1 Introduction

The most important international industrial organization innovation over the past half-century is the vertical disintegration of production, with separate stages carried out in different countries. In this study, we label this ‘global production sharing’ (henceforth GPS).Footnote 1 This has replaced the fully integrated, single-country (and typically single-firm) production process with decentralized multi-country operations in which the production process is ‘sliced up’ into separate, highly specialized and tightly integrated supplier networks. Particularly in the electronics, automotive, machinery, and precision-goods industries, it is now common for the final assembled product to consist of components produced in several countries. The cross-border dispersion of production processes is generally organized by large multinational enterprises (MNEs) with subsidiaries or long-term subcontractors in the producing countries. The location of these various suppliers is primarily market-driven: simple, labour-intensive activities are found in lower-wage economies, R&D-intensive activities are located in countries with the necessary scientific base, while final assembly typically occurs in countries that can manage large-scale, diverse production activities for export to the rest of the world.

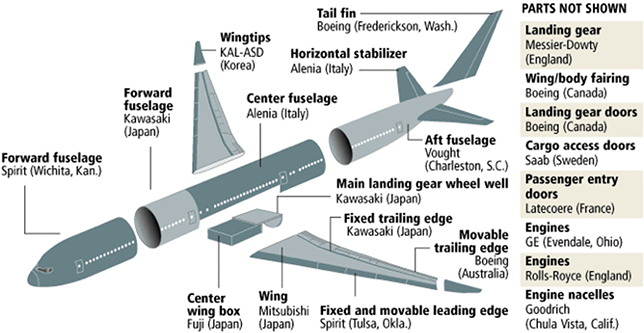

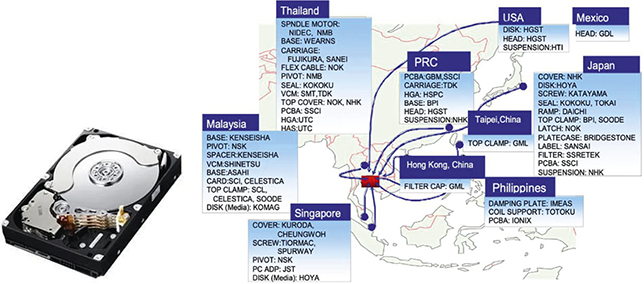

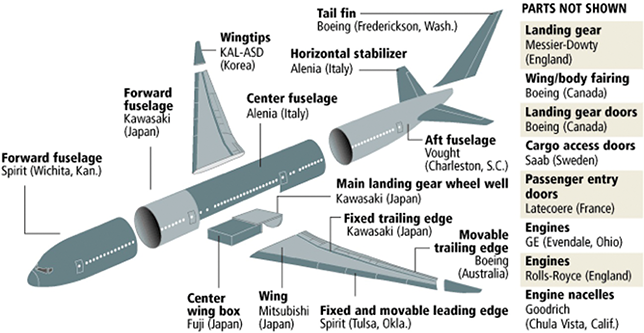

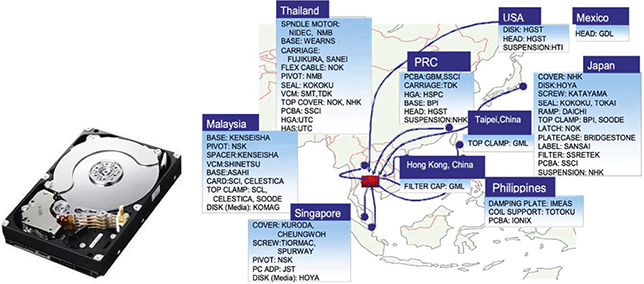

Two eye-catching examples underline the ubiquitous nature of this GPS: the cases of Boeing 787 ‘Dreamliner’ and hard disk drive assembly based in Thailand (Figures 1 and 2). Only about 1% of the components used in the Boeing 707, the first long-distance aircraft produced by Boeing in the early 1950s, were made outside the United States. By contrast, there are 43 parts and components, which accounted for 70% of the total production cost of the Boeing 787, coming from suppliers spread over 135 production sites located in over 20 countries. For example, the wings are produced in Japan, the engines in the United Kingdom and the United States, the flaps and ailerons in Australia and Canada, the fuselage in Japan, Italy, and the United States, the horizontal stabilizer in Italy, the landing gear in France, and the doors in Sweden and France. Boeing is responsible for only about 10% by value (principally the tail fin and final assembly) of the aircraft, even though it holds proprietary rights to the 787 technology. Similarly, a hard disk drive is only one of the many components embodied in a computer. However, hard disk drive assembly plants based in Thailand use components procured from at least ten countries (Hiratsuka, Reference Hiratsuka and Hiratsuka2006).

Boeing 787 Dreamliner

Hard disk drive

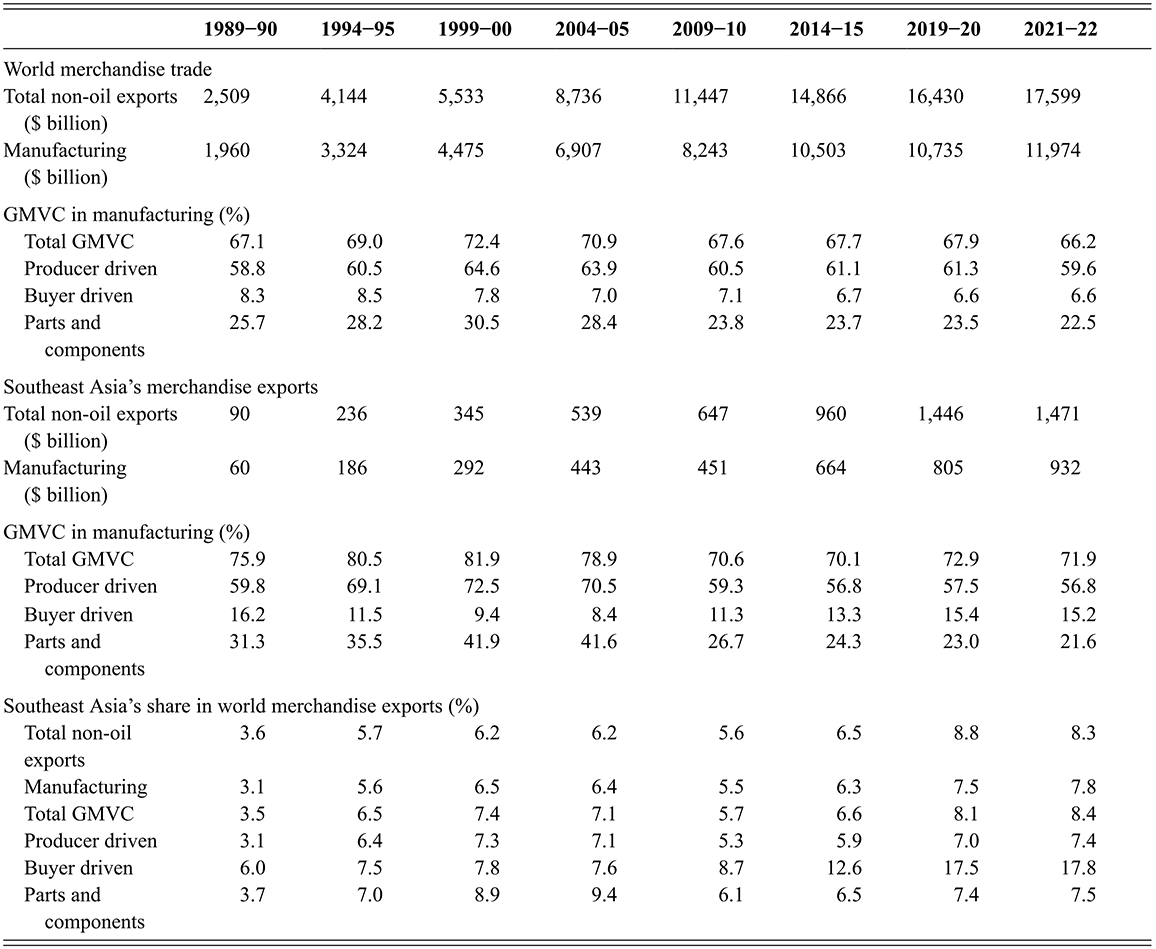

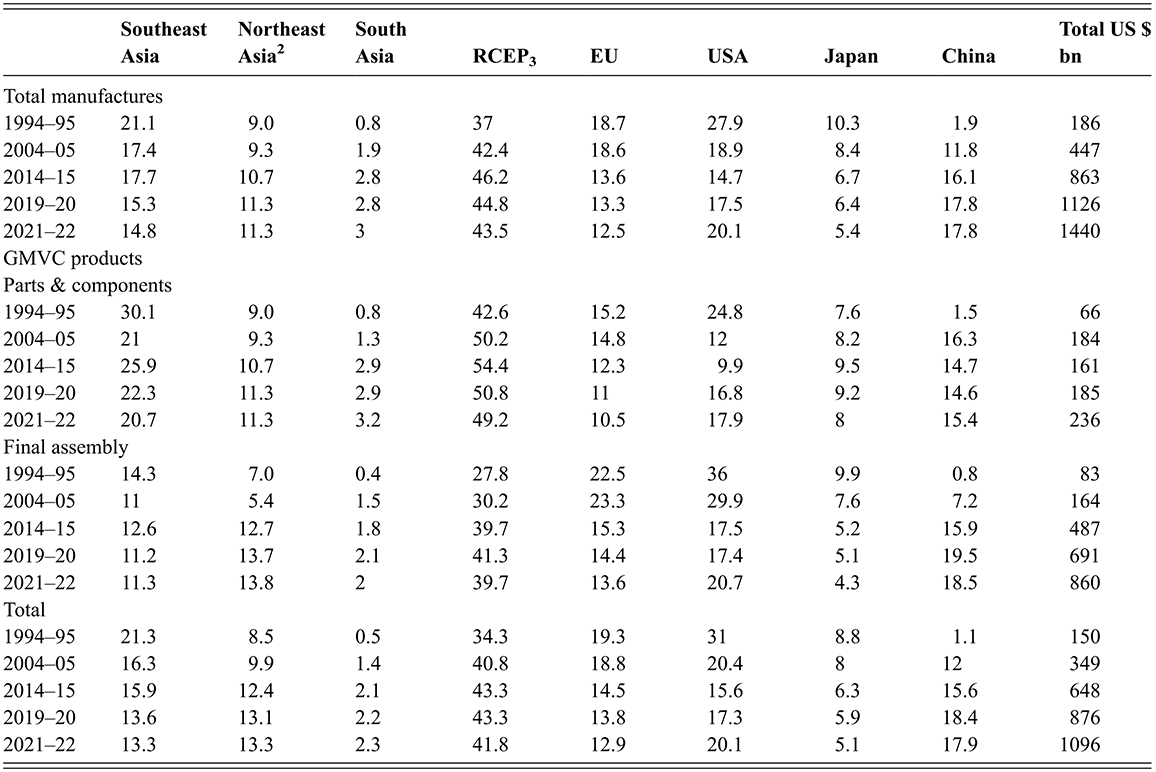

Trade based on GPS, that is trade in parts and components, and final assembly traded within global manufacturing value chains (GMVCs), has been the prime mover of the dramatic shift in the share of manufacturing exports in world trade from developed to developing countries. According to various estimates, trade within GMVCs accounts for half to two-thirds of total world merchandise trade and over two-thirds of manufacturing trade between developing and developed countries (Athukorala, Reference Athukorala2014b; World Bank, 2020). East Asia has been the dynamic core of these global production networks (GPNs). Specialization in specific tasks (‘slices’) in GPNs that fit well with their comparative advantage has played a pivotal role in export-oriented industrialization in these countries, resulting also in an impressive record of poverty reduction through rapid employment generation. China is the central player in these networks. No other country now matches China in scale and range across all but the most technologically advanced niches of manufacturing.

The term GMVC, rather than the widely used term ‘global value chain’ (GVC), is used in this study to reflect its specific focus on global production sharing in manufacturing.Footnote 2 The term GVC, popularized by economic sociologists working on the ‘structure of governance’ (interaction among different actors) involved in the value chain, encompasses both primary products and manufactured goods.Footnote 3 It is important to distinguish GMVC from the broader concept of GVC because, unlike in primary commodity production, manufacturing within GMVCs specifically involves specialization in customized stage-specific tasks (slices) of a given product. Broadening our understanding of the process of industrialization under GPS, therefore, requires systematic analysis of the interplay of country-specific relative cost advantage in this finer division of the production process, and trade and investment policy regimes of individual countries.

Against a backdrop of apparently declining enthusiasm for globalization and open economic policies, there are growing concerns in policy circles as to whether the process of GPS has begun to run out of steam. The prime perceived driver of the diminishing role of GMVCs is technological advancements, in particular industrial automation, robotics, and 3D printing (sometimes referred to as ‘additive manufacturing’) that provide an alternative to offshoring for firms in advanced economies seeking lower labour costs. It is further argued that wage convergence between developing countries and advanced countries is encouraging the ‘reshoring’ of production driven by these technological advancements. The gradual decline in the importation of parts and components for final goods assembly in China as vertical integration of production networks deepens within the country is said to be another reason for the contraction in trade within GMVCs.Footnote 4

The backlash against free trade, rooted in the geo-political rivalry between China and the United States, has contributed to the declining enthusiasm for GPS. The concern is that the global economy may come to be dominated by two substantially non-intersecting commercial worlds, one dominated by the United States and the other by China. This would undermine the liberal, multilateral ‘rules-based’ global commercial architecture that has enabled many developing countries to achieve rapid export-oriented industrialization. The so-called ‘chip wars’ are symptomatic of escalating commercial and strategic disputes among the world’s two economic superpowers. In 2022, the Biden administration promulgated the CHIPS and Science Act which provided approximately $52.7 billion in subsidies and incentives to strengthen and support national security by reducing reliance on foreign chip production, and promote technological leadership by making the United States a more competitive location for chip fabrication.

As the Global Trade Alert monitoring system has documented,Footnote 5 the world has been drifting towards protectionism for at least a decade, nowhere better illustrated than in President Donald Trump’s dramatic ‘Liberation Day’ announcement on 2 April 2025, of wide-ranging, country-specific tariff schedules, with China in particular to be subject to punitive trade barriers. Thus, ‘deglobalization’, ‘reshoring’, ‘on shoring’, ‘friend shoring’, and ‘decoupling’ are now centre stage in any discussion of globalization and international economic relations.

Globalization also has its discontents among so-called ‘left behind’ communities in high-wage economies where jobs have migrated offshore, and where alternative employment opportunities and social supports are minimal, exemplified and amplified for example in the ‘Hillbilly Elegy’ narrative (Vance, Reference Vance2016). The vaccine nationalism and supply disruptions that arose during the Covid-19 pandemic have added further weight to the arguments of the globalization sceptics, and to those who argue for greater national economic ‘self-reliance’. It is therefore not surprising that the Doha development round failed, that ‘trade-lite’ bilateral and regional trade agreements have proliferated, that the two economic superpowers are proposing alternative mega trade deals,Footnote 6 and that the World Trade Organization has been significantly disenfranchised. As a result, ‘Globalization [and] … free trade [are] almost dead’ declared Morris Chang, the founder of one of the most important companies in these networks, Taiwan Semiconductor Manufacturing Company, in December 2022.Footnote 7 Following the announcement of the proposed Trump tariff schedules, Singapore Prime Minister Lawrence Wong stated that the global order characterized as ‘one where rules-based globalisation and free trade is over’, and in its place is an order that is ‘more arbitrary, protectionist, and dangerous’.Footnote 8

There is also the structuralist school of thought, whose origins predate the recent views on limits to GPS, which emphasizes the limits to industrial upgrading through GMVC participation. The traditional horizontal specialization, so the argument goes, requires a country to develop a deep industrial base before achieving export success. Under industrialization based on the conventional horizontal specialization, that is, producing a good from beginning to end within a given establishment, a nation must develop a deeper industrial base encompassing all stages of the production process before successfully entering export markets. When a country specializes in a specific segment of the value chain, industrial upgrading is presumably constrained by the dictates of the ‘lead firm’. In addition, when stages of production are geographically dispersed, it is argued that the learning will be similarly dispersed, setting a limit on future technology transitions in a country within the production networks (Baldwin, Reference Baldwin, Feenstra and Taylor2014; Szirmai et al., Reference Szirmai, Naudé, Alcorta, Szirmai, Naudé and Alcorta2013; Doner & Schneider, Reference Doner and Schneider2016).

This view, which is also at the centre of the so-called ‘middle-income trap’ debate, has led in recent years to a revival of the old policy advocacy of selective intervention designed to develop infant industries and to foster their achievement of international competitiveness through rapid attainment of the required technological capabilities (Amsden, Reference Amsden2001; Westphal, Reference Westphal2002; Lall & Narula, Reference Lall and Narula2004; Lin & Monga, Reference Lin and Monga2010; Cantore et al., Reference Cantore, Clara, Lavopa and Soare2017). According to this reasoning, the most effective strategy is to build national champions along the lines of the Korean (and earlier Japanese) approach, employing an export-oriented strategy built upon restrictive trade and FDI regimes. Otherwise, it is further argued, a ‘passive’ approach to economic liberalization will simply result in ‘dead end’ or ‘sunset’ industries, with mobile foreign firms forever in search of cheaper labour or more attractive fiscal concessions in other locations.

The purpose of this Element is to contribute to this policy debate by analyzing Southeast Asia’s engagement in GMVCs in the context of the wider literature on the role of GMVCs in industrial transformation in developing countries. Global production sharing has been a major factor in the economic dynamism of this region. Featuring both broad similarities and notable diversity among countries in their engagement with GPNs, the Southeast Asian region provides an ideal laboratory for comparative analysis of these issues. These countries display great variety in their role within GPNs due in large part to differences in resource endowment, timing of policy reforms, stages of development, and the pace and extent of global economic integration. Despite rapid growth, there are significant differences in wages among the countries. Nevertheless, manufacturing wages in all countries in the region other than Singapore remain lower than in countries in the European periphery and most of Latin America.Footnote 9 This relative labour cost advantage, coupled with the region-wide embrace of the MNE-led development strategy and improvements of trade-related infrastructure, has made the region attractive for the cross-border spread of production networks.

An interpretive survey of the sizeable literature on policy shifts and export-oriented industrialization centred on joining GPNs provides the context for this study. Against this backdrop, a comparative empirical analysis of changing patterns of countries’ engagement in GPS and its implications for industrial upgrading is undertaken. The empirical analysis comprises three main components: a comparative analytical narrative of the Southeast Asian countries’ engagement in GPS; an analysis of the determinants of (factors driving) trade flows; and an analysis of the impact of GPS on the performance of domestic manufacturing in Southeast Asian countries with emphasis on industrial upgrading. This three-pronged analysis is undertaken in the broader global context of evolving patterns of GPS with a focus on contemporary policy debates on the limits to GPS as a prime mover of export-oriented growth in developing countries.

Our organization is as follows. Section 2 provides an analytical overview of the process of GPS and GMVCs, policy options and measurement of GMVC trade. Section 3 examines Southeast Asia’s economic development and the evolution of its policy regimes. In Section 4, we provide a detailed empirical analysis of Southeast Asia’s engagement with GPS, supplemented in Section 5 by an assessment of broader host-economy effects on employment and structural change. Section 6 concludes and draws out some general inferences.

2 The Process of Global Production Sharing

2.1 The Phenomenon of Global Production Sharing

Global production sharing is not a new phenomenon. There is ample anecdotal evidence of evolving trade in parts and components within branch networks of MNEs dating back to the early twentieth century (Wilkins, Reference Wilkins1970). Based on his extensive early research into US manufacturing, Allyn Young (Reference Young1928, p. 538) observed the emergence of ‘an increasingly intricate nexus of specialised undertakings … inserts itself between the producer of raw materials and the final products’. Kindleberger (Reference Kindleberger1967, pp. 108–109) wrote about growing trade in ‘semi-finished material’ (parts and components) between the Ford plants at Limburg in Belgium and Cologne in Germany in the mid-1960s. He used this example to question the validity of the conventional approach to analyzing the trade-growth nexus which was ‘developed almost entirely on the basis of trade in final products – that is, goods wholly produced in one country and consumed in another’. The US MNEs operating in the Australian automotive industry were found to be importing parts and components for local assembly operations and exporting some parts and components produced in Australia within their global networks from the early 1950s (Brash, Reference Brash1966).

What is unprecedented about the contemporary process of GPS over the past seven decades or so is its wider and ever increasing product coverage, and its rapid spread from mature industrial countries to developing countries. Over the past four decades, production networks have gradually evolved encompassing many countries and spreading to many industries such as sporting goods, garments, footwear, automobiles, televisions and radio receivers, sewing machines, office equipment, electrical machinery, machine tools, cameras, watches, light emitting diodes, solar panels, and surgical and medical devices. In general, industries with the potential to break up the production process without significantly increasing transport costs are more likely to move to peripheral countries.

At the formative stage of international product fragmentation, outsourcing predominantly took the form of locating small fragments of the production process in a low-cost country and re-importing the assembled components to be incorporated into the final product. Over time, the fragmentation process expanded to involve many countries in the assembly process at different stages, resulting in multiple border crossings of product fragments before getting incorporated in the final product. From about the late 1970s, there were two other important developments in the process, setting the stage for the rapid expansion in the share of fragmentation-based trade in world trade.

First, as an outcome of advances in modular production technology, some fragments of the production process in certain industries have become ‘standard fragments’ that can be effectively used in a number of products. Examples include long-lasting cellular batteries, originally developed by computer producers and now widely used in cellular telephones and electronic organizers; transmitters, which are now used not only in radios (as originally designed) but also in PCs and missiles; and semiconductors (also called integrated circuits or chips), which have spread beyond the computer industry into consumer electronics, motor vehicle production, and many other product sectors (Jones, Reference Jones2000; Jones & Kierzkowski Reference Jones, Kierzkowski, Arndt and Kierzkowski2001a; Brown et al., Reference Brown, Deardorff, Stern, Baldwin and Winters2004).

Second, there has been a noteworthy expansion of the coverage of global assembly operations from component production and assembly to assembly of final products (e.g., computers, cameras, TV sets, motor cars, and medical devices). In final assembly, labour costs, while significant, are of secondary importance compared with the availability of world-class operators; technical and managerial skills; a good domestic basis of supplies and services; relatively free access to world-priced inputs, including capital; and excellent infrastructure. In other words, the locational decisions of MNEs in this sphere depend on the availability of a wider array of complementary inputs that enable their facilities to be efficient by world standards. In addition, given the heavy initial fixed costs, MNEs are hesitant to establish overseas plants in final assembly without considerable first-hand commercial experience in the host country. For these reasons, overseas production units of MNEs involved in such final-stage assembly are located in countries that are at an advanced stage in the engagement in GPS. Thanks to the dramatic industrial transformation over the past three decades, China has now become the premier assembly centre within GMVCs.

As production operations in the host countries became firmly established, MNE subsidiaries began to subcontract some activities to local (host-country) firms, providing the latter with detailed specifications and even fragments of their own technology. Over time, many firms, which were not part of original MNE networks, have begun to undertake final assembly by procuring components globally through arm’s-length trade, benefitting from the ongoing process of standardization of parts and components.

These developments suggest that an increase in production-sharing-based trade may or may not be accompanied by an increase in the host-country’s stock of FDI (Jones, Reference Jones2000; Brown et al., Reference Brown, Deardorff, Stern, Baldwin and Winters2004). However, there is clear evidence that MNEs are still the leading vehicle for countries to enter GPNs. In particular the presence of a major MNE in a particular country is vital, both as a signalling factor to other foreign firms less familiar with that country and as an agglomeration magnet for the development of new cluster-related activities and specialized support services (Wells & Wint, Reference Wells and Wint2000; Ruwane & Gorg, Reference Ruwane, Gorg, Arndt and Kierzkowksi2001; Dunning, Reference Dunning2009).

In recent years, the popular press has begun to focus on whether GPS is ‘running out of steam’ due to the phenomenon of reshoring (also termed reverse offshoring or onshoring) – the shifting by MNEs of manufacturing facilities from overseas locations back to their home countries. This issue has gained added momentum amid the ongoing China–US geopolitical tensions and the ‘bringing manufacturing back home’ initiatives promoted under the Trump administrations. Several high-profile cases of US MNEs reshoring (or planning to reshore) assembly processes from China to plants in the United States, and some MNEs from the advance emerging economies setting up operations in the United States have received extensive media coverage. However, it remains to be seen whether this represents a structural, long-term shift or merely a temporary response to favourable financial incentives that attract media attention against a backdrop of political rhetoric. Moreover, the operations of multi-billion-dollar semiconductor factories recently established in the United States by MNEs from advanced emerging economies rely heavily on both local manpower and managerial know-how, while maintaining downstream assembly and packaging processes in their home countries. This adds a new dimension to GMVCs rather than diminishing their dynamism (Miller, Reference Miller2022).

A related issue concerns the implications of the Fourth Industrial Revolution (IR4) – the convergence of digital technology with breakthroughs in materials science and biotechnology – particularly in terms of the potential substitution of human tasks in GMVCs by artificial intelligence (AI), robotics, and 3D printing (additive manufacturing). Most of these innovations are still in their infancy, and the full extent of their transformative impact remains uncertain. So far, the early signs of IR4 have remained largely confined to mature industrial economies. While in principle almost all production processes can be automated, the actual incidence of automation depends on relative costs, which vary with the complexity and bulkiness of products. Additionally, some elements of IR4 may have positive effects on GPS by reducing service-link costs and stimulating aggregate world demand for GMVC-related products, including the emergence of entirely new ones.

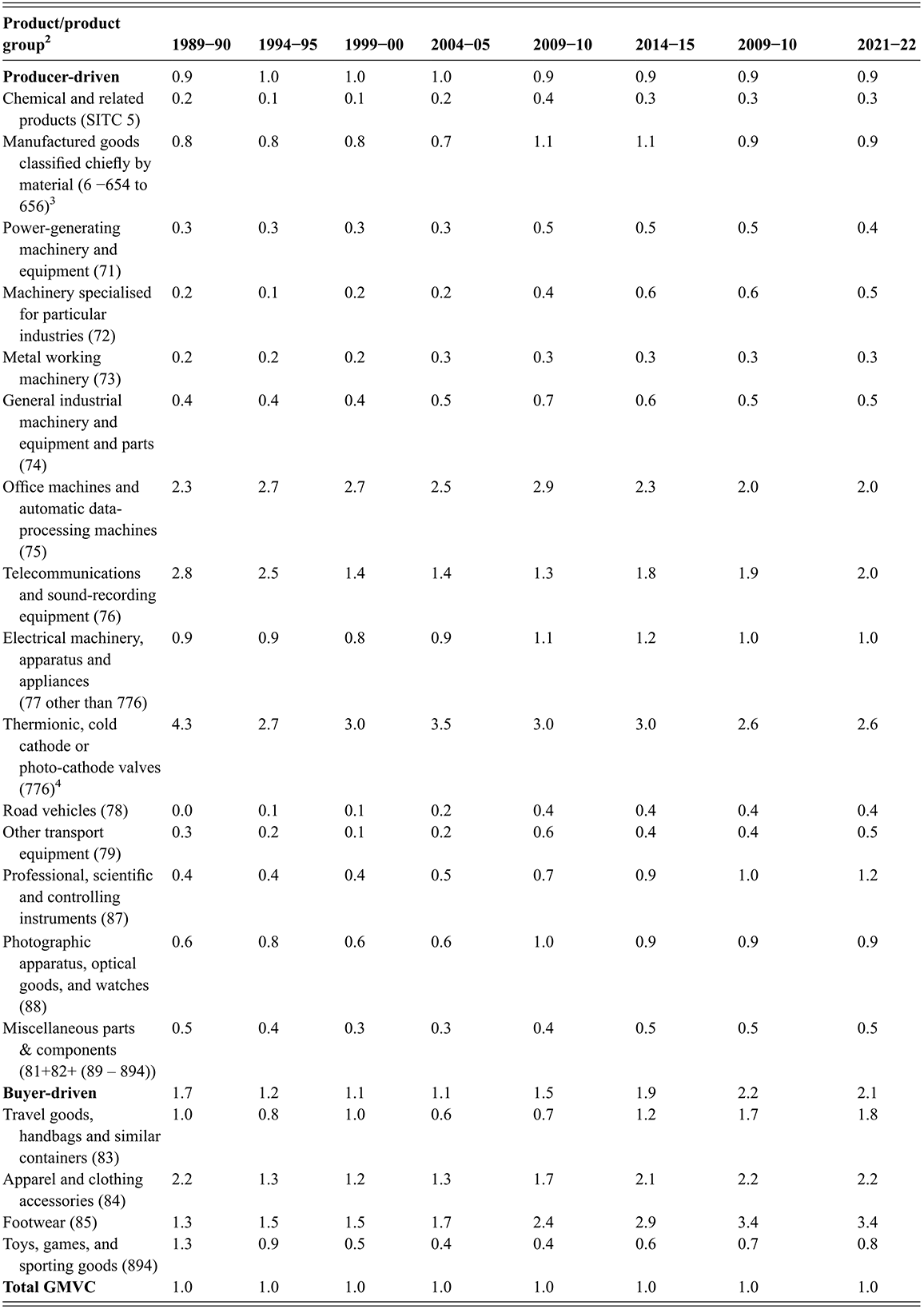

2.2 Typology of GMVC Trade

GMVCs are complex and diverse cross-border trading arrangements, ranging from arm’s-length, one-off commercial transactions through to long-term, vertically integrated, intra-firm transactions. In terms of the organizational structure of production sharing, GMVCs take two major forms: buyer-driven production networks and producer-driven production networks (Gereffi, Reference Gereffi1999).

Buyer-driven GMVCs are common in consumer goods industries with relatively standardized technologies, such as clothing, footwear, travel goods, toys, and sport goods. The ‘lead firms’ in such production networks are the international buyers: large retailers such as Walmart, Marks & Spencer, H&M or brand manufacturers such as Victoria’s Secret, Gap, Zara, Nike, Adidas, and Calvin Klein. A relatively recent major international player is the China-based (but now Singapore head-quartered) fashion manufacturer Shein. Production sharing within them takes place predominantly through arm’s-length relationships, with global sourcing companies (value-chain intermediaries) playing a key role in linking producers and lead firms (Keesing, Reference Keesing1983; Ganapati, Reference Ganapati2025). Therefore, there is room for local firms to directly engage in export through links established with foreign buyers, without the direct involvement of foreign investors. If foreign investors are involved, usually it is through joint ventures with local entrepreneurs, rather than by forming fully owned subsidiaries. The lead firm monitors input procurement, but there is room to use domestic inputs that meet the quality standards. As the East Asian experience indicates, joining buyer-driven production networks is a promising start for export-oriented industrialization. Producer-centred GMVCs are common in vertically integrated global industries such as electronics, electrical goods, automobiles, and scientific and medical devices. In these networks, the ‘lead firms’ are MNEs, such as Intel, Motorola, Apple, Toyota, and Samsung. Global production sharing takes place predominantly through the lead firms’ global branch networks and/or their close operational links with established contract manufacturers that undertake assembly for these global corporations.

In these high-tech industries, production technology is specific to the lead firm and is closely protected to limit imitations. Also, the production of final goods requires highly customized and specialized parts and components, whose quality cannot be verified or assured by a third party. Therefore, the bulk of GPS takes place through intra-firm linkages rather than in an arm’s-length manner. This is particularly the case when it comes to setting up production units in countries that are newcomers to GPNs. As the production unit becomes well established in the country and forges business links with private- and public-sector agents, arm’s-length subcontracting arrangements for components procurement could develop, depending on the conduciveness of the domestic business climate. However, the overall production process is continued to be governed by the lead firm.

The emergence of contract manufacturers – third-party companies hired by other businesses to produce goods or components according to specific client requirements – in the 1990s, and their renewed momentum since then, represents a significant development in the governance structure of producer-driven GPNs (Sturgeon, Reference Sturgeon2002). This new breed of MNEs arose from the modularization of production processes within GMVCs, enabling the formation of global supply networks based on standardized product designs.

Contract manufacturers initially emerged in the information and communication technology sector (e.g., Foxconn, Jabil, Pegatron, and Quanta) and later expanded into the pharmaceutical and medical device industries (e.g., Protech, Tele Links, Vasudha, and Welkin). These MNEs enable lead firms in GMVCs to focus on their core competencies, such as product design, specification, and marketing, while outsourcing manufacturing activities under strict oversight in terms of quality, cost, and third-party component procurement. For instance, Apple Inc. has developed a captive governance relationship with the Taiwanese firm Foxconn, which has long assembled nearly all iPhones and most of its other products (McGee, Reference McGee2025).

2.3 Drivers of Global Production Sharing

The expansion of GPS has been driven by three mutually reinforcing developments (Jones, Reference Jones2000; Jones & Kierzkowski, Reference Jones, Kierzkowski, Arndt and Kierzkowski2001, Reference 95Jones, Kierzkowski, Dornbusch, Calvo and Obstfeld2004; Yi, Reference Kei‐Mu2003; Helpman, Reference Helpman2011). First, rapid advancements in production technology have enabled the industry to slice up the value chain into finer, ‘portable’ components. As discussed, advances in modular production technology have made some components of the production process in certain industries ‘standard fragments’, which can be effectively used in several products.

The second factor has been the ‘death of distance’, the declining costs of international transport and telecommunications. Technological innovations in communication and transportation have shrunk the distance that once separated the world’s nations, and improved the speed, efficiency, and economy of coordinating geographically dispersed production processes. This has facilitated, and reduced the cost of, establishing ‘service links’ needed to combine various fragments of the production process across countries in a timely and cost-efficient manner. More efficient, internationally oriented logistics systems with ‘just-in-time’ inventory systems have facilitated the timely and speedy delivery of components between major production sites. Air freight has become increasingly common in the case of high-value/low-weight componentry (Hummels, Reference Hummels2007).

Third, liberalizing policy reforms across the world over the past four decades have considerably reduced barriers to trade and FDI. Trade liberalization is far more important for the expansion of GPS trade compared to the conventional horizontal trade. This is because a slice/task of the production chain operates with a smaller price-cost margin, and the profitability could be erased by even a small tariff. To operate effectively, these global networks require a liberal business environment for all participating firms; they especially require the unhindered movement of goods across international boundaries. Participating countries also need to be signatories to the WTO Information Technology Agreement (ITA) and similar trade-facilitating measures.Footnote 10

There is an important two-way link between improvements in communication technology and the expansion of production sharing within global industries. The latter contributes to lowering the cost of production and rapid market penetration of the final products through enhanced price competitiveness. Scale economies resulting from market expansion in turn encourage new technological efforts, enabling further product fragmentation. This two-way link has set the stage for GPN trade to expand more rapidly compared to conventional commodity-based trade (Jones, Reference Jones2000).

2.4 Policy Issues

Global production sharing and the expansion of GMVCs open new opportunities for developing countries and transition economies to participate in a new international division of labour. For instance, a country need not set up a motor vehicle plant to benefit from the growth of the automobile industry. It is enough to be competitive in the production of a single part.

At the early stages of international product fragmentation, some observers were sceptical about prospects for developing countries to rely on this form of international specialization for export expansion. They predicted that the process would be reversed because of the rapid automation of production processes in developed countries (see Frobel et al., Reference Frobel, Heinrichs and Kreye1980; Cantwell, Reference Cantwell, Greenway and Winters1994). In many high-tech industries (notably electronics and electrical products), however, rapid innovation and continuous technical change, which bring about a constant cycle of change and obsolescence, are formidable constraints on rapid automation as an alternative to offshore assembly. Therefore, the indications are that this form of internationalization of production will continue to expand, providing countries with the opportunity to find new niches for labour-intensive, export-oriented production (depending, of course, on their ability to provide an enabling domestic economic environment). Thus, international product fragmentation presents a challenge to those who believe in the so-called fallacy-of-composition argument against export-led industrialization in developing countries.

Capital, managerial know-how, and technology are highly mobile within GMVCs. Therefore, the availability of labour at competitive wages is a crucial determinant of a country’s participation in production sharing and specialization in different stages of the production process. The labour intensity of the given segments and the relative prices of factor inputs in comparison with their productivity jointly determine which country produces what tasks within a production network. It may be that workers in a given country tend to have different skills from those in other countries, and the skills required in each production block differ so that a dispersion of activity could lower marginal production cost. Alternatively, it may be that the production blocks differ from each other in the proportion of different factors required, enabling firms to locate labour-intensive production blocks in countries where productivity-adjusted labour cost is relatively low. In the initial stages, the availability of trainable unskilled labour and middle-level supervisory or technical manpower is key factor. Over the medium to long term, the presence of highly skilled technical and managerial personnel becomes essential for moving into higher-value segments of the value chain. Human capital development is, in part, endogenous to a country’s engagement in GMVCs (Jones, Reference Jones2000).

However, the availability of labour at competitive wages alone does not determine a country’s attractiveness to investors within GMVCs. Comparative advantage rooted in the labour endowment must be complemented with the advantage of ‘service link cost’ involved in GPS (Jones & Kierzkowski, Reference Jones, Kierzkowski, Arndt and Kierzkowski2001; Golub et al., Reference Golub, Jones and Kierzkowski2007). Here, the term service links refers to arrangements for connecting and coordinating activities in a smooth sequence to produce the final good within the production network. Service link cost in a given country depends on a whole range of factors impacting on the overall business environment: trade-related infrastructure and logistics, political stability and policy certainty, institutions, including property right protection and enforcement of contracts, and liberal trade and investment policy regimes. Unlike those involved in light consumer goods industries, foreign firms engaged in vertically integrated assembly industries are particularly sensitive to political stability because disruptions in one production base in the value chain disturb the entire value chain, and because they view investment risk from a long-term perspective.

The policy regime and the domestic investment climate also need to be conducive for involvement in production sharing. The decision of a firm to outsource production processes to another country – either by setting up an official company or establishing an arm’s-length relationship with a local firm – entails ‘country risks’. This is because supply disruptions in a given overseas location could disrupt the entire production chain. Such disruptions could be the product of shipping delays, political disturbances, or labour disputes (in addition, of course, to natural disasters). In many instances, it is impossible to fully offset these risks simply by writing complete contracts (Spencer, Reference Spencer2005; Helpman, Reference Helpman2011).

In the distinction between buyer-driven and producer-driven GMVCs, it is important to understand the policy options for effective participation in GMVCs and to assess the resulting implications for the economic development process. In the case of buyer-driven GMVCs, such as in garments, footwear and toys, for example, labour costs are a major determinant of industrial location, particularly for low-end, standardized products. For this reason, low-income countries such as Bangladesh and Cambodia have become major international suppliers. Low wages are of course a necessary but not sufficient condition for export success. Garment producers also require efficient duty drawback customs arrangements (since the cloth is very often imported), skilled supervisory and technical labour, and tolerably efficient infrastructure services and export-import procedures. Preferential market access arrangements sometimes also play a marginal role, a reflection of the residual impacts of the once pervasive international regulation of textiles and garments trade under the now abolished Multi-Fibre Agreement.

In the case of producer-driven networks, high-quality international logistics and an open FDI regime are more significant determinants of industrial location. This explains the success of Singapore and Malaysia, always relatively high-wage economies, in electronics, whereas they have been minor players in the garments and footwear industries. As noted, both these countries were early movers in export-oriented, FDI-led industrialization. Once these countries established international export reputations in the electronics industry, MNE investors have tended to be relatively immobile, since the costs of relocation are substantial, more so arguably than is the case for garments, especially in the latter case where there is no equity investment. Investors in electronics have also been willing to upgrade their operations to more advanced technologies if the domestic business environment is attractive.

2.5 Measurement of GMVC Trade

Global production sharing ‘calls for a change in the analytical and statistical tools we use to measure and understand the real world’ (Lamy, Reference Lamy2011). As production processes become increasingly fragmented across a wide range of industries and countries, the conventional approach to analyzing trade patterns – treating international trade as an exchange of goods produced entirely within each trading partner – is rapidly becoming obsolete.

There are two main methods to measure GMVC trade: (1) delineating GMVC trade from standard official (customs-record-based) trade data at a sufficiently disaggregated level, and (2) using global input-output tables to break trade into domestic and foreign value-added components, then using the latter to assess a country’s engagement in global production. As we will see next, given the current state of trade and national income data, these two approaches are complementary rather than mutually exclusive methods for understanding the extent and patterns of GMVC trade.

2.5.1 Trade Data Analysis

By the late 1960s, there were clear indications from the global operations of manufacturing firms in advanced countries that GPS was poised to become an increasingly important aspect of the evolution of global production and trade patterns. At that time, the national trade data reported under the first version of the United Nations’ Standard International Trade Classification (SITC) system did not allow for the separation of trade related to GPS from overall reported trade figures. As a result, early studies relied on trade data maintained by OECD countries – particularly the United States and the European Union – in connection with special tariff provisions for overseas processing and the assembly of domestically produced components. These are commonly referred to as outward processing trade (OPT) statistics (van Dam, Reference Van Dam1971; Helleiner, Reference Helleiner1973; Sharpton, Reference Sharpston1975). OPT records provide data on parts and components exported from source countries and the assembled goods received in return.

However, the OPT schemes covered only a limited range of products, and their actual product coverage has varied significantly over time, both within and across countries. More importantly, recent trends – such as unilateral trade and investment liberalization, as well as the proliferation of bilateral and regional economic integration agreements – have significantly diminished the role of such tariff concessions in promoting global sourcing (USITC, 1999).

Trade data based on the first major revision to the Standard International Trade Classification system – SITC Revision 2, introduced in the late 1980s – allowed, for the first time, the separation of component trade from the broader category of machinery and transport equipment (Section 7 of SITC). Yeats (Reference Yeats, Arndt and Kierzkowski2001) conducted the first quantification of component trade within this category, focusing on the global trade patterns of OECD countries. Following his seminal study, it became standard practice to use data on parts and components to measure trade within GMVCs. The subsequent revision, SITC Revision 3 (introduced in 1988) expanded the identification of parts and components to cover a broader range of manufactured goods beyond machinery and transport equipment. However, the separation of parts and components from final assembled products remains incomplete – and perhaps inherently unachievable – for certain goods, particularly those traded within buyer-driven production networks.

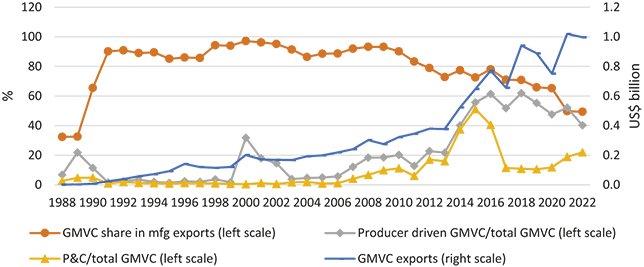

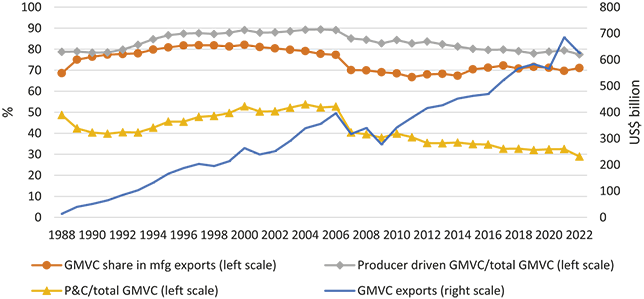

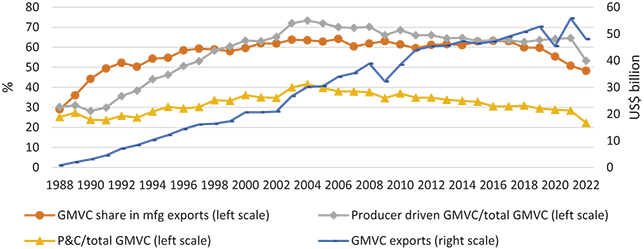

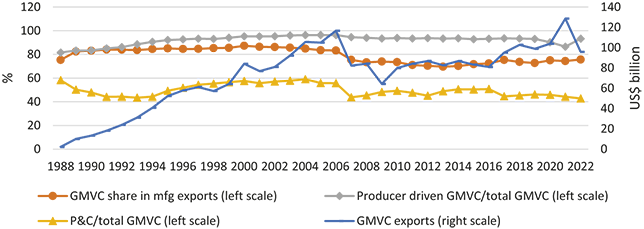

Cross-border trade in parts and components (intermediate goods) is obviously a ubiquitous indicator of GPS. However, it represents only one facet of GMVC trade. As previously discussed, GMVC activities have expanded significantly from the production of parts and components to include final assembly. Moreover, the relative importance of these two stages of production fragmentation varies across countries and changes over time within each country. This variation makes it problematic to rely solely on parts and components data as a general indicator of trends and evolving patterns in GMVC trade. For instance, as China’s participation in GMVCs has matured and deepened, imports of parts and components have declined, while exports of assembled final goods from China have expanded rapidly. An analysis that uses the growth of trade in parts and components as the sole indicator of GMVC activity would mistakenly interpret the decline in component imports as a sign of overall decline – or stagnation – in GMVC trade (as in Constantinescu et al., Reference Constantinescu, Mattoo and Ruta2020; World Bank, 2020).

To address this issue, researchers have begun to supplement data on directly reported parts and components with approximate estimates of assembled final goods. There is no hard and fast rule for delineating final goods assembled within GPNs from the standard trade data. The only practical way of doing this is to focus on the specific product categories in which GPN trade is heavily concentrated. Once these product categories are identified, trade in final assembly can be approximately estimated as the difference between parts and components, which are directly identified based on our list, and the total trade of these product categories. (Kimura Reference Kimura2006; Athukorala & Menon, Reference Athukorala and Menon2010; Athukorala, Reference Athukorala, Kaur and Singh2014a; Ando et al., Reference Ando, Kimura and Obashi2021). This is the methodology adopted in this study.

It is important to note that parts and components, as defined here, represent only a subset of intermediate goods, even though the two terms are often used interchangeably in recent literature on GPS. Parts and components are inputs that are employed further along the production chain. Unlike standard intermediate goods – such as iron and steel, industrial chemicals, or coal – parts and components are relationship-specific inputs. In most cases, they lack reference prices, are not traded on open markets, and require more complex contractual arrangements (Hummels, Reference Hummels, Arndt and Kierzkowski2002; Nunn, Reference Nunn2007). Moreover, most parts and components do not have a commercial life of their own; they only acquire value when embodied in a final product. Failing to distinguish parts and components from standard intermediate goods can result in an overestimation of the role of GMVCs in manufacturing trade.

We compiled data from the UN Comtrade database at the 5-digit level of the Standard International Trade Classification (SITC), based on SITC Revision 3. Parts and components were identified by mapping items in the intermediate goods subcategory of the UN Broad Economic Classification to corresponding codes in the SITC. This mapping enabled us to delineate parts and components from the reported trade data.

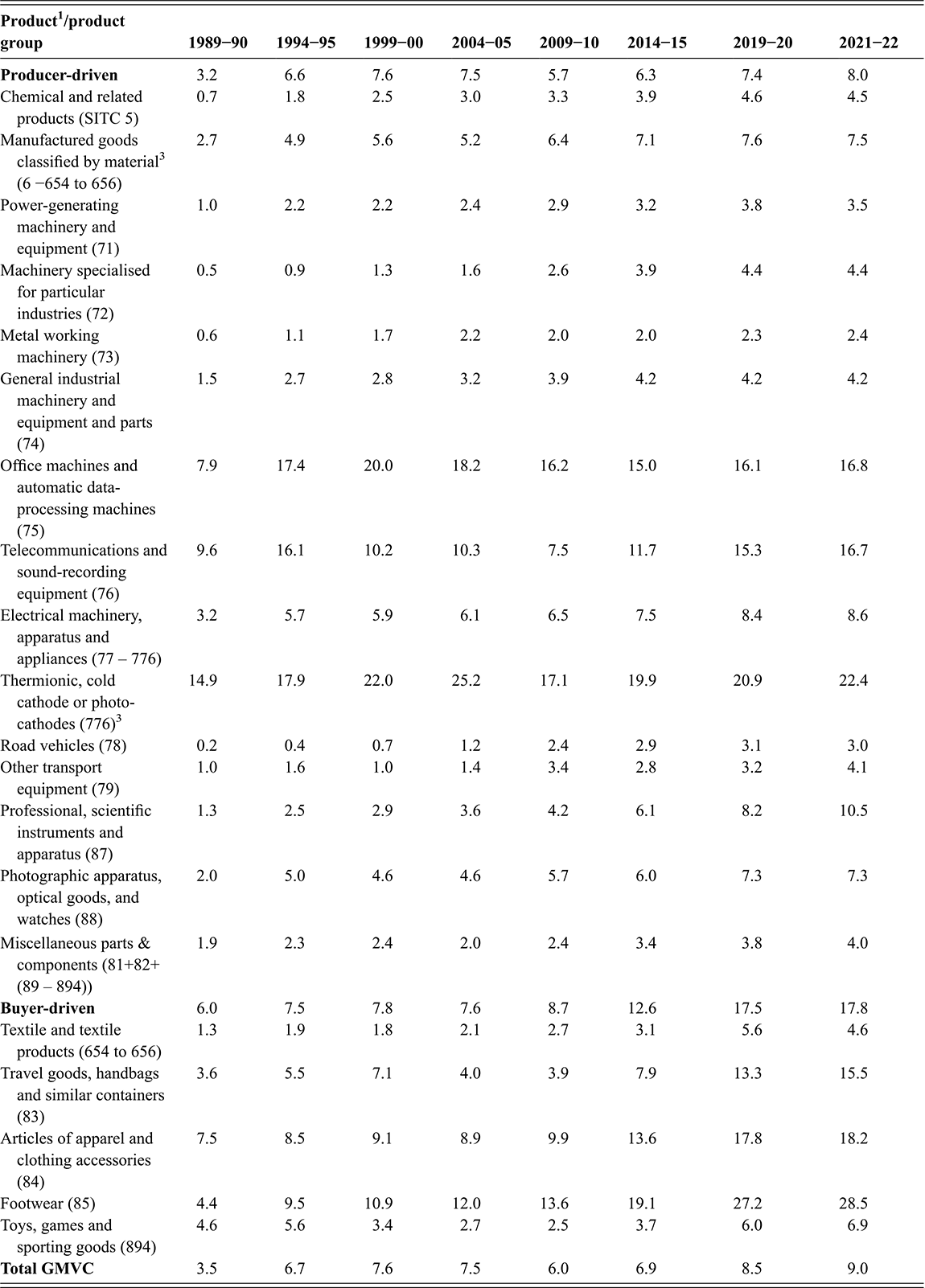

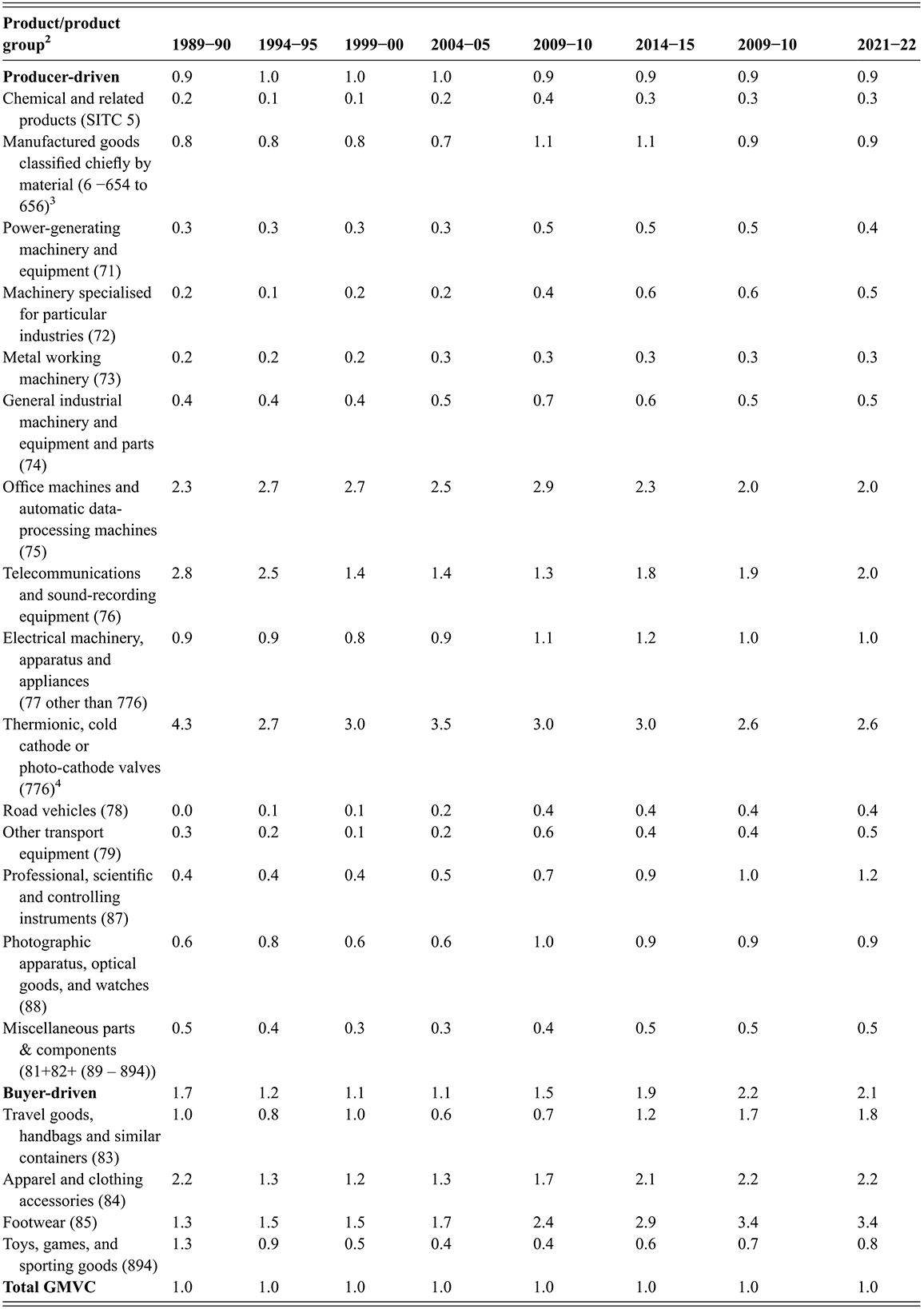

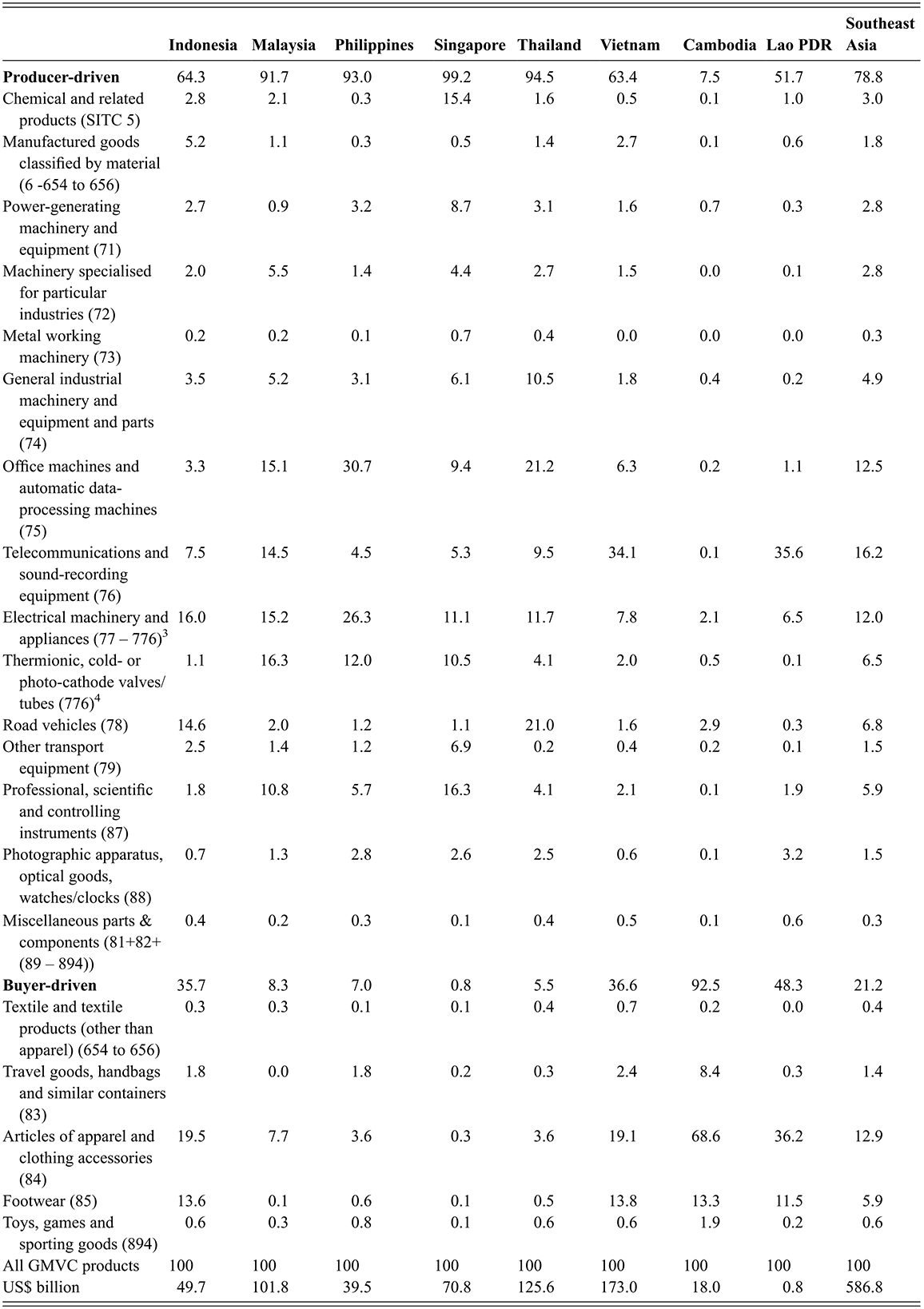

Guided by the existing literature on production sharing, we identified the following product categories to approximate final assembly: office machines and automatic data processing machines (SITC 75); telecommunications and sound recording equipment (SITC 76); electrical machinery (SITC 77); road vehicles (SITC 78); other transport equipment (SITC 79); travel goods (SITC 83); clothing and clothing accessories (SITC 84); footwear (SITC 85); professional and scientific equipment (SITC 87); photographic apparatus (SITC 88); and toys and sporting goods (SITC 894). It is reasonable to assume that these product categories contain virtually no items produced entirely within a single country. Among these, SITC 83, SITC 84, SITC 85, and SITC 894 are primarily traded through buyer-driven production networks, while the remaining categories are associated with producer-driven production networks.

Trade in final assembly is approximately estimated as the difference between reported trade in these eleven products categories and parts and components specifically assigned to them. Total GMVC trade is the sum of estimated final assembly and total parts and components.Footnote 11

2.5.2 Value-Added Trade

Conventional trade data, which attribute the full value of a product to the country from where the final product originates, do not accurately reflect the distribution of economic activity or the value added by different countries. As a result, analyses based on these data fail to meaningfully capture cross-country linkages within production networks and may present a distorted view of bilateral trade imbalances – especially in a context where global production is increasingly fragmented, and different stages of production are carried out in different countries.

To address this limitation, trade can be measured in terms of its value-added content using global input-output (I-O) tables. These tables integrate country-level input-output data with bilateral trade statistics within a consistent accounting framework. The most widely used databases for this purpose include the OECD’s Trade in Value Added (TiVA) database, the World Input-Output Database (WIOD) maintained by the University of Groningen, and the Asian Development Bank’s Regional Input-Output Tables, which cover twenty-nine Asia-Pacific economies.Footnote 12 The key advantage of the I-O approach is its ability to estimate both domestic and foreign value added embodied in trade, capturing not only direct inputs but also indirect contributions through intra-industry linkages within an economy.

The global input-output (I-O) methodology allows for the estimation of two key aspects of an economy’s participation in GMVCs: (1) backward GMVC participation, which refers to the foreign value added embodied in exports (or simply the ‘import content of domestic exports’), and (2) forward GMVC participation, which refers to the domestic intermediate inputs embodied in the exports of importing countries. Only backward GMVC participation is directly relevant for analyzing the impact of GMVC engagement on the domestic economy. Both aspects are of course important for understanding how a country is integrated into the global economy and how external economic shocks are transmitted within GMVCs.

The measurement of GMVC participation using existing input-output (I-O) tables is subject to significant data limitations. There is no standardized or coordinated approach across countries in constructing I-O tables, leading to inconsistencies and measurement errors when linking the input-output structures of trading partners. Moreover, for many countries, I-O tables are compiled only for intermittent years – typically every five years – necessitating mechanical extrapolation to construct time series. In addition, direct data on the use of key intermediate inputs by industry are not available for some major economies, including the United States, China, India, and Vietnam. As a result, global I-O databases often rely heavily on the so-called import comparability assumption – import content of export production in each industry is identical with that of production for the domestic market – when estimating domestic and foreign value added (Patunru & Athukorala, Reference Patunru and Athukorala2023; Yuscavage, Reference Yuscavage, Mattoo, Shi and Wei2020).Footnote 13

Even when taken at face value, I-O-based value-added trade measures do not replace conventional gross trade flow statistics for analyzing the patterns and economic implications of GMVC-related trade, for several reasons. First, these measures capture only intermediate input linkages across countries; trade in final assembly is not accounted for. Second, trade in intermediate inputs, as measured in I-O tables, includes both standard intermediate goods and parts and components. As noted earlier, this can lead to an overestimation of GMVC participation, especially given the highly aggregated level (typically at the 2-digit level of national accounts) at which I-O tables are constructed. Third, detailed trade statistics – by product and partner country, and measured in gross value – remain essential for analytical purposes related to trade and exchange rate policies. Under GPS, a country specializes in a specific slice (task) in the production chain, depending on the relative cost advantage and other factors. The value-added content per unit of production (value-added share) is determined by production fragmentation within the overall value chain, which is beyond the control of each country. The value-added content per unit of production (value-added share) is determined by the structure of production within the GVC, which is largely beyond the control of individual countries. The total value added – that is, the contribution to GDP – that a country gains depends on the overall volume of its gross exports, not just on the value-added share. Of course, the value-added share may increase over time as a country becomes more fully integrated into the value chain.

3 Initial Conditions and Policy Regime Shifts

This section has three objectives: to introduce the Southeast Asian economies and their place in the global economy, to provide brief country profiles relevant to our subsequent analysis, and to highlight empirically some aspects of these countries’ participation in GPNs.

3.1 An Overview

Over the last half-century, Southeast Asia has been the most economically dynamic region in the developing world. Four of the countries – Indonesia, Malaysia, Singapore, and Thailand – were classified as ‘miracle’ economies in the landmark 1993 World Bank study. A sequel to this study, the 2008 World Bank Growth Commission report, asked the question ‘how common is rapid sustained growth’ over the preceding century? Out of 150 countries (technically ‘economies’), it concluded that only 13 met the prescribed benchmark.Footnote 14 The same four were again among the high performers. If the study were being conducted today, two more Southeast Asian countries, Cambodia and Vietnam, would arguably be included in the group, and another, the Philippines, long characterized as the perennial ‘East Asian exception’, would nearly meet the threshold.

Economic openness has been a key driver of Southeast Asian economic success (Sachs & Warner, Reference Sachs and Warner1995). One important outcome of this openness, the subject of this monograph, is the region’s pioneering participation in GPS. In order to understand this phenomenon, and the role that these economies have played in these networks, we briefly examine the evolution of trade and commercial policy in the seven Southeast Asian countries (Indonesia, Malaysia, Philippines, Singapore, Thailand and Vietnam, and Cambodia in more recent years), which are the primary focus of this study.Footnote 15 Consistent with our analytical framework on the determinants of GMVC participation, we also document aspects of these countries’ international competitiveness and policy regimes, with particular reference to their service link costs.

Three major propositions are central to our analysis. First, economic openness accompanied by the requisite supply-side measures is the key determinant of success. Second, among these countries there are cases of missed opportunities, where they have only partially participated in GPNs, and these outcomes are explained by the analytical framework we are employing. The third point to emphasize is the latecomer success stories, which in turn draw attention to the fact that these networks are open and dynamic institutional arrangements that even these economies can join. At the risk of over-simplification, Singapore in particular, and Malaysia and Thailand especially in the late twentieth century, are examples of the first proposition. Indonesia and the Philippines, the two countries where reservations about the desirability of globalization are the strongest, are examples of the second. Vietnam and on a smaller scale Cambodia are twenty-first century examples of the third proposition.

Singapore and Malaysia were open economies during the colonial era, and they have never fundamentally deviated from this openness. Along with Thailand, they were among a tiny group of ‘always open’ developing economies according to the Sachs & Warner (Reference Sachs and Warner1995) binary trade regime classification. However, historically, these three were the regional exceptions. Indeed, ‘Southeast Asia in Turmoil’ (Crozier, Reference Crozier1965) was the title of a popular 1960s study of the region. Vietnam was consumed by war until 1975 and then, following reunification, an unsuccessful command-economy experiment for another decade. It took its Doi Moi reforms commencing in the mid-1980s to signal a change in direction, initially cautious but from the 1990s onwards increasingly decisive. Following the expropriation of Dutch (and later all foreign) property in 1958, Indonesia disengaged from the global economy, and for a period its major international institutions. Instead, it joined the Peking-Pyongyang-Hanoi-Phnom Penh-Jakarta axis of ‘newly emerging forces’. The Philippines remained closely aligned with the United States during the post-independence period, but a balance of payments crisis in the late 1940s resulted in the imposition of temporary import control measures which quickly became permanent, and it then embarked on a comprehensive import substitution strategy for several decades.

Around 1970, however, there was a turning point, for three main reasons and first clearly articulated by Hla Myint (Reference Myint1972). First, regime change in Indonesia in 1966 signalled a major change of direction in that country. The region’s most important country began to look outward, achieve macroeconomic stabilization, and indicate its wish to be at peace with its neighbours. Second, and related, the five anti-communist nations established the Association of Southeast Asian Nations, ASEAN, in 1967 as a means of fostering regional cooperation and neighbourly relations. Third, the intellectual climate had begun to change. By then Japan’s rapid export-led industrialization was clearly evident. There was also growing evidence that the four Asian NIEs’ outward orientation had lifted their economic growth. Importantly for Southeast Asia, Singapore was beginning to demonstrate the success of its innovative model of FDI and export-led industrial growth that was connecting it to the growing internationalization of manufacturing activity.

Reform continued apace during the 1980s. Vietnam’s decisive change of direction was followed by its two Mekong neighbours Cambodia and Laos. After a deep crisis during the 1980s the Philippine economy also began to recover, liberalize, and grow strongly. Even Myanmar appeared to be opening up, economically if not politically. At its 1992 Manila Summit ASEAN for the first time adopted the words ‘free trade’ in its agreement, with the milestone achievement that all sectors were to be included in the ASEAN Free Trade Area (AFTA) unless they were explicitly excluded. Its membership also expanded to include all ten countries during the 1990s.

Importantly, the global environment was accommodating over this period. The 1985 Plaza Accord triggered a massive relocation of labour-intensive Japanese manufacturing to Southeast Asia, principally to Indonesia, Malaysia, and Thailand. Industrial relocation from Korea and Taiwan also accelerated. Moreover, Asia’s two giants, China and India, were now looking outward, the former from 1978, and the latter from 1991. These changes in turn strengthened the position of the Southeast Asian reformers. It led to the establishment of the Asia Pacific Economic Cooperation and created a virtuous circle of what is sometimes termed concerted unilateral liberalization, or open regionalism (Garnaut, Reference Garnaut and Bhagwati2002; Bhagwati Reference Bhagwati2008). Over time ASEAN has de facto adopted a variant of this approach, often characterized as ‘outward-looking regional economic integration’, in which countries have tended to multilateralize concessions granted to other member countries (Soesastro, Reference Soesastro2008; Chia, 2011).

The 1997–98 Asian financial crisis (AFC) was Southeast Asia’s most serious economic recession in its independent history, but importantly, it did not lead to a retreat from the global economy. Several factors were at work here. First, the sharply depreciating currencies in the context of a buoyant global economy, in which China – largely unaffected by the crisis – was now a major actor, created the potential for export-led recovery and growth. Second, two of the crisis-affected economies, Indonesia and Thailand (and initially also Malaysia), had signed IMF emergency programs which precluded the introduction of any substantial trade barriers. Third, during the crisis the ministries of finance became more powerful, and these liberally inclined technocratic institutions generally resisted returning to inward-looking strategies. Fourth, owing to the effective responses, the recession was a short-lived V-shaped crisis and all the affected economies were again registering positive economic growth by 2000.

During the twenty-first century there have been no fundamental changes in trade policy in these countries. The major challenge has been adapting to a rapidly changing, and occasionally volatile, global economic environment. First, there have been two major external shocks, the 2008–09 global financial crisis and the 2020–21 Covid pandemic, in addition to smaller global shock events such as periodic GMVC disruptions, the 2013 ‘taper tantrum’ event, and the war in Ukraine and Gaza. Second, the global commercial architecture has become weaker: the Doha development round failed to materialize, the WTO has been sidelined, and consequently regional and bilateral, frequently ‘trade-lite’ preferential trade agreements (PTAs) have proliferated. Moreover, trade disputes between the two global superpowers have intensified since around 2015, with increased pressure on smaller economies to join one of the two emerging informal economic communities. Third, there is growing international concern about the potential dangers of catastrophic climate events, and inevitably some of the proposed remedies have implications for trade policy. Energy transitions require the introduction of carbon taxes and support for the emerging renewable energy technologies. The uneven pace of energy transitions around the world, between the early and late adopters of renewable technologies, has resulted in some countries imposing ‘carbon tax equivalents’ on imports, as illustrated for example by the EU’s carbon border adjustment mechanism, and by sharply increased US protectionism. Nevertheless, in spite of these challenges, and with country variations to be discussed shortly, the region’s trade policy settings have remained largely intact.

3.2 Country Profiles

We now briefly examine some salient country features as they affect their international economic orientation. As noted, although having less than 1% of the region’s population, Singapore spearheaded the adoption of outward-looking strategies by seizing on the commercial opportunities being created by the growing trend in international off-shoring of MNEs in the 1960s.Footnote 16 Building on its fortunate geographic location, Singapore’s remarkable success has been driven by highly pro-active and flexible policies: one of the world’s most open economies for trade and investment; an open labour market across the skill spectrum; top-ranked internationally oriented logistics, with its Changi Airport and the Port of Singapore Authority; a sophisticated financial sector; and attractive tax regimes. Importantly, the government anticipated the country’s changing comparative advantage in the transition from a labour-surplus to a high-wage economy. From the late 1970s it engineered transformative change in the labour market by instituting a ‘high-wage’ policy, inducing MNEs to relocate labour-intensive activities to lower-wage regional locations (Goh, Reference Swee1996), accompanied by major investments in advanced technologies and higher education.

Malaysia has also maintained liberal trade and foreign investment policies and an open labour market.Footnote 17 Being a federal entity, some reform-oriented states, Penang in particular, have been able to innovate more quickly than the national government (Athukorala, Reference Athukorala2014b). Nevertheless, the country’s development progress has been held back, in the 1980s by a misguided ‘Look East’ heavy industry strategy, in steel, automobiles and related sectors, supported by a mix of subsidies and trade restrictions. Some ethnic redistribution objectives have arguably complicated the reform agenda, including policies towards higher education and advanced training institutes, especially centred around the growth of a large and politicized state enterprise sector.Footnote 18

Similarly, although Thailand has remained a largely open economy, achieving notable early successes in hard disk drives and as a major regional automotive hub, it has failed to innovate on the basis of these early-mover advantages. It has under-invested on the supply-side, especially its skills and higher education (Doner & Schneider, Reference Doner and Schneider2019), while prolonged political uncertainty has deterred investors (Nidhiprabha, Reference Nidhiprabha2019; Jongwanich, Reference Jongwanich2022).

The automobile industry in Thailand has grown rapidly over the past four decades (Kohpaiboon, Reference Kohpaiboon2006; Warr & Kohpaiboon Reference Warr and Kohpaiboon2018). Until about the mid-1990s, automobile production in Thailand was well below that of India and Malaysia among the Asian countries. Following a notable policy shift from import-substitution to export orientation that began in the late 1980s and gained added impetus after the AFC (1997–98), a world-class automobile cluster has emerged through global integration. By 2010, Thailand had become the 13th largest automobile producer in the world, and the third largest in Asia, after Japan and South Korea; most of the major players in the world auto industry were using the country as a production platform. In 2008, the Economist dubbed Thailand the ‘Detroit of the East’ (Economist Intelligence Unit, 2008, p. 21). Over the ensuing decades, Thailand’s ranking in automobile production in Asia declined to sixth place due to the rapid expansion of production in China and India. However, in 2024, Thailand remained the 13th largest automobile producer in the world. In terms of export value, Thailand was the fourth-largest exporter in Asia, after China, Japan, and South Korea.Footnote 19

Indonesia has never fundamentally backtracked from the broad policy directions adopted in the late 1960s (Hill, Reference Hill2000). But its embrace of globalization has always been hesitant, and the trade policy pendulum has swung from relatively liberal to somewhat protectionist. During the Soeharto era 1966–98 there was a reasonably strong inverse relationship between the terms of trade and the openness of trade policy (Basri & Hill, Reference Basri and Hill2004): economic nationalism was in the ascendancy during periods of high oil prices, resulting in trade and investment policies becoming more restrictive, whereas the reverse was generally the case when oil prices declined. During the democratic era political and business interests have intruded more directly, for example, depending on which political party has control of the trade and sectoral ministries (Pangestu et al., Reference Pangestu and Rahardja2015). Except when reformers have been in the ascendancy, successive administrations have also employed domestic value added and export bans in a misguided attempt to promote ‘downstreaming’ (hilirisasi in Bahasa Indonesia). As we shall show in the following, one major consequence is that Indonesia has been a relatively minor participant in electronics GMVCs. It has a larger footprint in the automotive industry thanks to its larger domestic market, and it is competitive in certain niche export markets such as commercial utility vehicles.Footnote 20

The Philippine record resembles that of Indonesia in its hesitant engagement of globalization and missed commercial opportunities. But there are differences too, especially in the importance of services trade and labour exports, where in both cases the country has been the Southeast Asian leader. During the 1990s reforms it did emerge as a significant manufactured exporter, including electronics (Bautista & Tecson, Reference Bautista, Tecson, Balisacan and Hill2003). However, during the twenty-first century the reform momentum languished and manufactured exports grew slowly (Athukorala, Reference Athukorala and Patunru2024). Attempts to remove the constitutional restrictions on foreign ownership outside the export zones (known by their acronym PEZA) have also been a long-running policy battle.Footnote 21

As noted, the export success of Southeast Asia’s two latecomers, Vietnam and Cambodia, illustrates the openness of GPS provided countries introduce the requisite reforms. Vietnam has recorded the strongest regional export performance in the twenty-first century, building on its historic policy reorientation that commenced in the late 1980s.Footnote 22 In its export zones, it maintains very liberal trade and investment policies, together with efficient infrastructure and logistics services. Its labour force is well-trained, and wages are internationally competitive. It has been able to attract major international electronic investors, most notably the then world’s largest producer, Intel, in 2006. A feature of the country’s export profile, and one that is unusual in Southeast Asia, is the strong growth in both producer-driven and buyer-driven segments, including electronics, machine goods, garments, and footwear. The country has also been a favoured destination for firms seeking to diversify their China-based production activities in response to China–US trade tensions, although this is now threatened by the escalating China–US trade disputes. In the case of Cambodia, the return of peace, the adoption of open, business-friendly policies, and concessional export market access led to very rapid garment export growth from the late 1990s (Hill & Menon, Reference Hill and Menon2014). Initially the growth centred on simple CMT (cut, make, and trim) garments, but over time the firms have produced more elaborate, fashion-intensive products, while other industries, initially footwear, and more recently electronics and machine tools, have emerged (Menon & Naqvi, Reference Menon, Naqvi, Hill and Suryadarma2025).

3.3 A First Look at the Data

To complete this overview of Southeast Asia’s global economic integration, we now provide some empirical evidence on the factors determining participation in GMVCs. Our choice of variables is guided by the analytical framework developed in the previous section.

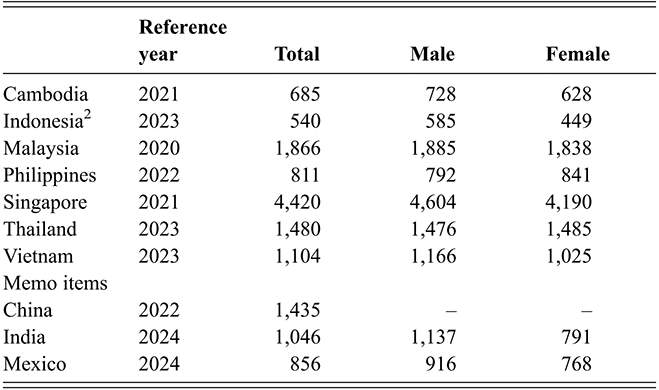

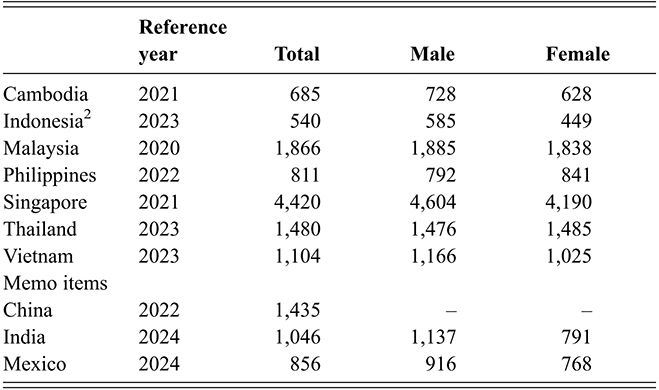

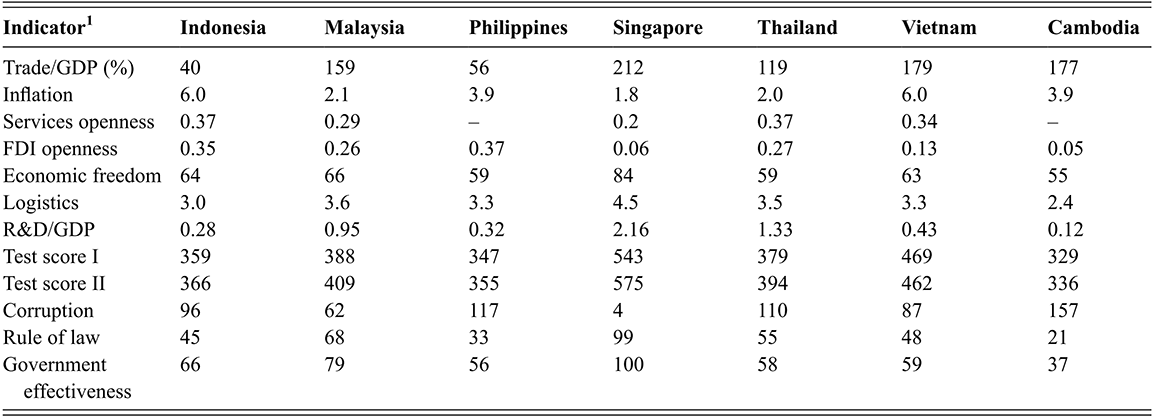

A prerequisite for initial entry into GPNs, for assembly, packaging and other simple tasks, is competitive labour markets, proxied in the first instance by average monthly earnings (wages) in the manufacturing sector (Table 1). The wages of the seven Southeast Asian countries more or less reflect differences in per capita GDP, with those in Singapore by far the highest and Indonesia the lowest.Footnote 23 Interestingly, wages in Indonesia are lower than those in India and Mexico, the two major countries often compared with Indonesia in media commentaries as alternative investment locations under the so-called ‘China Plus One’ phenomenon. The data clearly illustrate the incentive for firms in high-wage countries to relocate their labour-intensive activities to lower-wage countries. The wage data also provide an indication of the likely hierarchy of technological capabilities across countries, with the more skill-intensive activities locating in higher-wage economies, a point to which we return shortly.

Table 1 Long description

The data are given for Indonesia, Malaysia, Philippines, Singapore, Thailand and Vietnam and three comparator countries (China, India and Mexico), separately for male and female worker. Earnings refer to gross pay, in cash or kind, regularly paid to employees for work or for time off (such as vacation or holidays).

Notes:

(1) Earnings refer to gross pay, in cash or kind, regularly paid to employees for work or for time off (such as vacation or holidays). Minimum wages reflect the statutory monthly minimum as of 31st December. If there is no national rate, data are based on the capital, a major city, or a regional average. For sector- or occupation-based systems, figures are for manufacturing or unskilled workers. All values are in US dollars, adjusted for purchasing power (PPPs) to allow international comparisons.

(2) The figure for Indonesia is the average monthly earnings of workers in both organized and informal manufacturing.

– Data not available.

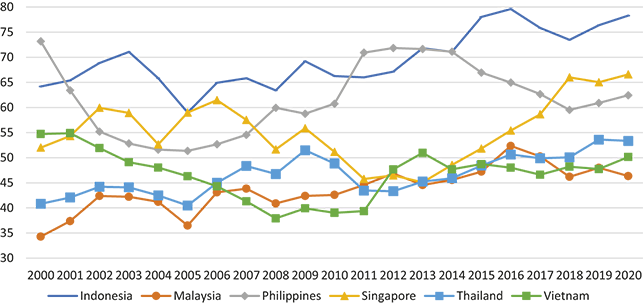

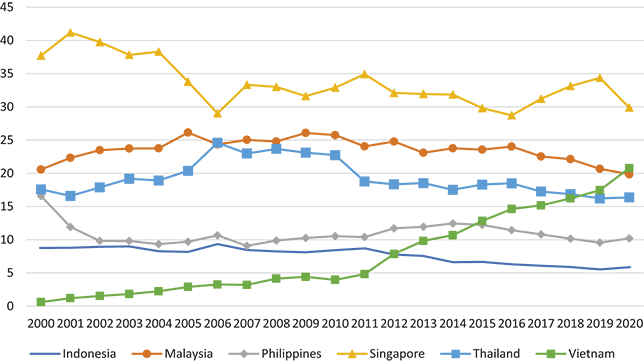

Competitive labour markets are a necessary but not sufficient condition for successful participation in GPNs. They need to be combined with the efficient availability of services, referred to here as ‘service link costs’ involved in GPS, as well as openness to foreign investors and buyers. Here, the term service link cost refers to costs involved in arrangements to connect and coordinate activities in each country with those in other countries within the production network (Jones & Kierzkowski, Reference Jones, Kierzkowski, Arndt and Kierzkowski2001; Golub et al., Reference Golub, Jones and Kierzkowski2007). Service link costs in each country depend on a whole range of factors impacting on the overall business environment. These include trade-related infrastructure and logistics; political stability and policy certainty; institutions, including protection of property rights (including importantly intellectual property) and enforcement of contracts; and liberal trade and investment policy regimes. Unlike firms involved in light consumer goods industries, foreign firms engaged in vertically integrated assembly industries are particularly sensitive to these factors, as they view investment risk from a long-term perspective. They are also particularly concerned about political stability because disruptions in a production base in a value chain of just-in-time delivery disturb the entire value chain.

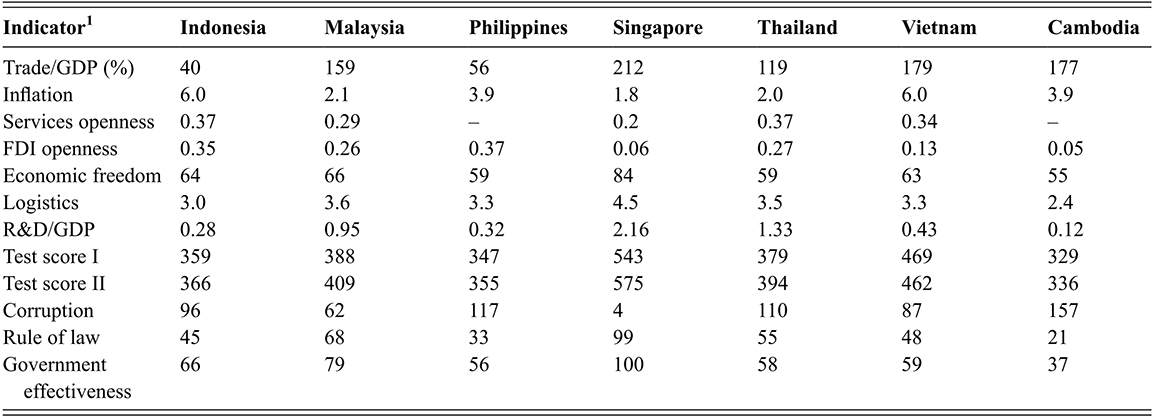

There is no single indicator that measures these service link costs. In Table 2 we therefore present a range of indicators that capture these factors, with a focus on trade-related logistics and the particular requirements of vertically integrated, internationally mobile capital.Footnote 24 The data are for the seven ASEAN countries that are the focus of this study. As we will discuss in more detail in the next section the needs of foreign investors and buyers will differ across industries. For international buyers in the garment industry, for example, the key variables are the ease of international trade (including import duty drawback facilities) and labour costs. For foreign investors in vertically integrated electronics production in multiple countries, to these variables need to be added the openness and stability of the FDI regime. In the automotive industry, an additional consideration is access to the domestic market in the case of larger countries.

Table 2 Long description

Data are provided for Indonesia, Malaysia, Singapore, Thailand, Vietnam and Cambodia based on several standard sources that provides comparative state of each country in terms of openness to merchandise and services trade, FDI regime, economic freedom, logistic quality, academic test score, corruption, R&D intensity, rule of law, and government effectiveness. Data source and methods of data compilation are described in notes to the table.

(1) Notes and Sources

Trade/GDP: exports plus imports divided by GDP (World Bank, World Development Indicators).

Inflation: average annual increase in the consumer price index 2000–23 (World Bank, World Development Indicators).

Services openness: Services Trade Restrictiveness Index (higher is more restrictive) (OECD Stat).

FDI openness: FDI Restrictiveness Index (higher is more restrictive) (OECD Stat).

Economic Freedom: the Heritage Foundation index (higher is more open).

Logistics: Logistics Performance Index (higher is better quality) (World Bank, World Development Indicators).

R&D/GDP: Research and development expenditure divided by GDP ((World Bank, World Development Indicators).

Test Score I and II: PISA OECD test scores for fifteen-year olds in 2022 for reading and mathematics, respectively (OECD Stat).

Corruption Perceptions Index, 2021 (180 jurisdictions ranked, lower ranking is less corrupt) (Transparency International).

Rule of law (World Bank, World Governance Indicators): percentile rank, higher number indicates higher quality.

Government effectiveness (World Bank, World Governance Indicators): percentile rank, higher number indicates higher quality.

– Data not available.

GMVCs operate most effectively when there are minimal restrictions on international trade in goods and services. The most widely used measure of trade openness is simply the ratio of trade in goods and services to GDP. Table 2 shows the very large differences among the group of countries. Singapore has always been one of the world’s most trade-dependent economies. Several other Southeast Asian economies are also highly trade-oriented, with the ratios for Cambodia, Malaysia, Thailand, and Vietnam exceeding 100. These numbers are significantly higher than those for India and Indonesia (and the Philippines) two much larger, less outward-looking economies. In spite of its well-known limitations as a measure of economic openness, including that participation in GPNs inflates the numerator in the ratio, this ratio has the attraction of simplicity (Irwin, Reference Irwin2024). It should be noted that many countries adopt a second-best approach to free trade through the establishment of free trade zones. These can be effective if accompanied by genuinely liberal customs arrangements, although they do create a dualistic economic structure consisting of enclaves largely unconnected from the rest of the economy. An additional trade arrangement is the WTO-sanctioned Information Technology Agreement (ITA II),Footnote 25 which has been a crucial facilitator of GPS, as signatories to the accord agree to the free and unhindered trade of goods (mainly electronics) specified in the ITA. Contrary to popular perceptions, preferential trading arrangements (PTAs) are not an important factor in the operation of GPS. The PTAs are typically highly complex legal arrangements with restrictive provisions relating to exemptions, phase-ins and rules of origin (ROOs).

Countries have typically liberalized goods trade more quickly than services trade. But services trade openness is an important pre-requisite for effective participation in GPNs because it can be expected to lower service link costs. The measurement of service trade openness is more complex given the diversity of traded services (transport, IT, finance, business services, etc.). A useful indicator here is the services trade restrictiveness index devised by the OECD.Footnote 26 The country rankings generally follow those for merchandise trade, with Singapore the most open and Indonesia (and Thailand) more restrictive. Note, however, that Singapore is not such an outlier in these comparisons, indicating that, unlike for merchandise trade, it has some service trade restrictions.

The foreign investment regime is a key determinant of GPN participation as MNEs are major players in GMVCs, especially in the producer-driven networks where, to assure product quality and reliable delivery, and to protect their intellectual property (IP), they frequently assume equity positions in supplier firms.

We present two indicators of the relative importance of MNEs in these countries, and they largely corroborate each other. First, in Table 2, we report the OECD’s attempt to measure comparatively the FDI policy openness of each country. As expected, Singapore is the most open economy. The latecomers, Cambodia especially, and Vietnam, are also very open, reflecting their explicit policy decisions to convince investors that they wish to join the global economy. By contrast, Indonesia and the Philippines are more restrictive compared to Malaysia.

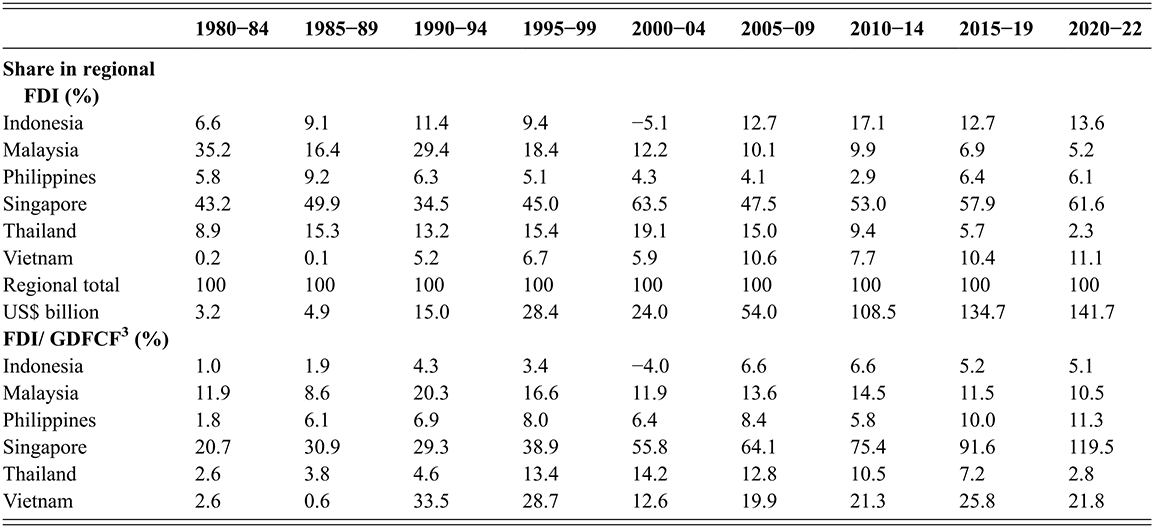

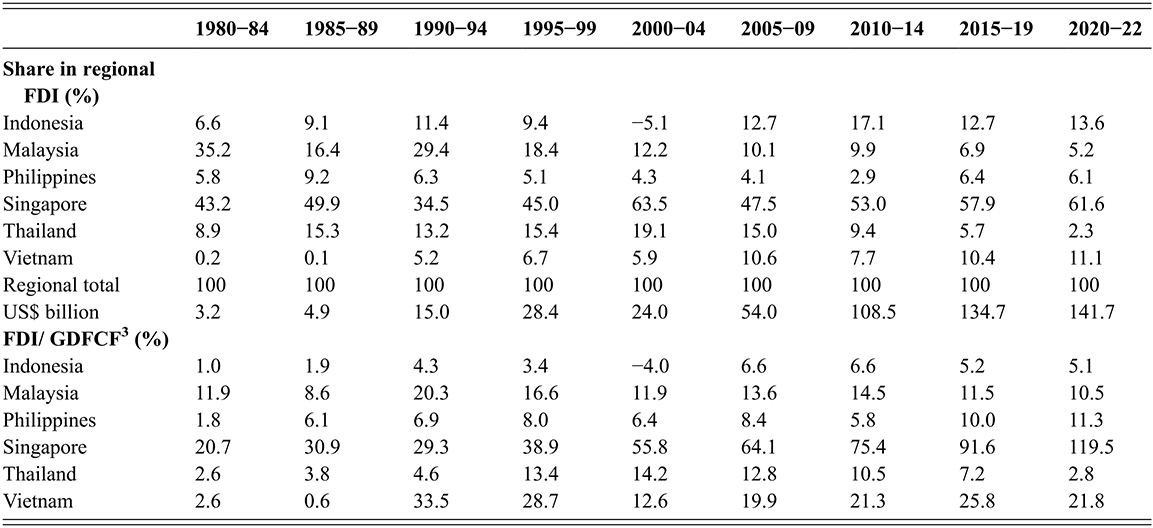

A second indicator is FDI inflows over time, relative to each host country’s total investment (specifically gross domestic fixed capital formation) for five-yearly intervals since 1970 (Table 3). The time series data provide evidence on whether the FDI policies have been broadly consistent over time, and they also enable identification of the timing of major liberalizations, especially for the latecomers. Three major patterns are evident. First, Singapore has been consistently open, a factor that has underpinned its superior credibility as a hospitable destination for foreign investors. Second, the data highlight the timing of Vietnam’s economic liberalization – until around 1990 it received trivial amounts of FDI, but once investors became convinced about the durability of its reforms it quickly became a major host country, which in turn helps explain its subsequent dramatic export performance. Third, although never on a scale matching Singapore, Malaysia has been a consistently welcoming country for MNEs, whereas Thailand has fallen out of favour since its political instability over the past decade and a half. The Philippines has gradually become more attractive as it has liberalized, especially in services. Finally, Indonesia has been a surprisingly small recipient of FDI throughout this period after its short-lived open-door policy was introduced in the late 1960s. Some of the volatility is also explained by fluctuations in mineral prices, where much of the FDI has been directed. Political uncertainty in the aftermath of the AFC was also a factor earlier this century.

Table 3 Long description

The first section of the table shows percentage share of Indonesia, Malaysia, Philippines, Singapore, Thailand and Vietnam in total FDI in these countries. The second section shows FDI as a percentage of gross domestic fixed capital formation in each country.

Notes:

(1) By definition, the reported FDI in the given country represents new capital and excludes any capital repatriation.

(2) Annual averages.

(3) Gross domestic fixed capital formation.