Introduction

New technologies introduced in financial markets are driving transformations of traditional institutions and governance modes rather than simply enhancing existing capacities (Campbell-Verduyn et al., Reference Campbell-Verduyn, Goguen and Porter2017). Here we ask how emerging technologies are transforming the governance of international taxation, particularly the issue of corporate tax avoidance. International tax avoidance is typically characterized as a cat and mouse game in which tax avoiders hide asset information from regulators, organizing information asymmetries in structures conceptualized as Global Wealth Chains (Seabrooke and Wigan, Reference Seabrooke and Wigan2017). As recent research has shown, these games have increased in sophistication, including through iterations of state strategy aligned with financial interests (Ní Chasaide and Ó Riain, Reference Ní Chasaide and Ó Riain2025). The rise of new technologies, however, particularly big data analytics and artificial intelligence, is changing how information, and information as data, is treated (Westermeier, Reference Westermeier2020; Hayes, Reference Hayes2021). These technologies are developing rapidly and upending several industries and fields (Petry, Reference Petry2021; Campbell-Verduyn and Hütten, Reference Campbell-Verduyn and Hütten2022). In the area of international taxation, new technologies may upend the logic of information asymmetry as the main mode of optimization.

This article responds to calls, especially in this journal (Samman et al., Reference Samman, Boy, Coombs, Hager, Hayes, Rosamond, Wansleben and Westermeier2022), to study how technology-driven companies are changing the relationship between finance and society. We know that the ‘platformization’ of finance has changed the materiality of data (Langley and Leyshon, Reference Langley and Leyshon2017; Westermeier, Reference Westermeier2020), that assetization is as much a technoscientific as financial process (Golka, Reference Golka2021), and that tech innovations in finance create new structural dependencies and asymmetries between the actors involved (Wood et al., Reference Wood, King, Catlow and Scott2016; MacKenzie, Reference MacKenzie2019; Svetlova and Arnoldi, Reference Svetlova and Arnoldi2026). This article asks: How do algorithmic technologies change assumed client-supplier-regulator relationships? Is the structural power wielded by those dominating transnational financial and legal management taking on a new form (Strange, Reference Strange1996)? Is this form articulated through new infrastructures (Bernards and Campbell-Verduyn, Reference Bernards and Campbell-Verduyn2019; Ylönen et al., Reference Ylönen, Raudla and Babic2024; Coombs, Reference Coombs, Westermeier, Campbell-Verduyn and Brandl2025)? How much emphasis should be placed on those who control the flows of financial information through proprietary technologies? Are forms of opacity in information flows moving from secret relations between suppliers and clients to avoid compliance – the emphasis in much work on GWCs (Sharman, Reference Sharman2010; Helgadóttir, Reference Helgadóttir2023) – into the opacity of algorithmically determined machine-based reasoning (Burrell, Reference Burrell2016; Hansen and Thylstrup, Reference Hansen and Thylstrup2024)?

To address these questions, we focus on the development of TaxTech and, in particular, three separate technologies being developed for distinct practices within international taxation: blockchains to ensure real-time verifiability of asset ownership; generative AI to minimize laborious manual processes in tax compliance; and algorithmic scenario planning for tax-planning purposes. These technologies can potentially change power dynamics between tax advice suppliers, their clients, and regulators. They can also heighten the infrastructural power of suppliers – their capacity to govern economic activity by controlling key devices within financial and informational infrastructures through which markets and policy interventions are operationalized (Coombs, Reference Coombs, Westermeier, Campbell-Verduyn and Brandl2025).

We evaluate the impact of technologies on the tax field using the Global Wealth Chains (hereafter GWC) framework, which explicitly focuses on power distribution among key actors – the suppliers, clients, and regulators – of a given asset structure (Finér and Ylönen, Reference Finér and Ylönen2017; Seabrooke and Wigan, Reference Seabrooke and Wigan2017; McKenzie and Atkinson, Reference McKenzie and Atkinson2020; Christensen et al., Reference Christensen, Seabrooke and Wigan2022). GWC research has identified how professionals, as suppliers, use various ‘legal affordances’ to engage in cat and mouse games (Grasten et al., Reference Grasten, Seabrooke and Wigan2023), especially by shifting profits to low-tax jurisdictions (Finér and Ylönen, Reference Finér and Ylönen2017; Stausholm, Reference Stausholm, Seabrooke and Wigan2022). Recent research points to how wealth chains are changing as algorithmic technologies are introduced. For example, in cities the use of algorithmic technologies can accelerate wealth chain extractivism, enabling racialized spatial restructuring around high-wealth ‘sovereign enclaves’ and devalued ‘sacrifice zones’ (McKenzie, Reference McKenzie2026). New technologies can be combined with legal affordances to the benefit of ‘secrecy-seeking capital’ (Ylönen et al., Reference Ylönen, Raudla and Babic2024). Capital concerned with tax savings rather than secrecy per se, however, may interact differently with new technologies. Such capital seeks to, for example, minimize the risks of tax disputes and controversies while keeping an eye on the wealth chain to empower those controlling the firm and to protect shareholder value (Leaver and Martin, Reference Leaver and Martin2021; Robé et al., Reference Robé, Seabrooke and Wigan2026).

Our research shows how new technologies are being designed by tax advisors, a development which is expected to significantly change the dynamics of tax planning, tax reporting, and tax auditing. What can be understood as new captive forms of GWCs are emerging, where lead suppliers control financial and legal technologies which seek not to create distance from regulators, but optimize the compliant use of existing legal affordances using algorithmic technologies.

In what follows, we first outline the GWC literature and how it is challenged by technologies which signal a move from cat and mouse games to strategic management of assets under conditions of compliance. We then discuss how new technologies are impacting regulation of markets and multinational enterprises (MNEs). After briefly discussing our methods, we outline three TaxTech examples emerging to rearticulate GWCs. We focus on how these three distinct technologies – algorithmic scenario planning, generative AI, and blockchains – are transforming tax governance and the relationships between taxpayers, tax advisors, and tax authorities.

Global wealth chains meet tech

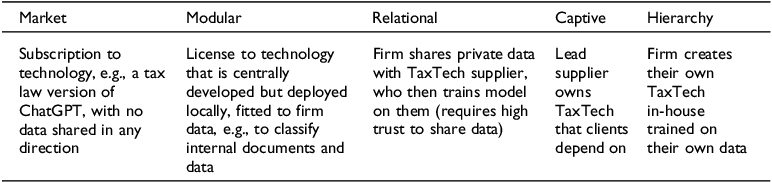

Research on GWCs points to how MNEs and elites use complex multijurisdictional layers of corporate entities to exploit legal affordances, including those embedded in reporting regimes, and to heighten information asymmetries between suppliers/clients and regulators (Castro and Seabrooke, Reference Castro and Seabrooke2026). The GWC framework has been widely applied, to cases such as real estate (McKenzie and Atkinson, Reference McKenzie and Atkinson2020; McKenzie et al., Reference McKenzie, Atkinson and Ingianni2023), art luxury goods (Helgadóttir, Reference Helgadóttir2023), beer and pharmaceuticals (Dahl, Reference Dahl, Seabrooke and Wigan2022), health care facilities (Bůžek and Scheuplein, Reference Bůžek and Scheuplein2022), and many others, placing such cases within a typology that mirrors that of the popular Global Value Chains (GVCs) literature (Gereffi et al., Reference Gereffi, Humphrey and Sturgeon2005). Like the GVC typology, work on GWCs has located five types of chains, distinguished by the complexity of transactions between the parties involved and the dominance of lead suppliers in controlling financial and legal technologies. These range from the market type, where little coordination is needed, through to partial customization in the modular type, trust-based relations with high switching costs in the relational type, strong control of financial and legal technologies in the captive type, and full integration under a lead supplier in the hierarchy type (Seabrooke and Wigan, Reference Seabrooke and Wigan2017). While research shows how GVCs and GWCs are often ‘entangled’ in practice (Bair et al., Reference Bair, Ponte, Seabrooke and Wigan2023; Wigan et al., Reference Wigan, Seabrooke, Ponte and Bair2024) – these governance modes are useful heuristics to think about where power lies and how transaction complexity mixes with information asymmetries between suppliers, clients, and regulators.

The Big Four global accounting firms – Deloitte, Ernst & Young, KMPG, and PriceWaterhouseCoopers – are prominent examples of suppliers that typically dominate within captive GWCs (Hearson, Reference Hearson2018; Stausholm et al., Reference Stausholm, Murphy and Seabrooke2025). These firms are often studied as exemplars of the cat and mouse tax avoidance game, enabling secrecy, creating obfuscation, and encouraging the opacity of information available to regulators (Ajdacic et al., Reference Ajdacic, Heemskerk and Garcia-Bernardo2021; Elemes et al., Reference Elemes, Blaylock and Spence2021). They are also known to be organizations that have expanded their geopolitical influence and actively monitor political and activist attempts to control them (Boussebaa and Faulconbridge, Reference Boussebaa and Faulconbridge2019; Christensen and Seabrooke, Reference Christensen and Seabrooke2022).

In the past 15 years, regulators have made strides in attempting to lessen the degree of information asymmetry between themselves and both the Big Four as suppliers of tax services as well as their key clients in large MNEs. The organization of tax-minimizing opacities has been targeted by regulators, who have made strong efforts at increased financial transparency, especially for the largest MNEs. Most prominent among these efforts has been the Organisation for Economic Co-operation and Development’s Base Erosion and Profit Shifting (BEPS) agenda (Büttner and Thiemann, Reference Büttner and Thiemann2017; Christensen and Hearson, Reference Christensen and Hearson2019). Such transparency initiatives have made it significantly harder to obfuscate the placement and beneficial ownership of assets (Alstadsæter et al., Reference Alstadsæter, Johannesen and Zucman2018; Christensen, Reference Christensen, Seabrooke and Wigan2021; Elemes et al., Reference Elemes, Blaylock and Spence2021). While pushback from business interests has meant that transparency efforts have been watered down (Elbra et al., Reference Elbra, Mikler and Murphy-Gregory2023), the regulatory focus on transparency and reporting has increased scrutiny of MNEs.

The drive toward transparency comes, in part, from the perception that big data can be combined with algorithms to govern complex markets as long as there is sufficient data quality (Campbell-Verduyn et al., Reference Campbell-Verduyn, Goguen and Porter2017). The rise of distributed ledger technologies has super-charged this inclination (Bernards et al., Reference Bernards, Campbell-Verduyn and Rodima-Taylor2024), with concerns about data veracity supplanting worries over opacity (Burrell, Reference Burrell2016). Our view is that technology is both part of the drive toward transparency, and a path toward enhanced wealth protection in the face of increased transparency.

A wealth protection imperative, rather than an imperative to achieve superiority in real-time market competition, is also what distinguishes TaxTech from commonly studied forms of algorithmic finance, such as High Frequency Trading (Campbell-Verduyn et al., Reference Campbell-Verduyn, Goguen and Porter2017; MacKenzie, Reference MacKenzie2021). In contrast to High Frequency Trading, TaxTech does not have to be real-time (reporting occurs after the fact), and is not a zero-sum domain given that one firm’s use of a tax provision does not preclude others from its use. Unlike FinTech that uses homogenized data sources to improve speed and scalability, TaxTech decision-making relies on heterogeneous and often unstructured data. Amidst this messiness, the Big Four’s interest in TaxTech is to promote it to both clients and to regulators, positioning themselves as those holding the infrastructural power.

Data and methods

Our first phase of data collection consisted of familiarizing ourselves with the actors in the field, the types of products being developed, and how these tech imaginaries are organized and promoted by the Big Four global accounting firms. Given their prominence in international tax practices (Ajdacic et al., Reference Ajdacic, Heemskerk and Garcia-Bernardo2021; Elemes et al., Reference Elemes, Blaylock and Spence2021; Elbra et al., Reference Elbra, Mikler and Murphy-Gregory2023), we began by reading the publications and web pages of the Big Four and noting down everything about digital strategy, tech collaborations, and TaxTech products. The second phase of data collection consisted of watching and transcribing the relevant parts of online live discussions between different actors in the field on the development of TaxTech products, primarily Big Four and technology firms. From 2017 to 2022, some of the Big Four firms started hosting online events and recording them, with some being available either on their web pages or YouTube. We identified and watched 15 of such webcasts. We used these to identify key people to invite for interviews but also found that the discussions answered some of our questions. The discussions centered on the re-organization of professional skills, and different perspectives on how emerging technologies might be applied to different types of client challenges. We followed up with a handful of tax professionals for online and in-person interviews. In the final phase we relied primarily on publications from the suppliers of tax advice to identify how they describe their services and their potential. These publications are considered sales products and should, of course, be handled critically. But because the technology is emerging, such publications are also the most up-to-date sources of information about the status of tech products in the tax field.

We are well aware that our data has limitations, especially given that the Big Four are actively selling TaxTech and engaging in performative digitalization (Rana and Cordery, Reference Rana and Cordery2024). TaxTech, like RegTech (Campbell-Verduyn and Lenglet, Reference Campbell-Verduyn and Lenglet2023), is an ensemble of tech imaginaries that seeks to provide a clear pathway for new product lines that raise revenue for the firms and exploit clients’ data as they seek new tax optimization solutions. Importantly, the Big Four’s claims should be viewed as promotional, actively trying to stoke ‘fear of missing out’ among clients and encouraging them to adopt new lines of product servicing and data sharing. The Big Four’s descriptions of technologies should be seen as signals of strategy and positioning, seeking to ensnare their clients into the need for TaxTech (Kuhn, Reference Kuhn2025), rather than evidence of real technological innovation and deployment. To the extent that technologies are already implemented, they may include performative ‘quasi-AI’ rather than actual technological novelty. Our focus is on how these actors understand the potential of the technology to transform their services and the market.

Emerging technologies transforming tax governance

The relationships between clients, suppliers and regulators are likely to be impacted in different ways by the introduction of new technologies. Here we provide three examples of TaxTech: Blockchains, Generative AI with natural language processing, and algorithmic scenario planning. Our aim is to conceptualize how technologies alter client-supplier-regulator relationships between the actors within GWCs, impacting taxpayers, tax professionals, and tax authorities.

Blockchains

The typical client-regulator relationship in GWCs is one characterized by high information asymmetry because information is either withheld or cannot be verified by the regulators. Classic GWC examples include the use of personal trusts to obscure economic activity (Sharman, Reference Sharman2017), or the use of assets like housing (McKenzie and Atkinson, Reference McKenzie and Atkinson2020) or art (Helgadóttir, Reference Helgadóttir2023) to conceal wealth from regulators. In other cases, tax authorities cannot verify information, and clients take advantage of gaps between national authorities. The ‘Cum-Ex’ scandal, which generated tax losses of more than €50 billion across Europe over a period of more than a decade, is a prominent example (Christensen et al., Reference Christensen, Seabrooke and Wigan2022). The Cum-Ex scheme was a game which allowed traders to get a refund for dividend taxes from tax authorities without having paid those taxes (Liste, Reference Liste2022). This arbitrage scheme was an extreme case of fraudulent manipulation, demonstrating the fundamental lack of verifiability of asset trades between national tax jurisdictions (Wigan, Reference Wigan2019).

The taxation of businesses is based on post-hoc reporting, wherein firms collect the data on transactions which they have executed and use this to prepare a tax return to various authorities. The important feature of this system is the sequencing of reporting after the fact, and that the transaction data is owned and controlled by private firms (overseen by auditors). Regulators are now imagining and innovating new potential technologies which would put transaction data into a blockchain web, where tax authorities could track and tax transactions instantaneously. The use case for such a technology is particularly apparent considering the ‘CumEx’ scandal (Gramlich et al., Reference Gramlich, Guggenberger, Ismer, Jackl, Urbach, Dietzel, Volland and Westhoff2024; on the broader implications of the blockchain web, see Garrod, Reference Garrod2025; Proskurovska and Birch, Reference Proskurovska and Birch2025).

A blockchain solution could significantly change the process around international taxation by increasing the verifiability of transactions while making this transparency instantaneous, thereby significantly limiting the scope for manipulation. EY has developed such a potential platform entitled ‘TaxGrid’, using blockchain technology to ‘automate, decentralize and securely share tax and financial information while maintaining data privacy between financial institutions and government agencies’ (EY, 2026). While the TaxGrid is an EY project, it is very much supported by tax authorities – including UK HM Revenue & Customs and the Netherlands tax authorities – who want to find solutions to increase transparency and verifiability. The project also includes other stakeholders including companies like BNP Paribas Securities Services, Citibank, N.A., JP Morgan Securities Services, Northern Trust, APG Asset Management N.V., PGGM Investments, and – on the academic side – Vienna University of Economics and Business, and the Tax Administration Research Centre at the University of Exeter (Kennedy, Reference Kennedy2021). Spearheading the development of blockchain TaxTech is EY, with Jeff Saviano, EY’s head of tax innovation, considering it part of a new ‘social contract’ (The Future of Tax Operations, 2022). While it is clear how tax authorities would benefit from ‘near-real-time’ compliance, a digital process would also benefit companies who currently deal with a cumbersome paper-based process across different filing countries. The ‘loser’ would be Cum-Ex traders who would no longer have this arbitrage opportunity. While the technology has already been developed, it still remains for legal frameworks to be harmonized between countries who would take it up, with important implications for tax withholding regimes. Koray Caliskan (Reference Caliskan2020) has explained how blockchain infrastructures are maintained by two groups of actors, the ‘transactioners’ and ‘accountants’. Working between these two groups on tax matters, EY seeks to create TaxTech blockchain services to sell to both the public and the corporate sector.

Blockchain TaxTech thereby transforms certain GWCs from ‘relational’ chains where taxpayers collude with tax advisors on how to hide information about transactions, to ‘captive’ chains where both taxpayers and tax authorities are dependent on the developers and owners of the blockchain infrastructure. While disempowering fraudulent actors, it also leaves regulators dependent on system suppliers.

Generative AI

Tax units of MNEs and large accounting firms spend a high proportion of their time performing relatively routine tasks required for tax compliance which could potentially be automated with the use of Generative AI trained specifically for tax work (Goto, Reference Goto2022). ‘GenAI tax assistants, which work alongside tax professionals, are being designed and piloted right now in an effort to empower their coworkers by automating and accelerating routine compliance work and exposing a wealth of structured and unstructured data trapped in organizational silos’ (EY, 2023). The second shift generative AI could bring in this space is in the handling of tax controversy (Köktener and Tunçalp, Reference Köktener and Tunçalp2021). Here, generative AI could provide a useful tool to prepare disputes by listing precedence and suggesting arguments.

The significant potential for efficiencies and the rapid pace of change in this area means that companies are faced with recruiting personnel with new skill sets who are in high demand. This has caused C-level executives to be increasingly open to outsourcing or co-sourcing their tax function, with survey data indicating that the number has increased from 43 percent to 94 percent in a single year between 2022 and 2023 (KPMG, 2023). 99 percent of C-level executives, meanwhile, would consider outsourcing tax functions to access technology and tech skills. While many are investing in these capabilities and actively changing hiring profiles and hierarchies to attract ‘coding elites’ (Burrell and Fourcade, Reference Burrell and Fourcade2021), not all firms will necessarily be able to attract the right individuals. From our data, we see that within the Big Four, tax advisors are changing their profiles to signal a data science background and avoid being seen as old-school accountants, a trend that reflects the emergence of data science as a profession in its own right (Brandt, Reference Brandt2025). As an EY executive remarked (commenting on data structures for tax insights rather than just tax):

I think in a year or two you’ll have to have 25 to 35 percent of your people that understand both tax and technology (…) The millennials coming out of university have an opportunity to express those skills in a way that gives value right away and then for individuals that are currently in the business environment, it’s time to retrain. Keep their domain knowledge, keep that up to speed, but also add these new skills so that they can stay current. I think the nice part of technology is you can learn it. (EY executive, EY webcast in 2017)

The shortage of professional talent that combines coding and data skills with tax expertise is significant because the large suppliers of tax expertise may have a competitive advantage in hiring talent and developing models for licensing, as compared to firms where tax planning is not the main function.

The Big Four have an additional advantage by having established trust relationships with clients, which helps in handing issues related to data ownership and privacy. PwC’s own marketing on this point is worth quoting at length:

One potential (and avoidable) risk comes from using public GenAI models. These models may not always give you full control over how your company’s data and intellectual property is used and protected. But you can often negotiate a license for access to a private version, then run it within a secure environment, which your data never leaves. This level of data security (a must for us at PwC) requires both rigorous governance and careful negotiations with GenAI vendors. At PwC, if a GenAI vendor offers a new capability that requires our data entering their systems, we don’t adopt it. If necessary, we develop our own version. Our clients usually choose a similar approach – and sometimes run their initial GenAI pilots within our secure systems. (PwC, n.d.)

The advantages held by large, established suppliers of tax expertise in hiring and developing tech means that they are well-positioned to become suppliers of TaxTech, providing them with an even more central role in tax, increased business volume, and potentially infrastructural power (Coombs, Reference Coombs, Westermeier, Campbell-Verduyn and Brandl2025). The efficiency gains from generative AI for compliance cases and routine work benefit taxpayers, but increase dependence on skills in high demand. This again moves the tax market towards a ‘captive’ GWC mode, as it makes more firms dependent on suppliers who have the models and data. Only the largest firms will be able to develop these tools in-house, and suppliers of tax advice will need to compete for a new type of talent to capture this market. Based on our study of tax advice suppliers, these technologies are first and foremost being developed for taxpayers, though one can imagine the benefits of generative AI’s efficiency for tax authorities as well. This might increase the talent competition and the reliance upon external suppliers with the needed expertise and models even further. Another question outstanding is how regulators approach and test algorithmically produced evidence.

Algorithmic scenario planning

While creating integrated and structured datasets of operations and policies presents a challenge, the data already present in tax departments is becoming valuable as a strategic tool to executive managers as they introduce TaxTech to enhance product services beyond tax compliance functions.

This category of TaxTech mostly exists currently in beta versions which are promising but difficult or impossible to scale across clients due to data challenges. While all MNEs are sources of incredibly rich operational and financial data, they have never had reasons to commensurate data (Espeland and Stevens, Reference Espeland and Stevens1998). This means that different parts of firms often store data in different ways and in formats that are not easy to integrate, making it difficult to apply ‘big data analytics’. It also means that across clients, the suppliers of TaxTech are not able to scale applications. Because different clients use different classifications for transactions, an application that works well for one company cannot necessarily be sold to another client. The Big Four are focused on generating data solutions, which are popular with clients due to their promise of efficiency in cutting down the costs of manually classifying inputs and dealing with data aggregation. These applications, such as EY’s ‘Global Tax Platform’, promise to provide a single cloud of very rich data which is more structured than current accounting data.

The challenge of unstructured data is duplicated in the tax field as tax regulation and legislation, including court cases, is not easily coded. Given advances in algorithmic technologies, the advent of more structured tax data is already underway, driven by tax authorities. Here, standardized and increasingly detailed reporting standards, such as Country-by-Country Reporting (CbCR) (De Simone and Olbert, Reference De Simone and Olbert2022), may drive digital transformation and data building. One webinar panelist remarked that headquarters were now, after CbCR, starting to pay newfound attention to the tax of their subsidiaries, indicating that heightened transparency standards are engendering further changes in firms’ strategies to leverage their own tax data.

Once structured and commensurable data are created, what can algorithmic technologies achieve when it comes to the GWC? In one webcast, EY managers presented how an intelligent finance and tax function can be used not only for cost reduction but also value creation, for instance by reducing effective tax rates. One example that was highlighted based on EY client projects demonstrated a tax saving of US$2 million in unclaimed research credits. Another client project had led to a reduction in transfer pricing audit exposure equivalent to €25 million.

The tax benefits of AI go far beyond document intelligence and classification. Really exciting things start to happen when teams use AI to assist with their tax planning. This involves a range of data inputs – including regulatory law, company performance data and corporate strategy – fed into an AI model so that it can proactively make tax recommendations. For example, the AI model might highlight a regulatory change in Spain that affects telecom companies and then offer suggestions on how to best manage the tax implications. Alternatively, a company might want to alter its tax strategy to free up more cash. In this case, the AI could offer a series of recommendations to achieve that goal. (EY Global, How Artificial Intelligence Will Empower The Tax Function)

While examples of this are not published widely, in one recording from 2018, managers from EY shared two examples of nascent technologies already producing great savings:

A program with quasi artificial intelligence with all the debt limitation rules (…) they would program the debt burdens between the Treasury Center and all their local country operations, and then they would link that to EBITDA forecasting. So, as EBITDA forecasting changed, and other input factors, they would get a weekly report out driven by a robot that said ‘you have more debt capacity in country A and less than country B’, and would make recommendations to the tax planners about ‘you could move money from a debt capacity that way’. And after running this robot in the company for about two years, they saved twenty million dollars through additional allocated efficient debt expense. (Flynn, Reference Flynn2017)

Another example highlighted a program to analyze risks of Permanent Establishment status based on travel booking data. Overall, the examples we have come across do not suggest that technology outperforms human experts in thinking up cat and mouse games which require legal ingenuity and creativity. Rather, technology serves to scale and speed up legibility processes which enable optimization within the law, allowing full advantage to be taken of more obvious legal affordances like debt allowances. This technology presents significant potential for clients where business integration is possible and again empowers suppliers of TaxTech. For tax authorities concerned with fraud and evasion, scenario planning techniques that are entirely within the law are not problematic – but such techniques might present a challenge to governments if they arrive at a scale at which the loss of tax paid becomes notable.

TaxTech may alter the dynamics of GWCs by replacing assumed information asymmetries between suppliers, clients, and regulators with heightened operational efficiency all entirely within the law. Opacity through undisclosed information between parties transforms into opacity via the illegibility of outputs from machine-learning systems (Burrell, Reference Burrell2016). In terms of governance, it is likely, in the first instance, that these changes empower suppliers who have developed and own the models. However, as a scalable technology, it is possible that TaxTech will make tax planning more accessible to clients who previously did not have the scale or resources to engage in tax planning. As explained by the CEO of TaxTech firm BlueJ, who is also a Professor of Business Law at the University of Toronto (cf. Raitasuo and Ylönen, Reference Raitasuo and Ylönen2022), the potential for tax planning using algorithms is large:

Until now, tax avoidance has been the exclusive preserve of the creative, dedicated, and ingenious human tax expert, often working in teams of like-minded tax specialists to create plans that crack the tax code through clever tax avoidance strategies. The emergence of ever more competent artificial intelligence is set to revolutionize tax avoidance – for good or for ill… The adoption of AI in tax planning will thus raise important considerations about the future social roles of tax professionals. Will we be seen as defenders of fiscal responsibility and restraint or as enablers of ruinous advanced tax avoidance techniques? The answer will be shaped by the future path of AI tax avoidance technologies and the legal and ethical standards that we choose to guide their use. (Alarie, Reference Alarie2023: 1809–1810)

Global wealth chains and TaxTech

The changing relationship between regulators, clients, and suppliers, and the technologies which they employ requires us to reconsider the governance of GWCs. Previously, strategic wealth creation was guided by different methods of opacity-creation opened up by agency-based information asymmetries between suppliers, clients, and regulators. Given this, regulators could advance in their objectives through transparency initiatives like CbCR. For MNEs subject to regulation and transparency requirements, however, it appears likely that TaxTech pushes them in a direction away from opacity as a strategy for tax avoidance, and towards opacity through algorithmic outputs. As power relations between taxpayers, tax professionals, and tax authorities become increasingly determined by control over data and models, access to good data becomes critical. Those in a strong position to access client data, such as the Big Four, are attempting to create an infrastructural advantage. Power is thus shifting away from the control of financial information to the control of proprietary technology.

The impact of TaxTech is not limited to transforming tax governance but has implications for business strategy more widely. Across the three technologies, tax expertise takes on a new role in business strategy, as tax data combined with other finance and operational data can be used to drive strategic planning. As was conveyed in an EY webinar:

the tax function is increasingly becoming a strategic partner across the business, a transformation which requires the liberation of tax professionals from routine tasks so they can focus on value. According to the latest survey, most (96%) companies are reallocating tax and finance budget to strategic activities – from routine activities such as tax compliance to strategic activities such as legislative, planning and controversy. (EY, 2023)

Within firms, tax units are also transformed as the use of technology makes their data more useful for both tax and business decisions. The tax function thus moves from a subsidiary role in the back office to steering strategy in the front office. Dirk Zorn described the ‘rise of the CFO’ in American firms as a response to new regulation and modes of financial organization (Zorn, Reference Zorn2004). There could be a similar story here, where tax becomes more closely tied to strategy and this requires the ‘rise of the CTO’ (Chief Tax Officer). The prevalence of this view is a clear trend within our data:

I think if you’re the VP of tax at a large global multinational your c-suite or CFO is looking at you to add value and have tax being a creative organization within a company not just a compliance function. (EY executive, 2017)

for many of us in the finance and tax field were perhaps more the back-office resourcing and now we are moving to the front of house which is an exciting time for many in this space because we always knew we had all this data and insight into the business but before we weren’t able to bring it to life and i think that’s changing. (Russell-Gilford, Reference Russell-Gilford2022)

This shift towards treating tax as central due to its data-heavy nature is a fundamental effect of improved algorithmic technologies. But since data is proprietary and not easily structured, and the talent shortage concentrates the development of technology, taxpayers as well as authorities will depend on suppliers to a larger extent than previously. We can understand this change through the lens of GWC-GVC typologies. In GVC scholarship, governance modes are determined by degrees of explicit coordination and power asymmetry between market actors (Gereffi et al., Reference Gereffi, Humphrey and Sturgeon2005). In GWC scholarship, governance modes are differentiated by degrees of explicit coordination and information asymmetry (Seabrooke and Wigan, Reference Seabrooke and Wigan2017). We suggest that in tech-driven GWCs, this situation is transformed into one in which governance modes differ by degrees of explicit coordination in terms of data sharing. Table 1 outlines how the ideal types of different governance modes work within TaxTech GWCs.

Applying the GWC typology to TaxTech.

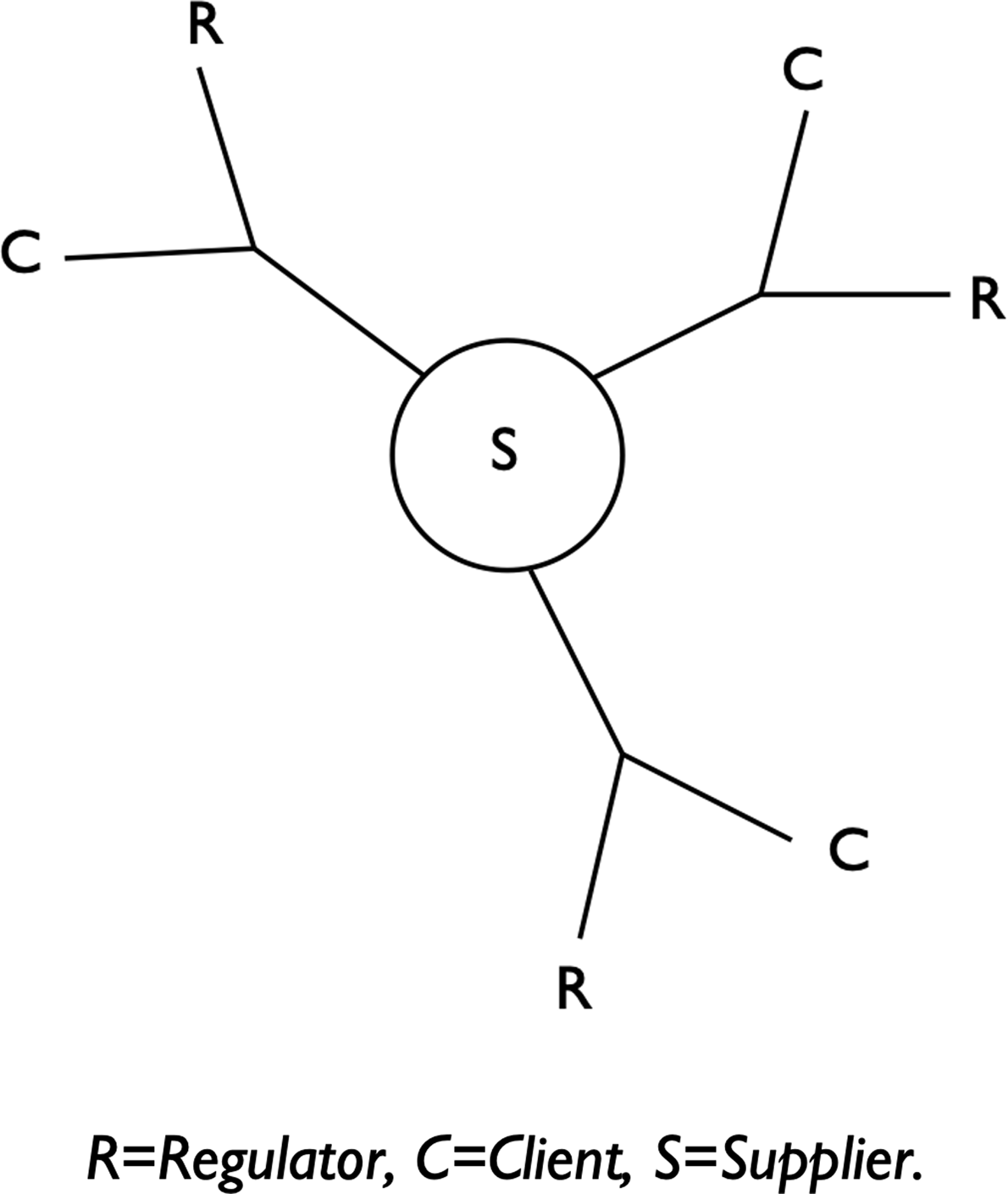

A key finding in our three cases is the impact of TaxTech on the power dynamics within GWCs. We illustrate this in Figure 1: suppliers become the central point of coordination through which everything must go. This results in a set of relations characterized not by the triangle of information asymmetries depicted in the original GWC framework (Seabrooke and Wigan, Reference Seabrooke and Wigan2017), but a network where everyone must go through the supplier.

Supplier centrality in algorithmic GWCs.

The TaxTech innovated for GWCs has the potential to make tax payments and asset transactions more verifiable, while simultaneously enabling the more effective exploitation of weaknesses in legal regimes through the application of generative AI. The Big Four accounting firms’ dominance in global accounting provides them access to tax data that places them in a superior position to develop models for predicting wealth management and tax-planning opportunities (Faulconbridge et al., Reference Faulconbridge, Sarwar and Spring2024; Goto, Reference Goto2022).

Agents are no longer separated by information asymmetry but are closer together in a network in which their relationships are intermediated by technology. The supplier can use generative AI in their communication toward the regulator. The client provides data for the supplier, who in turn use their technology and expertise to provide tax scenario planning in ways that are integrated with business. The regulator uses blockchain technology to obtain near-instant verification of client taxpayer data. As such, the potential for new technologies in this space is bi-directional, as was emphasized by Jeff Saviano, Tax Innovation Leader at EY, when speaking of their work with TaxTech:

And so, a lot of what we do is supporting our commercial clients, but also, we do some work for governments, as well. And we think that innovation, especially for such an important area as taxation, I think it’s important for governments, and I think it’s important for commercial taxpayers, and frankly, for all of us citizens as well. (The Future of Tax Operations, 2022)

TaxTech provides a new opportunity for suppliers to create two-sided markets, selling tax-planning products to corporate clients and tax-fraud detection to regulators. It is important to emphasize that these are not viewed as contradictory goals because TaxTech aims to optimize within the law.

Conclusion

Technology such as blockchains, generative AI and algorithms are transforming the logics of several markets and industries. In relation to taxation, GWC governance is being transformed from a cat and mouse game of hiding assets, into a game structured by the ability to use data and models strategically. This generates new inequalities between taxpayers, tax authorities, and tax advice suppliers, as their benefits or losses in this transformation depend on their success in the ‘arms race’ for TaxTech infrastructural power. As Benjamin Alarie of BlueJ put it:

The path ahead for tax avoidance, as it merges and converges with the development of AI, may lead to a future of more effective, insightful, and equitable tax planning. Alternatively, it could precipitate a future in which the divide between taxpayers and tax authorities grows, driven by unequal use of AI. The choices we and our governments make now and in the near future will have the potential to chart the fiscal narrative for years to come.

In this article, we have discussed three TaxTech technologies: blockchain, generative AI, and algorithmic tax planning. Rather than supercharging the cat and mouse game of secrecy-seeking capital, we find that the key transformation driven by these technologies is a move towards a new game within which control over data and models becomes the pivot around which strategy is directed. Modes of wealth chain governance concerned with asymmetric information do not apply as meaningfully to a tax space governed through technology. Not all suppliers, clients, or regulators can necessarily develop their own technology, and the Big Four global accounting firms are well positioned to increase their infrastructural power over TaxTech devices and practices.

The Big Four’s power should not be taken for granted, however. The race to develop TaxTech is a fast-moving target, and one which embodies Silicon Valley’s ‘move fast and break things’ energy. Assumed hierarchies of suppliers may be disrupted. Whether the Big Four and others with tax expertise and data access can remain the main suppliers, or other AI developers and tech companies can develop more competitive products, remains to be seen. On the one hand, the Big Four, as key suppliers, aim to use TaxTech to supercharge tax planning for their clients. On the other hand, regulators are also attempting to be first movers in some of these technologies. Their data is more structured, they have power over reporting formats, and clear incentives to apply technology to reduce fraud. TaxTech is beginning to rewire financial and legal management, concentrating power around those who can keep both their clients and regulators captive through technology.

Acknowledgments

We thank Rebecca Adler-Nissen, Daniel Mügge, Crawford Spence, Shogo Suzuki, and members of the Organizations, Markets and Governance research group for their feedback on earlier versions of this paper. Our thanks also to go the editors and reviewers for their excellent criticisms and guidance.

Funding statement

This research was funded by the Velux Foundation and Villum Foundation grant ‘Algorithms, Data, and Democracy’ (#37102/#39017).

Open access

Open access