1. Introduction

Over the past decade, market-consistent actuarial valuation techniques for quantifying risk have been increasingly embraced not only by academic research but also by the insurance industry, a development that has consequently led to the measurement of assets and liabilities. This shift has been driven by both regulatory and accounting standards and is reflected in frameworks such as the Solvency II Directive (European Parliament and Council, 2021) and the International Financial Reporting Standards (IFRS Foundation, 2017). In particular, under Solvency II, the valuation principle relies on fair value: assets and liabilities must be measured at amounts that could be exchanged or settled in an open market. The detailed valuation framework laid out in the Solvency II Delegated Acts (European Parliament and Council, 2014) prioritizes observable market prices where available. When the liabilities are not hedgeable, technical provisions are computed as the sum of the best estimate (BE) – the present value of expected future cashflows – and the risk margin (RM), which reflects the cost of capital associated with non-hedgeable risks (see, e.g., Olivieri & Pitacco, Reference Olivieri and Pitacco2008).

A key element of modern life-insurance valuation is the careful consideration of demographic risk (see, e.g., Asmussen & Steffensen, Reference Asmussen and Steffensen2020; Wüthrich & Merz, Reference Wüthrich and Merz2013), which captures the uncertainty related to mortality and longevity outcomes. These population-based uncertainties significantly impact the timing and amount of future benefit payments, making them crucial for both the valuation of insurance liabilities and the assessment of capital requirements. In this context, Savelli and Clemente (Reference Savelli and Clemente2013) develop a discrete-time model aimed at evaluating the capital requirement for a cohort of policyholders with homogeneous risks holding traditional life insurance policies, i.e., policies in which the sum insured is deterministic and not linked to financial variables, within a local Generally Accepted Accounting Principles (GAAP) framework. Subsequent studies, see Clemente et al. (Reference Clemente, Della Corte and Savelli2021) and (Reference Clemente, Della Corte and Savelli2022), focus on bridging the local GAAP framework with the market-consistent approach adopted under Solvency II. Within this framework, Wüthrich et al. (Reference Wüthrich, Bühlmann and Furrer2010) propose a model based on the concept of the Claims Development Result (CDR) – the random variable representing profits and losses over a one-year time horizon – used to quantify the risk associated with a cohort of policyholders holding the same type of policy.

In recent decades, insurance products have progressively shifted away from offering a fixed sum insured. Instead, the benefit amount is now tied to the performance of various financial variables, such as asset values, portfolios, or indices, giving rise to the concept of equity-linked policies. These contracts typically include embedded guarantees, which may take the form of terminal-value guarantees (i.e., guarantees at maturity) or Cliquet-type guarantees, where the policyholder annually compounds an interest equal to the maximum between a stochastic rate and a guaranteed minimum rate. A guarantee ensuring a minimum year-on-year return is particularly appealing to risk-averse policyholders, especially in environments characterized by severe, sporadic market downturns. Disruptive events such as the 2000 Dot-com bubble, the 2008 global financial crisis, the 2020 COVID-19 pandemic, the 2022 Russian invasion of Ukraine, and the ongoing 2025 uncertainty surrounding tariffs in the US have underscored the value of products that offer protection against severe market volatility while preserving some participation in upside gains during normal years.

In early contributions, Brennan and Schwartz (Reference Brennan and Schwartz1976) and (Reference Brennan and Schwartz1979) propose an actuarial model for pricing products with a minimum guarantee under no-arbitrage assumptions, leveraging the concept of a hedging portfolio. Specifically, abstracting from demographic considerations, they decompose the policy payoff into the payoffs of equities, bonds, and options. Subsequently, Bacinello (Reference Bacinello2001) introduces a no-arbitrage pricing approach for policies featuring Cliquet-style guarantees. More recently, Barigou and Delong (Reference Barigou and Delong2022) price equity-linked contracts under the assumption that the insurer hedges risks to minimize the local variance of the net asset value process, while requiring compensation for the non-hedgeable portion of the liability in the form of an instantaneous standard deviation RM.

The valuation of insurance products with financial components is therefore a well-established topic in the literature. Perman and Zalokar (Reference Perman and Zalokar2018) examine the conditions under which it becomes optimal to hedge liabilities using derivative instruments within the Cox-Ross-Rubinstein framework, while Møller (Reference Møller1998) focuses on the development of risk-minimizing trading strategies and analyzes the corresponding intrinsic risk processes for various types of unit-linked contracts.

With reference to demographic risk, much of the research has focused on quantifying longevity risk in isolation (see Yang & Zhou, 2023; Gasimova et al., Reference Gasimova, Haberman and Millossovich2025). For example, Stevens et al. (Reference Stevens, De Waegenaere and Melenberg2010) discuss how to determine capital reserves for longevity risk in life insurance under Solvency II, while Boonen (Reference Boonen2017) considers how the results under Solvency II would be affected by the choice of a different risk measure, i.e., Expected Shortfall rather than Value-at-Risk (VaR). Hari et al. (Reference Hari, De Waegenaere, Melenberg and Nijman2008) assess the impact of longevity risk on pension fund solvency, distinguishing between individual (micro) and population-wide (macro) mortality risks.

The fair dynamic valuation of insurance liabilities has been further explored by ensuring market- and time-consistency through mean-variance hedging in a multi-period setting (see Barigou & Dhaene, Reference Barigou and Dhaene2019), by merging actuarial judgment and market-consistency (see Dhaene et al., Reference Dhaene, Stassen, Barigou, Linders and Chen2017), and via a two-step generalized regression approach (see Barigou et al., 2021). Further research includes credit and interest rate risk (see, e.g., Bernard et al., Reference Bernard, Le Courtois and Quittard-Pinon2005; Grosen & Løchte Jørgensen, Reference Grosen and Løchte Jørgensen2000; Möhr, Reference Möhr2011). Comprehensive formulations for market-consistent liability valuations are offered in Wüthrich et al. (Reference Wüthrich, Bühlmann and Furrer2010) and Wüthrich and Merz (Reference Wüthrich and Merz2013), with recent developments introducing two- and three-step valuation procedures that integrate hedging techniques and risk measures (Linders, Reference Linders2023).

Recent work also includes Agarwal et al. (Reference Agarwal, Ewald and Wang2023), who solve a market-based optimal investment problem for a defined-contribution pension scheme with a minimum annuity-purchase guarantee via dynamic programming. They highlight the role of longevity bonds, explicitly distinguishing between systematic (non-diversifiable) and idiosyncratic (diversifiable) mortality risk. Similarly, Agarwal et al. (Reference Agarwal, Ewald and Wang2025), derive (semi-)analytic solutions to the Hamilton–Jacobi–Bellman for optimal investment and income drawdown under stochastic mortality with imperfectly correlated reference populations, showing that longevity bonds remain an effective hedge even in the presence of basis risk and when allowing for dependence between mortality and equity returns. These conceptual links closely relate to our decomposition of demographic uncertainty into idiosyncratic and trend components. In both frameworks, the non-diversifiable longevity component gives rise to market incompleteness, whereas the diversifiable component can be pooled or hedged. Our contribution offers an analogous decomposition and a dynamic market-consistent valuation in the context of equity-linked life insurance with Cliquet guarantees.

The existing literature provides limited insight into the integration of demographic risk modeling with market-consistent valuation, particularly in the context of capital requirement assessments. Bridging this gap would enable insurers to better understand their exposure to demographic risks – such as mortality and longevity – thus supporting more effective pricing, reserving, and capital management strategies. To this end, we propose a novel methodology for quantifying capital requirements related to demographic risk in an equity-linked insurance portfolio with a Cliquet-style guarantee. Building on the theoretical foundations in Wüthrich et al. (Reference Wüthrich, Bühlmann and Furrer2010), Wüthrich and Merz (Reference Wüthrich and Merz2013), our framework focuses on homogeneous risk groups and accounts for both idiosyncratic and trend risks, while also factoring in financial impacts through a market-consistent claims development approach.

Building on Clemente et al. (Reference Clemente, Della Corte, Savelli and Zappa2025), we present the model by moving beyond a purely matrix-based formulation and by providing a more explicit theoretical foundation for valuation and risk-capital analysis. Unlike Clemente et al. (Reference Clemente, Della Corte, Savelli and Zappa2025), who consider a terminal-value guarantee and yield results in line with traditional actuarial expectations, our work shifts the focus to year-on-year guarantees. To this end, we extend the VaPo and CDR framework with three main objectives. First, we establish a solid theoretical basis for the framework that underpins market-consistent valuation and risk measurement. Second, we complete the spectrum of guarantee designs by formally embedding year-on-year local guarantees within a unified market-consistent framework. In particular, the proposed structure generalizes the classical annual high step-up (ratchet) mechanism – typically corresponding to the case of a zero guaranteed rate – by allowing for a strictly positive annual guaranteed return. As a consequence, the guarantee base evolves according to a multiplicative local maximum rule that encompasses traditional reset and ratchet designs as special cases. This formulation makes the financial component of the liability amenable to dynamic hedging arguments consistent with modern arbitrage-free valuation theory. Third, we show that, under a Cliquet-type guarantee, the contract can exhibit negative sums-at-risk, thereby reversing the insurer’s demographic exposure, from mortality risk to longevity risk and vice versa, depending on the realized path of returns and guaranteed minimum rates.

Idiosyncratic risk, in our setting, consists of both diversifiable and systematic components: the former relates to random fluctuations and portfolio characteristics, while the latter reflects estimation uncertainty in mortality forecasting models. Throughout the paper, we use the term trend risk in the specific context of one-year updating as defined in Solvency II: it refers to the risk that the best-estimate mortality assumptions, and consequently the projected future death probabilities, are revised after observing one year of actual experience and recalibrating the selected stochastic mortality model. This definition is more specific than the broader notion of systematic longevity risk often adopted in the literature. In our framework, trend risk is precisely the component that drives the one-year revision of the BE and underlies the trend component of the change in future discretionary benefits.

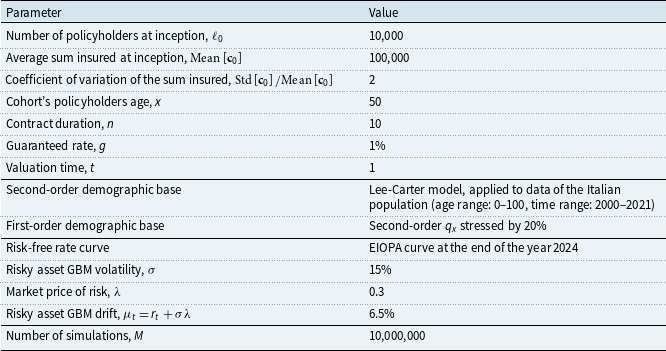

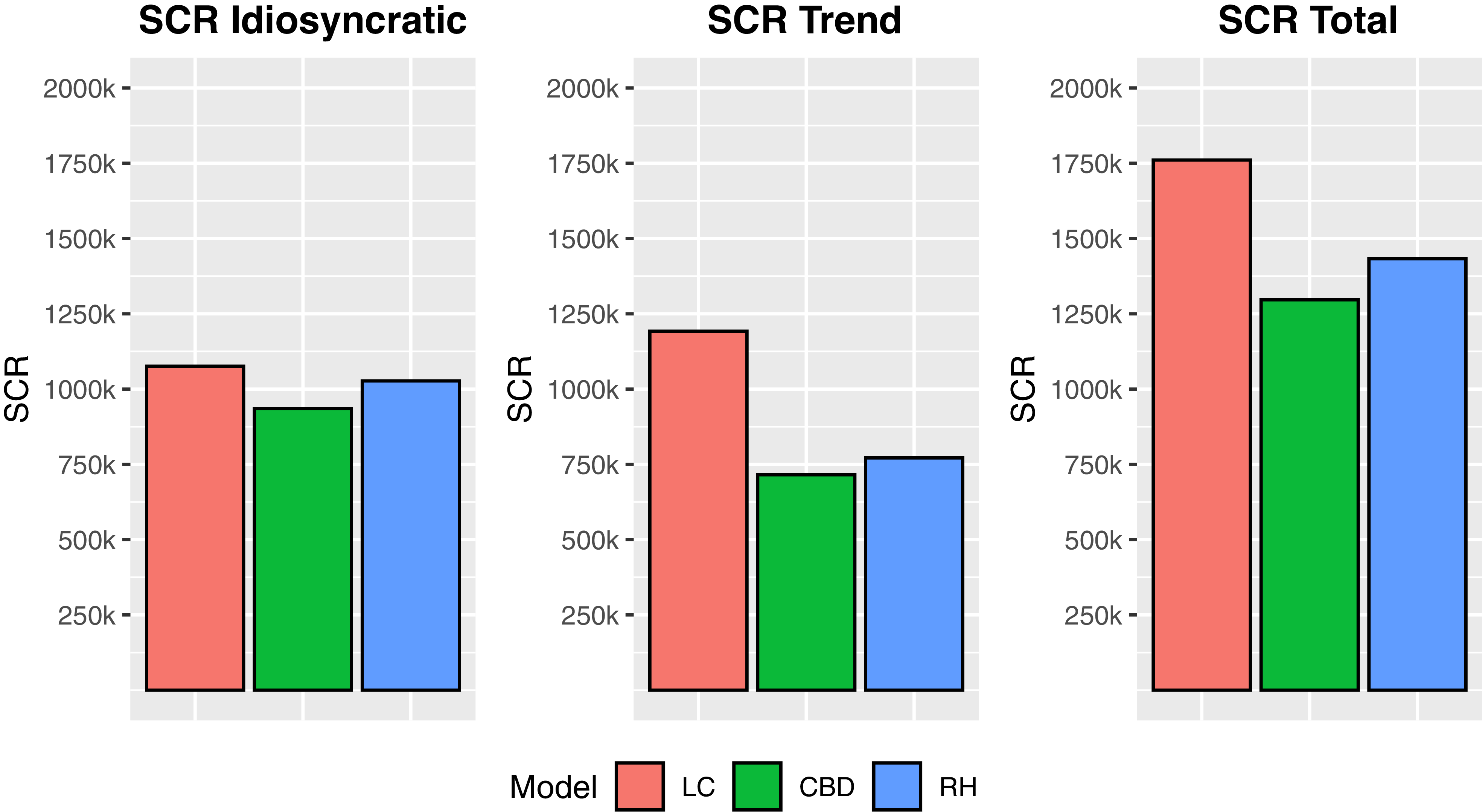

We develop a comprehensive simulation-based framework that captures both sources of demographic risk and considers contract-specific features, such as a Cliquet guarantee and the dispersion of the sums insured across policyholders. A numerical case study illustrates the application of the model and highlights how the capital requirement is influenced by key factors, such as policyholder age, contract duration, volatility of the financial asset, and guaranteed rate. Death probabilities are projected using well-established stochastic mortality models, including Lee-Carter (LC) (Brouhns et al., Reference Brouhns, Denuit and Vermunt2002), Cairns–Blake–Dowd (Reference Cairns, Blake and Dowd2006), and Renshaw–Haberman (Reference Renshaw and Haberman2006), with model uncertainty incorporated into the Solvency Capital Requirement (SCR) estimation.

While designed within the Solvency II regulatory context, the proposed framework is adaptable to alternative regimes and can serve as both a regulatory tool and an internal risk management tool. Furthermore, although our focus is on equity-linked contracts, the methodology naturally extends to traditional insurance products featuring constant benefits.

The remainder of the paper is organized as follows. Section 2 introduces the financial market and the cohort of policyholders. Section 3 outlines the valuation framework for evaluating cash inflows and outflows related to the contract, along with the strategy to replicate and price the contingent claim. In Section 4, we focus on demographic risk, examining its idiosyncratic and trend components, and propose a methodology to assess the capital requirements associated with each component. A numerical analysis is presented in Section 5. Section 6 concludes.

2. Financial and insurance environment

Consider a complete probability space

$\left (\Omega , \mathcal{F}, \mathbb{P}\right )$

equipped with a complete and right–continuous filtration

$\left (\Omega , \mathcal{F}, \mathbb{P}\right )$

equipped with a complete and right–continuous filtration

$\mathbb{F}=\left (\mathcal{F}_t\right )_{t\in [0,n]}$

satisfying the usual conditions. The time horizon

$\mathbb{F}=\left (\mathcal{F}_t\right )_{t\in [0,n]}$

satisfying the usual conditions. The time horizon

$n\lt +\infty$

is expressed in years.

$n\lt +\infty$

is expressed in years.

In the probability space

$(\Omega ,\mathcal F,\mathbb P)$

, we define a Wiener process

$(\Omega ,\mathcal F,\mathbb P)$

, we define a Wiener process

$W=(W_t)_{t\in [0,n]}$

modeling financial risk. We denote by

$W=(W_t)_{t\in [0,n]}$

modeling financial risk. We denote by

$\mathbb F^W=(\mathcal F_t^W)_{t\in [0,n]}$

the subfiltration generated by

$\mathbb F^W=(\mathcal F_t^W)_{t\in [0,n]}$

the subfiltration generated by

$W$

, where

$W$

, where

$ \mathcal F_t^W \;:\!=\; \sigma \left (W_u:\,0\le u\le t\right )$

,

$ \mathcal F_t^W \;:\!=\; \sigma \left (W_u:\,0\le u\le t\right )$

,

$t\in [0,n]$

. The subfiltration

$t\in [0,n]$

. The subfiltration

$\mathbb F^W$

represents the information generated by financial market variables.

$\mathbb F^W$

represents the information generated by financial market variables.

Insurance risk is described by an additional source of uncertainty whose detailed structure will be specified in Subsection 2.2. Since insurance events are observed at yearly dates, we model the corresponding information flow through a subfiltration

$(\mathcal{F}_t^{\mathbb I})_{t\in [0,n]}$

that evolves only on the annual grid and remains constant between observation dates.

$(\mathcal{F}_t^{\mathbb I})_{t\in [0,n]}$

that evolves only on the annual grid and remains constant between observation dates.

Assumption 2.1.

The subfiltrations

$\mathbb{F}^W =(\mathcal{F}_t^W)_{t\in [0,n]}$

and

$\mathbb{F}^W =(\mathcal{F}_t^W)_{t\in [0,n]}$

and

$\mathbb{F}^{\mathbb{I}} =(\mathcal{F}_t^{\mathbb{I}})_{t\in [0,n]}$

are independent (under

$\mathbb{F}^{\mathbb{I}} =(\mathcal{F}_t^{\mathbb{I}})_{t\in [0,n]}$

are independent (under

$\mathbb{P}$

), and we set

$\mathbb{P}$

), and we set

$\mathcal{F}_t \;:\!=\; \mathcal{F}_t^W \vee \mathcal{F}_t^{\mathbb{I}}$

$\mathcal{F}_t \;:\!=\; \mathcal{F}_t^W \vee \mathcal{F}_t^{\mathbb{I}}$

$(t=0,\ldots ,n)$

.

$(t=0,\ldots ,n)$

.

Under Assumption 2.1, financial and insurance risks are independent. This assumption, which is standard in the actuarial literature (see Wüthrich et al., Reference Wüthrich, Bühlmann and Furrer2010), is introduced for analytical tractability and to clearly disentangle demographic (insurance) risk from financial market dynamics in the subsequent valuation and hedging analysis. We proceed by introducing the financial market and the cohort of policyholders.

2.1 The financial market

We consider a risky asset

$\mathcal{S}$

whose time-

$\mathcal{S}$

whose time-

$t$

price,

$t$

price,

$S_t$

, is described under the objective probability measure

$S_t$

, is described under the objective probability measure

$\mathbb{P}$

by the following dynamics:

$\mathbb{P}$

by the following dynamics:

\begin{equation} \mathrm{d}S_t=\mu _t S_t \mathrm{d}t + \sigma _t S_t \mathrm{d}W_t. \end{equation}

\begin{equation} \mathrm{d}S_t=\mu _t S_t \mathrm{d}t + \sigma _t S_t \mathrm{d}W_t. \end{equation}

The stochastic differential equation above suggests that the price of the risky asset follows a geometric Brownian motion, where the time-varying parameters are the drift

$\mu _t$

and the relative volatility

$\mu _t$

and the relative volatility

$\sigma _t$

.

$\sigma _t$

.

We then characterize the bond market and assume deterministic dynamics of the term structure of interest rates, implying that the time-

$t$

instantaneous forward rate for a future date

$t$

instantaneous forward rate for a future date

$\tau \gt t$

,

$\tau \gt t$

,

$f_{t,\tau }$

, coincides with the actual time-

$f_{t,\tau }$

, coincides with the actual time-

$\tau$

instantaneous interest rate,

$\tau$

instantaneous interest rate,

$r_\tau$

. Consequently, denoting with

$r_\tau$

. Consequently, denoting with

$B\left (t,\tau \right )$

the time-

$B\left (t,\tau \right )$

the time-

$t$

price of a default-free zero-coupon bond maturing at time

$t$

price of a default-free zero-coupon bond maturing at time

$\tau \gt t$

, the following relation holds:

$\tau \gt t$

, the following relation holds:

\begin{equation} r_\tau = f_{t,\tau } = -\dfrac { \partial \ln \left (B \left ( t,\tau \right ) \right ) } {\partial \tau }. \end{equation}

\begin{equation} r_\tau = f_{t,\tau } = -\dfrac { \partial \ln \left (B \left ( t,\tau \right ) \right ) } {\partial \tau }. \end{equation}

Different zero-coupon bonds

$\mathcal{B}_i$

(

$\mathcal{B}_i$

(

$i\in \left \{1,\ldots ,N_{\mathcal{B}}\right \}$

) are traded on the financial market, with maturities given by

$i\in \left \{1,\ldots ,N_{\mathcal{B}}\right \}$

) are traded on the financial market, with maturities given by

$T_{\mathcal{B}_i}$

and time-

$T_{\mathcal{B}_i}$

and time-

$t$

prices denoted by

$t$

prices denoted by

$B_{i,t}=B(t,T_{\mathcal{B}_i} )$

.

$B_{i,t}=B(t,T_{\mathcal{B}_i} )$

.

Finally, we assume that European put options

$\mathcal{P}_i$

(

$\mathcal{P}_i$

(

$i\in \left \{1,\ldots ,N_{\mathcal{P}}\right \}$

) written on the underlying risky asset

$i\in \left \{1,\ldots ,N_{\mathcal{P}}\right \}$

) written on the underlying risky asset

$\mathcal{S}$

are traded on the market. The strike prices and maturities of the put options are

$\mathcal{S}$

are traded on the market. The strike prices and maturities of the put options are

$K_{\mathcal{P}_i}$

and

$K_{\mathcal{P}_i}$

and

$T_{\mathcal{P}_i}$

, respectively, while the time-

$T_{\mathcal{P}_i}$

, respectively, while the time-

$t$

prices of the options are denoted by

$t$

prices of the options are denoted by

$P_{i,t}=P(t,T_{\mathcal{P}_i},K_{\mathcal{P}_i})$

.

$P_{i,t}=P(t,T_{\mathcal{P}_i},K_{\mathcal{P}_i})$

.

In the following section, we derive a strategy replicating the financial claim and provide additional details on the maturities of the bonds, as well as on the maturities and strike prices of the put options, that are needed to construct the replicating strategy. The time-

$t$

trading strategy (

$t$

trading strategy (

$t\in \left \{0,\ldots ,n-1\right \}$

) is defined as a multi-dimensional process

$t\in \left \{0,\ldots ,n-1\right \}$

) is defined as a multi-dimensional process

$\left \{\boldsymbol{\theta }_t\right \}_{t\in \left \{0,\ldots ,n-1\right \}}$

predictable with respect to the filtration

$\left \{\boldsymbol{\theta }_t\right \}_{t\in \left \{0,\ldots ,n-1\right \}}$

predictable with respect to the filtration

$\mathbb{F}^W$

, i.e.,

$\mathbb{F}^W$

, i.e.,

$\boldsymbol{\theta }_t$

is

$\boldsymbol{\theta }_t$

is

$\mathcal{F}_{t}^W$

-measurable. More precisely,

$\mathcal{F}_{t}^W$

-measurable. More precisely,

$\boldsymbol{\theta }_t=\left (\theta ^{\mathcal{S}}_t,\theta ^{\mathcal{B}_1}_t,\ldots ,\theta ^{\mathcal{B}_{N_{\mathcal{B}}}}_t,\theta ^{\mathcal{P}_1}_t,\ldots ,\theta ^{\mathcal{P}_{N_{\mathcal{P}}}}_t\right )$

, where

$\boldsymbol{\theta }_t=\left (\theta ^{\mathcal{S}}_t,\theta ^{\mathcal{B}_1}_t,\ldots ,\theta ^{\mathcal{B}_{N_{\mathcal{B}}}}_t,\theta ^{\mathcal{P}_1}_t,\ldots ,\theta ^{\mathcal{P}_{N_{\mathcal{P}}}}_t\right )$

, where

$\theta ^{\mathcal{S}}_t$

is the number of units invested in the stock

$\theta ^{\mathcal{S}}_t$

is the number of units invested in the stock

$\mathcal{S}$

at time

$\mathcal{S}$

at time

$t$

, i.e., for the time interval

$t$

, i.e., for the time interval

$\left (t,t+1\right ]$

, while

$\left (t,t+1\right ]$

, while

$\theta ^{\mathcal{B}_i}_t$

and

$\theta ^{\mathcal{B}_i}_t$

and

$\theta ^{\mathcal{P}_i}_t$

are the analogous for bonds and put options.

$\theta ^{\mathcal{P}_i}_t$

are the analogous for bonds and put options.

Assumption 2.2. We assume that the financial market of traded assets is arbitrage-free and complete.

We consider a continuous-time financial market on the time horizon

$[0,n]$

and work under the objective probability measure

$[0,n]$

and work under the objective probability measure

$\mathbb{P}$

, where the source of uncertainty is the Brownian motion

$\mathbb{P}$

, where the source of uncertainty is the Brownian motion

$W$

. Let

$W$

. Let

$\lambda =\left (\lambda _t\right )_{t\in [0,n]}$

be an

$\lambda =\left (\lambda _t\right )_{t\in [0,n]}$

be an

$\mathbb{F}^W$

-adapted market price of risk process.Footnote 1 Define the stochastic discount factor (density process)

$\mathbb{F}^W$

-adapted market price of risk process.Footnote 1 Define the stochastic discount factor (density process)

$\xi ^\lambda =\left (\xi _t^\lambda \right )_{t\in [0,n]}$

by

$\xi ^\lambda =\left (\xi _t^\lambda \right )_{t\in [0,n]}$

by

\begin{equation} \xi _t^\lambda =\exp \left \{-\int _{0}^{t}\lambda _s\, \mathrm{d}W_s-\frac {1}{2}\int _{0}^{t}\lambda _s^{2}\, \mathrm{d}s\right \}. \end{equation}

\begin{equation} \xi _t^\lambda =\exp \left \{-\int _{0}^{t}\lambda _s\, \mathrm{d}W_s-\frac {1}{2}\int _{0}^{t}\lambda _s^{2}\, \mathrm{d}s\right \}. \end{equation}

Under the above integrability conditions,

$\xi ^\lambda$

is a strictly positive

$\xi ^\lambda$

is a strictly positive

$\mathbb{P}$

-martingale. Hence, following Munk (Reference Munk2013), we define an equivalent probability measure

$\mathbb{P}$

-martingale. Hence, following Munk (Reference Munk2013), we define an equivalent probability measure

$\mathbb{Q}$

on

$\mathbb{Q}$

on

$(\Omega ,\mathcal{F}_n)$

via the Radon–Nikodym derivative

$(\Omega ,\mathcal{F}_n)$

via the Radon–Nikodym derivative

$\frac {\mathrm{d}\mathbb{Q}}{\mathrm{d}\mathbb{P}}\Big |_{\mathcal{F}_n} \;:\!=\; \xi _n^\lambda ,$

so that

$\frac {\mathrm{d}\mathbb{Q}}{\mathrm{d}\mathbb{P}}\Big |_{\mathcal{F}_n} \;:\!=\; \xi _n^\lambda ,$

so that

$\xi _t^\lambda =\mathbb{E}^{\mathbb{P}}\left [\left .\frac {\mathrm{d}\mathbb{Q}}{\mathrm{d}\mathbb{P}}\right |\mathcal{F}_t^W\right ]$

for all

$\xi _t^\lambda =\mathbb{E}^{\mathbb{P}}\left [\left .\frac {\mathrm{d}\mathbb{Q}}{\mathrm{d}\mathbb{P}}\right |\mathcal{F}_t^W\right ]$

for all

$t\in [0,n]$

.

$t\in [0,n]$

.

In our framework, the absence of arbitrage and the completeness of the market are equivalent to the existence of a unique equivalent martingale measure

$\mathbb{Q}$

. Under

$\mathbb{Q}$

. Under

$\mathbb{Q}$

, the discounted price processes are

$\mathbb{Q}$

, the discounted price processes are

$\mathbb{F}^W$

-martingales and, in particular, for

$\mathbb{F}^W$

-martingales and, in particular, for

$t\in \{1,\ldots ,n\}$

,

$t\in \{1,\ldots ,n\}$

,

\begin{align} & S_{t-1} = \mathbb{E}^{\mathbb{Q}}_{t-1} \left [e^{-\int _{t-1}^{t}r_s\,\mathrm{d}s}\,S_t \right ], \end{align}

\begin{align} & S_{t-1} = \mathbb{E}^{\mathbb{Q}}_{t-1} \left [e^{-\int _{t-1}^{t}r_s\,\mathrm{d}s}\,S_t \right ], \end{align}

\begin{align} & B_{i,t-1} = \mathbb{E}^{\mathbb{Q}}_{t-1} \left [e^{-\int _{t-1}^{t}r_s\,\mathrm{d}s}\,B_{i,t} \right ] \quad \forall i\in \left \{1,\ldots ,N_{\mathcal{B}}\right \}, \end{align}

\begin{align} & B_{i,t-1} = \mathbb{E}^{\mathbb{Q}}_{t-1} \left [e^{-\int _{t-1}^{t}r_s\,\mathrm{d}s}\,B_{i,t} \right ] \quad \forall i\in \left \{1,\ldots ,N_{\mathcal{B}}\right \}, \end{align}

\begin{align} & P_{i,t-1} = \mathbb{E}^{\mathbb{Q}}_{t-1} \left [e^{-\int _{t-1}^{t}r_s\,\mathrm{d}s}\,P_{i,t} \right ] \quad \forall i\in \left \{1,\ldots ,N_{\mathcal{P}}\right \}. \end{align}

\begin{align} & P_{i,t-1} = \mathbb{E}^{\mathbb{Q}}_{t-1} \left [e^{-\int _{t-1}^{t}r_s\,\mathrm{d}s}\,P_{i,t} \right ] \quad \forall i\in \left \{1,\ldots ,N_{\mathcal{P}}\right \}. \end{align}

Note that we use the notation

$\mathbb{E}^{\mathbb{Q}}_t\left [\cdot \right ]=\mathbb{E}^{\mathbb{Q}}\big[\cdot \big |\mathcal{F}_{t}^W\big ]$

. For a proof of this equivalence, we refer to Delbaen and Schachermayer (Reference Delbaen and Schachermayer2006).

$\mathbb{E}^{\mathbb{Q}}_t\left [\cdot \right ]=\mathbb{E}^{\mathbb{Q}}\big[\cdot \big |\mathcal{F}_{t}^W\big ]$

. For a proof of this equivalence, we refer to Delbaen and Schachermayer (Reference Delbaen and Schachermayer2006).

2.2 The cohort of policyholders

We assume that, at time

$t=0$

, a cohort of

$t=0$

, a cohort of

$\ell _0\in \mathbb{N}_{\neq 0}$

policyholders with identical characteristics (same entry age

$\ell _0\in \mathbb{N}_{\neq 0}$

policyholders with identical characteristics (same entry age

$x$

, policy term, premium payment pattern, etc.) enters the insurer’s portfolio. The insurer sells equity-linked endowment policies with a Cliquet guarantee to this cohort. Hence, risks are homogeneous across policyholders, except for the sum insured: each policyholder

$x$

, policy term, premium payment pattern, etc.) enters the insurer’s portfolio. The insurer sells equity-linked endowment policies with a Cliquet guarantee to this cohort. Hence, risks are homogeneous across policyholders, except for the sum insured: each policyholder

$k\in \{1,\ldots ,\ell _0\}$

subscribes to the same contract structure with an individual sum insured

$k\in \{1,\ldots ,\ell _0\}$

subscribes to the same contract structure with an individual sum insured

$c_{k,0}$

. We assume that lapses (surrenders) are not allowed over the contract term, so that the only cause of contract termination before maturity is death.

$c_{k,0}$

. We assume that lapses (surrenders) are not allowed over the contract term, so that the only cause of contract termination before maturity is death.

Let

$T_{k,x}$

denote the (unconditional) future lifetime in years of policyholder

$T_{k,x}$

denote the (unconditional) future lifetime in years of policyholder

$k$

measured from time

$k$

measured from time

$t=0$

. Working in discrete time (annual periods), we define the residual lifetime at time

$t=0$

. Working in discrete time (annual periods), we define the residual lifetime at time

$t$

by the convention

$t$

by the convention

\begin{equation} T_{k,x+t} \;:\!=\; \max [T_{k,x}-t,0], \quad t=0,1,\ldots , \quad k\in \{1,\ldots ,\ell _0\}. \end{equation}

\begin{equation} T_{k,x+t} \;:\!=\; \max [T_{k,x}-t,0], \quad t=0,1,\ldots , \quad k\in \{1,\ldots ,\ell _0\}. \end{equation}

In particular,

$T_{k,x+t}=0$

when death occurs at or before time

$T_{k,x+t}=0$

when death occurs at or before time

$t$

. If

$t$

. If

$\{T_{k,x}\gt t\}$

, death occurs after time

$\{T_{k,x}\gt t\}$

, death occurs after time

$t$

and

$t$

and

$T_{k,x+t}=T_{k,x}-t$

represents the remaining lifetime measured from time

$T_{k,x+t}=T_{k,x}-t$

represents the remaining lifetime measured from time

$t$

.

$t$

.

Consistent with the benefit structure of an endowment contract, we introduce the following indicator:

\begin{equation} \mathbb{I}_{k,t}\;:\!=\; \begin{cases} \unicode {x1D7D9}_{\{T_{k,x+t}\in (0,1]\}}, & t=0,\ldots ,n-2,\\ \unicode {x1D7D9}_{\{T_{k,x+t}\gt 0\}}, & t=n-1. \end{cases} \qquad k\in \{1,\ldots ,\ell _0\}. \end{equation}

\begin{equation} \mathbb{I}_{k,t}\;:\!=\; \begin{cases} \unicode {x1D7D9}_{\{T_{k,x+t}\in (0,1]\}}, & t=0,\ldots ,n-2,\\ \unicode {x1D7D9}_{\{T_{k,x+t}\gt 0\}}, & t=n-1. \end{cases} \qquad k\in \{1,\ldots ,\ell _0\}. \end{equation}

For

$t=0,\ldots ,n-2$

, the event

$t=0,\ldots ,n-2$

, the event

$\{\mathbb{I}_{k,t}=1\}$

means that policyholder

$\{\mathbb{I}_{k,t}=1\}$

means that policyholder

$k$

dies during the period

$k$

dies during the period

$(t,t+1]$

, thereby representing the occurrence of the insured event that triggers a death benefit payment at time

$(t,t+1]$

, thereby representing the occurrence of the insured event that triggers a death benefit payment at time

$t+1$

. Accordingly, the sequence

$t+1$

. Accordingly, the sequence

$\{\mathbb{I}_{k,t}\}_{t=0}^{n-2}$

describes whether the policy is in force up to each time

$\{\mathbb{I}_{k,t}\}_{t=0}^{n-2}$

describes whether the policy is in force up to each time

$t$

. The final line in (2.8) is a contractual convention: at maturity (time

$t$

. The final line in (2.8) is a contractual convention: at maturity (time

$n$

), the endowment benefit is payable only if the contract is still in force at time

$n$

), the endowment benefit is payable only if the contract is still in force at time

$n-1$

, which is equivalent to

$n-1$

, which is equivalent to

$\{T_{k,x+t}\gt 0\}$

. This convention allows the use of a single indicator process

$\{T_{k,x+t}\gt 0\}$

. This convention allows the use of a single indicator process

$\{\mathbb{I}_{k,t}\}_{t=0}^{n-1}$

to model both the in-force status over time and the endowment payoff at maturity.

$\{\mathbb{I}_{k,t}\}_{t=0}^{n-1}$

to model both the in-force status over time and the endowment payoff at maturity.

For each

$t=0,\ldots ,n-2$

, the indicator

$t=0,\ldots ,n-2$

, the indicator

$\mathbb{I}_{k,t}$

is observed at time

$\mathbb{I}_{k,t}$

is observed at time

$t+1$

and is therefore

$t+1$

and is therefore

$\mathcal{F}_{t+1}^{\mathbb{I}}$

-measurable (and hence also

$\mathcal{F}_{t+1}^{\mathbb{I}}$

-measurable (and hence also

$\mathcal{F}_{t+1}$

-measurable). Moreover, under Assumption 2.1,

$\mathcal{F}_{t+1}$

-measurable). Moreover, under Assumption 2.1,

$\mathbb{I}_{k,t}$

is independent of

$\mathbb{I}_{k,t}$

is independent of

$\mathcal{F}_t^W$

.

$\mathcal{F}_t^W$

.

Assumption 2.3 (Conditional i.i.d. mortality (among survivors)). For each

$t=0,\ldots ,n-2$

, let

$t=0,\ldots ,n-2$

, let

$Q_{x+t}$

denote the stochastic one-year death probability at age

$Q_{x+t}$

denote the stochastic one-year death probability at age

$x+t$

in the standard actuarial sense, i.e., conditional on being alive at time

$x+t$

in the standard actuarial sense, i.e., conditional on being alive at time

$t$

.

$t$

.

Define the (random) set of policyholders alive at time

$t$

by

$t$

by

\begin{equation} \mathcal L_t \;:\!=\; \{k\in \{1,\ldots ,\ell _0\}:\ T_{k,x}\gt t\}, \qquad \ell _t \;:\!=\; |\mathcal L_t|, \end{equation}

\begin{equation} \mathcal L_t \;:\!=\; \{k\in \{1,\ldots ,\ell _0\}:\ T_{k,x}\gt t\}, \qquad \ell _t \;:\!=\; |\mathcal L_t|, \end{equation}

where

$\ell _t$

is the number of policyholders alive at time

$\ell _t$

is the number of policyholders alive at time

$t$

.

$t$

.

Conditional on

$Q_{x+t}$

, the random variables

$Q_{x+t}$

, the random variables

$\{\mathbb I_{k,t}\}_{k\in \mathcal L_t}$

are independent and identically distributed. Hence,

$\{\mathbb I_{k,t}\}_{k\in \mathcal L_t}$

are independent and identically distributed. Hence,

\begin{equation} \mathbb{I}_{k,t}\,\big |\,\left (Q_{x+t},\,k\in \mathcal L_t\right )\sim \mathrm{Ber}(Q_{x+t}). \end{equation}

\begin{equation} \mathbb{I}_{k,t}\,\big |\,\left (Q_{x+t},\,k\in \mathcal L_t\right )\sim \mathrm{Ber}(Q_{x+t}). \end{equation}

Moreover, for any distinct

$h,k$

,

$h,k$

,

\begin{equation} \mathbb{P}(\mathbb{I}_{h,t}=1,\mathbb{I}_{k,t}=1\,|\,Q_{x+t},\,h\in \mathcal L_t,\,k\in \mathcal L_t) = Q_{x+t}^{2}. \end{equation}

\begin{equation} \mathbb{P}(\mathbb{I}_{h,t}=1,\mathbb{I}_{k,t}=1\,|\,Q_{x+t},\,h\in \mathcal L_t,\,k\in \mathcal L_t) = Q_{x+t}^{2}. \end{equation}

Finally, we define the best-estimate (one-year) death probability at time

$t$

as

$t$

as

\begin{equation} q_{x+t}\;:\!=\; \mathbb{E}^{\mathbb{P}}\left [Q_{x+t}\,\big |\,\mathcal F_t\right ], \end{equation}

\begin{equation} q_{x+t}\;:\!=\; \mathbb{E}^{\mathbb{P}}\left [Q_{x+t}\,\big |\,\mathcal F_t\right ], \end{equation}

i.e., the conditional expectation given the information available up to time

$t$

.

$t$

.

At a generic time

$t\in \{1,\ldots ,n-1\}$

, the sum insured in force for policyholder

$t\in \{1,\ldots ,n-1\}$

, the sum insured in force for policyholder

$k$

is given by

$k$

is given by

\begin{equation} C_{k,t}\;:\!=\; c_{k,0}\prod _{s=0}^{t-1}\left (1-\mathbb{I}_{k,s}\right ), \qquad k\in \{1,\ldots ,\ell _0\}, \end{equation}

\begin{equation} C_{k,t}\;:\!=\; c_{k,0}\prod _{s=0}^{t-1}\left (1-\mathbb{I}_{k,s}\right ), \qquad k\in \{1,\ldots ,\ell _0\}, \end{equation}

which equals

$c_{k,0}$

if no death has occurred up to time

$c_{k,0}$

if no death has occurred up to time

$t$

and

$t$

and

$0$

otherwise. This representation is convenient at the portfolio level, as it allows for modeling the in-force status of contracts and to aggregate mortality-driven cash flows across policyholders.

$0$

otherwise. This representation is convenient at the portfolio level, as it allows for modeling the in-force status of contracts and to aggregate mortality-driven cash flows across policyholders.

3. Cashflows, pricing, and reserving

3.1 Premiums and benefits

Assumption 3.1.

Considering a generic time span

$\left (t,t+1\right ]$

, the premiums are paid by the policyholders at the beginning of the period, i.e., in

$\left (t,t+1\right ]$

, the premiums are paid by the policyholders at the beginning of the period, i.e., in

$t^+$

, while the sums insured of occurred deaths/survivals are paid at the end of the year (i.e., in

$t^+$

, while the sums insured of occurred deaths/survivals are paid at the end of the year (i.e., in

$t+1$

).

$t+1$

).

We first define the

$\mathbb{F}$

-adapted vector of the cashflows, generically indicated with

$\mathbb{F}$

-adapted vector of the cashflows, generically indicated with

$\textbf {X}$

:

$\textbf {X}$

:

\begin{equation} \textbf {X}_{(0)}=(\textit {X}_0,\textit {X}_1,\ldots ,\textit {X}_n). \end{equation}

\begin{equation} \textbf {X}_{(0)}=(\textit {X}_0,\textit {X}_1,\ldots ,\textit {X}_n). \end{equation}

Considering two vectors of random variables,

$\textbf {X}$

and

$\textbf {X}$

and

$\textbf {Y}$

, both of dimension

$\textbf {Y}$

, both of dimension

$n\times 1$

, we assume

$n\times 1$

, we assume

\begin{align} \mathbb{E}\left [\sum _{t=0}^{n}X^2_t\right ]&\lt \infty , \end{align}

\begin{align} \mathbb{E}\left [\sum _{t=0}^{n}X^2_t\right ]&\lt \infty , \end{align}

\begin{align} \mathbb{E}\left [\sum _{t=0}^{n}X_t\cdot Y_t\right ]&\lt \infty . \end{align}

\begin{align} \mathbb{E}\left [\sum _{t=0}^{n}X_t\cdot Y_t\right ]&\lt \infty . \end{align}

Consequently,

$\textbf {X}\in L^2_{n+1}\left (\mathbb{P},\mathbb{F}\right )$

, where

$\textbf {X}\in L^2_{n+1}\left (\mathbb{P},\mathbb{F}\right )$

, where

$L^2_{n+1}\left (\mathbb{P},\mathbb{F}\right )$

is a

$L^2_{n+1}\left (\mathbb{P},\mathbb{F}\right )$

is a

$(n+1)$

-dimensional Hilbert space. For a generic time

$(n+1)$

-dimensional Hilbert space. For a generic time

$t$

, we define inflows and outflows, representing cashflows as follows:

$t$

, we define inflows and outflows, representing cashflows as follows:

\begin{equation} X_\tau \;:\!=\; \begin{cases} -X_\tau ^{in} & \text{if $\tau =t$,} \\[5pt] X_\tau ^{out}-X_\tau ^{in} & \text{if $t\lt \tau \lt n$,}\\[5pt] X_\tau ^{out} & \text{if $\tau =n$}, \end{cases} \end{equation}

\begin{equation} X_\tau \;:\!=\; \begin{cases} -X_\tau ^{in} & \text{if $\tau =t$,} \\[5pt] X_\tau ^{out}-X_\tau ^{in} & \text{if $t\lt \tau \lt n$,}\\[5pt] X_\tau ^{out} & \text{if $\tau =n$}, \end{cases} \end{equation}

where

\begin{align} X_\tau ^{in} & \;:\!=\; \sum _{k=1}^{\ell _0}C_{k,\tau }\cdot \pi \cdot U_{\tau ,\tau }^{in}, \end{align}

\begin{align} X_\tau ^{in} & \;:\!=\; \sum _{k=1}^{\ell _0}C_{k,\tau }\cdot \pi \cdot U_{\tau ,\tau }^{in}, \end{align}

\begin{align} X_\tau ^{out} & \;:\!=\;\sum _{k=1}^{\ell _0}C_{k,\tau -1}\cdot \mathbb{I}_{k,\tau -1}\cdot U_{\tau ,\tau }^{out}. \end{align}

\begin{align} X_\tau ^{out} & \;:\!=\;\sum _{k=1}^{\ell _0}C_{k,\tau -1}\cdot \mathbb{I}_{k,\tau -1}\cdot U_{\tau ,\tau }^{out}. \end{align}

In formula (3.4), the generic time-

$\tau$

cashflow,

$\tau$

cashflow,

$X_\tau$

, is given by the sum of two components: the inflow

$X_\tau$

, is given by the sum of two components: the inflow

$X_\tau ^{in}$

and the outflow

$X_\tau ^{in}$

and the outflow

$X_\tau ^{out}$

. According to Assumption 3.1, the former are paid at the beginning of each time period and the latter at the end.

$X_\tau ^{out}$

. According to Assumption 3.1, the former are paid at the beginning of each time period and the latter at the end.

The inflow received from the

$k$

-th policyholder is the product of three terms: the sum insured at time

$k$

-th policyholder is the product of three terms: the sum insured at time

$\tau$

,

$\tau$

,

$C_{k,\tau }$

, the regular premium rate,

$C_{k,\tau }$

, the regular premium rate,

$\pi$

, and the payout of a unit zero-coupon bond maturing at

$\pi$

, and the payout of a unit zero-coupon bond maturing at

$\tau$

,

$\tau$

,

$U_{\tau ,\tau }^{in}$

. Although the last factor is identically equal to one and could be formally omitted, its role will be clear when the hedging portfolio and the mathematical reserve are determined.

$U_{\tau ,\tau }^{in}$

. Although the last factor is identically equal to one and could be formally omitted, its role will be clear when the hedging portfolio and the mathematical reserve are determined.

Regarding the outflows, the benefit of the

$k$

-th policyholder is the product of the sum insured at time

$k$

-th policyholder is the product of the sum insured at time

$\tau -1$

,

$\tau -1$

,

$C_{k,\tau -1}$

, a binary variable equal to

$C_{k,\tau -1}$

, a binary variable equal to

$1$

if the beneficiary becomes eligible for the benefit at time

$1$

if the beneficiary becomes eligible for the benefit at time

$t$

,

$t$

,

$\mathbb{I}_{k,\tau -1}$

, and the (unitary) revaluation of the sum assured,

$\mathbb{I}_{k,\tau -1}$

, and the (unitary) revaluation of the sum assured,

$U_{\tau ,\tau }^{out}$

. In accordance with the definition of a Cliquet guarantee (see Hipp, Reference Hipp1996; Bacinello, Reference Bacinello2001), such revaluation is defined as:

$U_{\tau ,\tau }^{out}$

. In accordance with the definition of a Cliquet guarantee (see Hipp, Reference Hipp1996; Bacinello, Reference Bacinello2001), such revaluation is defined as:

\begin{equation} U_{\tau ,\tau }^{\textit {out}}\;:\!=\;\prod _{s=1}^{\tau } (1+\max [R_s,g] ), \end{equation}

\begin{equation} U_{\tau ,\tau }^{\textit {out}}\;:\!=\;\prod _{s=1}^{\tau } (1+\max [R_s,g] ), \end{equation}

where

$R_s=\frac {S_s-S_{s-1}}{S_{s-1}}$

is the arithmetic return of the stock between time

$R_s=\frac {S_s-S_{s-1}}{S_{s-1}}$

is the arithmetic return of the stock between time

$s-1$

and time

$s-1$

and time

$s$

, while

$s$

, while

$g$

is the guaranteed per-period return.

$g$

is the guaranteed per-period return.

The quantity

$U^{out}_{\tau ,\tau }$

is the time-

$U^{out}_{\tau ,\tau }$

is the time-

$\tau$

payoff factor per unit of sum insured generated by the Cliquet crediting rule. It represents the value at time

$\tau$

payoff factor per unit of sum insured generated by the Cliquet crediting rule. It represents the value at time

$\tau$

of one monetary unit that is revalued each year by the credited gross return

$\tau$

of one monetary unit that is revalued each year by the credited gross return

$1+\max [R_s,g]$

. Accordingly,

$1+\max [R_s,g]$

. Accordingly,

$U^{out}_{\tau ,\tau }$

is an

$U^{out}_{\tau ,\tau }$

is an

$\mathcal{F}^W_\tau$

-measurable random variable (i.e., a contingent claim), whereas

$\mathcal{F}^W_\tau$

-measurable random variable (i.e., a contingent claim), whereas

$U^{out}_{t,\tau }$

denotes its time-

$U^{out}_{t,\tau }$

denotes its time-

$t$

market-consistent value obtained via the replicating portfolio constructed below.

$t$

market-consistent value obtained via the replicating portfolio constructed below.

3.2 Replication and pricing of the contingent claim

Given

$\tau \in [0,\ldots ,n]$

, the quantities

$\tau \in [0,\ldots ,n]$

, the quantities

$\left (U_{t,\tau }^{in}\right )_{t=0,\ldots ,n}$

and

$\left (U_{t,\tau }^{in}\right )_{t=0,\ldots ,n}$

and

$\left (U_{t,\tau }^{out}\right )_{t=0,\ldots ,n}$

are

$\left (U_{t,\tau }^{out}\right )_{t=0,\ldots ,n}$

are

$\mathbb{F}^W$

-adapted stochastic processes representing the time-

$\mathbb{F}^W$

-adapted stochastic processes representing the time-

$t$

values of the financial portfolios

$t$

values of the financial portfolios

$\mathcal{U}^{in}_{t,\tau }$

and

$\mathcal{U}^{in}_{t,\tau }$

and

$\mathcal{U}^{out}_{t,\tau }$

, respectively used at time

$\mathcal{U}^{out}_{t,\tau }$

, respectively used at time

$t$

to replicate the time-

$t$

to replicate the time-

$\tau$

quantities

$\tau$

quantities

$U_{\tau ,\tau }^{in}$

and

$U_{\tau ,\tau }^{in}$

and

$U_{\tau ,\tau }^{out}$

. While replicating the inflows is straightforward through zero-coupon bonds paying off future premiums, replicating the outflows is more challenging, due to the stochastic and nonlinear nature of the benefit in equation (3.7). The following theorem provides a replicating strategy and the price of the contingent claim.

$U_{\tau ,\tau }^{out}$

. While replicating the inflows is straightforward through zero-coupon bonds paying off future premiums, replicating the outflows is more challenging, due to the stochastic and nonlinear nature of the benefit in equation (3.7). The following theorem provides a replicating strategy and the price of the contingent claim.

Theorem 1.

The claim

$U_{\tau ,\tau }^{\textit {out}}$

is

$U_{\tau ,\tau }^{\textit {out}}$

is

$t$

-hedgeable because there exists a time-

$t$

-hedgeable because there exists a time-

$t$

self-financing strategy

$t$

self-financing strategy

$\boldsymbol{\theta }_{t,\tau }\in \Theta _{t,\tau }$

, with the following positions in the asset

$\boldsymbol{\theta }_{t,\tau }\in \Theta _{t,\tau }$

, with the following positions in the asset

$\mathcal{S}$

and a European put option

$\mathcal{S}$

and a European put option

$\mathcal{P}_t$

with a strike price

$\mathcal{P}_t$

with a strike price

$S_t(1+g)$

expiring at time

$S_t(1+g)$

expiring at time

$t+1$

:

$t+1$

:

\begin{align} \theta _{t,\tau }^{\mathcal{S}} & =\frac {U_{t,\tau }^{\textit {out}}}{S_t+P_t}, \end{align}

\begin{align} \theta _{t,\tau }^{\mathcal{S}} & =\frac {U_{t,\tau }^{\textit {out}}}{S_t+P_t}, \end{align}

\begin{align} \theta _{t,\tau }^{\mathcal{P}_t} & =\frac {U_{t,\tau }^{\textit {out}}}{S_t+P_t}. \end{align}

\begin{align} \theta _{t,\tau }^{\mathcal{P}_t} & =\frac {U_{t,\tau }^{\textit {out}}}{S_t+P_t}. \end{align}

$U_{t,\tau }^{\textit {out}}$

is the time-

$U_{t,\tau }^{\textit {out}}$

is the time-

$t$

price of the claim,

$t$

price of the claim,

\begin{equation} U_{t,\tau }^{\textit {out}}=U_{t,t}^{\textit {out}}\prod _{h=t}^{\tau -1}(1+p_h), \end{equation}

\begin{equation} U_{t,\tau }^{\textit {out}}=U_{t,t}^{\textit {out}}\prod _{h=t}^{\tau -1}(1+p_h), \end{equation}

where

$P_t=S_t p_t$

is the no-arbitrage price of the put option

$P_t=S_t p_t$

is the no-arbitrage price of the put option

$\mathcal{P}_t$

and

$\mathcal{P}_t$

and

$p_{t}$

represents the Black-Scholes price of a European put option on an underlying asset with current price equal to one, strike price equal to

$p_{t}$

represents the Black-Scholes price of a European put option on an underlying asset with current price equal to one, strike price equal to

$1+g$

, time-to-maturity equal to the time period

$1+g$

, time-to-maturity equal to the time period

$\Delta t$

(equal to one under yearly frequency), interest rate

$\Delta t$

(equal to one under yearly frequency), interest rate

$r_{t,t+1}=\frac {1}{\Delta t}\int _{t}^{t+1}r_{s}\mathrm{d}s$

, and volatility

$r_{t,t+1}=\frac {1}{\Delta t}\int _{t}^{t+1}r_{s}\mathrm{d}s$

, and volatility

$\sigma _{t,t+1}=\sqrt {\frac {1}{\Delta t}\int _{t}^{t+1}\sigma _{s}^{2}\mathrm{d}s}$

:

$\sigma _{t,t+1}=\sqrt {\frac {1}{\Delta t}\int _{t}^{t+1}\sigma _{s}^{2}\mathrm{d}s}$

:

\begin{align} p_{t} &=(1+g) e^{-r_{t,t+1}\Delta t}\mathcal{N}\left (-\frac {\log \frac {1}{1+g}+\left (r_{t,t+1}-\frac {\sigma _{t,t+1}^{2}}{2}\right )\Delta t}{\sigma _{t,t+1}\sqrt {\Delta t}}\right )\nonumber \\ &\quad -\mathcal{N}\left (-\frac {\log \frac {1}{1+g}+\left (r_{t,t+1}+\frac {\sigma _{t,t+1}^{2}}{2}\right )\Delta t}{\sigma _{t,t+1}\sqrt {\Delta t}}\right ), \end{align}

\begin{align} p_{t} &=(1+g) e^{-r_{t,t+1}\Delta t}\mathcal{N}\left (-\frac {\log \frac {1}{1+g}+\left (r_{t,t+1}-\frac {\sigma _{t,t+1}^{2}}{2}\right )\Delta t}{\sigma _{t,t+1}\sqrt {\Delta t}}\right )\nonumber \\ &\quad -\mathcal{N}\left (-\frac {\log \frac {1}{1+g}+\left (r_{t,t+1}+\frac {\sigma _{t,t+1}^{2}}{2}\right )\Delta t}{\sigma _{t,t+1}\sqrt {\Delta t}}\right ), \end{align}

where

$\mathcal{N}\left (\cdot \right )$

is the cumulative distribution function of a standard normal random variable.

$\mathcal{N}\left (\cdot \right )$

is the cumulative distribution function of a standard normal random variable.

Proof. See Appendix B.

The self-financing strategy described in Theorem 1 is dynamic, as the position in the risky asset,

$\theta _{t,\tau }^{\mathcal{S}}$

, is adjusted at the beginning of each time period, while the remaining fraction of the portfolio value is invested in a European put option expiring at the end of the relevant time period. The strategy is such that the portfolio is invested in an equal number,

$\theta _{t,\tau }^{\mathcal{S}}$

, is adjusted at the beginning of each time period, while the remaining fraction of the portfolio value is invested in a European put option expiring at the end of the relevant time period. The strategy is such that the portfolio is invested in an equal number,

$\frac {U_{t,\tau }^{\textit {out}}}{S_t+P_t}$

, of units of the stock and the put option. The put options have a strictly positive payoff when the stock return is lower than

$\frac {U_{t,\tau }^{\textit {out}}}{S_t+P_t}$

, of units of the stock and the put option. The put options have a strictly positive payoff when the stock return is lower than

$g$

, so that the minimum guaranteed return is delivered.

$g$

, so that the minimum guaranteed return is delivered.

The time-

$t$

value of the claim maturing at a future date

$t$

value of the claim maturing at a future date

$\tau$

equals the revaluation of the sum insured up to the current time,

$\tau$

equals the revaluation of the sum insured up to the current time,

$U_{t,t}^{\textit {out}} = \prod _{s=1}^{t}(1+\max [R_s,g])$

, increased by the cumulative multiplicative effect of the put option prices normalized by the asset value,

$U_{t,t}^{\textit {out}} = \prod _{s=1}^{t}(1+\max [R_s,g])$

, increased by the cumulative multiplicative effect of the put option prices normalized by the asset value,

$p_h=\frac {P_h}{S_h}$

, applied at each subsequent time step. This additional component ensures that the portfolio value is sufficient to purchase the put options required to guarantee the minimum return in all remaining periods.

$p_h=\frac {P_h}{S_h}$

, applied at each subsequent time step. This additional component ensures that the portfolio value is sufficient to purchase the put options required to guarantee the minimum return in all remaining periods.

3.3 The mathematical reserve and the valuation portfolio approach

Article 76 of Directive 2009/138/EC (European Parliament and Council, 2021) requires that the insurance and reinsurance undertaking hold technical provisions measured at fair value, i.e., “the current amount insurance and reinsurance undertakings would have to pay if they were to transfer their insurance and reinsurance obligations immediately to another insurance or reinsurance undertaking”.

Moreover, the Solvency II Delegated Regulation (see European Parliament and Council, 2014) requires that, with reference to non-hedgeable liabilities where the assessment necessitates the separate quantification of the BE and the RM, this second component should not be included in the calculation of the SCR. We therefore present a market-consistent approach for the calculation of the BE; this approach is coherent with Clemente et al. (Reference Clemente, Della Corte, Savelli and Zappa2025), Wüthrich et al. (Reference Wüthrich, Bühlmann and Furrer2010) and Wüthrich and Merz (Reference Wüthrich and Merz2013).

The purpose of this section is to show the construction of a VaPo and determine its value. A VaPo is a collection of financial instruments designed to replicate a given series of future cashflows. We will outline the steps to build a VaPo, ensuring the final result aligns with the cohort approach. Indicating with

$Q\left (\textbf {X}\right )$

a valuation functional, the mapping

$Q\left (\textbf {X}\right )$

a valuation functional, the mapping

$\textbf {X} \mapsto Q\left (\textbf {X}\right )$

assigns a monetary value, i.e., the market-consistent price, to each cashflow

$\textbf {X} \mapsto Q\left (\textbf {X}\right )$

assigns a monetary value, i.e., the market-consistent price, to each cashflow

$\textbf {X}\in L^2_{n+1}(\mathbb{P},\mathbb{F})$

.Footnote 2 We define the mathematical reserve

$\textbf {X}\in L^2_{n+1}(\mathbb{P},\mathbb{F})$

.Footnote 2 We define the mathematical reserve

$R_t$

at time

$R_t$

at time

$t$

as:

$t$

as:

\begin{equation} R_t\;:\!=\; Q_t(\textbf {X}_{(t)}) . \end{equation}

\begin{equation} R_t\;:\!=\; Q_t(\textbf {X}_{(t)}) . \end{equation}

-

Step 1: Choice of financial instruments. The first step involves selecting the financial basis: referring to Theorem 1, we focus on two groups of financial instruments, i.e., those used to replicate the outflows and inflows, respectively. We denote with

$\mathcal{U}^{out}_{t,\tau }$

the portfolio of financial instruments used at time

$t$

to replicate the outflow

$X_\tau ^{out}$

, which consists in a linear combination of financial instruments available on the market

$\mathcal{M}$

, with weights

$\boldsymbol{\theta }_{t,\tau }$

. Hence,

(3.13)Focusing on the inflows, the portfolio replicating a unitary cashflow at a future time

\begin{equation} \mathcal{U}^{out}_{t,\tau } = \theta ^{\mathcal{S}}_{t,\tau }\cdot \mathcal{S}+\theta ^{\mathcal{P}_t}_{t,\tau }\cdot \mathcal{P}_t . \end{equation}

$\tau$

, i.e., the term

$U_{\tau ,\tau }^{in}$

in equation (3.5), is given by a zero-coupon bond paying one dollar at time

$\tau$

:

(3.14)

\begin{equation} \mathcal{U}^{in}_{t,\tau } = \mathcal{B}_{\tau }. \end{equation}

$\mathcal{U}^{out}_{t,\tau }$

the portfolio of financial instruments used at time

$t$

to replicate the outflow

$X_\tau ^{out}$

, which consists in a linear combination of financial instruments available on the market

$\mathcal{M}$

, with weights

$\boldsymbol{\theta }_{t,\tau }$

. Hence,

(3.13)Focusing on the inflows, the portfolio replicating a unitary cashflow at a future time

\begin{equation} \mathcal{U}^{out}_{t,\tau } = \theta ^{\mathcal{S}}_{t,\tau }\cdot \mathcal{S}+\theta ^{\mathcal{P}_t}_{t,\tau }\cdot \mathcal{P}_t . \end{equation}

$\tau$

, i.e., the term

$U_{\tau ,\tau }^{in}$

in equation (3.5), is given by a zero-coupon bond paying one dollar at time

$\tau$

:

(3.14)

\begin{equation} \mathcal{U}^{in}_{t,\tau } = \mathcal{B}_{\tau }. \end{equation}

-

Step 2: Determine the number of shares of the hedging portfolio. After defining the financial instruments required to replicate outflows and premiums, we determine the BE of the positions in these instruments that the insurance company needs to take in order to replicate the future cashflows

$\textbf {X}_{(t)}$

. Starting from period

$t$

, future outflows begin at time

$t+1$

and require long positions in the VaPo, while the premiums are received from time

$t$

and correspond to short positions:

(3.15)

\begin{equation} \begin{aligned} \textbf {X}_{(t)} & \mapsto VaPo(\textbf {X}_{(t)}) \\ VaPo(\textbf {X}_{(t)}) & = \sum _{k=1}^{\ell _0} \sum _{s=0}^{n-t-1}C_{k,t}\cdot \mathbb{E}_t^{\mathbb{P}}\left [\left (\prod _{h=0}^{s-1}(1-\mathbb{I}_{k,t+h})\right )\cdot \mathbb{I}_{k,t+s}\right ]\cdot \mathcal{U}_{t,t+s+1}^{out} \\ & \quad -\sum _{k=1}^{\ell _0} \sum _{s=0}^{n-t-1}C_{k,t}\cdot \pi \cdot \mathbb{E}_t^{\mathbb{P}}\left [\left (\prod _{h=0}^{s-1}(1-\mathbb{I}_{k,t+h})\right )\right ]\cdot \mathcal{U}_{t,t+s}^{in}. \end{aligned} \end{equation}

-

Step 3: Apply an accounting principle to the VaPo in order to obtain a monetary value for the portfolio. Equation (3.15) provides the positions in a set of financial instruments allowing for hedging outflows and inflows. In this final step, we calculate the BE by assigning a monetary value to each financial instrument to obtain a valuation of the VaPo.

(3.16)The accounting principle

\begin{equation} \begin{aligned} VaPo(\textbf {X}_{(t)}) & \mapsto \upsilon _t\left (VaPo(\textbf {X}_{(t)})\right )=Q_t(\textbf {X}_{(t)})= R_{t} \\ R_{t} & = \sum _{k=1}^{\ell _0} \sum _{s=0}^{n-t-1}C_{k,t}\cdot \mathbb{E}_t^{\mathbb{P}}\left [\left (\prod _{h=0}^{s-1} (1-\mathbb{I}_{k,t+h} )\right )\cdot \mathbb{I}_{k,t+s}\right ]\cdot U_{t,t+s+1}^{out} \\ & \quad -\sum _{k=1}^{\ell _0} \sum _{s=0}^{n-t-1}C_{k,t}\cdot \pi \cdot \mathbb{E}_t^{\mathbb{P}}\left [\left (\prod _{h=0}^{s-1}(1-\mathbb{I}_{k,t+h} )\right )\right ]\cdot U_{t,t+s}^{in} . \end{aligned} \end{equation}

$\left (\upsilon _t\right )_{t\in \left [0,n\right ]}$

assigns a monetary value to the financial instruments and their linear combinations. Among all possible accounting principles,

$\upsilon$

represents the fair value, as required by Solvency II. Notably, each financial instrument is valued at the market price under the assumption of no arbitrage.

4. Demographic risk

Examining a generic time interval

$\left (t,t+1\right ]$

, we assume that, at the beginning of the year, the BE,

$\left (t,t+1\right ]$

, we assume that, at the beginning of the year, the BE,

$R_t$

, and the premiums received in

$R_t$

, and the premiums received in

$t$

,

$t$

,

$X^{in}_t$

, are available. These amounts, when properly allocated, allow for replicating the random claims

$X^{in}_t$

, are available. These amounts, when properly allocated, allow for replicating the random claims

$X^{out}_{t+1}$

and the new reserves

$X^{out}_{t+1}$

and the new reserves

$R_{t+1}$

. Next, we define the quantity

$R_{t+1}$

. Next, we define the quantity

$V_{t+1}$

as follows:

$V_{t+1}$

as follows:

\begin{equation} \begin{aligned} V_{t+1} \;:\!=\; & \sum _{k=1}^{\ell _0} \sum _{s=0}^{n-t-1}C_{k,t}\cdot \mathbb{E}_t^{\mathbb{P}}\left [\left (\prod _{h=0}^{s-1}(1-\mathbb{I}_{k,t+h})\right )\cdot \mathbb{I}_{k,t+s}\right ]\cdot U_{t+1,t+s+1}^{out} \\ &-\sum _{k=1}^{\ell _0} \sum _{s=1}^{n-t-1}C_{k,t}\cdot \pi \cdot \mathbb{E}_t^{\mathbb{P}}\left [\left (\prod _{h=0}^{s-1}(1-\mathbb{I}_{k,t+h})\right )\right ]\cdot U_{t+1,t+s}^{in}. \end{aligned} \end{equation}

\begin{equation} \begin{aligned} V_{t+1} \;:\!=\; & \sum _{k=1}^{\ell _0} \sum _{s=0}^{n-t-1}C_{k,t}\cdot \mathbb{E}_t^{\mathbb{P}}\left [\left (\prod _{h=0}^{s-1}(1-\mathbb{I}_{k,t+h})\right )\cdot \mathbb{I}_{k,t+s}\right ]\cdot U_{t+1,t+s+1}^{out} \\ &-\sum _{k=1}^{\ell _0} \sum _{s=1}^{n-t-1}C_{k,t}\cdot \pi \cdot \mathbb{E}_t^{\mathbb{P}}\left [\left (\prod _{h=0}^{s-1}(1-\mathbb{I}_{k,t+h})\right )\right ]\cdot U_{t+1,t+s}^{in}. \end{aligned} \end{equation}

Considering the cohort of policyholders alive at time

$t$

,

$t$

,

$V_{t+1}$

represents the difference between the expected present values of benefits and premiums that are paid and collected starting from time

$V_{t+1}$

represents the difference between the expected present values of benefits and premiums that are paid and collected starting from time

$t+1$

, based on the financial information available up to time

$t+1$

, based on the financial information available up to time

$t+1$

. In other words, we assume that the portfolio

$t+1$

. In other words, we assume that the portfolio

$VaPo(\textbf {X}_{(t)})$

is purchased at time

$VaPo(\textbf {X}_{(t)})$

is purchased at time

$t$

at its market price

$t$

at its market price

$R_t$

, while the insurance company receives the inflow

$R_t$

, while the insurance company receives the inflow

$X^{in}_t$

from the policyholders. At the end of the year–at

$X^{in}_t$

from the policyholders. At the end of the year–at

$t+1$

–the total market value is

$t+1$

–the total market value is

$V_{t+1}$

.

$V_{t+1}$

.

We define the CDR as:

\begin{equation} CDR_{t+1}\;:\!=\; V_{t+1}-X^{out}_{t+1}-R_{t+1} \end{equation}

\begin{equation} CDR_{t+1}\;:\!=\; V_{t+1}-X^{out}_{t+1}-R_{t+1} \end{equation}

Two sources of randomness affect

$CDR_{t+1}$

. Notably,

$CDR_{t+1}$

. Notably,

$X^{out}_{t+1}$

is influenced only by accidental mortality, as it does not depend on the technical bases of the insurance company. On the other hand,

$X^{out}_{t+1}$

is influenced only by accidental mortality, as it does not depend on the technical bases of the insurance company. On the other hand,

$R_{t+1}$

is affected by both accidental mortality, i.e., deaths between

$R_{t+1}$

is affected by both accidental mortality, i.e., deaths between

$t$

and

$t$

and

$t+1$

, reducing the number of individuals for whom reserves in

$t+1$

, reducing the number of individuals for whom reserves in

$t+1$

must be set aside, and uncertainty arising from the technical assumptions used. Indeed, at time

$t+1$

must be set aside, and uncertainty arising from the technical assumptions used. Indeed, at time

$t$

, the insurance company is uncertain about the technical bases it will apply in

$t$

, the insurance company is uncertain about the technical bases it will apply in

$t+1$

.

$t+1$

.

Following the observation above, we introduce the quantity

$\bar {R}_{t+1}$

, representing the mathematical reserve at time

$\bar {R}_{t+1}$

, representing the mathematical reserve at time

$t+1$

, based on contemporaneous market prices, but under the assumption that the company has not revised its demographic basis between times

$t+1$

, based on contemporaneous market prices, but under the assumption that the company has not revised its demographic basis between times

$t$

and

$t$

and

$t+1$

:

$t+1$

:

\begin{equation} \bar {R}_{t+1} = \sum _{k=1}^{\ell _0} C_{k,t+1}\cdot \beta _{t+1}, \end{equation}

\begin{equation} \bar {R}_{t+1} = \sum _{k=1}^{\ell _0} C_{k,t+1}\cdot \beta _{t+1}, \end{equation}

where

$\beta _{t+1}$

is the mathematical reserve rate:

$\beta _{t+1}$

is the mathematical reserve rate:

\begin{equation} \begin{aligned} \beta _{t+1}=&\sum _{s=0}^{n-t-2}\mathbb{E}_t^{\mathbb{P}}\left [\left (\prod _{h=0}^{s-1}(1-\mathbb{I}_{k,t+h+1})\right )\cdot \mathbb{I}_{k,t+s+1}\right ]\cdot U_{t+1,t+s+2}^{out}\\ &-\pi \cdot \sum _{s=0}^{n-t-2}\mathbb{E}_t^{\mathbb{P}}\left [\left (\prod _{h=0}^{s-1}(1-\mathbb{I}_{k,t+h+1})\right )\right ]\cdot U_{t+1,t+s+1}^{in}. \end{aligned} \end{equation}

\begin{equation} \begin{aligned} \beta _{t+1}=&\sum _{s=0}^{n-t-2}\mathbb{E}_t^{\mathbb{P}}\left [\left (\prod _{h=0}^{s-1}(1-\mathbb{I}_{k,t+h+1})\right )\cdot \mathbb{I}_{k,t+s+1}\right ]\cdot U_{t+1,t+s+2}^{out}\\ &-\pi \cdot \sum _{s=0}^{n-t-2}\mathbb{E}_t^{\mathbb{P}}\left [\left (\prod _{h=0}^{s-1}(1-\mathbb{I}_{k,t+h+1})\right )\right ]\cdot U_{t+1,t+s+1}^{in}. \end{aligned} \end{equation}

Based on the equation above,

$\beta _{t+1}$

, and consequently

$\beta _{t+1}$

, and consequently

$\bar {R}_{t+1}$

, are conditional on time-

$\bar {R}_{t+1}$

, are conditional on time-

$t+1$

market prices and the time-

$t+1$

market prices and the time-

$t$

demographic basis.Footnote 3

$t$

demographic basis.Footnote 3

The definition in (4.3) enables a breakdown of

$CDR_{t+1}$

into two distinct contributions, reflecting idiosyncratic and trend risks, respectively:

$CDR_{t+1}$

into two distinct contributions, reflecting idiosyncratic and trend risks, respectively:

\begin{align} CDR^{Idios}_{t+1} & = V_{t+1}-X^{out}_{t+1}-\bar {R}_{t+1}, \end{align}

\begin{align} CDR^{Idios}_{t+1} & = V_{t+1}-X^{out}_{t+1}-\bar {R}_{t+1}, \end{align}

\begin{align} CDR^{Trend}_{t+1} & = \bar {R}_{t+1}-R_{t+1}. \end{align}

\begin{align} CDR^{Trend}_{t+1} & = \bar {R}_{t+1}-R_{t+1}. \end{align}

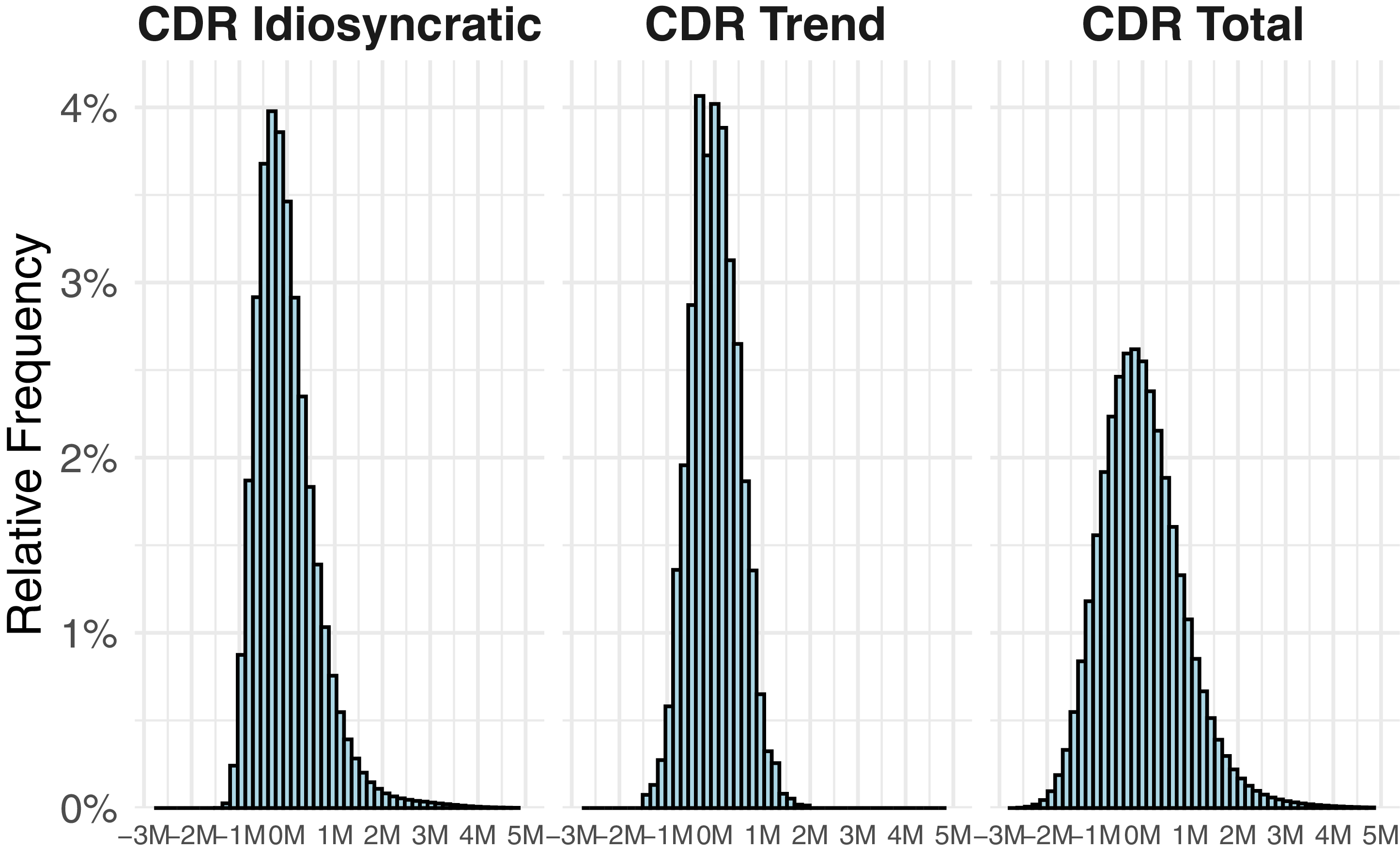

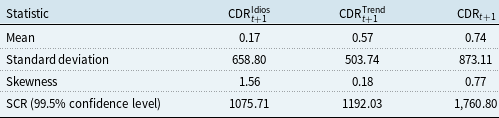

We proceed by analyzing the two components separately, studying their distributions and quantifying the corresponding capital requirements.

4.1 Characteristics of demographic – idiosyncratic risk

The following theorem provides a compact formula for the CDR due to the idiosyncratic component.

Theorem 2.

The idiosyncratic component of the Claims Development Result for a cohort of

$\ell _0$

policyholders can be calculated as:

$\ell _0$

policyholders can be calculated as:

\begin{equation} CDR^{Idios}_{t+1}=\left (\sum _{k=1}^{\ell _0}C_{k,t}\cdot \big(\mathbb{E}_t^{\mathbb{P}}[\mathbb{I}_{k,t}]-\mathbb{I}_{k,t}\big)\right )\cdot \eta _{t+1}, \end{equation}

\begin{equation} CDR^{Idios}_{t+1}=\left (\sum _{k=1}^{\ell _0}C_{k,t}\cdot \big(\mathbb{E}_t^{\mathbb{P}}[\mathbb{I}_{k,t}]-\mathbb{I}_{k,t}\big)\right )\cdot \eta _{t+1}, \end{equation}

where

$\eta _{t+1}$

is the stochastic Sum-at-Risk (SAR) rate, defined as:

$\eta _{t+1}$

is the stochastic Sum-at-Risk (SAR) rate, defined as:

\begin{equation} \eta _{t+1}= U_{t+1,t+1}^{out}-\beta _{t+1}, \end{equation}

\begin{equation} \eta _{t+1}= U_{t+1,t+1}^{out}-\beta _{t+1}, \end{equation}

where

$\beta _{t+1}$

is the BE rate at time

$\beta _{t+1}$

is the BE rate at time

$t+1$

based on the demographic basis defined at time

$t+1$

based on the demographic basis defined at time

$t$

, defined in formula (

4.4

).

$t$

, defined in formula (

4.4

).

Proof. See Appendix C.

The idiosyncratic component of the CDR is given by the product of two factors. The first is the most significant from a demographic standpoint and depends on the difference

$\mathbb{E}_t^{\mathbb{P}}\left [\mathbb{I}_{k,t}\right ]-\mathbb{I}_{k,t}$

, taking negative values when actual mortality is higher than expected mortality between

$\mathbb{E}_t^{\mathbb{P}}\left [\mathbb{I}_{k,t}\right ]-\mathbb{I}_{k,t}$

, taking negative values when actual mortality is higher than expected mortality between

$t$

and

$t$

and

$t+1$

, and positive values when it is lower.Footnote 4 The sums insured across the entire cohort of

$t+1$

, and positive values when it is lower.Footnote 4 The sums insured across the entire cohort of

$\ell _0$

policyholders,

$\ell _0$

policyholders,

$C_{k,t}$

, act as a scaling factor in this term.

$C_{k,t}$

, act as a scaling factor in this term.

The second term,

$\eta _{t+1}$

, represents the SAR rate of the contract. For traditional policies with fixed (non-revalued) benefits, the outflow settled at time

$\eta _{t+1}$

, represents the SAR rate of the contract. For traditional policies with fixed (non-revalued) benefits, the outflow settled at time

$t+1$

upon death is deterministic and equal to one per unit of sum insured, i.e.

$t+1$

upon death is deterministic and equal to one per unit of sum insured, i.e.

$U^{out}_{t+1,t+1}=1$

. In that setting, the best-estimate rate typically satisfies

$U^{out}_{t+1,t+1}=1$

. In that setting, the best-estimate rate typically satisfies

$0\lt \beta _{t+1}\lt 1$

, so that the SAR rate is positive.

$0\lt \beta _{t+1}\lt 1$

, so that the SAR rate is positive.

In our framework, instead,

$\eta _{t+1}=U^{out}_{t+1,t+1}-\beta _{t+1}$

is random at time

$\eta _{t+1}=U^{out}_{t+1,t+1}-\beta _{t+1}$

is random at time

$t$

, since both

$t$

, since both

$U^{out}_{t+1,t+1}$

and

$U^{out}_{t+1,t+1}$

and

$\beta _{t+1}$

depend on market outcomes between

$\beta _{t+1}$

depend on market outcomes between

$t$

and

$t$

and

$t+1$

, while the demographic assumptions underlying

$t+1$

, while the demographic assumptions underlying

$\beta _{t+1}$

are fixed at time

$\beta _{t+1}$

are fixed at time

$t$

. Economically,

$t$

. Economically,

$U^{out}_{t+1,t+1}$

is the amount required to settle the policy immediately at time

$U^{out}_{t+1,t+1}$

is the amount required to settle the policy immediately at time

$t+1$

upon death, whereas

$t+1$

upon death, whereas

$\beta _{t+1}$

is the market-consistent continuation value of the contract at time

$\beta _{t+1}$

is the market-consistent continuation value of the contract at time

$t+1$

. Hence, the sign of

$t+1$

. Hence, the sign of

$\eta _{t+1}$

determines whether idiosyncratic deviations generate losses through excess deaths or through excess survivals: if

$\eta _{t+1}$

determines whether idiosyncratic deviations generate losses through excess deaths or through excess survivals: if

$\eta _{t+1}\gt 0$

, an excess of deaths requires additional resources to settle the claim at

$\eta _{t+1}\gt 0$

, an excess of deaths requires additional resources to settle the claim at

$t+1$

, while if

$t+1$

, while if

$\eta _{t+1}\lt 0$

the opposite mechanism prevails and excess survivals are costly.

$\eta _{t+1}\lt 0$

the opposite mechanism prevails and excess survivals are costly.

The possibility of a negative SAR rate is specific to equity-linked contracts with path-dependent guarantees. Indeed, equation (3.10) implies that, for any

$t+1\lt \tau \le n$

,

$t+1\lt \tau \le n$

,

\begin{equation} {U^{out}_{t+1,\tau }=U^{out}_{t+1,t+1}\prod _{h=t+1}^{\tau -1}(1+p_h)\ \ge \ U^{out}_{t+1,t+1},} \end{equation}

\begin{equation} {U^{out}_{t+1,\tau }=U^{out}_{t+1,t+1}\prod _{h=t+1}^{\tau -1}(1+p_h)\ \ge \ U^{out}_{t+1,t+1},} \end{equation}

with strict inequality whenever

$p_h\gt 0$

on a set of positive probability. Therefore, the longer the policy remains in force, the greater the value of the future benefit that must be hedged, since in each remaining period the insurer must be able to finance the purchase of the put option required to enforce the guaranteed rate. When

$p_h\gt 0$

on a set of positive probability. Therefore, the longer the policy remains in force, the greater the value of the future benefit that must be hedged, since in each remaining period the insurer must be able to finance the purchase of the put option required to enforce the guaranteed rate. When

$\eta _{t+1}\lt 0$

(i.e.

$\eta _{t+1}\lt 0$

(i.e.

$\beta _{t+1}\gt U^{out}_{t+1,t+1}$

), the immediate settlement value upon death is smaller than the continuation value. Intuitively, an early death shortens the period over which the guarantee must be provided and releases part of the replicating resources, whereas an unexpectedly large number of surviving policyholders extends the hedging horizon and may render the financial positions established at time

$\beta _{t+1}\gt U^{out}_{t+1,t+1}$

), the immediate settlement value upon death is smaller than the continuation value. Intuitively, an early death shortens the period over which the guarantee must be provided and releases part of the replicating resources, whereas an unexpectedly large number of surviving policyholders extends the hedging horizon and may render the financial positions established at time

$t$

insufficient. In this case, additional options and stock positions are required to preserve the guarantee over the remaining periods, so that idiosyncratic losses are driven by deviations towards higher-than-expected survivorship.

$t$

insufficient. In this case, additional options and stock positions are required to preserve the guarantee over the remaining periods, so that idiosyncratic losses are driven by deviations towards higher-than-expected survivorship.

Applying the Tower Property to equation (4.5) implies that the expected value of the idiosyncratic component of the CDR is zero, i.e.,

\begin{equation} \mathbb{E}^{\mathbb{P}}_t\big[CDR^{Idios}_{t+1}\big]=0. \end{equation}

\begin{equation} \mathbb{E}^{\mathbb{P}}_t\big[CDR^{Idios}_{t+1}\big]=0. \end{equation}

In line with intuition, there is no expected accidental profit or loss, as, on average, accidental mortality aligns with expected mortality (see also Clemente et al., Reference Clemente, Della Corte, Savelli and Zappa2025 and Wüthrich & Merz, Reference Wüthrich and Merz2013).

The conditional variance of

$CDR^{Idios}_{t+1}$

is given by the following formula (proved in Appendix D):

$CDR^{Idios}_{t+1}$

is given by the following formula (proved in Appendix D):

\begin{equation} \mathrm{Var}_t\big [CDR_{t+1}^{Idios}\big ] = \big ( \ell _t\,\bar {C}_t^{2}\,q_{x+t}(1-q_{x+t} ) +\big (\ell _t^{2}\, \big(\bar {C}_t^{1} \big)^{2}-\ell _t\,\bar {C}_t^{2}\big)\sigma ^{2}_{Q_{x+t}} \big)\, \mathbb{E}_t^{\mathbb{P}}\left [\eta _{t+1}^{2}\right ], \end{equation}

\begin{equation} \mathrm{Var}_t\big [CDR_{t+1}^{Idios}\big ] = \big ( \ell _t\,\bar {C}_t^{2}\,q_{x+t}(1-q_{x+t} ) +\big (\ell _t^{2}\, \big(\bar {C}_t^{1} \big)^{2}-\ell _t\,\bar {C}_t^{2}\big)\sigma ^{2}_{Q_{x+t}} \big)\, \mathbb{E}_t^{\mathbb{P}}\left [\eta _{t+1}^{2}\right ], \end{equation}

where

$\bar {C}_t^j$

is the raw moment of order

$\bar {C}_t^j$

is the raw moment of order

$j$

of the vector of the sums insured and

$j$

of the vector of the sums insured and

$\sigma ^2_{Q_{x+t}}$

is the variance of the parameter of the mixed Bernoulli random variable,

$\sigma ^2_{Q_{x+t}}$

is the variance of the parameter of the mixed Bernoulli random variable,

$Q_{x+t}$

. Specifically, we observe that the idiosyncratic volatility consists of two components: the first is fully diversifiable by increasing the cohort size, while the second arises from the uncertainty in the BE of the Bernoulli parameter. Importantly, equation (4.11) relies on the assumption that, given the mortality parameter

$Q_{x+t}$

. Specifically, we observe that the idiosyncratic volatility consists of two components: the first is fully diversifiable by increasing the cohort size, while the second arises from the uncertainty in the BE of the Bernoulli parameter. Importantly, equation (4.11) relies on the assumption that, given the mortality parameter

$Q_{x+t}$

, the deaths of individual policyholders are conditionally independent and identically distributed. A natural extension would be to relax this assumption using a frailty model (Olivieri and Pitacco, Reference Olivieri and Pitacco2016), which introduces a latent random effect capturing unobserved heterogeneity and dependence between policyholders. This would allow the model to account for correlated mortality shocks.

$Q_{x+t}$

, the deaths of individual policyholders are conditionally independent and identically distributed. A natural extension would be to relax this assumption using a frailty model (Olivieri and Pitacco, Reference Olivieri and Pitacco2016), which introduces a latent random effect capturing unobserved heterogeneity and dependence between policyholders. This would allow the model to account for correlated mortality shocks.