On May 21, 2013, the Permanent Subcommittee on Investigations of the US Senate Homeland Security and Government Affairs Committee held a hearing into an alleged tax avoidance scheme perpetrated by the Apple group. One of the more outrageous tactics used by Apple, the committee concluded, was to set up two Irish affiliates in such a way that they ended up being tax residents neither of Ireland nor of the United States. The affiliates reported a net income of US$30 billion and US$74 billion respectively between 2009 and 2012, more than a quarter of Apple’s annual income during those years. Yet they ‘declined to declare any tax residence, filed no corporate income tax return, and paid no corporate income taxes to any national government for three years’ (Levin et al., Reference Levin, Pryor, Landrieu, Mccaskill, Tester, Baldwin, Heitkamp, Mccain, Johnson, Portman, Paul, Ayotte, Bean, Roach, Katz, Goshorn, Kerner, Hall, Patout, Wittman and Robertson2013, 2).

An even more elaborate scheme was set up by another paragon of contemporary capitalism, Google. In this scheme, known as Double Irish, Dutch Sandwich (Beebeejaun, Reference Beebeejaun2020; Darby and Lemaster, Reference Darby and Lemaster2007), Google transferred ownership of intellectual rights over vital patents and trademarks to a subsidiary incorporated in Ireland (Burke-Kennedy, Reference Burke-Kennedy2020; House of Commons, Committee of Public Accounts, 2013; Zucman, 2015). That subsidiary, although registered in Ireland, was domiciled in Bermuda, a zero-tax jurisdiction. The scheme ensured Google paid almost no tax at all. A variant of the scheme known as Double Irish and Single Malt (Coyle, Reference Coyle2017; Kelly, Reference Kelly2015; Loomis, Reference Loomis2011) emerged recently, replacing the Netherlands with Malta.

The discovery of the tactics employed by Apple, Google, Amazon, and many other leading corporate groups opened a Pandora’s box, revealing a shady world of modern corporate tax and regulatory planning consisting of an unknown number of schemes described by corporate lawyers as jurisdictional arbitrage (Avi-Yonah, Reference Avi-Yonah2017; Kerber, Reference Kerber1999; Marian, Reference Marian2013; Panayi, Reference Panayi2006a, Reference Panayi2006b, Reference Panayi2015). Jurisdictional arbitrage refers to tax planning and regulatory avoidance strategies that exploit gaps, loopholes, or inconsistencies in one country’s laws to circumvent the rules of another. These schemes are highly complex, shrouded in secrecy, and deeply embedded within intricate corporate structures.Footnote 1

‘Few, if any phenomena’, note Jan Friedrich and Mathias Thiemann, ‘threaten the goal of law-makers, market regulators or accounting standard-setters to issue adequate rules and ensure their rigorous application as does regulatory arbitrage’ (Friedrich and Thiemann, Reference Friedrich and Thiemann2021, 81). Yet such concerns have not given rise to anything approaching a systemic study of jurisdictional arbitrage. On the contrary, the literature on jurisdictional arbitrage in law and accounting, notes Annalise Riles, is ‘surprisingly thin’ (Riles, Reference Riles2013, 68). In other disciplines – such as economics, business, and political science – the literature is scarcer, bordering on non-existent.Footnote 2 Jurisdictional arbitrage schemes tend to be portrayed as isolated actions that take place on the margins, in offshore financial centres (OFCs). The European Union’s Anti-Tax Avoidance Directive, for instance, targets what it calls ‘artificial constructions’ designed to exploit differences between national tax laws to minimize the tax burden.Footnote 3 More broadly, jurisdictional arbitrage schemes are typically depicted using derogatory language, such as ‘gamesmanship’, ‘manipulation’, ‘artificial constructions’, ‘exotic planning devices’, or ‘phantom investments’, suggesting they raise few if any significant systemic issues (Damgaard et al., Reference Damgaard, Elkjaer and Johannesen2019a; Freedman, Reference Freedman and Schön2008; Kaye, Reference Kaye2014; Mitchell, Reference Mitchell2008; Post et al., Reference Post, Preston and Sauter-Sachs2002).

Is this approach justified? I do not think so. Far from being a fringe activity, jurisdictional arbitrage has become systemic, deeply embedded in the fabric of corporate strategy. In advancing this argument in the following pages, we must move beyond the traditional perspectives of economists, who focus on markets and actors, and political scientists, who emphasize the role of the state. Instead, we need to adopt the vantage point of corporations themselves – seeing the world through the eyes of their managers and shareholders. Paradoxically, it is only by seeing through the eyes of the corporation that we come to recognize the full extent to which modern multinational corporations (MNCs) are political entities – shaping and being shaped by the very systems they are presumed to merely operate within.

To support this argument, I will be making throughout this book seven interrelated points.

First, whereas most of what has been written about arbitrage tends to be from the perspective of corporate taxation, the strategic exploitation of differences in laws and regulations to minimize costs or avoid regulation extends well beyond taxation.Footnote 4 Taxation was, after all, only one facet of the broader emergence of the rise of what is described in scholarly circles as the regulatory state (Majone, Reference Majone1997). During the twentieth century, states increasingly replaced the nineteenth-century private litigation regimes with regulatory agencies and enacted a plethora of rules and regulations affecting businesses across various domains Today, business is subject to regulations extending from civil to administrative and sometimes criminal liability in all of the world’s major legal systems. Business is subject, in addition, to privately designed (or quasi-private) accounting rules, a ‘collection of dialects’ that evolved ‘when professionals applied quantitative methods to qualitative endeavours’ (King, Reference King2006, 203).Footnote 5

The point, as argued cogently by Annalise Riles (Reference Riles2013), is that any rules, however well designed, can be arbitraged, and most are likely to be arbitraged by someone, somewhere. Arbitraging schemes, she notes, are indeed most lucrative when spilling into new, often unsuspected regulatory spheres, not least because that is where money can be made (Riles, Reference Riles2013). The scope for arbitrage in the international sphere is far greater than commonly assumed.

Second, the focus on taxation has contributed to what seems to me fairly widespread (though often implicit) perception that MNCs behave like large profit harvesting machines. The corporate group is designed, or so it is believed, so that the parent company accumulates group-wide profits, which are then distributed as dividends to shareholders. The parent use subsidiaries in OFCs to avoid taxation.

While this model may seem reasonable, a moment’s reflection reveals major strategic and financial problems with such an approach. If all profits were systematically funnelled to the parent company, the corporate group would be disproportionately dependent on the tax and regulatory environment of the parent’s home country. This would expose the group to several risks. Many home countries tax worldwide income of their corporations, meaning that once profits are repatriated to the parent, they become fully taxable. For instance, a US-based parent would be subject to US tax rules on all repatriated profits, potentially eliminating the benefits of offshore tax planning.Footnote 6

I argue that when viewed from the perspective of capital market augmentation, the function of subsidiaries of MNCs changes considerably. Rather than merely funnelling earnings upward, a subsidiary can be logged as an asset on the parent’s consolidated accounts. Internal transfers between subsidiaries and the parent can then be treated as discretionary transactions, rather than mandatory profit distributions. This flexibility liberates the corporate group from strict dependence on revenue extraction, allowing it to focus on exogenous factors such as regulatory regimes (taxation, reporting rules, capital controls), market conditions (exchange rates, investment incentives, sector growth), and political and legal risks in different jurisdictions (Birkinshaw and Morrison, Reference Birkinshaw and Morrison1995; Dowd et al., Reference Dowd, Landefeld and Moore2017; Forte, Reference Forte2016, Greggi, Reference Greggi, Kraft and Striegel2019; Grubert and Mutti, Reference Grubert and Mutti1991; US Department of the Treasury, 2016).

MNCs are not profit harvesting machines but asset harvesting machines – a point that will become clearer throughout this book. This means that not only is the scope of jurisdictional arbitrage being much greater than assumed, and this is my third point, but the motivating rationale for employing jurisdictional arbitrage is not simply about taxation or circumvention of this or that regulation. At core, jurisdictional arbitrage arises from deep-seated contradictions that we have inherited from the period of the Second Industrial Revolution – a period of rapid technological advance that witnessed profound transformation in production, manufacturing, communication, and transportation. However, this era also witnessed the emergence of modern borders. This was the era when key nations such as Germany and Italy emerged, while the United States solidified its identity as a unified state. Meanwhile, countries such as Britain and France drew sharper distinctions between the motherland and their colonies. It was a period, therefore, that produced the rigid and somewhat arbitrary fragmentation of the world’s geographic space.

A system of states, founded on the principles of sovereignty, produced a fragmented regulatory landscape. Essential resources needed by the Second Industrial Revolution, such as raw materials, skilled labour, and market access, became unevenly distributed, located within institutional and political environments influenced by the historical and institutional legacies of wars and colonialism. It was during this period that the worlds of geopolitics and geoeconomics began to fall out of sync – not only spatially but also epistemologically. The world of states is a world of ‘things’, but advanced economies began a momentous process whereby they shifted gear into a forward-looking perspective, represented by the concept of intangible assets. The corporate world is not simply making money from coordinating factors of production efficiently while producing goods the market desires. The corporate world is augmenting value based on the principles of futurity, and it does so by augmenting the value of its assets.

Unfortunately, this fragmented and misaligned spatial environment became entrenched, and this is my fourth point, two, perhaps three, decades after the core ideas of economics had already been established. Since then, economics – along with related fields that built upon the epistemological foundations of what became known as neoclassical economics, such as international business and political science – has struggled to fully account for the complexities of the real world. The preferred approach has been rather to begin with a theoretical proposition – a theory of markets where people are exchanging ‘things’ – and then treat the countless contradictions arising from the misalignment of geopolitics and geoeconomics, the world of things, and the economy of intangibles as intellectual puzzles to be solved. But seen from the perspective of jurisdictional arbitrage, the limitation of the approach become clear.

Put simply, if the global economy truly resembled the seamless, homogeneous, and borderless ‘market’ depicted in economic textbooks, arbitrage would not exist and MNCs would be merely profit-harvesting machines. Arbitrage occurs, then, in an intellectual space overlooked by economics. One way to resolve this conundrum is to dismiss arbitrage as an ‘artificial’ construct. The advantage of this approach is that economics can then sidestep the issue altogether, focusing solely on what it deems ‘genuine’ or not artificially constructed. Needless to say, this is not the approach I take in this book.

But the same system of states that increasing misaligned with the needs of business also produced unwittingly, and this is my fifth point, gaps that could be exploited by those very same businesses. In this sense, jurisdictional arbitrage is both a product of and a strategic response to geopolitical and geoeconomic misalignments of the late nineteenth century. Arbitrageurs are not merely navigating an inherited geopolitical and geoeconomic ‘system’ that are arbitrary – they actively seek to create their own regulatory spaces, islands of stability in what was essentially an out of sync environment. By strategically exploiting the gaps and inconsistencies produced by sovereignty, the newly minted MNCs learned to shape, up to a point, the rules of the game to suit their interests.

Why then do businesses seek to control the environment? The answer seems obvious. We all want to limit our dependence on things that are beyond our control. But the answer is more complicated when it comes to business. A business entity whose value is based on future performance must control the environment – or must show, perform, if you wish, that it can control the environment and hence its future. In this way, jurisdictional arbitrage represents more than a set of strategic manoeuvres. These practices are both performatives as much as they threaten the foundational balance between private enterprise and public responsibility. But as economists are fond of saying, there are no free lunches. Establishing and vetting arbitrage schemes involves significant costs, which can be justified by the scale of operations. The larger and wealthier the MNC, the greater its potential gains from implementing internal treasury operations or engaging high-cost professional legal, accounting, and financial services.

In turn, and this is my sixth point, this positions arbitrage as a previously unrecognized form of power, making it a subject of significant interest to political science and international political economy. In Chapter 9, I argue the power dynamics of jurisdictional arbitrage resemble the predator–prey dynamics found in nature. Businesses, as the ‘prey’, outmanoeuvre their ‘predators’, the states, by camouflaging themselves and using the states’ own rules against them. Through this strategic adaptation, firms turn the constraints imposed by states into tools for their survival and advantage. To use another analogy, jurisdictional arbitrage acts as a canary in the coal mine, signalling a warning, in this case, how modern businesses transform challenges into solutions that, in turn, shape the fabric of contemporary life.

Behind these ‘corporations’ there are people, individuals making decisions, crafting strategies, and deliberately exploiting the complexities of legal and regulatory diversity for profit. Corporate actions, though executed under the guise of legal entities, ultimately reflect the choices, motivations, and agency of the individuals who lead and manage them. Executives, legal advisors, and financial experts serve as the architects and primary beneficiaries of a system designed by none other than themselves.

These people also act collectively, if unwittingly, undermining, and this is my seventh point, the implicit social contract between states, businesses, and citizens. The social contract that underpinned the rise of the regulatory state of the late nineteenth century was built on the expectation that businesses contribute to societal wealth, through taxation, job creation, and compliance with regulations, in exchange for the rights and privileges granted by states, such as access to markets, legal protections, and infrastructure. The ability to neutralize, or at least partially circumvent, the regulatory environments allows businesses to exploit the benefits provided by the state while avoiding some of the corresponding costs.

Arbitrage is closely tied, therefore, with broader issues of inequality and the emergence of what I call the rule-based transgressor elite – arguably the most powerful elite of our time. This group thrives on its ability to operate within the boundaries of legal frameworks while systematically exploiting their loopholes, leveraging arbitrage to amass wealth and power in ways that reinforce existing disparities and reshape global dynamics. Scientists often refer to theory of a ‘microcosm’ or ‘microcosmic event’, whereby a small-scale situation can encapsulate or reflect the characteristics of a larger system (Benton et al., Reference Benton, Solan, Travis and Sait2007). In this book, I treat jurisdictional arbitrage as a microcosmic event. I do not aim to provide exhaustive research into the various forms of jurisdictional arbitrage schemes, nor do I offer a complete theory of modern corporate groups. Instead, I argue jurisdictional arbitrage schemes open a unique window into the functioning of corporate power within a world of states, illuminating how corporate groups navigate and influence the boundaries and frameworks of national jurisdictions.

Why MNCs Are Not What They Seem

At first glance, the title of this section may seem provocative, even counterintuitive. How can MNCs, arguably the most important business organization today, ‘not exist’? The term ‘multinational corporation’ conjures up an image of a unified, centralized entity operating seamlessly across borders.Footnote 7 Yet the reality is far more complex, and it is far more complex for a reason.

In Global Political Economy: Understanding the International Economic Order (2011), Robert Gilpin recounts a story of a group of graduate students at Princeton University who asked their Economics professor to offer a course on MNCs. They were firmly rebuffed on the grounds that ‘multinational corporations do not exist’ (Gilpin, Reference Gilpin2011, 33). Gilpin interprets the rebuff as a vivid demonstration of the absurd limitations of neoclassical theory.

But perhaps the unnamed professor in Gilpin’s story had a point. A corporation is a licensed entity, granted existence by a sovereign authority. A corporation, by definition, cannot be multinational. Itzhak Hadari writes: ‘The typical MNC is a cluster of separate legal entities in several jurisdictions, which exist only if the laws of each jurisdiction recognize them as legal entities. It is a business and economic creature, and the usage of that term is presently found only in those fields’ (Hadari, Reference Hadari1973, 754; emphasis added).Footnote 8 Whereas we tend to speak of the MNC in the singular, the reality, at least as far as lawyers are concerned, is that there is no ‘MNC’ that can transact in markets, pay tax, or pay off politicians.Footnote 9 Lacking a formal legal personality, these business entities simply cannot perform any of the tasks generally assigned to them in the literature.

But before we conclude MNCs do not exist, let me modify the statement in a way that, in my view, deepens the puzzle. A single corporation can set up branches around the world and can then conceivably be described as an MNC. But it so happens that most modern MNCs – particularly the well-known household names – have opted for a different organizational modality. Hadari’s (Reference Hadari1973) concept of MNCs as ‘clusters’ of companies is not exactly true, either. Modern MNCs are not a mere assortment of independent entities; they are profoundly integrated, with a dual nature. I prefer to describe them as centrally coordinated multi-corporate enterprises (CCMCEs). These corporations are deliberately structured so they can function as a single, unified business in markets, coordinated at the highest level to achieve strategic cohesion across borders. Legally, however, they are structured as CCMCEs, or groups of independent companies, causing many to refer to them as a ‘corporate group’.

The question is whether the organization of the MNC as a CCMCE truly matters – and, if it does, for whom. At first glance, the question might seem inconsequential; after all, if it were significant, surely it would have garnered more attention by now.Footnote 10 Under the influence of two brilliant economists, Roland Coase and James Buchanan, economics gradually evolved from about the 1960s to incorporate ‘economics of choice’ stressing the market is exchange of property titles (Buchanan, Reference Buchanan1978). This perspective suggests that ‘firms’ internalize transactions that can be executed at a lower cost within the organization than through the market (Alchian and Demsetz, Reference Alchian and Demsetz1973; Demsetz, Reference Demsetz1988; Fama, Reference Fama1980; Jensen and Meckling, Reference Jensen and Meckling1976). This approach reframes firms, including MNCs, as legal and economic constructs designed to optimize efficiency, rather than as cohesive, centralized entities. Harold Demsetz argues, for instance, that the core question in economics is why a ‘firm-like’ web of contracts tends to coalesce in markets (Demsetz, Reference Demsetz1997). Firms, including MNCs, are viewed as ‘no more than a web of contracts and other legal documents that tie together various parties to a specific company’ (Cohen, Reference Cohen2007, 28).

Legal scholars question, however, why economists devote so much attention to contract, transaction, and property while ignoring a fundamental component in the creation and organization of business enterprises: entity law in the form of the laws of incorporation. There is evidence that the number of subsidiaries in the corporate group is rising. In an analysis they conducted for the US Fed, Dafna Avraham, Patricia Selvaggi, and James Vickery (Avraham et al., Reference Avraham, Selvaggi and Vickery2012) found the number of subsidiaries and affiliates owned by some of the largest US banking holding companies rose to an average of 3,400 in 2012, up from about 1,000 in 1990. Figures indicate an astounding proliferation over time. In 1985, Phillip Blumberg found that the 1,000 largest US industrial corporations had an average of forty-eight subsidiaries. In 2012, Stephen Cohen reported the entire group of MNCs had about 77,000 subsidiaries – and was surprised by this number. But by 2018, the top 100 alone were reported to have over 73,000 subsidiaries (Phillips et al., Reference Phillips, Petersen and Palan2020). The trend shows no signs of stopping, let alone slowing down: the number of subsidiaries had risen by an average 8 per cent when my colleagues and I took a second look eighteen months later (Palan et al., Reference Palan, Petersen and Phillips2021).

Why have ‘firm-like’ webs of contracts taken the form of an increasing number of subsidiaries and affiliates? There is nothing in the theory of the nexus of contracts – or indeed in any other economic theory – that begins to answer the question of why MNCs have such an extraordinary number of subsidiaries.

Business and management studies, in contrast, provide an answer – or so it seems. They argue subsidiaries play a critical role in enhancing operational efficiency, managing risk, and adapting to diverse markets (Desai, Reference Desai2009; Zey, Reference Zey1999; Zey and Camp, Reference Zey and Camp1996; Zey and Swenson, Reference Zey and Swenson1998). However, these explanations require closer scrutiny. The term ‘operational efficiency’ is remarkably broad and can encompass a wide range of practices. While it might refer to streamlining supply chains or optimizing resource allocation, it can just as easily serve as a euphemism for practices such as regulatory arbitrage.

This raises important questions about the true drivers of subsidiary proliferation. Is it genuinely about improving business operations, or is it a strategic response to a global system riddled with regulatory and jurisdictional inconsistencies?

Another set of developments largely overlooked by the web of contract theories is the structural organization of foreign direct investment (FDI). A significant portion of FDI is not direct at all; it is intermediated. Instead of a straightforward flow from a parent company to a subsidiary in a foreign country, investments are often routed through subsidiaries in third countries. The phenomenon of intermediated FDI accounts for a substantial share of global FDI flows. Put differently, the CCMCE is not a flat organizational structure but a three-dimensional one.

We are thus presented with four interrelated puzzles: why MNCs are organized as CCMCEs; why the rules of incorporation and entity law, central to the CCMCE structure, are so often overlooked; why the number of subsidiaries established as independent companies continues to rise; and why the organization of CCMCEs has become increasingly complex. Underlying these four puzzles is a fifth. How can we have a meaningful discussion about the organization of CCMCEs without comprehensive data and a clear understanding of how MNCs are structured?

Equity Mapping: A Methodological Approach to Uncovering Corporate Control

I was reminded of a story I heard at a conference many years ago about how the Chinese state prepared for the advent of the internet in the 1990s. Chinese officials had invited the CEO of a pioneering American internet company to a two-day event aimed at discussing the future of the internet in China. During the event, various officials presented their ideas and plans for both encouraging and regulating internet use. When it was the American CEO’s turn to speak, he began his talk with a simple question to the audience: ‘How many of you have ever used a computer?’ Only two officials raised their hands. He followed up with, ‘How many of you have ever surfed the internet?’ The answer was none of them had. Chinese officials in the 1990s were making grand plans for the internet without having basic, hands-on experience with computers or the internet itself. They were relying on theoretical knowledge or abstract ideas about what the internet could be, without engaging with the technology first hand.

I was reminded of this story because one of the significant challenges in having a meaningful discussion about jurisdictional arbitrage is the void of information – an informational desert that obscures its true scale and mechanisms. Despite the rich and expanding body of literature on MNCs and their subsidiaries, we know surprisingly little about how these corporate groups are actually organized. At best, we are presented with schematic diagrams of operational planning – visuals populated with empty boxes labelled ‘divisions’ or ‘organizations’ – that offer no insight into the actual subsidiaries underpinning these structures. Subsidiaries are often viewed as merely functional entities, serving operational purposes, akin to limbs of a larger body. This perspective assumes their distribution within corporate chains is largely random, guided by immediate needs rather than strategic design. Why bother with the anatomy of corporate groups if ‘physiology’ is good enough?

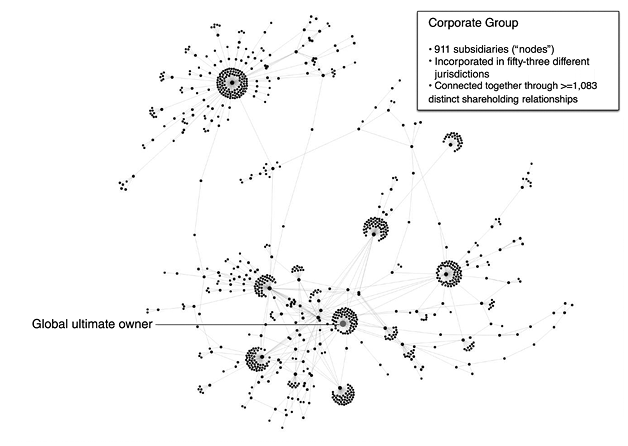

The CORPLINK project upon which this book relies sought to learn how CCMCEs are legally structured and how intra-firm transfers take place.Footnote 11 The technique uses an algorithm to capture information from corporate filings and converts the ownership data of MNCs and their subsidiary organizations, as recorded in the Orbis database, into visualized ‘maps’ using a standard social network analysis (SNA) approach. These visualizations, which the CORPLINK project designated as equity maps (EMs), provide a detailed and accessible representation of the ownership and control structures within corporate groups.

As the computer processed the data and began generating these maps, the resulting images were both surprising and revealing. The structures of modern CCMCE were far more complex and intricate than assumed. The CORPLINK project produced more than 250 EMs of large corporate groups, systematically mapping the structures of the 100 largest non-state, non-financial companies in the world in 2018 (based on revenue). These EMs represent raw data on and visualization of corporate organizations, collected directly from primary sources, before any analysis or processing has been applied.

Figures I.1 to I.3 showcase examples of some of the EMs of three CCMCEs. These maps vividly depict the vast, multi-tiered networks formed by CCMCEs, illustrating the intricate connections between parent companies and their numerous subsidiaries distributed across multiple jurisdictions.

Figure I.1 Volkswagen equity map, c. mid 2018.

Figure I.2 Wells Fargo equity map, c. 2021.

Figure I.3 Group structure of Apple Inc., highlighting Irish holding structure, c. January 2019.

In each of these maps, a corporate subsidiary is depicted by a dot, with each dot representing a separate entity, often a corporation. Each of these corporate entities has its own managers, board of directors, and shareholders, and each is required to file annual reports in its respective jurisdiction. The group’s global ultimate owner, typically a holding company, is depicted in red.

Subsidiaries that control other subsidiaries extend outward to form a chain, illustrating the hierarchical relationships within the group. Subsidiaries that do not control other entities are positioned closer to their parent company, often forming clusters around it. These clusters represent subsidiaries that are directly linked to their parent without holding further subsidiaries themselves.

Additionally, some subsidiaries are controlled through at least two separate subsidiaries or chains of subsidiaries, creating more complex ownership pathways. Palan et al. (Reference Palan, Petersen and Phillips2021) refer to these as ‘splitters’, where ownership is divided among multiple layers or paths within the group. In Figure I.2, the EM of Wells Fargo highlights these splitters ownership patterns in purple, showcasing the intricacies of its corporate structure.

Market Friction, Firms, and Jurisdictional Arbitrage

The debate about arbitrage is not particularly new. More than a century ago, US President Theodore Roosevelt sharply criticized lawyers for devising ‘bold and ingenious schemes by which very wealthy clients, individuals or corporate, can evade the law which are made to regulate the interest of the public’ (quoted in Fleischer, Reference Fleischer2010, 230). Decades later, President John F. Kennedy voiced similar concerns, lamenting the behaviour of the MNCs of his era.Footnote 12 President Barack Obama, echoing Kennedy’s concerns, observed: ‘The tax system is subject to gaming, as corporations manipulate complex tax rules to minimize taxes and, in some cases, shift profit actually earned in the United States to low-tax jurisdictions’ (The White House and the Department of Treasury, 2012, 13).Footnote 13

What tends to be missed, however, in the rather technical discussions about arbitrage is an underlying problem, the fundamental flaw that makes arbitrage both possible and desirable in the first place.Footnote 14 I discuss those broader historical conditions in Chapter 2. I trace the origins to the late nineteenth-century system of states and the fledgling American capitalism. Before the nineteenth century, state power was centralized, focusing on the monarch and the capital. State power tended to diminish with distance until it became tenuous in frontier regions in Europe such as Alsace-Lorraine or Trento. At its core, the modern state that was the product of the late nineteenth century established a system of rules that operated consistently, replacing fragmented and localized governance with a cohesive legal framework (Mann, Reference Mann2008; Poulantzas, Reference Poulantzas1978).

At the same time, and for complex reasons explored in the next section, the market underwent significant transformations after the US Civil War, centred on the rise of the corporation and, equally importantly, the emergence of intangible property. Likely influenced by the vast scale of the US market, the first large modern corporate forms emerged, starting with railway companies, followed by energy and steel giants such as Rockefeller’s Standard Oil and Morgan’s creation of US Steel in 1902. Consumer-focused companies such as Heinz soon began to appear as well.

These corporations were vast logistical enterprises, mastering the challenges of production and manufacturing across great distances and involving large numbers of people. They also required immense amounts of capital and investment. Investment is a bet on the future earning capacity of an organization. The forward-looking perspective of investors became increasingly tied to the concept of intangibles, marking a pivotal innovation in the evolution of modern capitalism.

This specifically American type of corporate organization soon began to spill across borders, starting with companies such as the sewing machine manufacturer, Singer. The interplay between these two trends – the rise of corporations and the role of the state – unfolded in a particularly intriguing way.Footnote 15 Large corporate organizations, with their future-oriented investments, rely heavily on the stability provided by legal systems. However, reliance on state and the law highlights two fundamental challenges of internationalization in the context of a dissected sovereign system.

First, states are not particularly good at providing the ‘rules of the game’ that economists would consider approximating anything like ‘Pareto optimality’ – a state where resources cannot be reallocated to make someone better off without making someone else worse off. The institutional environment provided by the state and the law, Douglas North argues, sets the parameters for the contracting process by establishing incentives and constraints for both individuals and firms (North, Reference North1982). Political systems, however, are not well designed to produce economically efficient working rules (Buchanan and Tollison, Reference Buchanan and Tollison1984; North, Reference North1990; Stigler, Reference Stigler1971). Instead, states evolved within a distinct context shaped by conflicts and wars among the nobility, where the primary concerns were power, territorial control, and survival, not the optimization of economic outcomes. The legacy of these historical evolution is a ‘property rights structure that will maximize rents to the ruler (or ruling class) [and] produce economic growth’ (North, Reference North1982, 28).Footnote 16

Second, legal systems are fragmented, and differing regulations and jurisdictions create obstacles to seamless operations. This problem is exacerbated because, as David Gerber notes, ‘the laws that are applied to global markets are not themselves global – or even transnational! Instead, the laws of individual states govern global markets’ (Gerber, Reference Gerber2010, 418; emphasis added). Consequently, the sort of rights and duties that are the backbone of market relationships are far less secure internationally, reliant on a system of bilateral agreements between states, and relatedly, there is no clear unifying fabric of laws and norms operating internationally.

What can business hope to achieve under such circumstances? Most of the literature focuses on two tactics adopted by the corporate sector. Business may try to relocate, to the extent it is possible, to jurisdictions with more favourable combinations of factors of production, political conditions, institutional stability, and regulatory environments. A great deal has been written about this option, especially policy advice such as the Washington Consensus, which advocates for governments, in return, to adopt business-friendly tax and regulatory regimes (Davies, Reference Davies2016; Dicken, Reference Dicken2007; Kahan and Kamar, Reference Kahan and Kamar2003; Stopford et al., Reference Stopford, Strange and Henley1991; Williamson, Reference Williamson1993).Footnote 17 But the tactic of relocation is limited by inherent factors such as the geographic distribution of resources and the size of specific markets. Furthermore, future political and institutional shifts are hard to predict, making this strategy vulnerable.

Relocation to preferable jurisdictions does not resolve the inherent limitations of the rules of the game of society as analysed by North (Reference North1990). Consequently, businesses often resort to a second, complementary tactic, seeking to influence the political process in each of the countries in which they trade in the hope of influencing governments to produce a regulatory environment that aligns better with their interests. Much has been written about this strategy as well (Hill et al., Reference Hill, Kelly, Lockhart and Ness2013; Kim and Milner, Reference Kim and Milner2019; Lee, Reference Lee2024; Saittakari et al., Reference Saittakari, Ritvala, Piekkari, Kähäri, Moisio, Hanell and Beugelsdijk2023; Truman, Reference Truman1971; Waterhouse, Reference Waterhouse2013). Naturally, the way businesses interact with politics is profoundly influenced by the nature of the political systems in their home or host countries. And while there is little doubt that businesses devote significant resources to lobbying, bribing, or even ‘capturing’ entire political systems, this approach is not without drawbacks either. Success can be tenuous, outcomes are uncertain, and there is always the risk of free riders – competitors who benefit from any favourable changes without incurring the costs of advocacy.

But there is a third option: engaging in arbitrage. This strategy entails establishing subsidiaries in third countries and channelling investments through them to circumvent undesirable rules or regulations, including taxation. At its core, this strategy seeks to combine the best of both worlds, ensuring the tangible aspects of a business – such as production, sales, or resource extraction – are placed where economic logic dictates, at least to the extent this is possible. In other words, in countries that, by a quirk of history, possess the essential factors businesses seek when internationalizing. The strategy is intended, at the same time, to ensure the legal and regulatory dimensions of transactions are insulated as much as possible from the same quirks of history.

This strategy is more cost-effective than the first two, as it does not require relocating production or manufacturing, incurring substantial expenses, or navigating political risks. Instead, it relies on an in-depth understanding of legal and accounting frameworks, coupled with the relatively low cost of establishing subsidiaries across jurisdictions. The strategy is also remarkably sophisticated. As I explain in Chapter 3, the strategy involves a decoupling of the physical from the legal, so that goods or services can be produced or exchanged in one country, but the legal exchange of property titles takes place elsewhere, in selected jurisdictions.

Erin O’Hare and Larry Ribstein refer to jurisdictional arbitrage as ‘repackaging arbitrage’ (O’Hara and Ribstein, Reference O’Hara and Ribstein2009, 108). Using a kind of ‘cut-and-paste’ strategy, MNCs establish subsidiaries and affiliates in a manner that allows each entity to select a distinct regulatory dimension. Together, these subsidiaries, often situated across multiple jurisdictions, construct a tailored regulatory pathway for transactions. Because businesses are not constrained to choosing complete regulatory packages from any single jurisdiction but can cherry-pick advantageous elements from different systems, jurisdictional arbitrage does not inherently promote regulatory optimization. By exercising this option, companies can present a more attractive profile to investors, who are increasingly drawn to firms that demonstrate adaptability and forward-looking value in a complex global environment.

Table I.1 summarizes the core principles of jurisdictional arbitrage from a business perspective.

| Aspect of Transaction | Economic Logic (Market Efficiency) | Regulatory Logic (Legal & Tax Framework) |

|---|---|---|

| Physical Exchange | Production and manufacturing are based in locations optimized for market conditions, such as low costs or strategic supply chains. | Regulatory and tax frameworks are applied based on physical presence. |

| Legal Registration | Production and manufacturing are relocated to jurisdictions offering better regulatory and tax environment | Registration occurs in jurisdictions with more favourable legal and tax conditions, reducing associated regulatory and tax burdens. |

| Jurisdictional Arbitrage | Physical and legal exchanges are decoupled to avoid higher regulatory costs in primary markets, allowing companies to focus on market efficiencies. | Legal and operational activities are separated across jurisdictions to maximize benefits from both economic and regulatory environments. |

| Common Treatment of Arbitrage | This has led to the proliferation of ‘empty’ shell companies and ‘phantom’ investments | These are artificial constructions. |

| Jurisdictional Arbitrage Thesis | Production and manufacturing are optimized in economically and regulatory favourable locations, achieving a balance of cost-efficiency and tax minimization. | Legal registration is shifted to jurisdictions with favourable tax and regulatory frameworks, minimizing compliance costs without physically moving operations. |

‘Accumulation’ versus Intangible Property

If the logic of arbitrage makes economic sense – and, indeed, there is nothing inherently surprising about arbitrage from an economic standpoint – why has so little attention been devoted to jurisdictional arbitrage as a general phenomenon in economics or political science? The ignorance of arbitrage goes deep. Even one of my all-time favourites, a survey of the field of law and economics written by Nicholas Mercuro and Steven Medema, which covers a range of approaches, including transaction cost economics, public choice theory, new and old institutional economics, and postmodernist legal theory, does not mention the word ‘arbitrage’ a single time (Mercuro and Medema, Reference Mercuro and Medema2020)! Why is that?

I now realize this must have to do with timing. By this, I mean the dominant theoretical frameworks we rely on today – whether drawn from neoclassical economics or Marxist thought – were formalized just before the emergence of a distinctly American form of capitalism. I highlight four key institutional transformations taking place in the United States, each of which has taken place a decade or more after the first wave of neoclassical theories. It is not surprising, therefore, that neither Marxism nor marginalism factored in those important changes.

The first important institutional transformation occurred when the US Supreme Court and UK House of Lords established the basic framework of the modern doctrine of corporate personality. In the United States, the concept of corporate personhood was reinforced by legal decisions and interpretations, including the Santa Clara County v. Southern Pacific Railroad Co. decision in 1886, when a corporation became ‘an incorporate body that is able to act as if they were real persons for legal purposes’ (Quentin, Reference Quentin2020). Corporations were granted the right of free speech under the First Amendment, and under the Fourteen Amendment can claim equal protection under the law and due process (Stern, Reference Stern2017, 34; for a discussion, see Robé, Reference Robé2020).Footnote 18

In the United Kingdom, in the case of Salomon v. Salomon & Co. Ltd. (1897), the House of Lords affirmed a corporation is a separate legal entity, granting it the status of a ‘legal person’ with rights and obligations like those of an individual.Footnote 19 These two cases (and similar decisions in France, Germany, and elsewhere) established the contemporary interpretation of company law.Footnote 20

Once incorporated, a company was considered a distinct legal entity, separate from its shareholders. The separation of the corporate entity from its shareholders creates what is known in legal jargon as a ‘corporate veil’ that protects shareholders from personal liability for the company’s debt; hence, the shareholders’ liability is limited to the amount unpaid on their shares. After these rulings, just as the state as an artificial legal person does not ‘belong’ to the monarchy, the corporation in Anglo-Saxon law does not belong to the principals, that is, the shareholders, and managers are no longer merely the agents of those shareholders.

The significance of modern entity law comes into sharp relief in the context of a second, important institutional mutation that took place first in the United States and was soon copied elsewhere. In a series of decisions between 1899 and 1892, the state of New Jersey enacted progressive corporate laws that allowed corporations to own stock in other corporations. The combination of the two sets of legal instruments gave rise to a new phenomenon, the corporate group or ‘going concern’. The corporate group structure that emerged in the United States during this time diverged significantly from the European model.Footnote 21 The US model was characterized by the use of holding companies and subsidiaries – distinct legal entities interconnected directly or indirectly through equity ownership to the parent. In this framework, corporate groups in the United States were legally structured as clusters of independent companies, often with opaque and complex relationships among their various entities in the group.Footnote 22

In a third and crucial innovation, in a series of landmark rulings by the US Supreme Court, the American legal system began to recognize a new form of property: intangible property. This category included from around the 1920s intellectual property (IP) such as patents and copyrights, trademarks, and more significantly – and most elusive of all – and surprisingly earlier, the concept of ‘goodwill’. Goodwill was another product of the New Jersey amendment and refers to the premium paid when one company acquires another – which it could do following the New Jersey amendment. If the purchase price of an acquired company was over the fair market value of the target company’s identifiable assets minus its liabilities, the excess can be attributed to factors such as brand reputation, customer loyalty, employee relationships, propriety technology, and overall competitive advantage. The excess value was written in the accounting books as ‘goodwill’ (Allan, Reference Allan1889; Commons, Reference Commons1919; Jaffé, Reference Jaffé1924), Simply stated, goodwill is the value the market places on the capacity of various properties of the corporate group, including estimates of robustness of its corporate organization or even corporate culture, to generate future income.

It was a moment of no return. Intangible capital is often defined in economics by what it lacks – that is, as ‘productive capital that lacks a physical presence’ (Crouzet et al., Reference Crouzet, Eberly, Eisfeldt and Papanikolaou2022). But that is the wrong way of looking at it. The shift in valuation from fair value based on tangible property towards intangibles that took place from the late nineteenth century onwards encouraged companies to think strategically about how to structure operations, allocate resources, and position intangible assets. Modern corporate groups increasingly link income projections to market size and growth potential, moving away from traditional profit-based assessments (Modigliani and Miller, Reference Modigliani and Miller1958). The value of intangibles, in turn, reflects several key factors. It encompasses the group’s access to and control over larger markets and the capacity to stabilize its future by reducing reliance on external factors – political processes that are beyond the group’s direct control – and its ability to safeguard IP and its goodwill within a world governed by sovereign states.

The valuation of companies in markets extends beyond taxation. For example, a company able to shield itself from liabilities, such as potential claims related to unknown risks (e.g., unforeseen asbestos use by subsidiaries in foreign markets) would likely have higher valuation of its goodwill. Similarly, a company with access to cheap capital, whether through financial innovation or by arbitraging restrictive financial regulations, would also enjoy a higher market valuation. And a company demonstrating an ability to minimize or, more importantly, control its global tax liabilities would be rewarded with enhanced market valuation as well.

The value of tangible property is seemingly tied to the physical asset; its materiality provides a clear basis for valuation. In contrast, the value of intangible property is inherently inseparable from the legal entity that holds it. A patent, trademark, or logo is intrinsically linked to the corporate organization that leverages, protects, and exploits it. In 2024, Coca-Cola’s brand was valued at approximately US$106.45 billion, but give the logo to, say, Toyota, and its value would plummet. The corporation as an artificial legal person underscores the strategic significance of intangible assets within the broader framework of what Berle and Means called the ‘corporate economy’ (Berle and Means, Reference Berle and Means1948, 2).Footnote 23

The traditional neoclassical models that focus on production and marginal cost do not adequately capture how the value of intangibles is created, stored, or traded. Assigning values such as ‘goodwill’ to a ‘firm-like nexus of contracts’ is inherently problematic. These concepts, which underpin much of modern firm theory, reflect a bygone era centred on tangible goods and the notion of a ‘productionist’ firm. Crucially, intangible property, unlike IP or data, has reoriented the economy towards valuation based on future potential rather than present assets alone.

However, there is much more to arbitraging. As I explain in Chapter 2, the early MNCs of the late nineteenth century were from inception organized according to the American corporate group model. They were never singular entities, and very soon after the introduction of the New Jersey amendments, they evolved into CCMCEs. They adopted the corporate group structure primarily to arbitrage incorporation laws and anti-trust regulations. Internationally, the CCMCE framework was adopted initially for a different reason: it offered an efficient and cost-effective method for establishing operations in foreign markets. Over time, the CCMCE model began to serve a second, equally significant, purpose: arbitrage. This evolution was closely tied to the management of intangibles, a factor that increasingly influenced the structure and strategy of multinational enterprises.

The three developments discussed here, the advent of the corporation as an artificial legal person, the right of those persons to hold stock in other artificial persons, and the innovation of intangible property, were closely intertwined therefore, both temporally and analytically, with a fourth development: the rise of the CCMCE. As discussed earlier, MNCs employed arbitraging as a key strategy for navigating political environments. For instance, Amazon’s strategic focus has historically emphasized market expansion and customer acquisition over immediate profit maximization. Amazon is not alone. Many corporate groups value long-term scalability and future market dominance, emphasizing how growth potential and market share can drive future revenues and profitability.

Such strategies are far easier to implement because MNCs are not singular companies but organized as clusters of independent companies. The CCMCE structure allows companies to play different roles and reorganize their subsidiaries in ways that facilitate higher valuation of the group. The logic of arbitrage as it works through these four institutional developments is summarized in Table I.2.

Table I.2Long description

The table lists six factors across six types of markets or firm characteristics. The data from the table are as follows.

For the Definition factor, a frictionless market is ideal with no transaction costs, a dissected market has barriers and regulatory divides, tangible assets are physical assets like machinery and property, intangible assets include IP, brand, R&D, and goodwill, firms as productive entities focus on production and output, and firms augmenting value in the market focus on enhancing market presence and goodwill.

For the Transaction Costs factor, frictionless markets have minimal to no transaction costs, dissected markets have high costs due to regulations, tangible and intangible assets are not applicable, firms as productive entities minimally focus on market friction, and firms augmenting value actively navigate market structure and perception.

For the Asset Mobility factor, frictionless markets have high mobility, dissected markets are limited by legal and logistical barriers, tangible assets are location-bound, intangible assets have high mobility, firms as productive entities primarily involve fixed assets, and firms augmenting value focus on reputation and value-building strategies.

For the Valuation factor, frictionless markets are transparent and supply-demand driven, dissected markets are less transparent due to regulations, tangible assets have straightforward valuation, intangible assets require subjective valuation, firms as productive entities are tied to physical output, and firms augmenting value are tied to brand value and market influence.

For the Investment Impact factor, in frictionless markets, investments increase efficiency; in dissected markets, investments navigate barriers; tangible assets benefit from capital infrastructure investments; intangible assets benefit from innovation, R&D, and brand investments; firms as productive entities expand productive capacity; and firms augmenting value enhance strategic market value.

For the Subsidiary Organization factor, tangible assets use subsidiaries for physical asset management, intangible assets use subsidiaries strategically across jurisdictions, firms harvest profits from subsidiaries, and firms use subsidiaries as assets.

CCMCEs, Jurisdictional Arbitrage, and the Question of Power

Since arbitrage is about the relationship between states and markets, it raises inevitably the question of power. The idea that MNCs have enormous power is well established. There is broad agreement that over the past three or four decades, the power pendulum has swung decidedly from the state towards the corporate sector (Hathaway, Reference Hathaway2020; Stopford, Strange, and Henley, Reference Stopford, Strange and Henley1991; Waterhouse, Reference Waterhouse2013).

What, then, is the true source of a firm’s power? Most answers focus on firms as singular entities, treating MNCs as monolithic actors.Footnote 24 Political scientists often assume that when MNCs engage in politics they do so as conventional political actors, operating within the rules of politics and leveraging traditional means such as financial resources to achieve their goals. In this view, MNCs are simply political entities with vast resources, and the question of their power becomes a matter of tactics.

My argument, however, is that instead of seeking to change regulations or influence governmental agendas, CCMCEs use jurisdictional arbitrage schemes as techniques of accommodation with existing legal frameworks. CCMCEs are using arbitrage not in order to persuade parent or host states to modify their regulatory environments, nor are they seeking to control the regulatory agenda or even persuade states to change their agendas. On the contrary, jurisdictional arbitrage is a power dynamic where the actors leverage existing rules to their advantage, creating a paradox where compliance becomes a tool for exercising power. Adherence to formalities allows CCMCEs to navigate and exploit inconsistencies or gaps in the regulatory framework. Arbitrage represents, therefore, a distinct form of power, arguably the primary technique wielded by CCMCEs in their interactions with states and the broader state system.

What Is Known about Jurisdictional Arbitrage: A History of Missing Opportunities?

What, then, is known about jurisdictional arbitrage? And why does the literature often dismiss arbitrage as an artificial construct? Much of this stems from the historical narratives surrounding firms and corporations.

The traditional theory of the firm developed from Adam Smith’s theory of the factory. It emphasized how firms produce and supply outputs. It resulted in a productionist-oriented perspective, whereby firms were seen primarily through the lens of production and manufacturing.Footnote 25 The conventional view of the market relationship was strongly influenced by the work of Alfred Marshall, who defined ‘markets’ as ‘public exchange, mart or auction rooms, where the traders agree to meet and transact business’ (Marshall, Reference Marshall2009, 270). For Marshall, ‘traders’ could be abstracted and theorized in the form of the ‘representative firm’.Footnote 26 Firms were supply-side traders transforming inputs (e.g., labour, raw materials, capital) into outputs (goods or services) using available technology.Footnote 27

This approach treated the firm as a ‘black box’, ignoring its internal workings, let alone paying attention to the purpose or functions of arbitrage.Footnote 28 In his seminal article ‘On the Nature of the Firm’, Roland Coase (Reference Coase1937) persuaded economists to abandon the simplified view. Coase suggested firms exist to minimize transaction costs associated with market exchanges. Transaction costs referred to the costs of participating in the market, such as negotiating, enforcing contracts, and dealing with legal and other externalities. Tantalizingly, Coase’s theory had the potential to open the door to a broader exploration of arbitrage – but it did not.

Coase argued firms operate within two distinct economies. Externally, they interact with the broader market economy, where goods, services, and resources are traded according to price signals. Here, the price mechanism serves as the organizing principle, allocating resources through supply and demand dynamics. Internally, firms establish an economy governed by a command-and-control structure. CEOs and managers direct resources and coordinate activities without the need for repeated bargaining, contracts, or external price-setting for every internal interaction.

The firm, as conceived by Coase, performs then an arbitrage function between these two economies. Firms leverage their internal economy to avoid the inefficiencies of the external market, while still interacting with the external market to acquire resources and sell products. As Coase saw it, firms internalize transactions for two primary reasons: to reduce certain costs associated with market transactions such as information gathering and to mitigate costs introduced by regulations. The first rationale, transaction costs, has garnered the lion’s share of attention from economists, becoming a cornerstone of the economic theory of the firm.

The second rationale concerning the role of regulation has been largely overlooked and forgotten. Since so much has been written about the first, I will focus on the second.

In the fourth part of his original article published in 1937, Coase argued regulatory burdens, such as taxes, compliance costs, or government interventions, often incentivize firms to internalize more transactions or vertically integrate to escape market regulations: ‘Transactions organized within a firm are often treated differently by Governments or other bodies with regulatory powers’ (Coase, Reference Coase1937, 391). He highlighted the case of sales taxes. His specific example is no longer relevant, but the principles he pointed out, namely that firms have incentives to internalize not just to reduce transaction costs but also to minimize regulatory burdens, remains salient.Footnote 29 Indeed, he argued, ‘Regulation would bring into existence firms which otherwise would have no raison d’être’ (Coase, Reference Coase1937, 391).

Over time, the trajectory of the interpretation of the theory of transaction cost theory has shifted. The contemporary focus is no longer on Coase’s broader considerations but emphasizes the problem of contractual weaknesses, such as incomplete contracts, enforcement difficulties, and information asymmetries (Allen, Reference Allen and Clark2005; Barzel, Reference Barzel, Anderson and McChesney2003; Rindfleisch, Reference Rindfleisch2020; Williamson, Reference Williamson2010; Williamson and Winter, Reference Williamson and Winter1993).Footnote 30 Coase’s analysis was targeted at national firms, but what many people forget is that his original article was published well before the concept of the MNC as a distinct field of research emerged in the 1960s.

When MNCs expand, they do more than simply enter new markets; they also extend their internal economies across borders. The arbitraging of the two economies identified by Coase – the internal and the external – has been internationalized as well. Internalized economies, known as intra-firm trade, now operate on a global scale and account for a significant portion of global commerce. According to some estimates (Borga and Zeile, Reference Borga and Zeilen.d.; Lanz and Miroudot, Reference Lanz and Miroudot2011; Ylönen and Teivainen, Reference Ylönen and Teivainen2018), approximately one-third of global trade consists of intra-firm transactions. This internal economy of intra-firm trade is, as I go on to show, the primary arena where jurisdictional arbitraging schemes are conceived and executed.

In support of the proposition that subsidiaries are independent legal persons, governments introduced strict rules on investment and transfers among subsidiaries, such as the arm’s length principle (Avi-Yonah, Reference Avi-Yonah1995; Eden et al., Reference Eden, Dacin and Wan2001; Wittendorff, Reference Wittendorff2010). The principle stipulates transactions among affiliated entities – whether located in the same country or other jurisdictions – must be conducted as if they were independent parties. While firms aim to internalize transactions to reduce costs and maintain control, they often find themselves constrained by the need to apply market-like logic within their own internal networks. This creates an internal economy that functions with elements of market pricing, contracts, and competitive pressures, despite being housed within a single corporate ‘organization’. So if MNCs cannot avoid the complexities of the market within their own boundaries, what benefits do they gain from engaging in large-scale intra-firm trade?

The logical answer points to the increasing importance of arbitrage. From a Coasian perspective, the large and expanding internal economy of the firm evolved not merely to bypass external markets but also to arbitrage certain types of regulations. As I explore more fully later, this core function – or potential interpretation – of Coase’s theory has been overlooked for a variety of reasons.Footnote 31

Another common mistake is to subsume regulatory costs under the broader umbrella of transaction costs, thus obscuring critical distinctions (Marjosola, Reference Marjosola2021). In Chapter 1, I challenge this conflation, arguing regulatory costs must be treated as conceptually distinct from transaction costs. By making this distinction, we can develop a theory of the limits of arbitrage, a framework that has remained elusive as long as these concepts are treated interchangeably.

The field of International Business (IB), which is shaped by economic theory, tends to discuss MNCs as singular as well. The origins of IB can be traced to a question posed by Hymer (Reference Hymer and Letiche1982): Why would companies pursue FDI, assuming the risks of unfamiliar and often volatile foreign markets? Soon thereafter, an interest in ‘multinational corporations’ gathered traction, and the new field of IB was born, developed by scholars such as John Dunning and Raymond Vernon (Dunning, Reference Dunning1988; Dunning and Lundan, Reference Dunning and Lundan2008; Vernon, 1981, Reference Vernon2013) who relied heavily on historical evidence.

The development of IB was a theoretical breakthrough, as it created a framework for understanding MNCs. However, this achievement was overshadowed by a significant epistemological oversight: MNCs were initially assumed to function like domestic firms, simply operating on an international scale. The IB literature provides plausible yet overly general and abstract answers to the question of why MNCs have so many subsidiaries and why they are spread around the world. A common explanation is the overarching concept of ‘operational flexibility’ – a term frequently invoked but seldom unpacked in detail (Andrews et al., Reference Andrews, Nell, Schotter and Laamanen2022, Reference Andrews, Fainshmidt, Fitza and Kundu2023, Birkinshaw and Morrison, Reference Birkinshaw and Morrison1995; Desai, Reference Desai2009; Fagre and Wells, Reference Fagre and Wells1982). IB focuses on how MNCs overcome economic risks in highly competitive and political volatile markets, such as exchange rate volatility, differences in consumer demand, and competition in foreign markets, managing asymmetric information, market failures, and transaction costs while exploiting their firm-specific advantages (e.g., technology or branding).

There is no doubt that many subsidiaries are established, as scholars have demonstrated so well, for operational flexibility. It is a strong and valid explanation, addressing the practical need for adaptability in production, marketing, and logistics. However, it is not the only answer. Setting up an investment involves more than deciding what will be produced or marketed. It also requires careful consideration of taxation, regulation, and the protection of investment from political or economic instability. Naturally, these two goals often intertwine, with sophisticated corporate planners seeking to seamlessly blend regulatory arbitrage strategies into their broader operational frameworks.

The most developed body of literature on jurisdictional arbitrage is that on taxation. Studies often focus on specific case studies or legal frameworks, providing detailed analyses of arbitrage strategies and their implications. Examples include transfer pricing, treaty shopping, and hybrid mismatch arrangements (Beer et al., Reference Beer, de Mooij and Liu2020a; Desai and Dharmapala, Reference Desai and Dharmapala2009; Eden, 1998, Reference Eden2009; Greggi, Reference Greggi, Kraft and Striegel2019; Grubert and Mutti, Reference Grubert and Mutti1991; Loretz et al., Reference Loretz, Sellner, Brandl, Arachi, Bucci, van’t Riet and Aouragh2017a; Wittendorff, Reference Wittendorff2010). The literature stresses jurisdictional arbitrage schemes are often deeply embedded in the architecture of corporate groups, making it challenging to identify and isolate them from an external perspective. Internally, these practices are often well understood by management teams but hidden from external stakeholders, regulators, and even shareholders. Firms deliberately obscure those practices, claiming the operational logic and the structural design of corporate groups are proprietary knowledge.

Opacity is the operational word here (Lambooy et al., Reference Lambooy, Diepeveen, Nguyen, de Rijk, van der Vlugt and van de Walle2013). While such strategies are ostensibly legal, the complexity of corporate arrangements – such as multi-tiered subsidiary networks, hybrid entities, and interwoven financing arrangements – makes it challenging to identify where, how, and to what extent arbitrage is taking place. The problem of opacity has given rise, in turn, to a literature that seeks to classify and typologize arbitraging schemes. A notable contributor to this literature is the Organisation for Economic Co-operation and Development (OECD), which has developed broad typologies of these schemes in its Base Erosion and Profit Shifting reports (Avi-Yonah, Reference Avi-Yonah2019; Crivelli et al., Reference Crivelli, Mooij and Keen2015; OECD, 2013). These works tend to discuss isolated instances of regulatory or tax loopholes, however, rather than framing them within a broader theory of arbitrage.

It is unfortunate that much of the tax and regulatory arbitrage literature fails to make explicit connections to the fields of law and accounting. Economics and IB tend to view MNCs through the lens of contract theory of the firm, but contract theory is considered by a majority of legal scholars to be simply incorrect (Blumberg, Reference Blumberg1993; Ferran, Reference Ferran1999; Orts, Reference Orts2013a; Robé, Reference Robé2011).Footnote 32 A doctrinal confusion is further obscured because of the tendency to confuse ‘firm’, which is an analytical category, with ‘corporation’, which is a legal concept.Footnote 33 Contract theory, argues Eva Micheler (Reference Micheler2021), is not wrong per se; it simply harkens back to the older doctrine of corporation prior to the US Supreme Court rulings of the late nineteenth century.

On the surface, the debate between economists and legal scholars about the nature of the firm seems pedantic or purely theoretical. It is not. The legal literature asks questions that economists and IB then attempt to answer. What is the rationale behind the incredible complexity of corporate group structures? Why are corporate groups organized as clusters of independent companies? Why do states fail to decree against such structures? Is arbitrage pervasive in these organizations or not? Economists like to say there is no free lunch, and jurisdictional arbitrage certainly comes with its own set of opportunities and constraints.

One stream of legal and business studies is more practical and targeted at managers and professionals – the use of entity law in strategy (Eicke, Reference Eicke2009a; Karayan et al., Reference Karayan, Swenson and Neff2002). A second stream is entity law and arbitrage. A great deal has been written about the abuse of entity law, particularly the legal fiction that each subsidiary within a corporate group is an independent legal person (Avi-Yonah, Reference Avi-Yonah2019; Beer et al., Reference Beer, de Mooij and Liu2020a; Blumberg, Reference Blumberg1993; Ferran, Reference Ferran1999; Greenfield, Reference Greenfield2008; Muchlinski, Reference Muchlinski2001; Robé, Reference Robé, Robé, Lyon-Caen and Vernac2016). At a more granular level, arbitraging schemes rely on exploiting jurisdictional divergences in areas such as entity classification laws (e.g., partnerships versus corporations), tax residency rules, and the like. This includes the ‘play-acting’ of independence, where entities are legally constructed to appear autonomous while remaining functionally interconnected (Dine, Reference Dine2012a; Kerber, Reference Kerber1999; O’Hara and Ribstein, Reference O’Hara and Ribstein2009; Palan and Phillips, Reference Palan and Phillips2022).

The legal and accounting literature also suggests jurisdictional arbitrage extends far beyond simple tax or regulatory exploitation, emphasizing the critical role of entity law and corporate legal organization in facilitating these practices (Blair, Reference Blair2002; Blumberg, Reference Blumberg1993; Micheler, Reference Micheler2021; Muchlinski, Reference Muchlinski2001; Robé, Reference Robé2011). Entity law, the treatment of each subsidiary as an independent legal person, allows corporate management to decide on lines of control of their subsidiaries. This literature tends to stress the importance of the enablers, the roles played by specialized legal and accounting teams that are either embedded within the corporate group or provide consultancy services and carefully design structures to maximize arbitrage opportunities (Mitchell, Reference Mitchell2008; Sikka, Reference Sikka2003; Sikka and Hampton, Reference Sikka and Hampton2005; West, Reference West2018). These specialized teams understand the opportunities for arbitrage created by legal divergence but rarely articulate them as part of a broader theoretical framework. Instead, they focus on navigating specific rules and systems, implicitly embedding an understanding of arbitrage into their analyses. The strategic use of these mechanisms is often codified internally in documents and models, but this information is not made available to external stakeholders.

Lawyers and accountants excel at dissecting the operational and structural mechanisms of jurisdictional arbitrage, but few if any step back to examine how these practices fit within the broader historical and systemic evolution of capitalism. Jean-Philippe Robé’s Property, Power, and Politics (Reference Phillips, Petersen and Palan2020) develops a comprehensive analysis of the interplay between property rights, corporate organization, and social power. Robé situates his work within the broader context of global capitalism and focuses on the evolving concept of property as a key factor in the distribution of social and political power. He emphasizes property is not just a passive asset but a social relation that grants power to its holders. In the modern era, this means those who control corporate property – large multinational firms – wield enormous influence over both economic and political systems. The legal frameworks that organize corporate ownership and control are crucial to understanding how power is distributed. Robé’s work is closely associated with the CORPLINK project, especially its aim to provide a theory of global power by examining the legal evolution of property and the corporate form. This approach is highly relevant to understanding jurisdictional arbitrage and its role in reshaping global power dynamics.

In The Architecture of Markets, Neil Fligstein (Reference Fligstein1993) argues firms must use institutional strategies to control their competitive environments, shaping market structures in ways that favour long-term survival and success. Fligstein alludes, in fact, to arbitrage as a form of control in the US context:

Corporate activities could be strictly limited by state action, but as interstate commerce expanded, states lost their ability to control corporations from a different state. Managers and entrepreneurs of the largest interstate firms became capable of dictating the rules by which they did business (Fligstein, Reference Fligstein1993, 23).

Similarly, Kimberly Hoang’s Spiderweb Capitalism (2022) provides a detailed study of how Vietnamese capital utilizes corporate shells and subsidiaries to navigate a challenging regulatory and economic environment. This perspective shifts the focus away from seeing corporations as monolithic entities and towards understanding the decisions, actions, and strategies of the individuals who direct and manage corporate activities. These individuals – managers, executives, board members, and investors – use their positions within the corporate form to exert influence and maintain control over market conditions, regulations, and competitive dynamics.

In fact, there have been many opportunities to conceptualize arbitrage as more than a series of isolated, artificially constructed phenomena. What consistently stands in the way is the lack of a theory – or rather, the absence of a framework robust enough to situate arbitrage within a broader systemic understanding. The broader theoretical framework I develop in this book is inspired by the work of Thorstein Veblen and John R. Commons.

What This Book Is About

The central argument of this book is that jurisdictional arbitrage schemes arise from the tension between historical forces and forward-looking imperatives. While powerful business actors push for global market integration, this process takes place within a fragmented political landscape, where each authority operates according to its own domestic priorities, vested interests, and unique institutional frameworks, rules, and laws. The tension between the weight of the past and the demands of a future-oriented economy where value is speculative necessitates the creation of schemes that are ‘past-proof’. These schemes aim to minimize disruptions from the past, embodied in states and their regulatory frameworks, ensuring historical constraints interfere as little as possible with projections of future value.

These schemes exploit the gaps, loopholes, and omissions in the laws of one country to arbitrage the laws and regulations of another. In this book, I present findings from the analysis of corporate EMs derived from the CORPLINK project. The bulk of the book explores the techniques and schemes of arbitrage, focusing on the underlying logic that connects the CCMCE model to the separation of actual exchanges from their legal registration. Specifically, I examine the intricacies of tax arbitrage, liability arbitrage, and corporate reporting arbitrage, uncovering how these strategies are employed within the modern corporate landscape. I also explore why Europe, despite the European Commission’s explicit objectives, has emerged as the central node in global corporate arbitrage. Additionally, I examine whether the United States government has developed sophisticated arbitrage strategies as a geopolitical tool to leverage other states.

A study of jurisdictional arbitrage is inherently a study of power in the modern world. The book concludes with a question that my friend and mentor Susan Strange often posed: Qui bono? Who benefits, and who loses, from arbitrage? This final inquiry seeks to unravel the broader implications of these practices for global governance, economic equity, and power dynamics.

The Technique of Equity Mapping

Surprisingly, little is known about the internal legal structures of MNCs, or, as Lewellen and Robinson describe it, ‘the way subsidiaries are arranged within ownership structures’ (Lewellen and Robinson, Reference Lewellen and Robinson2013, 3). One field that has traditionally attempted to map the internal organization of firms is due diligence.

The concept of a singular, unified MNC holds limited practical relevance for due diligence, as it offers no foundation for substantiating claims of improper fund allocation. Investigating corporate bankruptcies requires a granular mapping of how funds were allocated, by whom, and whether these allocations adhered to economic principles or involved fraudulent activity.