Introduction

Concerns about enduring economic stagnation in Britain have prompted a contentious debate in which the mismanagement of public infrastructure projects is used as both a proxy for general national malaiseFootnote 1 and as a vehicle for political polemics.Footnote 2 As a sub-set of this wider discussion, the high costs and delayed delivery of rail transport infrastructure in the UK have also been scrutinized closely and sometimes wrongly.Footnote 3 In this latter debate, skills and materials shortages, project complexity, technological uncertainty, demand uncertainty, lack of scope clarity, unexpected geological features, and negative plurality have all been identified as contributory factors.Footnote 4 We agree. But we also think that two enduring conceptual frameworks are visible through which all the individual factors above are perceived.

These frameworks are, above all, temporal. Ex post pricing primarily looks backward at how meeting the costs of the assets created through investment can be averaged out across society. Ex ante discounting primarily looks forward to the opportunity costs of an investment and to its marginal value to society.Footnote 5 We think that these discourses have influence beyond the intellectual and conceptual sphere in project management, and that by setting the parameters of the debate over the expected financial price and social value of infrastructure they have real-time, operational impacts in terms of what is permissible and how it gets done.Footnote 6 This paper explores those impacts via a specific, century-long, historical case study of London, the city with the world’s oldest underground system.

In the history of London’s underground transport infrastructure, we identify three distinct periods in which each of these approaches was dominant in public, managerial, political, and media discourses of the time.Footnote 7 We think that prior to World War I the discounting perspective of the value of new underground railway lines was the foremost consideration. What mattered was the projected future earnings of infrastructure projects as an incentive for private individuals to purchase shares in the companies that intended to build and operate the new underground railways. These future revenue considerations determined the route, scale, and standard of what was proposed, and, depending on the scale of share capital eventually pledged, what was actually built and what was not.Footnote 8 Following World War I, views changed in the 1920s. Spurred by economic difficulties, the government approved a series of major new programs of investments in underground railways financed by fixed interest, long-term bond issues. These projects were realized within the context of an organization expected to balance its revenues and operational expenditures taking each year with another. Investors’ returns were fixed, and the benefits were held to be social and collective, as well as individual and financial: alleviating unemployment, reducing congestion, and better connecting a vast suburban housing building boom on the outskirts of London to the center of the capital.Footnote 9 This very visible movement into the public realm arguably represented a “cleaning up” of the underground railway project in reputational terms after speculative financial excesses.Footnote 10 Moreover, the media held the new underground railway projects to be marvels of engineering and architecturally outstanding. The interwar projects engendered a palpable sense of pride and prestige in what had been achieved as a collective, national, and British—rather than a private—endeavor.Footnote 11

After World War II Britain faced more stringent national financial circumstances, yet the war had simultaneously normalized the ex post socialization of resource allocation and reinforced the sense that British national grandeur was somehow embodied in the capability to deliver major public infrastructures, sometimes regardless of cost.Footnote 12 It took until the early 1960s for the Treasury to begin to promote, and after the devaluation crisis of 1967 enforce, the use of discounting as a method of reining in nationalized utilities that it believed had been over ambitious in their use of public money.Footnote 13

As we show below, the introduction of ex ante discounting into the planning of London’s underground system is one of several instances of American influence on the development of the London Underground. The use of ex ante discounting in the evaluation of the social value of infrastructure projects was pioneered during the New Deal era by U.S. federal agencies such as the Army Corps of Engineers. In the post war period, American officials and economists from the Bureau of Agricultural Economics and the Bureau of Land Reclamation on the Inter-Agency River Basin Committee formalized and refined the process of cost-benefit analysis. This began with the “Proposed Practices for Economic Analysis of River Basin Projects” report (the so-called Green Book), first published in 1950.Footnote 14 Cost-benefit analysis became a respectable academic and bureaucratic activity in the United States by the late 1950s.Footnote 15 The nexus between a growing state bureaucracy looking to quantify benefits and welfare economists seeking to calculate utility burgeoned rapidly, quickly crossing the Atlantic.Footnote 16 The eventual outcome in Britain was that a highly regulated version of the previously free market ex-ante pricing orthodoxy from the early twentieth century, influenced by academics but controlled by bureaucrats, now asserted itself as a legitimating analysis of public investments.Footnote 17 The Treasury’s disbelieving scrutiny of the future and marginal value of London’s transport infrastructure projects became increasingly visible from the mid-1960s onward,Footnote 18 and became part of a general retreat by the state from capital investment in transport in the UK during the following decade.Footnote 19 Caution, skepticism, and an endless debate about what constituted real value for money became ubiquitous, and indeed generated a vast new industry of assorted academics, consultants, and lobbyists who could proffer speculative opinions about future individual gains and losses from any given project proposal. We think that these rent-seeking behaviors and resultant principal-agent dilemmas arose out of an infrastructure debate now framed by calculating future hypothetical, marginal, and individualized costs and benefits. Paradoxically, it is this ex ante pattern of managerial discussion and activity concerned with marginal efficiencies and pricing which can nevertheless appreciably add to uncertainty, delay, and costs to projects.Footnote 20

In summary, this paper is less a history of objective discrepancies over time in the cost of building underground railways in London, and more a history of the evolution of the framing and argumentation that preceded, surrounded, and followed those projects.Footnote 21 We argue that this is a significant but under acknowledged element of the riddle of why British infrastructural projects are perceived popularly as poor value for money.

The Historiography of Mega-projects

In understanding the evolution of Mega-projects Flyvbjerg has studied how rationality and power interact and manifest themselves in the provision of infrastructure.Footnote 22 Flyvbjerg argues that mega-projects,Footnote 23 defined here as complex capital-intensive projects with long planning and delivery horizons, and which involve multiple stakeholders spanning different sectors, are subject to an “iron law” in that they are usually delivered both behind schedule and over budget. This happens, not because of asymmetric information on the true costs of a project as Hirschman has argued,Footnote 24 but because large projects are entered into through the optimism bias of their promoters, who typically play down the inherent risk in favor of the claimed benefits of the project. Flyvbjerg identifies four sublimes, or factors, that seduce policymakers into undertaking mega-projects—the technological, political, economic, and aesthetic.Footnote 25 Flyvbjerg examines several projects from the late twentieth and early twenty-first centuries, postulating that the strategic misrepresentation of costs is universal. While there is evidence that projects are embedded in the practices of the parent organization and the socio-economic environment,Footnote 26 there has been little work on the changing institutional contexts in which the perception of failure occurs.Footnote 27 We suggest that to historicize the concept it is necessary to compare analogous projects in distinct eras, as well as considering the possibility that the sublimes are dynamic over time, with historical context governing which of the four takes precedence for policymakers.Footnote 28 The price, value, and project management of infrastructure developments have generated a very extensive and significant literature, though one which either does not engage with or misemploys archival records. Tennent and Gillett have adopted and built on Scranton’s view that projects are a legitimate focus for historical analysis while demonstrating that their time-bound nature makes them inherently appropriate for archival research, as is the case in this paper.Footnote 29

We now consider the historiography which looks at the specific context of this study, the development of London’s underground railway infrastructure. We note that the development of London’s transport system has produced a wide-ranging set of books and papers concerned with civil engineering, nevertheless only a few of them however make any systematic judgments about the costs or management of the projects. Amongst those that do, we think that they have become the prisoners of a set of rhetorics established in the early accounts of London’s transport history by historians who were often former senior officials of London Transport itself. These have become the consensus view of what and how London Transport developed, but they apply critical analysis only in the service of preconceived assumptions about the techno-rationality supposedly either desirable or inherent in transport provision.Footnote 30

This consensus holds that early underground railway projects before World War I were entirely the result of capricious speculative finance.Footnote 31 In this scenario, the literature dwells on the methods of persuasion that were used to inveigle private investors into buying shares on the basis of future projected passenger numbers and resulting revenues.Footnote 32 But while the projects were later deemed expensive by subsequent historians, it was underutilization which was the focus of analysis at that time. By contrast, all commentators hold the major projects of the inter-war period, notably the “New Works” program of 1935–1940, to be major successes.Footnote 33 However, just as with the commentary on the earlier period before World War I, there is very little attention paid to whether these visually impactful and culturally iconic projects cost more or less than what was expected. For example, Croome and Jackson comment that by 1939 the capital borrowed had set up an interest burden that would require £3 million of additional revenue but they make no judgment about whether this caused public and political consternation, indifference, or relief. The implicit and ahistoric sense is that the imminence of World War II and nationalization engendered an expectation that all project costs would be retrospectively written off, or at the very least considerably written down.Footnote 34

After World War II the literature again jointly decided that investment projects were generally too scarce, and that the few projects commissioned, such as the Victoria line in the 1960s or the Jubilee line in the 1970s and 1990s, ended as both delayed and expensive.Footnote 35 As previously, there is little analysis about whether or how the projects, undertaken in a much more corporatist and rationalist institutional context than those previously, were too expensive per se. The exception is Wolmar’s book Down the Tube which carefully dissects the Jubilee Line extension project in the 1990s which was built to stimulate the redevelopment of the former docklands. It finds that political insistence on keeping public investment in the project separate from the national debt via a complex set of financial instruments and intermediaries resulted in systematic project delays and mismanagement.Footnote 36

Therefore, we conclude that firstly there is a remarkable degree of consensus in the literature and many assumptions are so embedded in the stories that they are hard to extract and examine critically.Footnote 37 Secondly, little has been said to justify a position that they were necessarily more expensive than might reasonably be expected. Thirdly, while clear eras in the progress of major railway projects in London are visible in the literature, no attempt has been made to systematize or explain those periods.

Therefore, our approach makes explicit use of the archives to build the kind of case study assessing mega-project management that Flyvbjerg advocates. Primarily, we position this work as a story-telling historical narrative since we believe that this approach realistically encompasses the inherent subjectivity and relativist position that politics imposes on the management of organizations generally.Footnote 38 To address the influence of power politics, the media, and project management reliably we want to consider as broad a spectrum of opinion as possible, and thereby construct a valid and credible account. Therefore, we draw heavily from primary sources from a range of archives held by corporate and local authority repositories and a wide variety of documentary sources and then triangulate them against each other.Footnote 39 From the Transport for London (TfL) archive we used annual reports, internal and external consultancy reports, and strategy planning documents. The London Metropolitan Archive (LMA) provided the minutes of the meetings of the Transport Committee of the GLC, relations with the LTE and its long-term transport planning and applications for transport grants from central government. In addition, articles from the archives of national newspapers gave us perspectives from outside the organization itself. In summary, we employ a wide variety of sources to construct a “thick” historical description emphasizing a specific reality, though not rejecting theoretical import, as a counterpoint to both incorrect narratives in London’s transport history and a general ahistoricism in project management.

The Expectation of Realizing Private Gains: 1900–1914

In this era, we argue that the key motive for pursuing projects was economic. Literature of the period shows that diverse investors, wealthy and poor, were invited to speculate in projects whose future earnings might, or might not, make them rich on the basis of fairly scant and generalized information. We may assume that the risk involved fed a sense of economic delight in the dividends—if they arrived—and that discounting was an ineffable process made up of thousands of personal decisions whereby private individuals weighed up their own particular financial circumstances and prospects, as well as their personal knowledge and beliefs about the future of underground railways.Footnote 40 In autumn 1901 there were no less than thirty-two Bills deposited before Parliament proposing new underground railways beneath central London, of which about half a dozen were eventually built at broadly similar costs (Table 1 and Figure 1).Footnote 41 The details of how these were eventually whittled down to about half a dozen projects that were actually constructed related principally to the credibility of their financial proposals.Footnote 42 We focus on one exemplar here: the Baker Street and Waterloo Railway, whose inception, design, and construction extended across a decade and a half.

London underground railway projects 1900–1906

Sources: Croome and Jackson (Reference Croome and Jackson1993), Rails Through the Clay, London: Capital; London Metropolitan Archive, Board Meeting Minutes, ACC-1297-GNCY-1-5; Board Meeting Book, ACC-1297-GNPB-1-4; Transport for London Corporate Archives, LT171/001.

LU Pocket Map 1912, 1998–1856 © TfL from the London.

The initial prospectuses to investors offered 4% preference shares or ordinary shares at £10 each.Footnote 43 They went on to briefly explain the construction works and the expected opening date, which was heavily emphasized in the later prospectuses as being within one year. More extensive detail was reserved for the traffic forecasts, where the chairman provided the following encouraging statement:

This line will provide the long-required north-south communication across central London. It will afford facilities for exchange of traffic with no less than 12 other systems… and serve some of the most important shopping districts, government offices, clubs, large hotels, theatres and places of amusement as well as important business centres and tap into the most densely populated artisan districts of London so that it will doubtless carry a large and continuous traffic throughout the day and a great part of the night (see map). NET REVENUE: Net revenue should amount to £146,469 and a surplus after interest of £110,869.Footnote 44

However, the final prospectus of 1905 went further, using the expertise of a Mr Stephen Sellon, a civil engineer with experience in both Britain and America. In his report, Sellon admitted that: “In making an estimate of the extent to which a new means of communication will be used, it will be obvious that no direct process of calculation is applicable.” Nevertheless, Sellon modeled the use of omnibuses along the proposed route and thereby arrived at the confident expectation that 35 million passengers would use the Baker Street and Waterloo Railway annually.Footnote 45 There, in four pages and a map, was the entire proposition to invest in this mega-project, based on claims for the potential future traffic that would in turn drive the prospective profits accruable to private individuals. This approach was normal.Footnote 46

The Baker Street and Waterloo Railway opened for business on March 10, 1906. But the first Bill for its construction had been presented to Parliament in 1893, work itself had only begun in 1898, and this was then interrupted by a major financial scandal in late 1900 before resuming again in 1902. In the end, no less than four successive acts of Parliament were needed to buy more time and extend the financial powers of the Railway Company.Footnote 47 Nevertheless, holdups were not a preoccupation of the popular and financial media at the time, nor was the cost. On the day of opening, the Daily Mail gushed that “the new tube was surpassed for the comfort of its accommodation and the elegance of its appointments.”Footnote 48 Two days later the Mail trumpeted that 37,000 passengers had already used the new line. The article mentioned the cost of the line at £18 million but made no judgment or comment about the sum, instead preferring to repeat the claims made for extensive future population growth in London and a growing density of trips per head of population.Footnote 49 Neither did the financial press provide more critical scrutiny. The Economist ran an article which mentioned the postponements only in passing, the expense not at all, and instead dwelt at length on the new connections for traffic that the line facilitated.Footnote 50 The Financial Times concurred.Footnote 51 A year later, The Financial Times celebrated the similar opening of the Great Northern, Piccadilly and Brompton railway. The newspaper remained unconcerned with expense or overruns. Instead, it commented that:

One of the most interesting and significant features is the more the facilities for traction are increased the greater becomes the demand… It seems almost incredible that the system could have handled so heavy a number of passengers [this year]. There is room for all comers in the matter of London locomotion, and the ‘Tube’ has found its basis as far as the ordinary stockholders are concerned on a 4% return.Footnote 52

However, this optimism was unfounded. Passenger numbers never achieved the levels needed to provide returns to ordinary shareholders, and the underground railway companies were driven to declare technical bankruptcy a year after these Panglossian articles appeared.Footnote 53 This in turn created a degree of public distrust in private speculatory investments which did not abate for many years, and after 1910 there were no further major underground railway lines opened in central London for well over half a century.Footnote 54 We conclude that raising investment privately on the basis of an ex ante expectation of future returns proved to be a one-off event that had succeeded in creating a series of major transport infrastructures, but at the cost of demonstrating unequivocally to investors that they would lose money on their speculations. Therefore, while the lure of future economic delights had proved momentarily sufficient to generate the initial portions of an underground railway system in the context of a liberal free market society, this outcome would not be repeated.

The Expectation of Providing a Public Service: 1919–1948

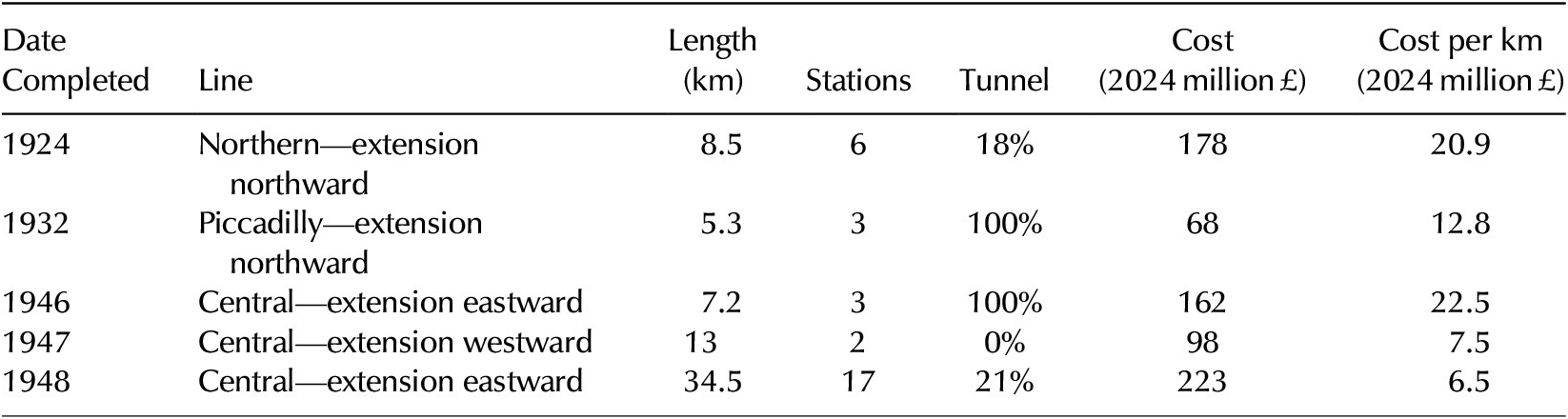

The 1920s and 1930s witnessed a very significant extension of the overground suburban railway network in London beyond the inner city (Figure 2), as well as some refurbishment of the existing underground system. These mega-projects came in two waves. The first between 1922 and 1928 constituted major renovation and minor “tidying up” of missing segments of the underground network, costing £15 million.Footnote 55 The subsequent period of activity between 1935 and 1940 combined with another brief post-war burst of completion in 1946–1948 focused on building the overground sections of the system at the cost of £40–45 million.Footnote 56 The costs varied, but broadly correlated to the extent of tunneling required (Table 2). After World War I discourse about these projects shifted markedly away from future expectations of individual monetary returns, and in the financial sphere moved toward secure, state-backed investments. There also remained a wider interest in the physicality of the system as a marvel of British engineering and architectural merit, as well as its broad social benefits for the metropolis. As such, the system became a growing symbol of prestige for London and perhaps even the British nation as a whole.

LU Pocket Map 1933, 1999–321 © TfL from the London Transport Museum collection

London underground railway projects 1924–1948

Sources: London Metropolitan Archive, Common Fund Companies, Financial Reports B Series, ACC1297/UER/4/39; Transport for London Corporate Archives, LT264/116/1 and 171/001.

The financial shift can be characterized as a move from an ex ante discounting perspective primarily looking forward at the opportunity costs of an investment and at its marginal value, to an ex post pricing perspective primarily looking backward at how meeting the costs of the assets created through investment could be averaged out across society. This is demonstrated by the prospectus issued by the London Electric Railway company to would-be investors in mid-1922. There were now no ordinary shares for sale, and guaranteed debentures at 4.5% made up the entire offering. Page two of the pamphlet offered a brief overview of the works to be carried out, and page four offered a scant half-page of financial information, mostly consisting of a simple table of the recent receipts, expenditures, and passenger traffic. We think that it is significant that the pamphlet contained no detailed discussion, surveys, or promises about future traffic and revenues.

Instead, we believe that the most important sentence in the document was on page two; it read: “His Majesty’s Government, under the provisions of the Trade Facilities Act 1921, have agreed to guarantee both the principal and the interest in respect of the present issues [of debentures].”Footnote 57 This statement reconfigured the balance of economic delight. What was being offered here was not an opportunity to speculate in a venture that might providentially at some future point transform an individual’s fortunes. Instead, the potential investor was being tendered fixed security, underwritten by central government. The government’s motives here were more social than financial. The primary intention of the Trade Facilities Act was for the state to indirectly alleviate the high level of national unemployment. It provided the taxpayer as a guarantee to private companies to encourage them to undertake major investment projects, and thereby employ workers, which would otherwise be regarded as offering insufficient financial returns.Footnote 58 In addition, in our specific case study there would also be a general benefit to the public arising from improvements in London’s transport system. Moreover, we think that the detail of the Treasury agreement with the London Electric Railway indicates the government’s confidence in the company rested on its ability to meet its obligations to service its debt on a rolling annual basis over many decades rather than repay it.Footnote 59

This approach was formalized in the London Passenger Transport Act of 1933. The Act created a public corporation board to run and develop all public transport, except mainline railways, within a 30-mile radius of central London. Section 3(1) laid out its general duties:

To secure the provision of an adequate and properly coordinated system of passenger transport for the London Passenger Transport Area… avoiding the provision of wasteful competitive services… taking such steps as they consider necessary for extending and improving the facilities… in such manner as to provide most efficiently and conveniently for the needs [of the area].

Section 3(4) went on to say:

It shall be the duty of the Board to conduct their undertaking in such manner… as to secure that their revenues shall be sufficient to defray all charges which are by this Act required to be defrayed out of the revenues of the Board.

In summary, we believe that the Board was being asked to operate efficiently but not profitably. It needed to meet its fixed obligations to pay its debtholders retrospectively, but it did not need to promise to make the value of their investments rise prospectively. To finance the second stage of the major infrastructural improvements in London’s transport system 1935–1940, the Board issued debentures through The London Electric Transport Finance Corporation. The security offered both by the Treasury and the sheer size of the Board meant that they could sell these at just a 3% discount and pay a fixed sum of only 2.5% interest annually, far lower than previous issues. The four-page pamphlet provided to potential private investors offered no information or persuasion at all about the future prospects of the London Passenger Transport Board, which were taken as read.Footnote 60 Clearly, key features of the debate around the value of transport infrastructure had moved on significantly.

We consider that the political and social discourse surrounding the projects undertaken in the 1920s and 1930s had progressed to a very different form of economic delight while still retaining some degrees of technological excitement and aesthetic pleasure, all of which can be seen in the popular and financial media of the period. To illustrate our case, we have selected two major schemes in the period as emblematic: the £14.5-million, 12.5-km (half overground, half underground) extension to the Piccadilly line completed in 1933, and the £3.5-million, 6.5-km entirely underground Central line eastern extension to Stratford, begun before the Second World War, but completed in 1946.

The Piccadilly extension proposals dated back to 1919. Until 1932 the terminus of the underground railway was at Finsbury Park where numbers of passengers at rush hours arrived far faster than trams, buses, and overground trains could take them away to further destinations. By the 1920s it was known as a notorious and increasingly dangerous bottleneck, but there was a long legal battle with the London and North-Eastern Railway who held a restrictive covenant over further transport construction in the area which was only finally and comprehensively removed by a House of Lords Committee in June 1930.Footnote 61 Fortunately, the underground railways had been able to anticipate the likely course of events and had already purchased and prepared many of the necessary sites for the extension, and by summer 1933 the entire project was complete and open for service. This was an impressive construction achievement, though a decade and half had elapsed since the need for the amenity had become pressing.

In the press, The Times was enthused, celebrating increased speeds, improved station layout, and decoration.Footnote 62 It also cast the whole project as something both patriotic and technological:

When the London Electric Railway planned the extension of the Piccadilly line, it determined that the whole of the work should be British… an experiment in mercury arc rectifiers of British design was carried out at Hendon in 1930. As a result, it was determined to equip the whole extension [with them]. The system is stated to have functioned perfectly, and its success is accepted as conspicuous disproof of the [earlier] belief propagated that it was necessary to place orders abroad for this kind of apparatus.Footnote 63

In the financial press, the issue of debentures to underwrite the construction was also viewed favorably. The Financial Times thought that:

An important point to note is that the Treasury has given an assurance that any London traffic legislation will accord adequate security to holders of these issues. The stocks yield 5.025%, running income for a reasonably long period, with a slight gain in redemption; they are trustee securities…[and] are assured of being well received.Footnote 64

The newspaper felt no need to outline the extension’s specific profit projections or say anything about London Transport’s outlook in order to endorse purchase.

Like the Piccadilly extension, proposals to lengthen the Central line eastward and northward from central London had a long antecedence before any work commenced. In late 1933 a petition by the East End London Borough of Ilford generated an internal paper by the London Passenger Transport Board into the feasibility of an “East End Tube.” Over the course of 23 pages, the report weighed up the area’s population density, probable growth, existing competing systems, and likely traffic.Footnote 65 The detailed figures and discussions of social issues were thorough, but the methods used to arrive at the conclusion that such a project would probably not yield more than a 3% return were somewhat opaque. Nevertheless, on that basis the Board rejected a proposal to extend the underground railway further east. However, by the time of the “New Works” scheme in 1935 the Board found that it could issue bonds at a mere 2.5%, justifying a project to augment the Central line eastward as part of the overall scheme on wider social grounds, even if the economics remained marginal.

The bond issues for the £40 million raised to pay for the “New Works” mega-project which included the Central line extensions were almost indistinguishable from central government debt, other than that they were marketed by The London Electric Transport Finance Corporation. Consequently, the commentary that surrounded the eventual opening of the new section of the Central line to Stratford in December 1946 was largely preoccupied with the technicalities: “This is not the place to discuss the detailed agreements and arrangements by which the schemes of transport improvements in London are to be financed” stated London Transport’s own publicity pamphlet produced to celebrate the opening the Central line extension in December 1946. It did mention that around £45 million had been spent on the whole project, but it did not detail the portion of that money which had been spent on the specific segment whose opening it was applauding.Footnote 66 The overall cost, plus the approximate calculation that 1.5 km of underground railway costs £1.5 million, was mentioned in the accompanying press release. But this too was merely presented as a fact rather than a cause for celebration or commiseration. Instead, it highlighted engineering achievements and social benefits:

These great improvements in travel facilities cannot but have significant effect on the life of the area…[now] efficiently linked by a modern system of transport making them full partners in the collective life of the metropolis. It represents a very great engineering achievement…that this intricate work was carried out without a hitch. We are entitled to take pride in the achievements of the engineers. Their fame is indeed worldwide, for the systems of New York and Moscow also benefited from their experience and skill.Footnote 67

The media was happy to re-print this commentary from London Transport uncritically. The Times reported the precise cost of the project at £3.5 million but offered no opinion on the figure. As was typical of the period, the articles marveled over the engineering, the décor, the air conditioning, and the soundproofing, before adding that: “London Transport was the finest example of transport organization in the world.”Footnote 68 In the midst of all this technological excitement, aesthetic pleasure—and patriotic bombast—we do nevertheless detect the first slight signs of concern over cost that would eventually come to overshadow much discussion about mega-projects in the later part of the twentieth century. While the price of the project as a whole was accepted without complaint, both London Transport and the wider media mentioned that the expense of 1.5 km of underground tunnel had doubled since before the war.

In summary, we think that following World War I there was an appreciable change in emphasis in how transport mega-projects in London were viewed. The justification for investment in those projects ceased to be a speculation in future financial prospects and became about wider social benefits underwritten by a fixed, secure, retrospective return. London Transport was not charged with making a profit, thereby inflating its future value to its owners, but to break even year on year balancing the interests of its passengers, employees, and debtholders. The wider language around how transport projects were described in the media also changed somewhat. Although technological excitement and aesthetic pleasure had always featured in public discourse, there was now a heavier emphasis on those benefits coupled with a strong patriotic theme. Future value, where it was discussed at all, was understood in a general, imprecise social sense as a benefit to the city or the nation as a whole.

The Expectation of Obtaining Value for Money: 1962–2000

After World War II the government recognized the need for new underground railways, specifically one linking the North-East of the capital with the West End and areas south of the River Thames (Figure 3). Other plans included a North-West to South-East line, and another East-West line, but in 1955 Parliament granted powers to start construction on the Northeastern scheme, costing the project £50 million.Footnote 69 Originally labeled “Route C,” the Chairman of London Transport chose the name “The Victoria Line” to try and personalize, legitimize, and facilitate acceptance of the project in official circles.Footnote 70 A decade and a half of discussion produced a slew of papers debating the merits of the project, gradually increasing in scope and detail.Footnote 71

LU Pocket Map 2001, 2001–53513 © TfL from the London Transport Museum collection

A significant factor in the growth in range, specificity, authority, and influence of these reports on London’s transport, especially after the early 1960s, was the formalization we noted earlier of cost-benefit analysis as fields of academic and bureaucratic activity which crystallized in America through the 1950s. In the 1960s and 1970s Cost-Benefit analysis developed rapidly in the UK, and it heavily impacted London Transport. This arose partly out of the general influence of American cost-benefit analysis on British discussion of public investment,Footnote 72 but also in a more deliberate way because in 1962 two consultants, Michael Beesley and Christopher Foster, were specifically commissioned by the chairman of London Transport to undertake a study employing this technique in support of the proposed “Victoria Line.”Footnote 73 Of these two individuals, Beesley appears to have been more important in the introduction of American-style analysis of social costs and benefits into British policymaking in general and London Transport in particular. Beesley (1924–1999), who was a self-described “Gladstonian Liberal,” had unsuccessfully stood as the Liberal candidate for the Birmingham constituency of King’s Norton before returning to the University of Birmingham, where he taught economics to commerce students. His work in conducting the cost-benefit analysis for the M1 motorway raised his national profile and led to his appointment first at the LSE and then as one of the founding Professors of London Business School. From this position, he promoted the use of novel ways of applying economic concepts to thinking about transport issues, advising the Treasury, proposing the measure that eventually became the London Congestion Charging Zone, and establishing how telecoms deregulation could take place.Footnote 74

Beesley and Foster were not the only individuals responsible for bringing cost-benefit analysis of proposed projects and ex ante discounting to Britain. Other examples of this phenomenon can be seen more generally by the extent of Nathaniel Lichfield’s work and influence in the field in Britain throughout the 1960s, following his time at the University of California, Berkeley, as well as further transport research by Foster himself and the broadening of Cost-Benefit analysis by the British economist Ezra Mishan.Footnote 75 At governmental level, the cost-benefit approach was endorsed by two white papers in 1966 and 1967. Writing in the 1970s, an economist recalled that in the 1960s it became standard in Whitehall departments for civil servants “to be packed off to a Centre for Administrative Studies for a quick injection of cost-benefit analysis and quantitative Techniques.”Footnote 76 The 1967 paper called for a cut-off discount rate of 8% for any public project, and subsequent responses to the government’s papers in academia called for a yet more detailed, codified, and standardized approach along the lines of American “Green Book.”Footnote 77 Eventually, the British Treasury would produce its own Green Book, a revised version of which continues to inform decisions about proposed infrastructure projects. Regarding our specific case study, it is also interesting to note that one of Michael Beesley’s PhD students and frequent visitor to Foster’s Oxford research unit was David Qwarmby, later the Managing Director of London Transport’s Road Operations. We think that cost-benefit analysis techniques were absorbed early and fully regarding London’s transport.

This new level and dimension of debate formally arrived in 1963 via Foster and Beesley’s academic study purporting to rationally analyze the costs and benefits of the proposed “Victoria Line” underground railway from an expansive perspective that included social benefits.Footnote 78 We argue that the depth and extent of their analysis set new standards and expectations of future justifications for government investment which then made their appearance in all subsequent projects.Footnote 79 Where there were criticisms of the paper, these were principally that the researchers had not gone far enough in trying to encompass all the possible benefits and detriments that building the Victoria line might give rise to.Footnote 80 Herein, we argue, was one of two major problems which the publication of their articles crystallized. The first was that for all their analytical sophistication, their overall framing was in fact a regression back to the shareholders’ prospectuses which had enticed investors in the early twentieth century in the sense that cost-benefit analysis also attempted to raise money by trying to plausibly demonstrate the existence of socio-economic gains ex ante. The second was that no matter how thorough the analytical approach, there was an inexhaustible supply of possible benefits to debate and a boundless number of queries that might be raised regarding the suitability of methodologies to assess them.

The problems inherent in attempts to objectify future social benefits were compounded by the emergence of central government as a single “investor” or decision maker for the nation at large, as it was subject to the vagaries of expedient pressures from a huge number of competing claimants. Moreover, after the 1967 devaluation of the pound the Treasury became markedly more conservative and risk adverse in its willingness to undertake major public investments.Footnote 81 We think that the Foster and Beesley approach had unwittingly, but significantly, escalated and normalized a scenario where London Transport was a supplicant to a single investor. Moreover, it now had to make the case that an investment in a specific infrastructure would give rise to future benefits, greater than a universal and arbitrary Treasury discount rate, based on a limitless range of supposedly calculable potential trade-offs, all of which were open to methodological challenge.

Nevertheless, the press and public reactions to the opening of the Victoria line in 1969 and its extension in 1972 were generally positive. The Telegraph announced its completion, mentioning the new automated ticketing system and the design of the tiles decorating each station. The cost of £70 million was noted but not commented on,Footnote 82 though the Queen’s difficulties in paying for her fare at an automatic machine provoked a column that was more skeptical of the new technology than London Transport’s press releases had eulogized over.Footnote 83 The Economist headline “At last - the Victoria line” told its own story about perceived project delays, while like The Telegraph its commentary also pivoted between the celebratory; “Automation will provide a 20% faster service” and the cautious “Automatic collectors will pay for themselves by catching fare dodgers, but they will have a long way to go before they start paying off the £70 million the line has cost so far.”Footnote 84 The Financial Times framing was more supportive: “Money well spent on public service,” though its subsequent analysis under the column headings “Planners complaint,” “Incompatible objectives,” and “Will not pay” were indicative of a more disbelieving detailed analysis.Footnote 85 Another article in the Financial Times on the same day raised questions about the cost-benefit study used to justify the line:

It is easy to pick holes in the Victoria line type cost-benefit analysis…The calculations often appear so arbitrary that virtually any type of project could be justified. The extreme dependence on speculative calculations about time savings…can produce very questionable results. Nevertheless, cost-benefit techniques are still improving [and] they will certainly play an increasingly important role in decisions like the Victoria line one.Footnote 86

The endless opportunities for the expansion of cost-benefit analyses attempting to prove a greater rate of future return than a standard central government discount rate—which itself varied over time—also appeared in the proliferation of the subsequent documents debating both the construction of original Jubilee Line which opened in 1979, and its extension which opened in 1999. Originally termed “The Fleet Line,” proposals and planning began in the mid-1960s for a new underground railway running roughly from the north-west of central London across the central area, and then south-eastward along the line of the River Thames toward the docklands area.Footnote 87 However, only a much shorter line transversing just the central area was completed in the 1970s and stages two and three of the project were abandoned. We think that from the outset, the public and political conditions in which the project took place were firmly set in an ex ante expectation of proving future gains. The correspondence between the chairman of London Transport and the Minister of Transport shows that disputes over financial forecasting escalated quickly after work began in 1971. In late 1972 the chairman wrote:

I recognise that on the basis of the methodology and the scale of values at present applied to the social cost/benefit analysis by your department and the Treasury, the present discounted values of the Fleet Line may not reach an acceptable level. But I believe that this would be true of any new underground railway…and that to base future policy on this method of appraisal would lead to the conclusion that no more underground lines should be built!

In early 1973 the chairman wrote again:

You say that you had been embarrassed by the degree of underestimation in our original figures…[but] of this increase of £8million, £7million is attributable to inflation…I am wholly convinced that no-one could or should have predicted such an increase, and if they had, your staff would not have believed them.Footnote 88

In June 1973 the Minister replied:

I accept, though with reluctance, that the major part of the increases result from inflation which it would have been difficult for your staff to foresee…so, whilst I must stress again the need for you to do everything possible to eliminate or reduce such increases to the lowest possible level, I agree to pay the grant…[with] two exceptions.Footnote 89

Disputes like these had, of course, occurred on previous projects. The change we consider visible in the Way-Peyton letters is the intensity with which expenditure was being monitored and the level of detail with which London Transport’s forecasts were being carefully and critically scrutinized. Grants would be reluctantly dispensed on a case-by-case basis where each request had to prove its future benefits against its opportunity costs.

This rather grudging atmosphere bled into the public realm via the media. When the re-christened “Jubilee” line opened in 1979, The Economist had this to say:

London got a new underground rail line this week: The 14-mile Jubilee Line. Of the 14 miles, only 2.75 are new, the rest being part of the old Bakerloo line re-named. The ticket was £87million and the first train was 18 months late.Footnote 90

The Financial Times published the briefest of notes that work had started eight years previously and that the project had cost £87 million, twice the cost budgeted for in 1971.Footnote 91 It was a very different verdict from the “Public money well spent” headline with which they had greeted the Victoria line ten years previously.Footnote 92 Thus, the “new” Jubilee line was portrayed as truncated, delayed, and over budget, all enduring themes in Flyvberg’s observations about the disappointing history of mega-projects.

The story of its extension in the 1990s unfolded in much the same way. Once again, there was a torrent of discussion papers and cost-benefit analyses from consultants preceding and during construction.Footnote 93 These attempted to prove the project’s future value to a skeptical Treasury, whose tests of social and economic viability shifted frequently as Britain’s wider economy moved in and out of growth. As the scheme was debated, the projected costs grew from £1.3 billion to £1.9 billion, and then to £2.1 billion. In the end, the Jubilee line cost £3.5 billion to construct.Footnote 94 Nevertheless, the project was completed just in time for the millennium, and its scale and architectural magnificence did win it technological and aesthetic plaudits.Footnote 95 However, neither this nor the close attention paid to the process of cost-benefit analysis was sufficient to protect the project from intense criticism over its cost overrun of £1.5 billion and a two-year delay in opening.Footnote 96

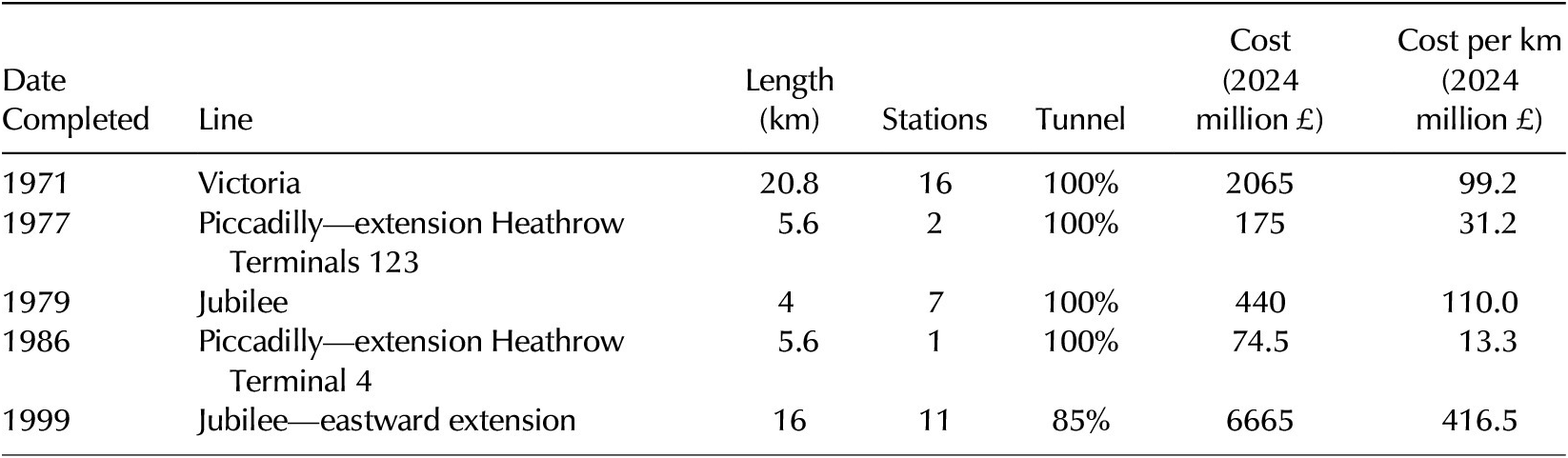

Costs in this period varied wildly, though there appears to be some connection with the number of stations required in each project (Table 3). However, we argue that between 1962 and 1979 a combination of much more important attitudinal factors changed the attitude toward transport infrastructure projects profoundly, and in favor of speculative cost-benefit analyses. The first was macro-economic. The devaluation crisis of 1967, the oil price shock of 1973, and the IMF crisis of 1976 all legitimized and accelerated skepticism and hostility in the Treasury toward the ex post view of major investment projects as sunk costs whose subsequent prices for the services provided only had to retrospectively cover their annual expenditures on a rolling basis.Footnote 97 This coincided with a second factor that emerged in the 1960s reflecting Morris’ narrative about the arrival of recognizably modern project management based on complex systems; a strong techno-rationalist belief, originating in the United States, that academics could provide objective data at a level of detail and virtuosity sufficient to prove both an economic and rational social case for bureaucrats to make apparently apolitical policy. Perhaps unwittingly, this bold claim cast project proposals back into an ex ante narrative of investment as something that must be justified by future returns, albeit in a different, and in some ways more problematic, form than in the early twentieth century.

London underground railway projects 1971–1999

Sources: Croome and Jackson (Reference Croome and Jackson1993), Rails Through the Clay, London: Capital; Horne (2007), The Piccadilly Tube: Capital; Transport for London Corporate Archives, LT111/001/005

Conclusions

Our narrative history and explanation of the changing debate over public transport infrastructure costs contain significant continuities. The intensity of criticism over how poor Britain’s performance is at building transport facilities is recent,Footnote 98 but the archives reveal that realities of delay and expense are not new: The Bakerloo line was a proposal established in 1893, and it eventually opened in 1906 after a succession of crises. The case for the northern extension of the Piccadilly line was first made in 1920, and it was completed in 1933. The Victoria line was mooted from 1948 onward, and it was, mostly, finished in 1969. Nevertheless, we think that there are also clear narrative discontinuities. In London Transport’s case, we think this is better explained by a series of changes in perceptions and discourses than the material facts of each project. When the Bakerloo line opened in 1906 it was obviously much delayed and almost certainly over its original budget. Yet the owners, the media, and the public were not dismayed. They were concerned with future usage and ex ante anticipated earnings, combined with a certain amount of technological excitement and aesthetic pleasure.

These speculative financial hopes were misguided, and after World War I the nature of economic expectations changed completely. London’s transport infrastructure projects were underwritten by secure fixed-interest bonds. Nobody would ever “get rich” by owning them, but equally they could be certain of a steady income. Backed by central government, these infrastructures’ future prospects were held to be as secure as the nation itself, and indeed we believe that these projects came to be viewed almost as embodiments of Britain, its prowess, and its technical achievement. As such, the generalized benefits of transport infrastructure to society were taken as read, and London Transport was required to operate efficiently rather than profitably, meaning that it charged for its services so that its income met its annual expenditures but no more. Ex post pricing had replaced ex ante discounting as the frame through which to appraise and approve investment in infrastructure.

From the mid-1960s the narrative changed again. The Treasury had a lengthy tradition of disliking retrospective average-cost pricing which it associated with wasteful nationalization, and a series of economic crises allowed it to insist after 1967 that cost-benefit analysis, discounting, opportunity costs, and marginal cost pricing should be the bases on which investment proposals were considered. This long-standing agenda was bolstered in the same period by developments from America in the sophistication, scope, and legitimacy of cost-benefit analyses. Social scientists joined welfare economists to claim that it was intellectually serious and practically useful to quantify the social benefits of public projects, even if that meant, however implausibly, making projections of future relative prices. As the economist Peter Self observed in a 1975 discussion of the rise of cost-benefit analysis: “Paradoxically the economist is now being called upon to achieve through his art what the market system was supposed to do by the light of nature.”Footnote 99 The art of persuading central government has become extremely lengthy and expensive, generating a myriad of analyses and consultations; moreover, picking over the detail provided in this torrent of documentation allows ample scope for challenge, delay, and a narrative of disappointed hopes to take shape in the media as projects fall behind the promised schedule and over budget. This increasingly contentious and complex modern story masks the reality that the objective costs and timeframes of the projects themselves, at least for London’s transport, have more in common with the past than is generally acknowledged.

Acknowledgments

This paper benefited from BA/Leverhulme Small Research Grant SG2122/210400 as well as the comments of colleagues at the British Academy of Management conference in 2024 and the Association of Business Historians conference in 2025.

Open access

Open access