1. Introduction

Cyber-risk is nowadays widely acknowledged as one of the major sources of operational risk for organizations worldwide. The 2024 ENISA Threat Landscape Report (ENISA, 2024) documents “a notable escalation in cybersecurity attacks, setting new benchmarks in both the variety and number of incidents, as well as their consequences.” According to the AON 9th Global Risk Management Survey,Footnote 1 cyberattacks and data breaches represent the foremost source of global risk faced by organizations, with the second biggest risk being business interruption, which is itself often a consequence of cyber-incidents. A recent poll on Risk.net confirms information security and IT disruption as the top two sources of operational risk for 2025.Footnote 2 According to IBM, the global average cost of a data breach has reached nearly 5 M USD in 2024, an increase of more than 10% over the previous year.Footnote 3

The rapid and widespread emergence of cyber-risk as a key source of operational risk has led to a significant increase in cybersecurity spending. In the 2025 ICS/OT cybersecurity budget survey of the SANS Institute (2025), 55% of the respondents reported a substantial rise in cybersecurity budgets over the previous two years. This trend underscores the importance of adopting effective cybersecurity investment policies that balance risk mitigation with cost efficiency.

The problem of optimal cybersecurity investment has been first addressed in the seminal work of Gordon and Loeb (Reference Fedele and Roner2002). In their model, reviewed in Section 2.1 below, the decision maker can reduce the vulnerability to cyberattacks by investing in cybersecurity. The optimal expenditure in cybersecurity is determined by maximizing the expected net benefit of reducing the breach probability. The Gordon–Loeb model laid the foundations for a rigorous quantitative analysis of cybersecurity investments and has been the subject of numerous extensions and generalizations: we mention here only some studies that are closely related to our context, referring to Fedele and Roner (Reference Gordon and Loeb2022) for a comprehensive overview. The key ingredient of the Gordon–Loeb model is represented by the security breach probability function (see Section 2.1), which has been further analyzed in Huang and Behara (Reference Huang and Behara2013) and Mazzoccoli and Naldi (Reference Mazzoccoli and Naldi2022). The risk-neutral assumption of the original model (Gordon & Loeb, Reference Gordon and Loeb2002) has been relaxed to accommodate risk-averse preferences in Miaoui and Boudriga (Reference Miaoui and Boudriga2019). The practical applicability of the Gordon–Loeb model for guiding cost-effective cybersecurity investment decisions has been examined in Gordon et al. (Reference Gordon, Loeb and Zhou2020) within the National Institute of Standards and Technology (NIST) cybersecurity framework.

The original Gordon–Loeb model is a static model and, therefore, does not allow addressing the crucial issue of the optimal timing of investment decisions. Adopting a real-options approach, Gordon et al. (Reference Gordon, Loeb and Lucyshyn2003) and Tatsumi and Goto (Reference Tatsumi, Goto, Moore, Pym and Ioannidis2010) have proposed dynamic versions of the model that allow analyzing the optimal timing and level of cybersecurity investment. Closer to our setup, a dynamic extension of the Gordon–Loeb model has been developed in Krutilla et al. (Reference Krutilla, Alexeev, Jardine and Good2021), considering the problem of optimal cybersecurity investment over an infinite time horizon and assuming that cybersecurity assets are subject to depreciation over time, while future net benefits of cybersecurity investment are discounted.

An effective cybersecurity investment policy must be adaptive and evolve in response to changing threat environments. As noted by Zeller and Scherer (Reference Zeller and Scherer2022), a key feature of cyber-risk is its dynamic nature due to the rapid technological transformation and the evolution of threat actors. Similarly, Balzano and Marzi (Reference Balzano and Marzi2025) emphasize the need for adaptable and responsive cybersecurity policies in order to face the challenge of dynamic cyberattacks. The framework of Krutilla et al. (Reference Krutilla, Alexeev, Jardine and Good2021) is based on a deterministic model and, therefore, cannot capture the dynamic behavior of cyber-risk. Addressing this need, the main contribution of this work consists in proposing a modeling framework for optimal cybersecurity investment in a dynamic stochastic setup, allowing for investment policies that respond in real time to randomly occurring cyberattacks. Our work contributes both to cyber-risk modeling and to cyber-risk management, as categorized in the recent survey by He et al. (Reference He, Jin and Li2024). Moreover, our stochastic modeling framework takes into account the empirically relevant feature of temporally clustered cyberattacks, as discussed in the next subsection.

1.1 Modeling cyberattacks with Hawkes processes

A distinctive feature of our modeling framework, which will be described in Section 2.2, is the use of a Hawkes process to model the arrival of cyberattacks. First introduced by Alan G. Hawkes in Hawkes (Reference Hawkes1971), these stochastic processes are used to model event arrivals over time and are particularly suited to situations where the occurrence of one event increases the likelihood of subsequent events (self-excitation), thereby generating temporally clustered events. In our context, we denote by

$N_t$

the cumulative number of cyberattacks up to time

$N_t$

the cumulative number of cyberattacks up to time

$t$

, modeled as a Hawkes process, and by

$t$

, modeled as a Hawkes process, and by

$\lambda _t$

the associated stochastic intensity (hazard rate), representing the instantaneous likelihood of an attack occurring.

$\lambda _t$

the associated stochastic intensity (hazard rate), representing the instantaneous likelihood of an attack occurring.

The self-exciting property of the Hawkes process

$(N_t)_{t\geq 0}$

is captured by the specification of its stochastic intensity:

$(N_t)_{t\geq 0}$

is captured by the specification of its stochastic intensity:

\begin{align} \lambda _t &= \alpha +(\lambda _0-\alpha )e^{-\xi t} + \beta \sum _{i=1}^{N_t} e^{-\xi (t-\tau _i)}, \end{align}

\begin{align} \lambda _t &= \alpha +(\lambda _0-\alpha )e^{-\xi t} + \beta \sum _{i=1}^{N_t} e^{-\xi (t-\tau _i)}, \end{align}

for all

$t\geq 0$

, where

$t\geq 0$

, where

-

•

$\alpha \gt 0$

is the long-term mean intensity;

$\alpha \gt 0$

is the long-term mean intensity; -

•

$\lambda _0\gt 0$

is the intensity at the initial time

$t = 0$

; -

•

$\xi \gt 0$

is the exponential decay rate; -

•

$\beta \gt 0$

determines the magnitude of self-excitation; -

•

$(\tau _i)_{i\in \mathbb{N}^*}$

are the random times at which attacks occur.

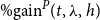

Figure 1 shows a simulated trajectory of

$N$

and

$N$

and

$\lambda$

, showing the clustering behavior induced by the self-exciting mechanism described above. General presentations of the theory and the applications of Hawkes processes can be found in Laub et al. (Reference Laub, Lee and Taimre2021) and Lima (Reference Lima2023).

$\lambda$

, showing the clustering behavior induced by the self-exciting mechanism described above. General presentations of the theory and the applications of Hawkes processes can be found in Laub et al. (Reference Laub, Lee and Taimre2021) and Lima (Reference Lima2023).

One simulated trajectory of

$N$

(top) and

$N$

(top) and

$\lambda$

(bottom), for

$\lambda$

(bottom), for

$\alpha =27$

,

$\alpha =27$

,

$\lambda _0=27$

,

$\lambda _0=27$

,

$\xi =15$

, and

$\xi =15$

, and

$\beta =9$

.

$\beta =9$

.

Figure 1 Long description

Panel A: A line graph shows the trajectory of N sub t over time in years. The x-axis represents time in years, ranging from 0 to 2. The y-axis represents N sub t, ranging from 0 to 120. The solid line represents N sub t, while the dashed line represents E sub N sub t. The graph shows an increasing trend for both N sub t and E sub N sub t over time. Panel B: A line graph shows the trajectory of lambda sub t over time in years. The x-axis represents time in years, ranging from 0 to 2. The y-axis represents lambda sub t, ranging from 0 to 100. The solid line represents lambda sub t, while the dashed line represents E sub lambda sub t. The graph shows fluctuations in lambda sub t with a general decreasing trend over time.

This modeling choice is particularly relevant in the context of cyber-risk. Cyberattacks frequently occur in bursts, for instance, following the discovery of a vulnerability or due to the propagation of malware across interconnected systems (see Nguyen et al., Reference Nguyen, Alain, Autrel, Bouabdallah, François and Doyen2024). Such clustered patterns are not adequately captured by memoryless models, such as those based on Poisson processes.

Empirical evidence supports the appropriateness of the Hawkes framework for modeling cyber-risk. A contagious behavior in cyberattacks has been documented in Baldwin et al. (Reference Baldwin, Gheyas, Ioannidis, Pym and Williams2017), analyzing the threats to key internet services using data from the SANS Institute. Using data from the Privacy Rights Clearinghouse, it has been empirically demonstrated in Bessy-Roland et al. (Reference Bessy-Roland, Boumezoued and Hillairet2021) that Hawkes-based models provide a more realistic representation of the interdependence of data breaches compared to Poisson-based models. The recent work (Boumezoued et al., Reference Boumezoued, Cherkaoui and Hillairet2023) reinforces this perspective by calibrating a two-phase Hawkes model to cyberattack data, taking into account the publication of cyber-vulnerabilities. These studies provide strong support for modeling cyberattacks via Hawkes processes, as described in more detail in Section 2.2.

1.2 Goals and main contributions

In this work, we address the challenge of optimal cybersecurity investment under temporally clustered cyberattacks, in line with the empirical evidence reported above. In particular, we aim at studying the adaptive investment policy that best responds in real time to the random arrival of cyberattacks, within a framework that balances realism with analytical tractability. To this end, we develop a continuous-time stochastic extension of the classical Gordon–Loeb model, describing attack arrivals with a Hawkes process. The model incorporates key operational features such as technological obsolescence and the decreasing marginal effectiveness of large investments. The resulting optimization problem is cast as a stochastic optimal control problem and solved via dynamic programming methods. We develop efficient numerical schemes to compute the optimal policy, and we quantify the benefits of dynamic investment strategies under clustered attacks. By integrating risk dynamics into the cybersecurity investment problem, our framework provides new insights into how organizations can better allocate resources to mitigate cyber-risk.

1.3 Structure of the paper

In Section 2, we recall the original Gordon–Loeb model and introduce our continuous-time stochastic extension. In Section 3, we formulate the cybersecurity investment problem and characterize the optimal policy. Section 4 details the model parameters and the numerical methods used in our analysis. Section 5 presents the results of our numerical analysis and discusses their practical implications for cyber-risk management. Section 6 discusses the relevance of our study from an insurance perspective, also in relation to the calculation of premia for cyber-insurance contracts. Section 7 concludes.

2. The model

We study the decision problem faced by an entity (a public administration or a large corporation) that is threatened by a massive number of randomly occurring cyberattacks with a temporally clustered pattern. As in the Gordon–Loeb model (reviewed in Section 2.1), not all cyberattacks result in successful breaches of the entity’s system. The success rate of each attack depends on the system’s vulnerability, which the entity can mitigate by investing in cybersecurity.

2.1 The Gordon–Loeb model

The Gordon–Loeb model, introduced in 2002 in the seminal work (Gordon & Loeb, Reference Gordon and Loeb2002), provides a static framework for determining the optimal investment in cybersecurity to protect a given information set under the threat of cyberattacks. In our context, the information set corresponds to the entity’s IT infrastructure. In the Gordon–Loeb model, the information set is characterized by three key parameters, all assumed to be constant:

-

•

$p \,{\in \,[0,\,1]}$

: the probability that a cyberattack occurs; -

•

$v \,{\in \,[0,\,1]}$

: the baseline probability that a cyberattack successfully breaches the information set (vulnerability); -

•

$\ell \,{\ge \, 0}$

: the loss incurred when a breach occurs.

The vulnerability

$v$

refers to a baseline level of security, reflecting the cybersecurity measures already in place before any new decision is taken. Without any further investment in cybersecurity, the expected loss is

$v$

refers to a baseline level of security, reflecting the cybersecurity measures already in place before any new decision is taken. Without any further investment in cybersecurity, the expected loss is

$vp\ell$

. To mitigate its vulnerability, the entity may invest an additional amount

$vp\ell$

. To mitigate its vulnerability, the entity may invest an additional amount

$z \geq 0$

in cybersecurity. The variable

$z \geq 0$

in cybersecurity. The variable

$z$

therefore represents incremental cybersecurity investment beyond the existing baseline protection. In particular,

$z$

therefore represents incremental cybersecurity investment beyond the existing baseline protection. In particular,

$z = 0$

means that no further investment is made, but the system still retains the prior protection embodied in

$z = 0$

means that no further investment is made, but the system still retains the prior protection embodied in

$v$

. Throughout the paper, absence of cybersecurity investment will refer to the case

$v$

. Throughout the paper, absence of cybersecurity investment will refer to the case

$z = 0$

. The effectiveness of the investment

$z = 0$

. The effectiveness of the investment

$z$

is measured by a security breach probability function

$z$

is measured by a security breach probability function

$S(z, v)$

, which represents the probability that an attack successfully breaches the information set, given investment level

$S(z, v)$

, which represents the probability that an attack successfully breaches the information set, given investment level

$z$

and the vulnerability

$z$

and the vulnerability

$v$

. The resulting expected loss is thus

$v$

. The resulting expected loss is thus

$S(z, v)p\ell$

. Gordon and Loeb require the function

$S(z, v)p\ell$

. Gordon and Loeb require the function

$S$

to satisfy the properties listed in the following assumption.

$S$

to satisfy the properties listed in the following assumption.

Assumption A.

-

(A1)

$S(z, 0) = 0$

, for all

$z\geq 0$

, i.e., an invulnerable information set always remains invulnerable;

-

(A2)

$S(0, v) = v$

, i.e., in the absence of investment, the information set retains its baseline vulnerability;

-

(A3)

$S$

is decreasing and convex in

$z$

, so that

$S_z(z, v) \lt 0$

and

$S_{zz}(z, v) \gt 0$

, for all

$z\geq 0$

, i.e., cybersecurity investment reduces breach probability with diminishing marginal effectiveness.

Gordon and Loeb consider two classes of security breach probability functions, which satisfy AssumptionA:

\begin{equation} S_I(z, v) = \frac {v}{(az+1)^b} \quad \text{and}\quad S_{II}(z, v) = v^{a z+1}, \end{equation}

\begin{equation} S_I(z, v) = \frac {v}{(az+1)^b} \quad \text{and}\quad S_{II}(z, v) = v^{a z+1}, \end{equation}

for some parameters

$a, b\gt 0$

.

$a, b\gt 0$

.

In Gordon and Loeb (Reference Fedele and Roner2002), the optimal investment in cybersecurity is determined by maximizing the Expected Net Benefit of Investment in Information Security (ENBIS), defined as follows:

\begin{equation} \text{ENBIS}(z) \,:\!=\, (v - S(z, v))p \ell - z. \end{equation}

\begin{equation} \text{ENBIS}(z) \,:\!=\, (v - S(z, v))p \ell - z. \end{equation}

The ENBIS function quantifies the net trade-off between the benefit (captured by the reduction in the expected loss due to the investment in cybersecurity) and the direct cost of investing. Under AssumptionA, the optimal investment level

$z^*$

is determined by the following first-order condition:

$z^*$

is determined by the following first-order condition:

\begin{equation*} -S_z(z^*,v)p \ell -1=0. \end{equation*}

\begin{equation*} -S_z(z^*,v)p \ell -1=0. \end{equation*}

Remark 1. For both classes of security breach functions in (2), Gordon and Loeb show that the optimal cybersecurity investment never exceeds

$1/e\approx 37\%$

of the expected loss:

$1/e\approx 37\%$

of the expected loss:

\begin{equation*} z^*\lt \frac {v p \ell }{e}. \end{equation*}

\begin{equation*} z^*\lt \frac {v p \ell }{e}. \end{equation*}

2.2 A continuous-time model driven by a Hawkes process

We now introduce a continuous-time model for randomly occurring cyberattacks. As discussed in Section 1.1, we want to capture the empirically relevant feature of clustering of cyberattacks while retaining the key elements of the original Gordon–Loeb model reviewed in Section 2.1.

The arrival of cyberattacks is described by a Hawkes process

$N=(N_t)_{t\geq 0}$

, defined on a probability space

$N=(N_t)_{t\geq 0}$

, defined on a probability space

$(\Omega , \mathcal{F}, \mathbb{P})$

, with

$(\Omega , \mathcal{F}, \mathbb{P})$

, with

$N_t$

representing the number of cyberattacks up to time

$N_t$

representing the number of cyberattacks up to time

$t$

, for all

$t$

, for all

$t\geq 0$

. As explained in Section 1.1, the process

$t\geq 0$

. As explained in Section 1.1, the process

$N$

is characterized by a self-exciting stochastic intensity

$N$

is characterized by a self-exciting stochastic intensity

$(\lambda _t)_{t\geq 0}$

solving the following stochastic differential equation:

$(\lambda _t)_{t\geq 0}$

solving the following stochastic differential equation:

\begin{equation} \mathrm{d} \lambda _t= \xi (\alpha -\lambda _t)\, \mathrm{d} t + \beta \mathrm{d} {N}_t, \quad \lambda _0\gt 0, \end{equation}

\begin{equation} \mathrm{d} \lambda _t= \xi (\alpha -\lambda _t)\, \mathrm{d} t + \beta \mathrm{d} {N}_t, \quad \lambda _0\gt 0, \end{equation}

whose explicit solution is given by (1). In the next proposition (adapted from Dassios & Zhao, Reference Dassios and Zhao2013), we compute the expectation of some basic quantities, which will be used later.Footnote 4

Proposition 1.

Let

$(N_t)_{t\geq 0}$

be a Hawkes process with intensity

$(N_t)_{t\geq 0}$

be a Hawkes process with intensity

$(\lambda _t)_{t\geq 0}$

given in (4

), with

$(\lambda _t)_{t\geq 0}$

given in (4

), with

$\beta \lt \xi$

. Then, for all

$\beta \lt \xi$

. Then, for all

$t\geq 0$

,

$t\geq 0$

,

\begin{align*} \mathbb{E}[\lambda _t]&=\frac {\alpha \xi }{\xi -\beta } + e^{-(\xi -\beta )t}\left ( \lambda _0-\frac {\alpha \xi }{\xi -\beta } \right )\!, \\[3pt] \mathbb{E}[N_t]&=\int _0^t \mathbb{E}[\lambda _s] \mathrm{d} s \\[3pt] &= \frac {\alpha \xi }{\xi -\beta } t - \frac {1}{\xi -\beta } \left (\lambda _0-\frac {\alpha \xi }{\xi -\beta } \right ) \big(e^{-(\xi -\beta )t}-1\big). \end{align*}

\begin{align*} \mathbb{E}[\lambda _t]&=\frac {\alpha \xi }{\xi -\beta } + e^{-(\xi -\beta )t}\left ( \lambda _0-\frac {\alpha \xi }{\xi -\beta } \right )\!, \\[3pt] \mathbb{E}[N_t]&=\int _0^t \mathbb{E}[\lambda _s] \mathrm{d} s \\[3pt] &= \frac {\alpha \xi }{\xi -\beta } t - \frac {1}{\xi -\beta } \left (\lambda _0-\frac {\alpha \xi }{\xi -\beta } \right ) \big(e^{-(\xi -\beta )t}-1\big). \end{align*}

We denote by

$(\tau _i)_{i\in \mathbb{N}^*}$

the random jump times of the process

$(\tau _i)_{i\in \mathbb{N}^*}$

the random jump times of the process

$N$

, representing the arrival times of cyberattacks. For each

$N$

, representing the arrival times of cyberattacks. For each

$t\geq 0$

, we denote by

$t\geq 0$

, we denote by

$\mathcal{F}_t\,:\!=\,\sigma (N_s; \, s\leq t)$

the sigma-field generated by the Hawkes process

$\mathcal{F}_t\,:\!=\,\sigma (N_s; \, s\leq t)$

the sigma-field generated by the Hawkes process

$N$

up to time

$N$

up to time

$t$

, representing the information generated by the history of the attack timings up to time

$t$

, representing the information generated by the history of the attack timings up to time

$t$

. In the following, this is assumed to be the information set available to the decision maker (see also RemarkReference Balzano and Marzi3 below).

$t$

. In the following, this is assumed to be the information set available to the decision maker (see also RemarkReference Balzano and Marzi3 below).

In the absence of cybersecurity investment, each attack is assumed to breach the entity’s IT system with fixed probability

$v$

(vulnerability). For each

$v$

(vulnerability). For each

$i\in \mathbb{N}^*$

, we introduce a Bernoulli random variable

$i\in \mathbb{N}^*$

, we introduce a Bernoulli random variable

$B^v_i$

of parameter

$B^v_i$

of parameter

$v$

, where the event

$v$

, where the event

$\{ B^v_i = 1 \}$

corresponds to a successful breach caused by the

$\{ B^v_i = 1 \}$

corresponds to a successful breach caused by the

$i$

-th attack. In the event of a breach, the entity incurs a random monetary loss

$i$

-th attack. In the event of a breach, the entity incurs a random monetary loss

$\eta _i$

, realized at the attack time

$\eta _i$

, realized at the attack time

$\tau _i$

. Otherwise, if

$\tau _i$

. Otherwise, if

$B^v_i = 0$

, the attack is blocked and no loss occurs at time

$B^v_i = 0$

, the attack is blocked and no loss occurs at time

$\tau _i$

.

$\tau _i$

.

The families of random variables

$(B^v_i)_{i\in \mathbb{N}^*}$

and

$(B^v_i)_{i\in \mathbb{N}^*}$

and

$(\eta _i)_{i\in \mathbb{N}^*}$

are assumed to satisfy the following standing assumption.

$(\eta _i)_{i\in \mathbb{N}^*}$

are assumed to satisfy the following standing assumption.

Assumption B.

The family

$(\eta _i)_{i\in \mathbb{N}^*}$

is composed of i.i.d. positive random variables in

$(\eta _i)_{i\in \mathbb{N}^*}$

is composed of i.i.d. positive random variables in

$L^1(\mathbb{P})$

. The families

$L^1(\mathbb{P})$

. The families

$(\eta _i)_{i\in \mathbb{N}^*}$

and

$(\eta _i)_{i\in \mathbb{N}^*}$

and

$(B^v_i)_{i\in \mathbb{N}^*}$

are mutually independent and independent of

$(B^v_i)_{i\in \mathbb{N}^*}$

are mutually independent and independent of

$N$

.

$N$

.

Remark 2. The assumption that the losses

$(\eta _i)_{i\in \mathbb{N}^*}$

are independent of the attack arrival process

$(\eta _i)_{i\in \mathbb{N}^*}$

are independent of the attack arrival process

$N$

can be restrictive from an empirical viewpoint. In practice, both the frequency and the severity of cyber losses can increase during periods of clustered attacks. From a modeling standpoint, this assumption can be relaxed, for instance, by allowing the loss distribution to depend on the current intensity, making use of the techniques recently developed in Hillairet et al. (Reference Hillairet, Peyrat and Réveillac2025). However, introducing such dependency would significantly complicate the analysis of the optimization problem in Section 3 and require precise information on the conditional distribution of losses given the attack dynamics. In the absence of sufficient publicly available data on cyber losses, we retain the independence assumption as a tractable and transparent modeling choice.

$N$

can be restrictive from an empirical viewpoint. In practice, both the frequency and the severity of cyber losses can increase during periods of clustered attacks. From a modeling standpoint, this assumption can be relaxed, for instance, by allowing the loss distribution to depend on the current intensity, making use of the techniques recently developed in Hillairet et al. (Reference Hillairet, Peyrat and Réveillac2025). However, introducing such dependency would significantly complicate the analysis of the optimization problem in Section 3 and require precise information on the conditional distribution of losses given the attack dynamics. In the absence of sufficient publicly available data on cyber losses, we retain the independence assumption as a tractable and transparent modeling choice.

The cumulative loss incurred over a planning horizon

$[0,T]$

, in the absence of cybersecurity investment, is given by:

$[0,T]$

, in the absence of cybersecurity investment, is given by:

\begin{equation} L_T^0 \,:\!=\, \sum _{i=1}^{N_T} \eta _i B_i^v. \end{equation}

\begin{equation} L_T^0 \,:\!=\, \sum _{i=1}^{N_T} \eta _i B_i^v. \end{equation}

In our dynamic model, the entity can react to the evolving threat environment by investing in cybersecurity in order to mitigate its vulnerability to cyberattacks. Investment occurs continuously throughout the planning horizon

$[0,T]$

and is described by a non-negative investment rate process

$[0,T]$

and is described by a non-negative investment rate process

$(z_t)_{t \in [0, T]}$

. For each

$(z_t)_{t \in [0, T]}$

. For each

$t\lt T$

, the quantity

$t\lt T$

, the quantity

$z_t$

represents the increase in the level of cybersecurity over the infinitesimal time interval

$z_t$

represents the increase in the level of cybersecurity over the infinitesimal time interval

$[t,t+\mathrm{d} t]$

and is assumed to be chosen based on the information set

$[t,t+\mathrm{d} t]$

and is assumed to be chosen based on the information set

$\mathcal{F}_{t-}$

available to the decision maker just before time

$\mathcal{F}_{t-}$

available to the decision maker just before time

$t$

.

$t$

.

Remark 3. In the terminology of stochastic processes, the requirement that the investment rate

$z_t$

must be chosen on the basis of

$z_t$

must be chosen on the basis of

$\mathcal{F}_{t-}$

corresponds to requiring the process

$\mathcal{F}_{t-}$

corresponds to requiring the process

$(z_t)_{t\in [0,T]}$

to be predictable with respect to the filtration generated by

$(z_t)_{t\in [0,T]}$

to be predictable with respect to the filtration generated by

$N$

. In particular, at any attack time

$N$

. In particular, at any attack time

$\tau _i$

, the value

$\tau _i$

, the value

$z_{\tau _i}$

is determined by the information

$z_{\tau _i}$

is determined by the information

$\mathcal F_{\tau _i-}$

: the decision maker may adjust investment after observing an attack, but not in a way that anticipates the attack at the same instant. We point out that, in our setup, the outcomes of previous attacks (i.e., whether an attack has successfully breached the system or not) do not carry any relevant informational content for decision making, as they do not affect the dynamics of future attack arrivals.

$\mathcal F_{\tau _i-}$

: the decision maker may adjust investment after observing an attack, but not in a way that anticipates the attack at the same instant. We point out that, in our setup, the outcomes of previous attacks (i.e., whether an attack has successfully breached the system or not) do not carry any relevant informational content for decision making, as they do not affect the dynamics of future attack arrivals.

Investment in cybersecurity is subject to rapid technological obsolescence (see, e.g., Hayes & Bodhani, Reference Hayes and Bodhani2013). In line with Krutilla et al. (Reference Krutilla, Alexeev, Jardine and Good2021), we take into account this significant aspect in our model by introducing a depreciation rate

$\rho \gt 0$

. The cybersecurity level reached at time

$\rho \gt 0$

. The cybersecurity level reached at time

$t$

is then defined as follows, for all

$t$

is then defined as follows, for all

$t\in [0,T]$

:

$t\in [0,T]$

:

\begin{equation} H^z_t=H_0e^{-\rho t}+\int _0^t e^{-\rho (t-s)}z_s \mathrm{d} s, \end{equation}

\begin{equation} H^z_t=H_0e^{-\rho t}+\int _0^t e^{-\rho (t-s)}z_s \mathrm{d} s, \end{equation}

which equivalently, in differential form, reads as follows:

\begin{equation*} \mathrm{d} H^z_t= \left(z_t-\rho H^z_t\right)\mathrm{d} t, \qquad H^z_0=H_0\geq 0. \end{equation*}

\begin{equation*} \mathrm{d} H^z_t= \left(z_t-\rho H^z_t\right)\mathrm{d} t, \qquad H^z_0=H_0\geq 0. \end{equation*}

As in Krutilla et al. (Reference Krutilla, Alexeev, Jardine and Good2021), we interpret the cybersecurity level as an aggregated asset, which can be thought of as a combination of technological infrastructures, software, and human expertise.

In our continuous-time framework, we let the breach probability evolve dynamically with the current cybersecurity level. More specifically, suppose that the decision maker adopts an investment policy

$z=(z_t)_{t\in [0,T]}$

. At each attack time

$z=(z_t)_{t\in [0,T]}$

. At each attack time

$\tau _i$

, a breach is assumed to occur with probability

$\tau _i$

, a breach is assumed to occur with probability

\begin{equation} S(H^z_{\tau _i},v), \end{equation}

\begin{equation} S(H^z_{\tau _i},v), \end{equation}

where

$H^z_{\tau _i}$

is given by (6) evaluated at

$H^z_{\tau _i}$

is given by (6) evaluated at

$t=\tau _i$

and

$t=\tau _i$

and

$S$

is a security breach probability function satisfying AssumptionA, as in the original Gordon–Loeb model. Hence, the probability that the

$S$

is a security breach probability function satisfying AssumptionA, as in the original Gordon–Loeb model. Hence, the probability that the

$i$

-th attack successfully breaches the IT system depends on the cybersecurity level

$i$

-th attack successfully breaches the IT system depends on the cybersecurity level

$H^z_{\tau _i}$

reached at the attack’s time

$H^z_{\tau _i}$

reached at the attack’s time

$\tau _i$

. In turn,

$\tau _i$

. In turn,

$H^z_{\tau _i}$

is determined by the investment realized over the time period

$H^z_{\tau _i}$

is determined by the investment realized over the time period

$[0,\tau _i]$

, taking into account technological obsolescence. If the

$[0,\tau _i]$

, taking into account technological obsolescence. If the

$i$

-th attack breaches the IT system, then the entity incurs a loss of

$i$

-th attack breaches the IT system, then the entity incurs a loss of

$\eta _i$

; otherwise, the attack is blocked and the entity does not suffer any loss at time

$\eta _i$

; otherwise, the attack is blocked and the entity does not suffer any loss at time

$\tau _i$

.

$\tau _i$

.

Remark 4. The proposed model allows for adaptive real-time cybersecurity investment. More specifically, the arrival of an attack triggers an increased likelihood of further attacks within a short timeframe due to the form (4) of the intensity. The decision maker can respond in real-time by increasing cybersecurity investment, which in turn reduces future breach probabilities through the function

$S$

in (7). The optimal investment policy will be determined in Section 3, while the practical importance of allowing for an adaptive real-time investment strategy – rather than a static policy as in the original Gordon–Loeb model – will be empirically analyzed in Section 5.3.

$S$

in (7). The optimal investment policy will be determined in Section 3, while the practical importance of allowing for an adaptive real-time investment strategy – rather than a static policy as in the original Gordon–Loeb model – will be empirically analyzed in Section 5.3.

Analogously to the case without investment in cybersecurity, we can write as follows the cumulative losses

$L^z_T$

incurred on the time interval

$L^z_T$

incurred on the time interval

$[0,T]$

when investing in cybersecurity according to a generic rate

$[0,T]$

when investing in cybersecurity according to a generic rate

$z=(z_t)_{t\in [0,T]}$

:

$z=(z_t)_{t\in [0,T]}$

:

\begin{equation} L_T^z \,:\!=\, \sum _{i=1}^{N_T} \eta _i B_i^{S(H^z_{\tau _i},v )}, \end{equation}

\begin{equation} L_T^z \,:\!=\, \sum _{i=1}^{N_T} \eta _i B_i^{S(H^z_{\tau _i},v )}, \end{equation}

where

$(B_i^{S(H^z_{\tau _i},v )})_{i\in \mathbb{N}^*}$

is a family of random variables taking values in

$(B_i^{S(H^z_{\tau _i},v )})_{i\in \mathbb{N}^*}$

is a family of random variables taking values in

$\{0,1\}$

and satisfying the following assumption.

$\{0,1\}$

and satisfying the following assumption.

Assumption C.

For any process

$(z_t)_{t\in [0,T]}$

, it holds that

$(z_t)_{t\in [0,T]}$

, it holds that

\begin{equation*} \mathbb{P}\Bigl (B_i^{S(H^z_{\tau _i},v )}=1 \Big | \mathcal{F}_T\Bigr ) = S(H^z_{\tau _i},v), \qquad \text{ for all } i\in \mathbb{N}^*, \end{equation*}

\begin{equation*} \mathbb{P}\Bigl (B_i^{S(H^z_{\tau _i},v )}=1 \Big | \mathcal{F}_T\Bigr ) = S(H^z_{\tau _i},v), \qquad \text{ for all } i\in \mathbb{N}^*, \end{equation*}

where

$(H^z_t)_{t\in [0,T]}$

is determined by

$(H^z_t)_{t\in [0,T]}$

is determined by

$(z_t)_{t\in [0,T]}$

as in (6

). Moreover, for each

$(z_t)_{t\in [0,T]}$

as in (6

). Moreover, for each

$i\in \mathbb{N}^*$

, the random variables

$i\in \mathbb{N}^*$

, the random variables

$B_i^{S(H^z_{\tau _i},v )}$

and

$B_i^{S(H^z_{\tau _i},v )}$

and

$\eta _i$

are conditionally independent given

$\eta _i$

are conditionally independent given

$\mathcal{F}_T$

.

$\mathcal{F}_T$

.

Remark 5. The cumulative loss process

$(L^z_t)_{t\in [0,T]}$

defined as in (8) constitutes a marked Hawkes process in the terminology of point processes (see Brémaud, Reference Brémaud1981). In our modeling framework, the marks (losses) are endogenous and depend on the dynamically evolving cybersecurity level

$(L^z_t)_{t\in [0,T]}$

defined as in (8) constitutes a marked Hawkes process in the terminology of point processes (see Brémaud, Reference Brémaud1981). In our modeling framework, the marks (losses) are endogenous and depend on the dynamically evolving cybersecurity level

$(H^z_t)_{t\in [0,T]}$

.

$(H^z_t)_{t\in [0,T]}$

.

For strategic decision making, a key quantity is represented by the expected losses due to cyberattacks over the time interval

$[0,T]$

when adopting a suitable cybersecurity policy. This is the content of the following proposition, which will be fundamental for addressing the optimal investment problem in Section 3. We denote by

$[0,T]$

when adopting a suitable cybersecurity policy. This is the content of the following proposition, which will be fundamental for addressing the optimal investment problem in Section 3. We denote by

$\bar {\eta }\,:\!=\,\mathbb{E}[\eta _i]$

the expected loss resulting from a successful breach, for all

$\bar {\eta }\,:\!=\,\mathbb{E}[\eta _i]$

the expected loss resulting from a successful breach, for all

$i\in \mathbb{N}^*$

.

$i\in \mathbb{N}^*$

.

Proposition 2. Under Assumptions B and C, it holds that

\begin{align*} \mathbb{E} \left[L_T^0 \right]&= \bar {\eta }\,v\,\mathbb{E}\left [\int _0^T \lambda _t \mathrm{d} t\right ]\!, \\[5pt] \mathbb{E} \left[L_T^z \right]&= \bar {\eta }\,\mathbb{E}\left [\int _0^T S (H^z_t, v )\lambda _t \mathrm{d} t\right ]\!. \end{align*}

\begin{align*} \mathbb{E} \left[L_T^0 \right]&= \bar {\eta }\,v\,\mathbb{E}\left [\int _0^T \lambda _t \mathrm{d} t\right ]\!, \\[5pt] \mathbb{E} \left[L_T^z \right]&= \bar {\eta }\,\mathbb{E}\left [\int _0^T S (H^z_t, v )\lambda _t \mathrm{d} t\right ]\!. \end{align*}

Therefore, the expected net benefit of investment is

\begin{align} \mathbb{E}\left[L_T^0-L_T^z\right]&= \bar {\eta }\,\mathbb{E}\left [\int _0^T \left(v-S(H^z_t, v)\right) \lambda _t \mathrm{d} t \right ]\!. \end{align}

\begin{align} \mathbb{E}\left[L_T^0-L_T^z\right]&= \bar {\eta }\,\mathbb{E}\left [\int _0^T \left(v-S(H^z_t, v)\right) \lambda _t \mathrm{d} t \right ]\!. \end{align}

Proof.

Let

$z=(z_t)_{t\in [0,T]}$

be an arbitrary cybersecurity investment rate process. Applying the tower property of conditional expectation and making use of AssumptionsB and C, we can compute

$z=(z_t)_{t\in [0,T]}$

be an arbitrary cybersecurity investment rate process. Applying the tower property of conditional expectation and making use of AssumptionsB and C, we can compute

\begin{align*} \mathbb{E}\left[L^z_T\right] &= \mathbb{E}\left [\sum _{i=1}^{N_T} \eta _i B_i^{S(H^z_{\tau _i},v)}\right ] \\[4pt] &= \mathbb{E}\left [\sum _{i=1}^{N_T}\mathbb{E}\left [ \eta _i B_i^{S(H^z_{\tau _i},v)}\Big |\mathcal{F}_T\right ]\right ] \\[4pt] &= \bar {\eta }\,\mathbb{E}\left [\sum _{i=1}^{N_T}S(H^z_{\tau _i},v)\right ] \\[4pt] &= \bar {\eta }\,\mathbb{E}\left [\int _0^TS(H^z_t,v)\mathrm{d} N_t\right ] \\[4pt] &= \bar {\eta }\,\mathbb{E}\left [\int _0^TS(H^z_t,v)\lambda _t\mathrm{d} t\right ]\!, \end{align*}

\begin{align*} \mathbb{E}\left[L^z_T\right] &= \mathbb{E}\left [\sum _{i=1}^{N_T} \eta _i B_i^{S(H^z_{\tau _i},v)}\right ] \\[4pt] &= \mathbb{E}\left [\sum _{i=1}^{N_T}\mathbb{E}\left [ \eta _i B_i^{S(H^z_{\tau _i},v)}\Big |\mathcal{F}_T\right ]\right ] \\[4pt] &= \bar {\eta }\,\mathbb{E}\left [\sum _{i=1}^{N_T}S(H^z_{\tau _i},v)\right ] \\[4pt] &= \bar {\eta }\,\mathbb{E}\left [\int _0^TS(H^z_t,v)\mathrm{d} N_t\right ] \\[4pt] &= \bar {\eta }\,\mathbb{E}\left [\int _0^TS(H^z_t,v)\lambda _t\mathrm{d} t\right ]\!, \end{align*}

where the last step follows by definition of intensity (see, e.g., Brémaud, Reference Brémaud1981, Definition II.D7), together with the continuity of the process

$H^z$

, which implies that

$H^z$

, which implies that

$H^z_{\tau _i}$

coincides with the left-limit

$H^z_{\tau _i}$

coincides with the left-limit

$H^z_{\tau _i-}$

, for all

$H^z_{\tau _i-}$

, for all

$i\in \mathbb{N}^*$

. The first equation in the statement of the proposition follows as a special case by taking

$i\in \mathbb{N}^*$

. The first equation in the statement of the proposition follows as a special case by taking

$z\equiv 0$

.

$z\equiv 0$

.

3. Optimal cybersecurity investment

In this section, we determine the optimal cybersecurity investment policy in the model setup introduced in Section 2.2. In the spirit of the original Gordon–Loeb model, we aim at characterizing the investment rate process

$z^*=(z^*_t)_{t\in [0,T]}$

which maximizes the net trade-off between the benefits and the costs of cybersecurity over a planning horizon

$z^*=(z^*_t)_{t\in [0,T]}$

which maximizes the net trade-off between the benefits and the costs of cybersecurity over a planning horizon

$[0,T]$

.

$[0,T]$

.

To ensure the well-posedness of the optimization problem, we constrain the admissible investment policies to a suitably defined admissible set

$\mathcal{Z}$

.Footnote 5 In line with RemarkReference Balzano and Marzi3, in the following definition we restrict our attention to processes that are predictable with respect to the filtration generated by

$\mathcal{Z}$

.Footnote 5 In line with RemarkReference Balzano and Marzi3, in the following definition we restrict our attention to processes that are predictable with respect to the filtration generated by

$N$

.

$N$

.

Definition 1.

The admissible set

$\mathcal{Z}$

is defined as the set of all non-negative predictable processes

$\mathcal{Z}$

is defined as the set of all non-negative predictable processes

$(z_t)_{t\in [0,T]}$

such that

$(z_t)_{t\in [0,T]}$

such that

$\mathbb{E}[\int _0^T z_t^2 \mathrm{d} t]\lt \infty$

.

$\mathbb{E}[\int _0^T z_t^2 \mathrm{d} t]\lt \infty$

.

We now formulate the central optimization problem, which generalizes the benefit-cost trade-off function in (3) to a dynamic stochastic setting. The objective is to maximize the expected net benefit of cybersecurity investments:

\begin{equation} \sup _{z \in \mathcal{Z}} \mathbb{E}\left [ L_T^0-L_T^z- \int _0^T \left (\delta z_t+\frac {\gamma }{2}z_t^2\right ) \mathrm{d} t + U (H^z_T )\right ], \end{equation}

\begin{equation} \sup _{z \in \mathcal{Z}} \mathbb{E}\left [ L_T^0-L_T^z- \int _0^T \left (\delta z_t+\frac {\gamma }{2}z_t^2\right ) \mathrm{d} t + U (H^z_T )\right ], \end{equation}

where

$L^0_T$

and

$L^0_T$

and

$L^z_T$

are defined in (5) and (8), respectively, and the state variables

$L^z_T$

are defined in (5) and (8), respectively, and the state variables

$\lambda$

and

$\lambda$

and

$H^z$

satisfy the dynamics

$H^z$

satisfy the dynamics

\begin{align} \mathrm{d} \lambda _t &= \xi (\alpha -\lambda _t)\mathrm{d} t + \beta \mathrm{d} {N}_t, \end{align}

\begin{align} \mathrm{d} \lambda _t &= \xi (\alpha -\lambda _t)\mathrm{d} t + \beta \mathrm{d} {N}_t, \end{align}

\begin{align} \mathrm{d} H^z_t &= \left(z_t-\rho H^z_t \right)\mathrm{d} t. \end{align}

\begin{align} \mathrm{d} H^z_t &= \left(z_t-\rho H^z_t \right)\mathrm{d} t. \end{align}

In the objective functional (10), the term

$\mathbb{E}[L_T^0-L_T^z]$

represents the reduction in the expected losses due to the investment in cybersecurity. Differently from (3), we consider in (10) a non-linear cost function

$\mathbb{E}[L_T^0-L_T^z]$

represents the reduction in the expected losses due to the investment in cybersecurity. Differently from (3), we consider in (10) a non-linear cost function

$z\mapsto \delta z+\gamma z^2/2$

, for

$z\mapsto \delta z+\gamma z^2/2$

, for

$\delta ,\gamma \gt 0$

. The non-linearity penalizes irregular or highly concentrated investment strategies, reflecting real-world constraints and incentivizing smoother, more sustained cybersecurity efforts (e.g., continuous IT updates versus abrupt large-scale interventions). The term

$\delta ,\gamma \gt 0$

. The non-linearity penalizes irregular or highly concentrated investment strategies, reflecting real-world constraints and incentivizing smoother, more sustained cybersecurity efforts (e.g., continuous IT updates versus abrupt large-scale interventions). The term

$U(H^z_T)$

accounts for the residual utility of the cybersecurity level reached at the end of the planning horizon. This accounts for the fact that cybersecurity investment carries a long-term benefit, since the entity does not cease to exist after the planning horizon. As usual, the function

$U(H^z_T)$

accounts for the residual utility of the cybersecurity level reached at the end of the planning horizon. This accounts for the fact that cybersecurity investment carries a long-term benefit, since the entity does not cease to exist after the planning horizon. As usual, the function

$U \, : \, \mathbb{R}_+\to \mathbb{R}$

is assumed to be an increasing and concave utility function.

$U \, : \, \mathbb{R}_+\to \mathbb{R}$

is assumed to be an increasing and concave utility function.

Up to a rescaling of the model parameters, there is no loss of generality in taking

$\delta =1$

. Hence, making use of Proposition2, we can equivalently rewrite problem (10) as follows:

$\delta =1$

. Hence, making use of Proposition2, we can equivalently rewrite problem (10) as follows:

\begin{equation} \sup _{z \in \mathcal{Z}} \mathbb{E}\left [\int _0^T \left ( \bar {\eta }\bigl (v-S (H^z_t,v )\bigr )\lambda _t-z_t-\frac { \gamma }{2}z_t^2 \right ) \mathrm{d} t + U (H^z_T )\right ]\!. \end{equation}

\begin{equation} \sup _{z \in \mathcal{Z}} \mathbb{E}\left [\int _0^T \left ( \bar {\eta }\bigl (v-S (H^z_t,v )\bigr )\lambda _t-z_t-\frac { \gamma }{2}z_t^2 \right ) \mathrm{d} t + U (H^z_T )\right ]\!. \end{equation}

Remark 6. The objective functional (10) is linear in the losses

$(\eta _i)_{i\in \mathbb{N}^*}$

. More specifically, formula (13) shows that the loss distribution enters into the optimization problem only through its first moment. In turn, this implies that the optimal policy derived in Theorem 1 below depends only on

$(\eta _i)_{i\in \mathbb{N}^*}$

. More specifically, formula (13) shows that the loss distribution enters into the optimization problem only through its first moment. In turn, this implies that the optimal policy derived in Theorem 1 below depends only on

$\bar {\eta }$

and not on higher-order moments of the loss distribution. Under non-linear objective functionals, higher moments and the tail behavior of the loss distribution would affect the optimal policy.

$\bar {\eta }$

and not on higher-order moments of the loss distribution. Under non-linear objective functionals, higher moments and the tail behavior of the loss distribution would affect the optimal policy.

Problem (13) is a bi-dimensional stochastic optimal control problem, where the stochastic intensity process

$(\lambda _t)_{t\in [0,T]}$

acts as an additional state variable beyond the controlled process

$(\lambda _t)_{t\in [0,T]}$

acts as an additional state variable beyond the controlled process

$(H^z_t)_{t\in [0,T]}$

. Due to the Markovian structure of the system, dynamic programming techniques can be applied for the solution of (13). To this end, we first introduce the following notation, for any

$(H^z_t)_{t\in [0,T]}$

. Due to the Markovian structure of the system, dynamic programming techniques can be applied for the solution of (13). To this end, we first introduce the following notation, for any

$(t,\lambda ,h)\in [0,T]\times (0,\infty )\times \mathbb{R}_+$

:

$(t,\lambda ,h)\in [0,T]\times (0,\infty )\times \mathbb{R}_+$

:

-

• for all

$s\in [t,T]$

,(14)represents the cybersecurity level reached at time

\begin{equation} H_s^{t,h; \, z} \,:\!=\, he^{-\rho (s-t)} + \int _t^s e^{-\rho (s-v)} z_v \mathrm{d} v \end{equation}

$s$

when starting from level

$H_t=h$

at time

$t$

and investing according to

$z\in \mathcal{Z}$

;

-

• for all

$s\in [t,T]$

,represents the stochastic intensity at time

\begin{equation*} \lambda _s^{t, \lambda } \,:\!=\, \alpha +(\lambda -\alpha )e^{-\xi (s-t)} + \beta \sum _{i=N_t+1}^{ N_s} e^{-\xi (s-\tau _i)} \end{equation*}

$s$

when starting from value

$\lambda _t=\lambda$

at time

$t$

.

For any stopping time

$\tau$

taking values in

$\tau$

taking values in

$[0,T]$

, we denote by

$[0,T]$

, we denote by

$\mathcal{Z}_{\tau }$

the admissible set

$\mathcal{Z}_{\tau }$

the admissible set

$\mathcal{Z}$

restricted to the stochastic time interval

$\mathcal{Z}$

restricted to the stochastic time interval

$[\tau ,T]$

.

$[\tau ,T]$

.

We define as follows the benefit-cost trade-off functional

$J$

associated with a given investment rate process

$J$

associated with a given investment rate process

$z$

:

$z$

:

\begin{align*} J(t,\lambda , h; \, z) \,:\!=\, \mathbb{E}\left [\int _t^T \bar {\eta }\bigl (v-S \big(H_s^{t,h; \, z},v \big)\bigr )\lambda _s^{t,\lambda }\mathrm{d} s - \int _t^T\left (z_s+\frac { \gamma }{2}z_s^2\right ) \mathrm{d} s+ U \big(H_T^{t,h; \, z} \big)\right ]\!. \end{align*}

\begin{align*} J(t,\lambda , h; \, z) \,:\!=\, \mathbb{E}\left [\int _t^T \bar {\eta }\bigl (v-S \big(H_s^{t,h; \, z},v \big)\bigr )\lambda _s^{t,\lambda }\mathrm{d} s - \int _t^T\left (z_s+\frac { \gamma }{2}z_s^2\right ) \mathrm{d} s+ U \big(H_T^{t,h; \, z} \big)\right ]\!. \end{align*}

As a consequence of Definition1 together with the concavity of the function

$U$

, the functional

$U$

, the functional

$J$

is always well-defined and finite. Consequently, the value function associated with the stochastic optimal control problem (13) is given by

$J$

is always well-defined and finite. Consequently, the value function associated with the stochastic optimal control problem (13) is given by

\begin{equation} V(t,\lambda , h) \,:\!=\, \sup _{z\in \mathcal{Z}_t} J(t,\lambda , h; \, z). \end{equation}

\begin{equation} V(t,\lambda , h) \,:\!=\, \sup _{z\in \mathcal{Z}_t} J(t,\lambda , h; \, z). \end{equation}

In our dynamic model, the value function

$V(t,\lambda ,h)$

encodes the benefit-cost trade-off of cybersecurity investment over the residual planning horizon

$V(t,\lambda ,h)$

encodes the benefit-cost trade-off of cybersecurity investment over the residual planning horizon

$[t,T]$

, when considered at time

$[t,T]$

, when considered at time

$t$

with current cybersecurity level

$t$

with current cybersecurity level

$h$

and intensity

$h$

and intensity

$\lambda$

.

$\lambda$

.

Remark 7. Standard arguments allow proving that the function

$V$

has the following behavior with respect to

$V$

has the following behavior with respect to

$\lambda$

and

$\lambda$

and

$h$

:

$h$

:

-

• for every

$(t,h)\in [0,T)\times \mathbb{R}_+$

, the map

$\lambda \mapsto V(t,\lambda ,h)$

is strictly increasing: the benefit of cybersecurity investment is greater in the presence of a greater risk of cyberattacks; -

• for every

$(t,\lambda )\in [0,T]\times (0,\infty )$

, the map

$h\mapsto V(t,\lambda ,h)$

is strictly increasing and concave: increasing the current cybersecurity level

$h$

always improves the expected future benefit, but the marginal value of additional protection decreases as the cybersecurity level

$h$

grows.

The optimization problem formulated in (10) falls within the framework of the optimal control of a piecewise deterministic Markov process, in the sense of Davis (Reference Davis1984). Under the admissibility conditions imposed in Definition1, the performance functional

$J$

is well-posed for every control

$J$

is well-posed for every control

$z\in \mathcal{Z}_t$

. As a consequence, the same techniques used in the proof of Pham (Reference Pham2009, Theorem 3.3.1) yield that the value function satisfies the dynamic programming principle. More precisely, for all

$z\in \mathcal{Z}_t$

. As a consequence, the same techniques used in the proof of Pham (Reference Pham2009, Theorem 3.3.1) yield that the value function satisfies the dynamic programming principle. More precisely, for all

$(t,\lambda ,h)$

in

$(t,\lambda ,h)$

in

$[0,T) \times (0,\infty ) \times \mathbb{R}_+$

and for every stopping time

$[0,T) \times (0,\infty ) \times \mathbb{R}_+$

and for every stopping time

$\tau$

taking values in

$\tau$

taking values in

$[t,T]$

, it holds that

$[t,T]$

, it holds that

\begin{align*} V(t,\lambda , h) = \sup _{z\in \mathcal{Z}_t} \mathbb{E}\left [ \int _t^{\tau }\bar {\eta }\bigl (v-S \big(H_s^{t,h; \, z},v \big) \bigr )\lambda _{s}^{t,\lambda }\mathrm{d} s -\int _t^{\tau }\left (z_s+\frac { \gamma }{2} z_s^2 \right ) \mathrm{d} s + V \big(\tau , \lambda _{\tau }^{t,\lambda }, H_{\tau }^{t,h; \, z} \big)\right ]. \end{align*}

\begin{align*} V(t,\lambda , h) = \sup _{z\in \mathcal{Z}_t} \mathbb{E}\left [ \int _t^{\tau }\bar {\eta }\bigl (v-S \big(H_s^{t,h; \, z},v \big) \bigr )\lambda _{s}^{t,\lambda }\mathrm{d} s -\int _t^{\tau }\left (z_s+\frac { \gamma }{2} z_s^2 \right ) \mathrm{d} s + V \big(\tau , \lambda _{\tau }^{t,\lambda }, H_{\tau }^{t,h; \, z} \big)\right ]. \end{align*}

We now proceed to characterize the value function

$V$

as the solution to a Hamilton-Jacobi-Bellman (HJB) partial integro-differential equation (PIDE). Further theoretical results on the value function, together with a verification theorem under suitable regularity assumptions, are proved in Ongarato (Reference Ongarato2026, Section 2.3).

$V$

as the solution to a Hamilton-Jacobi-Bellman (HJB) partial integro-differential equation (PIDE). Further theoretical results on the value function, together with a verification theorem under suitable regularity assumptions, are proved in Ongarato (Reference Ongarato2026, Section 2.3).

Theorem 1.

Suppose that the value function

$V$

defined in (15) is of class

$V$

defined in (15) is of class

$\mathcal{C}^{1,1,1}$

(i.e., continuously differentiable in all its arguments). Then, the function

$\mathcal{C}^{1,1,1}$

(i.e., continuously differentiable in all its arguments). Then, the function

$V$

solves the following HJB-PIDE:

Footnote

6

$V$

solves the following HJB-PIDE:

Footnote

6

\begin{equation} \begin{aligned} & \frac {\partial V}{\partial t} +\xi (\alpha -\lambda )\frac {\partial V}{\partial \lambda }-\rho h \frac {\partial V}{\partial h} \\ &\; + \lambda (V(t,\lambda +\beta ,h)-V(t,\lambda ,h)) + \bar {\eta }(v-S(h,v))\lambda \\ &\; + \frac {\bigl (\left (\frac {\partial V}{\partial h}-1\right )^+\bigr )^2}{2\gamma } =0,\\ & V(T,\lambda , h)= U(h). \end{aligned} \end{equation}

\begin{equation} \begin{aligned} & \frac {\partial V}{\partial t} +\xi (\alpha -\lambda )\frac {\partial V}{\partial \lambda }-\rho h \frac {\partial V}{\partial h} \\ &\; + \lambda (V(t,\lambda +\beta ,h)-V(t,\lambda ,h)) + \bar {\eta }(v-S(h,v))\lambda \\ &\; + \frac {\bigl (\left (\frac {\partial V}{\partial h}-1\right )^+\bigr )^2}{2\gamma } =0,\\ & V(T,\lambda , h)= U(h). \end{aligned} \end{equation}

In addition, the optimal investment rate process

$z^*$

is given by

$z^*$

is given by

\begin{equation} z^*=\frac {\left (\frac {\partial V}{\partial h}-1\right )^+}{\gamma }. \end{equation}

\begin{equation} z^*=\frac {\left (\frac {\partial V}{\partial h}-1\right )^+}{\gamma }. \end{equation}

Proof.

In view of the assumption that

$V$

is of class

$V$

is of class

$\mathcal{C}^{1,1,1}$

, standard arguments based on Itô’s formula together with (11) and (12) imply that

$\mathcal{C}^{1,1,1}$

, standard arguments based on Itô’s formula together with (11) and (12) imply that

$V$

satisfies the following HJB equation (see, e.g., Bensoussan & Chevalier-Roignant, Reference Bensoussan and Chevalier-Roignant2024, Section 5.2):

$V$

satisfies the following HJB equation (see, e.g., Bensoussan & Chevalier-Roignant, Reference Bensoussan and Chevalier-Roignant2024, Section 5.2):

\begin{align*} 0 &= \sup _{z\geq 0} \left (\frac {\partial V}{\partial t} +\xi (\alpha -\lambda )\frac {\partial V}{\partial \lambda } -\rho h \frac {\partial V}{\partial h} + z \frac {\partial V}{\partial h}\right .\\ &\qquad \qquad \left . +\lambda \bigl (V(t,\lambda +\beta ,h)-V(t,\lambda ,h)\bigr ) \right .\\ &\qquad \qquad \left . + \bar {\eta }(v-S(h,v))\lambda - z- \frac {\gamma }{2}z^2 \right ) \\ &= \frac {\partial V}{\partial t} +\xi (\alpha -\lambda )\frac {\partial V}{\partial \lambda } -\rho h \frac {\partial V}{\partial h}\\ &\quad + \lambda (V(t,\lambda +\beta ,h)-V(t,\lambda ,h) ) + \bar {\eta }(v-S(h,v))\lambda \\ &\quad + \sup _{z\geq 0} \left (z \frac {\partial V}{\partial h}- z- \frac {\gamma }{2}z^2\right )\!. \end{align*}

\begin{align*} 0 &= \sup _{z\geq 0} \left (\frac {\partial V}{\partial t} +\xi (\alpha -\lambda )\frac {\partial V}{\partial \lambda } -\rho h \frac {\partial V}{\partial h} + z \frac {\partial V}{\partial h}\right .\\ &\qquad \qquad \left . +\lambda \bigl (V(t,\lambda +\beta ,h)-V(t,\lambda ,h)\bigr ) \right .\\ &\qquad \qquad \left . + \bar {\eta }(v-S(h,v))\lambda - z- \frac {\gamma }{2}z^2 \right ) \\ &= \frac {\partial V}{\partial t} +\xi (\alpha -\lambda )\frac {\partial V}{\partial \lambda } -\rho h \frac {\partial V}{\partial h}\\ &\quad + \lambda (V(t,\lambda +\beta ,h)-V(t,\lambda ,h) ) + \bar {\eta }(v-S(h,v))\lambda \\ &\quad + \sup _{z\geq 0} \left (z \frac {\partial V}{\partial h}- z- \frac {\gamma }{2}z^2\right )\!. \end{align*}

The supremum in the last line is given by

\begin{equation*} \sup _{z\geq 0} \left (z \frac {\partial V}{\partial h}- z -\frac {\gamma }{2}z^2\right )= \begin{cases} 0, & \text{if }\frac {\partial V}{\partial h}\leq 1, \\ \frac {1}{2 \gamma }\left (\frac {\partial V}{\partial h}-1 \right )^2, & \text{otherwise,} \end{cases} \end{equation*}

\begin{equation*} \sup _{z\geq 0} \left (z \frac {\partial V}{\partial h}- z -\frac {\gamma }{2}z^2\right )= \begin{cases} 0, & \text{if }\frac {\partial V}{\partial h}\leq 1, \\ \frac {1}{2 \gamma }\left (\frac {\partial V}{\partial h}-1 \right )^2, & \text{otherwise,} \end{cases} \end{equation*}

and is reached by the optimal control given in equation (17).

A numerical method for the solution of the PIDE (16) will be presented in Section 4.2 and then applied in Section 5.

The optimal investment rate

$z^*_t$

in equation (17) depends on the current time

$z^*_t$

in equation (17) depends on the current time

$t$

, on the current level

$t$

, on the current level

$\lambda _t$

of the stochastic intensity, and on the current cybersecurity level

$\lambda _t$

of the stochastic intensity, and on the current cybersecurity level

$H_t$

. In particular, the dependence on

$H_t$

. In particular, the dependence on

$\lambda _t$

makes

$\lambda _t$

makes

$z^*_t$

adaptive, meaning that it reacts to the random arrival of cyberattacks. Since the arrival of an attack increases the likelihood of further attacks due to the self-exciting behavior of the Hawkes process, this enables the decision maker to strategically increase the cybersecurity investment in order to raise the cybersecurity level as a defense for the incoming attacks. This important feature will be numerically illustrated in Section 5.4.3.

$z^*_t$

adaptive, meaning that it reacts to the random arrival of cyberattacks. Since the arrival of an attack increases the likelihood of further attacks due to the self-exciting behavior of the Hawkes process, this enables the decision maker to strategically increase the cybersecurity investment in order to raise the cybersecurity level as a defense for the incoming attacks. This important feature will be numerically illustrated in Section 5.4.3.

Remark 8. The optimal policy described in equation (17) admits a clear economic interpretation: it is worth investing in cybersecurity whenever the marginal benefit of the investment is greater than its marginal cost. This insight aligns with the earlier results of Krutilla et al. (Reference Krutilla, Alexeev, Jardine and Good2021) in a dynamic but deterministic setup.

We close this section with the following result, which provides an explicit lower bound for the value function

$V$

.

$V$

.

Proposition 3.

For every

$(t,\lambda ,h)\in [0,T]\times (0,\infty )\times \mathbb{R}_+$

, it holds that

$(t,\lambda ,h)\in [0,T]\times (0,\infty )\times \mathbb{R}_+$

, it holds that

\begin{equation} V(t,\lambda ,h)\geq J(t, \lambda , h; \, \rho h), \end{equation}

\begin{equation} V(t,\lambda ,h)\geq J(t, \lambda , h; \, \rho h), \end{equation}

where

\begin{align*} J(t, \lambda , h; \, \rho h) &= U(h) - \rho h\left (1+\frac {\gamma }{2}\rho h\right )(T-t) \\ &\quad + \bar {\eta }(v-S(h,v) ) \left (\frac {\alpha \xi }{\xi -\beta } (T-t) - \frac {1}{\xi -\beta } \Big (\lambda -\frac {\alpha \xi }{\xi -\beta }\Big ) \left (e^{-(\xi -\beta )(T-t)}-1 \right )\right ). \end{align*}

\begin{align*} J(t, \lambda , h; \, \rho h) &= U(h) - \rho h\left (1+\frac {\gamma }{2}\rho h\right )(T-t) \\ &\quad + \bar {\eta }(v-S(h,v) ) \left (\frac {\alpha \xi }{\xi -\beta } (T-t) - \frac {1}{\xi -\beta } \Big (\lambda -\frac {\alpha \xi }{\xi -\beta }\Big ) \left (e^{-(\xi -\beta )(T-t)}-1 \right )\right ). \end{align*}

Proof.

By definition of the value function (15), it holds that

$V(t,\lambda ,h)\geq J(t,\lambda ,h,z)$

, for any given

$V(t,\lambda ,h)\geq J(t,\lambda ,h,z)$

, for any given

$z\in \mathcal{Z}_t$

. In particular, the constant process

$z\in \mathcal{Z}_t$

. In particular, the constant process

$\bar {z}\equiv \rho h$

belongs to

$\bar {z}\equiv \rho h$

belongs to

$\mathcal{Z}_t$

, and, therefore, inequality (18) holds. In view of equation (14), we have that

$\mathcal{Z}_t$

, and, therefore, inequality (18) holds. In view of equation (14), we have that

\begin{equation*} H_s^{t,h;\rho h} = he^{-\rho (s-t)} + \int _t^s e^{-\rho (s-v)} \rho h \mathrm{d} v = h, \end{equation*}

\begin{equation*} H_s^{t,h;\rho h} = he^{-\rho (s-t)} + \int _t^s e^{-\rho (s-v)} \rho h \mathrm{d} v = h, \end{equation*}

for all

$s\in [t,T]$

. Therefore, we obtain that

$s\in [t,T]$

. Therefore, we obtain that

\begin{align*} J(t, \lambda , h; \, \rho h) &= \bar {\eta }\bigl (v-S(h,v)\bigr )\mathbb{E}\left [\int _t^T\lambda _s^{t,\lambda }\mathrm{d} s\right ] - \rho h\left (1+\frac {\gamma }{2}\rho h\right )(T-t) + U(h). \end{align*}

\begin{align*} J(t, \lambda , h; \, \rho h) &= \bar {\eta }\bigl (v-S(h,v)\bigr )\mathbb{E}\left [\int _t^T\lambda _s^{t,\lambda }\mathrm{d} s\right ] - \rho h\left (1+\frac {\gamma }{2}\rho h\right )(T-t) + U(h). \end{align*}

The expectation

$\mathbb{E}[\! \int _t^T\lambda _s^{t,\lambda }\mathrm{d} s]$

can be computed by a straightforward adaptation of Proposition1 (compare also with Dassios & Zhao, Reference Dassios and Zhao2011, Theorem 3.6), thus completing the proof.

$\mathbb{E}[\! \int _t^T\lambda _s^{t,\lambda }\mathrm{d} s]$

can be computed by a straightforward adaptation of Proposition1 (compare also with Dassios & Zhao, Reference Dassios and Zhao2011, Theorem 3.6), thus completing the proof.

Remark 9. The lower bound obtained in Proposition 3 is associated with a fixed investment rate that offsets technological obsolescence by maintaining the cybersecurity level constant over time (this follows directly from equation (12)). In Section 5.3, we numerically show that the optimal dynamic investment policy characterized in Theorem 1 consistently outperforms any constant investment strategy, highlighting the value of real-time adaptability in cybersecurity investment.

4. Numerical methods

In this section, we describe the parameters’ choice and the numerical methods adopted for the solution of the optimization problem introduced in Section 3.

4.1 Specification of the model parameters

We report in Tables 1–3 the standard set of the model parameters. Unless mentioned otherwise, the numerical analysis will be performed using the standard set of parameters.

Specification of the security breach function

Parameters of the stochastic intensity

Parameters of the optimization problem

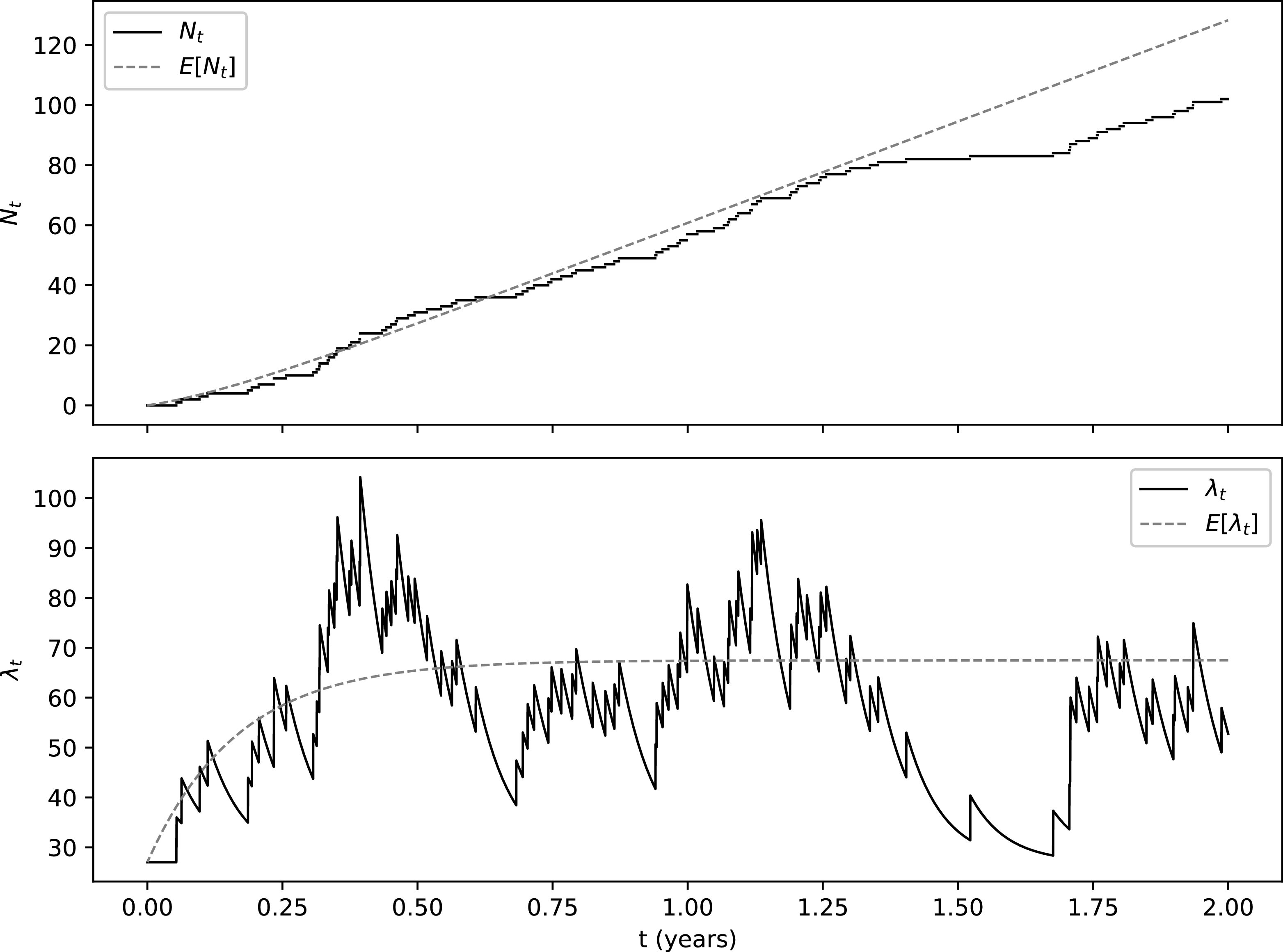

We employ a security breach probability function

$S$

of class I, as defined in (2). The parameters’ values in Table 1 are consistent with those determined in Naldi and Flamini (Reference Naldi and Flamini2017) through a calibration based on synthetic data and also used as benchmark inputs in subsequent works (see, e.g., Skeoch, Reference Skeoch2022; Mazzoccoli & Naldi, Reference Mazzoccoli and Naldi2020). Taking

$S$

of class I, as defined in (2). The parameters’ values in Table 1 are consistent with those determined in Naldi and Flamini (Reference Naldi and Flamini2017) through a calibration based on synthetic data and also used as benchmark inputs in subsequent works (see, e.g., Skeoch, Reference Skeoch2022; Mazzoccoli & Naldi, Reference Mazzoccoli and Naldi2020). Taking

$v,a,b$

as in Table 1, the function

$v,a,b$

as in Table 1, the function

$h\mapsto S_I(h,v)$

is plotted in Figure 2.

$h\mapsto S_I(h,v)$

is plotted in Figure 2.

Security breach function (parameters as in Table 1).

The parameters of the stochastic intensity of the Hawkes process (see Table 2) are chosen to generate on average approximately 60 cyberattacks per year. We believe that this is a reasonable figure, in the absence of reliable estimates of the number of cyberattacks targeting a single entity.Footnote 7

Remark 10. For the standard set of parameters, we have

$\lambda _0=\alpha$

, and so the stochastic intensity

$\lambda _0=\alpha$

, and so the stochastic intensity

$\lambda _t$

can be expressed as follows:

$\lambda _t$

can be expressed as follows:

\begin{equation} \lambda _t = \lambda _0+ \beta \sum _{i=1}^{N_t} e^{-\xi (t-\tau _i)}. \end{equation}

\begin{equation} \lambda _t = \lambda _0+ \beta \sum _{i=1}^{N_t} e^{-\xi (t-\tau _i)}. \end{equation}

We consider a one-year planning horizon (

$T=1$

) and set an average loss of

$T=1$

) and set an average loss of

$10\text{k}\ $

for each successful breach, resulting in a total expected annual loss of approximately

$10\text{k}\ $

for each successful breach, resulting in a total expected annual loss of approximately

$390 \text{k}\ $

without cybersecurity investments, which is in the same order of magnitude of Skeoch (Reference Skeoch2022). The depreciation rate is set at

$390 \text{k}\ $

without cybersecurity investments, which is in the same order of magnitude of Skeoch (Reference Skeoch2022). The depreciation rate is set at

$\rho =0.2$

, consistently with the technological depreciation rates considered in Krutilla et al. (Reference Krutilla, Alexeev, Jardine and Good2021). The parameter

$\rho =0.2$

, consistently with the technological depreciation rates considered in Krutilla et al. (Reference Krutilla, Alexeev, Jardine and Good2021). The parameter

$\gamma$

is set at a rather low value in order to avoid an excessive penalization of large investment rates. Finally, we choose

$\gamma$

is set at a rather low value in order to avoid an excessive penalization of large investment rates. Finally, we choose

$U(h)=\sqrt {h}$

, representing a strictly increasing and concave CRRA utility function.

$U(h)=\sqrt {h}$

, representing a strictly increasing and concave CRRA utility function.

4.2 Numerical solution of the HJB-PIDE

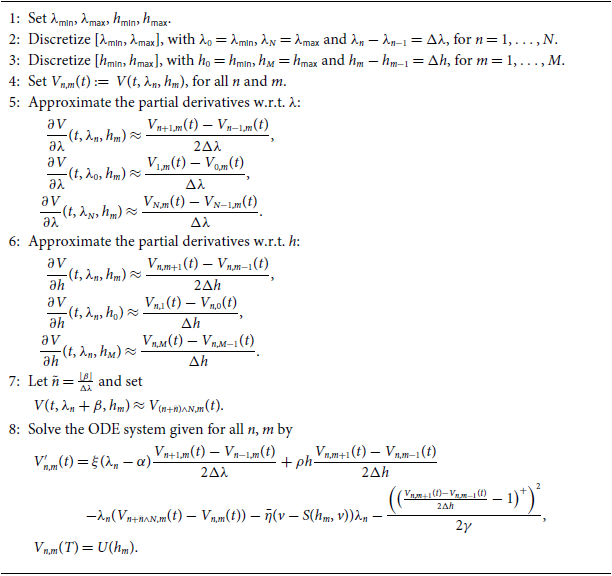

As shown in Section 3, determining the optimal cybersecurity investment requires the solution of the non-linear PIDE (16). Due to the complexity of the problem, one cannot expect to find explicitly an analytical solution, and, hence, numerical methods are required. We opt for the method of lines, as described in Yuan (Reference Yuan1999). This technique consists of discretizing the PIDE in the spatial domain

$(\lambda ,h)\in (0,\infty )\times \mathbb{R}_+$

but not in time and then in integrating the semi-discrete problem as a system of ODEs. In our setting, we discretize the

$(\lambda ,h)\in (0,\infty )\times \mathbb{R}_+$

but not in time and then in integrating the semi-discrete problem as a system of ODEs. In our setting, we discretize the

$(\lambda ,h)$

dimensions with a central difference and then numerically solve the resulting ODE system. Similarly to the case of PIDEs arising in Lévy models (see, e.g., Cont & Voltchkova, Reference Cont and Voltchkova2005), the unbounded space domain

$(\lambda ,h)$

dimensions with a central difference and then numerically solve the resulting ODE system. Similarly to the case of PIDEs arising in Lévy models (see, e.g., Cont & Voltchkova, Reference Cont and Voltchkova2005), the unbounded space domain

$(0,\infty )\times \mathbb{R}_+$

is localized into a bounded domain

$(0,\infty )\times \mathbb{R}_+$

is localized into a bounded domain

$[\lambda _{\text{min}},\lambda _{\text{max}}]\times [h_{\text{min}},h_{\text{max}}]$

. We refer to Algorithm1 for a precise description of the implementation of this method.

$[\lambda _{\text{min}},\lambda _{\text{max}}]\times [h_{\text{min}},h_{\text{max}}]$

. We refer to Algorithm1 for a precise description of the implementation of this method.

In our implementation, the algorithm’s meta-parameters are specified as in Table 4.

Meta-parameters for Algorithm1

The value

$h_{\text{min}} = 0$

corresponds to the absence of cybersecurity investment, while

$h_{\text{min}} = 0$

corresponds to the absence of cybersecurity investment, while

$h_{\text{max}} = 50$

represents an upper bound that is rarely achieved in our setup under the standard parameter set. We choose

$h_{\text{max}} = 50$

represents an upper bound that is rarely achieved in our setup under the standard parameter set. We choose

$\lambda _{\text{min}}=\lambda _0$

, which coincides with the lower bound of the stochastic intensity

$\lambda _{\text{min}}=\lambda _0$

, which coincides with the lower bound of the stochastic intensity

$\lambda _t$

; see equation (19). We set

$\lambda _t$

; see equation (19). We set

$\lambda _{\text{max}}=\mathbb{E}[\lambda _T] + 7 \sqrt {\text{Var}(\lambda _T)} \approx 216$

in order to ensure that the truncation of the intensity domain does not have any material impact on our numerical results. The value function

$\lambda _{\text{max}}=\mathbb{E}[\lambda _T] + 7 \sqrt {\text{Var}(\lambda _T)} \approx 216$

in order to ensure that the truncation of the intensity domain does not have any material impact on our numerical results. The value function

$V$

is extrapolated beyond

$V$

is extrapolated beyond

$[\lambda _{\text{min}}, \lambda _{\text{max}}]$

by setting

$[\lambda _{\text{min}}, \lambda _{\text{max}}]$

by setting

\begin{equation*} V(t,\lambda ,h) = V(t,\lambda _{\text{max}},h), \quad \text{for all } \lambda \gt \lambda _{\text{max}}, \end{equation*}

\begin{equation*} V(t,\lambda ,h) = V(t,\lambda _{\text{max}},h), \quad \text{for all } \lambda \gt \lambda _{\text{max}}, \end{equation*}

analogously to the scheme implemented in Ly Vath et al. (Reference Ly Vath, Scotti and Gaigi2025, Section 5.1). When plotting the function

$V$

in Section 5, we shall consider a subinterval of

$V$

in Section 5, we shall consider a subinterval of

$[\lambda _{\text{min}}, \lambda _{\text{max}}]$

: intensity values close to

$[\lambda _{\text{min}}, \lambda _{\text{max}}]$

: intensity values close to

$\lambda _{\text{max}}$

are rarely achieved and might lead to numerical instabilities.

$\lambda _{\text{max}}$

are rarely achieved and might lead to numerical instabilities.

We have implemented Algorithm1 in Python, using the built-in ODE solver scipy.integrate.solve_ivp. We make use of an implicit Runge–Kutta method of the Radau IIA family of order 5 (see Hairer et al., Reference Hairer, Nørsett and Wanner1993 for further details). The computations were performed on an Intel Xeon E5520 CPU equipped with 32 GB of RAM, requiring approximately 23 hours to compute the value function and the corresponding optimal control. To empirically assess the convergence of Algorithm1, we verified that standard discretization error metrics decrease consistently as the spatial grid in

$(\lambda , h)$

is refined.

$(\lambda , h)$

is refined.

Numerical solution of the PIDE (16)

Algorithm 1 Long description

An equation describing the numerical solution of a partial integro-differential equation for optimal cybersecurity investment. The equation involves discretizing the spatial domain and solving the resulting system of ordinary differential equations. The spatial domain is bounded by lambda min, lambda max, h min, and h max. The equation includes partial derivatives with respect to lambda and h, and it involves the function V of t, lambda, and h. The solution process involves approximating these partial derivatives and solving the resulting system of ordinary differential equations.

4.3 Optimal cybersecurity investment rate

Besides determining the optimal net benefit of cybersecurity investments, we aim at computing the real-time adaptive strategy that best responds to the arrival of cyberattacks. To this end, after solving the PIDE (16) via Algorithm1, we compute numerically the optimal investment rate given in equation (17) along a simulated sequence of cyberattacks. This entails simulating a trajectory of the stochastic intensity

$(\lambda _t(\omega ))_{t\in [t_{\text{init}},T]}$

, starting from an initial cybersecurity level

$(\lambda _t(\omega ))_{t\in [t_{\text{init}},T]}$

, starting from an initial cybersecurity level

$H_{\text{init}}$

at time

$H_{\text{init}}$

at time

$t_{\text{init}}$

. Our numerical method for the computation of the optimal investment rate is described in Algorithm2 and will be numerically implemented in Sections 5.4.2 and 5.4.3.

$t_{\text{init}}$

. Our numerical method for the computation of the optimal investment rate is described in Algorithm2 and will be numerically implemented in Sections 5.4.2 and 5.4.3.

Numerical computation of the optimal control

Algorithm 2 Long description

The image displays a list of steps for numerical computation of optimal control. Each step is numbered and described in detail. The steps involve setting initial parameters, discretizing intervals, computing values, simulating trajectories, and iterating through states to determine optimal investment rates.

5. Results and discussion

In this section, we report some numerical results that illustrate the key properties and implications of the model. In particular, we are interested in assessing the benefit of adopting the optimal dynamic cybersecurity investment policy.

Value function and optimal investment rate computed under the standard parameters set.

5.1 Value function and optimal cybersecurity policy

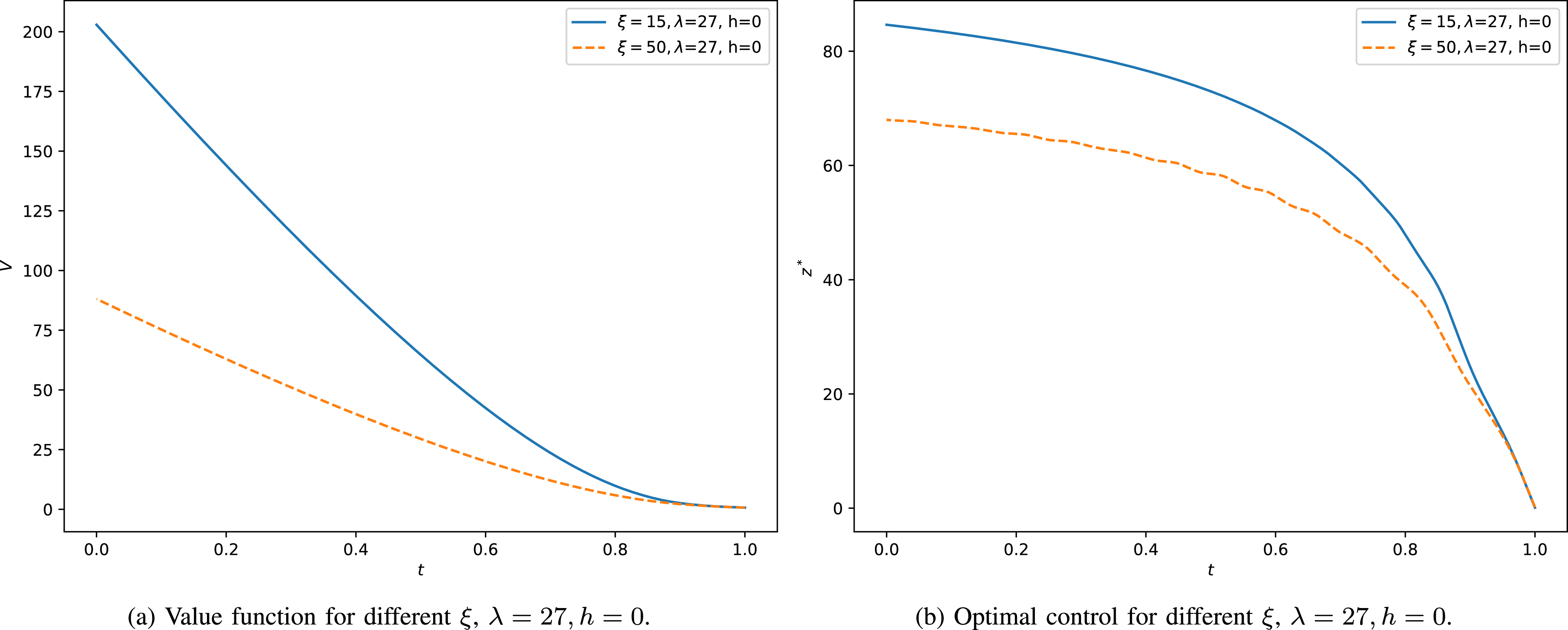

Figure 3 displays the value function

$V$

and the optimal cybersecurity investment rate

$V$

and the optimal cybersecurity investment rate

$z^*$

. In panels Figure 3(a) and (d), we plot, respectively,

$z^*$

. In panels Figure 3(a) and (d), we plot, respectively,

$V$

and

$V$

and

$z^*$

for fixed intensity

$z^*$

for fixed intensity

$\lambda =27$

, varying

$\lambda =27$

, varying

$t$

and

$t$

and

$h$

. Coherently with RemarkReference Bielecki and Jakubowski7, we observe that the value function is increasing in

$h$

. Coherently with RemarkReference Bielecki and Jakubowski7, we observe that the value function is increasing in

$h$

, while the optimal investment rate is decreasing. This behavior reflects the fact that higher cybersecurity levels yield greater benefits and reduce the need for further cybersecurity investments. In panels Figure 3(b) and (e) we plot, respectively,

$h$

, while the optimal investment rate is decreasing. This behavior reflects the fact that higher cybersecurity levels yield greater benefits and reduce the need for further cybersecurity investments. In panels Figure 3(b) and (e) we plot, respectively,

$V$

and

$V$

and

$z^*$

for fixed

$z^*$

for fixed

$h=0$

, varying

$h=0$

, varying

$t$

and

$t$

and