1 Introduction

1.1 Motivation

Classical linear-regression models are typically used to estimate the average change in a response variable associated with a unit change in an explanatory variable. These mean-based models have dominated empirical political research for decades because of their parsimony, computational convenience, and relative ease of interpretation. Yet their standard inferential framework is often most straightforward under assumptions such as homoscedasticity and, in some settings, normally distributed errors. These assumptions may be problematic when the outcome distribution is skewed or when dispersion varies systematically across values of the covariates. More fundamentally, mean-based models focus attention on the conditional mean of the response variable given a set of covariates. As a result, heterogeneity away from that conditional mean is typically absorbed into the error term rather than treated as substantively meaningful variation in its own right.

In many political settings, however, differences across individuals, parties, governments, or institutions reflect genuine heterogeneity in preferences, incentives, constraints, or strategic environments. Such differences are often central to political analysis and cannot be adequately understood as mere random deviations from an average relationship. Consequently, an exclusive focus on averages may provide only a partial account of many substantive research questions in political science.

Indeed, many research questions are concerned less with average effects than with how political behavior varies across groups, time periods, institutional settings, or stages of strategic interaction (Braumoeller, Reference Braumoeller2006; De Marchi & Laver, Reference De Marchi and Laver2023; Lu, Reference Lu2020; Rosenberg, Knuppe, & Braumoeller, Reference Rosenberg, Knuppe and Braumoeller2017; Weschle, Reference Weschle2019). In such cases, reliance on average effects alone can produce incomplete and, at times, potentially misleading conclusions (Winship & Mare, Reference Winship and Mare1992). Even when mean-based models allow for heteroscedasticity, they typically treat it as a problem for statistical inference to be corrected rather than as substantively meaningful variation to be examined in its own right. However, for many research questions, heterogeneity is precisely what matters. Units facing the same formal choice may behave differently because they are embedded in different contexts, constrained by different institutions, or guided by different preferences and incentives, including factors that are only imperfectly observed.

Quantile models, introduced in their modern form by Koenker and Bassett (Reference Koenker and Bassett1978), provide a powerful framework for analyzing heterogeneity in political data. Their intellectual roots reach further back: in 1760, Roger Boscovich posed to Thomas Simpson a problem involving the minimization of the sum of absolute residuals, anticipating what would later be recognized as median regression (Stigler, Reference Stigler1984). Two centuries later, this line of thinking helped lay the foundation for modern quantile methods, which are now widely used across the natural and social sciences. While mean-based models focus on how covariates shift the conditional mean of a response variable, quantile models examine how relationships vary across different points of the conditional outcome distribution. This makes them especially useful for studying heterogeneous effects that may be obscured by average-based analysis. Rather than reducing variation away from the mean to residual noise, quantile models allow researchers to investigate how explanatory variables matter differently across the distribution of the response variable. They are also less sensitive to extreme values and offer a richer picture of the underlying data-generating process than models centered solely on average effects. Quantile models therefore broaden the range of political questions that can be addressed empirically, particularly when heterogeneity is itself of substantive interest.

These features make quantile models especially attractive for political scientists whose research questions are not well captured by conventional mean-based approaches. However, despite the aforementioned advantages, quantile models have been underutilized in political science until recently. Recognizing the utility of quantile models, scholars have increasingly applied them to examine political topics as diverse as geopolitical risks (Caldara & Iacoviello, Reference Caldara and Iacoviello2022), political extremism (Bertelli & Richardson, Reference Bertelli and Richardson2008; Makowsky & Miller, Reference Makowsky and Miller2014), coalition building (Häge, Reference Häge2013), electoral change (Guinjoan & Rodon, Reference Guinjoan and Rodon2021; Hill, Hopkins, & Huber, Reference Hill, Hopkins and Huber2021), voter turnout (Kaniovski & Mueller, Reference Kaniovski and Mueller2006; Schafer & Holbein, Reference Schafer and Holbein2020), policy communication (Haan et al., Reference Haan, Peichl, Schrenker, Weizsäcker and Winter2022), political representation (Weschle, Reference Weschle2019), trade politics (Betz, Reference Betz2017), foreign aid (Okada & Samreth, Reference Okada and Samreth2012), public budgeting (Breunig, Reference Breunig and Jones2011; Breunig & Jones, Reference Breunig2011; Breunig & Koski, Reference Breunig and Koski2020), interest group ratings (Brunell et al., Reference Brunell, Koetzle, DiNardo, Grofman and Feld1999), executive constraints in parliaments (Abramson & Boix, Reference Abramson and Boix2019), political capital in developing countries (Appleton et al., Reference Appleton, Knight, Song and Xia2009), political economy of natural disasters (Neumayer, Plümper, & Barthel, Reference Neumayer, Plümper and Barthel2014), gender inequality in political participation (Arvate, Firpo, & Pieri, Reference Arvate, Firpo and Pieri2021), anchoring heuristic in public preference formation (Arceneaux & Nicholson, Reference Arceneaux and Nicholson2024), effects of wealth on political selection (Poulos, Reference Poulos2019), impact of democratization on corruption (Jetter, Agudelo, & Hassan, Reference Jetter, Agudelo and Hassan2015), confirmation delay in the executive appointment process (Krause & Byers, Reference Krause and Byers2022), grant retrenchments by US federal agencies (Krause & Zarit, Reference Krause and Zarit2022), economic consequences of terrorism on regional growth (Blomberg, Broussard, & Hess, Reference Blomberg, Broussard and Hess2011), distributional inequity in public service provision (Cheng, Yang, & Deng, Reference Cheng, Yang and Deng2022), citizen responsiveness to government performance (Holbein, Reference Holbein2016), and effects of political institutions on private investment (Stasavage, Reference Stasavage2002), among others.

Despite these applications, there are still several reasons that deter a wider application of quantile methods in the political science community. These mainly include (1) limited familiarity with quantile models due to the absence of a systematic introduction to the quantile approach in political science, (2) technical challenges in implementing quantile models and analyzing discrete choices in political settings, and (3) difficulties in presenting and interpreting results from quantile models due to multiple sets of coefficients for each quantile of interest.

This Element is designed to bridge the gap and provide political scientists with useful information about the most important aspects of quantile models. Throughout the Element, it becomes evident that the three primary obstacles in utilizing quantile models are straightforward to overcome. First, by explaining the basic concept of quantiles and quantile functions, I illustrate that the idea of quantiles is as intuitive as that of the mean, yet it offers greater flexibility in empirical analysis. Second, there is now an abundance of software packages and computational algorithms for implementing quantile methods in both continuous and discrete variable settings that remove the technical barriers to using quantile models. Applied political researchers can readily adopt existing quantile algorithms and software for their own research purposes. Third, although scholars unfamiliar with quantile regression might find it cumbersome to interpret results from quantile models – since each quantile requires its own interpretation and potentially its own graphical representation – this feature is what makes quantile models so useful. They provide a more complete picture of the relationship between variables by estimating effects at different points in the distribution of the response variable. Thus, the quantile approach offers significant advantages in terms of the ability to uncover nuanced insights across the distribution of the response variable. This benefit makes it a powerful tool for researchers interested in exploring the full complexity of their data.

Take vote choice as an example. Suppose we want to study how the ideological distance between voters and candidates influences voter decisions. A conventional mean-based model will summarize this relationship with a single average effect. However, it is entirely plausible that voters react differently to the ideological distance depending on their underlying propensity to vote for a certain candidate. In this case, unlike mean-based models, quantile models can capture this heterogeneity by showing how the effect of ideological distance varies across different points of the conditional distribution of support, rather than restricting attention to the mean alone. Substantively, this has important implications for the strategic positioning of political candidates within the policy spectrum. If ideological distance has different effects among voters with lower and higher propensities to support, then candidates’ strategic positioning in the policy space may influence core supporters and more persuadable voters in different ways. Subsequent sections will return to this and other political examples to illustrate how quantile effects can be interpreted and how quantile models can contribute to substantive political analysis.

In general, the Element is written as a combination of methodological innovation and practical guidance on quantile models. It introduces the basic properties of quantiles, illustrates quantile inference with continuous response variables, and then explores the potential of quantile methods in analyzing discrete choices. This Element also emphasizes that quantiles are as intuitive as the mean, yet they offer greater flexibility in modeling. Compared to existing books on quantile regression, this Element draws attention to discrete choice data in both binary and multiple choice forms, which play an especially important role in empirical research of political science. In particular, it introduces discrete quantile models for data with varying choice alternatives and for the estimation of multiple conditional quantiles. With real-world political examples, published software packages and hands-on computational codes, this Element demonstrates the utility of quantile models for a wide field of political research, and shows that estimating and interpreting quantile models can be as simple as estimating and interpreting the classical linear regression.Footnote 1

1.2 Aim and Organization

The aim of this Element is to encourage the practical use of the quantile approach in political science by introducing the concepts, functions, and applications of both the conventional and newly developed qauntile models. It builds on the prior work of quantile regression but emphasizes more on the ability of quantile models in dealing with discrete choices and examining competing political theories. The Element is not intended to provide a comprehensive overview of all existing quantile methods, which is an impossible mission for a single book. While quantile methods have been extensively discussed in a variety of publications such as the Handbook of Quantile Regression edited by Koenker, Chernozhukov, He and Peng (Koenker et al., Reference Koenker, Chernozhukov, He and Peng2017), and books written by Koenker (Reference Koenker2005), Hao and Naiman (Reference Hao and Naiman2007), Davino, Furno, and Vistocco (Reference Davino, Furno and Vistocco2014), Furno and Vistocco (Reference Furno and Vistocco2018), and Cleophas and Zwinderman (Reference Cleophas and Zwinderman2021), among others, these works are mainly geared toward statisticians and scholars outside the field of political science. On the contrary, this Element is tailored to the political science community, providing fundamental information on the properties and usage of quantile methods, along with instructional political examples and hands-on computational codes to demonstrate their substantive applications in the field. Because most political scientists have been exposed to mean-based models such as OLS, logit and probit models, this Element also compares their performance with quantile models to better illustrate the advantages of the latter in various political settings.

This Element is oriented mainly toward students and scholars in political science who are interested in utilizing quantile methods for their own learning and research purposes. For reproducibility and research purposes, the Element provides codes written in the R programming language, a popular and easy-to-learn open-source software project for data analysis and statistical computing (R Core Team, 2021). The advantage of using R is that it is free, publicly accessible, and allows readers to examine the source codes of the packages and functions, and consequently adjust and extend the functionalities as needed for their own research. This Element is not intended to provide an introduction to the R programming, as there are already a variety of excellent resources and tutorials available. The software is accessible via the CRAN website, which provides both source and binary versions for different operating systems and computing environments, including Windows, Linux, and Macintosh.Footnote 2

The Element is organized as follows. The rest of this section will show the use of quantiles by introducing the basic concepts and properties of quantiles, quantile functions, and conditional quantiles. In Section 2, the traditional quantile regression applied for response variables in a continuous scale will be introduced. Section 3 expands the application of quantile models to cases with binary response variables. In this section, the estimation procedure of the binary quantile model will be introduced. Following the discussion of Section 3, a more generalized discrete quantile model (the conditional binary quantile model) for multiple choices will be presented in Section 4. Section 5 will provide a brief discussion on some more quantile methods, including those for estimating quantile treatment effects and survival data. This section will also introduce how to perform variable selection and model comparison in quantile settings. Besides the advantages of quantile models, the summary subsection of the section will discuss practical issues of the quantile approach. The final section concludes by highlighting briefly why and when quantile models should be used.

1.3 Basic Concept of Quantiles

Generalizing notions such as median, quartile, decile, and percentile, quantiles are a set of values that divide a distribution into ordered parts. The

th quantile of a given set usually denotes the smallest value below which at least a proportion

th quantile of a given set usually denotes the smallest value below which at least a proportion

of the observations fall. One of the most well-known quantiles is the median (or the 0.5th quantile), which separates the lower half from the higher half of a distribution. Other widely used quantiles include the first and third quartile, which are also known as the 0.25th and 0.75th quantile, or the 25th and 75th percentile. They are commonly used to calculate the interquartile range as a measure of data dispersion.

of the observations fall. One of the most well-known quantiles is the median (or the 0.5th quantile), which separates the lower half from the higher half of a distribution. Other widely used quantiles include the first and third quartile, which are also known as the 0.25th and 0.75th quantile, or the 25th and 75th percentile. They are commonly used to calculate the interquartile range as a measure of data dispersion.

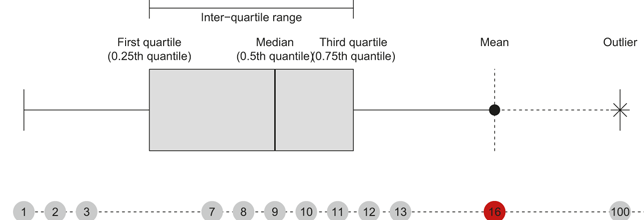

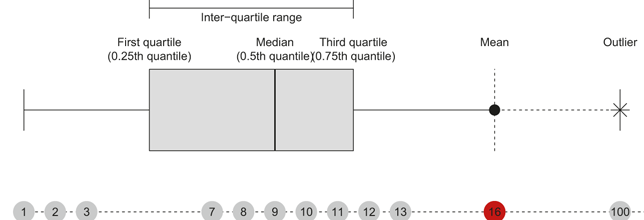

As quantiles are only sensitive to the ordering of the data but not to extreme values, they represent a robust alternative to the mean when evaluated at the center of a distribution. They can also offer a more informative summary of dispersion when the data are skewed or otherwise depart from normality. To illustrate these basic properties, consider for example in Figure 1 a set of values [1, 2, 3, 7, 8, 9, 10, 11, 12, 13, 100] arranged in ascending order. This set is clearly not normally distributed, but right-skewed in the sense that most observations are concentrated at lower values, with a long right tail. The 0.25th quantile, or equivalently the first quartile, of the set is the value below which there are at least 25% of cases, and in this example falls between 3 and 7 under common sample definitions. In the same vein, we can calculate the 0.75th quantile (third quartile), which is located between 11 and 12. Due to the existence of an extreme value (100) in this example, it is also apparent that compared to the mean 16, the median 9 is a more informative summary of the central location. These values can then be used to quantify the dispersion of the sample. Compared to the dispersion calculated by the sample standard deviation (approximately 28), which is more than twice the difference between the smallest and the second largest value of the sample, the interquartile range measured by the difference between the 0.25th and 0.75th quantile, as shown by the box plot in Figure 1, represents a more meaningful summary of the dispersion of the sample. Moreover, we can calculate another robust alternative to the mean-based standard deviation – the median absolute deviation (MAD), which is defined as the median of the absolute deviations from the median of the sample

:

:

Sample quantiles and box-plot

(1.1)

(1.1)

The MAD of the previous sample is 3, representing a more representative summary statistic for variability of the sample than the standard deviation.

As the figure also illustrates, the standard box-plots use quantiles to summarize the central tendency, dispersion, and skewness of a dataset, while also helping identify outliers. More generally, denote the value at

th quantile as

th quantile as

. For any

. For any

, the inter-quantile range between the lower (

, the inter-quantile range between the lower (

) and the upper (

) and the upper (

) quantile can be computed as follows:

) quantile can be computed as follows:

(1.2)

(1.2)

which denotes the dispersion of the middle

% of the sample.

% of the sample.

Because of their robustness and their ability to characterize different parts of a sample or distribution, quantiles have become common statistics in descriptive summaries, quantification of uncertainty, and hypothesis testing in empirical research. A familiar example is the quantile-to-quantile (QQ) plot, which is commonly used to assess whether an empirical distribution is approximately normal. By comparing the quantiles of the dataset with the theoretical quantiles of a normal distribution, the QQ plot provides a simple visual diagnostic of deviations from normality.

1.4 Cumulative Distribution Function and Quantile Function

The cumulative distribution is closely related to the concept of quantiles. To understand quantiles more formally, it is thus helpful to clarify the relation between the cumulative distribution function and the quantile function. For any random variable

, the cumulative distribution function evaluated at

, the cumulative distribution function evaluated at

is defined as the probability that

is defined as the probability that

is less than or equal to

is less than or equal to

:

:

(1.3)

(1.3)

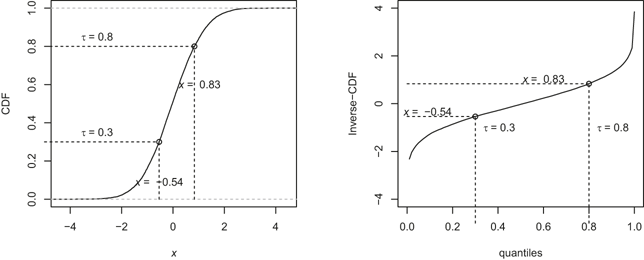

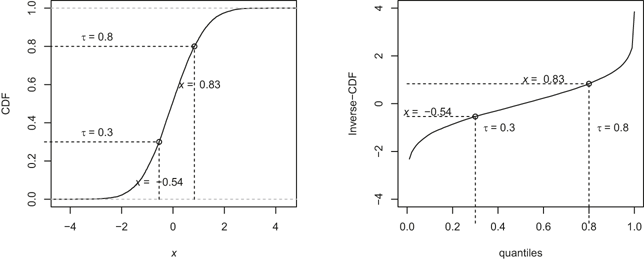

Statistically, scholars may be interested in knowing the location of a specific value within a distribution besides the mean. Consider the cumulative distribution function of the standard normal distribution as shown in Figure 2a. We might wish to know, for example, what proportion of the distribution lies below the values

0.53 and 0.84. To do so, we trace each value on the horizontal axis up to the CDF and then across to the vertical axis. The resulting values are approximately 0.3 and 0.8, respectively (Figure 2a). In other words,

0.53 and 0.84. To do so, we trace each value on the horizontal axis up to the CDF and then across to the vertical axis. The resulting values are approximately 0.3 and 0.8, respectively (Figure 2a). In other words,

0.53 corresponds to the 0.3th quantile and 0.84 to the 0.8th quantile of the standard normal distribution. The quantile function, as shown in Figure 2b, reverses this mapping by returning the value associated with a given cumulative probability.

0.53 corresponds to the 0.3th quantile and 0.84 to the 0.8th quantile of the standard normal distribution. The quantile function, as shown in Figure 2b, reverses this mapping by returning the value associated with a given cumulative probability.

Cumulative distribution function (a) and quantile function (b)

Formally, the

th quantile function of a random variable

th quantile function of a random variable

, denoted

, denoted

, is defined as the generalized inverse of its cumulative distribution function:

, is defined as the generalized inverse of its cumulative distribution function:

(1.4)

(1.4)

The quantile function is useful because it allows us to recover values associated with specified probability levels. This is central to many tasks in statistical analysis, including the construction of critical values, confidence intervals, prediction intervals, and other forms of uncertainty assessment.

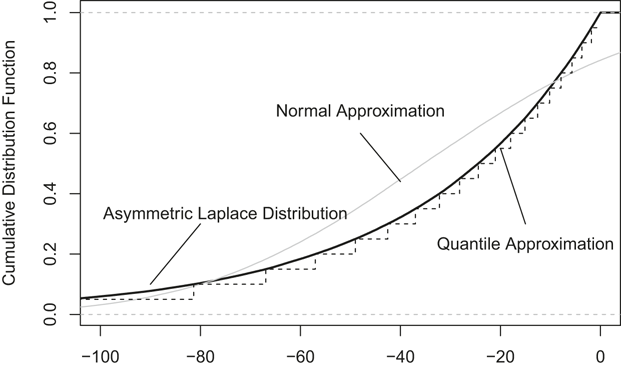

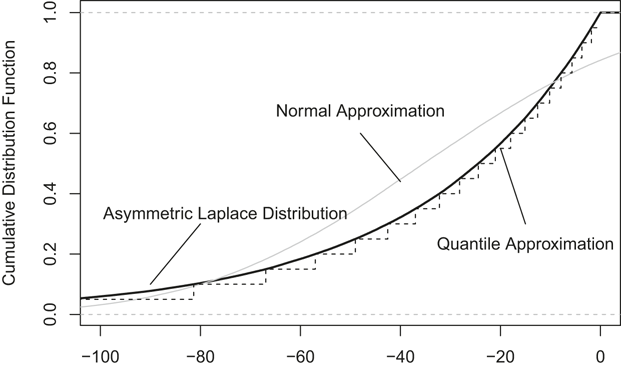

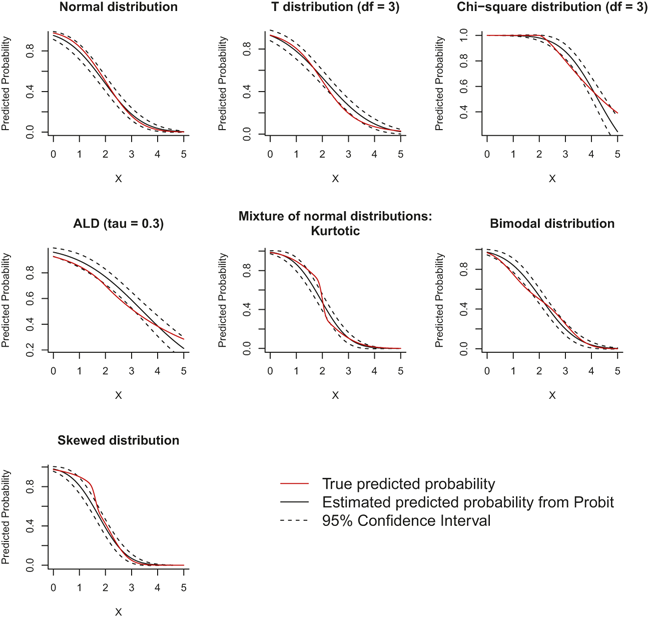

Although symmetrical distributions such as a normal distribution can often be summarized reasonably well by its central tendency and dispersion, that is, its mean and variance, the mean-based statistics become less informative when the distribution is asymmetric. Consider for instance a right-skewed distribution whose cumulative distribution function is plotted in Figure 3.Footnote 3 Approximating the distribution using a normal distribution with the corresponding mean and standard deviation will misrepresent the distribution around the median and in the tails. On the contrary, quantile approximation uses piece-wise information from the random sample, which, as shown by the dashed lines in the figure, yields a much better fit.

Approximation of a right-skewed distribution (asymmetric Laplace distribution with location parameter

, scale parameter

, scale parameter

, and skewness parameter

, and skewness parameter

)

)

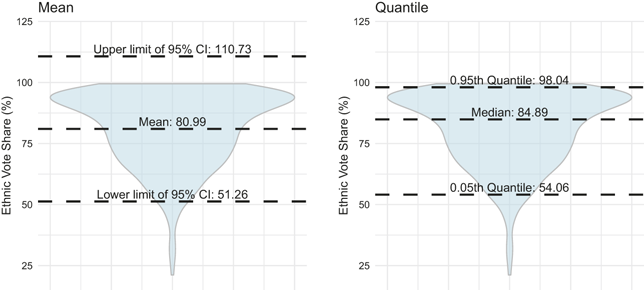

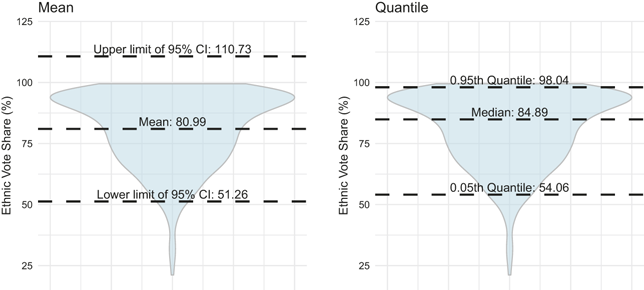

The substantive value of quantile-based summaries becomes especially clear when political outcomes are distributed unevenly across units. Take the distribution of ethnic voting in Bosnia as an example. Figure 4 illustrates the distribution using the violin plot. Based on data collected by Hadzic, Carlson, and Tavits (Reference Hadzic, Carlson and Tavits2020), the average municipal-level vote share of ethnic parties in national legislative elections is 80.99% (see Figure 4(a)). Compared to the median share of 84.89% (see Figure 4(b)), the mean value is a reduction of 4 percentage points. This indicates that the whole sample is distributed asymmetrically, with observations concentrated at relatively high vote shares and a longer tail toward lower values. In addition to the skewness, the spread of the distribution is wide, with the smallest share of 19.33% and the largest share of 99.49%.

Summary of the distribution of ethnic vote shares by mean (a) and quantile (b)

Moreover, as the left panel of the figure shows, if we use the 95% interval based on the normality assumption to quantify the spread of the variable, the upper limit of the 95% interval will exceed even the highest value of the sample, while the lower limit will underestimate the lowest values. Furthermore, because the quantification of the spread is symmetric around the mean, the mean-based approach is unable to reveal the skewness of the variable. In contrast, by examining the 0.95th and 0.05th quantile as illustrated in the right panel of Figure 4, we can find a sharp distinction between the upper and lower halves of the distribution: While there is only a 13.15% difference between the 0.95th quantile and the median, the difference between the median and the 0.05th quantile is 30.83%, more than twice the difference in the upper half. A focus on averages alone would therefore obscure substantively important variation across municipalities in the distribution of ethnic voting.

1.5 Conditional Quantiles

The illustrations in Section 1.4 show that quantiles provide added value to the mean by offering a more complete summary of a distribution. However, in political research, the central interest rarely lies in the distribution of a single variable alone. Instead, we want to investigate the effect of variables on the outcome of interest, that is, how changes in explanatory variables are associated with changes in the outcome. To reveal the conditional relationship between variables, we need to compute conditional quantiles. Conditional quantiles are “conditional” in the sense that the estimates depend on the covariates on the right-hand side of the estimation equation, and thereby they reveal local effects of a variable on the response across the whole distribution.

To show the benefits of using conditional quantiles, recall the standard linear model:

(1.5)

(1.5)

If we assume that the conditional expectation of the error term equals zero (i.e.,

), we obtain the conditional mean model. Subsequently, we can reformulate the equation with the response variable

), we obtain the conditional mean model. Subsequently, we can reformulate the equation with the response variable

on the left-hand side and a vector of explanatory variables

on the left-hand side and a vector of explanatory variables

on the right-hand side (Lewis-Beck & Lewis-Beck, Reference Lewis-Beck and Lewis-Beck2015):

on the right-hand side (Lewis-Beck & Lewis-Beck, Reference Lewis-Beck and Lewis-Beck2015):

(1.6)

(1.6)

This formulation summarizes the relationship between

and

and

at the conditional mean of the outcome. As a consequence, the covariate effect is represented by a single coefficient vector

at the conditional mean of the outcome. As a consequence, the covariate effect is represented by a single coefficient vector

, rather than being allowed to vary across different parts of the conditional distribution. The coefficients can then be estimated by solving:Footnote 4

, rather than being allowed to vary across different parts of the conditional distribution. The coefficients can then be estimated by solving:Footnote 4

(1.7)

(1.7)

the familiar least-squares problem. While highly useful, the conditional mean neglects important information about potentially heterogeneous effects of

on

on

.

.

On the contrary, if we introduce an alternative formula

(1.8)

(1.8)

by replacing the expectation

with conditional quantiles

with conditional quantiles

, we are in a more flexible modeling situation. In this formula, each coefficient vector

, we are in a more flexible modeling situation. In this formula, each coefficient vector

represents conditional effects at a specific quantile location

represents conditional effects at a specific quantile location

of the response variable (for a formal proof, see e.g. Ding (Reference Ding2025, 294–297)). For

of the response variable (for a formal proof, see e.g. Ding (Reference Ding2025, 294–297)). For

, this becomes the conditional median model, which can be estimated by minimizing the sum of the absolute deviations:

, this becomes the conditional median model, which can be estimated by minimizing the sum of the absolute deviations:

(1.9)

(1.9)

More generally, quantile regression estimates

by minimizing the asymmetric absolute loss:

by minimizing the asymmetric absolute loss:

(1.10)

(1.10)

where

(for details of derivation, see Section 2.2). This objective function, often called the check function, gives asymmetric weights to positive and negative residuals and thereby identifies the conditional quantile.

(for details of derivation, see Section 2.2). This objective function, often called the check function, gives asymmetric weights to positive and negative residuals and thereby identifies the conditional quantile.

Formally, the conditional quantile value of

given

given

can be written as

can be written as

(1.11)

(1.11)

where

is the conditional cumulative distribution function. For each quantile level

is the conditional cumulative distribution function. For each quantile level

, we are able to get a quantile-specific effect

, we are able to get a quantile-specific effect

that may differ from the average effect.

that may differ from the average effect.

To interpret

, we can regard it as the marginal change in the

, we can regard it as the marginal change in the

th quantile of the response variable due to a marginal change of the explanatory variable(s). In causal applications, and under additional identification assumptions, related quantile-based parameters can also be interpreted in terms of treatment effects at different points of the outcome distribution (Frandsen, Frölich, & Melly, Reference Frölich and Melly2010; Frölich & Melly, Reference Frandsen, Frölich and Melly2012), the details of which will be discussed in the subsection on quantile treatment effects in Section 5.

th quantile of the response variable due to a marginal change of the explanatory variable(s). In causal applications, and under additional identification assumptions, related quantile-based parameters can also be interpreted in terms of treatment effects at different points of the outcome distribution (Frandsen, Frölich, & Melly, Reference Frölich and Melly2010; Frölich & Melly, Reference Frandsen, Frölich and Melly2012), the details of which will be discussed in the subsection on quantile treatment effects in Section 5.

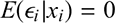

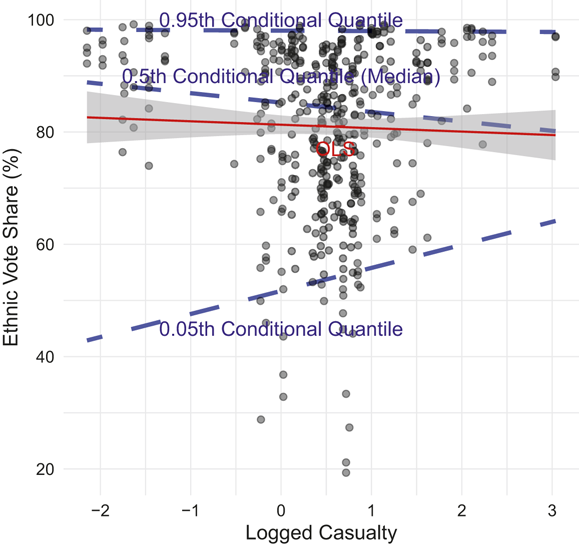

To illustrate the contrast between conditional means and conditional quantiles, return to the aforementioned example of ethnic voting. Suppose we are interested in the effect of wartime violence on ethnic voting, measured by wartime casualties and ethnic vote share, respectively (Hadzic, Carlson, & Tavits, Reference Hadzic, Carlson and Tavits2020). In a simple bivariate specification, the conditional mean can be calculated using the OLS regressing (logged) casualty against ethnic vote share. As illustrated by the solid line and the associated 95% confidence interval in Figure 5, the estimated mean relationship is not statistically distinguishable from zero. Once we examine the relationship across quantiles, however, a more differentiated pattern emerges. As shown by the fitted lines at the 0.05th, 0.5th, and 0.95th conditional quantiles in the figure, the positive relation between wartime violence and ethnic voting is strongest in lower quantiles of ethnic vote distribution and weakens as one moves toward the upper quantiles. This points to substantively meaningful heterogeneity across municipalities, possibly reflecting differences in prior levels or traditions of ethnic voting. Examining conditional quantiles alongside the conditional mean thus provides a fuller and more nuanced account of the relationship between wartime violence and ethnic voting.

Effects of wartime violence on ethnic voting

Note that for illustrative purposes, the depicted effects at this stage are solely based on the bivariate analysis, which consequently neglects potential confounding variables. In the following section, we will return to this example with a more complete analysis controlling for potential confounders.

1.6 Summary

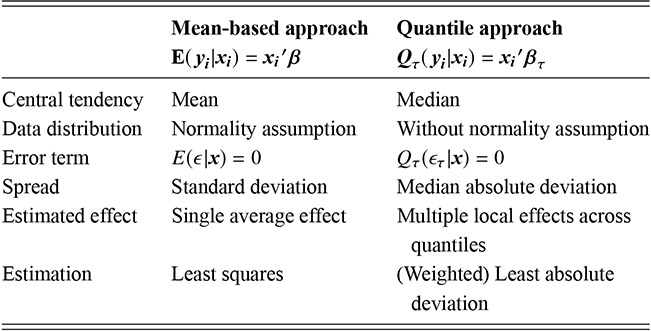

This section has introduced the basic features of quantiles, the role of quantile functions, and the logic of conditional quantiles. According to the above illustrations, Table 1 summarizes the main differences between the mean-based and the quantile approach.

Mean-based approach

| Quantile approach

| |

|---|---|---|

| Central tendency | Mean | Median |

| Data distribution | Normality assumption | Without normality assumption |

| Error term |

|

|

| Spread | Standard deviation | Median absolute deviation |

| Estimated effect | Single average effect | Multiple local effects across quantiles |

| Estimation | Least squares | (Weighted) Least absolute deviation |

The quantile approach can be used to achieve the same goal as the mean-based approach, that is, to represent the central tendency of a sample or distribution. Compared to the mean, the median is more robust to extreme values. While the mean-based approach is often most straightforward under assumptions such as symmetry, homoscedasticity, or normally distributed errors, the quantile approach allows for more flexible distributions and relaxes the conditional-zero-mean assumption of the error term. When data contain heterogeneous units or the distribution of interest is skewed and asymmetric, quantiles provide additional information that would be overlooked when using the mean-based approach.

Mean-based approaches often summarize dispersion with the standard deviation and typically rely on variance-based measures for statistical inference. Without appropriate adjustments, this will lead to biased estimates of standard errors in the presence of heteroscedasticity, that is, when the variance of the error term is not constant. The quantile approach overcomes this problem by estimating local effects at different quantiles. The power of quantiles is not only about the complete description of data or distributions, but also the ability to investigate conditional relations between variables. This is particularly useful when we want to know how changes of the explanatory variables affect the outcome across its entire distribution. Therefore, in addition to robustness checks, quantile models allow researchers to examine distributional effects among heterogeneous political units, which will provide a more complete picture of the relationship between variables of interest.

This does not mean that quantile methods replace mean-based analysis in all applications. Rather, they complement it by expanding the range of questions that can be asked and answered empirically. Building on these foundations, the sections that follow extend the discussion to multivariate settings and show how quantile methods can be applied to a variety of statistical and substantive problems in political science.

2 Quantile Models for Continuous Responses

2.1 Introduction

This section introduces the classical quantile model, which focuses on continuous response variables. In contrast to the univariate setting discussed in the previous section, it demonstrates how to estimate conditional quantiles for the continuous response variable in multivariate settings. In continuous scales, the response variable is represented by values on the real number line, providing rich information commonly seen in empirical political research. Variables of this kind, such as vote shares, party size, and level of turnout, carry substantive meanings through differences in magnitude. Modeling continuous response variables usually eliminates the need for additional data transformations that are common for evaluating discrete response variables discussed in the following chapters. Consequently, the coefficients obtained from quantile models directly reflect how the response variable changes when the explanatory variables shift by one unit at the specified quantile location.

Formally, adopting linear parameterization, quantile regression models the data with the continuous response variable

at

at

th quantile as

th quantile as

(2.1)

(2.1)

where

corresponds to the variables of the data, and

corresponds to the variables of the data, and

is a vector of coefficients associated with the variables at quantile

is a vector of coefficients associated with the variables at quantile

. The core task of quantile regression is to estimate values of

. The core task of quantile regression is to estimate values of

given

given

and

and

, the details of which will be discussed in the following subsection.

, the details of which will be discussed in the following subsection.

2.2 Estimation and Inference in Quantile Regression

In contrast to the conditional mean-based approach that minimizes a squared loss function, the conditional

th quantile as a solution to the above equation is obtained by minimizing an asymmetric loss function

th quantile as a solution to the above equation is obtained by minimizing an asymmetric loss function

, where each component is weighted either by

, where each component is weighted either by

or

or

(Yu & Moyeed, Reference Yu and Moyeed2001):

(Yu & Moyeed, Reference Yu and Moyeed2001):

(2.2)

(2.2)

In this formula,

is a cumulative distribution function, and

is a cumulative distribution function, and

represents the value of the

represents the value of the

th quantile as calculated by Equation (1.4). According to Equation (2.2), the quantile loss function uses all the sample information, instead of splitting the sample, to derive the quantile values. Because the linear loss function depends not on certain covariate values but on covariate orderings, the quantile estimators are more robust than the least squares estimators in the presence of extreme values.

th quantile as calculated by Equation (1.4). According to Equation (2.2), the quantile loss function uses all the sample information, instead of splitting the sample, to derive the quantile values. Because the linear loss function depends not on certain covariate values but on covariate orderings, the quantile estimators are more robust than the least squares estimators in the presence of extreme values.

By solving the first order condition, we have the

th sample objective function evaluated at

th sample objective function evaluated at

as

as

(2.3)

(2.3)

where

(2.4)

(2.4)

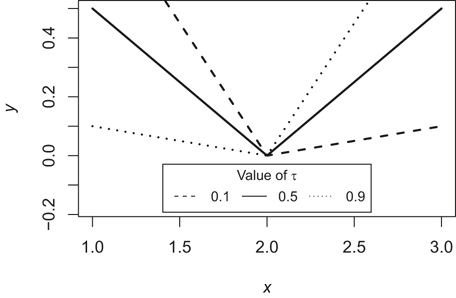

is known as the check function and

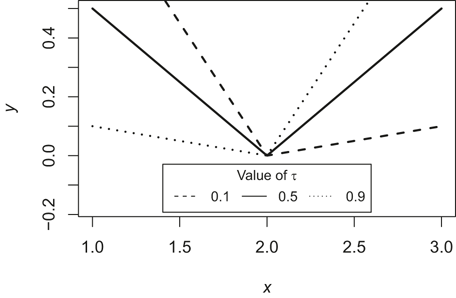

denotes the indicator function. As illustrated in Figure 6, the check function takes different shapes when different quantiles are specified. The function is symmetric when evaluated at the median (0.5th quantile shown by the solid line).

denotes the indicator function. As illustrated in Figure 6, the check function takes different shapes when different quantiles are specified. The function is symmetric when evaluated at the median (0.5th quantile shown by the solid line).

Check functions at different quantiles

Given a linear model

, the

, the

th quantile regression estimator minimizes the above equation by replacing

th quantile regression estimator minimizes the above equation by replacing

with

with

. In the model, we commonly assume

. In the model, we commonly assume

. If

. If

, the model reduces to a median regression. The goal is to estimate the values of

, the model reduces to a median regression. The goal is to estimate the values of

for each

for each

by solving the following minimization problem:

by solving the following minimization problem:

(2.5)

(2.5)

The common solution to this minimization problem is based on the technique of linear programming, which iterates through points and lines on a polyhedral surface to find the optimal estimates. The standard errors and confidence intervals are then calculated based on the asymptotic normality assumption or by repeated sampling using bootstrap methods (Davino, Furno, & Vistocco, Reference Davino, Furno and Vistocco2014; Koenker, Reference Koenker2005). It can be shown that under certain regularity conditions, the estimated quantile coefficients

are asymptotically normal:

are asymptotically normal:

(2.6)

(2.6)

where

and

and

is the conditional density of the error term evaluated at zero (Buchinsky, Reference Buchinsky1998).

is the conditional density of the error term evaluated at zero (Buchinsky, Reference Buchinsky1998).

Alternatively, recent developments in Bayesian methods allow researchers to estimate quantile regression using the Markov chain Monte Carlo (MCMC) sampling procedure (Yu & Moyeed, Reference Yu and Moyeed2001). This is done by imposing appropriate (or uninformative) priors on the parameters to be estimated, and then combining the prior with the likelihood function to form the posterior distribution, which can be subsequently sampled using MCMC algorithms. Compared to the frequentist approach which relies on asymptotic properties, the advantage of the Bayesian estimation is that it provides a natural quantification of estimation uncertainty from random draws of the posterior distribution.

As proved by Koenker and Bassett (Reference Koenker and Bassett1978, 39) (Theorem 3.2 of the paper), there are a number of desirable equivariance properties of the estimated coefficients

that can be statistically interesting to applied researchers:

that can be statistically interesting to applied researchers:

(2.7)

(2.7)

(2.8)

(2.8)

(2.9)

(2.9)

(2.10)

(2.10)

where the first two equations suggest that the coefficients are equivariant under scalar transformations of the response variable. This property is particularly useful for analyzing discrete response variables. The last two equations state that the coefficients are equivariant to a location shift of the response variable and reparameterization of the design matrix. Thus, it provides more flexibility for regression analysis.

To evaluate the goodness of fit of quantile regression, Koenker and Machado (Reference Koenker and Machado1999) also developed an analog of the

-squared measure:

-squared measure:

(2.11)

(2.11)

where

and

and

. Here,

. Here,

and

and

represent respectively the predicted response value and the sample quantile of the response variable without controlling for covariates.

represent respectively the predicted response value and the sample quantile of the response variable without controlling for covariates.

For applied researchers, fortunately, there are statistical software packages that can perform estimation tasks for us. So here I will not delve into the specifics of the various types of estimators and their solution concepts. To demonstrate the utility of quantile estimation tools for analyzing continuous response variables, we can utilize two open-source software packages written in the R language. The first is the quantreg package developed by Roger Koenker and continuously enhanced by numerous statisticians (Koenker, Reference Koenker2025). It offers a diverse set of functions for estimating conditional quantiles using a frequentist approach. The second package, bayesQR, was created by Dries Benoit, Rahim Al-Hamzawi, Keming Yu, and Dirk Van den Poel (Benoit & Van den Poel, Reference Benoit and Van den Poel2017), primarily based on the methods proposed in Benoit and Van den Poel (Reference Benoit and Van den Poel2012) and Benoit, Alhamzawi, and Yu (Reference Benoit, Alhamzawi and Yu2013). This package is used for Bayesian quantile regression estimation. To install and load these packages, we can execute the following codes, which download the package sources from the Comprehensive R Archive Network (CRAN) to the local drive and load the packages into the current working environment.

Code 1.1

1 # Install two packages from CRAN repository

2 install.packages(c("quantreg", "bayesQR"))

3 # Load the packages

4 library(quantreg)

5 library(bayesQR)

In what follows, the quantile estimation will be illustrated using two real-world political examples of ethnic voting and political representation. For the estimation of the data, the analysis will mainly exploit the rq() function from the quantreg package (details on the quantreg package are preserved for the next section). Note that estimating the data of the two examples using the Bayesian approach without informative priors yields similar results.

2.3 Example of Ethnic Voting

To illustrate the quantile model, consider again the ethnic voting example studied by Hadzic, Carlson, and Tavits (Reference Hadzic, Carlson and Tavits2020). The authors argue that community-level experience with wartime violence increases the salience of ethnic identities, making it important for postwar vote choice. Employing a difference-in-differences design on a panel dataset from pre- and postwar elections of Bosnia, Hadzic, Carlson, and Tavits (Reference Hadzic, Carlson and Tavits2020) find strong support for a positive effect of wartime violence on postwar ethnic voting. Yet the theoretical logic of the argument also suggests that this effect may not be uniform across communities. Quantile regression provides a natural way to examine this possibility by asking whether the relationship between wartime violence and postwar ethnic voting differs across the lower and upper parts of the conditional outcome distribution. In this example, different conditional quantiles represent the varying proportions of postwar ethnic voting in different communities. For example, a conditional quantile of 0.1 would roughly represent the bottom 10% communities (about 10 communities in the sample) where the proportion of ethnic voting is lower than the rest 90% of the communities in the sample. Because communities with low proportions of ethnic voting in postwar elections are mostly those communities with low prewar ethnic voting, the quantile approach also allows us to examine the variation of ethnic voting via the lens of diverse cultures of cooperation and inter-ethnic relations in different communities.

In the literature on civil conflict, there are at least two competing theories explaining the impact of wartime violence on the politicization of ethnicity. One theory posits that fears of violence and prewar norms of cooperation will reduce politicization of ethnicity after the war (Bellows & Miguel, Reference Bellows and Miguel2009; Blattman, Reference Blattman2009; Gilligan, Pasquale, & Samii, Reference Gilligan, Pasquale and Samii2014; Voors et al., Reference Voors, Nillesen and Verwimp2012; Wood, Reference Wood2003). This could be attributed to the possibility of more altruistic individuals remaining disproportionately in war-plagued communities, or to the need of the remaining populace to collectively confront threats and psychological distress (Gilligan, Pasquale, & Samii, Reference Gilligan, Pasquale and Samii2014). Conversely, another theory emphasizes the heightened salience of ethnicity and the role of war-enhanced group identification in promoting postwar ethnic voting (Hadzic, Carlson, & Tavits, Reference Hadzic, Carlson and Tavits2020; Wilkinson, Reference Wilkinson2006).Footnote 5 According to this theory, ethnic violence during wartime amplifies rather than diminishes inter-ethnic distrust, rendering ethnic parties a more appealing avenue for post-war representation (Hadzic, Carlson, & Tavits, Reference Hadzic, Carlson and Tavits2020). However, the conflicting theories and their empirical evidence also indicate possible diversity among various subgroups of a population that may react differently to ethnic violence. For example, based on the level of prewar social cohesion, the influence of exposure to ethnic violence during wartime on ethnic voting may fluctuate across different communities. It is plausible to expect that in regions where social cohesion is high and thus ethnic polarization is low, the experience of wartime violence is likely to reduce ethnic voting after the war. However, in regions where there is relatively high ethnic polarization, we may expect a positive effect of wartime violence on ethnic voting. If such heterogeneity exists, revisiting the data with quantile regression could potentially unveil varying subgroup effects that have significant implications but have been largely disregarded in the literature.

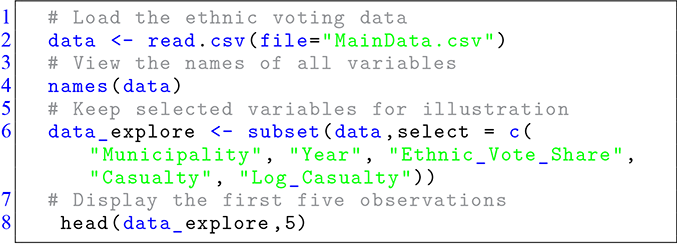

The data collected by Hadzic, Carlson, and Tavits (Reference Hadzic, Carlson and Tavits2020) record election results in Bosnia both before and after the Bosnian Civil War fought between 1992 and 1995, which are publicly available.Footnote 6 After downloading the data, we can load and explore the detailed features of the variables with the following codes.

Code 1.2

1 # Load the ethnic voting data

2 data <- read.csv(file="MainData.csv")

3 # View the names of all variables

4 names(data)

5 # Keep selected variables for illustration

6 data_explore <- subset(data,select = c(

"Municipality", "Year", "Ethnic_Vote_Share",

"Casualty", "Log_Casualty"))

7 # Display the first five observations

8 head(data_explore,5)

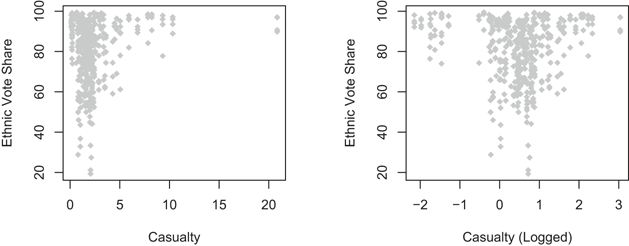

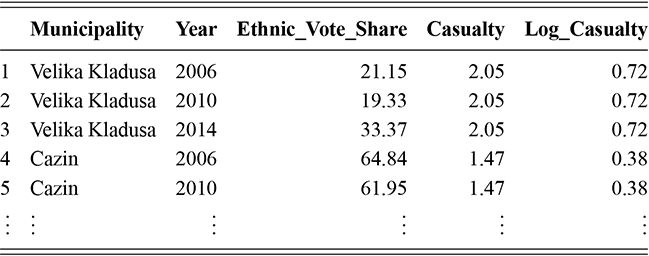

As shown in Table 2, the response variable Ethnic_Vote_Share measures the municipal-level percentage of votes cast for ethnic parties and varies over time. More specifically, the data come from 107 Bosnian communities, including Velika Kladusa and Cazin in years 1990, 2006, 2010, and 2014. The casualty measure records the intensity of ethnic violence and is taken from the Bosnian Book of the Dead, which records the percentage of the total number of confirmed dead and missing against the prewar municipal population (Hadzic, Carlson, & Tavits, Reference Hadzic, Carlson and Tavits2020, 350). The variable Log_Casualty is the log-transformed value of Casualty. Using these measures, we are able to first explore the primary relation between (logged) casualty and ethnic vote share using scatter plots.

Code 1.3

1 # Scatter plot of Casualty and Ethnic_Vote_Share

2 plot(x = data_explore$Casualty, y = data_explore$

# # #Ethnic_Vote_Share, pch = 18, col = "gray",

# # #xlab = "Casualty", ylab = "Ethnic Vote

# # #Share")

3 # # Scatter plot of Log_Casualty and Ethnic_Vote_Share

4 plot(x = data_explore$Log_Casualty, y = data_

# # #explore$Ethnic_Vote_Share, pch = 18, col =

# # #"gray", xlab = "Casualty (Logged)", ylab =

# # #"Ethnic Vote Share")

| Municipality | Year | Ethnic_Vote_Share | Casualty | Log_Casualty | |

|---|---|---|---|---|---|

| 1 | Velika Kladusa | 2006 | 21.15 | 2.05 | 0.72 |

| 2 | Velika Kladusa | 2010 | 19.33 | 2.05 | 0.72 |

| 3 | Velika Kladusa | 2014 | 33.37 | 2.05 | 0.72 |

| 4 | Cazin | 2006 | 64.84 | 1.47 | 0.38 |

| 5 | Cazin | 2010 | 61.95 | 1.47 | 0.38 |

|

|

|

|

|

|

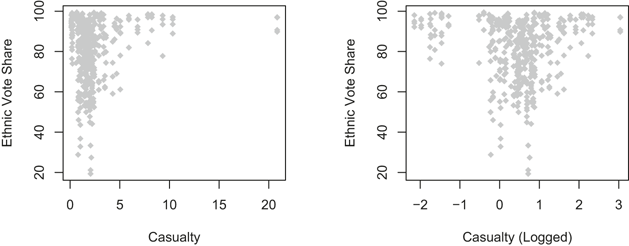

The scatter plots in Figure 7 reveal that the original measure of casualty is right-skewed (left panel), but is close to a normal distribution in the logarithmic scale (right panel). Therefore, as with Hadzic, Carlson, and Tavits (Reference Hadzic, Carlson and Tavits2020), the logged version of the casualty measure is adopted for the regression analysis. The quantreg package is used to estimate the conditional quantiles, with the parameter tau specifying the quantiles to be estimated. For the values of tau, a range of quantiles from 0.1 to 0.9 are specified. Here, lower quantiles may be interpreted as pertaining to communities where the proportion of ethnic voting is relatively low, and upper quantiles represent those communities where votes are more divided along ethnic lines. Given control variables, conditional quantiles can also be interpreted as capturing different positions in the distribution of ethnic vote share across communities, which may reflect varying degrees of ethnic political alignment. This allows us to ask whether the association between wartime violence and ethnic voting differs systematically across communities located at different points of the ethnic-voting distribution.

Scatter plots of correlation between casualty(a)/logged casualty (b) and ethnic vote share

For illustrating the quantile estimation of the effects of wartime violence on ethnic voting, let us first consider a simple model of the relation between the two variables. A more comprehensive model in the subsequent analysis will also take into account the spatial and temporal variation. Here, the rq function from the quantreg package is used (Koenker, Reference Koenker2025), and the computational codes are shown in the following. The results can be visualized and printed using the functions plot and summary.

Code 1.4

1 # Estimate the quantile model at quantiles from 0.1 to 0.9

2 mod1 <- rq(Ethnic_Vote_Share ~ Log_Casualty, data = data, tau = seq(0.1,0.9,0.1))

3 # Plot point estimates

4 plot(mod1)

5 # Summarize the estimation results with confidence intervals

6 summary(mod1)

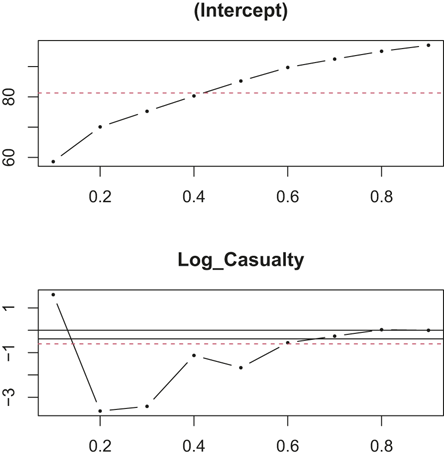

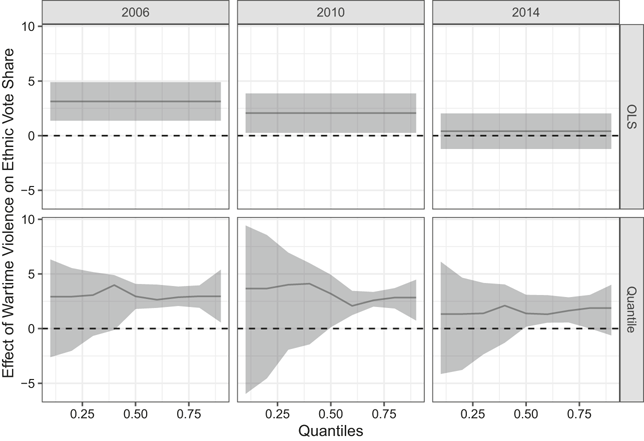

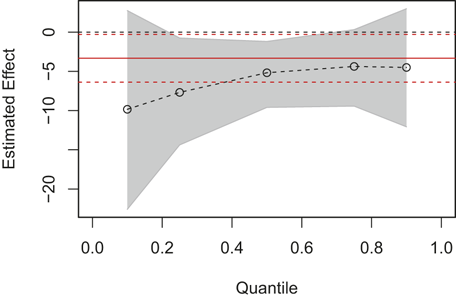

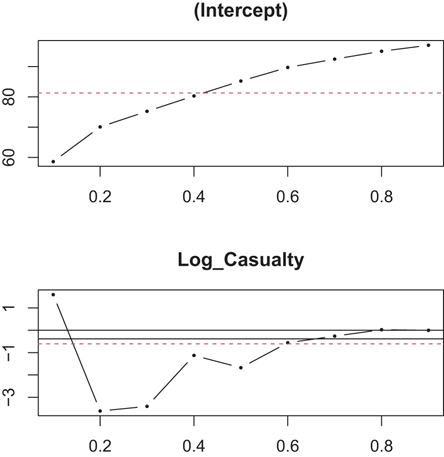

Figure 8 shows the point estimates of the effects for the intercept and casualty at different quantiles, where the dashed horizontal lines represent the OLS estimates. In both panels of the figure, the x-axis represents different quantile levels, and the y-axis shows the estimated effects of a variable at different quantiles, with the dotted line indicating how the effects change with increasing quantile levels. Compared to a single average effect estimated by the OLS, the U-shaped quantile estimation curve of casualty in the lower panel demonstrates that the effects of casualty on ethnic voting may differ across subgroups. In the lower quantiles less than 0.6 (except for 0.1), the effects are negative, while in the upper quantiles higher than 0.6, the effects become positive. These results reveal significant differences in the effects of casualty on ethnic voting between communities with diverse levels of ethnic voting in wartime. Because quantiles are measured on shares of ethnic votes (and thus ethnic polarization) across communities, it indicates that exposure to violence may affect ethnic voting differently depending on the ethnic polarization in each community. In particular, in lower quantiles where ethnic polarization is relatively low, the effects of wartime violence (Log_Casualty) on ethnic voting become negative, which suggests that in communities with low ethnic polarization, exposure to ethnic violence is likely to increase inter-ethnic trust and postwar social cohesion (and thus reduces the proportion of ethnic voting). This is the case for Bosnian communities such as Centar Sarajevo, Novo Sarajevo, Srebrenik, Tuzla, and Velika Kladusa, where the average proportion of ethnic voting is lower than the 0.1th quantile of the whole sample (i.e., 65% ethnic vote share). However, as demonstrated by the positive effects in the upper quantiles, the opposite is true in other communities where ethnic polarization is high. Overall, the results show that in lower quantile regions where the proportion of ethnic voting is relatively low, the OLS is likely to overestimate the effect of casualty, while in upper quantiles it is more likely to underestimate the effect.

Point estimates of quantile effects for ethnic voting example

The simple bivariate model is useful for illustration, but it leaves open the possibility that the estimated pattern is confounded by differences across years and municipalities. To better account for potential confounding factors, we now examine a more comprehensive model that takes into account the spatial and temporal variation. More specifically, we follow the model specification and the difference-in-differences (DID) design of Hadzic, Carlson, and Tavits (Reference Hadzic, Carlson and Tavits2020), with dummy controls of years before and after the civil war. The analysis also includes the fixed effects of regions. The following codes show the details of the quantile estimation procedure for the ethnic voting data.

Code 1.5

1 # DID design: Generate dummy matrix distinguishing between years before and after war

2 dummy.matrix <- as.matrix(cbind(as.numeric(dat_violence$Year == 2006), as.numeric(dat_violence$Year==2010), as.numeric(dat_violence$Year==2014)))

3 # Quantile estimation with municipality-fixed effects

4 mod2 <- rq(Ethnic_Vote_Share ~ Log_Casualty:dummy.matrix+dummy.matrix+Municipality-1, data = data, tau = seq(0.1,0.9,0.1))

5 # Summarize the results

6 mod2_est <- summary(mod2)

7 # Extract coefficient estimates of the main iv. while omitting others

8 extract_coef <- function(x) return(x$coefficients[111:113,])

9 # Put coefficients into a single data frame

10 coef_df <- as.data.frame(do.call("rbind",lapply(mod2_est, extract_coef)))

11 coef_df$Year <- rep(c(2006,2010,2014),9)

12 coef_df$quantile <- rep(seq(0.1,0.9,0.1),each = 3)

13 names(coef_df)[2:3] <- c("lower","upper")

14 # Visualize the coefficients

15 library(ggplot2)

16 ggplot(coef_df,aes(x = quantile, y = coefficients))+

17 geom_line()+

18 geom_ribbon(aes(ymin = lower, ymax = upper),alpha = 0.2)+

19 facet_wrap(~Year)+

20 geom_hline(yintercept = 0,linetype = "dashed")+

21 xlab("Quantiles")+

22 ylab("Effect of Wartime Violence on Ethnic Vote Share")+

23 theme_bw()

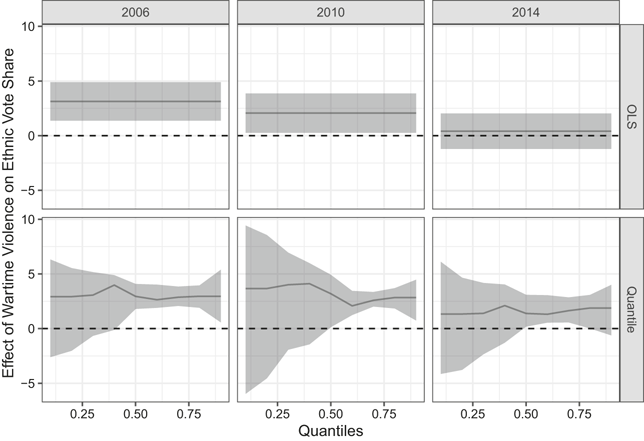

The results of the coefficient estimates of the OLS and quantile regression are displayed in Figure 9, which shows the results in 2006 (a – left panel), 2010 (b – middle panel), and 2014 (c – right panel) in comparison to the baseline year 1990 in the prewar period. The OLS estimation follows Model 1 in table 1 of Hadzic, Carlson, and Tavits (Reference Hadzic, Carlson and Tavits2020, 353) with clustered (on municipality and year) robust standard errors. Compared to the average positive estimates by the OLS, all three panels of the figure show that while the positive effects of wartime violence on ethnic voting are evident in the upper quantiles where ethnic voting is more common, the effects are insignificant in the lower quantiles (quantiles lower than 0.5). Compared to the results in 2006 and 2010, the reduced effect of wartime violence on ethnic voting in the middle and upper quantiles in 2014 also indicates that the impact of wartime memory of ethnic violence seems to be decreasing at the community level.

Estimated effects of wartime violence on ethnic vote share over postwar years and across quantiles

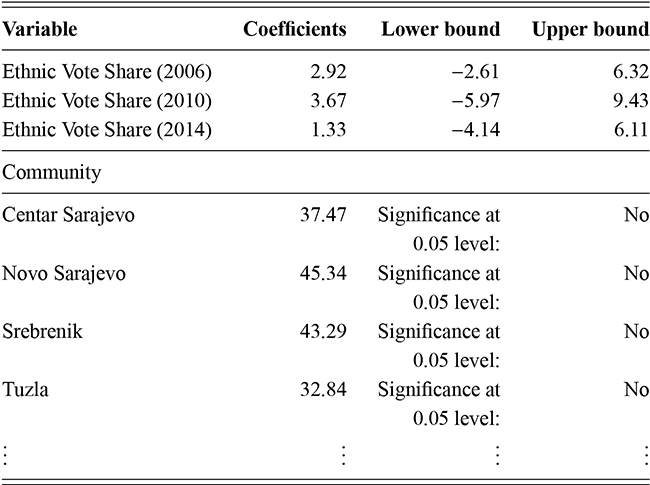

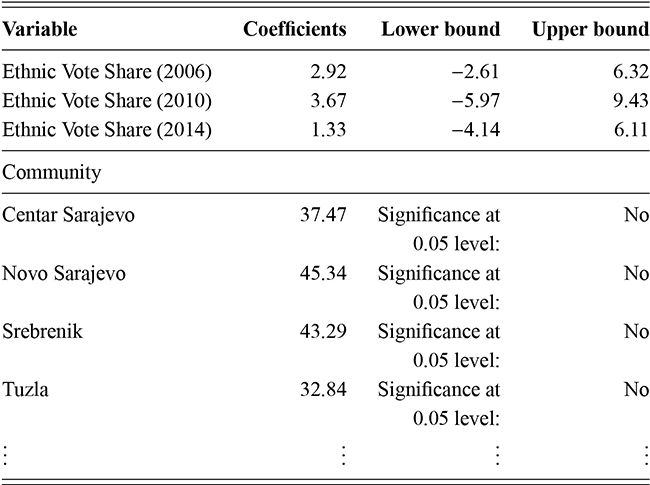

Given that communities with low proportions of ethnic voting in postwar elections are mostly those communities with low prewar ethnic voting, it is plausible to associate the level of ethnic voting with the culture of cooperation and inter-ethnic relations in different communities. For example, as shown in Table 3, for communities such as Centar Sarajevo, Novo Sarajevo, Srebrenik, and Tuzla, where wartime violence has no discernible effects, they are all below the 0.1th quantile (i.e., around 65%) measured by the proportion of ethnic voting in both pre- and postwar periods.Footnote 7 And except for Srebrenik, the rest of these communities have lower prewar ethnic concentration measured by Herfindahl–Hirschman indices compared to the average of the sample (Hadzic, Carlson, & Tavits, Reference Hadzic, Carlson and Tavits2020). This implies that in regions without a long-standing tradition of ethnic voting, the mechanism by which wartime violence affects ethnic voting may be different. In areas with a strong culture of cooperation and mild ethnic divisions, it may be easier to return to this norm after the ethnic conflict without a heightened risk of ethnic polarization. This process is less likely or much slower in regions where the culture of cooperation is absent.

Table 3 Long description

The table shows quantile regression results at the 0.1th quantile for ethnic vote share and community fixed effects in Bosnian municipalities. The first section lists coefficients for ethnic vote share in 2006 (2.92), 2010 (3.67), and 2014 (1.33), with 95% confidence intervals spanning -2.61 to 6.32, -5.97 to 9.43, and -4.14 to 6.11, respectively. The second section presents fixed-effects for selected communities: Centar Sarajevo (37.47), Novo Sarajevo (45.34), Srebrenik (43.29), and Tuzla (32.84). None of these fixed-effects are significant at the 5% level. Additional communities are included in the model but omitted here. These results highlight that communities with low prewar ethnic voting remain at the low end of the ethnic vote distribution postwar, suggesting a persistent culture of inter-ethnic cooperation.

Note: Fixed-effects of other communities omitted here. The upper and lower bounds correspond to the 95% confidence interval.

These empirical findings from estimating the quantile model help to reconcile the two competing theories of the effect of wartime violence on ethnic voting. This suggests that the concrete effect of violence may be dependent on the prior inter-ethnic relations in different communities. Thus, even this simple replication study using quantile models opens up interesting possibilities for further research, which could delve deeper into the local effects that explain the variation of ethnic voting between different regions.

2.4 Example of Political Representation

As another example, political representation by parties is usually not about reflecting average societal preferences. Parties tend to have closer ties to certain societal groups, and more conflictual relations with others. Because these relations can be disrupted or enhanced by external threats, Weschle (Reference Weschle2019) argues that economic crises impact the way parties represent the society, which further depends on whether the parties have cooperative or conflictual relations with different societal groups. Under external threats, political parties need not only to be responsive to their own constituencies, but also be responsible to other societal groups in order to unite the whole nation to better cope with the threats (Bueno de Mesquita, Reference Bueno de Mesquita1981; Chowanietz, Reference Chowanietz2011; Indridason, Reference Indridason2008; Lijphart, Reference Lijphart1996). This consequently leads to changes in the parties’ societal relations with the groups they are closest to and least close to. More specifically, parties have to trade-off between representing the interests of their own constituencies faithfully and being responsive to other societal groups for a collective effort in handling external threats. Therefore, in times of crises, we would expect empirically that parties’ relations with the societal group they are closest to become less cooperative, while their relations with the groups they are least close to become less conflictual (Weschle, Reference Weschle2019). However, these heterogeneous relations are difficult to investigate using the traditional mean-based models, which merely reveal a single average effect.

To investigate the influence of economic crises on the political representation of diverse societal groups, Weschle (Reference Weschle2019) developed a latent network model, which draws inferences about the relationship between political parties and societal groups. Subsequently, he utilized quantile models to analyze the effects of economic crises on parties’ relationships with different types of societal groups. The latent network model allows for identifying parties’ societal relations by estimating the cooperation scores, which measure the level of cooperation or conflict between a party and a societal group for eleven eurozone countries between 2001 and 2011. Using this measure as the dependent variable, the quantile models estimate varying effects of economic crises on political representation, with different quantiles capturing different parts of the latent cooperation-score distribution. More specifically, higher quantiles in the model indicate the societal groups with which parties have better initial relations, while lower quantiles focus on those groups that have a less cooperative relationship with the parties.

To demonstrate how quantile models improve our substantive understanding of political representation in times of crises, we replicate the analysis of Weschle (Reference Weschle2019). The following codes load the data and draw quantile fitting lines against a scatter plot. Here, the variable coopscore_1 represents a random draw of the cooperation scores from the latent network model of political representation, and GDP growth per capita is used to examine the impact of economic crises.Footnote 8

Code 1.6

1 # Load and clean data

2 library(foreign)

3 data <- read.dta("data.dta")

4 dat = data[which(data$type==3),]

5 # Scatter plot and quantile fitting lines

6 ggplot(dat, aes(x = gdppcgrowth, y = coopscore_1)) +

7 geom_point(color = "gray", alpha = 0.5,

8 size = 2, shape = 1 ) +

9 geom_quantile(quantiles = c(0.01, 0.5, 0.99),

10 aes(linetype = factor(after_stat(quantile))),

11 linewidth = 0.8, color = "black",

12 show.legend = TRUE) +

13 scale_linetype_manual(

14 name = "Quantiles",

15 values = c("dotted", "solid", "dashed"),

16 labels = c("0.01th Quantile", "0.5th Quantile (Median)", "0.99th Quantile")) +

17 labs(x = "GDP Growth per Capita (%)",

18 y = "Cooperation Score") +

19 theme_bw(base_size = 12) +

20 theme(plot.title = element_text(

21 face = "bold", size = 14,

22 hjust = 0.5, margin = margin(b = 10)),

23 axis.title = element_text(face = "bold"),

24 panel.grid.major = element_line(linewidth = 0.2),

25 panel.grid.minor = element_blank(),

26 legend.position = c(0.3, 0.85),

27 legend.background = element_rect(fill = "white", colour = "white"),

28 legend.key.width = unit(1.5, "cm"),

29 plot.caption = element_text(hjust = 0, face = "italic")) +

30 coord_cartesian(ylim = c(-0.15, 0.15)) +

31 annotate(

32 "text", x = Inf, y = -Inf,

33 label = "Gray circles: Observation points\nLine types: Quantile regression estimates",

34 hjust = 1.1, vjust = -0.5,

35 size = 3, color = "black")

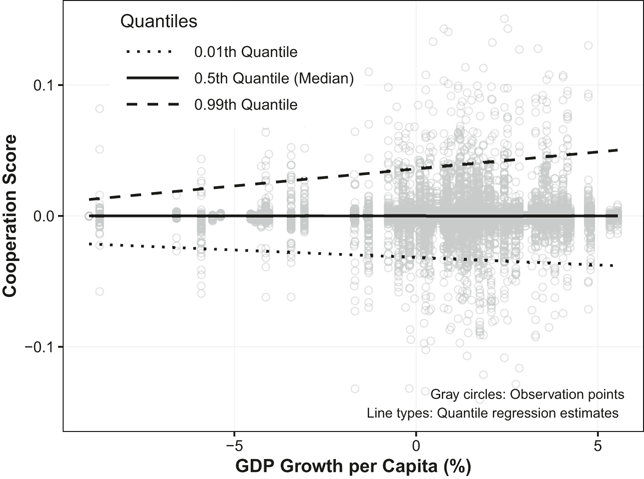

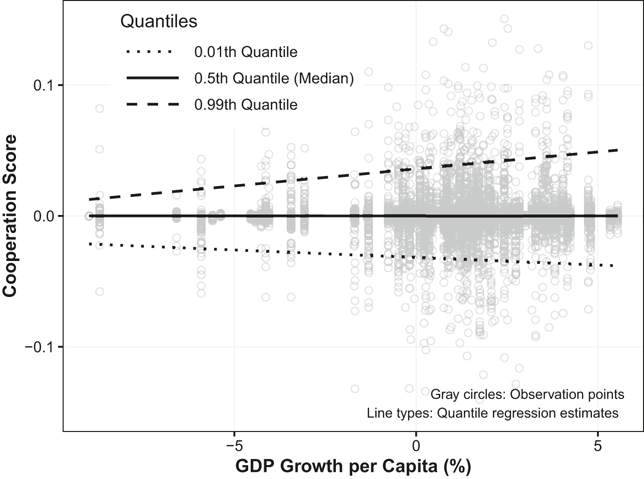

Figure 10 shows the three quantile fitting lines in the 0.01th, 0.5th, and 0.99th quantiles that are superimposed onto the scatter plot between GDP growth per capita and cooperation scores. The upper quantile (0.99th quantile) represents societal groups with which a party has a cooperative relationship, while the lower quantile (0.01th quantile) represents those with which a party has a conflictual relationship. The median (0.5th quantile), in contrast, represents groups with which a party has neither a close nor conflictual relation.

Scatter plot of GDP growth per capita and cooperation scores between political parties and societal groups

According to the fitted quantile lines in Figure 10, there is no discernible effect at the median, but the opposing effects at the lower and upper quantiles of 0.01 and 0.99 are visible. This suggests that the impact of the economic crisis on the relation between a party and a societal group may vary depending on the initial relationship between them. Specifically, as the economy expands, it will enhance parties’ cooperative relations with societal groups they are most aligned with (dashed line of the 0.99th quantile), whereas economic crises will damage these relationships, resulting in reduced cooperation. Conversely, as indicated by the dotted fitting line for the 0.01th quantile, during crises, parties endeavor to improve their relations with societal groups they originally have conflictual relations with. These results from the quantile models suggest that economic crises tend to disrupt representation and motivate politicians and parties to “put politics aside” by cooperating more with previously distant groups (Weschle, Reference Weschle2019). If researchers were to rely solely on mean-based models, these new theoretical and empirical perspectives would likely have gone uninvestigated.

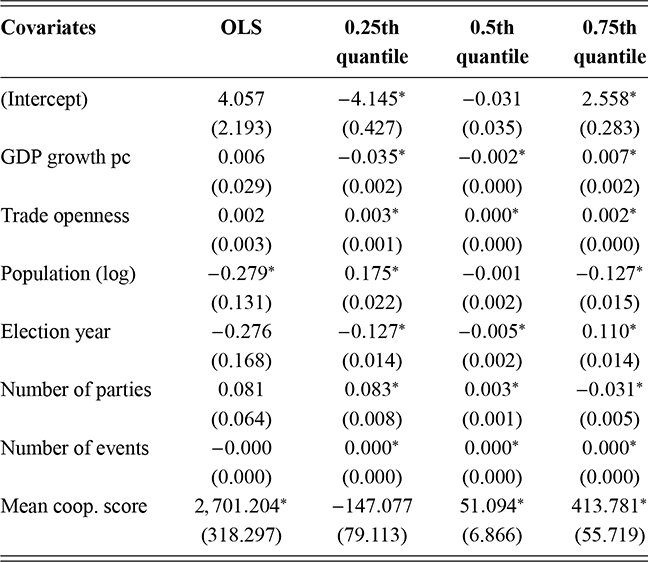

Note that the above analysis simply examines the relation between the main explanatory variable and the response variable. To account for potential confounding variables, the next step is to include them in the full model specification. Weschle’s (Reference Weschle2019) study includes control variables such as trade openness, population, election year, number of parties, number of events in political communication, and mean cooperation scores for each country and year, which are also included in this replication analysis. To demonstrate the varying effects of economic conditions on political representation, we can specify the lower (0.25th), middle (0.5th), and upper (0.75th) quantiles and estimate the respective conditional quantile effects.Footnote 9 Using the first random draw of cooperation scores, the following codes complete the task and summarize the estimation results for each quantile. Note that compared to the original analysis, the response variable is rescaled by a factor of 1,000 to make the estimates more interpretable.

Code 1.7

1 # Rescale the response variable by a factor of 1000

2 dat$coopscore_1_rescale = dat$coopscore_1 * 1000

3 # Specify quantile model

4 mod1 <- rq(coopscore_1_rescale ~ gdppcgrowth + openness + population_log + elec + nparties + events + coopscore_mean_1, tau = c(0.25,0.5,0.75) ,data = dat)

5 # Plot the coefficients

6 plot(mod1)

7 # Summarize the results

4 summary(mod1)

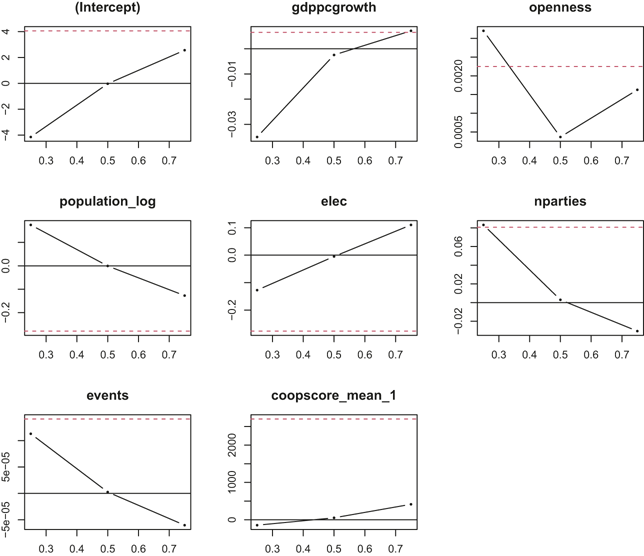

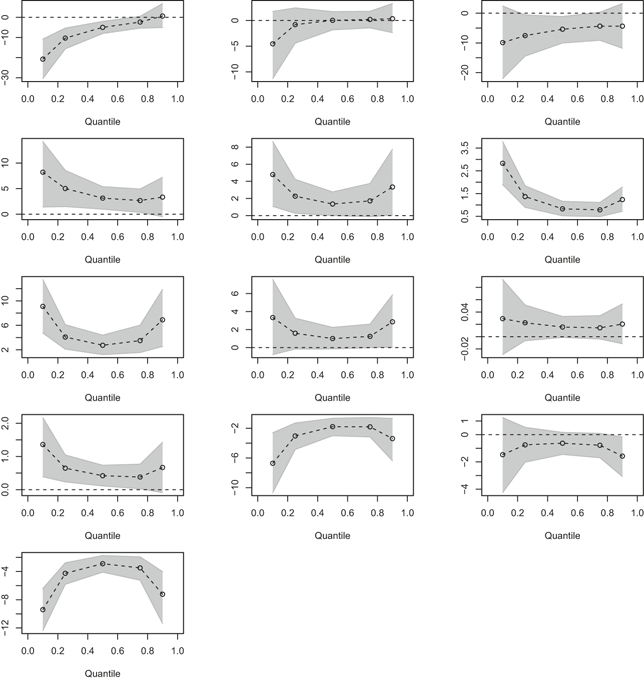

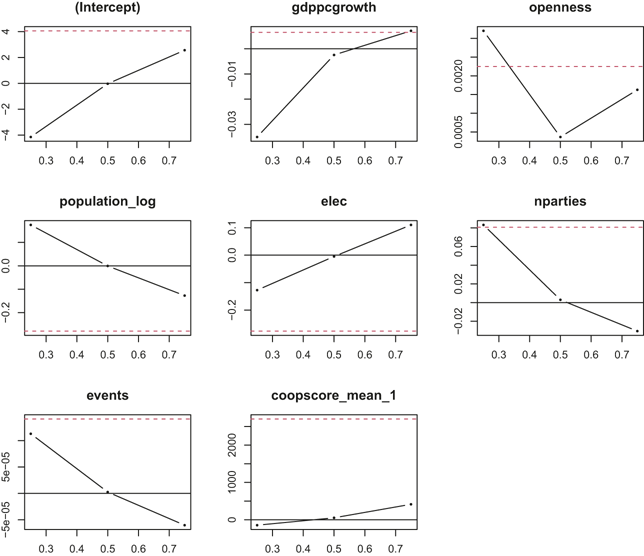

Figure 11 demonstrates that the quantile model reveals considerable variation of the effects of different covariates across quantiles compared to the OLS estimates shown by the dashed horizontal lines. For all the control variables, including the intercept, the estimated coefficients have opposite directions between the lower and upper quantiles. The large discrepancy between estimates of the OLS and median regression (quantile model evaluated at 0.5th quantile) also suggests that the heterogeneity in the data cannot be well accounted for by the mean-based model.Footnote 10

Coefficient estimates at three conditional quantiles (0.25th, 0.5th, and 0.75th) for political representation example

Note: Black dotted lines represent quantile estimates and horizontal dashed lines represent OLS estimates.

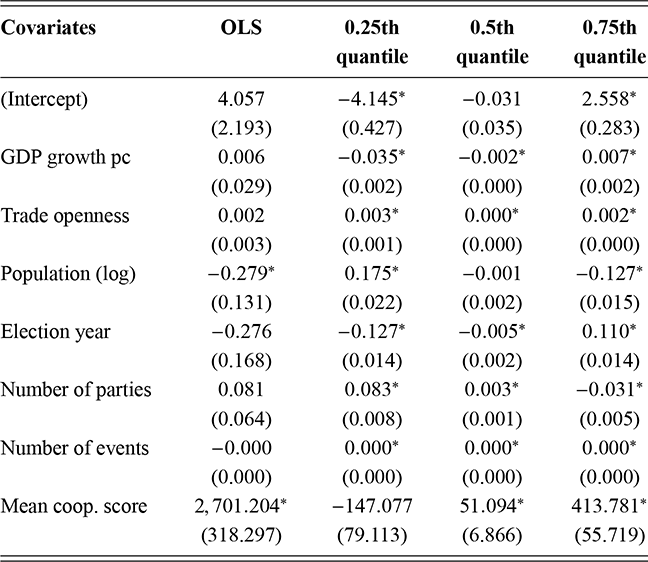

In addition to the average estimates by the OLS, the results of Table 4 indicate that the effect of GDP growth per capita on political representation varies across quantiles. In the lower quantile (0.25th quantile) of the response variable, the effect is significantly negative, while in the upper quantile (0.75th quantile) the effect is significantly positive. Although the median estimate is statistically distinguishable from zero, its magnitude is substantively very small. This suggests that on average economic conditions have little effect on political representation, but when the economy is doing well, parties are more likely to represent their core constituents. Conversely, when the economy is doing poorly, parties appear to move toward less conflictual relations with groups with which they originally conflict. Thus, this finding indicates that in times of economic crisis, political parties must navigate a distinct balance between catering to their own constituencies and addressing the interests of diverse societal groups to foster national unity. Compared to normal times, the relation between political parties and the societal groups they are least close to becomes less conflictual during periods of crisis. This is the kind of heterogeneous adjustment that a mean-based model is poorly equipped to detect.

Table 4 Long description

The table presents O L S and quantile regression results (0.25th, 0.5th, 0.75th quantiles) for a political representation outcome. Covariates include intercept, G D P growth per capita, trade openness, population (log), election year, number of parties, number of events, and mean cooperation score. Coefficients show substantial variation across quantiles: G D P growth is significantly negative at the 0.25th quantile, near zero at the median, and positive at the 0.75th quantile. Trade openness and population effects also vary by quantile. Mean cooperation score is strongly positive in O L S and upper quantiles. Asterisks indicate 95% significance. These results highlight that economic and structural factors affect political representation differently across the distribution, reflecting heterogeneous party responsiveness under different economic conditions.

The asterisk * denotes significance at 95% confidence level.

Standard errors are shown in parentheses.

As also shown in the table, the coefficients of the rest of the variables, such as population, election year, number of parties, and mean cooperation score, are significantly different between lower and upper quantiles.Footnote 11 These results are important for understanding democratic representation in times of crisis, which would remain unknown without exploring the quantile behavior of the explanatory variables over the distribution of the response variable.

To eliminate concerns about potential heterogeneity across countries and over years, we may also control for the country- and/or year-fixed effects. For simplicity, the example presented here uses a single draw of cooperation scores as the response variable. Yet the example is sufficient to demonstrate the substantive payoff of quantile analysis. To have a more complete analysis, more observations can be easily included from the data of Weschle (Reference Weschle2019), which will generate similar results.

2.5 Summary

The discussion in this section has shown that, although mean-based models remain central to empirical analysis, they are not always well suited to questions involving substantial heterogeneity. Concentrating on the means has prevented researchers from using more suitable techniques for analyzing heterogeneous political phenomena. For many political studies, the quantile approach allows for the evaluation of heterogeneous data that cannot be satisfactorily analyzed by mean-based models. It not only provides comprehensive summary statistics for the location and spread of a given sample, but also reveals a more detailed relationship between the dependent and explanatory variables. The utility of quantile models is not limited to examining heterogeneous data. Even when the primary interest is not heterogeneity itself, quantile models can still serve as a valuable diagnostic by revealing whether empirical relationships are stable across the distribution.

Using the examples of ethnic voting and political representation, this section illustrates the utility of the quantile approach for applied political research examining continuous response variables in multivariate settings. It shows how quantile models can be beneficial for exploring heterogeneous political units and identifying varying effects across the distribution of the outcomes. The new results have unveiled intriguing insights that were previously undisclosed by the traditional mean-based models.

For instance, in the case of the ethnic voting example, contrary to the average finding indicating a singular positive effect of wartime violence on postwar ethnic voting, the results based on the quantile model demonstrate that the effect is contingent on the degree of prewar ethnic polarization. In communities where there is a strong prewar norm of inter-ethnic cooperation, it is much easier to return to the norm without an increased risk of postwar ethnic polarization. Conversely, in communities with historically high ethnic divisions, the memory of conflict may instead intensify ethnic polarization. Revisiting the example of political representation also reveals heterogeneous effects of economic crises on political representation of parties with different societal groups. While economic conditions have little impact on political representation on average, parties tend to be more responsive to groups with which they originally conflict when the economy falters. These findings provide crucial insights that would otherwise remain unknown.

Overall, these examples highlight the broader contribution of quantile models to political analysis. They allow researchers to move beyond average effects, to detect substantively meaningful heterogeneity, and to generate more thorough interpretations of political processes. The sections that follow build on this foundation by extending the quantile framework to additional outcome types and modeling settings.

3 Quantile Models for Binary Choices

3.1 Introduction