A. Introduction

Antitrust regimes around the world shape the structure of global digital markets. Beginning in the 1980s, many African countries adopted antitrust laws alongside structural adjustment and trade liberalization measures, selectively borrowing from existing EU and U.S. regimes. A majority of African antitrust regimes specifically emulate core pillars of EU competition law, with differences reflecting development needs and local, cultural, and institutional specificities.Footnote 1

Today, in response to global consolidation in digital markets, governments are increasingly introducing sectoral regulatory schemes that have pro-competitive aims but go beyond antitrust law. A key example is the EU’s Digital Markets Act (DMA), which seeks to make digital markets fairer and more contestable by imposing a series of obligations on gatekeepers.Footnote 2 Through a dynamic known as the “Brussels Effect,” the DMA is being emulated in other regions,Footnote 3 from BrazilFootnote 4 to India.Footnote 5 The Protocol on Competition Policy to the Agreement establishing the African Continental Free Trade Area (AfCFTA Competition Protocol), is no exception.Footnote 6 Similar to the DMA, the AfCFTA Competition Protocol has pro-competitive and decentralizing aims: it imposes a list of obligations on platform gatekeepers to benefit the ability of smaller players to enter digital markets and compete. In parallel, South Africa, Kenya, and other African jurisdictions are adopting their own sets of pro-competitive measures for digital markets.Footnote 7 These efforts must be understood against a background of mounting tariff pressures and other preferential trade barriers which may change the regulatory landscape in the future.Footnote 8

Although the AfCFTA Competition Protocol and these localized reforms emulate the EU’s DMA, they are not motivated by the same goals. The latest wave of EU digital reforms has been driven by (a) consumer protection and fairness rationales relating to the limits of data protection and other EU law domains in protecting individuals against digital gatekeeper interferences, (b) competition and contestability rationales relating to the limits of case-by-case ex post antitrust enforcement in addressing digital monopolies and abuses of dominant digital power, and (c) an emphasis on growing an ecosystem of small- and medium-sized EU and foreign digital firms that can serve as competitive constraints against tech giants.Footnote 9 African pro-competitive reforms have different rationales. African jurisdictions are seeking to not only ensure fairness, contestability, and competitiveness in African digital markets. They also want to assert digital sovereignty both in global cross-border digital markets and against Western or foreign influences.Footnote 10

Given the different motivations underlying these regulatory schemes in different regions, we must ask why these frameworks look so similar. Scholars disagree on whether a DMA-like regime can successfully be implanted in African nations.Footnote 11 At the very least, a regulatory regime for digital markets spanning the AfCFTA needs to account for different economic development goals, local and regional diversity, institutional specificity, and the substantive antitrust culture that preceded it. In this Article, we examine how different African jurisdictions are importing parts of the DMA into their local contexts and argue that such emulations need to be more cautious about the different rationales that motivate pro-competitive reforms in Africa. In particular, we show how, in light of those rationales, the notions of contestability and fairness embedded in the DMA can be extended and transformed into a bolder vision of digital regulation in the African context. Such vision, in turn, could inspire ambitious enforcement beyond Africa including in the Global North.

As may be obvious from the range of goals and values that underlie them, not all of the legal instruments and policy proposals we analyze in this Article are exclusively guided by a pro-competitive agenda. The EU’s DMA and many of the African frameworks we discuss advance pro-competitive goals alongside other values such as fairness, local innovation, and development, each of which can arguably conflict with a conception of competition at all costs. We adopt the terminology of “pro-competitive regulation” to describe these frameworks despite their more complex nature because we believe that competition cannot be pursued in isolation from other productive rationales. Thus, any pro-competitive regime must include other values.

We proceed as follows. Section B introduces the DMA and similar gatekeeper regulation found in the AfCFTA, picking up on questions that such emulation raises in view of different economic, political, and legal circumstances. Section C describes the proliferation of regional and national competition law regimes in Africa, exploring their underlying goals and rationales. Section D focuses on South Africa and Kenya, two leaders in digital market regulation on the continent, analyzing the emergence of DMA-like frameworks, their objectives, and enforcement in these jurisdictions. Section E draws on the broader rationales that have shaped competition regimes in Africa, and on insights from South Africa and Kenya’s experiences, to propose implementation directions for the AfCFTA. It begins by outlining the structure and goals of Africa’s digital economy, and then suggests ways for AfCFTA to concretize substantive fairness and other pro-competitive safeguards for the African digital sector.

B. Emulating Digital Markets’ Norms

After describing the European DMA and the economic, political, and legal context in which it was adopted (Section B.I.),Footnote 12 we introduce the Pan-African AfCFTA Competition Protocol (Section B.II.) and articulate key research questions on its implementation (Section B.III.).

I. The EU’s Digital Markets Act

The DMA, adopted in 2022, is part of a package of EU digital market reforms intended to make Europe “fit for the digital age.”Footnote 13 In proposing the DMA, the European Commission described the legislation’s rationale as follows: “[W]hereas over 10,000 online platforms operate in Europe’s digital economy, most of which are [small and medium enterprises (SMEs)], a small number of large online platforms capture the biggest share of the overall value generated.”Footnote 14 Large online platforms are, in other words, too entrenched to be challenged by new market entrants, and they rely on their dominance to extract the value from platform’s business users and consumers.

The remedy to entrenched market power and to the imbalanced relations that it entails has traditionally been found in competition law. The DMA, however, starts from the premise that the slow and piecemeal case-by-case and ex post (after-the-fact) enforcement of competition law in digital markets has been ineffective.Footnote 15 The DMA therefore takes an ex ante (pre-emptive) approach, which may allow for a more timely and effective regulation of online platforms. It does so by pursuing the dual goals of fairness and contestability in digital platform markets via a list of obligations. Let us examine the DMA’s goals, scope, and obligations in turn.

The DMA is aimed at ensuring “fairness” and “contestability” in digital platform markets.Footnote 16 It is intended to rebalance the relation between powerful platforms and their business users (fairness) and to allow challengers to compete with incumbent platforms (contestability).Footnote 17 The two goals are related: the more contestable the market, the more equitable the division of rents between powerful platforms and business users; those business users, when given the room to do so, can then challenge incumbent platforms.

Textually, the DMA’s goals are clear: the instrument pursues fairness and contestability—not undistorted competition, as competition law does, or any other goals.Footnote 18 But that clear picture is complicated in two ways. First, as we discuss below, many of the DMA’s obligations are inspired by previous enforcement of competition law. Second, the DMA is often mentioned in the same breath as “digital sovereignty.”Footnote 19 Those discussions suggest that the DMA is, at least in part, a tool to untether the EU from the dominance of U.S. and Chinese-led innovation. This is arguably what placed the DMA in the eye of the tariff storm.Footnote 20 To be realistic, the DMA favors smaller businesses regardless of nationality and its effects are more decentralizing than protectionist. Non-EU companies are likely to benefit most from the regulation.Footnote 21 Epic Games was quick to launch its App Store on iOS, for example, and Microsoft could improve Bing now that Google must share its query data.

The scope of the DMA is limited to platform “gatekeepers.” To qualify as a gatekeeper, a firm must first provide a “core platform service” (CPS) such as online intermediation (for example, online marketplaces, app stores), search, social networking, or operating systems (OSs).Footnote 22 CPSs are considered the gateways of the digital economy, but the DMA is concerned with companies that (i) have a significant impact on the internal market, (ii) provide a CPS that is an important gateway for business users to reach end-users, and (iii) enjoy an entrenched and durable position.Footnote 23 Such gatekeeper status is presumed when the provider of a CPS meets certain quantitative thresholds relating to turnover (7.5 billion EUR) or market capitalization (75 billion EUR) and monthly active users (45 million end-users; 10,000 business users), and has served as many users for the last three years.Footnote 24

Based on these criteria, the European Commission initially identified six gatekeepers (for a total of twenty-two CPSs): Alphabet (Google), Amazon, Apple, ByteDance (TikTok), Meta (Facebook), and Microsoft.Footnote 25 The results of the designation exercise were no surprise as the DMA was designed to capture only the largest platforms.Footnote 26 However, the nationality of the gatekeepers, all American or Chinese, did not assuage concerns of protectionism. Neither did the fact that the originally European Booking.com later joined the list of gatekeepers.Footnote 27 Designations are regularly reviewed, meaning that current gatekeepers can lose their gatekeeper status (for specific services),Footnote 28 as was the case for Meta’s Facebook Marketplace, which was “undesignated.”Footnote 29 The Commission can also conduct market investigations to designate gatekeepers that do not meet the quantitative gatekeeper thresholds, as it did for X (Twitter).Footnote 30

Once designated, gatekeepers must comply with a list of obligations.Footnote 31 Some of them relate more to the DMA’s fairness objectives. App stores, search engines, and social networks must provide business users access to their platforms on fair, reasonable, and non-discriminatory (FRAND) terms.Footnote 32 Gatekeepers cannot engage in self-preferencing—meaning that they cannot treat their products more favorably than the competing ones of business users.Footnote 33 And they cannot rely on data collected from business users to compete with them.Footnote 34 Other obligations relate more closely to contestability. Gatekeepers cannot impose most-favored-nation clauses (MFNs), also known as “(price) parity clauses,” which prevent business users from offering their products on other platforms at more favorable terms.Footnote 35 Gatekeepers who run OSs must allow the un-installation of default apps; for certain apps (search engines, browsers, virtual assistants), they must even prompt users to make an active choice.Footnote 36

Importantly, most of the obligations find some precedent in competition law enforcement at the EU or national level. In a series of cases mostly centered around hotel booking platforms and online marketplaces, for example, competition authorities across the EU have prohibited platforms from imposing MFNs on business users.Footnote 37 But the obligations were not always inspired by such “hard” enforcement; market studies and investigations identifying potentially problematic conduct also played an important role. Many of the app store obligations, for example, can be traced back to reports published by the Dutch Authority for Consumers & Markets (ACM) and the UK Competition & Markets Authority (CMA).Footnote 38

At the time of writing, it is hard to judge the DMA’s effectiveness. It has already prompted change in the business models and product designs of the designated gatekeepers,Footnote 39 though perhaps not enough to effectively reach the DMA’s goals, which is why the European Commission opened non-compliance investigations into three gatekeepers.Footnote 40 The investigations against Apple and Meta have meanwhile resulted in a non-compliance decision,Footnote 41 and the Commission has also specified Apple’s interoperability obligations.Footnote 42 There is a fear that enforcement will suffer under the hostile U.S.–EU trade climate. So far, the DMA’s sister regulation, the Digital Services Act, which concerns speech, has served as a lightning rod.Footnote 43 Based on precedent in competition law, such as the Google Adtech decision, the EU appears poised to continue enforcing its market-based regulation.Footnote 44

The DMA has inspired similar regulation around the world,Footnote 45 with the clearest example being the AfCFTA Competition Protocol.

II. The AfCFTA Protocol on Competition Policy

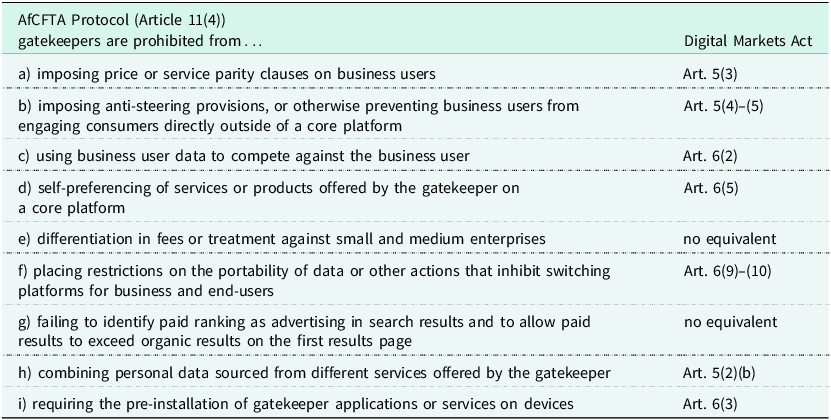

In 2023, the Assembly of fifty-four African countries’ Heads of State and Government adopted the AfCFTA Competition Protocol (the Protocol). Adoption is the first step towards the Protocol’s ratification and domestication by the AfCFTA Member States.Footnote 46 The AfCFTA is a free trade area that brings together almost all countries on the African continent.Footnote 47 The Protocol, which hasn’t yet been fully ratified, promotes and harmonizes competition laws across these African nations.Footnote 48 In addition, the Protocol imposes specific obligations on digital gatekeepers, mirroring the DMA.

Unlike the DMA, the Protocol does not put forward specific digital goals such as fairness or contestability. Its goals relate more generally to competition policy on the continent. The gatekeeper provisions, alongside the rest of the Protocol, are aimed at enhancing market efficiency, promoting inclusive growth, and advancing the structural transformation of African economies including through economic integration and sustainable development.Footnote 49

The ex ante obligations contained in the Protocol are targeted at “gatekeepers,”Footnote 50 defined as

undertaking[s] that ha[ve] a significant impact on the Market, operate … a core platform service that serves as an important gateway for business users to reach end-users, enjoy … an entrenched and durable position in [their] operations or it is foreseeable that [they] will enjoy such a position in the near future.Footnote 51

Like the DMA’s definition, this definition is centered around providers of CPSs that meet three criteria: significant market impact, important gateway, entrenched and durable position. Also in line with the DMA, the Protocol requires that gatekeepers be designated before incurring any obligations.

The Protocol’s obligations take the form of prohibitions—in other words, negative obligations. Gatekeepers are prohibited from imposing MFNs on business users, from using business user data to compete against business users, from self-preferencing, and from requiring the pre-installation of gatekeeper applications or services on devices, among others.Footnote 52 Each of these obligations can be found in the DMA, though the language of the two instruments differs slightly. The Protocol includes an additional prohibition not contained in the DMA: gatekeepers must not discriminate against SMEs through pricing or other conduct.Footnote 53 Other obligations contained in the DMA are absent from the Protocol, notably certain positive duties imposed on gatekeepers such as the obligation for search engines to share query data.Footnote 54

III. Open Questions: From Form to Substance

The Protocol aligns closely with the DMA but is less detailed on substance and enforcement modalities. This is not surprising given the wider diversity of legal regimes subject to the Protocol compared to EU Member States. The Protocol’s gatekeeper obligations are laid out in the form of a one-article outline compared to the DMA’s 54 articles and 109 recitals, and the Protocol tasks a separate authority—the Council of Ministers—with implementing the gatekeeper designation process.Footnote 55

Filling in the outline provided by the Protocol will require significant effort. While a regulatory model can be emulated, it must be given concrete shape within its specific economic, political, and legal context. To reach the Article’s goal of contributing to this shaping process, we look at the history, goals and rationales of African competition law regimes (Section C), and then investigate how two of the continent’s most active authorities have dealt with issues of digital competition (Section D). Finally, in Section E, we present a view on how the Protocol can be advanced and implemented in ways that are specific to the African digital economy and its goals, rather than a simple imitation of European values in digital markets.

Despite their importance, we largely stay away from institutional questions. The DMA is enforced almost exclusively by the European Commission, which is thus a federal regulator perhaps for the first time.Footnote 56 The Protocol comes with an equally unique—and no less complicated—framework: an authority that has to coordinate enforcement with the various regional and national regimes that are in place.Footnote 57 Others have already taken an in-depth look at the risks and opportunities of this setup,Footnote 58 which is why our focus is on substantive questions.

C. The Development of African Competition Law Regimes

African nations largely began to enact competition laws in the 1990s.Footnote 59 Prior to 1990, only three African countries—Gabon, Kenya, and South Africa—had competition law regimes.Footnote 60 Since then, over 30 countries have enacted national competition laws.Footnote 61 Most countries participate in one or more of the continent’s seven regional competition regimes, including the West African Economic Monetary Union (WAEMU), the East African Community (EAC), the Common Market for Eastern and Southern Africa (COMESA), the Economic Community of West African States (ECOWAS), and the Communauté Economique et Monétaire de l’Afrique Centrale (CEMAC).Footnote 62

In their book Making Markets Work for Africa, Eleanor Fox and Mor Bakhoum identify two clusters of competition law regimes in Sub-Saharan Africa, each with major institutional and substantive differences: West African Sub-Saharan countries (Senegal, Ivory Coast, Mali, and Guinea-Bissau) which have less developed competition law regimes, and East and Southern African Sub-Saharan nations (Kenya, Namibia, Botswana, Zambia, Zimbabwe, Mauritius, Malawi, and South Africa) with more established and working regimes.Footnote 63

The adoption of competition laws in African countries is closely linked to the global move towards trade liberalization beginning in the early 1980s and showcases three overlapping yet sometimes conflicting rationales: (1) “universal” ideas of efficiency and competitiveness, (2) foreign/globally-imposed goals related to the development imperative and the creation of market economies conducive to foreign direct investment, and (3) locally grounded inclusive development goals.

As further discussed below, many competition policy goals, concepts, and modalities of governance have been largely implanted into African jurisdictions from U.S. and European competition policy regimes.Footnote 64 These Western frameworks were designed to advance European and American economic concerns such as efficient, competitive, and dynamic markets, promoting consumer welfare, reducing production costs, and contesting concentrated economic power in liberal democracies.

As transplanted into African jurisdictions, these frameworks advanced a second set of development rationales. Indeed, it was thought that free market principles were the basis for economic development and would usher in a new world economic order of free trade and foreign investment. Antitrust regimes in many African nations were imposed at least in part as conditions for financing by the World Bank and the International Monetary Fund (IMF) as part of structural adjustment programs.Footnote 65 In this regard, competition policy was one of many prescriptions needed for the transition to market economies.Footnote 66

Efficiency and investment-related rationales are now deeply embedded in national and regional regimes, no longer viewed merely as Western imports. African countries have adapted to the prevailing market-oriented logic of national economic growth and globalization, treating competition law as essential for building competitive national economies and partaking in global markets. Still, African competition authorities face existential challenges, including: scarce resources, inadequate enforcement capability,Footnote 67 red tape and undue government interferences, cronyism,Footnote 68 and highly concentrated economic and political power.Footnote 69 These challenges also affect regional economic integration efforts.Footnote 70

In addition to efficiency and externally imposed rationales, African antitrust and competition policy regimes also advance a third set of goals relating to local realities and indigenous economic development,Footnote 71 which is of particular relevance in digital markets. These goals promote the development of a robust national private sector, regional trade, and also social welfare goals such as promoting the interests of SMEs, employees, and minority groups. Examples are Kenya’s early attempts at developing a home-grown competition policy frameworkFootnote 72 and the 1998 South African competition law which emphasizes ambitious anti-apartheid goals such as advancing “social and economic welfare,” “South African participation in world markets,” equity toward SMEs, and increasing “the ownership stakes of historically disadvantaged persons.”Footnote 73

The enforcement of competition policy regimes in these countries has continued to advance these three sets of goals in tandem. It should be noted that these goals are not clearly separable, in the sense that efficiency, Western values, and free trade and development rationales have become enmeshed in local governance frameworks.

As we argue in this Article, the third set of motivations for competition policy—home-grown innovation, local inclusive development, and fairness to SMEs and historically disadvantaged actors—is most relevant to evaluating the current wave of pro-competitive digital regulations inspired by the DMA such as AfCFTA. African nations must be encouraged to embrace a more bottom-up and home-grown vision for digital markets, away from the U.S. and EU-centric blueprint, and their efforts could also inspire European and U.S. policymakers to foreground values such as substantive fairness and equity in Western markets at a time of trade uncertainty and digital change.

We now look more closely at the contexts shaping the proliferation of competition law regimes in African countries. We begin with the impact of free trade and conditional loans, then move to regional and national competition policy arrangements, and conclude with the promotion of local values and interests.

I. The Impact of Global Trade Liberalization and Conditional Loans

In the wake of political decolonization in the late 1950s and 1960s, newly independent African nations sought to generate self-sustaining economic development through industrialization efforts. These initial efforts largely relied on significant state intervention and protectionist trade policies.Footnote 74 After initial growth, the economic instability and global oil crises in the late 1970s slowed or reversed many post-independence gains.Footnote 75 At the same time, international economic policies began to shift in favor of trade liberalization and multinational firms began to expand. By the 1980s, institutions like the World Bank and the IMF began pivoting towards free market policies that emphasized rapid privatization and capital market liberalization to boost development.Footnote 76 Structural adjustment programs (SAPs) conditioned loans to economically suffering nations on their enactment of a wide array of economic liberalization policies, often including competition laws.Footnote 77 Competition considerations were often one of many other facets of a broader market liberalization agenda that also included privatization of state-entities, cuts in public spending, reduction of trade barriers, and export promotion.Footnote 78 While the specific requirements and implementation strategies varied from nation to nation, around 32% of all conditionalities for World Bank loans in FY 98-00 included reforms relating to competition, up from only 7% in previous years.Footnote 79 Alongside these interventions, the World Trade Organization (WTO) also strongly encouraged developing countries to adopt competition regimes, mainly derived from U.S. and European frameworks, as a useful complement to free trade, and partly as a way to create a secure global business environment for multinational firms.Footnote 80

This external pressure demonstrates that early efforts to introduce competition law frameworks in many African nations often bypassed democratic processes and local interests. However, some nations were considering home-grown competition policies prior to SAPs. By the 1990s, Kenya had, for example, already assembled government committees proposing competition strategies.Footnote 81 Parliamentary debate from the passage of Kenya’s 1988 Restrictive Trade Practices, Monopolies and Price Control Act also shows that domestic competition laws were motivated, at least rhetorically, by nationalist concerns about indigenous control over the industry.Footnote 82

Among countries that did not adopt competition laws because of SAPs, some entered trade deals with other nations that required “harmonization” of competition laws, which amounted to the adoption of European competition rules and principles into African economic legal regimes with few carve outs and modifications allowed.Footnote 83 For example, Egypt pulled out of an IMF conditional loan plan before it would have had to adopt a competition law in the mid-1990s,Footnote 84 but later adopted competition measures in 2005 for the purpose of entering into trade agreements with the EU.Footnote 85 These laws broadly reflected Western concerns about efficiency, market competition, free trade, legal certainty, and openness to foreign investments.

II. Regional Bodies and Competition Regimes

African countries have also adopted regional competition regimes (RCRs), often as part of attempts to create common markets.Footnote 86 Such regional economic integration is a way for African countries to assert themselves economically and politically against larger powers. The first attempt at integration at the continental level was in 1963, when the Organization of African Unity (now AU) was formed.Footnote 87 The Treaty Establishing the African Economic Community was signed in 1991, with the overarching goal to “increase economic self-reliance and promote an endogenous and self-sustained development.”Footnote 88 Since then, numerous other regional economic communities have been established.

RCRs help address the resource problems that many nations face when it comes to establishing and enforcing competition laws. They also help address cross-border, anti-competitive behavior involving multinational firms, which harms a nation’s economy while occurring outside their national jurisdiction.Footnote 89 There are seven RCRs. Five have regional competition laws and enforcement bodies: WAEMU, COMESA, CEMAC, EAC, and ECOWAS.Footnote 90 Two others require members to adopt national competition laws and cooperate with each other in a “confederate model” with no supranational body: the Southern African Customs Union (SACU) and Southern African Development Community (SADC).Footnote 91 The Agadir Free Trade Area Agreement—which has several North African nations but also includes Jordan, Palestine, and Lebanon—also requires members to adopt economic policies that ensure objectively fair competition among Member States.Footnote 92

Some African nations have relied on RCRs to compensate for their lack of a national competition law. For example, Uganda’s competition law had been introduced and stalled for fifteen years before being adopted in 2024.Footnote 93 Uganda was, however, already part of both COMESA and EAC’s regional enforcement systems.Footnote 94 In addition, insofar as the RCRs boast their own competition authority, it may make up for the lack of a national authority.Footnote 95 Many countries have also been influenced by the competition law regimes of their neighbors. Namibia, Botswana, and Eswatini, for instance, all reference South Africa’s regime. This indicates that regional and national inter-dependencies might be a complicating bottom-up rationale for many local regimes.

III. The Promotion of Local Values and Interests

In addition, African competition law regimes reveal a process of indigenization. These regimes not only address efficiency, consumer welfare, and regional integration, but also embody specific national goals and values shaped by each country’s historical context. For instance, Kenya’s initial competition law prioritized fostering an indigenous capitalist class. Although this law was later repealed, Kenya’s current competition law enforcement still emphasizes the interests of SMEs and considers the impact of mergers on employees. For instance, the Competition Authority of Kenya (CAK) approved the merger between KenolKobil and Gulf Energy on condition that KenolKobil retain all employees of Gulf Energy for 24 months with no remuneration changes during that period. The CAK also required KenolKobil to maintain any existing contracts between Gulf Energy and SMEs for 24 months.Footnote 96 Similarly, South Africa’s competition policy aims to promote balanced economic development, promoting the ability of historically disadvantaged groups to gain a more substantial share of the economy. The appetite for promoting local interests and values could inspire interventions in digital markets.

As African countries begin to draw inspiration from the DMA in the design of local digital competition regimes, the question arises: how far should this legal borrowing extend, and can the competition policy rationales underlying the DMA in Europe be reconciled with the continent’s digital economy goals and those of individual African countries? We now analyze developments at the regional and local level in Africa to understand the suitability of a DMA-like regime for the continent. Our analysis focuses on South Africa and Kenya, two of the most active competition regimes in Africa.

D. African Digital Markets Regulation: The Case of South Africa and Kenya

In order to better understand the evolution of enforcement in digital markets—from pure competition law enforcement to hybrid pro-competitive regulatory frameworks—we now look more closely at the history and recent developments of competition law in South Africa and Kenya. In addition to having regimes that aim for more than just market efficiency and consumer protection, and that address socio-economic goals such as protecting employees and promoting the economic empowerment of SMEs and historically marginalized groups, these countries also exhibit specific concerns and characteristics when it comes to digital markets. The effects of global digital platform services on these economies are significantly different from those that motivated the DMA in the EU. As the competition enforcement surveyed in this section indicates, the different economic make-up of these regions demands more contextual approaches to principles such as “fairness” and “contestability,” not a blanket transplant of DMA obligations into the AfCFTA and local digital reforms.

I. South Africa

We start this subsection by giving a snapshot of South Africa’s tech landscape (Section 1) and of its antitrust regime and institutions (Section 2), which provides the necessary background to understand its enforcement of competition law in digital markets (Section 3), and related regulatory developments (Section 4).

1. A Snapshot of South Africa’s Tech Landscape

South Africa arguably has the most developed digital economy in Africa. It has one of the highest internet penetration rates in Africa at 72.3% (43.48 million internet users) and a mobile penetration rate of 187.4% (112.7 million cellular mobile connections).Footnote 97 Like other countries on the continent, most people access the internet through their mobile phones. South Africa also has robust digital infrastructure due to early investments made in fiber-optic cables and international submarine cables. International connectivity is set to increase significantly following the launch of Google’s Equiano sub-sea cable that connects South Africa to Europe.Footnote 98 These trends notwithstanding, the digital divide persists in South Africa: the cost and quality of access for poorer, more rural consumers is relatively worse than in comparable countries. Thus, improving the costs, choices, and quality of internet services is a priority of the South African government.

South Africa’s tech ecosystem is thriving with a variety of startups in sectors such as fintech, e-commerce, e-health, ed-tech, agri-tech, logistics, legal tech, and so forth. Fintech and e-commerce are the most prominent sectors accounting for 30% and 10.2% of startup economic activities respectively.Footnote 99 However, the ecosystem is also plagued by inequality in investor opportunities, which limits the growth of startups by historically marginalized groups. Black and female entrepreneurs struggle to raise capital compared to their white, male, and middle-class counterparts.

Due to its tech leadership, South Africa serves as a regional hub for global initiatives, including multinationals wishing to set up regional headquarters or to establish regional cloud hosting services and data centers. For instance, Microsoft, IBM, Amazon Web Services, Teraco, and Dimension Data have all made investments to offer these services from South Africa.Footnote 100 For South Africa, attracting such foreign investment is important, yet it might conflict with other goals such as strategically promoting the local economy, the growth of SMEs, and the participation of historically marginalized groups.Footnote 101

2. South Africa’s Antitrust Regime and Institutions

South Africa’s first competition law, the Regulation of Monopolistic Conditions Act, was passed in 1955. Under this law, the Minister of Trade and Industry could order investigations, which were then carried out by the Board of Trade and Industry. This enforcement structure, combined with a law with a “public interest” standard of analysis, led to a “cautious and permissive” system.Footnote 102 In 1979, a new law instituted a Competition Board, which was appointed by the Minister of Trade and Industry but could investigate matters on its own initiative. Real change, however, came around with the regime change in 1994, when the first broadly democratic government was elected.

In 1992, the African National Congress (ANC) adopted “policy guidelines for a democratic South Africa.”Footnote 103 A section on “antitrust, anti-monopoly, and mergers policy” declared:

The concentration of economic power in the hands of a few conglomerates has been detrimental to balanced economic development in South Africa. The ANC is not opposed to large firms as such. However, the ANC will introduce antimonopoly, antitrust and mergers policies in accordance with international norms and practices, to curb monopolies, continued domination of the economy by a minority within the white minority and promote greater efficiency in the private sector.Footnote 104

The ANC also stressed the “highly concentrated” nature of the domestic market in a white paper, concluding that market forces alone would not be enough to revitalize the economy—more active reforms in favour of SMEs would be needed.Footnote 105 The South African economy was indeed concentrated: five investment conglomerates accounted for 84% of the stock exchange’s total capitalization.Footnote 106 There are different reasons for this concentration. The conglomerates have their roots in the mining houses of the 19th century, which were historically the dominant economic force. Moreover, South Africa’s economic policy had been protectionist.

After a four-year process, the new Competition Act was adopted in 1998.Footnote 107 The goals of the Act were ambitious:

-

(a) to promote and maintain competition;

-

(b) to promote the efficiency, adaptability and development of the economy;

-

(c) to provide consumers with competitive prices and product choices;

-

(d) to promote employment and advance the social and economic welfare of South Africans;

-

(e) to expand opportunities for South African participation in world market and recognize the role of foreign competition;

-

(f) to ensure that SMEs have an equitable opportunity to participate in the economy; and

-

(g) to promote a greater spread of ownership; in particular to increase the ownership stakes of historically disadvantaged persons (HDPs).Footnote 108

These atypically broad goals distinguish the Act from EU and U.S. competition laws. Goals (d)–(g) in particular are broadly absent from EU and U.S. competition regimes. While the Act has been amended many times, its goals remain largely unchanged to this day.Footnote 109 The Act also embeds competition law’s three typical prohibitions—agreements, unilateral conduct, and mergers—but with greater detail on their bounds and more idiosyncrasies than their U.S. and EU counterparts.Footnote 110 We focus on the two provisions that relate directly to market power.

The Act prohibits “abuse of dominance,” thus using the EU’s—rather than U.S.’ “monopolization”—terminology.Footnote 111 There is a presumption of dominance when a firm holds a market share exceeding 45%, which approximates the EU’s threshold of 50%.Footnote 112 The Act prohibits both exploitative practices—for example, excessive prices—and exclusionary practices—for instance, refusal to supply.Footnote 113 Through active intervention of the competent minister, SMEs and firms controlled by HDPsFootnote 114 can benefit from extra protections against dominant firms. The law accords special attention to price discrimination. The U.S. also has a specific statute on price discrimination, which shares the goal of protecting SMEs,Footnote 115 but the South African Act is specific in its focus on HDPs. Exemptions from competition rules are possible, inter alia when they contribute to (i) maintenance or promotion of exports; (ii) expansion by SMEs and firms controlled by HDPs; (iii) economic development and growth of an industry; and (iv) the promotion of employment.Footnote 116

Next, the Act institutes an ex ante merger control regime, which prohibits mergers that are likely to “substantially prevent or lessen competition.”Footnote 117 As in the prohibition of abuse of dominance, a concern for efficiency is clear: anticompetitive effects can generally be offset by procompetitive gains. More than in those other prohibitions, however, “substantial public interest grounds” are front and center in merger control.Footnote 118 Such grounds include employment, SMEs and HDPs, competition in international markets, and the promotion of a greater spread of ownership, all of which can justify an otherwise anticompetitive merger.

Enforcement of competition law is entrusted to the independent Competition Commission of South Africa (CCSA), which has strong investigatory and remedial powers, investigates potential infringements, can impose fines and penalties, and authorizes or prohibits mergers.Footnote 119 The CCSA can also conduct larger market and sector-specific inquiries.Footnote 120 Decisions of the CCSA can be appealed to a specialized Competition Tribunal, which can also adjudicate competition law matters without a previous CCSA decision.Footnote 121 Decisions of the Competition Tribunal can then be appealed before the Competition Appeals Court.Footnote 122

3. South African Competition Law in Tech Markets

The CCSA has been paying close attention to competition in the digital economy. Its focus is set out clearly in a 2021 Digital Markets Paper:

The arrival and rapid rise of the digital economy presents South Africa with an opportunity to reverse the pervasive, triple scourge of unemployment, inequality and poverty. But in order to harness the promised benefits of digitalisation South Africa must create a commercial and regulatory environment designed to extract those benefits and distribute them in a way that ensures inclusive economic growth, that is 1) greater participation by black and women-owned firms and 2) increased and meaningful employment.Footnote 123

The overall view is that digital economy could benefit the South African economy, but only if it does not further a historical trend towards concentration—and characteristics such as network effects make platform markets especially susceptible to concentration. Countering concentration in tech markets requires proactive competition law enforcement.

Although the pace of enforcement has been picking up, the CCSA’s efforts in digital markets were, until recently, quite limited.Footnote 124 In line with EU and U.S. trends, merger control in the digital economy has been hands-off. As the CCSA noted in 2021:

[T]here may have been under enforcement in this area. This can be seen in the Commission’s statistics which show that of the 87 mergers in digital markets notified between 2011 and 2018, 82 were approved without conditions and the remaining 5 were approved with public interest conditions. Notably, no conditions have been imposed to address substantive competition concerns.Footnote 125

In recent years, the CCSA has become more proactive on merger enforcement. While in 2016 the CCSA approved Microsoft/LinkedIn without conditions, it imposed conditions in Google/Fitbit in 2020. As in the EU,Footnote 126 commitments related to access to the Android OS for manufacturers of competing wearables, data separation between Google and Fitbit, and continued access to Fitbit data by third parties such as app developers.Footnote 127 At the time of writing, the last major international, digital merger scrutinized by the CCSA is Microsoft/Activision-Blizzard. The CCSA approved the $69 billion acquisition without conditions in 2023,Footnote 128 while other major jurisdictions either approved the merger with conditionsFootnote 129 or tried unsuccessfully to block it.Footnote 130

The CCSA also frequently examines domestic tech mergers. The 2014 Takealot/Kalahari merger involved two of the largest online retailers in South Africa. Nevertheless, the CCSA approved the merger subject to conditions related to employment.Footnote 131 The most aggressive stance was taken in MIH eCommerce/WeBuyCars in 2018. MIH eCommerce is a holding company fully owned by Naspers Group, South Africa’s premier tech conglomerate. It operated a classified ads platform for new and used vehicles called Autotrader. The transaction would give it a 60% stake in WeBuyCars, which operated an online used car buying service. The merger did not present any actual overlap. However, Naspers had already acquired a stake in Frontier Car Group—an acquisition through which it intended to enter the South African market for online car buying. Based on this potential horizontal competition, combined with conglomerate effects, the CCSA recommended that the Tribunal prohibit the merger,Footnote 132 which it did.Footnote 133

When it comes to anticompetitive conduct, there have been two consequential abuse of dominance proceedings.Footnote 134 The first one was the Metered Taxi Industry v. Uber, in which the former accused the latter of, inter alia, predatory pricing. The CCSA took the view that Uber’s conduct did not contravene the Competition Act.Footnote 135 Given that the complaint was rejected, the record is short on reasons for the decision but is in line with those of other African competition authorities. The second proceeding concerned Meta, and in particular its WhatsApp messaging service. WhatsApp’s Business API, application programming interface, allows for mass messaging, advanced automation, e-commerce integration, and so forth.Footnote 136 A South African startup made use of this API to launch the GovChat platform, which enables government–citizen communication on anything from pothole alerts to covid awareness. When Meta off-boarded GovChat from the WhatsApp Business API, halting communication, the CCSA started an investigation. It sought and received interim relief from the Tribunal, which prevented the off-boarding.Footnote 137 Subsequently, it referred the full case to the Tribunal for prosecution, asking for the maximum fine, 10% of South African turnover.Footnote 138 In terms of abuse, it has identified either a refusal to supply, a refusal of access to an essential facility, or another exclusionary act. The underlying idea is that WhatsApp is the only communication platform with the necessary scale to host an effective government communication service. The Tribunal has yet to decide on the merits.Footnote 139

Both cases illustrate the quasi-regulatory role of the CCSA in South Africa that is unlike the role of competition authorities in Europe or the U.S. Indeed, they show that the CCSA acts as a guarantor of public services and of competition between private and public options on South African tech markets. The GovChat case in particular denotes an appetite on the part of South African competition authorities for treating Meta as a quasi-utility: an essential facility or critical infrastructure that must act in the public interest and ensure the smooth provision of government services to South African digital citizens.

4. South African Regulatory Developments in Tech Markets

In spite of their regulatory flavor, the competition law proceedings discussed above have been one-off, conduct-specific and backward-looking. The CCSA has also pursued a more comprehensive and forward-looking approach with its Online Intermediation Platforms Market Inquiry, the final report of which was published in July 2023.Footnote 140 The CCSA recognized the international context of its enforcement actions:

[T]he global reach of digital markets means that conduct found to be anticompetitive in one jurisdiction could easily be considered anticompetitive in other jurisdictions. We note, however, that each case would need to be assessed on its merits to determine the existence or otherwise of anticompetitive effects in South Africa.Footnote 141

With its Inquiry, the CCSA was meant to get a good overview of the specific competitive conditions of South Africa’s platform economy. It focused on the “leading” platform(s) in different categories:

-

• Search: Google;

-

• Travel and accommodation: Booking.com;

-

• E-commerce: Takealot;

-

• Software application stores: App Store (Apple) and Play Store (Google);

-

• Online classifieds: Autotrader and Cars.co.za (automotive), Property24 and Private Property (real estate);

-

• Food delivery: UberEats and Mr D Food.

The CCSA found that these platforms were engaging in anticompetitive conduct, ranging from self-preferencing to high commission fees to exclusive agreements, and ordered remedial actions. The remedial actions were platform-specific and often far-reaching. In the case of Google’s search engine, for example, the CCSA imposed the following:

On organic results, Google must introduce a new platform sites unit (or carousel) to display smaller SA platforms relevant to the search (e.g travel platforms in a travel search) for free and augment organic results with a content-rich display. Google must also introduce an SA flag identifier and SA platform search filter to aid consumers to easily identify and support local platforms in competition to global ones. On paid results, Google must provide R180m in advertising credits for small platforms to use in customer acquisition along with free training to optimize advertising campaigns. Google must also provide a further R150m in training, product support and other measures for SME and black owned online firms to offset the competitive disadvantages faced on Google Search.Footnote 142

On certain points, the Inquiry is strongly aligned with the EU’s DMA, to which it explicitly refers. To prevent Google from favoring its own specialized search services in its general search results, for example, “Google is required to implement in SA, measures taken in Europe to comply with similar provisions in the Digital Markets Act to address self-preferencing.”Footnote 143 But the above measures, which require Google to actively aid local competitors, go further. Other measures are more traditional: Booking.com, for example, is required to remove parity clauses, which it had previously done in the EU in response to antitrust investigations.Footnote 144

The CCSA and its remedial actions are effectively changing the market dynamics. This is thanks, in part, to the cooperation by the platforms in question. About half of the dozen platforms immediately started implementing the inquiry’s remedies; the other half filed appeals with the Competition Tribunal, but most of them have now settled.Footnote 145 Google is singled out as an example of a platform that has been implementing the remedies without contestation.Footnote 146

Building on the success of the platforms’ inquiry, the CCSA has followed up with an inquiry targeted specifically at platforms–news media relations, issuing a provisional report in 2025.Footnote 147 The report focuses the unequal bargaining position of publishers vis-à-vis Google (including YouTube) and Meta, and its effects.Footnote 148 It examines a variety of practices that might adversely affect competition, including imbalanced value extraction from news and the under-representation of local vs foreign media. Suggested remedies center around the representation of South African news, visibility, referrals, and a redistribution of value from platforms to publishers via a bargaining model and/or digital advertising levies.Footnote 149 The report also tackles Google’s dominant position across the AdTech stack.Footnote 150 The CCSA notes the strong appeal of a structural solution but considers it unworkable given South Africa’s small market size. However, the CCSA does propose that Google implement globally any structural remedy imposed by EUFootnote 151 and U.S.Footnote 152 agencies in their ongoing AdTech cases.

II. Kenya

We start this subsection by giving a snapshot of Kenya’s tech landscape (Subsection 1) and of its antitrust regime and institutions (Subsection 2), which provides the necessary background to understand the antitrust and regulatory developments in tech markets (Subsection 3).

1. A Snapshot of Kenya’s Tech Landscape

Kenya has one of the biggest digital economies in Africa. The country’s internet penetration rate is 32.7% representing 17.86 million internet users, while its mobile penetration rate is 117.2% representing 63.94 million cellular mobile connections.Footnote 153 Most Kenyans access the internet through their mobile phones, underscoring the role of mobile network operators (MNOs) in expanding internet connectivity. Digital penetration notwithstanding, the digital divide persists and is largely due to high cost of data and limited expansion of digital infrastructure beyond major towns.

Bridging the digital divide is one of the goals of the Kenyan government. It pursues this through national government projects such as the National Optic Fiber Backbone Project and through international submarine cables that are often laid by private sector investments by Big Tech companies from the U.S. and China. Elon Musk’s company SpaceX also launched its satellite internet service Starlink in Kenya, which the government hopes will enhance internet speeds in rural areas, schools, and institutions around the country.Footnote 154

The digital economy has stimulated innovation in sectors such as education, agriculture, finance, and logistics, which have propelled Kenya forward to the extent of being dubbed “the Silicon Savannah,” a moniker that likens it to Silicon Valley. There are a variety of technology hubs, accelerators and incubators which provide business support to startups. Nevertheless, startups face funding challenges.

Kenya’s most prominent innovation is the M-PESA mobile money platform, which in turn spurred innovations in other digital financial services. While the platform positively transformed the lives of many Kenyans, its dominance, alongside Safaricom’s, the MNO that owns the platform, has created a spate of challenges for the competition and communications authorities of Kenya, which have in turn pushed the development of the competition regime in Kenya.

2. Kenya’s Antitrust Regime and Institutions

Kenya was one of the earliest African countries to adopt a competition law. The first law, the Restrictive Trade Practices Monopolies and Price Control Act (RTPMPCA), was enacted in 1988 and entered into force in 1989. Its adoption was motivated by World Bank structural adjustment policies of the 1980s that were intended to shift the country from a price control regime with significant state intervention towards a market economy.Footnote 155

Prior to this, Kenya’s economy had a distinctively state-driven nationalistic bent intended to promote the participation of indigenous Kenyans in key sectors. This was largely a reaction to the pre- and post-independence domination by foreign multinationals and an Asian minority class that controlled the country’s middle-range retail commerce. Some of the measures adopted in furtherance of this goal included enactment of the Trade Licensing Act of 1967, which excluded non-citizens from trading in specific commodities/sectors,Footnote 156 and the creation of large state corporations to drive industrialization. The government also passed a Price Control Act in 1956 to control prices and introduce consumer subsidies as a mechanism for redistribution.Footnote 157

Following criticism that the 1988 RTPMPCA was outdated and ineffective,Footnote 158 a new Competition Act of Kenya (the Act) was introduced in 2010. Enforcement of the Act is undertaken by an independent national competition agency, the Competition Authority of Kenya (CAK), and a specialized quasi-judicial tribunal, the Competition Tribunal.

The Act is aimed at increasing consumer welfare, promoting and protecting competition and market-oriented objectives such as:

-

(a) increasing efficiency in the production, distribution and supply of goods and services;

-

(b) promoting innovation;

-

(c) maximizing the efficient allocation of resources;

-

(d) protecting consumers;

-

(e) creating an environment conducive to foreign and local investment;

-

(f) capturing national obligations in competition matters with respect to regional integration initiatives;

-

(g) bringing national competition law, policy and practice in line with best international practices; and

-

(h) promoting the competitiveness of national undertakings in world markets.Footnote 159

While these objectives focus primarily on efficiency and productivity, the Act’s provisions on mergers and restrictive trade practices also reveal a concern for public interest considerations.Footnote 160 For example, the CAK assesses mergers and acquisitions by looking not only at their effects on competition as traditionally understood in price and output terms, but also at their effects on job losses, the SME landscape, and the competitiveness of national industries in the world.Footnote 161

Abuse of dominance is prohibited and is deemed to include practices such as unfair pricing, limiting production, abusing an intellectual property right, applying dissimilar conditions to equivalent transactions, and imposing irrelevant conditions to the conclusion of contracts.Footnote 162 In general, a firm is dominant if it controls not less than one-half (50%) of the total goods or services produced/rendered in Kenya or a substantial part of Kenya.Footnote 163 Dominance can also be found below this threshold if there is evidence of market power.Footnote 164 The 2010 Act defines market power as “the power of a firm to control prices, to exclude competition or to behave to an appreciable extent, independently of its competitors, customers or suppliers.”Footnote 165 This definition of dominance, as well as the 50% market share threshold, is aligned with EU competition law.Footnote 166

The notion of an abuse of dominance and its application to digital markets is currently subject to potential reform by the Competition (Amendment) Bill.Footnote 167 The Amendment adds greater specificity to the manifestation of market power and dominance in digital markets and provides strategic tools for CAK to deal with it, as explained further below.

Another specificity of Kenyan competition law is its explicit prohibition of abuse of buyer power. The 2010 Act has a non-exhaustive list of examples of what might constitute abuse of buyer power including: payment delays to suppliers without justification, unjustified unilateral termination or threats of termination of a commercial relationship without notice or on an unreasonably short notice period; buyer’s transfer of commercial risks to suppliers; and anticompetitive price reductions.Footnote 168

3. Kenyan Antitrust and Regulatory Developments in Tech Markets

So far, the CAK’s enforcement has been less proactive than the CCSA’s. The CAK has not, to date, investigated any global tech mergers. It has, however, considered disruptions to the local economy resulting from the prevalence of (foreign) Big Tech platforms in the sectors of ride hailing services, online food deliveries, and digital financial services.

Like the CCSA, the CAK investigated a complaint on predatory pricing brought by traditional taxi operators against Uber.Footnote 169 It found that Uber did not have “market power or the ability to behave independently of its competitors and consumers.”Footnote 170 It noted that Uber faced significant competition from other app-based taxi companies and traditional taxis, and that its price per kilometer was above the average cost charged for taxi services.Footnote 171 For these reasons, the predatory pricing test was not met, and the investigation closed.Footnote 172 Given the pushback by traditional taxi operators, however, the CAK recommended further inquiry on the taxi transport sector prior to introducing new regulations.Footnote 173

In the food retail sector, the CAK investigated allegations of abuse of dominance against food delivery platform Glovo, UberEats, and Jumia Kenya.Footnote 174 The claim was that these apps imposed exclusivity clauses on third-party vendors, restricting entrants’ ability to develop or market competing applications.Footnote 175 After investigating the relevant markets, the CAK established that the apps were not dominant by market share because of a wide range of substitutable online instant delivery platforms. Nevertheless, it still recommended removal of any clauses that limited vendors’ access to other competing platforms.Footnote 176

CAK regularly conducts sector-specific market inquires, often seen as a preliminary means for advocating pro-competitive policies and regulations in given industries. Some of these inquiries offer useful insights into how CAK may handle digital platform markets that present similar challenges in the future. They show that CAK values competition as advanced through transparency and non-discrimination measures, as well as the sustenance of smaller firms.

The CAK conducted an important market inquiry into the pricing and other conditions for accessing unstructured supplementary service data (USSD) platforms owned by MNOs.Footnote 177 The USSD platform is a communications protocol used to send messages between MNOs and users. It is the predominant infrastructure used by banks and fintech services to offer mobile financial services. The MNOs providing this infrastructure also compete with banks and fintech apps in offering mobile financial services.

The inquiry surveyed whether the MNO-set terms of access restricted competition in financial services and whether Safaricom, the leading MNO, had abused its dominance. The CAK found excessively high prices charged by MNOs, which undermined the ability of smaller firms to offer competitive financial services. It also found that Safaricom had anticompetitively charged even higher prices to its biggest rivals and had denied access to its network outright. As regards remedies, the CAK required Safaricom to publish on its website the standard prices for USSD services for mobile financial services, in the hope of fostering greater transparency and lower overall prices. The CAK also recommended interoperability between the dominant M-PESA mobile wallet and other mobile money providers.Footnote 178

More recently, the CAK carried out a market study on online food delivery and grocery platforms to understand their business models and recommend appropriate regulation.Footnote 179 The report identifies several issues spanning the entire value chain, from retailers’ market power over digital platforms, to platform power over labor—for example, couriers—to the restrictiveness of data-related terms and conditions. Its recommendations included continuous monitoring and self-regulation through codes of conduct as well as the setup of physical offices on Kenyan territory.Footnote 180

The CAK is beginning to make strides towards establishing competition frameworks for digital markets. Although the 2010 Act does not include digital-specific provisions, the recently revised Guidelines on Relevant Market Definition recognize that “multi-sided markets,” “non-price markets,” and “digital markets” warrant special scrutiny, and provide that precedents from other jurisdictions will be followed in such cases.Footnote 181 More significantly, the Competition Amendment Bill of 2026—currently only a draft—would introduce specific provisions on competition in digital markets inspired by competition reforms across the globe.

The Amendment Bill defines “digital activities” to include: (a) online intermediation services, including online marketplaces and app stores; (b) online search engines; (c) online social networking services; (d) video-sharing platform services; (e) independent interpersonal communication services; (f) operating systems; (g) cloud computing services; and (h) online advertising services.Footnote 182 Save for the exclusion of web browsers and virtual assistants, this definition matches exactly the list of CPSs under the DMA.Footnote 183 The Amendment also expands the notion of market power in digital markets, via the concept of “strategic market position.”Footnote 184 The concept seems inspired by the UK’s Digital Markets, Competition and Consumer Act (DMCCA), which focuses on digital firms with “strategic market status.”Footnote 185 A strategic market position may be found even below market shares of 40%. The Amendment also directs regulators to consider factors such as direct and indirect network effects; economies of scale and scope, including access to competitively relevant data; switching costs for users and the ability to multi-home; the competitive pressure driven by innovation; and the importance of the intermediary services’ role as bottlenecks or infrastructures for the provision of other goods and services.

More innovatively, the Amendment adapts and extends the idea of abuse of buyer power to digital markets, introducing the notion of abuse of superior bargaining power.Footnote 186 Here, the CAK must first ascertain whether an undertaking has superior bargaining power, for example, because it is an unavoidable or critical business partner on which many other businesses depend, and whether it abuses or is likely to abuse such power. Examples of abuses of superior bargaining power include the list of abuses of buyer power but also include digital-specific examples such as unreasonable collection and processing of data or making it difficult to leave or terminate a service or digital account. Once a likelihood of abuse is determined, the CAK can then impose certain quasi-regulatory measures on the undertaking, including reporting, prudential requirements, and codes of practice.

The proposed Amendment has faced criticism from Big Tech interest groups, which may resonate more strongly in the midst of a tariff discussions, so it remains to be seen whether it ends up passing.Footnote 187

III. Conclusions

Our analysis of competition enforcement in two jurisdictions, South Africa and Kenya, does not justify broad claims on “African competition enforcement” and yet it is more informative than it may seem. The competition authorities we studied are two of the most active on the continent, certainly in digital markets, and their focus and approach are consistent with that of other authorities.Footnote 188 Their shared enforcement attitudes are increasingly leading to continental collaboration on digital competition.Footnote 189

We noted that many African competition law regimes are influenced by European competition law. Although enforcement in digital markets has been sparse in African jurisdictions until recently, a wave of interest in more proactive digital enforcement is visible, as illustrated by numerous sectoral inquiries and ongoing reforms to the existing competition law apparatuses. South African and Kenyan competition regimes illustrate a growing appetite for pro-competitive regulation, and for treating foreign tech companies such as Meta and Google as critical infrastructures that must advance local public options and promote local businesses. The enthusiasm for competition law enforcement in digital markets that we observe in South Africa and Kenya as well as the broader continental push for pro-competitive regulation through the Protocol raises a question we now turn to: What values and interests motivate these ongoing reforms? Do they respond to concerns about efficiency and consumer welfare? Are they primarily motivated by trade and investment rationales? Or, alternatively, are they motivated by national and regional interests and geared toward the health and diversity of local digital African economies? And how can these reforms be better aligned with the needs and priorities of African populations?

E. Toward Pro-competitive Regulation of Africa’s Digital Markets

In this final section, we build on the case studies and context to scrutinize the pan-African move toward pro-competitive tech regulation under the Protocol. We begin with an overview of the African digital economy, paying particular attention to its composition and the goals driving the development of policy and regulation (Subsection I). We then ask which goals and values should underlie pro-competitive gatekeeper regulation under the Protocol in light of present realities and goals of the African digital economy (Subsection II). We finally specify the Protocol’s scope of application and the meaning of the obligations it creates (Subsection III). We believe it crucial that the goals and values, scope, and obligations of proposed pro-competitive obligations reflect both the economic context and the legal tradition of the countries who are parties to the Protocol. Institutional realities must also be accounted for.Footnote 190

I. An Overview of the African Digital Economy

Digitalization is a key priority for African nations. While the continent has the lowest internet penetration rate, 38% compared to 87–92% in Europe and the Americas in 2024,Footnote 191 Africa’s digital economy has immense potential and is anticipated to reach 180B USD in value or 5.2% of gross domestic product (GDP) by 2025, and 712B USD or 8.5% of GDP by 2050.Footnote 192 Presently, this growth is largely concentrated in four markets—South Africa, Kenya, Nigeria, and Egypt, which collectively represent 51% of the continent’s GDP—but other nations’ digital economies also have growth potential.

As noted by a report of the African Union, with such growth on the horizon, Africa aspires toward an “integrated and inclusive digital society and economy that improves the quality of life of its citizens, strengthens the existing economic sector, enables its diversification and development, and ensures continental ownership with Africa as a producer and not only a consumer in the global economy.”Footnote 193 In furtherance of these goals, various countries are implementing national digital development strategies. At a regional level, countries are working together within the ambit of the AfCFTA to boost cross-border digital trade, and promote competition, itself understood as a key driver of innovation, industrialization, and sustainable development. AfCFTA’s Digital Trade and Competition Protocols serve as key instruments for advancing these objectives.

Africa’s digital economy has traditionally promoted solutions to persisting problems in sectors of the African economy such as education, healthcare, logistics, agriculture, and financial services. This is exemplified by tech companies such as Zipline, a logistics company that started out by using drones to deliver life-saving blood and medicines in Rwanda but has now expanded to other countries and regions.Footnote 194 Another example is Apollo Agriculture,Footnote 195 a Kenyan fintech startup that uses satellite data, machine learning, and mobile money to offer lending products, insurance, and farming inputs to smallholder farmers.Footnote 196 The main players in these lines of digital products are typically a mix of local and foreign tech companies. It is difficult to give precise figures on how many companies operate regionally or per country because the dynamic ecosystem of new startups changes rapidly.

Digital platforms are also on the rise. A digital platforms trends report suggests that while there are more homegrown platforms in operation, 82% in 2019, foreign platforms have a larger user base and are used more.Footnote 197 In 2019, for instance, the average number of users per platform was three times larger on platforms originating from outside of Africa than on homegrown platforms.Footnote 198 Commentators surmise that this could be because foreign platforms began operations earlier than domestic platforms and thus obtained a first-mover advantage.Footnote 199 Other reasons could be that local entrepreneurs face challenges raising capital to build, advertise, and operate at scale successful businesses that effectively compete with foreign-backed tech companies with fewer funding challenges. In addition, dominant global platforms possess key physical and data infrastructures that enable them to perform market-shaping functions that smaller tech companies rely on.Footnote 200 The same is true for local dominant platforms such as mobile money service M-PESA.Footnote 201

A variety of global and homegrown digital platforms operate in different markets, concentrated around a few key sectors: online shopping—for example, Jumia, Takealot, Konga, Kilimall, and Alibaba; food delivery services—for example, UberEats, Glovo, Mr.D, Jumia Food; ride hailing—for example, Uber, Bolt, Taxify, Little Cab, SafeBoda; hotel and accommodation—for example, Airbnb, Booking.com; social media—for example, Facebook, Instagram, TikTok, Snapchat, Twitter, LinkedIn; instant messaging—for example, WhatsApp; search engines, Google, Bing; music streaming—for example, Spotify, Apple Music, Boomplay, YouTube Music, Mdundo, MusikBi; video streaming—for example, Netflix, Showmax, NollyLand, Canal+, Disney+; e-logistics—for example, Lori Systems, Ngamia, Leta, Sendy, Bwala, Kobo360, Truckr. Presently, platforms that have attained considerable cross-border expansion include Jumia (Nigeria), Takealot (South Africa), Spotify (U.S.), Alibaba (China), Uber (U.S.), Bolt (Estonia), YouTube Music (U.S.), Airbnb (U.S.), Booking.com (Netherlands), Netflix (U.S.), Showmax (South Africa), and the various U.S. social media and messaging platforms.

While Africa’s digital economy is very much locally rooted, it is also shaped by foreign ownership of and access to market-shaping digital infrastructure. In addition, African countries are economically dependent on large foreign technology companies, such as those mentioned above, which are seen as essential partners in digital development projects aimed at increasing internet connectivity. Regulating the digital economy through competition policy or otherwise therefore involves a delicate consideration of government interests, key international and local tech players, SMEs, and local groups.

Nevertheless, African countries are pushing their technological vision forward. Their vision involves balancing these competing interests in pursuit of inclusive socio-economic development, the overarching goal of the AfCFTA. In the digital sphere, inclusive development is articulated through both the AfCFTA’s Digital Trade Protocol and the continent’s Digital Transformation Strategy, each emphasizing the need to harness digital technologies for inclusive economic growth. The Digital Trade Protocol in particular aims to “generate sustainable and inclusive economic growth, stimulate job creation, reduce inequality, and eradicate poverty.”Footnote 202 To this end, it promotes the development of an integrated African digital market with strong domestic content; it also promotes support for African firms, the use of African digital platforms,Footnote 203 and the inclusion of SMEs and marginalized groups such as women, youth, indigenous peoples, rural communities, and persons with disabilities in digital trade.Footnote 204 Universal internet access is also prioritized, coupled with a regulatory environment that attracts investment in digital infrastructure.Footnote 205 Within this framework, competition and investment policy are viewed as essential and operating in tandem. The pressing question is how African nations can leverage competition policy not only to encourage investment but also to strengthen indigenous economic development and ensure the meaningful participation of SMEs and historically marginalized groups in the digital economy.

II. Goals and Values

We have described pro-competitive regulation as an extension of competition law. Here, we examine pro-competitive regimes’ underlying goals and values as they arise in the EU’s regulatory model and examine how they could change in the African context.

1. The EU’s Influence: Fairness and Contestability

The EU has been a source of global inspiration, especially in the digital economy.Footnote 206 The values underlying the European approach to digital markets have evolved over time. Europe has moved from a focus on removing barriers to digital trade and competition in the internal market to an approach that actively promotes the fairness and contestability of digital markets, and positively enables a better exercise of consumer and entrepreneurial choice. Fairness implies equalizing relations in digital markets by imposing obligations on gatekeepers to prevent them from extracting disproportionate rents compared to their business users, and to prohibit discriminating against business users, that is to say, not to engage in self-preferencing.Footnote 207 In digital markets, the notion of fairness, in other words, translates into ideas of balanced and equal access to powerful platforms. Beyond the DMA, fairness can also inform an industrial policy agenda favoring greater market opportunities, which can be promoted for instance by government investments and rules favoring entrepreneurship and innovative small businesses. Contestability, a term coined by William Baumol and others and repurposed by DMA drafters, is about enabling entrants and smaller firms to exert competitive pressure on incumbents.Footnote 208 This is done by lowering barriers to entry, for example, via interoperability and data sharing obligations. These values are being incorporated in African jurisdictions in more or less clear-cut ways and for a variety of different reasons.

The clearest-cut examples of legal borrowing are the pro-competitive regulatory regimes in South Africa, Kenya and under the AfCFTA Protocol that form this Article’s primary object of inquiry. The South African CCSA’s Online Intermediation Platforms Market Inquiry has led to new pro-competitive obligations being imposed on tech companies in search, travel, e-commerce, app stores and food delivery markets.Footnote 209 Many of these obligations address conduct, such as self-preferencing by search engines, in a way similar to the DMA. Yet South Africa is also pushing these obligations further, asking companies like Google to ensure that the interests of local South African businesses are represented and prompting criticism that the DMA model is being taken “to the extreme.”Footnote 210 In Kenya, the Competition Amendment Bill would introduce new provisions that impose stricter obligations on digital services that have a strategic market position.Footnote 211 Here, there seems to be a mix of influences, as the list of services matches the DMA, but the notion of “strategic market position” seems inspired by the UK’s DMCCA. As noted, and further discussed below, the AfCFTA Protocol is also largely inspired by the European approach to pro-competitive digital market regulation.Footnote 212