I. Introduction

In recent decades, criticism of fractional-reserve banking has reemerged within academic debate, particularly among Austrian School economists.Footnote 1 This critique transcends technical objections to modern finance, grounding itself in legal, ethical and institutional principles such as respect for private property and the framework of a genuinely free market.Footnote 2 Analysing money creation through fiduciary credit exposes deep inconsistencies in both economic coordination and legal coherence.Footnote 3

Fractional-reserve banking creates money ex nihilo, distorting market signal, encouraging over indebtedness, and generating recurrent business cycles through intertemporal discoordination.Footnote 4 Legally, it violates private law principles, as simultaneous claims to the same monetary base breach the essential duty of safekeeping in deposit contracts, undermining ownership rights and contractual integrityFootnote 5.

An original contribution of this study – first developed under Professor Jesús Huerta de Soto and later cited in his Money, Bank Credit, and Economic Cycles,Footnote 6 – clarifies that even in irregular deposits of fungible goods, the depositary’s obligation to safeguard and the prohibition of use remain valid. This doctrinal clarification reinforces the illegality of fractional banking by differentiating it clearly from the mutuum or loan contract.

Moreover, the article also analyses two common defences of fractionality: demand loans and the issuance of real bills by private banks in competitive systems without a central bank.Footnote 7 It concludes that demand loans cannot provide true, immediate availability of capital and that real-bills proposals still entail monetary expansion without prior saving, producing inflationary and redistributive effects like fiat moneyFootnote 8.

Finally, the study proposes an institutional alternative aligned with Austrian doctrine: a 100 % reserve requirement on demand deposits, a strict legal separation between deposit and loan contracts, and the recovery of sound, commodity-based moneyFootnote 9. Such reform would restore a just, stable and law-abiding monetary order consistent with individual freedom, market discipline, and the principles of classical private law.

II. Literature review: the debate on fractional reserves and the reserve ratio

The debate surrounding the legitimacy and stability of fractional-reserve banking is one of the most profound and persistent in monetary and financial theory, especially within the Austrian School. Far from being a merely technical dispute, the different positions reveal radically opposed conceptions of the nature of money, credit, property rights and the origin of economic instability. To properly contextualise the critique developed in this article, it is essential to analyse the main schools of thought that have addressed this question. The debate not only divides the Austrian School but also triggers intense disputes within liberal thought itself and among more Keynesian and monetarist schools.

1. The orthodox thesis of the Austrian School: legal illegitimacy and economic instability

The main current of the Austrian School of Economics – whose foremost contemporary exponents in this subject are Murray N Rothbard and Jesús Huerta de Soto – argues that fractional-reserve banking is both legally fraudulent and the main cause of business cyclesFootnote 10.

From a legal standpoint, as Huerta de SotoFootnote 11 explains, the practice violates the Roman law distinction between deposit (depositum), whose purpose is safekeeping and conservation, and the contract of loan (mutuum), which entails a transfer of ownership and availability. In a sight deposit – even of fungible goods like money – the depositary must maintain full availability for the depositor. Using these funds for loans creates two simultaneous claims over the same money, amounting to misappropriation and breach of contract. Such duplication is considered a legal impossibility and a fraud, regardless of its acceptance in positive law, as it infringes property rights.Footnote 12

From an economic perspective, the illegitimacy extends to the creation of fiduciary media – money created ex nihilo through fractional reserves – representing credit expansion without real saving. According to Austrian Business Cycle Theory (MisesFootnote 13 and Friedrich A HayekFootnote 14), this artificial expansion lowers interest rates and sends false signals to entrepreneurs, leading to unsustainable long-term investments and widespread capital misallocation. The ensuing boom inevitably collapses into crisis and recession as the economy readjusts to genuine levels of saving.Footnote 15

The only coherent remedy, in this view, is to prohibit fractional reserves on demand deposits through a 100% reserve requirement, ideally under a system of free, commodity-based money such as gold.Footnote 16

2. The internal dispute: the free-banking school and market self-regulation

Within the liberal field, an influential school of thought known as the Free-Banking School disagrees with the 100% thesis. Authors such as Lawrence H. White,Footnote 17 George SelginFootnote 18 and Kevin DowdFootnote 19 argue that a competitive banking system with fractional reserves is not only legitimate but also economically stable, provided it operates without a central bank and without state privileges.

In the first place, the Free-Banking School argues that competition serves as an effective disciplinary mechanism. In such a system, each bank issues its own notes redeemable in base money (typically gold). If a bank over-expands credit, rival banks will demand redemption, drain its reserves and force restraint.Footnote 20 Thus, the market naturally limits money creation, aligning supply with the public’s liquidity demand and preventing inflation.Footnote 21

Supporters often cite the Scottish system (1716–1845) as an exampleFootnote 22 of stability and growth,Footnote 23 though critics note it was partly regulated, suffered crises, and relied on the Bank of England. Legally, this school sees fractional deposits not as fraud but as voluntary, informed agreements between banks and clients.Footnote 24

However, a modern variant of this school, defended by authors such as Juan Ramón Rallo,Footnote 25 revives the Real Bills Doctrine of John Law and Adam Smith, claiming that money issued against short-term, self-liquidating commercial debt expands in line with real trade. Orthodox Austrians reject this, arguing it still constitutes credit creation without prior saving, distorting production.Footnote 26

3. External views: monetarist, neoclassical, and Keynesian justifications

Outside the Austrian tradition, fractional reserves are interpreted in contrasting ways. First, Monetarists, led by Milton Friedman, criticised banks’ ability to create money as a key source of instability that undermines central control of the money supply. His proposal, surprisingly close in form to the Austrian 100% reserve plan though different in spirit, was to enforce full reserves to grant the central bank complete authority over money creation, ensuring a predictable growth rate to stabilise prices.Footnote 27

On the other hand, Neoclassical economics, accepts fractional reserves as an efficient mechanism of intermediation that channels short-term savings into long-term investment, thereby fostering growth. It does not see them as the cause of business cycles, instead attributing crises to problems such as information asymmetries or self-fulfilling bank runs. The Diamond–Dybvig model frames run as equilibria that justify regulation, deposit insurance, and a lender of last resort.Footnote 28

Finally, post-Keynesian economics advances a radically different vision: fractional reserves are essential to a monetary economy of production. For Basil Moore,Footnote 29 Marc LavoieFootnote 30 or WrayFootnote 31 money is endogenous loans create deposits. Banks generate purchasing power ex nihilo in response to demand, while central banks accommodate reserve needs to maintain payment stability, influencing only through interest rates. Fractional reserves thus define modern capitalism itself.

4. Synthesis of the debate

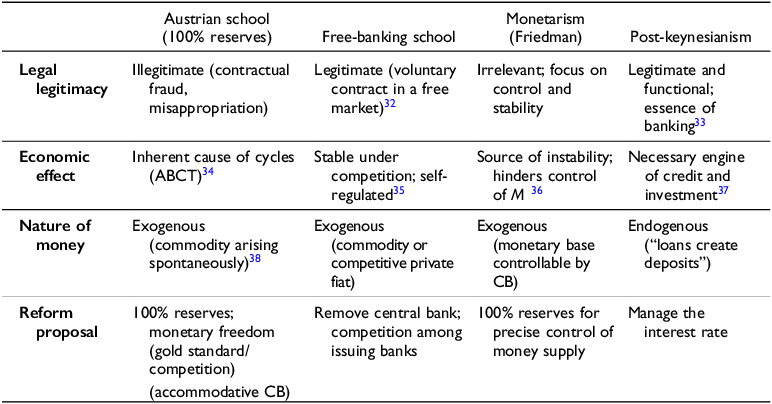

The points of friction among these schools are irreconcilable and center on the nature of the banking contract, the cause of economic instability, the endogeneity or exogeneity of money, and the legitimate role of the state in the monetary sphere. The following table summarises each paradigm’s fundamental positions.

III. Conceptual and legal foundations of the critique of fractional reserves

1. The classical distinction between deposit and loan

A central legal critique of fractional- reserve banking lies in the precise distinction between deposit and loan (mutuum). Rooted in Roman law and upheld by the Spanish Civil Code (Articles 1758 ff. for deposit, and Articles 1740 ff. for mutuum), this distinction highlights two opposing contractual logicsFootnote 39. The deposit’s essence is safekeeping: the depositor retains ownership, and the depositary must preserve and return the same thing. Even in irregular deposits, where fungible goods are commingled, the key is the prohibition on the depositary’s use or disposal of the asset. Conversely, in a loan or mutuum, ownership is transferred, granting the borrower free use, with the duty to return an equivalent amount of the same kind and quality. Modern banking blurs these categories: while current accounts are presented to clients as deposits – implying immediate availability – banks operate them as loans, deploying deposited funds at will. This legal and conceptual confusion underpins the controversy surrounding the legitimacy of fractional-reserve bankingFootnote 40.

2. The doctrinal contribution to the distinction between irregular deposit and loan

A correct understanding of the banking contract requires distinguishing between the irregular deposit of fungible goods and the loan, since the legality of banks’ use of deposited money depends on this difference. In a regular deposit, what is delivered is a quantity of a generic good – such as money or gold – not specific items. Its essence lies in maintaining the depositor’s immediate availability over quantity, not in preserving physical identity.Footnote 41 As highlighted by César Martínez Meseguer and adopted by Huerta de SotoFootnote 42, the object of the irregular deposit is always an abstract quantity, and what must be returned is the tantundem – the same amount and quality – without any transfer of ownership.

Thus, the depositor retains ownership and expects the preservation of his right of disposal, while the depositary is prohibited from using the funds unless expressly authorised. This view aligns with Articles 1768, 1281 and 1255 of the Spanish Civil Code, which regulate the use of deposits, the intent of the parties and contractual freedom.

Against this background, the key distinction lies in authorisation: in a loan, the borrower gains ownership, whereas in a deposit, the depositary must safeguard and immediately return the funds.Footnote 43 Therefore, bank deposits are true deposits, not loans. Using them to grant credit without consent constitutes contractual breach and misappropriation.Footnote 44

3. The protection of property and the principle of contractual typicality

The legal critique of fractional reserves is reinforced by an appeal to the principle of contractual typicality, which imposes limits on freedom of contract.Footnote 45 The Spanish legal system does not allow a contract called a “deposit” to be configured de facto as a concealed loan – especially when it concerns relationships of special economic significance that affect millions of citizens.Footnote 46

Accepting that bank deposits may imply the bank’s use and disposal of funds amounts to denying the depositor’s property right over the money and thus establishing a legal anomaly that contradicts essential principles of private law: clear contractual will, equivalence of performances, informed consent, contractual good faith, and the inviolability of property.

Moreover, the habitual practice of allowing banks to use deposited funds without expressly warning clients or requiring their informed consent constitutes a systemic breach of the principle of transparency, which, in other branches of law (such as consumer law), is considered essential.

4. The evolutionary definition of money: means of payment, use value and material standard

A clear understanding of money is vital to assess today’s monetary system, yet most modern definitions – often limited to a “medium of exchange” – lack precision and ignore its legal and institutional nature.

From the perspective of the Austrian School of Economics, and in line with research conducted by one of the authors of this workFootnote 47, money must be understood as a spontaneously arisen social institution, the result of an evolutionary processFootnote 48 through which certain commodities – such as gold or silver – came to be commonly used not only to facilitate exchanges but also to safeguard value, discharge debts, and serve as a price standard.Footnote 49

Accordingly, money must possess the following characteristics:

-

• Be a material, fungible economic good with use value.Footnote 50

-

• Have exchange value recognised by market participants.

-

• Be accepted as a means of payment, i.e., as an instrument capable of extinguishing economic obligations.

-

• Act as a monetary price standard within a given community.

On this basis, the following alternative, more precise definition is proposed: money is a type of evolutionary social institution consisting of any (material) economic good which, being subjectively attributed use value and exchange value, is commonly and freely accepted as a means of payment by a society.

This definition, in turn, allows us to distinguish with precision three concepts that are often conflated:

-

• Medium of exchange (ME): any good that facilitates barter without necessarily extinguishing debts.

-

• Means of payment (MP): any good that, by discharging an obligation, allows a contract or debt to be deemed fulfilled.

-

• Money (M): that good which, in addition to being ME and MP, arises from spontaneous order, maintains objective use value, and operates as a socially shared standard.

Therefore, neither fiat money nor cryptocurrencies qualify as genuine money. Fiat currencies rely on state coercion and lack material backing, while cryptocurrencies lack intrinsic value and widespread acceptance. Both are artificial substitutes, revealing the fictional nature of today’s monetary system and highlighting the need for market-based institutional reform.

5. Cryptocurrencies, promissory notes and “fiat money”: are they truly money?

One of the greatest doctrinal confusions in contemporary monetary analysis lies in the conceptual amalgam between exchange instruments and money proper. This confusion has been accentuated by the rise of new forms of value representation such as cryptocurrencies, electronic means of payment, private promissory notes or accounting units issued by centralised or decentralised entities.

Moreover, contemporary legal and monetary scholarship has analysed how many of these instruments acquire monetary functions or degrees of “moneyness” through legal recognition, institutional backing, and balance-sheet operations.Footnote 51 This institutional and balance-sheet conception of money is developed in contemporary legal and monetary theory by various authors. In this literature, monetary instruments acquire degrees of “moneyness” through legal recognition, tax acceptability and their integration into regulated payment and settlement systems. In this way, money is conceived as a legally anchored liability embedded in public and private balance sheets.Footnote 52

From the perspective proposed in the previous section, only that material economic good with use and exchange value, spontaneously arisen and freely accepted as an effective means of payment in a society (market), can be considered money.Footnote 53 Strictly speaking, money is not a credit right, nor a promise, nor a symbol, but a present good that extinguishes obligations.

On this basis, the following clarifications can be made:

-

a) Contemporary fiat money

Fiat currencies like the euro or the dollar cannot be considered genuine money because they are not backed by any tangible good, possess no use value and owe their acceptance to state coercion rather than voluntary market evolution. Their legal tender status forces their use for paying taxes, fines and public obligations. Economically, they function as instruments for financing government spending, socialising bank losses and enabling credit expansion without prior saving.Footnote 54 Thus, they are not real money, but fiduciary means of payment sustained by law, not by market confidence.

-

b) Cryptocurrencies and digital assets

Cryptocurrencies (such as Bitcoin or Ethereum), although they arise in a decentralised, private and voluntary manner, do not meet the requirements to be considered genuine money. They present the following limitations:

-

• They have no prior use-value: Unlike money as an evolutionary institution, cryptocurrencies lack a use-value prior to their potential exchange value, which conflicts with Mises’s regression theorem.Footnote 55

-

• They are not universally or generically accepted as a means of payment: acceptance is limited and volatile, with neither institutional nor physical backing.

-

• They do not operate as a broadly used price standard.

-

• In many cases, they do not discharge legal obligations but function as intermediate means subject to subsequent conversion into fiat currency.

Therefore, at best, they can be considered freely accepted media of exchange that may play an important role as such, but not money in the evolutionary or institutional sense.

-

-

c) Promissory notes, bills and other representative instruments

A particularly relevant case is that of promissory notes, bills of exchange or commercial paper, which some authors – such as RalloFootnote 56 – propose as a foundation for free-banking systems with quasi-money issuance backed by “real bills.”

However, these instruments are not money either. They are promises to pay – legal documents representing rights to a future delivery of money. They may circulate, be discounted, and serve as collateral, but they do not extinguish obligations unless actually paid with real money.Footnote 57 Their circulation is secondary and derivative; they are neither a unit of account nor a stable standard.

Therefore, neither the use of promissory notes, nor cryptocurrencies, nor fiduciary units backed by debt can circumvent the need for a material, present universally accepted means of payment – that is, genuine money in the classical sense.Footnote 58

6. Considerations on deflation before addressing the economic arguments

Before proceeding to the next section, it is important to recall the context of the fear of deflation that permeates economic thought and public administrations and trade unions.Footnote 59 In fact, fear of deflation is common ground between monetarists and Keynesians alike, such as Keynes.Footnote 60 Krugman,Footnote 61 or Bernanke.Footnote 62

Deflation is the contraction of the money supply – or equivalently, an increase in the demand for money – resulting in a general fall in prices and a rise in purchasing power. It can take several forms depending on its origin.

The first is government-induced deflation, exemplified by post–World War I England, where Churchill’s return to the gold standard at the pre-war parity caused a monetary contraction and pound appreciation. For an export-driven economy, this policy proved disastrous, collapsing exports, production, and employment – hence a “bad deflation.”

The second arises from the fractional-reserve banking system. Artificial credit expansion generates booms, but when errors emerge, crises ensue: assets lose value, liabilities persist and defaults rise. During downturns, loan repayments outpace new credit creation, shrinking the money supply and producing deflation. The core issue, however, is not deflation itself but the preceding inflationary credit expansion made possible by fractional reserves.

The third type, “good deflation,” stems from productivity gains. With a stable money supply, rising productivity lowers prices naturally, as occurred in the United States between 1865 and 1900 – an era of strong growth and moderate annual deflation.Footnote 63

Since the mid-twentieth century, inflationary policies have dominated, obscuring deflation’s virtues. Yet deflation promotes saving, the basis of sustainable growth and long-term prosperity.

IV. Economic and legal arguments against fractional reserves (Austrian view)

1. Legal incompatibility between deposit and fractional reserves

From a classical legal perspective, fractional-reserve banking contradicts the nature of the deposit contract. The depositor believes he retains ownership and immediate availability of his funds, while the bank treats them as a loan, using them freely and keeping only a fraction in reserve.

This creates a duplicity of ownership claims over the same money – an impossibility under private law, as noted by Huerta de Soto.Footnote 64 The practice thus entails artificial credit expansion and violates the legal principle of exclusive ownership.Footnote 65 Even if the client is aware, contractual typology forbids disguising a loan as a deposit without meeting its legal conditions.Footnote 66

2. Credit expansion as the origin of the business cycle

From an economic standpoint, the critique of fractional reserves is articulated chiefly around their capacity to provoke recurrent business cycles, according to the theory developed by Ludwig von Mises and formalised by Friedrich A. Hayek: The Austrian Business Cycle Theory (ABCT).Footnote 67

The issuance of fiduciary media by banks – that is., money not backed by prior real saving – permits a bank credit expansion with no correlate in voluntary saving, which distorts the price system and generates false signals for economic agents.Footnote 68 An artificial reduction in interest rates ensues, leading to unsustainable investments (malinvestment), especially in capital goods in stages of production distant from consumption.Footnote 69 This mechanism of bank-driven money creation through credit expansion is explained in mainstream theory through the money multiplier framework and credit expansion.Footnote 70

Fractional reserves trigger artificial booms followed by crises, as monetary manipulation distorts the balance between consumption and investment. As Mises and Hayek argued, this process creates macroeconomic imbalances, over-indebtedness and systemic discoordination, undermining the real foundations of economic stability.

3. Fractional reserves and the dual-liquidity problem

The Austrian School highlights the problem of dual liquidity: both depositor and bank claim full ownership of the same funds, creating an illusion of solvency that collapses in bank runs. Central banks and deposit guarantee merely conceal this risk, transferring losses to taxpayers and weakening individual responsibility.Footnote 71

Consequently, the modern banking system rests on an artificial and very dangerous institutional scaffolding whose purpose is to conceal and sustain a structural legal-economic error.Footnote 72

4. The special case of demand loans: a fictitious category

An additional argument of weight – scarcely explored by conventional economic literature – concerns the practical and legal infeasibility of so-called “demand loans,” which have been used as a justification to try to legitimise fractional reserves.Footnote 73

According to this thesis, it would be legally valid for a client to lend money to a bank on the condition that it be repaid immediately upon request.Footnote 74 However, closer scrutiny reveals that this figure is technically unworkable, both contractually and operationally.

Every loan, even a “demand loan,” requires a reasonable repayment period based on custom and practice; immediate availability is impossible. Thus, the so-called demand loan is a legal fiction used to disguise a breach of the mutuum’s principles and a substitution for the true deposit contract.

5. Ethical and moral considerations: intertemporal justice

The Austrian School asserts that justice demands absolute respect for property rights and genuinely free contracts consistent with their true nature.Footnote 75

Fractional reserves institutionalise money creation, benefiting first receivers like banks and governments while harming wage earners and savers through the regressive Cantillon effect.Footnote 76 Moreover, fractional reserves discourage genuine saving, promote present consumption, and cause unsustainable wealth redistribution, distorting individual economic decisions and undermining intertemporal responsibility.Footnote 77

V. Institutional and macroeconomic consequences of fractional-reserve banking

1. Forced bank-intermediation and the privilege of fiduciary issuance

Fractional reserves have transformed the economy, turning banking into a state-favoured monopoly. Financial intermediation is no longer voluntary but imposed, as money is created ex nihilo by privileged private banks, forcing firms, consumers, and governments into systemic credit dependence.

This phenomenon has caused a mutation in money. Money ceases to be an economic good arising spontaneously from the market – as historically occurred with gold or silverFootnote 78 – and becomes a fiduciary unit created by decree and maintained by state and banking monopolies.Footnote 79 The institutional consequence is clear: fractional reserves have given way to a financial architecture based on legal privileges, information asymmetries, negative externalities and morally unacceptable risks.

2. The origin of the modern central bank: lender of last resort

The fragility of fractional-reserve banking – exposed by liquidity crises and bank runs – led to the creation of central banks as lenders of last resort. However, this intervention entrenched the problem by legitimising insolvent banks sustained by state support.Footnote 80 As Huerta de SotoFootnote 81 observes, the result is a system of socialised losses and privatised profits, where taxpayers bear the cost of systemic errors. Central banks thus become political instruments of redistribution, undermining individual responsibility and replacing the spontaneous market order with centralised financial planning favouring those closest to power.Footnote 82

3. Monetary financing of the public deficit and the erosion of fiscal discipline

Fractional reserves enable indirect state financing: banks create money by purchasing public debt, backed by central banks. This feedback loop fuels credit expansion and public spending, encouraging fiscal irresponsibility. Governments bypass real saving and revenue constraints, replacing budgetary discipline with dependence on artificially created money and privileged banking support.

From the Austrian perspective, this situation is extremely dangerous: it disincentivises democratic control of public spending, dilutes fiscal transparency and generates institutionalised, persistent inflation that acts as a hidden tax on citizens’ purchasing power, especially on the most vulnerable.

4. Volatility, bubbles and structural instability

The systematic use of fractional reserves amplifies macroeconomic volatility, allowing fluctuations in risk perception and credit conditions to translate into abrupt changes in the quantity of money and investment. As explained earlier, this artificial credit expansion is the origin of financial bubbles, followed by sharp and painful adjustments that punish agents less connected to the financial system.

Thus, the current model is not only inefficient from an intertemporal standpoint but becomes structurally unstable – generating cycles that arbitrarily redistribute wealth, reward short-term speculation and penalise productive saving.

The historical experience of recent decades – with successive crises in different arenas (real estate, technology, financial, sovereign) – shows that these are not anomalies but logical consequences of a system based on fiduciary monetary expansion facilitated by fractional reserves.Footnote 83

5. Institutional effects: financial clientelism and regulatory capture

Finally, at a deeper institutional level, fractional reserves have contributed to consolidating a financial elite closely linked to political power, generating phenomena of clientelism, regulatory capture and institutional corruptionFootnote 84. Large banking entities not only influence economic policy through their systemic size but also benefit from rules designed for their protection and survival, to the detriment of competition and citizens’ sovereignty.

This process produces a serious distortion of the rule of law: laws are crafted to suit the needs of the banking system rather than as general laws applicable to all citizens and firms on equal terms. Law thus becomes a tool of institutional engineering in the service of particular interests, undermining the legitimacy of the political and economic system as a whole.Footnote 85

VI. Critiques of alternative proposals: demand loans and real bills as a justification for fractionality

In response to the Austrian critique of fractional-reserve banking, some authors have formulated alternative proposals or justifications seeking to legitimise this system within a context of contractual freedom. Two such proposals merit special attention: the one that defends the existence of a demand loan as the legal foundation for the operation of current accounts,Footnote 86 and the one that proposes the issuance of money backed by real bills in a banking system without a central bank.Footnote 87 This section analyses both approaches, showing their theoretical, practical and legal weaknesses.

1. Real bills as a monetary base: limits and contradictions

The “real bills” proposal seeks to legitimise fiat money creation without central banks by allowing private banks to issue money backed by short-term commercial debt linked to real goods in production or transit. Defended by figures such as Henry ThorntonFootnote 88 and revived by Juan Ramón Rallo,Footnote 89 it claims that such issuance merely reflects real output and satisfies temporary liquidity needs, supposedly avoiding inflation through market discipline.Footnote 90

However, the Austrian School rejects this view. First, issuing money against real bills still constitutes ex nihilo creation, distorting prices, interest rates and production structures.Footnote 91 Second, when the bill is repaid, the money usually remains in circulation, creating a lasting inflationary effectFootnote 92. Third, the supposed backing by goods is weak, as these are often illiquid, perishable or unenforceable. Finally, historical evidence from relatively free banking systems like Scotland or Canada shows that market discipline failed to prevent overexpansion, crises, and concentration.Footnote 93

Institutionally, the real-bills doctrine does not correct the fundamental flaws of fiat money. At most, it would produce a private fiduciary system with slightly stronger constraints but still based on monetary creation without prior real saving – an accounting and contractual fiction incompatible with a sound monetary order.Footnote 94

2. The contractual limits of demand loans: an analysis from commercial law

A frequent defence of fractional-reserve banking is to present current accounts not as deposits but as demand loans, whereby the client allegedly transfers ownership of money to the bank with the right to reclaim it at any time. This interpretation, however, faces serious legal and practical objections. In civil law, demand loans are possible but remain exceptional and difficult to operate. In banking practice, the concept is largely fictitious: the client’s balance appears as his own and as instantly available, yet the bank has already lent those funds to a third party. This creates a duplication of capital, incompatible with sound accounting and contractual responsibility.

Moreover, jurisprudence on open-ended loans requires a reasonable period for repayment, considering custom, banking practice and technical feasibility. Thus, genuine instantaneous restitution is impossible.

Consequently, the demand-loan argument cannot legitimise a bank’s promise of immediate availability of funds that have been simultaneously transferred elsewhere. Far from resolving the issue, it exposes a structural contradiction: fractional-reserve banking, even under this interpretation, rests on legal inconsistency and amounts to economic fraud.

3. The 100% reserve requirement: legal certainty for demand deposits

The heart of the reform proposed by the Austrian School lies in the radical separation between deposit contracts and loan contracts. At present, fractional reserve banking has blurred that difference, allowing demand deposits to be used as the basis for new credit operations, despite their legally custodial nature, and without the depositor’s consent or any genuine possibility of choice.

Accordingly, this distortion can be addressed by establishing a 100% reserve requirement for demand deposits (and equivalents); which obliges banks to keep the totality of deposited funds available for immediate return and prevents their use as a basis for credit expansion.Footnote 95 In doing so, the reform restores legal coherence by protecting depositors’ property rights and eliminates banks’ capacity to expand fiduciary money autonomously.

At the institutional level, implementation may be gradual and compatible with contractual freedom. However, it requires clear legislative reform that qualifies fractional-reserve banking applied to demand deposits as fraud, thereby restoring market discipline and aligning banking practice with the principles of private law.Footnote 96

From an institutional and regulatory perspective, under a system of custodial banking with a 100% reserve requirement, the traditional functions of a central bank as lender of last resort become largely redundant. Consequently, the elimination of the central bank would not constitute an immediate process, but rather a gradual, stage-based transition, with the effective establishment of a 100% reserve requirement representing the key step. Once this stage is reached, demand deposits would be fully backed by reserves and legally segregated from banks’ balance sheets. As a result, even in the event of bank failure, deposited funds could be returned to depositors in full, thereby eliminating the risk of bank runs.Footnote 97 In this context, regulatory frameworks designed to safeguard liquidity, capital adequacy, and depositor protection lose much of their rationale with respect to custodial banking activities.

Moreover, the full viability of this institutional framework would require the replacement of the current system of monopolistically issued fiat money with a system of private money,Footnote 98 emerging from a spontaneous and evolutionary market process. In this sense, such money would need to consist of the monetary medium historically selected by society, namely gold.

By contrast, credit intermediation would operate under normal market discipline. Savings voluntarily invested through loan contracts would remain subject to entrepreneurial risk, and losses would be borne by investors, as in any other economic activity. However, such failures would not trigger systemic banking crises, since credit expansion would be constrained by prior saving. The recurrent financial and economic crises characteristic of fractional-reserve systems – driven by artificially low interest rates and intertemporal discoordination – would therefore be structurally avoided.

4. The restoration of sound money: gold, cryptocurrencies and the evolution of commodity money

The third axis of Austrian reform is the recovery of a sound monetary system, that is, a system in which the unit of account and exchange cannot be manipulated by political power. Historically, gold has fulfilled this function, and the Austrian School has defended its use as a spontaneous commodity money, arising from the market and the institutional evolutionary process described by Menger.Footnote 99

Today, technical conditions make possible competition between different forms of non-state money, such as gold, silver or even certain cryptocurrencies backed by real assets or with strict mechanisms of limited issuance (such as Bitcoin, in its original design).

The proposal does not require imposing by law a specific form of money but rather removing the monopoly of the central bank and allowing genuine competition between monetary units, so that individuals voluntarily and in a decentralised way choose the most reliable and stable medium of exchange and store of value. As HayekFootnote 100 notes, the key lies in monetary choice as the foundation of spontaneous order and fiscal responsibility.

5. Feasibility, transition and possible objections

It is foreseeable that this alternative model will encounter resistance, both from financial elites and from States, which would see much of their capacity for financing eliminated. However, the periodic crises of the current system, together with the discrediting of conventional monetary policy, open a window of opportunity to seriously discuss a transition towards a more stable order.Footnote 101

The transition may be approached gradually through:

-

• Progressive elimination of the legal privilege of fractional reserve banking.

-

• Voluntary introduction of the 100% reserve requirement in certain accounts.

-

• Full legalisation of contracts in other currencies or cryptocurrencies as means of payment.

-

• Legislative reform to clearly distinguish deposits from loans.

-

• Gradual substitution of the central bank as a monopoly issuer, reducing its power to set interest rates artificially, etc.

The usual objections – such as the alleged lack of liquidity or the “rigidity” of the system – have been widely refuted in Austrian literature.Footnote 102 Indeed, the existence of a system of genuine rather than fictitious saving is the only basis for a sustainable economy, as demonstrated by the Theory of Capital and Interest developed by Böhm-BawerkFootnote 103 and later by Mises,Footnote 104 HayekFootnote 105 and Rothbard.Footnote 106

The claim that a strict gold standard without demand deposits would restrict liquidity is contradicted by historical evidence. Between 1865 and 1900, the United States enjoyed strong growth alongside moderate, sustained deflation.Footnote 107 The gold standard maintained purchasing power and channelled credit toward productive uses, limiting speculation. In a system based solely on genuine loans, interest rates naturally coordinate saving and investment, ensuring that credit supply adjusts to real economic conditions. Thus, market forces, not central intervention, guarantee liquidity and stability.Footnote 108

This mechanism was described in pioneering fashion by Böhm-BawerkFootnote 109 and subsequently developed by Wicksell,Footnote 110 MisesFootnote 111 and Hayek,Footnote 112 who explained how the interest rate acts as the price that coordinates saving and investment decisions. Furthermore, there would be the possibility of incorporating money with other standards – silver, platinum, etc. – as well as the creation of multiple means of exchange – non-monetary – which would facilitate transactions.

VII. Discussion: internal coherence, institutional robustness and scientific superiority of the Austrian paradigm

1. Internal coherence of Austrian analysis: theory of capital, of the cycle and of law

Austrian economic thought – from Menger, Böhm-Bawerk and Mises, to Hayek, Rothbard and Huerta de Soto – has always been characterised by its methodological, analytical and epistemological unity. Its approach to monetary and financial phenomena is articulated around:

-

• A solid theory of capital and of the temporal structure of production, which makes it possible to understand the intertemporal distortions caused by artificial credit expansion.Footnote 113

-

• A theory of the business cycle (Austrian Business Cycle Theory), which is not an ad hoc construction, but a logical derivation from the interaction between saving, investment and interest rates.Footnote 114

-

• A coherent defence of Natural Law and Private Law as the institutional framework of spontaneous order, where contracts must be respected in their form and substance, without privileges or exceptions.Footnote 115

From this perspective, the current system of fractional reserve banking, sustained by central banks and backed by permissive legislation, represents both an epistemological and moral rupture, incompatible with the principle of individual responsibility and respect for private property.

2. Institutional robustness: spontaneous order, legal certainty and patrimonial responsibility

The Austrian paradigm does not propose a utopian or idealised system, but the restoration of an evolutionary institutional framework, in which money, contracts and financial institutions emerge from the free actions of individuals and not from political imposition.Footnote 116

The core of this institutional proposal can be summarised in three fundamental principles:

-

a) Separation between deposit and loan, guaranteeing the legal nature of each contract.

-

b) Full patrimonial responsibility of financial institutions, eliminating bailouts, privileges and lenders of last resort.

-

c) Freedom of monetary choice, breaking the central bank’s monopoly and allowing competition between different monetary units.

These principles are not only consistent with the Western legal tradition but also align with the evolutionary theory of law and with contemporary developments of decentralised institutions.Footnote 117

3. Scientific superiority: explanatory, predictive and normative capacity

In contrast with the dominant theory – Keynesian, monetarist or neoclassical – which has repeatedly failed to anticipate or explain financial crises, the Austrian paradigm possesses greater scientific capacity in three key dimensions:

-

• Explanatory: Austrian business cycle theory has accurately described the mechanism by which artificial credit expansion generates unsustainable booms followed by crises.

-

• Predictive: Authors such as Mises, Hayek or Huerta de Soto have theoretically anticipated the Great Depression, the stagflation of the 1970s, and the 2008 crisis, in contrast with the blindness of economic orthodoxy.

-

• Normative: The proposal of free banking with a 100% reserve requirement offers a robust normative framework, consistent with basic legal principles, without internal contradictions or arbitrary privileges.

The superiority of the Austrian paradigm is not based solely on its theoretical elegance, but on its logical consistency, legal rigour and profound respect for individual rights, which are the ultimate foundation of any truly free and stable economic system.

4. An ethical and politically viable proposal

Beyond its theoretical robustness, the Austrian model constitutes an ethical proposal, insofar as it rejects the coercive use of monetary and financial power by the State and privileged agents.Footnote 118 In a context of growing distrust of public institutions, structural inflation, massive indebtedness and banking fragility, the idea of a transition towards a system of sound money, banking without privileges and fully respected contracts is not only desirable, but urgent.

The political and technical feasibility of this transition requires courage, well-designed gradualism, and an effort of institutional pedagogy. But the costs of maintaining the current system are already unsustainable, both in economic terms and in terms of democratic legitimacy.

VIII. Conclusions

This article has argued – combining insights from monetary theory, civil law and institutional philosophy – that fractional-reserve banking is conceptually inconsistent, economically unstable and legally indefensible. Attempts to justify it through notions such as demand loans, real bills or free banking fail to resolve – and often intensify – the system’s structural flaws.

In legal terms, fractional reserves create a duplication of rights over the same capital, violating basic principles of private law. The confusion between irregular deposit and loan, sustained by regulatory complicity between banks and the State, has produced a hybrid contract imposed on citizens without genuine consent.

From an economic perspective, credit expansion without prior saving distorts market signals, artificially lowers interest rates, and triggers recurrent boom–bust cycles. As Austrian theorists show, manipulating money and interest disrupts intertemporal coordination, generating deep imbalances.

For these reasons, the article calls for an institutional redefinition of money as a spontaneously evolved social institution composed of material goods with use and exchange value, freely accepted as payment. This distinction clarifies the difference between money, means of payment and means of exchange – revealing that fiat currencies, promissory notes, and cryptocurrencies lack the essential characteristics of true money, as they rest on coercion or speculation rather than intrinsic value.

Against this background, the so-called demand loan, even if formally valid, cannot ensure true instant availability of funds and thus rests on a legal fiction incompatible with accounting reality. Likewise, the proposal to issue money backed by real bills fails to solve the underlying problem: it still involves monetary creation without prior saving, preserving inflationary pressures and systemic fragility.Footnote 119

In conclusion, the article advocates a banking model with 100% reserves on demand deposits, a strict legal separation between deposits and loan, and return to sound, freely chosen commodity money. Only such reform can restore a just, stable, and liberty respecting monetary order.

Table preserved conceptually.

Table 1 Long description

The table compares four economic schools: Austrian school, Free-banking school, Monetarism, and Post-keynesianism across four categories: Legal legitimacy, Economic effect, Nature of money, and Reform proposal. The table has four rows and five columns, including the headers. Row 1: Legal legitimacy, Austrian school: Illegitimate (contractual fraud, misappropriation), Free-banking school: Legitimate (voluntary contract in a free market), Monetarism: Irrelevant; focus on control and stability, Post-keynesianism: Legitimate and functional; essence of banking. Row 2: Economic effect, Austrian school: Inherent cause of cycles (A B C T), Free-banking school: Stable under competition; self-regulated, Monetarism: Source of instability; hinders control of M, Post-keynesianism: Necessary engine of credit and investment. Row 3: Nature of money, Austrian school: Exogenous (commodity arising spontaneously), Free-banking school: Exogenous (commodity or competitive private fiat), Monetarism: Exogenous (monetary base controllable by C B), Post-keynesianism: Endogenous (loans create deposits). Row 4: Reform proposal, Austrian school: 100 percentage reserves; monetary freedom (gold standard/competition), Free-banking school: Remove central bank; competition among issuing banks, Monetarism: 100 percentage reserves for precise control of money supply, Post-keynesianism: Manage the interest rate (accommodative C B).

Source: Authors’ own elaboration

Competing interest

The authors have no conflicts of interest to declare.

Open access

Open access