1 Introduction

1.1 Overview

This Element will establish the crucial role of the 2008 financial crisis for the populist wave in Europe. We focus first on how the crisis affected voters across different occupations. And then on the consequent structural transformation of political parties and movements. Our work contributes to several strands of literature: how old and new parties compete in terms of policy platforms as a function of changes in voters’ preferences and beliefs; what determines the preferences of different occupational groups on economic and cultural dimensions of politics; and what shapes their beliefs about the value of different policies. While focusing simultaneously on both voters and parties is not unique to this Element, our conceptual framework offers a novel interpretation by emphasizing the crisis’s effects on beliefs about the feasibility and desirability of different policies. This focus provides the key to our interpretation and helps us maintain a coherent view of the broader picture.

Economic crises tend to generate economic insecurity and erode trust in existing institutions – both market and governmental. However, while the economic threats posed by immigration, globalization, and automation primarily impact low-skilled workers and their communities, financial crisis tend to have distinct effects on groups that are more exposed to dependent from financial markets, such as the middle class. We illustrate this empirically using a novel methodological approach. The extension of distrust to include the middle class is a critical development, as it signals to politicians and parties that winning over this broader group of disillusioned voters can be decisive for electoral success. Consistent with this intuition, we show that the transformation of the political supply, in terms of new and transformed parties and manifestos, happened right after the financial crisis. Moreover, the transformation and the increase in populist voting happened more evidently in countries plagued by low fiscal space, where the feasibility of inclusive welfare redistributive policies is lower. This, in turn, increases the appeal of exclusionary policy commitments, which are more easily championed by populist parties on the extreme right of the ideological spectrum.Footnote 1

The shrinking fiscal space in many European countries made the financial crisis particularly conducive to the rise of right-wing populist parties. The reason is straightforward: Identity-based protection policies typically require limited public spending, whereas the redistributive welfare policies advocated by left-wing populists became increasingly infeasible and less credible – despite remaining ideologically appealing to a significant portion of the population. As a result, the shift toward right-leaning economic policy preferences can be partly attributed to the perceived decline in the feasibility of more inclusive welfare policies.

Shifts in beliefs about the relative feasibility of left- and right-leaning economic policies have also influenced cultural-political cleavages. Macroeconomic and institutional constraints on fiscal policy have altered perceptions of self-interest about public policies, contributing to polarization along the cultural dimension. When individuals lose faith in the feasibility of inclusive welfare policies – particularly those benefiting minorities – or perceive such policies as misaligned with their own self-interest, they are more likely to support exclusionary measures that heighten cultural tensions. As belief grows that anti-immigration and nationalist identity-protection policies are the most effective means of safeguarding personal interests, support increases for politicians who promote anti-pluralism and oppose values such as diversity, equity, inclusion, and minority rights.

1.2 Some Preliminary Look at the Different Crises

We view the 2008 financial crisis and the resulting great recession as a major factor in the spread of populism in Europe during the twenty-first century. It happened before: One of the first examples of a populist policy in history is that of Urukagina, who seized power in Lagash – a city-state of ancient Mesopotamia – by dethroning his corrupt predecessor Lugalanda. This ruler promised to restore the power of ordinary people during an economic downturn while highlighting his predecessor’s lack of credibility. To gain consensus, Urukagina forgave all loans, relieving debtors while demonizing financiers. He lumped usurers with criminals to be cast out of the city (see Goetzmann, Reference Goetzmann2015).

Much of the economic literature on populism has sought to examine the effect of immigration, globalization, and automation on job destruction, primarily among low-skilled workers. This is thought to have created voter disillusionment in liberal democracies, gradually transforming the demand for policies. In this context, the financial crisis has been treated as yet another factor that enhanced voter appetite for populist policies as a response to economic insecurity. However, this approach has tended to ignore the peculiar effects and consequences of the financial crisis on the middle class.

The effects of globalization and automation on some segments of society are not uniformly negative: There are losers, but undoubtedly there are also winners. Apart from the inequality generated by job destruction and lower wages among workers affected by foreign competition or automation, consumers as a whole have benefited from lower prices of final goods and firms’ intermediate inputs.

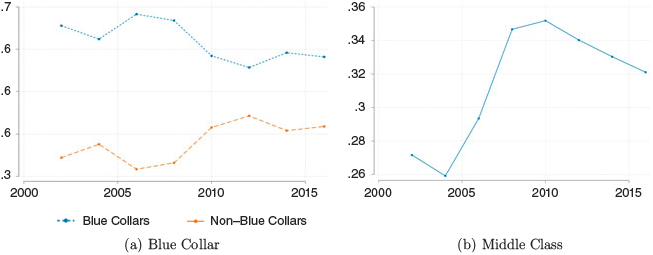

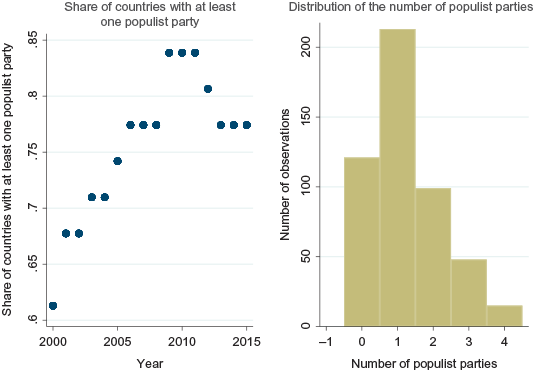

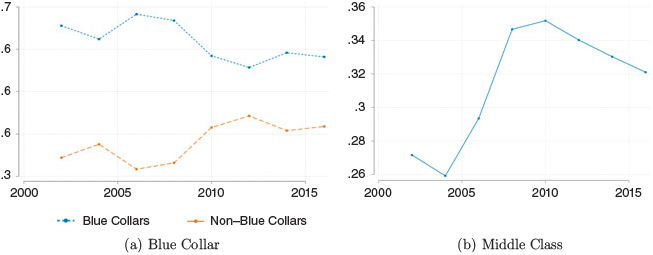

This cannot be said of financial crises. It is difficult to think of a beneficial effect that a financial crisis-induced recession might have. Thus, most people, across the entire spectrum of the voter population, lose out. Income losses tend to be deep and universal. Hence, the discontent fostered by the resulting economic insecurity tends to be more pervasive and thus more politically relevant. Moreover, the first thing to note about the financial crisis is that the economic insecurity following the onset of the crisis in 2008 spread to segments of the population that were less affected by the globalization shock. Figure 1, panel (a) shows the share of blue-collar and non-blue-collar workers in the top quartile of economic insecurity in each year of our sample. Prior to the financial crisis, when globalization was the main source of economic insecurity, blue-collar workers were those predominantly experiencing a high level of insecurity (66% on average); during the years after 2008, the share of non-blue-collar increases substantially (by more than 8 percentage points) compared to the years prior to the financial crisis.

Insecurity among blue-collar workers and members of the middle class

Figure 1 Long description

Figure 1 contains two line graphs on economic insecurity. Panel (a), “Blue Collar,” plots the share of blue-collar and non-blue-collar workers in the top quartile of economic insecurity between 2002 and 2016. The blue-collar line remains consistently higher, fluctuating around 0.56–0.68 and declining slightly after 2008. The non-blue-collar line ranges around 0.31–0.44, rising gradually after 2008 and narrowing the gap with blue-collar workers. Panel (b), “Middle Class,” shows the share of people in the middle 50% of the income distribution experiencing insecurity. Values rise from about 26 in 2004 to a peak above 35 around 2010, then gradually decline to about 32 by 2016.

Panel (b) shows that the financial crisis also increased economic insecurity among the middle class, as shown by the average share of people in the mid-50% of the distribution of income in each country-year. The share of middle-class voters suffering from serious economic insecurity, that is, in the top quartile of insecurity, climbs during the years of the Great Recession. Thus, the financial crisis not only increased insecurity among social strata that were already distressed by globalization and other processes before the crisis (namely, low-skilled workers at the bottom of the income distribution), but it also spread insecurity among segments of the population that had been relatively sheltered from globalization.

In advanced Western countries, where both firms and households are heavily dependent on financing, a financial collapse can represent an existential threat. Obtaining credit becomes more difficult in a financial crisis, as markets stop working smoothly and financial constraints become tighter. In addition, the accompanying fall in asset prices reduces the value of precautionary savings, thus limiting people’s ability to cope with economic insecurity. On the contrary, up until the financial crisis, financial markets were intact and credit was abundant, implying that some of the people hit by the first wave of globalization threats could use borrowing or their own savings when asset prices were still high. The dramatic spike in the bond spread during the years of the European sovereign debt crisis demonstrates quite clearly how difficult it became for governments to secure funding to run their programs during the financial crisis relative to the globalization years.

The different composition of the population feeling economic insecurity is only one effect. Another factor – more difficult to measure but intuitively central to our argument – is the level of confidence in the existing institutional framework and in the credibility of government objectives and traditional policy commitments. Any rational agent applying standard Bayesian updating must be revising downward such a confidence when a large crisis such as the Great Recession finds the status quo elites unprepared (or complicit). Our novel theoretical framework will allow us to explicitly consider these additional differences, and the theory will guide an empirical analysis that will add important nuances to the simple first observation of Figure 1.

1.3 Introducing the Theoretical Framework

As explained in Bellodi et al. (Reference Bellodi, Morelli, Nicolo and Roberti2025), there are clear reasons – from standard principal-agent logic to endogenous changes in accountability – to expect that a decline in trust in governments and politicians determines what they call a “shift to commitment politics,” whereby the trustee model of political agency is replaced by agents proposing implicit contracts based on simple commitments made ex ante.Footnote 2

The shift to commitment politics generates as an epiphenomenon the strategic use of anti-elite rhetoric and identity protection rhetoric for the people, which are the essential parts of observable political strategies that constitute the definition of populist vs non-populist parties in the political science literature. Moreover, as argued formally in Bellodi et al. (Reference Bellodi, Morelli, Nicolo and Roberti2025), it is also intuitive that parties and politicians shifting more and more to policy commitments desire to weaken the checks and balances, bureaucrats, judges, experts, and intellectuals: because they all could constitute obstacles to the implementation of commitments when proved to violate constitutional or international laws (like in the case of deportations).

The theory presented in Section 2 of this Element develops an important feature of the populist commitments: they are almost always “exclusionary commitments” of protection – protectionism on markets, protection from immigrants, identity protection, nationalism, protection from external influences, and even from international organizations and laws.

The financial crisis has played a crucial role in reshaping political preferences. For individuals weighing a policy agenda centered on open borders, open markets, and inclusive policies against one favoring closed borders, protected markets, and the rollback of inclusion efforts, the crisis disproportionately undermined confidence in the former. In contrast, the latter – an agenda of closure – can come to be seen as not only viable but necessary, particularly when the crisis is perceived as stemming from external forces and internal responses are constrained by limited fiscal space.

We capture all the above complex logical connections with a simple theoretical model that clarifies the determinants of both voters’ policy preferences between open market status quo and various types of protectionist commitments as well as voters’ participation decisions given their abilities and ideologies. The simple model will clarify why one should expect the financial crisis to induce differential turnout effects between left and right and thereby cause the entry and success of right-wing populist protectionist parties.

To anticipate some important details of the theory, we assume that individuals are heterogeneous in ability (and hence type of occupations they can obtain), cost of voting, and ideology. The expected utility of an individual if the open market status quo is kept depends both on the probability of being a winner from the open market and on the probability of being bailed out or compensated by institutions when happening to be a loser. Hence, this expected utility (which we also call economic security) can be different across occupations. Ideology enters the picture when considering an alternative policy commitment to protect from the open market, which typically is a bundle of closures, from closed markets to closed borders and beyond. Such closure policy commitments typically give a higher expected utility to right-wing individuals, since left-wing individuals are typically closer to the moral universalism description of Enke et al. (Reference Enke, Rodríguez-Padilla and Zimmermann2023) and hence have some moral disutility from policies that benefit a subset of the population (the “citizens”) while excluding others (the “immigrants”). Thus, when a crisis arrives and reduces the appeal of the open status quo, right-wing individuals can more readily embrace populist protection commitments, whereas left-wing individuals equally disappointed by the status quo may instead choose to abstain. This differential incentive to participate in elections is what triggers the increased probability of winning of right-wing populist parties after the financial crisis.

1.4 Empirical Methodology

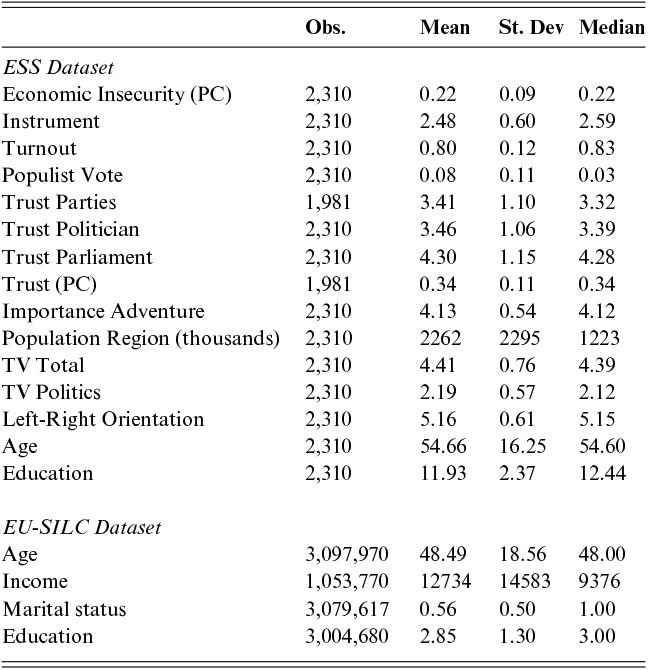

On the voters’ side, we use the European Social Survey (ESS), which is conducted in repeated cross-section waves. The data is used to produce an instrumented pseudo-panel analysis of the economic and financial drivers of change in political attitudes and voter behavior in Europe during the financial crisis and subsequently. Each element of the pseudo-panel is a synthetic cohort of individuals and can be associated with a distribution of occupations. This survey data will be complemented by labor market data that will allow us to construct a methodology for identifying the causal effects of the financial crisis, exploiting heterogeneity in the distribution of occupations across cohorts.

In order to establish a causal link between the financial crisis and economic insecurity, trust in politics, and voter abstention, we build a novel instrumental variable that leverages the idea that financial crises are most damaging to individuals who depend more on borrowing to buffer income shocks and thus to manage economic insecurity. Dependence on borrowing is a function of the steepness of an individual’s age-earnings profile: people with a steeper profile must rely more on borrowing to smooth consumption, which makes them more vulnerable to financial shocks.

The cohorts of respondents to the ESS over time and across countries vary in their distribution by occupation. We find marked differences between occupations in the steepness of the age-earnings profiles. Thus, there will be heterogeneity in the sensitivity to a financial crisis across occupations and hence cohorts. We construct a shift-share instrument where the shifter is the aggregate economic shock affecting a country, the share is the weighted average sensitivity/dependence on borrowing by cohort, and the weights are the shares of each occupation within the cohort.

On the supply side, we document in multiple ways the death of traditional parties, birth of new parties, and transformation of the manifestos of surviving parties, giving a comprehensive picture of the transformation of the whole landscape of political platforms after the financial crisis.

In order to define a European party as populist in a given year, we rely on the PopuList proposed by Rooduijn et al. (Reference Rooduijn, Van Kessel, Froio, Pirro, De Lange, Halikiopoulou, Lewis, Mudde and Taggart2019), which is available at www.popu-list.org. This classification is consistent with both the ideational approach and the political strategic approach to defining populism.Footnote 3 Accordingly, the people-vs-elite rhetoric is a straightforward manifestation of populism, which is also the most common measure used in empirical work (Pauwels, Reference Pauwels2011; Hawkins and Littvay, Reference Hawkins and Littvay2019; Gennaro et al., Reference Gennaro, Lecce and Morelli2024).

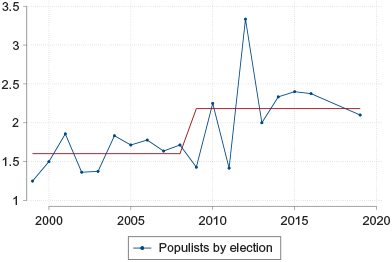

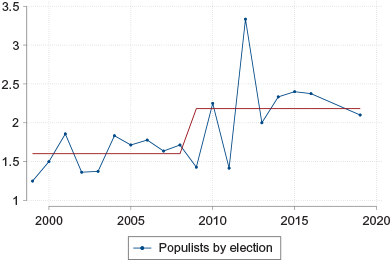

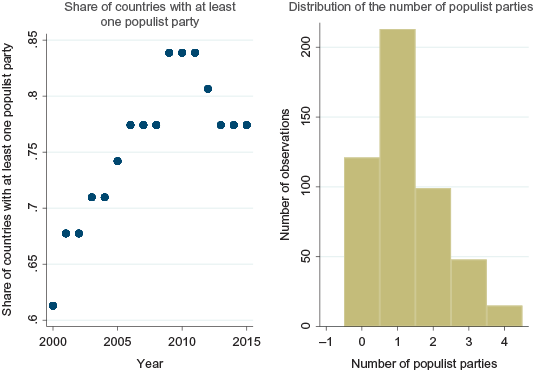

To give a first sense, just looking crudely at the number of coded populist parties entering, we can already get a sense of the change: Figure 2 plots the average number of populist parties participating in elections up to 2008 and in subsequent years. It is clear that the Great Recession marks a watershed in terms of the supply of populist parties competing for voters.

Populist parties

Figure 2 Long description

Before 2008, the blue line fluctuates between 1 and 1.7 with no clear trend, and the red average line sits near 1.6. After 2008, the number rises sharply, spiking to about 3.3 around 2012 before settling between 2 and 2.5 in subsequent years. The red average line steps up to approximately 2.2, indicating a structural break in the supply of populist parties after the financial crisis.

Up until 2008 an average of 1.7 populist parties took part in an election with no clear trend over time. In the years following 2008, the average number of participating populist parties jumps to 2.4 – a 33% increase compared to the precrisis mean – with a spike in the 2012 elections. The financial crisis appears to mark a structural break in the supply of populist parties. And this is just looking at quantity, but, as we will see, content also changes in directions consistent with our arguments within long-lived parties.

The Manifesto Project dataset (Volkens et al., Reference Volkens, Burst, Krause, Lehmann, Matthieß, Regel, Weßels, Zehnter and Sozialforschung2018) will be useful because with the use of Lasso regressions we will be able to trace the most important topic shifts and position shifts directly from the texts. We will complement the analysis on party manifestos over time with the insights from expert surveys, which are useful especially to detect major items of convergence or divergence between populist and non-populist parties on both sides of the ideological spectrum.

1.5 Main Empirical Findings

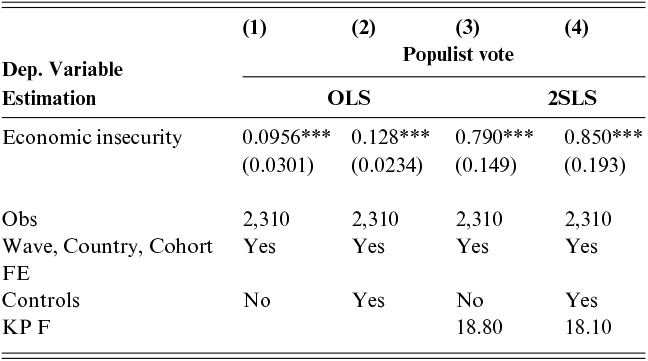

Our main empirical finding is that economic insecurity triggered by the financial crisis had a causal effect on turnout and on voting choices. Financial shocks specifically hamper the ability to borrow, which particularly affects segments of the middle class characterized by steep age-earnings profiles. This, in turn, significantly expands the pool of voters seeking economic support and who are at the same time losing confidence in the ability of the government to deliver such support. In view of this disappointment in traditional politics, there is an increase in voter abstention, especially among those who had not previously been seriously affected by globalization. Meanwhile, those who were subject to previous crises as well are the most likely to vote for a populist party, especially if ideologically not opposed to exclusionary policy commitments.

The results show that the instrument has a strong predictive power on both the self-reported as well as wage-based measures of economic insecurity. In turn, in IV regressions (that also control for cohort fixed effects as well as for country and time fixed effects), shocks to instrumented economic insecurity tend to cause a reduction in voter turnout, especially among left-wing voters.Footnote 4 The shock also increased populist voting (conditional on turnout). The effects on voter behavior along all three dimensions are significant in magnitude: an increase of one standard deviation in economic insecurity increases populist voting by 7 percentage points, which is about 94% of the sample mean, and it lowers turnout by more than 8 percentage points (about 10% of the sample mean).Footnote 5 We will show that indeed back-of-the-envelope calculations support our financial crisis mechanism, since roughly 70% of the change in voting for populist parties comes from the middle class.

The above numbers suggest that the financial crisis may indeed have been the moment of maximum entry and transformation of parties on the supply side, which in turn gave disillusioned voters new hope. To investigate this hypothesis, we conduct a novel analysis of the dynamics of the supply of populist parties in Europe. We first examine the manifestos of all European parties, distinguishing between long-lived parties (existing both before and after the financial crisis) from the parties that disappeared or emerged at the time of the crisis. The quantitative structural break documented already in Figure 2 is corroborated by a number of findings on contextual interactions and textual content.

In terms of contexts, the party structure transformation phenomenon occurred particularly in countries with a shrinking fiscal space, which is in line with the expectations given our theory and the considerations of credibility of policies mentioned above. A shrinking fiscal space has dramatically different effects on left-oriented versus right-oriented parties. It also reduces the feasibility and thus the credibility of protection policies that are focused on the supply of expensive public goods and on redistributive spending. Hence, the traditional leftist parties suffered the most in terms of credibility, leading to the exit of traditionally leftist parties and the entry of new parties such as the Five Star Movement in Italy and Podemos in Spain. The nationalism and identity protection policies championed by right-wing parties did not need to be altered because they were less dependent on the level of public spending. Thus, nationalist or far-right ideologies do not need to change in a financial and/or fiscal crisis; in contrast, such crises force a shift on the left from (unaffordable) redistributive platforms towards protection rhetoric and pre-distribution. This creates an advantage for right-leaning parties, which are able to advocate the same policies and measures that depend less on public spending.

In terms of textual content, we corroborate the insights on party transformation using expert survey data on topics and salience shifts to see whether non-populist parties also modified their platform and in which direction. We show that there is a postcrisis convergence, with non-populist parties modifying their platforms in the direction of populist ones.

1.6 Contribution to Comparative Politics Literature

Our contribution to the comparative politics literature is on multiple levels. First, we contribute to the understanding of the effects of economic shocks of different nature on the political preferences of voters (see Margalit (Reference Margalit2019) for a review); second, we contribute to the documentation of changes over time in the political attitudes of occupational groups and the corresponding evolution of parties in the electoral space in the last decades in Europe, thereby complementing the work in the Element by Hall et al. (Reference Hall, Evans and Kim2023); third, we emphasize the key role of the financial crisis in the determination of the success of populists, also due to the strong incentives of political entrepreneurs to politicize this issue that captured and interested the middle class – a point well illustrated by De Vries et al. (Reference De Vries, Hobolt and Walter2021). It is useful to zoom separately on these three contributions.

1.6.1 Voters’ Reaction to Shocks

Regarding the first contribution – namely, the channels through which economic shocks can alter political preferences – the macro-level arguments explaining how major economic shocks influence key cleavages and political coalitions are developed in the works of Gourevitch (Reference Gourevitch1986), Rogowski (Reference Rogowski1987), Kriesi et al. (Reference Kriesi, Grande, Lachat, Dolezal, Bornschier and Frey2008), and Bartels (Reference Bartels2014).

For the micro-level analysis of the effects of individual shocks on individual preferences and voting behavior, perhaps the richest empirical studies are Malhotra and Margalit (Reference Malhotra and Margalit2010), Dancygier and Donnelly (Reference Dancygier, Donnelly, Bermeo and Bartels2014), and Ahlquist et al. (Reference Ahlquist, Copelovitch and Walter2020), while on the theory side the role of self-interest is underlined in Meltzer and Richard (Reference Meltzer and Richard1981), Iversen and Soskice (Reference Iversen and Soskice2001), and Mares (Reference Mares2006).

Our contribution here is to reinforce the view that economic shocks do not affect ideologies, but rather the policy preferences for people of the different ideologies. As emphasized in Campbell (Reference Campbell1960), ideological dispositions rarely change. Even significant economic shocks do not change voters’ preferences or views from left to right or vice versa: ideologies tend to persist over people’s lifetime (Krosnick and Alwin, Reference Krosnick and Alwin1989; Newcomb, Reference Newcomb1967) and are resistant to new information (Taber and Lodge, Reference Taber and Lodge2006). However, “within” one’s ideology a significant economic shock can affect trust, willingness to participate in politics, and the decision to continue to support a traditional party or to embrace a new movement.Footnote 6

Golder (Reference Golder2016) and Hobolt and Tilley (Reference Hobolt, Tilley and Laffan2018) focus on an emotional channel for the differential effects between left and right. They focus attention on the anger against the status quo, which often translates in hate or resentment against existing institutions and newly included members of society that should instead be excluded. In our Element we do not focus on the emotional aspects, but rather on the (potentially complementary) rational comparison between exclusionary policies and inclusive redistributive welfare policies. The increase in salience of cultural divisions emphasized by De Vries and Hobolt (Reference De Vries and Hobolt2020) can be perfectly consistent with our conceptual framework. In fact, we stress that even this change in salience may be in part generated by a lower confidence that the economic protection can be obtained other than with exclusionary policies.

As shown in Margalit (Reference Margalit2013), the experience of a job loss typically makes individuals more likely to support welfare measures of the left. But, as we will see, the financial crisis hits in particular the occupations with steep age-earning profiles, namely with potential growth of income over time when initial investments are made possible, and this class of people, such as small employers, typically displays a right-wing propensity. Like us, Oesch and Rennwald (Reference Oesch and Rennwald2018) identify small employers as one of the key swing groups between the center-right and the radical-right (in their categorization) or between opposing and favoring exclusionary policies (in our framing), but our framework and methodology allows us to see why this swing group (together with others with similar age earning profile) reacted to the financial crisis more than to other crises.

1.6.2 Occupational Groups and Parties’ Platforms

As far as the second contribution is concerned, we agree with the Hall et al’s (Reference Hall, Evans and Kim2023) perspective that gives a key role to occupations and views party strategies (in terms of platform choice) as best responses to the changes of political preferences of the occupational groups that they traditionally represent.Footnote 7 We zoom in particular on the role of the 2008 financial crisis but enlarge the analysis to all European countries. Their analysis is instructive on existing pre-trends and connects well also to the theoretical framework that we discuss in the next section. To anticipate, in our framework the preferences on the socio-cultural dimensions that are typical of populist parties can be shaped by changes in the credibility of different policies after crises. Hence, looking at the different impact of the financial crisis on the fears and expectations of different occupations can explain the positioning of parties on both the economic and cultural dimensions.

The employment transformations already started in the 1990s, with jobs being created in the service sector and information technology (see Oesch, Reference Oesch2013; Goos et al., Reference Goos, Manning and Salomons2009; Autor and Dorn, Reference Autor and Dorn2013) obviously matter, but the financial crisis is the one that created fear also for people in occupations with steep age-earning profiles, hence enlarging the pool of social groups and occupations feeling in danger. A set of scholars contends that the creation of populist attitudes relates mostly to the increasing cultural difference between the progressive and inclusive cosmopolitans and those wanting to protect and preserve the identity of the true people (the true settlers, looking at the manifesto of the People’s Party of Bryan in 1890). Our results will support the possibility that the increase in identity politics and exclusionary policy preferences derive from a deterioration of trust in the ability of government institutions to protect the losers from market competition with inclusive welfare policies.Footnote 8 Hence, the economic and cultural dimensions do not evolve independently; they both depend on the changes in beliefs and trust in the feasibility and desirability of different economic policies.

Thus, in contrast with Inglehart (Reference Inglehart2013), Kitschelt (Reference Kitschelt1994), Kriesi et al. (Reference Kriesi, Grande, Lachat, Dolezal, Bornschier and Frey2006), De Vries et al. (Reference De Vries, Hakhverdian and Lancee2013), and Häusermann and Kriesi (Reference Häusermann, Kriesi, Beramendi, Häusermann, Kitschelt and Kriesi2015), we do not frame the political transformation related to populism and its causes as a horse race between the economic and cultural hypotheses. Most importantly, the financial crisis operates almost exclusively on the economic policy preferences, and it would be difficult to identify a direct influence on the cultural dimension that is not mediated by the negative shock on the feasibility of inclusive redistributive policies.

Our interpretation of the fact that radical-right parties have become more important contenders for power, increasingly crucial to governing coalitions on the right (Kriesi et al., Reference Kriesi, Grande, Lachat, Dolezal, Bornschier and Frey2006, Reference Kriesi, Grande, Lachat, Dolezal, Bornschier and Frey2008; Bornschier, Reference Bornschier2010; Häusermann and Kriesi, Reference Häusermann, Kriesi, Beramendi, Häusermann, Kitschelt and Kriesi2015; Hooghe and Marks, Reference Hooghe and Marks2018; Rovny and Polk, Reference Rovny and Polk2020; Marks et al., 2021), is that this is not only due to a greater salience of the cultural dimension, but also to a reduction in trust that other policies, non-exclusionary and hence more inclusive, can work. And this lower trust is the variable affected by the financial crisis, our focus in this Element.

Hall et al. (Reference Hall, Evans and Kim2023) find that, between 1990 and 2018 across eight countries, cultural preferences generally shifted in a more cosmopolitan direction – likely driven in part by the sharp rise in tertiary education. In contrast, they observe a consistent shift to the right on the economic dimension. As we argue in our theory section, declining trust in the feasibility of inclusive, redistributive welfare policies fosters protectionist and nationalist preferences in both economic and social spheres. This, in turn, contributes to growing affective polarization on the cultural dimension, as exclusionary policies increasingly conflict with cosmopolitan and universalist values, producing divergent effects on political engagement and turnout. Hall et al. also show that the shift toward economically right-wing preferences is not limited to workers but extends to small employers, particularly after 2006, aligning with our finding that the financial crisis expanded economic vulnerability to include the middle class. Meanwhile, cultural attitudes became markedly more cosmopolitan among professionals, skilled white-collar workers, lower-level service workers, and managers, whereas production workers, craft and trade workers, and small employers showed little change in their cultural views on average.

Hall et al. (Reference Hall, Evans and Kim2023) use the schema devised by Wagner and Meyer (Reference Wagner and Meyer2017) to group parties into the categories of mainstream left, mainstream right, and radical-right and examine the movement of these party families in the two-dimensional space of economic and cultural positions across all eight countries over the period between 1990 and 2018. We do not group parties that way, because the notion of populism has only a partial overlap with extremism and radicalism. What constitutes the logical link from crisis to support for populist parties is different from the emotional link from anger to hate. However, their classification is nonetheless useful for us to illustrate some parts of our argument that relate to different types of protection policies and their appeal to voters of different occupations and ideologies. Both types of analysis support the view that the change came mostly from the radical right parties (in their analysis) and new populist parties and movements (in our analysis) who moved their economic positions to the left in order to capture the concerns of the occupational classes most concerned by technological change and globalization and now access to credit.

After the crisis, the share of voters experiencing economic insecurity – and therefore demanding economic protection typically associated with left-wing policies – expanded. Beyond this quantitative shift, many of these voters also lost confidence in the feasibility of maintaining, let alone expanding, inclusive welfare policies. As a result, support for exclusionary, conservative positions on the cultural dimension also grew. In other words, for individuals seeking economic protection and weighing the relative merits of traditional redistributive welfare policies versus exclusionary measures – such as anti-immigration and discriminatory policies – the latter become increasingly attractive when the former are seen as less feasible. This shift is further reinforced when trust in politicians’ commitment to protective goals is low. The financial crisis played a significant role in undermining confidence in the viability of open-market solutions, thereby contributing to growing support for policies favoring closed markets, closed borders, and a more exclusionary societal model.

Kitschelt and Rehm (Reference Kitschelt and Rehm2023) interpret electoral realignment of parties as follows: they argue that people with different levels of income and education have stable preferences on economic and cultural issues but salience changes. We argue that crises change preferences for policies by affecting trust and beliefs on what can work. Moreover, we agree with Hall et al. that occupations matter as much as income and education levels.

1.6.3 The Entrepreneurship of Manipulation and Euroskepticism

De Vries (Reference De Vries2018) and Hutter et al. (Reference Hutter, Grande and Kriesi2016) are examples of political analyses of the public opinion backlash against European institutions. De Vries et al. (Reference De Vries, Hobolt and Walter2021) discuss the important role of political entrepreneurs of challenger parties on the extreme left and extreme right to channel the public discontent toward European institutions to gain votes. They argue that what is new in recent years is the level of politicization of the arguments pro and against international cooperation and their salience.

Our Element clarifies why this politicization (and, in particular, manipulative politicization) may have become easier as a consequence of the financial crisis. The key role of the financial crisis in the determination of the success of populists is due to the strong incentives of political entrepreneurs to politicize the issue of how much European institutions constitute a constraint to the implementation of simple protection policies – policies such as citizenship income, reduction of pension age, low carbon prices ignoring green external mandates, and so on. Moreover, as we also argued earlier, the issue of external constraints to simple protection commitments becomes salient also for the middle class, given the shock determined by the financial crisis on the confidence in open markets and market integration. The increased salience of the inability of European institutions to counter the crisis gave overall a greater push to the mobilizers of discontent. The analysis of parties’ manifestos in this Element confirms the anti-internationalism trend on both sides of the ideological spectrum.

The financial crisis has increased Euroskepticism (Fernández-Albertos and Kuo, Reference Fernández-Albertos and Kuo2016; Hobolt and De Vries, Reference Hobolt and De Vries2016), but we stress, in line with our proposed mechanism, that it is mostly in occupations with steep age-earning profiles and small employers that this changed after the financial crisis. For example, a party such as Lega in Italy changed its policy platform after the financial crisis, promising policies that could be implemented more likely in the absence of European constraints, legal constraints, and constraints in terms of macro stability.

1.7 Contribution to the Political Economy of Populism Literature

The conceptual framework developed in Bellodi et al. (Reference Bellodi, Morelli, Nicolo and Roberti2025) and the theory proposed in Section 2 of this Element, which adapts the logic of commitment politics to the differences we want to explain, together push the view that populist policy commitments are a political strategy. The typical features of populist platforms can be traced back to the shift to commitment politics, which in turn emerges naturally at a time of increasing distrust, which is itself shown to be endogenous.

Technological change, and in particular the use of the internet and social media for political communication, have endogenously reduced trust in political agents, and this reduction in trust has increased the use of simple policy commitments; in turn, once political campaigns become more and more focused on policy commitments to voters, this determines the rational use of typical populist strategies such as anti-elite rhetoric, misinformation, and rhetoric and actions against judges, bureaucrats, and all checks and balances to make the executive as free as possible to implement the promised policies.Footnote 9

Our theory presented below makes this general logic more specific to the financial crisis by zooming in on the particular type of policy commitments that we can call commitments to protect. The financial crisis makes governments, and especially those with low fiscal space, unable to continue to support traditional welfare programs. This makes those affected by the market shocks shift to demand of simple exclusionary commitments.

There is an immense literature on the economic and cultural causes of populism. The survey article by Guriev and Papaioannou (Reference Guriev and Papaioannou2022) contains almost all of them. Gidron and Bonikowski (Reference Gidron and Bonikowski2013), Mudde and Kaltwasser (Reference Mudde and Kaltwasser2017), and especially Norris and Inglehart (Reference Norris and Inglehart2019) highlight the relevance of cultural backlashes, which clearly occur simultaneously with an increase in economic insecurity. Both economic and cultural factors matter, but here we want to zoom in particular on the strands of this literature related to the financial crisis and to the role of the fiscal space. Foster and Frieden (Reference Foster and Frieden2017) present the correlation between distrust measures and debt using the Eurobarometer survey. Algan et al. (Reference Algan, Guriev, Papaioannou and Passari2017) show that in elections after 2008, the regions where unemployment rose saw the sharpest decline in the trust placed in institutions and traditional politics,Footnote 10 while Dustmann et al. (Reference Dustmann, Eichengreen, Otten, Sapir, Tabellini and Zoega2017) show that in the aftermath of the crisis, the distrust of European institutions was correlated with the populist vote. Using the age-earnings profiles typical of different occupations, we are able to directly identify the channel through which the specific features of the financial crisis (primarily the inability to borrow) impacted each cohort of citizens in Europe. We are therefore able to provide evidence of causal effects by differentiating such effects across cohorts with different occupational distributions.

There is an interesting literature on financial crises as determinants of extremism (see, for example, Funke et al. Reference Funke, Schularick and Trebesch2016 and Galofré-Vilà et al. Reference Galofré-Vilà, Meissner, McKee and Stuckler2021).Footnote 11 Our analysis of the 2008 financial crisis emphasizes their impact on the political orientation and feasibility of policy platforms on either side of the political spectrum, rather than focusing on extremism specifically.Footnote 12 Voth et al. (Reference Voth, Doerr, Gissler and Peydró2020) were the first to present causal evidence that a financial crisis can fan extreme right populism, based on variation in failing banks in Germany prior to the 1932 elections. In contrast to their findings, we show that the 2008 financial crisis shifted politics in the direction of populism on a broader scale, rather than only on the right. Indeed, the transformation after 2008 occurred primarily on the left.Footnote 13 Furthermore, our method of identification makes it possible to zoom in on the heterogeneous impact of the financial crisis by occupation and to identify the mechanism that creates economic insecurity, regardless of preexisting anti-Semitism or some similar types of ideology.

On the relevance of the fiscal space, Arias and Stasavage (Reference Arias and Stasavage2019) and Fetzer (Reference Fetzer2019) look at the political costs of austerity politics, although they ignore the dynamic transformation we focus on. The role of fiscal constraints in shaping political trust and populist support has also been documented in the Latin American context by Baccini et al. (Reference Baccini, Hicks and Rettl2025). Indeed, we find that it is precisely in the countries with the smallest fiscal space that the financial crisis had a greater impact on politics (and especially on the left).Footnote 14

Rodrik (Reference Rodrik2018) traces the increase in populism to the globalization shock. While this may be true when considered in isolation and for specific events,Footnote 15 Guiso et al. (Reference Guiso, Herrera, Morelli and Sonno2019) show that globalization shocks alone cannot account for the cross-country pattern of populism in Europe. They show that the interaction of globalization with a euro-dummy accounts for the large majority of the explanatory power, and, in the presence of such an interaction variable, globalization shocks alone have little effect. In Section 7, we show that whereas the supply of populism displays a discontinuous jump in 2008, there was no similar increase in 2004, the year of the globalization shock due to the expansion of the EU. One may argue that, in a deep sense, the globalization shock is the root cause of populism, because a macro literature traces the burst of the crisis to the imbalances that originated from globalization. What we show is that a globalization that does not involve a financial crisis is unlikely per se to generate the spread of populism that we have witnessed in Western countries, particularly in countries that are heavily dependent on credit and financial markets.

Moreover, while globalization primarily reduced trust in free markets, the conjunction of the financial crisis and shrinking fiscal space reduces trust in all other institutions as well. It is the collapse of confidence in representative democracy that increases the demand and supply of simple protection commitment policies such as walls, protectionism, and Brexit.

The rest of the Element is organized as follows: Section 2 draws the conceptual framework that generated all our ideas on the role of all crises, and in particular the financial crisis, on voters’ policy preferences and on asymmetric turnout. Parties enter the picture simply in terms of whether they are likely to adopt a populist protectionist commitment or not and why. Section 3 describes our data and measurements. Section 4 describes the important role of voters’ participation incentives and displays descriptive results that are in line with the asymmetric turnout effects of crises that we explain in the theory. Section 5 describes our empirical methodology and identification strategy, and Section 6 displays causal estimates of the effects of the financial crisis on all aspects of voters’ preferences and behavior. section 7 uses manifestos of parties to show the different effects of globalization and the financial crisis on the party structure and policy platforms. Section 8 analyzes strategic entry and strategic positioning by parties in the aftermath of the crisis and looks at the convergence of platforms across parties on each side of the political spectrum using expert surveys. Section 9 concludes with some remarks on the persistence of some of the effects of the financial crisis.

2 Theory

In this section we aim to clarify the effect of a crisis on voters’ preferences on policies through a simple theory on the voters’ thought process when evaluating the pros and cons of the open market status quo with a policy commitment proposal to close markets and/or borders. In the first part of this section we take it as given that there exists a choice like this for a voter, and only at the end of the section we explicitly consider the intuitive conditions for entry of populist parties with such a type of policy closure commitments on the supply side.

2.1 Voters’ Preferences on Closed vs Open Markets

We start from a voter’s evaluation of the tradeoffs involved when considering her expected utility from an open market status quo versus a protectionist reform that would cut out competitors to the voter’s employing firm or potential employing firms, reducing also the instability and market dependence on prices and wages.Footnote 16 The perception of threat to jobs and wages created by the technological changes that were permitting greater and greater open market integration was the central cause of populist voting already in the United States in the last quarter of the nineteenth century.Footnote 17 The globalization literature on the role of the China shock in the determination of populist voting in many Western democracies in the twenty-first century gave rise to an analogous tradeoff. The same tradeoff must have been a central one in the decision by American voters to vote or not to vote for Donald Trump, who made protectionism a central pillar of his campaign(s). Since this key tradeoff has been at the center of so many studies on the fears and insecurities that led to populist voting, let us zoom on this tradeoff.

When evaluating her prospects in an open market status quo, we can simplify the voter’s thought process as follows: she has a belief  to be a winner from the open market and a probability

to be a winner from the open market and a probability  to be a loser from it. Let us normalize the utility for a winner to 1 and the loser’s utility to 0.Footnote 18 However, in the open market status quo, with a representative democracy determining the functioning of government institutions, the voter expects that in case she turns out to be a loser from the market process, she will be compensated by such institutions with probability

to be a loser from it. Let us normalize the utility for a winner to 1 and the loser’s utility to 0.Footnote 18 However, in the open market status quo, with a representative democracy determining the functioning of government institutions, the voter expects that in case she turns out to be a loser from the market process, she will be compensated by such institutions with probability  . For example, if a voter expects that her government has both “the objective” to protect the losers from market competition with redistribution or public jobs and “the capacity” to do so, then

. For example, if a voter expects that her government has both “the objective” to protect the losers from market competition with redistribution or public jobs and “the capacity” to do so, then  is a high number; whereas if one expects the government either to be attentive to other objectives (or interest groups’ influences) or not to have the capacity to compensate, then

is a high number; whereas if one expects the government either to be attentive to other objectives (or interest groups’ influences) or not to have the capacity to compensate, then  is a low number. Putting things together, the expected utility from an open market status quo (

is a low number. Putting things together, the expected utility from an open market status quo ( ) with a representative government that could, in principle, try to compensate losers is

) with a representative government that could, in principle, try to compensate losers is

(1)

(1)We can think of  as representing the voter’s self-confidence in her skill and the fit of such skills for the open competition. Hence,

as representing the voter’s self-confidence in her skill and the fit of such skills for the open competition. Hence,  can be very different from voter to voter, because it depends on education, acquired skills, psychology, and so on.Footnote 19 The second parameter,

can be very different from voter to voter, because it depends on education, acquired skills, psychology, and so on.Footnote 19 The second parameter,  , captures in a nutshell “trust” in the government, where once again trust can be high or low depending on both the government or politicians’ objectives and incentives on one hand and capacity on the other. One might have low trust because she does not think that politicians will even care and try to compensate, derailed by other objectives, or may think that the objectives are aligned but there are not enough resources to effectively counter the negative market prospects of a market loser. We will come back to these components of trust when we introduce the mechanism through which the financial crisis and fiscal space interact.

, captures in a nutshell “trust” in the government, where once again trust can be high or low depending on both the government or politicians’ objectives and incentives on one hand and capacity on the other. One might have low trust because she does not think that politicians will even care and try to compensate, derailed by other objectives, or may think that the objectives are aligned but there are not enough resources to effectively counter the negative market prospects of a market loser. We will come back to these components of trust when we introduce the mechanism through which the financial crisis and fiscal space interact.

A protectionism reform can be captured for simplicity by a fixed expected utility  that the voter expects if all external competitors are shut out of the market.Footnote 20 The expected utility

that the voter expects if all external competitors are shut out of the market.Footnote 20 The expected utility  parsimoniously captures the perception of many workers and/or firms that, on the one hand, the market winner’s payoff is higher in an open market, but, on the other hand, with no competitors, her industry, job, and wage are sheltered, and hence the low loser’s payoff can be avoided.

parsimoniously captures the perception of many workers and/or firms that, on the one hand, the market winner’s payoff is higher in an open market, but, on the other hand, with no competitors, her industry, job, and wage are sheltered, and hence the low loser’s payoff can be avoided.

Thus, a voter prefers a protectionist commitment iff

(2)

(2)Hence, a voter is the more likely to support a protectionist commitment the lower are her confidence  and her trust

and her trust  , and the higher is her expected utility from protectionism

, and the higher is her expected utility from protectionism  . Even though in reality voters are heterogeneous in all these three parameters, let us simplify the analysis by assuming

. Even though in reality voters are heterogeneous in all these three parameters, let us simplify the analysis by assuming  is fixed for all; and as far as

is fixed for all; and as far as  is concerned, let’s assume for simplicity that it can take two values,

is concerned, let’s assume for simplicity that it can take two values,  and

and  , where

, where  ,

,  represents the expected utility of the protectionist policy for voters of ideology

represents the expected utility of the protectionist policy for voters of ideology  , where

, where  denotes the standard left(right) ideology. Given that the populist exclusionary commitments typically include not only protectionism in trade policies but also closed borders and nationalist policies on multiple dimensions, we can safely assume that

denotes the standard left(right) ideology. Given that the populist exclusionary commitments typically include not only protectionism in trade policies but also closed borders and nationalist policies on multiple dimensions, we can safely assume that  : The typical left ideology dislikes exclusions, closed borders, closure to other cultures, and so on; hence, a policy bundle based on exclusions and closures gives lower overall utility to left-wing voters. Assuming a fixed share

: The typical left ideology dislikes exclusions, closed borders, closure to other cultures, and so on; hence, a policy bundle based on exclusions and closures gives lower overall utility to left-wing voters. Assuming a fixed share  of left-wing voters in the population, we denote by

of left-wing voters in the population, we denote by  the average utility from a bundle of closure policies.Footnote 21 Finally, we let

the average utility from a bundle of closure policies.Footnote 21 Finally, we let  be distributed on the interval [0,1] with density

be distributed on the interval [0,1] with density  . Assuming that a polity has a unit mass of voters, the standard economic belief that free trade is good in the aggregate can be captured by the following assumption:

. Assuming that a polity has a unit mass of voters, the standard economic belief that free trade is good in the aggregate can be captured by the following assumption:

Market Efficiency Assumption (MEA):  .

.

Even if all voters believe in the MEA, consistent with most economic studies, it is clear that those for whom (2) holds prefer the protectionist commitment.

2.2 The Effects of Different Types of Crises

A globalization shock, caused, for example, by a technological change making transportation of goods easier or by innovations and new competitors (humans or robots) who appear as external threats, typically determines a reduction in  for some classes or occupational groups. Thus, the common opinion that globalization shocks like the entry of China into the WTO may have been a trigger of populism can be parsimoniously captured by this heterogeneous reduction in

for some classes or occupational groups. Thus, the common opinion that globalization shocks like the entry of China into the WTO may have been a trigger of populism can be parsimoniously captured by this heterogeneous reduction in  values in the model. In the binary simplification below, where

values in the model. In the binary simplification below, where  can take only two values,

can take only two values,  and

and  , the globalization and automation shocks affect mostly

, the globalization and automation shocks affect mostly  , namely the probability of success for low-skill individuals (or individuals working in exposed industries).

, namely the probability of success for low-skill individuals (or individuals working in exposed industries).

A financial crisis such as the Great Recession affects all levels of  and

and  : an economic agent who was counting on good access to reliable financial markets and banking for her economic prospects and future now sees the probability

: an economic agent who was counting on good access to reliable financial markets and banking for her economic prospects and future now sees the probability  of the good outcome go down and, at the same time, perceives a lower

of the good outcome go down and, at the same time, perceives a lower  that market and government institutions can “bail” her out in case of a negative realization of economic conditions. The financial crisis made most market operators tighten credit, and government institutions had a hard time helping the many losers. Thus, and naturally more so in countries with very low fiscal space,

that market and government institutions can “bail” her out in case of a negative realization of economic conditions. The financial crisis made most market operators tighten credit, and government institutions had a hard time helping the many losers. Thus, and naturally more so in countries with very low fiscal space,  must have been shocked downward. Given that

must have been shocked downward. Given that  applies to all, this common component of the crisis effects is what relates in the model to the enlargement of the set of people for whom (2) starts holding after the crisis.

applies to all, this common component of the crisis effects is what relates in the model to the enlargement of the set of people for whom (2) starts holding after the crisis.

The importance of the trust parameter  can also be appreciated through a number of historical comparisons. At the time of increased import exposure and price instability exposure caused by technological change in the US after the Civil War, there were no income taxes (only una tantum taxes to recover from the Civil War and reconstruction costs). Hence, when the Democratic Party saw the growing success of the People’s Party in 1890 and 1892 with a protectionist campaign due to the perceived effects of market integration on

can also be appreciated through a number of historical comparisons. At the time of increased import exposure and price instability exposure caused by technological change in the US after the Civil War, there were no income taxes (only una tantum taxes to recover from the Civil War and reconstruction costs). Hence, when the Democratic Party saw the growing success of the People’s Party in 1890 and 1892 with a protectionist campaign due to the perceived effects of market integration on  , they managed to take back such voters by acknowledging such grievances and by making a pledge to support the demand for a graduated income tax, which had been one of the economic policy components of the People’s Party platform. A federal progressive income tax system came later, but the alignment of the Democratic Party with those stances of the People’s Party was enough, because in case of success of the introduction of redistributive taxes, the perception was that

, they managed to take back such voters by acknowledging such grievances and by making a pledge to support the demand for a graduated income tax, which had been one of the economic policy components of the People’s Party platform. A federal progressive income tax system came later, but the alignment of the Democratic Party with those stances of the People’s Party was enough, because in case of success of the introduction of redistributive taxes, the perception was that  could be high. On the other hand, in the twenty-first century the vast majority of liberal democracies are plagued by high debts and low fiscal space, in spite of income taxes already on the downward-sloping portion of a hypothetical Laffer curve. Thus, in the twenty-first century the “capacity” part of the trust parameter

could be high. On the other hand, in the twenty-first century the vast majority of liberal democracies are plagued by high debts and low fiscal space, in spite of income taxes already on the downward-sloping portion of a hypothetical Laffer curve. Thus, in the twenty-first century the “capacity” part of the trust parameter  is very low. Hence, it is more difficult to gain back the support of those who shifted their support to populist protectionist parties.

is very low. Hence, it is more difficult to gain back the support of those who shifted their support to populist protectionist parties.

In all historical cases it is the case that the populist campaigns focused a lot on corruption, and on capture by the elites, and on difficult accountability of traditional politicians, because that “objectives” component of  does not depend on the capacity component, and hence regardless of the latter, an anti-elite and corruption denunciation rhetoric play well as complementary to a protectionist commitment.Footnote 22 In other words, if a party or politician proposes itself as a credible protectionist, then it is in their campaign strategy interest to focus the campaign on further reducing

does not depend on the capacity component, and hence regardless of the latter, an anti-elite and corruption denunciation rhetoric play well as complementary to a protectionist commitment.Footnote 22 In other words, if a party or politician proposes itself as a credible protectionist, then it is in their campaign strategy interest to focus the campaign on further reducing  with claims or pointers to the capturability of traditional discretionary politicians by interest groups. Anti-elite rhetoric is therefore a clear complement to a policy commitment strategy, especially when running against a candidate proposing themselves as able to handle the potential consequences for some people of a free market economy that is efficient.Footnote 23 Given that anti-elite rhetoric is one of the key elements of what constitutes the measure of populism in parties and politicians in political science, the association of populists with parties and politicians championing protection policy commitments is an “equilibrium” one. Anti-elite rhetoric can also be linked directly to

with claims or pointers to the capturability of traditional discretionary politicians by interest groups. Anti-elite rhetoric is therefore a clear complement to a policy commitment strategy, especially when running against a candidate proposing themselves as able to handle the potential consequences for some people of a free market economy that is efficient.Footnote 23 Given that anti-elite rhetoric is one of the key elements of what constitutes the measure of populism in parties and politicians in political science, the association of populists with parties and politicians championing protection policy commitments is an “equilibrium” one. Anti-elite rhetoric can also be linked directly to  and

and  : if the financial crisis and its handling have determined an increase in the belief that elite capture of the institution is responsible, then a corresponding reduction in

: if the financial crisis and its handling have determined an increase in the belief that elite capture of the institution is responsible, then a corresponding reduction in  for non-elite members follows naturally, as well as a reduction of

for non-elite members follows naturally, as well as a reduction of  .

.

A similar logic could be invoked to capture the tradeoff between open- and closed-border policies: on the one hand, in many European countries the demographic trends and the sustainability issues for social security systems make many economists think that free movement of labor is good in the aggregate for a country, and the pros of open borders on average dominate the cons. But, on the other hand, those who fear losing the job or jobs for their children or fear lower wages may support closed borders in spite of what economists claim on the aggregate effects. This is especially true when there is low trust in the willingness or capacity of institutions to protect potential losers under open competition. As the literature on social identification suggests (see, e.g., Bonomi et al. (Reference Bonomi, Gennaioli and Tabellini2021) and the survey by Nouri and Roland), voters who fear being on the losing side of markets have shifted from identifying with other poor people and demanding redistribution, to identifying with their social or ethnic group and demanding protection through exclusion of outsiders – external competitors, other groups, and minorities.

Thus, the logic behind closed border policies is very similar to that behind closed market protectionism. If the protectionist policy bundle on the voter’s table also contains closed borders and anti-immigration stances, the difference between  and

and  can be expected to be larger than in the case of economic protectionism alone. This is because left-wing ideology is socially more inclusive, and hence the threshold to switch to an exclusionary immigration policy is much higher for left-wing than for right-wing voters. The implication is that when

can be expected to be larger than in the case of economic protectionism alone. This is because left-wing ideology is socially more inclusive, and hence the threshold to switch to an exclusionary immigration policy is much higher for left-wing than for right-wing voters. The implication is that when  is shocked downward by a crisis, a disproportionately large fraction of the voters who shift from opposing to supporting condition (2) are right-wing.

is shocked downward by a crisis, a disproportionately large fraction of the voters who shift from opposing to supporting condition (2) are right-wing.

2.3 The Consequent Cultural Clashes

One of today’s most pronounced cultural cleavages pits the traditional left’s progressive, inclusive vision – centered on diversity and equal opportunity – against a conservative impulse to protect identity by excluding immigrants and minority cultures from the political agenda. In other words, an “open” versus “closed” society. While other external factors (see Section 1.6) may also have heightened this divide, our key argument is that polarization on cultural issues can emerge naturally from shifting preferences over economic openness versus protectionism, even if individual ideologies remain unchanged.

In fact, for a moderate voter with no animosity against other groups based on hate or conflict history or whatever, but simply concerned about jobs and wages and alike, the decision to endorse a protectionist policy in the economic domain goes hand in hand with a closed borders support, which naturally leads to support a politician who campaigns on a set of exclusionary commitments. Thus, even moderate people now split in supporters for exclusion versus inclusion, even though they are still the same ideologically moderate people.

While any type of economic crisis may shift individual preferences toward protectionist commitments, it is important to distinguish which occupational groups are primarily affected. In our simplified model with two types of agents – those with low and high baseline probability  of being a market winner – globalization shocks (e.g., the China shock) mainly reduce

of being a market winner – globalization shocks (e.g., the China shock) mainly reduce  , thereby increasing insecurity particularly among occupations already vulnerable to external competition. Financial crises, by contrast, typically affect both

, thereby increasing insecurity particularly among occupations already vulnerable to external competition. Financial crises, by contrast, typically affect both  and

and  . Thus, the above implications for cultural division coming from the policy preferences effects extend to the classes that were not affected by the globalization shock. The increase in survey responses highlighting divisions on inclusion versus exclusion preferences is, therefore, potentially a simple byproduct of the extension of protection commitment preferences to the middle class.

. Thus, the above implications for cultural division coming from the policy preferences effects extend to the classes that were not affected by the globalization shock. The increase in survey responses highlighting divisions on inclusion versus exclusion preferences is, therefore, potentially a simple byproduct of the extension of protection commitment preferences to the middle class.

If the model is correct, we should observe that the China shock increased reported economic insecurity mostly among the “low- ” occupations, whereas the financial crisis triggered declines across the board but relatively more for the “high-

” occupations, whereas the financial crisis triggered declines across the board but relatively more for the “high- ” group. This suggests that cultural polarization may be an indirect effect of differentiated economic shocks across occupational strata, and the empirical analysis will support this mechanism. Posturing on culturally divisive issues has always been an equilibrium behavior (see Ash et al., Reference Ash, Morelli and Van Weelden2017), but especially so when traditional economic policy positions on left and right lost support across classes due to the crises affecting most of them.

” group. This suggests that cultural polarization may be an indirect effect of differentiated economic shocks across occupational strata, and the empirical analysis will support this mechanism. Posturing on culturally divisive issues has always been an equilibrium behavior (see Ash et al., Reference Ash, Morelli and Van Weelden2017), but especially so when traditional economic policy positions on left and right lost support across classes due to the crises affecting most of them.

2.4 Turnout Effects

In the simple theoretical framework described so far, we used the language of “preferences” for one or the other policy; but having a preference for one policy over another does not necessarily mean that the voter will turn out to vote. Participation is, of course, a crucial component of elections.

Using the as-if-pivotal voting assumption (see, e.g., Alesina and Rosenthal, Reference Alesina and Rosenthal1996), combined with the standard assumption of an orthogonal distribution of stochastic voting costs, the simplest theory of turnout predicts that a citizen will vote whenever the difference in expected utility between her preferred policy and the alternative exceeds her realized cost of voting. In this framework, citizens who are nearly indifferent between alternatives (i.e., for whom  is very close to

is very close to  ) are the least likely to vote.

) are the least likely to vote.

Thus, a downward shock in  caused by a crisis or corruption scandal is likely to increase abstention among those who previously had

caused by a crisis or corruption scandal is likely to increase abstention among those who previously had  . Given that the

. Given that the  shock affects everyone in the same direction, those who were previously abstaining may now shift to voting for a populist protectionist platform. For citizens experiencing a very large drop in the expected utility of the status quo, there can be a direct switch from one voting choice to the other. More commonly, however, the two effects operate separately: abstention becomes more attractive for those who previously supported open markets, while the populist option becomes more appealing to those who were previously near-indifferent and abstaining.

shock affects everyone in the same direction, those who were previously abstaining may now shift to voting for a populist protectionist platform. For citizens experiencing a very large drop in the expected utility of the status quo, there can be a direct switch from one voting choice to the other. More commonly, however, the two effects operate separately: abstention becomes more attractive for those who previously supported open markets, while the populist option becomes more appealing to those who were previously near-indifferent and abstaining.

Moreover, given  , the prediction on turnout for left- and right-wing voters when

, the prediction on turnout for left- and right-wing voters when  is shocked downward by a crisis is different: turnout of left-wing voters may go down because the distribution of

is shocked downward by a crisis is different: turnout of left-wing voters may go down because the distribution of  values is correlated with income and class, such that the increased fraction of potential losers is more concentrated on the left, but since

values is correlated with income and class, such that the increased fraction of potential losers is more concentrated on the left, but since  is lower such left-wing citizens are more likely to station in the abstention pool; on the other hand, among those right-wing voters who were close to indifferent before the crisis, it is more likely that they jump over to vote for a protectionist closed markets and closed border party, since

is lower such left-wing citizens are more likely to station in the abstention pool; on the other hand, among those right-wing voters who were close to indifferent before the crisis, it is more likely that they jump over to vote for a protectionist closed markets and closed border party, since  is higher.

is higher.

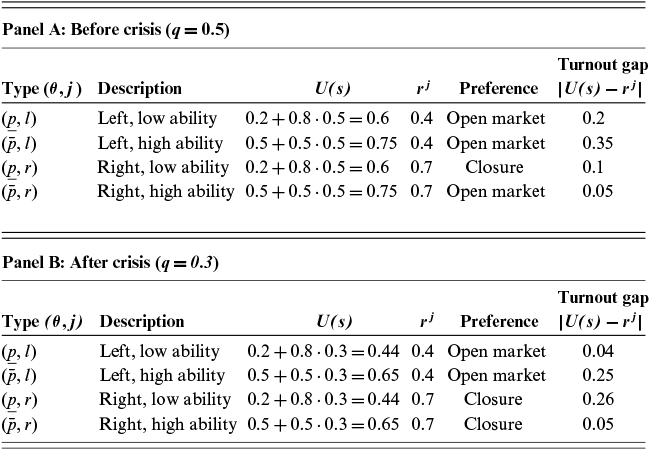

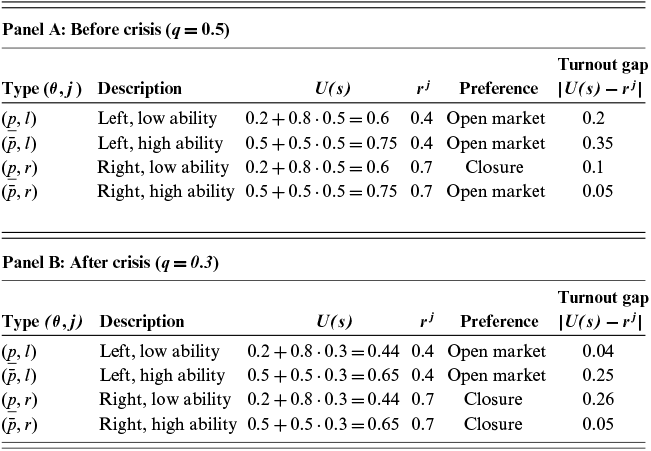

Let us illustrate the point with a numerical example.

Suppose  ,

,  ,

,  ; the initial

; the initial  was 0.5 and the new after crisis is 0.3. Finally, suppose that among left-wing voters

was 0.5 and the new after crisis is 0.3. Finally, suppose that among left-wing voters  is simply that half have

is simply that half have  and the other half have

and the other half have  . Among right-wing voters, those with

. Among right-wing voters, those with  are actually 70%. Thus, within this numerical example, condition (2) has to be evaluated differently not only for left and right but also for

are actually 70%. Thus, within this numerical example, condition (2) has to be evaluated differently not only for left and right but also for  and

and  types within each ideology; hence there are four different conditions.

types within each ideology; hence there are four different conditions.

For a high-ability right-wing citizen, the expected utility of open market is 0.75 before the crisis, thus greater than the 0.7 of protectionism; hence before the crisis all the high-ability right-wing prefer open markets. Low ability  types among right-wing citizens have 0.6 from open market, hence they prefer protectionism. On the left, all prefer open markets or borders over closed markets or borders before the crisis because of the much lower

types among right-wing citizens have 0.6 from open market, hence they prefer protectionism. On the left, all prefer open markets or borders over closed markets or borders before the crisis because of the much lower  . So, in terms of preferences between the two alternative policies, only low-ability right-wing citizens prefer to close everything, but for any cost of voting

. So, in terms of preferences between the two alternative policies, only low-ability right-wing citizens prefer to close everything, but for any cost of voting  we need to zoom in on willingness to turnout as well: for high-ability right-wing voters, the difference in expected benefit between the two alternative policies is only 0.05; hence only those in that set with very low cost realization will turn out to vote. On the other hand, for low-ability right-wing people the difference in expected benefit is 0.1 (in favor of protectionism), and thus the expected turnout among right-wing voters is higher within the low-ability segment. On the left, on the other hand, for high-ability citizens the expected benefit gap is 0.35, and hence they likely vote, if the distribution of costs, for example, goes from zero to 1. Finally, among low-ability left-wing people the expected benefit gap is 0.2, and therefore their turnout rate is somewhere between that of high-ability left-wing and that of right-wing voters. Thus, in the status quo precrisis only low-ability right-wing people would be interested in a populist protectionist policy, and they would almost surely lose, given the higher turnout on the left and low expected turnout on the right. Hence, a populist party might not even enter the race.

we need to zoom in on willingness to turnout as well: for high-ability right-wing voters, the difference in expected benefit between the two alternative policies is only 0.05; hence only those in that set with very low cost realization will turn out to vote. On the other hand, for low-ability right-wing people the difference in expected benefit is 0.1 (in favor of protectionism), and thus the expected turnout among right-wing voters is higher within the low-ability segment. On the left, on the other hand, for high-ability citizens the expected benefit gap is 0.35, and hence they likely vote, if the distribution of costs, for example, goes from zero to 1. Finally, among low-ability left-wing people the expected benefit gap is 0.2, and therefore their turnout rate is somewhere between that of high-ability left-wing and that of right-wing voters. Thus, in the status quo precrisis only low-ability right-wing people would be interested in a populist protectionist policy, and they would almost surely lose, given the higher turnout on the left and low expected turnout on the right. Hence, a populist party might not even enter the race.