Introduction

Since the onset of the Covid-19 pandemic, early retirement rates, i.e. retiral before State Pension Age (SPA), in the United Kingdom have reversed their historic downward trajectory. The year 2021 witnessed a significant rise in self-reported retirement and, by mid-2022, the economic inactivity rates of those aged fifty to sixty-four (henceforth mid-later life workers, MLLW) had reached 28 per cent – a figure not seen since 2015 (ONS, n.d.). The rise in inactivity was primarily driven by people in their late fifties and early sixties; however, the explanation for the increase has remained elusive. Poor health and caring responsibilities explain barely half of the upturn, and a substantial cohort of healthy MLLW appears to have voluntarily exited the labour market (Cribb & Emmerson, Reference Cribb and Emmerson2022). The vulnerability to Covid-19, whether physical or psychological, may have prompted early retirement, as might have a revaluation of MLLW priorities in the pandemic’s wake (Bell, Reference Bell2024). Another possible driver was rising asset values; ‘Pension freedoms’ mean most UK workers can access some pension savings at age fifty-five, and two-thirds of fifty- to sixty-four-year-olds are homeowners (Centre for Ageing Better, 2025). A comfortable early retirement is predominantly enjoyed by the top 20 per cent of the wealth spectrum. Nevertheless, a significant proportion of less well-provisioned MLLW also took early retirement following the pandemic (Cribb, Reference Cribb2023).

This early retirement shift runs contrary to the UK Government’s policy orientation of extending working lives (EWL), aimed at encouraging MLLW to remain in the workforce longer (Vickerstaff & Loretto, Reference Vickerstaff, Loretto and Ní Léime2017). EWL responds to rising life expectancy, shifting old-age dependency ratios, and the increasing costs of state pension expenditure (Foster, Reference Foster2023; Lain, Reference Lain2016). A notable feature has been the graduated increase in, and phased gender equalisation of, the SPA, which is set to reach sixty-seven by 2028. While this increase in the SPA has raised the de facto retirement age, it has also negatively impacted the financial wellbeing of many individuals in their sixties, particularly women who previously could have received their state pension at age sixty (Della Giusta & Longhi, Reference Della Giusta and Longhi2021). The UK employment market has not fully adapted to a larger older workforce. Ageism (Loretto & Vickerstaff, Reference Loretto and Vickerstaff2015) and lack of suitable job opportunities mean that older jobseekers experience longer periods of unemployment (Centre for Ageing Better, 2025). In the UK, most full-time workers leave the workforce before reaching SPA eligibility, but many lack sufficient savings or benefits provision to compensate for the loss of earned income. Working-age state benefits are predominantly means-tested, and households with savings over £16,000 are usually ineligible. Almost half of those who retired in 2020–2021 were living in relative poverty, and for most individuals, stopping work results in significantly lower income (Cribb, Reference Cribb2023). This raises the question of why, if given the choice, some MLLW would contemplate leaving the workplace before SPA and risk poorer financial outcomes.

Drawing on qualitative interviews conducted in 2021–2022 with fifty-four workers aged sixty and above, we investigate how MLLW interpret their future financial wellbeing needs and how this influences their retirement timing. In doing so, we develop an understanding of MLLW retirement preparation strategies within the context of the increasing SPA and the after-effects of the Covid-19 pandemic. Our paper begins with an explanation of the UK pensions landscape, followed by a discussion on financial wellbeing, highlighting the importance of subjective financial wellbeing. The methods section includes a broad explanation of participants’ employment background, salary levels, and pension arrangements. The analysis identifies debt reduction, particularly mortgage redemption, as important. Being mortgage-free, even at the risk of decreased or underfunded pensions, increases individuals’ sense of control over potential pre-retirement income shocks. Secondly, we highlight the importance of social influences. Cultural perceptions of the ‘ideal’ retirement age influence financial wellbeing retirement decisions, with many MLLW willing to trade a few years of lower income for earlier retirement. Thirdly, we provide evidence that accessing pension savings before retirement is viewed as a way of facilitating phased retirement. The final discussion section considers the implications of our findings for future research and policy.

Financial context: the pensions and savings landscape

To qualify for the UK State Pension, individuals need ten to thirty-five years of National Insurance (NI) contributions. Some individuals in receipt of state benefits have NI contributions credited by the state. Nevertheless, because thirty-five qualifying years is difficult to achieve without a minimum and regular earned income, individuals with broken work histories, primarily women, immigrants, and the self-employed, may receive proportionately less than a full pension. The current full State Pension is a flat-rate amount of £11,500 per annum, insufficient to maintain basic living standards (Centre for Ageing Better, 2025), and pensioners are expected to supplement their State Pension with other savings or additional pensions. Additional pension saving is not compulsory, but automatic enrolment (AE), introduced in 2012, has nudged increasing numbers into saving for retirement. However, many MLLW started saving too little too late. The self-employed are excluded from AE, and the lower earnings threshold for AE (currently £10,000 pa) eliminates many, primarily female and part-time and lower-income workers, exacerbating inequalities in retirement savings.

The ability to generate retirement income before SPA largely depends on the generosity and adherence to pension schemes throughout the working life. Around 18 million working-age individuals have accumulated earnings-based defined benefit (DB) occupational pensions, which pay out a regular income at retirement: 8,056,000 people are active DB members, and 10,579,000 are deferred members (Pensions Regulator, 2024). Most of these DB schemes start paying at age sixty to sixty-five, consequently, some workers are able to afford to retire prior to SPA. For example, the average age of retirement for civil servants, who have DB pensions, is sixty-two, three years earlier than those in the private sector (Almeida, Reference Almeida2023).

While DB schemes persist in the public sectors, only 4 per cent of private sector DB schemes are still open to new entrants, and another 4 per cent permit accruals for existing members. Almost all AE pension schemes in the private sector are market-linked Defined Contribution (DC) schemes. In DB schemes the employer carries the risk of providing an earnings-related pension, whereas the risk is carried by the employee in DC funds because the fund’s size is determined by the contributions made and the investment performance of the individual account.

‘Pension freedoms’ introduced in 2015 enhanced flexibility: individuals can now access their DC pension fund as a lump sum at age fifty-five (rising to fifty-seven in April 2028). Paradoxically, these freedoms introduced a counter-current to efforts aimed at keeping MLLW in the workplace. Individuals have a preference to front-load access to pension funds – making higher withdrawals early on – so that they can retire early (Hagen et al., Reference Hagen, Hallberg and Sjögren Lindquist2022). Although pension assets constitute the largest source of MLLW net wealth, around 70 per cent of those aged sixty to sixty-four in the UK are homeowners, with two-thirds owning outright (Department for Work and Pensions, 2026). Around one-third of homeowners expect to downsize to provide money in retirement, this proportion being greater amongst those in higher value properties (Crawford, Reference Crawford2018). Being mortgage-free correlates with enhanced financial wellbeing (Hermann et al., Reference Hermann, Herbert and Molinsky2020) and earlier age at retirement (Cribb, Reference Cribb2023). In the UK, most MLLW with mortgages remain in the workforce. Pension flexibility coupled with increased wealth has led to the evolution of conventional retirement boundaries. The misalignment between the SPA and most workers’ private pensions access age, coupled with the removal of compulsory retirement ages in 2011, can result in individuals simultaneously being in work and in receipt of pensions. Cliff-edge retirements are becoming less common as MLLW ease gradually into economic inactivity. How individuals manage and cope with the transition is important because the route taken towards retirement may have significant implications for subsequent financial satisfaction and overall wellbeing (Palomäki, Reference Palomäki2019).

Financial wellbeing and retirement decisions

Considerable research attention has been directed to objective measures of MLLWs’ financial wellbeing, including income poverty (Centre for Ageing Better, 2025; Cribb, Reference Cribb2023) and gender-based disparities of pension savings (Foster, Reference Foster2023). Life-course research approaches provide valuable insights into why individuals’ experience of financial wellbeing varies across socio-economic groups and how it is shaped by key life transitions, such as career progression, and family responsibilities (Salignac et al., Reference Salignac, Hamilton, Noone, Marjolin and Muir2020). The cumulative impact of earlier life disadvantages has profound implications for retirement planning and financial wellbeing outcomes (Swain et al., Reference Swain, Carpentieri, Parsons and Goodman2020).

Researchers generally conceptualise financial wellbeing along two temporal dimensions: the current state and the longer-term financial outlook (Kempson et al., Reference Kempson, Finney and Poppe2017; Netemeyer et al., Reference Netemeyer, Warmath, Fernandes and Lynch2018). In the current state, having an adequate income is a crucial element of financial wellbeing, alongside holding savings to absorb financial shocks and related stressors. Longer-term financial wellbeing is positively associated with savings and pension security (Olivera & Ponomarenko, Reference Olivera and Ponomarenko2017) and achieving the financial goal of owning a mortgage-free property (Hermann et al., Reference Hermann, Herbert and Molinsky2020). The alignment between these elements varies across income groups (Kempson et al., Reference Kempson, Finney and Poppe2017), but as individuals age, the future-orientated aspect of accumulating adequate pension income becomes increasingly relevant. James (Reference James2021) provides an example of these temporal dimensions through the cultural embeddedness of retirement saving; the engagement of younger perfunctory savers is shaped by key life transitions, such as career progression, housing stability, and family responsibilities, towards prudent saving to ensure later-life security.

Accumulated pension wealth does not fully explain individuals’ perception of their financial wellbeing or their pre-retirement financial behaviour. Swain et al. (Reference Swain, Carpentieri, Parsons and Goodman2020) make the point that although there is a correlation between pension savings and the propensity to work in later life, the decision to retire is influenced by a complex interplay of financial and non-financial factors such as health, job satisfaction, and ageism.

The importance of subjective financial wellbeing

Brüggen et al. (Reference Brüggen, Hogreve, Holmlund, Kabadayi and Löfgren2017) expanded the conceptualisation of financial wellbeing by introducing the notion of financial freedom and placing greater emphasis on the subjective. Key components of subjective wellbeing include anxiety, perceptions of stress and financial security, and the control over one’s financial life. According to Vlaev and Elliott (Reference Vlaev and Elliott2014), the feeling of being in control of personal finances is the paramount predictor of financial wellbeing. However, despite the importance of emotions in financial decision-making, limited research has delved into how MLLW feel about their financial circumstances as they approach SPA.

Existing literature observes that older adults tend to report more financial satisfaction than do younger adults (Delaney et al., Reference Delaney, Maxwell and McCalman2006; Hira & Mugenda, Reference Hira and Mugenda1999). Hansen et al.’s (Reference Hansen, Slagsvold and Moum2008) view is that minimal debt and accumulated assets, which are more common in older than in younger workers, explain the differences in financial satisfaction. However, the phenomenon known as the ageing paradox, or satisfaction paradox, whereby subjective wellbeing is stable, or increases in mature adulthood, holds true even when individuals have limited income (Grable et al., Reference Grable, Cupples, Fernatt and Anderson2013). One possible explanation is that older people psychologically adapt to financial constraints (Francoeur, Reference Francoeur2002). An additional strand of research points to the relevance of cohort differences by suggesting that if older people see positive comparisons between present and past circumstances due to rising standards of living, this may lead them to feel more financially satisfied because financial wellbeing is mainly viewed in relativistic terms (Burholt & Windle, Reference Burholt and Windle2006). Dolan et al. (Reference Dolan, Peasgood and White2008) revealed that income relative to a reference group is more significant than absolute income – an effect that is more pronounced in wealthier countries (Corazzini et al., Reference Corazzini, Esposito and Majorano2012). In theoretical models, relativistic terms refer to points of comparison that individuals use to evaluate their own financial status and satisfaction, such as social and cultural markers including home ownership, age, and life stage.

The subjective financial wellbeing of those on the cusp of retirement is an area lacking in-depth research in the UK. To fill this knowledge gap, our study embarked on a nuanced exploration of how MLLW perceive their financial circumstances and the impact of these perceptions on retirement decision-making. We aimed to answer the question: How do MLLW feel about their financial wellbeing as they approach the end of their paid working lives? We shed light upon the determinants and future-oriented strategies that contribute to the overall subjective wellbeing within this demographic group. Our qualitative analysis builds on the conceptual distinction between objective financial wellbeing and subjective financial wellbeing.

Methodology

Research context and data collection

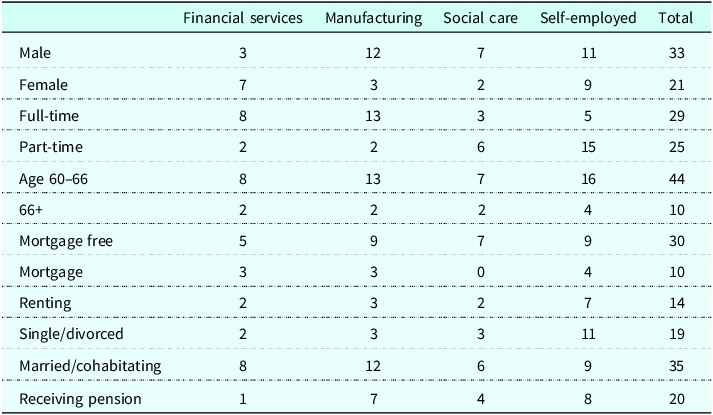

The research project interviewed 156 workers age fifty over about supporting healthy ageing at work. Interviews of all participants age sixty and over (n=54) formed the dataset for this examination of financial wellbeing approaching retirement, as initial coding of intentions revealed sixty was the age atwhich priority to retirement planning was marked. The study encompassed four distinct case study settings: a large manufacturing company, a financial services company, a social care provider, and self-employed individuals. The interview pool was purposively selected to ensure representation and diversity in terms of age, gender, and socio-economic backgrounds. Seven female and two male participants were over their SPA.

Data collection

Drawing on a life-course approach, the research team conducted in-depth semi-structured interviews designed to explore MLLW current and past experiences of work, health, and mental and financial wellbeing within the broader contexts of their family and socio-economic circumstances. Video and face-to-face interviews were conducted at multiple locations across Scotland and England. The researchers collected demographic information and details about housing tenure (Table 1). Data collection took place from late 2021 to early 2023. All interviews were audio-recorded, fully transcribed, and anonymised. Informed consent was obtained from all individual participants included in the study, which was approved by and conducted in accordance with the ethical standards of the University of Edinburgh Research Ethics Committee.

Participant summary

Managers and other discipline experts employed at the three case study organisations were interviewed to verify details of the respective pension schemes and arrangements.

Data analysis

The data were analysed using thematic analysis, focusing on financial wellbeing. Key themes were systematically identified and coded to uncover patterns within the data. The analysis gave emphasis to common experiences among MLLW across industries and case study settings. Coding followed an inductive approach (Braun & Clarke, Reference Braun and Clarke2006), allowing themes to be determined from participant narratives. Individual codes evolved through refinement, reflecting relationships between concepts and integrating broader categories into themes. To ensure the themes accurately represented participants’ experiences, a thematic overview was developed for each participant, facilitating cross-case comparisons and enabling a grounded, narrative-driven interpretation of the data.

Participant incomes ranged between £8,000 and £170,000 per annum. Twenty participants had individual income below £30,000. Lower earners were predominantly self-employed or working in social care.

Pension and salary arrangements

Manufacturing: The majority of participants in the manufacturing company were male, long-standing employees, several advancing from physically demanding occupations to office-based positions. The DB pension scheme was closed to new members but still accrued benefits, and an index-linked pension was paid at sixty or sixty-five, depending on recruitment date. As is typical with DB schemes, members received an additional tax-free lump sum on retirement. Newer employees were automatically enrolled in a less-generous DC scheme where the employer matched contributions up to 8 per cent. Salaries were well above the national average and, as DB pensions are calculated based on years of service and salary history, most participants had built up substantial pension entitlement. The organisation offered the option to commute or ‘cash out’ some or all of the pension benefits from age fifty-five – members received a (potentially taxable) lump-sum payment instead of the future pension income. Commutation lump-sum calculations took into account the individual’s age, life expectancy, and the amount of commuted pension. The commutation workers received independent financial advice (IFA) paid for by their employer and so they were generally well-informed about their retirement options. According to a trade union representative, the size of the lump sums may have accelerated the trend towards early retirement.

Financial services: The financial services company had complex pension arrangements with varied accrual rates, retirement ages, and employee contribution requirements. Around 30 per cent of employees were still contributing to the DB pension – the retirement age had risen to sixty-five but members could increase contributions by 5 per cent to keep it at sixty. Recruits were automatically enrolled in a DC scheme to which the employer contributed. Consequently, workers of a similar age could have different pension entitlement and pension payment ages depending upon their career history. The primarily female participants included part-time workers, and renumeration levels were wide ranging.

Social care: Workers were automatically enrolled in a DC pension scheme, and the employer paid the statutory minimum employers’ contribution of 3 per cent of salary. Salaries were below the national average. There was limited career and salary progression in most positions, but the company was very flexible around working hours, offering both condensed hours and variable part-time work. Employees were primarily female, and many had broken career histories with periods of part-time work or self-employment.

Self-employed: The twenty self-employed participants were all responsible for their own pension provision but several had access to occupational pensions from previous employment. The self-employed fell into two broadly equal financial camps. The first had either accumulated savings through successful businesses, had high earnings, and/or supplemented self-employment with occupational pensions or spousal income. The highest earners owned property or rented through choice. The second self-employed group were more financially precarious, having broken work histories, low pension provision, and relied on self-employment for survival or to supplement other income or state benefits. Seven of the lowest earners were female and eight of the ten lowest earners claimed to have no pension savings. Income volatility posed a significant challenge for some of the self-employed, particularly for those who relied on the next job or commission for income.

Financial vulnerability was more pronounced for the single self-employed who lacked the safety net of a partner’s salary or pension. Some of the self-employed had been forced to use pension savings to replace lost income during the Covid-19 pandemic.

Research findings

Mortgage redemption and subjective financial wellbeing

The first significant finding is that paying off a mortgage prior to retirement was a critical factor in financial wellbeing and the decision to retire. Forty of the participants were homeowners, and home ownership was typically deeply integrated into their retirement plans. Mortgage terms influenced the length of time individuals anticipated working and how they used their retirement savings. Participants who still had a mortgage attached importance to retiring without any outstanding mortgage debt. Having a mortgage was generally seen as a burden and, as the following respondent highlights, removing that burden enhanced wellbeing: ‘So, for the last four years I don’t have to care because I got a lump sum and access to my pension so I was able to pay off my mortgage which was amazing’. (Male, 62, social care, part-time, single, homeowner).

Those who had low or no housing debt generally exhibited higher financial wellbeing and a more relaxed approach to the prospect of retiring. However, it was notable that several participants had redeemed their mortgages with funds taken from pension savings, which ultimately would lead to lower income in retirement. Thus, although financial wellbeing had improved in the short-term, it might deteriorate over the longer-term.

Practically speaking, mortgage redemption resulted in lower financial outgoings, and surplus income could then be redirected towards pensions and other investment avenues. Beyond this, redemption also improved subjective financial wellbeing by promoting a sense of achievement and financial control. Those who owned their homes outright felt more confident about their overall financial security because lower housing costs allowed for more flexibility in managing financial risks. Moreover, for some, housing was viewed as an alternative or supplementary source of pension funds. Several participants had already downsized or were planning to downsize as part of their retirement strategy if this would result in better financial security.

Being mortgage-free reduced stress and increased flexibility about when to retire. Those who had been fortunate enough to have no mortgage in their early sixties had greater flexibility about choosing the date of retirement, whereas those with mortgages were usually obliged to continue working, sometimes even beyond SPA.

Disparities in achieving early mortgage-free status often stemmed from earlier life events such as divorce. Some participants had bought out their former spouse’s share, funding this by extending their mortgage term. Starting second families later in life could also lead to long mortgages. Extended mortgages and the associated inability to retire at SPA contributed to poor financial wellbeing. One participant, who needed to work beyond sixty-seven to meet mortgage obligations, noted her concerns: ‘[the] future, that worries me. Only because I’ve got a mortgage, because having to get divorced and you have to take out a mortgage, you didn’t expect to go so far into age’. (Female, 61, financial services, divorced).

Vulnerability to income shocks

One positive of being free from mortgage debt is that it reduces an individual’s vulnerability to income shock. Being a mortgage-free homeowner significantly mitigated the financial risks associated with unemployment – a notable benefit given the challenging jobs market for MLLW. Most participants had stable jobs or took a relaxed approach to potential unemployment because, having pensions and housing equity, they considered themselves financially secure enough to transition into retirement. For instance, one sixty-seven-year-old remarked that she would welcome redundancy. However, several spoke about past unemployment and one observed that using his redundancy payment to settle his mortgage reduced the anxiety of managing finances without a regular salary and made him feel more confident facing financial uncertainty.

Unemployment uncertainty was more apparent in those who did not consider themselves financially secure enough to retire and, as exemplified in the following quote, felt that the jobs market discriminated against older workers: ‘Who’s going to hire a 62-year-old? …, all I could apply for is minimum wage jobs’. (Female 62, self-employed, social renter, very low income).

Health

Concerns about ill health, or premature death could prompt contemplation of early retirement: ‘When you hear somebody dying quite young, you say to yourself “I’m getting old here”. I think about retiring then’. (Male, 62, manufacturing, mortgage-free, younger partner).

Property equity and other income sources during the pre-retirement stages provided a psychological safety net, offering early retirement options in the face of potential health stressors. Although, in financial wellbeing terms, health uncertainty was rarely spoken of directly, analysis uncovered intriguing insights into how individuals projected their current and past health, along with their earning capacity, into the future. The self-employed expressed greater reliance on their own ability to generate income in later life; several talked about working well into their seventies, despite the fact that the majority of individuals over seventy in the UK are neither in employment nor good health. A notable example was a self-employed individual with health issues and no retirement investments who nevertheless expressed confidence in his ability to manage future financial needs. This tendency for individuals to evaluate themselves and their outcomes positively and underestimate the risks revealed the inherently subjective nature of financial wellbeing.

Renting

Given the importance of (outright) home ownership to financial wellbeing, one might have expected that those participants who rented their homes would feel less secure. However, overall, the picture was mixed, illustrating the salience of subjective financial wellbeing. Many of the participants who had experienced a low standard of living throughout their lives were positive about approaching retirement. Factors such as past experiences, self-resilience, and self-perception mitigated how they felt about lack of housing equity.

For example, for one participant judged her financial wellbeing to be high because of the relative improvement in her life from being a single parent to being re-married: ‘I have a wee bit saved up in the bank for a rainy day. I never had that before. My finances is better than it’s ever been in my whole life. We’re not poor you know!’ (Female, 60 social care, part-time, low-income, married, renting).

Another participant, a single sixty-two-year-old self-employed male who described his life as having ‘zero security’, was also happy about his financial wellbeing because he valued autonomy and flexibility over traditional markers of financial success such as housing equity. In contrast, a third participant spoke about how unhappy she felt about renting and the impact it had, not just on herself, but her adult child. Her distress centred on her altered circumstances, which had changed from previously being a homeowner and financially comfortable: ‘Which is very challenging in the sense of financial security, and it freaks my youngest child out. So, the whole, for me it’s the whole psychology of being, I’m renting. Which is sad’. (Female 67, financial services, divorced).

Social influences and benchmarking

Comparison to peers, family or one’s own financial situation or financial goals and aspirations impacted individuals’ perceptions of financial wellbeing, and participants applied their own rationale to these comparisons. A positive comparison contributed to higher subjective financial wellbeing as exemplified by the following participant acknowledging their fortunate position compared with friends: ‘Most of our friends are separated or divorced and they’ve used up their pensions and everything and we reckon that’s where we’ve landed lucky’. (Female, 65, social care, married, mortgage-free).

Divorce was a common thread that impacted later financial wellbeing because changes in marital status could throw early retirement preparations off course. Divorce altered the burden of care, making it harder for some parents to earn sufficient income to fund pensions. Later parenthood, second families, and children requiring financial support in early adulthood also put pressure on parents in later life when they might have hoped to be retired. Significantly, an individual’s relative position compared with their expectations for their stage and age in life influenced how they felt about their financial situation as they approached retirement. Perceiving oneself as falling behind ones chosen comparison points resulted in lower levels of financial satisfaction. Several participants made reference to friends or relatives who were already retired and expressed dissatisfaction their own inability to do so. One self-employed respondent who could not afford to retire noted: ‘Frankly I didn’t expect to be working [ at age 68] …I suppose overall, I’m doing it [working] grudgingly. I really used to enjoy it because it was, you know an add on, it was something I was doing because I chose to. Now that I have to, I do resent it a bit’. (Male 68, self-employed, divorced, renting).

Changes to SPA

Women facing an increased SPA from sixty to sixty-seven were generally less satisfied than men with their financial wellbeing. Objectively, working beyond sixty should have enabled women to accumulate retirement savings; however, several women expressed strong emotional dissatisfaction because their retirement expectations had not been met. For example: ‘I was very angry when they put up the pension age because I should have been retired when I was 60 and you just look at it and you just think well, we [my husband and I] should have retired together’. (Female, 65, social care, married, mortgage-free).

The emotional reaction to increased SPA disrupted retirement planning, often by affecting subjective financial wellbeing. Most women felt compelled to continue working beyond what was previously considered their retirement age. However, the emotional response to how they managed their financial wellbeing varied. One participant, although having some pension savings, felt resigned that retirement was no longer in her control: ‘So, I just need to keep going until whenever it is we’re allowed to retire’. (Female, 61, social care, part-time, low-earner, mortgage-free).

A more common response was to consider retiring early, even if this would be financially disadvantageous. The indications were that few of the women in the study would remain in employment until the SPA of sixty-seven. Many women in their sixties had slightly older husbands who could trigger their early retirement even if this was financially disadvantageous.

The milestone age of sixty-five held a strong sway, influenced both by occupational pensions payouts and social norms. Some were willing to substantially reduce their current outgoings or deplete pensions and savings, risking a lower standard of living in later life, as a trade-off for a few years of free time prior to the SPA. For example: ‘I’m already looking forward to sending them a “Sorry for your loss” card and just rely on my self-employment, because I’ve only got two years before I would qualify for my pension. I think I will probably have enough savings to last that two years if I needed to’. (Female, 64, self-employed, part-time, divorced, low-earner, mortgage).

The desired retirement age seemed to be a compromise between maximising income and the perceived benefits of not engaging in paid work. Retiring later allowed individuals the chance to continue earning and accrue pensions for longer but risked having limited time left to enjoy retirement. So, the favoured retirement age was not at the point when in receipt of both state and private pensions, but appeared to be at a point of compromise between having a reasonable standard of living and enjoying the benefits of no longer working. This presents an income/free time compromise. For example:

Well, my current plan, because I’ve got that extra bit of money, is to work until I’m 65, so I’ve only got just over two years, just about two years left to work, because then I’d get my work pension. It’s not a lot, but you know it’ll be enough for me until I get my state pension. (Female, 63, financial services, husband not working, mortgage almost paid off).

The SPA was the, albeit reluctantly, accepted target retirement date for those with the least non-state pension savings. Financial reasons for continuing to work were most often cited by women in their sixties and indeed, two divorced women continued to work beyond the SPA for financial reasons.

Legacy of the Covid-19 pandemic

The experience of the Covid-19 pandemic had a lasting impact on some of the participants and their appraisal of where the income/free time compromise lay. While a minority in this study, particularly the self-employed, suffered a significant decline in income during the lockdowns, for many employees the pandemic response included working from home or paid furlough. The additional forced halt to consumption helped some households build up savings and reduce mortgage debts. The lockdowns provided an opportunity to appraise lives and gain a clearer understanding of what was important in their lives and the level of income required to survive in retirement. For some, the lockdowns had been positive because they found working from home fitted better with family responsibilities. However, others had felt more conscious of time passing and opportunities missed. Post-pandemic, several of the participants, such as the undernoted, had reduced their economic activity and redirected focus onto their wellbeing: ‘And so, when we went back to normal, I just sort of said that I’ve decided to cut my hours down so I wouldn’t be coming back’. (Female, 64, self-employed, divorced, mortgage-free).

By cutting hours this individual was most probably facing lower income, but in common with many others approaching retirement, she had mentally adapted to the prospect by lowering consumption and cutting expenses.

Pension availability and retirement timing

Fourteen of the participants under SPA were already receiving work-related pensions, mostly paid out at sixty or sixty-five. However, the availability of private/occupational pensions before reaching the SPA did not automatically trigger a willingness to retire. Many participants enjoyed working, valuing the mental health benefits of remaining socially engaged, and saw the advantages to both drawing pensions and remaining employed. Some used pensions to finance a reduction in working hours, or become self-employed, and pensions were a solution to the dilemma of either being employed full-time or experiencing reduced income. Part-time employment was a popular way of managing the physical challenges of ageing, and the study revealed that many MLLW would prefer this type of gradual retreat from the workplace. However, the challenge for those not already working for accommodating employers was the scarcity of suitable quality part-time work. Some had resorted to self-employment instead, with one participant commenting that fatigue meant that nine-to-five employment was no longer an option. Becoming self-employed was a trade-off between the financial security of regular income and control over working hours. Fifteen of the part-time workers were self-employed and gender differences emerged – more than half of the women in the sample were working part-time – and for many, wellbeing was closely tied to a level of autonomy over working hours and conditions.

Finally, our analysis suggests that even if pensions were not needed, some participants accessed their pensions anyway – especially if there was a cash lump sum component. Having substantial cash savings generally improved subjective financial wellbeing because it improved flexibility in the face of future uncertainties. For example: ‘…it’s like, grab it and run really isn’t. It’s just you know, nothing safe these days… who knows what the future holds? So just as well to take it’. (Female, 67, manufacturing, full-time, single, good income, mortgage-free).

Discussion

This article’s principal contribution is to the field of subjective financial wellbeing and builds on Easterlin’s (Reference Easterlin2001) insights into adequacy. Specifically, we found that although financial considerations often drove the timing of retirement, individuals’ perceptions of the adequacy of their savings were highly subjective. While financial assets equated with financial wellbeing for many participants, some relatively poorer individuals felt financially secure enough to retire whereas, ironically, some objectively wealthier participants were concerned about financial adequacy in retirement.

Three main factors underpinned our findings on subjective financial wellbeing: the importance of freeing oneself of mortgage debt; social influences including cultural perceptions of the ‘ideal’ retirement age; and the nexus between flexible working, Covid-19, and pension freedoms.

The importance of mortgages

Firstly, our study revealed the deep-rooted connection between home ownership, financial wellbeing, and the retirement plans of participants. Those who had little or no mortgage debt exhibited a more relaxed approach to the possibility of financial shocks in the years leading up to state pension entitlement. Although it is known that financial wellbeing is negatively correlated with housing debt, this is not fully explained by associated housing costs, and there could be a psychological explanation (Hermann et al., Reference Hermann, Herbert and Molinsky2020). Our premise is that the focus on bricks and mortar throughout the life-course is a preventive coping strategy (Aspinwall, Reference Aspinwall and Folkman2011) that helps individuals feel more in control of the financial consequences of approaching retirement. An important contribution we make to this thesis is the finding that some individuals accessed pension savings to redeem mortgages well before retirement. This decision is currently hidden in official statistics, which do indicate pension decumulations being used for debt redemption, but do not differentiate between mortgages and other debts (Financial Conduct Authority, 2025a). Eliminating mortgage debt improved financial wellbeing because it lowered anxiety about potential employment and health risks. Furthermore, we argue that subjective feelings of self-reliance in income generation, as exhibited by some of the self-employed participants, are equally important to maintaining healthy financial wellbeing. This accords with Vlaev and Elliott’s (Reference Vlaev and Elliott2014) view that control is the paramount predictor of financial wellbeing.

In addition, our analysis suggests that individuals who own mortgage-free properties are more inclined to contemplate retiring early, aligning with prior research by Lain (Reference Lain2016) and Wildman (Reference Wildman2020) pointing to a correlation between housing debt and retirement age. However, our study goes further by highlighting that achieving mortgage redemption may come at the cost of early pension encashment. We identified several examples of individuals who had accessed their DB pensions to free up lump sums, whereas, from a long-term financial perspective, they might have benefited from postponing drawing their pensions, thereby allowing savings to accumulate in a tax-free environment. There is clearly an unmet, and possibly unrecognised, need for financial advice regarding the relationship between mortgage redemption and pensions, which surfaces well before anticipated retirement dates. Some of the participants in the study benefitted from employer-provisioned access to independent financial advice; for MLLW without that support, there is a risk the emotional drive to reduce mortgage debt might hamper long-term pension savings.

Social influences and benchmarking

The study makes a contribution to the literature on subjective financial wellbeing and social influences by highlighting the relative and context-dependent nature of how individuals assess their financial situation and overall wellbeing. Historical retirement norms meant that the UK’s SPA was rarely seen as the ideal retirement age by participants. Comparisons with others influenced when participants wanted to retire. Furthermore, lower subjective financial wellbeing among those unable to retire when they expected to adds support to the view that financial wellbeing is mainly viewed in relativistic terms (Burholt & Windle, Reference Burholt and Windle2006; Dolan et al., Reference Dolan, Peasgood and White2008; Corazzini et al., Reference Corazzini, Esposito and Majorano2012).

We also add to the literature on the role of emotions on financial decision-making. Variance between the expected retirement age and the SPA had the potential to override financial rationalism. Strong emotional responses can impinge on rational decision-making (Zaleskiewicz & Traczyk, Reference Zaleskiewicz, Traczyk, Zaleskiewicz and Traczyk2020), which we evidence by demonstrating that some individuals choose to trade long-term financial security for early retirement. As feelings of control of personal finances is the main predictor of financial wellbeing (Vlaev & Elliott, Reference Vlaev and Elliott2014), this aspect of counter-intuitive choice enables subjective financial wellbeing, arguably at the expense of increasing objective financial wellbeing. The motivation for this type of behaviour has potential for further study and may have its roots in fears associated with future time perspective.

Covid-19, flexible working and pension freedoms

The Covid-19 pandemic appears to have altered financial decision-making by giving people the opportunity to re-evaluate their priorities. MLLW retiring early could have been a strategy to mitigate potential regret about not taking advantage of good health when available. Regarding the impact of Covid-19 on future-orientated behaviour, we posit that investigating how MLLW respond to future time perspective in relation to retirement is a promising avenue for future research. The zeitgeist of the 2020s has generated greater focus on the life side of the work/life balance. Understanding this shift is critical to understanding why MLLW might choose to retire even if it leads to poorer objective financial outcomes.

Government and organisational policy agenda around extending the working lives of MLLW must offer meaningful and appropriate flexible work choices. Although many MLLW express a preference for transitioning to part-time work, there is a relative lack of opportunities that are tailored towards the flexibility needs of people in stages of the life-course beyond early parenthood (Loretto & Vickerstaff, Reference Loretto and Vickerstaff2015). Since April 2024, UK law grants the right to request flexible working, but does not guarantee employer approval. For MLLW wishing to change employment, there is a scarcity of advertised, high-quality, part-time employment prospects. Although beyond the scope of this study, the challenges MLLW face because of ageism in securing new employment are well-documented (Centre for Ageing Better, 2025). Our study noted sectoral and gendered differences in MLLW part-time opportunities, with low-paid social care dominating. Further research is merited into how long-highlighted issues of pension adequacy and gender (Foster, Reference Foster2023; Loretto & Vickerstaff, Reference Loretto and Vickerstaff2015) intersect with sectoral differences.

We argue that pension savings are no longer seen purely in terms of post-employment income. While for some, pensions are a means of reducing the risks of severe income shocks prior to SPA, for others pensions are a means to maintain a foothold in the working environment. It might seem paradoxical that having saved throughout their working lives into pensions for retirement income, those on the cusp of retirement take actions that effectively reduce their retirement income in later old age. Our view is that this is indicative of the subjectivity of financial wellbeing as people age and reassess their multi-domain priorities of work, health, leisure, and family life.

Implications of findings and policy recommendations

The phenomenon of individuals taking pensions early has its roots in perceptions of risk, and in the UK’s diminishing state-funded social security safety net for MLLW. Since pension freedoms, many choose to mitigate perceived risks through drawing on personal pension savings in cash rather than buying income-producing annuities. Over 50 per cent of DC pensions accessed are full encashment (Financial Conduct Authority, 2025b). A participant’s comment that ‘nothing is safe these days’ is key. Our premise is that cash has psychological value in that it provides an appearance of security. However, taken early from pension savings, it increases the risk of running out of funds once the individual is in retirement.

The freedom to choose how to spend retirement savings is sacrosanct, but that decision-making must be made from an informed position. Regrettably, past policies have created a Byzantian pension system that few can navigate without support. The over fifties with DC pensions are entitled to a free government funded face-to-face guidance appointment but, crucially, this does not cover the State Pension or DB pensions (Money Helper, n.d.). Such limited guidance is insufficient and needs to be enhanced for those with multiple pension pots and complex decisions to make about the timing and scope of pension withdrawal in the decade before retirement.

In line with neo-liberal approaches to later-life working and retirement, the UK’s extending working lives agenda promotes individual choice and control, with support provided by heralding the benefits of flexible working and including age as a protected characteristic under the Equalities Act 2010. In fact, neither of those supports prioritises older age, and, in reality, the main response to the ageing population has been largely transactional, through limiting access to state benefits and raising the SPA so that older people are forced to continue working full time (Street & Ní Léime, Reference Street, Ní Léime, Wilmoth and London2021). Our study underscores that these economic-orientated approaches fail to acknowledge the lived experience of MLLW, and that the choices made will revolve around how income is valued relative to time, positioned here as the income/free time compromise. These choices are made through emotional and comparative assessments of whether individuals have sufficient resources for retirement. As the proportion of MLLW in the workforce is set to rise rapidly in coming years (Centre for Ageing Better, 2025), an appreciation of the complex interactions between objective and subjective factors influencing decisions on the timing and nature of later-life work and retirement is needed to move policy forward.

Data availability statement

Data are available from Edinburgh Data Share https://datashare.ed.ac.uk/handle/10283/8871.

Author contributions

Professor Loretto is the Principal Investigator of the SHAW project.

Funding statement

The authors are project members of the Supporting Healthy Aging at Work project, which was funded through UKRI Healthy Ageing Challenge Social, Behavioural and Design Research Program, grant number ES/V016148/1.

Competing interests

The author(s) declare none.

Open access

Open access