Aggregate US household debt rose to $18.04 trillion in 2024, a sharp increase since the end of 2019, prior to the COVID-19 pandemic (Federal Reserve Bank of New York, 2024). Both housing debt (mortgages and home equity lines of credit) and non-housing balances (credit cards, auto loans, and consumer loans) increased, and delinquency transition rates also increased for most types of debt. Of particular interest to the present study, there is evidence that older Americans are increasingly likely to carry debt into retirement (see, e.g., Butrica and Karamcheva, Reference Butrica and Karamcheva2018; Lusardi et al., Reference Lusardi, Mitchell and Oggero2018; Lusardi and Mitchell, Reference Lusardi, Mitchell, Lusardi and Mitchell2020; Brown et al., Reference Brown, Dynan, Figinski, Mitchell and Lusardi2020a). Not only are older individuals more likely to hold debt than in the past, but their volume of debt has also grown substantially, both in absolute terms and relative to income and assets. For instance, Lusardi et al. (Reference Lusardi, Mitchell and Oggero2020a) showed that the median debt-to-asset ratio for pre-retirees rose almost four-fold among Early Boomers compared to previous generations.Footnote 1 As a consequence, managing debt and personal finances may be particularly problematic for the older population (Agarwal et al., Reference Agarwal, Driscoll, Gabaix and Laibson2009), which often lacks financial sophistication (Lusardi et al., Reference Lusardi, Mitchell and Curto2014).

This reality gives rise to concerns regarding retirement security for several reasons. For one, rising debt burdens may shape how much older workers can contribute to their retirement accounts and how they must manage their retirement savings. Additionally, as interest rates have continued to rise, near-retirees and retirees must allocate larger fractions of their income to service their debts. Rising debt can also prompt delayed retirement, as people seek to recover their financial standing (Lusardi and Mitchell, Reference Lusardi, Mitchell, Goldin and Kat2017). Furthermore, the ability of pre-retirees to repay their debt may decrease once they retire and no longer have paychecks. As people age, they are more likely to experience negative events such as health problems that not only threaten their capacity to service previous debt but may also result in more borrowing, for example, to cover medical expenses (Butrica and Mudrazija, Reference Butrica and Mudrazija2020).Footnote 2 Finally, studies have shown that carrying debt has a negative impact on physical and mental health for older adults, with unsecured debt having a larger adverse effect. Debt levels matter too: the more debt older people hold, the more detrimental it is for their health (Mudrazija and Butrica, Reference Mudrazija and Butrica2023).

While past studies have examined wealth and wealth accumulation, far less is known about debt and debt management among older people, and most of the datasets previously examined did not provide disaggregated debt indicators.Footnote 3 Some authors have investigated the links between debt-related behavior and financial literacy, but few have focused on individuals at older ages. For example, Lusardi and Tufano (Reference Lusardi and Tufano2015) found that Americans with lower levels of debt literacy tend to use high-cost methods of borrowing, such as payday loans, pawn shops, and auto title loans, and incur high fees. Similarly, studies focusing on the UK showed that borrowers who lacked financial literacy held higher proportions of high-cost credit and were more likely to feel over-indebted (Gathergood, Reference Gathergood2012; Disney and Gathergood, Reference Disney and Gathergood2013). Additionally, low levels of financial literacy increased the likelihood that people chose mortgages with larger balloon payments (Gathergood and Weber, Reference Gathergood and Weber2017) and did not refinance their mortgages when the opportunity arose (Barbi and Bajo, Reference Barbi and Bajo2018). Focusing instead on older persons, Fong et al. (Reference Fong, Koh, Mitchell and Rohwedder2021) found that higher financial literacy was associated with a greater propensity to pay off credit card balances on time.

In this paper, we examine the prevalence of debt in the older population, evaluate people’s assessment of their credit records and financial distress, and assess their understanding of fundamental financial concepts. To this end, we use data from the 2018 National Financial Capability Study (NFCS), collected well before the start of the COVID-19 pandemic and the economic shutdown, and we focus on respondents aged 51–61 years, i.e., before they could claim Social Security retiree benefits. The NFCS provides uniquely valuable information on how households manage their liabilities, as it includes subjective measures of respondents’ financial distress and debt burdens. The survey also asks individuals a set of questions intended to measure respondents’ financial well-being. Additionally, it offers information on the potential determinants of financial perceptions and behaviors, such as socio-demographic characteristics, negative income shocks, and health insurance coverage. Finally, the NFCS includes a set of financial literacy questions, allowing us to assess respondents’ understanding of simple concepts such as interest compounding in the context of debt, inflation, risk diversification, bond prices, and mortgages, as well as respondents’ capacity to do simple calculations. Moreover, the 2018 NFCS offers insight into older Americans’ indebtedness in an expansionary phase characterized by economic growth and low interest rates, and we show that, even during normal times and prior to the pandemic, a sizable proportion of older Americans was financially distressed.

We contribute to the literature in two ways. First, we exploit new information about individuals’ debt behaviors and financial perceptions,Footnote 4 and we confirm that, even in later life, older Americans have difficulty managing their debt. Over one-third (36%) of older adults in our sample reported feeling over-indebted, 15% had been contacted by debt collectors, and just under half (49%) were satisfied with their financial situations. Nevertheless, being more financially literate contributed to positive financial perceptions and behaviors, such as reporting better-than-average credit records and planning for retirement. Second, we highlight the need for researchers and policymakers to devote attention to two particular types of debt: student loans and medical debt, and also to particularly vulnerable groups such as African-Americans, women, the least-educated, and the low-income.

In what follows, we first describe our dataset and methodology. Next, we report both descriptive statistics and results from multivariate analyses of the NFCS to identify those most affected by debt and financial outcomes related to debt. A final section offers a discussion of our findings and concluding remarks.

1. Methodology and data

The National Financial Capability Study is an online survey that was commissioned for the first time in 2009 by the FINRA Investor Education Foundation. The survey is designed to understand and measure financial perceptions, attitudes, and behaviors among American adults, with the aim of offering a comprehensive analysis of household financial capability (FINRA Investor Education Foundation, 2019). The NFCS is a very large survey (with over 25,000 US respondents per wave); not only does it provide unique information on families’ finances, but it also allows researchers to study population subgroups. The data are representative of the national population in terms of age, gender, ethnicity, education, and census division.Footnote 5 The 2018 NFCS included a rich set of information on how households manage their liabilities, including sources of debt, perceived levels of indebtedness, and measures of financial distress.Footnote 6

To help assess whether high levels of debt at older ages are a cause for concern, we take as a frame of reference the intertemporal model of saving under uncertainty, which posits that people save to protect against shocks (to income, health, interest rates, and more) and for retirement. By focusing on respondents aged 51–61, we study individuals close to or at the peak of their wealth accumulation and before they can claim Social Security benefits.

Our goal is to evaluate the causes and consequences of debt later in life, and whether people are indeed forward-looking and plan for retirement. The 2018 NFCS incorporated several uniquely valuable questions about how people perceived their personal financial situations. Specifically, it asked respondents whether they were satisfied with their financial situations, whether they believed they had too much debt, how they rated their credit records, and whether they had outstanding student loans (on their own accounts or for partners/children). In addition, the NFCS asked whether they had past-due medical debt, as this type of debt is becoming increasingly common for Americans (Lusardi et al., Reference Lusardi, Mitchell, Oggero, Mitchell and Lusardi2020b). Respondents were also asked whether they had been contacted by debt collectors, which allows us to judge the severity of potential debt problems. Finally, regarding long-term financial planning, the survey asked respondents whether they had ever tried to figure out how much they needed to save for retirement. This is an important question, given that planning for retirement is a strong predictor of wealth (Lusardi and Mitchell, Reference Lusardi and Mitchell2011).

The NFCS also included Lusardi and Mitchell’s ‘Big Three’ financial knowledge questions, which were devised to evaluate people’s capacity to understand simple interest rate calculations, inflation, and risk diversification.Footnote 7 The survey also included additional questions related to bond prices, mortgages, and interest compounding in the context of debt, which we use to construct a broader measure of financial literacy as a robustness check (a set of these questions on financial literacy has become known as the Big Five). Finally, the NFCS also allows us to identify those who experienced a large and unexpected income drop in the previous year, permitting us to assess the effects of recent financial shocks on debt.

In what follows, we first provide an overview of the dataset, followed by a multivariate analysis of positive and negative financial behaviors and perceptions.

2. Empirical findings

Table 1 reports key characteristics of the NFCS older respondents. About half (53%) were women; additionally, most were married, White, and had at least a high school degree. Almost one-fifth (17%) said they had experienced a large and unexpected income drop in the previous year. While one might expect that people close to retirement would have acquired some basic financial knowledge, only 43% of older Americans in our sample correctly answered the Big Three financial literacy questions. We also see that older respondents were quite uninformed about how mortgages work, basic asset pricing, and interest compounding in the context of debt (‘FinLitScore_6’). On average, older respondents could correctly answer only 3.52 of the six financial literacy questions (and only 2.05 of the Big Three questions measured as ‘FinLitScore_3’). Evidently, financial illiteracy is a widespread phenomenon even among the older population, despite the fact that this group has already made many critical financial decisions over their lifetimes. In other words, experience was apparently not very useful in enhancing older people’s financial sophistication.

Descriptive statistics on respondents' characteristics

Note: All Big Three correct is a dummy variable that takes the value 1 if the respondent answered all the Big Three questions correctly; FinLitScore_3 is the number of correct answers to the Big Three questions; FinLitScore_6 is the number of correct answers to the six financial literacy questions.

Source: Authors’ calculations, 2018 NFCS respondents aged 51–61 years (N = 4,670).

Table 2 provides an overview of key financial perceptions and behaviors, differentiating between positive and negative ones to offer a rich view of debt and the consequences of carrying debt close to retirement. The top panel of Table 2 reports positive financial behaviors and perceptions. Here, just under half (49%) of the NFCS respondents in the age range (51–61 years) we considered were satisfied with their personal financial situations (answering 7–10 on a 10-point scale). We also see that 70% of our NFCS respondents believed they had above-average credit records, a proxy for good financial behavior and outcomes. When asked whether they had planned for retirement, only half (54%) of the respondents said they had tried to figure out how much they need to save for retirement.

Self-reported financial behaviors and perceptions

Source: Authors’ calculations, 2018 NFCS respondents aged 51–61 years (N = 4,670).

The lower panel of Table 2 displays negative perceptions and outcomes. Rather discouragingly, over one-third (36%) of older adults in our sample reported being over-indebted. Specifically, on a scale from 1 to 7, they answered 5, 6, or 7 to the question, ‘How strongly do you agree or disagree with the following statement? “I have too much debt right now.”” Moreover, 15% had been contacted by a debt-collection agency in the previous year, and one-fifth (20%) had unpaid past due medical bills. These are disquieting percentages, given that these older respondents should be close to the peak of their life cycle wealth accumulation. Moreover, 9% of these older respondents held student loans for themselves or their spouses/partners. We consider outstanding student loans to be a negative behavior because of the respondents’ ages, as they face only limited opportunities to take advantage of future educational payoffs. Overall, these statistics indicate that debt looms large for substantial groups of pre-retirees. The percentages in our sample underscore the fact that older Americans carry debt not only to retirement but also into retirement.

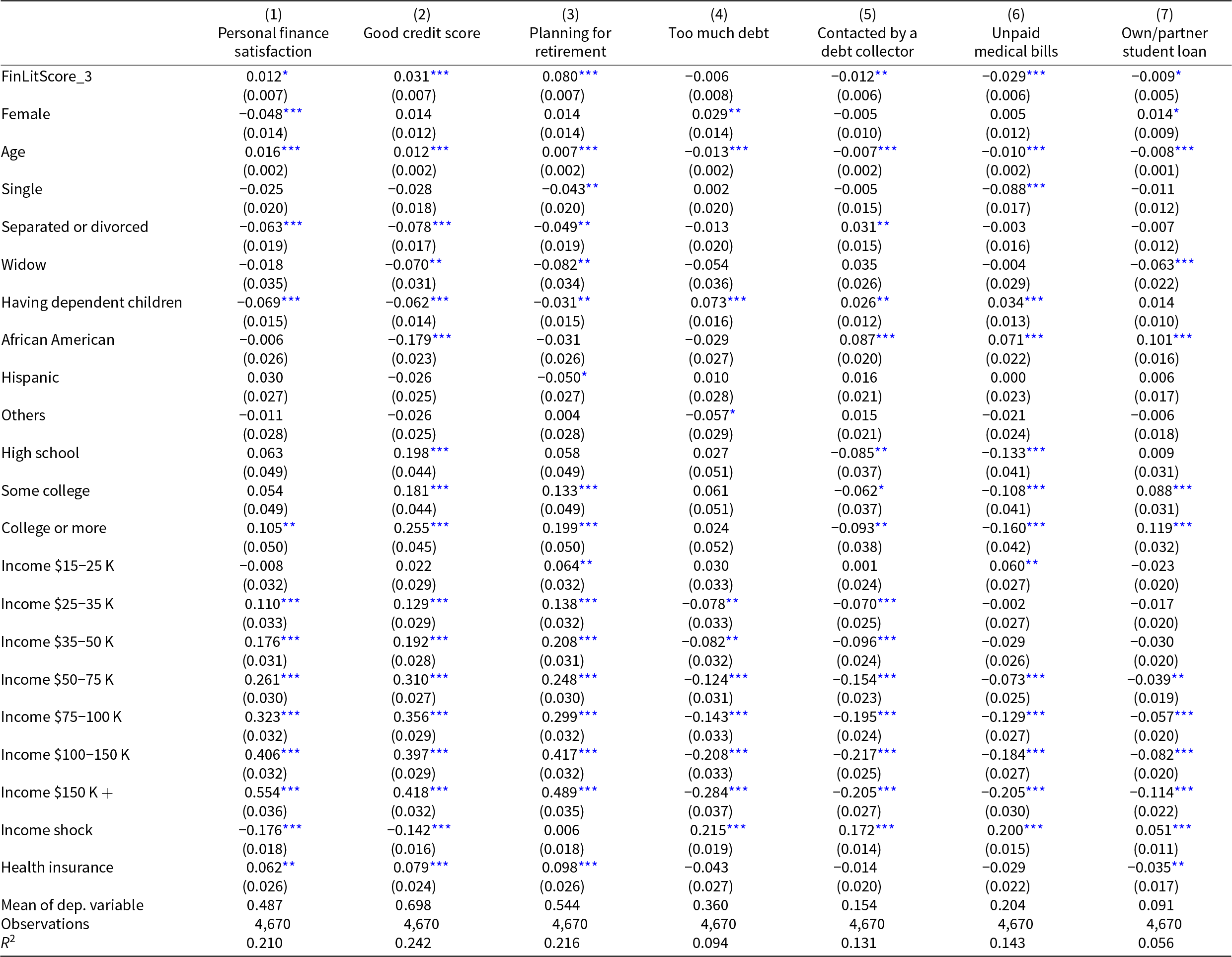

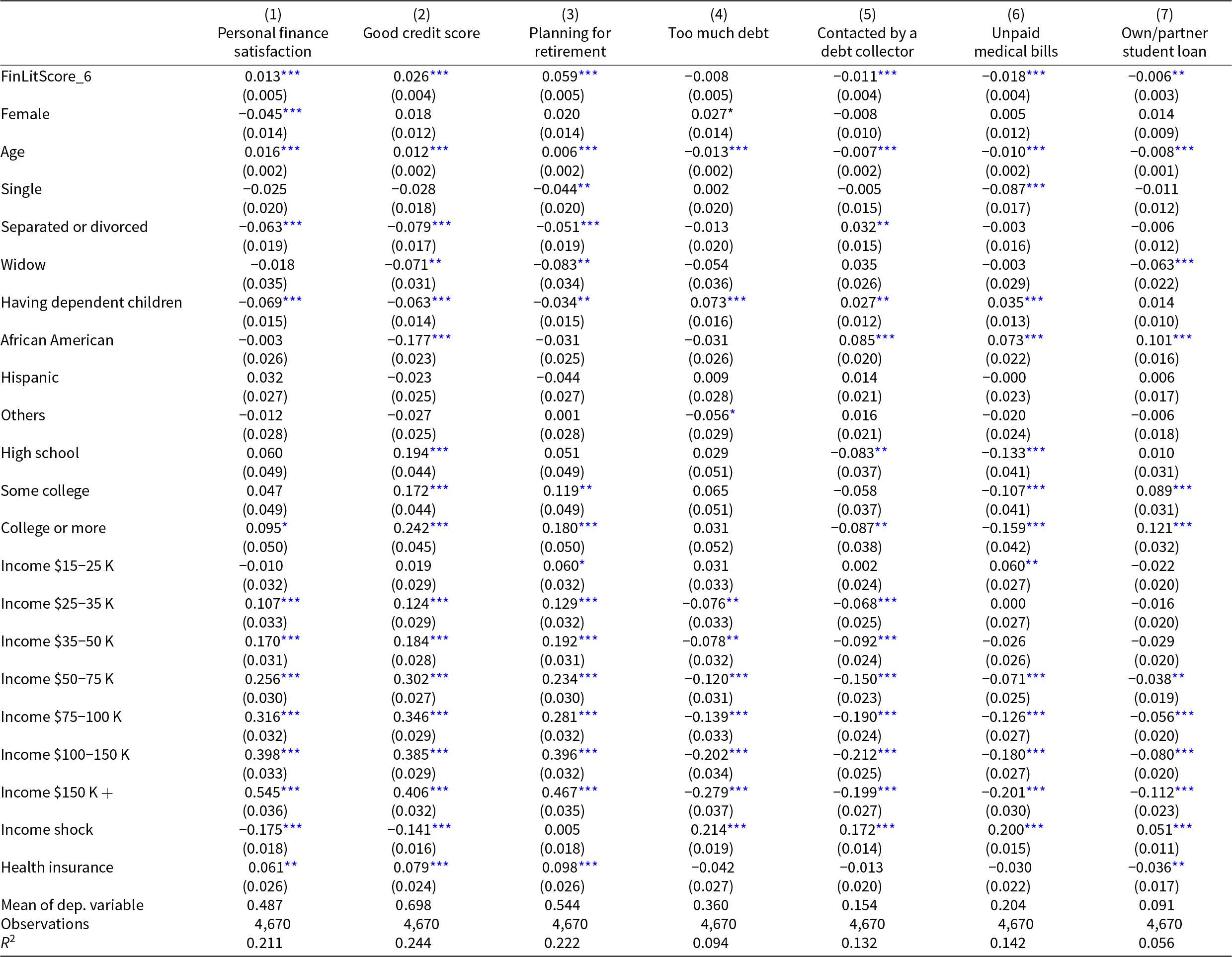

Tables 3 and 4 offer multivariate analyses of the positive and negative financial perceptions and behaviors. In each case, we estimate OLS models. Each column includes sociodemographic controls, an indicator of whether the respondent gave the correct answers to the Big Three financial literacy questions, and whether respondents had experienced a large and unexpected income drop in the previous year.

Multivariate analysis of positive financial perceptions and behaviors

Note: All Big Three correct is a dummy variable that takes the value 1 if the respondent answered all the Big Three questions correctly. Coefficient estimates are from OLS regressions, with standard errors in parentheses.

*** P < 0.01, ** P < 0.05, * P < 0.1.

Source: Authors’ calculations, 2018 NFCS respondents aged 51–61 years.

Multivariate analysis of negative financial perceptions and behaviors

Note: All Big Three Correct” is a dummy variable that takes the value 1 if the respondent answered all the Big Three questions correctly. Coefficient estimates are from OLS regressions, with standard errors in parentheses.

*** P < 0.01, ** P < 0.05, * P < 0.1.

Source: Authors’ calculations, 2018 NFCS respondents aged 51–61 years.

Table 3 provides a multivariate regression analysis of each of the three positive outcomes: whether people reported satisfaction with their personal finances, whether they believed that their credit scores were at least good or very good, and whether they had planned for retirement. The first row of Table 3 shows the importance of financial literacy: Those correctly answering the Big Three financial literacy questions were more likely to report positive outcomes, even after controlling for many demographic characteristics, including education. In our sample, basic financial literacy was associated with a 32% higher probability of planning for retirement (17 percentage points on a 0.54 base), a 9% higher chance of reporting good credit scores (6 percentage points on a 0.70 base), and a 6% higher probability of expressing positive views about the respondent’s financial situation (3 percentage points on a 0.49 base).

Turning to other important variables, we find that negative shocks also matter. The estimates reported in Table 3 also show that respondents who had experienced an income shock in the previous year were 17 percentage points (or 36% on a base of 0.49) less likely to be satisfied with their personal finances, and 14 percentage points (or 20% on a base of 0.70) less likely to report good credit scores compared to those who did not face unexpected income drops. These estimates already hint at the difficulty even older people would face in a pandemic bringing large health shocks and income declines.

Results in Table 3 also show a substantial degree of heterogeneity: older people in our sample were slightly more likely to be satisfied with their personal financial conditions, report good credit scores, and have planned for retirement. Additionally, married respondents were more likely to report positive financial perceptions and behaviors; singles were 4 percentage points (or 8% on a base of 0.54) less likely to have planned for retirement, and separated/divorced individuals were between 5 and 8 percentage points less likely to report positive financial perceptions and behaviors. Moreover, widowers were less satisfied with their credit scores and were less likely to have planned for retirement. Having dependent children contributed to poorer financial satisfaction, lower credit scores, and less retirement planning. We also show that African-Americans in our sample were significantly less sanguine about their financial situations, being 18 percentage points less likely to report good credit scores compared to Whites (26% on a base of 0.70). Interestingly, better-educated respondents were more likely to report good credit scores and plan for retirement, but their financial satisfaction was above-average only for the college-educated. As expected, those with higher incomes were more likely to report positive financial outcomes.

Table 4 reports multivariate regression estimates of factors associated with the four negative perceptions and behaviors related to respondents’ debt positions in the NFCS data. As for positive outcomes, those with a basic level of financial knowledge were less likely to report negative debt perceptions and behaviors. For instance, people who answered the Big Three financial literacy questions correctly reported a 23% lower probability of having unpaid medical bills (5 percentage points on a 0.20 base), a 23% lower chance of having outstanding student loans (2 percentage points on a 0.09 base), a 15% lower probability of being contacted by a debt collector (2 percentage points on a 0.15 base), and a 7% lower chance of saying they were over-indebtedFootnote 8 (3 percentage points on a 0.36 base). Thus, having basic financial literacy helps people limit their debt exposure at older ages.Footnote 9

We also see that older individuals in our sample were less likely to report having too much debt: they were less likely to have been contacted by a debt collector, to hold medical debt, and to have student loans for themselves or their partners. The fact that indebtedness and over-indebtedness decrease as people age echoes our prior study (Lusardi et al., Reference Lusardi, Mitchell and Oggero2020a), indicating that debt continues to be repaid at older ages. Nevertheless, debt remains pervasive among people on the verge of and moving into retirement, and there are signs of financial distress, as indicated, for instance, by the percentage of older people contacted by debt collectors.

Table 4 also documents that respondents with dependent children were more likely to feel over-indebted, by 7 percentage points (or 20% on a base of 0.36). Additionally, these individuals were more likely to have been contacted by a debt collector or to have unpaid medical bills, although not student loans. African-Americans in our sample were disproportionately more likely to report negative debt perceptions and behaviors, despite controlling for income and other demographic characteristics: they were 9 percentage points (or 58% on a base of 0.15) more likely to be contacted by a debt collector, 7 percentage points (or 37% on a base of 0.20) more likely to have unpaid medical bills, and 10 percentage points (or 112% on a base of 0.09) more likely to have student loans. Those with some college education were 9 percentage points (or 95% on a base of 0.09) more likely to hold student loans, possibly meaning that they did not complete the educational program for which they borrowed money and yet still had to repay their student debt. Higher-income respondents were less likely to report negative financial outcomes.

Interestingly, respondents reporting a negative income shock were up to 21 percentage points more likely to report any of the four negative outcomes, exacerbating their debt situations. In particular, they experienced a sharply higher chance of being contacted by a debt collector (a 115% increase on a base of 0.15) and were much more likely to have unpaid medical bills (a 100% increase on a base of 0.20) and outstanding student loans (a 57% increase on a base of 0.09). Without the governmental support provided during the pandemic, many of the older families carrying debt would have suffered from financial distress.

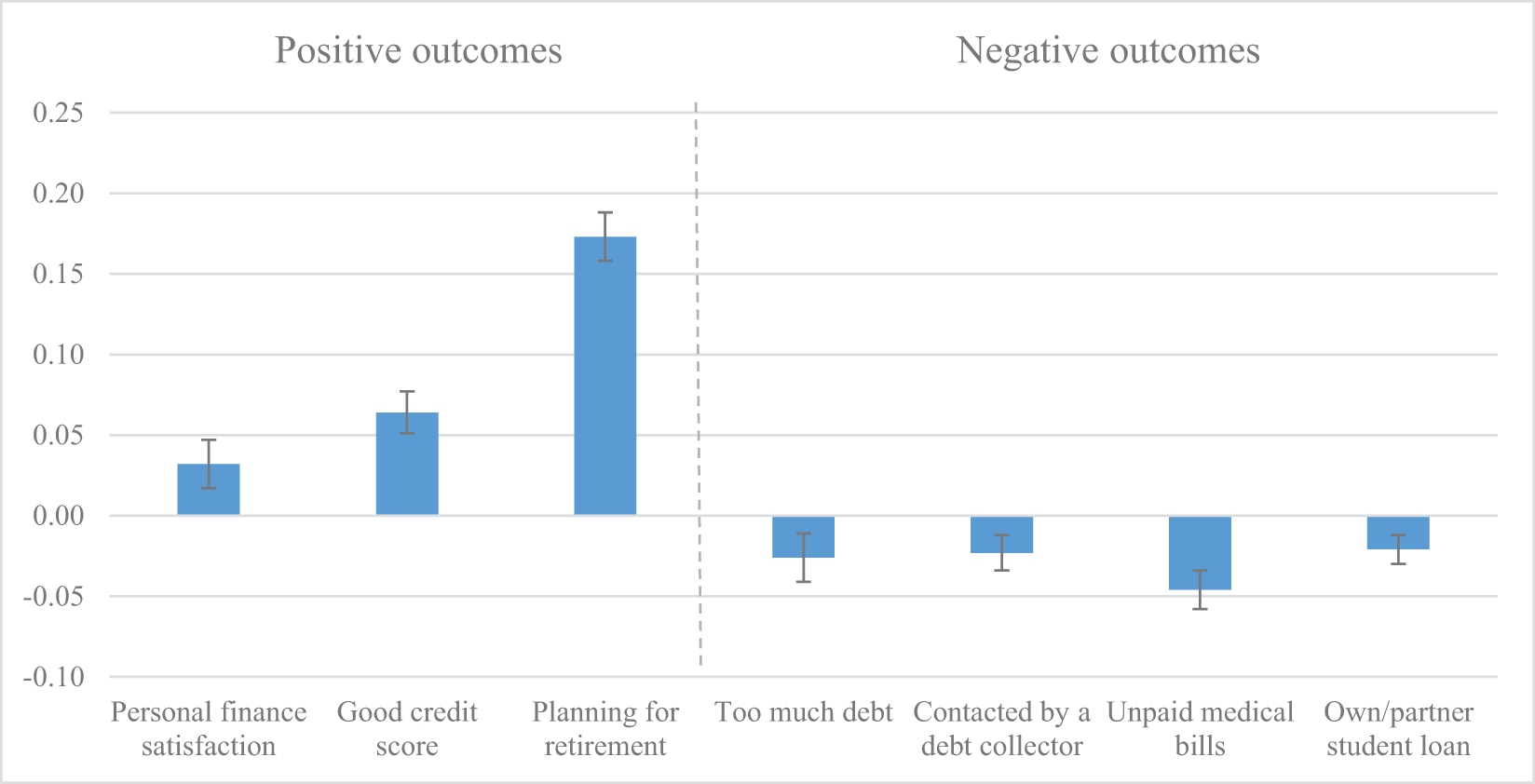

Given the importance of financial literacy, we summarize the evidence on the relationship between financial knowledge and positive and negative financial perceptions and behaviors at older ages in Figure 1, which plots the estimated financial literacy coefficients (and standard errors) from the multivariate analyses in Tables 3 and 4. The largest (statistically significant) association is between financial literacy and retirement planning, yet positive effects are also seen for personal finance satisfaction and having a good credit score. Conversely, the more financially literate were less likely to state that they had too much debt, to be contacted by a debt collector, to have unpaid medical bills, and to hold student loans.

Financial literacy coefficients from multivariate analysis of positive and negative outcomes.

Note: Authors’ calculations, 2018 NFCS respondents aged 51–61 years (N = 4,670). Coefficient estimates from the regressions reported in Tables 3 and 4. Bars represent estimated standard errors.

Source: Authors’ calculations.

The multivariate analyses reported in Tables 3 and 4 account for up to 24% of the variation in the dependent variables for positive perceptions and behaviors, and 14% for negative outcomes; moreover, our estimates are robust to the addition of extra variables.Footnote 10 To corroborate our findings on financial literacy, in Appendix B, we provide results using alternative measures of financial knowledge in place of the Big Three.Footnote 11 Interestingly, results are similar regardless of which of the two financial knowledge indexes we use. Additionally, our findings on outstanding student loans still hold when we consider loans for children’s education as well as for oneself or a partner (Table B3).

3. Conclusions and implications

Our empirical analysis of debt among older respondents (ages 51–61 years) shows that, even before the pandemic, a sizable proportion of older Americans was financially dissatisfied and felt that they held too much debt, despite being on the verge of retirement. Indeed, over one-third (36%) of older adults in our sample reported being over-indebted, one in five (20%) had unpaid past-due medical bills, and 15% were contacted by debt collectors. Our analysis also highlighted the importance of population heterogeneity, with low-income individuals and those with children in the home being particularly vulnerable. Moreover, African-Americans on the verge of retirement were significantly more financially vulnerable than Whites in our sample. Respondents who confronted an income shock the previous year were 20% less likely to report good credit scores and 36% less likely to be satisfied with their personal finances, while they faced about twice the chance of being contacted by a debt collector or having unpaid medical bills. Importantly, we find that financially literate respondents reported more positive financial perceptions and behaviors, like planning for retirement, reporting a good credit score, and being financially satisfied. Additionally, having basic financial knowledge was associated with a 23% lower probability of having unpaid medical bills, a 23% lower chance of having outstanding student loans, a 15% lower probability of being contacted by a debt collector, and a 7% lower chance of reporting over-indebtedness.

Accordingly, it is clear that older people who are more financially knowledgeable are also better at managing their debt exposure. These empirical findings are associations rather than causal relationships, as the acquisition of financial knowledge may be endogenously determined. Nevertheless, studies that account for the potential endogeneity of financial literacy, as well as measurement error using instrumental variable estimation, tend to conclude that those estimated effects are even larger than the uncorrected ones (Lusardi and Mitchell, Reference Lusardi and Mitchell2014).

To date, the personal finance literature has devoted relatively little attention to older Americans’ debt and debt management. Accordingly, our paper contributes to knowledge by identifying which older individuals may need assistance coping with money management problems. We also suggest that guidance and training programs are likely to be effective in enhancing older persons’ financial literacy, capability, and retirement planning/saving outcomes. In other words, in addition to focusing on retirement savings as a means to enhance retirement security, it is also crucial to understand and help older people manage debt. Financial education programs have positive, sizable effects on financial literacy and consequent behaviors, and many interventions are cost-effective (Kaiser et al., Reference Kaiser, Lusardi, Menkhoff and Urban2022). Additionally, the evidence from large-scale programs in schools shows that financial education can have long-term effects on outcomes later in life (Bruhn et al., Reference Bruhn, de Souza Leão, Legovini, Marchetti and Zia2016, Reference Bruhn, Garber, Koyama and Zia2022; Frisancho, Reference Frisancho2023). While programs in schools are the starting point for policy interventions, programs directed at adults can be effective too, as long as their content is related to the life phase of the participants (Lusardi and Kaiser, Reference Lusardi, Kaiser, Berger, Molyneux and Wilson2025).

More generally, to increase retirement security, additional research on older people’s balance sheets is needed. For instance, in view of the high rates of older people’s medical debt, more attention could be brought to bear on how to better protect against health shocks and high medical costs. Additionally, the extent and prevalence of student loans held by older people could benefit from additional policy attention. Finally, employer-provided retirement wellness programs could investigate not only how to foster savings but also how to help insulate people against high debt as they near retirement. Enhancing financial literacy can also build more resilience and reduce indebtedness at older ages.

Acknowledgements

This project received funding from the TIAA Institute and the Wharton School’s Pension Research Council/Boettner Center. We thank participants at the 2020 TIAA Fellows Symposium and the 2020 Academic Research Colloquium for Financial Planning and Related Disciplines, Alexandria, VA, for suggestions and comments. The content is solely the responsibility of the authors and does not necessarily represent the official views of the above-named institutions.

Appendix A: NFCS questions

PERSONAL FINANCE SATISFACTION

Overall, thinking about your assets, debts, and savings, how satisfied are you with your current personal financial condition? Please use a 10-point scale, where 1 means ‘Not at All Satisfied’ and 10 means ‘Extremely Satisfied.’

PLANNING FOR RETIREMENT

Have you ever tried to figure out how much you need to save for retirement?

[IF Q.A10a = 2 INSERT: Before you retired, did you try to figure out how much you needed to save for retirement?][IF Q.A10a = 3 INSERT: Before your [spouse/partner] retired, did you try to figure out how much you needed to save for retirement?]

INCOME SHOCK

In the past 12 months [IF Q.A7a = 3 INSERT: have you/IF Q.A7a = 1 OR 2 INSERT: has your household], experienced a large drop in income which you did not expect?

GOOD CREDIT SCORE

How would you rate your current credit record? Very bad, bad, about average, good, or very good?

UNPAID MEDICAL BILLS

Do you currently have any unpaid bills from a health care or medical service provider (e.g., a hospital, a doctor’s office, or a testing lab) that are past due?

OWN/PARTNER STUDENT LOAN

Do you currently have any student loans? If so, for whose education was this/were these loan(s) taken out? Select all that apply. Yes, have student loan(s) for: yourself, your spouse/partner, your child(ren), your grandchild(ren), other person, or No, do not currently have any student loans.

CONTACTED BY A DEBT COLLECTOR

Have you been contacted by a debt collection agency in the past 12 months?

TOO MUCH DEBT

How strongly do you agree or disagree with the following statement? I have too much debt right now. Please give your answer on a scale of 1 to 7, where 1 = ‘Strongly Disagree,’ 7 = ‘Strongly Agree,’ and 4 = ‘Neither Agree nor Disagree.’ You can use any number from 1 to 7.

INTEREST QUESTION

Suppose you had $100 in a savings account and the interest rate was 2% per year. After 5 years, how much do you think you would have in the account if you left the money to grow?

More than $102

Exactly $102

Less than $102

Don’t know

Prefer not to say

INFLATION QUESTION

Imagine that the interest rate on your savings account was 1% per year and inflation was 2% per year. After 1 year, how much would you be able to buy with the money in this account?

More than today

Exactly the same

Less than today

Don’t know

Prefer not to say

BOND QUESTION

If interest rates rise, what will typically happen to bond prices?

They will rise

They will fall

They will stay the same

There is no relationship between bond prices and the interest rate

Don’t know

Prefer not to say

MORTGAGE QUESTION

Please indicate whether each statement is true or false. A 15-year mortgage typically requires higher monthly payments than a 30-year mortgage, but the total interest paid over the life of the loan will be less.

True

False

Don’t know

Prefer not to say

RISK DIVERSIFICATION QUESTION

Please indicate whether each statement is true or false. Buying a single company’s stock usually provides a safer return than a stock mutual fund.

True

False

Don’t know

Prefer not to say

INTEREST COMPOUNDING KNOWLEDGE

Suppose you owe $1,000 on a loan and the interest rate you are charged is 20% per year compounded annually. If you didn’t pay anything off, at this interest rate, how many years would it take for the amount you owe to double?

Less than 2 years

At least 2 years but less than 5 years

At least 5 years but less than 10 years

At least 10 years

Don’t know

Prefer not to say

Appendix B

Multivariate analysis of positive and negative financial perceptions and behaviors using an alternative measure of financial literacy: FinLitScore_6

Note: FinLitScore_6 is constructed as the number of correct answers to the six financial literacy questions. Coefficient estimates are from OLS regressions, with standard errors in parentheses.

*** P < 0.01, ** P < 0.05, * P < 0.1.

Source: Authors’ calculations, 2018 NFCS respondents aged 51–61 years.

Multivariate analysis of positive and negative financial perceptions and behaviors using an alternative measure of financial literacy: FinLit_Score_3

Note: FinLitScore_3 is constructed as the number of correct answers to the Big Three questions. Coefficient estimates are from OLS regressions, with standard errors in parentheses.

*** P < 0.01, ** P < 0.05, * P < 0.1.

Source: Authors’ calculations, 2018 NFCS respondents aged 51–61 years.

Multivariate analysis of having student loans outstanding for themselves, partners, or children

Open access

Open access