On May 27, 2010, Malaysia’s sovereign wealth fund (SWF) Khazanah initiated a hostile takeover of Asia’s largest healthcare chain, Singapore-based Parkway.Footnote 1 The surprise move was implemented through Khazanah’s newly established healthcare firm, Integrated Healthcare Holdings (IHH). Such an aggressive move by a SWF was nearly unheard of, and it was the first time that a SWF attempted a hostile takeover of a foreign firm.Footnote 2

The acquisition was provoked by the actions of two billionaire brothers, Malvinder and Shivinder Singh, who controlled the largest private hospital chain in India through their firm, Fortis.Footnote 3 Two months earlier, Fortis bought just enough shares in Parkway to overtake Khazanah’s dominant ownership position.Footnote 4 On hearing that the Singh brothers were sending out feelers to other stakeholders about selling their shares, Khazanah initiated its hostile takeover.Footnote 5 But before Khazanah’s offer could be finalized, it would require approval by the shareholders, creating the potential for a bidding war.Footnote 6

At stake was a big and rapidly growing medical tourism market.Footnote 7 In the eyes of Fortis and Khazanah, Parkway was worth fighting for as the only Pan-Asian medical care provider, making it an ideal foundation for a regional healthcare platform.Footnote 8

After a series of offers and counteroffers, Khazanah finally prevailed.Footnote 9 The deal was the fifth-biggest acquisition of a Singaporean company in history.Footnote 10 Parkway would now be owned by Khazanah via IHH. About a month later, a new chairman and two non-executive directors were appointed to Parkway, leading to the departure of numerous top managers in subsequent months.Footnote 11

This episode illustrates an important new trend in the global economy – state-owned entities that engage in increasingly aggressive foreign investment behavior. The government entity that has attracted the greatest attention is the SWF. SWFs are state-owned investment vehicles that invest globally in various types of assets ranging from financial to real to alternative assets. Notable examples include Singapore’s Temasek, the China Investment Corporation, and Norway’s Pension Fund Global.Footnote 12

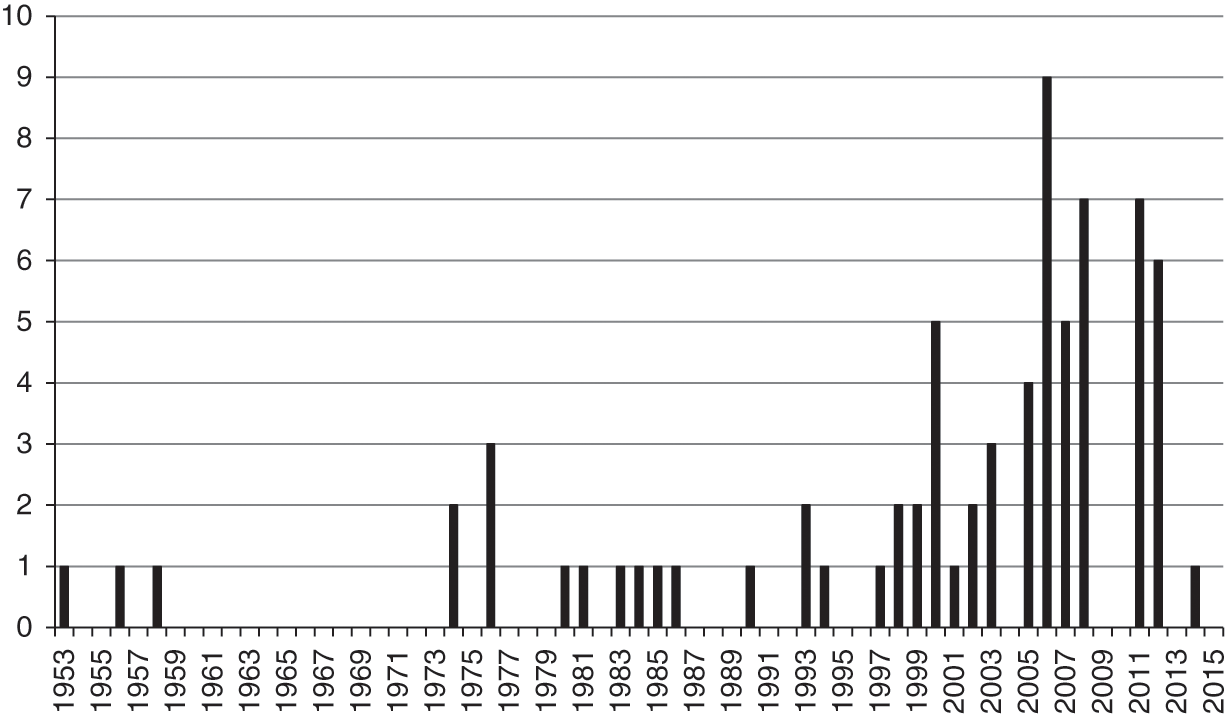

In 2000, SWF assets amounted to approximately US$1 trillion. By 2007, they had increased to over US$3.3 trillion, with shares held in one of every five listed firms worldwide.Footnote 13 By 2015, SWF assets had risen to US$7.2 trillion. Moreover, seventeen of the twenty largest SWFs, accounting for approximately 75 percent of total SWF assets, are currently located in authoritarian regimes.Footnote 14 By comparison, private equity firms managed assets of around US$2.4 trillion, while hedge funds managed about US$3.2 trillion in assets in 2015, and they are primarily located in the United States and the United Kingdom.Footnote 15 Figure 1.1 shows the surge in the number of SWFs initiated since the late 1990s.

Number of SWFs established over time, 1953–2015.

SWFs becoming more, rather than less, prominent in the global economy is both surprising and puzzling because such growth contradicts theories about the global diffusion of liberalizing reforms, as manifested by several waves of privatization since the 1980s.Footnote 16 According to this line of argument, regimes of all stripes should be reducing the state’s role in the economy, including in the corporate sector, as liberalizing reforms spread across the world. However, many states have used the diffusion of liberalizing reforms to expand state investment. For example, from 2001 to 2012, governments acquired more assets through stock purchases ($1.52 trillion) than they sold through share issue privatizations and direct sales ($1.48 trillion),Footnote 17 with much of this state investment channeled through SWFs.Footnote 18

The rise of SWFs and other state-owned entities poses serious risks because of the tremendous scale of the assets they control, the risk that political objectives might influence their management, and their potential to influence or even control the most economically important corporations of foreign countries. Among advanced and most emerging economies, the firms of greatest importance to the national economy are usually publicly listed. Large-scale capital requirements lead these firms to sell shares to raise financing, in addition to other benefits associated with listing on a stock market (e.g., adopting market-oriented reforms to improve corporate governance and performance). However, this situation can also create the opportunity for investors with sufficient capital to buy a large enough stake in the firm to alter how it is governed. Because of their vast resources, SWFs are uniquely positioned to engage in these types of activities with regard to the world’s largest firms. Understanding what drives this type of state investment behavior is this book’s core research question: why do some states engage in more aggressive corporate intervention in foreign listed firms than others?

The hostile takeover initiated by Khazanah, Malaysia’s SWF, is a prime example of aggressive state intervention. This type of investment behavior is indicative of the strategies employed by private equity firms.Footnote 19 Such firms purchase large stakes in target companies in order to implement value-enhancing strategies over the course of several years, often through management changes, streamlining operations, or expansion. Immediately following its takeover of Parkway, Khazanah appointed a new chairman and directors and integrated Parkway into its regional healthcare network. However, most SWFs act in a passive manner that involves exiting the investment when the SWF disagrees with management decisions. For example, the Brunei Investment Agency, which is headquartered next door to Malaysia, rarely takes large ownership positions and consistently adheres to a passive investment strategy.Footnote 20

To explain the investment behavior of state entities such as SWFs, we must consider both the capacity of the state that owns them to engage in aggressive corporate interventions and whether the state possesses the motivation to do so. The capacity of a state to intervene aggressively in a foreign company depends on three attributes. First, the state must have a vehicle capable of initiating large ownership stakes that are held over an extended period of time, thereby enabling the implementation of major changes to target firms. This normally occurs either via SWFs or state-owned enterprises (SOEs; often owned by a SWF), but SWFs can facilitate this process by centralizing control over the activities of sprawling corporate assets, pooling resources and information, and identifying and assisting with investment opportunities on behalf of SOEs. But as I will discuss below, not all SWFs are equally suited to engaging in large, long-term holdings of foreign corporations. Second, the state must provide adequate transparency about the vehicle initiating the investment so that private investors can properly value the risk associated with co-investing with it and so that host country officials can decide whether to permit the investment. Third, the state investment vehicle must be capable of and willing to manage its ownership stake alongside other private investors (in a public-private co-ownership arrangement). This setup can be challenging for some states and private investors when the state entity seeks to intervene in firm governance.

State capacity is a necessary, but insufficient, condition. For example, some SWFs may take a large position in a listed firm but are unwilling to put pressure on managers to alter firm strategy. States must also be motivated to intervene aggressively. The most fundamental motivation driving state investment behavior regards leaders’ desire to remain in power. For democratic leaders, institutional constraints normally restrict the duration of their position, granting an opportunity for members either of the same party or an opposing party to hold the position. For authoritarian rulers, institutional constraints are normally weaker, thereby granting political incumbents the opportunity to hold on to power for a longer, potentially indefinite, duration. Thus the strongest motivation to intervene arises from threats to authoritarian rulers’ hold on power.Footnote 21 To the extent that such authoritarian leaders rely on state ownership of large corporations to maintain their rule, two threats are of particular salience – the crowding-out effects that accompany economic development and economic liberalization. Both of these threats enhance the ability of private capital to challenge incumbent rulers and the SOEs they rely on to preserve their rule. To account for the varying capacity and motivation of states to intervene aggressively in foreign listed firms, I offer a novel political explanation.

A New Political Explanation

I argue that the propensity for a state to engage in aggressive foreign corporate interventions depends on the structure of its political regime. My argument differs from the existing literature on SWFs and SOEs in two important ways. First, I focus on common underlying political determinants of SWFs and SOEs. Because both of these entities are controlled by the government, with SOEs often owned by a SWF, similar political pressures influence their behavior. Yet the literature on the political determinants of SWFs examines them separately from SOEs.Footnote 22 Moreover, the literature on SOEs largely developed before the rise of SWFs.Footnote 23 A common political explanation is therefore lacking.

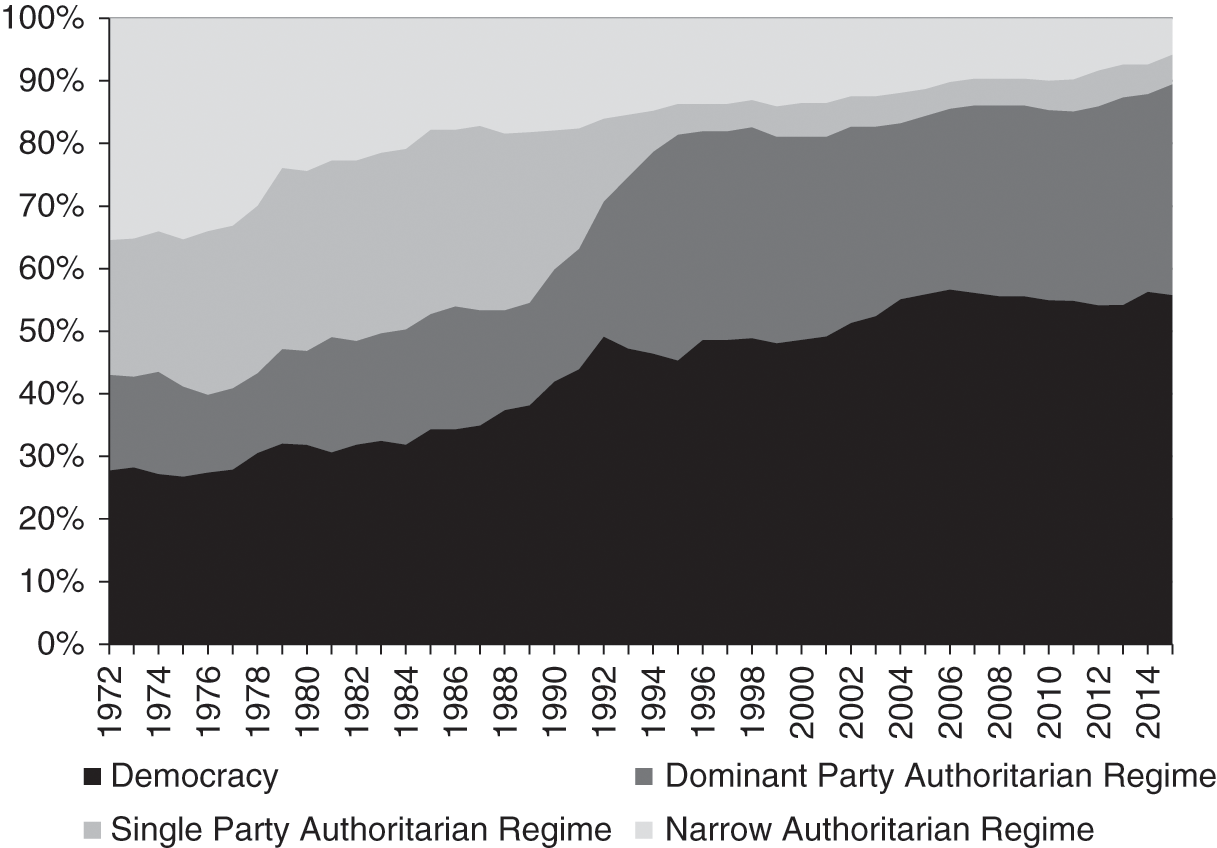

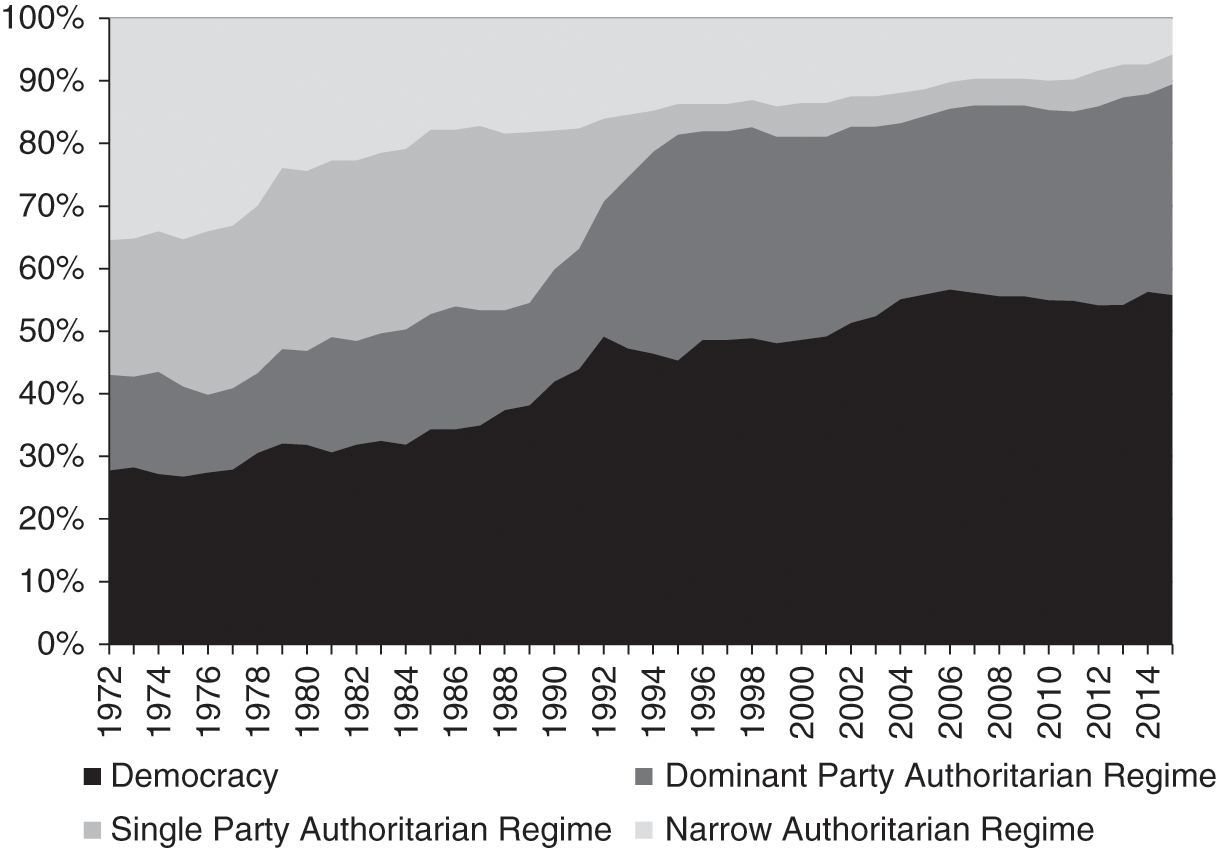

The second difference concerns the political determinants themselves. The literature on both SWFs and SOEs has overlooked an important political development since the end of the Cold War – the rise of dominant-party authoritarian regimes (DPARs). Few would have predicted that the “third wave” of democratization, which came to a halt in the mid-1990s, would be eclipsed by the diffusion of DPARs into the first decade of the twenty-first century.Footnote 24 However, DPARs are now the most common type of authoritarian rule, constituting one-third of the total number of regimes in the world, as illustrated in Figure 1.2. Given the contemporary importance of DPARs, it is critical to understand the relationship of these regimes to the corporate sector and to SWFs and SOEs more specifically.

The prevalence of political regimes, 1972–2015.

Note: Narrow authoritarian regimes have an ifhpol score lower than 7 out of 10 without the representation of multiple parties in a legislature; single-party authoritarian regimes have an ifhpol score lower than 7 and a legislature with a single party; dominant-party authoritarian regimes have an ifhpol score lower than 7 and a legislature with multiple parties; democracies have an ifhpol score of 7 or above. The ifhpol score combines the Freedom House and Polity IV scores to generate a democracy index that encompasses more countries than either index alone. It comes from Hadenius et al. (2007), Authoritarian Regimes Data Set, version 5.0. Whether countries have a legislature with multiple parties is based on the lparty variable from Cheibub, Gandhi, and Vreeland’s (Reference Cheibub, Gandhi and Vreeland2010) Democracy and Dictatorship Revisited data set for data from 1972 to 2008. Both variables have been updated to 2015. For additional details, see Chapter 3.

I argue that characteristics specific to each political regime affect the capacity and motivation of a state to intervene in the corporate sector. I place political regimes into one of four categories: (1) narrow authoritarian regimes (NARs), (2) single-party authoritarian regimes (SPARs), (3) dominant-party authoritarian regimes (DPARs), and (4) democracies.Footnote 25 NARs are those in which no meaningful competition for political office occurs, such as a monarchy or those ruled by the military (e.g., Brunei and Myanmar until 2012). To secure their rule, political elites in these regimes monopolize the control of information and resources – unlisted SOEs are one manifestation of this. SPARs are those in which a ruling party monopolizes the political arena by occupying all the seats in the national legislature and proscribing political opposition (e.g., China, Vietnam, and Laos). Competition for political office occurs within the party but not between parties, yielding a modest loosening of the control over information and resources. Consequently, partially state-owned enterprises are more likely to arise. DPARs hold elections in which competing political parties vie for public office, but rarely do these elections result in the handover of power. The usual result is a dominant ruling party with opposition parties holding a small minority of legislative seats (e.g., Malaysia and Singapore). The ruling party dominates the control of politically sensitive information and resources, though opposition parties also gain limited access, which corresponds to an increased reliance on partially state-owned enterprises. Finally, democracies are those in which competitive elections occur between candidates from multiple parties. Access to politically sensitive information and resources is not restricted to members of any single group or political party, and this corresponds to relatively few corporations with state ownership (e.g., Japan, South Korea, and the Philippines).

I argue that among the four political regimes, DPARs have the greatest capacity and motivation to intervene aggressively in foreign listed firms. With regard to capacity, DPARs are relatively more likely to host mixed public-private corporations, corresponding to their semirestricted control of information and resources. Because of their capacity to host hybrid SOEs in the home market, DPARs can more easily engage in public-private ownership in foreign markets. Compared with other authoritarian regimes (i.e., SPARs and NARs), DPARs can also meet the transparency requirements of a larger set of foreign countries in order to acquire a large position in a target firm. Additionally, DPARs are more likely to have a strong motivation to intervene in the corporate sector compared with other regimes because they permit opposition parties to compete in elections but are unwilling to hand over power. As the threat of political opposition rises, DPAR leaders will engage in more aggressive tactics to protect their rule. An implication of this argument is that China’s SOEs and SWFs are not as aggressive with their foreign investments as they can be; instead, Malaysia’s SOEs and SWFs display more aggressive behavior compared with any other state entities in East Asia. This behavior is attributable not only to their regime differences but also to China’s lack of a fully functional savings SWF. To appreciate why this matters, we must consider the varying types of SWFs and their role in mediating government involvement in the corporate sector.

The Importance of Savings SWFs to State Intervention

SWFs are conventionally categorized as foreign exchange reserve funds, stabilization funds, pension reserve funds, or savings funds.Footnote 26 As the name suggests, foreign exchange reserve funds are funded by foreign exchange reserves. Their purpose is to invest these funds overseas to reduce the negative carry costs of holding reserves or to earn higher returns on ample reserves through sizable allocations to equities and alternative investments.Footnote 27 However, a stockpile of reserves must be available at short notice to defend the value of the currency; thus these funds generally do not take large positions to be held for a long period. Therefore, reserve funds are invested in a relatively passive, diversified manner that generally maintains a small ownership stake in any one company.Footnote 28

The purpose of stabilization funds is to buffer the economy – usually the financial markets – from external shocks. To this end, stabilization funds will invest in equities to buffer stock market volatility (e.g., Taiwan’s Stabilization Fund), but this is normally short-lived because it is simply intended to stabilize the market. When they are not invested in domestic equities, stabilization funds invest primarily in a highly liquid portfolio of assets, such as fixed-income and government securities, that are not strongly correlated with boom/bust cycles.Footnote 29

By comparison, the purpose of pension reserve funds is to invest so as to meet future expenditures associated with an aging population. In essence, pension reserve SWFs act as a commitment mechanism for politicians who might prefer to spend their countries’ wealth today instead of saving it for future generations (e.g., Australia, Ireland, and New Zealand). These funds are more likely to initiate long-term ownership positions through equities purchases, but they are unlikely to pursue political objectives at the expense of prudent portfolio allocation. They differ from traditional pension funds in that they have no designated claimants on the available assets; rather, the legal or beneficial owner is the institution that administers the public pension system (social security reserve funds) or the government (sovereign pension reserve funds). This feature exposes them to potentially greater state influence than pension funds,Footnote 30 but because the purpose of these funds is specifically intended for the aging population and they are located primarily in Organisation for Economic Co-operation and Development (OECD) countries, pension reserve funds exhibit the highest levels of transparency and compliance with the Santiago Principles concerning SWF best practices compared with other types of SWFs.Footnote 31 Hence discretionary investment strategies are significantly curtailed.

The aim of savings funds is to share wealth across generations. This objective leads to investments via a high risk-return profile, including a high proportion of equities and other investments.Footnote 32 But because these funds are not specifically targeted for pension payments or other funding obligations, officials have more freedom to choose how they invest. Although many seek to transform commodities assets into diversified financial assets, this condition is a relatively minor restriction that grants significant freedom to decide how investment allocations are made. Consequently, savings funds are the most capable of taking large, long-term corporate ownership positions.

As shown in Figure 1.1, the number of SWFs has increased since 1997, suggesting that the Asian financial crisis may have spurred their creation. Although the crisis led to “profound changes in the demand for international reserves, increasing over time the hoarding by affected countries,” more reserves did not necessarily equate to more SWFs.Footnote 33 The new reserve SWFs that have been created in Asia since 1997 (e.g., Korea Investment Corporation and China Investment Corporation) are relatively few in comparison with the number of countries that have accumulated them without also creating a reserve SWF (e.g., Malaysia, Indonesia, Thailand, and the Philippines). Indeed, most of the SWFs created since 1997 are savings funds rather than reserve funds.Footnote 34 Worldwide, more than half of all SWFs are savings funds, followed by stabilization funds at approximately 30 percent, with pension (9 percent) and reserve funds (7 percent) being relatively few in number. Savings funds therefore deserve close scrutiny both because they are the most capable of taking large, long-term corporate ownership positions and because they are the most prevalent type of SWF.

The Existing Literature with Regard to SOEs and SWFs

Because SWFs are a relatively recent phenomenon, the existing literature has mainly focused on SOEs to explain the varied nature of state intervention in the corporate sector. I therefore begin by discussing the literature on SOEs.

State-Owned Enterprises

There are two dominant views regarding the state’s role with regard to SOEs. The first perspective emphasizes the public benefits that SOEs can generate, including a welfare role and their capacity to compensate for institutional voids. The second perspective considers the political benefits to business owners or politicians from state participation. The first public benefit that SOEs can serve occurs via a welfare role. For example, governments may force SOEs to reduce unemployment, invest in geographically remote areas, cater to less-profitable customer segments, or keep prices low.Footnote 35 State ownership may also be desirable when some quality-based dimensions are difficult to measure and enforce, as with pay-for-performance contracts to promote effective student learning in schools.Footnote 36 Finally, state ownership may be necessary for the successful financing and completion of long-term projects that private investors are unwilling or unable to fund.Footnote 37

State ownership can also help to overcome institutional “voids” in product, labor, and financial markets that reduce the potential productive efficiency of a country.Footnote 38 Such voids are likely to occur among countries in the early stages of development. The state can step in to compensate for these voids by providing capital in cases where financial markets are underdeveloped or by coordinating the local deployment of complementary resources where product markets are underdeveloped.Footnote 39 The early industrial development of many countries was often associated with massive state involvement through SOEs or state-owned development agencies.Footnote 40

However, the public benefits view of SOEs fails to explain a wide range of state interventions. On the one hand, this gap arises from questions about how the state reconciles competing welfare demands or how it chooses which institutional voids to fill. With limited resources, the state must make political decisions about how to allocate them. On the other hand, empirical questions arise as to why some countries with few institutional voids maintain high levels of state ownership, such as Singapore, or why countries with low development have so few SOEs compared with countries at comparable or higher levels of development, such as the Philippines in comparison with Malaysia.

The political view posits that politically connected firms can benefit from state intervention in the corporate sector. By acting as intermediaries for the distribution of state resources, SOEs may grant politically connected firms preferential access to government contracts or financing. For example, in a study of emerging markets, state-owned banks were found to lend more than private banks during election years.Footnote 41 The moral hazard accompanying this practice magnifies the problem, also known as the soft budget constraint.Footnote 42 The provision of abundant capital by the state will increase the likelihood of misallocation and inefficient bailouts. This is likely to result in bad investments and the use of public funds to rescue failed projects. Additionally, politically connected firms may successfully lobby government officials for the selective enforcement of costly regulations, giving them a competitive advantage over their rivals. Thus the political view predicts that state ownership and state strategic support for private firms will be more common in countries with weak institutions where corruption and cronyism can flourish.Footnote 43

Politicians with authority over SOEs can likewise use these firms for direct political gain.Footnote 44 As a result, SOE managers are often poorly selected and lack the necessary incentives to pursue efficiency and profitability relative to private firms.Footnote 45 In some cases, direct conflicts of interest arise when SOE managers may themselves be appointed politicians or political allies. Consequently, compensation schemes are often not linked to economic performance but instead follow bureaucratic criteria such as hierarchy and seniority.Footnote 46

However, focusing only on political benefits to political leaders and their cronies fails to explain a wide variety of state interventions. Specifically, this view disregards the capacity for political institutions to reduce investment risks such as expropriation risk and contracting risk, thereby decreasing the inefficient allocation of state resources or selective regulatory enforcement. For example, political institutions can be designed to constrain the self-serving behavior of politicians. If threats to the survival of the regime are severe enough, then political leaders may implement new political arrangements that limit their rent-seeking capacity and thereby reduce expropriation risk. North and Weingast illustrate how the English parliament, under severe pressure to deal with crushing sovereign debt, successfully curtailed the expropriation powers of the king, yielding declines to the cost of capital and the subsequent development of stock and bond markets.Footnote 47 Stasavage further demonstrated that the benefits associated with the addition of parliamentary veto power over the executive were contingent on the heterogeneity of policy preferences among members of parliament.Footnote 48

In addition to successfully reducing expropriation risk, political institutions can also help reduce a second type of investment risk – contracting risk.Footnote 49 Jensen et al. find that authoritarian regimes with legislatures and multiple parties yield improvements to investor protections by creating a forum for agreements that can reduce contracting risk.Footnote 50 Even though the executive retains confiscatory powers (i.e., expropriation risk), legislatures still serve a useful function by permitting nonstate/private actors to negotiate, monitor, and enforce agreements among themselves, thereby reducing the potential for selective or discriminatory regulatory enforcement.Footnote 51 Although Jensen et al. explicitly say that their argument does not apply to SOEs, there are good reasons to think that it might have traction with respect to partially state-owned enterprises whose performance depends on a properly functioning marketplace. By extension, SWFs with equity stakes in publicly listed firms will also value the reduction of contracting risk.

Sovereign Wealth Funds

A surge of recent research seeks to explain SWF investment behavior from different disciplinary perspectives, including finance,Footnote 52 strategy,Footnote 53 political economy,Footnote 54 economics,Footnote 55 international law,Footnote 56 and organizational theory.Footnote 57 These studies recognize that SWFs can potentially have a tremendous impact on the firms in which they invest. SWFs’ control of vast resources allows them to take sizable ownership positions in listed companies, thus allowing the SWF to intervene in the management of the firm and force changes such as initiating mergers and acquisitions or divestitures, expanding the firm’s business prospects by partnering with other firms also owned by the SWF, or even changing the CEO and top management team.Footnote 58 As mentioned earlier, Malaysia’s SWF, Khazanah, initiated a hostile takeover of Parkway Health in 2010. It subsequently replaced the top executives and integrated the firm into Khazanah’s regional healthcare network (i.e., IHH).

Despite the propensity toward activism by some SWFs, most SWFs follow more passively oriented investment strategies.Footnote 59 SWFs employing a passive strategy usually acquire a relatively small ownership stake in a target firm and then sell the stake if they disagree with the strategic decisions of the firm. Brunei’s SWF, the Brunei Investment Authority, is typical of SWFs with a passive strategy – it rarely takes large ownership positions in listed firms. Passive SWFs may sometimes take a large stake (>5 percent) simply because the target firm is perceived to be a good investment, illustrating that the size of the SWF’s position is a necessary, but insufficient, condition for governance activism. For example, the China Investment Corporation occasionally takes ownership stakes greater than 5 percent but refrains from intervening in the invested firm.Footnote 60 However, some SWFs engage in limited forms of governance activism despite owning a small stake (<5 percent), such as engaging in informal discussions with management or submitting shareholder proposals for the proxy statement. Such proposals can include a range of corporate governance requests such as separating the chairman and CEO, placing alternative board candidates on the company’s proxy card for the company’s annual shareholder meeting, or requesting the firm to address social/environmental issues. Norway’s Government Pension Fund Global has recently engaged in these kinds of tactics.

The prevailing view is that domestic political arrangements have the greatest influence on SWF activities.Footnote 61 For example, in a special issue about SWFs in China, Singapore, Saudi Arabia, and Norway, Helleiner concludes that “the political logic that drives [SWFs’] behavior is much more often domestically than internationally focused.”Footnote 62 While Clark, Dixon, and Monk point to the importance of both domestic and international legitimacy as influencing the governance of SWFs, a critical dimension of this governance – transparency – seems to be determined primarily by domestic factors.Footnote 63 If foreign regulations were the primary determinant of SWF transparency, then such high variance would not exist; we would instead observe uniformly high levels of transparency as SWFs cater to foreign regulators. Aizenman and Glick, for example, identify a strong correlation between the domestic governance indicator “voice and accountability” and SWF transparency.Footnote 64 Other studies corroborate this view. For example, Bernstein, Lerner, and Schoar find that SWFs invest more in firms headquartered in the home country (45 percent) versus firms headquartered in foreign countries (31 percent).Footnote 65 In another study, Bortolotti, Fotak, and Megginson find that SWFs take director board seats in only 6.74 percent of foreign investments compared with 30.3 percent of domestic investments.Footnote 66 Finally, Dewenter, Han, and Malatesta report that SWF activist tactics are twice as common for board representation, senior management turnover, and government influence when the target is a home-country firm.Footnote 67 Thus there is a growing body of work suggesting that the home country is of primary importance to SWF investment behavior.

However, this emergent literature has four limitations. First, it often treats SWFs as a homogeneous group. Without considering the limitations imposed on SWF activities due to their investment objectives (as with savings, stability, reserve, and pension SWFs), making comparisons among them can be problematic. Second, the literature either identifies broad correlations between SWF characteristics and political regimes (e.g., transparency and the level of democracy), or it focuses on individual country cases. Consequently, important patterns regarding SWF activities specific to certain political regimes have been overlooked. Third, as mentioned earlier, much of the SWF literature is divorced from the SOE literature. But because SOEs increasingly mix public and private ownership, with the public component frequently administered by a SWF, considering them together is necessary. Fourth, neither the SOE nor the SWF literature considers the rise of DPARs since the mid-1990s and how the impact of this type of regime differs from that of other regimes. To explain the varied nature of state involvement in the corporate sector while addressing these shortcomings in the existing literature, I now turn to my argument.

Summary of the Argument

I argue that the aggressiveness of state intervention in foreign listed firms is determined by the capacity and motivation of the home state to intervene. State capacity to intervene is determined by the type of political regime and the extent of control over information and resources that rulers depend on for regime survival. The motivation to intervene arises from efforts of rulers to reduce risks to regime survival, which is also determined by the structure of the political regime.

State Capacity to Intervene

As mentioned earlier, I place political regimes into one of four categories. Political leaders in these regimes engage in varying degrees of control over information and resources to uphold their rule. Such controls are tightest in NARs and loosen as one proceeds toward democracy. SOEs manifest these varying degrees of control with regard to their level of transparency and the nature of state ownership (i.e., wholly state owned, partially state owned, or no state ownership). Regimes with a predominance of state ownership – authoritarian regimes – are more likely to host a savings SWF because these have the greatest capacity for large, long-term ownership stakes, and they facilitate the centralized administration of the state’s sprawling corporate assets. Democracies will be more likely to have foreign exchange reserve, macro-stability, or pension SWFs.

With regard to the implications for state capacity to intervene in foreign corporations, NARs will have a relatively low capacity because of their preference for wholly state-owned enterprises coupled with low transparency. Private investors will be reluctant to co-invest with a state entity that discloses little information. Host governments will also be reluctant to permit investments in local firms without a sufficient level of transparency about the investing entity. Democratic states will also have a reduced capacity to intervene in foreign corporations because state ownership will be relatively low (many types of activist shareholder tactics require a large ownership stake). SPARs and DPARs will have the greatest capacity to intervene in foreign firms because they will be the most likely to host partially state-owned enterprises, and they will be more inclined than NARs to meet the disclosure requirements of host governments. However, DPARs possess a greater capacity than SPARs because their SOEs have more balanced public-private ownership, which is favorable to private investors, and because DPARs can meet a higher transparency threshold, which allows them to access more foreign markets.

State Motivation to Intervene

Among the three types of authoritarian regimes, incumbent leaders of DPARs face the most persistent threats to regime stability.Footnote 68 These regimes permit multiparty elections that commonly yield legislative representation for opposition parties even though competition is restricted. From this toehold, opposition parties can pose an increasing threat to the ruling party. One source of threat emerges from the institutional capacity of DPARs to reduce investment risk, which yields a larger presence for private capital. As the economy develops, tensions will increase with regard to the state’s presence in the corporate sector – the ruling party must balance the need for political control via SOEs with the need to maintain popular support by reducing SOEs’ crowding-out effects. Opposition parties can tap into private capital’s desire for a reduced state-sector presence in the economy.

Economic liberalization magnifies the opportunities for private capital, thereby producing more powerful business owners who will seek more political representation to voice their preference for a reduced role for the state. But when political opponents threaten to depose the ruling party, I expect incumbent leaders of DPARs to react in two ways: (1) they will aggressively intervene in the domestic corporate sector to strengthen the state’s control of vital resources and information, and (2) they will aggressively pursue higher investment returns in foreign markets to maintain the support of voter-investors and attempt to alleviate crowding-out effects to placate domestic business.

The story about Khazanah and Parkway matches this prediction. In 2008, Malaysia’s ruling party coalition, Barisan Nasional (BN), suffered its worst electoral outcome since the country’s independence in 1957. Following this election, the government engaged in a range of aggressive tactics via state-owned entities (SWFs and SOEs) to bolster the BN’s support from strategically important groups and to aggressively improve investment returns. Khazanah’s hostile takeover of Parkway is one manifestation of this.

Organization of This Book

Chapter 2 elaborates the argument more fully and systematically. It develops the theoretical model to be tested in subsequent chapters with global, regional, and individual country evidence. Chapters 3 and 4 focus on measures for the capacity of different regimes to engage in aggressive interventions in foreign listed firms, including the scope of public-private ownership, state- and corporate-sector transparency, and SWF indicators. Chapter 3 engages in quantitative tests of the predicted relationships with global data. In this chapter, I use a measure for state ownership of corporations that captures the extent of government intervention in the economy through both listed and unlisted firms. Although this general measure fails to identify specific ownership positions for the state in relation to families and other shareholders, it is useful for gauging the overall importance of SOEs to all types of regimes (i.e., including those that do not have a stock market and therefore lack SOEs with public-private ownership). I also examine various measures of political, corporate, and SWF transparency in addition to the prevalence of different SWF types across political regimes.

Chapter 4 narrows the focus to East Asia. This region is of intrinsic interest because it is the fastest growing in the world with the largest contribution to global gross domestic product (GDP). Methodologically, this region is well suited for this research topic because East Asian countries offer sufficient heterogeneity to examine regimes from each of the four categories. The chapter presents a descriptive overview of states’ “capacity” characteristics from before to after the Asian financial crisis. This includes detailed assessments regarding the prevalence of state ownership of large firms in each country in relation to private ownership and how this public-private ownership balance changed over time. I also examine various cross-national state- and corporate-sector transparency measures over time. Finally, I survey the types of SWFs that states have established, their transparency, and their propensity for large corporate holdings both domestically and in foreign markets.

Chapters 5 through 7 present analytic narratives of countries that typify each regime type. The aim is to establish whether the necessary capacity conditions are met and then examine whether states have sufficient motivation to aggressively intervene in foreign listed firms. Chapter 5 studies a NAR, a SPAR, and a regime that transitioned from a SPAR to a democracy. For the case of a NAR, I examine Brunei, which has a savings SWF – the Brunei Investment Agency. Brunei is a useful NAR to study because it experienced an economic crisis in 1998 that illustrates how this type of regime responds to the risks associated with economic liberalization. Neither North Korea nor Myanmar experienced a comparable shock. Brunei is also an interesting case because its political regime resembles many of those located in the Middle East, a region that hosts many large SWFs. Through the investigation of Brunei, we can draw useful insights for these other oil-rich monarchies.

For a SPAR, I examine China, which has several SWFs, including the China Investment Corporation, the State Administration of Foreign Exchange, and the National Social Security Fund. Focusing on China is also beneficial because it has liberalized its economy far more extensively than the other two SPAR candidates – Vietnam and Laos – enabling comparisons to be drawn for other authoritarian regimes in the region that have also liberalized their economies, such as Singapore and Malaysia. I also choose to focus on China because of its intrinsic importance both globally and regionally.

Finally, I study a country that transitioned from a SPAR to democracy – Taiwan. Taiwan underwent regime change over the last several decades while retaining a commitment to openness, especially with the United States. Thus we can assess whether regime change exhibited corresponding changes to the nature of state involvement in the corporate sector. I focus on Taiwan rather than Japan because the latter did not experience a financial crisis in 1997–98, making it difficult to draw comparisons with the reactions of other regimes in the region. I also choose to focus on Taiwan rather than South Korea because the former hosts political parties that are strong and more capable of overcoming coordination problems. As discussed in Chapter 2, a regime’s coordination capacity influences its ability to implement nontargeted goods and services such as a SWF. In comparison with the Philippines, a country with weak coordination capacity, Taiwan’s political system provides a cleaner test for this argument than South Korea’s.

Chapters 6 and 7 examine two DPARs – Malaysia and Singapore. These regimes are of interest because they share several important features in common while differing with respect to one key dimension that can account for their varying levels of state intervention. The features that they share in common include (1) well-established stock markets where they have listed most of their SOEs, (2) large, economically significant savings SWFs, (3) a sustained high level of growth over a long period of time, which allows for examination of how these regimes have coped with the rising pressures associated with the state’s crowding-out effects, (4) the early implementation of liberalizing reforms that permit a longer time span to be examined to test the theory’s predictions, and (5) having the distinction of being the two oldest DPARs in the world (Malaysia and Singapore gained independence in 1957 and 1965, respectively), thus granting sufficient time for each regime’s institutional arrangements to produce regularized patterns concerning state involvement in the corporate sector. The key dimension of difference between them regards the level of threat to each regime’s ruling party since the Asian financial crisis. Malaysia’s ruling party became weakly dominant following the 1997 crisis, and it has confronted a growing threat from political opponents ever since, whereas Singapore’s ruling party has remained strongly dominant.

I conclude in Chapter 8. I begin by concisely summarizing the argument and evidence. I then discuss this book’s theoretical contributions to several additional literatures and to the SOE and SWF literatures mentioned in this chapter, including the role of the state to spur economic development in the presence of weak institutions, the stability and growth of DPARs, comparative corporate governance, and the global diffusion of liberalizing reforms. Finally, I offer some thoughts about areas for future research, including additional work on SWFs, the role of SWFs as institutional intermediaries, state-owned business groups within and between countries, the nature of state investment between countries with large state sectors, and extending the framework developed here to other aspects of “economic statecraft.”