1. Introduction

Public controversies are often channelled into constitutional narratives, including issues that arise in the tax discourse.Footnote 1 The public sphere encompasses encounters between tax issues that have entered constitutional discourse and, conversely, constitutional issues that have spilled over into tax discourse.Footnote 2 From a narrative perspective, prevailing tax narratives are generally incapable of translating or communicating issues that lie outside tax discourse and are articulated within a constitutional discourse. This article challenges that pattern by proposing a tax-based approach to one of Israel’s most contentious constitutional crises – the unequal burden of mandatory military service.

Deep disagreements about inequality are a well-known phenomenon in many societies which face the challenge of quantitatively measuring or estimating the harm to equality. Constitutional discourse frames conscription inequality as a fairness issue but, in general, offers no feasible and reasonable method of quantifying it. By shifting the discussion to a tax discourse, we develop a framework that will measure inequality. Mandatory military service functions as a tax in-kind in that it is an imposed obligation that carries an economic burden similar to monetary taxation. Although, politically, tax discourse focuses traditionally on classical tax regimes (such as income tax and value-added tax), there is room to extend it to taxes in-kind, like conscription. Even if the proposed framework is not adopted into legislation, it is crucial for understanding the extent of inequality in the constitutional debate over mandatory service.

Israeli society is broadly divided into four main groups – ultra-Orthodox, secular, religious, and non-Jewish minorities – yet only the secular and religious communities are broadly subject to conscription.Footnote 3 The exemption of ultra-Orthodox men, initially a small-scale arrangement,Footnote 4 has escalated into a significant legal and political crisis, exacerbated by Israel’s Supreme Court rulings striking down legislative attempts to address the issue on constitutional grounds based on inequality,Footnote 5 as those attempts exempt many young persons from military service and shorten its duration dramatically for others. The constitutional framework, therefore, has been unable to produce a politically viable resolution. This failure stems mainly from a fundamental ethos – the ‘people’s army’ – which sees service as a civic duty, based on social and cultural narratives, rather than a quantifiable economic burden, based on economic narrative. Framing conscription solely within constitutional discourse has entrenched the political divide rather than offering a path towards resolution.

This article proposes a regime that can serve as the essential foundation in a complex, multi-faceted solution aimed at reducing military inequality in Israeli society, acknowledging that universal conscription is politically and socially infeasible. Even a volunteer army that eliminates general conscription is not a viable solution, mainly because of the ethos of a ‘people’s army'. This ethos also prevents appropriate market-based compensation for recruits. Tax discourse provides a way to bridge this divide by reframing military service in economic terms. This approach draws on cognitive biases observed in other contexts. Applying the observed framing effect of tax expenditure to military service, the use of the tax regime may serve as an alternative to direct payments that might be rejected because of the ethos of a ‘people’s army’. Hence, we propose a mandatory army tax credit (MATC), compensating conscripts through future tax credits equal to the tax in-kind embodied within the mandatory army service. This mechanism acknowledges the economic disparity between those who serve and those who do not, while preserving the ethos.

The inequality issue has been reflected in the recent war in Gaza, and the military’s manpower shortages have reignited the conscription debate. While the MATC will not resolve completely the enlistment crisis, especially the manpower shortage, it can help to mitigate and alleviate the inequality, and facilitate a more balanced and equal arrangement. The insights of this article extend beyond Israel. Countries with mandatory military service worldwide, particularly in the light of rising security tensions, such as in Eastern Europe, face similar questions: should conscription be managed solely through constitutional or tax-based solutions? Treating military service as a tax in-kind may provide a more effective and measurable approach.

The proposed approach is relevant when measuring the tax burden at the national level and in international comparisons. The traditional measurement, which includes only monetary taxes calculated based on cash flow collection, is incomplete as it does not account for in-kind taxes, such as mandatory military service that is not compensated at market value. Additionally, this approach highlights the limitations of conventional tax burden measurements, which may overlook significant non-monetary contributions imposed by the state. By incorporating in-kind obligations into the analysis, a more comprehensive and accurate representation of the total tax burden can be achieved.Footnote 6

The article proceeds as follows. Section 2 explores military service in Israel and the inequality crisis it presents. Section 3 discusses the ethos of the ‘people’s army’, its historical development, and the growing dissonance between it and reality. The discussion shifts from a constitutional to a tax discourse in Section 4, explaining why mandatory military service can be considered a tax in-kind. The MATC regime is introduced in Section 5 as a proposed solution to address these inequalities. Section 6 explains why a tax discourse, through a tax credit regime, is effective in addressing the ethos of the ‘people’s army’ and the associated inequalities, using the framing effect. Section 7 presents the database, the empirical findings on the extent of inequality in military service participation revealed through the MATC regime, using a detailed database to support the analysis and a discussion regarding the highly inequitable consequences that emerge from the findings. Concluding remarks are given in Section 8, emphasising that incorporating a tax discourse can significantly alleviate the inequality crisis.

2. Military service in Israel: The inequality crisis

2.1. In general: Military service in Israel

The personnel comprising the Israel Defense Forces (IDF), Israel’s army, consist of three main groups.Footnote 7 The first group includes the recruits, for whom mandatory conscription requires men to serve in the IDF for 32 months and women to serve for 24 months.Footnote 8 The second group is the permanent army. It is composed mainly of career soldiers, including officers of all ranks, who have chosen to continue serving in the IDF after concluding their mandatory service. The third group includes reserve soldiers whose main role is performed during times of war.Footnote 9 Current estimates, according to foreign sources, indicate that there are approximately 170,000 active personnel and 465,000 reservists.Footnote 10

2.2. The inequality crisis

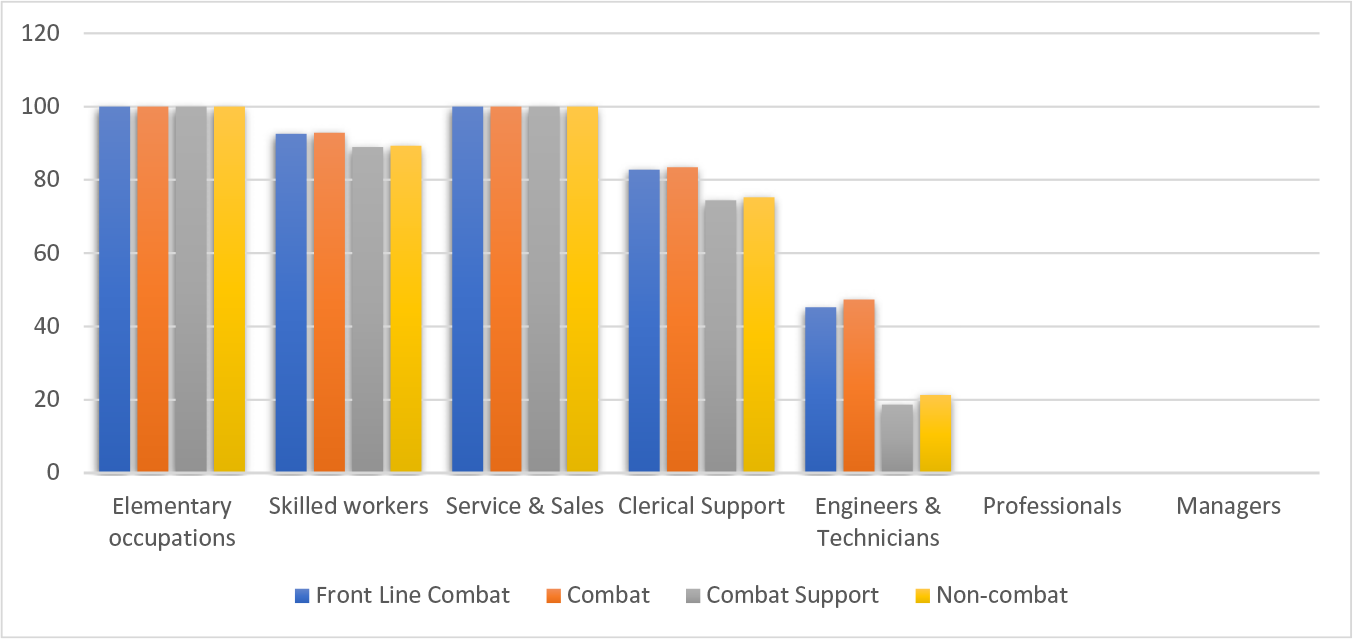

Israeli society is dealing with a major issue of inequality in the burden of military service. This is evident from the growing percentage of the annual cohort receiving exemptions from military service.Footnote 11 Large sections of society do not enlist, with only 44% of the annual cohort enlisting.

The 2022 draft-eligible population figures were drawn from an official Knesset report. This report provided a demographic breakdown distinguishing between Jewish and non-Jewish minorities, as well as detailing the percentage of exemptions granted within the Jewish population.Footnote 12 Additionally, most non-Jewish minorities are exempt from military service.Footnote 13 According to the state comptroller, in 2021 17.6% of Jewish males received exemptions based on ultra-Orthodox status, 8.8% for medical reasons, 1.5% on account of being deemed unfit for service or having adaptability issues, 0.1% following a ‘special decision,’ 0.7% as a result of criminal records, 2.4% for residing outside Israel, and 0.3% for choosing civil service as an alternative.Footnote 14 Notably, the Israeli public is generally more accepting of the fact that religious Jewish women are exempt from military service.

Enrolment percentages (2022, %)

This severe inequality is recognised, by both the public and the legal system, as a purely constitutional issue.Footnote 15 It has never been discussed through a tax-based lens, even though mandatory army service is a tax in-kind.Footnote 16 To understand more deeply the Israeli conflict regarding conscription we must delve into the cultural depths of the Israeli perception of the IDF: the ethos of the ‘people’s army’. This ethos dominates the public discourse revolving around conscription.

3. The Meta principle: The ethos of the people’s army

3.1. The development of the ethos

To understand the inability to shift the IDF to a volunteer army, or to retain the current model and raise the compensation given to soldiers to a level that reflects the real value of their service, the article will delve into one of the most important cultural aspects of Israel from its establishment to this day.

As Israel declared independence in 1948, battles were already occurring on its borders, making a universal draft essential for survival.Footnote 17 The politcal leadership, holding collectivist and socialist views, rejected the conservative notion of a volunteer army and strongly promoted the idea of a ‘people’s army’. Between 1947 and 1960, Israel’s Jewish population more than tripled, with 1.5 million immigrants from diverse backgrounds becoming citizens.Footnote 18 The scale of immigration and the need for IDF manpower led Prime Minister Ben Gurion to see the IDF as a ‘melting pot’ for the population.Footnote 19 This vision for the IDF had three key elements: (i) defending the state; (ii) maintaining a universal and equal draft, with every eligible individual receiving the same opportunities with non-market value compensation; and (iii) participating in national missions beyond security.Footnote 20

Over the years, Israel has endured a great deal, from political crises to wars, yet the fundamental concept of the IDF as the ‘people’s army’ remains a cornerstone of public discourse.Footnote 21 The ‘people’s army’ concept is now synonymous with the IDF itself. Speeches given by IDF commanders attest to the ongoing significance that the army places on preserving and nurturing this idea.Footnote 22 The term that defines the relationship between the IDF and this concept is ‘ethos’, which the Oxford Dictionary defines as ‘the characteristic spirit of a people, community, culture, or era as manifested in its attitudes and aspirations; the prevailing character of an institution or system’.Footnote 23 This definition captures the situation in Israeli society, where the ‘people’s army’ has evolved into an ethos over the years.Footnote 24

The ethos of the ‘people’s army’ has, in today’s meaning, three key dimensions.Footnote 25 The first is a universal compulsory draft, reflected in Israeli laws under which the entire annual cohort is required to enlist at the age of 18 (the universal dimension). The second is modest compensation for service, below fair market value (FMV), ensuring that the IDF is not a ‘mercenary army’, meaning that military service is not part of the labour market (the non-FMV compensation dimension). The third is the IDF’s association with values like statism, patriotism, diversity and collectivism in Israeli society (the societal dimension).Footnote 26 This ethos is crucial for sustaining the mandatory recruitment model.

The ethos of a ‘people’s army’ has dominated for decades, despite the growing dissonance between reality and its ideals. The main cause is the sharp decline in conscription, now below 50% of the annual cohort.Footnote 27 With the natural growth of the ultra-Orthodox and minority populations who do not enlist, the percentage of conscripts is likely to continue to fall.Footnote 28 This low rate deepens the growing dissonance in the societal dimension of the ethos. Soldier remuneration has increased to compensate for service and show public appreciation,Footnote 29 but it remains significantly below market value as a result of the non-FMV compensation dimension of the ethos. Public discourse still supports mandatory conscription and resists a voluntary army, despite the growing dissonance and inequality. In other words, the ‘people’s army’ ethos is still seen as the dominant factor in the public debate regarding the desirable army model.

3.2. The challenge: Ethos v inequality

Israeli society is struggling with the ongoing tension between the ethos of a ‘people’s army’ and the growing inequality in military service participation. Imposing mandatory service on the entire annual cohort is unrealistic given the political, social and religious realities, and will probably remain so in the future.Footnote 30 At the same time, despite the increasing influence of libertarian and economic views supporting such a model,Footnote 31 transitioning to a volunteer army is not viable because of the enduring ethos of a ‘people’s army’.Footnote 32

The ethos remains firm on mandatory conscription but in recent years is showing flexibility regarding conscripts’ living allowances, reflected in the policy of increasing the allowance for all service groups, thereby reducing inequality.Footnote 33 This increase indirectly reduces the scope of the public criticism of the ‘people’s army’ that the ethos faces on the inequality front, actually preventing the complete collapse of the ethos. The increase, however, does not reach FMV wages for their service: in accordance with the ‘people’s army’ ethos, soldiers cannot be compensated by FMV payments because it conflicts with the ethos.Footnote 34

In the foreseeable future, the current conscription regime will change at most in three ways: (i) extending the compulsory service period for many soldiers,Footnote 35 (ii) drafting small portions of non-enlisting sectors,Footnote 36 and (iii) increasing compensation for compulsory service,Footnote 37 noting that the ethos of the ‘people’s army’ will not permit FMV payments. These three changes leave inequality on the agenda in terms of the extended service period, non-universal conscription, and in terms of the non-granting of FMV compensation. Therefore, the issue, which has been hovering over the public discourse for a long time, arises: how does the public simultaneously address inequality and the ethos of a people’s army?

The current legal discourse revolving around the issue of the inequality of mandatory conscription is of a constitutional nature. As mentioned earlier,Footnote 38 the constitutional debate has persisted for many decades without leading to even a partial resolution; if anything, it has only grown more intense over time. This is in part because of the limits of the constitutional discourse when facing the unique political circumstances of this issue. This article, therefore, proposes to ‘change the lens’ by looking at the issue from a new angle, the tax angle. The tax discourse has real potential to create a new regime that will be able substantially to alleviate inequality, by providing a significant and reasonable regime, which could be defined as constitutional by Israel’s Supreme Court.Footnote 39

4. Moving from a constitutional to a tax discourse

4.1. Why is mandatory military service considered a tax?

Prima facie, mandatory military service is not typically regarded as a form of taxation within the modern social order. Classical, prevalent tax regimes rely on monetary payments from the public to the state treasury, and the prominent examples are tax based on income (such as income tax or capital gains tax) and tax based on consumption (value added tax, for example). However, one can conceive of a tax regime that obligates taxpayers to provide the state with goods or services of an equivalent value. This tax in-kind regime is ancient,Footnote 40 and modern tax regimes have shifted towards monetary payments. The foundational framework of our tax discourse, which serves as the cornerstone of our analysis, is that mandatory military service is, first and foremost, a tax in-kind regime.

Why is mandatory military service a tax in-kind? Suppose a municipality has the authority to impose a cleaning tax of $100 per resident to fund the cleaning of the city streets. Instead, it may impose a cleaning duty on every resident, establishing a municipal rotation system whereby each resident is occasionally required to perform cleaning duties on the street where they live. In both alternatives, there is a forced transfer of resources from the resident to the authority. Both alternatives constitute a tax.Footnote 41 The first alternative is a tax paid through cash payment. The second alternative is a tax in-kind: a 100% tax is imposed on human capital return, by the forced appropriation of the resident’s cleaning work and its transfer to the authority’s jurisdiction. This appropriation is expressed by the forcible seizure of the return on the resident’s human capital produced by cleaning services.

One of the most notable exceptions in modern times to the classic tax regime based on monetary payments is compulsory military service. The tax that an individual pays upon being conscripted into the army consists basically of two main components. The first component of the tax taken from an individual during forced military service is the net (after tax) FMV wage for the service that the conscript provides to the army minus the payments actually received from the army for compulsory military service. The second component is the economic value of the violation of human rights that are taken from soldiers during their mandatory service – such as the right to life, the right to bodily integrity and freedom of expression. The measurement of human rights violations and the FMV of the soldier’s service component is a substantive challenge.

4.2. Measuring the mandatory army tax: Methodological issues and a simplified approach

In analysing the economic literature on developing a methodology for assessing the amount of the tax in-kind paid by those in mandatory service, three fundamental tensions emerge. They present choices and raise complex questions that must be addressed in any such methodology. The first tension is between opportunity cost and actual income: should the tax be measured by the opportunity cost (the salary a conscript would earn if not serving in the military) or by the FMV wage of the military profession in which they are engaged as a conscript?Footnote 42 The second tension concerns the perspective on the individual’s preferences: should one consider how much an individual would pay to avoid mandatory military service, or how much compensation would be required for an individual to serve willingly?Footnote 43 The third tension is between the individual and society: should the tax be measured based on the individual perspective, or according to the overall cost to society?Footnote 44

Resolving the issues that arise from these basic tensions is difficult theoretically and practically. In order to advance the proposed regime in the public sphere, simplification is one of the main foundations of the proposed regime. We do not rule out other methods of calculation but, for the sake of the discussion, we choose the most direct and straightforward way. This work is intended primarily to create a new agenda for decision-makers and, therefore, the proposed model must be simple and feasible. Using complicated and theoretical approaches requires a more complex analysis,Footnote 45 which is inappropriate for the current stage of the public discourse regarding ideas even remotely similar to ours. In addition, addressing a complex analysis may steer the discussion away from the substantiality and essentiality of the proposed regime to a methodological discussion, secondary in importance. As a result of our simplifying approach, the proposed tax regime measures the size of the tax in-kind by referring to the FMV of an individual’s army profession.Footnote 46 The proposed model is applicable based on the database presented below.Footnote 47

Generally, mandatory military professions are very specialised. Theoretically, in most cases it is a substantial challenge to determine FMV wages. In our case, however, the army structure makes it possible to successfully address this challenge because of the existence of the permanent army alongside the mandatory army. The data includes the wages of the volunteer army (permanent army) for military professions similar to the mandatory army’s professions and it enables determination of the FMV wages of the mandatory army’s professions.Footnote 48 This measurement mechanism internalises, inter alia, the risk to the recruit’s life, physical and mental wellbeing, and the military lifestyle. However, it disregards the compulsory component associated with mandatory service. Assessing the compulsory component and the value of training presents challenges and, for this reason, it is not a component figured into the calculation of the mandatory army tax (MAT).Footnote 49 Estimating additional costs is difficult, but it should not prevent us from addressing measurable tax-related variables. Dismissing significant factors just because others cannot be measured is illogical. The proposal does not aim to resolve the entire issue but seeks to ease constitutional tensions and open the door to political solutions, even without full equality in burden-sharing. In the current political deadlock, this step is vital.

The FMV of the wage during the entire period of mandatory service in the proposed model is based on wages in the permanent army, which are FMV wages, as follows. Typically, service in the permanent army begins immediately upon completion of mandatory service. As a result, the FMV of the wage at the end of mandatory service is equated with the starting wage of permanent army personnel. Hence, the wage used in the proposed regime is the wage at the start of the first year in the permanent army (usually at the age of 21) as the baseline FMV wage, and adjusts it backwards by a factor (hereinafter, ‘the factor’) of one year to age 20,Footnote 50 and then takes the FMV wage for age 20 and adjusts it backwards to ages 19 and 18, using the factor.Footnote 51 The advantage of this model is that it is a complete military professions-based approach and our analysis connects with the same professions in the permanent army and the mandatory army.

5. The proposed tax regime: MATC

The transition to a tax discourse means addressing the inequality through a new tax regime. Under the proposed regime, soldiers serving in the mandatory army will be entitled to claim a tax credit for the tax they paid during the mandatory service, the MAT.Footnote 52 The MAT is the net FMV wage that a conscript would have received, minus the total remuneration a soldier receives in the mandatory army and the tax that would be paid on the FMV wage if he worked.Footnote 53 For example, assume that the FMV wage of John, a mandatory army soldier, is 10,000 and he receives 4,000 as remunerationFootnote 54 for his mandatory army service. The tax he would have paid on the FMV wage if he worked and earned 10,000 as his wage (FMV wage) is 2,000. Therefore, John pays 4,000 (6,000 minus 2,000) as tax in-kind by forcibly serving in the military.

The MAT is the concrete expression of the inequality in the tax discourse. How does the erosion of inequality occur through the tax discourse? Inequality can be substantially eroded via the tax discourse in two ways. The first is by imposing on those who do not enlist an equal tax burden. This alternative resembles the practice in several countries, now and in the past, where individuals who do not enlist ‘redeem’ themselves by paying a monetary sum.Footnote 55 This approach faces challenges in both practical and theoretical terms when it comes to determining the precise tax liability for each non-enlisted individual. As a result, a lump sum amount – a poll tax – may be imposed, which comprises roughly both efficiency and fairness in the system. However, delving deeper into this alternative is unnecessary given its impracticality in the Israeli context. The two primary groups that abstain from enlistment – the ultra-Orthodox and minority communities – are situated within the lower income deciles in Israel,Footnote 56 and as such are unable to shoulder the complete burden of such a tax. The second alternative suggests reimbursing the MAT. Theoretically, a soldier can be reimbursed every month, annually or at the end of their service. However, again, under the perspective of the ‘people’s army’ ethos, if the timing of the reimbursement is too close in time to the military service, it might have a significant impact on this ethos in a way that could harm it. Payments during military service at its end, or even shortly after completion, could portray the reimbursement as payment for the military service in a manner that negatively affects the ‘people’s army’ ethos. Therefore, our model proposes that the MAT would be reimbursed to the soldier/taxpayer via a military army tax credit (MATC) regime. This regime would effectively erode the inequality that exists with regard to mandatory army service. The proposed MATC regime, as detailed below,Footnote 57 adopts a multi-year tax credit mechanism, to utilise the tax credit. As elaborated below, the paradigm of ‘tax expenditure’ bias enables legislating for the MATC despite the ‘people’s army’ ethos, and the disconnect of the tax credit flow from the time of service strengthens the ability to use the MATC without harming the ethos.Footnote 58

6. Why does the use of a tax discourse succeed in addressing the ethos and consequently inequality?

6.1. In general

The economic alternative of reducing inequality by directly compensating soldiers according to their FMV wage seems a more natural and reasonable approach, but is rejected because of the ‘people’s army’ ethos.Footnote 59 Economically, there is usually no difference between compensation through taxes and direct compensation through wages. After all, direct expenditures by government or government waiver of tax collection are basically the same financially.Footnote 60 In addition, there is the argument that the tax system is generally less efficient in allocating resources than in direct government payments.Footnote 61 If so, why reframe the discourse as a tax discourse, and propose a model that uses the tax system to reduce inequality rather than conduct the discourse within a classic constitutional framework focusing on violation of inequality and, under the circumstances, seek to rectify inequality by directly compensating with a market wage? In other words, why is direct compensation at FMV infeasible by the ‘people’s army’ ethos while the proposed tax credit regime is not, especially when one of the fundamental variables in calculating the tax in-kind is the FMV wage for soldiers’ mandatory service?

6.2. The framing effect: Tax expenditures v direct governmental expenses

The paradigm on which the proposed tax regime is based states that using a tax credit regime is perceived differently by the public compared with direct governmental payments. The literature on cognitive biases (such as in behavioural economics) explains this difference and legislators, globally, have been using such tools for more effective regulation.Footnote 62 One theory regarding cognitive biases introduces the concept of the ‘framing effect’. Briefly, this effect examines human responses to identical hypothetical scenarios framed in different ways and shows that the different framing changes people’s choices.Footnote 63 The concept was coined by Tversky and Kahneman in a series of well-known experiments.Footnote 64 One example of the framing effect as a cognitive bias is the preference found in the public perception regarding tax expenditure compared to direct government spending, despite the similarity of these two alternatives. Applying this framing effect to our analysis leads to the proposed tax regime. The tax credit mechanism as compensation for conscript soldiers compared to direct payments stems from a framing effect that exists among the general public regarding tax expenditure versus direct compensation. The phenomenon holds even when the public is informed that the two alternatives are economically identical.Footnote 65

Zelinsky investigated the framing effect produced by tax expenditure versus direct grants. In the study Zelinsky examined tax benefits given to firefighters in several US states. He investigated whether the framing effect could explain why communities sought to maintain their firefighters as volunteers using tax benefits instead of direct payments, even though economically they are similar. His research considered a phenomenon found in many communities in the US, where, for years, it was accepted that the local community fire department was staffed by volunteer firefighters who donated their free time to this endeavour. The ageing of the baby boomer generation and the younger generation’s unwillingness to continue volunteering for the fire department, combined with the increasing complexity of fire extinguishing equipment and training, led to a serious shortage of firefighters in many communities.Footnote 66 Why, then, did these communities not switch to a model of hiring firefighters for pay? Given the challenges of equipment and lack of volunteer manpower, the obvious solution is market wages. Zelinsky argues that ‘[t]here is powerful, indeed iconic, imagery underpinning the appeal of the citizen-volunteer, a modern-day Cincinnatus who drops his civilian role in the face of emergency, fights fire, and then returns to his regular job’.Footnote 67 This deep-rooted cultural perception led communities to prefer volunteer firefighters and reject hiring firefighters for pay. A solution was found in the tax discourse. Volunteers were offered property tax benefits. Essentially, there is no doubt that by receiving tax benefits, firefighters lose their status as volunteers from any objective point of view. This phenomenon shows that these communities distinguished between tax benefits and direct payments. According to Zelinsky, based on empirical research, this community behaviour stems from the framing effect, and allows volunteer firefighters to receive payment (in-kind) while retaining their voluntary status.Footnote 68

Several disciplines – mainly, psychology, political science and (behavioural) economics – have provided explanations for this effect. Some of these explanations stem from the political perceptions about the institution of ‘tax’: namely, the political view of ‘pre-tax income’ in which a tax benefit does not ‘give’ something new to taxpayers but returns what belonged to them before.Footnote 69 Some scholars have based this on, or connected it with people’s cognitive bias of loss aversion, in which the public perspective of tax liabilities is considered a loss, thus making tax benefits a form of loss aversion preferable to direct payments.Footnote 70 Another approach explained that the public preference for tax-based programmes could be attributed to opportunity cost neglect. Tax expenditures, being less transparent about their opportunity costs, could potentially explain why the public tends to favour such programmes.Footnote 71

The phenomenon of the framing effect can be applied to our analysis as well. The framing effect with reference to the use of tax benefits versus direct payments, as shown by Zelinsky, supports the proposed tax regime. Zelinsky’s research on the influence of the framing effect, which shows that tax discourse (tax benefits) allows for the preservation of the volunteer ethos in contrast to receiving direct wages, strongly supports our approach, in which tax expenditures ease the tension between inequality and the ethos of the ‘people’s army’ (the feature of receiving non-market-value wages [‘volunteering’]). According to this research the proposed regime could be satisfied by granting tax credits that are equal economically to the FMV wages throughout compulsory military service. However, in practice, soldiers do not earn a taxable income during their mandatory military service that would enable them to utilise these credits. Therefore, the regime uses a multi-year tax credit mechanism. In doing so, the proposed regime further reinforces the bias by distancing the payment even more from the time of military service, thereby diminishing the impact of economic compensation on the ethos.

In conclusion, even if the public knows that the two alternatives are economically identical, they still perceive that receiving a tax credit in consideration for service, applied through tax expenditure, is different from receiving direct consideration for services through government spending, in addition to which receiving the tax benefit does not mean that the soldier loses status as a volunteer. By the tax credit regime, the ‘people’s army’ ethos is preserved while the inequality is narrowed dramatically.

7. The MATC regime: Database and empirical findings of the extent of inequality and discussion

7.1. The database

Our database is required, first and foremost, to contain information regarding the extent of the inequality, in tax discourse terms, according to the proposed tax model. Our research findings regarding the number of future years in which the MATC can be used, and the conscript soldier be exempt from income tax, has a fundamental importance. Its importance goes beyond the practical implications in that it reflects the tremendous significance of the MAT burden and its unequal consequences.

Looking at Table 2 and Table 3, there are three components that determine the size of the MAT: (i) the FMV wage (Component I) that a conscript soldier would have received for their service; (ii) the tax liability (Component II) that the FMV wage would have incurred; (iii) the total remuneration (Component III) that a conscript receives under the current arrangements. These three components are calculated differently for the four groups of military professions – front-line combat, combat, combat support, non-combat – upon which the IDF’s remuneration structure is explicitly based. This means that both the current remuneration and the FMV wage differ substantially among these four groups. The MAT is calculated by subtracting the tax liability and the current remuneration from the FMV wage for the four groups of soldiers.

The measurement’s components of the mandatory army tax (MAT) for the entire mandatory service (men; ILS)

The FMV wages (Component I) were calculated using a Ministry of Defence (MOD) research study published in 2021, which shows the wages of different IDF professions at the age of 21 to 22 (the age at which most soldiers complete their mandatory service).Footnote 72 Then, using the factor mentioned above at Section 4.2, the wages were calculated back to the ages of 19 and 18. The factor was derived from the average growth in salary between the ages of 18 to 30.Footnote 73 The tax on the FMV wage (Component II) was calculated using the official Israeli tax authority calculator.Footnote 74 Total remuneration (Component III) includes the monthly living allowance for conscript soldiers, a lump sum payment (additional payments) given after completing mandatory service for basic needs (education, business, and so on), accrued monthly during service. Soldiers also receive essential services (‘benefits’) such as food and lodging, which would otherwise incur costs,Footnote 75 along with a social security tax exemption.Footnote 76 These were calculated using information from MOD and IDF resources.Footnote 77 All wages and payments were adjusted to October 2023.

The measurement’s components of the mandatory army tax (MAT) for the entire mandatory service (women; ILS)

Under the current ethos, the article proposes the MATC regime in which the MAT will be offset as a tax credit against the demobilised soldier’s future tax liabilities. This regime is based on the framing effect, which effectively addresses the ethos of the ‘people’s army’.Footnote 78 Does the MAT burden in Table 2 amount to a significant or an insignificant sum? The larger the MAT, the greater the inequality. To determine whether the discussed MAT amounts are significant or not, the article chooses to answer this within the tax discourse framework by the following criterion: at what age will the released soldier use their tax credit?Footnote 79 Thus, the demobilised soldier has a tax reserve in the form of a tax credit, and the article therefore examines the range of this tax credit. The MATC will be activated only upon the individual’s request, not automatically, based on the soldier’s advantage. It should be noted that if the total MATC is not fully utilised in the current year, as a result of low income or a large family size that reduces the tax liability,Footnote 80 it will be transferred to the next year in a manner that will preserve its economic value over the years. Thus, it will bear indexation and real interest. In such situations, a specified period can be set after which the reserve is depleted, with any remaining balance being directly paid as a tax refund, rather than utilised as a tax credit through offsetting. Another alternative is to use the tax credit to offset other taxes.

We have not found reliable empirical evidence regarding the correlation between the soldier’s profession during mandatory army service and their profession after release, in the sense that one’s profession in the army cannot really provide any useful hints about the nature of their civilian profession.Footnote 81 Therefore, the analysis uses data that includes the seven major professional sectors of workers in Israel: Elementary Professions, Skilled Workers, Service and Sales, Clerical Support, Engineers and Technicians, Professionals, and Managers – as they appear in the data of the Central Bureau of Statistics (CBS)Footnote 82 – and it includes the average wage for each sector based on age and gender.Footnote 83 The tax liability of the various wages of the sectors is calculated according to the tax authority’s calculator, which takes into account, among other things, all the variables that affect the tax liability – which include gender,Footnote 84 length of marriage,Footnote 85 number of children and their agesFootnote 86 – based on data from the CBS (2023).Footnote 87 The following charts display the duration required to utilise fully the tax credit for each of the four soldier groups, divided among the seven professional sectors.

7.2. Findings

The findings that emerge from the data are shown below. Figures 1, 3, 5 and 6 show the age at which men and women, performing the various military professions across different market sectors, would fully or partially use their MATC.

For example, an individual employed in an Elementary Profession, who served in a non-combat unit, would not use their MATC until the age of 67 (Figure 1). The percentage of unutilised MAT for them would be close to 100% (Figure 2). Another example, Clerical Support workers, would use their MAT at the age of 67 (Figure 1). Those who served in combat and front-line combat units, would have zero per cent MAT left unused (Figure 2); those who served in combat support and non-combat have unused MAT of less than 10% (Figure 2).

Age of MATC partial or full utilisation (retirement age 67; men).

The percentage of unutilised MATC at retirement (retirement age 67; men).

Suppose the database presented above is mistaken and the calculated MAT is actually 20% lower, Figures 5 and 6 show what the duration of using the tax credit for men and women would be.

7.3. Discussion

As emerges from Figures 1, 2, 3 and 4, there might be scenarios where it would take a long time for a soldier to use their tax credits, based on their lower income in the future. These charts demonstrate that there are sectors which would be able to use their military tax credits for no less than 42 years (!). In fact, workers in these sectors will retire before fully utilising their military tax credit. The reason for this is that throughout their working lives, they earn a low wage, making their tax liability minimal. In contrast, those who earn more (for example, managers) offset their tax credit over far fewer years. This finding does not have such a negative distributional effect because the MATC is indexed and bears real interest. One might claim that the proposed regime sets a disparity in that the weak sectors seldom have access to financial markets, and they cannot borrow money against the MATC. Even if they do have such access, there is no certainty that the cost of borrowing would be the same as the real interest and indexation on their MATC. The disparity is even more pronounced when looking at the impact of the MAT on women. From Figure 4 it is quite clear that the percentage of unutilised MATC is much greater for women than it is for men, the main reason being the vast disparity in wages, resulting from discrimination against women.Footnote 88 This is interesting given that most of the discourse about inequality in military service in Israel revolves around men. This aspect of disparity among the various sectors can be narrowed dramatically by reducing the period within which the proposed tax credit could be utilised, or by allowing the credits to be utilised against taxes other than income tax.

Age of MATC partial or full utilisation (retirement age 65; women).

The percentage of unutilised MATC at retirement (retirement age 65; women).

The proposed MAT does not consider several elements which may have affected, not substantially, the MAT measurement, both upwards and downwards, as they are unmeasurable because of a lack of an agreed and applicable method of calculation. These include, mainly, disregarding the impact of military service on future income, the compulsory element and the unmeasurable benefits to soldiers,Footnote 89 such as the social status gained from service and other factors.Footnote 90 Hence, the proposed MAT model adopts a cautious and conservative approach based on the assumption that the model might have overestimated the MAT, and the model was recalculated with a reduced MAT of 20%. Figures 5 and 6 show that even under the 20% MAT reduction, our results only slightly change.

Age of partial or full MATC utilisation, sensitivity check – 20% MAT reduction (retirement age 67; men).

Age of partial or full MATC utilisation, sensitivity check – 20% MAT reduction (retirement age 67; women).

What about the distributional aspects? The fact that the current situation is flawed, even regressive, is not disputed, both from a broader societal perspective, comparing the enlisted to the non-enlisted and, from a narrower perspective, focusing solely on the enlisted population. From a broader perspective, the enlisted bear a higher income tax burden because of the MAT, as compared to non-enlisted. This outcome does not align with the progressive structure of the income tax regime. Figures 1, 2, 3 and 4 illustrate that for large portions of the population, the MAT credits exceed all the income tax they would pay throughout their working years until retirement. This population belongs largely to the lower and middle classes of Israeli society based on their low wages. As a result, this tax harms both horizontal and vertical equity. In terms of horizontal equity, comparing two individuals with identical incomes, one enlisted and one not, the enlistee bears a higher tax burden as a result of the MAT. The distortion exists also in terms of vertical equity. Two taxpayers with different incomes, where one is enlisted and the other is not, might bear the same tax burden. This occurs even though the enlistee’s income is often significantly lower because of the additional MAT burden. Furthermore, in some cases, the impact of the MAT on vertical equity is even more pronounced. There are circumstances where a non-enlistee with a higher income still bears a lower tax burden than an enlistee because of the MAT. Even within the narrow perspective of the enlisted group, it is difficult to justify the distributional differences between the various tax burdens of the four soldier groups as shown in Figures 1, 2, 3 and 4.Footnote 91

The proposed regime faces potential political resistance arising from moral concerns about quantifying human lives. Despite numerous instances in the legal system where economic values are assigned to human life, this practice remains controversial.Footnote 92 However, the proposed MATC presents a compelling case for such quantification, as it relies on concrete data rather than estimates. Specifically, it uses actual salaries of permanent army personnel, which reflect the compensation that individuals receive for risking their lives in military service.Footnote 93

The MATC regime has budgetary implications in that total tax revenue will decrease as a result of the tax credits granted to the discharged soldiers. The extent of this reduction also depends on the macroeconomic effects of the new tax regimeFootnote 94 and on a gradual decrease, as the tax credit reimbursement is spread over many years. The budgetary implications would not be negligible, but they will be of a magnitude that Israel’s economy can withstand with budgetary adjustments to both government expenditure and revenue.Footnote 95 Rough estimates suggest that the total MATC cost for 170,000 soldiers (75% men; 25% women) amounts to 27.6 billion ILS for the entire service period. Annually, the cost is about 11 billion ILS, or approximately 1.8% of the 2023 national budget (and 0.5% of GDP). Of greater importance, the MATC payments are spread over many years, thus reducing immediate cash flow impact. Even if there is potential for a significant budgetary impact, the urgency of the profound crisis of military service inequality in society leaves it with no choice. Addressing the budgetary effect would require either reducing government expenses, increasing the tax burden, or increasing the governmental deficit.

The choice of the budgetary tools that would be used to fund the implementation of the MATC regime presents budgetary and distributional challenges. This is because the budgetary tools chosen would need to align with the regime’s goals of reducing inequality in the general population and within the enlistee population. For instance, if governmental expenses are cut in a way that disproportionately harms the enlistee public compared to the impact on the non-enlistee public, then the distributional outcomes of the MATC would be undesirable. In addition, increasing income tax rates tends to disproportionately increase the tax burden on the enlistee population compared to the non-enlistee population. Those who do not enlist tend to be those who pay less tax.Footnote 96 The additional tax intended to finance the MATC must be designed in a way that addresses fairly and justly the distributional effects. Nevertheless, the distributional outcome would be better than the current situation within the enlisted group since the MATC creates a fairer distribution of the MAT burden by guaranteeing that the MAT is levied in alignment with the overarching principles of the progressive income tax regime. Additionally, in order to maximise the distributional effects of the MATC, the budgetary tools used to finance the new regime should consist of a mixed set of tools that may include several tax regimes, including those borne by the entire public, despite being regressive, such as increasing VAT.Footnote 97

While the proposed MATC may not gain traction because of political or economic opposition based on budgetary considerations, it offers a valuable new perspective on the current conscription discourse. By framing the economic burden of service through the lens of taxation, it exposes the vast inequality inherent in the system. This tax-based approach makes the economic disparity clear, potentially sparking conversation and reform even if the proposed regime is not adopted.

8. Conclusion

The deep social and political crisis concerning inequality in Israeli society, particularly regarding mandatory military service, has traditionally been managed through constitutional discourse. For decades, Israel has grappled with growing inequality as a significant portion of its youth does not enlist for mandatory military service. Efforts to mitigate this inequality by transitioning to a professional army or expanding conscription have been hindered by entrenched ideological and political factors. The enduring ethos of a ‘people’s army’, which has underpinned compulsory service in the public sphere for decades, not only sustains existing inequalities but also obstructs the shift to a volunteer army and prevents substantial increases in payments to enlistees, even those below the FMV wage. Consequently, inequality widens as the non-enlisting population grows each year, driven by higher birth rates among non-enlistees compared to those who enlist. Attempts to reach political compromises have repeatedly been struck down by the Supreme Court as unconstitutional, highlighting the limitations of constitutional discourse in addressing this issue.

This article proposes a novel transformative shift from a constitutional discourse to a tax discourse as a means to effectively reduce inequality. By reframing mandatory military service as an in-kind tax and introducing a mandatory army tax credit (MATC) mechanism, this aims to reimburse enlistees for the implicit tax payments they make through their service. This tax-focused approach not only offers a more balanced and constitutional framework but also leverages cognitive biases through the framing effect, making the payment appear aligned with the ethos of a ‘people’s army’. Such a shift has the potential to create a social and political environment conducive to substantial alleviation of the existing crisis.

This article underscores the necessity for further research across various disciplines – including economics, sociology and political science – to explore the social and political effects of ethos narratives, national identity, national security, equality, and defence economics. By moving beyond traditional constitutional discourse and embracing a tax-based framework, society can better navigate and mitigate the persistent inequalities associated with mandatory military service, paving the way for a more equitable future.

Acknowledgements

I am very grateful to Netta Barak-Corren, Yoav Dotan, Yehonatan Givati, Yotam Kaplan, Udi Nisan, David Schizer, Eyal Zamir, and the participants of the 2023 Tax Conference of the Columbia and Hebrew University Law Schools for their useful comments. I would like to thank Adir Kingsley, Amichai Friedman and Alexander Fedan for their excellent research assistance. Thanks to the Aharon Barak Center for Interdisciplinary Legal Research and Aumann-Fischer Center for Law, Economics and Public Policy at the Hebrew University for their financial support. Last but not least, I thank Zohar Goshen and Columbia Law School for their wonderful hospitality while I was writing the main parts of the article.

Financial support

This research was supported by a grant from the Aharon Barak Center for Interdisciplinary Legal Research and Aumann-Fischer Center for Law, Economics, and Public Policy at the Hebrew University.

Competing interests

The author declares none.

Open access

Open access