1. Introduction

Risk-based solvency principles for insurance companies are at the heart of modern insurance regulation, see for instance the currently enforced Solvency II regulation in the European Union (European Union 2009; 2025) and the Swiss solvency test (SST) in Switzerland (Federal Office of Private Insurance 2006). According to these principles, the valuation of insurance liabilities must reflect not only expected future cash flows but also the uncertainty surrounding them. A central component in this process is the cost of capital, which represents the return that investors demand for providing capital to absorb unexpected losses, where the necessary amount of capital to ensure solvency is set by the regulator on the basis of the underwritten policies and a risk measure. While financial risks can typically be priced in a market-consistent way (cf. Koch-Medina and Munari Reference Koch-Medina and Munari2020), this is more subtle for insurance risk (see e.g., Salahnejhad Ghalehjooghi and Pelsser Reference Salahnejhad Ghalehjooghi and Pelsser2023; Engsner et al. Reference Engsner, Lindskog and Thøgersen2023 and Artzner et al. Reference Artzner, Eisele and Schmidt2024; Oberpriller et al. Reference Oberpriller, Ritter and Schmidt2024). In the absence of a liquid market for insurance risks, one typically needs to adhere to a mark-to-model approach. The economic value of the insurance liabilities is then defined as the expected claim costs (“best estimate”) plus a margin (called risk margin in Solvency II, and market value margin in the SST), which reflects these capital costs. The justification is that for this monetary amount another insurance undertaking should then be willing to take over these liabilities, as it covers the costs it generates for integrating it into one’s business (an arm’s length transaction, cf. European Union 2009). The suggested cost-of-capital rate (above the risk free rate) for such considerations, and the standard value currently implemented, is 6%. Recently, the European union decided to lower this value to 4.75%, cf. Jones (2023), European Union (2025), which after national transposition is expected to be enforced in the member countries by January 2027. See, for example, Floreani (Reference Floreani2011), Albrecher et al. (Reference Albrecher, Eisele, Steffensen and Wüthrich2022) for economic considerations to justify particular cost-of-capital rates.

It may be natural to interpret that the insurance premiums should match the economic value of liabilities that the issuance of these insurance policies generates (as this is the value for which also another party should be willing to accept these risks). This would mean that the safety loading (on top of the pure premium reflecting expected claim costs) corresponds to the risk margin discussed above. From an actuarial perspective, this is a natural starting point for the concrete pricing of the policies, although several other factors will eventually play a role (including competition, demand/supply patterns, solidarity considerations, etc.). More than that, at the general level of asset-liability management of the company, the company is exposed to several other sources of risks, and the regulatory rules ask to determine the solvency capital requirement that each of these generate, and the resulting values then need to be added up for the overall solvency capital satisfying the regulatory demand. That is, for simplicity, these risks are considered independently at first, and based on some (often very coarse) dependence assumptions between the different risk categories, the obtained sum can in a second step potentially be reduced by a diversification benefit, taking into account the fact that not all of these risks are likely to lead to losses at the same time.

In the approach as described above, the insurance liabilities are considered in a stand-alone fashion, with the capital costs they generate (and therefore the necessary insurance premiums) possibly overestimated, as they rely on the assumption that the solvency capital is invested solely in risk-less bonds. But in practice some of that capital can be invested into risky assets, generating higher returns than the risk-less bond and providing additional income that reduces the claim costs. At the same time, this position in risky assets introduces additional risk, which itself translates into the need for further solvency capital.

In this paper, we would like to specifically investigate this trade-off directly by considering those two risks together. Concretely, considering a mix of risky and risk-less investment of the solvency capital, we would like to study up to which degree of ‘riskiness’ of the investment the policyholders can benefit from smaller premiums for the same level of solvency of the insurance undertaking (under the assumption that the safety loading is determined by the generated capital costs). Our focus is on short-tailed risks in the nonlife domain. Despite extensive literature on the joint valuation of actuarial and financial risks within the insurance product itself (particularly with life insurance applications in mind, see, e.g., Dhaene et al. Reference Dhaene, Stassen, Barigou, Linders and Chen2017; Delong et al. Reference Delong, Dhaene and Barigou2019; Barigou and Dhaene Reference Barigou and Dhaene2019; Barigou et al. Reference Barigou, Bignozzi and Tsanakas2022), to the best of our knowledge an explicit analysis of the trade-off between risky and risk-less assets of a nonlife insurer for a policyholder’s perspective was not considered before. We therefore deliberately decide to keep the underlying model assumptions simple, in order not to blur the main analysis by overlays with other factors. This includes the restriction to a one-period model, independence between insurance and financial risk as well as a focus on the value-at-risk and expected shortfall as a risk measure, see Section 2 for details.

It turns out that one can specify conditions under which the needed insurance premiums decrease with increasing weight in risky investment, up to a certain limit weight, up to which also the overall capital requirement is reduced. That is, a mild weight in risky investment is of advantage to all involved parties. Beyond that limit, the needed insurance premiums may decrease even further, but at the expense of overall increased capital requirements for the additionally introduced investment risk. Such considerations may also add to reflections about the justifications of currently implemented solvency capital charges in the standard model of Solvency II for equity risk (e.g., 39% shock for Type 1 assets and 49% shock for Type 2 assets, cf. European Union 2015). We reiterate that the purpose of the paper is to establish some concrete quantitative insights into the matter under very concrete and simple model assumptions.

The rest of the paper is organized as follows. Section 2 lays out the concrete model assumptions on which we base the considerations of the paper and establishes a number of general monotonicity results for the needed insurance premium, the invested amount of the shareholders and the overall solvency capital requirement when increasing the proportion of risky assets in the management of insurance risks. For the more particular case of normally distributed insurance and financial risks, we derive explicit formulas for the involved quantities in Section 3. In Section 4, we then give and discuss concrete numerical illustrations of the effects of risky investments on the needed insurance premiums and solvency requirements, and Section 5 concludes. All proofs are delegated to an appendix.

2. A cost-of-capital valuation with risky assets

Assume that at time 0 liabilities corresponding to an aggregate claim amount

$X_1$

at time 1 are transferred from an insurance company to an empty company whose purpose is to carry out the runoff of the liabilities.

$X_1$

at time 1 are transferred from an insurance company to an empty company whose purpose is to carry out the runoff of the liabilities.

$X_1$

is not replicable and no replicating portfolio is considered. For simplicity, we assume that all payoffs at time 1 are discounted to monetary values at time 0 (alternatively, that the risk-less interest rate is zero). Along with the liabilities, the following cash amounts are transferred: a cash amount

$X_1$

is not replicable and no replicating portfolio is considered. For simplicity, we assume that all payoffs at time 1 are discounted to monetary values at time 0 (alternatively, that the risk-less interest rate is zero). Along with the liabilities, the following cash amounts are transferred: a cash amount

$C_0$

from the shareholders and a cash amount

$C_0$

from the shareholders and a cash amount

$V_0$

from the insurance company. Since only the liabilities and the cash amount

$V_0$

from the insurance company. Since only the liabilities and the cash amount

$V_0$

are transferred from the insurance company,

$V_0$

are transferred from the insurance company,

$V_0$

should be interpreted as a theoretical premium for these liabilities. The cash transfers are necessary because the new entity receiving the liabilities needs capital in order to comply with the solvency standards of insurance regulation.

$V_0$

should be interpreted as a theoretical premium for these liabilities. The cash transfers are necessary because the new entity receiving the liabilities needs capital in order to comply with the solvency standards of insurance regulation.

Assume now that the (deterministic) cash amount

$R_0=V_0+C_0$

is immediately invested into an asset (or a collection of assets) with gross return

$R_0=V_0+C_0$

is immediately invested into an asset (or a collection of assets) with gross return

$Z_1$

giving the risky amount

$Z_1$

giving the risky amount

$R_0Z_1$

at time 1. At time 1, the payoffs to the shareholders and to the policyholders, respectively, are

$R_0Z_1$

at time 1. At time 1, the payoffs to the shareholders and to the policyholders, respectively, are

\begin{align*}Z_{\text{sh}}\;:\!=(R_0Z_1-X_1)^+, \quad Z_{\text{ph}}\;:\!=(R_0Z_1)\wedge X_1,\end{align*}

\begin{align*}Z_{\text{sh}}\;:\!=(R_0Z_1-X_1)^+, \quad Z_{\text{ph}}\;:\!=(R_0Z_1)\wedge X_1,\end{align*}

where

$x\wedge y$

means

$x\wedge y$

means

$\min(x,y)$

and

$\min(x,y)$

and

$x^+=\max\!(x,0)$

. The interpretation is that the policyholders receive what they are entitled to if there is sufficient capital available at that time, and any remaining available capital goes to the shareholders. For a discussion on the effects of the limited liability of the shareholders, see, for example, Filipović et al. (Reference Filipović, Kremslehner and Muermann2015), Albrecher et al. (Reference Albrecher, Eisele, Steffensen and Wüthrich2022).

$x^+=\max\!(x,0)$

. The interpretation is that the policyholders receive what they are entitled to if there is sufficient capital available at that time, and any remaining available capital goes to the shareholders. For a discussion on the effects of the limited liability of the shareholders, see, for example, Filipović et al. (Reference Filipović, Kremslehner and Muermann2015), Albrecher et al. (Reference Albrecher, Eisele, Steffensen and Wüthrich2022).

The shareholders assign at time 0 a value

$C_0$

to their payoff

$C_0$

to their payoff

$Z_{\text{sh}}$

at time 1, and the aggregate theoretical premium is the remaining amount

$Z_{\text{sh}}$

at time 1, and the aggregate theoretical premium is the remaining amount

$V_0=R_0-C_0$

needed to finance

$V_0=R_0-C_0$

needed to finance

$R_0$

. Cost-of-capital valuation corresponds to

$R_0$

. Cost-of-capital valuation corresponds to

\begin{align}C_0=\mathbb{E}[Z_{\text{sh}}]/(1+\eta),\end{align}

\begin{align}C_0=\mathbb{E}[Z_{\text{sh}}]/(1+\eta),\end{align}

where

$\eta\gt0$

represents the cost-of-capital rate, which is the spread over the risk-free rate for the more risky investment (which corresponds to betting on a favorable runoff result). Writing

$\eta\gt0$

represents the cost-of-capital rate, which is the spread over the risk-free rate for the more risky investment (which corresponds to betting on a favorable runoff result). Writing

$(R_0Z_1-X_1)^+=R_0Z_1-(R_0Z_1)\wedge X_1$

, we get in the cost-of-capital case that

$(R_0Z_1-X_1)^+=R_0Z_1-(R_0Z_1)\wedge X_1$

, we get in the cost-of-capital case that

\begin{align}V_0=\frac{1}{1+\eta}\,\mathbb{E}[(R_0Z_1)\wedge X_1]+\frac{\eta}{1+\eta}\,R_0+\frac{1}{1+\eta}R_0\,\mathbb{E}[1-Z_1].\end{align}

\begin{align}V_0=\frac{1}{1+\eta}\,\mathbb{E}[(R_0Z_1)\wedge X_1]+\frac{\eta}{1+\eta}\,R_0+\frac{1}{1+\eta}R_0\,\mathbb{E}[1-Z_1].\end{align}

If the investment is into a risk-less bond, then

$Z_1\equiv 1$

which gives as a special case of the valuation formula (2.2)

$Z_1\equiv 1$

which gives as a special case of the valuation formula (2.2)

\begin{align*}V_0=\frac{1}{1+\eta}\,\mathbb{E}[R_0\wedge X_1]+\frac{\eta}{1+\eta}\,R_0,\end{align*}

\begin{align*}V_0=\frac{1}{1+\eta}\,\mathbb{E}[R_0\wedge X_1]+\frac{\eta}{1+\eta}\,R_0,\end{align*}

which appears as Equation (8.16) in Mildenhall and Major (Reference Mildenhall and Major2022), p. 199. It also corresponds to the one-period case of Engler and Lindskog (Reference Engler and Lindskog2025), Equation 10 and to Albrecher and Dacorogna (Reference Albrecher and Dacorogna2026), Equation 12 in the absence of limited liability of the shareholders.

The cash amount

$R_0$

is the smallest amount such that the new entity managing the liability runoff is allowed to operate (is considered solvent).

$R_0$

is the smallest amount such that the new entity managing the liability runoff is allowed to operate (is considered solvent).

$R_0$

cannot be determined unless the associated investment strategy is given. Concretely,

$R_0$

cannot be determined unless the associated investment strategy is given. Concretely,

$R_0$

must satisfy

$R_0$

must satisfy

\begin{align}\rho(R_0Z_1-X_1)=0\end{align}

\begin{align}\rho(R_0Z_1-X_1)=0\end{align}

so that the final net worth

$R_0Z_1-X_1$

is acceptable according to a solvency criterion given by a risk measure

$R_0Z_1-X_1$

is acceptable according to a solvency criterion given by a risk measure

$\rho$

. That is, each choice of the risk measure

$\rho$

. That is, each choice of the risk measure

$\rho$

entails an overall needed cash amount

$\rho$

entails an overall needed cash amount

$R_0$

for each given insurance risk

$R_0$

for each given insurance risk

$X_1$

and chosen asset strategy

$X_1$

and chosen asset strategy

$Z_1$

. In terms of risk measure, in this paper, we focus on the value-at-risk and the expected shortfall. For

$Z_1$

. In terms of risk measure, in this paper, we focus on the value-at-risk and the expected shortfall. For

$\alpha\in (0,1)$

small, for example,

$\alpha\in (0,1)$

small, for example,

$0.5\%$

or 1%, these are defined as, with

$0.5\%$

or 1%, these are defined as, with

$Y=R_0Z_1-X_1$

,

$Y=R_0Z_1-X_1$

,

\begin{align*}\operatorname{VaR}_{\alpha}\!(Y)=F_{-Y}^{-1}(1-\alpha) \quad\text{and}\quad \operatorname{ES}_{\alpha}\!(Y)=\frac{1}{\alpha}\int_0^{\alpha}\operatorname{VaR}_{\beta}\!(Y)d\beta.\end{align*}

\begin{align*}\operatorname{VaR}_{\alpha}\!(Y)=F_{-Y}^{-1}(1-\alpha) \quad\text{and}\quad \operatorname{ES}_{\alpha}\!(Y)=\frac{1}{\alpha}\int_0^{\alpha}\operatorname{VaR}_{\beta}\!(Y)d\beta.\end{align*}

Since

$Z_1$

and

$Z_1$

and

$X_1$

are discounted, no discount factor appears in front of the quantile

$X_1$

are discounted, no discount factor appears in front of the quantile

$F_{-Y}^{-1}(1-\alpha)$

.

$F_{-Y}^{-1}(1-\alpha)$

.

Remark 2.1. We could consider the more general

$\min\{r\;:\;\rho(rZ_1-X_1)\leq 0\}$

as definition of

$\min\{r\;:\;\rho(rZ_1-X_1)\leq 0\}$

as definition of

$R_0$

instead of (2.3) since there are stochastic models for which no

$R_0$

instead of (2.3) since there are stochastic models for which no

$R_0$

satisfies (2.3). However, under reasonable assumptions (see Proposition 2.1 below),

$R_0$

satisfies (2.3). However, under reasonable assumptions (see Proposition 2.1 below),

$R_0$

is the unique solution to

$R_0$

is the unique solution to

$\rho(R_0Z_1-X_1)=0$

.

$\rho(R_0Z_1-X_1)=0$

.

Remark 2.2. A model-independent upper bound for

$V_0$

is obtained from using

$V_0$

is obtained from using

$\mathbb{E}[Y^+]\geq \mathbb{E}[Y]$

, which, applied to (2.2), gives

$\mathbb{E}[Y^+]\geq \mathbb{E}[Y]$

, which, applied to (2.2), gives

\begin{align*}V_0\leq R_0-\frac{1}{1+\eta}\mathbb{E}[R_0Z_1-X_1]=\frac{1+\eta-\mathbb{E}[Z_1]}{1+\eta}R_0+\frac{1}{1+\eta}\mathbb{E}[X_1].\end{align*}

\begin{align*}V_0\leq R_0-\frac{1}{1+\eta}\mathbb{E}[R_0Z_1-X_1]=\frac{1+\eta-\mathbb{E}[Z_1]}{1+\eta}R_0+\frac{1}{1+\eta}\mathbb{E}[X_1].\end{align*}

If

$Z_1$

and

$Z_1$

and

$X_1$

have finite variances and if the risk measure

$X_1$

have finite variances and if the risk measure

$\operatorname{VaR}_{\alpha}$

is used to determine

$\operatorname{VaR}_{\alpha}$

is used to determine

$R_0$

, then a lower bound for

$R_0$

, then a lower bound for

$V_0$

follows from combining the Cauchy–Schwarz inequality

$V_0$

follows from combining the Cauchy–Schwarz inequality

$\mathbb{E}[|AB|]\leq \mathbb{E}[A^2]^{1/2}\mathbb{E}[B^2]^{1/2}$

with the identity

$\mathbb{E}[|AB|]\leq \mathbb{E}[A^2]^{1/2}\mathbb{E}[B^2]^{1/2}$

with the identity

$Y^+=Y\unicode{x1D7D9}_{[0,\infty)}(Y)$

. Concretely,

$Y^+=Y\unicode{x1D7D9}_{[0,\infty)}(Y)$

. Concretely,

\begin{align*}\mathbb{E}[(R_0Z_1-X_1)^+]\leq \mathbb{E}[(R_0Z_1-X_1)^2]^{1/2}(1-\alpha)^{1/2}\end{align*}

\begin{align*}\mathbb{E}[(R_0Z_1-X_1)^+]\leq \mathbb{E}[(R_0Z_1-X_1)^2]^{1/2}(1-\alpha)^{1/2}\end{align*}

and

$\mathbb{E}[Y^2]=\operatorname{var}(Y)+\mathbb{E}[Y]^2$

then lead to the lower bound

$\mathbb{E}[Y^2]=\operatorname{var}(Y)+\mathbb{E}[Y]^2$

then lead to the lower bound

\begin{align*}V_0\geq R_0-\frac{(1-\alpha)^{1/2}}{1+\eta}\Big(R_0^2\operatorname{var}(Z_1)+\operatorname{var}(X_1)+\big(R_0\mathbb{E}[Z_1]-\mathbb{E}[X_1]\big)^2\Big)^{1/2}.\end{align*}

\begin{align*}V_0\geq R_0-\frac{(1-\alpha)^{1/2}}{1+\eta}\Big(R_0^2\operatorname{var}(Z_1)+\operatorname{var}(X_1)+\big(R_0\mathbb{E}[Z_1]-\mathbb{E}[X_1]\big)^2\Big)^{1/2}.\end{align*}

Remark 2.3. Limited liability means that shareholders do not have to inject capital at time 1 to offset a possible deficit at that time. Limited liability increases the value

$C_0$

for shareholders from

$C_0$

for shareholders from

$\mathbb{E}[R_0Z_1-X_1]/(1+\eta)$

to

$\mathbb{E}[R_0Z_1-X_1]/(1+\eta)$

to

$\mathbb{E}[(R_0Z_1-X_1)^+]/(1+\eta)$

. The difference

$\mathbb{E}[(R_0Z_1-X_1)^+]/(1+\eta)$

. The difference

\begin{align*}\frac{1}{1+\eta}\big(\mathbb{E}[(R_0Z_1-X_1)^+]-\mathbb{E}[R_0Z_1-X_1]\big)=-\frac{1}{1+\eta}\mathbb{E}[(R_0Z_1-X_1)^-]\end{align*}

\begin{align*}\frac{1}{1+\eta}\big(\mathbb{E}[(R_0Z_1-X_1)^+]-\mathbb{E}[R_0Z_1-X_1]\big)=-\frac{1}{1+\eta}\mathbb{E}[(R_0Z_1-X_1)^-]\end{align*}

is referred to as the value of the limited liability option. Note that this value coincides with the difference between the upper bound for

$V_0$

in Remark 2.2 and the value of

$V_0$

in Remark 2.2 and the value of

$V_0$

in case of limited liability.

$V_0$

in case of limited liability.

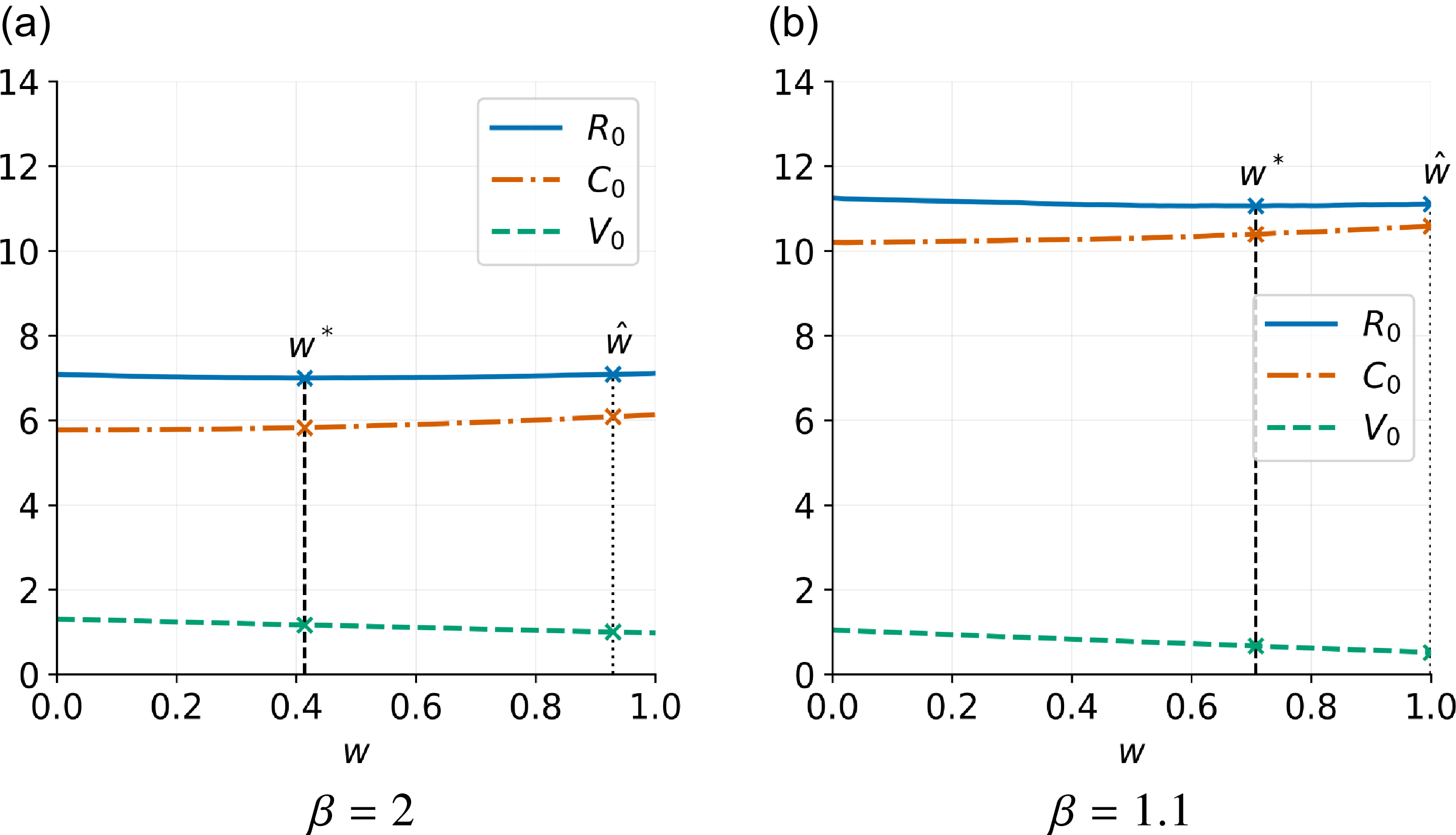

Example 2.1. As an illustration, consider a Pareto-distributed insurance risk

$X_1$

with cumulative distribution function

$X_1$

with cumulative distribution function

\begin{equation}F(x)=1-(x/x_m)^{-\beta}, \quad x\gt x_m\gt0\end{equation}

\begin{equation}F(x)=1-(x/x_m)^{-\beta}, \quad x\gt x_m\gt0\end{equation}

and suppose that

$\beta\gt1$

, ensuring a finite mean

$\beta\gt1$

, ensuring a finite mean

$\mathbb{E}[X_1]=x_m\beta/(\beta-1)$

. Consider a purely risk-less investment and

$\mathbb{E}[X_1]=x_m\beta/(\beta-1)$

. Consider a purely risk-less investment and

$R_0$

determined by

$R_0$

determined by

$\operatorname{VaR}_{\alpha}$

,

$\operatorname{VaR}_{\alpha}$

,

\begin{align*}R_0=\operatorname{VaR}_{\alpha}\!({-}X_1)=x_m\alpha^{-1/\beta}=\frac{\beta-1}{\beta}\alpha^{-1/\beta}\mathbb{E}[X_1].\end{align*}

\begin{align*}R_0=\operatorname{VaR}_{\alpha}\!({-}X_1)=x_m\alpha^{-1/\beta}=\frac{\beta-1}{\beta}\alpha^{-1/\beta}\mathbb{E}[X_1].\end{align*}

In this Pareto model with only risk-less investment, we can compute the value of the limited liability option (cf. Remark 2.3) explicitly. It is given by the expression

\begin{align*}\frac{1}{1+\eta}\frac{\alpha^{-1/\beta+1}}{\beta}\mathbb{E}[X_1].\end{align*}

\begin{align*}\frac{1}{1+\eta}\frac{\alpha^{-1/\beta+1}}{\beta}\mathbb{E}[X_1].\end{align*}

For nonnegative

$R_0,Z_1,X_1$

, the (typically crude) upper bound

$R_0,Z_1,X_1$

, the (typically crude) upper bound

$(R_0Z_1-X_1)^+\leq R_0Z_1$

gives the general upper bound

$(R_0Z_1-X_1)^+\leq R_0Z_1$

gives the general upper bound

$\mathbb{E}[X_1]/(1+\eta)$

for the value of the limited liability option. Here, with

$\mathbb{E}[X_1]/(1+\eta)$

for the value of the limited liability option. Here, with

$Z\equiv 1$

and

$Z\equiv 1$

and

$X_1$

Pareto distributed, we see that we can actually come arbitrarily close to this upper bound by letting

$X_1$

Pareto distributed, we see that we can actually come arbitrarily close to this upper bound by letting

$\beta$

approach 1.

$\beta$

approach 1.

Consider

$\alpha=0.005$

. For

$\alpha=0.005$

. For

$\beta=2$

and

$\beta=2$

and

$\beta=1.1$

, the two values of the limited liability option are approximately

$\beta=1.1$

, the two values of the limited liability option are approximately

$0.03\cdot \mathbb{E}[X_1]$

and

$0.03\cdot \mathbb{E}[X_1]$

and

$0.53\cdot \mathbb{E}[X_1]$

, respectively. The two corresponding values of

$0.53\cdot \mathbb{E}[X_1]$

, respectively. The two corresponding values of

$R_0$

are approximately

$R_0$

are approximately

$7.07 \cdot \mathbb{E}[X_1]$

and

$7.07 \cdot \mathbb{E}[X_1]$

and

$11.23 \cdot \mathbb{E}[X_1]$

, respectively. The upper bound for

$11.23 \cdot \mathbb{E}[X_1]$

, respectively. The upper bound for

$V_0$

in Remark 2.2 (corresponding to unlimited liability) is here

$V_0$

in Remark 2.2 (corresponding to unlimited liability) is here

\begin{align*}\frac{\eta}{1+\eta}\frac{\beta-1}{\beta}\alpha^{-1/\beta}\mathbb{E}[X_1]+\frac{1}{1+\eta}\mathbb{E}[X_1]=\frac{\mathbb{E}[X_1]}{1+\eta}\bigg(1+\frac{\alpha^{-1/\beta}}{\beta}\eta(\beta-1)\bigg).\end{align*}

\begin{align*}\frac{\eta}{1+\eta}\frac{\beta-1}{\beta}\alpha^{-1/\beta}\mathbb{E}[X_1]+\frac{1}{1+\eta}\mathbb{E}[X_1]=\frac{\mathbb{E}[X_1]}{1+\eta}\bigg(1+\frac{\alpha^{-1/\beta}}{\beta}\eta(\beta-1)\bigg).\end{align*}

For

$\beta=2$

and

$\beta=2$

and

$\beta=1.1$

, the two values of the upper bound for

$\beta=1.1$

, the two values of the upper bound for

$V_0$

are therefore approximately

$V_0$

are therefore approximately

$1.34\cdot \mathbb{E}[X_1]$

and

$1.34\cdot \mathbb{E}[X_1]$

and

$1.58\cdot \mathbb{E}[X_1]$

, respectively. We obtain the actual value of

$1.58\cdot \mathbb{E}[X_1]$

, respectively. We obtain the actual value of

$V_0$

by subtracting the value of the limited liability option:

$V_0$

by subtracting the value of the limited liability option:

\begin{align*}V_0=\frac{\mathbb{E}[X_1]}{1+\eta}\bigg(1+\frac{\alpha^{-1/\beta}}{\beta}(\eta(\beta-1)-\alpha)\bigg).\end{align*}

\begin{align*}V_0=\frac{\mathbb{E}[X_1]}{1+\eta}\bigg(1+\frac{\alpha^{-1/\beta}}{\beta}(\eta(\beta-1)-\alpha)\bigg).\end{align*}

For

$\beta=2$

and

$\beta=2$

and

$\beta=1.1$

the two values of

$\beta=1.1$

the two values of

$V_0$

are therefore approximately

$V_0$

are therefore approximately

$1.31\cdot \mathbb{E}[X_1]$

and

$1.31\cdot \mathbb{E}[X_1]$

and

$1.05\cdot \mathbb{E}[X_1]$

, respectively. The fact that, for a fixed

$1.05\cdot \mathbb{E}[X_1]$

, respectively. The fact that, for a fixed

$\mathbb{E}[X_1]$

, the heavier tail implies a considerably smaller value of

$\mathbb{E}[X_1]$

, the heavier tail implies a considerably smaller value of

$V_0$

is due to the relatively large value of the limited liability option.

$V_0$

is due to the relatively large value of the limited liability option.

Investing in a risk-less bond means

$Z_1\equiv 1$

and then (for translation-invariant

$Z_1\equiv 1$

and then (for translation-invariant

$\rho$

), we have

$\rho$

), we have

$R_0=\rho({-}X_1)$

. Our interest lies in the consequences of investing the capital

$R_0=\rho({-}X_1)$

. Our interest lies in the consequences of investing the capital

$R_0$

in (at least partially) risky assets. Therefore, the case

$R_0$

in (at least partially) risky assets. Therefore, the case

$Z_1\equiv 1$

is only a benchmark here, and we will in general consider random variables

$Z_1\equiv 1$

is only a benchmark here, and we will in general consider random variables

$Z_1$

of the form

$Z_1$

of the form

\begin{align}Z_1=Z^{w}_1\;:\!=wS_1+1-w\quad \text{for}\;w\in [0,1].\end{align}

\begin{align}Z_1=Z^{w}_1\;:\!=wS_1+1-w\quad \text{for}\;w\in [0,1].\end{align}

This corresponds to investing a fraction w in a risky asset (with value

$S_0=1$

at time 0 and discounted value

$S_0=1$

at time 0 and discounted value

$S_1$

at time 1) and the remainder in a risk-less bond. When considering

$S_1$

at time 1) and the remainder in a risk-less bond. When considering

$Z_1$

of the form (2.5), we will sometimes write

$Z_1$

of the form (2.5), we will sometimes write

$R_0^{w}, C_0^{w}, V_0^{w}$

to emphasize the dependence on w for fixed

$R_0^{w}, C_0^{w}, V_0^{w}$

to emphasize the dependence on w for fixed

$S_1$

and

$S_1$

and

$X_1$

. In the sequel, we will always assume the following:

$X_1$

. In the sequel, we will always assume the following:

Assumption 1. The risk measure

$\rho$

is either

$\rho$

is either

$\operatorname{VaR}_{\alpha}$

or

$\operatorname{VaR}_{\alpha}$

or

$\operatorname{ES}_{\alpha}$

.

$\operatorname{ES}_{\alpha}$

.

$X_1$

and

$X_1$

and

$S_1$

are independent, and

$S_1$

are independent, and

$S_1$

is absolutely continuous (having a density). There exists a unique solution

$S_1$

is absolutely continuous (having a density). There exists a unique solution

$R_0\geq 0$

to

$R_0\geq 0$

to

$\rho(R_0Z_1-X_1)=0$

.

$\rho(R_0Z_1-X_1)=0$

.

The independence assumption between

$X_1$

and

$X_1$

and

$S_1$

is for simplicity of exposition (see also Remark 3.5 and Section 5). The assumption on the existence of a unique solution

$S_1$

is for simplicity of exposition (see also Remark 3.5 and Section 5). The assumption on the existence of a unique solution

$R_0$

is in fact not very restrictive. For instance, one can derive the following result (the proof of which is given in Appendix A).

$R_0$

is in fact not very restrictive. For instance, one can derive the following result (the proof of which is given in Appendix A).

Proposition 2.1. If

$\rho$

is either

$\rho$

is either

$\operatorname{VaR}_{\alpha}$

or

$\operatorname{VaR}_{\alpha}$

or

$\operatorname{ES}_{\alpha}$

,

$\operatorname{ES}_{\alpha}$

,

$X_1$

and

$X_1$

and

$S_1$

are independent and take nonnegative values only,

$S_1$

are independent and take nonnegative values only,

$S_1$

is absolutely continuous and

$S_1$

is absolutely continuous and

${\mathbb{P}(X_1=0) \lt 1-\alpha}$

, then there exists a unique

${\mathbb{P}(X_1=0) \lt 1-\alpha}$

, then there exists a unique

$R_0\gt0$

solving (2.3).

$R_0\gt0$

solving (2.3).

Remark 2.4. Since we are considering positively homogeneous risk measures,

$0=\rho(R_0Z_1-X_1)=\rho(aR_0Z_1-aX_1)$

for any

$0=\rho(R_0Z_1-X_1)=\rho(aR_0Z_1-aX_1)$

for any

$a\gt0$

. Hence, for a fixed

$a\gt0$

. Hence, for a fixed

$Z_1$

, replacing

$Z_1$

, replacing

$X_1$

by

$X_1$

by

$aX_1$

changes the necessary invested amount from

$aX_1$

changes the necessary invested amount from

$R_0$

to

$R_0$

to

$aR_0$

. Correspondingly,

$aR_0$

. Correspondingly,

$C_0=\mathbb{E}[(R_0Z_1-X_1)^+]/(1+\eta)$

changes to

$C_0=\mathbb{E}[(R_0Z_1-X_1)^+]/(1+\eta)$

changes to

\begin{align*}\mathbb{E}[(aR_0Z_1-aX_1)^+]/(1+\eta)=a\mathbb{E}[(R_0Z_1-X_1)^+]/(1+\eta)=aC_0.\end{align*}

\begin{align*}\mathbb{E}[(aR_0Z_1-aX_1)^+]/(1+\eta)=a\mathbb{E}[(R_0Z_1-X_1)^+]/(1+\eta)=aC_0.\end{align*}

As a result,

$V_0$

also changes to

$V_0$

also changes to

$aV_0$

. Hence, it is sufficient to restrict the analysis to insurance liability variables

$aV_0$

. Hence, it is sufficient to restrict the analysis to insurance liability variables

$X_1$

satisfying

$X_1$

satisfying

$\mathbb{E}[X_1]=1$

.

$\mathbb{E}[X_1]=1$

.

2.1. Monotonicity properties

Throughout this paper, for any two random variables

$Y_1,Y_2$

the notation

$Y_1,Y_2$

the notation

$Y_1\leq_{\text{st}} Y_2$

refers to first-order stochastic dominance, that is, for the respective cumulative distribution functions, we have

$Y_1\leq_{\text{st}} Y_2$

refers to first-order stochastic dominance, that is, for the respective cumulative distribution functions, we have

$F_{Y_1}(x)\ge F_{Y_2}(x)$

for all

$F_{Y_1}(x)\ge F_{Y_2}(x)$

for all

$x\in{\mathbb R}$

.

$x\in{\mathbb R}$

.

We need to establish some overall soundness of the functionals

$R_0$

and

$R_0$

and

$V_0$

.

$V_0$

.

Proposition 2.2. Assume that Assumption 1 holds and that

$Z_1$

takes only nonnegative values.

$Z_1$

takes only nonnegative values.

-

(i) For

$Z_1$

fixed,

$X_1\mapsto R_0$

is increasing with respect to increasing first-order stochastic dominance.

$Z_1$

fixed,

$X_1\mapsto R_0$

is increasing with respect to increasing first-order stochastic dominance. -

(ii) For

$X_1$

fixed,

$Z_1\mapsto R_0$

is decreasing with respect to increasing first-order stochastic dominance. -

(iii) For

$Z_1$

fixed and and

$\mathbb{E}[Z_1]\leq 1+\eta$

,

$X_1\mapsto V_0$

is increasing with respect to increasing first-order stochastic dominance. -

(iv) For

$X_1$

fixed and

$\mathbb{E}[Z_1]\leq 1+\eta$

,

$Z_1\mapsto V_0$

is decreasing with respect to increasing first-order stochastic dominance.

Let

$S_1\leq_{\text{icx}}\widetilde{S}_1$

mean that

$S_1\leq_{\text{icx}}\widetilde{S}_1$

mean that

$\widetilde{S}_1$

is larger than

$\widetilde{S}_1$

is larger than

$S_1$

in increasing convex order (which is equivalent to stop-loss order, and also equivalent to

$S_1$

in increasing convex order (which is equivalent to stop-loss order, and also equivalent to

$\int_{\beta}^{1}F_{S_1}^{-1}(u)du\leq \int_{\beta}^{1}F_{\widetilde{S}_1}^{-1}(u)du$

for all

$\int_{\beta}^{1}F_{S_1}^{-1}(u)du\leq \int_{\beta}^{1}F_{\widetilde{S}_1}^{-1}(u)du$

for all

$\beta\in [0,1]$

, see, e.g., Denuit et al. Reference Denuit, Dhaene, Goovaerts and Kaas2005). Take

$\beta\in [0,1]$

, see, e.g., Denuit et al. Reference Denuit, Dhaene, Goovaerts and Kaas2005). Take

$S_1\geq_{\text{icx}} 1$

. Then, for

$S_1\geq_{\text{icx}} 1$

. Then, for

$\widetilde{w}\geq w$

$\widetilde{w}\geq w$

\begin{align*}&\int_{\beta}^{1}F_{\widetilde{w}S_1+1-\widetilde{w}}^{-1}(u)du-\int_{\beta}^{1}F_{wS_1+1-w}^{-1}(u)du\\&\quad = (\widetilde{w}-w)\int_{\beta}^{1}F_{S_1}^{-1}(u)du+(1-\beta)(w-\widetilde{w})\\&\quad = (\widetilde{w}-w)\bigg(\int_{\beta}^{1}F_{S_1}^{-1}(u)du-(1-\beta)\bigg)\geq 0.\end{align*}

\begin{align*}&\int_{\beta}^{1}F_{\widetilde{w}S_1+1-\widetilde{w}}^{-1}(u)du-\int_{\beta}^{1}F_{wS_1+1-w}^{-1}(u)du\\&\quad = (\widetilde{w}-w)\int_{\beta}^{1}F_{S_1}^{-1}(u)du+(1-\beta)(w-\widetilde{w})\\&\quad = (\widetilde{w}-w)\bigg(\int_{\beta}^{1}F_{S_1}^{-1}(u)du-(1-\beta)\bigg)\geq 0.\end{align*}

Hence, for

$S_1\geq_{\text{icx}} 1$

, we see that

$S_1\geq_{\text{icx}} 1$

, we see that

$Z_1^w=wS_1+1-w$

increases in increasing convex order with w. The condition

$Z_1^w=wS_1+1-w$

increases in increasing convex order with w. The condition

$S_1\geq_{\text{icx}} 1$

is easily checked. For a random variable with symmetric density, it simply means that the mode (mean if it exists) is greater than one.

$S_1\geq_{\text{icx}} 1$

is easily checked. For a random variable with symmetric density, it simply means that the mode (mean if it exists) is greater than one.

Increasing convex order enables results on how the fraction of the invested amount in the risky asset affects the value of liabilities. Let

$\mu_w=w\mathbb{E}[S_1]+1-w$

and let

$\mu_w=w\mathbb{E}[S_1]+1-w$

and let

$R_0^w$

refer to the quantity

$R_0^w$

refer to the quantity

$R_0$

in (2.3) under (2.5) (in particular,

$R_0$

in (2.3) under (2.5) (in particular,

$R_0^0=\rho({-}X_1)$

).

$R_0^0=\rho({-}X_1)$

).

Proposition 2.3. Assume that Assumption 1 holds, that

$S_1$

takes only nonnegative values, and that

$S_1$

takes only nonnegative values, and that

$S_1\geq_{\text{icx}} 1$

. If

$S_1\geq_{\text{icx}} 1$

. If

$\widetilde{w}\geq w$

,

$\widetilde{w}\geq w$

,

$R_0^{\widetilde{w}}\leq R_0^{w}$

and

$R_0^{\widetilde{w}}\leq R_0^{w}$

and

$1+\eta\geq \mu_w$

, then

$1+\eta\geq \mu_w$

, then

$V_0^{\widetilde{w}}\leq V_0^{w}$

.

$V_0^{\widetilde{w}}\leq V_0^{w}$

.

Proposition 2.4. Assume that Assumption 1 holds. If

$R_0^{w}\mu_w\geq R_0^{0}$

, then

$R_0^{w}\mu_w\geq R_0^{0}$

, then

$C_0^{w}\geq C_0^0$

. If

$C_0^{w}\geq C_0^0$

. If

$R_0^{w}\mu_w\geq R_0^{0}\geq R_0^{w}$

, then

$R_0^{w}\mu_w\geq R_0^{0}\geq R_0^{w}$

, then

$V_0^{w}\leq V_0^0$

.

$V_0^{w}\leq V_0^0$

.

The following result says that, under mild conditions, some risky investment, that is a small

$w\gt0$

compared to

$w\gt0$

compared to

$w=0$

, is always beneficial in the sense that

$w=0$

, is always beneficial in the sense that

$R_0^w\lt R_0^0$

and

$R_0^w\lt R_0^0$

and

$V_0^w\lt V_0^0$

.

$V_0^w\lt V_0^0$

.

Proposition 2.5. Let

$\rho=\operatorname{VaR}_{\alpha}$

and take

$\rho=\operatorname{VaR}_{\alpha}$

and take

$S_1$

and

$S_1$

and

$X_1$

to be nonnegative and independent. Assume that

$X_1$

to be nonnegative and independent. Assume that

$\mathbb{E}[S_1]\gt1$

and that

$\mathbb{E}[S_1]\gt1$

and that

$X_1$

has a bounded and continuous density that is nonvanishing in a neighborhood of

$X_1$

has a bounded and continuous density that is nonvanishing in a neighborhood of

$R_0^0=F_{X_1}^{-1}(1-\alpha)$

. If

$R_0^0=F_{X_1}^{-1}(1-\alpha)$

. If

$w\mapsto R_0^w$

is continuously differentiable, then

$w\mapsto R_0^w$

is continuously differentiable, then

\begin{align*}\lim_{w\to 0}\frac{d}{dw}R_0^w=\lim_{w\to 0}\frac{d}{dw}V_0^w=-R_0^0(\mathbb{E}[S_1]-1)\lt0, \quad \lim_{w\to 0}\frac{d}{dw}C_0^w=0.\end{align*}

\begin{align*}\lim_{w\to 0}\frac{d}{dw}R_0^w=\lim_{w\to 0}\frac{d}{dw}V_0^w=-R_0^0(\mathbb{E}[S_1]-1)\lt0, \quad \lim_{w\to 0}\frac{d}{dw}C_0^w=0.\end{align*}

Remark 2.5. If

$X_1=x\gt0$

is degenerate, then the assumptions in Proposition 2.5 do not hold. In this case,

$X_1=x\gt0$

is degenerate, then the assumptions in Proposition 2.5 do not hold. In this case,

$0=\operatorname{VaR}_{\alpha}\!(R_0^w(wS_1+1-w)-x)=R_0^w(w(\!\operatorname{VaR}_{\alpha}\!(S_1)+1)-1)+x$

. If further

$0=\operatorname{VaR}_{\alpha}\!(R_0^w(wS_1+1-w)-x)=R_0^w(w(\!\operatorname{VaR}_{\alpha}\!(S_1)+1)-1)+x$

. If further

$\operatorname{VaR}_{\alpha}\!(S_1)\in ({-}1,0)$

, then

$\operatorname{VaR}_{\alpha}\!(S_1)\in ({-}1,0)$

, then

\begin{align*}\lim_{w\to 0}\frac{d}{dw}R_0^w=x(\!\operatorname{VaR}_{\alpha}\!(S_1)-1)\gt0.\end{align*}

\begin{align*}\lim_{w\to 0}\frac{d}{dw}R_0^w=x(\!\operatorname{VaR}_{\alpha}\!(S_1)-1)\gt0.\end{align*}

The conclusion is that there is no w which gives

$R_0^w\lt R_0^0$

for all possible insurance risks

$R_0^w\lt R_0^0$

for all possible insurance risks

$X_1$

. In order for risky investment to reduce

$X_1$

. In order for risky investment to reduce

$R_0^w$

, some uncertainty about the outcome of

$R_0^w$

, some uncertainty about the outcome of

$X_1$

is needed. This conclusion is consistent with Theorem 1.1 in Filipović (Reference Filipović2008), although Filipović (Reference Filipović2008) focuses on convex risk measures.

$X_1$

is needed. This conclusion is consistent with Theorem 1.1 in Filipović (Reference Filipović2008), although Filipović (Reference Filipović2008) focuses on convex risk measures.

Remark 2.6. We focus on cost-of-capital valuation in this paper, but we could consider replacing

$C_0=\mathbb{E}[Z_{\text{sh}}]/(1+\eta)$

in (2.1) by risk-neutral valuation

$C_0=\mathbb{E}[Z_{\text{sh}}]/(1+\eta)$

in (2.1) by risk-neutral valuation

$C_0=\mathbb{E}^{\mathbb{Q}}[Z_{\text{sh}}]$

and still obtain the qualitative conclusion that some risky investment is always beneficial. Under the additional assumptions that

$C_0=\mathbb{E}^{\mathbb{Q}}[Z_{\text{sh}}]$

and still obtain the qualitative conclusion that some risky investment is always beneficial. Under the additional assumptions that

$\mathbb{E}^{\mathbb{Q}}[S_1]=1$

, that independence between

$\mathbb{E}^{\mathbb{Q}}[S_1]=1$

, that independence between

$S_1$

and

$S_1$

and

$X_1$

holds also with respect to

$X_1$

holds also with respect to

$\mathbb{Q}$

, and that

$\mathbb{Q}$

, and that

$X_1$

has a continuous density with respect to

$X_1$

has a continuous density with respect to

$\mathbb{Q}$

, which is nonvanishing in a neighborhood of

$\mathbb{Q}$

, which is nonvanishing in a neighborhood of

$R_0^0$

, the expression for the limit of the derivative for

$R_0^0$

, the expression for the limit of the derivative for

$V_0^w$

takes the form

$V_0^w$

takes the form

\begin{align*}\lim_{w\to 0}\frac{d}{dw}V_0^w=R_0^0(F^{\mathbb{Q}}_{X_1}(R_0^0)-1)(\mathbb{E}[S_1]-1)\lt0,\end{align*}

\begin{align*}\lim_{w\to 0}\frac{d}{dw}V_0^w=R_0^0(F^{\mathbb{Q}}_{X_1}(R_0^0)-1)(\mathbb{E}[S_1]-1)\lt0,\end{align*}

where

$F^{\mathbb{Q}}_{X_1}(R_0^0)=\mathbb{Q}(X_1\leq R_0^0)$

. A proof of this fact follows along the same lines as the proof of Proposition 2.5.

$F^{\mathbb{Q}}_{X_1}(R_0^0)=\mathbb{Q}(X_1\leq R_0^0)$

. A proof of this fact follows along the same lines as the proof of Proposition 2.5.

3. The Gaussian model

Let us now assume that

$X_1$

and

$X_1$

and

$Z_1$

are normally distributed. In that case, one obtains explicit expressions for

$Z_1$

are normally distributed. In that case, one obtains explicit expressions for

$R_0$

,

$R_0$

,

$C_0$

, and

$C_0$

, and

$V_0$

. Let us focus on the value-at-risk first.

$V_0$

. Let us focus on the value-at-risk first.

3.1. Value-at-risk

For

$Y\sim N(\mu,\sigma^2)$

, it is well known that

$Y\sim N(\mu,\sigma^2)$

, it is well known that

\begin{align} \operatorname{VaR}_{\alpha }\!(Y) = -\mu + \sigma \Phi ^{-1}(1 - \alpha).\end{align}

\begin{align} \operatorname{VaR}_{\alpha }\!(Y) = -\mu + \sigma \Phi ^{-1}(1 - \alpha).\end{align}

We will always assume that

$\alpha\in (0,1/2)$

so that

$\alpha\in (0,1/2)$

so that

$ \Phi ^{-1}(1-\alpha)\gt0$

.

$ \Phi ^{-1}(1-\alpha)\gt0$

.

Proposition 3.1. Suppose that

$X_1\sim N(\gamma,\nu^2)$

and

$X_1\sim N(\gamma,\nu^2)$

and

$Z_1\sim N(\mu,\sigma^2)$

are independent with

$Z_1\sim N(\mu,\sigma^2)$

are independent with

$\mu,\gamma,\sigma,\nu\gt0$

. Then,

$\mu,\gamma,\sigma,\nu\gt0$

. Then,

\begin{align} \operatorname{VaR}_{\alpha }\!(R_0Z_1-X_1)=\gamma-R_0\mu+\Phi^{-1}(1-\alpha)\sqrt{R_0^2\sigma^2+\nu^2}. \end{align}

\begin{align} \operatorname{VaR}_{\alpha }\!(R_0Z_1-X_1)=\gamma-R_0\mu+\Phi^{-1}(1-\alpha)\sqrt{R_0^2\sigma^2+\nu^2}. \end{align}

-

(i) If

$\mu\gt\sigma\Phi^{-1}(1-\alpha)$

, then

(3.3)is the unique

\begin{align} R_0=\frac{\mu\gamma+\Phi^{-1}(1-\alpha)\sqrt{\gamma^2\sigma^2+\mu^2\nu^2-\sigma^2\nu^2\Phi^{-1}(1-\alpha)^2}}{\mu^2-\sigma^2\Phi^{-1}(1-\alpha)^2} \end{align}

$R_0\gt0$

solving Equation (2.3).

-

(ii) If

$\mu\le \sigma\Phi^{-1}(1-\alpha)$

, then Equation (2.3) has no positive solution

$R_0$

.

Remark 3.1. If

$\gamma\neq \nu\Phi^{-1}(1-\alpha)$

, then

$\gamma\neq \nu\Phi^{-1}(1-\alpha)$

, then

$R_0$

in (3.3) is equivalent to

$R_0$

in (3.3) is equivalent to

\begin{align*}R_0=\frac{\gamma^2-\nu^2\Phi^{-1}(1-\alpha)^2}{\mu\gamma-\Phi^{-1}(1-\alpha)\sqrt{\gamma^2\sigma^2+\mu^2\nu^2-\sigma^2\nu^2\Phi^{-1}(1-\alpha)^2}}.\end{align*}

\begin{align*}R_0=\frac{\gamma^2-\nu^2\Phi^{-1}(1-\alpha)^2}{\mu\gamma-\Phi^{-1}(1-\alpha)\sqrt{\gamma^2\sigma^2+\mu^2\nu^2-\sigma^2\nu^2\Phi^{-1}(1-\alpha)^2}}.\end{align*}

This follows by multiplying both the numerator and denominator of (3.3) by

\begin{align*}\mu\gamma-\Phi^{-1}(1-\alpha)\sqrt{\gamma^2\sigma^2+\mu^2\nu^2-\sigma^2\nu^2\Phi^{-1}(1-\alpha)^2},\end{align*}

\begin{align*}\mu\gamma-\Phi^{-1}(1-\alpha)\sqrt{\gamma^2\sigma^2+\mu^2\nu^2-\sigma^2\nu^2\Phi^{-1}(1-\alpha)^2},\end{align*}

and factoring out

$\mu ^2 - \sigma ^2 \Phi ^{-1}(1 - \alpha )^{2} $

from the numerator. The usefulness comes from the fact that we will consider

$\mu ^2 - \sigma ^2 \Phi ^{-1}(1 - \alpha )^{2} $

from the numerator. The usefulness comes from the fact that we will consider

$\gamma$

and

$\gamma$

and

$\nu$

fixed while allowing

$\nu$

fixed while allowing

$\mu$

and

$\mu$

and

$\sigma$

to vary as a result of considering different positions in a risky asset.

$\sigma$

to vary as a result of considering different positions in a risky asset.

Remark 3.2. Taking derivatives in (3.3), we immediately get the (intuitive) result that

$\mu \mapsto R_{0} $

is decreasing and the functions

$\mu \mapsto R_{0} $

is decreasing and the functions

$\sigma \mapsto R_{0} $

,

$\sigma \mapsto R_{0} $

,

$\gamma \mapsto R_{0}$

and

$\gamma \mapsto R_{0}$

and

$\nu \mapsto R_{0}$

are increasing.

$\nu \mapsto R_{0}$

are increasing.

Remark 3.3. Note that for the existence of

$R_0\gt0$

, the mean return

$R_0\gt0$

, the mean return

$\mu$

of the assets needs to exceed the threshold

$\mu$

of the assets needs to exceed the threshold

$\sigma\Phi^{-1}(1-\alpha)$

. The latter expression depends on the volatility

$\sigma\Phi^{-1}(1-\alpha)$

. The latter expression depends on the volatility

$\sigma$

of the assets as well as the security level

$\sigma$

of the assets as well as the security level

$\alpha$

. Only in case of a purely risk-less investment (

$\alpha$

. Only in case of a purely risk-less investment (

$\mu=1,\sigma=0$

), the existence of

$\mu=1,\sigma=0$

), the existence of

$R_0\gt0$

is guaranteed for all parameter values (and then trivially reduces to

$R_0\gt0$

is guaranteed for all parameter values (and then trivially reduces to

$R_0={\gamma+\nu\Phi^{-1}(1-\alpha)}$

).

$R_0={\gamma+\nu\Phi^{-1}(1-\alpha)}$

).

Investing a portion

$0\lt w\lt 1$

of the wealth in the risky asset according to (2.5), in the Gaussian model, this simply translates into replacing the parameters

$0\lt w\lt 1$

of the wealth in the risky asset according to (2.5), in the Gaussian model, this simply translates into replacing the parameters

$(\mu,\sigma)$

by

$(\mu,\sigma)$

by

$(\mu_{w},\,\sigma_{w})\;:\!=(w\mu+1-w,w\sigma)$

. The following result shows that, under very mild conditions, the function

$(\mu_{w},\,\sigma_{w})\;:\!=(w\mu+1-w,w\sigma)$

. The following result shows that, under very mild conditions, the function

$w\mapsto R_0^{w}$

is strictly convex and in addition strictly decreasing for w sufficiently small.

$w\mapsto R_0^{w}$

is strictly convex and in addition strictly decreasing for w sufficiently small.

Proposition 3.2. Suppose that

$X_1\sim N(\gamma,\nu^2)$

and

$X_1\sim N(\gamma,\nu^2)$

and

$S_1\sim N(\mu,\sigma^2)$

are independent with

$S_1\sim N(\mu,\sigma^2)$

are independent with

\begin{align*}\nu\gt0,\sigma\gt0,\gamma\gt\nu\Phi^{-1}(1-\alpha) \text{ and } \mu\gt\max\!(1,\sigma\Phi^{-1}(1-\alpha)).\end{align*}

\begin{align*}\nu\gt0,\sigma\gt0,\gamma\gt\nu\Phi^{-1}(1-\alpha) \text{ and } \mu\gt\max\!(1,\sigma\Phi^{-1}(1-\alpha)).\end{align*}

For

$w\in [0,1]$

, let

$w\in [0,1]$

, let

$R_0^{w}$

be the positive solution to

$R_0^{w}$

be the positive solution to

\begin{align*}\operatorname{VaR}_{\alpha}\!(R_0^w(wS_1+1-w)-X_1)=0.\end{align*}

\begin{align*}\operatorname{VaR}_{\alpha}\!(R_0^w(wS_1+1-w)-X_1)=0.\end{align*}

Then,

$w\mapsto R_0^{w}$

is strictly convex. Moreover,

$w\mapsto R_0^{w}$

is strictly convex. Moreover,

$R_0^{w}\lt R_0^0$

for all

$R_0^{w}\lt R_0^0$

for all

$w\in (0,\widehat{w})$

, where

$w\in (0,\widehat{w})$

, where

$\widehat{w}=1$

if

$\widehat{w}=1$

if

$\mu\geq 1+\sigma\Phi^{-1}$

$\mu\geq 1+\sigma\Phi^{-1}$

$(1-\alpha)$

, and otherwise

$(1-\alpha)$

, and otherwise

\begin{align*}\widehat{w}=\frac{2(\mu-1)\nu\Phi^{-1}(1-\alpha)}{(1+\sigma\Phi^{-1}(1-\alpha)-\mu)(\mu-1+\sigma\Phi^{-1}(1-\alpha))(\gamma+\nu\Phi^{-1}(1-\alpha))}.\end{align*}

\begin{align*}\widehat{w}=\frac{2(\mu-1)\nu\Phi^{-1}(1-\alpha)}{(1+\sigma\Phi^{-1}(1-\alpha)-\mu)(\mu-1+\sigma\Phi^{-1}(1-\alpha))(\gamma+\nu\Phi^{-1}(1-\alpha))}.\end{align*}

Note that the quantity

$\widehat{w}$

is of particular interest, since in view of Proposition 2.3, it represents the limit weight of risky assets until which the overall capital requirement is not larger than

$\widehat{w}$

is of particular interest, since in view of Proposition 2.3, it represents the limit weight of risky assets until which the overall capital requirement is not larger than

$R_0^0$

(the one for purely risk-less assets), and the needed premium

$R_0^0$

(the one for purely risk-less assets), and the needed premium

$V_0^w$

is smaller than the one for

$V_0^w$

is smaller than the one for

$w=0$

. If

$w=0$

. If

$\max\!(1,\sigma\Phi^{-1}(1-\alpha))\lt$

$\max\!(1,\sigma\Phi^{-1}(1-\alpha))\lt$

$\mu\lt 1+\sigma\Phi^{-1}(1-\alpha)$

, then it is easily verified that

$\mu\lt 1+\sigma\Phi^{-1}(1-\alpha)$

, then it is easily verified that

$\nu\mapsto \widehat{w}$

is strictly increasing. Hence, more insurance risk allows for more risky investment without increasing the total capital requirement above the level corresponding to purely risk-less investment.

$\nu\mapsto \widehat{w}$

is strictly increasing. Hence, more insurance risk allows for more risky investment without increasing the total capital requirement above the level corresponding to purely risk-less investment.

The capital

$C_0$

given by (2.1) can be computed explicitly in the Gaussian setting. Together with the explicit expression for

$C_0$

given by (2.1) can be computed explicitly in the Gaussian setting. Together with the explicit expression for

$R_0$

in Proposition 3.1, this means that all the quantities

$R_0$

in Proposition 3.1, this means that all the quantities

$R_0,C_0,V_0$

can be computed explicitly.

$R_0,C_0,V_0$

can be computed explicitly.

Proposition 3.3. Suppose that

$X_1\sim N(\gamma,\nu^2)$

and

$X_1\sim N(\gamma,\nu^2)$

and

$Z_1\sim N(\mu,\sigma^2)$

are independent with

$Z_1\sim N(\mu,\sigma^2)$

are independent with

$\mu,\gamma,\sigma,\nu\gt0$

. If there exists an

$\mu,\gamma,\sigma,\nu\gt0$

. If there exists an

$R_0\gt0$

solving

$R_0\gt0$

solving

$\operatorname{VaR}_{\alpha}\!(R_0Z_1-X_1)=0$

, then

$\operatorname{VaR}_{\alpha}\!(R_0Z_1-X_1)=0$

, then

\begin{align*}C_0&=\frac{R_0\mu-\gamma}{1+\eta}(1+\delta(\alpha))\quad \text{and} \\V_0&=\frac{\gamma(1+\delta(\alpha))}{1+\eta}+R_0\frac{1+\eta-\mu(1+\delta(\alpha))}{1+\eta},\end{align*}

\begin{align*}C_0&=\frac{R_0\mu-\gamma}{1+\eta}(1+\delta(\alpha))\quad \text{and} \\V_0&=\frac{\gamma(1+\delta(\alpha))}{1+\eta}+R_0\frac{1+\eta-\mu(1+\delta(\alpha))}{1+\eta},\end{align*}

where

\begin{align*} 0\lt\delta(\alpha)\;:\!=\frac{\varphi(\Phi^{-1}(1-\alpha))}{\Phi^{-1}(1-\alpha)}-\alpha\lt\frac{\alpha}{\Phi^{-1}(1-\alpha)^2}.\end{align*}

\begin{align*} 0\lt\delta(\alpha)\;:\!=\frac{\varphi(\Phi^{-1}(1-\alpha))}{\Phi^{-1}(1-\alpha)}-\alpha\lt\frac{\alpha}{\Phi^{-1}(1-\alpha)^2}.\end{align*}

Remark 3.4. From Proposition 3.3, it follows that the value of the limited liability option (cf. Remark 2.3) in the Gaussian model and

$R_0$

determined by the risk measure

$R_0$

determined by the risk measure

$\operatorname{VaR}_{\alpha}$

is

$\operatorname{VaR}_{\alpha}$

is

\begin{align*}\delta(\alpha)\frac{R_0\mu-\gamma}{1+\eta}.\end{align*}

\begin{align*}\delta(\alpha)\frac{R_0\mu-\gamma}{1+\eta}.\end{align*}

For

$\alpha$

small, for example,

$\alpha$

small, for example,

$\alpha=0.005$

, the value of the limited liability option is very small due to the light Gaussian tails.

$\alpha=0.005$

, the value of the limited liability option is very small due to the light Gaussian tails.

The following result shows that investment in the (sufficiently attractive) risky asset always makes the payoff for a capital provider more attractive compared to the case with only risk-less investment. Hence, the contribution

$C_0$

to the financing of the capital requirement should increase if risky investments are allowed.

$C_0$

to the financing of the capital requirement should increase if risky investments are allowed.

Proposition 3.4. Suppose that

$X_1\sim N(\gamma,\nu^2)$

and

$X_1\sim N(\gamma,\nu^2)$

and

$S_1\sim N(\mu,\sigma^2)$

are independent with

$S_1\sim N(\mu,\sigma^2)$

are independent with

$\gamma,\sigma,\nu\gt0$

and

$\gamma,\sigma,\nu\gt0$

and

$\mu \gt \sigma \Phi ^{-1}(1-\alpha )$

. For

$\mu \gt \sigma \Phi ^{-1}(1-\alpha )$

. For

$w\in [0,1]$

, let

$w\in [0,1]$

, let

$R_0^{w}$

be the positive solution to

$R_0^{w}$

be the positive solution to

\begin{align*}\operatorname{VaR}_{\alpha}\!(R_0^w(wS_1+1-w)-X_1)=0.\end{align*}

\begin{align*}\operatorname{VaR}_{\alpha}\!(R_0^w(wS_1+1-w)-X_1)=0.\end{align*}

Then,

$C_{0}^{0} \lt C_{0}^{w}$

for all

$C_{0}^{0} \lt C_{0}^{w}$

for all

$w \in (0,1]$

.

$w \in (0,1]$

.

If

$R_0^w\lt R_0^0$

and

$R_0^w\lt R_0^0$

and

$C_0^w\gt C_0^0$

, then

$C_0^w\gt C_0^0$

, then

$V_0^w\;:\!=R_0^w-C_0^w\lt R_0^0-C_0^0=\!:\;V_0^0$

. Hence, by combining Propositions 3.2 and 3.4, we immediately obtain the following result.

$V_0^w\;:\!=R_0^w-C_0^w\lt R_0^0-C_0^0=\!:\;V_0^0$

. Hence, by combining Propositions 3.2 and 3.4, we immediately obtain the following result.

Corollary 3.5. Suppose that

$X_1\sim N(\gamma,\nu^2)$

and

$X_1\sim N(\gamma,\nu^2)$

and

$S_1\sim N(\mu,\sigma^2)$

are independent with

$S_1\sim N(\mu,\sigma^2)$

are independent with

$\sigma,\nu\gt0$

,

$\sigma,\nu\gt0$

,

$\gamma\gt\nu\Phi^{-1}(1-\alpha)$

and

$\gamma\gt\nu\Phi^{-1}(1-\alpha)$

and

$\mu\gt\max\!(1,\sigma\Phi^{-1}(1-\alpha))$

. For

$\mu\gt\max\!(1,\sigma\Phi^{-1}(1-\alpha))$

. For

$w\in [0,1]$

, let

$w\in [0,1]$

, let

$R_0^{w}$

be the positive solution to

$R_0^{w}$

be the positive solution to

\begin{align*}\operatorname{VaR}_{\alpha}\!(R_0^w(wS_1+1-w)-X_1)=0.\end{align*}

\begin{align*}\operatorname{VaR}_{\alpha}\!(R_0^w(wS_1+1-w)-X_1)=0.\end{align*}

Then,

$V_0^{w}\leq V_0^0$

for all

$V_0^{w}\leq V_0^0$

for all

$w\in (0,\widehat{w})$

, where

$w\in (0,\widehat{w})$

, where

$\widehat{w}$

is given in Proposition 3.2.

$\widehat{w}$

is given in Proposition 3.2.

Note that the statement of Corollary 3.5 is stronger than what we would get by combining Propositions 2.3 and 3.2, since we do not need any condition involving the cost-of-capital rate

$\eta$

. The statement of Corollary 3.5 is a statement for w sufficiently small where

$\eta$

. The statement of Corollary 3.5 is a statement for w sufficiently small where

$R_0^w\lt R_0^0$

. For w larger with

$R_0^w\lt R_0^0$

. For w larger with

$R_0^w\gt R_0^0$

, there is no hope for a simple statement to hold regardless of the parameter

$R_0^w\gt R_0^0$

, there is no hope for a simple statement to hold regardless of the parameter

$\eta$

. Note that if we let

$\eta$

. Note that if we let

$\eta\to\infty$

, then

$\eta\to\infty$

, then

$V_0^w\to R_0^w$

and

$V_0^w\to R_0^w$

and

$R_0^w$

is typically not monotone, although decreasing for w sufficiently small. However, by evaluating

$R_0^w$

is typically not monotone, although decreasing for w sufficiently small. However, by evaluating

$V_0^w$

numerically, we do observe that

$V_0^w$

numerically, we do observe that

$V_0^{w}\leq V_0^0$

for all w for realistic parameter values, see, for example, Figure 1 in Section 4 for an illustration. We emphasize that the statement about

$V_0^{w}\leq V_0^0$

for all w for realistic parameter values, see, for example, Figure 1 in Section 4 for an illustration. We emphasize that the statement about

$V_0^w$

for realistic parameter values implicitly assumes that

$V_0^w$

for realistic parameter values implicitly assumes that

$\mu\geq 1$

is not too small. That is, for

$\mu\geq 1$

is not too small. That is, for

$\mu=1$

, it follows immediately from Proposition 3.3 that

$\mu=1$

, it follows immediately from Proposition 3.3 that

\begin{align*}V_0^w=\frac{\gamma(1+\delta(\alpha))}{1+\eta}+R_0^w\frac{\eta-\delta(\alpha)}{1+\eta}.\end{align*}

\begin{align*}V_0^w=\frac{\gamma(1+\delta(\alpha))}{1+\eta}+R_0^w\frac{\eta-\delta(\alpha)}{1+\eta}.\end{align*}

So for

$\mu=1$

, we see that

$\mu=1$

, we see that

$V_0^{w}\gt V_0^0$

is equivalent to

$V_0^{w}\gt V_0^0$

is equivalent to

$R_0^{w}\gt R_0^0$

. From Remark 3.1, it follows that

$R_0^{w}\gt R_0^0$

. From Remark 3.1, it follows that

$R_0^{w}\gt R_0^0$

holds for all

$R_0^{w}\gt R_0^0$

holds for all

$w\in (0,1]$

if

$w\in (0,1]$

if

$\mu=1$

and

$\mu=1$

and

$\gamma\gt\nu\Phi^{-1}(1-\alpha)$

.

$\gamma\gt\nu\Phi^{-1}(1-\alpha)$

.

Remark 3.5. In this paper, we restrict our attention to the setting where

$S_1$

and

$S_1$

and

$X_1$

are independent. If the correlation coefficient

$X_1$

are independent. If the correlation coefficient

$\operatorname{Cor}(S_1,X_1)\gt0$

, then risky investments would not only generate a more favorable expectation (assuming

$\operatorname{Cor}(S_1,X_1)\gt0$

, then risky investments would not only generate a more favorable expectation (assuming

$\mu\gt1$

) but also partly hedge the insurance liability. One may wonder whether risky investments could be advisable even in the case

$\mu\gt1$

) but also partly hedge the insurance liability. One may wonder whether risky investments could be advisable even in the case

$\operatorname{Cor}(S_1,X_1)\lt0$

. In this case, the expressions for

$\operatorname{Cor}(S_1,X_1)\lt0$

. In this case, the expressions for

$V_0$

and

$V_0$

and

$C_0$

in Proposition 3.3 remain the same, but the expression for

$C_0$

in Proposition 3.3 remain the same, but the expression for

$R_0$

changes. With

$R_0$

changes. With

$c\;:\!=\operatorname{Cor}(S_1,X_1)\leq 0$

, and under the assumption that

$c\;:\!=\operatorname{Cor}(S_1,X_1)\leq 0$

, and under the assumption that

$\mu\gt\sigma\Phi^{-1}(1-\alpha)$

and

$\mu\gt\sigma\Phi^{-1}(1-\alpha)$

and

$\gamma\neq\nu\Phi^{-1}(1-\alpha)$

,

$\gamma\neq\nu\Phi^{-1}(1-\alpha)$

,

\begin{align*}C^w_0&=\frac{R^w_0\mu_w-\gamma}{1+\eta}(1+\delta(\alpha)), \\V^w_0&=\frac{\gamma(1+\delta(\alpha))}{1+\eta}+R^w_0\frac{1+\eta-\mu_w(1+\delta(\alpha))}{1+\eta}, \\R^w_0&=\frac{\gamma^2-\nu^2\Phi^{-1}(1-\alpha)^2}{h(w)},\end{align*}

\begin{align*}C^w_0&=\frac{R^w_0\mu_w-\gamma}{1+\eta}(1+\delta(\alpha)), \\V^w_0&=\frac{\gamma(1+\delta(\alpha))}{1+\eta}+R^w_0\frac{1+\eta-\mu_w(1+\delta(\alpha))}{1+\eta}, \\R^w_0&=\frac{\gamma^2-\nu^2\Phi^{-1}(1-\alpha)^2}{h(w)},\end{align*}

where

$\mu_w\;:\!=w\mu+1-w$

,

$\mu_w\;:\!=w\mu+1-w$

,

$\sigma_w\;:\!=w\sigma$

, and

$\sigma_w\;:\!=w\sigma$

, and

\begin{align*}h(w)&=\mu_w\gamma-c\sigma_w\nu\Phi^{-1}(1-\alpha)^2-\Big((\mu_w\gamma-c\sigma_w\nu\Phi^{-1}(1-\alpha)^2)^2 \\&\quad-(\mu_w^2-\sigma_w^2\Phi^{-1}(1-\alpha)^2)(\gamma^2-\nu^2\Phi^{-1}(1-\alpha)^2)\Big)^{1/2}.\end{align*}

\begin{align*}h(w)&=\mu_w\gamma-c\sigma_w\nu\Phi^{-1}(1-\alpha)^2-\Big((\mu_w\gamma-c\sigma_w\nu\Phi^{-1}(1-\alpha)^2)^2 \\&\quad-(\mu_w^2-\sigma_w^2\Phi^{-1}(1-\alpha)^2)(\gamma^2-\nu^2\Phi^{-1}(1-\alpha)^2)\Big)^{1/2}.\end{align*}

The only difference from the case

$c=0$

is that a term involving c appears twice in the expression for h(w). Straightforward computations give

$c=0$

is that a term involving c appears twice in the expression for h(w). Straightforward computations give

\begin{align*}\frac{dR^w_0}{dw}(0)&=-(\gamma^2-\nu^2\Phi^{-1}(1-\alpha))\frac{h'(0)}{h^2(0)}\\&=-(\gamma+\nu\Phi^{-1}(1-\alpha))(\mu-1+c\sigma\Phi^{-1}(1-\alpha)).\end{align*}

\begin{align*}\frac{dR^w_0}{dw}(0)&=-(\gamma^2-\nu^2\Phi^{-1}(1-\alpha))\frac{h'(0)}{h^2(0)}\\&=-(\gamma+\nu\Phi^{-1}(1-\alpha))(\mu-1+c\sigma\Phi^{-1}(1-\alpha)).\end{align*}

We conclude that as long as

$\mu\gt1-c\sigma\Phi^{-1}(1-\alpha)$

, small positions

$\mu\gt1-c\sigma\Phi^{-1}(1-\alpha)$

, small positions

$w\gt0$

in the risky asset will still imply

$w\gt0$

in the risky asset will still imply

$R_0^w\lt R_0^0$

.

$R_0^w\lt R_0^0$

.

3.2. Expected shortfall

In the case of normal distributions, the expected shortfall of

$Y\sim N(\mu,\sigma^2)$

at safety level

$Y\sim N(\mu,\sigma^2)$

at safety level

$\alpha$

can simply be expressed as

$\alpha$

can simply be expressed as

\begin{align*} \text{ES}_{\alpha }(Y) = -\mu + \sigma \frac{\varphi (\Phi ^{-1}(1-\alpha ) ) }{\alpha },\end{align*}

\begin{align*} \text{ES}_{\alpha }(Y) = -\mu + \sigma \frac{\varphi (\Phi ^{-1}(1-\alpha ) ) }{\alpha },\end{align*}

so the constant

$\Phi ^{-1}(1-\alpha)$

for the value-at-risk in (3.1) is just replaced by another constant

$\Phi ^{-1}(1-\alpha)$

for the value-at-risk in (3.1) is just replaced by another constant

\begin{align*}\psi=\frac{1}{\alpha}\int_0^{\alpha}\Phi^{-1}(1-\beta)d\beta=\frac{1}{\alpha}\int_{\Phi^{-1}(1-\alpha)}^{\infty}z\varphi(z)dz=\frac{\varphi(\Phi^{-1}(1-\alpha))}{\alpha}.\end{align*}

\begin{align*}\psi=\frac{1}{\alpha}\int_0^{\alpha}\Phi^{-1}(1-\beta)d\beta=\frac{1}{\alpha}\int_{\Phi^{-1}(1-\alpha)}^{\infty}z\varphi(z)dz=\frac{\varphi(\Phi^{-1}(1-\alpha))}{\alpha}.\end{align*}

Correspondingly, we can directly adapt the results previously obtained for the value-at-risk. For instance, Proposition 3.1 turns into the following result.

Proposition 3.6. Suppose that

$X_1\sim N(\gamma,\nu^2)$

and

$X_1\sim N(\gamma,\nu^2)$

and

$Z_1\sim N(\mu,\sigma^2)$

are independent with

$Z_1\sim N(\mu,\sigma^2)$

are independent with

$\mu,\gamma,\sigma,\nu\gt0$

. Then, for

$\mu,\gamma,\sigma,\nu\gt0$

. Then, for

$\rho(\!\cdot\!) = \operatorname{ES}_{\alpha}\!(\!\cdot\!)$

,

$\rho(\!\cdot\!) = \operatorname{ES}_{\alpha}\!(\!\cdot\!)$

,

Proposition 3.2 is easily adjusted to

$\operatorname{ES}_{\alpha}$

instead of

$\operatorname{ES}_{\alpha}$

instead of

$\operatorname{VaR}_{\alpha}$

. Replacing

$\operatorname{VaR}_{\alpha}$

. Replacing

$\Phi^{-1}(1-\alpha)$

by

$\Phi^{-1}(1-\alpha)$

by

$\psi$

gives the following result.

$\psi$

gives the following result.

Proposition 3.7. Suppose that

$X_1\sim N(\gamma,\nu^2)$

and

$X_1\sim N(\gamma,\nu^2)$

and

$S_1\sim N(\mu,\sigma^2)$

are independent with

$S_1\sim N(\mu,\sigma^2)$

are independent with

$\nu\gt0,\sigma\gt0$

,

$\nu\gt0,\sigma\gt0$

,

$\gamma\gt\nu\psi$

and

$\gamma\gt\nu\psi$

and

$\mu\gt\max\!(1,\sigma\psi)$

. For

$\mu\gt\max\!(1,\sigma\psi)$

. For

$w\in [0,1]$

, let

$w\in [0,1]$

, let

$R_0^{w}$

be the positive solution to

$R_0^{w}$

be the positive solution to

\begin{align*}\operatorname{ES}_{\alpha}\!(R_0^w(wS_1+1-w)-X_1)=0.\end{align*}

\begin{align*}\operatorname{ES}_{\alpha}\!(R_0^w(wS_1+1-w)-X_1)=0.\end{align*}

Then,

$w\mapsto R_0^{w}$

is strictly convex. Moreover,

$w\mapsto R_0^{w}$

is strictly convex. Moreover,

$R_0^{w}\lt R_0^0$

for all

$R_0^{w}\lt R_0^0$

for all

$w\in (0,\widehat{w})$

, where

$w\in (0,\widehat{w})$

, where

$\widehat{w}=1$

if

$\widehat{w}=1$

if

$\mu\geq 1+\sigma\psi$

, and otherwise

$\mu\geq 1+\sigma\psi$

, and otherwise

\begin{align*}\widehat{w}=\frac{2(\mu-1)\nu\psi}{(1+\sigma\psi-\mu)(\mu-1+\sigma\psi)(\gamma+\nu\psi)}.\end{align*}

\begin{align*}\widehat{w}=\frac{2(\mu-1)\nu\psi}{(1+\sigma\psi-\mu)(\mu-1+\sigma\psi)(\gamma+\nu\psi)}.\end{align*}

Proposition 3.3 is also easily adjusted to

$\operatorname{ES}_{\alpha}$

instead of

$\operatorname{ES}_{\alpha}$

instead of

$\operatorname{VaR}_{\alpha}$

. Replacing

$\operatorname{VaR}_{\alpha}$

. Replacing

$1+\delta(\alpha)$

in Proposition 3.3 by

$1+\delta(\alpha)$

in Proposition 3.3 by

$\Phi (\psi) + {\varphi(\psi)}/{\psi}$

gives the following result.

$\Phi (\psi) + {\varphi(\psi)}/{\psi}$

gives the following result.

Proposition 3.8. Suppose that

$X_1\sim N(\gamma,\nu^2)$

and

$X_1\sim N(\gamma,\nu^2)$

and

$Z_1\sim N(\mu,\sigma^2)$

are independent with

$Z_1\sim N(\mu,\sigma^2)$

are independent with

$\mu,\gamma,\sigma,\nu\gt0$

. If there exists an

$\mu,\gamma,\sigma,\nu\gt0$

. If there exists an

$R_0\gt0$

solving

$R_0\gt0$

solving

$\operatorname{ES}_{\alpha}\!(R_0Z_1-X_1)=0$

, then

$\operatorname{ES}_{\alpha}\!(R_0Z_1-X_1)=0$

, then

\begin{align*} C_{0} &= (R_0 \mu - \gamma ) \frac{\Phi (\psi ) + \varphi (\psi ) /{\psi } }{1 + \eta },\\ V_{0} &= \gamma \frac{\Phi (\psi) + {\varphi(\psi)}/{\psi}}{1+\eta} + R_0 \frac{1+\eta -\mu(\Phi (\psi) + {\varphi(\psi)}/{\psi})}{1+\eta}.\end{align*}

\begin{align*} C_{0} &= (R_0 \mu - \gamma ) \frac{\Phi (\psi ) + \varphi (\psi ) /{\psi } }{1 + \eta },\\ V_{0} &= \gamma \frac{\Phi (\psi) + {\varphi(\psi)}/{\psi}}{1+\eta} + R_0 \frac{1+\eta -\mu(\Phi (\psi) + {\varphi(\psi)}/{\psi})}{1+\eta}.\end{align*}

Finally, Corollary 3.5 has the following version for

$\operatorname{ES}_{\alpha}$

instead of

$\operatorname{ES}_{\alpha}$

instead of

$\operatorname{VaR}_{\alpha}$

.

$\operatorname{VaR}_{\alpha}$

.

Corollary 3.9. Suppose that

$X_1\sim N(\gamma,\nu^2)$

and

$X_1\sim N(\gamma,\nu^2)$

and

$S_1\sim N(\mu,\sigma^2)$

are independent with

$S_1\sim N(\mu,\sigma^2)$

are independent with

$\sigma,\nu\gt0$

,

$\sigma,\nu\gt0$

,

$\gamma\gt\nu\psi$

and

$\gamma\gt\nu\psi$

and

$\mu\gt\max\!(1,\sigma\psi)$

. For

$\mu\gt\max\!(1,\sigma\psi)$

. For

$w\in [0,1]$

, let

$w\in [0,1]$

, let

$R_0^{w}$

be the positive solution to

$R_0^{w}$

be the positive solution to

\begin{align*}\operatorname{ES}_{\alpha}\!(R_0^w(wS_1+1-w)-X_1)=0.\end{align*}

\begin{align*}\operatorname{ES}_{\alpha}\!(R_0^w(wS_1+1-w)-X_1)=0.\end{align*}

Then,

$V_0^{w}\leq V_0^0$

for all

$V_0^{w}\leq V_0^0$

for all

$w\in (0,\widehat{w})$

, where

$w\in (0,\widehat{w})$

, where

$\widehat{w}$

is given in Proposition 3.7.

$\widehat{w}$

is given in Proposition 3.7.

4. Numerical illustrations

Let us now put the results of the previous sections into concrete numerical conclusions for realistic parameter choices. Throughout this section, we assume the cost-of-capital rate to be

$\eta=0.06$

(see Section 1 for a discussion of that parameter).

$\eta=0.06$

(see Section 1 for a discussion of that parameter).

$R_{0}^{w}, C_{0}^{w}$

, and

$R_{0}^{w}, C_{0}^{w}$

, and

$V_{0}^{w}$

for the Gaussian model with

$V_{0}^{w}$

for the Gaussian model with

$\mu = 1.05, \gamma = 1,\nu =0.3 $

,

$\mu = 1.05, \gamma = 1,\nu =0.3 $

,

$\rho=\operatorname{VaR}_{0.005}$

, and various values of

$\rho=\operatorname{VaR}_{0.005}$

, and various values of

$\sigma$

.

$\sigma$

.

4.1. The Gaussian model

Assuming that both the insurance risk

$X_1$

and the financial risk

$X_1$

and the financial risk

$Z_1$

are normally distributed, we can use the explicit formulas from Section 3 to study the effect of the choice of w on the resulting requirements for insurance premium

$Z_1$

are normally distributed, we can use the explicit formulas from Section 3 to study the effect of the choice of w on the resulting requirements for insurance premium

$V_0$

, solvency capital requirement

$V_0$

, solvency capital requirement

$C_0$

, and their sum

$C_0$

, and their sum

$R_0$

. Let us focus on the case of value-at-risk with safety level

$R_0$

. Let us focus on the case of value-at-risk with safety level

$\alpha = 0.005$

, which is the risk measure used in Solvency II. Let us further assume

$\alpha = 0.005$

, which is the risk measure used in Solvency II. Let us further assume

$\mu = 1.05$

,

$\mu = 1.05$

,

$\sigma =0.2$

, which may be considered a realistic return and volatility for an institutional investor, as well as the variations

$\sigma =0.2$

, which may be considered a realistic return and volatility for an institutional investor, as well as the variations

$\sigma=0.1$

and

$\sigma=0.1$

and

$\sigma=0.3$

. For the insurance risk

$\sigma=0.3$

. For the insurance risk

$X_1$

, we assume a mean of

$X_1$

, we assume a mean of

$\gamma = 1$

(cf. Remark 2.4) and a standard deviation of

$\gamma = 1$

(cf. Remark 2.4) and a standard deviation of

$\nu =0.3$

(which corresponds to a coefficient of variation of the total claim size of 0.3), together with a few variations of

$\nu =0.3$

(which corresponds to a coefficient of variation of the total claim size of 0.3), together with a few variations of

$\nu$

. Figure 1 plots the resulting values of

$\nu$

. Figure 1 plots the resulting values of

$R_{0}$

,

$R_{0}$

,

$C_{0}$

and

$C_{0}$

and

$V_{0}$

as functions of w (recall that

$V_{0}$

as functions of w (recall that

$w=0$

corresponds to purely risk-less investment and

$w=0$

corresponds to purely risk-less investment and

$w=1$

corresponds to purely risky investment, cf. (2.5)).

$w=1$

corresponds to purely risky investment, cf. (2.5)).

Note that while the needed insurance premium

$V_0^{w}$

reduces with increasing risky asset allocation for all w, the needed solvency requirement

$V_0^{w}$

reduces with increasing risky asset allocation for all w, the needed solvency requirement

$C_0^{w}$

from shareholders increases correspondingly, and the minimal overall capital requirement

$C_0^{w}$

from shareholders increases correspondingly, and the minimal overall capital requirement

$R_0^{w}$

for

$R_0^{w}$

for

$\sigma=0.2$

is achieved for

$\sigma=0.2$

is achieved for

$w^*=0.083$

, for example, only 8.3% of the assets are invested in the risky asset, which then constitutes the most capital-efficient solution under the present model assumptions. One sees how this value

$w^*=0.083$

, for example, only 8.3% of the assets are invested in the risky asset, which then constitutes the most capital-efficient solution under the present model assumptions. One sees how this value

$w^*$

decreases for increasing volatility in the risky asset, which matches the intuition. It is also insightful to see that for larger values of w the solvency requirement

$w^*$

decreases for increasing volatility in the risky asset, which matches the intuition. It is also insightful to see that for larger values of w the solvency requirement

$C_0^w$

starts to dominate the needed insurance premium

$C_0^w$

starts to dominate the needed insurance premium

$V_0$

, more prominently for larger values of

$V_0$

, more prominently for larger values of

$\sigma$

. The value

$\sigma$

. The value

$\widehat{w}$

until which the overall capital requirement

$\widehat{w}$

until which the overall capital requirement

$R_0^{w}$

is smaller than

$R_0^{w}$

is smaller than

$R_0^{0}$

indeed corresponds to the one obtained from Proposition 3.2. Figure 2 plots the corresponding results for fixed

$R_0^{0}$

indeed corresponds to the one obtained from Proposition 3.2. Figure 2 plots the corresponding results for fixed

$\sigma=0.2$

, but varying standard deviation

$\sigma=0.2$

, but varying standard deviation

$\nu$

of the insurance risk. One observes how the overall capital requirement

$\nu$

of the insurance risk. One observes how the overall capital requirement

$R_0^w$

increases with

$R_0^w$

increases with

$\nu$

, and how

$\nu$

, and how

$C_0^w$

becomes larger than the needed insurance premium

$C_0^w$

becomes larger than the needed insurance premium

$V_0^{w}$

already for smaller values of w. One also observes from Figure 2 that the riskier the insurance risk

$V_0^{w}$

already for smaller values of w. One also observes from Figure 2 that the riskier the insurance risk

$X_1$

is (larger value

$X_1$

is (larger value

$\nu$

), the larger fraction

$\nu$

), the larger fraction

$w^*$

of the initial capital should be invested in the risky asset in order to minimize the total capital requirement

$w^*$

of the initial capital should be invested in the risky asset in order to minimize the total capital requirement

$R_0^w$

.

$R_0^w$

.

$R_{0}^{w}, C_{0}^{w}$

, and

$R_{0}^{w}, C_{0}^{w}$

, and

$V_{0}^{w}$

for the Gaussian model with

$V_{0}^{w}$

for the Gaussian model with

$\mu = 1.05, \sigma=0.2,\gamma = 1$

,

$\mu = 1.05, \sigma=0.2,\gamma = 1$

,

$\rho=\operatorname{VaR}_{0.005}$

and various values of

$\rho=\operatorname{VaR}_{0.005}$

and various values of

$\nu$

.

$\nu$

.

Finally, at first sight, it may seem surprising that the increase of

$R_0^{w}$

for increasing standard deviation

$R_0^{w}$

for increasing standard deviation

$\nu$

of the insurance risk is almost exclusively swallowed by the increase of

$\nu$

of the insurance risk is almost exclusively swallowed by the increase of

$C_0^{w}$

and leaves the premium

$C_0^{w}$

and leaves the premium

$V_0^{w}$

virtually unchanged. The explanation is that the increased standard deviation (for fixed

$V_0^{w}$

virtually unchanged. The explanation is that the increased standard deviation (for fixed

$\mathbb{E}[X_1]$

) raises the value of the limited liability option. Concretely, for any absolutely continuous random variable

$\mathbb{E}[X_1]$

) raises the value of the limited liability option. Concretely, for any absolutely continuous random variable

$X_1$