Introduction

Economists of the past as well as the present have been getting involved in an important debate about the determinants of inflation rate in a country; whether the inflation rate is due to a fiscal component or to a monetary component, or something else. The classical school did not consider the effect of public policies on deciding output, employment and price level, or inflation rate. To them, money is a veil and is neutral in the long run, although it determines price at the full extent of monetary shock. However, the modern economist, Keynes, defended the classical line on the virtue of the Great Depression in the 1920s and 1930s, where the roles of fiscal policy were considered as the panacea to rescue the economies, and the short-term effects of this policy were also able to determine the inflation rate. In the aftermath, the monetarist’s school rejected the Keynesian money supply effects on prices as the effects were unstable in the region of the liquidity trap. They, thus, proposed that the supply of money has the ability to generate output and price levels, but a consistent money supply, which usually happens in the long run, is inflationary in nature. Friedman and Schwartz (Reference Friedman and Schwartz1963) stated that inflation was essentially a monetary phenomenon and that stabilizing the supply of money could maintain price stability. In contrast, Sargent and Wallace (Reference Sargent and Wallace1985) showed that monetary policy and fiscal policy were entangled through the government’s budgetary constraints. With the development of economies in the last couple of centuries, in the discussion of determining inflation there have been many indicators that come into play. These are international trade, corruption, hikes in material costs, geo-political factors and so on.

Governments in countries, both developed or developing, or others, have now strongly involved themselves in investing in capital and revenue expenditures, to be an active partner in the growth process and to maintain social capital formations. This trend was boosted during the COVID-19 pandemic. Hence, it is now the phenomenon that government should be there in the economy. Further, with the belief of rent or bribe-seeking at the authority levels in several public projects, as well as dealing with monetary and financial transactions, there have been unethical and unaccounted monies which are in the system but do not contribute to economies’ output and real effects. Rather, their effects fall upon the volume of excess demand, which pushes up the inflation rate. Hence, from the monetarists, Keynes and the political economists’ perspectives, the new theoretical foundation is that inflation might be due to a fiscal component, a monetary component and a corruption component.

In the end part of the past century and in the early part of the new century, there were a number of notable works on the fiscal and monetary components’ link to inflation, such as in Leeper (Reference Leeper1991), Sims (Reference Sims1994) and Woodford (Reference Woodford1994), Bassetto (Reference Bassetto2002, Reference Bassetto2005). To date, no consensus has been built up on whether inflation is the result of monetary or fiscal policies, or of any political factors, or even any interacting components of the existing factors. It is therefore, in this milieu, required to investigate empirically whether the inflation rate has equilibrium relationships for the long run with public spending, the supply of money and corruption attitudes. This is what the current study focuses upon.

Motivation for the Study

Traditional macroeconomic tools, such as monetary and fiscal policies, are used mainly to counter the inflationary situations in the countries with different levels of development, but in many cases it is found that the inflationary situations are not controlled, even if the monetary and fiscal authorities of the countries are well executed. There are certain factors, such as earning through corrupt activities, that are added to the demand flow of the country but not recorded as inputs for production and supply, as they are hidden. Thus, there is a gap between demand and supply of goods and services, leading to excess demand, which pushes up the general price level. One of the important channels through which these corruption activities are noticed is the government’s fiscal spending upon the head of revenue expenditure, where mainly unproductive and the non-creation of assets are recorded. This study aims to intervene in this area to investigate how fiscal policy and monetary policy, mixed up with corruption activities, do have any relationships with the inflation levels of the selected developed and developing countries in the world.

Existing Literature

Leeper (Reference Leeper1991) reinterpreted Friedman’s 1948 policy framework on the interactions of monetary policy and fiscal policy, and reconsidered the result that general prices were indeterminate when the nominal rate of interest was pegged. According to Sims (Reference Sims1994) and Woodford (Reference Woodford1994), the government’s fiscal policy affected the price level; for the prices to be stable, the government must run a balanced budget over a business cycle and not with a structural deficit. In addition, Sims (Reference Sims1994) showed that the equilibrium price could be determined not only by the monetary policy alone, but also that a combination of fiscal and monetary policy would be responsible for price determination in an economy. Al-Marhubi (Reference Al-Marhubi2000), in the selection of 41 countries for 1980–1995, found positive relationships between corruption and inflation. Bassetto (Reference Bassetto2002) probed the validity of the fiscal theory of price level by explicitly modelling the market structure in which households and the government made their decisions, and showed that there existed government strategies that had led to a form of the fiscal theory in which price level was determined by fiscal components alone. Bassetto (Reference Bassetto2005) further discussed the fiscal theory with the observation that government debt and fiscal policy alone would determine price level, unlike the monetary policy. Galí (Reference Galí2015) explained the changing dimensions and trajectories of inflation due to monetary policy in the New Keynesian framework and also showed the business cycles that are affected by monetary policy and inflation. In a discussion on the effects of monetary policy and fiscal policy upon inflation in the European Union, Issing (Reference Issing2005) opined that monetary policy largely influenced inflation, compared with the fiscal policy in the EMU. From the good governance perspective, Piplica (Reference Piplica2011) found that corruption had a positive influence on price level in the EU. From a different angle, Akça and Karaca (Reference Akça and Karaca2012) also showed that corruption influenced the macro-economic performance of countries in general. According to Sabade (Reference Sabade2014), the inflation dynamics in developing countries such as India are diverse, and it is necessary to re-examine the significance of the belief that inflation is a monetary attribute. The study finds that money supply and inflation rates are not uniform, there are other factors too. Sami and Sassi (Reference Sami and Sassi2016) showed a positive and significant relationship between corruption and inflation in a list of 100 developing and developed economies for 2000–2012. Özşahin and Üçler (Reference Özşahin and Üçler2017) indicated that high corruption led to high inflation rates for 20 countries during the 1995–2015 period. Elkamel (Reference Elkamel2019) observed that corruption had led to an increase in the inflation level using panel data. In a recent study, Jorgensen and Ravn (Reference Jorgensen and Ravn2022), through their empirical work, have shown the puzzling response of prices, in that prices do not increase in response to a positive government spending shock. In an IMF Blog, Gaspar et al. (Reference Gaspar, Goncalves, Mauro and Poplawski-Ribeiro2023) shared their view that smart fiscal policy can tame inflation and maintain price stability without putting a burden on the cost of living. Chatterjee et al. (Reference Chatterjee, Bhattacharjee and Das2024) have investigated how income and capacity utilization maintain co-movements with inflation, and they found a clear long-term relationship among the three variables. However, in the short term, capacity utilization and income are found to influence inflation in developed countries but not in developing countries. Other notable theoretical and empirical works on the roles of fiscal policy and monetary policy, and governance factors upon inflation are Barro (Reference Barro1995); Blanchard and Fischer (Reference Blanchard and Fischer1989); Kilindo (Reference Kilindo1997); Bhattacharya (Reference Bhattacharya1985); Laurens and de la Piedra (Reference Laurens and de la Piedra1998); Rangarajan (Reference Rangarajan2001); Mohan (Reference Mohan2005); Prasanna and Gopakumar (Reference Prasanna and Gopakumar2010); Tiwari and Shahbaz (Reference Tiwari and Shahbaz2013); Banerjee and Das (Reference Banerjee and Das2018); Huria and Pathania (Reference Huria and Pathania2018); Shabbir et al. (Reference Shabbir, Saleem and Khan2021); Das and Mandal (Reference Das and Mandal2022), Aguilar et al. (Reference Aguilar, Cantú and Guerra2023), Grigoli and Sandri (Reference Grigoli and Sandri2023), among others.

Barro (Reference Barro1995) has shown how inflation impacts the growth rate as well as other economic and political indicators, such as rule of law, black market premium, democracy, etc., and has found that inflation negatively affects growth rate and black market premium while it positively affects rule of law and democracy. Blanchard and Fischer (Reference Blanchard and Fischer1989) descriptively explained the interlinked relationship between policy variables and inflation for a capitalistic society, with the usual positive impacts of the former upon the latter. Bhattacharya (Reference Bhattacharya1985) covered the discussion on the trade-off between inflation and growth, a major issue in economics, and opined that in developing countries the problem arises mainly as a result of the dual roles played by public expenditure – which generates income and employment – and deficit financing – which triggers inflation. Rangarajan (Reference Rangarajan2001) discussed the evolution of monetary policy, emphasizing the importance of adapting to a more complex financial system. Mohan (Reference Mohan2005) analysed the puzzles of monetary policy in contemporary times, after India’s economic reforms, and argued that the oil price boom might affect the formulation of monetary policy. Prasanna and Gopakumar (Reference Prasanna and Gopakumar2010) argued that the government needs to control budget deficits to promote growth and keep inflation low. While simulations indicate that this can be achieved by switching public expenditure from consumption to investment, this may be a difficult policy to pursue, especially in a developing country with a multiparty democracy. Das and Mandal (Reference Das and Mandal2022) investigate whether corruption and inflation maintain long-run relations and short-run dynamics in a panel of 30 countries at different development levels in a corruption perception index for the period 1996–2017, and they arrive at the conclusion that control of the corruption and inflation rates has long-run equilibrium consequences for the panel, and there is long-run as well as short-run causality observed from corruption to inflation.

Research Gap

The existing literature has two strands of coverage: (1) some studies have purely focused on the effects of fiscal or monetary policies upon the inflationary levels in the countries, groups and regions; (2) there are some studies that covered up the impacts of good governance factors, mainly the corruption factor, upon inflation in countries and groups. However, no study so far has addressed the effect of fiscal and monetary policy effects combined with good governance factors, corruption, upon inflation. Unlike earlier studies, this study aims to fill the gap by investigating how fiscal policy and monetary policy, combined with corruption activities, the interaction effects, have relationships with the inflation levels of the selected developed and developing countries.

Materials and Methods

Theoretical Underpinning and Empirical Methodology

From the theories it is clear that, inflation rate (I) (the increase in the general price level, i.e. dP/P>0, where P is the general price level) can be determined by, among other less relevant factors, the fiscal component (G), monetary component (M), governance component (CC, the control of corruption). Thus,

$${\rm{d}}P/P = I= f(G, M, CC)$$

$${\rm{d}}P/P = I= f(G, M, CC)$$

where dI/dG > 0, dI/dM > 0 and dI/dCC > 0. As mentioned in the introduction, that government spends in two head, capital expenditure, the asset creating and liability reducing expenditure component, and revenue expenditure, the recurring public spending which are non-asset creating and liability increasing. Capital expenditure is long-term expenditure while revenue expenditure is short-term expenditure. In both the head of expenditures, corruption activities might be associated but the association of corruption might be intensified in the case of the revenue expenditure. So, these two expenditures should have interactions with the control of corruption. As developed countries have relatively low government participation in economic activities compared with the developing countries, the issue of corruption associated with fiscal and monetary policies is relatively more pertinent in the case of the latter. After separating G into capital expenditure (Capex) and revenue expenditure (Revex), the inflation generating function is transformed into

$${{I = f}}({{Capex}},{{Revex}},{{M}},{{CC}})$$

$${{I = f}}({{Capex}},{{Revex}},{{M}},{{CC}})$$

For the empirical analysis, two models, Model I and II, are considered depending upon the theoretical literature (such as Barro Reference Barro1995, Das and Mandal Reference Das and Mandal2022, etc) as well as the theoretical underpinning developed above (equations (1) and (2)).

Model I: Cointegration involving inflation (I), money supply (M), government expenditure (G) and control of corruption (CC)

The model to be estimated for the three separate panels is

$${I_{t,i}} = {\rm{ }}{\beta _{0i}} + {\rm{ }}{\beta _{1i}}^{*}{I_{t - i}} + {\rm{ }}{\beta _{2i}}^{*}{M_{t - i}} + {\rm{ }}{\beta _{3i}}^{*}{G_{t - i}} + {\rm{ }}{\beta _{4i}}^{*}C{C_{t - i}} + {\rm{ }}{u_{ti}}$$

$${I_{t,i}} = {\rm{ }}{\beta _{0i}} + {\rm{ }}{\beta _{1i}}^{*}{I_{t - i}} + {\rm{ }}{\beta _{2i}}^{*}{M_{t - i}} + {\rm{ }}{\beta _{3i}}^{*}{G_{t - i}} + {\rm{ }}{\beta _{4i}}^{*}C{C_{t - i}} + {\rm{ }}{u_{ti}}$$

Model II: Cointegration involving inflation (I), money supply (M) and interactions of capital expenditure with corruption (Capexcorr) and revenue expenditure of the government with corruption (Revexcorr)

The model to be estimated for the three separate panels is

$${I_{t,i}} = {\rm{ }}{\beta _{0i}} + {\rm{ }}{\beta _{1i}}^{*}{I_{t - i}} + {\rm{ }}{\beta _{2i}}^{*}{\rm{ }}{M_{t - i}} + {\rm{ }}{\beta _{3i}}^{*}{\rm{ }}Capexcor{r_{t - i}} + {\rm{ }}{\beta _{4i}}^{*}Revexcor{r_{t - i}} + {\rm{ }}{u_{ti}}$$

$${I_{t,i}} = {\rm{ }}{\beta _{0i}} + {\rm{ }}{\beta _{1i}}^{*}{I_{t - i}} + {\rm{ }}{\beta _{2i}}^{*}{\rm{ }}{M_{t - i}} + {\rm{ }}{\beta _{3i}}^{*}{\rm{ }}Capexcor{r_{t - i}} + {\rm{ }}{\beta _{4i}}^{*}Revexcor{r_{t - i}} + {\rm{ }}{u_{ti}}$$

The VAR Model for Model I

$${I_t} = {\rm{ }}{\alpha _1} + {\rm{ }}\sum\limits_{j=1}^{n} {{\beta _{1j}}{I_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\gamma _{1j}}{M_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^{n} {{\delta _{1j}}{G_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^{n} {{\theta _{1j}}C{C_{t - j}}} + {u_{1t}}$$

$${I_t} = {\rm{ }}{\alpha _1} + {\rm{ }}\sum\limits_{j=1}^{n} {{\beta _{1j}}{I_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\gamma _{1j}}{M_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^{n} {{\delta _{1j}}{G_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^{n} {{\theta _{1j}}C{C_{t - j}}} + {u_{1t}}$$

For Model II

$${I_t} = {\rm{ }}{\alpha _1} + {\rm{ }}\sum\limits_{j = 1}^n {{\beta _{1j}}{I_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\gamma _{1j}}{M_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\delta _{1j}}Capexcor{r_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\theta _{1j}}Revexcor{r_{t - j}}} + {v_{1t}}$$

$${I_t} = {\rm{ }}{\alpha _1} + {\rm{ }}\sum\limits_{j = 1}^n {{\beta _{1j}}{I_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\gamma _{1j}}{M_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\delta _{1j}}Capexcor{r_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\theta _{1j}}Revexcor{r_{t - j}}} + {v_{1t}}$$

ECM for Model I

$$\eqalign{\Delta {I_t} = {\rm{ }}& {\alpha _1} + {\rm{ }}\sum\limits_{j = 1}^n {{\beta _{1j}}\Delta {I_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\gamma _{1j}}\Delta {M_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\delta _{1j}}\Delta {G_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\theta _{1j}}\Delta C{C_{t - j}}} \cr & + \sum\limits_{j = 1}^n {{\eta _{1j}}{e_{t - j}}} + {\omega _{1t}}}$$

$$\eqalign{\Delta {I_t} = {\rm{ }}& {\alpha _1} + {\rm{ }}\sum\limits_{j = 1}^n {{\beta _{1j}}\Delta {I_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\gamma _{1j}}\Delta {M_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\delta _{1j}}\Delta {G_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\theta _{1j}}\Delta C{C_{t - j}}} \cr & + \sum\limits_{j = 1}^n {{\eta _{1j}}{e_{t - j}}} + {\omega _{1t}}}$$

For Model II

$$\eqalign{\Delta {I_t} = {\rm{ }}& {\alpha _1} + {\rm{ }}\sum\limits_{j = 1}^n {{\beta _{1j}}\Delta {I_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\gamma _{1j}}\Delta {M_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\delta _{1j}}\Delta Capexcor{r_{t - j}}} \cr & + {\rm{ }}\sum\limits_{j = 1}^n {{\theta _{1j}}\Delta Revexcor{r_{t - j}}} + \sum\limits_{j = 1}^n {{\eta _{1j}}{e_{t - j}}} + {\varepsilon _{1t}}}$$

$$\eqalign{\Delta {I_t} = {\rm{ }}& {\alpha _1} + {\rm{ }}\sum\limits_{j = 1}^n {{\beta _{1j}}\Delta {I_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\gamma _{1j}}\Delta {M_{t - j}}} + {\rm{ }}\sum\limits_{j = 1}^n {{\delta _{1j}}\Delta Capexcor{r_{t - j}}} \cr & + {\rm{ }}\sum\limits_{j = 1}^n {{\theta _{1j}}\Delta Revexcor{r_{t - j}}} + \sum\limits_{j = 1}^n {{\eta _{1j}}{e_{t - j}}} + {\varepsilon _{1t}}}$$

For an empirical exercise, first the panel unit root tests in the lines of Levin et al. (Reference Levin, Lin and James Chu2002) and Im et al. (Reference Im, Pesaran and Shin2003) are carried out, then a panel cointegration test follows, after checking the cross-sectional dependence test. Pedroni (Reference Pedroni2004) and Fisher-Johansen tests are used for the purpose. After that, the VECM is exercised to find short-run dynamics and the Wald test is carried out to get short-run causal interplays among the variables in the two models. The Histogram-LM test is done for robustness checking.

Data Descriptions

The study uses six indicators, which are inflation rate (the consumers’ price index, I), public spending (G), broad money supply (M), control of corruption (CC), interactions of capital expenditure with corruption (Capexcorr) and interactions of revenue expenditure of the government with corruption (Revexcorr) for the period 1996–2020. The principal sources of data for all level variables (the first four) are taken from the World Bank (www.worldbank.org). Using aggregate data, the data on capital and revenue expenditures are derived. Further, the magnitudes of CC of the countries are multiplied with their capital expenditures and revenue expenditures to derive the interaction variables, Capexcorr and Revexcorr.

Results and Discussion

Descriptive Statistics and Correlations

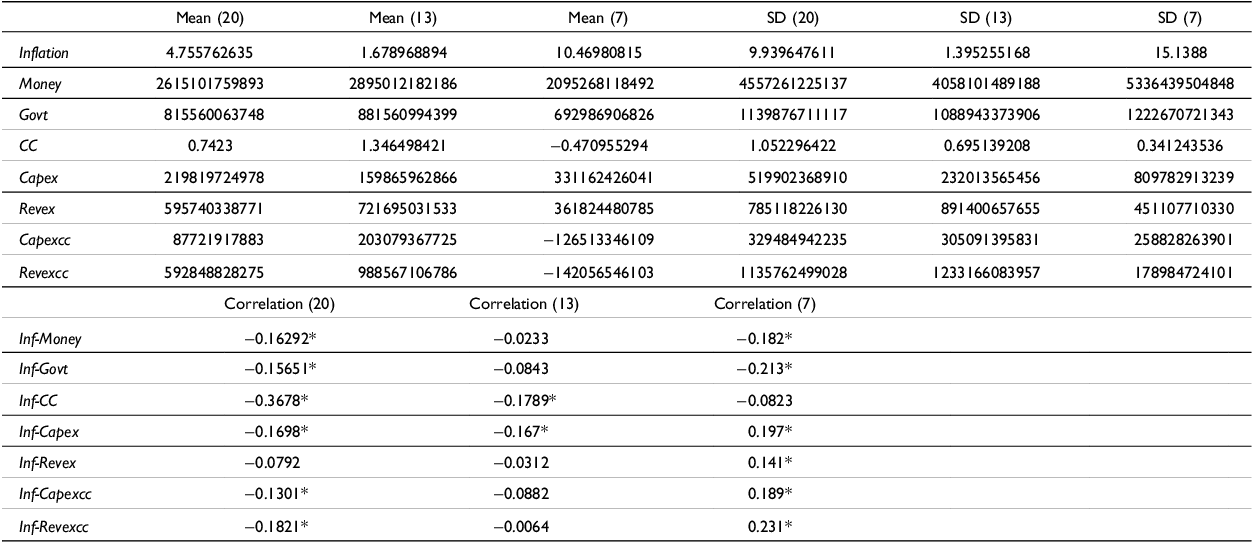

Before entering into the rigorous time series econometric analysis on the associated objectives, this study views the basic form of the data on the indicators through descriptive statistics such as mean and standard deviations in the three different panel data sets for a total of 20 countries: for 13 developed countries and seven developing countries. In addition, the study performs a correlation analysis of the pairs of the indicators, involving inflation in one side and on the other fiscal, monetary, and institutional components (see Table 1).

Descriptive statistics and correlation coefficients

Note: * indicates significant results at 5% level.

Source: Author’s own computations.

The study observes that the average values of supply of money and government expenditure in the panel of the developed economies (13) are larger than that of the panel of the developing economies (7). Alternatively, the average standard of the institution as measured by the magnitudes of control of corruption is better in the panel of the developed economies (1.3465) compared with that of the panel of the developing countries (–0.4709). The outcomes of these fiscal, monetary and institutional components probably fall in relation to the magnitude of inflation, as the average magnitude of inflation – as measured by CPI – is lower in the case of the developed economies (1.678) compared with the developing countries (10.469). Again, the magnitudes of fluctuations of the indicators as measured by the SD values are greater in the case of the developing countries as compared with the developed countries.

The correlation results show some interesting facts. The inflation trend is downward in the panel of all types of countries, while that trends of the supply of money and government expenditure are rising, and that of the CC is rising. The negative and significant correlation of inflation with money supply and government expenditure is observed in all types of panels, which seems unusual and forces us to identify of other indicators associated with inflation. The negative and significant correlation between inflation and CC becomes a good explanation of why inflation is decreasing. As CC has good scores over time (having rising trends in most countries) the downward trend of inflation may then be justifiable. Whenever we segregate government expenditure into capital and revenue expenditures, the results get changed in different panels. Similar types of negative and significant correlations are observed in the total and developed countries’ panels between inflation and capital expenditure. However, the results depict an affirmative association between inflation and capital as well as revenue expenditures in the case of the developing countries, which means increasing inflation rates are directly associated with increasing amounts of capital and revenue expenditures in these countries, leading us to believe that these two types of expenditures may be the factors behind their inflation scenarios. Further, as the interaction terms of corruption with the two types of government expenditures are considered, similar positive correlation results are detected in the case of the panel of the developing economies while no such significant associations are observed in the case of the panel of the developed economies, while the negative and significant associations are observed in the case of the total panel. The results influence us to consider money, different types of public expenditures and their corruption interactions to be the factors behind inflation.

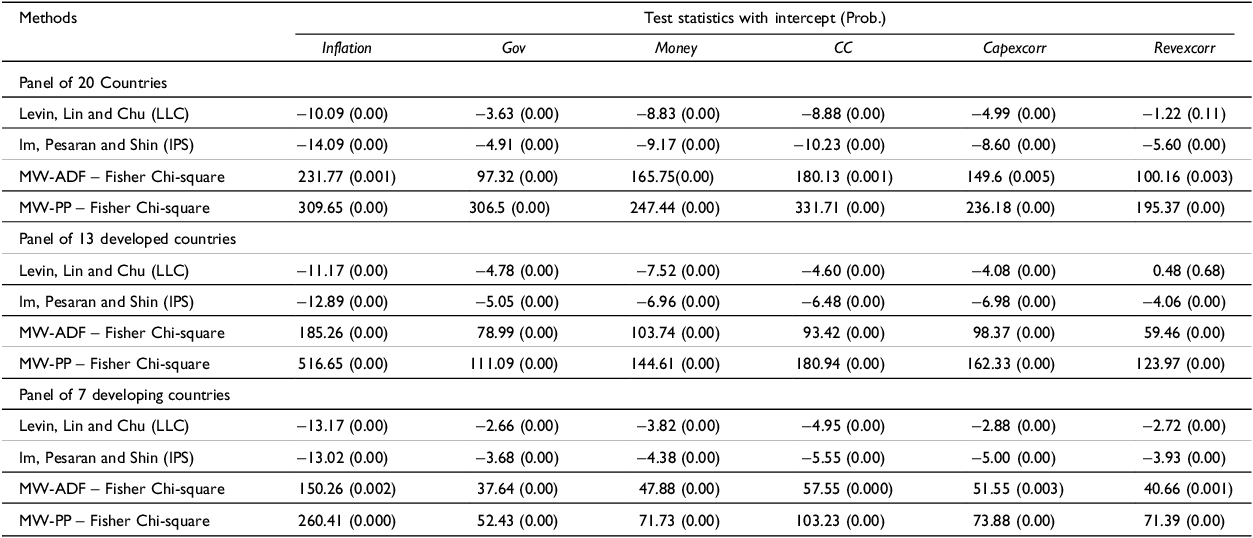

Panel Unit Root Test Results

The exercises for cointegration or long-run associations between the selected determinants require the concerned time series to be stationary at levels or first differences. The related tests for unit root for the different panels following the standard test techniques, LLC, IPS, MW-ADF-Fisher and MW-PP-Fisher, are done and the outcomes for first difference tests are given in Table 2. All the level values of the series are not stationary and so their outcomes are not shown in the table to avoid issues of space.

Results of unit root tests for the selected six indicators in different panels

Note: Selection of automatic lag length is based on AIC: 1 to 4. The LLC tests are for the unit roots for the common unit root process whereas IPS, MW-ADF–Fisher and MW-PP–Fisher tests are for the individual unit root process.

Source: Author’s calculations.

It is detected that the series of the first differences are stationary, with the specification of ‘with intercepts’, for all the test statistics as all the probabilities are far below the value of 0.01, that is highly able of refusing the hypothesis of panel unit roots process for all the three separate panels. Hence, the application of cointegration technique among the series in the three panels is appropriate without any loss of generality.

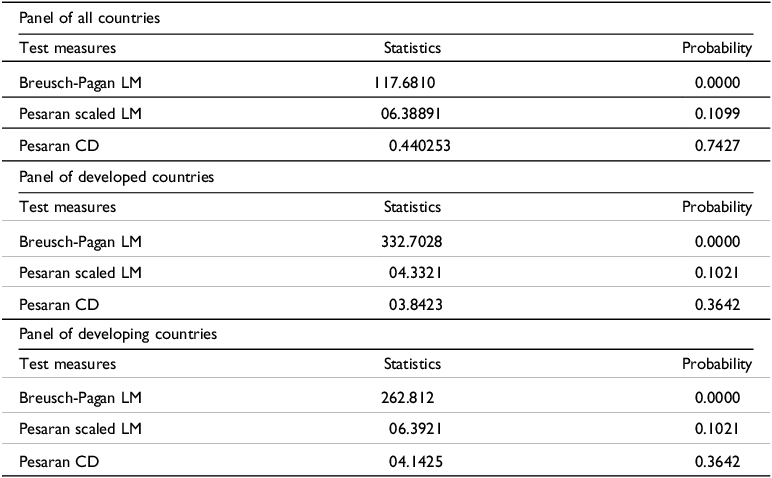

Tests for Cross-sectional Dependence Among the Countries

The upshots from the LM tests of Breusch and Pagan (Reference Breusch and Pagan1980) and Pesaran (Reference Pesaran2004, Reference Pesaran2007) are displayed in Table 3. The statistics of Pesaran’s scaled LM and cross-sectional dependence tests are not statistically significant (p > 0.10), while the Breusch-Pagan LM statistic is significant (p < 0.01).

Findings of residual cross-sectional dependence test

Source: Author’s calculations.

Thus, considering most of the findings, the study concludes that there is no cross-sectional dependence between the concerned indicators as per the considered models among the three panels of countries under study, in the heterogeneous panel data. Thus, the study conducted the first-generation panel unit root, cointegration and causality tests methods as follows.

Cointegration Test Results for the Panels

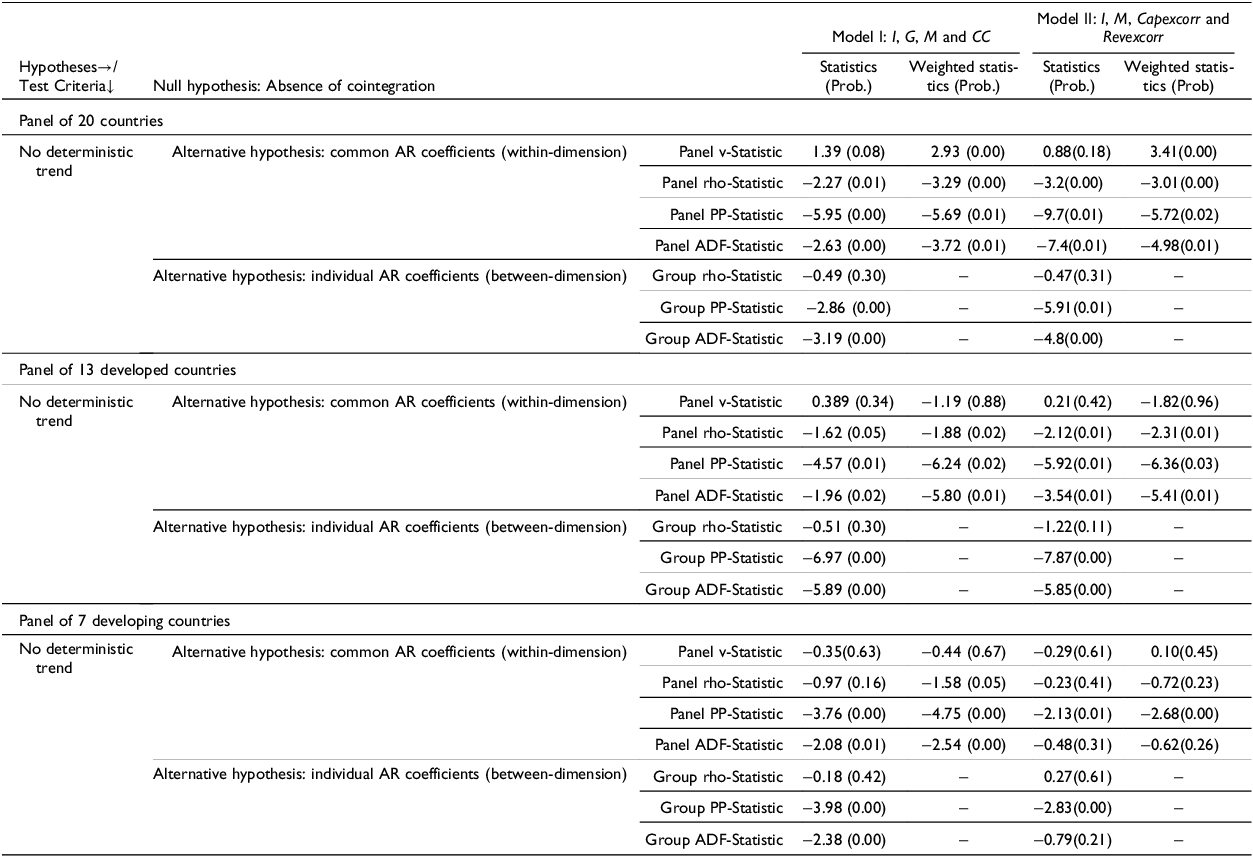

Pedroni’s residual and Fisher-Johansen’s eigen-value based cointegration tests are carried out. The Kao test is not attempted as the set of variables and time length generate singular matrices. Table 4 presents the test results under Pedroni for three stipulations following Model I and Model II as stated in the methodology part. The indicators contained in Model I are I, G, M and CC, and that in Model II are I, M, Capexcorr and Revexcorr.

Results of Pedroni test for inflation, government expenditure, money supply and CC

Note: The figures indicating probability (in parentheses) with a value less than or equal to 0.05 indicate the outcomes of significance relation.

Source: Author’s own calculations.

The results in Table 4 show that the indicators in both models are cointegrated. This means, inflation, money, government expenditure and control of corruption maintain long-run relations for all the three sets of panels for Model I. After replacing government expenditure with the interaction terms of capital and revenue expenditures with control of corruption, Model II, a significant cointegrating result is detected in all three panels of the countries. Therefore, inflation rates of the countries maintain similar natures with the series for money supply, government expenditure and control of corruption as far as the Pedroni test is concerned.

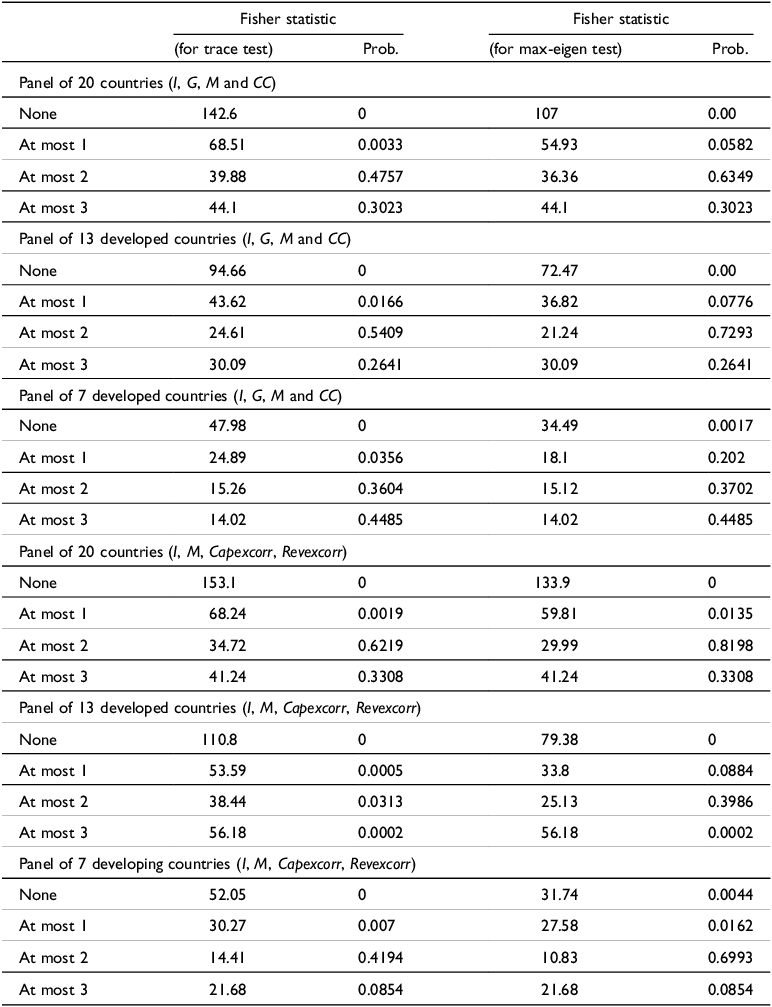

Table 5 presents the outcomes of the Fisher-Johansen test of cointegration for Models I and II. The results demonstrate the existence of the cointegrating relations (cointegrating vectors) between inflation rate money supply, government expenditure and control of corruption in the panel of countries.

Fisher-Johansen cointegration test results for inflation, government expenditure, money supply and CC

Source: Author’s calculations.

The experimented results reveal that the set of variables covered under both the models is cointegrated in all the separate panels of the countries, with no less than one cointegrating equation among the concerned variables. Combining all the outcomes of cointegration (Tables 4 and 5), it can be seen that, in an overall sense, the series for inflation rate, money supply, government expenditure and control of corruption in the three separate panels are cointegrated and they have equilibrium or a long-run relation. Thus, inflation rates in the countries are determined by the combinations of fiscal policy, monetary policy and governance policy.

VECM Test Results

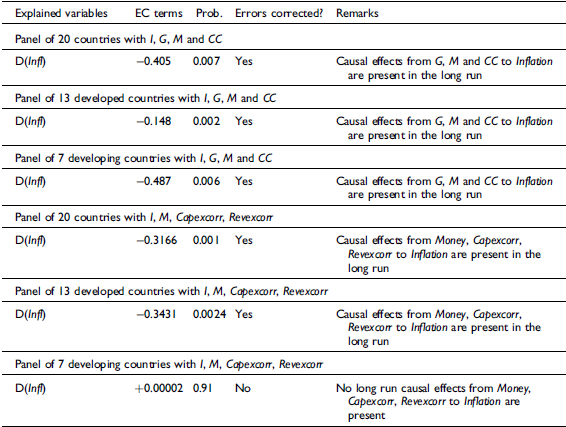

The prevalence of long-run relationships among the selected fiscal, monetary and governance policy variables (through Models I and II) do not necessary mean that the errors around such relationships are not present there. If they are present. then the question is whether they get corrected or not to establish stable long-run relations. These questions are to be answered through the analysis for the short-run dynamics in a VAR model using the VECM. The optimum lag is 3 using standard measures. The VECM results (using equations (7) and (8)) are given in Table 6 with the endogenous variables for all three separate panels. As the system provides the results for all the variables acting as the endogenous dependent variables, the table presents the results for those where first difference values of inflation rate are considered as the dependent endogenous variable since the aim of the study is to find out whether fiscal policy, monetary policy and governance policy aspects are accountable for explaining the former. The study did not present the reverse causality results to capture the issue of endogeneity as the primary objective is to analyse the policy effects coupled with corruption upon the inflation level.

VECM test outputs for all the selected variables

Note: Optimum lag is calculated to be 3. EC means error correction.

Source: Author’s calculations.

The results reveal significant error corrections in Model I when inflation is the dependent endogenous variable in all three panels. The error correction terms of the model are negative in sign with probability well below 0.05. Any deviation from the equilibrium relation is brought back to the equilibrium, making the error temporary in nature. Moreover, the results depict long-run causality from the money supply, government expenditure and control of corruption to the inflation rates. In contrast, when the study considers the VECM results for Model II then it is observed that significant error corrections are found in the case of the total panel and that of the developed countries, making a meaningful causal influence for the long run from money supply and interaction terms of CC and capital and revenue expenditures to inflation rates. But the study does not observe any such error correction or long-run causality results in the case of the panel of the developing economies as the EC term is positive.

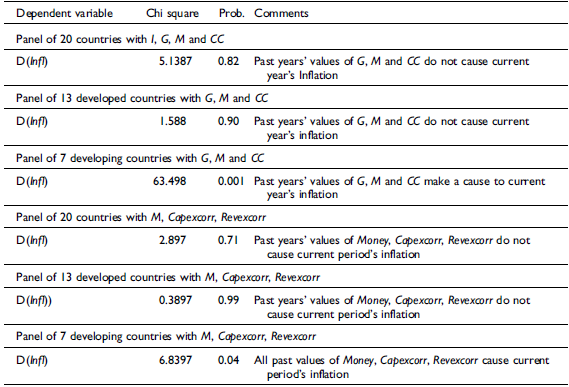

The short-run causality results under inflation being the dependent variable in Modes I and II, in line with the Wald test (Table 7), reveal an interesting contrast to the long-run causality results as explained under the VECM structure. There is no causal influence from government expenditure, money supply and corruption to inflation in Model I, in the case of the panel of all countries and all the countries from the developed group, but inflation being caused by the said exogenous variables in the case of the developing countries’ panel. Again, as the study considers the interaction terms of control of corruption with the revenue and capital expenditures as stipulated in Model II, it is still observed that inflation is caused by capital and revenue expenditures with money supply in the case of the developing countries’ panel only, unlike that of the developed and all countries’ panels.

Results of causal interplay through Wald test

Source: Author’s calculations.

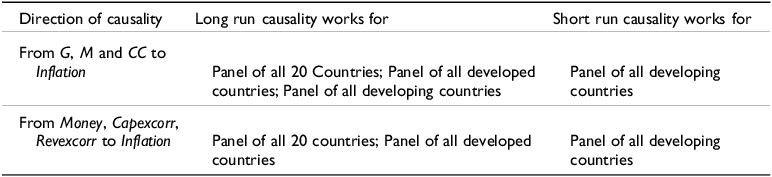

Table 8 gives a summary of the significant causality results for the long run and the short run. Comparing the long-run and short-run causality results, it is evident that capital and revenue expenditures of the developed countries led to improvements in the economic and social capital on a long-term basis, leading to low inflation (as the average value of inflation for the countries in the panel is low compared with that of the panel of the developing countries – refer to the descriptive statistics as reported in Table 1) through more supplies of outputs, while, in case of the developing countries, such causal influence works in the short run in the way that the corruption factor combined with relatively low economic and social capital formation leads to lower supply outcomes and high inflation.

Significant causality results for long run and short run

Source: Author’s calculations.

Therefore, fiscal, monetary and governance policy variables are accountable to inflationary situations in both the short run and long run respectively, depending upon the panels of developing and developed countries. Hence, the theory of inflation or price determination in the mainstream macroeconomics should be reconstructed in order to accommodate factors such as corruption capital expenditure and revenue expenditure.

The computed research outcomes are scrutinized through diagnostic checking by a histogram normality test as mentioned in the methodology section. The statistic used for the test, as stated, is Jarque-Bera. The results are depicted in Table 9.

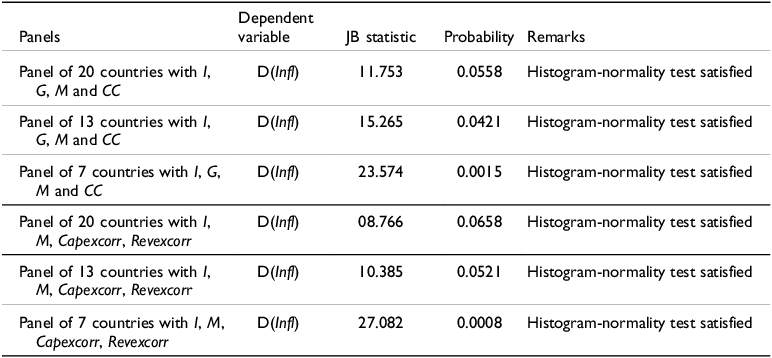

Histogram-normality test

Source: Author’s calculations.

It is seen that the J-B statistic carries a very large value with low probability, which is able to reject the presence of normal distribution of the residuals. Therefore, the research outcomes are statistically robust. Thus, it is confirmed that monetary, fiscal and governance (institutional) factors are accountable to the determination of inflation in all sorts of countries in the long run, but for the short run, the presence of revenue and capital expenditures has led to the influence of inflation in developing countries, which involves relatively poor levels of good governance in terms of high levels of corruption.

Scientific Contribution of the Study

The existing literature has focused on the effects of fiscal or monetary policies upon the inflationary levels in the countries, groups and regions, on the one hand, and the impacts of good governance factors, mainly the corruption factor, upon inflation in the countries and groups, on the other. However, no study has so far addressed the fiscal and monetary policy effects combined with good governance factors, corruption, upon inflation. In contrast to the earlier studies, this study contributes to the existing literature by investigating how fiscal policy and monetary policy, combined with corruption activities, the interaction effects, affect the inflation levels of the selected developed and developing countries. The results show the role of such interaction effects upon inflation in the panel of the countries as analysed.

Conclusion

This study aimed to explore, empirically, whether the inflation rate has long-term relationships with the fiscal components (public spending), monetary components (money supply) and governance components (corruption attitudes) in developed and developing countries for the period 1996–2020. The study has tracked two separate models, where Model I involves inflation, money supply, government expenditure and control of corruption, and Model II involves inflation, money supply and interactions of capital expenditure with corruption and revenue expenditure of the government with corruption. Using the panel unit roots test, the appropriate panel cointegration test, following VECM, and the Wald test, the study obtains for both Models I and II that the series for inflation rate, supply of money, government expenditure and control of corruption in the three separate panels are cointegrated, and so they maintain equilibrium or a long-run relation. Thus, inflation rates in the countries are dependent upon the combinations of fiscal policy, monetary policy and governance policy. The interactions of capital and revenue expenditures with corruption along with the monetary component in the developing countries maintain long-run relationships and short-run causal interplay with inflation rates in the panel of these countries.

Policy Recommendations

As a good governance indicator, the control of corruption has significant interaction effects with capital and revenue expenditures in the countries of the total panel and that of the panel of the developing countries in particular, to justify inflation. The following policies are recommended:

-

The governments in the developing countries in particular, and all the countries in general, should maintain good institutional supports through good governance practices to mitigate corruption issues to maintain price stability in the countries.

-

The revenue expenditure is to be controlled to reduce corruption.

-

Proper vigilance and necessary measures are to be framed for controlling corruption.

-

Capital expenditures are to be managed and controlled by proper auditing processes.

-

Fund allotments in all the head are to be made in a phase-wise manner.

Ways of Executing Policies to Control Inflation for the Developing Countries

The governments in the developing countries should consider the following policies to control corruption as well as inflation:

-

strengthen anti-corruption laws,

-

promote transparency in resource allocation,

-

enhance digital financial systems,

-

foster citizen participation and accountability through technology and education,

-

implement reforms that reduce red tape, empower independent institutions, and ensure robust financial oversight that can curb illicit activities,

-

improve service delivery and stabilizing the economy.

Limitations of the Study

Despite some good results, the study still has some limitations.

-

The sample of countries could be increased in all levels to have better and robust outcomes.

-

The case of endogeneity is not considered, which means the causal influence from inflation to the policy variables and the interaction terms are not considered.

-

The estimation of the effects of different policies and the interaction terms could be done using GMM.

-

Total time length could be divided into two periods, say pre- and post-financial crisis phases, to find better policy outcomes.

Data Availability Statement

The author has used the database of the World Bank on the related indicators on government’s expenditure, money supply, control of corruption and rate of inflation for the selected countries. The data are available freely from www.worldbankindicators.org. If any raw data are required the author can share, although they are openly available.

Disclosure Statements

It is declared that the author did not use any animal or human being in the work and did not have any conflict of interest while developing the manuscript. Further, it is declared that the author did not possess any funding source to give financial support for this work.

Ramesh Chandra Das, PhD, is a professor at the Department of Economics of Vidyasagar University, India, with more than 25 years of teaching and research experience in the fields of applied macroeconomics, environmental economics and political economics. He has around 200 publications with internationally reputed publishing companies.

Open access

Open access