Before the adoption of the name “Euro” in 1995, the “ECU” (European Currency Unit) was supposed to become the single European currency. Created as part of the European Monetary System (EMS) in 1979, the ECU was the unit of the central rates around which currencies had to fluctuate. It also served as a means of settlement between the European Economic Community’s (EEC) central banks and as a unit of account for European institutions. Technically, it did not differ very much from its predecessor, the European Unit of Account (EUA), originally conceived as part of the European Payments Union in the 1950s and incorporated by the EEC in 1975.Footnote 1 Both were so-called “currency cocktails” or “basket currencies,” whose value was composed of the EEC members’ currencies. Replacing EUA with ECU primarily had a psychological function. The new EMS, established to build a European monetary identity, required a rebranded unit of account.Footnote 2 However, alongside the “public” ECU used by EEC central banks, a “private” ECU soon emerged. It was called “private” because it was created by commercial banks and by various enterprises, which were mostly private, even though some of them were state-owned.

Cocktail currencies did not exist only in Europe, nor was the ECU the only example of these. They developed in response to the unstable monetary environment of the 1970s, in the wake of the fall of the Bretton Woods system and the advent of flexible exchange rates. The private ECU was often compared to the International Monetary Fund’s (IMF) Special Drawing Rights (SDR), introduced in 1969. In 1973, the European Investment Bank created Eurco, the European Composite Unit, with the help of a group of commercial banks.Footnote 3 In 1974, Hambros Bank introduced the Arab Related Currency Unit, which included 10 Arab currencies and weighted them equally. Barclays created the B-unit in 1974, which was never used. Crédit Lyonnais created the Unité Financière Internationale, which was never used either, as it was too similar to the IMF’s SDR. All these monetary and financial experiments had in common the combination of several currencies in one product, with different weights and combination processes. However, none of them was as successful as the ECU.

By the early 1990s, the ECU became the third denomination currency in the bond market, after the dollar and the yen.Footnote 4 This “private” ECU had been created by banks and mirrored the official ECU. Companies used it increasingly over the 1980s as a financial product offering specific advantages, such as hedging clients or themselves against the volatility of exchange rates and interest rates. Stock Exchanges in various places in the world had developed a futures and options market in the ECU. The financial success of the ECU was unquestioned and went far beyond European countries, as US and Japanese banks also used the ECU.

The ECU story entails many paradoxes: while “public” and “private” ECUs were technically different, they remained strongly intertwined; the ECU market was private and developed by enterprises, but in close connection with European institutions; while being one of many financial innovations of the 1980s, the ECU was also the prototype of a European currency. The article unpacks these paradoxes and argues that the political dimension of the ECU was central to its development, but also that companies, by devising a marketable ECU, played a role in advancing EMU, voluntarily or not. By doing so, the study offers an archive-informed history of the ECU private market, which has so far been researched mostly in the 1980s and 1990s by economists and practitioners. The article also contributes to different fields of historiography: the business influence in public affairs in the late twentieth century, the history of monetary integration and the making of EMU, and the history of money.

Recent scholarship has highlighted the role of business actors in the remaking of an international order after the 1970s crisis.Footnote 5 The European integration literature in particular stressed how lobbying contributed to the relaunch of the European project in the 1980s through the Single Market.Footnote 6 By looking at EMU from the much less researched perspective of enterprises, the article shows how business involvement in monetary integration escapes the traditional lobbying, understood as companies’ attempts at influencing policymakers.Footnote 7 It shows that political motivations drove many of the actors involved in the ECU private market, and that representatives of European institutions strongly encouraged them. The article thus builds on the literature challenging the division into “private” and “public” actors in European integration.Footnote 8 Instead, it sheds light on the public-private “ECU network” involving individuals - businessmen, economists, commissioners, and central bankers, who, for political and economic reasons, promoted the idea of a European currency since the 1970s.

At the same time, however, financial and non-financial companies using the ECU but indifferent to the political project underpinning it, involuntarily became agents of political integration.Footnote 9 In the 1980s, plans for EMU were neither definite nor clear. For instance, some thought of the ECU as a parallel currency, which meant a European currency that would double existing national currencies without suppressing them, as opposed to a single currency. Eventually, when the euro was introduced in 1999, 1 euro was equal to 1 ECU, even though it was not a parallel currency, but a single one. By testing an early form of European currency, companies helped to define its form, demonstrate the feasibility of EMU, and increase its general recognizability. In this way, firms involved in the ECU private market played a pivotal role in enhancing the credibility of an early form of European currency, credibility being essential for any currency.Footnote 10 As this article argues, the private ECU market served as a “rehearsal” for EMU.

The history of the private ECU market also provides an interesting case study in the history of money. Without an issuing state and a central bank, the ECU was technically a private currency. While the concept has a long history, it reentered economic debates in the 1980s.Footnote 11 With financialization, digitalization, and the rise of neoliberal economic thought, the idea of divorcing money from a state acquired particular prominence, only to explode with the cryptocurrencies in the 2010s.Footnote 12 Nevertheless, none of the 1980s attempts at creating alternative currencies, or other currency cocktails such as the SDR, gained popularity comparable to the ECU. Its success was closely related to the political project underpinning it.Footnote 13 While there was no binary choice for companies between the private ECU and political EMU, companies considered that an increased use of the private ECU was conditioned to a move towards single or at least common European currency. Politically-led solutions were not considered necessary for an occasional use of the ECU, but provided more guarantees for an extensive one. Despite being born in the heyday of neoliberalism, the private ECU demonstrates that when it came to currency, business actors, in particular the non-financial sector, still preferred politically-led solutions.

The argument unfolds over three sections. First, the paper looks at individuals from the public and private sectors, who often shifted between the two, and who, since the 1970s, promoted the idea of a European currency. We call this group the “ECU network.” Second, the paper scrutinizes the rise of the ECU in the financial sector, where offering products in the ECU did not necessarily go hand in hand with support for EMU. Third, the paper zooms in on the non-financial sector, for which the ECU was usually closely linked with EMU.

The paper relies on vast archival research, primarily focusing on private firms. Contrary to many business history studies, it delves into both the banking and non-financial sectors. In particular, the paper relies on material from banks (Barclays, Lloyds, Crédit Lyonnais, Société Générale, and Istituto Bancario San Paolo di Torino), non-financial businesses (Fiat, Saint-Gobain), and business associations. It also builds upon material from the Historical Archives of the European Union (HAEU), central banks, and the French Ministry of Finance.

The ECU Network

When the private ECU developed in the 1980s, the use of a European unit of account for commercial activities was not a new idea. Robert Triffin, an economist known for his forecast of the Bretton Woods System collapse, promoted it since the 1950s.Footnote 14 In 1961, the Kredietbank SA Luxembourgeoise, on the board of which Triffin had a seat, had issued a bond in a European unit of account for a Portuguese company, the Sociedade Anónima Concessionára da Refinação de Petróleos em Portugal (SACOR).Footnote 15 The European Investment Bank was explicitly discussing the possibility of issuing bonds in a European unit of account at the same time.Footnote 16

Among European policymakers, however, the idea of a European currency unit gained momentum only with the monetary instability of the 1970s caused by the collapse of the Bretton Woods system. It came up in discussions within the European Commission, in particular within the Directorate-General for Economic and Financial Affairs (DG II), concerning the Werner Report, the first and abandoned roadmap towards EMU from 1970, and accelerated with the introduction of the European Unit of Account (EUA) in 1975, and eventually the creation of the EMS in 1979. The postulate to create a parallel currency was put forward in expert reports commissioned by the DG II, such as the Magnifico Report from 1973 or the Optica Report from 1976.Footnote 17 Triffin, who was still very active in the promotion of European units of account, both in their private and public forms, became one of the key minds behind the re-launch of monetary initiatives in the late 1970s leading to the creation of the EMS.Footnote 18

European institutions were important players in the discussions on parallel currency, but they were not the only ones. Several central bankers, economists, and business actors formed networks interested in European units of account. Since 1963, the Bellagio Conferences set up by a group of economists, including Triffin, gathered policymakers and economists to discuss the future of world monetary architecture. In 1968, the organizers extended this format to Burgenstock conferences, which also involved business leaders.Footnote 19 In Europe, such a space for debate was offered, for instance, by the Monetary Commission and Monetary Panel of the European League of Economic Cooperation (ELEC), a business organization created in 1946 in close cooperation with the European Federalist Movement. These units, serving as spaces for knowledge pooling and social network building, brought together central and commercial bankers as well as economists, and remained in close contact with representatives of the European Commission and national policymakers.Footnote 20 Triffin, as a board member of Kredietbank, also maintained close ties with the ELEC’s Monetary Panel led by Kredietbank’s chairman Luc Wauters.Footnote 21

Simultaneously, in the early 1970s, the European Investment Bank (EIB) initiated practical discussions on a parallel currency, which it called “Eurco” (European Composite Unit), and involved business actors for that purpose. Driven by the desire to provide instruments capable of addressing global monetary instability, the EIB sought to develop an innovative European basket currency. To do so, it asked a few European commercial banks, including Rothschild, Kredietbank, and Société Générale (France), to submit their proposals on the composition of this new currency cocktail. It had also received unsolicited proposals from these banks.Footnote 22 However, due to legal obstacles and increasing market stability in the mid-1970s, the Eurco created based on these debates, was a short-lived experiment.Footnote 23

Next to the EIB-centered Eurco experience, other groups devised products in European units of account. One of them revolved around the ABECOR banks, a European banking club established in the early 1970s and involving BNP, BNL, and Barclays, among other banks.Footnote 24 The Eurco product these banks developed was to be used for commercial transactions, whereas the one that the EIB developed with Kredietbank and Rothschild was to be used for floating bond issues.Footnote 25

Echoing previously formulated postulates, ELEC also issued in 1978 a statement calling for the development of a parallel European currency named EUROPA, which the private sector could use. The association believed it would “at the same time offer an initial solution for the international exchange problem and relaunch monetary union in Europe.”Footnote 26 ELEC had written to several banking clubs (ABECOR, EBIC, and Interalpha) and individual banks to popularize its idea. However, Barclays, for instance, received the ELEC proposal unenthusiastically. When circulating the ELEC letter inside the company, a Barclays official wrote: “I enclose a letter addressed to Mr. Bevan by these tiresome ELEC people.”Footnote 27 The ELEC network did not represent the entire business community.

The EMS and its associated public ECU gave supporters of European currency further impetus. Only a few days after their implementation, Triffin set up a new platform to discuss the future of European monetary arrangements: a series of seminars, taking place in Louvain-la-Neuve, on the EMS. While the first two gathered above all policymakers, central bankers, and economists, the third one aimed to attract business representatives and cover the development of the private ECU market. In order to select the right participants for such a gathering, Triffin consulted the leaders of ELEC, including its long-standing president and major shareholder, the president of Solvay René Boël. They committed to providing him with a list of suitable participants who had responded enthusiastically to ELEC’s EUROPA initiative from 1978.Footnote 28

The collaboration between the ELEC and Triffin resulted in the seminar on “The Private Use of ECU” in June 1980. Gathering representatives of over thirty commercial banks alongside economists and representatives of the European Commission, such as Tommaso Padoa-Schioppa, the newly appointed head of DG II, and EIB, it articulated discussions on the ECU to reflections on a possible EMU. It thereby created a network of actors connecting the two questions. For this group of people, the role of businesses was supposed to move beyond a simple contribution to the discussion. At the time, the private market for the ECU had already emerged, but was very small and limited by the absence of a proper clearing mechanism. Triffin recognized the need to replace the complex ad hoc existing clearing mechanism based on cooperation between a few banks with a comprehensive clearing system. Paul M. Caron, Vice President of Morgan Guaranty Trust, well acquainted with both Triffin and Padoa-Schioppa, advised on how to get commercial banks on board for this project. In his letter from 1981 to Padoa-Schioppa, he claimed: “it seems to me that we must catch their interest, give them a feeling that the ‘train is already leaving the station’ and force them to concentrate on solid, workable ideas.”Footnote 29 Similarly, Caron wrote Triffin that “the active collaboration on the part of the major European banks” might be conditional upon “‘plus value’ for them.”Footnote 30

Clearing operations in the ECU were initially complex, which hampered their attractiveness. As the ECUs were made out of nine component currencies, operations in the ECU could require transactions in all of them. For instance, matching assets and liabilities was difficult and often required splitting the ECUs into component currencies.Footnote 31 Similarly, deposits from EEC institutions initially exceeded possible services in the ECU, which forced banks to fragment these deposits into national currencies.Footnote 32 Banks using the ECU opened an account at Kredietbank because it was the most active bank in the ECU market.Footnote 33 Therefore, Kredietbank played the role of a clearing house for the ECU. Lloyds, then, provided similar services, and both Lloyds and Kredietbank had opened accounts with each other.Footnote 34 By 1984, other banks joined them and concluded bilateral clearing agreements to enable transfers in the ECU: Société Générale Brussels, Crédit Lyonnais, and Banque Bruxelles Lambert. Each had an account in the ECU with one another, and banks that were not part of this group could have an account with only one of them. Banks that opened deposits in the ECU for their clients also used the ECU accounts between themselves, which they could debit or credit on a daily basis. This group of five (then, seven) banks then set up the Mutual ECU Settlement Account (MESA) whereby each of them served as the clearing agent for the banks for one month, alternatively. Additionally, banks agreed not to have to settle their ECU accounts as long as their balance was below 10 million ECU (then 20 million), so as to minimize transfers.Footnote 35

However, this system was still complex, and some banks felt excluded from the core group. Therefore, a few ECU supporters from both the European Commission and commercial banks had endeavored to set up a group working on this project in parallel. In a report to DG II on the need for an ECU clearing system, the official in charge of selecting banks and individuals best suited for the project wrote that even though the ECU clearing system would have a private character, “individuals whose personal judgement carries with it an obligation to achieve some form of European structure” remain crucial for the project.Footnote 36 Indeed, the participants invited by Padoa Schioppa to the ECU clearing system informal group confirm this logic.Footnote 37 Apart from Caron from Morgan Guaranty Trust, the initial composition of the ECU clearing working group involved Kredietbank (André Swings), Instituto Bancario San Paolo di Torino (Alfonso Iozzo), Crédit Lyonnais (Dominique Rambure), and Lloyds (Leonard Dewes). All these banks had already experimented with the ECU. It was, above all, the case of Kredietbank, one of the pioneers of European private currency. Its ties to Triffin and its role in the ELEC’s Monetary Commission and Panel demonstrate a strong European orientation. Such pro-European sympathies also characterized the mid-level managers selected to participate in the making of the ECU clearing. The case of Alfonso Iozzo, who, alongside a career in Istituto Bancario San Paolo di Torino, was a member of the federalist European Movement since his student years, best illustrates this point.

By July 1983, the ECU clearing working group had 18 members.Footnote 38 The banks of this group played a crucial role in popularizing the ECU. From 1982 onwards, Istituto Bancario San Paolo di Torino issued the ECU Newsletter, which monitored the development of the ECU private market and encouraged businesses to experiment with the currency. Numerous publications, seminars, and promotional activities carried out by these banks served the same goal. In September 1985, they created the ECU Banking Association with Rambure from the Crédit Lyonnais as president and Iozzo as vice president. By 1988, the organization had over 100 members.Footnote 39 The ECU Banking Association was responsible for supervising the new ECU clearing system, which was eventually set up in October 1986 and replaced the complex clearing mechanism mentioned above, limited to a few banks, while conferring the role of clearing agent to the Bank for International Settlements (BIS).

Although the ECU Banking Association was officially concerned with the ECU, many of its leaders openly considered it a tool for advancing EMU. For instance, Rambure saw the clearing mechanism playing “a role in the growing monetary integration of the European countries” and expected that in the future “central banks will use the clearing system to intervene and regulate the ECU market, perhaps via common organization.”Footnote 40 European institutions closely followed the activities of the ECU Banking Association and financed some of them. EIB’s representatives were members of the ECU Banking Association’s executive committee, and officials from DG II participated in all conferences and seminars set up by this group.

While DG II, EIB, and Triffin played a central role in its initial stages, Valery Giscard d’Estaing and Helmut Schmidt, the French president and the German chancellor whose cooperation in the late 1970s enabled the implementation of the EMS, gave the ECU further impetus. In 1986, they set up the Committee for the Monetary Union of Europe (CMUE), which initially adopted a parallel currency strategy for monetary unification. This body gathered figures from European central banks, universities, and European institutions previously active in the debates on the European currency. Aiming to extend this group to business, Giscard and Schmidt asked for support from Etienne Davignon. At the time, Davignon was president of the Société Générale de Belgique; however, from 1977 to 1985, he occupied positions in the European Commission, including the post of Commissioner for the Industrial Market. While on the Commission, Davignon participated in the creation of the ERT (European Round Table of Industrialists). In 1987, drawing from this network and experience, he selected a group of individual European business leaders who would launch a business association mirroring the goals of the CMUE: the Association for the Monetary Union of Europe (AMUE). Apart from Davignon, its founders and leaders included Giovanni Agnelli (Fiat), Cornelis van der Klugt (Philips), Jacques Solvay (Solvay), and Francois-Xavier Ortoli (TOTAL).Footnote 41 Ortoli, before moving to TOTAL, had been president of the European Commission and the Commissioner for Economic and Financial Affairs between 1973 and 1977.

Leaders of Fiat and Philips played a central role in the AMUE, as they did in the ERT. Agnelli was particularly well-known for his involvement in political affairs, private advocacy forums, and support of the European integration process.Footnote 42 That was also the case with Solvay management. Boël, chairman of the company until 1971, was president of ELEC between 1951 and 1981. Even when AMUE reached almost 200 firms in 1990, the leaders of these three companies remained critical for its activities.Footnote 43

The AMUE presented the private ECU as a “vehicle currency” for EMU.Footnote 44 Its main objective was to encourage companies, in particular non-financial companies, to increase their use of the ECU and to promote the idea of monetary integration. Its activities involved hosting events and seminars, conducting surveys, and issuing a newsletter, ECU for European Business, and other publications. For instance, by October 1989, the AMUE’s guide “The ecu for the Europe of 1992” was distributed in 400,000 copies.Footnote 45 During the late 1980s and early 1990s, 1992 functioned as a critical deadline for EEC member states. This was the year by which they aimed to complete the Single Market, a commitment made in the 1985 White Paper and the 1986 Single European Act, through hundreds of directives. The AMUE collaborated with the ECU Banking Association and maintained very close ties with the CMUE, which monitored the activities of its business branch. European institutions also collaborated with the AMUE. Jacques Delors, president of the European Commission from 1985 to 1995, regularly kept in touch with its leadersFootnote 46 , and the European Commission financed many of the AMUE’s projects.Footnote 47

The ECU network played a central role in developing the ECU private market. Using enterprises to strengthen the ECU was a conscious strategy applied by individuals such as Triffin, Padoa-Schioppa, and, later, the leaders of the CMUE. European institutions continued to support the overall project. As later admitted by Thiery Vissol from DG II, in the 1980s, mobilizing business support was one of the European Commission’s key strategies for EMU.Footnote 48

The ECU and the Financial Sector

The “private” ECU was more successful in the financial sector than in the non-financial sector, but the use of the ECU in financial companies was not necessarily linked with political support for the EMU. Over the 1980s, an increasingly complete financial market in the ECU developed. However, the ECU banking and financial market growth was extremely heterogeneous (not all banks embraced the ECU market), and at the intersection of public and private forces.

During most of the 1980s, the private market for the ECU was structured around four main countries.Footnote 49 Belgium and Luxembourg (counted as one country) provided most deposits, mostly from European institutions.Footnote 50 Italy provided most of the borrowings from non-banking enterprises. France provided part of the borrowings from non-banking enterprises and played a role in the interbank market in the ECU. And the UK was the center of the interbank market in the ECU, an interbank market much larger than that of other Eurocurrencies. These centers thus had complementary functions. Germany opposed the ECU until 1987. It did not want to consider it a currency and sought to preserve the standing of the Deutsche Mark as an international currency. Therefore, German regulations forbade or strictly limited German banks from engaging in the ECU operations.Footnote 51

As shown in the previous section, when the EMS and the ECU were established in 1979, the idea of a private market for a European unit of account did not arrive in a vacuum, and banks had long been participating in various related experiments. If, in January 1975, the ABECOR European banking club’s members considered that there was little demand for a commercial Eurco, they had already devoted careful thinking to these experiments, some of which could be of interest to banks’ clients in the complex 1970s monetary environment.Footnote 52

For example, Barclays developed its own unit of account: the B-Unit, which included dollars. It considered it a more flexible tool in the sense that the method of valuing the B-Unit could be agreed upon between the contracting parties and that currencies could be substituted.Footnote 53 In 1975, Barclays reported that Atlantic Container Lines, an international consortium of European shipping companies, had “adapted the B-Unit in developing a mechanism for currency freight surcharges.”Footnote 54 In March 1976, a staff member of the European Commission visited Giles Davison from Barclays Bank International to ask him whether Barclays would be ready to handle transactions in a European unit of account, as they were “considering the development of a unit based on the B-unit concept.”Footnote 55 Later, in 1978, Barclays was very disappointed that the management of the account of the Joint European Torus, a large scientific structure whose aim was to study nuclear fusion in Culham in the UK, went to Sal. Oppenheim Bank, because that bank could convince the project leaders that they could operate an account in a European unit of account.Footnote 56 In the 1970s, European units of account already had a commercial interest for banks, and were not a political investment only.

Later, in October 1978, the Barclays group economics department portrayed the EMS as a commercial opportunity in relation to the future European unit of account: “The City took a lead in developing the Eurodollar market following the change in the status of sterling as a reserve currency: with EMS it can look forward to playing a leading role in developing the ECU as a commercial currency.”Footnote 57 What changed in the following years was that they would be marked by the EMS’ more successful development compared to the previous experiments of European monetary cooperation schemes. In addition, the European integration dynamic renewal in the 1980s, the progressive financial sector’s liberalization and internationalization, the support of individual member states to the ECU private market, and the boom in financial innovations gave further support to its growth.

Commercial banks did not have the same opinion about the ECU private market but generally tended to be initially skeptical. In June 1980, the European Banking Federation (EBF) issued a rather unenthusiastic booklet on the subject.Footnote 58 Reporting on a recent EBF meeting in October 1983, a note from the British Bankers’ Association (BBA) stated: “The question of the ECU is a major subject on which the Commission are clearly seeking our support. Indeed, we were criticized by them in 1980 over our unenthusiastic attitude.”Footnote 59 Even though the Federation amended its booklet in a more optimistic way in October 1982, it still considered that there was “little evidence of sufficient demand to develop a market in the ECU; and that this demand was unlikely to be generated until the ECU was seen as a currency in its own right, rather than just a basket.”Footnote 60 In 1983, the BBA considered that the private use of the ECU as an international currency remained modest compared to the US dollar and other international currencies, but that it was attractive for European traders, investors, and borrowers as a means to hedge against currency movements.Footnote 61

However, international discussions within banks revealed different positions. Lloyds (which was part of the ECU clearing working group) supported the private market for the ECU, and considered that the EBF should set up a working party on the question.Footnote 62 Officials from Lloyds felt that there was a growing interest in using the ECU as a billing currency, particularly among airline companies. Since the end of the Bretton Woods system and the advent of floating exchange rates, airlines had been struggling to accommodate the influence of currency changes on fares. Fares were set in two currencies, US dollars and pounds sterling, but were sold to customers in local currencies, and the conversion raised serious challenge. Currencies’ different values and exchange rates variability created differences in fares according to where tickets were purchased. The International Air Transport Association had tried to rely on the IMF’s SDR to face this problem, but could not secure an agreement on a global scale, and therefore, regional solutions such as the ECU were considered more practicable.Footnote 63 On the other hand, Barclays, along with the British accepting houses, was much less enthusiastic. National Westminster recognized that the ECU market had grown significantly, but expected future growth to be slow. Much criticism revolved around the fact that setting up a service in the ECU was costly and that this would not encourage its commercial use.Footnote 64 The ECU private market was actually championed by a few particularly involved banks: Lloyds in the UK, Crédit Lyonnais in France, Banque Bruxelles Lambert, Kredietbank, and Banque Générale du Luxembourg in Belgium and Luxembourg, and Istituto Bancario San Paolo di Torino in Italy, many of which were the original members of the ECU clearing working group, and whose managers formed a part of the “ECU network.”

Banks’ interest in the ECU, however, increased over time. By 1985, in particular, the BBA, the EBF, and some initially reluctant banks expressed clearer support.Footnote 65 Supporting a wider use of the ECU enabled peak associations and banks to show goodwill vis-à-vis the Commission, which could then be useful on other occasions. The development of the ECU market was perceived as a relatively uncontroversial area where profits could be made and was, therefore, easy to support. In August 1985, Barclays told the EEC and the EIB that the UK should now take a targeted issue in the ECU and that it wanted to lead it.Footnote 66 In September 1985, Barclays was very disappointed not to have been included among the participating banks in the setting up of the ECU clearing system and expressed this to the ECU Banking Association because it now wanted to be perceived as an important player in this market.Footnote 67

The development of the ECU private market was linked to its recognition by national authorities. In April 1981, a letter from the French Treasury to the Bank of France highlighted two reasons for supporting the use of the ECU: reinforcing European integration and supporting Paris against London as a financial center. The author noted that developing the use of the ECU could be done “from the top” (via the public ECU) or “bottom-up” (via the financial and banking markets), but that this opposition was artificial in the sense that both approaches should be combined.Footnote 68 In September 1981, the Banca d’Italia recognized the ECU as a currency.Footnote 69 The Belgian-Luxembourgish Monetary Institute did so too in March 1982, and the Bank of France in May 1982. From then, French banks could freely lend in the ECU to non-residents, and could lend in the ECU to residents without the regulations imposed on credits in French Francs. Banks could directly declare their operations in the ECU to the Bank of France. No restriction existed in the UK, the Netherlands, and Denmark. The easing of regulation in EEC countries (except in Germany, which opposed the ECU until 1987) contributed to the development of the private ECU market. In the first half of the 1980s, banks started to treat the ECU as any other foreign currency.

The links between politics and banking were manifold regarding ECU affairs. In September 1985, a Barclays observer noted at a lunch with the French commissioner Claude Cheysson and European bankers that the delegate from Crédit Lyonnais “Virtually repeated everything that Cheysson had said and it was obvious that the act had been well rehearsed between them. He also made a strong plea for more use to be made of the ECU.”Footnote 70 He underlined “the French intention of promoting the use of the ECU at every conceivable opportunity.”Footnote 71

The ECU business, in practice, was initially complex, which made it costly, as it involved transactions in all currencies composing the basket. Private ECUs had downsides. Operations in the ECU were under the threat of insufficient counterparties, which prevented them from going over a year, as they risked fragmentation into national currencies.Footnote 72 Lastly, there was always a possibility that the composition of the public ECU would change, and that was detrimental to the private ECUs’ (which mirrored the public one) attractiveness.

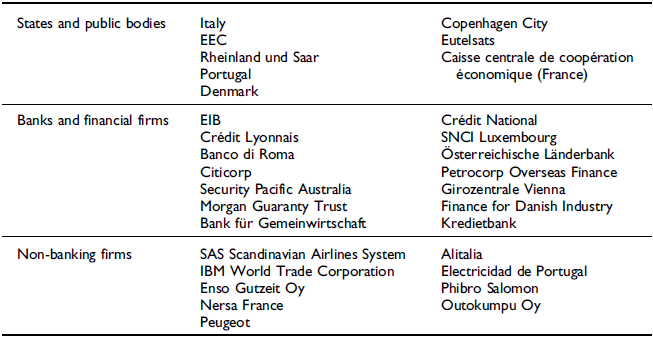

However, private ECUs also had a commercial interest. In 1981, Lloyds was the first bank to issue a certificate of deposit of one month in the ECU, for the EIB.Footnote 73 Other banks followed, such as the Banca Nazionale del Lavoro in 1982. Credits in the ECU developed more slowly, but soon overtook deposits. In June 1981, the French bank Crédit Lyonnais issued a syndicated loan of 200 million ECU to the Crédit National, composed of several certificates of deposits placed by a syndicate led by Goldman Sachs. Italian companies tended to use more credits in the ECU because interest rates in the ECU were lower than in the Italian lira, and the foreign exchange risk was limited, particularly for short-term credits. The first public issue of a bond in the ECU was done by Kredietbank in April 1981 for SOFTE/STET, an Italian telecommunication company.Footnote 74 The bond market in the ECU continued to grow during the first half of the 1980s, and therefore, a secondary bond market also developed. Borrowers also included non-European enterprises, such as the Canadian company Hydro-Québec or City Corp. For investors, investments in the ECU could limit exchange risk and interest rate risk compared to investments in one currency. ECU products could also enable access to currencies that did not have a well-developed financial market. Initially, excessive deposits in the ECU from European institutions, compared to the potential services available in the ECU, forced banks to fragment these deposits again to place them in national currencies. However, the development of the financial market in the ECU helped readjust this market.Footnote 75 Between July 1, 1985, and June 30, 1986, the Europartners banks, a European banking club including Crédit Lyonnais, Banco di Roma, Commerzbank, and Banco Hispano Americano, led or co-led several international credits in the ECU for states and public bodies, banks and financial firms, and non-financial firms, as shown in Table 1.Footnote 76

International Lending in the ECU Led or Co-Led by Europartners Banks between July 1, 1985, and June 30, 1986

The demand for the ECU was stronger in Italy than in other countries because of the instability and the high interest rate of the Italian lira. Dominique Rambure (Crédit Lyonnais) stated in 1983 that in Italy, about 20% of exports were financed in the ECU – a number already significant, but in September 1985, Timothy Bevans, chairman of Barclays, assessed this number at 50%.Footnote 77 In 1985, Barclays advertised that for Italian firms, borrowing in the ECU in 1984 was cheaper than borrowing in Italian lira or in US dollars. Indeed, the borrowing cost of the Italian lira was between 14 and 16% at the time, whereas that of the ECU was about 9.75%. The borrowing cost of the US dollar was then around 9.5%, but because of the depreciation of the lira against the dollar, it was actually more expensive than borrowing in the ECU. Furthermore, the lira was also appreciating against the ECU, which made borrowings in the ECU even cheaper for Italian firms at that time.Footnote 78

Banks also devised various products to promote the use of the ECUs. ECU credit cards were first issued in Luxembourg in 1983.Footnote 79 Visa International and Eurocard International accepted the ECU as an official denominator for payments and transactions. In 1984, Visa International proposed an ECU credit card.Footnote 80 At the time, European banks and the Commission worked on the improvement of European payment systems, with a particular focus on the interoperability of credit cards across the EEC. In September 1985, the Commission issued a discussion paper entitled “Payment cards. Possible Community action,” which stressed the necessity to allow for payments in the ECU via credit cards: “It must also be possible for the new means of payment to be denominated in the ECU. Standardization should allow for this.”Footnote 81 However, progress was slow in the area of payment systems. By 1992, the French “CB Bank Card Group,” bringing together all card operators, was still working on the acceptance of payments in the ECU via payment cards. In addition, some banks started to issue ECU-denominated “Travelers’ cheques” from 1985 onwards. Two different organizations were involved in this initiative: the “Société du Cheque de Voyage en Ecu,” a group of French banks in association with American Express, and the Euro Travellers’ Cheque International group, a group of banks from nine European countries, in association with Thomas Cook.Footnote 82

Banks quickly integrated the private ECU into their routine banking practices. In October 1983, National Westminster Bank, for instance, already offered foreign exchange rates, deposit rates, and account facilities in the ECU.Footnote 83 Within their organization, ECUs were traded as a currency on an equal status with all other major currencies. Wholesale deposits in the ECU of 50,000 ECU and over were directed to National Westminster’s subsidiary International Westminster Bank. Current and interest-bearing accounts could be opened with its Overseas Branch in London. In an internal note to Lloyds, the most active of the British banks in the ECU market, the general manager of the overseas division noted: “we have built up a commanding position in the ECU Market in London […] We made good profits last year in our ECU dealings but as I have suggested in my forthcoming report to the Board of Directors we may face finer margins in the years to come.’Footnote 84 The business of the private ECU was not a political move only: commercial interest was the main logic for selling ECUs to customers.

As already explained, the establishment of a clearing system in the ECU was a major step in the development of the private market for ECUs. Clearing operations in the ECU were complex as they involved many transactions, limiting the potential for private market development. The clearing system that was set up in October 1986 and replaced the previous limited clearing mechanism enabled “its members to offset their reciprocal claims and debts in Ecu and to balance their creditor or debtor positions in Ecu.”Footnote 85

Over time, an increasingly complete financial market developed: loans, bonds, and from 1986, options and futures in the ECU were issued. The development of a futures and options market in the ECU was important. The Amsterdam Stock Exchange was the first to set up an ECU-dollar futures market, on the initiative of its CEO, Tjerk Westerterp, who was also chairman of the European Association of Futures Markets, based in Amsterdam.Footnote 86 Tjerk Westerterp was a former Dutch politician who had been a member of the European Parliament and State Secretary for Foreign Affairs responsible for European cooperation, and was a long-standing advocate of European integration.Footnote 87 But the ECU financial market went far beyond Europe: after Amsterdam, New York, Philadelphia, and Chicago were among the first to develop this futures and options market.Footnote 88

Along with the political support coming from the “ECU network,” the variability of exchange rates and interest rates, the divergence of inflation rates, and the diversity of regulations between countries also favored the development of the private ECU market, just like other financial innovations. In the late 1980s, the liberalization of capital flows, enacted by an EEC directive in 1988, as well as the accumulation of assets in the ECU by central banks and the borrowing of several EEC member states in the ECU, further supported the private ECU market.Footnote 89 This market also became more international over time. In 1983, the primary bond market in the ECU was dominated by French and Belgian banks, whose share in the market was 45% and 30% respectively.Footnote 90 In 1990, banks from these two countries totaled less than 40%, whereas Swiss banks had 18%, American banks 17%, German banks 11%, and Japanese banks 17.5%.

Germany was the last EEC state to accept the private ECU as a currency, in June 1987, and German banks followed suit.Footnote 91 In 1989, Commerzbank suggested offering retail deposits in the ECU to the individual customers of their banking club Europartners.Footnote 92 The same year, the chairman of Deutsche Bank’s supervisory board, and member of CMUE Wilfried Guth underlined the credibility dimension that the “test of the markets” provided, and portrayed the ECU as linked with European monetary unification: “[the ECU] will have to stand the test of the markets. Its success in competition with other currencies will depend (…), in the final analysis, on the apparent political determination to proceed on the road towards European integration beyond 1992.”Footnote 93 The private dimension of the ECU brought credibility to the overall monetary unification project as much as the political will to embark on monetary unification brought credibility to the private ECU.

Thus, several features summarize the financial sector’s contribution to the private market for the ECU: the active role of a few banks whose managers were involved in the “ECU network,” a political game between banking associations and the Commission, and a typical financial innovation development process going from devising products in the ECU to integrating them in banks’ usual business practices. All in all, these features highlight the double nature of the ECU: a political project and a business product. It thereby shows the deep intertwining of market and political forces in ECU affairs.

The ambiguous development of the ECU market also resulted from the uncertainty regarding the future European monetary environment. In December 1993, a consulting firm reported on how bankers and leaders of the financial sector perceived the monetary environment’s future in Europe. Based on 400 interviews, they highlighted a lack of confidence and uncertainty regarding the monetary environment of the 1990s. Only 30% of them believed that more than half of interbank transactions would be in a common currency by 2000.Footnote 94 As late as 1993, bankers were still not sure whether EMU would actually happen. This uncertainty features the role of the private ECU experience as a step in the trust-building process necessary for EMU.

The ECU and the Non-Financial Sector

The rise of the ECU private market in the early 1980s involved the non-financial sector to a small extent. In contrast to banks, the gradual removal of legal obstacles to the use of the ECU, the establishment of the ECU clearing system, and the liberalization of capital flows did not encourage companies to apply the ECU in their transactions. Similarly, a campaign conducted by the politically-inspired AMUE did not bring significant change in this respect. Although by 1990, this Association had almost 200 members, only 10% of them used the ECU.Footnote 95

In 1985, Instituto Bancario San Paolo di Torino, under the supervision of Iozzo, surveyed 200 European non-financial companies that used the ECU. According to the results, 10% of companies used it for invoicing, while 60% for financing foreign trade, and 36% for long-term financing.Footnote 96 In 1988, the AMUE, in cooperation with the European Banking Association and the European Commission, conducted another study among 1,036 managers in European companies, which confirmed that while experimenting with the ECU as a means of financing, very few companies would use it in their transactions. The study also revealed national differences in attitudes towards the ECU. Italian companies were the most eager to use the ECU, while German ones remained the most skeptical. The main reasons for these differences were the weakness of the Italian lira compared to the Deutsche Mark and persistent legal obstacles to the ECU’s use in Germany.Footnote 97 However, the negative attitude toward the ECU among German companies, which British ones also shared, also reflected the positions of these countries regarding EMU. As the ECU was widely considered a tool towards EMU, companies in these countries were hesitant to go against the government’s stance and thus avoided signaling their support of the monetary integration of Europe.Footnote 98

European airlines became early leaders in the non-financial private use of the ECU by the mid-1980s because their operations entailed structural multi-currency exposure across revenues, costs, and interline settlements, making exchange-rate volatility a significant operational concern. This development was closely linked to international and European institutions regulating air traffic and seeking to standardize settlement methods. EUROCONTROL, an intergovernmental organization responsible for European air navigation charges and closely linked to the EEC through overlapping membership and cooperation agreements, announced the ECU as its unit of account in 1986, a change formally implemented in 1990.Footnote 99 The International Air Transport Association followed suit by enabling the ECU alongside the US dollar as a clearing currency between airlines in 1988.Footnote 100 While some companies, notably British Airways, strongly supported this institutionalization of ECU-denominated settlements in order to mitigate dollar volatility, others simply adapted to the changes that necessitated and encouraged the use of the ECU.Footnote 101

Saint-Gobain, a French construction company, began using the ECU as early as 1980 when it became a unit of account within the group. This decision reflected the company’s increasingly multinational character. Having a standardized unit of account encouraged internal cohesion within the group, and the idea of establishing an internal currency for this purpose was considered even before the creation of the ECU.Footnote 102 This initial step soon led to other ECU initiatives. In 1981, the company started using the ECU for invoicing and payments related to internal sales, and since 1982, annual ECU issues were floated. These issues increased in number and variety each year and were offered in collaboration with over 20 banks, including all five original members of the ECU clearing working group.Footnote 103

While facilitating Saint-Gobain’s internal transactions and diversifying its financing methods, the ECU was also interesting due to its political significance. As explained by the company’s president in 1989, the ECU was more attractive than an internal private currency because of its “official aspect.”Footnote 104 Moreover, when justifying the use of the ECU, the company’s management emphasized Saint-Gobain’s “European approach.”Footnote 105 Similarly, the press portrayed Saint-Gobain’s ECU initiatives as “heralding a bright future for the EEC’s currency.”Footnote 106 While going from private to public hands in 1982 and returning to private ownership in 1986, Saint-Gobain maintained a strong pro-European orientation. Its management participated in the establishment of the ERT in 1983 and the company became one of the first members of the AMUE in 1988. This orientation also reflected Saint-Gobain’s business strategy in the 1980s. After experiencing heavy financial pressure in the early years of the decade, the company was reluctant to undertake risky global investments and instead focused on the European market.Footnote 107

Similar to Saint-Gobain, Fiat, whose president, Agnelli, was one of the founders of AMUE, began experimenting with the ECU in the early 1980s. The company also experienced serious losses as a consequence of the 1970s stagflation, as well as rising competition from the US and Japan, which resulted in a major reorganization and created a favorable climate for financial innovations.Footnote 108 The company took mid-term loans in the ECU with the purpose of “diversifying the structure of the company’s indebtedness.”Footnote 109 Fiat also wanted to use the ECU for the financing and invoicing of third-party transactions. However, this objective was difficult given that “foreign customers are not sufficiently familiar with the characteristics of ECU and do not find the interest rate attractive.”Footnote 110

While the EEC-based companies remained reluctant, the interest in the ECU arrived from the outside. The European socialist regimes looking for a stable alternative to the dollar, expressed enthusiasm towards the ECU.Footnote 111 As one of the Western European leaders in building business ties with Eastern Europe since the 1960s, Fiat in 1989 concluded a joint venture agreement with the Soviet Union, which implied an investment of 1.2 billion ECUs.Footnote 112 According to the deal, all transactions were supposed to be recorded in the ECUs convertible into roubles, which allowed Fiat to “manage the company and take decisions as if they were in Turin, Frankfurt or Paris.”Footnote 113 However, the agreement never materialized because of the crisis in the Soviet Union and its subsequent collapse in 1991.

While in the early 1980s, Crédit Lyonnais encouraged Saint-Gobain to broaden its use of the ECU, a similar role was played by Instituto Bancario San Paolo di Torino for Fiat.Footnote 114 The bank was instrumental in popularizing the ECU among Italian companies, and by 1984, it became the largest ECU lender worldwide.Footnote 115 The connection between Fiat and Instituto Bancario San Paolo di Torino was further strengthened by the connection between Iozzo and one of Fiat’s experts on the EEC affairs, Antonio Mosconi, both of whom were members of the European Movement. In the 1980s, Mosconi served on the editorial board of the ECU Newsletter led by Iozzo. The role of individuals knowing the ECU and interested in the development of its private market was instrumental in the implementation of this currency in companies’ transactions. As revealed by Yvonne van Everdingen’s study, the use of the private ECU largely depended on the initiative of individual managers.Footnote 116

In the case of Fiat, the political objectives behind the broader use of the ECU were evident. The company’s management participated in the establishment of the ERT and, later, the AMUE. Agnelli also attended CMUE meetings and became one of the most vocal business leaders supporting the monetary integration of Europe. The 1988 report on Fiat’s use of the included a section entitled “What can be done in addition.”Footnote 117 Using the ECU was not an obvious business choice, but something that management in some companies wanted to develop for political purposes.

However, other companies whose leaders steered AMUE hardly used the ECU, despite voicing support for the parallel currency strategy for European monetary integration. This was the case of Philips, whose CEO Cornelis van der Klugt, while calling for the wider use of the ECU as the president of the AMUE also admitted that it “plays a modest role within Philips.”Footnote 118 Indeed, by 1988, Philips had issued only one loan worth 75 million ECUs.Footnote 119 Similarly, Bosch, a German technology company, did not use the ECU despite being represented on the AMUE board. The company’s report from 1988 pointed out that although the Bundesbank finally recognized the ECU in 1987, “traditional objections within the German business community do not change as long as exchange rates are necessary to balance different prices and developments between the countries.” According to the document, in such circumstances “invoicing in ECU would cause negative Terms of Trade.”Footnote 120

The lack of short-term benefits emerging from the ECU, persistent legal obstacles, and the stability of European currencies such as the deutsche mark and guilder limited the rise of the private ECU in these countries. However, studies conducted by the AMUE in collaboration with the European Commission revealed that crucially, companies did not use the ECU because they did not know it, because they had different corporate habits, and because of the currency’s private character.Footnote 121 As demonstrated by the 1985 survey funded by the banks from the European Banking Association, the ECU was known by 6 out of 10 citizens of France, Belgium, and Luxemburg, 3 out of 10 citizens of Italy, Germany, and the Netherlands, and only 1 of 10 British citizens.Footnote 122 Popularizing the ECU among the companies was the primary objective of the AMUE. Similarly, the Association tried to encourage companies to revise their corporate habits. However, this proved very difficult given that the ECU did not offer immediate benefits to most companies and that it was still technically not a currency. The lack of a European central bank was named as one of the key factors limiting the wider use of the ECU, according to The Strategy for ECU, the AMUE’s flagship study from 1990.Footnote 123

In addition to highlighting the need for institutional supervision, the study showed that a parallel currency made little sense for the non-financial sector and that a single currency could offer companies greater benefits, above all by reducing their international transaction costs.Footnote 124 In this shift from a parallel to a single currency approach, the AMUE followed the 1989 Delors Report, which offered a blueprint for EMU. The AMUE’s support served the European Commission as a useful argument for this project.Footnote 125

At the same time, despite abandoning the parallel currency idea, the private ECU still mattered for EMU. As explained by Niels Thygesen, an economist and member of the Delors Committee working on EMU and of the CMUE: “The [Delors] Report does, however, give indirect and fundamentally more important support to the present ECU. It emphasizes the benefits of a single currency, and it states that the ECU has the potential to become the future common currency…It is very important for markets to know that at an advanced stage of integration there will be a unit defined in continuity with the present ECU…”Footnote 126 Eventually, the ECU was also mentioned in the 1992 Maastricht Treaty, which established the EMU. According to the document, the European Monetary Institute—the forerunner of the European Central Bank—was supposed to “facilitate the use of the ECU and oversee its development, including the smooth functioning of the ECU clearing system.”Footnote 127 Although the name ECU disappeared and the European currency did not ultimately take a parallel form, the ECU nonetheless played a crucial role in the transition to EMU and in defining the value of the euro.

The ECU’s political dimension had a strong influence on whether the non-financial sector used it or not. On the one hand, support for European integration encouraged, as in the case of Saint-Gobain, or motivated, as in the case of Fiat, developing transactions in the ECU. On the other hand, some companies disregarded the ECU because of their, or their countries of origin’s, negative attitude towards EMU. At the same time, for some non-financial businesses, the ECU was not certain enough. Increasing the use of the ECU implied leaving behind verified corporate habits. Few companies were willing to do so for a financial innovation that was loosely linked with European institutions and which, at that time, could be short-lived. Except for small transactions and individuals involved in the “ECU network,” companies were also not committed enough to the EMU project to make an effort in the name of this goal. However, their experiments with the ECU helped to popularize the idea of a European currency and to define its eventual form.

Conclusion

The public-private “ECU network” played a pivotal role in popularizing the ECU, encouraging its adoption among businesses to advance a political agenda. This strategy proved especially effective with banks, for which the ECU represented a profitable financial innovation. However, the uptake among non-financial industries was hampered by the impractical dimension of the ECU, which offered few immediate advantages to these sectors.

The history of the ECU private market challenges conventional views of business involvement in politics. Some individuals—for example, firm leaders or those involved in foreign exchange—in both financial and non-financial companies were central players in the “ECU network,” actively participating in debates on parallel currencies and in the creation of institutions dedicated to promoting the ECU. For most of those, business interests aligned with political support for European integration. Meanwhile, other companies, particularly banks, became unintentional agents of integration. Their use of ECU for commercial purposes furthered EMU goals. Neither of these forms of business involvement aligns with traditional lobbying practices.

The growth of the ECU private market, driven by both individuals involved in the “ECU network” and by enterprises indifferent to European integration, strengthened the political EMU project. By popularizing the ECU, it enhanced credibility and awareness of European monetary integration, allowing businesses and the public to grow accustomed to the concept of European money. Banks played a crucial role by devising innovative ways to use the ECU and offering these solutions globally. The private ECU familiarized actors with the idea of a stable and independent European currency, laying the groundwork for principles that shaped the euro. In this way, the private ECU served as a “rehearsal” for European currency in real-world conditions.

While this currency desired by business was to be stable and independent, it was not to be private. Thanks to political backing by European institutions, its success was larger than that of other basket currencies. The connection with the European project motivated individuals to engage in the “ECU network” and later use their professional position to popularize the ECU, but the absence of a clear institutional link to European authorities also deterred some companies. Many saw the ECU as a temporary experiment, lacking long-term commitment. In particular, non-financial sectors were discouraged by the lack of a central bank overseeing the ECU. The ECU’s history thus highlights the limits of business support for private money: even in the heyday of neoliberalism, business actors valued political oversight of currency.

Acknowledgments

We would like to thank Alfonso Iozzo and Éric De Keuleneer for finding time to discuss with us the ECU private market. We are also grateful to Ivo Maes and Emmanuel Mourlon-Druol for commenting on drafts of this article.

Funding statement

This project has received funding from the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation programme (grant agreement No 716849).

Author biography

Alexis Drach is assistant professor in modern economic history at Paris 8 Vincennes-Saint Denis University. His interests lie in the history of banking regulation and supervision, banks’ internationalization, European integration, globalization, and expertise. He is author of Liberté surveillée: supervision bancaire et globalisation financière au Comité de Bâle, 1974-1988 (2022) and co-edited, with Youssef Cassis, Financial Deregulation: A Historical Perspective (2021). He has published articles in journals such as Enterprise & Society, Business History, Financial History Review, and the European Review of History.

Aleksandra Komornicka is an assistant professor at the Faculty of Arts and Social Sciences at Maastricht University. Her research covers the international and economic history of post-war Europe in particular the history of the Cold War, European integration, and business. Aleksandra is the author of Poland and European East-West Cooperation in the 1970s The Opening Up (2023) and co-author of the second edition of The Unfinished History of European Integration (2024). Her research has appeared in journals such as Business History, Cold War History, and Contemporary European History.