2.1 Introduction

As the idea that society’s long-term prosperity requires replacing the extractive shareholder value model with a participative stakeholder approach that ensures the sustainable creation of shared value gains momentum, efforts to reimagine the business corporation are underway (Morrow et al. Reference Morrow, Gregor and Veldman2016; British Academy 2019; Alvarez et al. Reference Alvarez, Zander, Barney and Afuah2020; Mayer Reference Mayer2021; Meyer et al. Reference Meyer, Leixnering and Veldman2022). In this context, Simon Deakin (Reference Deakin2012a, Reference Deakin, Clarke, O’Brien and O’Kelley2019) has suggested that valuable insights can be found in Elinor Ostrom’s (Reference Ostrom1990, Reference Ostrom2005) work on natural resource management. If we think of the corporation not as shareholders’ property but rather as a commons – as a shared but depletable resource which is collectively held and managed for the benefit of multiple interests – then the participative stakeholder model ought to follow.

Deakin’s argument rests on two moves. First, Deakin shows that the legal system sees the firm as an organizational entity constituted around a pool of shared resources, which it seeks to preserve. Hence, the bodies of law shaping and regulating the economic operations of the firm (corporate law, employment law, commercial law, insolvency law, and so on) specify the conditions under which various stakeholders contribute to and draw on the firm’s resources, while maintaining the firm’s asset pool and going concern value. The partially overlapping rights stakeholders hold in the corporate context, Deakin argues, are analogous to the partially overlapping combinations of property rights (access, withdrawal, management, exclusion, alienation) various actors hold in natural commons (Schlager and Ostrom Reference Schlager and Ostrom1992).

Deakin then transposes Ostrom’s design principles for the sustainable governance of common-pool resources from the natural resource to the corporate context. For Deakin, this implies that boards ought to be accountable to all stakeholders and that stakeholders ought to be involved in crafting the rules that govern them. And for such self-governance to be sustainable, governance norms limiting the excessive extraction of resources by one stakeholder group (most notably shareholders) and relative immunity from global capital market pressures are required. There is more to Deakin’s discussion, but for our present purposes, this outline of the argument will suffice.

We welcome Deakin’s invitation to extend the Ostromian perspective to the firm and seek to advance it in this chapter. But we do not go about it in the same way. While the design principles may well be generalizable beyond the natural resource context (Wilson et al. Reference Sloan Wilson, Ostrom and Cox2013), we should not expect them to be transposable by intuitive analogy, without qualifications. Any design principles applicable to corporations or other types of business firms must be established empirically. A meta-analysis of a wide range of case studies is needed (Poteete et al. Reference Poteete, Janssen and Ostrom2010; Cole Reference Cole, Frischmann, Madison and Strandburg2014). We do not pursue this sort of worthwhile analysis here.

Nor do we take the property rights route with a view to weighing in on the corporate governance debate. The analogy between the rights of corporate stakeholders and those held by users in natural commons is not a sufficient justification for the stakeholder governance model. Not all those with ownership claims have ownership competence – the ability to match judgment about resource uses and governance with the firm’s evolving environment under uncertainty (Foss et al. Reference Foss, Klein, Lien, Zellweger and Zenger2020). In any case, the property rights route is complicated by the fact that many of the firm’s key resources are not appropriable. Some are even shared with other firms (Aoki Reference Aoki2010).

We propose that, to take the corporation-as-commons idea forward, we need to think about the kinds of shared resources firms rely on or manage and ask whether it makes sense to view the corporation as such a resource. If we take commons to be a kind of institutional arrangement enabling community governance of shared resources (Frischmann et al. Reference Frischmann, Madison and Strandburg2014; McGinnis Reference McGinnis, Hudson, Rosenbloom and Cole2019) – which need not be common-pool resources – the challenge is to specify what we mean by corporation in this context. We also need to determine who shares the corporation and identify the rules and practices that enable its provision, production, and reproduction in relevant action arenas. This chapter is an attempt to chart this course.

Drawing on insights from the literature on the firm, we conceptualize firms as systems of shared heterogeneous resources and argue that the firm’s most critical resource is what we call its corporate mask.Footnote 1 The corporate mask is a special kind of institutional resource that exhibits infrastructural and intellectual features, which the Governing Knowledge Commons (GKC) framework (Ostrom and Hess Reference Ostrom, Hess, Hess and Ostrom2007; Madison et al. Reference Madison, Frischmann and Strandburg2010, Reference Madison, Frischmann, Strandburg, Hudson, Rosenbloom and Cole2019; Frischmann et al. Reference Frischmann, Madison and Strandburg2014) is well-suited to study. Its provision by the legal system enables the firm’s members to operate as a singular actor in the legal and commercial spheres (Gindis Reference Gindis2016). This helps address collective action problems, reduces transaction costs, and unlocks an important source of economies of scale and scope.

The corporate mask, however, is not merely a legal construct – the social recognition of the firm as a corporate actor, a reliable business partner, a reputable producer of goods or services, and so on, matters a great deal as well. The corporate mask is a legal and epistemic focal point (McAdams 2015) shared by insiders and third parties with whom the firm contracts and more generally interacts in a network of adjacent action situations (McGinnis Reference McGinnis2011a), ranging from commercial negotiation to enforcement and dispute resolution in the courts or some other relevant forum. The boundaries of the communities that govern its production and reproduction are open and evolve with the firm’s activities.

2.2 Firms and Corporate Masks

Ostrom frequently sought to remind us that commons are neither relics nor confined to nature but can instead be found all around us today. Ostrom listed corporate treasuries and income as examples of common-pool resources (Ostrom Reference Ostrom and Newman1998), and noted that a corporation, though frequently thought of as the epitome of private property, was in fact an example of a common property regime featuring a mix of commonly and individually held property rights (Ostrom Reference Ostrom, Bouckaert and Geest2000).Footnote 2 Fundamentally, Ostrom (Reference Ostrom1990) observed, the firm is one institutional arrangement among others that addresses the problem of independent action in situations of interdependence. These limited statements require clarification and elaboration.

Though limited, these observations echo Ostrom’s recurring insistence on the need to distinguish resources (or resource systems) from the institutional regimes that govern them. Any Ostromian perspective on the question at hand must differentiate these aspects. Conceptual and terminological clarity was of paramount importance to Ostrom (Cole Reference Cole, Frischmann, Madison and Strandburg2014), so we should seek to emulate this stance here. But while a suitably Ostromian point of departure would be to think of firms as resource systems and corporations as institutional artifacts that enable their governance, this distinction, which works for natural resources that can exist independently of any institutional regime, breaks down for resource systems that only really come into existence thanks to the institutional regime. Firms are examples of the latter kind. Let us, nevertheless, first examine the idea of the firm as a resource system. A wealth of insights can be found in economics, management, and organization studies. We summarize these in the next two sections, before introducing the concept of the corporate mask.

2.2.1 Thinking about the Firm

The contractual theory of the firm builds on Ronald Coase’s (Reference Coase1937) suggestion that the firm emerges when it can economize on the transaction costs of organizing production relative to the market. This is the case when resource owners choose to contract with a central agent – an entrepreneur – instead of contracting with each other, as would be necessary if production were organized exclusively through bilateral exchanges (Eggertsson Reference Eggertsson1990). The intrafirm cost of organizing production is further reduced because long-term authority- or fiat-based relationships (between the entrepreneur-employer and employees) are open-ended and do not require frequent renegotiations. These institutional features of the firm help resource owners create a greater joint surplus value than would have otherwise been possible.

While some resources used by the firm can earn just as much elsewhere, the value of others is enhanced through firm-specific investments, with the implication that they have a significantly higher value within the firm than outside it. Realizing the potential value of such resources sometimes requires mutually compatible specialization among the participants (Alchian Reference Alchian1984). But firm-specific investments are at risk because opportunistic participants can credibly threaten to withdraw their cooperation, with a view to capturing a greater share of surplus (Klein et al. Reference Klein, Crawford and Alchian1978). Anticipating this hold-up risk, participants will tend to underinvest, such that at least some potential value will be foregone. Various kinds of institutional arrangements – ranging from monitoring to contractual incentives and career rewards – are needed to reduce the likelihood of this outcome (Rubin Reference Rubin1990).

The logic extends to interfirm supplier-buyer relationships, where one or both firms need to make relationship-specific investments: Each firm can use the threat of exit to extract a greater share of the surplus. Since both firms are likely to underinvest, institutional arrangements – ranging from contractual specifications of penalties to joint ventures and vertical integration – are needed (Williamson Reference Williamson1985).Footnote 3 The greater the value of a firm’s specific investments, the more it stands to lose from the opportunistic behavior of its partner, and, therefore, the greater the likelihood that it will choose to eliminate the threat by buying out the other firm (Hart Reference Hart1995). Expanding the firm’s boundaries by turning outside parties into employees mutes their incentives to behave opportunistically, but does not eliminate opportunism, and free-riding and other collective action problems remain (Miller Reference Miller1992).

A distinct though somewhat complementary explanation of how and why firms grow can be found in the resource dependence approach proposed by Jeffrey Pfeffer and Gerald Salancik (Reference Pfeffer and Salancik1978). In this view, given that some key resources the firm requires to fulfill its strategic objectives are not tied to or controlled by it, the firm will try to manage external resource dependencies – through mergers, joint ventures, or board interlocks, as well as through various forms of political or legal action (Hillman et al. Reference Hillman, Withers and Collins2009). By securing at least some control over external resources, firms both diminish their exposure to the power of other organizations and reduce environmental uncertainty. This insight is found across a broad range of literatures: The importance of access to external resources for the creation of value by firms is well understood (Aoki Reference Aoki2010; Mayer Reference Mayer2020; Berti and Pitelis Reference Berti and Pitelis2022), as is the idea that not having the right kinds of resources at the right time can significantly hurt a firm’s competitive prospects (Langlois Reference Langlois1992).

The focus on links between competitive advantage and the growth of the firm is the hallmark of the resource-based view. Stemming from Edith Penrose (Reference Penrose1959), this approach revolves around the idea that the firm’s productive resources are heterogeneous and must be specialized, combined, arranged, and organized by entrepreneurs or managers seeking to generate a surplus by selling a good or service that creates value for third parties in the market (Barney Reference Barney1991).Footnote 4 The ability to reconfigure internal and external resources in rapidly changing environments matters (Teece et al. Reference Teece, Pisano and Shuen1997). Novel resource combinations lead to innovation (Galunic and Rodan Reference Galunic and Rodan1998), while excess capacity may lead to diversification and firm growth. Diversified or multiproduct firms benefit from economies of scope, as David Teece (Reference Teece1982) showed, when they are able to share some resources across production processes or businesses without congestion. Various kinds of governance arrangements – ranging from the sequentialization of production to the divisionalization of the firm – are needed to minimize the incidence of this collective action problem (Teece Reference Teece1980).

We can retain five points from this brief survey of extant thinking about the firm. First, firms and markets are alternative institutional settings within which the transactions enabling the organization of production are negotiated and executed. Second, when resource owners come together in firms, the resulting institutional structure is characterized by the presence of a central contractual agent. Third, firm-specific investments can enhance the value of the firm’s heterogeneous resources, at least some of which need to be shared to make the most of economies of scope. Fourth, some of the resources firms need to create value for both participants and third parties in the market lie beyond their boundaries. Finally, given the range of inevitable collective action problems, firms can only succeed (and perhaps even thrive) if they evolve adequate governance arrangements.

2.2.2 The Firm’s Shared Resources

Firms rely on a range of shared resources. Whether tangible or intangible, specialized or not, a shared resource is effectively a common input into two or more production processes (Teece Reference Teece1980, Reference Teece1982). Some production processes require shared tangible resources, such as IT networks, buildings, office space, parking, and certain machines. These resources can be more or less excludable and more or less subtractable, depending on the institutional setup (Rayamajhee and Paniagua Reference Rayamajhee and Paniagua2021). Crafting governance arrangements to prevent their exploitation, congestion, and overuse can be relatively straightforward by assigning different bundles of rights to different people, that is, distinguishing, to use Ostromian terminology, authorized users (those with access and withdrawal rights), claimants (access, withdrawal, and management rights), proprietors (access, withdrawal, management, and exclusion rights), and owners (access, withdrawal, management, exclusion, and alienation rights).

The firm’s production processes also rely on a range of shared intangible resources. This category includes software and things like legal, administrative, human resource, secretarial, procurement, or marketing services. Like many of the tangible resources listed above, services of this kind are infrastructural resources, which can be private, club, or common-pool, depending on the context (Ellig Reference Ellig2001). As they are inputs into many different intrafirm processes, they are often centralized to make the most of the economies of scale and scope. But such pooled interdependence means that they are easily congestible when demand is high (Frost and Morner Reference Frost and Morner2005). Here, too, it may be relatively easy to devise suitable rules to prevent congestion and overuse by assigning different bundles of rights to different people.

The resources discussed so far are unlikely to determine the firm’s competitive advantage, which stems from its ability to develop imperfectly imitable and non-substitutable resources to create value for third parties (Barney and Clark Reference Barney and Clark2007).Footnote 5 From this perspective, the firm’s distinctive know-how and knowledge base are vital. At the firm level, knowledge exhibits high degrees of non-excludability and non-subtractability (Frost and Morner Reference Frost and Morner2010), not least because much of it is tacit and dispersed (Spender Reference Spender1996; Foss Reference Foss1999). Pieces of knowledge are held by individuals, who must be motivated to communicate and share their ideas and skills (Cabrera and Cabrera Reference Cabrera and Cabrera2002; Osterloh and Frost Reference Osterloh, Frost, Frey and Osterloh2002; Grandori Reference Grandori, Foss and Michailova2009). The collective action problem arising from the fact that hoarding one’s knowledge may be more rational than communicating it is more likely to be overcome when individuals share group norms or a collective identity (Argote and Kane Reference Argote, Kane, Foss and Michailova2009; Camera and Hohl Reference Camera and Hohl2021).

But the imperative to forge and maintain the firm’s identity (Kogut and Zander Reference Kogut and Zander.1996) or corporate culture (Engel and Güth Reference Engel and Güth2006) is also vulnerable to collective action problems. A key governance challenge arises from the fact that it is difficult to assign specific bundles of rights to such intellectual resources. Different degrees of access to or control over artifacts and facilities representing or storing intellectual resources can be assigned to different people, but it is much more difficult to assign access to or control over knowledge or ideas themselves (Hess and Ostrom Reference Hess and Ostrom2003). Anyone who contributes to the firm’s know-how may have a property-like claim (Hess and Ostrom Reference Hess, Ostrom, Hess and Ostrom2007), but what shape an individual claim may take, and how it may relate to others’ claims, is far from obvious. It is perhaps more useful to think of these claims as held in common. Similar considerations apply to the firm’s reputation (Tadelis Reference Tadelis1999) and organizational memory (Olivera Reference Olivera2000).

The intersubjective beliefs and mental models that underpin such intellectual resources express certain values, provide meaning, and inform the organized interactions of firm participants (Cohendet and Llerena Reference Cohendet, Llerena and Becker2008; Nooteboom Reference Nooteboom2009). A firm’s identity and culture guide the participants’ productive routines (Nelson Reference Nelson, Becker and Lazaric2009; Witt Reference Witt2011) – which newcomers must learn through firm-specific investments – and are therefore constitutive of the firm’s capabilities (Levinthal Reference Levinthal, Dosi, Nelson and Winter2000). They are, at the same time, grounded in the participants’ cognition and emergent properties of the firm.Footnote 6 Furthermore, these intellectual resources are both inputs into and outputs of the firm’s operations: A shared understanding of “the way we do things” is not just a factor of production but also something that is instantiated and reproduced, unintentionally, with the ordinary process of production. Since the maintenance of shared intellectual resources thus rests on a process of joint production, there is a sense in which even a monoproduct firm is effectively a multiproduct firm (Lloyd Reference Lloyd1983).Footnote 7

In this process of joint production and reproduction, shared intellectual resources may be gradually transformed. For example, if we think of organizational routines as grammars of action (Pentland and Rueter Reference Pentland and Rueter1994), routinized individual and group activities instantiate and replicate the routines. But because routine replication is not a high-fidelity process, which is to say that it often is imperfect and subject to local variation, whether by accident or design, evolutionary mechanisms kick in, as Geoffrey Hodgson and Thorbjørn Knudsen (Reference Hodgson and Knudsen2004) have shown. Accordingly, the firm’s routines – its instructions for future growth (Kogut and Zander Reference Kogut and Zander1992) – effectively change over time. Evolutionary processes of this kind are relevant in explanations of the nature and transformation of the firm’s other shared intellectual resources.

These resources are not private goods because they are indivisible, non-subtractable, and exhibit high exclusion costs, but they are not exactly public goods either. They are perhaps more akin to club goods shared by insiders. However, this presupposes institutional arrangements keeping them within firm boundaries. These will always be imperfect because, to paraphrase Kenneth Arrow (Reference Arrow1996), knowledge and intellectual resources more generally are “fugitive.” This affects their production and maintenance – a challenge that is compounded by internal problems of shirking and free-riding. Just as the revenue generated from employees’ firm-specific human capital investments must be shared by employers and employees (Hashimoto Reference Hashimoto1981), the benefits of investments in intellectual resources must also be shared. It is easy to see why participants may have an incentive to reduce their contributions without a proportional reduction in their rewards.

To summarize, if we view the firm as a system of shared tangible, intangible, infrastructural, and intellectual resources, we must pay attention to different sorts of governance dilemmas that affect each of these resource subsystems. Some of the firm’s resources are appropriable, others are not. Some can be private, common-pool, or public, depending on the institutional context, while others cannot possibly be private. This is the case of many of the important shared intellectual resources that enable firms to operate and attain or maintain competitive advantages. Firm participants jointly produce, reproduce, and gradually transform these intellectual resources, which should accordingly be seen as both inputs into and outputs of the firm’s operations. We are now in a better position to think about the corporate form.

2.2.3 The Firm’s Corporate Mask

Our initial distinction between firms as resource systems and corporations as the institutional artifacts that govern them should not lead us to confine the concept of the corporation to the separate legal entity created by incorporation under the corporate law of some jurisdiction. Likewise, while there is a sense in which the business corporation is a type of firm (Deakin et al. Reference Deakin, Gindis and Hodgson2021), in the context of the present discussion, it would be unhelpful to limit the analysis to the corporation so understood. We do not wish to focus on incidental features like limited liability or tradable shares. A broader concept of the corporation qua corporate actor – used by philosophers like Christian List and Philip Pettit (Reference List and Pettit2011) or sociologists like James Coleman (Reference Coleman1990) – can help us maintain the discussion at a more general level. In principle, we should be able to extend the corporation-as-commons idea to any legal form the firm may take. Indeed, the idea ought to extend to all the types of business and nonbusiness organizations that enable societies to function.

The various legal forms a firm can take – including, besides the business corporation, partnerships of various sorts, limited liability companies, and cooperatives – are institutional artifacts enabling people to hold property or interests in common. But this characteristic of being a common property regime, as suggested by Ostrom, is not what matters the most to the corporation-as-commons idea as we envisage it here. For us, the more significant feature is that all legal forms provide the firm with a singular vector for collective action, effectively transforming a group of resource owners into a corporate actor. The firm is thus endowed with a capacity to act as a singular whole in the legal and commercial spheres, and it is legally recognized and regulated as such (Deakin et al. Reference Deakin, Gindis and Hodgson2021).Footnote 8

The firm’s corporate capacity and legal identity are separate to some degree (depending on the legal form and the jurisdiction) from all the individuals involved. This is what enables resource owners to contract with the firm, rather than with each other, and why internal employment or external commercial contracts are typically made with firms, not their shareholders or managers (Gindis and Hodgson Reference Gindis, Hodgson, Windsperger and Raha2026). Organizational law, which Henry Hansmann and Reinier Kraakman (Reference Hansmann and Kraakman2000) define as the law governing the standard legal forms used by business and nonbusiness organizations, supports this transaction cost-reducing institutional structure. It also enables autonomous organizational action (Micheler Reference Micheler2021; Gindis and Micheler Reference Gindis and Micheler2024). The firm, as a result, is a self-governing entity.

Because the law distinguishes to some degree (depending on the legal form and the jurisdiction) the firm’s business assets from the personal assets of its founders or shareholders, its contractual and financial commitments can survive changes in its membership (Spulber Reference Spulber2009). Removing the incentive for new participants to walk back on the firm’s past promises or to use that threat to renegotiate existing deals supports the continuity of the firm’s activities and makes it a more reliable business partner. And by vesting the ownership of shared tangible and intangible infrastructural resources in the firm, the law gives managers the authority to assign access, use, and other rights that help prevent (where possible) their exploitation, congestion, and overuse. The firm controls the internal rules of the game: It can design jobs, set working rules, assign tasks, decide on strategic plans, delegate authority, control information channels, or foster a particular corporate culture (Holmström Reference Holmström1999).

It follows that, absent some form of legal recognition of the firm’s corporate capacity, the firm would be unable to operate effectively. But it is important to acknowledge that social recognition of the firm as a corporate actor likewise constitutes it as such and enables it to operate in the commercial realm (Adelstein Reference Adelstein2010). As John Searle (Reference Searle2005) explained, official and social recognition of institutional facts go hand in hand. Firms are intentional objects (Searle Reference Searle1983): They are the objects of our thoughts; we see them as singular actors in our individual and collective representations. This is aided by the fact that firms typically adopt distinctive identifiers, such as logos or mottos, that provide insiders with a sense of shared identity and project an outward appearance of unity. Ownership of such intellectual resources is also vested in the firm, such that it has significant control over how it presents itself to both insiders and outsiders. Legal and social recognition of the firm come together in our notion of corporate mask, which expresses the view that the firm is at the same time a legal and a social actor.

The corporate mask is represented in identifying legal and social artifacts – registration documents, company or employer identification numbers, contracts, bank accounts, annual reports, websites, logos, brands, mottos, and so on – but the mask itself is an intangible institutional resource. Several conceptions of institutional assets have been proposed in the literature. One approach sees them as a category of a firm’s capabilities that enable it to deal with and take advantage of a given institutional environment (Jansson Reference Jansson2007). Another takes the view that they are the beneficial features of the environment itself (Teece et al. Reference Teece, Pisano and Shuen1997). Institutional assets have also been conceptualized as the set of institutions governing value-generating processes both inside the firm and between the firm and its external stakeholders (Dunning and Lundan Reference Dunning and Lundan2008). Our view relates to all three definitions: institutional resources, such as the corporate mask, are drawn from and are anchored in specific institutional environments, help actors navigate those environments, and govern a range of intrafirm and interfirm value-generating processes.

As such, the corporate mask combines features of infrastructural and intellectual resources. The infrastructural dimension comes into focus when we think of the role played by the central contractual agent highlighted in the Coasean tradition. The value of having a single referent for contracts that are bonded by a separate pool of assets is not merely that it helps reduce transaction costs, but that it unlocks an important source of economies of scale and scope. The firm grows by entering new contractual arrangements, so the centralization of the firm’s legal infrastructure largely simplifies the simultaneous pursuit of multiple lines of business.Footnote 9 That the central contractual agent is an input into many different intrafirm and interfirm processes underpins the organizational capabilities of the firm (Deakin Reference Deakin, Clarke and Branson2012b; Gindis Reference Gindis2016), which is to say its ability to acquire, specialize, and combine heterogenous resources in value-generating ways. But while the corporate mask shares some characteristics of mundane infrastructural resources (such as procurement services), it is not congestible, even when demand is high. Nor can it be depleted.

The nature of the corporate mask is further revealed when its intellectual dimensions are considered. Implicitly or explicitly, the notion of the firm as an identifiable and singular entity serves as a coordinating focal point (Basu Reference Basu2018) for both insiders and outsiders. Insiders and outsiders refer to this “extended cognitive resource,” as Masahiko Aoki (Reference Aoki2010) put it, to position themselves vis-à-vis the firms they work for or deal with, and to interpret signals about and give meaning to the firm’s activities. It is with an image of an identifiable and singular whole in mind that insiders and outsiders, who normally recognize the firm’s boundaries (Santos and Eisenhardt Reference Santos and Eisenhardt2005), impute objectives and actions to the firm when they interact with it and with each other. The identity of the firm enters into contracts made with it, expressing the expectation that it will honor its commitments (Pettit Reference Pettit2023), and is reproduced when those commitments are honored. This is how firms acquire and maintain reputations, and why these reputations attach to the firm itself, independently of the reputations any of its representatives may have.Footnote 10

Overall, the firm relies on a legally and socially recognized identity to engage in the economic life of society. The legal recognition of the firm, which is essential for its centralized contractual structure, establishes it as a corporate actor. But the firm cannot operate based solely on its legal status. It must also be socially recognized as not only a corporate actor but also a reliable business partner, a reputable producer of goods or services, and so on. The firm’s corporate mask is thus both legal and social: It is a special kind of shared institutional resource that combines the features of infrastructural resources (because it is as a pooled input in many intrafirm production processes) and intellectual resources (because it underpins and feeds into shared beliefs about the firm and its activities). We now need to take a closer look at how the provision, production, and reproduction of the corporate mask takes place across adjacent action situations.

2.3 Constructing the Corporate Mask across Adjacent Action Situations

We have suggested that the corporation-as-commons idea requires thinking about the kinds shared resources firms rely on or manage and have argued that the corporate mask is an institutional resource of this kind. Our next task is to provide a clearer sense of who shares this resource and to specify some of the contexts within which it is shared. This requires zooming in on the rules and practices that govern its provision, production, and reproduction in the relevant action arenas. Action arenas, which are core units of analysis in both the GKC framework and the Institutional Analysis and Development (IAD) framework (Ostrom Reference Ostrom2005; Cole Reference Cole2017) upon which it is built, are broadly speaking interaction settings within which more specific action situations can be scrutinized.

We connect the discussion with the theory of the firm by translating into Ostromian terms the Coasean approach of viewing firms and markets as alternative “institutional matrices” within which transactions are negotiated and executed (Williamson Reference Williamson1996). However, contrary to the standard Coasean account, which misses the essential role played by the legal system in the constitution of the firm (Gindis and Hodgson 2026), we view the legal system as the third action arena of interest and characterize the legal system’s role in the provision of the corporate mask. We then examine the analytically relevant adjacent action situations (McGinnis Reference McGinnis2011a) in which the legal and social recognition of the firm produces and reproduces the corporate mask.

2.3.1 The Firm and the Market as Adjacent Action Arenas

To say that firms and markets are alternative institutional matrices within which transactions are negotiated and executed is to say that firms and markets are alternative action arenas within which specific action situations take place. But where transaction cost economists like Williamson (Reference Williamson1985) focus the characteristics of a given transaction (primarily the degree of asset specificity involved) to determine the appropriate governance structure, an Ostromian does not presume to know which governance structures are appropriate and instead tries to gain a deeper understanding of internal structure of action situations. The relevant variables are the participants; the positions they fill; the set of actions they can take by virtue of their positions; the set of potential outcomes; the information participants have about actions, outcomes, and their linkages; the control participants can exercise over these linkages; and the criteria participants use to evaluate outcomes (Ostrom Reference Ostrom2011). It is useful to express the Coasean theory of the firm in these terms.

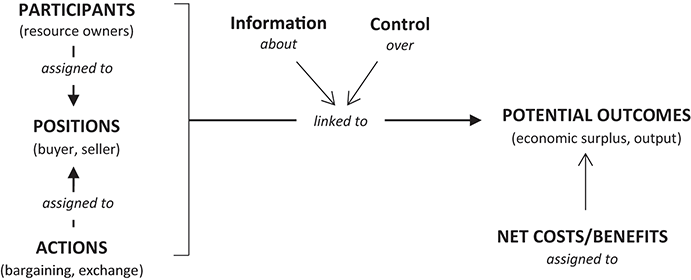

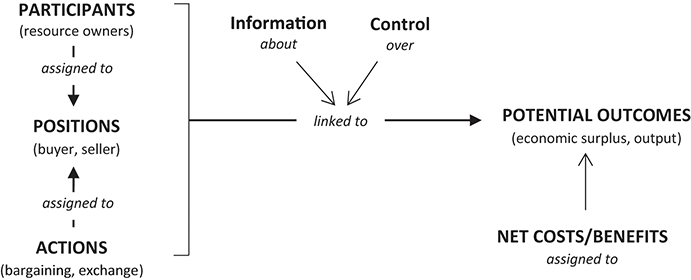

Assuming that “in the beginning there were markets,” as Oliver Williamson (Reference Williamson1975) famously put it, we take the market as our initial action arena (Figure 2.1). Given the position, boundary, choice, aggregation, information, payoff, and scope rules governing this action arena,Footnote 11 market action situations involve participants (resource owners) in specific positions (buyer, seller), by virtue of which they can engage in certain kinds of actions (bargaining, exchange of property rights) and produce certain outcomes (economic surplus, if the action situation involves interpersonal exchange; output, if the action situation involves the Coasean scenario of organizing production through bilateral exchange). Note that participants must have some common information about their relative positions, their available actions, and the potential outcomes – otherwise they would not be in the same situationFootnote 12 – and that they also have some control over the allowable actions, outcomes, and their linkages.

Market action situation.

The distribution of costs and benefits associated with outcomes may incentivize certain actions and deter others in the next iteration of the participants’ interactions. Participants will exercise their control over the structure of the action situation when costs exceed benefits, when benefits seem small relative to costs, or when potential benefits seem unrealized. They may, for example, rely on their bargaining power and threaten to withhold cooperation to get a better deal. But they may also switch to or create a new action situation, in the hope of realizing greater benefits. The rules of this new action situation place participants in different positions, by virtue of which they may engage in a new set of actions. Their control over the allowable actions, outcomes, and their linkages is exercised through different channels. We can think of the emergence of the firm from the market in these terms.

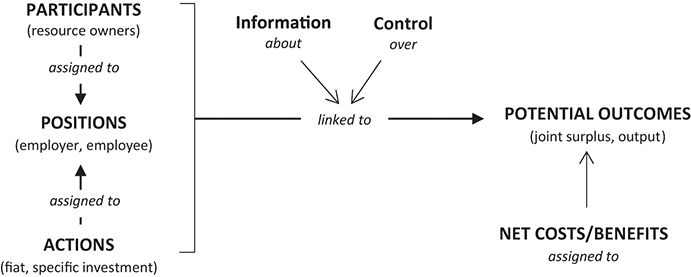

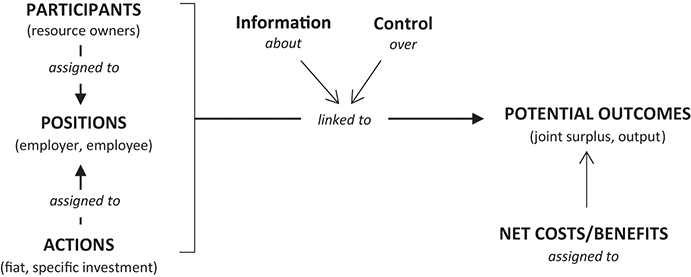

Our second action arena, and indeed our focal one, is inside the firm (Figure 2.2). The firm emerges from the market when one of the participants (resource owners) takes on the role of an entrepreneur. Positions change from buyer and seller to employer and employee, with a new set of permissible actions (fiat, specific investment) and outcomes (joint surplus, output). As before, participants have some common information about their relative positions, their available actions, and the potential outcomes – otherwise they would not be in the same action situation. They also have some control over the allowable actions, outcomes, and their linkages. Free-riding, hold-up behavior, and other collective action problems arise because they can act independently in situations of interdependence.

Intrafirm action situation.

Per Coase (Reference Coase1937), it is only worth moving from a market action arena (Figure 2.1) to the intrafirm action arena (Figure 2.2) if the firm can produce the same outcome (output) at a lower cost. Since any productive activity can be contracted out to an outside supplier or be undertaken in-house – recall that firms and markets are alternative institutional matrices within which transactions are negotiated and executed – it should be clear that these action arenas are in fact adjacent, with the choice of moving from the market to the firm and vice versa guided by the comparison of net costs and benefits (Figure 2.3).

Make-or-buy.

That the firm and the market are adjacent action arenas is reinforced by the fact that the firm must return to a market arena as a seller and create value for buyers in excess of its production costs, if it is to make a profit. The firm will fail to sell its output if the price exceeds the benefits to buyers (firms, if the output is an intermediate good; consumers, if the output is a final good). In this case, the firm’s evaluation of this signal sends it back to the drawing board: It uses its control over the structure of the action situation (fiat) to reduce costs before coming back to the market to try again. Both the make-or-buy decision and this ongoing process of responding to market signals suggest that one cannot understand action situations within our focal action arena without placing them alongside various action situations in the market arena. The analysis, however, is incomplete.

2.3.2 The Legal System and the Provision and Coproduction of the Corporate Mask

A significant shortcoming of most of the literature on firms and markets developed in Coase’s footsteps is that the essential roles played by organizational law and the legal system more broadly are overlooked (Deakin et al. Reference Deakin, Gindis, Hodgson, Huang and Pistor2017; Gindis and Hodgson 2026). While participants in market action situations (Figure 2.1) may wish to switch to an intrafirm action situation (Figure 2.2) because output can be produced at a lower cost or because greater benefits can be realized, the move between the two situations requires an intermediate step. The firm can only engage in transactions in which the make-or-buy decision is relevant if it has its own legal identity and contracting capacity (Iacobucci and Triantis Reference Iacobucci and Triantis2007; Kornhauser and MacLeod Reference Kornhauser, MacLeod, Gibbons and Roberts2013). It follows that placing our focal action arena alongside the market arena is insufficient; a third action arena – the legal system – must be included in the discussion. Recall that, as an institutional resource, the corporate mask is drawn from and is anchored in the legal environment.

In Ostromian jargon, provision refers to the public availability of goods or services for collective consumption (McGinnis Reference McGinnis2011b). The legal system provides a range of such goods and services (with varying quality across jurisdictions). Among other things, entrepreneurs or coalitions of resource owners have an array of legal forms to choose from when setting up firms; they can access a system of property and business registries; and they can turn to impartial courts in cases of disputes. The benefits of being able to simply “plug into” such shared legal platforms are enormous (Hadfield Reference Hadfield2017), not least because the services provided are generic, partly modular, and adaptable, which makes them valuable in a wide set of context-specific circumstances. The legal system’s services can be consumed non-rivalrously and their demand, as Brett Frischmann (Reference Frischmann2012) has argued, is driven by downstream activities requiring them as an input for the production of a range of private, public, or club goods and services.

In most jurisdictions, there is virtually no restriction on who counts as an authorized user (with access and withdrawal rights) of the shared business registration system. The firm becomes operational when its founder or founders plug into the relevant platform. Whether the firm is merely registered with tax authorities to separate business from personal income or is formally incorporated by a state registrar, this legal recognition of the firm (embodied for example in a company or employer identification number) is a process of coproduction (Parks et al. Reference Parks, Baker and Kiser1981), in the sense that the users’ input is required for the institutional resource to be produced. The public authority records the users’ input and gives it legal effect. The legal constitution of the corporate mask is therefore neither private nor public; it is “essentially hybrid,” to borrow Katharina Pistor’s (Reference Pistor2013) expression.

These considerations have a broader relevance. Depending on the legal form and the jurisdiction, there may be a requirement to file any amendments made to constitutional documents (such as articles of association or incorporation) that intervene after the firm’s initial registration. Likewise, there may be a requirement to register any variations of share capital or capital stock, as well as any charges or secured interests over the firm’s assets. Each of these commonplace situations in the life of a firm involves a process of coproduction: Governance actions are initiated by the firm’s managers, shareholders, or creditors, but registration gives them legal effect. Significantly, in each of these instances where the publicly available information about it is modified, the firm must be legally re-recognized: The registration authority must confirm the identity of the firm before changing its registered characteristics. The firm remains the same, but its properties or qualities evolve.

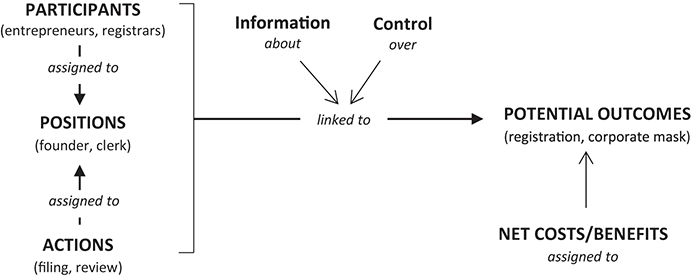

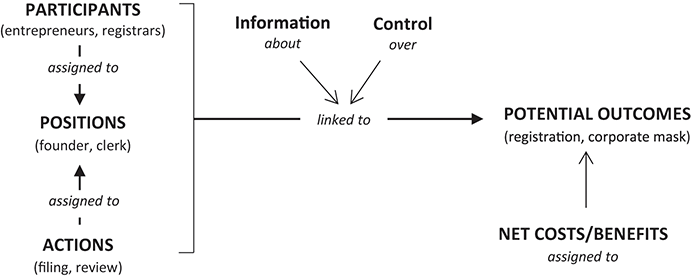

Because the legal system is in fact a set of subsystems (legislation, regulation, courts, registries), each producing distinct resource units (statutes, rules, decisions, identification numbers) in a large range of different action situations, capturing it in a simple illustration is going to be difficult. Suffice it to say that the rules-in-form promulgated by legislators and regulators expand, restrict, or qualify the position, boundary, choice, aggregation, information, payoff, and scope rules-in-use governing many action situations in firms and markets. Importantly, rules-in-form determine both who or what is to be registered and the legal effects of registration. It is not surprising that policymakers in many developing countries have liberalized access to business and property registries and sought to make these more accommodating and cost-effective for users. Registries and third-party access to them for verification purposes are essential forms of institutional support for firms (Arruñada, Reference Arruñada2010). Importantly, these systems involve the provision and coproduction of the corporate mask (Figure 2.4).

Provision and coproduction of the corporate mask.

2.3.3 Producing and Reproducing the Corporate Mask

Once constituted and in possession of their own legal identity and contracting capacity, firms are participants in a range of analytically relevant market action situations. For example, they hire and fire workers in labor markets, buy and sell intermediate goods in producer markets, pledge assets and raise finance in capital markets, and acquire and sell intellectual property in the market for technology. All parties in such transactions will occupy a set of positions and have a set of authorized actions, some control over their actions and the linkages between these and the potential outcomes, and of course some common information about the situations they find themselves in. A key part of this common information is the mutual understanding that deals are being made with firms. Prospective employees know that the product of their labor will be appropriated by the firm and not the manager hiring them, and those negotiating interfirm deals know that the contracts thus entered into will bind not them but their firms.

While shared social perceptions and understandings are not backed by the state and thus may not bind in quite the same way as legal actions do (McAdams Reference McAdams2017), they nevertheless have the constitutive force captured in Searle’s (Reference Searle1995) famous formula, “X counts as Y in context C.” Note that this constitutive force is in operation whether we mean “a group of resource owners” counts as “a corporate actor” in context C1 or infer that “an authorized agent” counts as (represents, binds) “a corporate actor” in context C2. In both cases, a combination of formal rules, informal norms, and their situational interpretations comes into play. The process of interpretation is straightforward when formal rules are sufficient and informal norms are relegated to the background, but the weight of informal norms and situational interpretations increases when formal rules are insufficient (Cole Reference Cole2017).

Compare first two contexts C1 where “a group of resource owners” counts as “a corporate actor.” The first scenario, C1(a), is that of an incorporated firm, which unequivocally counts as a corporate actor, if the appropriate registration papers were filed with the state registrar, if various bureaucratic procedures (such as registration with the tax authorities) have been followed, and so on.Footnote 13 In this case, the provision and coproduction of the corporate mask occurs in an ex ante action situation (incorporation and registration), enabling the firm to operate legally as a corporate actor in the network of subsequent adjacent action situations. When the firm’s trade name includes “Ltd.” or some other such signifier that performs a semiotic mediation between the legal and social worlds (Bau Macedo and Herrmann-Pillath Reference Bau Macedo and Herrmann-Pillath2021), parties perceive it as such and deal with it accordingly.

The second scenario, C1(b), is that of the unincorporated partnership, which as a matter of rules-in-form is not a corporate actor in England (contrary to numerous other jurisdictions). Here, the beliefs and representations of both participants and third parties matter a great deal, as do the courts’ norms of statutory interpretation and their attitudes toward context-specific business conventions. There is, for example, a long tradition of courts treating unincorporated partnerships as if they were corporate entities to uphold deals third parties struck with the firm in good faith, based on the firm’s outward appearance of unity (Wells Reference Wells2021). The corporate mask had already been produced and reproduced thanks to the parties’ shared understandings and interpretations of the nature and effect of their business interactions, so when the court enforces contracts entered into on this basis, it recognizes this state of affairs by providing, so to speak, the corporate mask ex post.

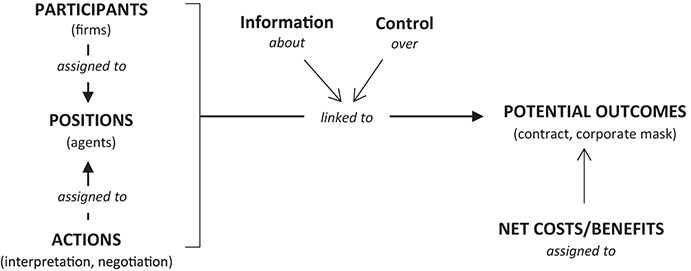

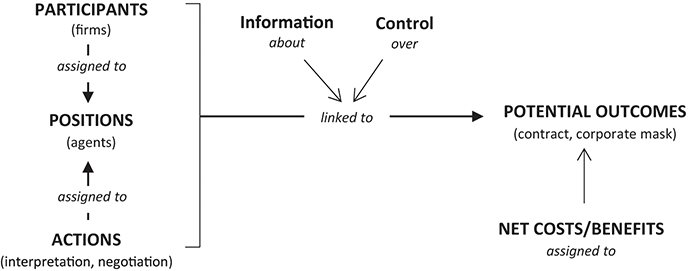

That the social recognition of the firm as a corporate actor matters at least as much as its formal legal recognition is thrown into relief when we look at the set of contexts C2 where “an authorized agent” counts as (represents, binds) “a corporate actor.” In any contractual negotiation between two firms, each firm’s authorized agent presents themselves as having the capacity to bind a corporate actor and assumes that the other’s analogous representation can be reasonably relied upon. The negotiation will proceed if both parties are satisfied that they are indeed in a C2 context and that the result will legally bind their respective firms. The idea of the firm as a corporate actor helps align the parties’ shared beliefs and expectations and is therefore an input into the negotiation, while the actions and outcomes based on these beliefs and expectations instantiate and reproduce it. The corporate mask, in other words, is produced jointly with interfirm contractual agreements in markets (Figure 2.5).

Joint production of the corporate mask.

The role played by shared understandings in this process means that it is vulnerable to conflicting interpretations. Where the parties’ interpretations of their situations and positions differ, or where their understandings of the formal rules and informal norms in operation diverge, contractual negotiations can become more complicated. If one of the parties doubts that the other is properly authorized, there will be disagreement about whether they are in fact in a C2 context until further assurances can be made. The doubting party may proceed without further assurances, but if it then turns out that the counterparty lacked actual authority, it may be difficult to enforce the agreement. It is important to note that the governance of such disputes and the enforcement of agreements take place in a range of adjacent action situations – from the informal meeting of the parties to the courtroom – in which the firm’s rights and duties are defined or redefined. It is the firm, not its agents, that is recognized as having standing to enforce agreements or adjudicate disputes in courts (Vining Reference Vining1978). Its corporate mask is an input into and a jointly produced outcome of these processes.

The problem of conflicting interpretations also complicates the distribution of the joint surplus created by the firm, which exhibits, as Ostrom (Reference Ostrom and Newman1998) intimated, features of a common-pool resource. Distributional conflicts are compounded when outsiders also present themselves as legitimate claimants. While both insiders and outsiders have a shared understanding that the surplus belongs to the firm, they also have a shared understanding that many of the key resources that help produce, maintain, and enhance that surplus are not strictly speaking owned by the firm but can instead be said to be held in common. Insiders and outsiders will often justify their claims based on different evaluative criteria (contribution, efficiency, equity, legitimacy), and it is the central problem of corporate governance to resolve such disputes (Bridoux and Stoelhorst Reference Bridoux and Stoelhorst2022). The corporate mask is ever-present in these debates.

2.4 Conclusions

We welcome Deakin’s (Reference Deakin2012a, Reference Deakin, Clarke, O’Brien and O’Kelley2019) corporation-as-commons idea and have sought to take it forward in this chapter. We have argued that this requires thinking about the kinds of shared resources firms rely on or manage and asking whether, and in what sense, we can view the corporation as such as resource. We have shown that the corporate mask is the firm’s most critical resource, enabling it to operate as a singular actor in the legal and commercial spheres. The corporate mask functions as a legal and epistemic focal point shared by insiders and third parties with whom the firm interacts in a network of adjacent action situations both within and across firm boundaries.

More specifically, we characterized the corporate mask as a special kind of institutional resource that combines features of infrastructural and intellectual resources, because it is a pooled input in many intrafirm and interfirm processes, and at the same time underpins and feeds into shared beliefs about the firm and its activities. It is provided by the legal system when it recognizes (ex ante or ex post) the firm’s capacity to act as a singular whole, and is coproduced through various forms of registration. It is also produced and reproduced jointly with the firm’s interactions with third parties, including contracting parties and the courts. The shared understanding that a corporate actor is involved is both an input into and an output of these interactions, which we have examined in representative action situations.

We believe that the focus on adjacent action situations is a productive way to think about and extend the GKC research program. In this respect, despite some differences, this chapter is a continuation of Erwin Dekker and Pavel Kuchař’s (Reference Dekker and Kuchař2024) work on the governance of markets as knowledge commons. Further advances in this direction will require more detailed analyses of the connections between relevant action situations in the three action arenas. It will also be important to gain a better understanding of how resource and governance systems coevolve. And there is certainly much more to say about how the analysis relates to, or has bearing on, ongoing debates in corporate governance. Different versions of the corporation-as-commons idea should be proposed and compared, and case studies of specific types of corporations and other kinds of corporate knowledge commons should be developed. We look forward to the growth of this exciting new area of interdisciplinary institutional research.

Open access

Open access