I cannot keep sitting here for another night watching for my child to stop breathing.

For Carol and Jason, parents of four children in Arizona, the emergency department visit for their four-year-old daughter felt overwhelming. They were scared about their daughter Emma’s worsened ability to breathe. And they were scared about the medical costs that would ensue, given their limited economic means. Their UnitedHealthcare plan was provided through Jason’s employer, an airline.

One day, Emma developed a sore throat, and because of her thinness, they could see her tonsils protruding out of her neck. Their doctor informed them that because of the significant enlargement of her tonsils, she would require a tonsillectomy, and they were referred to a specialist. In fact, one of her tonsils was so abnormally large that it was closing in on her windpipe and there was even concern that it was cancerous. However, they would have to wait a week for the operation.

“It was scary, and being just four years old, it was hard for her to communicate to us what was happening as she gasped for air,” Carol recounted of the wait for surgery. “I was watching her in the dark and she stopped breathing several times. Then, she would wake up crying and upset.”

For two consecutive nights, Carol stayed awake watching Emma try to sleep. But, fearful of yet another night when Emma would stop breathing, especially as it seemed to be getting worse, Carol broke down in tears and took Emma to the local emergency department. The doctors administered steroids which shrank her tonsils a bit, and when Emma was able to relax, there was enough of an airway that she could breathe again. Two days later, the surgery was performed, and the biopsies were negative.

The problem was that when she and Jason went to the emergency department’s intake, Emma’s condition was classified as a “sore throat,” and not a breathing difficulty amid severe tonsillitis. Consequently, approximately five weeks later, they received a bill for $8,800 for the emergency department visit because UnitedHealthcare did not deem treatment of a sore throat to be medically necessary, nor did it seemingly fall within the scope of the “prudent layperson standard” in coverage of emergency care.

Jason was sure it had to be a mistake. “The frustrating thing was they kept saying it was non-emergent and I kept trying to figure out, How is our daughter not being able to breathe not a medical emergency? We would have been absolutely devastated financially if we had to pay in full. We don’t have anywhere near the access to that kind of money. We don’t have savings. We could have lost our house.”

“To me, that was sad because I wouldn’t take my daughter to the ER for a sore throat,” Carol reflected of this. “It’s so expensive that we don’t even take them to urgent care for anything. Most of the time, we just hope for the best.”

This was neither the first nor the last time that Carol and Jason struggled to pay for their children’s needs, whether clothes or health care. Insurance challenges made it difficult for them to take their children to their annual wellness visits, lest their providers perform tests that their insurance would decline to cover. “Four kids times a $25 copay is $100 just to see the doctor. One time we got another bill for $8.36 per kid because UnitedHealthcare denied payment for the eye exam even though they just stood in the hallway, looked at a chart at the end of the hallway, and read off the chart. They charged for that, and the insurance company wouldn’t pay for it. We don’t have an extra $32. The nickel and diming is too much.”

Appealing UnitedHealthcare’s denial was far from easy when raising four children, taking time and energy that they did not have. “You can’t run around copying and faxing things when you’re looking after kids.” Enraged by the denial, Jason took to Twitter initially just to vent, but the tweet went viral, at which point Jason became hopeful that UnitedHealthcare would respond and be shamed into assisting him with this predicament.

That’s exactly what happened. After a reply to Jason’s tweet, UnitedHealthcare contacted Carol and Jason. Ultimately, the hospital resubmitted the billing under different codes, and after a few weeks, they were left only with the cost of the emergency department copayment.

Carol observed that it felt like the insurer “hoped that people won’t complain. They’ll just go, ‘This is terrible, but I have to pay it.’ But as a low-income family, there’s no chance in the world that we would have been able to pay that. But we know health is important, and we made the choice to protect our kids insurance-wise. After all of that, getting that $8,800 bill was heart-wrenching on top of the other stress.”

The effects of this denial would extend well beyond the month that it took to rectify it. There would be dozens of times that they waited in pain to go to the emergency department because of money and wondered, “Is this worthy of going to the emergency room? Will we get another huge bill? Sometimes we just deal with it and hope for the best.”

“I really think they make it so difficult that people just give up. And I find myself giving up too when they tell me these things aren’t medically necessary,” Emily reflected of her experience with coverage denials and subsequent efforts at appealing.

Emily, a forty-nine-year-old disabled woman in Palm Beach County, Florida, formerly did correspondence work for the governor, in addition to working as a therapist and a health care case manager. Given her background, Emily thought that it would be relatively easy to navigate the health care system to support her needs through her privatized Medicaid plan through Humana. Nothing could be farther from the truth.

“I think it makes it that much worse to be honest,” Emily reflected of this irony. “I know what their job is, and I know when they’re lying to me, and half the time, they’re making stuff up as they go along. It’s so infuriating.”

No stranger to the American health insurance system, Emily has epilepsy, takes antidepressants, and has a foot deformity that precludes her from walking with any semblance of ease. She can sometimes use a walker, though it strains her greatly. Like most Medicaid enrollees in most states, Emily is covered by a private managed care insurer, despite being in a public health insurance program. Her plan will not cover the cost of a wheelchair. If she attempts to wear shoes, she develops cuts and sores on her feet, which sometimes get infected and necessitate intravenous antibiotics in the emergency department. After seeing multiple podiatrists, she pursued a referral to a foot surgeon who could correct the condition without resorting to amputation.

Despite numerous complications from the deformity, the surgery to correct her condition was denied because it was deemed cosmetic “as though I just want my toes to look pretty,” and thus outside the scope of her plan benefits.

“I’m not walking again. My feet drag and get bruised,” she emphasized. While a rehabilitation center helped her to regain some function, her insurer suddenly withdrew from Palm Beach County, leaving her without anyone to cover her ongoing medical needs. She would be out of options.

“It makes you feel completely impotent and ineffective and it’s dehumanizing …. We’re talking about four years where I can’t walk. Four years between forty-four and forty-nine. Those are prime years, and I’ll never get that time back. I’ll never recover what it did to my life. And it’s emotionally devastating to constantly get these letters of denial, saying you’re not worth it.”

Looking ahead to a possible diagnosis of oral cancer, Emily has already elected not to pursue chemotherapy. “If the fight to get coverage for diagnostics is this hard, can you imagine how hard I’m going to have to fight to get coverage for treatment? That’s not how I want to spend my final days.”

The reality is that few, if any, are immune to these challenges.

When Mark and his wife Annie enrolled in her employer’s health insurance plan with Blue Cross Blue Shield of Georgia (Anthem), they were relieved to learn that their plan would cover infertility testing and treatment, which would otherwise cost tens of thousands of dollars. Before pursuing intrauterine insemination (IUI) cycle treatments and invitro fertilization (IVF) treatments, the couple consulted with Emory Healthcare’s financial counseling office, which confirmed after communicating with Anthem that the pursued treatment was within their plan benefits and thus would be covered in-network. They could not foresee the insurance challenges that they would face over the course of these treatments.

Healthy thirty-four-year-old attorneys, they were both highly educated and financially comfortable. They had consulted with their insurer and the hospital. They knew the system as well as patients might be expected to.

Yet after covering the IUI procedure without incident, Anthem declined to cover the egg retrieval on the ground that Annie’s plan did not cover this care, leaving them with a $13,213 bill.

What would next unfold would be a bureaucratic nightmare made more complicated by the timing of their IVF procedures such that simply postponing care until the issue was resolved would be infeasible. There would be several more appointments over the course of which the eggs would be fertilized, grow into embryos, and be transferred into the uterus. Because of Anthem’s denial, Mark and Annie could not proceed with the scheduled treatment dates (including the embryo transfer) until Anthem paid the claim or until Mark and Annie supplied on a self-paid basis the $4,341 cost of the embryo transfer.

Supplying a large sum of money is no easy task for most Americans, who cannot afford an unexpected $1,000 bill,1 and Mark and Annie were fortunate in this respect. Though confident that Anthem would reprocess the claims, they had to pay the hospital $4,341 with the promise of reimbursement from Emory Healthcare upon Anthem’s claim payment. So would begin Mark and Annie’s navigation of not one, but two health care bureaucracies: the insurer and the hospital. Mark spoke with a customer service representative who could find no basis for the IVF coverage denial, and Anthem reversed its denial about two weeks later, but not without costs: they had charged the payment for the egg retrieval, incurring credit card interest while they awaited claim resolution and later, delays in hospital reimbursement.

Carol and Jason’s, Emily’s, and Mark and Annie’s are but three of the stories that, along with the data that I describe below, shape my analysis of health insurance coverage denials and how this insurer practice deepens health and economic inequality by imposing unevenly distributed administrative burdens (or the costs of navigating programs, the benefits of which may be kept of reach). The diversity of these stories highlights not only the profound disruptions that coverage denials can have on patients’ health and economic lives, but also the broadly American experience of these everyday insurance barriers.

That is, the average American sees a physician four times annually. These visits might lead to the ordering of a scan or procedure, or the prescribing of a new medication, which might be among the 10 percent of prescriptions dispensed that are brand-name (and therefore more expensive than generic alternatives).2 Each interaction with the American health care system presents opportunities to experience barriers not only to care (e.g., due to physician shortages in one’s community), but also to coverage even if one is enrolled in an insurance plan. Though the notorious fragmentation of the American health insurance system makes it challenging to know exactly how many denials occur, one estimate in the Wall Street Journal put the total at a whopping 850 million claims per year.3 And while no patients are immune from experiencing denials, I argue over the pages that follow that their effects are more pronounced for patients from marginalized groups. And these burdens don’t only keep care of out of reach for many Americans: they also weaken patients’ sense of trust in the health care system on which they rely.

This chapter highlights the scope of this policy problem of a less discussed dimension of underinsurance – health insurance coverage denials – and the political context that contributes toward this practice, which over the course of this book I argue undercuts patients’ (especially marginalized patients’) health and economic security. Before evaluating the health and economic impact of this insurer practice, it is helpful first to consider what coverage denials are, and the political context fueling privatization, from which this insurance practice emerges and comes to impact American patients.

Understanding Denials in the American Health Care System

A notorious irony of the American health care system is that despite an ostensible goal of cost containment, it often drastically overspends. The United States spent 17.7 percent, or nearly a fifth, of its gross domestic product (GDP) on health care in 2024 (projected to grow to 19.7 percent in 2032), with total health care spending reaching $4.9 trillion in 2023.4 Yet, for all these rising health care costs, not only is there significant wasteful spending (whether on administrative costs or the prescribing of medical care that is of low or questionable value), but also there are overall poor population-level health outcomes when looking at such subjects as life expectancy, infant and maternal mortality, chronic disease, and avoidable deaths.5

Moreover, in addition to an estimated 25.4 million non-elderly adults being uninsured in 2024,6 the underinsured rate was 23 percent in 2024.7 For these 23 percent of Americans, the health insurance plan in which they are enrolled is inadequate, whether due to high health plan deductibles or other high out-of-pocket medical expenses (excluding premiums). Thus, these individuals are still exposed to substantial financial risk if medical needs arise. This can lead patients to forego care or else struggle to pay their medical bills if they do utilize their health plans in the most expensive health care system in the world.8 Indeed, The Commonwealth Fund finds that the highest rates of medical bill problems and medical debt were reported among adults who were underinsured or who lacked continuous health insurance coverage, and 57 percent of the underinsured reported that they avoided getting needed medical care due to cost.9 It is in this context of high costs and inadequate coverage that health care expert Shannon Brownlee observes, “It’s not as if we haven’t tried to fix the system …. Instead, we’ve decided to put up with an unfair, dysfunctional, and spectacularly expensive system.”10

We often hear talk of Americans being uninsured or underinsured, which makes it challenging for them to access health care when they need it. This book looks at a more specific barrier: that of health insurers deciding whether to cover prescribed medical care (whether a prescription drug, surgery, a scan, an emergency department visit, or other care). This is a story of coverage denials, which contribute to underinsurance in a way that has historically been overlooked. This dimension of underinsurance is the inability to access care within one’s plan benefits not because of cost per se, but because of insurer decisions not to supply the needed coverage, whether because it is “not medically necessary,” is “experimental or investigational” for the patient’s condition and thus outside the scope of health plan benefits, “lacking in the required prior authorization” (also known as pre-certification, or pre-approval for coverage of health services), or for other reasons on which I elaborate in Chapter 2. These determinations are made even more complicated by the opacity of medical necessity definitions, which in turn create uncertainties for patients and physicians alike.

It is this medical necessity on which political scientist Daniel Skinner focuses his superb scholarly attention, observing the intensely political context in which medical necessity is defined to the consternation of professional associations, which have tended to resist oversight of physicians’ assessments of their patients due to concerns about autonomy. Ongoing medical necessity debates can “collectively amount[] to a persistent uncertainty about the basic mechanisms and aims of medical decisionmaking,”11 which is no longer solely between patients and their physicians, but rather with the insurer ultimately determining courses of treatment. In this context, Skinner observes persistent uncertainty about the fundamental aims of medical decisionmaking, the repercussions of which are at the heart of my analysis because patients can and often do get caught in the middle between their physicians and insurers (and are themselves typically poor judges of medical necessity).

The story of shifting risk from corporations (in this case, health insurers) to the public is a familiar one, confronted notably by political scientist Jacob Hacker, who observes in the context of economic insecurity that “a myriad of risks that were once managed and pooled by government and private corporations have been shifted onto workers and their families … creat[ing] both real hardship for millions and growing anxiety for millions more.”12 This disrupts individuals’ economic (and in this case, health) security in ways that are reinforced by the politics of health care reform over the decades. In this setting, health insurers are mindful not only of cost containment, but also of their profit maximization, shifting risk to American patients who are faced with insecurity about whether they can access prescribed care that may be prohibitively expensive absent insurance approval. Thus, the lack of health security is felt even among those with comprehensive benefit plans because this system allows insurers to overrule physician determinations, keeping care out of reach.

These coverage denials can come pre- or post-treatment, with pre-treatment denials constituting prior authorization denials and post-treatment denials including such care as emergency department care or other claims reviewed and later deemed to be not medically necessary. Prior authorization is a common vehicle for coverage denials outside of traditional, or original Medicare, which relies on this tool very sparingly and consequently issues few denials. And as I argue throughout the book, the type of denial one experiences can have an immense impact on the patient’s resulting health versus financial fragility. Because coverage denials are driven in part by insurers’ economic concerns, it is instructive first to consider America’s largely for-profit health care system in which these delays and denials – and their associated, inequitable administrative burdens – arise.

Privatization of American Health Insurance

Political scientist E. E. Schattschneider famously declared that “a new policy creates new politics.”13 That is, policy can be both an outcome (e.g., resulting from bipartisan cooperation to adopt legislation) as well as a cause, reshaping the subsequent political environment. This observation of policy feedback rings true in the context of health insurance, where one can observe a new politics of insurance evolving and becoming increasingly entrenched, especially as new constituencies form in defense of health insurance programs. This observation is consistent with Theda Skocpol’s assessment that “policies, once enacted, restructure subsequent political processes” – that is, there is path dependence.14

Much of traditionally government-run health insurance is now in private hands, such that, according to the United States Census, just over 65 percent of Americans had private health insurance in 2023.15 This privatization fits squarely within the framework of the social policies explored by political scientist Suzanne Mettler in her analysis of the “submerged state.”16 That is, rather than federal policymakers directly disbursing benefits, they increasingly turn to less visible private entities that can obscure the role of government and create critical gaps in knowledge of individuals navigating entities such as health insurance companies. Such policies thus, through reliance on private actors, lie “beneath the surface of U.S. market institutions and within the federal tax system.”17

Americans can enroll in one of any number of types of health insurance – whether Medicare (typically for the elderly, and much of which is privatized through Medicare Advantage), Medicaid (typically for the low-income, and often administered through private insurers such as Centene or Elevance (formerly Anthem)), a private plan through the Affordable Care Act marketplace exchange, or (most commonly) a private plan through one’s employer. In fact, employer-sponsored insurance (ESI) through insurers such as UnitedHealthcare and Elevance is the primary source of health insurance in the United States, covering 63 percent of working-age adults18 and nearly half of children.19

Though this particular constellation of options has been a familiar arrangement since the Affordable Care Act’s implementation in January 2014, the prevalence of private health insurance was not always the case. It is thus instructive to consider the cost containment goals that emanated from the adoption of public insurance and subsequent concerns about runaway spending by these health programs.

For decades, America had contemplated the prospects of national health insurance, but to no avail amid concerns from the American Medical Association and others about the dangers of “socialized medicine.”20 While President Franklin Delano Roosevelt spoke clearly in 1934 about the importance of providing for unemployment insurance amid the Great Depression,21 he was more cautious when speaking of national health insurance, offering instead, “Whether we come to this form of insurance soon or later on I am confident that we can devise a system which will enhance and not hinder the remarkable progress which has been made and is being made in the practice of the professions of medicine and surgery in the United States.”22

Though the Committee on Economic Security had recommended tying Social Security to a national health care program, it was ultimately removed from the legislation, with the Social Security Act signed into law in 1935 focused more squarely on the provision of pensions, unemployment insurance, and assistance for dependent mothers and children. Much of this shift in policy has been attributed to the ardent opposition of the American Medical Association’s decrying of the prospects of “socialized medicine,” though it was ultimately likely that, even with Roosevelt’s popularity, pursuing both Social Security and national health insurance would have met with more expansive opposition that would have imperiled the passage of both programs.23

Instead, amid World War II, America witnessed the proliferation of employer-sponsored insurance, offering new protection for those in the workforce, but leaving many behind. The explanation for these developments was simple: amid wartime, America faced a critical labor shortage alongside inflation that led to the freezing of wages, so employers turned to offering health insurance as an alternative means to remain competitive. It is for this reason that employer-sponsored insurance – the dominant model in the United States today – has been characterized by some as an “accident of history,”24 though in 1943 the Internal Revenue Service acted to accelerate this trend by exempting employer-based health insurance from taxation. By 1945, 32 million people had employer-sponsored health benefits,25 offering new access to care though at the risk of perpetuating job lock, or the reluctance to leave a place of employment due to dependence on the health benefits. What’s more, the share of Americans reliant on employer-sponsored insurance would be quick to balloon to 142 million just five years later amid the post-war economic boom.26

While Social Security would prove to be unparalleled in impact, national health insurance would have to wait until President Roosevelt’s successor, Harry S. Truman, took up the mantle.

President Truman did not waste time upon assuming office. In fact, in a Special Message to Congress on November 19, 1945, he called attention to the inequities of the American health care system, in which “the benefits of modern medical science have not been enjoyed by our citizens with any degree of equality,” and laid out his preferred plan for a compulsory health insurance system to be financed through a new tax that all Americans would pay.27 Though adamant that “[t]his is not socialized medicine,” and emphasizing in a May 19, 1947 Special Message to Congress that the program protecting against the “economic threat of sickness” is “crucial to our national welfare,”28 the American Medical Association again decried this government intervention into health insurance delivery. Indeed, in 1950, the American Medical Association spent $1.1 million on advertising in 11,000 newspapers, 30 national magazines, and 1,000 radio stations, with an additional $2 million in tie-in advertising to help kill the proposal.29

President Truman would admit defeat toward the end of his presidency, after years of advocacy, and his successor, President Dwight D. Eisenhower, fueled the national opposition to “socialized medicine,” though he did not undo the progress of the New Deal. However, what this era marked was on the one hand an acknowledgment that “too many of our people find the cost of adequate medical care too heavy,” while also arguing in the 1954 State of the Union Address that access to hospital and medical services would best be assured not through government intervention, but through the initiative of private and non-profit insurance plans.30 It is hardly surprising, then, that it was during this time that America continued to cement its reliance on employer-sponsored insurance, made even more convenient by the Internal Revenue’s 1954 decision to treat these premiums as tax deductible.31

On January 31, 1955, President Eisenhower offered a Special Message to Congress, in which he recommended the establishment of a federal health reinsurance service to encourage private health insurance plans to offer broader benefits to American individuals and families.32 Thus, America would see the proliferation of privatization in the health care sector, though the seeds for Medicare would soon be planted by President John F. Kennedy, who as part of his “New Frontier” program called for the expansion of Social Security to provide for medical care for the elderly.

President Kennedy’s preferred Medical Care Bill failed by just two votes in the Senate in 1962, on the one hand constituting what he called “a most serious defeat for every American family, for the 17 million Americans who are over 65,” and on the other also indicating that the need for health insurance expansion was not lost on many within Congress and the public. President Kennedy added, “ I hope that we will return in November a Congress that will support a program like.Medical Care for the Aged, a program which has been fought by the American Medical Association and successfully defeated.”33 He would not live to see health insurance reform come to fruition, but he successfully laid the groundwork for what would become Medicare.

Taking up this cause under the umbrella of the expansive Great Society reforms, President Lyndon B. Johnson assured the nation that health insurance expansion was a “logical extension of our proven social security system” and “will supply the prudent, feasible and dignified way to free the aged from the fear of financial hardship in the event of illness.”34

Eventually signed into law together on July 30, 1965 by President Lyndon B. Johnson and through extensive compromise with influential House Ways and Means Committee Chairman Wilbur Mills, Medicare and Medicaid were designed as amendments to the Social Security Act and offered a vast expansion of health care options for the elderly and the poor respectively. This legislation was what Mills had termed a “three layer cake”: first the Johnson Administration’s proposed Medicare program (what would come to be known as Medicare Part A’s hospital insurance), then the voluntary coverage for the elderly’s physician costs (what would come to be known as Medicare Part B’s medical insurance), then finally the expansion of federal funds to states to offer health insurance for the indigent (Medicaid). As a nod to the hard-fought efforts toward this end by his predecessors, upon signing the bill into law, President Johnson spoke in Independence, Missouri alongside President Truman, saying, “No longer will older Americans be denied the healing miracle of modern medicine. No longer will illness crush and destroy the savings that they have so carefully put away over a lifetime so that they might enjoy dignity in their later years.”35

President Johnson would find in his successor, President Richard Nixon, an unlikely advocate for health insurance expansion, who offered in 1971 the Family Health Insurance Plan (FHIP), a health insurance proposal that would have mandated employer health coverage, federalized government-supported health insurance for the poor, and offered sliding scale subsidies to assist with the purchase of health insurance – a model not unlike that of the Affordable Care Act.36 However, this proposal was ultimately abandoned.

Though the sole purpose of Medicare was to expand health insurance for the elderly, cost was still a concern. It was estimated that Medicare would come with a $2.2 billion price tag, but by 1969, the initial price had doubled. It was in this setting of concern about runaway costs from government health insurance that, in 1970, pediatrician Paul Ellwood put forward the idea of health maintenance organizations (HMOs), which were perceived as incentivizing the provision of better care at a lower cost than the traditional fee-for-service model in which the plan pays the provider a specific fee for each service provided to the insured.37

President Nixon then signed into law the Health Maintenance Organization and Resources Development Act of 1973, seen as an opportunity to develop a private sector-based alternative to the national health care proposals that had been offered from the left. The legislation likewise accelerated America’s reliance on employer-sponsored insurance, not only encouraging private investment in HMOs, but requiring employers with twenty-five or more employees to offer these plans.

This would not be the last of President Nixon’s health reform efforts, though it would be his only success in this space. On February 6, 1974, President Nixon would again deliver a special message to Congress, offering a Comprehensive Health Insurance Plan (CHIP) because “gaps in health protection can have tragic consequences.” This plan was centered largely around the employer-sponsored health insurance that was housed in the private sector and relied on “maintaining a private enterprise approach” seen by President Nixon as more effective at the plan’s cost containment objectives.38 The Watergate scandal would ultimately undercut the proposal’s success and lead to his resignation later that year, on August 8, 1974, so as to avoid inevitable impeachment and removal from office.

While President Nixon was ultimately unable to achieve most of his goals of reforming America’s health insurance system, the spirit of his proposals has influenced subsequent efforts to privatize American health insurance, whether by expanding reliance on employer-sponsored insurance or by privatizing the traditionally public realms of insurance.39 Indeed, even as HMOs fell out of favor due to their narrow provider networks, they paved the way toward Medicare Advantage.

Thus, with the creation of Medicare and Medicaid, America saw a vast expansion in insurance coverage, including for marginalized populations,40 though reliance on private insurance within these spheres would soon continue to proliferate and, beginning in 1982, states began to get Section 1115 waivers from the federal government to experiment with managed care programs consistent with promoting the Medicaid program’s objectives.

These decades of efforts toward health care reform in the United States have been thorny to put it mildly, rife with competing stakeholders, and with emerging political compromises typically operating within the constraints of a for-profit health care system dominated by entities such as private health insurance companies, the pharmaceutical industry, and pharmacy benefit managers (the latter of which I discuss in greater detail in Chapter 4). That is, while the United States witnessed great progress in the number of insured individuals, the politics typically drove policy adoption toward privatization in health insurance delivery – a series of choices that would contribute not only to job lock for the large swath of the public enrolled in employer-sponsored insurance, but also to growing exposure to coverage denials as private insurers’ cost containment tools of prior authorization proliferated.

The growth of managed care over the course of the 1980s and 1990s was quite dramatic, with the US Bureau of Labor Statistics reporting just 1 percent of employer plan enrollment in managed care in 1980, compared with 81 percent by 1997, when Congress further accelerated privatization through the creation of Medicare Advantage (also known as Medicare Part C). Though these managed care arrangements were seen as advantageous from a cost containment perspective, their business model was also seen as running counter to patients’ interest in quality health care as well as disrupting doctor–patient relationships.41

It was alongside this growth of managed care that state legislatures, in response to stories of denials of coverage, began to pass laws aiming to protect health care consumers, though with mixed success in view of the health care advocacy organization Families USA.42 What’s more, state efforts toward reform were stymied in the context of employer-sponsored insurance, much of which is governed by the Employee Retirement Income Security Act (ERISA) of 1974, which preempts state laws that “relate to” self-insured (or self-funded) health plans, according to which the employer (typically, a larger employer) collects premiums from employees and directly pays for medical claims, often relying on a third-party administrator (typically a private insurer). Not only does ERISA’s preemption provision run counter to the notions of federalism embedded in many domestic policies, but also, given that the KFF 2023 Employer Health Benefits Survey finds that 65 percent of covered workers are in self-insured health plans, the limitations of state efforts to more tightly regulate health insurance practices are all too clear.

Thus, while managed care backlash manifested itself amid concerns about health care access and quality, political scientist Mark Peterson observed that the “backlash … has not … engendered a true counterrevolution,” rather leaving the status quo “deeply imbued” with managed care features.43 The failures at efforts toward comprehensive health reform in the 1990s offer insights into the persistence of the cost containment-minded practices fueling coverage denials.

Health Reforms that Weren’t.

Even the most ambitious efforts at health coverage expansion have operated within the confines of the private health insurance model. The notoriously failed efforts at expansive health care reform through the Health Security Act under President Clinton were, though critical of shortcomings to health care access, deeply rooted in the belief that health insurance could be achieved through the private sector such as through a mandate to hold insurance (whether public or private), with subsidies for those in need. Despite the absence of proposed radical transformation of the American health insurance framework, in September 1994, Senator George Mitchell (Democrat, ME) declared the bill DOA, leading health policy scholar Paul Starr to characterize this as “one of the great lost political opportunities in American history.”44

After the failures of the Health Security Act, Congress and the Clinton Administration pursued some health reforms to expand protections on the margins, though they did not confront the broader philosophical arrangement of privatization of health insurance. In 1996, Congress passed and President Clinton signed into law the Health Insurance Portability and Accountability Act to safeguard sensitive patient health information from disclosure without the patient’s consent. Just one year later, amid increased media portrayal of patients being injured by their private health plans’ decisions, Representative John Dingell (Democrat, MI) and Senator Ted Kennedy (Democrat, MA) pursued the passage of a Patient’s Bill of Rights that would, among other things, provide legal remedies for those who were denied coverage by the increasingly prevalent ERISA-governed self-insured employer-provided plans.

The absence of legal remedies was seen as a core impediment to health insurer accountability, leading Senator Kennedy to observe in a 1998 Senate HELP Committee hearing on ERISA remedies that this statutory feature was “an incentive for unscrupulous plans to deny payment for costly services, knowing they can’t be held liable for the serious injuries that result.” However, there were concerns about cost containment in the event of added insurer liability, as well as concerns about the exacerbation of frivolous lawsuits, and as Republicans turned their eye toward President Clinton’s sex scandal and the looming impeachment process, the Patients’ Bill of Rights was abandoned.45

Medicare and Medicaid Get Privatized.

It was around this time that Congress advanced legislation that set ostensibly public health insurance programs down on the path of privatization. Though private plans have been an option within Medicare since the 1970s, with sixty-five HMOs contracting with Medicare in 1979,46 it was in the Balanced Budget Act of 1997 (PL 105-33) that Congress created Medicare Part C (then called Medicare + Choice, now known as Medicare Advantage). The dual aims were to offer enrollees a greater choice of health insurance plans beyond traditional Medicare and to bring to the Medicare program the private sector’s motives of efficiency and cost savings,47 in addition to some other covered services (e.g., vision and dental care, both largely excluded from traditional Medicare). Political scientist Jonathan Oberlander observes that in expanding private insurance options for Medicare, the Balanced Budget Act was able to “fundamentally alter Medicare’s character as a public, federally operated insurance program,” such that many Medicare beneficiaries were expected to leave traditional Medicare in favor of enrollment in managed care organizations.48

In the early years of Medicare Part C, payments to plans were initially set at 95 percent of the average per-beneficiary costs in traditional Medicare. This was based on the principle that these private plans could provide care that was of both higher quality and lower cost than would be possible in traditional fee-for-service Medicare.49 Though private plan enrollment within Medicare had increased from 1.3 million in 1985 to 6.9 million in 2000, the Balanced Budget Act of 1997 limited annual payment increases in Medicare private plan capitation rates, or the fixed payments to health care providers for patients under their care, in addition to changing health insurer risk adjustment methods. Following the introduction of these changes, Medicare private plan enrollment declined to 5.8 million by 2005.50

In light of this declining enrollment, Congress sought to find new ways to promote health insurer participation and beneficiary enrollment in private plans, and the Medicare Prescription Drug, Improvement, and Modernization Act (MMA) of 2003 did just that. The MMA not only increased Medicare Advantage plan payment rates in an effort to reverse the downward trend in enrollment, but also saw the establishment of Medicare Part D Prescription Drug Plans, creating new private plan options such that by 2006 all Medicare beneficiaries had access to at least one private plan.

Not surprisingly, given these boosted rates and enhanced benefits, America soon witnessed a skyrocketing of Medicare Advantage enrollment, with 24 percent of all beneficiaries being enrolled in Medicare Advantage plans by 2010. And with the MMA’s increase of Medicare payments to Medicare Advantage, such plans were paid more for their enrollees than would be expected under traditional Medicare.51 It is this heavy reliance on private insurance in the business of Medicare benefit delivery that leads political scientists Kimberly Morgan and Andrea Campbell to characterize the MMA as a “paradigmatic example of marketized, delegated governance.”52 By 2024, 54 percent of Medicare beneficiaries were enrolled in a Medicare Advantage plan, with the share projected to continue to increase.53

Medicare is not the only ostensibly public insurance program that has been increasingly privatized, with the 1990s also seeing a growing reliance on Managed Medicaid. In fact, according to the Medicaid and CHIP Payment Access Commission (MACPAC), 15 percent of Medicaid beneficiaries were enrolled in comprehensive risk-based managed care plans in 1995,54 and the share increased to 75 percent by 2022.55 This growth is no accident, but reflects political choices by state and federal governments such that, by 1997, the federal government had approved fourteen Medicaid waivers, enrolling 8 million individuals in managed care.56

The legislation further permitted states to impose deductibles, copayments, and other cost-sharing mechanisms on Medicaid beneficiaries who were enrolled in managed care organizations (MCOs).57 This cost-sharing primarily seeks to deter overuse of health care services, a goal underlying the utilization management practices (e.g., prior authorization) on which this book focuses. Moreover, in the Balanced Budget Act of 1997 through which America saw the emergence of Medicare Advantage, Congress also allowed states to compel Medicaid beneficiaries to enroll in managed Medicaid plans without obtaining a waiver. This privatization only increased in the 2000s with Congress’s passage of the Deficit Reduction Act of 2005, which promoted state flexibility in requiring cost-sharing for Medicaid enrollees despite the (by definition) low-income nature of this patient population.

Not only are the vast majority of Medicaid beneficiaries now enrolled in a managed care plan, but nearly 52 percent of federal and state Medicaid spending in fiscal year 2023 (nearly $457 billion) was on managed care.58 With approval from the Centers for Medicare and Medicaid Services (CMS), states are empowered to require that beneficiaries enroll in a managed care plan to obtain some or all Medicaid benefits. The MCOs with which many states have these contractual arrangements are prominent figures in the private health care setting, with UnitedHealth Group, Centene, Elevance (formerly Anthem), Molina, and CVS (Aetna) comprising half of all Medicaid MCO enrollment as of 2020.59

The shift from traditional Medicaid to managed Medicaid can be attributed to a couple of central goals (however unrealized) on the part of states: to increase the predictability of health care spending and to facilitate better coordination of care. That private insurers would come to occupy such a large space in health care provision even within ostensibly public programs reflects the divided welfare state characterized by Jacob Hacker,60 which would in turn inform and constrain future health reform efforts to promote access to care. But while the extent of managed care was only growing, absent even a floor vote on the Patient’s Bill of Rights, attention shifted back from coverage denials within the insured population to expanding the number of covered persons.

Major, But not Radical.

The 2010 enactment of the Patient Protection and Affordable Care Act (ACA) (PL 111-148) expanded coverage to millions of Americans – the largest health care expansion since 1965’s creation of Medicare and Medicaid – while preserving the core private health insurance infrastructure that would now provide more expansive coverage to more Americans through the newly created marketplace exchanges and compelling the purchase of health insurance.

Indeed, on March 22, 2010, the day after the ACA’s historic vote in Congress, President Barack Obama assured the American public that, quite apart from moving away from a private insurance model to something akin to “socialized medicine” as some conservatives denigrated the Act, the ACA had instead drawn inspiration from former Republican Governor Mitt Romney of Massachusetts and operated within the constraints of the private insurance system while “reining in the worst excesses and abuses of the insurance industry” – that is, fixing what was wrong rather than targeting its elimination. President Obama continued that “long after the debate fades away … what will remain standing is not the government-run system some feared … or the status quo that serves the interests of the insurance industry, but a health care system that incorporates ideas from both parties …. [T]his isn’t radical reform. But it is major reform.”61 This pattern of reliance on private insurance – not to mention the complicated role of the American Medical Association amid proposed and enacted health reforms over the decades – is consistent with health policy scholar Paul Starr’s observation that the unique complexity of the American health care system has led liberal reformers to avoid interest group resistance associated with upending its public–private fragmentation, by instead seeking to build upon existing law and institutions.62

Of course, this fragmentation – or the multitude of administrative actors with which individuals (e.g., patients) interact to access their benefits (e.g., health care) – comes at a price. As public policy scholar Pamela Herd and her coauthors keenly observe, fragmentation not only emerges amid preferences for market-based delivery of public services, but in the process imposes added administrative costs to those navigating the system at hand (in this case, the American health care system) because “[a] person walking between organizations can get lost,”63 potentially losing out on benefits.

Though the ACA sought to constrain payments to Medicare Advantage plans so that they would be on par with traditional Medicare, the existing structure of Medicare Advantage was left undisturbed, with incentives for Medicare Advantage plans to improve quality and patients’ experiences. The result has been that the share of Medicare beneficiaries enrolled in Medicare Advantage plans has continued to climb, with the Congressional Budget Office projecting that 61 percent of Medicare beneficiaries will be enrolled in such plans by 2032. This growing reliance on Medicare Advantage is notable because, in stark contrast with traditional Medicare, 99 percent of Medicare Advantage enrollees have prior authorization requirements in their plans, and there were over 49.8 million prior authorization requests in Medicare Advantage plans in 2024.64 Barriers for the Medicare Advantage population can be particularly consequential because this population may at the same time have more pressing health needs but lack the cognitive capacity to successfully challenge health insurers’ decisions. What’s more, though the ACA’s passage saw the encouragement of Medicaid expansion to those with incomes up to 138 percent of the federal poverty level,65 it did not disrupt Medicaid’s overarching managed care arrangements, which for some can come at the price of experiencing barriers to care.

The Price of Privatization.

This privatization comes at a price for American patients. In the United States, business interests (including health insurers) are well-resourced “repeat players” in pursuit over policy control.66 According to law professor Marc Galanter in his seminal analysis of inequitable features of the American legal system, “one-shotter” plaintiffs who only infrequently navigate the legal system are disadvantaged in facing “repeat players,” or those entities (e.g., employers, insurers) who know the system well through repeated litigation. In the business setting, insurers (the “haves”) are advantaged over “one-shotter” patients who are less familiar with the ins and outs of the complex American health care system.67 Ultimately, for insurers, “the critical prize is the ability to shape the terms, distribution, and boundaries of economic governance, and the contest for this prize is waged over an extended period and on multiple fronts.”68 The nature of this American political economy story is such that these political and economic systems are linked, shaping the policy that emerges.

What these pages have sought to illuminate so far is that insurer discretion over health coverage determinations has been facilitated by decades of intentional political choices that have facilitated the growth of privatized health coverage even in the traditionally public spheres of Medicare and Medicaid. Indeed, for all the exorbitant spending that the United States contributes toward health care, Jacob Hacker aptly notes that what sets the American welfare state apart from other nations is not its level of spending, but rather the source of that investment, with many duties otherwise carried out by the government instead placed in the hands of private actors such as employers.69 This public–private framework characterizes the American health care system, in which entities making decisions about health coverage often have fiduciary obligations to shareholders, which can in turn inform how much they want to cover. In this divided welfare state, while we see the expansion of the private sector’s ability to administer and finance benefits, this system “substitutes in whole or in part for the emergence of comparable state capacity, reinforcing reliance on alternative policy instruments such as tax subsidies and regulation.”70

Cumulatively, this points to entrenchment and seeming path dependence of health insurance privatization consistent with political scientist Margaret Levi’s assertion that “once a country or region has started down a track, the costs of reversal are very high.”71 And it is with this privatization of the American welfare state that we see starkly the motivation and persistence of coverage denials (including, but extending beyond, prior authorization) largely by for-profit payers.

Unsurprisingly, this privatization has been fueled not only by the preferences of those holding political office, but also by the powerful organized interests influencing them.

The Role of the American Medical Association

While the American Medical Association (AMA) historically opposed the enactment of national health insurance, instead advancing a politics that pushed America toward health insurance privatization, it is now among the leading champions of reforming managed care practices (including coverage denials) that are harmful to physicians and their patients – namely, prior authorization. So, how did we get here?

As Jacob Hacker observes, the battle over health care has historically been as much about politics as it is about policy.72 Reform efforts can easily be stymied because, while organized interests such as health insurers have become increasingly entrenched amid America’s growing reliance on managed care, the patients harmed by this system are far more diffuse.

Many physicians have expressed consternation about the intrusion on their autonomy that prior authorization can constitute,73 with ophthalmologist and comedian “Dr. Glaucomflecken” repeatedly characterizing this practice as “practicing medicine without a medical license.”74 However, physician organizations have historically characterized reform efforts toward national health insurance as “socialized medicine” or, as with the Health Security Act, otherwise leveled critiques over potential impacts on doctors’ practice of medicine. The devil is in the details of health reform, to paraphrase the leaders of the AMA in their 1993 op-ed in the Journal of the American Medical Association, in which they argued that managed competition demands a “new public–private partnership” among the government, employers, insurers, and the medical profession.75

That is, while the AMA and other physician associations have ardently opposed the utilization management system currently in practice, rife as it is with coverage denials and administrative burdens for physicians and their patients, decades of political choices concerning advocacy efforts have contributed to the current extent of reliance on managed health care. Health policy scholar Paul Starr observes that the interest group power of physicians helped tip the balance against health insurance under the Franklin D. Roosevelt Administration, such that it was extracted from Social Security legislation.76 The AMA likewise decried as “socialized medicine” President Harry Truman’s efforts to adopt a unified national health insurance system, instead seeking to preserve the “American way,”77 despite that American way involving high uninsured rates. And the AMA additionally famously decried Medicare as “the beginning of socialized medicine” that would be characterized by bureaucratic incompetence, though they did support the extension of health insurance to low-income individuals through the creation of Medicaid. Thus, at every available turn in early-to-mid-twentieth-century health insurance reform moments, the AMA opposed universal public insurance, instead seeing privatization as a superior alternative.

Of course, the AMA’s fears about Medicare proved not to be realized: doctors and hospitals cooperated with Medicare implementation, America would not see the long waiting lines feared by some, and interest group opposition to the program disappeared as the policy became entrenched in American political life.78 Here, we see policy feedback in action, with the Medicare program’s adoption creating a new politics surrounding its defense, including the investment of the American Association of Retired Persons (AARP) in Medicare’s preservation, and leading to large majorities of both political parties supporting Medicare today.79

The AMA’s role in health care reform in recent years has been conciliatory, though it has shied away from endorsing a more radical transformation of the American health insurance system that would reduce reliance on private insurance. Though ultimately endorsing the passage of the ACA in 2010, at its 2019 House of Delegates meeting, it voted narrowly to maintain its opposition to a single-payer system, even as a growing majority of physicians come to support the policy.

It is hardly unusual to see evolving political stances, especially in a complex and fluid policy domain such as health insurance reform. But, as this section highlights, it is ironic that the organization leading the call to “#FixPriorAuth” has typically, even recently, opposed the reform efforts that would scale back this health policy problem faced by physicians and their patients. Health insurance coverage denials have been empowered by decades of political choices by politicians and powerful organized interests safeguarding a substantial private sector role in America’s health care delivery. This is all to say that the story of health insurance coverage denials in this largely managed care setting is also one of “political–economic outcomes [being] forged within … coalitional politics” because “building and transforming large-scale policies requires sustained efforts by well-organized and highly motivated organized actors, operating in interaction (and often in partnership) with other similarly institutionalized actors.”80

Having elaborated on the coalitional politics that led to this current state in managed care-dominated American health policy, I turn now to examine the types of health insurance coverage barriers to which American patients are vulnerable, focusing in particular on the role of prior authorization in the American health care system.

Types of Coverage Denials

Every time American patients utilize their health plans, they run the risk of an insurance barrier in one form or another as health insurers seek to impose guardrails on prescribing behaviors and the resulting costs of care. To understand the potential impact of managed care practices on patients, one must know not only whether one was denied coverage, but also when and why.

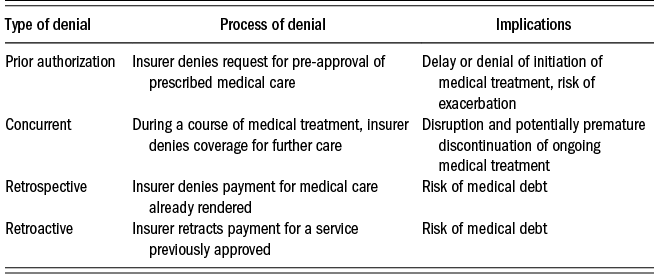

There are four types of denials that one might experience when utilizing one’s health benefits: prior authorization, concurrent, retrospective, and retroactive. Their respective processes and impacts on patients are summarized in Table 1.1.

When a prior authorization denial arises, the physician has prescribed a medical service (e.g., prescription drug, scan, procedure) that requires insurer pre-approval, or pre-certification, but which the insurer determined does not constitute a covered service, is experimental or investigational for the patient’s condition, or is not medically necessary according to the guidelines on which they rely, often developed by the medical benefits management company EviCore, which is owned by Cigna. Even though, in the notoriously expensive American health care system, prior authorization-induced denials do not leave American patients saddled with medical debt, this is a setting in which prescribed medical care is kept out of reach, at least pending appeal, thus raising the possibility that the patient’s condition could worsen. This is a significant, though by no means exclusive, mechanism through which denials are issued.

Some patients may also experience coverage denials through concurrent review processes, according to which the insurer reviews and makes judgments about the necessity of continued treatment, whether inpatient or outpatient. Adverse decisions might be rendered for any number of reasons, including the medical necessity of the treatment as well as its apparent efficacy for the patient at hand. In some cases, the insurer may decide that a lower level of care is more appropriate moving forward. When denials arise in this setting, decisions must be made as to whether to discontinue the current treatment or continue to appeal the denial, which can typically be handled by the insurer on an expedited basis if the patient is currently in the hospital.

When a patient experiences a retrospective review, they have already received their prescribed care, but the health insurer has determined that it does not meet coverage guidelines and thus they deny the claim. As with the other forms of denial, this may be because it is not a covered service, because it is deemed experimental or investigational for the patient’s condition, or because it is not medically necessary, though some denials are also elicited due to billing code errors. While the patient in this case need not worry as much about their health status – they have not been denied care – they may receive unexpected medical bills for potentially large amounts. Thus, they might find themselves among the 20 million American adults who have medical debt, with an astonishing 41 percent of patients having a broader definition of medical debt that includes debt owed on credit cards as well as debt owed to family members.81 While some of this debt is certainly attributable to high deductibles and other high out-of-pocket medical costs, some is undoubtedly attributable to insurer denials of payment.

Lastly, patients may experience retroactive denials, in which case the insurer, upon review, retracts its coverage for services previously approved or for which it has rendered payment, leaving the patient responsible for the amount. The result is that, as with retrospective denials, the patient may be asked to assume new medical debts, which can have a broader economic destabilizing effect (e.g., affecting credit).

On the basis of analysis of 124 million claims, Optum (affiliated with UnitedHealthcare) identified that nearly half (44 percent) of denials are “front-end,” such as through prior authorization.82 Given the significance of this as a vehicle for coverage denials, an in-depth analysis of this subject is critical to understanding American patients’ barriers to health care and coverage, and the ways that these processes can be especially harmful to those from marginalized groups.

Implementation and Origins of Prior Authorization

Though I examine the practice of medical coverage denials across all rationales – whether prior to or following a patient’s receipt of medical care – it is instructive to understand the origins of one of the most widely used utilization management controls: prior authorization. Prior authorization’s implementation has been to the chagrin of many, with physician researcher Andrew Miller and his coauthors characterizing the challenges of prior authorization as “among the biggest pain points for health care professionals” across America.83

Current Implementation of Prior Authorization.

According to current procedures, the prior authorization process operates in several steps. First, the provider is notified whether prior authorization is required, in order to provide the test or treatment at hand. If it is required, they submit the prior authorization request, which is then received by the health plan. The provider may then be asked to submit additional documentation to demonstrate medical necessity, which is then received by the health plan, which then adjudicates and replies to the provider, who will then be notified of the decision whether to approve or deny the health care service in question. If the care is approved, the patient can schedule the treatment or pick up their prescription, as the case may be. And about 10 percent of the time, it will be denied, in which case there is an appeal process, rife though it can be with burden to patients and their physicians.

A prominent justification for the imposition of this practice is the avoidance of unnecessary medical care – especially that which can pose risk to the patient. After all, Dr. Mario Molina, former CEO of Molina Healthcare, emphasized, “Even things like CT scans, which seem fairly benign, expose someone to something like 40 times the radiation of a chest x-ray. So do you really need that? There are some more invasive procedures, where people are sticking catheters in you, sticking needles in you, doing biopsies. Those kinds of invasive procedures often require prior authorization as well.”84 While the Peter G. Peterson Foundation finds that as much as 25 percent of health care prescribed in the United States is “wasteful,”85 contributing to the country’s notably high health costs, the question remains how best to identify which care meets this definition, and whether prior authorization is the best tool to eliminate it. Related to the health policy problem of overutilization is the effort to guard against excess health costs, and Dr. Molina noted that it is for this reason that higher-cost procedures often require prior authorization, which was put in place broadly to guard against fraud, waste, and abuse.

Despite physician consternation with insurer overreach into clinical decisionmaking, a 2019 survey by America’s Health Insurance Plans (AHIP), the national association of health insurers, found that the primary perceived objectives of prior authorization were “improve quality/promote evidence-based care” (98 percent), “protect patient safety” (91 percent), “address areas prone to misuse” (84 percent), and “reduce unnecessary spending” (79 percent), with the lion’s share of respondents perceiving positive impacts on patient care (91 percent), affordability (91 percent), and safety (84 percent),86 a stark contrast with physician perspectives on prior authorization reflected in American Medical Association surveys.

This, however, raises the question of how evidence bases for prescribed care are assessed. In keeping with Daniel Skinner’s observation about the discretion-laden nature of medical necessity, 70 percent of AHIP respondents indicated that they relied on “vendor-provided proprietary evidence-based resources.” The vendor on which insurers typically rely is EviCore by Evernorth, a medical benefits management company owned by Cigna, which scrutinizes prior authorization requests for approximately 100 million patients nationwide and “highlight[s] areas of over-utilization and unnecessary spending, and pinpoints areas of the greatest opportunity to improve care and increase savings.”87 These prior authorizations are reviewed by the hundreds of physicians, therapists, and nurses employed by EviCore to ensure that prescribed care is safe, necessary, and cost-effective.

While EviCore states that its assessment of medical necessity and appropriateness is based on large-scale statistical studies, ProPublica and Capitol Forum analysis found that EviCore’s AI-backed algorithm can yield inappropriate denials, which can in turn reap a profit for the large health insurers with which it contracts with a promise of a three-to-one return on investment.88

To be sure, prior authorizations do not necessarily result in denials. However, the American Hospital Association reported in 2020 that 89 percent of hospitals and health systems have seen an increase – often a significant increase – in denials in the last three years,89 with many of those denials occurring through prior authorization. In fact, despite prior authorization being aimed in no small part at imposing guardrails amid overprescribing, they observe that prior authorization was being applied to wide-ranging services “including those for which the treatment protocol has remained the same for decades and there is no evidence of abuse.”90 This perceived rise in prior authorization is supported by a Medical Group Management Association survey from September 17, 2019, which reflected a widespread perception (90 percent) among health care leaders that prior authorization requirements were on the rise compared with the previous year.91

One speculated reason for the growth in reliance on prior authorization is the increasing consolidation of managed care,92 which imposes on insurers financial pressures in reporting quarterly profits that may benefit from utilization management if it reduces the number of medical services paid for. In fact, as of 2022 and in the aftermath of a series of mergers and acquisitions over the course of the 2000s and 2010s, at the national level the top five health insurers control 54 percent of the commercial health insurance market share and 69 percent of the Medicare Advantage market share, an increase from two years previously.93

Insurers have three main tools with which to remain competitive amid consolidation: they can increase premiums, which is not feasible in the long run, given consumers’ finite resources; they can lower costs by fixing how much will be paid for a service (which raises political barriers with physician associations); or they can impose administrative hurdles through utilization management to reduce prescribing, especially amid consolidation-related financial pressures. Former Aetna Chief Medical Director Dr. Troyen Brennan noted, “I think anybody in the insurance industry is not going to be telling the truth if they say that anything but cost is driving prior authorization.”94

Increased reliance on prior authorization may also reflect an unintended consequence of the implementation of the Affordable Care Act. Though constituting a once-in-a-generation expansion of health coverage, compelling health insurers to cover patients with previously declinable preexisting medical conditions imposed new cost pressures for which utilization management proved a potent tool in reducing services covered by private insurers. As former Vice President of Cigna Wendell Potter reflected, “When you’re putting new requirements and new restrictions on these companies to have them operate more fairly, they are still under the same pressure from investors and Wall Street analysts to meet profit expectations. What’s left to them is the tools of managed care, which have long been available to them, which they can ratchet up. This is one of the reasons we’re seeing increases in prior authorization. It’s a means to avoid paying claims they would have paid back in the old days.”95

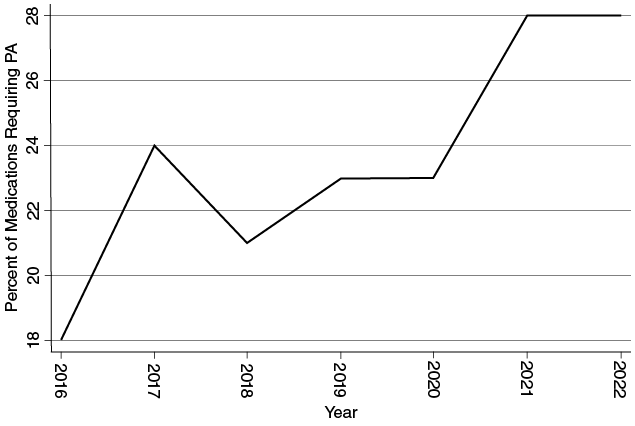

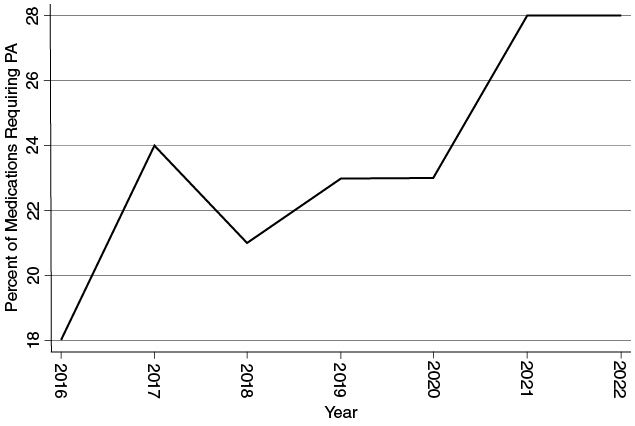

Hospital and physician impressions of increasing reliance on prior authorization are borne out by the data within the realm of prescription drugs. I analyzed the 2016 through 2022 formularies of Cigna, a major health insurer whose formularies are made public online over several years.96 Identifying the total number of formulary drugs and the total with prior authorization requirements for each year, I find that the share of prescription drugs in the formularies requiring prior authorization has increased from 18 percent in 2016, to 23 percent in 2019, to 28 percent in 2022, a marked (albeit nonlinear) increase in just six years (see Figure 1.1). This coding accounts specifically for prior authorization, and not the broader constellation of barriers that patients might face in filling their prescriptions (e.g., quantity limits on prescribing), but offers a glimpse at the increasing opportunities for patients to experience coverage denials that necessitate either delays in care (or delays in optimal care) or out-of-pocket medical expenditures.

Cigna prescriptions requiring prior authorization, 2016–2022.

Having considered the overarching role that prior authorization plays in American health insurance, I now turn to discuss the political conditions from which prior authorization originated.

The Early Years of Utilization Management.

Between 1920 and 1965, as more Americans gained access to health care through their employers’ insurance plans, health insurers’ main tools with which to contain the costs of health care involved management of who could enroll (the risk pool), what plan benefits could be offered, and controls on payments to providers.97 With advancements in medical technology and more modernized techniques came increased treatments and longer survival times with illnesses, potentially necessitating more costly and ongoing medical care. Also developing during the 1950s were retrospective utilization reviews (a distinction from prior authorization, but a foreshadower of it) to identify fee-for-service payments for what were ultimately deemed to be unnecessary hospital services.

By the early 1960s, over sixty Blue Cross insurance plans had begun to review hospital claims to assess the appropriateness of hospital admissions and, in many cases, length of hospital stay.98 These review efforts drew the ire of physicians, who suddenly saw themselves caught in the health insurance bureaucracy, needing to justify medical decisionmaking in ways that they felt impeded quality patient care.99

However, unlike contemporary practices, these earlier measures primarily reviewed the appropriateness of medical care after its receipt. Prior authorization only emerged in 1965 amid the enactment of Medicare and Medicaid and the resulting emergence of concerns about runaway costs and how to curb them.100

The goals in adopting these utilization controls were simple: to avoid the possibility of paying for unnecessary use of medical services and to encourage reasonable, less expensive health care treatments when available. To participate in Medicare, hospitals and extended-care facilities were required to operate utilization review committees that would assess both quality of care and medical necessity.101 This utilization review was typically administered by registered nurses (RNs) in acute hospital settings. But even as health plans began to review the medical necessity of hospital admissions and subsequent admission days, this was a far narrower sphere of health care than that in which such reviews would ultimately become adopted throughout the health care system.

The 1970s saw further developments in utilization review amid the development of managed care, with the primary goal of guarding against costly and unnecessary treatments. In the Social Security Act Amendments of 1972 (PL 92-603), Congress established a peer review system, in which physicians would review through physician-controlled community organizations (PSCOs) the health care services provided under the Medicare and Medicaid programs. In the mid 1970s, furthermore, Congress gained interest in surgical second-opinion programs to guard against performance of unnecessary surgeries.

Prior Authorization in the 1980s and 1990s.

In the Tax Equity and Fiscal Responsibility Act of 1982 (PL 97-248), Congress instituted utilization and quality control peer review organizations (PROs) comprised of physicians tasked with ensuring “efficient and effective administration” by performing reviews of the patterns of quality of care measured against “objective criteria which define acceptable and adequate practice.” Specifically, they would review whether specific health care services or items were “reasonable and medically necessary or otherwise allowable,” and whether the service quality met professionally recognized standards of health care. In the event of a denial, there would be an opportunity for review of the decision.

During this time, America saw substantial growth in the number and types of organizations that integrated cost containment efforts into their business model. The number of health maintenance organizations (HMOs) in the United States grew from 175 in 1976 to over 600 in 1988,102 with 25.2 percent growth between 1985 and 1986 alone.103 In backlash against managed care plans’ narrowing of networks, preferred provider organizations (PPOs) were developed, beginning in 1983.104 The irony was that this meant losing another mechanism for cost control, thus creating another incentive to use greater utilization management. This time also witnessed a proliferation of managed care organization (MCO) approaches to states’ Medicaid implementation, with the share of Medicaid enrollees in managed care more than tripling between 1987 and 1995.105

While prior authorization programs still focused on hospital admissions and high-cost procedures, with more widespread prescription drug coverage as well as pharmaceutical spending, both public and private insurers began to extend utilization management to include medication prior authorization, quantity and dosage limits, and step therapy (or “fail first”) requirements.106 The result has been the rapid spread of prior authorization requirements pertaining to prescription drugs, sometimes even for generic drugs that lack a lower-cost substitute. This thus represents a departure from earlier prior authorization efforts more squarely aimed at reducing lower-value, costly tests and hospitalizations.

By the late 1990s, dissatisfaction with managed health care fostered the emergence of a “patient rights movement” aimed at curbing managed health care plans’ ability to limit patients’ access to certain kinds of hospital and physician care.107 In fact, over thirty states passed legislation aimed at guaranteeing access to certain forms of health care absent interference from managed care plans upon coverage denial.108 However, because states are unable to regulate traditional Medicare or self-insured employer-provided plans governed by ERISA, the scope of possible intervention by means of such state legislation is limited.

All this while per capita health spending was on the rise, from $353 in 1970 to $4,845 in 2000, to eventually $12,531 in 2020.109

Unlike the private insurance setting, traditional Medicare plans require prior authorization only under a limited number of conditions (e.g., for durable medical equipment or prostheses). But, with the adoption of Medicare Advantage in the Balanced Budget Act of 1997, beneficiaries gained access to health insurance plans beyond the traditional Medicare program, and, in this setting, prior authorization became a staple of plan terms.

Prior Authorization Since the Affordable Care Act.

With the enactment of the Affordable Care Act (ACA) in 2010, Congress left intact much of private health insurers’ ability to use prior authorization, though it was prohibited as applied to emergency department visits at out-of-network hospitals, and non-grandfathered health plans (that is, plans not yet in effect as of March 23, 2010) were prohibited from requiring prior authorization to see an obstetrician/gynecologist (OB-GYN), pediatrician, or primary care provider. While preserving much of prior authorization’s role within the affected plans, the ACA also provided for both internal (within the health plan) and external (with an independent reviewer apart from the insurer) appeal processes upon denial of prior authorization, denial of other claims, or rescission of coverage. Thus, while the implementation of the ACA imposed only modest restrictions on prior authorization within a subset of health plans, it provided recourse for those who faced denials and sought to secure eventual coverage.

While it is difficult to gauge precisely what percentage of treatments are subject to prior authorization, a 2021 study of Medicare Part B (which is not subject to prior authorization requirements) by physician and health services researcher Aaron Schwartz and his colleagues found that 41 percent of beneficiaries received at least one service that would have been subject to prior authorization under a different form of health insurance.110 This highlights not only the profound differences between Medicare Part B (traditional Medicare) and other forms of health insurance, but also the broad scope of services potentially subject to prior authorization requirements, including even less costly care.

Having evaluated the conditions accounting for the proliferation of prior authorization, it is helpful to understand the factors affecting whether health insurers choose to approve or deny coverage of prescribed care within this setting.

Health Insurers’ Decisionmaking Process