Key messages

Chapter 2.1 tackles risk pooling. Risk pooling refers to the way prepaid funds are combined and then used to provide care for a covered population. Pooling is an often underappreciated aspect of health financing which shapes the overall health system. Key learning includes that:

Pooling prepaid funds is central to progressing towards universal health coverage (UHC). It bolsters health system efficiency and equitable access to services.

Pooling maximizes redistributive capacity and allows the health system to align funding with needs and social priorities.

Having multiple risk pools can be problematic, particularly if:

○ pools have too few people;

○ if everyone in the pool has similar risks; and

○ if there is no redistribution of resources across pools.

Structuring and managing risk pools well can offset problems associated with fragmentation by:

○ reducing duplication or overlap, making purchasing and service delivery more effective;

○ avoiding disproportionately large financial burdens falling on particular pools; and

○ minimizing risk selection and “cream-skimming”, whereby pools try to exclude high-risk (and therefore high-cost) individuals.

Policy-makers can use a range of pooling strategies to enhance efficiency, equity and access but path dependencies, politics and context matter. Options include:

○ encouraging the integration (i.e. consolidation or merger) or coordination of pooling schemes;

○ boosting funding for less endowed pools;

○ equalization through risk adjustment across pools via direct transfers between schemes;

○ making membership compulsory; or

○ aligning data systems, benefit packages and payment infrastructure across pools.

Introduction

We first outline what pooling is and its purpose. We explain how risk pooling works and introduce the problems of incomplete risk pools and pool fragmentation that are particularly apparent in low- and middle-income countries (LMICs) and are key to much of what follows in the rest of chapter.

Pooling as a health financing function is concerned with the assignment of prepaid funds to the institutions that purchase health services on behalf of some or all of the population. As such, pooling is a policy instrument: pooling structures and related mechanisms can be changed as part of policy reforms to achieve wider objectives.

Pooling interacts significantly with other health financing functions. For example, revenue raising affects the overall magnitude of prepaid funds, i.e. the total amount that can be pooled. While pooling determines the redistributive potential of any given level of prepaid funds, redistribution only happens when the funds are spent, i.e. during purchasing. The method of pooling chosen can affect the overall efficiency of the health system: pooling structures can influence the extent of duplication or overlap in purchasing and service delivery, and help make purchasing incentives more or less coherent. However, even with a good pooling structure, poor purchasing or budgetary discipline can limit the amount of redistribution that actually takes place. So to properly understand pooling, it is important to understand how it aligns with other health financing functions.

The primary purpose of pooling is to maximize the redistributive capacity of prepaid funds and is referred to as risk pooling, which allows the decoupling of payments from service use. This means that the cost risks that ill health poses to individuals and households are also in effect pooled. Though risk pooling aims to redistribute resources according to need, it is difficult to predict an individual’s or a household’s future need for health services. Without mitigating measures in place, potential illness and disease expose individuals and families to huge health and financial risks. For this reason, societies have developed various approaches towards pooling risk, so that the randomness is shared across a broader population, reducing the aggregate risk confronting that population. Such pooling is in effect an insurance function that usually entails redistribution from healthy to sick and, to the extent that poorer persons are in worse health, from wealthy to poor (Smith & Witter, Reference Smith and Witter2004).

Risk pools can be formed at different levels of a health system and vary in size, from the whole nation to a local hospital which pools risks by offering free or subsidized access to a group within the local population. The nature of risk pools in a particular health system may result from historical path dependency and wider political decisions as much as explicit design choices. No society lacks pooling, nor is pooling ever complete – so all are on a spectrum of degrees of pooling which places individuals at a greater or lesser level of exposure to risk, often in the form of out-of-pocket (OOP) payments or barriers to access for health services.

Decisions about risk pooling are crucial to the operation of the health system and health care markets. However, recent papers argue that risk pooling issues have received much less attention than other health financing functions in the global literature (Mathauer, Saksena & Kutzin, Reference Mathauer, Saksena and Kutzin2019). Pooling also raises inherently political issues, as it is central to the distribution of costs and benefits across different social groups. In many LMICs, risk pools are incomplete – individuals remain exposed to coverage and payment risk – and fragmented, which means that an individual may get very different protection depending on which pool they belong to. Pool fragmentation means that, for any given level of prepaid funds in a health system, there are barriers to redistribution (e.g. across insurance funds, or across levels of government). Therefore, pool fragmentation undermines risk pooling because the more fragmentation that exists in a system, the lower the redistributive capacity of the aggregated prepaid funds. Fragmentation thus contributes to inequities in access and use, poor financial protection and inefficient purchasing (WHO, 2010).

High reliance on OOP payments, which is a feature of many low-income settings, is an indicator of limited fiscal capacity that leads to low levels of public funding for health, and hence constrains the aggregate level of funds that are pooled in a health system. Poor pooling arrangements limiting the redistributive capacity of these funds (either across individuals or time) compound the problem.

In this chapter, we first examine what makes a good pooling system and then go on to describe how risk pools are organized in practice and the strategies adopted to overcome their problems of incompleteness and fragmentation. We present a case study of Thailand’s reform of its pooling system and draw on this and other work on the political economy of health reforms to understand how best to manage the politics of pooling reforms.

What makes a good pooling system?

Pooling creates opportunities for the efficient redistribution of resources to support equitable access to needed services, with financial protection arising from any given level of prepaid funding (Mathauer et al., Reference Mathauer2020). Ensuring redistribution at the system level and across different pools is key to making progress towards UHC. Closely related health financing actions are to decouple contributions, such as taxes or premiums, from health needs or risks, and move towards uniform benefits packages (WHO, 2010).

However, fragmented pooling creates its own set of problems. It often contributes to inequities, where people in different pools have different benefit entitlements; for example, de facto through varying levels of per capita funding across pools. It can contribute to health system inefficiencies, too, due to a duplication of tasks that results in higher overall health system administration costs, as well as, potentially, less effective purchasing, if providers are able to shift costs between multiple, uncoordinated purchasers (Mathauer, Saksena & Kutzin, Reference Mathauer, Saksena and Kutzin2019).

Desirable attributes of pooling

In response to the problems of fragmentation, the World Health Organization’s (WHO’s) health financing progress matrices highlight two main desirable attributes for pooling: integrating, or at least coordinating, pooling schemes and increasing the ability to redistribute available prepaid funds according to needs and social priorities (Jowett et al., Reference Jowett2020). Where there are multiple pools, risk adjustment between them can ensure that average per capita expenditure on health, adjusted for the pool members’ health risks, is equal or similar across pools, but this option is relatively complex to administer. Other corrective mechanisms include establishing common benefits packages and merging data systems across schemes.

Further desirable attributes of pooling include:

compulsory membership (to avoid adverse selection, whereby only those with high needs join the pool, and cream-skimming, whereby insurers encourage membership only by healthier members, for example);

payments by members being unrelated to utilization (otherwise it negates the sharing of risks); a large population size (to ensure diversity of risks and ability to cross-subsidize during health shocks) (Mathauer et al., Reference Mathauer2020); and

administrative feasibility (for example, for health insurance, the pool has to have the capacity to check on membership, ensure that entitlements are fulfilled, avoid illegitimate calls on funds and check on provider performance).

There are a number of rudimentary universal indicators of the success of risk pool harmonization arrangements (Smith & Witter, Reference Smith and Witter2004), which include:

the number of different pools in a health system and the population affiliated to or benefiting from each;

variations in expenditure on the package of care: the extent to which there exist differences between risk pools in the expenditure per member, which may influence the real level of benefits available for covered individuals in each pool;

variations in quality: the extent to which there exist qualitative differences in health care received by members of different risk pools; for example, in the form of waiting time variations, which may be a consequence of the level of per capita subsidy;

variations in OOP spending: the extent to which there exist differences between risk pools in the OOP charges experienced by individuals in receipt of health care.

Some observed variations between pools may be due to factors other than risk pool fragmentation, such as variations in purchaser efficiency. However, large variations in such indicators offer strong prima facie evidence of the harmful consequences of fragmentation.

Evidence of poor risk pooling

Challenges can be seen in LMICs, in particular, regarding a lack of effective coverage and pooling demonstrated in variations of utilization, quality of care and financial protection (which also relate to health care supply features). WHO’s 2019 UHC monitoring report, for example, found that in many systems poor people have lower coverage even for basic services such as immunization, sanitation and antenatal care (WHO, 2019). For these basic services, rural areas generally have lower coverage than urban areas. In addition, the global incidence of catastrophic health expenditure (Sustainable Development Goal indicator 3.8.2), defined as large OOP spending in relation to household consumption or income, increased continuously between 2000 and 2015. As risk-rated private insurance affiliation is low in most LMICs, it may pool risks over time but not across individuals, while community-rated health insurance schemes have typically suffered from adverse selection, whereby only the poor and sick join and risk pooling collapses (Ekman, Reference Ekman2004).

Fragile and conflict-affected settings have higher need and unmet need for health services as well as significantly higher OOP expenditure, external dependency and health-related impoverishment (Witter et al., Reference Witter2020). Overall financing for health tends to be low and also inequitably distributed, and low trust and conflict undermine pooling and prepayment, as well as the stable institutions to oversee risk pooling. Risk pools therefore tend to be highly fragmented and with poor coverage, with populations further segmented where there are substantial refugee and displaced populations, having varying protection provided by different humanitarian agencies, each with their own mandate, resources and focus. These complex emergencies have been particularly challenging in the WHO African and Eastern Mediterranean regions.

The indicators of pool harmonization outlined above mask those who cannot afford to use care, which can be a prima facie indicator of inadequate risk pooling arising primarily from shortcomings on the revenue raising and supply side. Analysis shows that the incidence of catastrophic health expenditures or impoverishment due to OOP health expenditures (using global poverty lines) is negatively correlated with the share of compulsory prepaid and pooled expenditure (government spending) in total current health spending, and hence positively correlated with the share of OOP health spending in total health expenditure. The 2019 report also found that the majority of household OOP health spending is related to medicines and outpatient care, and not necessarily to larger but more infrequent hospital bills (WHO, 2019). Further recent research has highlighted challenges for specific populations, such as women, female-led households and the large informal employment sector, when health coverage is linked to employment (Vijayasingham et al., Reference Vijayasingham2020). It is important to focus on the indicators of failures in practice, rather than de jure pronouncements. The experiences of pool members can often vary considerably from their theoretical entitlements.

The objectives embedded in the concept of UHC offer good guiding principles for the design of risk pools, and the financial transfers between them. UHC is a set of health policy objectives that applies to an entire system and population, so calls for harmonization of benefits across that population (see Chapter 2.2).

How can countries organize risk pools?

Risk pooling typologies and features

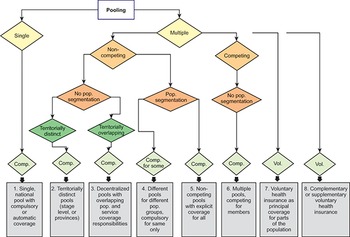

A paper examined key features of risk pools for health care globally, highlighting the importance of the basis for enrolment (whether it is voluntary, compulsory or automatic), the number of risk pools, whether they are in competition, whether they cover specific population segments, and the extent of territorial overlaps. This led to eight different scenarios which can operate singly or multiply within a country (Fig. 2.1.1).

Pooling arrangement classifications

Comp: compulsory; Pop.: population; Vol: voluntary.

Figure 2.1.1 Long description

The flowchart starts with Pooling, and divided into 2 branches: Single and Multiple. Single moves to a compulsory measure: 1. Single, national pool with compulsory or automatic coverage. Multiple branches to Non-competing and Competing. Non-competing branches to No population segmentation and Population segmentation. No population segmentation branches to Territorially distinct (compulsory: 2. Territorially distinct pools (stage level, or provinces)) and Territorially overlapping (compulsory: 3. Decentralized pools with overlapping pop. and service coverage responsibilities). Population segmentation splits to a compulsory-for-some measure (4. Different pools for different pop. groups, compulsory for same only) and another compulsory measure (5. Non-competing pools with explicit coverage for all). Competing moves to No population segmentation, with a compulsory measure: 6. Multiple pools, competing for members. Further, there are two voluntary measures as well: 7. Voluntary health insurance as principal coverage for parts of the population. 8. Complementary or supplementary voluntary health insurance.

Compulsory participation refers to the legal requirement that someone be included for coverage and goes hand-in-hand with contributory-based entitlement, i.e. there must be a specific contribution made by or on behalf of the covered person. The “on behalf” may come from public budgets for specific groups of individuals whose participation is fully or partially subsidized, or it may come from traditional insurance contributions that cover individuals beyond the contributor (e.g. family members).

Automatic participation is typically based on legal or constitutional obligations, and the basis for entitlement is noncontributory, deriving from citizenship, residence or other factors, such as poverty status, etc. As such, automatic entitlement is typically solely funded from general budget revenues. However, mandatory coverage is often not implemented effectively because it is difficult to enforce, while the de facto experience of automatic entitlement often differs from the de jure promise due to underfunding relative to promised entitlements, leading to supply shortages, informal payments or both.

Enforcement is a particular problem in countries where a large proportion of the population works in the informal economy. The result is that even where it is legally mandatory for the entire population, it is de facto voluntary coverage. For example, Ghana instituted “compulsory” social health insurance (SHI) in 2003 with numerous population groups covered by national subsidies, but by 2021 only 35% of the population was covered (Smith & Witter, Reference Smith and Witter2004) (for multiple reasons, including residual access costs for these groups and reimbursement delays). This means that de jure pooling is not translated into de facto pooling of risks, leaving these population groups still exposed to access and financial barriers for health care.

What are the different ways countries can administer risk pooling? Are there key contrasts in decentralized versus centralized administration, or those formed by sociodemographic characteristics?

Most countries have limited and multiple funding sources and use different pools to fund specific programmes, with voluntary health insurance (VHI) sometimes existing in parallel. Where pools are multiple, they may compete for members (for example, through offering greater convenience or quality), or may cover different populations, such that there is no competition between them. Although there is an argument for competition driving choice and innovation, the evidence for this in practice is weak, and cream-skimming can occur, which adversely affects progress towards universal health coverage (Mathauer, Saksena & Kutzin, Reference Mathauer, Saksena and Kutzin2019). For those countries with insurance competition, such as Germany, the Netherlands or Switzerland, considerations need to be made about what combination of ex ante risk adjustment and ex post reconciliation will adequately reduce insurer interest in cream-skimming.

A one-pool system

However, some countries do have a single main national pool funded from general government revenues, covering the whole population. This may be administered by a ministry of health, through budgets to providers or via an independent purchasing agency. The agency, often a health insurance fund, may pool general tax revenues and insurance contributions from employers and employees. Both of these options offer maximum redistributive capacity from prepaid funds because of the integration of the main public revenue sources (social insurance contributions and general revenues, or just general revenues), into a single fund. A growing number of countries, for example, Kyrgyzstan and Moldova, have reformed their pooling arrangements to unify multiple funding sources into a common pool. In such cases, it is important to build on existing capacities and ensure that there are clear roles for any new fund and lack of duplication with the ministries of health, alongside a strengthening of the purchasing functions (Kutzin, Cashin & Jakab, Reference Kutzin, Cashin and Jakab2010).

Employment-based pools

Pools may be segmented based on employment status (e.g. formal employment), demographic status (e.g. older people or young), health status (e.g. pregnant women), location (targeting specific regions) or wealth (certain schemes being only affordable to higher income groups, or government-funded programmes for low-income persons, for example). Segmentation raises risks of inequity reflected in differences in benefits across pools.

Pools based on geographical area or administrative level

Decentralization can create separate risk pools by area or by administrative level of the system (with funds covering specific services and populations at each level, although there is sometimes duplication of coverage across levels, as in the former USSR (Union of Soviet Socialist Republics), where rayons and cities within oblasts often managed overlapping health networks and budgets). This can raise efficiency, capacity and stability concerns, if risk pools are small, as well as concerns about redistribution across pools (Mathauer, Saksena & Kutzin, Reference Mathauer, Saksena and Kutzin2019). A paper on health financing in devolved settings, which included seven case studies (Burkina Faso, Indonesia, Kenya, Mozambique, Nigeria, Philippines, Uganda), concluded that devolution contributed to fragmentation of the pooling function, making equitable distribution of resources across subnational units more difficult (ThinkWell & WHO, 2022). The study authors found that subnational territories differed in terms of their fiscal capacity relative to their needs, thereby requiring fiscal equalization arrangements (this was also at the core of the pooling reforms in Kyrgyzstan and Moldova (Kutzin, Cashin & Jakab, Reference Kutzin, Cashin and Jakab2010)). Yet the existing intergovernmental grant transfers were not adequate to equalize these differences across territorial units, which is a common challenge. The authors also remarked that it is challenging to strike a balance in horizontal transfers between multiple considerations, such as the needs of health versus other sectors and allocating resources according to fiscal need, while also incentivizing fiscal effort.

Category-specific risk pools

Risk pools may be territorially overlapping but addressing different disease or condition categories. For example, in the USA it is common to find that health care costs associated with particular conditions (such as mental illness or end-stage renal failure) are “carved out” of regular risk pools, and placed in a condition-specific risk pool (Smith & Witter, Reference Smith and Witter2004). A similar approach was taken by the Seguro Popular (People’s Health Insurance) in Mexico. The intention is to remove very unpredictable but high-cost needs from the regular health care pool, and to transfer the associated risk to a higher level of aggregation (for example, from state to federal level, which has a larger population across which to share risks). However, in countries with limited health budgets, this can be regressive, with relatively small numbers of well-connected patients benefiting from support from the dedicated fund (e.g. to fund renal dialysis) while basic services used by the majority remain underfunded (Witter, Reference Witter2010).

Overcoming the inequities of fragmentation: reforms to risk pooling

Where pools cover different socioeconomic groups, this often creates fragmentation and inequities, with better protection for more privileged groups such as civil servants or the formal employment sector through social or private health insurance, while mandates for the less powerful population segments, such as user fee exemptions for the poor, are typically underfunded and face challenges of quality and coverage (Witter, Reference Witter2009). Such arrangements typically fail to redistribute effectively, especially when relying on de facto voluntary enrolment and contributions; for example, for the informal sector (Mathauer, Saksena & Kutzin, Reference Mathauer, Saksena and Kutzin2019).

Provide automatic coverage, retain separate pools

Some countries have successfully provided automatic coverage for their populations despite retaining risk pools which are segmented by population groups. For example, Thailand managed to increase equalization of funding for its Universal Coverage Scheme (UCS) and avoided eroding the existing benefits received by civil servants (Prakongsai, Limwattananon & Tangcharoensathien, Reference Prakongsai, Limwattananon, Tangcharoensathien, Chernichovsky and Hanson2009). This option can be politically easier, though while the Thai reforms introduced since 2002 have reduced fragmentation, they have not eliminated it (see the Evidence in practice section) (Mathauer, Saksena & Kutzin, Reference Mathauer, Saksena and Kutzin2019).

Risk adjustment of revenues

A few countries, such as the Netherlands, combine competition among insurers with individual choice of insurer and compulsory participation. This is commonly referred to as a competitive SHI arrangement. Each of the insurance schemes thus constitutes a separate pooling agency. A critical requirement of this pooling arrangement is risk adjustment of the revenues that go to each insurer, either from a national fund or between pools, to reduce risk-based selection and inequalities of revenues and therefore benefits across pools (Mathauer, Saksena & Kutzin, Reference Mathauer, Saksena and Kutzin2019). If effective, this risk adjustment, which is more typically found in HICs, can reduce or eliminate the consequences of fragmentation while retaining devolved administration.

VHI generally covers small population segments. Premiums are often risk rated, and voluntary insurance may offer supplementary or duplicating services to the main risk pool. Typically, members have higher incomes and entitlements. South Africa provides the most extreme example, with 42% of its health expenditure coming from voluntary insurance in 2020, but only covering 15% of the population (Mathauer & Kutzin, Reference Mathauer and Kutzin2017). Such schemes can be highly distorting, allowing enrolled members to disproportionately benefit from underlying public subsidies in terms of trained health staff and infrastructure. Supplementary insurance can fill gaps in publicly funded coverage but still risks increasing inequities unless it is covering a large part of the population (Thomson, Sagan & Mossialos, Reference Thomson, Sagan and Mossialos2020).

Mathauer and colleagues set out four options for addressing fragmented risk pools, which can be used individually or in combination (Mathauer et al., Reference Mathauer2020).

The first is consolidation or merger of pools, with the aim of increasing their size and the diversity of members’ health needs and risks, so reducing administrative costs while at the same time increasing purchasing power and internal redistributive capacity. Consolidation may occur as part of wider changes, for example, recentralization, where regional pools are merged into a national one, or as vertical merging, where funds covering different levels of care for overlapping populations are merged. It could also take the form of merging coverage of population segments, i.e. bringing together health insurance programmes covering, for example, the informal sector and mandatory schemes for public servants. This type of merger typically generates more resistance as members of some pools may view the reforms as risking a dilution of their benefits. There may also be concerns about the institutional and administrative limits to the optimal size of purchasing agencies linked to risk pools; however, effective data systems can mitigate such concerns.

Despite these challenges, some countries have managed to merge risk pools in the past two decades, including Indonesia, the Republic of Korea and Türkiye (Mathauer et al., Reference Mathauer2020). In each of these countries, the merging of pools significantly increased the risk diversity in the merged pool and was the starting point for reducing inequities in access to health services. However, in a review of these changes, authors noted that some undesirable effects also ensued; for example, when state budget transfers to finance the coverage of poor and vulnerable population groups were “captured” by better-off groups with better access to services (e.g. in urban areas) and therefore higher utilization. This reinforces the point that pooling alone only creates the potential for redistribution; other health system features have to be aligned to produce redistributive benefits. Indonesia provides a clear example of this: the Indonesian National Health Insurance Scheme, Jaminan Kesehatan Nasional, has national pooling, but there are major supply-side imbalances across the country, and at least for inpatient care, the payment methods relate to service use. Thus, the national pool is distributing to where the providers are, not to where the needs are (for example, in more remote rural areas) (Nugraheni, Mubasyiroh & Hartono, Reference Nugraheni, Mubasyiroh and Hartono2020).

A second option which may reduce the risk of those stakeholders who benefit from the status quo resisting reforms to pooling is to retain separate risk pools, but compensate for differences between them by, for example, increasing the funding to less endowed pools. Redistribution is achieved by providing budget transfers and gradually increasing these, with the ultimate aim of achieving equitable access to health services and harmonized benefit packages. Countries that have pursued this pooling reform option include, for example, Colombia, Gabon, Mexico, Peru and Thailand (Mathauer et al., Reference Mathauer2020). In these countries, reforms have substantially reduced the differences in per capita expenditure between different population groups, and thus helped to improve financial protection and equitable access to health services.

Equalization through risk adjustment across pools is a more systematic approach to ensure equal spend per capita across pools. That can occur through direct transfers between insurance agencies or via a national risk adjustment fund, but also through adjustments of fiscal equalization arrangements between areas in a devolved context (see Box 2.1.1). ThinkWell and WHO’s (2022) multi-country study of devolved health financing, for example, found that more focus on health needs (rather than health infrastructure) was required in resource allocation and revenue sharing formulae in order to protect more disadvantaged areas. Conditional grants to local administrations, as used in countries like South Africa, and central government subsidies for health insurance coverage for the poor can indirectly contribute to resource equalization across subnational territories (ThinkWell & WHO, 2022).

Prospective risk adjustment between risk pools is almost invariably accompanied by a retrospective stage in which prospective allocations are altered in the light of actual expenditure experience (Smith & Witter, Reference Smith and Witter2004). A number of arrangements exist for handling retrospectively variations in actual expenditure from the prospective budget. These include renegotiating the budget retrospectively with the central payer, running down (or contributing to) the pool’s reserves, varying the future premiums or local taxes paid by the pool members, varying the user charges paid by the patients, varying the package of benefits available to patients, and delaying or rationing health care to the population at risk. However, some of these may perpetuate inequities between pools.

From a public policy perspective, in a competitive SHI context risk adjustment needs to be sufficient to reduce or eliminate the incentive for insurers to invest in risk selection. The combination of ex ante and ex post risk adjustment is adequate to the extent that it eliminates such socially unproductive investment.

In addition, where the above are challenging to achieve, is what the authors called “as-if pooling” (Mathauer et al., Reference Mathauer2020), meaning taking measures such as harmonizing data systems, benefits packages, contracting and provider payments across pools. These actions fall outside of pooling but can mitigate the consequences of fragmentation and pave the way for future reforms to risk pools.

The role of external actors in fragile and conflict-affected settings is typically larger, and the ideal of integrating their funds into pooling arrangements to support broad packages of services may be limited by organizational policies as well as low trust in public financing systems (Witter et al., Reference Witter2020). Strategies to address this may be similar to “as-if pooling”, including stronger aid coordination mechanisms and shadow alignment. In these settings, policies to increase financial access and decrease OOP payments (for example, through user fee exemptions, health equity funds, health insurance, vouchers and cash transfers, conditional or unconditional) play an increased role, given the combination of low, unstable and inequitable incomes; social and cultural barriers to access, and high health needs.

Finally, making membership of risk pools compulsory is an important reform, although for lower income populations it will likely require public funding to support its realization. Reviewing experiences in reforming risk pools in transitional economies, Kutzin and colleagues observed that early health reformers had identified a number of expected gains from the introduction of compulsory health insurance (Kutzin, Cashin & Jakab, Reference Kutzin, Cashin and Jakab2010). These included higher funding levels, improved accountability, greater efficiency and higher quality, through new payment incentives and the separation of purchaser from provider. Experience with the introduction of compulsory health insurance in LMICs elsewhere in the world suggested, however, that such reforms tend to worsen inequities and duplication by setting into motion the establishment of separate, segmented health financing (and often delivery) systems for the insured (often formal sector) and uninsured (often informal) populations. The core lesson for implementing compulsory risk pool membership reforms is thus to pool contributions from SHI schemes with general revenues from the outset, to ensure that contributors and non-contributors are in the same pool with the same benefits, rather than starting with the formal sector and then attempting to expand into the informal sector from there.

A sequencing of reforms will be contextual but might start with consideration of merger possibilities, depending on the political economy, which we discuss below. If those are not possible, compensation or equalization should be considered, which may meet less resistance as they do not directly threaten existing favoured group interests. This was the course taken by pooling reforms in Thailand, for example and Mexico (Mathauer et al., Reference Mathauer2020). If neither of these approaches is possible, then mitigation strategies such as harmonized data systems to prepare for future pooling reforms could be pursued.

Evidence in practice: the UCS in Thailand

The following example is based on the analysis carried out by Bertone, Pholpark and Witter (Reference Bertone, Pholpark and Witter2022).

Political background

During its modern history, Thailand has alternated periods of democracy with others of military rule. A major turning point was the 1997 Constitution (the “People’s Constitution”), which was the first to be drafted by a popularly elected Constitutional Drafting Assembly and entailed a reformist approach and renewed attention to civil liberties and public participation. This had important effects on the political and cultural context and influenced the results of the 2001 elections, paving the way for social reforms, including in the health sector.

However, the struggle to get the Constitution passed became intertwined with the Asian Financial Crisis of 1997. Thailand was one of the fastest growing economies in Asia between the 1960s and 1990s, but experienced cyclical economic crises, including the 1997 crisis, which led to the country relying on an International Monetary Fund support package to ensure recovery. The country completed the repayment of loans in 2003, but it took almost 10 years for gross national income per capita to reach 1997 levels. However, despite political and economic crises, social and health development has always been prioritized in Thailand, with a focus on pro-rural health development to help fight poverty.

In the 2001 elections, the newly formed, populist Thai Rak Thai Party led by Thaksin Shinawatra agreed with a proposal by health reformists to introduce a universal coverage programme that appealed to the mass electorate and won with a large popular mandate. Since 2001, the political history of Thailand has been dominated by the rise and fall from power of former Prime Minister Thaksin Shinawatra, and conflict over the rising military influence in politics.

Risk pooling context and reforms

Prior to the 2000s, there were multiple health risk pools in Thailand, including (i) the Civil Servant Medical Benefit Scheme (CSMBS) for government employees; (ii) SHI for private sector employees; (iii) a Health Welfare scheme for low-income households; (iv) a health coverage programme for older people; and (v) a public subsidized voluntary scheme for other population groups. Some 30% of the population was not affiliated to one of these explicit coverage programmes.

In 2002, the National Health Security Act was passed to set up the UCS, to provide essential health services for the population not covered by the civil servant and private sector employees’ schemes. This resulted in consolidation, with the low-income scheme, older people scheme and voluntary scheme all eliminated and explicit affiliation extended to all. This was later followed by the extension of health coverage to the stateless population in 2010, to ensure health coverage through annual budget subsidies for 0.45 million people, mostly marginalized minorities living in the mountainous northern provinces. Subsequently, there were several attempts to harmonize the three public health insurance schemes (CSMBS, SHI and UCS), without success. A new (successful) attempt started in 2012, with a focus on emergency medical services. Migrant VHI to provide health coverage to informal/undocumented migrant health workers was implemented in 2014, but with limited success because the scheme remains voluntary and needs to be purchased at designated one-stop service centres only in provinces where migrants reside.

Key features of the UCS

The aim of the creation of the UCS was to extend health coverage to the entire population. The scheme was tax-funded, initially with a co-payment of Baht 30 per visit or admission (which was then terminated in November 2006), to cover automatically those who were not covered by the civil servants’ or private employees’ schemes. It established a comprehensive benefits package, including a negative list, with a primary care focus and gatekeeping function. Strategic purchasing was introduced with a fixed annual budget per member (capitation based) and a cap on provider payments (age-adjusted capitation for outpatient services, and diagnosis-related groups within an annual global budget for inpatient services), which aimed to put a “hard” limit to the budget and contain costs. The reform also introduced a provider-purchaser split through the establishment of the National Health Security Office, responsible for purchasing health services, and its multistakeholder governing body, the National Health Security Board. The Board is chaired by the Minister of Health, and includes government officials, including the Ministry of Finance; representatives of local governments, nongovernmental organizations, health professionals and private hospitals; and experts in insurance, medical and public health, traditional medicines, alternative medicines, financing, law and social science. Overall, the reform has been considered a major success and has improved access to essential health services, especially for the poor and all the informal sector. It has decreased catastrophic expenditure and increased the satisfaction of the UCS’s beneficiaries and health care providers.

Analysis of the political economy of UCS reform

Analysis of the political economy of the UCS reforms using the WHO framework highlights the role of the change team in the design, adoption and implementation of the reforms. Technically strong, politically savvy and well-connected, the change team was ideologically committed to UHC, but seen as politically impartial and free from conflicts of interest. The change team was a close-knit group with key contacts inside and outside of the Ministry of Public Health. The change team demonstrated not only their technical skills and knowledge, but also their experience in navigating bureaucracy and governmental politics and their capacity to mobilize different sources of power at political, societal and international levels and use effective strategies to move the reform agenda forward. They saw themselves (and were in practice) policy entrepreneurs or “match makers” between evidence and politics.

Political leadership played a key role – UHC was promised in the Thai Rak Thai political manifesto and generated great popularity for the party, enabling it to win the election. Civil society was also a key player, strongly aligned to the UCS and working in alliance with the change team. The Ministry of Public Health was not a strong advocate as its financing authority was transferred during the reforms to the National Health Security Office as new purchaser. However, health workers were supportive of the scheme, having witnessed directly the access difficulties of the poor and informal sector workers, especially for high-cost interventions. The private hospital association and clinics were worried about losing business to public providers and wanted to maintain fee-for-service charging. The Ministry of Finance was neutral on the scheme, being mainly concerned with budget neutrality. International partners held less leverage, in that Thailand is not an aid-dependent country, but played a role in relation to normative power, with some players (such as the World Bank) being opposed initially, while others (such as WHO) were supportive and were mobilized by the change team.

In relation to strategies to manage the process of adoption, use of evidence and information was very important, along with coalition building, and enhancing the legitimacy of the policy (for example, by connecting to traditional social values in Thailand). Mobilizing support (for example, by creating alliances with civil society) and addressing opposition (for example, from beneficiaries of existing schemes who feared dilution of their benefits, from the Ministry of Public Health because of changes to its role, and from private providers) by meeting some of their demands were also key. In Thailand, the change team made strategic use of the evidence available and its capacity to generate locally relevant knowledge, based on experience and international literature. In relation to external actors, the change team drew on international learning early in the process, but also used international approbation to cement the reforms as the Thai experience was shared internationally and received a strong positive reaction. The successful reform of the scheme also highlights more overt political adoption strategies, including changing the decision-making processes (for example, shifting budget decisions to the Prime Minister to bypass challenges from the Ministry of Finance). Some of these, such as the establishment of the National Health Security Board and later the National Health Assembly, not only increased supporters for these reforms but also likely changed the margins of manoeuvre for future reforms.

Thailand’s reforms: summary

Thailand has managed to provide near-universal access to essential health care by establishing a risk pool on the basis of automatic entitlement which covers all who were not already members of the civil servants’ and private sector employees’ schemes, including the previously unaffiliated 30% of the population. The UCS replaced three previously existing schemes but did not change the status of those for civil servants and private sector employees. Instead, it compensated for the existence of those two by extending coverage to the population groups that did not have access to them and gradually increasing the level of per capita subsidy to the new UCS as a means to reduce inequities in benefits, which was a more politically expedient route. Tangcharoensathien and colleagues (Reference Tangcharoensathien2019) highlighted this as an example of path dependency: although a merger of pools would have been ideal, compromises had to be made to reduce threats to existing beneficiaries of other schemes, enabling overall gains despite reduced efficiency and equity relative to an optimal design.

The political economy of risk pool reforms

Risk pooling reforms are inherently controversial and political as they rely on a shared objective to move towards UHC, which itself depends on the existence of social solidarity – a willingness by the better-off and healthier to redistribute resources to the less well-off and sicker – and a feeling of connectedness with social groups despite their diversity (of ethnicity, religion, gender, region, caste, etc.). An investigation into solidarity for health risks across 24 countries in 2010 found wide support for assisting the poor and sick with health care costs, but only to some extent (most supported subsidies of half of the cost or less) (James & Savedoff, Reference James and Savedoff2010). Although results varied by country, there was also evidence of self-interest in that healthier respondents were less likely to express solidarity. This suggests mixed support for pooling reforms that focus on redistributing benefits. These reforms are also quite public in that the changes in entitlement commonly require legislative change too, which is more complex to manage than reforms in other areas of health financing which can be achieved through technical reforms (e.g. adjusting provider payments).

WHO has developed a framework for analysing the political economy of health financing, which is structured by six main domains (Sparkes et al., Reference Sparkes2019). It is interesting to consider each of these in relation to risk pooling and the kind of strategies which might enable more successful risk pooling reforms. The section below draws on work by Özçelik and colleagues (Reference McIntyre, Doherty and Gilson2003) to describe the potential political dynamics that play out during pooling reform, as well as strategies that were undertaken in a set of countries that successfully moved forward reform to manage these dynamics.

Interest group politics

Reforms are hard to achieve when perceived losses are focused on organized or higher profile groups, while potential winners are diffused. Where there is an entrenched private sector, or high-income group within society, that has claimed certain benefits and sees itself as standing to lose from reforms to pooling (as is the case with the challenges made to the adoption of the National Health Insurance in South Africa) the resistance can be protracted and well resourced (McIntyre, Doherty & Gilson, Reference McIntyre, Doherty and Gilson2003). The communication strategies around these reforms (and reform resisters) are often quite sophisticated, as the perceived losses may not accrue to the beneficiaries themselves, but rather to enterprises that enable coverage. This can be connected with inherent insurance market failures where relevant, whereby cream-skimming or risk profiling occurs by private sector actors in a way to maximize their profits rather than providing benefits for the whole. Strategies to manage interest group politics include building coalitions with groups that might favour reforms, engaging civic and professional groups before reforms and during the consolidation phase after they are implemented, mobilizing public support and ensuring a participatory approach to policy development. In recognizing the potential opposition to pooling expansion or consolidation, health reform leaders employed these strategies in Mexico and the Republic of Korea (Kwon & Reich, Reference Kwon and Reich2005).

Bureaucratic politics

Pooling reforms may threaten the role, resources and interests of influential organizations such as ministries and social insurance agencies, leading to blocking and other forms of resistance. This is particularly relevant in many LMICs where the government civil service often comprises a large share of the formal sector. This can create both a potential conflict of interest where a scheme already exists that extends preferential benefits to civil servants, and can also lead to capture, whereby SHI for the formal sector is put forward as a first step towards universal coverage reform. For example, these dynamics were present in Türkiye, but it was possible to put strategies in place to mitigate these bureaucratic interests. Beginning in 2001, plans were put in place to consolidate five pools under a new umbrella organization (Sparkes, Bump & Reich, Reference Sparkes, Bump and Reich2015). Strategies to manage resistance from the Ministry of Labour and Social Security, which operated the largest social security system in the country, aimed to persuade, placate and reassure those whose interests it represented. These strategies included: developing a clear vision in the Ministry of Health and its reform team; establishing an interministerial committee to voice and incorporate concerns from key ministries; using close personal relationships with the Prime Minister to address resistance; bundling the health care legislation with measures to address Ministry of Labour and Social Security concerns about retirement ages; and guaranteeing that no one would lose benefits through the reforms.

Budget politics

Reforms to pooling are often seen as presenting public finance risks to the Ministry of Finance in cases where the focus is on expansion of coverage expansion, while the Ministry of Health is seen as an advocate for more resources (though not always an effective advocate). To proactively manage these two sets of concerns, in Mexico, during the design of the Seguro Popular (People’s Health Insurance), the Ministry of Health set up an Economic Analysis Unit to produce technical evidence to support its plans and built a reform team within the ministry with technical, political and communication skills (Gomez-Dantes, Reich & Garrido-Latorre, Reference Gomez-Dantes, Reich and Garrido-Latorre2015). By institutionalizing the relationship between the Ministry of Health and the Ministry of Finance, concerns around fiscal sustainability could be incorporated into the reform plans as a way to build a coalition and assuage resistance. However, despite these efforts, the actual efforts to establish a single, unified risk pool at each state level did not succeed in Mexico.

Leadership politics

In the face of competing political and ideological interests, getting support from the head of government and making the risk pooling reforms a central part of a wider political manifesto can be effective, as illustrated in the Thai UHC reforms and, less successfully, in Mexico ((Tangcharoensathien et al., Reference Tangcharoensathien2019; Gomez-Dantes, Reich & Garrido-Latorre, Reference Gomez-Dantes, Reich and Garrido-Latorre2015). Framing policies in line with local historical and social values is key here. For example, in Ethiopia, it has been argued that the policy idea of health insurance secured elite commitment due to its fit with deeply held ideas within the ruling coalition concerning the importance of self-reliance and resource mobilization for development (Lavers, Reference Lavers2019).

Beneficiary politics

The implications of reforms in relation to changes in contributions and in benefits are not simple to communicate to the public and can also be subject to political capture. Where coverage has been extended to new population groups through expanded risk pools, this has often been communicated through political campaigning, making electoral promises through the media. This was the case in Ghana with the introduction of its National Health Insurance Scheme, which has gained traction with the public (previously widely opposed to the “cash and carry” user fee) to the extent that it is hard to envisage new governments or parties being able to withdraw the offer (Novignon, Lanko & Arthur, Reference Novignon, Lanko and Arthur2021). Democratic politics tend to encourage policies which increase coverage, though there are risks where this is done without adequate funding or implementation support (Witter & Adjei, Reference Witter2007; Yates, Reference Yates2009).

External actor politics

External actors can play a crucial role in the design and implementation of health financing policies in LMICs (Chi & Bump, Reference Chi and Bump2018) and often have distinct agendas, which are sometimes in competition with one another as well as domestic policies. In particular, historically, global health institutions have funded priority programmes, creating fragmentation of risk pools by disease area (Biesma et al., Reference Biesma2009). Domestic fiscal capacity is a key factor, but even in aid-dependent settings, domestic reform teams can influence external actor policies through the development of clear national strategies, evidence and capacity to deliver, as well as drawing on their local legitimacy. A number of key pooling reforms, such as the National Health Insurance Scheme in Ghana and user fee removal in Uganda, took place despite, not because of, external actors, although they were engaged in technical support after the decision had been taken. However, despite these reforms, in both countries vertical, disease-oriented risk pools persist to this day, showing how powerful these interests can be in a system.

Policy relevance and conclusions

Risk pooling is critical for reducing the exposure of individuals and their families to health-related financial risks and securing equitable access to health services, alongside other relevant health financing reforms as described. Historical performance in relation to UHC has been significantly associated with the level of pooled financial resources for health per capita (Global Burden of Disease Health Financing Collaborator Network, 2018). As risk pooling becomes more integrated, the uncertainty associated with health care expenditure can be reduced. Its importance is well recognized, as reflected in the WHO Health Financing Progress Matrices, which set a norm that pooling structures and mechanisms across the health system enhance the potential to redistribute available prepaid funds, and that health system and financing functions are integrated or coordinated across schemes and programmes (Jowett et al., Reference Jowett2020).

Risk pooling also affects and is affected by other health financing functions, including the health financing institutions, their governance, information flows and trust placed in them (Smith & Witter, Reference Smith and Witter2004). Revenue-raising policies determine the prepaid share of health expenditure and whether funds are raised equitably (Mathauer et al., Reference Mathauer2020). Pooling reforms are necessary but not sufficient to achieve redistribution if appropriate arrangements for purchasing health services are lacking (Kutzin, Cashin & Jakab, Reference Kutzin, Cashin and Jakab2010). These arrangements include setting suitable and coherent incentives for providers to deliver quality and equitable health care services. Provider payment methods and amounts of payments to health care providers should in general (unless there is a need for enhanced benefits) be the same for all members of the pool, independent of whether people pay direct contributions or not.

Misalignment of pooling and purchasing arrangements is common, including in systems funded from tax revenues with universal entitlement on a noncontributory basis, in which the health budget is the dominant pooling arrangement; for example, if budgets and funds are poorly allocated across programmes and areas (and hence those programmes and areas become distinct pools) or if payment methods reflect and reinforce the distribution of service providers and infrastructure rather than population health needs. The nature of the benefits package is also key to the type of risks pooled (and the degree to which they are predictable or not) and the extent to which any cost-sharing obligations effectively limit the OOP liability of individuals relative to their capacity to pay. Effective public financial management procedures are also key, including those that determine how budgets are formulated and implemented.

Wider epidemiological factors are also crucial for risk pooling – as chronic illnesses rise, for example, risks become more predictable for some population groups (for example, those who are HIV-positive or diabetic), which present predictable health care needs. These reduce the redistributive capacity of the pools; a substantial emphasis on prevention and health promotion will therefore be appropriate to reverse that trend and maintain risk pooling.

The evidence is clear on different pooling arrangements, their effects and how they can be mitigated in theory (through the various strategies for defragmentation, linked to appropriate changes to other connected health financing function), but understanding how to manage the politics of reform is more challenging, and this is an important focus for evidence gathering at present (Witter et al., 2024). Work is underway to document comparative lessons in how to overcome political economy blockages to reforms in different settings (and how these link to context features, such as the history and political settlement), as well as how shocks, such as the COVID-19 pandemic, may (or may not) be used to enable reforms (Witter et al., 2025). Lessons on sequencing, engagement strategies for the wide range of actors (internal and external) with power to advance or block agendas, and the capacities needed will be important to the next wave of pooling reforms globally.Footnote 1

Open access

Open access