Trends and key challenges in health care financing

Health financing is a key component of any health system, but its role is more complex than simply raising and spending money on health. It is a crucial determinant of the overall performance of the health system, defining, among other things, how much money is available to be spent on health and who pays for it, who gets to benefit from those financial resources, what services that money can purchase and who ultimately receives resources from the health system as income. Without careful attention to the way health financing systems are designed, incentives for providers or patients can be misaligned with policy goals, leading to poor health outcomes, financial hardship for users of health care, wasted resources, failure to address inequalities and disruption of countries’ progress towards universal health coverage (UHC) (Box 0.2.1).

UHC refers to the concept that all individuals and communities receive the quality health services they need without suffering financial hardship (WHO, 2023). It is widely seen as a goal of societies to ensure that everyone has access to essential health services, including prevention, promotion, treatment, rehabilitation and palliative care, without facing financial barriers. UHC as a policy objective is enshrined in numerous international and regional agreements, including the Sustainable Development Goals (United Nations, 2024).

In 2002, the European Observatory on Health Systems and Policies published a volume on health financing entitled Funding health care: options for Europe (Mossialos et al., 2002). Despite being more than 20 years old, that book remains one of the most downloaded and referenced books in the Observatory’s study series. Since its release, there have been important global shifts in health financing, including the ways revenues for health are generated and pooled, and advances in topics such as priority-setting, approaches to purchasing and provider payment methods.

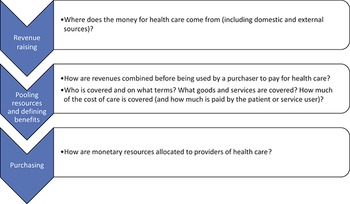

In this book, our aim is to go beyond simply producing an update of that 2002 volume, which focused primarily on the ways revenues for the health system are generated but devoted less attention to other aspects of health financing. We have assembled a team of distinguished authors from around the world with expertise in theory and practice to provide an up-to-date analysis of recent experience in different topics of health and long-term care (LTC) financing. The following chapters are organized systematically around the three key health financing functions: revenue raising, pooling resources and defining benefits, and purchasing services. This structure follows the well-established framework first published by Kutzin (Reference Kutzin2001) and later adapted elsewhere (Papanicolas et al., 2022). These functions describe the way money flows through any health system, from collection to payment, in distinct stages (Fig. 0.2.1). Each of the chapters within these three broad sections of the book examines a particular aspect of the corresponding financing function. For each chapter, the authors begin by discussing the relevance of the topic, followed by an exploration of relevant academic theory. Finally, authors survey recent literature and global country experiences to provide insights into the current state-of-the-art of health financing.

How does money flow through the health system? The health financing functions

Figure 0.2.1 Long description

The flowchart starts with Raising revenue - Where does the money for health care come from (including domestic and external sources)? The next step is Pooling resources and defining benefits - How are revenues combined before being used by a purchaser to pay for health care? Who is covered and on what terms? What goods and services are covered? How much of the cost of care is covered (and how much is paid by the patient or service user)? The final step is Purchasing - How are monetary resources allocated to providers of health care?

By expanding the geographical coverage beyond Europe, this volume addresses key health financing issues relevant around the world, including topics which have historically received less attention such as community-based health insurance (CBHI), official development assistance (ODA) and pandemic preparedness, among others. Our goal is to provide a key resource for policy advisors at national and international levels, as well as a textbook for postgraduate students and others with interest in health financing.

In the following sections we provide a brief introduction to each of the financing functions for readers to better understand what each function includes, why it is relevant and how it can impact wider health system objectives, including efficiency, equity and quality of health care services (see Box 0.2.2). The aim here is not to provide a summary of the ensuing chapters, but rather, to provide motivation to read the material to come.

Throughout this book, references are made to concepts such as efficiency, equity and quality. We use the following definitions for these:

Efficiency: “Health system efficiency seeks to capture the extent to which inputs to the health system, in the form of expenditures and other resources, are used to secure valued health system goals” (EOHSP, 2024).

Equity: “ … the absence of unfair, unavoidable or remediable differences among groups of people, whether those groups are defined socially, economically, demographically, or geographically or by other dimensions of inequality (e.g. sex, gender, ethnicity, disability, or sexual orientation)” (WHO, 2024a).

Quality: “Quality of care is the degree to which health services for individuals and populations increase the likelihood of desired health outcomes. It is based on evidence-based professional knowledge and is critical for achieving universal health coverage” (WHO, 2024b).

Revenue raising

Revenue raising is the way that funding is generated for the health system and includes a description of the sources that fund the health system. In this first section of this book, our focus is on the funding mechanisms of entities (e.g. insurance schemes) that pool resources to purchase health goods and services on behalf of individuals. Historically, analysts have often distinguished between public sources of financing collected by governments or quasi-governmental entities (e.g. in the form of taxes), and private sources of financing such as voluntary insurance premiums or user charges paid at the point of service use. While the public versus private funding dichotomy is relevant, some analysts have begun to take a different approach after realizing that in some countries private sources of funding share a lot of characteristics with public sources of funding. For example, where payment of private insurance premiums is mandatory, it can be difficult to argue that it differs from a tax from the perspective of a household making payments (although there may be differences from the perspective of the fairness of financing as well as pooling (see below)). In this case, the degree of compulsion (i.e. if prepayment is mandatory or voluntary) may be more relevant than a distinction between public versus private.

Moreover, the public versus private funding distinction alone may not reveal much about the reliability or stability of a funding source, or the fairness of financing. For example, there are important differences between different types of revenue raising-mechanisms that are collected by the public sector, such as various forms of taxation. As an illustration, income taxes, sales taxes, excise taxes and social health insurance (SHI) might vary in their ability to generate revenues depending on the objectives of the tax system, the state of the economy and labour market participation levels in a country. Furthermore, the various sources may differ in terms of their progressivity or regressivity (that is, who ultimately bears the financial burden of an employment tax?). And even when taxes are intended to be progressive, they have the potential to become regressive if there is a cap on the amount paid through general or local taxes or SHI contributions. This can all lead to important variations in the equity implications of different forms of compulsory health contributions.

While compulsory revenue raising-mechanisms can therefore be either public or private, voluntary health insurance (VHI) mechanisms are distinctly private. There are still differences across various forms of VHI, such as between medical savings accounts (MSAs) which allow individuals to save their own money for medical expenses, typically in a tax-advantaged manner, and which as a result pool risk within an individual or household; CBHI which pools resources within a local community in contexts where formal health insurance coverage is otherwise limited; and mechanisms which pool across a wider scheme, namely complementary insurance (which provides additional coverage for services which are already part of a statutory benefits package, such as compensation to households to cover the cost of user charges), or supplementary insurance (which provides increased choice of provider and offers expedited access to health care providers and enhanced amenities in hospitals, such as single-room accommodations).

MSAs are not the predominant source of funding in any health system and feature only as a minor portion of revenue in a few countries (China, Singapore, South Africa and the United States of America (USA)). In all countries, a key characteristic of VHI is that the decision to participate in these revenue raising-mechanisms is optional. This has important implications, as individuals with a lower perceived risk of needing health care may opt out of participation in a VHI scheme. Spending on voluntary insurance is typically a small portion of total expenditure, and in many countries VHI acts as a fringe benefit for employees or is purchased by wealthier people to obtain preferred access to care or, in a few countries, is used to mainly cover statutory co-payments for publicly funded services.

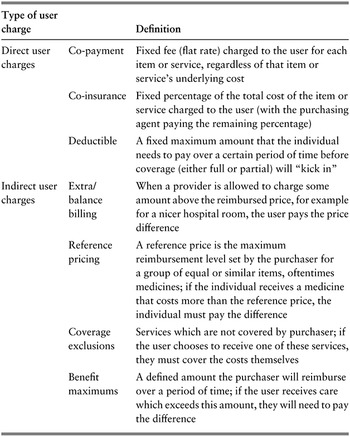

Another important source of funding for the health system is out-of-pocket (OOP) payments. These are payments made by households at the point of accessing health care goods and services. They do not typically serve as revenues per se from the perspective of this book because they are not necessarily pooled or redistributed across users of health services unless they are transferred from providers to ministries of health or finance, which oftentimes is not the case. However, they do serve as a major source of health financing, albeit one which we address more substantively elsewhere in this book (e.g. in Chapter 2.4 on user charges and Chapter 3.3 on informal payments). There are two broad types of OOP payments: those which are paid for covered (i.e. statutory) services and those which are paid for non-covered services. The former includes user charges (see Table 0.2.1 and Chapter 2.4) whereas the latter includes OOP payments for items such as over-the-counter medicines and services that are not part of a statutory benefits package.

Table 0.2.1 Long description

The table has 2 main columns: Type of user charge and Definition. Under Direct user charges. Co-payment: Fixed fee (flat rate) charged to the user for each item or service, regardless of that item or service’s underlying cost. Co-insurance: Fixed percentage of the total cost of the item or service charged to the user (with the purchasing agent paying the remaining percentage). Deductible: A fixed maximum amount that the individual needs to pay over a certain period of time before coverage (either full or partial) will kick in.

Under Indirect user charges. Extra or balance billing: When a provider is allowed to charge some amount above the reimbursed price, for example, for a nicer hospital room, the user pays the price difference. Reference pricing: A reference price is the maximum reimbursement level set by the purchaser for a group of equal or similar items, oftentimes medicines; if the individual receives a medicine that costs more than the reference price, the individual must pay the difference. Coverage exclusions: Services which are not covered by the purchaser; if the user chooses to receive one of these services, they must cover the costs themselves. Benefit maximums: A defined amount that the purchaser will reimburse over a period of time; if the user receives care that exceeds this amount, they will need to pay the difference.

Importantly, while households are primarily responsible for paying taxes, social insurance contributions, private insurance premiums and OOP payments, it is only the first two which are traditionally considered as public spending, while the latter two are considered as private.

Ultimately, whichever revenue raising-mechanisms are used, they must generate sufficient resources for the health system so that it is properly resourced. To this end, there will naturally be differences across countries in terms of the most efficient and sustainable revenue bases. In settings with large informal economies, generating adequate resources for the health system through compulsory financing mechanisms can be challenging, often resulting in a heavy reliance on user charges.

Most commentators would argue that revenues should be generated fairly and equitably so that those who pay the most for health do so because they can afford to do so, not because they are less healthy and need more services. When considering equity, one can think of different financing sources as regressive – where the poor end up paying a higher percentage of their income than the rich – or progressive – where the rich pay a higher percentage of their income than the poor. While it is uncontroversial to assert that OOP payments at the point of use are regressive because poor households are likely to have higher health needs and in many instances face the same prices for services as wealthier people, different forms of prepayment (e.g. taxes or insurance contributions) which are paid in advance of care provision irrespective of an individual’s eventual use of goods and services may have different equity implications depending on their design. For example, sales and value-added taxes (VAT) are typically somewhat regressive as they usually charge a fixed percentage on a good or service regardless of the income of the person purchasing it. However, if these taxes are structured with tiered rates, particularly with significantly higher VAT taxes imposed on luxury goods, their regressivity can be alleviated to some degree.

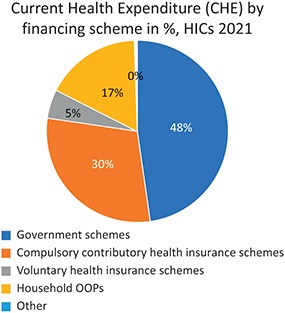

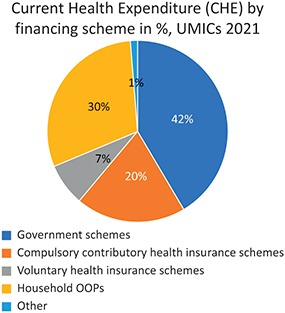

There are also external sources of financing, such as charitable donations, bilateral and multinational development assistance for health and philanthropic donor funds, to consider. These sources often come with important conditions of how the funds can be used, implicitly shaping some aspects of the health system. They are most common in developing country settings (though they still account for less than 10% of total revenue in low- and middle-income countries (LMICs)) although some high-income countries (HICs) also do benefit from some external financing sources (see Fig. 0.2.2). For example, there are a range of mechanisms that provide some European Union (EU) funding to EU countries’ health systems, although this is in a fairly limited capacity. Furthermore, external assistance can often come in the form of technical assistance or infrastructure projects and does not always entail direct subsidies for operational health services.

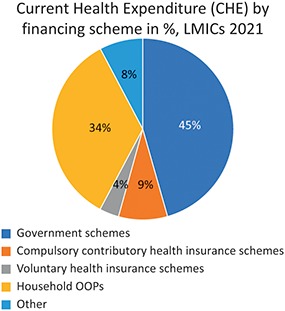

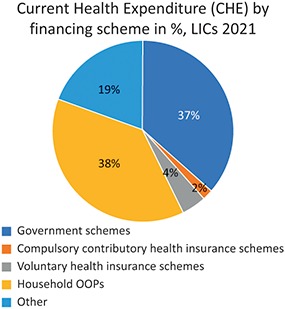

Average share of health spending by financing agent, by country income grouping, 2021.CHE: current health expenditure; HIC: high-income country; LIC: low-income country; OOP: out-of-pocket; UMIC: upper-middle-income country.

Notes: Unweighted average. Democratic People’s Republic of Korea, Libya, Somalia (no data available for 2000–2021), Syrian Arab Republic and Yemen (no data were available for later years and not included in 2020–2021 data) were excluded from average calculation. The “Other” category subsumes a variety of other financing schemes including foreign aid in-kind (e.g. provided by nongovernmental organizations). Government, and other compulsory, schemes may include revenues from foreign transfers.

Fig. 0.2.2a Long description

The pie chart outlines 5 schemes. Government schemes: 48 percent. Compulsory contributory health insurance schemes: 30 percent. Voluntary health insurance schemes: 5 percent. Household O O Ps: 17 percent. Other: 0 percent.

Fig. 0.2.2b Long description

The pie chart outlines 5 schemes. Government schemes: 42 percent. Compulsory contributory health insurance schemes: 20 percent. Voluntary health insurance schemes: 7 percent. Household O O Ps: 30 percent. Other: 1 percent.

Fig. 0.2.2c Long description

The pie chart outlines 5 schemes. Government schemes: 45 percent. Compulsory contributory health insurance schemes: 9 percent. Voluntary health insurance schemes: 4 percent. Household O O Ps: 34 percent. Other: 8 percent.

Fig. 0.2.2d Long description

The pie chart outlines 5 schemes. Government schemes: 37 percent. Compulsory contributory health insurance schemes: 2 percent. Voluntary health insurance schemes: 4 percent. Household O O Ps: 38 percent. Other: 19 percent.

What is in the chapters?

This section of the book includes four chapters. The first focuses on revenues generated through compulsory contributions in the form of taxation and SHI. As mentioned, these public sources of financing are widely recognized as a key prerequisite for countries to progress towards UHC. The chapter discusses the complexities governments encounter in raising public revenue, examining challenges such as low levels of economic development, weak governance, narrow and unstable tax bases, high levels of informal economic activity, an ageing population exiting the labour force en masse and the growing incidence of noncommunicable diseases and comorbidities. Through various examples, the chapter provides insights into the efficiency and equity of relying on different forms of public financing to pay for health care in different countries and proposes solutions to some of the main challenges.

Next, are two chapters on VHI. Chapter 1.2 is on CBHI, a form of voluntary insurance used in some low-income settings to expand access to care. Various forms of CBHI acted as a precursor to more formal health systems in many HICs and can be viewed as stepping stones towards more mandatory arrangements. However, as the authors describe, CBHI is insufficient on its own to serve as a mechanism for progressing towards UHC. Some of the distinguishing characteristics of CBHI schemes are its community ownership and participatory management of the schemes, as well as being non-profit. Chapter 1.3 covers VHI more generally, considering the ways voluntary insurance can and cannot improve access to care. While prepayment and risk pooling are positive attributes of VHI schemes, they cannot serve as a legitimate basis for progress towards UHC due to their inherent feature that not everyone will participate in them, and may in some cases prove inimical to that objective. Countries will always find it challenging to achieve UHC solely through VHI, as economic theory and country experiences demonstrate that those who are poor or in ill health are most likely to be excluded from coverage. Indeed, many VHI systems use risk-adjusted premiums based on health status, and as a result cannot efficiently cover the poor (and even the middle classes). Making VHI compatible with UHC requires political commitment, careful policy design, strong regulatory capacity and efforts to ensure that publicly financed coverage meets the needs of individuals with lower incomes or chronic conditions.

Lastly in the Revenue raising section of the book is a chapter on ODA as a source of revenues for health systems. The chapter uses the coronavirus disease (COVID-19) pandemic to argue the case for development assistance for health. It considers why ODA is important, how it works and which key actors have been involved historically.

Pooling resources and defining benefits

Pooling is the health system function whereby prepaid health revenues are aggregated and transferred to organizations that plan and purchase health services for a defined population. The primary purpose of pooling is to spread financial risk across the specified population so that no individual carries the full burden of paying for health care. The intention is, so far as possible, to make an individual’s financial contributions to the health system independent of their medical needs.

Risk pooling exists, to different extents, in all countries and is in effect a health insurance function for the covered population. However, there are numerous possible pooling modalities. There may be single or multiple pools, competing or non-competing pools, territorially distinct or overlapping coverage, and insurance options tailored for specific population groups or designed to cover the entire population. The pooling arrangements found in particular countries are often the result of historical path dependencies and political decisions in the development of their health system. These decisions may have been influenced by factors such as previous reliance on employer-based health insurers, the role of local governments to organize health services, or the establishment of discrete health insurance schemes for civil servants.

Among the three fundamental functions in health system finance – raising revenue, pooling and purchasing of services – it is risk pooling that has received least academic and policy attention. Yet the design of pooling arrangements is a crucial determinant of the efficiency and equity of the health system.

The nature of a country’s pooling choices can be examined using the coverage “cube” first conceptualized by Busse, Schreyögg & Gericke in 2007 and further developed by the World Health Organization and others since to illustrate progress towards UHC (WHO, 2021). The three dimensions along which policy choices must be made for UHC are:

1. Population: which population groups are covered?

2. Services: which services are covered, and of what quality?

3. Direct costs: what proportion of the costs of access must be covered by the beneficiary?

These choices mirror the fundamental aspects of design that must be addressed when creating pooling arrangements.

A fundamental decision is the nature of the population group covered by each risk pool. In many health systems, early forms of risk pooling covered only workers in formal employment (and in some cases their dependants). For example, early forms of SHI used separate risk pools for different industrial groups. The financial capacity and medical needs of these pools could vary considerably, leading to variations in insurance premiums and the medical services covered, giving rise to manifest inequalities and administrative complexity.

While many health systems still only cover a portion of the population through risk pools, defined by factors such as employment status, age or deprivation status, there is growing recognition that risk pools should be structured to provide coverage to the entire population, irrespective of medical or economic status. This concept underpins the idea of “universal” health coverage. This does not necessarily rule out the creation of separate or supplementary risk pools to cover specific services, such as LTC or mental health services, if such “carve outs” are deemed to be favourable for either medical quality, administrative efficiency or even political reasons.

The services covered by a risk pool are commonly referred to as the health benefits package (HBP), which should in principle specify both the services covered and the circumstances in which they can be received. The benefits package can be explicitly defined, but, in a surprisingly large number of systems, is either undefined, or defined only partially or in very loose terms. In a health system with fragmented risk pools, citizens may have access to very different packages, depending on the resources available to the risk pool of which they are a member. However, under UHC there is a policy intention to mandate a nationally uniform HBP, defined in terms of its contents, the quality of services and the population groups entitled to secure access to specific treatments.

User charges are the third aspect of risk pooling design. They can be defined in terms of how the amount charged is determined, the type of service being used and the circumstances of the service user (see Table 0.2.1). For example, many systems waive some user charges for lower-income users. As for the benefits package, insurance premiums and user charges can vary considerably between pools in a fragmented system. However, under UHC they should be nationally mandated. In combination, the nature of the benefits package and the system of user charges are fundamental determinants of the level of financial protection offered to individuals by the pooling arrangements.

There are some commonly used variations from the simple design of risk pools described above. For example, some services (especially for high cost, low frequency treatments) might be transferred from local risk pools to a national risk pool in order to mitigate the financial risk to the lower-level pool arising from such services. It is also sometimes the case that certain services, such as LTC or public health, are carved out of the benefits package to create separate risk pools administered by separate institutions.

A well-established principle of health insurance, known as adverse selection, is that – if membership of an insurance scheme is voluntary – healthier individuals may opt out of the scheme, leaving the scheme with an increasingly unhealthy population base, increasing levels of premiums, and the eventual breakdown of the insurance arrangements (referred to as the “death spiral”). For this reason, it is generally considered essential that membership of statutory risk pools should be compulsory to assure the financial stability of the health system. In some countries there may nevertheless be additional VHI provision, which enables people with adequate resources to purchase insurance beyond the standard risk pool. The effect of such provision depends on whether it is a complement to or replacement for coverage offered by the standard risk pools, and whether it enables purchasers of private insurance to opt out of premiums for the standard risk pool, as is the case in Germany or Chile.

What is in the chapters?

This section of the book includes five chapters. The first examines principles and practices of risk pooling in modern health systems. It considers the merits of consolidating or merging pools, boosting funding for less well-endowed pools in a fragmented system, implementing and improving risk adjustment across separate pools via direct transfers between pools, making membership compulsory and aligning benefit packages and payment systems across pools. The second chapter examines the setting of benefits packages. Although it highlights the important role of economic analysis in this task, it refers to the wider political, administrative and ethical context within which benefits package choices must be made. In principle, setting a benefits package requires the specification of services to be excluded from statutory provision as well as those to be included. In particular, with rapid technological developments, there are often treatments that have historically been provided by the health system that no longer offer value for money. The next chapter, Chapter 2.3, discusses the challenging task of identifying and disinvesting from such treatments.

Chapter 2.4 discusses the two main forms of direct user charges for goods and services that are included in the benefits package: fixed co-payments, which are a fixed amount of money that are not linked to the cost of the good or service, and percentage-based co-payments, based on a proportion of the price of the good or service. Such user charges are introduced in the belief that they will generate revenue for the health system, or moderate demand for services. However, research consistently finds that user charges have unintended consequences: they cause patients to skip necessary as well as unnecessary health care resulting in financial hardship (and potentially higher health care costs borne by the purchasing agency in the future if patients end up requiring more expensive hospital services), particularly for people with low incomes and people with chronic conditions. Unless direct user charges exempt high users of health care, they essentially become a tax on people in poor health.

The final chapter examines the especially challenging issue of designing pooling arrangements for LTC, a policy issue of rapidly increasing importance given population ageing and older peoples’ care needs, and the changing structure of families who might hitherto have offered informal care.

Purchasing health care

Purchasing is the final stage in the flow of funds. Pooled resources are used by a purchaser (the entity responsible for spending pooled funds) to pay providers for goods and services, often on the basis of some predetermined contract. The overarching aim of purchasing is to ensure that monetary resources are used efficiently and equitably and that resources are allocated according to the purchaser’s objectives. In the context of UHC, the purchasing function should ensure that appropriate, high-quality care is delivered to patients who need it in a way that minimizes waste and other forms of inefficiency (e.g. prices which do not reflect actual costs or value, or over- or underprovision of services). An intrinsic element of the purchasing function is to provide appropriate incentives to service providers beforehand (ex ante), and that the performance of the provider is monitored afterwards (ex post).

Purchasing is often described in terms of being either strategic (alternatively, active) or passive. In essence, strategic purchasing refers to the deliberate ability to make key evidence-based decisions regarding the utilization of pooled resources. This means that purchasers are able to decide which providers to purchase from (selective contracting), which services to purchase from those providers, how to pay providers and how much to pay. Strategic purchasing is the concept that emphasizes active deliberation by purchasers to determine how money is spent within health systems. And yet, while this may be an ideal objective, purchasing is rarely, if ever, done in a fully strategic manner, even in well-developed health systems (Klasa, Greer & van Ginneken, 2018). In many instances, health care providers are reimbursed regardless of the appropriateness of services provided or even when the quality of those providers has not been evaluated.

Providers should be held accountable based on explicit or implicit criteria, which ideally specify the expected performance standards. Therefore, a key and often-neglected component of purchasing is performance monitoring. Monitoring is necessary to ensure that services are delivered in line with patient and purchaser expectations, and that fair prices are paid for goods and services. Monitoring is also essential for comparing the performance of different providers, establishing benchmarks for future performance and informing decisions regarding provider selection in the future.

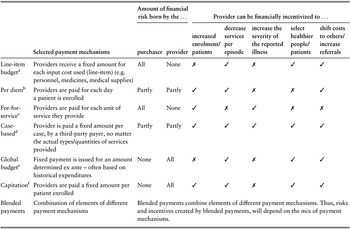

There are different payment mechanisms used for different types of care and across different care settings, which can be either prospective or retrospective (i.e. before or after care is delivered, respectively). These include line-item budgets, per diem, fee-for-service (FFS), case-based payments, global budgets, capitation and blended payments which combine different payment mechanisms (Table 0.2.2).

Table 0.2.2 Long description

The table has 3 main columns (and multiple subcolumns): Selected payment mechanisms, Amount of financial risk born by the (purchaser and provider), and Provider can be financially incentivized to (increased enrolment or patients, decrease services per episode, increase the severity of the reported illness, select healthier people or patients, and shift costs to others or increase referrals. It reads as follows. Row 1. Line-item budget: Providers receive a fixed amount for each input cost used (line-item) (for example, personnel, medicines, medical supplies); All; None; cross; tick; cross; tick; tick. Row 2. Per diem: Providers are paid for each day a patient is enrolled; Partly; Partly; tick; tick; cross; cross; tick. Row 3. Fee-for-service: Providers are paid for each unit of service they provide; All; None; tick; cross; tick; cross; cross. Row 4. Case-based: Provider is paid a fixed amount per case, by a third-party payer, no matter the actual types or quantities of services provided; Partly; Partly; tick; tick; tick; tick; tick. Row 5. Global budget: Fixed payment is issued for an amount determined ex ante - often based on historical expenditures; None; All; cross; tick; cross; tick; tick. Row 6. Capitation: Providers are paid a fixed amount per patient enrolled; None; All; tick; tick; cross; tick; tick. Row 7. Blended payments: Combination of elements of different payment mechanisms; Blended payments combine elements of different payment mechanisms. Thus, risks and incentives created by blended payments will depend on the mix of payment mechanisms.

Note: This “cheat sheet” provides simplified information around how different provider payment mechanisms typically work and incentivize financially. However, it is essential to note that there are exceptions and nuances in reality that cannot be reflected with binary labels. Some of these are listed in the notes below. Further, a payment structure may create financial incentives but does not necessarily dictate provider behaviours as there are other nonfinancial incentives that will play a role in decision-making.

a Under line-item payments, whether providers lack incentives to increase enrolment or amplify the severity of reported illnesses hinges heavily upon how the line-item budget is structured and what expenses are deemed justifiable. However, generally, line-item budgeting can lead to strong cost control and risk of under provision of services.

b Generally, under per diem payment structures providers are incentivized to increase admissions/enrolment and patients’ length of stay. If there is a fixed payment per day and it remains consistent for all days of hospitalizations, providers might be incentivized to exaggerate the severity of a patient’s condition to justify an extended length of stay, and they may lack the incentive to increase the number of patients. Under this scenario of a fixed, consistent payment per day per patient providers may also opt to select healthier patients who will require less services during the days that they are hospitalized.

c Generally, under FFS payment systems, the provider may be financially incentivized to overprescribe/overprovide costly services/care.

d Under case-based payments, the purchaser faces risk depending on the number of cases and the case severity classification, but the provider faces the risk of cost of treatment for a given case. Generally, however, most of the risk falls on the purchaser unless the number of cases to be delivered is contractually specified. Therefore, it is important to consider how providers will be compensated if they exceed the contractually specified cases, such as reimbursement of variable costs only. Typically, case-based payments can incentivize higher volumes (of patients, care episodes), efficiency improvements, shifts to ambulatory care strategies and selection of low-cost patients.

e Global budgets/salary payments typically incentivize cost control and may risk under provision and/or low productivity.

f Under capitated payment systems, providers are typically incentivized to enrol more patients and control costs. There is a risk of under provision of care, patient selection and cost shifting.

Different payment mechanisms vary in the financial incentives they offer providers, and the extent to which they put the bulk of the financial risk on the provider or the purchaser (see Table 0.2.2). They therefore have a profound effect on provider behaviour, and ultimately patient care. For example, FFS, where a provider is paid a specific amount for each specific service they offer, puts the financial risk on a purchaser because the purchaser is effectively reimbursing the services delivered by the provider retrospectively. FFS is also typically used to financially incentivize providers to deliver greater volumes of care, since the more they do, the more they are paid. In contrast, capitation, where a provider is paid a lump sum to cover the treatment costs of a particular patient over a period of time, puts more of the financial risk on the provider; there can be important differences in how capitation is applied. If there is a fixed amount paid on behalf of each patient (i.e. ex-post capitation), providers may take on more volumes of patients to earn greater revenues but they may skimp on the volume or quality of care provided because the provider bears financial risk if use and costs are too high. As a result, they may be incentivized to take on low-complexity patients. If providers are paid based on a block (global) budget determined by the expected number of patients (i.e. ex-ante capitation) then providers are incentivized to reduce patient volumes and care use in an effort to be profitable. However, the financial incentive to ration services may be mitigated if the capitated payments are risk adjusted. In some systems, expensive cases (outliers) or certain treatments may be excluded from the capitated budget, and this may lead providers to increase the number of referrals to other providers if referrals are not capped.

What is in the chapters?

The Commissioning and purchasing section of the book includes 10 chapters, a reflection of the complexity of the purchasing function. The first two consider paying for primary care and hospital care, respectively, by purchasers. In the case of primary care, the chapter explores the potential of diverse payment methods in primary care to tackle policy challenges faced by health care systems, specifically addressing the issues of avoidable referrals to secondary care and the misalignment between actual care in primary settings and evidence-based clinical guidelines. The chapter emphasizes how various payment models create incentives and outlines their intermediate and long-term effects on achieving health systems’ objectives. The next chapter on paying for hospital care covers four approaches to payment – line-item budgeting, FFS, block contracts and activity-based funding – and considers practical issues and the reasons for favouring one mechanism over another depending on context. Mixed payments methods which combine different payment approaches with different incentives are often preferable to try and strike a balance between competing incentives. For example, primary care providers may receive a capitation fee that provides adequate upfront resources for patient care without incentivizing overprovision of services. Additionally, they may also receive some FFS to encourage particular services, such as preventive activities, that may not be provided otherwise.

User payments are a fundamental element of provider reimbursement in many health systems. Chapter 2.4 has already given a general treatment of user charges. However, Chapter 3.3 specifically considers informal payments – direct payments by patients to providers, which are not sanctioned officially – and why they are used, particularly in low-resource settings. It explores some potential ways to try to limit their use, noting the complexities and that informal payments often emerge due to low levels of public spending on health care. Chapter 3.4 discusses the financing of medicines, aiming to encourage investment in research and development (R&D) by manufacturers, particularly in areas with high unmet need. It also covers pricing and reimbursement models for medicines already on the market.

The subsequent chapter focuses on the challenges and strategies for paying for care that requires the coordination of different types of providers. Integrated or coordinated care is particularly important for frequent users of the health system, such as those with chronic conditions. Therefore, mechanisms that bundle payment or which pool resources to be shared across providers may help to encourage better care coordination and ultimately, quality. LTC faces similar challenges given the need for a spectrum of providers to work collaboratively to deliver services. To this end, Chapter 3.6 discusses approaches both to resource allocation and payment in LTC. LTC differs from other types or providers in several ways, including the need to integrate social care services that support people with activity limitations and health care services, as well as the typically longer duration of care. LTC therefore poses specific challenges for payment mechanisms. The chapter explores the different factors which may need to be taken into account when implementing risk adjustment to ensure that LTC is adequately resourced based on population needs. Chapter 3.7 discusses the challenges associated with transitioning from vertical priority-setting which focuses on specific conditions or populations to horizontal priority-setting which emphasizes affordable access to care more generally. It also delves into the role of financing arrangements in facilitating this transition.

The final three chapters address areas that often do not receive adequate attention despite their collective and global implications. Chapter 3.8 considers financing of pandemic preparedness, an issue which has become more salient since the COVID-19 pandemic but nevertheless was relevant before. The authors discuss mechanisms at the global, national and regional levels and conclude that effective planning requires more than just attention to resource allocation. Rather, preparedness is dependent on public financial management mechanisms, incentive structures and international collaboration. The next chapter looks at issues related to financing investments in antibiotic R&D and incentives for research to combat antimicrobial resistance. This is an important area because antibiotics are increasingly becoming less effective, in part due to overuse and more drug-resistant infections. The final chapter discusses financing mechanisms aimed at developing medicines to treat neglected diseases. Despite accounting for a large share of disease burden, there is often a perception that these medicines are not profitable, leading to a lack of resources dedicated to R&D. The chapter discusses incentives to address this historic mismatch.

Monitoring health financing globally: National Health Accounts

To monitor and compare health financing across countries, most countries produce National Health Accounts (NHA). These serve as a systematic and comprehensive approach towards capturing all financial transactions related to health care within a country over a specific period. NHA are designed to track and analyse the flow of funds within the health sector, offering insights into how resources are raised, allocated and utilized in health-related activities. They consist of information on financing sources including both public and private sources of funding for health care (both compulsory and voluntary), the distribution of spending among providers and health spending by type of services (or alternatively, function).

By compiling and analysing this information, NHA contribute to a better understanding of a country’s health financing landscape. Policy-makers, researchers and international organizations use NHA data to assess the efficiency, equity and sustainability of health financing systems to the extent possible with aggregated country-level data, enabling evidence-based decision-making and policy development in the health sector. For example, although NHA do not allow for stratification of health spending by socioeconomic class, the mix between OOP, VHI and compulsory health financing sheds some (limited) light on the redistributive nature of the health system.

While it is challenging to draw conclusions on health spending trends globally, we briefly attempt to give a sense of some of the overarching patterns in health financing. Across 186 countries, the average country health expenditure overall as a share of gross domestic product (GDP) increased from 5.5% in 2000 to 6.6% in 2019. This increased further during the COVID-19 pandemic to 7.4% of GDP by 2021, but much of this increase can be attributed to slower growth in GDP as well as one-time additional spending on health in response to the pandemic. Over the same time period, government spending as a share of current health spending remained relatively stable in the average country, increasing slightly from 51.2% in 2000 to 52.9% in 2019. OOP spending as a share of current health spending declined from 36.9% in the average country in 2000 to 30.9% in 2019, falling further to 28.2% in 2021. VHI remained fairly stable at just under 5.0% of current health expenditure. The role of external sources of financing showed the most variability, increasing from 6.2% of health spending in 2000, to around 11% between 2006 to 2015, and then falling to 9.4% in the average country by 2019. In the case of external sources of funding, just over one third of countries had more than 5% of their health spending coming from external sources in 2019. Likewise, government spending as a share of current expenditure varied in 2019 from under 10% in Afghanistan and Guinea-Bissau to over 90% in Kiribati, Cook Islands and Brunei.

The mix of funding sources varies substantially across countries as well as across-country income groups (Fig. 0.2.2). For example, government and compulsory insurance schemes comprised nearly 80% of health spending in 2021 in the average high-income country, whereas in the average low- or middle-income country these sources accounted for just over half of health spending. This speaks to the fact that it is difficult to raise such sources of financing in countries with large informal sectors. Moreover, the reliance on OOP spending on average is highest in LMICs (35%) which is approximately half the level observed in HICs. Importantly, VHI schemes are among the least utilized sources of financing globally, although on average they pay for a slightly greater share of health care in upper-middle-income countries (UMICs) than they do in HICs. Of course, these averages mask significant heterogeneity, which is beyond the scope of this introductory chapter.

Future challenges

As detailed extensively throughout this volume, the methods used to collect and distribute funds directly influence the overall shape and performance of the health system. Aiming to capture the changes in the global landscape of health financing since the 2002 book, this updated text brings in real-world and recent evidence from countries of varying income levels and regions to discuss the policy areas relevant to health financing in the pursuit of UHC. Not only does the wide geographical coverage in this book provide contemporary insights into topics ranging from developmental assistance to integrated care to pandemic preparedness, but it also gives readers the opportunity to understand what has been achieved in recent years and what still needs to be done. It is in that context that we wrap up this introduction by briefly touching on the major challenges for each of the financing functions (revenue raising, pooling resources and defining benefits, purchasing) that demarcate the sections of this book.

Revenue raising

To secure necessary financing for the health system, countries have to ensure that they are drawing on the appropriate sources of funds given their own national contexts. For example, revenues generated via taxation or compulsory SHI contributions are the dominant public funding mechanisms used in HICs to promote equity and efficiency. In lower-income contexts, however, although countries do make some use of taxation or SHI systems, their use tends to be more limited in scope. Their systems therefore also feature a larger role for other financing sources, especially OOP payments, but also VHI (including CBHI in some countries), or external sources of financing (such as charitable donations or developmental assistance for health). The differences in how the revenue raising function is organized reflect historical factors and path dependencies, as well as constraints on the use of some sources of finance, and are not necessarily an indication of policy failure, though it should be noted that a high reliance on voluntary funding sources can inhibit affordable access. Indeed, across all country income settings, securing reliable and sustainable revenue sources of adequate size to fund the desired health system is a major challenge, especially given the increasing prevalence of informal economy work, population ageing, conflict and migration. Furthermore, the inexorable rise of new technologies and changes in the epidemiology of disease can have a profound impact on the demand for finances. The continued use of user charges to pay for services is a challenge with often inequitable impacts – the most disadvantaged (lower-income, the least healthy, the most geographically remote) are often subject to the most catastrophic expenditure risks. Countries of all types therefore have a major challenge to ensure that sufficient and stable revenues are raised equitably, with the largest financial burden borne by those who can most afford it.

Pooling

Risk pooling entails bringing together different sources of revenue and transferring them to the organizations that commission and pay for health services for defined populations. This tool spreads financial risk across a population so that individuals’ abilities to pay for health care is not linked to their medical need, and can be seen around the world at different levels and in different formats. A future focus area for policy-makers pursuing UHC is to ensure that all population groups are included in risk pools that require equitable financial contributions (either by them themselves or paid on their behalf by governments) and offer similar HBPs. This challenge becomes more acute in countries with more fragmented pooling (single versus multiple pools, pools overlapping geographies, pools competing against one another), especially where there are entrenched interests and limited resources. It will often be necessary to implement financial transfers from better endowed, healthier risk pools to poorer, less healthy risk pools in order to promote the chosen concepts of equity. Setting a realistic benefits package to maximize health benefits is another challenge for countries, and requires stakeholders to work together on an ongoing basis to decide what to define explicitly and what to leave adaptable to local circumstances.

Purchasing health care

As the final of the three functions, purchasing from the raised and pooled resources is typically based on a contract between the purchaser and the provider. The first requirement related to this function is therefore to establish or strengthen the institutions that make such strategic purchasing decisions, i.e. the conscious, evidence-based approach of deciding which services to buy from which providers, at what cost and how to pay for them. Payment mechanisms should be designed to offer providers incentives that align with the purchaser’s objectives, which often focus on maintaining and/or improving access to health services that provide value for money, especially for disadvantaged groups. To ensure that the care is high-quality, performance monitoring is necessary for benchmarking and informing contracting choices in the future. In situations where an individual’s care takes place across multiple providers (especially common in cases of those with long-term and chronic care needs), contracts and care collaborations between providers need to be designed to promote continuity and coordination of care. Finally, the COVID-19 pandemic and other global crises, like growing antibiotic resistance, have demonstrated the need to secure global cooperation in financing global public goods.

How to read this book?

Despite the aforementioned challenges, there has been immense progress in health financing in recent decades. We believe the policy lessons and insights set out in this volume can help researchers and policy-makers to continue to make further progress towards UHC in the years to come. Each chapter of this book has been written as a standalone piece allowing the book to reflect the diverse voices and expertise of its contributors. However, efforts have been made to highlight and cross-reference areas where readers would benefit from broader understanding of topics covered in other chapters. As such, the arrangement of the chapters in this volume allows readers to read the text sequentially from front-to-back, or to navigate freely between chapters based on their specific interests. Each chapter contains (i) a set of key messages at the start of each chapter, and (ii) a list of key resources (such as other books, journal articles, websites) where the reader can go to examine the topic area in further depth (in addition to the full list of references) at the end of the chapter. These are intended to serve as easily digestible resources to aid the reader in understanding the most important points of each chapter.

It must be emphasized that the book does not provide specific how-to guides or endorse particular models. Instead, it conducts a thorough examination of the expanding body of evidence related to these various health financing elements to highlight ongoing debates and stimulate further discussion. Each chapter presents both theoretical frameworks as well as empirical findings from around the world. Unless noted otherwise in the chapter text, the book covers developments up until the end of 2023.

Open access

Open access