1. Introduction

Over half a century ago, Solow (Reference Solow1956) and Swan (Reference Swan1956) developed a one-sector growth model that serves as the foundation for all neo-classical growth models. The qualitative dynamics of this model are rather simple, as capital-to-labour ratios either converge monotonically to a unique steady state or become unbounded. The purpose of this article is to demonstrate that a parsimonious extension of the Solow–Swan model to a two-sector growth model with a constant propensity to save out of aggregate income allows for endogenous cycles and complex dynamics.

The literature has addressed the limitation that the Solow–Swan model in discrete time cannot explain for endogenous cycles in two primary ways: first, by endogenising the savings propensity, and second, by incorporating multiple production sectors. In a seminal paper Day (Reference Day1982) showed that one-sector growth models can exhibit cyclical growth patterns if the savings function depends non-linearly on aggregate income. In his model the difference equation governing growth paths is, in essence, a logistic map, which is well known for its capacity to generate complex dynamics, see Devaney (Reference Devaney1989). However, a number of contributions have shown that Day’s ad hoc savings function is generally inconsistent with intertemporal utility maximisation, for example, see the survey by Boldrin and Woodford (Reference Boldrin and Woodford1990). In hindsight, it is somewhat surprising that it took considerable time to recognise that Kaldor (Reference Kaldor1956, Reference Kaldor1957) simple modification of the Solow–Swan model permits complex dynamics. Böhm & Kaas (Reference Böhm and Kaas2000) demonstrated that Kaldor’s model can exhibit topological chaos as defined by Li and Yorke (Reference Li and Yorke1975) even with small variations in savings propensities, provided the distribution of factor incomes varies sufficiently. Cycles of any order and complex dynamics become possible both in optimal growth and OLG models with two sectors as soon as the single all-purpose good is replaced by two distinct goods, one for consumption and one for investment purposes, see Stachurski et al. (Reference Stachurski, Venditti and Makoto2012).

Most of the literature on two-sector growth models adopts the so-called no-factor-intensity-reversal condition, also referred to as capital-intensity condition, according to which the capital-to-labour ratio in one sector consistently exceeds that in the other for all wage-rental ratios. This assumption is crucial in the classical continuous time two-sector growth model with a constant savings propensity, which dates back to Uzawa (Reference Uzawa1961, Reference Uzawa1963), Inada (Reference Inada1963), and Drandakis (Reference Drandakis1963), and is needed to address the existence of steady states. However, in continuous time, complex dynamic behaviour is precluded by the well-known Poincaré–Bendixson Theorem. In Galor (Reference Galor1992), the capital-intensity condition is essential for the existence and uniqueness of perfect-foresight equilibria. Some contributions allow for factor-intensity reversals but limit their focus to specific technologies, such as a Cobb–Douglas and Leontief production functions, for example, see Boldrin and Deneckere (Reference Boldrin and Deneckere1990) or Ralf (Reference Ralf2001) and references therein. [Uzawa (Reference Uzawa1963), p. 109], in response to the Solow (Reference Solow1961) critique, acknowledged that ruling out factor-intensity reversals is ‘required mainly for reasons of a mathematical nature and for which it seems to be difficult to give any economic justification’. Unfortunately, the capital-intensity condition imposes significant restrictions on production functions and, aside from Cobb–Douglas functions, excludes already those with a constant elasticity of substitution (CES).

The aim of this article is to present a two-sector growth model without a priori restrictions on factor-intensity reversals, allowing for a general class of homogeneous production functions, including CES production functions. The model employs a novel parametrisation of the production-possibility frontier in terms of wage-rental ratios, as introduced by Ritschel and Wenzelburger (Reference Ritschel and Wenzelburger2024). The other features of the model are sparse and standard. The savings propensity remains constant, resulting in dynamics governed by a univariate map. We will demonstrate that the non-linear dependency of the economy’s propensity to invest on capital-to-labour ratios is responsible for endogenous business cycles and complex dynamic behaviour. This market mechanism has yet to be identified as a cause of non-monotonic dynamics.

2. The model

This section develops a two-sector extension of the neo-classical growth model, introduced by Solow (Reference Solow1956) and Swan (Reference Swan1956). Two distinct sectors employ capital and labour to produce consumption goods for consumption needs and investment goods for investment purposes. Neither consumption of investment goods nor investment in consumption goods is possible. Markets are perfectly competitive, and capital and labour are perfectly mobile between sectors. The investment good is chosen as numéraire and the prices of labour, capital, and the consumption good in period

$t$

are denoted by

$t$

are denoted by

$w_t$

,

$w_t$

,

$r_t$

, and

$r_t$

, and

$p_t$

, respectively.

$p_t$

, respectively.

Time is discrete. In every period

$t=0,1,\ldots$

, consumers supply capital

$t=0,1,\ldots$

, consumers supply capital

$K_t$

and labour

$K_t$

and labour

$L_t$

inelastically to the markets and receive factor income in return from which they save and invest a constant proportion

$L_t$

inelastically to the markets and receive factor income in return from which they save and invest a constant proportion

$0 \leq s \leq 1$

. The factor income per capita in terms of the investment good is

$0 \leq s \leq 1$

. The factor income per capita in terms of the investment good is

$w_t+r_tk_t$

, where

$w_t+r_tk_t$

, where

$k_t\,:\!=\,K_t/L_t$

is the economy-wide capital-to-labour ratio. Per capita, consumers invest

$k_t\,:\!=\,K_t/L_t$

is the economy-wide capital-to-labour ratio. Per capita, consumers invest

$s[w_t+r_tk_t]$

units of the investment good and spend

$s[w_t+r_tk_t]$

units of the investment good and spend

$(1-s)[w_t+r_tk_t]$

units on consumption.

$(1-s)[w_t+r_tk_t]$

units on consumption.

2.1 Technology

The consumption-goods sector

$(x)$

and the investment-goods sector

$(x)$

and the investment-goods sector

$(y)$

operate time-invariant constant-returns-to-scale production technologies given by the production functions

$(y)$

operate time-invariant constant-returns-to-scale production technologies given by the production functions

\begin{equation*} f_j \, : \, \mathbb{R}_+ \to \mathbb{R}_+,\quad k^j \mapsto f_j(k^j),\quad j=x,y, \end{equation*}

\begin{equation*} f_j \, : \, \mathbb{R}_+ \to \mathbb{R}_+,\quad k^j \mapsto f_j(k^j),\quad j=x,y, \end{equation*}

where

$k^j$

denotes the capital intensity in sector

$k^j$

denotes the capital intensity in sector

$j$

. The sector-specific marginal products of labour and capital are

$j$

. The sector-specific marginal products of labour and capital are

$w_j(k^j)\,:\!=\,f_j(k^j)-f^{\prime }_j(k^j)k^j$

and

$w_j(k^j)\,:\!=\,f_j(k^j)-f^{\prime }_j(k^j)k^j$

and

$f_j^\prime (k^j)$

, respectively, so that the corresponding marginal rates of technical substitution (MRTS) take the form

$f_j^\prime (k^j)$

, respectively, so that the corresponding marginal rates of technical substitution (MRTS) take the form

\begin{equation} \Omega _j(k^j)\,:\!=\,\frac {w_j(k^j)}{f_j^\prime (k^j)}=\frac {f_j(k^j)}{f_j^\prime (k^j)}-k^j,\quad j=x,y. \end{equation}

\begin{equation} \Omega _j(k^j)\,:\!=\,\frac {w_j(k^j)}{f_j^\prime (k^j)}=\frac {f_j(k^j)}{f_j^\prime (k^j)}-k^j,\quad j=x,y. \end{equation}

Assumption 1 (Technologies). The technologies of the two production sectors satisfy the following.

-

(i) Each production function

$f_j\, : \, \mathbb R_+\to \mathbb R_+$

,

$j=x,y$

, is twice continuously differentiable, strictly increasing,

$f_j^\prime \gt 0$

, and strictly concave,

$f_j^{\prime \prime }\lt 0$

.

$f_j\, : \, \mathbb R_+\to \mathbb R_+$

,

$j=x,y$

, is twice continuously differentiable, strictly increasing,

$f_j^\prime \gt 0$

, and strictly concave,

$f_j^{\prime \prime }\lt 0$

. -

(ii) Each marginal rate of technical substitution

$\Omega _j\, : \, \mathbb R_+\to \mathbb R_+$

,

$j=x,y$

, fulfils the boundary conditions

\begin{equation*} \lim _{k\to 0}\Omega _j(k)=0\quad \text{and}\quad \lim _{k\to \infty }\Omega _j(k)=\infty . \end{equation*}

Assumption1 dates back to Drandakis (Reference Drandakis1963).Footnote

1

It follows from Assumption1 (i) that the MRTS functions

$\Omega _x$

and

$\Omega _x$

and

$\Omega _y$

are continuously differentiable and strictly increasing. Assumption1 (ii) ensures that there exist continuously differentiable relative factor demand functions

$\Omega _y$

are continuously differentiable and strictly increasing. Assumption1 (ii) ensures that there exist continuously differentiable relative factor demand functions

$\kappa _j \, : \, \mathbb{R}_{+} \to \mathbb{R}_{+}$

,

$\kappa _j \, : \, \mathbb{R}_{+} \to \mathbb{R}_{+}$

,

$j=x,y$

, defined by

$j=x,y$

, defined by

\begin{equation} \Omega _j(\kappa _j(\omega ))=\omega \quad \text{for all }\,\omega \in \mathbb R_+. \end{equation}

\begin{equation} \Omega _j(\kappa _j(\omega ))=\omega \quad \text{for all }\,\omega \in \mathbb R_+. \end{equation}

These functions determine the sector-specific capital-to-labour ratios

$\kappa _j(\omega )$

, given a wage-rental ratio

$\kappa _j(\omega )$

, given a wage-rental ratio

$\omega$

. Factor-intensity reversals arise if

$\omega$

. Factor-intensity reversals arise if

$\Omega _x$

and

$\Omega _x$

and

$\Omega _y$

intersect. Specifically, if

$\Omega _y$

intersect. Specifically, if

$\Omega _x(k)\lt \Omega _y(k)$

, then

$\Omega _x(k)\lt \Omega _y(k)$

, then

\begin{equation} \kappa _y(\omega )\lt k\lt \kappa _x(\omega ) \quad \text{for all }\, \omega \in \bigl (\Omega _x(k),\Omega _y(k)\bigr ). \end{equation}

\begin{equation} \kappa _y(\omega )\lt k\lt \kappa _x(\omega ) \quad \text{for all }\, \omega \in \bigl (\Omega _x(k),\Omega _y(k)\bigr ). \end{equation}

Vice versa, if

$\Omega _x(k)\gt \Omega _y(k)$

, then

$\Omega _x(k)\gt \Omega _y(k)$

, then

\begin{equation} \kappa _x(\omega )\lt k\lt \kappa _y(\omega ) \quad \text{for all }\, \omega \in \big (\Omega _y(k),\Omega _x(k)\bigr ). \end{equation}

\begin{equation} \kappa _x(\omega )\lt k\lt \kappa _y(\omega ) \quad \text{for all }\, \omega \in \big (\Omega _y(k),\Omega _x(k)\bigr ). \end{equation}

The class of production functions with a constant elasticity of factor substitution (CES) satisfies Assumption1. This class features factor-intensity reversals and, in general, violates one of the Inada (Reference Inada1963) conditions, a rather restrictive property typically assumed in the literature.

For any wage-rental ratio

$\omega$

, the production elasticity in sector

$\omega$

, the production elasticity in sector

$j$

is determined by a function

$j$

is determined by a function

$\varepsilon _j\, : \, \mathbb R_{++}\to \mathbb R$

, defined by

$\varepsilon _j\, : \, \mathbb R_{++}\to \mathbb R$

, defined by

\begin{equation*} \varepsilon _j(\omega ) \,:\!=\,\frac {f_j^\prime (\kappa _j(\omega ))\kappa _j(\omega )}{f_j(\kappa _j(\omega ))}. \end{equation*}

\begin{equation*} \varepsilon _j(\omega ) \,:\!=\,\frac {f_j^\prime (\kappa _j(\omega ))\kappa _j(\omega )}{f_j(\kappa _j(\omega ))}. \end{equation*}

The elasticity of factor substitution in sector

$j$

is determined by the function

$j$

is determined by the function

$\sigma _j\, : \, \mathbb R_{++}\to \mathbb R_+$

, defined byFootnote

2

$\sigma _j\, : \, \mathbb R_{++}\to \mathbb R_+$

, defined byFootnote

2

\begin{equation} \sigma _j(\omega )\,:\!=\,\frac {\kappa _j^\prime (\omega )\omega }{\kappa _j(\omega )}. \end{equation}

\begin{equation} \sigma _j(\omega )\,:\!=\,\frac {\kappa _j^\prime (\omega )\omega }{\kappa _j(\omega )}. \end{equation}

Example 1 (CES production functions). CES production functions

$f_j\, : \, \mathbb R\to \mathbb R_+$

are defined by

$f_j\, : \, \mathbb R\to \mathbb R_+$

are defined by

\begin{align} f_j(k) = \left \{ \begin{array}{l@{\quad \mbox{if}\ }l} \displaystyle \frac {a_j}{b_j}\ k^{b_j} & \sigma _j=1 \\ \displaystyle \frac {a_j}{b_j} \left [b_j k^{\frac {\sigma _j-1}{\sigma _j}} +(1-b_j)\right ]^{\frac {\sigma _j}{\sigma _j-1}} & \sigma _j \neq 1 \end{array} \right ., \end{align}

\begin{align} f_j(k) = \left \{ \begin{array}{l@{\quad \mbox{if}\ }l} \displaystyle \frac {a_j}{b_j}\ k^{b_j} & \sigma _j=1 \\ \displaystyle \frac {a_j}{b_j} \left [b_j k^{\frac {\sigma _j-1}{\sigma _j}} +(1-b_j)\right ]^{\frac {\sigma _j}{\sigma _j-1}} & \sigma _j \neq 1 \end{array} \right ., \end{align}

where

$a_j\gt 0$

scales the total factor productivity,

$a_j\gt 0$

scales the total factor productivity,

$0\lt b_j \lt 1$

stipulates the factor-income distribution, and

$0\lt b_j \lt 1$

stipulates the factor-income distribution, and

$\sigma _j\gt 0$

determines the constant elasticity of factor substitution. The case of Cobb–Douglas production functions,

$\sigma _j\gt 0$

determines the constant elasticity of factor substitution. The case of Cobb–Douglas production functions,

$\sigma _j=1$

, is the only case in which both Inada conditions are satisfied. The MRTS functions

$\sigma _j=1$

, is the only case in which both Inada conditions are satisfied. The MRTS functions

$\Omega _j \, : \, \mathbb{R}_+\to \mathbb{R}_+$

,

$\Omega _j \, : \, \mathbb{R}_+\to \mathbb{R}_+$

,

$j=x,y$

take the form

$j=x,y$

take the form

\begin{equation*} \Omega _j(k)=\dfrac {1-b_j}{b_j}k^{\dfrac {1}{\sigma _j}}. \end{equation*}

\begin{equation*} \Omega _j(k)=\dfrac {1-b_j}{b_j}k^{\dfrac {1}{\sigma _j}}. \end{equation*}

The relative factor demand functions

$\kappa _j\, : \, \mathbb R_+\to \mathbb R_+$

,

$\kappa _j\, : \, \mathbb R_+\to \mathbb R_+$

,

$j=x,y$

are

$j=x,y$

are

\begin{equation} \kappa _j(\omega )=\left (\dfrac {b_j}{1-b_j}\omega \right )^{\sigma _j}. \end{equation}

\begin{equation} \kappa _j(\omega )=\left (\dfrac {b_j}{1-b_j}\omega \right )^{\sigma _j}. \end{equation}

Unless

$\sigma _x=\sigma _y$

, exactly one factor-intensity reversal occurs at

$\sigma _x=\sigma _y$

, exactly one factor-intensity reversal occurs at

\begin{equation*} \overline {\omega }\,:\!=\, \left (\dfrac {b_x}{1-b_x}\right )^{\frac {\sigma _x}{\sigma _y-\sigma _x}} \left (\dfrac {1-b_y}{b_y}\right )^{\frac {\sigma _y}{\sigma _y-\sigma _x}}. \end{equation*}

\begin{equation*} \overline {\omega }\,:\!=\, \left (\dfrac {b_x}{1-b_x}\right )^{\frac {\sigma _x}{\sigma _y-\sigma _x}} \left (\dfrac {1-b_y}{b_y}\right )^{\frac {\sigma _y}{\sigma _y-\sigma _x}}. \end{equation*}

Specifically, for

$\sigma _x\lt \sigma _y$

,

$\sigma _x\lt \sigma _y$

,

\begin{equation*} \kappa _y(\omega )\gtreqless \kappa _x(\omega ) \iff \omega \gtreqless \overline \omega , \end{equation*}

\begin{equation*} \kappa _y(\omega )\gtreqless \kappa _x(\omega ) \iff \omega \gtreqless \overline \omega , \end{equation*}

where

$\overline {k}=\kappa _x(\overline {\omega })=\kappa _y(\overline {\omega })$

is the critical value at which the factor intensities revert.

$\overline {k}=\kappa _x(\overline {\omega })=\kappa _y(\overline {\omega })$

is the critical value at which the factor intensities revert.

2.2 Temporary equilibria

A feasible allocation in period

$t$

is a list of relative factor inputs

$t$

is a list of relative factor inputs

$(k^x_t,k^y_t, l^x_t,l^y_t)\geq 0$

that satisfies

$(k^x_t,k^y_t, l^x_t,l^y_t)\geq 0$

that satisfies

\begin{equation} l_t^x + l_t^y=1 \quad \text{and}\quad l_t^x k_t^x + l_t^y k_t^y=k_t, \end{equation}

\begin{equation} l_t^x + l_t^y=1 \quad \text{and}\quad l_t^x k_t^x + l_t^y k_t^y=k_t, \end{equation}

where

$l^x_t\,:\!=\,\frac {L^x_t}{L_t}$

and

$l^x_t\,:\!=\,\frac {L^x_t}{L_t}$

and

$l^y_t\,:\!=\,\frac {L^y_t}{L_t}$

are the sector-specific labour shares,

$l^y_t\,:\!=\,\frac {L^y_t}{L_t}$

are the sector-specific labour shares,

$k^x_t$

and

$k^x_t$

and

$k^y_t$

the sector-specific capital-to-labour ratios, and

$k^y_t$

the sector-specific capital-to-labour ratios, and

$k_t=\frac {K_t}{L_t}$

is the economy-wide capital-to-labour ratio. A temporary equilibrium in period

$k_t=\frac {K_t}{L_t}$

is the economy-wide capital-to-labour ratio. A temporary equilibrium in period

$t$

is a feasible allocation

$t$

is a feasible allocation

$(k_t^x,k_t^y, l_t^x,l_t^y)$

together with prices

$(k_t^x,k_t^y, l_t^x,l_t^y)$

together with prices

$(r_t,w_t,p_t)$

denominated in the investment good at which all markets clear and profits in both sectors a maximised.

$(r_t,w_t,p_t)$

denominated in the investment good at which all markets clear and profits in both sectors a maximised.

Since capital and labour are allowed to move frictionless, both sectors must pay the same factor prices. The first-order conditions for profit maximisation are

\begin{equation} p_t f'_x(k^x_t)=f'_y(k^y_t)=r_t \quad \text{and}\quad p_tw_x(k^x_t)= w_y(k^y_t)=w_t. \end{equation}

\begin{equation} p_t f'_x(k^x_t)=f'_y(k^y_t)=r_t \quad \text{and}\quad p_tw_x(k^x_t)= w_y(k^y_t)=w_t. \end{equation}

Denote output per unit of aggregate labour input in sector

$j=x,y$

by

$j=x,y$

by

$x_t= l^x_tf_x(k^x_t)$

and

$x_t= l^x_tf_x(k^x_t)$

and

$y_t=l^y_tf_y(k^y_t)$

, respectively. Given the exogenous savings propensity

$y_t=l^y_tf_y(k^y_t)$

, respectively. Given the exogenous savings propensity

$0\leq s\leq 1$

, the market-clearing condition in the investment-goods market is

$0\leq s\leq 1$

, the market-clearing condition in the investment-goods market is

\begin{equation} s[w_t+r_tk_t]=l^y_tf_y(k^y_t) \end{equation}

\begin{equation} s[w_t+r_tk_t]=l^y_tf_y(k^y_t) \end{equation}

and the market-clearing condition in the consumption-goods market is

\begin{equation} (1-s)[w_t+r_tk_t]=p_t l^x_t \, f_x(k^x_t). \end{equation}

\begin{equation} (1-s)[w_t+r_tk_t]=p_t l^x_t \, f_x(k^x_t). \end{equation}

Definition 1 (Temporary equilibrium). Given

$k_t$

, a temporary equilibrium in period

$k_t$

, a temporary equilibrium in period

$t$

is an allocation

$t$

is an allocation

$(k^x_t,k^y_t,l^x_t,l^y_t)$

and a price vector

$(k^x_t,k^y_t,l^x_t,l^y_t)$

and a price vector

$(r_t,w_t,p_t)\gg 0$

that satisfy (8)–(11).

$(r_t,w_t,p_t)\gg 0$

that satisfy (8)–(11).

It follows from Assumption1 that for any feasible allocation (8) at prices

$(r_t,w_t,p_t)$

that satisfies (9), aggregate factor income is equal to the value of aggregate output, that is,

$(r_t,w_t,p_t)$

that satisfies (9), aggregate factor income is equal to the value of aggregate output, that is,

\begin{equation} w_t+r_tk_t=p_tx_t+y_t. \end{equation}

\begin{equation} w_t+r_tk_t=p_tx_t+y_t. \end{equation}

A temporary equilibrium may now be characterised as follows. Denoting the wage-rental ratio by

$\omega _t=\frac {w_t}{r_t}$

, the first-order conditions (9) may be rewritten as

$\omega _t=\frac {w_t}{r_t}$

, the first-order conditions (9) may be rewritten as

\begin{equation} \Omega _x(k^x_t)=\Omega _y(k^y_t)=\omega _t \quad \text{and}\quad \frac {f_y^\prime (k^y_t)}{f_x^\prime (k^x_t)}=p_t. \end{equation}

\begin{equation} \Omega _x(k^x_t)=\Omega _y(k^y_t)=\omega _t \quad \text{and}\quad \frac {f_y^\prime (k^y_t)}{f_x^\prime (k^x_t)}=p_t. \end{equation}

The relative factor demand functions (2) fulfil the first equation in (13) by construction, so that

$k^j_t=\kappa _j(\omega _t)$

,

$k^j_t=\kappa _j(\omega _t)$

,

$j=x,y$

for any

$j=x,y$

for any

$\omega _t\in \mathbb R_+$

. As a consequence, all equilibrium prices become functions of the wage-rental ratio, so that

$\omega _t\in \mathbb R_+$

. As a consequence, all equilibrium prices become functions of the wage-rental ratio, so that

\begin{equation} r_t=f_y^\prime (\kappa _y(\omega _t)),\quad w_t=w_y(\kappa _y(\omega _t)), \quad \text{and}\quad p_t= p_x(\omega _t)\,:\!=\,\frac {f_y^\prime (\kappa _y(\omega _t))}{f_x^\prime (\kappa _x(\omega _t))}. \end{equation}

\begin{equation} r_t=f_y^\prime (\kappa _y(\omega _t)),\quad w_t=w_y(\kappa _y(\omega _t)), \quad \text{and}\quad p_t= p_x(\omega _t)\,:\!=\,\frac {f_y^\prime (\kappa _y(\omega _t))}{f_x^\prime (\kappa _x(\omega _t))}. \end{equation}

Given an economy-wide capital-to-labour ratio

$k_t\in \mathbb R_+$

, there are two cases, the ‘generic’ case

$k_t\in \mathbb R_+$

, there are two cases, the ‘generic’ case

$\Omega _x(k_t)\neq \Omega _y(k_t)$

and the ‘non-generic’ case

$\Omega _x(k_t)\neq \Omega _y(k_t)$

and the ‘non-generic’ case

$\Omega _x(k_t)=\Omega _y(k_t)$

. Following Ritschel and Wenzelburger (Reference Ritschel and Wenzelburger2024), for each

$\Omega _x(k_t)=\Omega _y(k_t)$

. Following Ritschel and Wenzelburger (Reference Ritschel and Wenzelburger2024), for each

$k_t\in \mathbb R_+$

, set

$k_t\in \mathbb R_+$

, set

\begin{equation*} \Omega _{\mathrm{min}}(k_t)\,:\!=\,\min \bigl \{\Omega _x(k_t),\Omega _y(k_t)\bigr \} \quad \text{and}\quad \Omega _{\mathrm{max}}(k_t)\,:\!=\,\max \bigl \{\Omega _x(k_t),\Omega _y(k_t)\bigr \}. \end{equation*}

\begin{equation*} \Omega _{\mathrm{min}}(k_t)\,:\!=\,\min \bigl \{\Omega _x(k_t),\Omega _y(k_t)\bigr \} \quad \text{and}\quad \Omega _{\mathrm{max}}(k_t)\,:\!=\,\max \bigl \{\Omega _x(k_t),\Omega _y(k_t)\bigr \}. \end{equation*}

For each

$k_t\gt 0$

with

$k_t\gt 0$

with

$\Omega _x(k_t)\not =\Omega _y(k_t)$

, define the two sector-specific labour-share functions

$\Omega _x(k_t)\not =\Omega _y(k_t)$

, define the two sector-specific labour-share functions

\begin{equation} \ell _j(k_t,\cdot) \,:\, [\Omega _{\mathrm{min}}(k_t),\Omega _{\mathrm{max}}(k_t)] \to [0,1], \quad j=x,y, \end{equation}

\begin{equation} \ell _j(k_t,\cdot) \,:\, [\Omega _{\mathrm{min}}(k_t),\Omega _{\mathrm{max}}(k_t)] \to [0,1], \quad j=x,y, \end{equation}

by setting

\begin{equation*} \ell _x(k_t,\omega ) =\frac {\kappa _y(\omega )-k_t}{\kappa _y(\omega )-\kappa _x(\omega )} \quad {and}\quad \ell _y( k_t,\omega ) =\frac { k_t-\kappa _x(\omega )}{\kappa _y(\omega )-\kappa _x(\omega )}, \end{equation*}

\begin{equation*} \ell _x(k_t,\omega ) =\frac {\kappa _y(\omega )-k_t}{\kappa _y(\omega )-\kappa _x(\omega )} \quad {and}\quad \ell _y( k_t,\omega ) =\frac { k_t-\kappa _x(\omega )}{\kappa _y(\omega )-\kappa _x(\omega )}, \end{equation*}

respectively.Footnote 3 It is straightforward to verify that any list

\begin{equation*} \bigl (\kappa _x(\omega _t),\kappa _y(\omega _t),l_x(k_t,\omega _t),l_y(k_t,\omega _t)\bigr ) \,\text{with}\, \bigl (f_y^\prime (\kappa _y(\omega _t)),w_y(\kappa _y(\omega _t)), p_x(\omega _t)\bigr ), \end{equation*}

\begin{equation*} \bigl (\kappa _x(\omega _t),\kappa _y(\omega _t),l_x(k_t,\omega _t),l_y(k_t,\omega _t)\bigr ) \,\text{with}\, \bigl (f_y^\prime (\kappa _y(\omega _t)),w_y(\kappa _y(\omega _t)), p_x(\omega _t)\bigr ), \end{equation*}

where

$\omega _t\in \bigl [\Omega _{\mathrm{min}}(k_t),\Omega _{\mathrm{max}}(k_t)\bigr ]$

, fulfils (8) and (9) and hence is a feasible factor allocation. The remaining market-clearing conditions (10) and (11) in the two goods markets are satisfied as follows. For any

$\omega _t\in \bigl [\Omega _{\mathrm{min}}(k_t),\Omega _{\mathrm{max}}(k_t)\bigr ]$

, fulfils (8) and (9) and hence is a feasible factor allocation. The remaining market-clearing conditions (10) and (11) in the two goods markets are satisfied as follows. For any

$k_t$

with

$k_t$

with

$\Omega _x(k_t)\neq \Omega _y(k_t)$

, define the excess demand function for investment goods

$\Omega _x(k_t)\neq \Omega _y(k_t)$

, define the excess demand function for investment goods

$T(k_t,\cdot ) \, : \, \bigl [\Omega _{\mathrm{min}}(k_t),\Omega _{\mathrm{max}}(k_t)\bigr ]\to \mathbb R,$

by setting

$T(k_t,\cdot ) \, : \, \bigl [\Omega _{\mathrm{min}}(k_t),\Omega _{\mathrm{max}}(k_t)\bigr ]\to \mathbb R,$

by setting

\begin{equation} T(k_t,\omega )\,:\!=\, s\bigl [w_y(\kappa _y(\omega ))+f_y'(\kappa _y(\omega ))k_t\bigr ] -\ell _y(k_t,\omega )f_y(\kappa _y(\omega )). \end{equation}

\begin{equation} T(k_t,\omega )\,:\!=\, s\bigl [w_y(\kappa _y(\omega ))+f_y'(\kappa _y(\omega ))k_t\bigr ] -\ell _y(k_t,\omega )f_y(\kappa _y(\omega )). \end{equation}

Invoking Walras’ law, the next lemma provides a characterisation of temporary equilibria.

Lemma 1 (Chracterisation of temporary equilibria). Let Assumption 1 be satisfied. Then the following holds true.

-

(i) If

$\Omega _x(k_t)\not =\Omega _y(k_t)$

, then

is a temporary equilibrium if and only if there exists

\begin{equation*}\bigl (\kappa _x(\omega _t),\kappa _y(\omega _t),\ell _x(k_t,\omega _t), \ell _y(k_t,\omega _t)\bigr ) \,\text{with}\, \bigl (f_y^\prime (\kappa _y(\omega _t)),w_y(\kappa _y(\omega _t)), p_x(\omega _t)\bigr ) \end{equation*}

$\omega _t\in \bigl [\Omega _{\mathrm{min}}(k_t),\Omega _{\mathrm{max}}(k_t)\bigr ]$

such that

(17)

\begin{equation} T(k_t,\omega _t)=0. \end{equation}

-

(ii) If

$\Omega _x(k_t)=\Omega _y(k_t)$

, then

where

\begin{equation*} (k_t,k_t,1-s,s) \,\text{with}\, \bigl (\,f_y^\prime (k_t), w_y(k_t),p_x(\omega _t)\bigr ), \end{equation*}

$\omega _t=\Omega _y(k_t)$

, is a temporary equilibrium.

Lemma1 states that a temporary equilibrium is determined by a wage-rental ratio

$ \Omega _{\mathrm{min}}(k_t) latbreak{} \leq \omega _t\leq \Omega _{\mathrm{max}}(k_t)$

for which the market for investment goods clears. In the non-generic case, the labour share in the investment-goods market is

$ \Omega _{\mathrm{min}}(k_t) latbreak{} \leq \omega _t\leq \Omega _{\mathrm{max}}(k_t)$

for which the market for investment goods clears. In the non-generic case, the labour share in the investment-goods market is

$l^y_t=s$

.

$l^y_t=s$

.

Proposition 1 (Existence of temporary equilibria). Let Assumption

1

be satisfied and

$0\leq s\leq 1$

be an arbitrary but fixed savings propensity. Then there exists a uniquely determined continuous map

$0\leq s\leq 1$

be an arbitrary but fixed savings propensity. Then there exists a uniquely determined continuous map

$\Omega \, : \, \mathbb R_+\to \mathbb R_+$

with the following properties.

$\Omega \, : \, \mathbb R_+\to \mathbb R_+$

with the following properties.

-

(i) For each

$k\in \mathbb R_+$

with

$\Omega _x(k)\neq \Omega _y(k)$

, the map

$\Omega$

satisfies

where the inequalities are strict whenever

\begin{equation*} T(k,\Omega (k))=0\quad \text{and}\quad \Omega _{\mathrm{min}}(k)\leq \Omega (k)\leq \Omega _{\mathrm{max}}(k), \end{equation*}

$s\in (0,1)$

.

-

(ii) For each

$k\in \mathbb R_+$

with

$\Omega _x(k)=\Omega _y(k)$

, the map

$\Omega$

satisfies

$ \Omega (k)=\Omega _y(k).$

Since a temporary equilibrium in period

$t$

is uniquely determined by the wage-rental ratio

$t$

is uniquely determined by the wage-rental ratio

$\omega _t=\Omega (k_t)$

, will refer to

$\omega _t=\Omega (k_t)$

, will refer to

$\Omega$

as the temporary equilibrium map of the economy. We show in Lemma6, Appendix A.1 that

$\Omega$

as the temporary equilibrium map of the economy. We show in Lemma6, Appendix A.1 that

$\Omega$

is differentiable.

$\Omega$

is differentiable.

Example 2 (Temporary equilibria for CES production functions). Let

$k_t\neq \overline {k}$

, with

$k_t\neq \overline {k}$

, with

$\overline {k}$

as defined in Example

1

, be given and

$\overline {k}$

as defined in Example

1

, be given and

$\omega _t$

be the equilibrium wage-rental ratio. The equilibrium factor allocation obtains from inserting the corresponding capital-to-labour ratios (7) into the labour-share functions (15). For

$\omega _t$

be the equilibrium wage-rental ratio. The equilibrium factor allocation obtains from inserting the corresponding capital-to-labour ratios (7) into the labour-share functions (15). For

$\sigma _x\neq 1$

and

$\sigma _x\neq 1$

and

$\sigma _y\neq 1$

, the equilibrium wage and rental rate are

$\sigma _y\neq 1$

, the equilibrium wage and rental rate are

\begin{align} \begin{aligned} w_y(\kappa _y(\omega _t))&= \dfrac {a_y}{b_y}\left (b_y^{\sigma _y}\omega _t^{\sigma _y-1}+(1-b_y)^{\sigma _y}\right )^\frac {1}{\sigma _y-1} \\ f_y^\prime (\kappa _y(\omega _t))&= \dfrac {a_y}{b_y}\left (b_y^{\sigma _y}+(1-b_y)^{\sigma _y}\omega _t^{1-\sigma _y}\right )^\frac {1}{\sigma _y-1}. \end{aligned} \end{align}

\begin{align} \begin{aligned} w_y(\kappa _y(\omega _t))&= \dfrac {a_y}{b_y}\left (b_y^{\sigma _y}\omega _t^{\sigma _y-1}+(1-b_y)^{\sigma _y}\right )^\frac {1}{\sigma _y-1} \\ f_y^\prime (\kappa _y(\omega _t))&= \dfrac {a_y}{b_y}\left (b_y^{\sigma _y}+(1-b_y)^{\sigma _y}\omega _t^{1-\sigma _y}\right )^\frac {1}{\sigma _y-1}. \end{aligned} \end{align}

The consumption-goods price is

\begin{equation} p_x(\omega _t)= \frac {\frac {a_y}{b_y}\Bigl (\alpha _y^{\sigma _y}+(1-b_y)^{\sigma _y}\omega _t^{1-\sigma _y} \Bigr )^\frac {1}{\sigma _y-1}} {\frac {a_x}{b_x}\Bigl (b_x^{\sigma _x}+(1-b_x)^{\sigma _x}\omega _t^{1-\sigma _x} \Bigr )^\frac {1}{\sigma _x-1}}. \end{equation}

\begin{equation} p_x(\omega _t)= \frac {\frac {a_y}{b_y}\Bigl (\alpha _y^{\sigma _y}+(1-b_y)^{\sigma _y}\omega _t^{1-\sigma _y} \Bigr )^\frac {1}{\sigma _y-1}} {\frac {a_x}{b_x}\Bigl (b_x^{\sigma _x}+(1-b_x)^{\sigma _x}\omega _t^{1-\sigma _x} \Bigr )^\frac {1}{\sigma _x-1}}. \end{equation}

2.3 Capital accumulation

Applying the identity (2) twice, aggregate factor income per capita at any

$(k,\omega )\in \mathbb R_{++}^2$

satisfies

$(k,\omega )\in \mathbb R_{++}^2$

satisfies

\begin{align} w_y(\kappa _y(\omega ))+f_y^\prime (\kappa _y(\omega ))k & =[\omega +k]f_y^\prime (\kappa _y(\omega )) =\left [\frac {\omega +k}{\omega +\kappa _y(\omega )}\right ] f_y(\kappa _y(\omega )). \end{align}

\begin{align} w_y(\kappa _y(\omega ))+f_y^\prime (\kappa _y(\omega ))k & =[\omega +k]f_y^\prime (\kappa _y(\omega )) =\left [\frac {\omega +k}{\omega +\kappa _y(\omega )}\right ] f_y(\kappa _y(\omega )). \end{align}

The economy’s propensity to invest in a temporary equilibrium may now be defined as a function of the economy-wide capital intensity

$\mathcal S\, : \, \mathbb R_+\to \mathbb R_+$

by settingFootnote

4

$\mathcal S\, : \, \mathbb R_+\to \mathbb R_+$

by settingFootnote

4

\begin{equation} \mathcal S(k)\,:\!=\,s\left [ \frac {\Omega (k)+k}{\Omega (k)+\kappa _y(\Omega (k))}\right ]. \end{equation}

\begin{equation} \mathcal S(k)\,:\!=\,s\left [ \frac {\Omega (k)+k}{\Omega (k)+\kappa _y(\Omega (k))}\right ]. \end{equation}

Market clearing requires the propensity to invest to be equal to the labour share of the investment-goods sector, so that

\begin{align} \mathcal S(k)= \begin{cases} \ell _y(k,\Omega (k))&\text{if }\,\Omega _x(k)\neq \Omega _y(k) \\ s&\text{if }\,\Omega _x(k)=\Omega _y(k) \end{cases}. \end{align}

\begin{align} \mathcal S(k)= \begin{cases} \ell _y(k,\Omega (k))&\text{if }\,\Omega _x(k)\neq \Omega _y(k) \\ s&\text{if }\,\Omega _x(k)=\Omega _y(k) \end{cases}. \end{align}

Assuming that capital depreciates at the rate

$0 \leq \delta \leq 1$

and that labour supply grows at the rate

$0 \leq \delta \leq 1$

and that labour supply grows at the rate

$n\gt -1$

so that

$n\gt -1$

so that

$L_{t+1}=(1+n)L_t$

, the capital-to-labour ratio in period

$L_{t+1}=(1+n)L_t$

, the capital-to-labour ratio in period

$t+1$

is equal to the sum of depreciated capital and investments in period

$t+1$

is equal to the sum of depreciated capital and investments in period

$t$

. Given an initial capital-to-labour ratio

$t$

. Given an initial capital-to-labour ratio

$k_0\geq 0$

, the evolution of the capital-to-labour ratios

$k_0\geq 0$

, the evolution of the capital-to-labour ratios

$k_t=\frac {K_t}{L_t}$

is thus governed by the time-one map

$k_t=\frac {K_t}{L_t}$

is thus governed by the time-one map

$G\, : \, \mathbb R_{+}\to \mathbb R_{+}$

, defined by

$G\, : \, \mathbb R_{+}\to \mathbb R_{+}$

, defined by

\begin{equation} k_{t+1}=G(k_t)\,:\!=\, \tfrac {1}{1+n} \bigl [(1-\delta )k_t +\mathcal S(k_t)f_y(\kappa _y(\Omega (k_t)))\bigr ],\quad t\geq 0. \end{equation}

\begin{equation} k_{t+1}=G(k_t)\,:\!=\, \tfrac {1}{1+n} \bigl [(1-\delta )k_t +\mathcal S(k_t)f_y(\kappa _y(\Omega (k_t)))\bigr ],\quad t\geq 0. \end{equation}

We will show next that our parsimonious growth model (23) allows for multiple steady states, cycles of any order, and complex dynamics. Since the maps

$f_y$

,

$f_y$

,

$\kappa _y$

, and

$\kappa _y$

, and

$\Omega$

are all strictly increasing, all non-linearities of the map

$\Omega$

are all strictly increasing, all non-linearities of the map

$G$

must originate from the economy’s propensity to invest

$G$

must originate from the economy’s propensity to invest

$\mathcal S$

.

$\mathcal S$

.

Lemma 2 (Properties of

$\mathcal S$

). The propensity to invest

$\mathcal S$

). The propensity to invest

$\mathcal S$

takes the form

$\mathcal S$

takes the form

\begin{equation} \mathcal S(k)=\frac {s}{s+(1-s)h(\Omega (k))},\quad k\in \mathbb R_{++}, \end{equation}

\begin{equation} \mathcal S(k)=\frac {s}{s+(1-s)h(\Omega (k))},\quad k\in \mathbb R_{++}, \end{equation}

where

$h\, : \, \mathbb R_{++}\to \mathbb R_+$

is defined by

$h\, : \, \mathbb R_{++}\to \mathbb R_+$

is defined by

\begin{equation} h(\omega )\,:\!=\,\frac {\omega +\kappa _y(\omega )}{\omega +\kappa _x(\omega )}. \end{equation}

\begin{equation} h(\omega )\,:\!=\,\frac {\omega +\kappa _y(\omega )}{\omega +\kappa _x(\omega )}. \end{equation}

Moreover,

$\mathcal S^\prime (k)\lt 0$

if and only if

$\mathcal S^\prime (k)\lt 0$

if and only if

$h^\prime (\Omega (k))\gt 0$

.

$h^\prime (\Omega (k))\gt 0$

.

In the proof of Lemma2 in Appendix A.1, we will show with equation (50) that the function

$h$

may be rewritten as

$h$

may be rewritten as

\begin{equation} h(\omega )=\frac {f_y(\kappa _y(\omega ))}{ p_x(\omega ) f_x(\kappa _x(\omega ))} =\frac {1-\varepsilon _x(\omega )}{1-\varepsilon _y(\omega )}, \quad \omega \in \mathbb R_{++}. \end{equation}

\begin{equation} h(\omega )=\frac {f_y(\kappa _y(\omega ))}{ p_x(\omega ) f_x(\kappa _x(\omega ))} =\frac {1-\varepsilon _x(\omega )}{1-\varepsilon _y(\omega )}, \quad \omega \in \mathbb R_{++}. \end{equation}

Thus, Lemma2 implies that the propensity to invest is a decreasing function of the economy-wide capital-to-labour ratio whenever the investment-good output

$f_y(\kappa _y(\omega ))$

increases faster with an increase in the wage-rental ratios than the value of the consumption-good output

$f_y(\kappa _y(\omega ))$

increases faster with an increase in the wage-rental ratios than the value of the consumption-good output

$p_x(\omega )f_x(\kappa _x(\omega ))$

. Stated differently, a price effect is responsible for a decreasing propensity to invest. It follows from (22) that the equilibrium labour-share of the investment-goods sector must then be a non-increasing function of the capital-to-labour ratio.Footnote

5

The classical one-sector Solow–Swan growth model excludes such a nonlinearity because the propensity to invest is constant. With two sectors, investment is solely generated out of income earned in the investment-goods sector and (20) shows that factor incomes no longer add up to output of that sector. Therefore, a negative effect of an increase in

$p_x(\omega )f_x(\kappa _x(\omega ))$

. Stated differently, a price effect is responsible for a decreasing propensity to invest. It follows from (22) that the equilibrium labour-share of the investment-goods sector must then be a non-increasing function of the capital-to-labour ratio.Footnote

5

The classical one-sector Solow–Swan growth model excludes such a nonlinearity because the propensity to invest is constant. With two sectors, investment is solely generated out of income earned in the investment-goods sector and (20) shows that factor incomes no longer add up to output of that sector. Therefore, a negative effect of an increase in

$k$

on capital income may dominate the positive effect on labour income.

$k$

on capital income may dominate the positive effect on labour income.

Example 3 (Propensity to invest for CES production functions). Suppose that both production functions are of the CES type specified in Example 1 . Inserting the capital intensities (7) into (25) yields

\begin{equation} h(\omega ) =\frac {1+\left (\frac {b_y}{1-b_y}\right )^{\sigma _y}\omega ^{\sigma _y-1}} {1+\left (\frac {b_x}{1-b_x}\right )^{\sigma _x}\omega ^{\sigma _x-1}}. \end{equation}

\begin{equation} h(\omega ) =\frac {1+\left (\frac {b_y}{1-b_y}\right )^{\sigma _y}\omega ^{\sigma _y-1}} {1+\left (\frac {b_x}{1-b_x}\right )^{\sigma _x}\omega ^{\sigma _x-1}}. \end{equation}

Since by Lemma

6

, Appendix A.1 the temporary equilibrium map

$\Omega$

is strictly increasing, it follows from (27) that for

$\Omega$

is strictly increasing, it follows from (27) that for

$\sigma _x\lt 1\leq \sigma _y$

, the propensity to invest

$\sigma _x\lt 1\leq \sigma _y$

, the propensity to invest

$\mathcal S$

is strictly decreasing with

$\mathcal S$

is strictly decreasing with

$\lim _{k\to 0}\mathcal S(k)=1$

. This case, therefore, has the potential for non-monotonic time-one maps

$\lim _{k\to 0}\mathcal S(k)=1$

. This case, therefore, has the potential for non-monotonic time-one maps

$G$

. For

$G$

. For

$\sigma _x\geq 1\geq \sigma _y$

, the propensity to invest

$\sigma _x\geq 1\geq \sigma _y$

, the propensity to invest

$\mathcal{S}$

is non-decreasing. The corresponding time-one maps

$\mathcal{S}$

is non-decreasing. The corresponding time-one maps

$G$

will therefore be strictly increasing. In Section 3 below, it will be shown that

$G$

will therefore be strictly increasing. In Section 3 below, it will be shown that

$G$

is strictly increasing whenever

$G$

is strictly increasing whenever

$\sigma _x\geq 1$

. The analysis of the remaining case

$\sigma _x\geq 1$

. The analysis of the remaining case

$\sigma _x,\sigma _y\lt 1$

is tedious and must be considered elsewhere.

$\sigma _x,\sigma _y\lt 1$

is tedious and must be considered elsewhere.

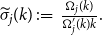

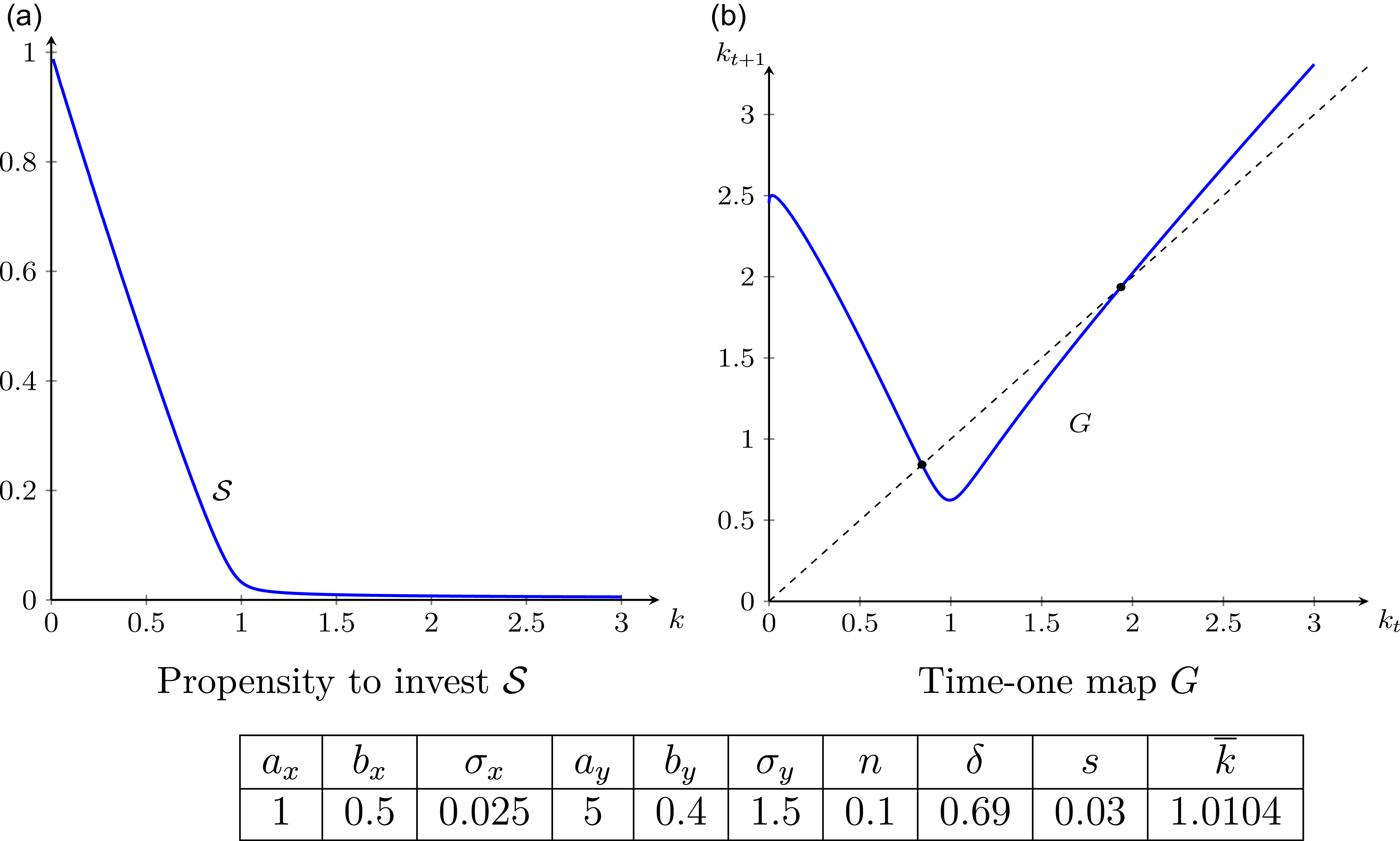

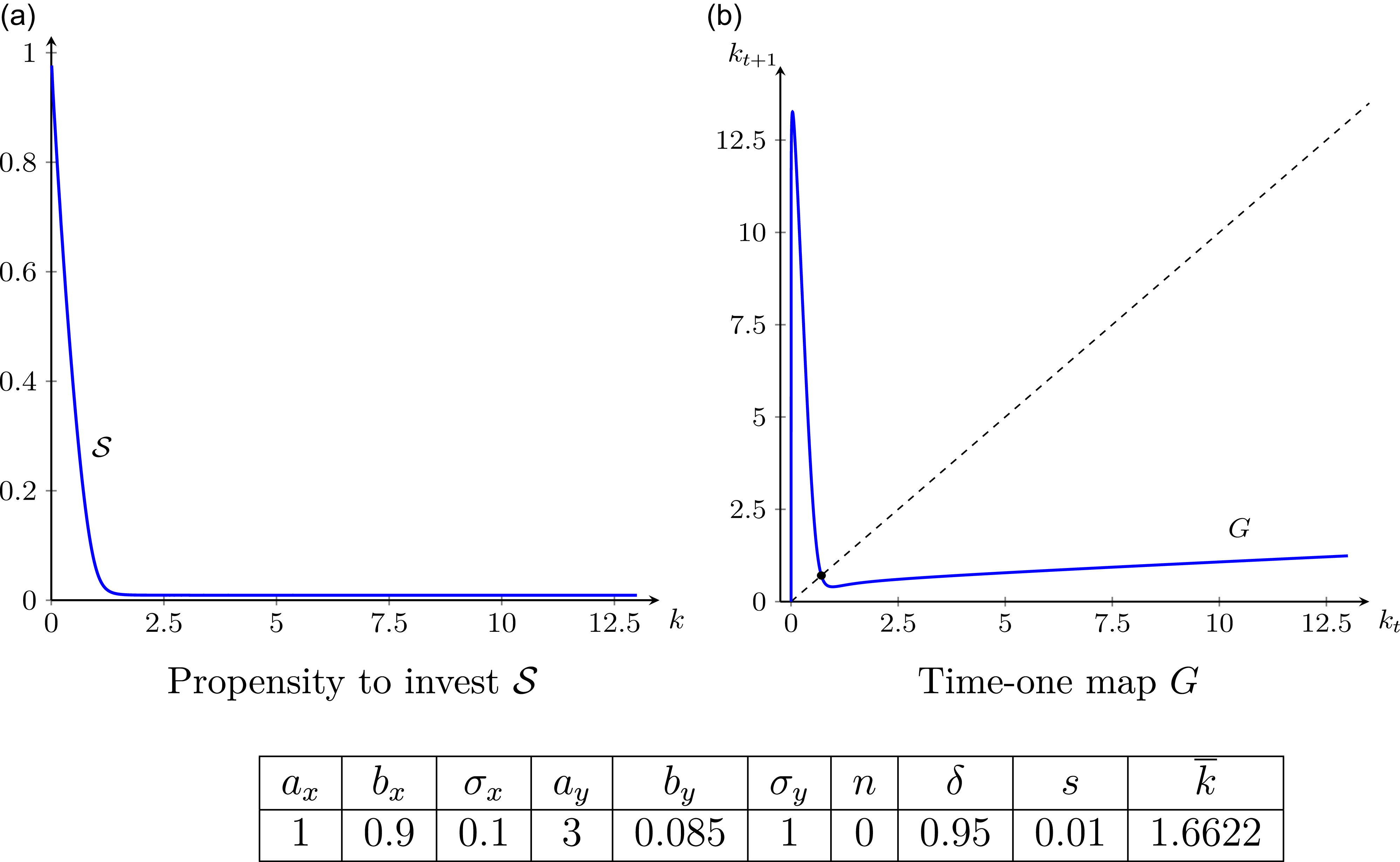

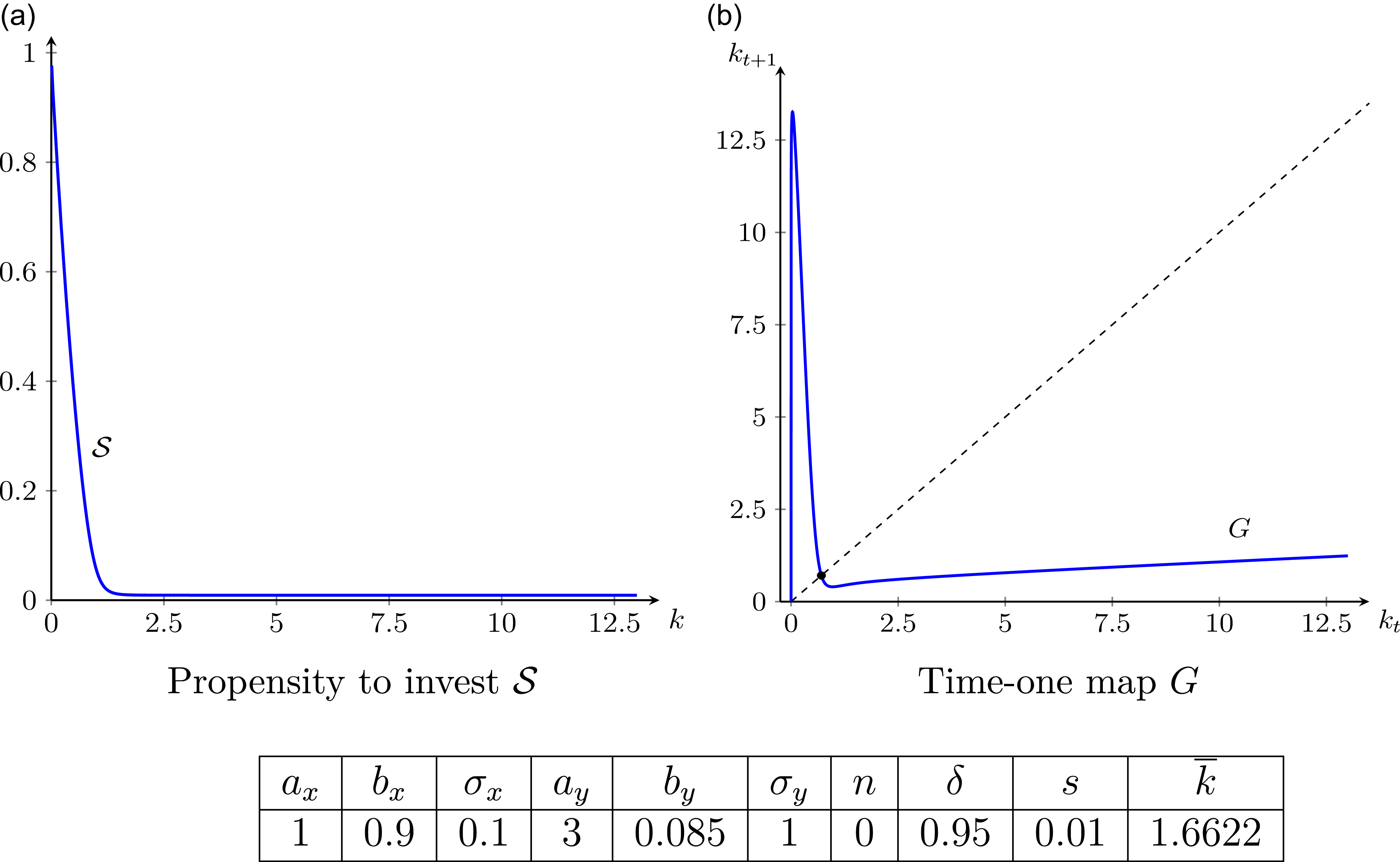

Example3 is illustrated in Figures 1–3 with three specific parametrisations of CES production functions. These figures show that non-monotonic time-one maps

$G$

obtain whenever

$G$

obtain whenever

$\mathcal S$

is decreasing sufficiently fast. Figures 1 and 2 portray two parametrisations with non-monotonic time-one maps

$\mathcal S$

is decreasing sufficiently fast. Figures 1 and 2 portray two parametrisations with non-monotonic time-one maps

$G$

; Figure 3 portrays a parametrisation in which

$G$

; Figure 3 portrays a parametrisation in which

$\mathcal S$

may be decreasing while

$\mathcal S$

may be decreasing while

$G$

is nevertheless increasing. Since in all three cases

$G$

is nevertheless increasing. Since in all three cases

$\sigma _x\lt \sigma _y$

, we know from Example1 that the investment-goods sector is more capital intensive for all

$\sigma _x\lt \sigma _y$

, we know from Example1 that the investment-goods sector is more capital intensive for all

$k$

above the critical value

$k$

above the critical value

$\overline k$

. The figures suggest that

$\overline k$

. The figures suggest that

$G$

is increasing for

$G$

is increasing for

$k\gt \overline k$

in all three cases.

$k\gt \overline k$

in all three cases.

Case A. CES production functions,

$\sigma _x\lt 1\lt \sigma _y$

.

$\sigma _x\lt 1\lt \sigma _y$

.

Case B. CES production functions,

$\sigma _x\lt \sigma _y=1$

.

$\sigma _x\lt \sigma _y=1$

.

3. Steady states and long-run behaviour

In this section, we will investigate the existence, uniqueness, and stability of steady states and explore the scope for unbounded growth and development traps. To rule out uninteresting scenarios, we assume throughout the remainder of this article that

$n+\delta \gt 0$

.

$n+\delta \gt 0$

.

A steady state is a capital-to-labour ratio

$k^\ast$

that satisfies

$k^\ast$

that satisfies

$k^*=G(k^*)$

. It follows from (23) that positive steady states

$k^*=G(k^*)$

. It follows from (23) that positive steady states

$k^*\gt 0$

are solutions to the equation

$k^*\gt 0$

are solutions to the equation

\begin{equation} \phi (k)=\frac {n+\delta }{s}, \end{equation}

\begin{equation} \phi (k)=\frac {n+\delta }{s}, \end{equation}

where

$\phi\, : \, \mathbb{R}_{++} \to \mathbb{R}_{+}$

is defined by

$\phi\, : \, \mathbb{R}_{++} \to \mathbb{R}_{+}$

is defined by

\begin{equation} \phi (k)\,:\!=\, \frac {\mathcal S(k)}{s} \cdot \frac {f_y\bigl (\kappa _y(\Omega (k))\bigr )}{k}. \end{equation}

\begin{equation} \phi (k)\,:\!=\, \frac {\mathcal S(k)}{s} \cdot \frac {f_y\bigl (\kappa _y(\Omega (k))\bigr )}{k}. \end{equation}

The intermediate-value theorem guarantees the existence of

$0\lt k^*\lt \infty$

if

$0\lt k^*\lt \infty$

if

\begin{equation} \lim _{k\to \infty } \phi (k) \lt \tfrac {n+\delta }{s}\lt \lim _{k\to 0} \phi (k). \end{equation}

\begin{equation} \lim _{k\to \infty } \phi (k) \lt \tfrac {n+\delta }{s}\lt \lim _{k\to 0} \phi (k). \end{equation}

In the proof of Theorem1 in Appendix A.2, it will be shown that

\begin{equation} f_y^\prime (\kappa _y(\Omega (k)))\lt \phi (k)\lt \frac {1}{s}\frac {f_y(\kappa _y(\Omega (k)))}{\kappa _y(\Omega (k))} \quad \text{for all }\,k\in \mathbb R_{++}. \end{equation}

\begin{equation} f_y^\prime (\kappa _y(\Omega (k)))\lt \phi (k)\lt \frac {1}{s}\frac {f_y(\kappa _y(\Omega (k)))}{\kappa _y(\Omega (k))} \quad \text{for all }\,k\in \mathbb R_{++}. \end{equation}

Since by Assumption1,

$\lim _{\omega \to 0}\kappa _y(\omega )=0$

and

$\lim _{\omega \to 0}\kappa _y(\omega )=0$

and

$\lim _{\omega \to \infty }\kappa _y(\omega )=\infty$

, and by Lemma6, Appendix A.1,

$\lim _{\omega \to \infty }\kappa _y(\omega )=\infty$

, and by Lemma6, Appendix A.1,

$\lim _{k\to 0}\Omega (k)=0$

and

$\lim _{k\to 0}\Omega (k)=0$

and

$\lim _{k\to \infty }\Omega (k)=\infty$

, the following existence result is intuitively clear.

$\lim _{k\to \infty }\Omega (k)=\infty$

, the following existence result is intuitively clear.

Case C. CES production functions,

$\sigma _x\lt \sigma _y\lt 1$

.

$\sigma _x\lt \sigma _y\lt 1$

.

Theorem 1 (Existence of positive steady states). Let Assumption 1 be satisfied and assume that

\begin{equation*} (i)\quad \lim _{k\to 0} f'_y(k) \gt \frac {n+\delta }{s} \qquad \mbox{and} \qquad (ii)\quad \lim _{k\to \infty } \frac {f_y(k)}{k} \lt n+\delta . \end{equation*}

\begin{equation*} (i)\quad \lim _{k\to 0} f'_y(k) \gt \frac {n+\delta }{s} \qquad \mbox{and} \qquad (ii)\quad \lim _{k\to \infty } \frac {f_y(k)}{k} \lt n+\delta . \end{equation*}

Then there exists a positive steady state

$k^\ast =G(k^\ast )\gt 0$

.

$k^\ast =G(k^\ast )\gt 0$

.

The existence conditions in Theorem1 are sufficient but not necessary. They are fulfilled, in particular, by all production functions

$f_y$

that satisfy both Inada conditions.

$f_y$

that satisfy both Inada conditions.

Example 4 (Existence of positive steady states for CES production functions). The limits of the marginal product of capital

$f_j^\prime$

for CES production functions are

$f_j^\prime$

for CES production functions are

\begin{align} \lim _{k\to 0} f'_j(k) = \left \{ \begin{array}{l@{\quad \mbox{if}\ }l} a_j b_j^{\frac {1}{\sigma _j-1}} & \sigma _j \lt 1 \\ \infty & \sigma _j \geq 1 \end{array} \right . \, \text{and}\quad \lim _{k\to \infty } f'_j(k) = \left \{ \begin{array}{l@{\quad \mbox{if}\ }l} 0 & \sigma _j \leq 1 \\ a_j b_j^{\frac {1}{\sigma _j-1}} & \sigma _j \gt 1 \end{array} \right . . \end{align}

\begin{align} \lim _{k\to 0} f'_j(k) = \left \{ \begin{array}{l@{\quad \mbox{if}\ }l} a_j b_j^{\frac {1}{\sigma _j-1}} & \sigma _j \lt 1 \\ \infty & \sigma _j \geq 1 \end{array} \right . \, \text{and}\quad \lim _{k\to \infty } f'_j(k) = \left \{ \begin{array}{l@{\quad \mbox{if}\ }l} 0 & \sigma _j \leq 1 \\ a_j b_j^{\frac {1}{\sigma _j-1}} & \sigma _j \gt 1 \end{array} \right . . \end{align}

Since

$\lim _{k\to \infty }f(k)/k=\lim _{k\to \infty }f^\prime (k)$

, Theorem

1

is applicable.

$\lim _{k\to \infty }f(k)/k=\lim _{k\to \infty }f^\prime (k)$

, Theorem

1

is applicable.

The examples in Figures 1 and 3 suggest that there must exist scenarios with multiple positive steady states. Condition (28) implies that a positive steady state is uniquely determined if

$\phi$

is strictly decreasing at any steady state

$\phi$

is strictly decreasing at any steady state

$k^\ast \gt 0$

. It turns out that the relative sizes of the production elasticities and the elasticity of factor substitution in producing consumption goods detemine the uniqueness of positive steady states. The following theorem generalises a well-known result in Drandakis (Reference Drandakis1963).

$k^\ast \gt 0$

. It turns out that the relative sizes of the production elasticities and the elasticity of factor substitution in producing consumption goods detemine the uniqueness of positive steady states. The following theorem generalises a well-known result in Drandakis (Reference Drandakis1963).

Theorem 2 (Uniqueness of positive steady states). Under the hypotheses of Theorem

1

, a positive steady state of

$G$

is uniquely determined if each

$G$

is uniquely determined if each

$k^\ast =G(k^\ast )\gt 0$

with

$k^\ast =G(k^\ast )\gt 0$

with

$\omega ^\ast =\Omega (k^\ast )$

satisfies either

$\omega ^\ast =\Omega (k^\ast )$

satisfies either

\begin{equation*} (i)\quad \sigma _x(\omega ^\ast ) \geq \varepsilon _y(\omega ^\ast ) \quad \mbox{or}\quad (ii)\quad \varepsilon _x(\omega ^\ast )\geq \varepsilon _y(\omega ^\ast ). \end{equation*}

\begin{equation*} (i)\quad \sigma _x(\omega ^\ast ) \geq \varepsilon _y(\omega ^\ast ) \quad \mbox{or}\quad (ii)\quad \varepsilon _x(\omega ^\ast )\geq \varepsilon _y(\omega ^\ast ). \end{equation*}

Since

$f_y$

is strictly concave, Condition (i) is automatically satisfied if the elasticity of substitution in the consumption-goods sector is always larger than unity, that is, if

$f_y$

is strictly concave, Condition (i) is automatically satisfied if the elasticity of substitution in the consumption-goods sector is always larger than unity, that is, if

$\sigma _x(\omega ) \geq 1$

for all

$\sigma _x(\omega ) \geq 1$

for all

$\omega \gt 0$

. This case obtains for all CES production functions with

$\omega \gt 0$

. This case obtains for all CES production functions with

$\sigma _x\geq 1$

and, in particular, for all Cobb–Douglas production functions.

$\sigma _x\geq 1$

and, in particular, for all Cobb–Douglas production functions.

Cycles and complex dynamics requires the time-one map

$G$

to be decreasing around a steady state. To address the question of whether or not such time-one maps are possible, we define an auxiliary function

$G$

to be decreasing around a steady state. To address the question of whether or not such time-one maps are possible, we define an auxiliary function

$g\, : \, \mathbb R_+\to \mathbb R$

by setting

$g\, : \, \mathbb R_+\to \mathbb R$

by setting

\begin{equation} g(\omega )\,:\!=\, \varepsilon _x(\omega )\bigl [1-\sigma _x(\omega )\bigr ]-\varepsilon _y(\omega ). \end{equation}

\begin{equation} g(\omega )\,:\!=\, \varepsilon _x(\omega )\bigl [1-\sigma _x(\omega )\bigr ]-\varepsilon _y(\omega ). \end{equation}

Lemma 3 (Monotonicity of

$G$

). Let Assumption

1

be satisfied. Then

$G$

). Let Assumption

1

be satisfied. Then

$G^\prime (k)\gt 0$

if

$G^\prime (k)\gt 0$

if

$\omega =\Omega (k)$

satisfies

$\omega =\Omega (k)$

satisfies

\begin{equation} g(\omega ) \lt \left (\frac {s}{1-s}\right ) \frac {\sigma _y(\omega )\varepsilon _y(\omega )[1-\varepsilon _y(\omega )]}{1-\varepsilon _x(\omega )}. \end{equation}

\begin{equation} g(\omega ) \lt \left (\frac {s}{1-s}\right ) \frac {\sigma _y(\omega )\varepsilon _y(\omega )[1-\varepsilon _y(\omega )]}{1-\varepsilon _x(\omega )}. \end{equation}

Specifically, Condition (34) holds if one of the following two conditions is satisfied: either

\begin{equation*} (i)\quad \sigma _x(\omega ) \geq 1 \quad \text{or} \quad (ii)\quad \varepsilon _y(\omega ) \geq \varepsilon _x(\omega ). \end{equation*}

\begin{equation*} (i)\quad \sigma _x(\omega ) \geq 1 \quad \text{or} \quad (ii)\quad \varepsilon _y(\omega ) \geq \varepsilon _x(\omega ). \end{equation*}

If, in addition, capital depreciates fully,

$\delta =1$

, then Condition (34) is also necessary.

$\delta =1$

, then Condition (34) is also necessary.

Since

$g$

is bounded from above and the r.h.s. in (34) is non-negative, Condition (34) is satisfied whenever the savings propensity

$g$

is bounded from above and the r.h.s. in (34) is non-negative, Condition (34) is satisfied whenever the savings propensity

$s$

is sufficiently large or if

$s$

is sufficiently large or if

$g(\omega )\lt 0$

. Since

$g(\omega )\lt 0$

. Since

$\kappa _y(\omega )\geq \kappa _x(\omega )$

if and only if

$\kappa _y(\omega )\geq \kappa _x(\omega )$

if and only if

$\varepsilon _y(\omega )\geq \varepsilon _x(\omega )$

, Condition (ii) implies that

$\varepsilon _y(\omega )\geq \varepsilon _x(\omega )$

, Condition (ii) implies that

$G$

is increasing whenever the investment-goods sector is more capital intensive. In particular, if the consumption-goods sector is governed by a CES production function with

$G$

is increasing whenever the investment-goods sector is more capital intensive. In particular, if the consumption-goods sector is governed by a CES production function with

$\sigma _x\geq 1$

, it follows from Lemma3 that the dynamics of the model are monotone.

$\sigma _x\geq 1$

, it follows from Lemma3 that the dynamics of the model are monotone.

The following stability result is an immediate consequence of Lemma3.

Theorem 3 (Asymptotic stability of positive steady states). Under the hypotheses of Theorem

1

, a positive steady state

$k^*\gt 0$

of

$k^*\gt 0$

of

$G$

is asymptotically stable if

$G$

is asymptotically stable if

$\omega ^\ast =\Omega (k^\ast )$

satisfies one of the following conditions: either

$\omega ^\ast =\Omega (k^\ast )$

satisfies one of the following conditions: either

\begin{equation*} (i)\quad \sigma _x(\omega ^\ast ) \geq 1 \quad \text{or} \quad (ii)\quad \varepsilon _y(\omega ^\ast )\geq \varepsilon _x(\omega ^\ast ). \end{equation*}

\begin{equation*} (i)\quad \sigma _x(\omega ^\ast ) \geq 1 \quad \text{or} \quad (ii)\quad \varepsilon _y(\omega ^\ast )\geq \varepsilon _x(\omega ^\ast ). \end{equation*}

If, in addition,

$\sigma _x(\omega )\geq 1$

for all

$\sigma _x(\omega )\geq 1$

for all

$\omega \gt 0$

, then

$\omega \gt 0$

, then

$k^\ast$

is asymptotically stable, globally on

$k^\ast$

is asymptotically stable, globally on

$\mathbb R_{++}$

.

$\mathbb R_{++}$

.

Theorem3 implies that cycles and complex behaviour require a steady state

$k^\ast$

in which the substitution elasticity of the consumption-goods sector is less than unity or the consumption-goods sector is more capital intensive than the investment-goods sector. The second condition is well known, see Boldrin and Deneckere (Reference Boldrin and Deneckere1990) and Galor (Reference Galor1992).

$k^\ast$

in which the substitution elasticity of the consumption-goods sector is less than unity or the consumption-goods sector is more capital intensive than the investment-goods sector. The second condition is well known, see Boldrin and Deneckere (Reference Boldrin and Deneckere1990) and Galor (Reference Galor1992).

Example 5 (Monotonicity with CES production functions). We analyse the shape of

$G$

in Case A and in Case B, depicted in Figures

1

and

2

, respectively. Since

$G$

in Case A and in Case B, depicted in Figures

1

and

2

, respectively. Since

$\sigma _x\lt \sigma _y$

, the investment-goods sector is more capital intensive for all

$\sigma _x\lt \sigma _y$

, the investment-goods sector is more capital intensive for all

$k\gt \overline {k}$

, so that in both cases, the time-one map

$k\gt \overline {k}$

, so that in both cases, the time-one map

$G$

is increasing for all

$G$

is increasing for all

$k\gt \overline {k}$

. Inserting the expressions (68) provided in Appendix A.3

, the map (33) takes the form

$k\gt \overline {k}$

. Inserting the expressions (68) provided in Appendix A.3

, the map (33) takes the form

\begin{equation*} g(\omega )=\frac {1-\sigma _x} {1+\left (\frac {1-b_x}{b_x}\right )^{\sigma _x}\omega ^{1-\sigma _x}} - \frac {1} {1+\left (\frac {1-b_y}{b_y}\right )^{\sigma _y}\omega ^{1-\sigma _y}} \end{equation*}

\begin{equation*} g(\omega )=\frac {1-\sigma _x} {1+\left (\frac {1-b_x}{b_x}\right )^{\sigma _x}\omega ^{1-\sigma _x}} - \frac {1} {1+\left (\frac {1-b_y}{b_y}\right )^{\sigma _y}\omega ^{1-\sigma _y}} \end{equation*}

and the r.h.s. of (34) the form

\begin{equation*} \chi (\omega )= \frac {\frac {s}{1-s}\,\sigma _y\left [1+\left (\frac {b_x}{1-b_x}\right )^{\sigma _x}\omega ^{\sigma _x-1}\right ]} {2+\left (\frac {1-b_y}{b_y}\right )^{\sigma _y}\omega ^{1-\sigma _y} +\left (\frac {b_y}{1-b_y}\right )^{\sigma _y}\omega ^{\sigma _y-1}}. \end{equation*}

\begin{equation*} \chi (\omega )= \frac {\frac {s}{1-s}\,\sigma _y\left [1+\left (\frac {b_x}{1-b_x}\right )^{\sigma _x}\omega ^{\sigma _x-1}\right ]} {2+\left (\frac {1-b_y}{b_y}\right )^{\sigma _y}\omega ^{1-\sigma _y} +\left (\frac {b_y}{1-b_y}\right )^{\sigma _y}\omega ^{\sigma _y-1}}. \end{equation*}

For

$\sigma _x\lt 1\leq \sigma _y$

, the map

$\sigma _x\lt 1\leq \sigma _y$

, the map

$g$

is strictly decreasing with

$g$

is strictly decreasing with

$\lim _{\omega \to 0}g(\omega )\leq 1-\sigma _x$

, while

$\lim _{\omega \to 0}g(\omega )\leq 1-\sigma _x$

, while

$\lim _{\omega \to 0}\chi (\omega )=\infty$

if, in addition,

$\lim _{\omega \to 0}\chi (\omega )=\infty$

if, in addition,

$\sigma _x+\sigma _y\lt 2$

. This shows that in both cases, the time-one maps must be increasing in a neighbourhood of the origin.

$\sigma _x+\sigma _y\lt 2$

. This shows that in both cases, the time-one maps must be increasing in a neighbourhood of the origin.

A development trap occurs if the origin is an asymptotically stable steady state, so that there exists

$\underline k\gt 0$

such that any growth path

$\underline k\gt 0$

such that any growth path

$k_{t+1}=G(k_t)$

,

$k_{t+1}=G(k_t)$

,

$t=0,1,\ldots$

starting from some

$t=0,1,\ldots$

starting from some

$k_0\lt \underline k$

converges to

$k_0\lt \underline k$

converges to

$0$

. An economy admits unbounded growth if there exists

$0$

. An economy admits unbounded growth if there exists

$\underline k\geq 0$

such that the capital-to-labour ratios

$\underline k\geq 0$

such that the capital-to-labour ratios

$k_{t+1}=G(k_t)$

,

$k_{t+1}=G(k_t)$

,

$t=0,1,\ldots$

starting from some

$t=0,1,\ldots$

starting from some

$k_0\geq \underline k$

become arbitrarily large. Since

$k_0\geq \underline k$

become arbitrarily large. Since

\begin{equation} G(k) \gtreqless k \quad \iff \quad \phi (k) \gtreqless \dfrac {n+\delta }{s}, \end{equation}

\begin{equation} G(k) \gtreqless k \quad \iff \quad \phi (k) \gtreqless \dfrac {n+\delta }{s}, \end{equation}

a necessary condition for the existence of a development trap is

$\lim _{k\to 0} \phi (k)\lt \frac {n+\delta }{s}$

, while a necessary condition for unbounded growth is

$\lim _{k\to 0} \phi (k)\lt \frac {n+\delta }{s}$

, while a necessary condition for unbounded growth is

$\lim _{k\to \infty } \phi (k)\gt \frac {n+\delta }{s}$

. Observe that the two boundary functions in (31) are strictly decreasing. Together with (35), this observation yields two conditions under which no positive steady state exists.

$\lim _{k\to \infty } \phi (k)\gt \frac {n+\delta }{s}$

. Observe that the two boundary functions in (31) are strictly decreasing. Together with (35), this observation yields two conditions under which no positive steady state exists.

Lemma 4. Let Assumption 1 be satisfied. Then the following holds true.

-

(i) Global development trap. If

$\lim _{k\to 0}f_y(k)/k\lt n+\delta$

, then

$G(k)\lt k$

for all

$k\gt 0$

. -

(ii) Global unbounded growth. If

$\lim _{k\to \infty }f_y^\prime (k)\gt \frac {n+\delta }{s}$

, then

$G(k)\gt k$

for all

$k\gt 0$

.

4. Qualitative dynamics for CES technologies

In this section, we illustrate the theoretical results of Section 3 with CES production functions. Analytical results are developed in Section 4.1, numerical results of a variety of simulation exercises are presented in Section 4.2.

4.1 Steady states, development trap, and unbounded growth

For CES production functions, the map

$\phi$

defined in (29) takes an analytically tractable form so that all theoretical results of Section 3 can be applied. The limits for the marginal products (32) suggest to distinguish between three cases:

$\phi$

defined in (29) takes an analytically tractable form so that all theoretical results of Section 3 can be applied. The limits for the marginal products (32) suggest to distinguish between three cases:

$\sigma _y\lt 1$

,

$\sigma _y\lt 1$

,

$\sigma _y\gt 1$

, and

$\sigma _y\gt 1$

, and

$\sigma _y=1$

. For

$\sigma _y=1$

. For

$\sigma _y\neq 1$

, two mutually exclusive sets of model parameters

$\sigma _y\neq 1$

, two mutually exclusive sets of model parameters

$(b_x,\sigma _x,a_y,b_y,\sigma _y,n,\delta ,s)$

turn out to be crucial. First, the case

$(b_x,\sigma _x,a_y,b_y,\sigma _y,n,\delta ,s)$

turn out to be crucial. First, the case

\begin{align} \frac {n+\delta }{a_yb_y^\frac {1}{\sigma _y-1}} \lt \begin{cases} s&\text{if }\, \sigma _x\lt 1 \\ \dfrac {s}{(1-b_x)s+b_x} &\text{if }\,\sigma _x=1 \\ 1&\text{if }\, \sigma _x\gt 1 \end{cases}. \end{align}

\begin{align} \frac {n+\delta }{a_yb_y^\frac {1}{\sigma _y-1}} \lt \begin{cases} s&\text{if }\, \sigma _x\lt 1 \\ \dfrac {s}{(1-b_x)s+b_x} &\text{if }\,\sigma _x=1 \\ 1&\text{if }\, \sigma _x\gt 1 \end{cases}. \end{align}

Second, the case

\begin{align} \frac {n+\delta }{a_yb_y^\frac {1}{\sigma _y-1}} \gt \begin{cases} s&\text{if }\, \sigma _x\lt 1 \\ \dfrac {s}{(1-b_x)s+b_x} &\text{if }\,\sigma _x=1 \\ 1&\text{if }\, \sigma _x\gt 1 \end{cases}. \end{align}

\begin{align} \frac {n+\delta }{a_yb_y^\frac {1}{\sigma _y-1}} \gt \begin{cases} s&\text{if }\, \sigma _x\lt 1 \\ \dfrac {s}{(1-b_x)s+b_x} &\text{if }\,\sigma _x=1 \\ 1&\text{if }\, \sigma _x\gt 1 \end{cases}. \end{align}

Observe that the factor productivity

$a_x$

of the consumption-goods sector does not appear in the above expressions. From Example2, we infer that any change in

$a_x$

of the consumption-goods sector does not appear in the above expressions. From Example2, we infer that any change in

$a_x$

affects solely output quantity and price of the consumption good.

$a_x$

affects solely output quantity and price of the consumption good.

Proposition 2.

Consider the case with CES production functions (

6

) and let

$\sigma _y\lt 1$

. Then the following holds true.

$\sigma _y\lt 1$

. Then the following holds true.

-

(i) The origin is a steady state,

$G(0)=0$

. -

(ii) If the model parameters

$(b_x,\sigma _x,a_y,b_y,\sigma _y,n,\delta ,s)$

satisfy Condition (36), then the origin is unstable and there exists at least one positive steady state

$G(k^\ast )=k^\ast \gt 0$

. This steady state is the only positive steady state if

$\sigma _x\geq 1$

. -

(iii) If the model parameters

$(b_x,\sigma _x,a_y,b_y,\sigma _y,n,\delta ,s)$

satisfy Condition (37), then the origin is asymptotically stable. In particular, if

$a_yb_y^{\frac {1}{\sigma _y-1}}\lt n+\delta$

, then the origin is globally asymptotically stable and no positive steady state exists.

-

(iv) All growth paths are bounded.

Proposition2 states that for

$\sigma _y\lt 1$

, a positive steady state exists whenever the savings propensity

$\sigma _y\lt 1$

, a positive steady state exists whenever the savings propensity

$s$

and/or the factor productivity

$s$

and/or the factor productivity

$a_y$

are sufficiently large. Since

$a_y$

are sufficiently large. Since

$f_y(0)=0$

, capital is an essential input for producing investment goods so that the origin is a steady state. A development trap obtains whenever the savings propensity and/or the factor productivity

$f_y(0)=0$

, capital is an essential input for producing investment goods so that the origin is a steady state. A development trap obtains whenever the savings propensity and/or the factor productivity

$a_y$

is too low so that Condition (37) is satisfied. Figure 3b portrays an example with an asymptotically stable origin and two positive steady states. Since Condition (37) holds, this example shows that Condition (36) is sufficient but not necessary for the existence of positive steady states. If the factor productivity is too low, then no positive steady state exists and the development trap is globally asymptotically stable.

$a_y$

is too low so that Condition (37) is satisfied. Figure 3b portrays an example with an asymptotically stable origin and two positive steady states. Since Condition (37) holds, this example shows that Condition (36) is sufficient but not necessary for the existence of positive steady states. If the factor productivity is too low, then no positive steady state exists and the development trap is globally asymptotically stable.

Proposition 3.

Consider the case with CES production functions (

6

) and let

$\sigma _y\gt 1$

. Then the following holds true.

$\sigma _y\gt 1$

. Then the following holds true.

-

(i) The origin is not a steady state as

$G(0)=\tfrac {1}{1+n}f_y(0)\gt 0$

. -

(ii) If the model parameters

$(b_x,\sigma _x,a_y,b_y,\sigma _y,n,\delta ,s)$

satisfy Condition (37), then there exists at least one positive steady state

$G(k^\ast )=k^\ast \gt 0$

and all growth paths are bounded. This steady state is uniquely determined if

$\sigma _x\geq 1$

. -

(iii) If the model parameters

$(b_x,\sigma _x,a_y,b_y,\sigma _y,n,\delta ,s)$

satisfy Condition (36), then the model exhibits unbounded growth. If, in particular,

$a_yb_y^{\frac {1}{\sigma _y-1}}\gt \frac {n+\delta }{s}$

, then no positive steady state exists and all growth paths are unbounded.

Proposition3 states that for

$\sigma _y\gt 1$

, a positive steady state exists whenever the savings propensity

$\sigma _y\gt 1$

, a positive steady state exists whenever the savings propensity

$s$

and/or the factor productivity

$s$

and/or the factor productivity

$a_y$

is not too large. Condition (36) implies that except for the case

$a_y$

is not too large. Condition (36) implies that except for the case

$\sigma _x\gt 1$

, unbounded growth occurs if the savings propensity

$\sigma _x\gt 1$

, unbounded growth occurs if the savings propensity

$s$

in relation to factor productivity

$s$

in relation to factor productivity

$a_y$

is sufficiently large. The origin is not a steady state, because capital is not essential for producing investment goods. The example portrayed in Figure 1b demonstrates that Condition (37) is sufficient but not necessary. The time-one map

$a_y$

is sufficiently large. The origin is not a steady state, because capital is not essential for producing investment goods. The example portrayed in Figure 1b demonstrates that Condition (37) is sufficient but not necessary. The time-one map

$G$

has two positive steady states even though Condition (37) is violated and unbounded growth is possible.

$G$

has two positive steady states even though Condition (37) is violated and unbounded growth is possible.

Lemma 5.

Consider the case with CES production functions (

6

) and let

$\sigma _y=1$

. Then the following holds true.

$\sigma _y=1$

. Then the following holds true.

-

(i) The origin

$0=G(0)$

is an unstable steady state.

-

(ii) There exists at least one positive steady state

$G(k^\ast )=k^\ast \gt 0$

. -

(iii) All growth paths are bounded.

Lemma5 states that neither a development trap nor unbounded growth is possible if the output of the investment-goods sector is determined by a Cobb–Douglas production function. This case is illustrated in Figure 2b, which depicts a time-one map

$G$

with a hump.

$G$

with a hump.

An immediate consequence of the last three results is the following corollary, which summarises conditions under which the dynamics are qualitatively indistinguishable from the dynamics of the classical Solow–Swan model.

Corollary 1.

Consider the case with CES production functions (

6

) and let

$\sigma _x\geq 1$

. Then

$\sigma _x\geq 1$

. Then

$G^\prime \gt 0$

. If, in addition, one of the following three conditions,

$G^\prime \gt 0$

. If, in addition, one of the following three conditions,

\begin{equation*} (i)\quad \sigma _y=1,\quad (ii)\quad \sigma _y\lt 1\, and \ (36) \ holds, \quad or \,\quad (iii)\quad \sigma _y\gt 1\, and \ (37) \ holds, \end{equation*}

\begin{equation*} (i)\quad \sigma _y=1,\quad (ii)\quad \sigma _y\lt 1\, and \ (36) \ holds, \quad or \,\quad (iii)\quad \sigma _y\gt 1\, and \ (37) \ holds, \end{equation*}

is satisfied, then there exists a uniquely determined positive steady state

$G(k^\ast )=k^\ast \gt 0$

, which is asymptotically stable on

$G(k^\ast )=k^\ast \gt 0$

, which is asymptotically stable on

$\mathbb R_{++}$

.

$\mathbb R_{++}$

.

4.2 Numerical evidence for complex dynamics

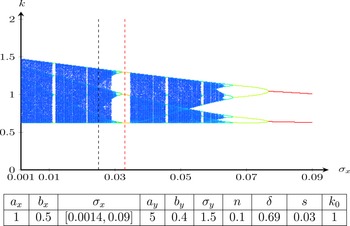

The simulation results presented next provide numerical evidence for complex dynamics if the substitution elasticity

$\sigma _x$

is sufficiently small.Footnote

6

$\sigma _x$

is sufficiently small.Footnote

6

Figure 1 shows that the time-one map

$G$

in Case A has at least two positive steady states, which are both unstable. By Proposition3, the origin is not a steady state and unbounded growth obtains for all sufficiently large initial values. All growth paths

$G$

in Case A has at least two positive steady states, which are both unstable. By Proposition3, the origin is not a steady state and unbounded growth obtains for all sufficiently large initial values. All growth paths

$\{k_t\}_{t=0}^{\infty }$

with initial values

$\{k_t\}_{t=0}^{\infty }$

with initial values

$k_0$

below the larger steady state are bounded. For the initial value

$k_0$

below the larger steady state are bounded. For the initial value

$k_0=1$

, the bifurcation diagrams in Figures 4 and 5 illustrate how changes in the elasticities of factor substitution affect the qualitative dynamics. The growth path corresponding to

$k_0=1$

, the bifurcation diagrams in Figures 4 and 5 illustrate how changes in the elasticities of factor substitution affect the qualitative dynamics. The growth path corresponding to

$\sigma _x=0.025$

in Figure 4 provides numerical evidence that the model exhibits non-periodic business cycles. For

$\sigma _x=0.025$

in Figure 4 provides numerical evidence that the model exhibits non-periodic business cycles. For

$\sigma _x=0.033$

, Figure 4 shows that the growth path starting in

$\sigma _x=0.033$

, Figure 4 shows that the growth path starting in

$k_0=1$

converges to a period-3 cycle. Similarly for

$k_0=1$

converges to a period-3 cycle. Similarly for

$\sigma _y=1.4$

instead of

$\sigma _y=1.4$

instead of

$\sigma _y=1.5$

, Figure 5 shows that the growth path starting in

$\sigma _y=1.5$

, Figure 5 shows that the growth path starting in

$k_0=1$

converges to a period-3 cycle as well. By Li and Yorke (Reference Li and Yorke1975), the period-3 cycles ensure the presence of topological chaos, implying that cycles of any order and irregular fluctuations exist.

$k_0=1$

converges to a period-3 cycle as well. By Li and Yorke (Reference Li and Yorke1975), the period-3 cycles ensure the presence of topological chaos, implying that cycles of any order and irregular fluctuations exist.

Case A. Bifurcation over the substitution elasticity

$\sigma _x$

.

$\sigma _x$

.

Case A. Bifurcation over the substitution elasticity

$\sigma _y$

.

$\sigma _y$

.

Case A. Bifurcation over the savings propensity

$s$

.

$s$

.

In many cases, however, only the period-3 cycle is numerically detected, because the other patterns exist only for a set of initial values of Lebesgue-measure zero. In contrast to topological chaos, numerical evidence for observable chaos is easier to detect. A model is said to exhibit observable chaos if a so-called strange attractor is observed, for example, see Onozaki et al. (Reference Onozaki, Sieg and Yokoo2000). These are numerically detected by computing Lyapunov exponents.Footnote

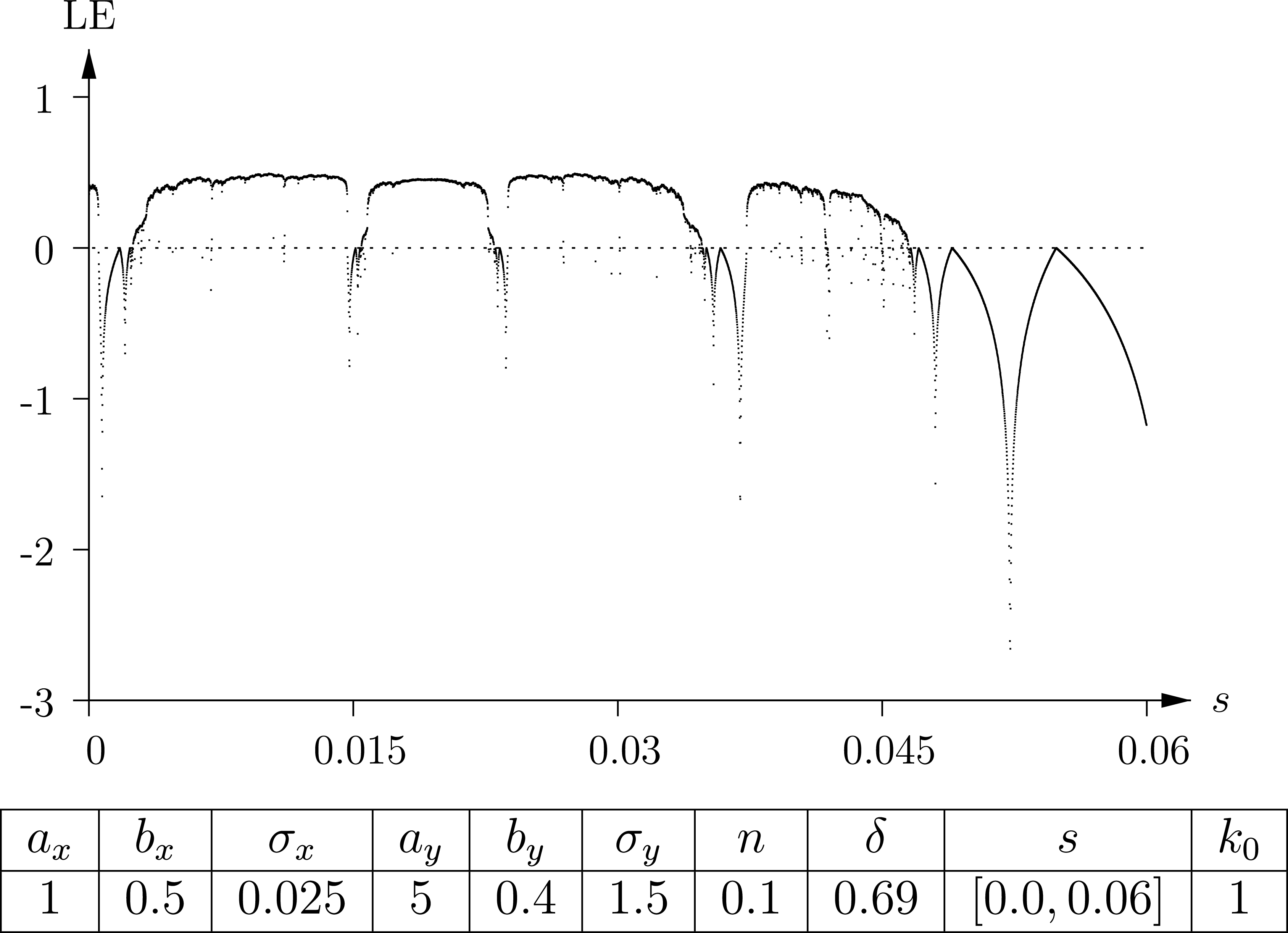

7

A positive Lyapunov exponent implies that the growth of capital-to-labour ratios depends sensitively on the initial capital-to-labour ratio. An attractor with such a property is called strange attractor. The bifurcation diagram in Figure 6 indicates that the savings propensity

$s$

has to be very small in order for strange attractors to exist. The Lyapunov exponents of the corresponding growth paths over the same range of savings propensities are depicted in Figure 7. The diagrams lead the the conjecture that savings propensities above

$s$

has to be very small in order for strange attractors to exist. The Lyapunov exponents of the corresponding growth paths over the same range of savings propensities are depicted in Figure 7. The diagrams lead the the conjecture that savings propensities above

$5.5\%$

yield stable states, which confirms Lemma3 and our earlier analysis in Example5.

$5.5\%$

yield stable states, which confirms Lemma3 and our earlier analysis in Example5.

Case A. Lyapunov exponents.

Case B. Bifurcation diagramm over

$b_y\in [0.01,0.09]$

.

$b_y\in [0.01,0.09]$

.

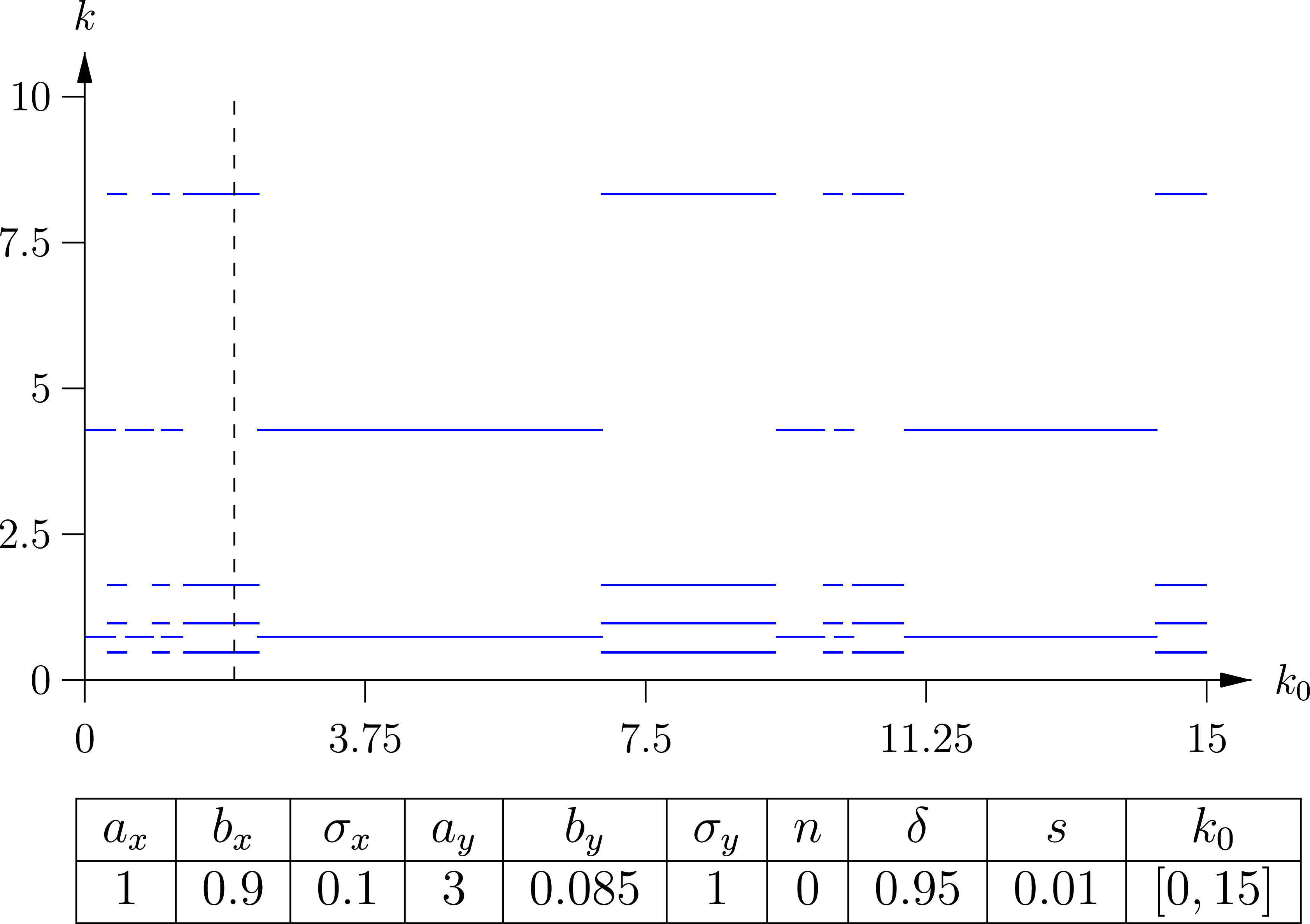

In view of Lemma5, the time-one map for case B depicted in Figure 2b has two steady states, a unique positive steady state and the origin. The dashed vertical line in the bifurcation diagram in Figure 8 shows that a period-4 cycle obtains for

$b_y=0.085$

, indicating that both steady states may be unstable. This bifurcation diagram provides numerical evidence for topological chaos whenever the income distribution parameter

$b_y=0.085$

, indicating that both steady states may be unstable. This bifurcation diagram provides numerical evidence for topological chaos whenever the income distribution parameter

$b_y$

assumes values, for example, in the neighbourhood of

$b_y$

assumes values, for example, in the neighbourhood of

$0.05$

.Footnote

8

$0.05$

.Footnote

8

Case B. Dependence on initial conditions

$k_0\in [0,15]$

.

$k_0\in [0,15]$

.

Figure 9 provides numerical evidence for the dependence on initial conditions. For initial capital-to-labour ratios

$k_0$

ranging from

$k_0$

ranging from

$0$

to

$0$

to

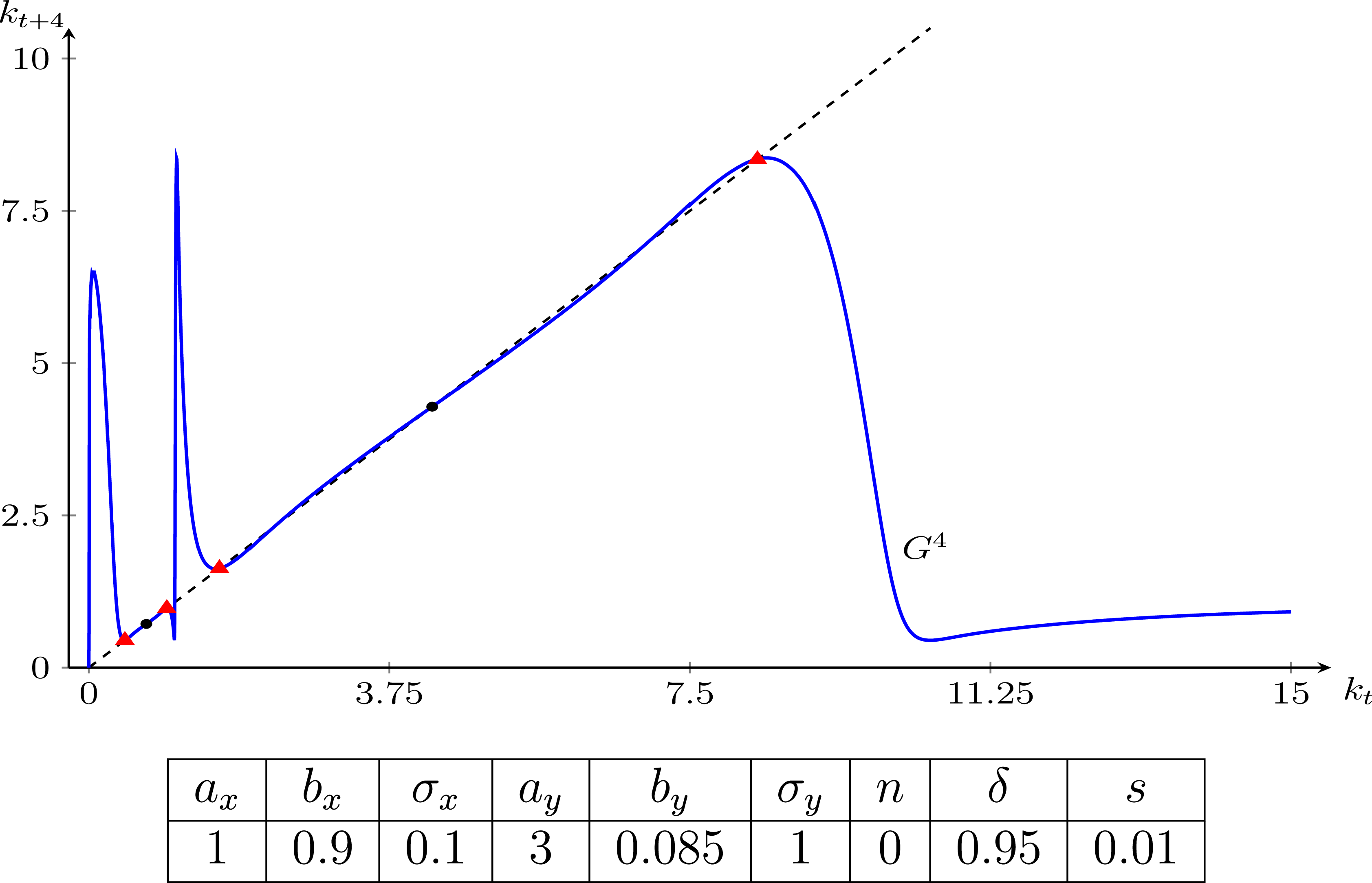

$15$

, the corresponding growth paths either converge to a period-2 cycle or to a period-4 cycle. The shape of the fourth iterate

$15$

, the corresponding growth paths either converge to a period-2 cycle or to a period-4 cycle. The shape of the fourth iterate

$G^4$

of the time-one map

$G^4$

of the time-one map

$G$

portrayed in Figure 10 provides some more insight into this phenomenon. A subcritical pitchfork bifurcation occurs when increasing the parameter

$G$

portrayed in Figure 10 provides some more insight into this phenomenon. A subcritical pitchfork bifurcation occurs when increasing the parameter

$b_y$

from

$b_y$

from

$0.08$

to

$0.08$

to

$0.09$

. The period-2 cycle indicated by two dots, which already exists for

$0.09$

. The period-2 cycle indicated by two dots, which already exists for

$b_y=0.08$

, becomes asymptotically stable. Decreasing

$b_y=0.08$

, becomes asymptotically stable. Decreasing

$b_y$

from

$b_y$

from

$0.09$

to

$0.09$

to

$0.08$

, an asymptotically stable period-4 cycle, marked by four triangles, emerges in addition to the existing period-2 cycle via a saddle-node bifurcation.

$0.08$