In 2021, at the 26th Conference of the Parties (COP 26) in Glasgow, Scotland, the Glasgow Financial Alliance for Net Zero (GFANZ) was the object of intense media fanfare. The umbrella initiative had brought together ambitious platforms for asset owners, asset managers, insurers, and banks to address climate change and reduce greenhouse gas emissions associated with their business operations to net zeroFootnote 1 by mid-century. Hundreds of organizations participated, collectively managing over US$130 trillion in assets. Co-chaired by former G20 Financial Stability Board chair and Bank of England Governor Mark Carney,Footnote 2 and co-launched by the UK’s COP 26 Presidency, GFANZ’s respective alliances brought together the most prominent names and brands in the world of finance, from BlackRock to Swiss Re, from Citigroup to Allianz. Net-zero targets marked a novel turn in the history of ‘green finance’ initiatives: companies were committing to significant whole-of-company emissions reductions on a fixed timeline.

GFANZ joined a constellation of United Nations (UN)- and civil society-led efforts to mobilize the private sector toward net-zero targets, collectively acting on the scientific consensus that halting further accumulation of carbon dioxide in the atmosphere also pauses related global warming.Footnote 3 The promise of the Paris Agreement and its temperature goal of limiting global warming to 1.5°C (and well below 2°C) above pre-industrial levelsFootnote 4 thus hinges on delivering net zero globally.Footnote 5 With the Paris Agreement’s emphasis on ‘aligning financial flows consistent with a pathway toward low greenhouse gas emissions,’Footnote 6 the UN Framework Convention on Climate Change’s (UNFCCC) increasing emphasis on non-state actors as stakeholders and agents of change,Footnote 7 and the central role of the financial sector in energy infrastructure, GFANZ’s emergence was especially significant. On paper, at least, if the global titans of finance were signing on to limit their financed emissions to net zero by 2050, a rapid transition beyond coal, oil, and gas would surely be possible.

Soon after Glasgow, however, the mood shifted. Non-governmental organizations (NGOs) criticized the lackluster commitments of signatories to GFANZ-affiliated alliances, noting misalignment with credible emissions reduction trajectories across investment, lending, and underwriting portfolios. More dramatically, from 2022 to 2024, unsubstantiated yet loud accusations of antitrust violations by US State Attorneys General led many US and non-US companies alike to ultimately defect en masse from GFANZ-affiliated platforms.Footnote 8 Under legal pressure, the Net-Zero Insurance Alliance (NZIA) and the Net-Zero Banking Alliance (NZBA) ceased operations, and in the former case, reconstituted as a non-prescriptive, multi-stakeholder forum. The Net Zero Asset Managers Initiative (NZAM) suspended its activities and, following a strategic review, scaled back requirements that scientists typically associate with credible net-zero targets.Footnote 9 GFANZ itself shifted focus away from coordinating alliances altogether.

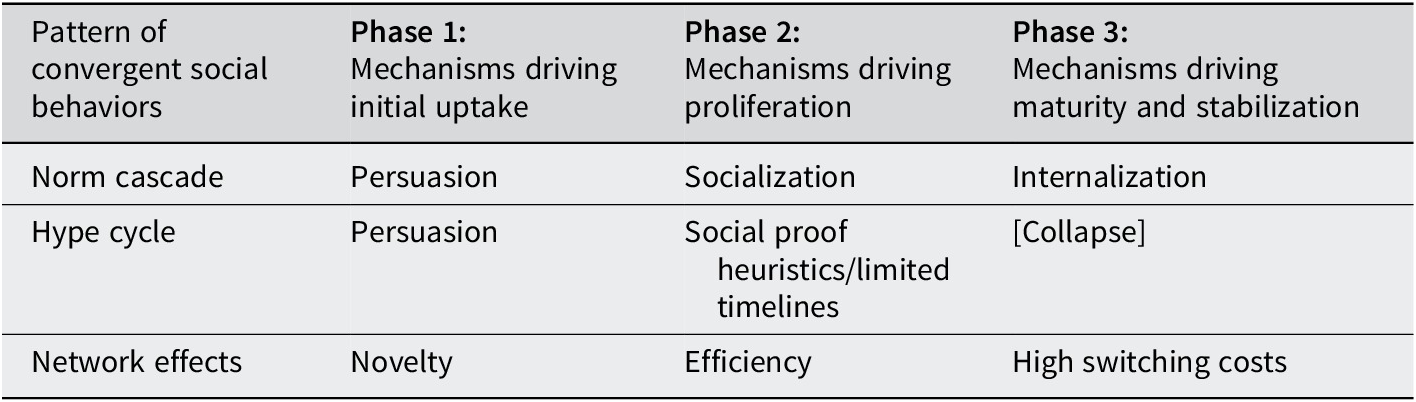

Why did this rapid uptake of net-zeroFootnote 10 norms end up being so fragile in finance? The initial non-linear change suggested the precipitation of a norm cascade, as hundreds of companies flocked to GFANZ’s banner. As International Relations (IR) scholars have repeatedly demonstrated across units of analysis and issue areas, such processes can lead to enduring social and political transformation. And yet, the ultimate taken-for-grantedness of net zero did not materialize, despite a similar pattern of escalating group conformity and broad global participation. While the sigmoidal S-curve of the norm cascade accurately captures the acceleration of net-zero initiative memberships and commitments, the associated mechanisms – persuasion, socialization, and internalization – arguably did not unfold in a way that would motivate norm adherents to resist contestation.

In this paper, I argue that ‘hype cycles’ may better describe the underlying dynamic in cases such as GFANZ. In taking the concept out of the vernacular and into analytical usage, I pinpoint three related and necessary conditions for hype cycles: ambiguity and uncertainty constrain the ability of actors to make calculative or normative decisions, decision-making relies on the ‘heuristic of social proof’ or bandwagoning whereby the ‘right’ course of action is determined by what a critical mass of other actors are doing, and time is perceived to be limited. Under these conditions, actors may crowd into norm-prescribed behaviors without socialization taking effect. These patterns are fragile because new information may reveal a weaker-than-expected justification for compliance, prompting actors to experience ‘buyer’s remorse’ and change course, especially when the costs of exit or switching behaviors are low.

I substantiate these claims in the GFANZ case using semi-structured interviews with representatives from financial companies and other actors involved in related net-zero initiatives. I find that there was immense momentum building toward the formation of private sector coalitions in 2021, especially as part of the United Kingdom’s goal of platforming private finance as a climate solution during its Presidency of COP 26. Many financial institutions were swept up in the ambition and energy, saw their peers joining, and followed suit. These commitments were made amid significant ambiguity about what net zero meant in terms of decarbonization timelines, interim targets, and even what implementation in finance was supposed to look like – something that was clarified in more detail after alliances were joined. Amid growing legal threats from US politicians, widespread support for these coalitions ultimately collapsed. While hype cycles do not offer a complete explanation of all actors’ behavior, motivations, and engagement with net zero, the framework largely explains the rise and fragility of commitments observed since 2021.

In the next section, I discuss the differences and similarities between norm cascades and hype cycles. In the third section, I describe my empirical methodology and the results subsequently. Finally, in the conclusion, I discuss the implications of this research for scholars and practitioners.

Norm cascades and hype cycles

Norm cascades: a brief review

The norm cascade concept was introduced to IR by Martha Finnemore and Kathryn Sikkink in a 1998 International Organization article. In it, they pointed out that constructivism was, up until that point, better suited to explaining why ideas and norms persisted, and that new approaches were needed to develop theories of normative change.Footnote 11 In a now-canonical discussion, they used the concept of a norm cascade, adapted from behavioral economics and social psychology, to describe how agents could reconstitute stubborn normative orders.

They explain normative change in a three-stage process: (1) concerned norm entrepreneurs reframe issues strategically to persuade actors to change practices, standards, or behaviors; (2) norms ‘cascade’ as more actors are persuaded and peer pressure dynamics kick in, and (3) norms reach saturation in a relevant population and become taken for granted.Footnote 12 The subtle power of this explanation is in how it accommodates shifting mechanisms for norm adherence over time. In the first phase, the pressure and persuasive efforts from norm entrepreneurs lead actors to reconsider their behaviors and conform. In the second phase, change is driven by benchmarking behavior against peers and attempts to maintain the integrity of one’s identity in relation to evolving group standards.Footnote 13 At its zenith, international norms become thoroughly interwoven into salient identities in global society (modern, European, liberal, etc.) and take on a self-enforcing quality independent of agents.Footnote 14

The emphasis on identity and socialization was a critical contribution. Finnemore and Sikkink adopted the term from Cass Sunstein in his book, ‘Free Markets and Social Justice,’ yet Sunstein’s emphasis contained a sociologically thin description of actor motivations. While the core problematique also involved explaining normative change, Sunstein’s usage hinged on rational utility maximization.Footnote 15 As described, oppressive or socially damaging norms could be likened to a collective action problem: obeyed with some private dissatisfaction, but difficult to resist given the high costs of coordinating dissent. Norm entrepreneurs changed this dynamic by exploiting dissatisfaction, making defiance less costly, and clarifying the benefits of newer, alternative norms. When the costs and benefits of conformity reach parity, a tipping point could shift equilibria and lead to rapid bandwagoning that, like in the case of South African apartheid, results in sudden changes to seemingly impenetrable legal regimes.Footnote 16 Finnemore and Sikkink shifted the discussion by emphasizing the sociological and the degree to which collective behaviors relied on a sense of shared identity and alignment among group members. Doing so arguably cohered more closely with accumulating evidence for how international norms changed in global politics.

In the intellectual history of constructivism, norm cascades are, perhaps, treated as a necessary but insufficient step in understanding the socially constructed nature of international politics. Indeed, Martha Finnemore and Alexander WendtFootnote 17 describe their contributions in the 1990s as ‘old/structural’ in contrast to newer veins of scholarship, including practice or securitization theory. More recent approaches to norm constructivism have built on – but also challenged – this precedent by shifting attention to normative contestation, translation, and resistance by actors with differing identities, roles, and ideologies,Footnote 18 or by emphasizing a more relational or discursive approach empirically.Footnote 19 As HoffmannFootnote 20 describes, the trend in constructivism has generally been to move away from static notions of norms as regulative rules and toward a more dynamic, constitutive interpretation.

And yet, the norm cascade has remained remarkably robust as a description and explanation for normative change. It continues to wield explanatory power across a wide range of issue areas, encompassing the behavior of state and non-state actors alike. Examples span the formation of the International Criminal Court,Footnote 21 the proliferation of election monitoring by NGOs,Footnote 22 and corporate social responsibility initiatives.Footnote 23 The norm lifecycle is also frequently referenced to explain (or motivate) climate action across levels of analysis,Footnote 24 including to understand the emergence of net-zero commitments specifically.Footnote 25

Defining hype cycles

The potential problem for scholars is that it is possible to observe the same empirical pattern of the norm cascade over time – slow emergence and then rapid proliferation of a novel standard, expectation, or behavior among a group of actors with a shared identity – without the sequence of specific mechanisms that Finnemore and Sikkink outline, and even for issues with clear ethical or normative implications. The difference in mechanisms is critical for understanding the durability of group behavioral change, but parsing norm cascades from other patterns requires care. In this section, I build an argument for how a ‘hype cycle’ might be defined in contrast. I will argue that hype cycles involve three essential and distinctive conditions: (1) uncertainty or ambiguity limits the ability of norms or incentives to guide action; (2) in such cases, actors rely on the ‘heuristic of social proof’; and (3) time is limited, threatening actors with being labeled inactive or left behind. Once outlined, I will discuss how hype cycles overlap and contrast with norm cascades.

The first two conditions are closely related. The ‘heuristic of social proof,’ which essentially describes the degree to which decision-making is influenced by the observable actions of others, is a concept first coined by psychologist Robert Cialdini and later adopted by behavioral economists. One of its clearest expressions and applications is found in Timur Kuran’s 1995 book, Private Truths, Public Lies: The Social Consequences of Preference Falsification. In it, he explains that, given the limited cognitive capacities we wield as individuals, ‘free-riding on the knowledge of others is an essential vehicle.’Footnote 26 We may turn to experts to help, but we also turn to each other: our decisions can rely on ‘society’s collective judgment … if a great many people think in a particular way, they must know something we ourselves do not.’Footnote 27 In other words, the ‘proof’ that a course of action is the right one is defined by the extent to which others are doing it.

Heuristic-driven decision-making, as behavioral economists and psychologists would emphasize, reflects our psychological tendency toward ‘good enough’ solutions, especially when high levels of complexity or uncertainty limit our ability to determine the optimal path forward. Relatedly, ambiguity can imply the absence of strong normative directives and shared meaning, leading to conflicting interpretations that undermine the possibility of a consensus on how to behave.Footnote 28 If regulative norms are an adaptive response to intractable uncertainty overwhelming the possibility of calculative decision-making,Footnote 29 heuristic choices of this nature reflect a third-best approach when there are no clear guidelines, and our best bet may be to follow the crowd wherever it leads.

The heuristic of social proof, by definition, is a mechanism by which collective patterns of behavior emerge. Economists describe these collective patterns as ‘information cascades,’ where ‘a decision maker will act only on the information obtained from previous decisions.’Footnote 30 When one actor assumes another is making choices with full private information, the result is a self-reinforcing dynamic: greater adherence to specific courses of action strengthens its case with others. Scholars working on this topic have shown, theoretically and empirically, that the heuristic of social proof can operate as a mechanism of conformity independent of group-level and individual factors such as social influence, comfort with conformity, or fear of normative sanctions.Footnote 31

Like norm cascades, hype cycles can be catalyzed by the external interventions of issue entrepreneurs. As Kuran describes, groups may find social proof dynamics convenient for advancing their political interests: ‘Insofar as there are people trying to free ride on the thoughts of others, one can enhance the popularity of a position by offering convenient rides to it … making such rides available is essential to political success.’Footnote 32 As with norm dynamics more generally, successful issue entrepreneurs often wield the authority (political, epistemic, market-based, etc.) to be heard and to persuade. The difference for hype cycles may lie in the content of persuasion. In the absence of strong normative directives, advocacy might instead amplify perceptions of social proof (‘everyone else is doing it’). Or, issue entrepreneurs may use the tools of normative persuasion (and to successful effect for early adopters), yet for the general population, the messaging that gets across is about what others are doing, rather than the logic behind why they are doing it.

The fragility of information cascades stems from a vulnerability to new information disclosures. If a decision-making context is suddenly awash with clear facts about the costs, benefits, or risks associated with a particular course of action, actors may suddenly realize that the ‘wisdom of the crowd’ was folly. In turn, if the sudden availability of information reveals a yawning gap between the anticipated and actual benefits, adherents may experience ‘buyer’s remorse’ and change course. Information disclosures may also have a normative bent. If adherents find that a particularly nefarious actor champions the practice in question, or if it becomes apparent that the norm is linked to standards or practices that violate other, more valued principles, compliance may look less appealing.

The ability to change course, ultimately, is likely affected by the costs and sanctions associated with reversal. In institutional contexts with both relatively costless entry and exit (as with many voluntary transnational initiatives governing corporate behavior), hype cycle dynamics may be more likely. In contrast, when entry costs are high, it may be difficult for the general population to follow early adopters, thereby reducing the likelihood that a hype cycle will emerge in the first place. When exit or reversal costs are high, either because of sunk costs or the possibility of significant reputational consequences for noncompliance, actors may experience buyer’s remorse internally but nonetheless stay the course.

The idea of social proof overlaps with stage two of the norm cascade, in part. Finnemore and Sikkink acknowledge that socialization processes driven by legitimation, esteem, and conformity have psychological micro-foundations,Footnote 33 and that ‘in situations where the objective reality is ambiguous, individuals are even more likely to turn to “social reality” to form and evaluate their beliefs.’Footnote 34 Yet the motivation in stage two is also argued to be explicitly normative: even before a norm is taken for granted, momentum is driven forward when ‘leaders conform to norms in order to avoid the disapproval aroused by norm violation.’Footnote 35 In other words, behavior change is driven by the close connection between identity as a member of a group and the group’s evolving normative demands. This contrasts with hype cycles, where normative guidelines are weakly defined, and group membership is not obviously at stake. This is not to say that viral events driven by alternative mechanisms are void of normative content. The sudden rise of cryptocurrency meme coins is a domain of human activity shot through with norms, altogether made sensible by insider knowledge, identity, normative frameworks, and social cues. These structuring ideas give rise to a narrow set of choices in different circumstances. What makes something a hype cycle is precisely the absence of clear, specific normative directives to sustain compliance amid rising costs or risks.

However, there is a weak instantiation of group membership that defines hype cycles; it is something more sociological than the economic description of information cascades allows. This relates to the third defining feature of hype cycles: a limited window of time to act and the ‘fear of missing out’ (FOMO).Footnote 36 The urgency of FOMO in a hype cycle is driven, as I’ll argue, by actors’ avoidance of identification as non-participants as the cycle accelerates. If the wisdom of the crowd is to do A, then, as the heuristic of social proof would dictate, it looks increasingly unwise to do B. As such, and in addition to the anticipated benefits of being rewarded for taking a certain action, doing A is a kind of conspicuous consumption or hedge against being identified as inactive or behind the curve. These concerns may not rise to the level of legitimation motives that drive socialization in norm cascades, but being perceived as slow or behind the times may affect one’s reputation. For competing businesses, reputation is implicated in tangible concerns such as client acquisition and employee retention.

Time matters explicitly because, as the adoption rate for a given behavior increases, the perceived risk of being left out also increases. The more compressed the timeline seems, or the more visible the deadline for joining in, the more immediate the risk looms. As a result, creating a sense of urgency can be a useful strategy for issue entrepreneurs; advocates can advance ‘temporal focal points’ that can catalyze collective action.Footnote 37 Emphasizing deadlines and a lack of time is a kind of temporality that makes possible and gives meaning to specific patterns of behavior.Footnote 38 Without a sense of urgency, conditions of ambiguity about novel standards or expectations may lead actors to cling to precedent, reinforcing path dependence rather than precipitating new collective behaviors.Footnote 39

Further distinguishing hype cycles

With a set of defining characteristics laid out (social proof, uncertainty, time limits), I make several additional clarifications and distinctions relevant to the empirical task of identifying hype cycles. First, I discuss non-linear patterns of behavior that involve rational decision-making and explain why these phenomena have different implications. Second, I describe why hype cycles are not just failed norm cascades. Finally, I briefly articulate the ideal-typical nature of hype cycles as a conceptual construction.

Non-linear social behaviors can have rational foundations that offer an alternative explanation to hype cycles and norm cascades. For instance, network effects operate on the principle that individuals gain from a standard or technology as a function of the number of other actors involved, leading to accelerating convergence on one choice among alternatives.Footnote 40 In later stages, network effects consolidate as switching costs become prohibitively expensive.Footnote 41 The overall result is a parallel empirical pattern of slow beginnings but accelerating movement toward shared and universal participation. Similarly, diffusion can also lead to rapid uptake of new practices, policies, or technologies across a social network with non-linear dynamics. Typically, these explanations rest on the assumption of complete information and actors capable of means-ends calculation. These patterns diverge from hype cycles because ambiguity and uncertainty defy the informational requirements of idealized rational decision-making that otherwise lead to the realization of common standards.Footnote 42 Similarly, innovations do not diffuse if they fail to offer an unambiguous improvement over the existing suite of choices available to an agent.Footnote 43

Are hype cycles merely failed norm cascades? As I have argued, hype cycles entail an inherent fragility: regression to the mean, expansion and retraction, or cycling back to the point of origin, with the possibility of repetition. But hype cycles are not necessarily destined to collapse. This creates an additional empirical challenge, where durable social change and consolidation might result from weakly entrenched incentives and hype dynamics early on. If and when information is disclosed and actors start to tally the benefits and costs, they may find the wisdom of the crowd reliable, and no one experiences buyer’s remorse. Or, no full accounting emerges, but the novel behavior in question persists and becomes taken for granted, despite its tenuous origins, through repetition, habit, or momentum. The transition from cryptocurrencies as a niche medium of exchange for illicit dark web transactions to celebrity-endorsed pump-and-dump schemes and finally to a topic of serious debate among central bankers is but one example.Footnote 44

At the same time, and perhaps especially from the perspective of well-intentioned issue entrepreneurs, a hype cycle might reflect a failed effort to precipitate a norm cascade. There are certainly cases where this might be true, and both patterns can start from similar initial conditions. For example, norm entrepreneurs may frame and develop strong arguments for a new standard of behavior, and early adopters may be motivated to engage because they perceive its inherent or instrumental value. However, as the number of adherents grows, the salient justification may become ‘if other people are doing it, we probably should be doing it too.’ The norm in question does not shape how actors see themselves as members of peer groups. Social proof heuristics lack the strong legitimation and esteem concerns that otherwise define the socialization stage of the norm cascade.

Conversely, norm cascades can fail for other reasons. As Finnemore and SikkinkFootnote 45 describe in their review of the constructivist literature, momentum can falter because early adopters lack status, the norm itself may have limited appeal, or the norm awkwardly fits with the existing ideational landscape. As more recent scholarship in this area has shown, norm cascade processes might precipitate genuine socialization dynamics, but are confronted by stringent efforts to contest the norm, inhibiting internalization. None of these potential causes of failure requires uncertainty, social proof dynamics, or time limits. Ultimately, regardless of outcome, what distinguishes norm cascades and hype cycles are the mechanisms and conditions that motivate actors as momentum builds (see Table 1).

Logics of action across frameworks

As a final point, and in reflecting on the realities of the GFANZ case as I describe it here, a hype cycle has an ideal-typical aspect. In any social, political, or economic phenomenon driven by mass behaviors, actors are diversely constituted and motivated. However, an overarching tendency toward one analytical story – hype cycles, norm cascades, or some other pattern – can tell us a lot about what to expect.Footnote 46

Methods

At a general level, parsing a hype cycle from a norm cascade involves empirically identifying specific mechanisms encompassed by its necessary conditions. First, we should observe ambiguity or uncertainty that clouds the possibility of both calculative action and normative directives, as reflected in deliberations of the target population. Second, there should be direct evidence that decision-makers refer to others’ actions in making their own determinations, given these conditions. Third, there needs to be some indication that decisions were being made in a time-compressed or time-constrained manner. Finally, some longitudinal evidence of impermanence or decline arriving after information disclosures strengthens the certainty of the diagnosis.

To conduct this analysis for GFANZ, I rely on 23 semi-structured interviews conducted in person and via Zoom between September 2022 and February 2023. Appendix A provides further details, but the pool of respondents included representatives from asset managers, banks, insurance companies, NGOs party to GFANZ-affiliated initiatives, and international organizations working in the green finance space. Firms were largely headquartered in the UK and France, providing some ability to account for variation in institutional and regulatory factors. Given the near-zero response rate from US firms, American NGOs helped provide a North American perspective. Evaluations of press releases, framework publications, news articles, and initiative reports were also reviewed as supplementary evidence.

Interviews focus on three associated GFANZ initiatives: The NZIA, the NZAM, and the NZBA. In each case, I test for the presence or absence of relevant conditions.

Note that the objective, methodologically, is to establish the plausibility of hype cycles as an explanation for rapid behavioral change, but not to definitively establish this as the only explanation for understanding the motivation of actors, nor to test a hypothesis per se. Implications for generalization follow.

The case of GFANZ

The emergence of GFANZ

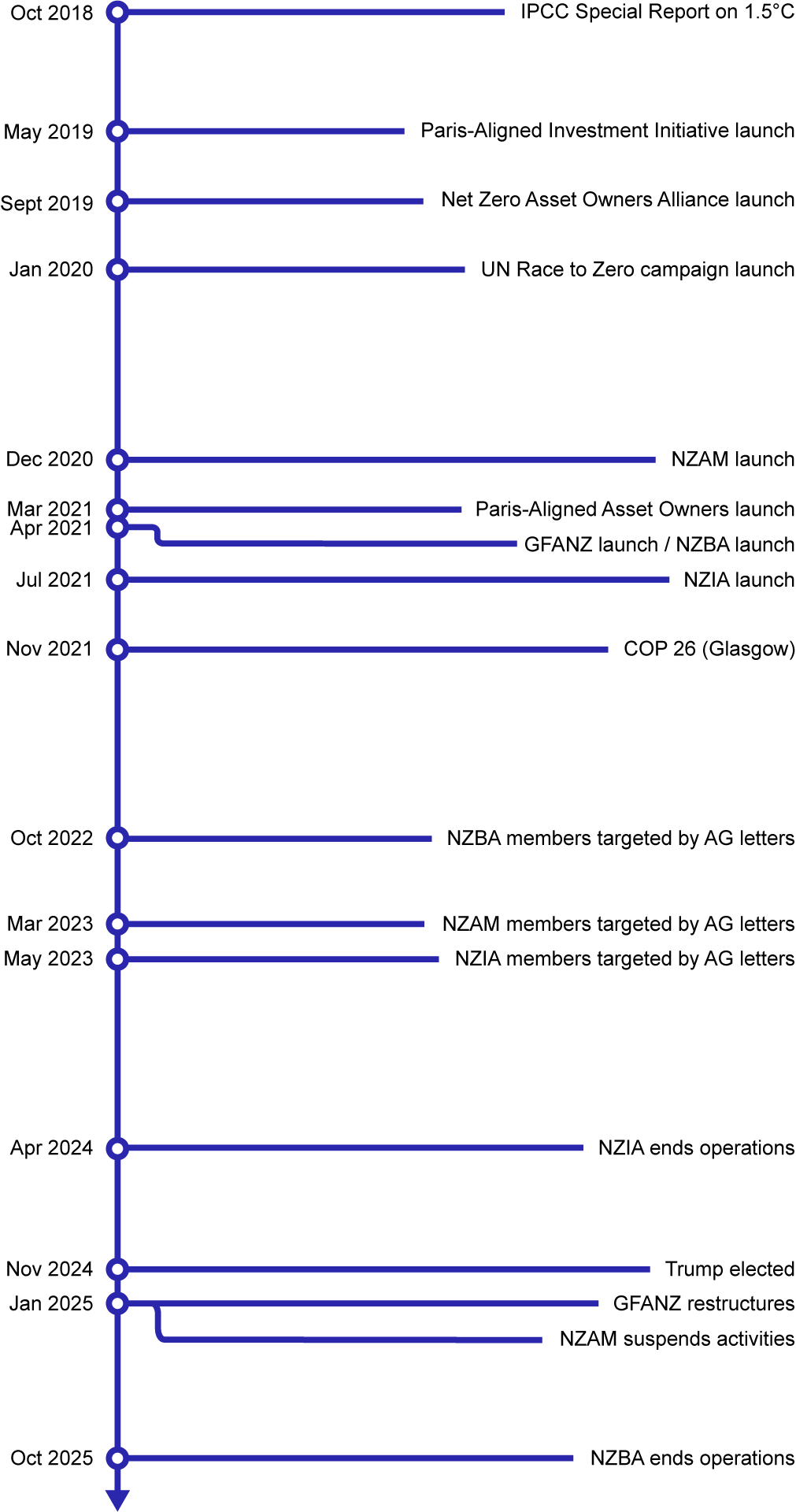

While financial actors have long been partnering with international organizations and NGOs to navigate the rising risks associated with a changing climate, the emergence of net-zero targets is a unique product of the Paris Agreement’s aftermath, and the 2018 Intergovernmental Panel on Climate Change (IPCC) Special Report on Global Warming of 1.5°C specifically. In the latter case, scientific modeling suggested that the Paris Agreement’s temperature goals of 1.5°C of global warming could in part be achieved by reducing carbon dioxide emissions to net zero by 2050.Footnote 47 A growing consensus supported the notion that net zero would be a pivotal benchmark for states and non-state actors alike – though there was some ambiguity about implementation and tracking progress.Footnote 48 International organizations were quick to use the 1.5°C target and net zero to launch mobilizing efforts for companies, including the UN Global Compact’s ‘Business Ambition for 1.5C’ campaign in 2019 and the UN Climate Champion’s ‘Race to Zero’ campaign in 2020.

In finance, institutional investors such as pension funds were early adopters of net zero. The predominantly European and UK-based Institutional Investor Group on Climate Change (IIGCC) formed the Paris-Aligned Investment Initiative in 2019, which published a ‘Net Zero Investment Framework,’ and in 2021, expanded to build out a signatory commitment platform with other investor networks called the Paris-Aligned Asset Owners. In parallel, the United Nations Environment Programme Finance Initiative (UNEP FI) and the UN Principles for Responsible Investment (UN PRI) leveraged their own institutional investor networks to launch the Net-Zero Asset Owners Alliance in September 2019 at the UN Secretary-General’s Climate Summit.Footnote 49 Asset managers, in partnership with many of the same early-moving institutional investor networks and NGOs, committed to their own net-zero platform, NZAM, announced in December 2020.

After the downshifting of activity in the first year of the COVID-19 pandemic, climate summitry rebounded in 2021. COP 26 in Glasgow was the fifth anniversary of the Paris Agreement, and the UK, as host, put special emphasis on mobilizing finance and ‘unleashing’ private capital for net zero.Footnote 50 This emphasis was evident earlier at COP 25, when the UK’s COP 26 Presidency co-hosted the launch of NZAM, and the CEO of one of NZAM’s founding signatories, Michelle Scrimgeour, joined the UK’s COP 26 Business Leadership Group.Footnote 51

2021 saw a rapid succession of UK-led expansions to net zero in finance. In April, the GFANZ was created, chaired by former Financial Stability Board Chair and Bank of England Governor Mark Carney, and co-launched by the UK COP 26 Presidency. The operational goal was to consolidate a coalition of financial institutions following the broader UN ‘Race to Zero’ campaign. For Carney’s part, his chairship dovetailed with his roles as the UN Special Envoy for Climate Action and Finance and the UK Prime Minister’s Financial Advisor for COP 26. Though GFANZ is a self-described ‘stand-alone, private-sector group,’Footnote 52 it is clear that its objectives were (at least initially) intended to galvanize action toward achieving the UK’s goals for COP 26. That point was further made clear by Nigel Topping’s position as a member of GFANZ’s ‘Principals Group,’ then a UN High-Level Climate Action Champion at COP 26, appointed by the UK Prime Minister in 2020.

The creation of GFANZ catalyzed the formation of several new, additional net-zero platforms. The NZBA was launched alongside GFANZ at the 2021 Leaders Summit on Climate, convened by former US President Joe Biden that April. As GFANZ conveners described, ‘this momentum continued to accelerate,’ resulting in additional initiatives, including the NZIA and similar platforms for consultants and financial service providers.Footnote 53 UNEP FI was critical to banking and insurance as platforms were built on its existing private sector networks: the Principles for Responsible Banking and the Principles for Sustainable Insurance, respectively. As a result of this push for expanding the umbrella of net zero, Carney and Rishi Sunak, then Chancellor of the Exchequer, were able to take some credit publicly for assembling US$130 trillion of assets under management, at least nominally committed to financing climate action, by the commencement of COP 26 in Glasgow that November. The UK government celebrated this headline figure as a major accomplishment.

Constrained timelines and social proof

For banking, insurance, and asset management, participation among companies exploded in the run-up to COP 26. NZAM launched with 30 founding investor signatories in December 2020. One year later, their numbers swelled to 220 members, a 633.3% increase.Footnote 54 Between the founding of the NZBA in April 2021 and COP 26, member banks grew from 43 original signatories to 92. For NZIA, between July 2021 and November, growth was more modest but with a shorter runway: from 8 founders to 13 insurers and reinsurers. The initiatives continued to grow after Glasgow, but much of the expansion had occurred during 2021. By roughly the end of 2024, NZAM had 325 participants, with 144 for NZBA and 30 for NZIA at its height.Footnote 55

Behind the broad trends, the UK government’s focus on finance and climate change, building toward the COP 26 deadline, mattered for companies. For asset managers, even though NZAM was launched a year prior, the drive toward COP 26 heightened the salience of membership, especially for companies with a UK footprint – a ‘no-brainer’ as the summit approached and GFANZ gained attention.Footnote 56 Mark Carney’s extensive leadership in climate and financeFootnote 57 and UNEP FI’s orchestrationFootnote 58 provided backing that boosted the standing and salience of the respective initiatives.Footnote 59 Keeping pace with industry trends was also important for complying with evolving expectations from pension clientsFootnote 60 and for avoiding being identified as out of step with global goals such as the Paris Agreement.Footnote 61 The actions of particularly influential market leaders were also catalytic: not only was BlackRock CEO Larry Fink part of GFANZ’s ‘Principals Group,’ but the company’s participation in NZAM drew significant attention from others in the industry.Footnote 62

Social proof heuristics were evident across sectoral initiatives. In asset management, companies reportedly looked to one another, saw a growing trend toward net-zero commitments, and recognized the possibility that they might be left behind.Footnote 63 Ultimately, as one banking representative stated, ‘There was a hype … everybody was jumping on the bandwagon.’Footnote 64 For banking, the role of celebrity boosters such as Mark Carney in the run-up to COP 26 was also galvanizing, overcoming initial concerns that taking on net zero might involve costly failures or competitive disadvantages if undertaken unilaterally.Footnote 65 Similarly, for insurance, the NZIA was seen as a tool for managing one’s reputation with peers and stakeholders as the initiative gained momentum.Footnote 66 As Director of Environmental, Social, and Governance (ESG)Footnote 67 for Prudential Plc, Kerry Adams-Strump noted more generally, ‘We certainly do not want to be the ones that are seen to not be doing or playing our part.’Footnote 68

In general, climate summit deadlines around which issue entrepreneurs could mobilize financial institutions clearly leveraged growing social proof heuristics and concern around being out of step. Yet it is important to recognize that, across sectors, other motivations were also important for financial institutions. Insurers felt pressure from NGOs scrutinizing dealings with fossil fuel companies.Footnote 69 Banks with long histories of working on corporate sustainability saw it as an opportunity to fulfill their sector’s social and environmental responsibilities.Footnote 70 Smaller, sustainability-minded banks saw the NZBA as an occasion to increase their impact by helping larger, more conservative institutions on their journeys.Footnote 71 Certain collective action dynamics were also important, in which taking on costly commitments individually might lead to competitive disadvantages or limited impact.Footnote 72 Nonetheless, observers noted the importance of peer benchmarking across the NZAM, NZIA, and NZBA in the run-up to COP 26, especially.

Ambiguity and uncertainty

At the outset of GFANZ-associated initiatives, the costs and benefits of participation and commitment to net zero were unclear. Indeed, in the run-up to COP 26, net zero in practice was more of a ‘mantra’ in the financial industry than a scientifically grounded or agreed-upon set of prescriptions.Footnote 73 In part, this reflected the fact that many new members of net-zero platforms lacked the capacity to navigate multi-decadal strategies for assessing and reducing the indirect emissions associated with complex financing and insurance activities.Footnote 74 As a result, GFANZ partner organizations, including those in the non-profit sector, played a critical role in backstopping membership by facilitating peer-to-peer learning opportunities in working groups and providing technical assistance. Though whole-of-company commitments were a significant departure from norms and standards governing private finance and climate change prior to that point, the perception that net zero was a ‘natural evolution’ and involved many familiar and trusted authorities in the space was important.Footnote 75 In other words, the feasibility of net zero was frequently presumed, rather than assessed.

Indeed, net-zero initiatives were operating at the methodological frontier for the financial industry. The NZIA, for instance, was defining what ‘insured emissions’ meant for the first time. Before that point, insurers were mostly acting on climate change in their secondary role as institutional investors, rather than as underwriters. A ‘Target Setting Protocol’ was released in 2023, following consultation and involvement from NZIA signatories over a nearly two-year process.Footnote 76 Insurers were learning and doing at the same time,Footnote 77 navigating ambiguities that, in some cases, persisted despite the NZIA’s efforts.Footnote 78

The NZBA, for its part, struggled to arrive at a framework for net zero that did not scare off member banks with significant ties to the fossil fuel industry, attempting to balance credibility around what net zero meant for banking with membership accessibility.Footnote 79 The balance of flexibility and prescription was also important in the NZBA due to varied experience and familiarity with approaches such as carbon accounting,Footnote 80 which underpin the assessment of net-zero alignment.Footnote 81 This systematic difficulty is reflected in the flexibility of NZBA requirements early on, which stated that targets ‘should include their clients’ Scope 1, 2, and 3 emissions where significant and where data allows.’Footnote 82

Though climate-sensitive investing has a longer history, even for NZAM, the initial requirements of a net-zero commitment were nonetheless riddled with unanswered methodological questions. Debates emerged over whether absolute portfolio emissions reductions would cut off asset managers from engaging as shareholders and from prodding companies in the real economy to improve their environmental footprint.Footnote 83 Certain assets, such as derivatives, did not fit obviously into a carbon accounting framework at all.Footnote 84

Across sectors, the rigor required for planning for and implementing net-zero commitments was unanticipated.Footnote 85 One ESG professional at a Dutch bank explained that they were unsure whether they could live up to the commitment at launch and that, in retrospect, many banks were unaware of the implications of signing up.Footnote 86 Participants were largely engaging in a learning-by-doing process,Footnote 87 including navigating what net zero even meant for day-to-day operations. For one insurer, even after the frameworks were ultimately settled, the implications for whole-of-organization operations remained a matter of experimentation.Footnote 88 Information and data gaps on the emissions of underlying assets were also systematic,Footnote 89 limiting most companies’ ability to discern their direct and indirect emissions and, thus, the real costs associated with decarbonization.

Information disclosures and decline

Social proof dynamics and information cascades are sensitive to information disclosure. Net-zero initiatives in finance arguably experienced two episodes of disclosure that precipitated ‘buyer’s remorse’ and reinforced the conclusion that GFANZ alliances were, in part, driven by hype cycle dynamics.

First, processes of learning-by-doing elucidated once-obscured details about what net zero would entail in practice. As described, signing up for net-zero initiatives was relatively easy and required little initial preparation. Once companies began working through the requirements and implications of targets, the difficulty and costs of doing so became increasingly evident.Footnote 90

Second, the ESG backlash made visible costs that companies did not anticipate. As investigations have since shown, the momentum of net zero in finance and its implications for phasing out coal investment precipitated a coordinated political response among fossil fuel executives and conservative American elected officials at the state level.Footnote 91 The retaliation included a suite of antagonistic legislative proposals, as well as threats from groups of state Attorneys General accusing GFANZ initiatives and their participants of violating US antitrust law through coordinated market boycotts. Accusatory letter-writing exercises began in late 2021, with intensifying pressure in 2022 and 2023, as the anti-ESG campaign escalated into civil investigative demands issued against US banks, a panoply of state-level legislation, and other forms of legal harassment and political targeting. As a result, companies began withdrawing from net-zero initiatives, especially US-headquartered companies and non-US companies with significant operational footprints in the United States.Footnote 92

The consequences were widely felt. The NZIA lost over half its members after antitrust allegations were leveled in May 2023 and ultimately ceased operations in April 2024. By contrast, the volume of departures as a percentage of total membership was more modest in asset management and banking (roughly 10% of NZAM and 6% of NZBA signatories) but accelerated in 2025. The reelection of Donald Trump in November 2024 only promised further politicization and legal harassment (see Figure 1), leading to a mass exodus. For the NZBA, the departure of some of the largest global banks by market capitalization – including Morgan Stanley, Goldman Sachs, JPMorgan Chase, HSBC, RBC, and TD – precipitated a member-driven process to end operations by October 2025.Footnote 93 Similarly, NZAM suspended activities in January 2025 after its most prominent member, BlackRock, left the alliance.Footnote 94 NZAM is reformulating its methodologies and standards, though it does not appear to be planning its termination at the time of writing. In general, politicization was not a cost that companies fully anticipated, and for many, it forced internal reevaluations. As of January 2025, GFANZ has since refocused on mobilizing private capital for decarbonization in emerging economies, distancing itself from its original convening role for membership-based alliances.Footnote 95

Timeline of Net Zero in finance.

Yet an important possibility remains. Might companies comply with net-zero norms individually, despite the destabilization of public-facing platforms? Might processes of socialization and internalization have occurred before this collapse in membership, such that net zero has become a defining feature of what it means to be an international financial institution? While ‘greenhushing’ and quietly adhering to environmental norms amid political antagonism are arguably now taking place in the US private sector,Footnote 96 the evidence does not suggest this is widely the case in finance. In banking, according to a network of environmental NGOs, financing flows to the fossil fuel industry have been systematically increasing across the world’s largest lenders. This trend persisted during the life of the NZBA – including during its politicization – for banks in China, the UK, France, Spain, Japan, and the US.Footnote 97 With a few important exceptions (Generali, Allianz, AXA), major insurers have received similarly poor evaluations with respect to aligning underwriting and investing with climate mitigation in recent years, both before and after NZIA membership.Footnote 98 The view is somewhat more sanguine for investors and asset managers, though after an internal review with signatory members, NZAM has watered down its framework, eliminating the target date of net zero by 2050.Footnote 99

In summary, with both sensitivity to implementation costs and vulnerability to the ESG backlash, the effect of information disclosure arguably reflects the absence of systematic norm internalization that defines norm cascades after successful stages of persuasion and socialization.

Discussion

The essential question is whether the evidence can establish that a hype cycle dynamic characterizes GFANZ and its alliances. As I argued in the previous section, a hype cycle has three important observable implications: prevailing ambiguity and/or an inability to make calculative decisions; evidence that decision-makers use the actions of others as social proof under such conditions; and a time-constrained decision-making environment. An important additional consideration is the conditions precipitating the observed decline. Based on these criteria and my assessment of the evidence, the GFANZ initiatives examined – NZAM, NZBA, and NZIA – all illustrate hype cycle dynamics.

Yet, from a diagnostic point of view, it should also be clear that a given case is not merely a norm cascade gone awry. I consider a handful of factors here, including the effectiveness of issue entrepreneurs, the dynamics of norm contestation that might otherwise explain interruption, and the qualities of the norm of net zero itself.

First, the problem was not that issue entrepreneurs were insufficiently persuasive or effective at early mobilization: at its height, NZBA’s collective membership swelled to a scale where, for instance, members represented 80% of all systemically important banks worldwide.Footnote 100 Second, companies backtracked under political pressure, but not necessarily because antagonists successfully contested a norm. The ESG backlash was framed by its campaigners in normative terms, yet its political logic was entirely material, using legal and financial punishments to shift behavior by brute force (regardless of the underlying legal validity of the antitrust accusations), rather than through contention, objection, ignoring, or questioning to challenge the legitimacy of net-zero standards discursively.Footnote 101 The quality of net zero as a norm in isolation does not seem to be the core issue either, given widespread acceptance by governments and markets, its linkages to the Paris Agreement’s temperature goals, and its reinforcement by IPCC reports and scientific consensus – altogether, a resilience-providing normative structure.Footnote 102 In sum, it is not clear that a norm cascade failed per se; instead, the necessary conditions for one never quite materialized in the financial sector.

Based on the evidence and discussion, I therefore conclude that net-zero initiatives in finance exhibited hype cycle dynamics. Yet there are several important caveats. First, an assessment of group-level dynamics does not mean that all actors operated exclusively on the heuristic of social proof. Early movers and leaders at the climate-finance nexus were, in many cases, more clear-eyed about the instrumental value of methodological development, industry standards, and the importance of preparing for alignment with future policy trajectories. Still more felt pressure from stakeholders to comply, as opposed to peers. Second, in jurisdictions such as the UK and the EU, regulatory developments and public policy were pointing strongly toward both decarbonization and additional reporting burdens for companies on climate-related risks.Footnote 103 Government signals might have lessened some aspects of both ambiguity and uncertainty for those in forward-thinking jurisdictions, where navigating new voluntary standards would likely tie into regulatory compliance. Third, actors with more experience and knowledge in ‘green financing’ may not have confronted net zero with the same sense of uncertainty as others. At the same time, the delayed arrival of frameworks for operationalizing net zero, as discussed in the previous section, indicates that implementation was genuinely novel in areas such as insurance underwriting.

These caveats call for some theoretical nuance. It is fundamental to recognize that hype cycles are ideal-typical descriptions of group-level behavior, not a complete accounting of actor motivations. Instead, the conditions that constitute a hype cycle and how widespread they are in a given population are warnings about the durability of collective behavioral change. The severity of the warning and risk of collapse will undoubtedly vary from case to case. Further, an exogenous shock in something like the costs of compliance – such as the election of Donald Trump, which triggered a deluge of defections from initiatives such as the NZBAFootnote 104 – does not mean that all decisions are based on cost–benefit calculations at all times. As stated, information disclosures that lead to behavioral collapses do so precisely because a cost–benefit (or normative) accounting ex post does not align with expectations derived from social proof ex ante. The value of the hype cycle framework, theoretically, lies in explaining behavioral trends across the proliferation and decline of standards or behaviors, where the logic of action might shift.

Conclusion

Why did GFANZ, an umbrella organization mobilizing financial industry actors to commit to rapid greenhouse gas emissions reductions, emerge so quickly and with such enthusiasm, yet falter under relatively mild political pressure? To understand this pattern, I argue that we need new frameworks for thinking about mass social behaviors in international affairs. While the norm cascade is a well-established theory for explaining similar empirical patterns of normative emergence and consolidation, in some cases, norm-compliant behavior spreads widely without the socialization processes that norm cascades typically entail. In these instances, different mechanisms may be driving rapid change. As a response, I introduce the concept of a ‘hype cycle’ in which, under conditions of uncertainty and ambiguity, actors look to one another for evidence on how to act; i.e., a heuristic of social proof. Especially when the decision to participate in a group behavior is time-limited, actors fear being perceived as falling behind. In cases where information is later made available about the ultimate costs, benefits, or appropriateness of a course of action, and where the resulting accounting countervails initial expectations about the benefits of group behaviors, ‘buyer’s remorse’ collapses the case for participation and induces fragility that we do not observe in norm cascades. Institutional factors may also play an accelerating role: low costs of entry and exit from commitments likely increase the likelihood of hype cycle dynamics.

As an abductive theoretical project, these conceptual distinctions illuminate the case of net-zero initiatives in finance once under the GFANZ umbrella. With qualitative data, I evaluate the presence or absence of key conditions of possibility and mechanisms for hype cycles across the NZBA, the NZAM, and the NZIA. Across cases, actors were generally uncertain about what they were signing up for and the long-term implications of implementing net zero. The decisions of peers played an important role for many in ultimately deciding to join alliances. The run-up to COP 26 in Glasgow, Scotland, where finance was being platformed as a climate solution, and the surrounding endorsements and fanfare created a sense of urgency to participate in order to avoid being identified as a laggard. Finally, once actors began implementing commitments, many encountered unexpectedly demanding requirements for data collection and financial reallocation. The emergence of the ESG backlash and legal threats against alliances and companies, as a second kind of disclosure about commitment costs, ultimately led to mass defections and the reorganization or termination of alliances. Though I find confirmatory evidence in all cases, I note the diversity of actors’ motivations and the genuine commitment of issue entrepreneurs and many companies to addressing climate risk.

Because the outcome of this analysis is theory creation rather than validation or testing, the extent to which hype cycles predominate in international affairs requires further study. At the same time, potential cases are relatively easy to conjure. Similar dynamics may apply to the ‘empty institutions’ following G20 conferences that track popular issues but often lack substance,Footnote 105 or to the Responsibility to Protect norm that some human rights advocates embrace but that has arguably failed to deliver results.Footnote 106 These examples involve both state and non-state actors across different issue areas: I expect hype cycle dynamics to apply at multiple levels of analysis and across domains of international affairs, much as norm cascades do. Of course, further empirical validation will be the judge, ultimately.

The discussion contributes to and complements a rich literature on norm contestation and the failure of normative change. Scholars have argued that new norms depend on precedent successes in issue emergence that are not guaranteed in later stages,Footnote 107 that normative and institutional structures defining world politics endogenously produce contestation,Footnote 108 and that the opportunity to contest norms can be intrinsic to the legitimacy of norms themselves.Footnote 109 Norm ‘antipreneurs’Footnote 110 are easy enough to find across issue areas, and even norm adherents themselves can compromise or transfigure deeply established principles through incremental changes in practices.Footnote 111 What the concept of hype cycles adds to this conversation is a recognition that even with similar empirical signatures, conditions, and processes, efforts to catalyze normative change can fail for reasons independent of a norm’s fit with broader structures or challenges to its legitimacy. In other words, the question raised here is not only ‘when and under what conditions are norms contested?’ but also ‘how do we know when normative change is actually at stake?’

Answering this question is crucial, especially for issue advocates and practitioners. If underlying conditions resemble a hype cycle rather than a norm cascade, preparing for instability in support may be necessary. Most likely, the circumstances observed in finance may have benefited from less bullishness on the part of GFANZ’s founders and boosters, who claimed that these alliances were ‘unleashing’ private capital for net zero,Footnote 112 and that signatories would ‘deliver the estimated $100 trillion of finance needed for net zero over the next three decades.’Footnote 113 Such rhetoric may have been galvanizing but also likely created hype within and beyond the financial industry, as expectations became untethered from looming implementation challenges and political risk. More generally, gaining critical mass rapidly may be an enticing prospect for global governance contexts where coercive regulatory power is limited, compliance is voluntary, and impact is bottlenecked by scale and collective action. However, there are likely to be tradeoffs, where rapid growth comes at the cost of slower socialization dynamics that otherwise consolidate deeper regulative norms and standards. Some of the reported difficulties in strengthening net-zero commitments among states and companies in other sectors may reflect such a dilemma.Footnote 114

On the other hand, and while the collapse of a hype cycle might depress progress, net zero in finance is, among other things, a governance experiment. The same conditions of uncertainty and ambiguity that seed the possibility of hype cycles also necessitate experimentation at some level.Footnote 115 Inevitably, by definition, some experiments fail. How we judge experiments depends most on what we learn in the aftermath, given that resulting innovations can nevertheless lower the costs of future action,Footnote 116 disrupt the status quo in unexpected ways,Footnote 117 or gestate ideas for use in more amenable times.Footnote 118 Indeed, even in the absence of ongoing membership platforms, initiatives nevertheless developed a set of standards, informed by market actors, that make some progress toward addressing the challenges of implementing climate mitigation targets in abstract areas such as bank loans and car insurance. Those contributions may still prove catalytic within the broader, still-surviving institutional governance complex of ‘sustainable finance,’Footnote 119 regardless of whether they originated in a hype cycle or a norm cascade. At the same time, and more skeptically, the biggest lesson from GFANZ may be about the political economy of the climate transition more broadly: this episode suggests that the private sector will not sustain a commitment to finance the green transition, nor publicly commit to doing so, if it is costly, unprofitable, or politically inconvenient.

Acknowledgments

A previous version of this paper was presented at ISA 2024 and the International Theory ISA Pre-Conference Workshop in 2025. Thanks to workshop and panel participants for their feedback, and especially to Mark Raymond, David Welch, Stefano Ponte, and Steven Bernstein, who shared very helpful comments and thoughts on earlier versions of this paper.

Appendix A: Semi-structured interviews

Interview 1: Confidential Interview, Senior Manager, Asset Management Arm of Multinational Bank. London, UK. September 2022.

Interview 2: Confidential Interview, Former Advisor, The Climate Bonds Initiative. Online.

Interview 3: Confidential Interview, Program lead, Intergovernmental organization. Online.

Interview 4: Blandine Machabert, ESG Investment Specialist, RAISE France. Paris, France. October 2022.

Interview 5: Confidential Interview, Project Manager, sustainable finance NGO. Online.

Interview 6: Maria Lombardo, Head of ESG Advisory, Standard Chartered Bank. London, UK, September 2022.

Interview 7: Confidential Interview, Analyst, Affirmative Asset Management. London, UK, September 2022.

Interview 8: Confidential Interview, CEO, Sustainable Finance NGO. London, UK, September 2022.

Interview 9: Caroline Le Meaux, Head of ESG Research and Engagement, Amundi Asset Management. Paris, France, October 2022.

Interview 10: E. Colgan Powell, Manager, Ceres Investor Network. Online. January 2023.

Interview 11: Confidential Interview, Project Manager, Ceres. Online. January 2023.

Interview 12: Iancu Daramus, Responsible Investment Associate, Fulcrum Asset Management. London, UK. September 2022.

Interview 13: Anne-Claire Imperiale, Head of ESG, Sycamore Asset Management. Paris, France. October 2022.

Interview 14: Confidential Interview, Senior-Level executive, AXA Global. Online, October 2022.

Interview 15: Adam Matthews, Head of Climate Division, Church of England Pension Fund. Online, October 2022.

Interview 16: Interview, Michèle Lacroix, Group Head of Sustainability, SCOR. Online, October 2022.

Interview 17: Alex Hindson, former Chief Risk and Sustainability Officer, Argo Global. In-person, London, UK. September 21, 2022.

Interview 18: Kerry Adams-Strump, Director of Group ESG, Prudential Plc. Online. August 16, 2022.

Interview 19: Confidential Interview, former investment consultant, Aon. Online. March 2023.

Interview 20: Confidential Interview, Executive, Zurich Insurance Group. Online. September 2022.

Interview 21: Confidential Interview, Senior ESG Professional, Dutch Bank. Online. February 2023.

Interview 22: Confidential Interview, Executive, North American Bank. Online. April 2023.

Interview 23: Denisa Avermaete, Senior Policy Advisor, European Banking Federation. Online. January 31, 2023.

Open access

Open access