoCs) through lobbying and engagement.Footnote 24 We argue that MoCs may serve as important partners for foreign investors seeking to enter the U.S. market in at least three ways.

Facilitating access to favorable regulatory policy

First, MoCs can support foreign investors by helping them navigate and access favorable regulatory environments. Various federal policies affect foreign investors, including sector-specific regulations in pharmaceuticals and energy, environmental standards, and laws that shape business formation and licensing procedures. Federal labor regulations generate compliance costs, immigration policy affects specialty labor availability, and trade policy affects the costs of imported inputs and competitiveness of outputs.

MoCs do not singlehandedly design or control these regulations, but they play an important facilitative role within the institutional structure of U.S. federalism. Through their legislative authority, MoCs may influence the regulatory landscape by introducing or supporting laws that mandate or restrict agency behavior.Footnote 25 They participate in congressional hearings that scrutinize regulatory agencies, and they can indirectly shape enforcement intensity—e.g., weakening environmental enforcement by reducing an agency’s budget. While many relevant regulations are implemented at the state level, MoCs can indirectly affect state policy by leveraging federal incentives or pursuing preemptive federal legislation. For instance, federal visa programs for foreign workers are subject to legislative oversight, renewal, and appropriations. Sympathetic MoC can assist individuals and companies in their district navigate visa approval processes more efficiently. In this sense, MoCs serve less as decisive actors and more as access points who help investors interpret complex regulatory environments and signal continuity in institutional priorities.Footnote 26

Facilitating access to federal funding

Second, MoCs can play an important role in helping investors access federal funding opportunities that can shape the feasibility of large-scale investment projects.Footnote 27 Firms may hesitate to invest in regions lacking critical infrastructure, skilled labor, or technological capacity. While states and localities may offer incentives, their fiscal capacity is often constrained. Federal support—channeled through congressional appropriation and oversight—covers these gaps. For example, BMW wanted to expand its manufacturing plant in South Carolina in the early 2000s, but only if critical road infrastructure was upgraded. Jim DeMint, who represented the district in which the BMW plant was located, lobbied through the House Transportation Appropriations Subcommittee to use federal dollars to cover the $10 million shortfall necessary to build a highway interchange necessary to secure BMW’s expansion.Footnote 28 While MoCs do not unilaterally control the flow of funds, they can help firms identify relevant programs, advocate for district-level priorities, and reduce uncertainty around access. As BartikFootnote 29 notes, congressional involvement in directing federal funds can enhance local economic development initiatives, thereby making locations more attractive for foreign investment.

The out-of-sample case of Taiwan Semiconductor Manufacturing Company (TSMC) illustrates this facilitative role. TSMC requested $15 billion in federal support for its Arizona-based semiconductor facilities, including $7–8 billion in tax credits under the CHIPS Act and an additional $6–7 billion in federal grants. The company expressed concern about specific subsidy requirements—such as profit-sharing provisions—that could undermine the project’s financial viability.Footnote 30 , Footnote 31 MoCs representing affected districts did not control these provisions directly but played a key role in negotiating with federal agencies, conveying constituent concerns, and emphasizing the strategic value of semiconductor investments.Footnote 32 Their involvement helped clarify program expectations and facilitate continued engagement between investors and the federal bureaucracy. Congresswoman Lesko, who represented the area in which TSMC’s plant located, also led a successful effort to roll back specific air quality regulations that the Environmental Protection Agency planned to impose on the area, highlighting the negative consequence of the regulation for TSMC.Footnote 33

Facilitating network and coordination effects

Third—and in our view, most importantly—MoCs play a critical role in facilitating coordination and serving as access points within the institutional and political networks that foreign investors must navigate. FDI projects often involve complex, long-term undertakings that span multiple levels of government and policy domains—ranging from infrastructure development and permitting to workforce training and community engagement. These responsibilities are typically distributed across jurisdictions: local officials manage zoning and outreach, governors administer state-level incentives, and federal agencies oversee national funding programs. Without effective coordination among these actors, foreign investments risk delays, misalignment, or cost overruns. MoCs do not control these processes directly, but they can help investors navigate the federal system, align priorities across levels of government, and identify strategic points of access. In doing so, they contribute to the creation of more investment-friendly environments, particularly in districts where bureaucratic complexity might otherwise be a deterrent.

MoCs are especially well-positioned to support these coordination functions by bridging institutional divides between local, state, and federal authorities.Footnote 34 Kenyon and KincaidFootnote 35 note the importance of federal officials in fostering intergovernmental alignment, while PosnerFootnote 36 highlights how MoCs act as intermediaries across competing jurisdictional priorities. By representing districts that often span multiple municipalities, MoCs serve as informal liaisons between mayors and governors, helping to align political and administrative incentives. Through their committee memberships, agency relationships, and constituent offices, MoCs help stakeholders interpret program requirements, engage with federal actors, and anticipate procedural bottlenecks. This brokerage function becomes especially valuable in the context of competitive investment attraction, where procedural certainty and cross-level coordination can make or break project feasibility.

Foreign firms are particularly likely to benefit from these facilitative roles. Unlike domestic firms with established networks, foreign investors often lack familiarity with the decentralized U.S. system and its layered regulatory environments. Language barriers, cultural differences, and limited local presence further complicate navigation. By helping foreign firms understand relevant processes and by signaling the availability of support, MoCs reduce informational asymmetries and improve the credibility of a district as a stable investment location. Importantly, these functions do not require MoCs to deliver outcomes singlehandedly; rather, they operate through informal guidance, advocacy, and the signaling effects of political continuity.

This facilitative role is illustrated by the out-of-sample case of Representative Debbie Dingell, whose district hosted a federally subsidized electric vehicle battery plant. While she did not directly determine funding allocations or project approvals, Dingell’s advocacy—amid national scrutiny over the plant’s ties to a Chinese company—underscored her role as a political intermediary. Her seniority enabled her to publicly defend the project and engage with federal stakeholders, even participating in a subcommittee hearing outside her formal jurisdiction. This example demonstrates how MoCs can help sustain momentum for complex projects, not through decisive intervention, but by reducing reputational risk, coordinating messaging, and maintaining federal engagement.

Data and sample

We test our argument by examining how the competitiveness of congressional elections affects the timing of FDI announcements across congressional districts. Our sample includes yearly data from 2003 through 2017. Our sample ends in 2017 for two reasons, one practical and one theoretical. Practically, our underlying greenfield FDI announcement data come from a proprietary database, and we do not have access to data post-2017. Theoretically, rhetoric and policy around foreign investment in the United States changed substantially in the latter half of the 2010s. These include the partisan realignment on trade and industrial policy that began in the 2016 cycle, the expansion of national-security-based investment screening under the Foreign Investment Risk Review Modernization Act of 2018, and the proliferation of large place-based industrial-policy instruments associated with the CHIPS and Science Act and the Inflation Reduction Act. We treat the question of whether the same logic travels to the post-2017 environment as a productive direction for future research and return to this point in the conclusion.

Our dependent variable is a binary indicator capturing whether a congressional district announced at least one greenfield FDI project in a given year. Greenfield investment includes both investments in de novo business locations (e.g., a new manufacturing plant) and follow-on investment for an existing locations (e.g., an expansion or retooling of an existing manufacturing plant). Greenfield investment does not include cross-border merger and acquisition activity, that is the acquisition in part or whole of an existing business by a foreign entity. We focus on announcements—rather than completed projects—to capture our theoretical mechanism: the strategic advantage firms gain from signaling alignment with an entrenched politician. We limit the analysis to greenfield investments for two reasons. The first is theoretical—greenfield projects are directly tied to job creation and new economic activity, which are more visible and politically salient than mergers and acquisitions. The second is practical—we are unaware of any dataset that provides comprehensive information on cross-border mergers and acquisitions in the United States nor one that provides geo-location data for such investments.

The data come from the fDi Markets database, maintained by the Financial Times, which is a widely used global repository of greenfield FDI projects.Footnote 37 As stated above, the database covers both new physical facilities and expansions that generate jobs and capital investment. Projects are compiled from public sources, including global media outlets, investment promotion agencies, and company press releases. All entries are reviewed and validated by fDi Markets analysts, and when investment or employment figures are not publicly available, they are estimated using proprietary econometric models. Each project is geolocated to subnational regions and categorized by sector according to an internal classification system.

This dataset is well suited to our analysis. It captures the timing and location of investment announcements, enabling us to examine how visible economic activity intersects with electoral dynamics. In contrast to aggregated FDI flow data, fDi Markets allows for fine-grained, district-level measurement and reflects the moment of political salience—when a project is announced—rather than its eventual implementation. Nonetheless, there are important limitations. Not all announced projects are ultimately realized, and the database may underreport smaller or unpublicized investments. To mitigate these concerns, we rely on a binary indicator (project announced or not), which avoids dependence on headline investment or job figures and reduces sensitivity to overreporting or subsequent revisions.Footnote 38

In aggregate, 97% of all 435 districts received at least one FDI project announcement between 2003 and 2017. All states had at least one FDI announcement, though the geographical distribution is highly skewed toward three heavyweights: Texas (1,241), New York (1,658), and California (2,110). Wyoming (8), Montana (11), and Alaska (11) exhibited the fewest project announcements.Footnote 39

Our main independent variable distinguishes between three types of district-year observations: non-election years (coded as 0), election years with clear winners (1), and election years with close races (2). This coding allows us to isolate the effect of electoral competitiveness within election years, using non-election years as a baseline to control for general election-related dynamics. Classification is based on anticipated competitiveness, proxied by the Cook Partisan Voting Index (CPVI), which captures the structural partisan lean of each district. This aligns with our theoretical claim that firms prefer stable, predictable political environments when announcing investments.

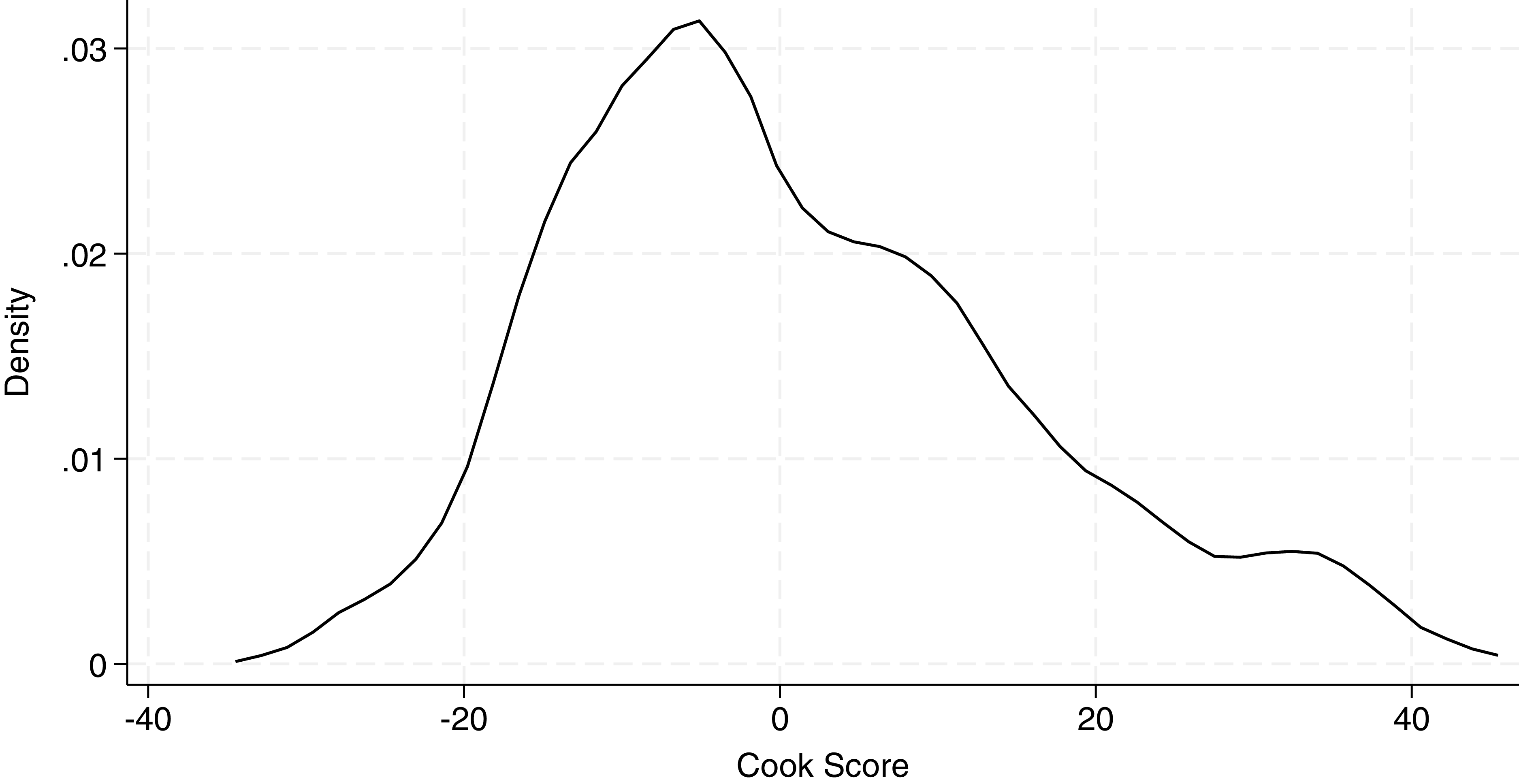

The CPVI, sourced from the Cook Political Report,Footnote 40 provides a continuous, objective measure of a district’s partisan leaning. It compares the district’s average two-party presidential vote over the past two elections to the national average, with greater weight given to the most recent cycle. For example, a score of D + 2 indicates a district that voted two percentage points more Democratic than the national mean. The distribution is shown in Figure 1.

Cook score capturing the degree of competitiveness across electoral districts.

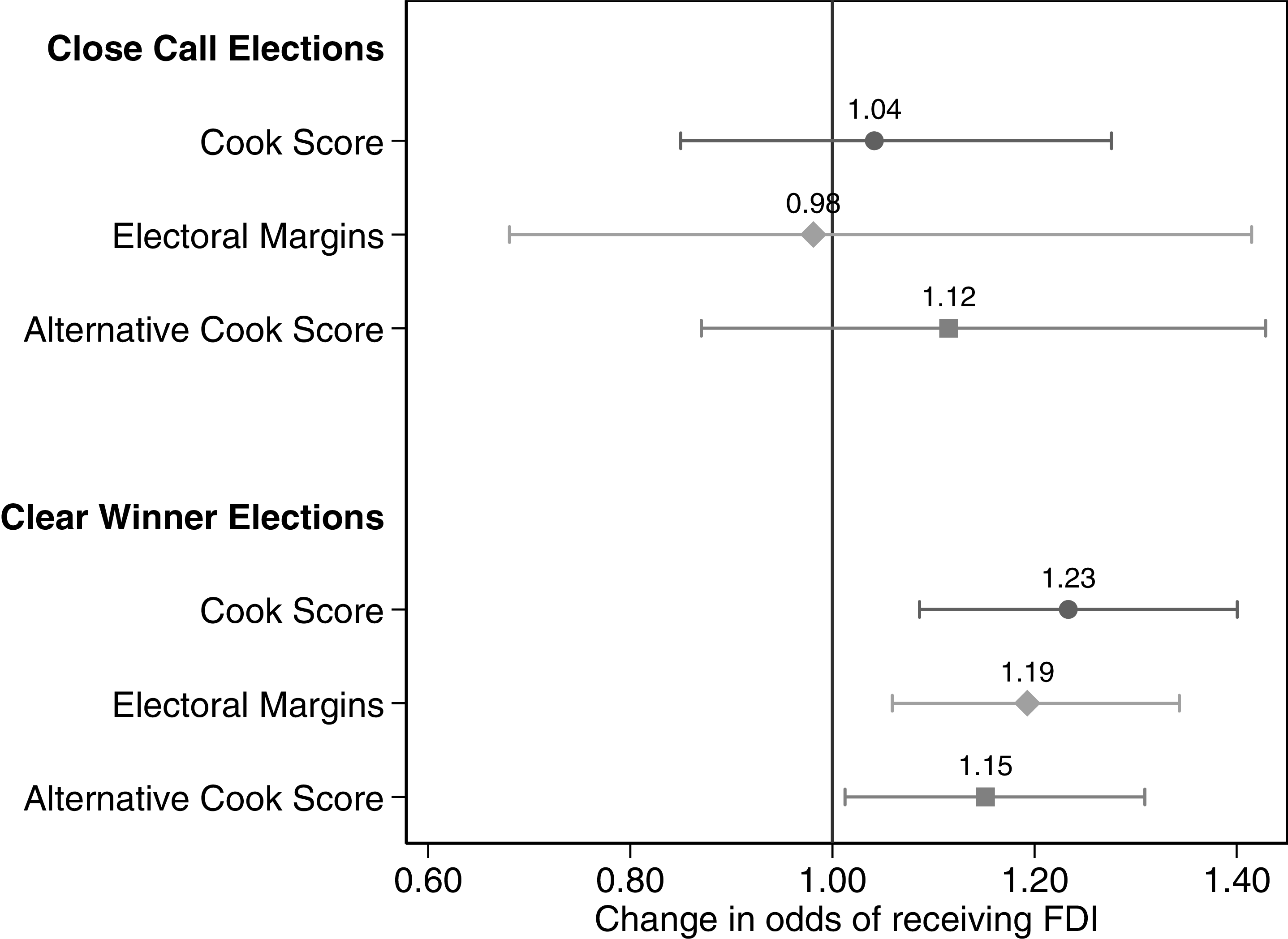

We use the CPVI because it offers an ex ante proxy for how firms assess electoral competitiveness. Investment decisions and accompanying announcements are made before election outcomes are known, so what matters is not actual results but expectations based on publicly observable signals. The CPVI captures these expectations. The CPVI also offers technical advantages. As a continuous measure, it allows us to model fine-grained variation in perceived political safety.Footnote 41 Because it relies on presidential vote share rather than House-specific outcomes, it avoids noise from campaign-specific factors—like candidate quality or late-stage fundraising—that firms are unlikely to track systematically. One concern with this measurement strategy is that CPVI reflects partisan structure rather than campaign dynamics. To account for this, we re-estimate our models using ex post vote margins from House elections. As shown in Figure 4 and the appendix, results are substantively unchanged.

Districts close to “Even” (usually within D + 5 to D−5, which corresponds to R + 5) are classified as competitive, while those with a higher CPVI lean are considered non-competitive. Following this, we code elections with a CPVI between −5 and 5 as close-call elections, while those with a CPVI greater than 5 or less than −5 are considered clear-winner elections.Footnote 42 According to this measure, there are 1,583 district-years with clear-winner elections and 594 with close-call elections.

Given our focus on firms’ investment decisions, we control for several factors that might influence announcements of investments in a particular district. To capture the business environment, we control for the state corporate income tax rate. We account for the quality of existing infrastructure by including a state measure of highway mileage per square mile. The local labor market is considered through the district’s education level (measured by the percentage of the population with a high school degree) and the unemployment rate. We control for state GDP per capita to capture possible wealth effects. Lastly, we account for the party identification (ID) of both the congressional incumbent and the governor to consider partisan effects. Our district-level control variables are sourced from the Census Bureau’s American Community Survey, while most of our state-level variables are obtained from the Bureau of Economic Analysis’ regional database. Summary statistics of all variables are available in Table 1.

Summary statistics

Our specification includes district fixed effects, which ensures that identification comes from within-district variation over time. That is, we compare the same district across non-election years, competitive elections, and non-competitive elections. This design allows us to assess whether FDI announcements are more likely when the political environment is stable and the incumbent’s re-election is virtually assured—without conflating this effect with the general presence of an election. The statistical significance of the two election-year categories, relative to the non-election-year baseline, thus provides a direct test of our core hypothesis.

Findings

The effect of electoral competition on FDI announcements

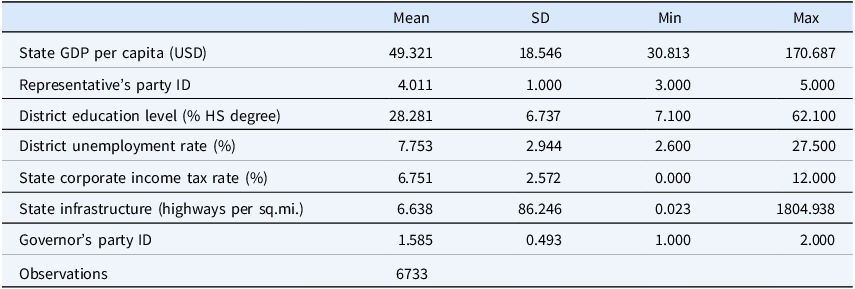

We begin by descriptively examining the dynamics of FDI announcements over time. Figure 2 plots the average number of FDI announcements in the dataset across the congressional electoral cycle by year. For example, the plot for “election month” represents the average number of investment announcements in November during election years from 2004 to 2016, with whiskers indicating the distribution of investment counts across these years. The pattern reveals that FDI announcements tend to be higher in the six months leading up to an election, peaking in the month before congressional elections. Post-election, average FDI announcements decline. These monthly averages of FDI announcements provide initial evidence that FDI follows electoral cycles, consistent with our argument.

FDI announcements counts higher prior to elections.

Next, we examine FDI announcement patterns across districts. At the district-year level, 1,042 observations report no projects in election years, while 1,135 record at least one project, suggesting minimal difference between election and non-election years overall. However, when distinguishing between district-years with close-call elections and those with clear-winner elections, clear differences emerge. In districts with close-call elections, the number of district-years with and without project announcements is roughly equal (294 vs. 300). In contrast, districts with clear-winner elections report more district-years with project announcements (846) than without (737). This suggests that FDI announcements are more frequent in clear-winner districts, particularly during election periods.

We then explicitly test the effect of electoral competitiveness on FDI announcements. For this reason, we estimate panel logit models with fixed effects, equivalent to a conditional logit model:

$\eta _{ij} = {{\exp (x_i \beta _j + z_{ij}\gamma )}\over{\sum _i^\prime \exp (x_i^\prime \beta _j + z_{i^\prime j}\gamma )} }$

$\eta _{ij} = {{\exp (x_i \beta _j + z_{ij}\gamma )}\over{\sum _i^\prime \exp (x_i^\prime \beta _j + z_{i^\prime j}\gamma )} }$

Here, η ij represents the probability of receiving an investment announcement in period i for district j, x i captures the predictors, and z ij includes district fixed effects to account for unobserved heterogeneity across districts.

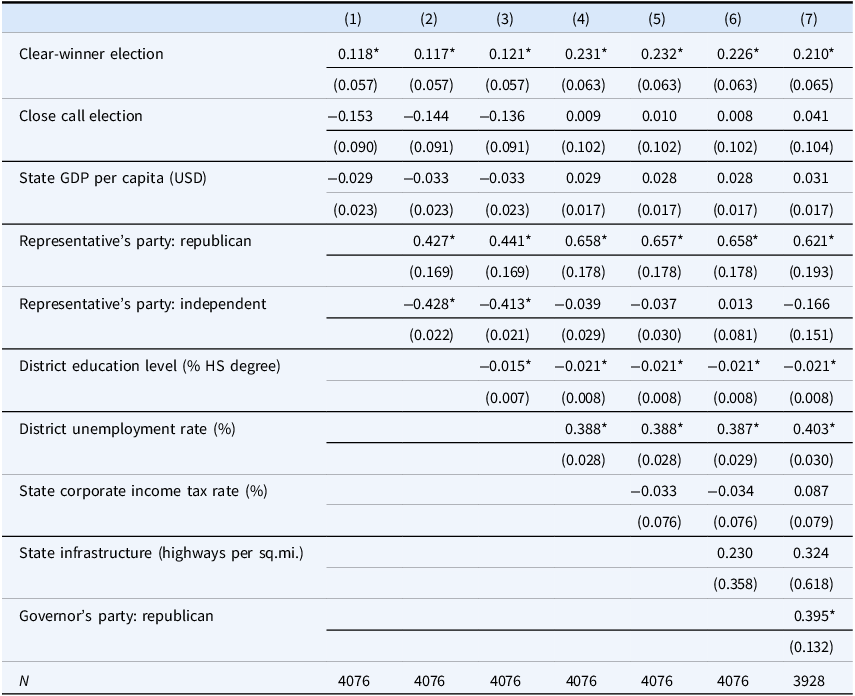

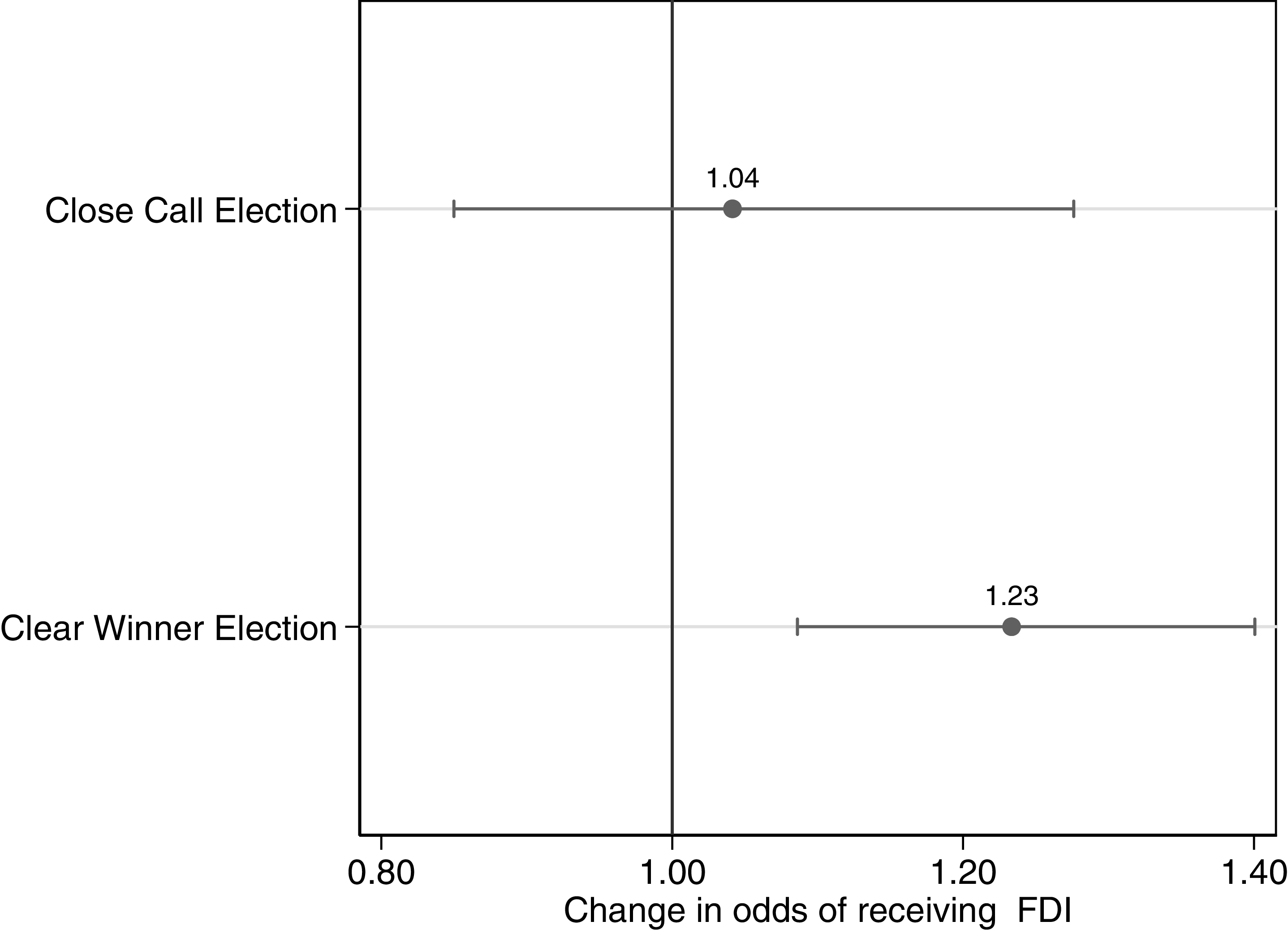

As hypothesized, districts with clear-winner elections are more likely to attract FDI announcements than those with close-call elections. Table 2 presents these findings.Footnote 43 Figure 3 visually displays the odds of FDI announcements relative to non-election years, conditional on the type of electoral race.

Main findings

Note: The findings demonstrate a statistically significant increase in the odds of a district receiving FDI in elections with expected winners, whereas this is not the case for close-call elections. *p < 0.05. All models include district fixed effects.

Competitiveness of elections and FDI announcements.

Note: The findings show a statistically significant increase in the odds of FDI in districts with elections featuring expected winners, but not in close-call elections. 95% confidence intervals. All models include district fixed effects.

To illustrate the substantive magnitude of the effect, we translate the estimated change in investment probability into expected investment values using the observed distribution of project sizes. Moving from close-call elections to clear-winner elections increases the probability that a district receives an FDI announcement from 17 percent to 22 percent, a five percentage-point increase, which corresponds to roughly a 29 percent higher probability relative to the close-call baseline. Applied to the 594 close-call district-years in our sample, this implies that if all of these cases had instead been clear-winner elections, approximately 25 additional district-years (about 25.27 out of 594) would have received at least one FDI announcement. Using the average investment amount among district-years with FDI, this corresponds to roughly $4.597 billion in additional announced investment in the United States. Because the distribution of FDI project values is highly skewed, we also compute estimates using the median investment amount, which implies about $1.365 billion in additional investment. Given that the average district-year in our dataset receives roughly $165 million in announced investment, these estimates correspond to the equivalent of roughly eight–28 average-sized projects.

Addressing methodological concerns

We estimate several additional models to ensure that the effect identified above is methodologically robust.

First, we test whether our findings are sensitive to how we define the independent variable—namely, the distinction between close-call and clear-winner elections. In the main analysis, we relied on the CPVI, an ex ante measure of electoral competitiveness based on the structural partisan lean of each district. The CPVI captures expectations about political safety from the perspective of firms making investment decisions before election outcomes are known. However, one might ask whether our results depend on this ex ante proxy.

To address this, we re-estimate our models using an ex post measure: the actual margin of victory in House elections. This approach classifies competitiveness based on realized vote shares, allowing us to test whether districts with narrow or wide electoral outcomes exhibit patterns consistent with our theory. As shown in Figure 4, the results remain robust. Even when using realized election outcomes rather than anticipated competitiveness, we continue to observe that FDI announcements are more likely in election years when the likely winner is clear.

Cook scores vs. margin of electoral victory.

Note: Findings are consistent regardless of whether Cook Scores or electoral margins are used to distinguish between close-call and clear-winner elections. 95% confidence intervals. All models include district fixed effects.

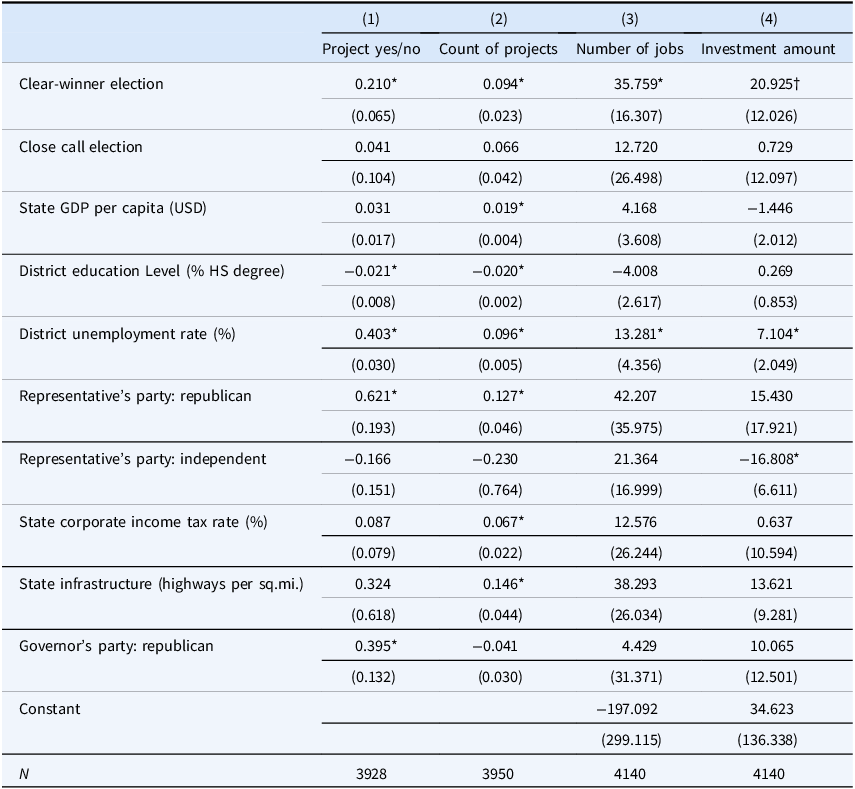

Second, we examine the robustness of our findings by testing alternative operationalizations of the dependent variable. Our main analyses focus on the occurrence of FDI announcements. However, one might reasonably ask whether these patterns extend to more tangible investment outcomes.

To address this, we replicate our analyses using three additional outcomes: the count of projects in a district, the reported volume of investment, and the number of jobs created, all drawn from the same dataset. As shown in Table 3, the results are consistent. Districts with clear-winner elections are not only more likely to attract FDI announcements but also tend to secure larger investment commitments and greater projected job creation. These findings further reinforce our core claim: electoral clarity is associated with stronger and more consequential investment activity.

Likelihood of FDI project vs. investment volume and number of jobs

Note: Results indicate that clear-winner elections positively affect all outcome measures. *p < 0.05, † p < 0.10. All models include district fixed effects.

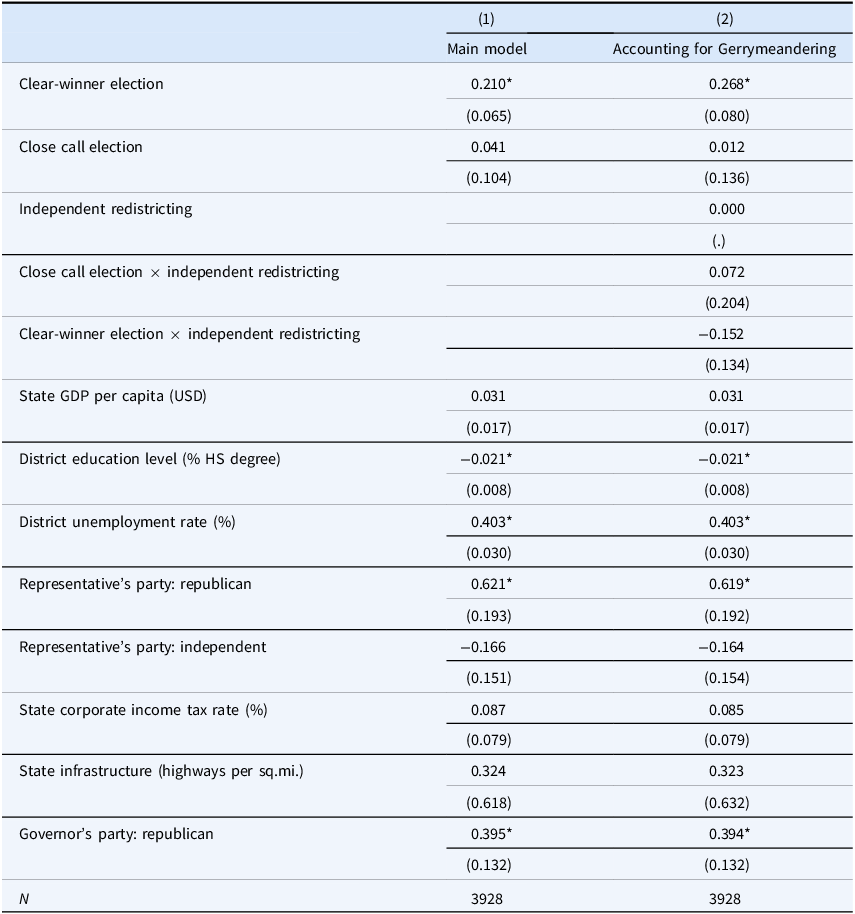

Third, we considered the methodological concern that close-call elections are not randomly distributed across districts. Gerrymandering, for example, may systematically eliminate close-call districts over time. Consequently, there is a possibility that FDI is disproportionately allocated to districts with clear-winner elections due to gerrymandering rather than underlying substantive factors.

We address this concern in two ways. First, we argue that endogeneity is unlikely to be a major issue in our analysis because we employ a conditional logit model, which focuses exclusively on within-district variations rather than cross-district comparisons. This approach estimates how election years correlate with changes in FDI investment announcements within districts characterized by close elections and within districts characterized by clear-winner elections. By design, this method avoids directly comparing close-call and clear-winner districts, thereby mitigating concerns about systematic differences driven by gerrymandering.

Second, approximately one-third of all states implement redistricting procedures specifically designed to prevent partisan gerrymandering. We leverage this variation by re-estimating our main models with an indicator variable for districts located in states with nonpartisan or bipartisan redistricting processes. If gerrymandering were driving the results, we would expect the findings to differ significantly between states with and without such safeguards. However, our results remain consistent across both subsets, reinforcing the robustness of our conclusions (Table 4).

Gerrymandering

Note: The findings show that the effect of electoral competitiveness on FDI announcements is robust to different subsamples. Specifically, clear-winner elections increase the likelihood of FDI announcements both in states where gerrymandering is allowed as well as those where it is not allowed. *p < 0.05. All models include district fixed effects.

Fourth, we test whether state-level political characteristics, rather than district-level electoral competitiveness, drive our results. Two related concerns motivate this test. First, large states such as California, New York, and Texas account for a disproportionate share of U.S. FDI activity and are also lopsidedly partisan, raising the possibility that state-level partisan structure drives FDI cycles rather than district-level electoral predictability. Second, investors might respond to unified state-level government control rather than the predictability of any particular district. We address both possibilities directly. We re-estimate our main specification including (a) a binary indicator for whether one party controls the governorship and both chambers of the state legislature (a “trifecta”), (b) party-specific trifecta indicators, (c) the state-level Cook Partisan Voting Index, and (d) a population-weighted state-level aggregate of district-level Cook scores. Across all four specifications, the coefficient on clear-winner election remains positive and statistically significant. Republican-trifecta states do attract additional FDI, consistent with the broader political geography of inbound investment in the United States, but this state-level effect operates alongside, rather than displacing, our district-level electoral-competitiveness mechanism. Full results are reported in the online appendix.

Fifth, we examine whether the relationship is sensitive to the nationality of the investor. A reasonable conjecture is that investors from countries closely allied with the United States may assess electoral and regulatory risk differently than investors from strategic competitors. We re-estimate our main specification separately for OECD-based and BRIC-based investors. Across both groups, the coefficient on clear-winner election is positive, comparable in magnitude, and statistically significant. Full results are reported in the online appendix.

Sixth, we examine whether our result is driven by the three states that account for the largest share of FDI announcements during our sample period: California, New York, and Texas. We re-estimate our main specification dropping each of these three states individually and then jointly. Across all four exclusion specifications, the coefficient on clear-winner election remains positive and statistically significant. The point estimate is in fact larger when the three highest-volume states are jointly excluded, indicating that our finding reflects a broad pattern across districts rather than an artifact of a small number of high-volume FDI destinations. Full results are reported in the online appendix.

Exploring causal mechanisms

We argue that foreign investors value politicians because they play a vital role in facilitating coordination and serving as access points within the institutional and political networks that investors must navigate. In the context of US. congressional races, MoCs help firms access federal programs, interpret political signals, and assess the feasibility of proposed projects. To evaluate whether the effect we identify operates through this mechanism, we test for evidence that the relationship between electoral competition and FDI announcements is mediated by the role MoCs play in channeling public resources to their districts.

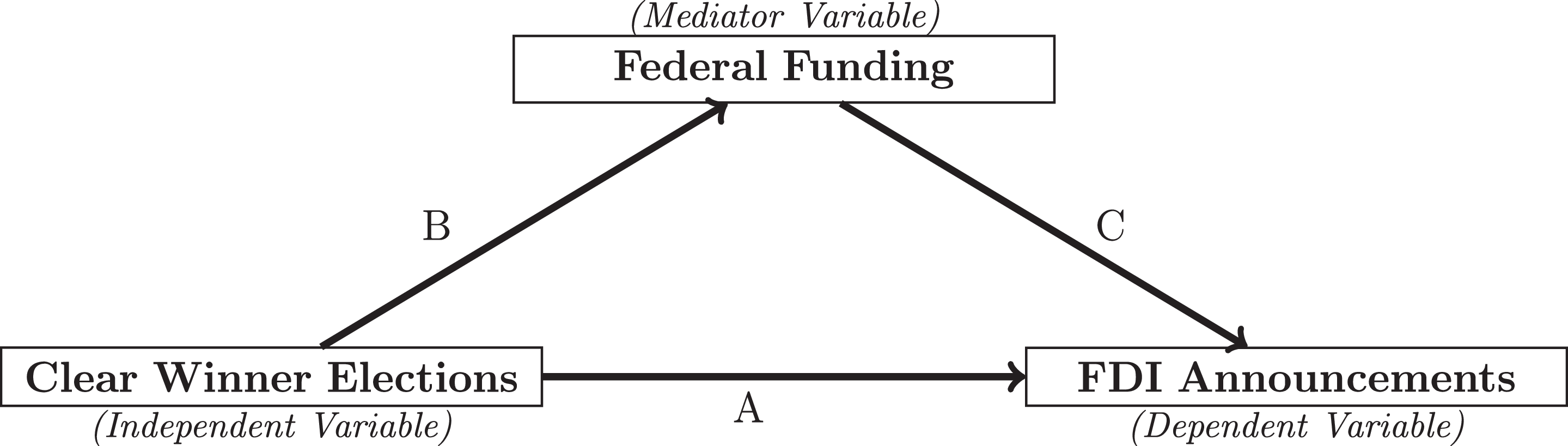

While direct measures of coordination or political signaling are difficult to obtain due to their tacit nature, data on federal spending directed to congressional districts are available. We therefore conduct a causal mediation analysis to assess whether federal appropriations serve as an indirect channel linking electoral predictability to investment announcements. As illustrated in Figure 5, this approach decomposes the total effect of electoral competition on FDI announcements into two parts: a direct effect of competition on announcements and an indirect effect operating through federal funding. If our hypothesized mechanism holds, the mediation pathway via federal spending should yield a positive and statistically significant estimate.

Illustration of a mediation analysis. Mediation Analysis decomposes the total effect of the independent variable on the dependent variable. It determines whether the effect operates primarily through the direct effect (A) or the indirect effect (B and C).

The total effect reflects the overall impact of X on Y, encompassing all potential pathways (i.e., estimating a regression of Y on X without including M). The direct effect captures the impact of X on Y that is not mediated by M (i.e., estimating a regression of Y on X, controlling for M). The indirect effect measures the portion of X’s impact on Y that operates through the mediator M. This indirect effect is calculated as Indirect Effect = (Effect of X on M) × (Effect of M on Y), thereby capturing the pathway in which X affects M, which in turn influences Y.Footnote 44

To evaluate whether electoral competition affects FDI announcements via federal spending, we use grant and contract data from the Federal Assistance Award Data System (FAADS), compiled quarterly by the U.S. Census Bureau. FAADS aggregates award-level data submitted by federal agencies—covering grants, cooperative agreements, and assistance awards under the Catalog of Federal Domestic Assistance (CFDA). Each record includes the fiscal quarter, award amount, CFDA program, recipient type (e.g., congressional district), and geographic location (typically at county level).

We convert these records into an annual, district-level aggregate of “district federal appropriations” (our mediator M). This total includes formula grants, discretionary project grants, and cooperative agreements intended for public goods—such as infrastructure, workforce development, R&D, and broadband. We exclude awards directed to individuals (e.g., Social Security) or procurement contracts, as well as loan instruments and sub-awards routed through state agencies where the ultimate district beneficiary cannot be geolocated. Award amounts are adjusted to 2020 dollars using the CPI and aggregated by fiscal year, which closely aligns with calendar-year patterns of public investment relevant to our FDI announcement timing.

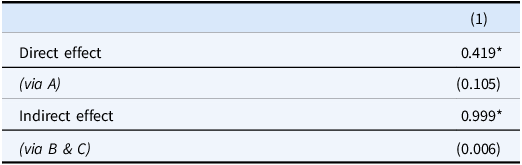

The results of the mediation analysis are summarized in Table 5.Footnote 45 Both the direct and indirect effects are statistically significant and positive. The significant direct effect of electoral competition underscores the pivotal role congressional representatives play in facilitating FDI announcements, in addition to their role in securing beneficial federal funding. These findings also validate the importance of federal appropriations as a mechanism linking electoral competition to investment behavior.

Mediation analysis

Note: Clear-winner elections have both a direct effect on FDI announcement and an indirect effect on FDI announcements through their positive effect on federal funding to the district *p < 0.05.

Conditional effects

In addition to testing the mechanism through which the effect operates, we also explore the conditions under which the effect should be especially pronounced—or absent altogether. To do so, we estimate a series of interaction models designed to assess whether the patterns we observe align with our theoretical expectations. The logic is straightforward: if our proposed mechanism is correct, the effect should be more visible under certain conditions and diminished under others. We estimate four interaction models in total—two focused on characteristics of the FDI projects and two on characteristics of the politicians.

Heterogeneity across FDI characteristics

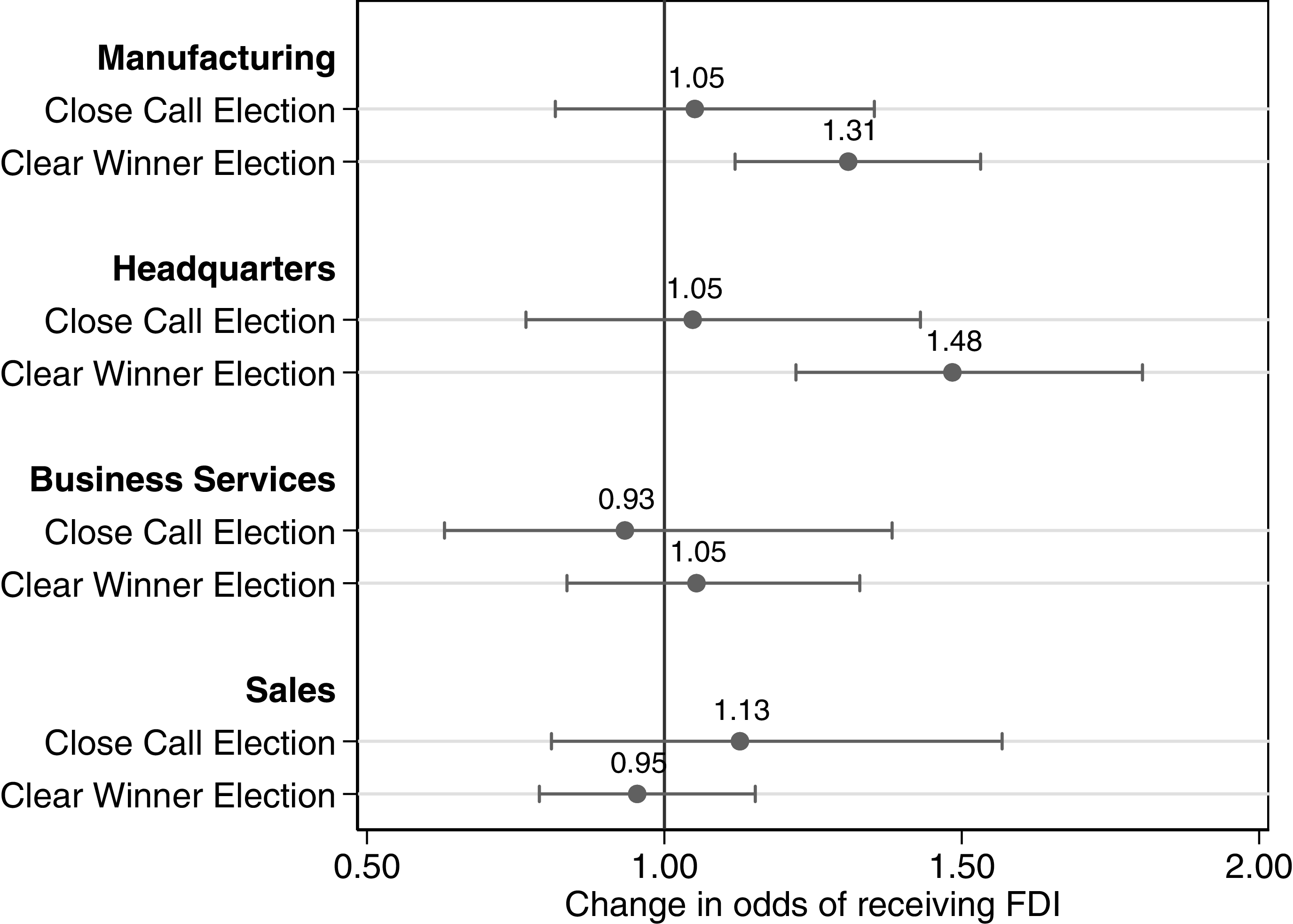

Our first model explores heterogeneity across FDI projects by distinguishing between capital-intensive and non-capital-intensive investments. As our argument suggests, firms are sensitive to potential shifts in the regulatory environment and political access associated with elections—but this sensitivity likely varies depending on the nature of the investment. Projects with high fixed costs, such as the construction of manufacturing facilities or regional headquarters, involve substantial sunk costs and are difficult to relocate once initiated. These types of investments are therefore more vulnerable to political uncertainty. By contrast, less capital-intensive projects—such as call centers or back-office operations—require smaller upfront commitments and can more easily adjust to changing political conditions.

If our theoretical argument is correct, then districts with clear-winner elections should be particularly attractive to capital-intensive investors because they offer a higher degree of political predictability. Moreover, these projects often require larger complementary public goods (e.g., infrastructure or workforce development support), further increasing the value of political stability.

To test this implication, we estimate interaction models using an indicator for project type. As shown in Figure 6, the results support our expectations: capital-intensive investments, including manufacturing sites and headquarters, are significantly more likely to be announced in districts with clear-winner elections. In contrast, less capital-intensive investments show much weaker sensitivity to electoral uncertainty.

Electoral competition and capital intensity.

Note: Firms intending to make investments with high fixed costs are more likely to invest when elections are expected to have a clear winner than firms contemplating investments with low capital requirements. 95% confidence intervals. All models include district fixed effects.

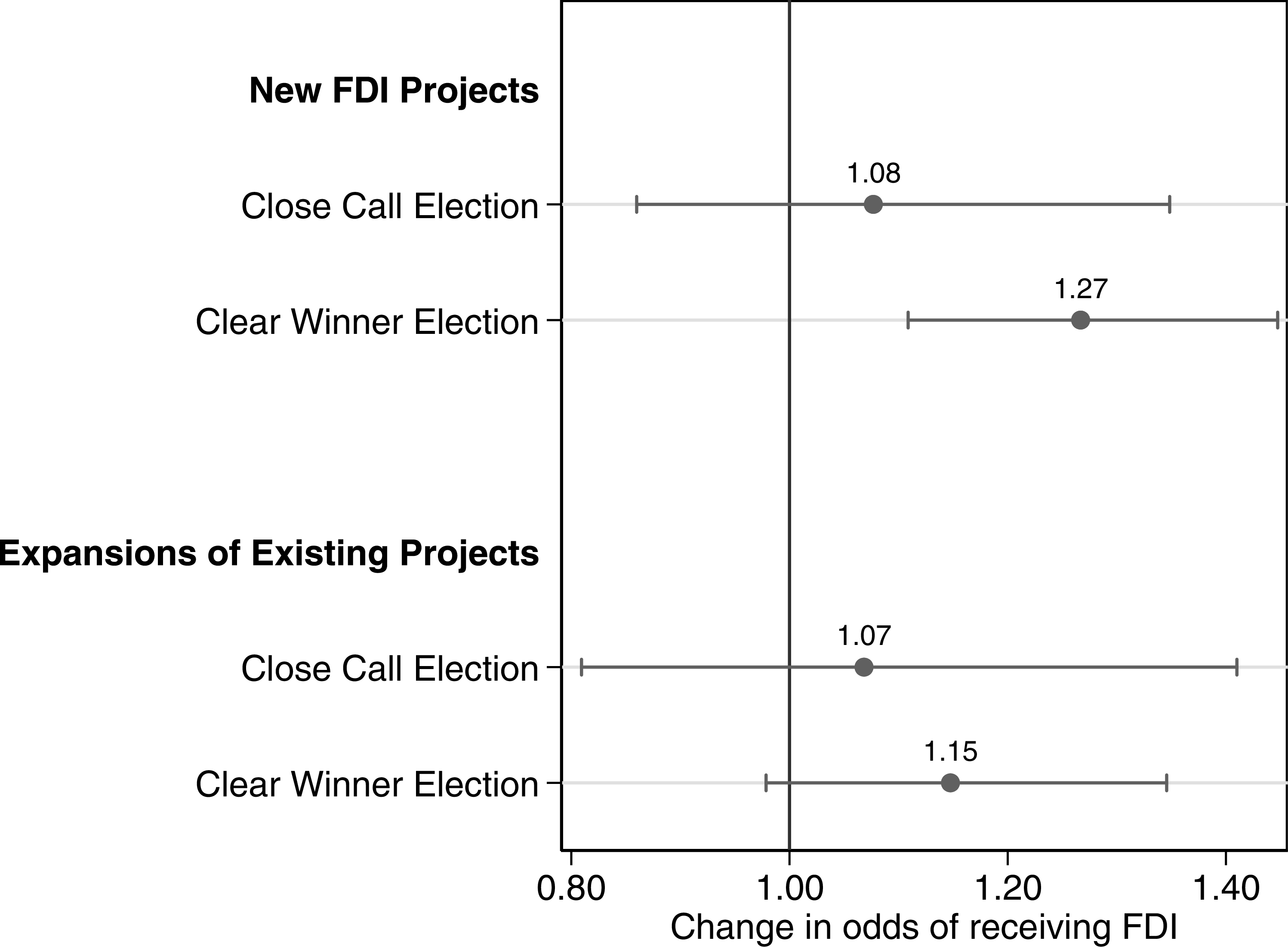

Our second model examines heterogeneity across FDI projects by distinguishing between new greenfield investments and expansions of existing sites. These project types differ in their exposure to political uncertainty. Investors undertaking expansions are already committed to a particular location, having established infrastructure, workforce ties, and institutional familiarity. As a result, electoral uncertainty is less likely to influence their decision-making. In contrast, new greenfield investments can potentially locate anywhere and thus require firms to weigh political risks more carefully. For these investors, electoral predictability becomes a more salient consideration.

To test this implication, we estimate an interaction model that captures the effect of electoral competitiveness on FDI announcements, conditional on whether the project is new or an extension. As shown in Figure 7, we find that close-call elections do not increase FDI announcements for either type of project. However, clear-winner elections are associated with a significant increase in new investment announcements, while the likelihood of expansion projects remains unaffected. This pattern is consistent with our expectation that political stability is especially relevant when firms are making initial location decisions.

Electoral competition and types of investment.

Note: Firms intending to make new investments are more likely to invest when elections are expected to have a clear winner than firms contemplating to expand existing investments. All models include district fixed effects.

Heterogeneity across politicians’ characteristics

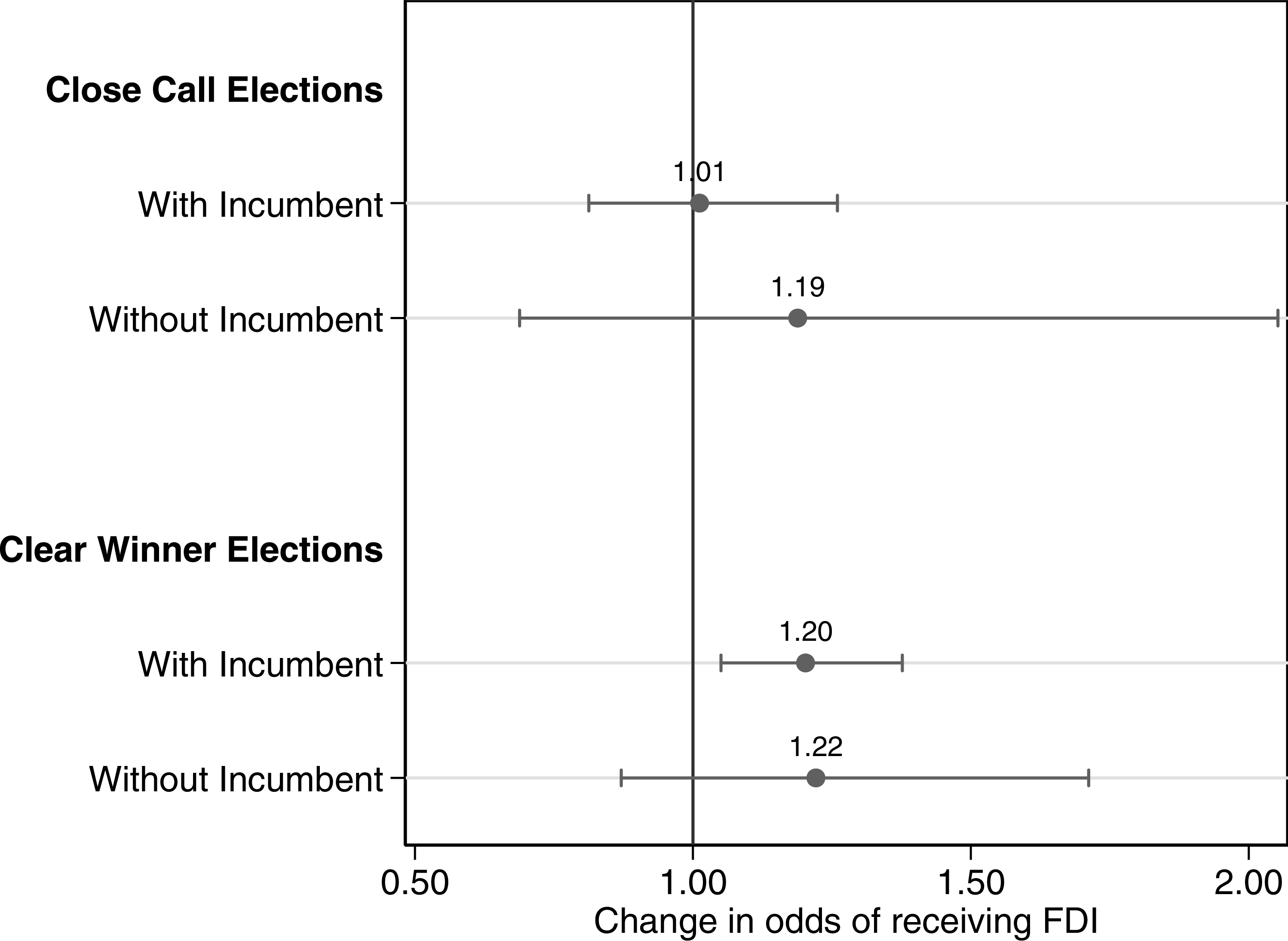

Our third conditional model investigates variation within the category of clear-winner elections, focusing on whether the expected winner is an incumbent or a new, unknown candidate. While our argument emphasizes that firms favor political certainty and stability—explaining the general preference for clear-winner districts—even among these cases, important differences remain. Some clear-winner elections involve well-known incumbents seeking re-election, while others feature open-seat contests where the incumbent has retired, passed away, or lost a primary. In the latter scenario, firms may anticipate the party outcome but still face uncertainty due to the absence of an established political actor.

Firms tend to prefer working with incumbents who have a known policy track record and established relationships, which helps reduce informational uncertainty and ensures more reliable access to the political process. Senior incumbents, in particular, are often better positioned to secure federal resources for their districts—through influence, committee assignments, or familiarity with bureaucratic processes. In contrast, unknown candidates introduce several layers of risk. Their positions on key regulatory issues may be unclear, existing networks of political access are disrupted, and their ability to advocate effectively for district-level support may be untested.

If our argument is correct, we should observe that districts with clear-winner elections only attract greater FDI when the expected winner is a returning incumbent. As shown in Figure 8,Footnote 46 the results align with this expectation: significant increases in FDI announcements are concentrated in districts where the clear winner is an incumbent, while open-seat races—even with predictable outcomes—do not produce a comparable investment response.

Incumbents versus open seats.

Note: Firms consider the variation across expected winners. They are more likely to invest when elections are expected to have a clear winner and if that winner is a known quantity. 95% confidence intervals. All models include district fixed effects.

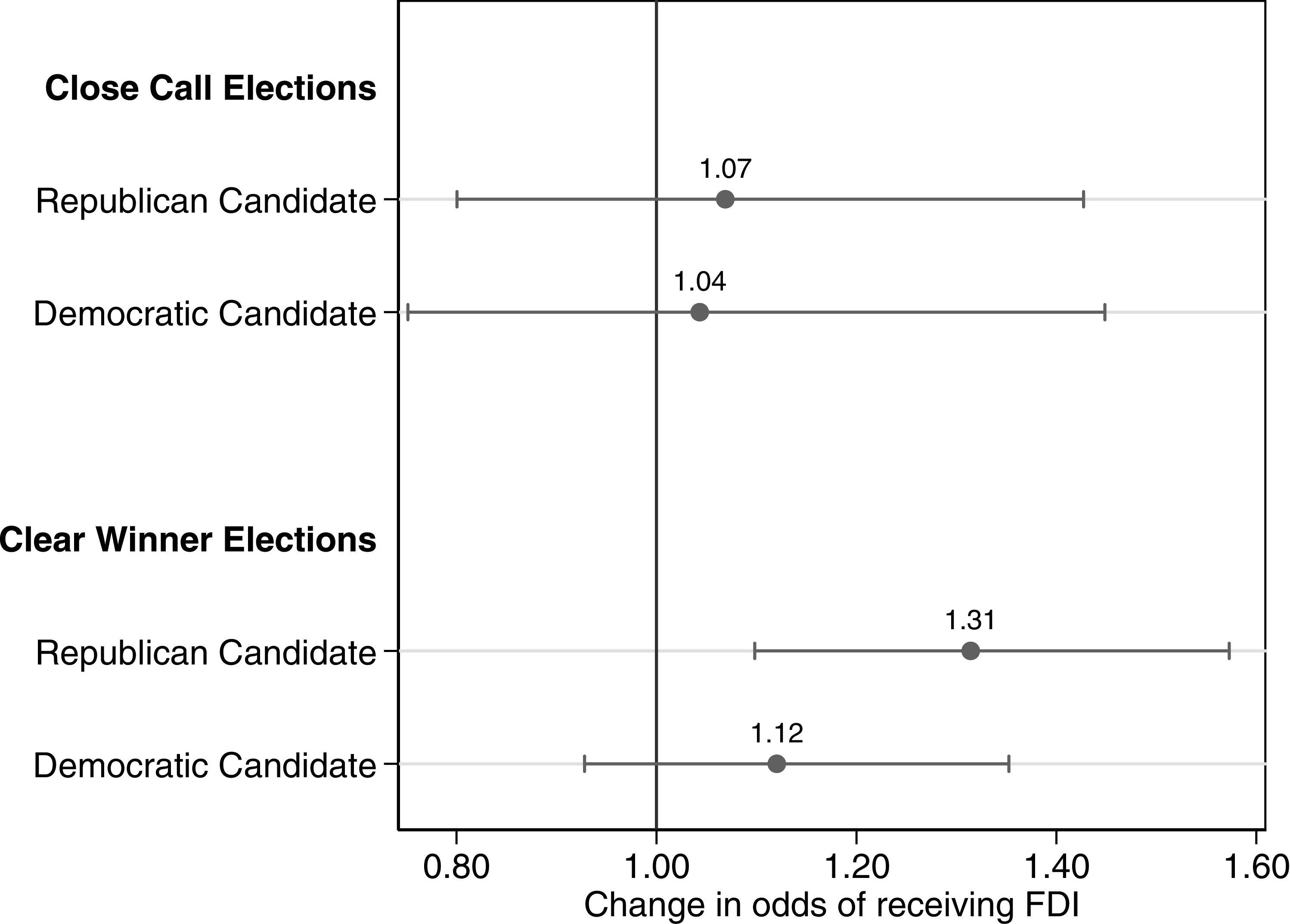

Finally, we examine variation across incumbents, focusing on their partisanship and ideological orientation. As outlined in our theory, firms are drawn to districts with clear electoral outcomes because these provide predictable political representation and stable channels for legislative advocacy. In the U.S. context, such predictability is closely tied to both incumbency and party affiliation. Republican incumbents in safe districts are often perceived as especially business-friendly—due to their reputations for policy stability, deregulatory preferences, and longer average tenures in office.

Empirically, Figure 9 shows that FDI announcements increase significantly in election years only when the expected winner is a Republican incumbent in a clear-winner district. While investors appear to respond to electoral timing overall, this partisan pattern reinforces our core claim: it is not simply the occurrence of an election that matters but the predictability and ideological orientation of its likely outcome.

Democratic vs. Republican incumbent.

Note: Only Districts With elections with expected winners and Incumbent Republicans Receive More FDI Announcements in Election Years. All models include district fixed effects.

Conclusion

In this paper, we use rich, deal-level data on FDI announcements in the U.S. to adjudicate between competing expectations in the CPE and IPE literatures about how foreign firms respond to electoral cycles. On the one hand, political incumbents wishing to generate electoral benefits associated with an influx of new investment are likely to exert more effort and offer more concessionary incentives to MNEs willing to announce investment plans in the months preceding elections. This would suggest that FDI announcements follow a political investment cycle similar to political business cycles in other areas. On the other hand, electoral competition generates uncertainty about future policy environments, and risk-avoidant managers may prefer to delay their investment decisions when the future of political representation remains unclear. Finally, the long-lasting nature of FDI might mean investors simply ignore electoral cycles all together.

Our findings provide robust evidence that electoral predictability shapes where and when foreign firms choose to invest. Our analysis focuses on U.S. congressional elections, which we justify because members of Congress serve as crucial access points—helping investors navigate regulations, access federal resources, and coordinate across levels of government. Across multiple empirical tests, we show that congressional districts with clear-winner elections—those offering political stability and continuity—are significantly more likely to attract FDI announcements in election years. We further demonstrate that this relationship is partially mediated by federal appropriations, suggesting that experienced MoCs play a key role in facilitating investment by directing public resources to their districts. Importantly, the effect is concentrated in capital-intensive and new greenfield projects—investments that are particularly sensitive to political risk—and is strongest when the expected winner is a Republican incumbent.

Our theoretical expectations reach beyond this specific case. Politicians across branches and levels of government all provide important material, informational, and coordinating resources to investors. Therefore, locating investment in areas with stable and friendly political representatives can help firms navigate bureaucratic complexity, gain access to supportive infrastructure, and generally manage political risk. Future research could examine whether and when these findings adhere in different contexts.

The normative implications of our findings are consequential and complex. Foreign direct investment remains a key driver of local economic development and employment, and yet our evidence shows that politically monopolistic districts—i.e., those with little electoral competition—are significantly more likely to attract FDI in election years. In contrast, vibrant electoral contestation appears to constitute a barrier, raising fundamental questions about fairness and democratic equity. This challenges the conventional assumption that foreign investors uniformly prefer pluralistic democratic environments. Instead, many firms appear to associate electoral competition with policy instability, creating a paradox in which democracy—especially in its most dynamic forms—may inadvertently deter economic prosperity under certain conditions.

From a policy standpoint, these dynamics are concerning. Policymakers often rely on high-visibility investment announcements as electoral signals, yet investor aversion to electoral uncertainty in competitive races may undercut such strategies. While incumbents in safe seats might capitalize on announcements, their counterparts facing competitive re-election cannot reliably mobilize investment this way—highlighting a structural imbalance between political contexts.

A final caveat concerns external validity. Our analysis spans the United States from 2003 to 2017, a period characterized by relative institutional stability and a comparatively settled bipartisan consensus on the value of inbound foreign direct investment. We acknowledge that post-2017 political and policy disruptions including heightened polarization, the 2018 expansion of national-security-based investment screening, the proliferation of place-based industrial policy under the CHIPS and IRA Acts, and the rise of ally-shoring as an explicit federal objective may all alter how foreign firms perceive the risk associated with electoral uncertainty and clear-winner incumbency. Whether and how the institutional mechanism we identify continues to operate in this new environment is a productive direction for future research.

Supplementary material

The supplementary material for this article can be found at https://doi.org/10.1017/bap.2026.10026.

Acknowledgements

This paper greatly benefited from the comments by conference participants at IPES, EPSA and SPSA. Any remaining errors are ours.

Competing interests

The author(s) declare none.

Open access

Open access