1. Introduction

The Autumn 2025 Budget highlighted just how dysfunctional the UK’s process for setting fiscal policy is. The process was punctuated by systematic briefing from the Government to the media about the course of the Office for Budget Responsibility’s (OBR) forecasts, what they implied for fiscal policy space and what was being planned by the Treasury in response.

Perhaps the most glaring—though by no means the only—example of this pattern of behaviour was the decision not to proceed forward with the income tax rise that was heavily hinted at in the run-up to the 2025 Budget. The Chancellor of the Exchequer gave a press conference on 4 November in which she heavily hinted at what would be a manifesto-breaking policy measure, before a Financial Times (FT) article on 13 November revealed the plan had been dropped. The FT reported that according to ‘government figures’, better than expected forecasts from the OBR had allowed the plan to be dropped.

This was despite the fact that the OBR had already provided their final pre-measures forecast to the Treasury on 31 October—a full five days before the Chancellor’s press conference. But the OBR, bound by silence in advance of publishing its forecasts, could not rebut that assertion. This is far from the only occasion in which details of the forecast were given to the press and subsequently published prior to the forecast being made available to the general public. In fact, in all but one fiscal event since the 2022 ‘mini-budget’ there have been leaks or briefings to journalists, as Table 1 shows, which compiles these from newspapers of record (The Times and the Financial Times).

A list of briefings and leaks of the forecast contents in advance since the 2023 March Budget onwards

Table 1. Long description

From the top row, the table begins with March 2023, dated 19 January, reported by The Times, article ‘Jeremy Hunt wants 5p fuel duty cut to run year longer’, with forecast detail stating the Office for Budget Responsibility lowered initial pre-budget forecasts. The next row is November 2023, 12 November, The Times, article ‘Hopes for autumn statement tax cuts as Jeremy Hunt finds wiggle room’, forecast detail ‘his headroom had grown to between 13 billion and 15 billion’. The third row is March 2024, 27 February, FT, article ‘Jeremy Hunt struggles to find Budget goodies as he faces fiscal headlock’, forecast detail ‘latest OBR forecasts only give Hunt about 13 billion of headroom against his self-imposed fiscal rule’. The fourth row is March 2024, 3 March, The Times, article ‘Jeremy Hunt looks for 9 billion to balance his budget’, forecast detail ‘12.8 billion of fiscal headroom projected by the Office for Budget Responsibility’. The fifth row is October 2024, 15 October, The Times, article ‘Rachel Reeves plans 40 billion in tax rises and spending cuts’, forecast detail ‘as much as 40 billion will be needed to avoid real-terms cuts to departments, most of which will need to come from tax rises unless there is a big improvement in the economic outlook’. The sixth row is March 2025, 12 February, The Times, article ‘OBR forecast tells Rachel Reeves she has run out of headroom’, forecast detail ‘government’s 9.9 billion in fiscal headroom had been wiped out by low growth, higher-than-expected interest rates and higher borrowing costs’. The seventh row is March 2025, 12 February, FT, article ‘Treasury fears UK watchdog will give it little credit for pro-growth reforms’, forecast detail ‘James Bowler, Treasury permanent secretary, launched an inquiry into a potential leak of the OBR submission, saying it was vital that the watchdog and Treasury ministers could discuss forecasts in private’. The eighth row is March 2025, 19 March, The Times, article ‘Rachel Reeves not expected to raise taxes in spring statement’, forecast detail ‘chancellor is attempting to fill a hole of between 15 billion and 20 billion in the public finances after the Office for Budget Responsibility downgraded its growth forecasts’. The ninth row is November 2025, 27 October, FT, article ‘Reeves faces 20 billion hit to UK public finances from productivity downgrade’, forecast detail ‘Office for Budget Responsibility is expected to cut its trend productivity growth forecast by about 0.3 percentage points’. The tenth row is November 2025, 14 November, FT, article ‘How did fiscal forecasts affect Reeves’ income tax U-turn?’, forecast detail ‘Rachel Reeves was able to ditch a plan to raise income tax rates in the Budget because of favourable changes in forecasts from the UK’s fiscal watchdog’. All articles are from The Times or Financial Times, containing forecast details known only to OBR and the Government at the time, with OBR not commenting publicly.

Note: All articles from The Times or the Financial Times. All of these contain detailed descriptions of the forecast at times when these are only known to the OBR and the Government, and during which the OBR does not comment publicly.

This contrasts with the UK’s historically highly secretive budget process, in which decisions tended to be taken behind closed doors, in contrast with much more open processes in parliamentary systems (Sousa, Reference Sousa2025). This has been linked to the strength of the executive in the Westminster system, which requires the ability to pass a money bill for a government to maintain the confidence of the House of Commons.

But this appears to no longer be the case. Contents of the budget and the details of the underlying forecasts are speculated constantly in the press, encouraged by the government’s unofficial communications to the press. Language is often coded, but often refers to a ‘person briefed on the matter’ or ‘Treasury sources’. The result is the direction of travel and often specific figures of the OBR forecast become part of the speculation.

However, there is no guarantee that the information briefed is timely, accurate and/or complete. There is a fundamental asymmetry between the Treasury and the OBR. The latter is staffed by civil servants and led by publicly appointed commissioners. The OBR has not until now—rightly—engaged in media briefing of advance details of its forecasts, and it is easy to see how that would run counter to the code civil servants must abide by and the principles of public life that public appointees are expected to comply with. The Treasury, on the other hand, is staffed by civil servants but led by politicians and special advisers not bound by these rules. In fact, it is clear that politicians and their advisers clearly use the media to test out and pre-announce measures, and to set the scene (‘pitch rolling’ in the jargon) for what will happen.

The OBR produces a series of iterative forecasts, in which it adds new data and modelling assumptions until it achieves a stable base. This is then followed by direct and indirect effects of policy decisions, which are added on top of that base to reach the final, published forecast. This is the only forecast to see the light of day in all its detail.

The Treasury, however, is provided with details of each round of the forecast, which gives it the tools to shape the narrative while the process is still underway. When it briefs the media about the OBR’s forecasts, it can do so selectively while remaining unchallenged: the OBR has no right of reply. This was exemplified by the post-2025 Budget debate as to whether the Chancellor exaggerated the state of the public finances forecast by the OBR.Footnote 1

This article describes the current forecast process in detail, including breaking down the information asymmetry at each round. It then proposes a relatively narrow but significant reform that would provide greater transparency and equality of access to information while minimising disruption to the established working processes between the OBR and the Treasury. This would see the OBR ‘bookend’ the Budget: it would publish the pre-measures forecast around three weeks before the Budget, following it up with a post-measures forecast just after the Budget is published by the Treasury to incorporate any changes announced by the Chancellor. This would effectively decouple the OBR’s technocratic process from the political decisions of the Budget while retaining its official forecasting role.

This proposal takes inspiration from the Dutch model, in which the pre-measures forecasts are published in the Summer as a standalone forecast, thereby avoiding the pressure on OBR to make judgements in the heat of the political process. It would also reduce incentives for the Treasury to selectively brief contents of the OBR forecast to set a narrative, given that the pre-measures forecast would become known well in advance of policy announcements, while minimising changes to the timeline of the current process.

It would also provide opposition politicians and economic commentators an opportunity to prepare positions on how they would handle the issues rather than being faced with immediately responding without time to digest the forecasts, therefore levelling the playing field for all actors. This matters beyond transparency: this reform would provide financial markets with a set of clear pre-measures assumptions, reducing the incentives for feeding speculation and strengthening fiscal institutions.

The remainder of the article is structured as follows: Section 2 documents the current fiscal policy process; Section 3 analyses the private and public information of different actors in the forecast process; Section 4 compares the UK’s process with other international examples and literature on the desirable properties of an effective independent fiscal institution (IFI); Section 5 presents the reform proposal, describes its strengths and addresses potential objections; and Section 6 concludes.

2. The current fiscal policy process

The UK’s process for setting fiscal policy is relatively unusual among countries with IFIs. The OBR, while an independent body, is heavily embedded in the Budget process while remaining heavily reliant on the government for its modelling capability (Trapp and Nicol, Reference von Trapp and Nicol2017).

This is in many ways a mutualistic relationship. The OBR produces the official forecasts that the Treasury must use in its publications, as prescribed by the Budget Responsibility and National Audit Act 2011—the piece of legislation which governs the OBR’s roles and responsibilities—and therefore the Treasury has a built-in incentive to cooperate with the process. But this set-up makes the OBR one of only three IFIs tasked with producing official forecasts rather than producing alternative scenarios or assessing the reasonableness of the government’s macroeconomic scenarios (OECD, 2020).

To produce its forecasts, the OBR employs a multi-round approach, in which the OBR takes on new outturn data, modelling changes and assumptions in order to converge towards a stable pre-measures base forecast. This has historically been up to four rounds, but in recent years it has stabilised at three (Tetlow and Pope, Reference Tetlow and Pope2024).

Two to three weeks before a fiscal statement to the Commons (and no more than 21 working days other than in exceptional circumstances), the OBR provides the Chancellor with a final pre-measures forecast. This is governed by the OBR’s Memorandum of Understanding (MoU) with government departments.Footnote 2 This creates a hard cut-off for substantive changes that are not due to policy. No new outturn data is taken on past this date, be it economic or fiscal, and no further modelling decisions are made.

This is a step that is necessary for operationalising a forecasting process in which Treasury policy has to be incorporated for a final forecast which is published on the same day by both the Treasury and the OBR. While the Treasury provides a ‘scorecard’—a list of policies under consideration—at various points during the pre-measures forecast, these are not binding, but merely illustrative. It is only when the pre-measures base is finalised that the Treasury then provides what is known as the ‘major measures scorecard’—a provisional list of the policies the government intends to take forward, although still subject to change.

There are two ‘major measures’ rounds, the purpose of which is twofold: to allow the Treasury to iterate its decision-making, while also providing the OBR with the opportunity to incorporate any ‘indirect’ effects of policy. An example of this would be a measure which increases inflation, which therefore affects assumptions about interest rates set by the Bank of England, as well as revenues from taxes whose rates are linked to inflation measures.

The OBR has a materiality threshold for these policies—their indirect effects have to be rather large for them to be incorporated in the forecast at that stage. But there can also be a whole package effect: a group of small measures can together clear the threshold of affecting the whole economy. It is also at this stage that the OBR considers the overall change in fiscal stance and applies any fiscal multipliers to account for changes in tax and spending in the round.

The first ‘major measures’ submission is not binding, but the second one is. At that point, all economy-moving measures should be taken into account, and only small movements should happen in the scorecard. The two post-measures rounds were an innovation brought into place for the March 2023 forecast—prior forecasts would have had only one ‘major measures’ round.

After the ‘major measures’ are locked in, the OBR then produces the second post-measures round of economic and fiscal forecasts. Any subsequent tweaks are added to those forecasts to produce what is the final economic and fiscal forecast, usually on the Friday prior to publication. It is on the basis of this final forecast that the OBR and the Treasury then produce their explanatory documents: the EFO in the case of the former, the Budget Report (nicknamed the ‘Red Book’) for the latter—or the Spring Statement, in the case of the year’s second forecast. Both the OBR and the Treasury’s documents are laid before the House of Commons and are made available to Members of Parliament (MPs) in the Vote Office after the Budget Statement (Erskine May, Reference May2019).

Alongside this work, the OBR scrutinises the government’s costings of policy measures to ensure that the methodology used is both reasonable and ‘central’—which in this sense means that there is as much chance of underestimating the cost of measures as there is of overestimating. Centrality is a core remit of the OBR, as stated in the MoU.Footnote 3

On the day of publication, the Chancellor of the Exchequer makes a statement to the House of Commons, usually around lunchtime. The Treasury documents are then made available to the public at the end of the speech, as are the OBR’s publications. The OBR then does a press conference a few hours later, highlighting their main messages from the forecast.

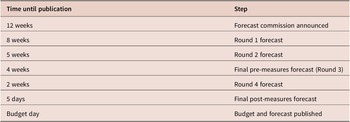

The Autumn 2025 forecast timetable is shown in Table 2, with dates presented as days or weeks until the statement. This was broadly a representative example of the post-2022 forecast process. Note that these are the dates of the fiscal forecast being sent to the Chancellor—the OBR produces its economic assumptions earlier, and disseminates them with the Treasury and government analysts a few days before for modelling purposes. The Treasury has access to a ‘ready reckoner’ model, which allows it to estimate the effects of economic assumption changes on fiscal outcomes with a reasonable degree of accuracy.Footnote 4

A list of the steps in a representative forecast timetable, based on recent OBR publications

Table 2. Long description

From the top row downward, the table has two columns. The left column is labeled Time until publication, and the right column is labeled Step. The first row shows 12 weeks and Forecast commission announced. The second row shows 8 weeks and Round 1 forecast. The third row shows 5 weeks and Round 2 forecast. The fourth row shows 4 weeks and Final pre-measures forecast (Round 3). The fifth row shows 2 weeks and Round 4 forecast. The sixth row shows 5 days and Final post-measures forecast. The last row shows Budget day and Budget and forecast published. Each step is aligned with its corresponding time interval, progressing from earliest to latest.

3. Private and asymmetric information in the forecast process

The setup of the forecast process creates significant amounts of private and privileged information. When the OBR produces economic assumptions and fiscal forecasts, it then sends them to government analysts and ministerial leadership at the Treasury. These forecasts can and do change significantly during the three-month process leading up to the Budget, but they provide an initial indication of magnitudes of movement in the public finances.

This private information creates a substantial asymmetry between insiders and outsiders. It also creates incentives to disseminate selective information, and not all actors have the same constraints.

In this scenario, it is useful to consider three main actors with an interest in the evolution of the public finances:

-

• The OBR, whose role is to produce economic and fiscal forecasts and publish them to the public just after they are presented to the House of Commons by the Chancellor.

-

• HM Treasury (HMT), including both civil servants and political leadership—with the Chancellor of the Exchequer at the helm. The Treasury’s role is to set fiscal policy on the basis of the OBR’s economic and fiscal forecasts, but it is also a political body—and therefore has much more direct interaction with both the public and journalists than the OBR.

-

• The public, who represent both taxpayers and beneficiaries of public spending, and on behalf of whom the Treasury sets policy. The public is a very disparate set of actors, including other politicians, informed observers, financial markets, and members of the public. But all of these subgroups interact with fiscal policy both in their day-to-day lives, and through the receipt of communications—both directly (from the Treasury and the OBR) and indirectly (via the media, which reports on the basis of both public and private knowledge).

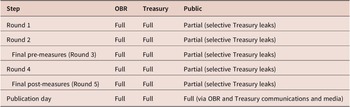

Table 3 shows the information available to each of these actors at the points in the forecast described in Table 2. Table 3 clearly highlights the asymmetry in information across the universe of actors. The OBR and the Treasury have full information over the process throughout. But in a scenario where the Treasury selectively leaks information during the process—as has happened in recent years—all information making it to the public comes through partial information communicated via media stories writing up leaks.

Information matrix for each of the actors in the forecast (OBR, Treasury and the public)

Table 3. Long description

The table has seven rows and four columns. The first row contains headers: Step, OBR, Treasury, and Public. The subsequent rows detail information access for each actor at each forecast stage. For Round 1, Round 2, Final pre-measures (Round 3), Round 4, and Final post-measures (Round 5), both OBR and Treasury have ‘Full’ information, while Public has ‘Partial (selective Treasury leaks)'. On Publication day, all three actors— OBR, Treasury, and Public—have ‘Full’ information, with Public's access specified as ‘Full (via OBR and Treasury communications and media)'.

The OBR, for their part, have no right of reply. Their only meaningful official communication comes on publication day. It means that by then, the Treasury has had nearly three months of bedding in a narrative that is based on only partial information, and which can be selectively disclosed for political purposes.

The public also end up operating on less information than they would like, and crucially, on information that is based on self-selection by the Treasury. Even when the Treasury communicates directly instead of via the media—for example, the Chancellor’s scene-setting speech on 4 November 2025—the information set being conveyed to the public is still partial and determined by the Treasury. An example would be the setting up of a well-known UK tradition for Chancellors to pull a ‘rabbit from the hat’ on the day of a fiscal statement, often announcing a new policy that is not known about or announcing that some unpleasant policy is no longer needed.Footnote 5

This partial and selective information, coming through noisy signals in the media, has real costs in terms of uncertainty. It also almost does not even need saying that it is a dysfunctional way to conduct fiscal policy, leaving weeks of speculation about what the Chancellor might do on the basis of less than a complete picture and incentivising the delaying of consumption and investment decisions.

4. Comparison with approaches in other jurisdictions

While every country’s budget process will have its own unique elements, it is fair to say that the UK’s approach and the role of the OBR are rare among peers. For one, the OBR’s role in providing an official forecast, which the government must use for its tax and spending decisions, is uncommon. According to the OECD (2021), of the OECD’s 35 national IFIs, only two others—Belgium’s Federal Planning Bureau (FPB) and the Netherlands’ Centraal Planbureau (CPB)—produce the official macroeconomic forecast underlying the budget, and the OBR stands alone in producing the official fiscal forecast. A much more common setup is for institutions either to produce alternative macroeconomic (11 out of 35) and/or fiscal forecasts (12 out of 35), or to endorse or assess those forecasts. Of the 35, 29 either endorse or assess the government’s macroeconomic forecasts, while 27 do so for the government’s fiscal forecast.

The most common powers and processes should not however be misunderstood for being the most desirable. The CPB is the world’s oldest IFI, having been established in 1945 and with a total staff of 125, much larger than the average of 34 across the OECD. It has also consistently been ranked as world-leading by OECD and scores in the top four for classifications in all domains considered in the OECD Fiscal Advocacy Index for 2024—independence, analytical focus, communications apparatus and communications impact (OECD, 2025).

The OBR is one of the other three world-leading IFIs in OECD (2025), alongside the United States’ Congressional Budget Office (CBO) and Canada’s Office of the Parliamentary Budget Officer (PBO). These are all institutions that score above 3 out of 4 in the Fiscal Advocacy Index for 2024; no other IFI scores above 2.5. The CBO and the PBO are legislative bodies to serve parliamentarians, and therefore the OBR’s role as an independent agency interacting with the executive is more comparable to the CPB’s.

The OBR is a relatively new body, having only been established in 2010. But despite what is natural criticism, it has established a strong reputation both domestically and internationally, with the most recent external review (van-Geest, Reference van-Geest2025) finding that the OBR had ‘retained its reputation as an organisation committed to the values enshrined in its Charter, working “objectively, transparently and impartially”’.

The 2025 Van Geest Review appraised the obligation of the government to use the OBR’s fiscal projections as standing out internationally and as best practice, but it also recognised that this setup has the effect of putting significant political pressure on the OBR.

This pressure on the OBR crystallised a trade-off for IFIs between relevance in the fiscal policy debate and insulation from outside pressure. The more timely and binding their assessments are in terms of constraining government action, the more in the crossfire they tend to be. From a first principles point of view, this pressure could potentially compromise the OBR’s independence, which is one of the key principles of effective IFIs set out by the OECD (Trapp and Nicol, Reference von Trapp and Nicol2017).

Independence and the perception of independence are of course related to transparency—another of the OECD’s key principles. Greater transparency can have the effect of providing not more information to the public, but also enhancing the independent standing of an IFI by setting out how that independence is delivered in practice. Making more information publicly available in a timely fashion can increase the reputational and electoral costs of imprudent government policy, as set out by Trapp and Nicol (Reference von Trapp and Nicol2017), which reinforces the perception of independence.

In the case of the OBR, publication occurs on Budget Day immediately after the Chancellor of the Exchequer presents their political document to Parliament, with no information disclosed by the OBR in advance. This is only one model; other IFIs tend to publish their assessment days after the Budget, although this difference should be viewed in the context of the embedded nature of the OBR’s role in the forecasting process.

While the OBR only publishes its post-measures forecast, the publication of the standalone pre-measures forecast prior to the Budget is not unprecedented internationally. The CPB publishes a macroeconomic update in the Spring (the Centraal Economisch Plan, or CEP) and a pre-measures draft economic outlook (concept-Macro Economische Verkenning, or concept-MEV, previously known as the koninginne-MEV) in the Summer, before publishing their post-measures forecasts on Budget Day.

5. A proposed reform: decoupling the OBR publication from fiscal statement day

At the moment, official publications come in ‘big bang’ form. On fiscal statement day, both the OBR and the Treasury put out documents and comment to the media on the post-measures forecast, while looking retrospectively at what the government chose to do in response to the pre-measures state of the public finances—which was not known to the public until then.

This essentially conflates two issues:

-

• The underlying pre-measures, technical set of changes that the OBR and modellers include in the forecast. This comprises both methodological changes and outturn data, as well as judgements about the outlook for the economy.

-

• The policy decisions taken by the government, be they due to measures the government wants to take anyway or in response to the fiscal forecasts.

There is however no reason why these need to come at the same time. In fact, waiting until both are fully accounted for creates the vacuum of information mentioned in Section 3, in which selective briefing of privileged Treasury information to the media can set in train a narrative that is not necessarily the full story.

This article takes inspiration from the process run by the CPB in the Netherlands, in which the pre-measures forecast is published in advance of the Budget decisions. It proposes a narrow but potentially impactful change that would decouple the OBR’s publications from the Treasury’s while minimising changes to the current forecasting process.

In this reformed forecasting process, the OBR would bookend the Treasury’s Budget as follows:

-

• The OBR would produce and publish the pre-measures forecast around three weeks before the day of the fiscal statement. This would be essentially the same time at which it already produces the final pre-measures forecast.

-

• The government would then have three weeks to decide its measures and to present them to the House of Commons.

-

• The OBR would subsequently incorporate the government’s measures, alongside any second-round macroeconomic effects (if any), in its fiscal figures and publish the final fiscal forecast sometime after the Budget—perhaps a few days, or maybe a week or two.

In this proposal, the Treasury would publish the Budget measures themselves. While there are different options as to how involved the OBR could or should be, this article advocates for a scenario in which the OBR does not publish a final, post-measures forecast alongside the Budget, but instead has a buffer of time to incorporate the cost of those measures into its models.

5.1. Strengths of this proposed reform

There are two main advantages of this setup. One is that there would be more transparency regarding the underlying situation of the public finances. Instead of waiting until fiscal statement day to be clear on what the government’s options were, this proposal would mean that the public would be informed in advance.

The government would also have a time-limited window in which to make an argument for what fiscal stance it wanted to take. This could then be scrutinised by informed observers such as think tanks and research institutes, but based on firmer evidence than is the case at present. Opposition politicians would also have time to work out their own response and plan for how to deal with the underlying fiscal situation, instead of having to reply immediately with no preparation time (Table 4).

Information matrix for each of the actors in the forecast (HMT, OBR and the public) under the proposed reform

Table 4. Long description

From top to bottom, the table lists six steps: Round 1, Round 2, Final pre-measures (Round 3), Policymaking phase, Budget Day, and Final OBR publication. For OBR, information is full in all rounds except the policymaking phase, where it is marked N slash A. H M T has full information throughout. The public receives partial information via noisy signals through media in Rounds 1 and 2, full information in Final pre-measures (Round 3) via OBR communications and media, baseline full and policy partial (leaks via media) in the policymaking phase, full information on Budget Day via H M T communications and media, and full information in the Final OBR publication via OBR communications and media. The main differences are in the public’s access during early rounds and the policymaking phase, with OBR excluded from the policymaking phase.

Note: The main differences are in the information sets available to each actor in the final pre-measures round and in the policymaking phase. All actors have full information about the baseline, but the Treasury can still decide to brief during the policymaking phase. The OBR’s information set is presented as ‘N/A’ because it has no formal role in the policymaking phase.

Instead, this proposed reform significantly reduces the scope for the Treasury to influence the narrative. With the OBR publishing the pre-measures forecast three weeks before the fiscal statement day, both the media and the public would have full information about the baseline prior to the start of the formal policymaking phase.

Beyond that point, the OBR would have no formal role until the Budget measures are in the public domain. There might still be scope for Treasury briefings during the policymaking phase, but that would be all about the policy decisions the government is considering rather than the OBR’s view of the economy, which would by then be public knowledge.

The second main advantage of this institutional setup would be to remove the OBR from the firing line in one of the major points of conflict between it and the Treasury around the scoring of fiscal policies—particularly in terms of second-round effects. At the moment, the OBR is put in an impossible situation: it has to adjudicate whether or not policies have a large enough effect to move the economic forecast, but it is often very hard to say anything credibly prior to the policies taking effect. At the same time, the Treasury is often fine-tuning final measures to hit particular targets, which puts pressure on the OBR to incorporate these second-round effects.

But it is a situation in which even the absence of a statement can be interpreted as a statement in and of itself. If the government claims, for example, that a policy will have a large supply-side effect, the OBR can incorporate that effect, but it leaves itself open to accusations of favouritism and risks its credibility if it does not materialise. But if the OBR does not incorporate it, then it is in the firing line for being pessimistic about the government’s policies.

In either case, the OBR cannot really win. It is thrust into a discussion about the effectiveness of government policy, when its original mandate is to provide unbiased forecasts as a basis for the Chancellor to make decisions. This is an uncomfortable position for an independent body to be in.

In this proposed reform, however, there would be a clear separation between the OBR’s forecasting role and the Treasury’s role in policymaking:

-

• The OBR stays in its analytical lane prior to the Budget, producing pre-measures forecasts on which the Chancellor can then make decisions;

-

• The government is free to make claims about the effectiveness of policy without being able to hide behind the OBR’s assessment;

-

• The government still needs to be credible in its claims about the effectiveness of policy in order to maintain market confidence, and so market discipline is maintained;

-

• The OBR can then incorporate the policies into the economic and fiscal forecasts when they have already been decided on, therefore breaking the immediate cycle of fine-tuning and reducing pressure on it to accept the government’s view.

This would have the effect of allowing for the possibility of genuine differences of opinion between the Treasury and the OBR without undermining the forecasting process. The government would still be able to pursue the policies it sees fit and which it might genuinely believe to have positive second-round economic effects without having the OBR appraising them before they are even announced. And it would take the OBR away from making judgements on politically contentious areas immediately, preserving the independence of the institution.

5.2. Potential objections and responses

This reform would represent a significant departure from the current setup, so it is important to recognise and address potential objections and whether they might undermine the case for reform. The most important objections are addressed below.

5.2.1. The Treasury would not have enough time to respond

Three weeks might be argued not to be enough time to properly assess the pre-measures forecast and design an adequate policy response.

But the Treasury already has a three-week window in which it makes final policy decisions: it gets the pre-measures forecast three weeks before fiscal statement day, and so it would mean no change to that dynamic. The main difference is that the forecast would be in the public domain, and so there may be additional debate as to what course of action the Treasury takes. In this reform, the Treasury would still have access to the results of interim forecast rounds, therefore giving it more time to consider what policies it might wish to pursue.

5.2.2. Potential adverse market reaction

It may be argued that this process could introduce additional market volatility by publishing a set of pre-measures forecasts without a clear plan from the government for how to address them.

While this might be an important objection in a world in which the forecasts are not known in advance at all, this is far from the current situation. Instead, as shown in Table 1, markets have to make do with months of partial, selectively leaked information. This reform would provide markets with full information about the pre-measures forecast, followed by a three week window of policy speculation—far less than the current three months of partial information about both forecasts and policy.

The Dutch example is also useful in mitigating the extent of this issue. The CPB has been releasing the official draft macroeconomic outlook of the Budget in advance of negotiations for decades, with seemingly no adverse market impact.

Of course, a narrow proposal such as this cannot fully deal with politicians intent on disregarding OBR’s input altogether, but the short window between the Budget and the publication of the post-measures forecast would act to mitigate the incentives of producing costings that are much too optimistic. If the market did not find that out immediately after the Budget, the OBR’s subsequent publication would make that clear pretty quickly.

5.2.3. OBR certification of policy costings is needed for market credibility of the Treasury’s post-measures figures

At the moment, the OBR certifies the reasonableness and centrality of the costings done by the Treasury, which are then used for incorporation in the final, post-measures forecast. Note that these are already Treasury calculations—the OBR can choose to incorporate a different figure, but it has not done so with any meaningfully large measures. An issue might arise, however, around the incentives for the Treasury to produce estimates that are too optimistic, thereby undermining the credibility of the forecasts.

There are two features of the reform that mitigate this. One is that the Treasury would need to retain market credibility in its assessment of policies, which would guard against overly optimistic projections. But the OBR would also come to assess the revenue raised or spending committed through policy decisions relatively swiftly afterwards, and therefore its role is maintained—just with added time to consider its judgements and with a larger buffer against pressure to incorporate overly optimistic second-round effects.

5.2.4. The OBR needs to assess the government’s compliance with the fiscal rules

One of the features of the OBR’s publication on fiscal statement day is a formal assessment of the likelihood of the government meeting its fiscal rules, and it does so on a post-measures basis. Removing the post-measures steps would make it impossible to do so on fiscal statement day.

However, this is a technical question rather than a substantive one. The Budget Responsibility and National Audit Act 2011 only provides for there to be a once-a-year assessment of the meeting of the fiscal rulesFootnote 6 in some form of report.Footnote 7

The OBR could still easily comply with this requirement by incorporating its assessment in the post-measures report, incorporating the government’s policy measures into the forecast.

5.2.5. The baseline would be frozen three weeks in advance, but there might be shocks in the meantime

The most significant risk in this situation is that if there were a significant economic shock, the government might have to operate on the basis of a baseline which is frozen and out of date by the time the Chancellor comes to present their policy decisions.

While this is a valid critique, it applies equally to the current system. Take the March 2020 OBR forecast, for example: between the closing of the pre-measures forecast and publication day, the spread of the Covid pandemic meant that the OBR no longer viewed its own forecast as central by the time it was published.Footnote 8

This is an inevitable consequence of an iterative process in which a very complex economic forecast has to be translated into fiscal forecasts and in which policy requires a stable base to be costed against, and this will be the case regardless of whether the pre-measures forecast is published or not. What this reform does is ensure that all interested parties have full information about what that frozen baseline is rather than having to rely on speculation that is fuelled by Treasury leaks.

5.2.6. There might be a multi-stage ‘media circus’ instead of just one

There might be some concern about the media focussing heavily on three events—the OBR’s pre-measures forecasts, the subsequent fiscal statement and the post-measures report—rather than just the day of the Chancellor’s speech, creating more opportunity for speculation.

But this concern must be viewed in the face of the current situation. At the moment, there are already months of speculation, but based on asymmetric information disseminated by Treasury leaks and media stories (see Table 1) rather than full information about what is in the OBR’s forecast. This puts the OBR in an uncomfortable position of being used like a political football, where the Treasury can use a partial view of the forecasts to justify decisions without the OBR having the ability to counter that narrative. A three-stage process in which the OBR’s bookending role reduces the asymmetry of information between all actors would be far healthier than the current process.

5.2.7. The opposition and other interest groups might use this time to present ‘shadow budgets’, putting pressure on the government

Another argument against this might be that the opposition and other interest groups might use the OBR’s forecast and that three-week window for policymaking to present their own alternative policies and put pressure on the government to respond to those rather than set its own agenda.

This however reveals a strength of this reform rather than a weakness. Opposition parties and civil society groups presenting alternative fiscal responses based on a shared OBR baseline would improve democratic debate and increase engagement with the fiscal policy process. In the current process, the Chancellor has a huge informational advantage when they come to present policies to the House of Commons at a fiscal statement: they know both the pre-measures forecast and the impact of their policies. The opposition and the public only have the selective leaks that have been reported before, and must respond with little to no preparation time. Informed responses would strengthen fiscal scrutiny of the government, which would improve democratic accountability.

6. Conclusion

The UK’s process for setting fiscal policy has become dysfunctional. Particularly since the 2022 ‘mini-budget’ episode, a consistent pattern has been established of briefing of the contents of the OBR’s forecast to the media by the Treasury at a point when those details are meant to be private. The Treasury, of course, has access to the full details of the forecast, and has used this to create a narrative about what it might or might not do, fostering speculation based on partial, selectively leaked information. The result is a relatively opaque process in which economic agents might make decisions on the basis of unrepresentative information, with speculation filling the debate in advance of the Chancellor’s statement, as the Budget process has moved away from its historical secrecy.

This article proposes a narrow reform to mitigate this uncertainty while retaining most of the structure of the forecast process. The OBR would ‘bookend’ the Budget, publishing both a pre-measures forecast three weeks before the Budget and a final, post-measures forecast a few days or a couple of weeks after Budget Day, thus clearly separating the OBR’s analytical modelling from the Treasury’s policy and political statements.

This would change little in terms of the timing of the closing of the pre-measures forecast, but would increase transparency by making information about the underlying state of the public finances available to all actors in the forecast. It would also level the playing field with the opposition and reduce the window for market volatility due to uncertainty about policy decisions based on partial information.

And by moving the post-measures forecast after Budget Day, the OBR would be slightly removed from the political firing line. It would no longer be required to make an assessment of the likely first- and second-round effects of policies before they are announced, allowing it more time to consider policy costings and reducing the incentives for the Treasury to pressure it while fine-tuning fiscal targets.

Given the debate in the UK about how to preserve the independence of the OBR and how to combat the volatility in the period leading up to fiscal statements, this proposal deserves serious consideration as a practical reform aimed at both securing the former and minimising the latter.

Acknowledgements

The author is thankful to Mairi Spowage and Alison Todd for helpful feedback on the proposal and on some of the highlighted potential issues with the reform. The author also thanks the two anonymous NIER reviewers whose comments greatly improved this article. The author used Claude Sonnet 4.5 (Anthropic) to assist with manuscript preparation, including editing, LaTeX formatting and providing feedback on structure and argumentation. All substantive content, analysis, reform proposals and empirical documentation are the author’s own work.

Open access

Open access