IntroductionFootnote 1

Why and how does legalism emerge in policy domains long governed by informal coordination? Japan offers an especially revealing case. Despite being considered a “hard case” for judicializationFootnote 2—given a regulatory style defined by informality, bureaucratic control, long-term single-party dominance, and a comparatively low litigation rate—it has nonetheless experienced a gradual yet significant legalistic turn across several policy fieldsFootnote 3 (for example, Kidder and Miyazawa Reference Kidder and Miyazawa1993; Upham Reference Upham2011; Arrington Reference Arrington2016, Reference Arrington2025; Akiba Reference Akiba2023; Higa and Faumuina Reference Higa and Faumuina2024; Sala Reference Sala2024). This evolution supports Judith Shklar’s observation that “it is (…) necessary to think of legalism as a matter of degree, rather than as either ‘there’ or ‘not there,’ as lawyers think of law” (Shklar 1986 [Reference Shklar1964]:15). Legalism, in this sense, is not a fixed institutional condition but a continuum of practices through which law progressively permeates governance. Drawing from this scholarship, this paper argues that legalism in Japan is best understood as an emergent, embedded process of institutional realignment rather than a fixed mode of governance.

This analysis resonates with a complementary strand of scholarship that conceptualizes legalism as a mode of governance structuring economic and regulatory relations. Building on Robert Kagan’s (Reference Kagan, Miller and Barnes2004, Reference Kagan2007, Reference Kagan2019) concept of Adversarial Legalism—a distinctly American system of rule enforcement characterized by formal procedures, adversarial dispute resolution, and litigation-based accountability—Daniel Kelemen (Reference Kelemen2011) developed Eurolegalism as its European counterpart. Eurolegalism emphasizes judicialized policy enforcement and procedural accountability, yet operates in a more restrained form shaped by national legal traditions and institutional norms (Barnes and Burke Reference Barnes and Burke2020). Kelemen identifies two key mechanisms driving this transformation. The first is the dual process of deregulation and juridical re-regulation accompanying the creation of the EU single market: as economic liberalization eroded informal and corporatist modes of regulation, they were replaced by pan-European legal frameworks emphasizing transparency, formality, and rights-based enforcement—often through private litigation (Kelemen Reference Kelemen2011, 7–8). The second arises from the EU’s fragmented institutional architecture, where limited administrative capacity and dispersed authority led policymakers to rely on courts and private actors for decentralized implementation (Cichowski Reference Cichowski2006; Hofmann Reference Hofmann2019).

Extending the Framework: Legalism from Below and the Rationale for Case Selection

While US and European perspectives highlight how fragmented authority and weak administrative capacity foster adversarial and judicialized forms of governance, Celeste Arrington’s analysis of Japan and South Korea demonstrates how legalism can also emerge from below, through the coordinated actions of lawyers and activists rather than judicial or bureaucratic initiative (Arrington Reference Arrington2025). Building on her insights, this paper analyzes Japan’s legalistic turn as a process of institutional formalization in which spheres once governed by informal and voluntary practices become subject to legal oversight and procedural enforcement. The shift from informality to formalization captures the trajectory of Japan’s legalistic governance, where courts and lawyers shape the process of legalization within areas deliberately left underregulated by political and economic elites (for example, Cichowski Reference Cichowski2006; Barnes and Burke Reference Barnes and Burke2015; Vanhala Reference Vanhala2018). The Japanese consumer finance case exemplifies this dynamic particularly well.

The politics of debt has long been structured by competing moral and legal imaginaries. Michael Hudson’s analysis of the Greco-Roman rupture—where absolute creditor rights replaced earlier traditions of contextualized or collective debt relief—highlights how legal regimes embed normative assumptions about responsibility, fairness, and economic order (Hudson Reference Hudson2018). This historical contrast provides a productive backdrop for analyzing the Japanese case, where the unsecured non bank loan sector became a key arena for contesting both the moral assumptions and the weak legal foundations that had long structured indebtedness. In the early 2000s, a sequence of Supreme Court decisions required lenders to reimburse interest charged above the Interest Rate Restriction Act ceiling, dismantling the previously tolerated grey zone and gradually redefining key elements of financial regulation (Pardieck Reference Pardieck2008; Ono Reference Ono2011; Colombo and Shimizu Reference Colombo and Shimizu2016). These rulings provoked strong reactions from industry actors and some policymakers, who framed judicial intervention as excessive (Kozuka and Nottage Reference Kozuka and Nottage2009a; Ramseyer Reference Ramseyer, Wulf, Schmidt and Schwartze2014). This conventional opposition between judicial power, political branches, and administrative agencies often tends to oversimplify the judiciary’s role, portraying courts either as neutral enforcers of the law or as overreaching policymakers (for example, Guarnieri and Pederzoli Reference Guarnieri and Pederzoli2002). By framing the process as a zero-sum struggle rather than an integral component of democratic governance, the binary perspective overlooks the more nuanced ways in which judicial institutions interact with and respond to policymaking dynamics (for example, Tate and Vallinder Reference Tate and Vallinder1995).

While existing scholarship has examined the Japanese consumer finance case for its remarkable policy outcomes—particularly the Supreme Court’s role in generating one of the strictest interest-rate regulatory regimes among liberal economies—it has rarely been analyzed through a theoretical lens capable of identifying the broader mechanisms it reveals. Moreover, comparative scholarship on varieties of legalism has not incorporated this case into broader analyses of Japan, despite its relevance for understanding how legalism can emerge within a consensus-oriented and informally coordinated governance system. This paper addresses these gaps by theorizing the mechanisms at work and demonstrating their significance for the study of legalism beyond this specific policy field.

First, this case reveals how regulatory ambiguity and weak enforcement functioned as integral features of Japan’s governance architecture—mechanisms designed to preserve flexibility through institutional complementarity between the formal banking and informal non bank sectors. Second, from a bottom-up perspective, it also exposes a mechanism that complements Arrington’s framework: the transformation of individualized claims into a collective cause in the absence of preexisting collective identities or rights-based narratives. Unlike disability rights movements, which mobilized around clear collective identities and normative legitimacy, or tobacco control activism, which challenged entrenched social practices through public health and rights-based arguments, consumer lending posed the opposite challenge. With borrowers stigmatized, litigation individualized, and no class action mechanism available, debt was widely perceived as a moral rather than structural problem. Lawyers, therefore, had to construct a collective problem where none existed, reframing indebtedness as a symptom of broader governance asymmetries and institutional shortcomings. This dynamic exemplifies a form of cause lawyering in which legal professionals initiate and sustain mobilization in the absence of preexisting collective identities or organized constituencies (Sarat and Scheingold Reference Sarat and Scheingold2005; Cummings et al. Reference Cummings, Butter, Hammerslev and Anzola Rodriguez2025).

Research Aim and Analytical Contribution

First, the paper conceptualizes Japan’s legalistic turn as an incremental process of formalization that emerges when informal or voluntary mechanisms prove insufficient, whereby courts, lawyers, and policymakers reallocate responsibility across administrative, political, and corporate domains, thereby redefining the contours of accountability within the governance system. Bringing Japanese sociolegal scholarship into dialogue with Western analyses is particularly valuable for understanding these dynamics. Scholars studying why citizens turn to courts to defend causes, safeguard interests, or contest perceived injustices consistently show that legal action often emerges from gaps in political representation, weak participatory channels, or widening disconnections between policymakers and public concerns (for example, Zemans Reference Zemans1982; Tanaka and Takeuchi Reference Tanaka and Takeuchi1987; Tanaka Reference Tanaka1979, Reference Tanaka1996; Cichowski and Stone Sweet Reference Cichowski, Stone Sweet, Bruce, Dalton and Susan2003; Awaji Reference Awaji2011, Reference Awaji, Awaij, Teranishi, Yoshimura and Okubo2012; Arrington Reference Arrington2016, Reference Arrington2025; Vanhala Reference Vanhala2012; Israël Reference Israël2020; Lehoucq and Taylor Reference Lehoucq and Taylor2020). Second, by framing judicialization as a form of responsive justice embedded within Japan’s informal, bureaucratic, consensus-oriented order, the paper offers an analytical complement to theories of responsive law and work on how judges internalize shifting normative and evidentiary frames (Nonet and Selznick Reference Nonet and Selznick1978; González-Ocantos Reference González-Ocantos2016; Watanabe Reference Watanabe2019; Sala Reference Sala2025b). Third, the consumer finance case contributes to debates on judicial behavior in Japan. Scholars have shown that courts operate strategically within a political landscape dominated by the Liberal Democratic Party (LDP), exercising restraint in politically sensitive domains such as national security or socioeconomic policy while showing greater assertiveness in areas with lower political costs, including individual or minority rights (Akiba Reference Akiba2023; Kitade Reference Kitade2023; Higa and Faumuina Reference Higa and Faumuina2024).Footnote 4 Ginsburg and Matsudaira (Reference Ginsburg, Matsudaira and Dressel2012) argue that such restraint reflects not weakness but a calculated effort to preserve institutional legitimacy within a bounded political environment. Acknowledging these constraints, the paper argues that Japan’s legalistic turn extends beyond identity- and human-rights-based domains to encompass socioeconomic regulation. Fourth, it contributes to the institutional change literature by examining how inter-branch relations—particularly the interaction between courts, bureaucracies, and legislators—shape policy transformation in a coordinated market economy (for example, Streeck and Thelen Reference Streeck and Thelen2005; Barnes and Burke Reference Barnes and Burke2015). It also builds on work that foregrounds the understudied role of lawyers and advocates in activating these dynamics and shows how their mobilization mediates judicial influence and channels it into institutional change (Epp Reference Epp2009; Cummings Reference Cummings2020; Arrington Reference Arrington2025, 48–49).

I propose a processual and integrative framework for analyzing Japan’s legalistic turn, identifying three mechanisms through which institutional design, legal advocacy, and consensus formation interact to produce regulatory change.

The consumer finance case illustrates these mechanisms and shows how their interaction produces incremental yet durable legalization, with institutional change emerging as the cumulative outcome of these linked processes over time.

Methodological Approach and Structure of the Paper

This study employs a process-tracing approach to analyze the sequential interaction between social mobilization, judicial interpretation, and legislative adaptation, drawing on a longitudinal review of court decisions (from the 1950s to the 2000s); statistical data from industry associations, the Ministry of Health, Labor and Welfare (MHLW), the Supreme Court, and the Japan Federation of Bar Associations (JFBA); and a close study of parliamentary debates, working-group deliberations, and media coverage across the 1983 and 2005–2010 reform cycles.Footnote 5 Together, these sources reveal how political actors, industry groups, lawyers, and consumer advocates negotiated regulatory scope, enforcement mechanisms, and borrower protections, enabling the incremental formalization of governance in the consumer finance regime.

The paper proceeds in four sections. Section 1 develops the theoretical framework of processual legalism, introducing the three mechanisms that guide the analysis. Sections 2–4 trace how these mechanisms unfold sequentially over time, making visible the processual dynamics through which legalism develops. Section 2 examines the emergence of institutional friction from the evolving formal-informal complementarity of Japan’s financial system and the resulting reliance on courts to compensate for regulatory gaps. Section 3 analyzes the limited reach of judicial influence in the first lawmaking cycle and traces the gradual emergence of normative reframing through lawyers’ mobilization over time. Section 4 shows how the eventual convergence of judicial reasoning, normative reframing, and political opportunity produced consensus realignment and enabled the reregulation process. The conclusion argues that Japan’s legalistic turn is best understood as episodic, incremental, and consensus-dependent, thereby revealing a distinctive variety of legalism.

Conceptual Framework: Mechanisms of Processual Legalism

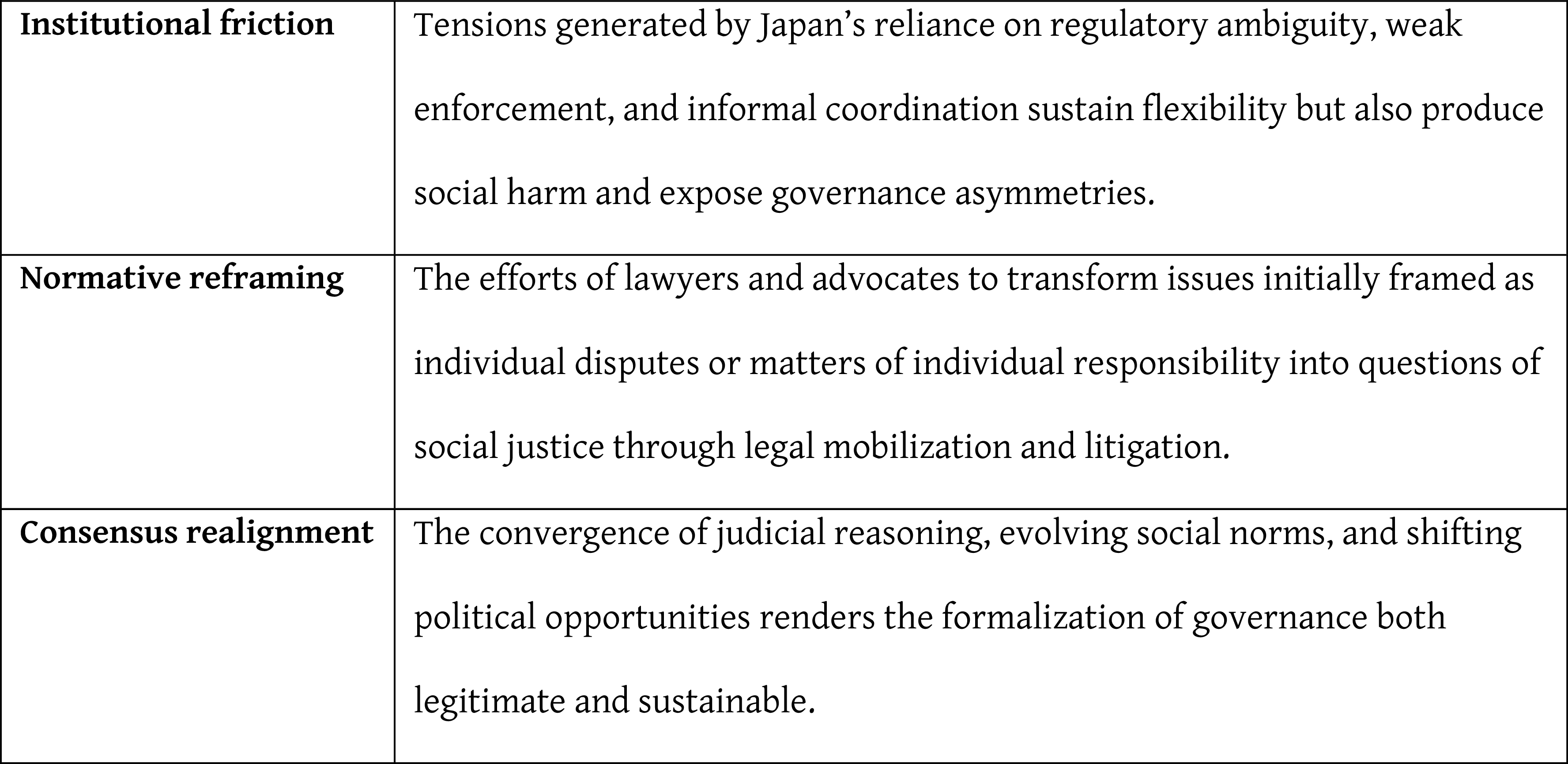

This section develops the theoretical framework of processual legalism by introducing the three mechanisms—institutional friction, normative reframing, and consensus realignment—that unfold sequentially and interactively, showing institutional change as the cumulative outcome of linked processes that unfold over time.

Institutional Friction: The Tension Between Governance Flexibility and Regulatory Accountability

Japan’s governance style rests on close coordination among ruling political elites—particularly the LDP—powerful ministries such as the Ministry of Economy, Trade and Industry (METI), and major business federations like Keidanren (Japan Business Federation) (Johnson Reference Johnson1982; Lechevalier Reference Lechevalier2014). While this coordinated model succeeded in establishing stability and policy continuity, it simultaneously generated significant regulatory blind spots—stemming from regulatory capture, industry collusion, and a reliance on nontransparent administrative practices (Kagan Reference Kagan2019). In practice, the Japanese government privileges soft law: ministries steer firms through industry self-regulation, and negotiated compliance rather than through binding, enforceable rules (Upham Reference Upham1987). Administrative guidance (gyōsei shidō) remains the core enforcement tool, offering flexibility for industrial policy but weakening mechanisms of corporate accountability, particularly given ministries’ limited coercive authority and resources (Haley Reference Haley1991, 163–64). As lawyer Hamada Kunio observes, even with an independent and competent judiciary, longstanding bureaucratic–industry networks enable privilege-based abuses—such as bid-rigging and collusive contracting—that diffuse legal responsibility and shield powerful actors from meaningful oversight.Footnote 6 Overall, rather than imposing strict oversight, the government preserved a degree of flexibility by relying on institutional complementarity between formal and informal practices—a structural feature that extended across the dual organization of Japan’s economy (Boyer and Yamada Reference Boyer and Yamada2016).

Streeck and Thelen (Reference Streeck and Thelen2005) define institutions broadly as normative constraints on behavior, enforced either through third-party legal authority or through social norms and expectations. Formal and informal institutions differ in origin, not in obligatory force—the former emerge through deliberate legal design, the latter through social practice. Crucially, informal institutions are not residual; they operate as integral components of governance. In Japan, formal rules and informal practices were mutually reinforcing, sustaining a system that privileged negotiated compliance over coercive enforcement. This configuration reflected the hierarchical logic of Japan’s postwar capitalism, in which long-term relational lending and state-coordinated oversight prioritized large firms, leaving individuals and SMEs at the periphery of credit access (Aoki and Patrick Reference Aoki and Patrick1994; Yamori Reference Yamori2004). The non bank sector thus occupied a central position: it filled the gaps left by the formal banking system while operating through opaque and weakly regulated mechanisms. This sectoral interdependence reveals a deeper structural feature of Japan’s coordinated market economy,Footnote 7 whose institutional foundations explain the persistence of regulatory ambiguity (Hall and Soskice Reference Hall and Soskice2001). Scholars such as Ronald Dore have emphasized the flexible rigidities of Japanese capitalism, showing how highly regulated formal sectors were stabilized by adaptive, less regulated spheres sustained by informal practices and administrative guidance (Dore Reference Dore2000; see also Vogel Reference Vogel2006). These mechanisms enabled the system to absorb economic pressures and adapt without abandoning its core institutional logic (Vogel Reference Vogel1996; Hamada Reference Hamada, Coen, Grant and Wilson2010; Lechevalier Reference Lechevalier2014; Boyer Reference Boyer2015).

Consequently, when administrative oversight proved ineffective or absent, courts emerged as an alternative forum for enforcing accountability, challenging corporate negligence, and state inaction (Tanaka Reference Tanaka1996; Ginsburg Reference Ginsburg, Ginsburg and Albert2008; Awaji Reference Awaji2011). Japanese sociolegal scholars have conceptualized this phenomenon through key frameworks that link litigation to policymaking: gendai-gata soshō (contemporary-type litigation), seisaku keisei soshō (policy-formation litigation), and seido kaikaku soshō (institutional reform litigation). These concepts illuminate how courts, when confronted with administrative inertia, can serve as catalysts for institutional adaptation. Tanaka’s notion of policy-formation litigation highlights how judicial rulings prompt bureaucracies and political actors to revise enforcement practices and refine procedural norms (Tanaka Reference Tanaka1996). Awaji’s institutional reform litigation further develops this framework, capturing later waves of legal mobilization—particularly following the pollution trials of the 1970s—where litigation operated in tandem with legislative advocacy, public campaigning, and policy reform efforts (Awaji Reference Awaji, Awaij, Teranishi, Yoshimura and Okubo2012, see also McCann Reference McCann1994; Barnes Reference Barnes, Barnes and Mark2004; Anderson Reference Anderson2005; Vanhala Reference Vanhala2012; Barnes and Burke Reference Barnes and Burke2015). Thus, institutional friction operates as a triggering mechanism: regulatory ambiguity, weak enforcement, and informal coordination produce recurrent implementation failures and perceived injustices, creating tensions that prompted legal activism and demands for legal and policy redress.

Normative Reframing: From Individual Grievances to Structural Critique

Through litigation, public advocacy, and coordinated outreach, Japanese lawyers have, in various cases, strategically leveraged judicial rulings to catalyze public debate, pressure bureaucratic and political actors, and translate courtroom outcomes into policy reform, particularly in areas such as human rights, minority protection, labor relations, and consumer and environmental governance (for example, Otsuka Reference Otsuka2009; Arrington Reference Arrington2016; Foote Reference Foote and Patricia2014; Kawahito Reference Kawahito2022; Akiba Reference Akiba2023; Sala Reference Sala, Cummings, Hammerslev, Butter and Anzola2025a). These committed lawyers frequently coordinate with civil society organizations, plaintiffs’ groups, scholars, doctors, and journalists to generate data, shape narratives, and sustain political visibility—exemplifying the processes of naming, blaming, and claiming (Felstiner et al. Reference Felstiner, Abel and Sarat1981; see also Feldman Reference Feldman2000, Reference Feldman2009; Oyama Reference Oyama2020). Arrington (Reference Arrington2025) illuminates the bottom-up mechanisms through which lawyers and advocates—rather than judges or bureaucrats—drive Japan’s legalistic turn. Her framework identifies five mechanisms—rights framing, coalition building, information subsidies, strategic litigation, and accountability politics—that explain how legal mobilization expands access to policymaking arenas and gradually formalizes governance from below (Arrington Reference Arrington2025, 42–43).

This study highlights a related yet distinct process: normative reframing. In terms of social-movement theory, this mechanism is closest to diagnostic and injustice framing, through which actors define what is wrong, attribute responsibility, and infuse a situation with moral indignation (Gamson Reference Gamson1992; Benford and Snow Reference Benford and Snow2000). In the Japanese consumer credit case, legal professionals strategically transform individualized claims into collective problems by converting the moralized understanding of debt—anchored in a discourse of individual responsibility—into a structural and legally actionable critique. In Gamson’s terms, they do so by combining an injustice component with an adversarial component: they express moral outrage at borrowers’ hardship and attribute responsibility to concrete, motivated actors—consumer finance companies and, increasingly, regulators and policymakers who enabled their practices—rather than to borrowers’ alleged irresponsibility. Litigation allows them to construct a concrete “they” through defendant-plaintiff relations and doctrinal argument.

In contexts such as Japan, where adversarial rights’ claims often clash with cooperative governance logics, lawyers and advocates adapt by mobilizing alternative normative frames. Rather than grounding their arguments in rights discourse, they draw on culturally resonant notions of responsibility, fairness, and social obligation to expose governance asymmetries and legitimize calls for reform (Rozen Reference Rosen2001). This responsibility discourse operates as a conceptual complement to rights framingFootnote 8: it translates moral expectations into political claims while remaining compatible with bureaucratic coordination and consensus-oriented politics. In doing so, it redefines accountability by shifting it from the individual to the institutional and collective levels, articulating social justice not as an entitlement but as a shared duty extending across state, corporate, and civic actors.Footnote 9

Normative reframing thus provides a critical bridge between institutional friction and consensus realignment. By translating structural tensions—such as regulatory gaps and uneven enforcement—into compelling moral and political claims, lawyers and advocates create the interpretive space for courts and policymakers to adjust existing norms. This dynamic resonates with findings by González-Ocantos (Reference González-Ocantos2016), who shows that judicial change often follows sustained efforts by lawyers and civil society actors to supply new interpretive frames, evidence, and normative categories that enable judges to rethink the moral and legal meaning of contested practices. Recent work on prosecutors similarly demonstrates how legal professionals’ framing work shapes which issues the prosecutorial institution treats as salient and actionable (Vilaça Reference Vilaça2024). In the Japanese case, responsibility-centered normative reframing prepares the ground for consensus realignment by redefining responsibility itself—shifting it from an individualized moral burden to a collective institutional duty placed on lenders, regulators, and legislators. In doing so, it transforms the normative foundations of Japan’s informal governance model into a basis for its gradual formalization.

Consensus Realignment: Structuring Moral, Social, and Political Support for Institutional Reform

Scholars analyzing litigation rates and constitutional review often characterize the Japanese judiciary as passive and conservative, arguing that its limited engagement with major policy issues reflects a comparatively low level of judicialization (for example, Helmke and Rosenbluth Reference Helmke and McCall Rosenbluth2009; Satō Reference Satō2008; Law Reference Law2009; Matsui Reference Matsui2011). Judith Shklar’s work offers an important corrective to this view. Her notion of the “conservatism of consensus” provides a key theoretical lens for understanding the mechanism of consensus realignment (Shklar Reference Shklar1964, 10). For Shklar, law’s conservatism does not derive from judicial passivity but from its stabilizing function: “law is itself a conservatizing ideal and institution.” The judiciary sustains social continuity by presenting adaptation as neutrality—“the judiciary demonstrated its neutrality by adapting to the new order as it had supported the old” (1964, 11). Judicial change, therefore, occurs when courts adjust existing norms to reflect new moral or political realities that have gained sufficient legitimacy to be incorporated into law (for example, Nonet and Selznick Reference Nonet and Selznick1978; Watanabe Reference Watanabe2019; Sala Reference Sala2025b). González-Ocantos (Reference González-Ocantos2016) shows that judicial change becomes possible when new norms gain legitimacy in the broader political environment, reducing the reputational or institutional risks for judges. As Shklar emphasizes, judicial authority is grounded in consensus: “Without consensus the appearance of neutrality evaporates,” and when decisions threaten entrenched interests, judges are swiftly accused of “legislating” rather than applying law (1964, 11). Under such conditions, courts tend to retreat into formalism to preserve institutional legitimacy.

In the Japanese context, consensus realignment operates in close interaction with normative reframing. Courts seldom initiate transformative change without a prior shift in social consensus; instead, they respond once institutional frictions between formal and informal practices provoke changes in public discourse, governance failures, or political fragmentation that unsettle established expectations. In fields such as consumer finance, labor, and environmental governance, landmark judicial rulings typically follow the groundwork laid by lawyers and advocates who redefine norms of individual responsibility into structurally framed problems. Through this reframing, they generate the minimal consensus necessary for judicial adjustment, enabling courts to reinterpret ambiguous norms without appearing politically confrontational. Consensus realignment, however, does not arise from legal mobilization alone. As Ran Hirschl (Reference Hirschl and Robert2011) emphasizes, judicial influence becomes most effective when court decisions align with the interests and priorities of key political and economic stakeholders. When judicial interpretations resonate with evolving policy agendas, they furnish political actors with a legitimate legal basis for pursuing regulatory reform (Anderson Reference Anderson2005, 6). This convergence—linking judicial reasoning, emergent social consensus, and favorable political opportunity structures—creates the conditions under which judicial influence becomes credible, sustainable, and embedded within broader coalitions advocating institutional change. Consensus realignment thus describes the process through which evolving legal, moral, and political understandings become sufficiently consolidated to authorize legal reinterpretation and enable policy transformation.

Figure 1 presents the three core mechanisms underlying the theoretical framework of processual legalism.

Core Mechanisms Driving Legalistic Transformation

The following section turns from theoretical mechanisms to their empirical manifestation in Japan’s consumer finance case.

Institutional Friction and Judicial Response: Regulatory Ambiguity, Limited Enforcement, and Japan’s Dual Credit System

This section examines how institutional friction emerged within Japan’s consumer finance regime and how it activated judicial involvement.

Formal - Informal Complementarity in Japan’s Consumer Credit Market

Japan’s postwar banking policies created a highly regulated financial environment that restricted credit access for many borrowers. Banks operated under strict government oversight, with regulations that included interest rate controls, the allocation of credit to strategic industries, and restrictions on market competition (Okazaki Reference Okazaki1995; Aoki and Patrick Reference Aoki and Patrick1994). These measures safeguarded weaker banks from failure, directed capital into industrial development, and mitigated systemic financial risks. However, these stringent controls came at a cost: they stifled financial innovation, increased banks’ dependence on government policies, and created a rigid system that prioritized stability over competition (Hoshi Reference Hoshi2002; Amyx Reference Amyx2004; Boyer and Yamada Reference Boyer and Yamada2016). As a result, banks were limited in their ability to extend credit to individual borrowers and small businesses. This gap was filled by non bank lenders, whose legal framework remained far more flexible.

Since 1954, two key laws have shaped the non bank credit sector, creating a structural discrepancy in interest rate regulation. Under the Civil Code, the Interest Rate Restriction Act (IRRA, risoku seigen hō)Footnote 10 sets a formal interest rate limit of 20 percent, but it lacks enforcement provisions, meaning lenders face no legal penalties for exceeding this cap. By contrast, the Penal Code’s Act on the Regulation of Acceptance of Investment, Deposits, and Interest Rates (IA, shusshi hō)Footnote 11 governs interest rates for unsecured loans, capping total credit charges at 109.5 percent and imposing criminal sanctions only if this upper threshold is breached. This legal misalignment has created a grey zone: a regulatory gap between 20 percent and 109.5 percent, within which lenders can impose high-interest rates without facing criminal penalties. As a result, non bank lenders consistently leveraged regulatory ambiguity to operate within a legally undefined space, supported by an implicit consensus that tolerated grey-zone lending as part of Japan’s broader financial architecture. Rather than imposing strict oversight, the government preserved a degree of flexibility, allowing non bank lenders to continue serving borrowers who lacked access to formal credit channels.

The coexistence of these two financial spheres—one heavily regulated, the other largely unrestricted—exemplifies an institutional complementarity, where formal and informal credit markets evolved in response to regulatory constraints (Shem and Atieno Reference Shem and Atieno2001; Liang Reference Liang1988). The non bank sector thus occupied a paradoxical position: it addressed market gaps left by the formal system. Yet, the absence of formal regulation did not imply an absence of governance: in many areas—particularly the non bank consumer credit market—social norms operated as powerful regulatory forces. In the unsecured loan sector, regulatory leniency was counterbalanced by social norms and moral values shaped by government savings policy, banking restrictions, and broader societal expectations. While non bank lenders provided an alternative source of credit, strict banking oversight and limited consumer credit options contributed to a financial culture that emphasized caution and self-reliance (Horioka Reference Horioka, Garon and Patricia2006; Gordon Reference Gordon and Logemann2012). These banking regulatory constraints did more than restrict borrowing; they actively institutionalized saving patterns and structured access to credit, further embedding social norms that stigmatized debt (Nishimura Reference Nishimura, Sheldon and Patricia2006; Gordon Reference Gordon and Logemann2012). By diffusing norms that discouraged borrowing, rigid banking regulations indirectly constrained demand for unsecured non bank credit, ensuring that it remained a marginalized yet functionally necessary market. Non bank lenders continued to serve borrowers with urgent financial needs, operating within localized networks. These influences collectively discouraged excessive borrowing and reinforced a deeply rooted ethos of individual responsibility.

Whereas much of the scholarship suggests that excessive regulation pushes informality underground, Japan’s non bank credit sector reveals a more mutually dependent configuration. Formal oversight and informal financial practices evolved together, producing a tolerated space of regulatory ambiguity. Within this intermediary space, moneylenders operated under a regime of adaptive compliance, exploiting flexibility while remaining nominally lawful—leaving courts to adjudicate the boundaries of legality case by case.

Judicial Alignment to Regulatory Ambiguity and Limited Enforcement

This regulatory ambiguity allowed moneylenders to charge high interest rates while shifting the burden of oversight onto the judiciary, which was compelled to assess legality on a case-by-case basis. Judicial reasoning was guided by a form of substantive justice concerned with the moral fairness of credit relationships, balancing borrower protection with notions of individual responsibility through legal principles such as public order and good morals (kōjo ryōzoku) (Pardieck Reference Pardieck2008). Borrowers lacked direct mechanisms to contest excessive interest rates unless they initiated individual legal action, and courts could not automatically invalidate unlawful rates without a specific claim. Judicial rulings therefore became crucial in determining whether lending practices aligned with broader legal principles such as public order, morality, borrower protection, and fairness in lending (Ono Reference Ono2011). Judicial decisions in the 1950s reflected a prevailing social consensus that legitimized voluntary and self-regulatory approaches to lending. At the time, borrowing outside personal or corporate networks was socially exceptional—most individuals obtained credit informally from family, acquaintances, or employers, while small and micro-enterprises relied on trusted lenders within their local communities. The non bank unsecured loan market, by contrast, was associated with short-term cash needs and carried a moral stigma. Within this context, courts placed the burden of proof on borrowers, who had to demonstrate exploitation to obtain relief. Judges thus operated within what Shklar (Reference Shklar1964) calls the conservatism of consensus: they reinforced existing social norms rather than contesting them.

For instance, in a 1954 Supreme Court decision, the Justices examined a case where interest rates reached 120 percent, far exceeding IRRA limits.Footnote 12 The ruling held that if a debtor voluntarily paid excessive interest without objection, they could not later reclaim those payments or challenge how the payments were allocated. This decision applied the principle of voluntary payments, emphasizing that a borrower’s acquiescence was central to their ability to seek refunds. The Court also clarified that excessively high interest rates were not automatically deemed void as violations of public policy unless special circumstances—such as exploitation of a borrower’s financial distress—were evident. Similarly, in a 1957 Supreme Court case, the Court reviewed a loan with a 10 percent monthly interest rate (equivalent to 120 percent per annum) and ruled that despite it violated the IRRA,Footnote 13 the interest rate was not deemed to contravene public order and morals, as there was no evidence of exploitation or predatory targeting of a vulnerable borrower. This ruling established that courts assessed high-interest loans not only by the rates charged but also by the transactional context, particularly whether the lender took advantage of the borrower’s vulnerability.

The Expansion of Non bank Lending and the Emergence of Structural Enforcement Gaps

The 1960s marked a pivotal turning point in the evolution of Japan’s non bank credit landscape. Traditional moneylenders and pawnbrokers began adapting to new social and economic demands, giving rise to a modernized, unsecured consumer lending market—popularly known as sarakin finance—by introducing the “salary loan,” a product specifically designed for salaried workers. The following decade saw the rise of four major lenders specializing in salary loans – Promisu, Aiful, Acom, and Takefuji. Their rapid rise underscored the comparative advantage of non bank lenders, who initially relied on their close community ties and local borrower knowledge to mitigate repayment risks and agency costs.Footnote 14 However, as their operations expanded beyond familiar networks, these major lenders shifted toward more impersonal, unsecured lending, extending credit to a broader range of borrowers with limited screening mechanisms. This transformation fueled a surge in demand, encompassing needs ranging from cash flow management for small enterprises to leisure, gambling, and emergency expenses.Footnote 15 By capitalizing on regulatory gaps and operating within the legally ambiguous grey zone, major lenders grew far beyond the modest, community-based role originally envisioned for moneylenders. Their expansion strained the tacit social and political consensus that had justified permissive regulation. Moreover, although the Ministry of Finance (MoF) was formally tasked with oversight, weak enforcement allowed abusive lending practices to proliferate.Footnote 16 While lenders were required to undergo official examinations and obtain authorization to operate, enforcement mechanisms remained weak. Noncompliant lenders faced fines, yet limited regulatory resources resulted in infrequent and insufficient inspections.

This market evolution exemplifies the dynamics of institutional friction, exposing the structural limitations of a framework originally designed for a fragmented, small-scale lending environment. While such arrangements preserved flexibility and discretion, they also blurred accountability and enabled exploitative lending and over-indebtedness to increase. As administrative agencies failed to enforce strict oversight on lenders’ registration, practices, and borrower protections, judicial rulings curtailed exploitative practices and redefined the boundaries of permissible lending.

In 1964, the Supreme Court ruled that loans charging interest above the 20 percent statutory cap were partially void and that any overpayments beyond this limit must be deducted from the principal, preventing lenders from profiting from unlawful interest charges.Footnote 17 In 1968, the Court held that if a borrower voluntarily paid excessive interest and those payments fully repaid the principal, any additional payments could be reclaimed.Footnote 18 This ruling protected borrowers from financial disadvantage due to voluntary overpayments, ensuring that lenders could not retain unlawfully collected funds. In 1969, the Court further ruled that overpayments exceeding both the principal and lawful interest could be reclaimed as unjust enrichment unless the lender could prove otherwise.Footnote 19 This decision reinforced the principle that excess payments should benefit borrowers by reducing their outstanding debt rather than enriching lenders. These rulings marked a shift in the judiciary’s role: from assessing fairness in individual cases to consistently enforcing statutory interest limits. By clearly defining how excess payments should be handled, the courts established legal predictability in credit disputes, ensuring that borrowers were systematically protected from predatory lending practices, even when borrowers had ostensibly consented to waive certain rights (Ono Reference Ono2011). Japanese courts shifted their responses and refined their application of legal norms to ensure statutory protections took precedence over contractual agreements (Pardieck Reference Pardieck2008).Footnote 20

Normative Reframing: Contesting the Absence of Legalistic Regulatory Enforcement

Between 1978 and 1983, rising judicial concern over excessive lending prompted legislative debates on regulating the non bank sector. The bill introduced by LDP Diet member Ōhara Kazumi, became the object of protracted negotiations among the Ministries of Justice (MoJ), Finance (MoF), and International Trade and Industry (MITI), as well as representatives from opposition parties such as the Japan Communist Party (JCP) and the Japan Socialist Party (JSP), alongside the JFBA. Although lawyers secured a presence in the policymaking arena, their ability to shape the regulatory framework remained sharply constrained. Competing definitions of the sarakin mondai and strong resistance from political and industry actors limited the reach of the normative reframing advanced by lawyers and consumer advocates. In response to this first policymaking cycle, lawyers expanded their mobilization into civil society—organizing citizen assemblies and collaborating with local consumer protection groups—to press their reframing of the sarakin mondai onto the legislative agenda.

Normative Contestation Around the Sarakin Mondai

An analysis of the parliamentary committee debates reveals how deeply contested the definition of the sarakin mondai was.Footnote 21 On one side, the JFBA—represented by lawyers and backed by opposition parties—framed the issue around borrower vulnerability and structural exploitation within the unsecured credit market. On the other side, LDP parliamentarians defended the interests of non bank lenders, arguing for a regulatory framework that would preserve their market function and secure the continued viability of the industry. They argued that these lenders filled a critical gap left by formal credit institutions and that Japan’s unique financial landscape required regulations tailored to its specific circumstances rather than broad, restrictive measures.Footnote 22 This permissive stance reflected a broader political and social consensus that viewed non bank lending as a functional necessity within Japan’s financial system.

By contrast, representatives from opposition parties raised two critical concerns: the indecent profits earned by moneylenders through exorbitantly high interest rates; and the pressing need for socioeconomic reforms to establish accessible credit systems with significantly lower interest rates.Footnote 23 While legal professionals and opposition parties pressed for stronger borrower protections and a fundamental restructuring of lending practices, LDP members, financial regulators, and moneylenders’ representatives argued that preserving flexibility in the non bank sector was essential to avoid destabilizing a core component of Japan’s consumer credit market. To maintain the existing consensus, industry advocates actively opposed the normative reframing advanced by lawyers and consumer groups, reaffirming the institutional complementarity between banks and non banks as the appropriate solution to credit gaps. By framing non bank lending as a functional necessity that mitigated—rather than produced—social harm, they sought to neutralize institutional friction and preserve the permissive regulatory settlement. In this context, lawyers and consumer advocates were unable to displace the prevailing consensus, limiting their influence over the policymaking process. In 1983, the government enacted the Money Lending Business Act (MLBA) to regulate the consumer finance sector.Footnote 24 Yet rather than consolidating the borrower protections progressively strengthened through case law, lawmakers prioritized preserving lender flexibility, leaving substantial enforcement gaps (Ōmori 1983). This was most evident in Article 43, the Act’s most contentious provision, which allowed non bank lenders to continue operating within a legal grey zone by legitimizing high-interest lending under narrowly defined conditions—particularly when borrowers made “voluntary” payments, a mechanism known as minashi benzai (Ōmori 1983; Pardieck Reference Pardieck2008).

Although judicial decisions in the 1960s had begun curbing exploitative practices, the legislative process did not integrate these developments; courts were relegated to reactive adjudication of individual disputes rather than given a meaningful role in informing broader regulatory reform. Nevertheless, the policymaking process exhibited a distinctive form of legalistic adaptation: judicial reasoning was in fact selectively incorporated into statutory design. The 1954 and 1957 rulings were central to this dynamic. By reaffirming the principle of voluntary payment, they established that a borrower’s acquiescence determined their eligibility for restitution. They also held that excessive interest rates did not violate public order and morality unless the lender exploited the borrower’s vulnerability. These decisions were ultimately codified in Article 43 of the MLBA, which authorized above-cap interest rates under specific conditions—regulatory approval, absence of coercive practices, and formal borrower consent—reinforced by disclosure obligations in Articles 17 and 18.Footnote 25

The Act thus reaffirmed legislative and bureaucratic primacy in financial regulation, deliberately narrowing judicial authority to case-by-case adjudication while avoiding structural oversight. This outcome contrasts sharply with the dynamic identified by Kelemen (Reference Kelemen2011) in the European Union, where economic liberalization undermined corporatist regulation and was accompanied by juridical re-regulation—replacing informal coordination with transparent, rights-based frameworks enforced through courts and private litigation. In Japan, by contrast, despite the neoliberal reforms under the Nakasone administration (1981–1987), the MLBA policymaking process reflected the government’s intent to preserve informality and opacity in regulatory governance, sustaining consensus-based bargaining among ministries, industry actors, and ruling-party elites. Rather than empowering courts, the MLBA institutionalized ambiguity: Article 43 operated as a strategic compromise that met external pressures for regulation—from the police and judiciary—while simultaneously constraining judicial intervention by embedding the grey zone within statutory law itself. Where Eurolegalism broadened access to judicial enforcement, Japan’s moneylending regulation strategically curtailed it. Article 43 exemplifies this logic: rather than eliminating legal uncertainty, the provision formalized it, specifying the circumstances under which lenders could continue charging above-cap interest rates. Instead of addressing the structural dysfunctions of the consumer credit market, the MLBA codified prevailing practices and narrowed the scope for judicial protection. In the absence of complementary reforms—such as accessible bankruptcy procedures or robust consumer protection laws—the MLBA exposed the deeper governance asymmetries underpinning Japan’s financial regulatory regime.

Political and Normative Obstacles to Judicial Influence

Despite favorable judicial rulings, the case demonstrates that access to policymaking does not automatically confer substantive influence for lawyers or consumer advocates—a finding that echoes Gerald Rosenberg’s argument that courts, while symbolically powerful, have limited capacity to drive progressive reform without coordinated support from the legislative and executive branches (Rosenberg Reference Rosenberg1991). Likewise, Donald Horowitz emphasizes that litigation alone rarely produces durable policy change, as judicial influence is filtered through political alignments, economic interests, and institutional constraints (Horowitz Reference Horowitz1977). Japanese sociolegal scholarship reaches similar conclusions. Tanaka (Reference Tanaka1996) observed that litigation often had a limited direct impact on policymaking through formal judicial decisions—for instance, despite several landmark judicial rulings, the government never codified an enforceable environmental right (Okubo Reference Okubo2023). Awaji (Reference Awaji, Awaij, Teranishi, Yoshimura and Okubo2012) identified clearer instances of judicial influence but stressed that durable regulatory change typically emerged through negotiation and political settlement rather than judicial authority alone. In the case of the MLBA, judicial efforts to strengthen borrower protections were ultimately constrained by a legislative process shaped by political compromise and limited administrative responsiveness. Litigation helped articulate legal problems and expose structural deficiencies, but it remained insufficient in the absence of the other two mechanisms—normative reframing and consensus realignment.

The absence of sustained normative reframing by lawyers and consumer advocates during this period meant that the moral and social meanings of debt, as well as the legitimacy of moneylenders’ economic role, remained largely intact. This reflects not only limited mobilizing capacity but also the profound power asymmetry between consumer groups and the well-organized moneylender associations shaping legislative outcomes.Footnote 26 Borrowers were socially stigmatized and politically fragmented, making collective mobilization difficult and reducing their ability to exert pressure on lawmakers. By contrast, the moneylenders’ sector exercised substantial political influence through powerful associations such as the Moneylenders Association and the Consumer Finance Association. These organizations provided institutionalized representation, enabling lenders to consolidate interests, lobby effectively, and preserve the grey zone that sustained their profitability. Their influence was further reinforced through campaign contributions and close ties with key members of the ruling LDP.Footnote 27 This imbalance was compounded by prevailing societal norms that framed indebtedness through a discourse of individual responsibility rather than structural injustice. LDP legislators drew on this cultural repertoire to legitimate the continued role of moneylenders within Japan’s financial system, portraying their activities as socially necessary rather than exploitative. Judicial reasoning that aligned with these political and economic interests was selectively incorporated into regulatory design, further limiting the prospects for borrower-oriented reform.

At the same time, intra-party conflicts within the LDP revealed deeper tensions over financial regulation. While some conservative factions sought to maintain industry-friendly policies that favored non bank lenders, others pushed for stronger consumer protections and financial sector reform. However, in the absence of a broader normative reframing or a shift in social consensus, these reformist impulses remained only partially realized. Nevertheless, it is important to note that this consensus was not unanimous, as evidenced by the resignation of Koizumi Junichirō—then a member of the Diet and designated rapporteur for the 96th session—Committee on Financial Affairs—who publicly expressed opposition to the proposed legislation.Footnote 28 His opposition foreshadowed his later role as a reformist Prime Minister (2001–2006), during which he actively challenged the LDP’s traditional patronage networks and pursued financial deregulation along with anti pork barrel policies (Tiberghien Reference Tiberghien2006). This underscores how conflicts within political elites can create openings for policy change, a dynamic that aligns with Sidney Tarrow’s (Reference Tarrow1994) argument that divisions among ruling elites incentivize resource-poor groups to engage in collective action.

Legal Mobilization and the Construction of a Normative Reframing

The diffuse and fragmented nature of borrower interests made collective representation difficult. In this context, a few committed legal professionals emerged as key advocates in a policy landscape dominated by non bank lenders. Beginning in the 1970s, a small but increasingly influential group of lawyers played a central role in organizing the anti sarakin movement, transforming isolated cases of high-interest lending into a broader legal and social issue (Otsuka Reference Otsuka2009; Oyama Reference Oyama2020). The movement took shape in 1978 in Osaka under the leadership of Kimura Tatsuya, who founded the National Association of Sarakin Victims,Footnote 29 and soon expanded to Tokyo, where Utsunomiya Kenji led efforts to mobilize legal professionals and advocate for consumer credit reform (Utsunomiya Reference Utsunomiya2007). In reaction to the MLBA enactment, this group of lawyers developed a sustainable advocacy model by pooling resources and coordinating litigation strategies. These efforts were reinforced by alliances with consumer rights advocates and labor unions, many of whom were also engaged in other cause-oriented legal networks, such as the Karōshi Bengodan (the network of lawyers involved in the mobilization against overwork-related deaths and suicides).Footnote 30 This interconnected legal activism facilitated the exchange of strategies across different fields of mobilization. For example, lawyers established free legal clinics and hotlines (110 ban) to provide direct legal assistance to borrowers facing exploitative lending practices, a strategy widely employed by Japanese lawyers in various social and environmental cases (Sala Reference Sala, Cummings, Hammerslev, Butter and Anzola2025a).

As demand for legal support grew, these clinics addressed specific concerns—such as illicit lending practices and lender violence,Footnote 31 debt repayment,Footnote 32 contract transparency,Footnote 33 illegal lenders (yamikin),Footnote 34 and personal data protectionFootnote 35—as well as broader social problems associated with unsecured borrowing, including gambling addiction and alcoholism.Footnote 36 Beyond their immediate legal function, these clinics also served as key sites of knowledge production. By documenting borrowers’ experiences and collecting empirical data on lending practices, lawyers generated a systematic understanding of the structural mechanisms driving indebtedness. In this sense, they provided information subsidies—credible, experience-based evidence that informed policymakers, journalists, and social workers, strengthening the broader advocacy infrastructure surrounding consumer credit reform (Arrington Reference Arrington2025).

During the 1990s, these committed lawyers broadened their advocacy efforts by organizing symposiums to mobilize key civil society actors, including counseling centers, consumer associations, and citizen advocacy groups. These initiatives enhanced their visibility in the public sphere and strengthened their influence in policy debates.Footnote 37 In parallel, they strategically leveraged media scandals to raise public awareness of predatory lending practices (Sala Reference Sala2017). Whenever a lending scandal surfaced, they issued strong condemnations, frequently using evocative terms such as sarakin jigoku (“the sarakin hell”) and drawing comparisons to American loan sharks. Drawing on litigation experience, these lawyers advanced and popularized the term tajūsaimu (“excessive/multiple indebtedness”) to describe the pattern of borrowers stacking high-interest loans from multiple lenders. The concept did two things: it highlighted debt’s self-reinforcing spiral—new loans taken to service old ones—and it reframed borrowers as targets of systemic lending practices rather than merely irresponsible actors (Suda Reference Suda2006; Utsunomiya Reference Utsunomiya2007). In so doing, it directly contested the institutionalization of individual responsibility embedded in Article 43’s voluntary-payment provision and cut against long-standing narratives that treated indebtedness as personal mismanagement.

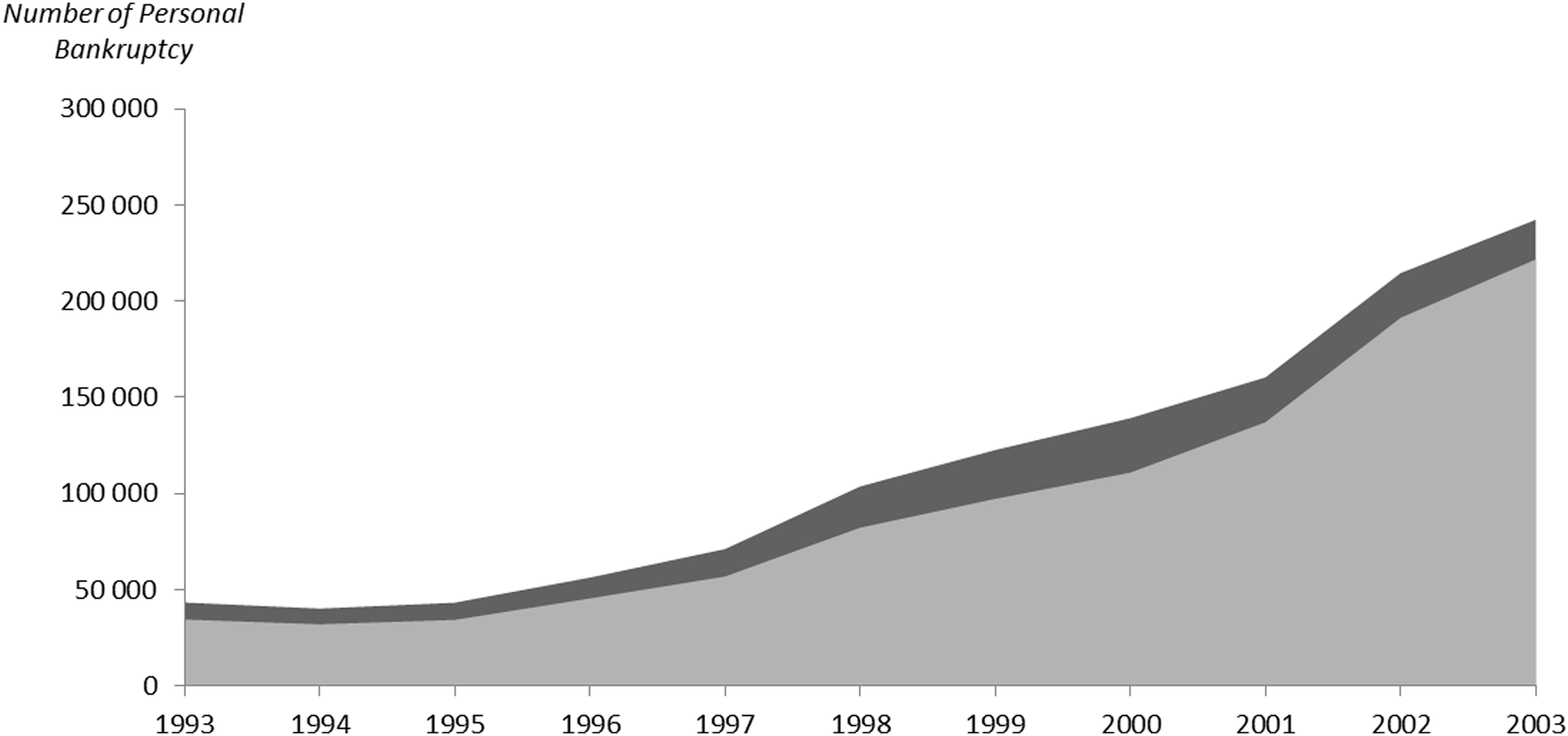

By the 2000s, prolonged economic stagnation and growing concerns over social inequality had transformed consumer credit reform into a salient political issue.Footnote 38 Through the JFBA, anti sarakin lawyers began publishing annual statistical reports on household debt, focusing in particular on the socioeconomic profiles of individuals filing for bankruptcy (JFBA 2009). The production of these statistics was facilitated by reforms to the Bankruptcy Law,Footnote 39 which sought to simplify procedures in response to the economic and financial crises of the late 1990s. Moreover, the Civil Rehabilitation Law—originally designed for small and medium-sized enterprises—was also extended to individuals, aiming to establish a simpler and more accessible procedure.Footnote 40 These legal reforms also relaxed restrictions on legal advertising, enabling lawyers to more actively promote their services and assist debtors.Footnote 41 These changes contributed to a sharp rise in legal actions, particularly those related to debt rescheduling. As a result, personal bankruptcy filings surged from 122,241 in 1999 to over 240,000 in 2003, reflecting both the growing debt burden and the enhanced responsiveness of the legal community.Footnote 42 According to Supreme Court data, nearly all personal bankruptcy filings between 1998 and 2004 resulted from unsustainable debt linked to the accumulation of high-interest loans from unsecured lending institutions (see Figure 2).

Number of personal bankruptcies caused by over-borrowing in the unsecured personal loan sector out of the total number of personal bankruptcy declarations

Source: Compilation of data based on the Supreme Court of Japan, Annual Report of Judicial Statistics (saikō saibanjo shihō tōkei nenpō).

Beyond high-interest lending, another key driver of personal bankruptcy during this period was the burden of guarantee obligations, which placed significant financial strain on third parties. Unlike systems that assess credit risk based on a borrower’s repayment capacity, Japan’s reliance on joint liability shifted financial risk onto guarantors. Many guarantors, unaware of the full extent of their obligations, found themselves unexpectedly burdened with unmanageable debt when primary borrowers defaulted. This extended cycles of indebtedness to individuals who had never directly borrowed, drawing them into bankruptcy proceedings. Lawyers from the anti sarakin mobilization also used data from the MHLW on suicide to highlight the correlation between over-indebtedness and rising suicide rates (West Reference West2005; Pardieck Reference Pardieck2008). By integrating statistical analysis, survey data, and litigation records, they quantified the scale of sarakin-related social issues and strengthened collective legal mobilization (Sala Reference Sala2017). Lawyers mobilized civil society—convening citizen assemblies and partnering with local consumer protection groups—to bring the issue onto the reform agenda. Ultimately, the government’s response unfolded through a series of legal and regulatory reforms aimed at formalizing the unsecured credit market and curbing illicit lending practices.

The first major step came in 2003 with revisions to the MLBA, which introduced criminal penalties for unlicensed lenders. This was followed by the 2004 Measures Against Predatory Lending Act, which strengthened oversight of lending activities and targeted criminal networks operating within the industry.Footnote 43 The new law mandated stricter verification of lenders’ identities and capital sources, alongside tighter licensing and registration requirements. These reforms contributed to an expansion of the “legal stock”—the cumulative growth of statutes, penalties, and procedural detail that signals a shift toward a more legalistic regulatory style (Arrington Reference Arrington2025, 34–35). Judicial decisions also became part of this expanding legal stock: successive rulings clarified statutory ambiguities, reinforced borrower protections, and imposed tighter compliance obligations on lenders.

Consensus Realignment: Judicial Decisions, Social Consensus, and Political Opportunity in Japan’s Legalistic Regulatory Style

As courts increasingly ruled in favor of borrowers, judicial decisions played a central role in consolidating consensus realignment by translating emerging social expectations into adjusted legal norms. These rulings created new legal opportunities for advocacy, generating a feedback loop between litigation and regulatory reform. Successful lawsuits secured compensation for borrowers and allowed lawyers to reinvest portions of recovered fees into further mobilization. Through this cumulative process, lawyers transformed fragmented borrower grievances into a sustained campaign for institutional and social reform.

The Transformative Impact of Judicial Rulings

Beginning in early 2004, the Supreme Court reversed a series of lower-court rulings that had favored lenders. It held that even minor deviations from statutory documentation requirements defeated reliance on Article 43.Footnote 44 In a series of landmark decisions, the Court further clarified that any omission or inaccuracy—such as missing collateral information or delayed receipts—negated the presumption of “voluntary payment.” In a particularly significant case on revolving credit, a form of lending not contemplated by the original MLBA, the Court required lenders to specify minimum repayment amounts and terms even under flexible schedules, ensuring borrowers had sufficient information to make informed choices.Footnote 45 These decisions exemplify the judiciary’s compensatory role in Japan’s governance structure—acting to fill enforcement gaps left by administrative agencies. By imposing stricter interpretive standards, the Supreme Court curtailed lenders’ ability to exploit regulatory ambiguity and reinforced the principle that compliance with procedural requirements is a precondition for legitimate profit.

The judiciary’s restrictive interpretation of Article 43 culminated in the six landmark Supreme Court decisions of early 2006 (Pardieck Reference Pardieck2008; Kozuka Reference Kozuka2009; Kozuka and Nottage Reference Kozuka and Nottage2009a). Building on the 1954 and 1957 rulings, the Court underscored that borrower consent obtained under exploitative conditions could not legitimize unlawful lending practices. The Court also institutionalized the kabarai procedure, enabling borrowers to reclaim excess interest paid above the 20 percent ceiling set by the IRRA. Through these rulings, judges dismantled the previously tolerated grey zone and reshaped the contours of financial regulation (Ono Reference Ono2011).

Industry actors and several policymakers reacted sharply, depicting judicial intervention as excessive and destabilizing to established market practices (Kozuka and Nottage Reference Kozuka and Nottage2009a; Ramseyer Reference Ramseyer, Wulf, Schmidt and Schwartze2014). The series of decisions—particularly the kabarai jurisprudence—has often been interpreted as an instance of judicial activism (Pardieck Reference Pardieck2008; Kozuka Reference Kozuka2009; Colombo and Shimizu 2016). This paper, however, argues that these rulings were part of a broader, long-term process of judicialization that is best understood through the interaction of the three mechanisms developed in this study, rather than by isolating the decisions themselves or portraying the courts as overreaching policymakers. These rulings strengthened the normative reframing advanced by lawyers and consumer advocates, shifting public perceptions and bolstering political momentum. They signaled the erosion of the social consensus underpinning Article 43 and affirmed the advocates’ long-standing claim that over-indebtedness stemmed not from individual irresponsibility but from inadequate regulation of the non bank lending market.

Figure 3 illustrates the evolution of court rulings over time. It includes only decisions that assigned responsibility to both lenders and borrowers, in order to highlight the impact of normative reframing on judicial reasoning.

Annual Judiciary Decision Highlighting Lender versus Borrower Responsibilities

Source: Author’s compilation based on decisions retrieved from the Japanese Courts Case Search System.

The anti sarakin mobilization can be read as a collective effort to reconstruct the moral premises that would legitimize judicial adaptation. Lawyers first deconstructed the notion of individual responsibility by showing its social determinants and the structural asymmetry between lenders and borrowers. Then, through free counseling, coordinated test cases, and public advocacy, they shaped awareness of the externalities produced by weak regulation and forged a baseline consensus for redress. When courts ultimately curtailed excessive interest rates, their opinions plausibly present themselves as neutral—grounded in legal reasoning rather than activism. In this sense, the movement illustrates Judith Shklar’s insight: judicial capacity for reform depends on prior shifts in social consensus, through which legalism absorbs and legitimizes social transformation.

The impact of legal mobilization extended beyond the judiciary, triggering broader inter-branch shifts in financial regulation (Barnes and Burke Reference Barnes and Burke2020). Following the 2006 Supreme Court’s rulings, the surge in interest refund claims significantly weakened Consumer Finance Companies’ position in both the lower courts and their lobbying efforts. This shift in judicial interpretation effectively constrained the Diet from raising interest rate caps, thereby limiting legislative flexibility on consumer credit policy. At the same time, administrative agencies—historically seen as “passive enforcers of Diet legislation”—adopted a more proactive stance (Pardieck Reference Pardieck2008). After the Supreme Court’s de facto rejection of grey-zone interest rates, the Financial Services Agency (FSA) promptly announced plans to abolish grey-zone lending altogether.Footnote 46 This development illustrates how judicial decisions not only redefined the legal boundaries of lending practices but also compelled legislative and administrative actors to adjust their policies accordingly—exemplifying the legalistic turn this paper seeks to elucidate.

The dynamic interplay between the judiciary, legislature, and administrative agencies contrasted sharply with the enactment of the first MLBA. In the 1980s, despite court rulings invalidating exploitative lending practices, legislative and administrative bodies largely resisted incorporating judicial interpretations into policy. Instead, they formalized the grey zone through Article 43, preserving lenders’ ability to charge excess interest. By contrast, in the 2000s, sustained judicial intervention intensified regulatory scrutiny, making it more difficult for policymakers to circumvent judicial precedents. The judiciary thus shifted from a peripheral role to one that reshaped financial governance through its interpretive and enforcement effects. Politically, the Koizumi administration (2001–2005) capitalized on this altered opportunity structure to reconfigure Japan’s consumer finance regime.

Consensus Realignment and the MLBA Reform

Unlike the 1980s, when lawyers’ advocacy efforts were sidelined by a closed policy process dominated by lenders’ interests, the 2005–2006 reform process unfolded in a more transparent and participatory environment (Cichowski and Stone Reference Cichowski, Stone Sweet, Bruce, Dalton and Susan2003). The Koizumi administration’s decision to convene a working group provided a key institutional opening for consumer advocates, lawyers, the FSA, and reformist policymakers to push for stricter lending regulations.Footnote 47 This shift also enabled lawyers to act as insider activists within policymaking circles (Arrington Reference Arrington2021).Footnote 48

The influence of judicial rulings on the policymaking process became most visible when conflicts of interest emerged within the consensus-driven coalition of bureaucrats from key ministries, LDP policymakers, and industry representatives. During the 2005–2006 reform cycle, the Koizumi-led reformist factions sought to restructure the consumer credit market by strengthening regulatory oversight and abolishing the grey zone. This initiative, however, encountered strong resistance from conservative LDP factions closely aligned with moneylenders and consumer finance companies, who aimed to preserve the grey zone and maintain regulatory flexibility for the industry.Footnote 49 By participating directly in working-group deliberations, lawyers strategically positioned themselves to scrutinize both the non bank sector and the broader financial system.Footnote 50 Their normative reframing—grounded in empirical data and borrower testimonies—effectively challenged industry narratives and exposed the socio-economic consequences of abusive lending practices. They argued that, far from promoting financial inclusion, these practices systematically trapped borrowers in cycles of debt and exacerbated the vulnerability of already at-risk individuals. For example, data published by JFBA and presented during the working group discussions revealed the scale of the problem: approximately 14 million people had borrowed from consumer finance companies and non bank moneylenders, with 2.3 million indebted to more than five different lenders. The figures also reported 184,000 personal bankruptcies and 7,800 suicides linked to financial distress. Moreover, out of the 14,000 lenders registered with central or local authorities in 2005, only 2,079 were recorded in a credit bureau, meaning that many lenders—and the borrowers they serve—operated outside formal financial oversight.Footnote 51 By juxtaposing these figures with rising unemployment and declining incomes, lawyers sought to demonstrate how wider economic and social conditions were fueling over-indebtedness.

A comparison between the first period—culminating in the enactment of the MLBA in 1983—and the 2005–2006 reform debates reveals striking similarities in the arguments advanced by lawyers. However, the policymaking processes differed sharply: whereas the 1980s period reflected an informal, consensus-based mode of governance, the later reforms embodied a distinctly legalistic regulatory style, characterized by formal rulemaking, greater transparency, and participatory deliberation (Arrington Reference Arrington2025). The ensuing policy debates reflected an attempt by lenders and their allies to restore the previous consensus that had legitimized the grey zone. Credit companies sought to reassert the narrative that non bank lenders fulfilled a socially valuable role by extending credit to groups excluded from the formal banking sector.Footnote 52 They argued that these institutions were essential to Japan’s financial ecosystem, meeting the credit needs of small businesses, farmers, and low-income households. Framing the issue as one of market efficiency rather than consumer protection, lenders contended that excessive regulation would distort credit allocation and advocated an Anglo-Saxon-style credit regime prioritizing deregulation and financial literacy over legal constraint.

More broadly, Japan’s consumer credit market stood at a pivotal moment, shaped by both domestic regulatory shifts and evolving international influences. In 2005, the booming US subprime market and the growing presence of major foreign lenders—most notably GE Consumer Finance—underscored the stakes. Backed by the American Chamber of Commerce in Japan, GE Consumer Finance advocated for deregulation and interest rate liberalization, but only if paired with enhanced consumer education and stricter controls on illicit lenders. This landscape gave rise to a power struggle between two competing pressure groups. On one side, major lenders—including GE—pushed for further deregulation, emphasizing the need to maintain broad credit availability. On the other hand, specialized credit companies and certain business lenders called for structural reform, demanding greater transparency, the elimination of the grey zone, and lower interest rates to stabilize the market. Koizumi’s evolving stance on consumer credit regulation was particularly significantFootnote 53: By the 2000s, he became a leading advocate for formalizing the credit market.Footnote 54 The banking sector’s proximity to Koizumi also suggests an indirect but notable influence on the reform process. This dynamic aligns with Kent Calder’s (1988) argument that civil society actors in Japan can exert influence over policymaking when divisions emerge among bureaucrats, the LDP, and dominant industrial actors. When the traditional collusion of interests among these groups weakens, space opens for civil society intervention—particularly when legal advocates align with reformist LDP factions and bureaucratic interests against industry resistance. Patricia Maclachlan’s study on consumer rights similarly demonstrates how social mobilization can capitalize on political and institutional shifts to drive policy reform (Maclachlan Reference Maclachlan2002). Ultimately, the government introduced stricter regulations on the consumer finance market to curb exploitative lending practices and strengthen borrower protections. Key measures included: interest rate caps to prevent predatory lending; credit volume controls to mitigate borrower over-indebtedness; a centralized credit information system to enhance transparency and prevent reckless lending; strengthened oversight of personal bankruptcy procedures to support debtors and prevent financial collapse (Pardieck Reference Pardieck2008). These regulatory changes, backed by sustained litigation and court rulings, fundamentally reshaped Japan’s consumer lending landscape (Trumbull and Kanno Reference Trumbull and Kanno2009). Consumer Finance Companies, facing mounting legal liabilities and mandatory repayments to borrowers, experienced severe financial strain. Judicial proceedings forced several major lending companies into bankruptcy, while others were absorbed by Japanese mega-banks as part of broader financial sector restructuring (Kozuka Reference Kozuka, Backert, Block-Lieb and Niemi2010). Thus, this case illustrates how judicial rulings, when combined with legal mobilization and shifting political alignments, can act as catalysts for policy change.

Conclusion

This study demonstrates that judicial action in Japan evolved from a marginal channel for individual redress into a central mechanism of institutional coordination activated and shaped by lawyers’ strategic intervention. While reaffirming long-standing features of Japanese governance—bureaucratic discretion, informal consensus-building, and industry dominance—it reveals the limits of soft-law mechanisms that rely on administrative guidance rather than enforceable rules to stabilize the relationship between formal and informal practices when these practices produce social harm. Under conditions of institutional friction, particularly where statutory ambiguities created regulatory gaps, lawyers mobilized litigation as an instrument for exposing structural deficiencies, prompting courts to assume a corrective role that reshaped enforcement practices and triggered broader institutional adjustment. Litigation thus shifted from a narrow mode of dispute resolution to a catalyst for reform, not through judicial initiative alone, but through the coordinated efforts of lawyers and advocates who reframed grievances, aggregated information, and supplied courts with the normative and evidentiary resources necessary for intervention (González-Ocantos Reference González-Ocantos2016; Arrington Reference Arrington2025). Rather than treating policymaking as the exclusive domain of state actors, this study shows that courts constitute a site of institutional coordination precisely because lawyers and advocates use judicial forums to extend contestation into otherwise closed political arenas (Cichowski and Stone Reference Cichowski, Stone Sweet, Bruce, Dalton and Susan2003; Cichowski Reference Cichowski2006; Awaji Reference Awaji, Awaij, Teranishi, Yoshimura and Okubo2012; Hirschl Reference Hirschl and Robert2011; Barnes and Burke Reference Barnes and Burke2015).

The paper advances the concept of processual legalism to explain how judicialization unfolds through the iterative interaction of three mechanisms: institutional friction, normative reframing, and consensus realignment. Institutional friction exposes the limits of informal governance; normative reframing transforms individual grievances into structural critique through lawyers’ interpretive and advocacy work; and consensus realignment describes how judicially articulated norms are selectively taken up by bureaucrats and ruling-party policymakers, lowering the political costs of reform and converting litigation-driven critiques into bounded regulatory adjustments that remain compatible with existing governing coalitions. Together, these mechanisms illuminate legalism as a contingent process rather than a fixed mode of governance. While legalism is episodic in its activation, the institutional changes it generates are incremental and consensus-dependent, revealing important varieties of legalismFootnote 55 (Hall and Soskice Reference Hall and Soskice2001; Arrington Reference Arrington2025).