Introduction

Shortly after the launch of live cattle futures trading in 1964, Stanley Waldner asked “a well-to-do, weather-beaten old cattleman,” “Aren’t you interested in becoming a ‘futures cattleman’?” Waldner was a Kansas-based cattle feeder and self-appointed booster for the new futures market. The elder producer “smiled, slowly shook his head and said, ‘Not me, Sonny, I just can’t eat those paper steaks’.”Footnote 1 Waldner’s readers would have recognized the humorous anachronism in the cattleman’s reference to nineteenth-century populist arguments against “paper” commodities, but his quip was also timely. Cattle on the Southern plains had been abstracted into marketable commodities within a complex, continental supply chain for at least a century, but on the eve of November 30, 1964, they were still, nonetheless, living animals that would mostly be killed and eaten by people for nourishment. Live cattle futures represented a new way to capitalize cattle that did not exist in the physical world of grass-to-hamburgers. Waldner was among a select few cattle producers in leadership roles who collaborated with economists and speculative exchange leaders to bring a new market form into existence and to ensure its early success. Waldner proudly claimed the distinction of making the first-ever sale of a “non-storable” derivative, a financial instrument that would fuel the most valuable sector of the global capitalist economy just a few decades later.

Cattle futures reinvigorated the Chicago Mercantile Exchange (CME) and the derivatives industry in general. Futures and other derivatives are financial instruments that originated in agriculture and derive value from other material commodities. Until 1964, derivatives markets had only succeeded for commodities that were mostly uniform, available in storage, and easy to transport, and experts believed this was necessary to ensure the financial market did not become unhinged from the material and social reality of farmers’ fields. According to economists, live cattle were “non-storable”—a conceptual synecdoche meaning not fungible (homogeneous), storable, or deliverable in the traditional sense—and there was a widely-held estimation that cattle futures were “doomed to fail.”Footnote 2 Instead, cattle futures were the biggest success the CME had since its formation, and economists and the CME both interpreted the success of agricultural nonstorables to mean there were no material limits on what kinds of commodities could trade on derivatives markets. This idea would transform global finance and make the CME the largest derivatives exchange in the world. Results were more mixed for cattle producers, who had not seen an issue with the nonstorability of cattle in the first place.

My central argument is that derivatives exchange leaders, agricultural economists, and cattle producers collaborated to create a new, more abstract type of financial market in 1964. The apparatus for their collaboration, and the measure of the market’s abstraction, came from hedging models and related economic theory. This claim makes three interrelated interventions in our understanding of the history of financial innovation and growth. First, it shifts the periodization of financial turning points because live cattle futures launched eight years before the widely accepted revolution in abstract financial derivatives and over seventy years after agricultural derivatives stopped being revolutionary. Second, it demonstrates the leading role of underappreciated people, especially agricultural economists and agricultural producers, in financial transformation. Even derivatives industry leaders receive less credit than they deserve, since most scholarship on the causes of late-twentieth-century financial growth and innovation emphasizes factors exogenous to the financial sector, including structural and institutional changes in global manufacturing, trade, and monetary policy.Footnote 3 Third, it challenges the assumption that the changing relationship between derivatives and the physical economy was caused by the industry’s expansion beyond agriculture. Cattle futures demonstrate that abstract innovation began not against, but within, the context of agricultural derivatives, which enabled future developments. Live cattle futures predated broader shifts in the economy and, thus, reveal the internal, human work of financial revolutions.

Scholars and industry insiders recognize two revolutionary periods in the history of US derivatives, neither of which line up with cattle futures. Historians have demonstrated that agricultural derivatives challenged and transformed broader conceptions of markets and the “very reality of the economy itself,” when they first exploded in the later nineteenth century.Footnote 4 However, the structures of modern derivatives stabilized with narrow victories in legal and political challenges, such as proposed congressional bills to ban futures in 1892. Social scientists have identified another, even more sudden, turning point leading to the abandonment of any lingering corporeality underlying derivatives in the late twentieth century. Following industry insiders, these scholars describe the transformation as a turn away from agriculture, and, thus, date the “new era” to May 16, 1972, the termination date of the Bretton Woods agreement linking currencies to gold.Footnote 5 In other words, between about 1892 and 1972, nothing new or consequential happened in derivatives. This periodization is consistent with the broader emphasis on external forces of change, but it neglects to explain how derivatives traders, stuck in a world of nineteenth-century commodities, could respond immediately to structural changes in 1972 with new financial instruments that were more abstract than anything existing before.

Cattle futures help explain why the derivatives industry was prepared for 1972. Take CME chairman Leo Melamed’s reminiscence, for example: “Finally, I came to the thought that Bretton Woods, the fixed-exchange-rate system, was coming apart, and when it finally comes apart, wouldn’t there be a need for foreign-exchange futures?”Footnote 6 “Our board thought I was crazy,” Melamed recalled, “and very frankly I thought it was a little crazy too, because why hadn’t anybody else done this?”Footnote 7 In reality, Melamed was not alone. Within months of the termination of Bretton Woods, the United States Department of Agriculture (USDA) received requests from “several other” exchanges for permission to trade abstract financial things, including some that had no linkage to the changes in currency rates.Footnote 8 Elsewhere, Melamed revealed that he had been enquiring into futures with no legal delivery mechanism as early as 1969.Footnote 9 Melamed’s role in launching the first financial derivatives earned him some self-congratulation, but a singular moment of genius is not a sufficient historical explanation. Why would Melamed’s board approve something then unbelievable, and why were several other exchange leaders also ready and waiting? A precursor to the 1972 revolution happened within agricultural derivatives eight years before the termination of Bretton Woods, and it was far more surprising to the people involved than financial futures would later be. Live cattle futures were “crazy” first. In fact, they were crazier.

What does it mean to describe derivatives as abstract? Critical scholarship on contemporary derivatives has emphasized their “strangely imaginary” or “virtual” properties.Footnote 10 As Jacob Arnoldi put it, derivatives are “assets based on nothing, values created out of thin air.”Footnote 11 Yuval Millo called post-1972 derivatives “strange assets” because they lacked “straightforward physical characteristics, and therefore cannot be delivered.”Footnote 12 Of course, these scholars did not mean that derivatives ever did, or could, become truly immaterial. As Donald MacKenzie explained, “The materiality of financial markets involves physical objects, technological systems and human bodies, but also the legal systems, cultures, procedures, beliefs and social relations that objects and bodies express, make possible, are shaped by and are enmeshed in,” which is to say, everything.Footnote 13 Arnoldi clarified that derivatives were “virtual” because they existed “in [social] practice” but “but not in [physical] reality in the strict sense.”Footnote 14 Scholars often frame these innovations as a response to the particular challenges of foreign exchange risk after Bretton Woods relinquished its hold on currency rates, but the literature is less clear about what existed in derivatives beforehand that was apparently less abstract. Though critical scholars rarely use the terminology, their definitions reveal that all these “strange” and lucrative contracts were what derivatives traders and agricultural economists used to call “non-storables.”

This article aims to explain more precisely what it means for derivatives markets to be more or less abstract and how that changes over time. This objective is challenging because abstraction is synonymous with imprecision. Leigh Claire La Berge estimated that “‘abstraction’ is perhaps the most commonly employed category used to describe finance,” but she warned that it is most often a trope that obfuscates more than it illuminates about finance in practice.Footnote 15 Nevertheless, abstraction is a good word for the changes in derivatives because it captures both a distance from physical things and human feelings about that distance. Melamed’s financial derivatives had no meaningful requirement that traders hold any stake in a parallel physical market, and he thought that was “crazy.” In truth, there is nothing inherently abstract about finance or derivatives that distinguishes them from the rest of the capitalist political economy. Rather, the abstraction of finance is a practiced reality that changes over time. We can only quantify abstraction relatively, since, as La Berge pointed out, “abstraction, by its very nature, is not [precisely] quantifiable; if it were, it would hardly be abstract.”Footnote 16 Cattle futures make clear, though, that the trajectory of relative abstraction shifted with a specific event. I argue that agricultural derivatives became steadily less abstract in both practice and perception between 1892 and 1964. Experts from industry and academia believed in essential material limits on derivatives, and they constructed market technologies to match that belief. Speculative trading in living animals broke down prevailing assumptions that derivatives markets only worked for specific kinds of grain-like commodities. By 1972, Melamed could call financial futures “crazy,” but he harbored no sincere doubts that they would work.

My case study of cattle futures builds on the critical literature on internal mechanisms of financial innovation, in particular, who drives market creation and how they do it. Social studies of finance have documented a close working relationship between professional economists and derivatives industry leaders to put new theories and models into practice, making derivatives among the strongest case examples of “market performativity.” Drawing from John Austin’s theory of speech acts and Judith Butler’s work on the performativity of gender, economic sociologists have argued that privileged actors, especially economists, and their calculative technologies, such as theoretical models, influence, change, and even produce the markets they seek to describe.Footnote 17 As Alice Bamford and Mackenzie asserted, “a model can do things.”Footnote 18 Though “markets seldom if ever behave exactly as posited by even the most sophisticated model,” models act like “scripts” through which ideas and beliefs about markets “mould the world in their image.”Footnote 19 Models are simplifications of reality with the power to simplify reality. Models provide the concrete rules governing financial abstractions, but they also frequently misfire or fail to perform.Footnote 20 In some cases, models may even alter markets to look less like themselves, a phenomenon Bamford and MacKenzie call “counterperformativity.” Some scholars treat performativity as a “general theory of the social world,” but the most useful approaches regard performativity “as a historical trend” that waxes and wanes alongside other institutional changes.Footnote 21 The theoretical work in market performativity can be prohibitively specific at times, but it is a helpful theoretical and empirical response to the apparent abstraction and complexity of contemporary finance. The case studies in the field provide the richest historical documentation of new derivatives markets after 1972, and performativity scholars provide convincing evidence that derivatives traders worked closely with economists and their models to construct the revolution in abstract financial instruments of the later twentieth century.

I draw on the performativity approach but apply it to a different period, different people, and different models. The most significant mistake and limitation in the performativity literature is its consensus that “the academic discipline of economics had little effect on derivatives trading before 1970.”Footnote 22 We know that financial economists, like Milton Friedman and Merton Miller, had a tremendous impact on the derivatives industry in the 1970s and 1980s, but the close association of economists and exchange leaders was nothing new. Less-known agricultural economists have been essential to the social permissibility and everyday operation of derivatives markets since the 1890s. Furthermore, professional economists’ relationships with agricultural producers were just as important as those with derivatives leaders in animating new ideas. For the occasion of cattle futures, professional economists, exchange members, and cattle producers assembled to share models and discuss how they would create and use a new market. Those models differed from the “mathematical models of finance” emphasized by most performativity scholars because they could not always be queried against real pricing data.Footnote 23 Hedging models before 1964 included both mathematical models, with specific variables and equations, and also conceptual models, which made sense of the broader set of mathematical versions for potential model users. Most hedging models provided a general framework for practice that each user had to adapt or refine based on the realities of their business. Conceptual models guided calculation, but we cannot test the impact of those calculations on the market directly. Attention to conceptual models opens greater space to narrative and qualitative ideas about calculation as elements of performativity.Footnote 24 It is especially in the Austinian and Butlerian sense of speech-acts and scripts that live cattle futures were performative or counterperformative.

Before 1964, hedging models matched the classic description of a performative model that “escapes the lecture theatres and pages of academic journals into the wild,” where it “starts being used by financial practitioners” to make the real market resemble the modeled version. As hedging models developed and proliferated, and more agricultural producers used the models, some qualitative observations suggested hedging grew more effective. More importantly, hedging conceptually modeled a socially permissible type of exchange, and derivatives, in practice, increasingly resembled the model in terms of who was participating and what they were trying to do. Hedging models, especially the mathematical versions, also included assumptions about what types of commodities could be hedged, and the broader belief in material limits on derivatives trading constrained innovation to match those assumptions. After 1964, hedging models became counterperformative, which refers to “a very particular form of misfire, of unsuccessful framing, when the use of a mathematical model does not simply fail to produce a reality […] that is consistent with the model, but actively undermines the postulates of the model.”Footnote 25 Cattle futures tested the assumption that derivatives markets could only function for commodities with specific material characteristics, and the assumption failed. Economists and derivatives insiders interpreted that result to mean there were no material limits on what could trade on derivatives, and they spent the next three decades creating an industry that exactly contradicted the original assumption. Materiality was not just wrong; people worked to make it profoundly wrong. Another form of counterperformativity occurs when a model “is ‘gamed’ by financial practitioners taking self-interested actions that are informed by the model but again have the effect of undermining it.”Footnote 26 Cattle producers carefully considered hedging models, and it seems the most enthusiastic contingent among them decided to do the exact opposite of what the models instructed, a practice that became known as the “Texas hedge.” We cannot say whether or not Texas hedging was directly responsible for the nonconformity of live cattle futures to hedging models, but it was clear that Texas hedging undermined model hedging as the dominant social purpose of derivatives markets and the dominant role of commodity owners in them. This was how people performed and counterperformed a financial revolution in abstraction.

Historical sources pertaining to live cattle futures provide a rare opportunity to scrutinize the creation of a new market from multiple perspectives. Derivatives markets are physical things, but they mostly operate anonymously and save a limited amount of data about their transactions. Empirical research on twentieth-century derivatives has, thus, relied heavily on interviews, and this study adds an expanded set of primary sources to the historical approach.Footnote 27 Archival records from the derivatives and cattle industries, including correspondence and clipping files, showed close engagement with economists and their publications.Footnote 28 Proceedings from exchange-hosted conferences and seminars recorded the literal conversations between different people about economic ideas. Newspaper articles, organization surveys, and Congressional hearings solicited expert opinions on what would happen, and later what had happened, with cattle futures. For the twenty-fifth anniversary of cattle futures, CME archivist Joan Daley conducted three oral history interviews about the design and launch of the contract. Finally, Waldner’s reporting for a producers’ trade magazine left a remarkably detailed insider narrative of the first year of the market. We can see how conceptual models scripted behavior before and after cattle futures because we can hear economists and market users talking to each other about it.

This article has three parts. The first section looks at the development of derivatives exchanges and derivatives contracts, as well as the development of ideas about them, from the 1890s to the 1960s. Over this period, derivatives trading became increasingly narrow in both practice and imagination, such that by the end of the period, academic and industry experts alike ascribed firm material limits on the types of things that could trade within speculative commodity markets. The second section examines the activism of exchange leaders, economists, and cattle producers, who treated live cattle futures as a test of those limits. It also analyzes the immediate impacts of cattle futures’ success for the derivatives industry. The final section homes in on cattle producers more specifically to interrogate what happened when cattle existed both on hoof and on paper. From the perspective of cattle producers, the miracle of nonstorable derivatives was somewhat undeserved. The material infrastructure of cattle dealing needed little adjustment to accommodate abstract financial trading, and the modeled vision of nonstorable hedging never came to fruition. Nonetheless, cattle producers’ experience revealed how the fundamental justification for derivatives, hedging by producers, gradually stopped being a meaningful criterion for derivatives markets’ success after 1964. Live cattle futures did change everything, but the revolution really was a paper one.

More or Less Like Grain

During the discussion period at a 1959 Chicago Board of Trade (CBOT) seminar, two futures traders broached the pressing issue of what things could trade on futures markets. First, Walter Goldschmidt asserted, “I think all of us realize that some commodities are more suitable to futures trading than others, […] We know that wheat is more suitable [than are] refrigerators.”Footnote 29 Goldschmidt was an ambitious grain elevator worker and futures clerk, who would eventually lead Continental Grain into abstract financial futures.Footnote 30 At the time, though, his imagination was still constrained by prevailing academic wisdom, which assumed that futures trading could only function for commodities that were fungible, storable, and deliverable. Academic research on derivatives had been essential for the social justification and regulatory permissibility of futures, but it inadvertently embedded an assumption about material characteristics that sharply constrained the realm of what was possible to commodities that were more or less like grain, historically the most successful futures. The next speaker, Gerald Gold, retorted, “I think you are beginning to get some challenge as to the criteria […] necessary to futures markets characteristics. And I don’t think we want to go into that too much right now; but I think it is important to watch.”Footnote 31 Gold was a professional futures expert and broker, and just a few hours earlier he witnessed the first documented case of an economist arguing against the prevailing wisdom on material limits to speculation. Goldschmidt and Gold’s conversation captured the way derivatives traders interpreted knowledge from professional economics to guide their own market decisions. Goldschmidt was trying to interpret the script provided by economic theory. Gold was implying they might toss the script away, but he knew the industry was not ready for that yet. Most economists, exchange members, and agricultural producers in the audience probably sympathized with both Goldschmidt’s and Gold’s perspectives. They confidently believed trading in derivatives only worked for commodities with certain material “characteristics,” but being wrong would be exciting.

From the 1860s to 1890s, derivatives in the United States grew in volume and complexity. Starting with the CBOT’s forward, or “to-arrive,” grain contracts, commodity exchanges across the country began organizing markets for people with no interest in owning physical commodities to speculate on the seasonal price changes of those commodities.Footnote 32 The exchanges did exist to market real agricultural products, but their business in “paper wheat” and other imaginary commodities became far more lucrative. In 1895, the New York Produce Exchange (NYPE) marketed 43,405,076 bushels of real wheat and 1,443,875,000 bushels of wheat futures.Footnote 33 That was roughly half a billion more bushels of wheat than existed in the country, and the NYPE was only the second-largest grain dealer in the group. In addition to over twenty large derivatives exchanges, “hundreds” of smaller exchanges and “bucket shops” offered variations of futures, options, and swaps on a dizzying list of things that might or might not exist.Footnote 34 William Cronon argued that the nineteenth-century “revolution” in futures developed from technologies and institutions, including grain elevators and commodity grading, that allowed people to trade “homogeneous abstractions” of goods that had previously been distinguishable to the individual sack and farm of origin.Footnote 35 Jonathan Levy argued even more forcefully that nineteenth-century futures represented “trade in increments of abstract, homogeneous time” that required “a concrete labor of continual abstraction.”Footnote 36 Historians’ descriptions of agricultural derivatives in the nineteenth century are, thus, similar to social scientists’ analysis of the underlying materiality of “virtual” or “strange” derivatives after 1972. In both periods, derivatives “quickly” became “the cutting edge of the American corporate financial system.”Footnote 37

In contrast to the later debate on technical constraints on live cattle futures, the nineteenth-century debate over abstraction focused explicitly on moral and metaphysical concerns. Resolving those concerns ultimately made abstraction an apolitical technicality. Opponents of derivatives enacted various anti-futures laws in eleven states from 1879 to 1889, culminating in two barely-failed efforts in the United States Congress in 1892.Footnote 38 As Levy explained, the driving complaint was that these “financial abstractions […] had lost touch with the reality of the waving fields of wheat.”Footnote 39 Public backlash and the enormous growth of these markets motivated political economists Albert Stevens and Henry Crosby Emery to conduct and publish the first academic studies of derivatives in the late 1880s and 1890s. They were both drawn to the intellectual challenge and to the opportunity to prove “thousands of intelligent people” wrong.Footnote 40 The economists’ desire to correct “inaccurate ideas” and to elucidate the finer theoretical workings of derivatives tended them toward the defense of futures against their critics. Emery believed it was “impossible to deal intelligently with the evils of the speculative system without first recognizing its real relation to all business.”Footnote 41 Stevens and Emery shifted the debate from what was plain in practice—“evil” in Emery’s words—to the more challenging question of how the markets ought to work in theory.Footnote 42

Stevens and Emery’s response to the moral and metaphysical critique of derivatives was that futures were indelibly linked to the material reality of farmers’ fields by “hedging.” Hedging, as explained to cattle producers decades later, “is offsetting the ownership of a [real] commodity—or the obligation to deliver or accept delivery of a commodity—by a counter-balancing sale or purchase in the futures market.”Footnote 43 Taken differently, hedging was the conceptual notion that frenzied speculation in imaginary commodities provided a sort of “price insurance” for agricultural producers.Footnote 44 Traders and economists developed hedging practices and ideas reciprocally. As David Pinzur demonstrated, hedging originated in the exchanges, and it varied based on different exchanges’ delivery mechanisms and rules.Footnote 45 Economists discovered and generalized hedging, and exchange traders and regulators then drew from the experts’ versions.Footnote 46 Already in 1896, Emery reported that “this practice of hedging is now universal in the trade in grain and cotton.”Footnote 47 By 1931, Columbia law professor Edwin Patterson asserted that hedging was the “chief” “justification for the continuance of futures trading.”Footnote 48 Patterson, a leading expert on insurance law, explicitly stated that if there were any other way to provide the price-risk insurance of hedging, futures ought to be abolished as gambling, but there was not.

Hedging upended normal understandings of market transactions, but once grasped, it had great explanatory power. First, dispense with the notion that markets are composed of buyers and sellers, who want to exchange goods for money. In derivatives markets, people are hedgers or speculators, who instead want to exchange risk. Hedgers are the participants, who also have an interest in real commodities, such as cotton spinners or, later, cattle feeders. Because they buy agricultural commodities at one point in time, then process, move, or store them, and resell them at another point in time, they face the risk that prices will change in the intervening period. If the hedgers sell futures on spun cotton, as they buy raw cotton, and buy back those futures, when they sell the real spun cotton, the futures, and wholesale markets will offset each other (Figure 1). Hedging linked and subordinated the “paper” futures markets to real commodity transactions. As James Bloss of the New York Cotton Exchange explained, even if a hedged contract on “actual cotton” sold to others without cotton “nine times or a hundred times,” it was still a transaction in cotton benefiting the original producer.Footnote 49

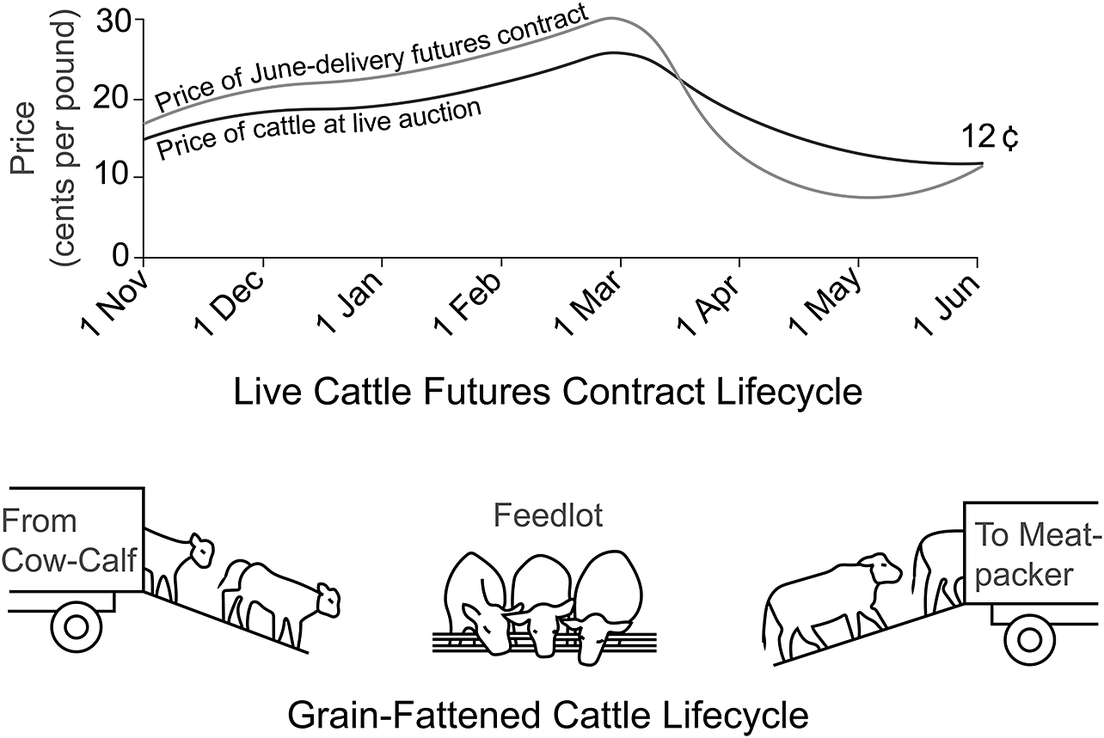

Live cattle hedging model.

Note: As explained to US cattle producers, a hedge worked by executing equal, same-day transactions in the futures and live-auction markets. Imagine a cattle feedlot operator buys twenty-five calves on November 1 to fatten them on grain (to approximately 1,000 lbs. each) and sell them for slaughter on June 1. The feeder needs to make at least 17¢/lb. to sustain the business, so the feeder sells a futures contract for 25,000 lbs. of Choice grade steers for June delivery at that rate to an anonymous speculator. Come June, the real price of fat cattle has fallen disastrously to 12¢/lb., but the cattle feeder may now buy back the futures contract for just 12¢/lb. The 5¢ gain in the futures market, thus, offsets the 5¢ loss at the live auction and ensures the desired outcome of 17¢/lb. This version of the model assumes no cost of storage or delivery. (See, for example, Black, “Guaranteed.”; Turner et al., “Livestock.”).

In the first half of the twentieth century, most research on futures markets aimed to understand hedging and help agricultural producers do it better. Agricultural economics valued applied research foremost and drew on institutional approaches well after their general decline in the 1940s.Footnote 50 Even so, futures were a niche research interest. Of the economists interested in futures, only Holbrook Working of Stanford had a significant impact on economics outside derivatives, and his most influential econometric modeling research occurred decades before he began publishing on futures. However, these economists were influential among their intended audiences—derivatives users and regulators. By 1953, Working defined futures as financial instruments that “serve primarily to facilitate hedging,” and he further argued that futures markets would necessarily fail without sufficient hedgers.Footnote 51 However, hedging proved challenging, and economists who scrutinized agricultural producers’ use of hedging found that “so-called hedging transactions shade into operations that fall far short of a practical hedging purpose.”Footnote 52 The USDA and agricultural extension programs distributed research findings about hedging through existing agricultural knowledge networks, and derivative exchange leaders also took an active role in developing and disseminating knowledge about hedging by hosting conferences and speaking tours that assembled academics and producers. As performativity theory would expect, the increasing availability of hedging models enabled futures markets to strike the desired balance of commodity owners and speculators described by theorists. Studies from 1948 to 1951 determined that 74 to 84% of open contracts in wheat were hedges; in 1959, they made up 85%.Footnote 53 This was good news, but economists and exchange leaders also came to believe the existing markets were exceptional, and in most other cases would not work.

The concept of material constraints on futures sneaked into this conversation from multiple directions. In the twentieth century, experts knew that actual deliveries of goods on futures contracts were negligible, but they still thought them necessary. First, futures had to be about the price of something else, and exchange leaders long believed traders could only agree to that price if the contract were interchangeable with some readily available goods.Footnote 54 For example, in the 1950s, the Chamber of Commerce of Minneapolis was pricing “ordinary protein wheat” on futures, but Minneapolis only had “better wheat” in storage, which meant buyers could demand higher cash prices by threatening to take delivery.Footnote 55 Second, economists and other experts had a tendency to evaluate potential futures contracts based on their similarity to grain crops, and grading, storage, and delivery conditions had been fundamental to the early and ongoing success of those markets. During an analysis of “why futures trading succeeds or fails,” economist Roger Gray, Working’s successor at Stanford and a consultant for the CBOT, compared or contrasted various commodities to grain five times in his presentation and four times in the discussion period.Footnote 56 It made sense because only wheat, corn, and soybean futures had large and sustained trading in Gray’s or Goldschmidt’s professional lifetimes.Footnote 57 Even cotton futures, which had been the most-traded nongrain contract of the nineteenth century, dwindled to below 100 bales per year by the 1960s.Footnote 58 Third, and most importantly, economists argued that hedging only worked if a producer could accurately calculate the costs of real storage and delivery on their commodities and execute parallel trades in futures contracts on the same day.Footnote 59 This difference between futures prices and commodity prices due to invisible (but calculable) supply chain costs was called the “basis,” and it also became important for speculators’ calculations.Footnote 60 Material constraints on “commodities adaptable to futures” appeared as facts in the few textbook descriptions of futures from the period.Footnote 61 The increasing emphasis on hedging and storability made derivatives markets less abstract, both conceptually and in practice.

The only record of any academic dissent on the material limits of derivatives before 1964 occurred in an oral presentation at the 1959 CBOT futures seminar cited at the beginning of this section. Mere hours before the exchange between Goldschmidt and Gold, Henry Bakken of the University of Wisconsin ignited controversy by explicitly and forcefully doubting the prevailing wisdom on futures. “Most of our contemporary writers seem to be in agreement on one point,” he observed, “They contend that trading in futures contracts is circumscribed in its application to a limited number of commodities.” “In my opinion,” Bakken offered with abundant prescience but scant evidence, “this thesis [is] entirely fallacious.”Footnote 62 Granted the first question from the floor, University of Illinois economist Thomas Hieronymus demanded an explanation for how a “futures market that does not involve delivery” could be “reasonably possible.”Footnote 63 Hieronymus was an early advocate for the expanded use of futures by farmers. Bakken argued that there was no reason for the cash and futures markets to “be tied together by an antiquated concept of delivery” because futures were useful for pricing and people used them as such. If futures markets stopped being useful, people would stop using them, so there was no actual need to punish the traders with delivery of things. The discussion provoked Leonard Schruben of Kansas State University to ask for clarification: “Do you regard hedging as essential for futures trading?” “Not at all,” Bakken replied, “hedging is incidental to futures trading.”Footnote 64 Pushed further, Bakken observed that futures emerged in Chicago around 1867, but the first known hedges happened in the “early eighties,” so for about fifteen “formative” years…. Schruben finished Bakken’s thought: “…you have speculators speculating with other speculators[!]”Footnote 65

Bakken took a historical institutionalist approach to studying derivatives markets that ignored theoretical questions to an even greater degree than his peers. He looked at futures trading in practice and observed, “the brokers and traders in the world’s exchange centers and elsewhere are as often as not unconcerned, oblivious, and incurious about materiality.”Footnote 66 Bakken’s polemic contained wisdom, but he was exaggerating for effect. After all, Goldschmidt and Gold’s conversation in the next session betrayed a great deal of concern, awareness, and curiosity about materiality. From 1959 to 1962 just under 2% of all contracts at the CME were closed out in actual commodities, but audience members knew how misleading that statistic sounded.Footnote 67 Two percent of contracts was a huge amount of deliveries in physical things, and making those deliveries work was a central preoccupation of derivatives experts, including those on the industry side. Gray swiftly stood up and asked Bakken to consider deleting the “two bad paragraphs” that dismissed material constraints before submitting the final draft for publication.Footnote 68 Gray had built his career explaining the direct relationship between cash and futures markets, and people like Goldschmidt had built their companies by studying it. Allen Paul of the USDA next accused Bakken of going “off the ‘deep end’ by doing away with hedging.”Footnote 69 Bakken refused to rescind his comments.

For five years, Bakken would have to remain confidently incorrect in the eyes of his field, but his presentation made material constraints a question for the first time. Material constraints had come from basis calculations; the basis had come from hedging models; and hedging had come from social concerns with untethered abstraction. By 1959, though, economists like Working alleged that material constraints were basic facts of the market, and that made them testable. When rumors first broke that the CME was considering launching live cattle futures, it was immediately framed as a test of theoretical material constraints. As Gold suggested, people were watching to see who was right: Bakken and a handful of people at the CME, or everyone else? Following Goldschmidt’s metric, were cattle more like wheat, the model futures commodity, or refrigerators, an absurd impossibility? Journalists asked economists and livestock industry experts for predictions about the futures market. The American Meat Institute (AMI), an organization “representing meatpacking companies of all sizes, located in all parts of the country,” even hosted a private presentation and dinner to solicit Hieronymus’ expert prediction on the “troublesome” “matter” of the “list of conditions that must be met before a futures contract is feasible.”Footnote 70 Although economists typically used storability, deliverability, and fungibility interchangeably, Hieronymus determined that only deliverability truly mattered, which still excluded living animals. Hieronymus, like Goldschmidt, was willing to revise the script but not reject it. The belief in material constraints was so deeply entrenched that only a real test in the wild could dislodge it. A futures contract had never before gotten so much attention before it took off, but in all the fanfare around 1964, Bakken’s ultimate point was overlooked. Cattle futures would not just test material constraints; they would also upend the social and economic justification for the existence of futures markets: hedging.

The Financial Revolution of 1964

Reflecting in 1986, Miller of the University of Chicago and CBOT suggested, “No word is more overworked these days than ‘revolution.’ Yet, in its original sense of a major break with the past, the word revolution is entirely appropriate for describing the changes in financial institutions and instruments that have occurred in the past twenty years.”Footnote 71 Miller missed cattle futures by two years, but he recognized that the revolution began well before 1972. The CME anticipated the potential for Miller’s perspective in promotional materials about cattle futures in 1964. The CME giddily publicized cattle futures as an important test, which, “if successful,” would provoke “a revolution in United States agriculture” that could “affect every consumer in the country and large segments of the banking and other industries.”Footnote 72 The CME did not foresee the derivatives industry’s leap beyond agriculture, but they knew cattle futures would have implications far beyond themselves. According to Michel Callon, truth in economics is an event—a success or failure.Footnote 73 Cattle futures, as a test, became an event with the power to change what was true. People recognized cattle futures as revolutionary at the moment, and other people acted on the new possibilities that cattle opened in ways that extended the revolution in derivatives. Miller and others have failed to recognize the revolutionary power of live cattle because derivatives have grown so much since 1964 that the early volume of trading in live cattle is rendered nearly invisible in retrospect. To see how much cattle futures mattered, we need to appreciate how little growth or innovation there was in derivatives before 1964. Taken in the context of widespread doubt and a stagnant derivatives industry, cattle futures were an outstanding success that reinvigorated the CME and changed the way industry and academic experts approached abstract derivatives.

The increasingly narrow theoretical vision of possibilities for derivatives matched their historical reality in the twentieth century. From 1892 to 1964, the CBOT was the uncontested largest futures exchange in the world, and its only significant innovation in the period was to add soybeans to its older list of grain offerings. Hieronymus determined that the CBOT consistently sold about 15 to 25 billion bushels of grain per year from the 1880s to 1930s and just under 10 billion bushels in the 1940s and 50s.Footnote 74 Smaller exchanges launched a plethora of contracts in the first half of the twentieth century, but their universal failure only confirmed the economists’ suspicion that speculation was made for grains. Contracts failed in lard, pork, silk, hides, wool, tobacco, peanuts, tallow, pepper, lead, crude oil, and a range of other things that technically fit the specifications. The Chicago Livestock Exchange even attempted trading in live hogs in 1930, but the market was “monotonous” within a year and nearly erased from memory by 1964.Footnote 75 Derivatives markets were, thus, enormous but static. It is out of this context that abstract derivatives seemed to explode as if from nowhere. After cattle futures, new contracts appeared with far greater frequency, they were more likely to succeed over the long term, and the majority of them were in nonstorables.Footnote 76

The most interesting innovator, and failure, of the period was the CME. Like the CBOT before it with grains, the CME emerged organically out of forward contracting in eggs and butter, and it was organized formally in 1919. The CME gained a low reputation as the rougher and more volatile of the Chicago exchanges, and CME leaders had to work harder to attract clients. The CME was founded on a bold idea—perishable or seasonal commodities like vegetables and frozen or refrigerated meats produced larger, less predictable short-term volatility, which made them lucrative for speculation. The commodities had to be storable, but the potential to spoil in storage made things interesting. The CME experimented with potatoes, onions, turkeys, chickens, shrimp, and hams, but only pork bellies, launched in 1962, had any lasting impact, and even they “didn’t really start to take off until about 1965.”Footnote 77 Failure drove the CME to the brink of obscurity. By the early 1960s, the CME accounted for less than 4% of US futures trading volume, and in 1963, the total volume of trading dropped to its lowest levels in ten years.Footnote 78 The CME resorted to buying back thirty-nine of its memberships for $3,000 each to prevent their value from collapsing further.Footnote 79 CME president Everette Harris appointed Glenn Andersen to lead a “New Commodities Committee” to save the exchange.Footnote 80 “At this point,” remembered Working, “the outlook for the [CME] might have been judged hopeless.”Footnote 81

Then, while promoting the ill-fated shrimp contract in Texas, Harris sat for a meeting with James Sartwelle, who had an idea for a futures contract on living cattle.Footnote 82 The meeting reflected how deep Harris was digging for new ideas. Sartwelle’s family owned a livestock yard and auction near Houston, but, in 1963, Sartwelle was just 23 years old and in his final year of an agricultural economics degree from Texas A&M. Harris was a former economics instructor and well aware of the literature on material constraints, but Sartwelle caught his attention. Shortly thereafter, a prominent Pittsburgh banker told Harris he had lots of customers in need of a hedging mechanism for cattle, which “lent just an awful lot of support and credibility” to Sartwelle’s idea.Footnote 83 Harris and Andersen swiftly re-organized a “Cattle Committee” and brought in experts like Lennart Palme, an Armour trader with a past in cattle feeding. Palme had studied under Working and Gray at Stanford, and he helped the committee research “a whole background” on the theoretical and practical “feasibility” of a “living animal” contract.Footnote 84 The committee also surveyed several dozen meat industry experts and discovered that a sizable minority were interested in trying something, theory aside.Footnote 85 The committee commissioned a report that predicted, “We cannot overstate the likelihood that there will be a volume of trading that will completely astound even the most optimistic of the proponents of the futures.”Footnote 86 Based on Sartwelle’s initial draft, the team designed a futures contract for 25,000 pounds of Choice grade steers for delivery to Chicago or Omaha on the first day of 4 months of the year. The contract represented an imaginary truck with twenty-five uniform animals of 1,000 pounds each inside.

We know little about Sartwelle’s motivation directly, but elsewhere he bemoaned how marketing in the livestock industry had “become a jungle” with about 185 auctions in Texas alone.Footnote 87 The Sartwelles made their fortune by providing a physical marketplace and collecting a modest rent on transactions between cattle sellers and buyers but the younger Sartwelle’s ability to do so was slipping away. Competition in the stockyards business increased even as the industry turned toward a general decline. Sartwelle worked with the CME to create an alternative, nonphysical pricing and marketing option, and within months he formed “the state’s first exclusively livestock futures trading company.”Footnote 88 Sartwelle helped the CME design the contract to align with how producers sold real cattle by the truck-load, and he also acted as a “very, very helpful” spokesperson for the market “on the producer side.”Footnote 89 Sartwelle figuratively and literally sold futures to cattle producers, and he made $36 on every contract.Footnote 90

It took relatively few cattle producers to make financial history. Most people in the cattle industry were opposed or indifferent to futures in 1964. Acting on Hieronymus’ expert predictions, the AMI forcefully opposed the establishment of a cattle futures market. They circulated a short essay on the undesirability of futures for beef consumers, cattle producers, and especially meatpackers that concluded with the observation that even if some sad cattleman did still want to use futures, they simply would not work because cattle lacked “certain fundamental characteristics that students of futures markets feel are necessary to success.”Footnote 91 “Chances are,” the AMI opined, “the futures market for cattle and beef will either die like those for onions, potatoes, broilers, and butter or be of no greater importance than those for turkeys, shrimp and fresh and frozen eggs.” The American National Cattlemen’s Association (ANCA) had no comment when asked about it in 1964 because the organization had not yet bothered to discuss it.Footnote 92 Privately, an executive of the National Livestock Feeders Association told Andersen, “You can’t deliver live animals. Drop dead.”Footnote 93 W.D. Roberts, President of the Florida Cattlemen’s Association, may well have represented the majority view when he declared, “It’s not worth a doodle as far as I’m concerned.”Footnote 94

There was certainly no national-scale, organized movement for cattle futures. And yet, when the contract launched, calls gushed in because people like Sartwelle in Texas and Waldner in Kansas were stomping boots in cattle country converting producers to futures.Footnote 95 Harris appeared at livestock conventions and “virtually every agricultural school in the country,” sometimes uninvited.Footnote 96 Economists from Iowa State University circulated a seventy-seven-slide presentation on hedging cattle.Footnote 97 The CME knew it needed hedgers, but its research also predicted diverse speculators would be attracted to cattle as a “Glamour Industry.” “It would not be strange at all,” suggested CME research, “for people who have little knowledge of the industry, and even no real desire to make a speculative profit, to play the futures on cattle […] just to be able to say at the cocktail parties that they have X number of cattle on feed.”Footnote 98 Urs Stäheli argued that the abstraction of derivatives, troubling for some, also made them attractive and “voyeuristic” to others.Footnote 99 The debate about live cattle’s theoretical contradictions ended up being great publicity, and the CME played it up. CME leaders wore cowboy hats, distributed commemorative livestock canes, and welcomed real cattle onto the trading floor as door prizes (Figure 2).Footnote 100 There were plenty of commodities in 1964 that already fit the accepted requirements for futures trading, but the CME wanted cattle and they wanted cowboys because cattle and cowboys were exciting.

Live cattle contract opening, 1964.

Note: “Contract opening — live cattle futures, group photograph with cow.” [1964]. CME records, Folder 4.12.13. Gratefully reprinted with permission from Special Collections and University Archives, University of Illinois at Chicago.

Waldner felt the revolutionary weight of cattle futures, and he wanted a stake in their story. Eager to make a “tangible demonstration of [his] faith and confidence” in the new market, Waldner phoned his broker at the CME on November 30, 1964, and placed the world’s first sale of cattle futures.Footnote 101 They sold to an agent of the DuPont chemical company, which might have surprised others, but Waldner already understood that his buyer was irrelevant, since no one actually wanted to trade cattle. Waldner had to be a quick dialer to earn his prize because seventy-two contracts were sold in the first 45 minutes of trading, dwarfing the CME’s goal of fifty to sixty trucks for the whole day. By the end of the day, open interest swelled to 191 contracts from sellers as far as Honolulu, Hawaii. Harris called it “by far the most aggressive opening of any commodity we have had on the exchange.”Footnote 102 Privately, Harris worried that the volume “was mostly contrived” since people “wanted their pictures in the papers,” but his doubt was fleeting.Footnote 103 On February 26, 1965, the market hit a peak volume of 665 contracts. This was the kind of action only the eldest exchange members would have experienced before, and it would only keep growing. In the first six months of 1965, paper cattle dealers traded thirty thousand contracts, and in the first six months of 1966, they traded over eighty-four thousand.Footnote 104 In their first 20 months, the total value of live cattle futures would exceed one billion dollars.Footnote 105 Sartwelle stated plainly: “Cattle futures tore up the record books.”Footnote 106 All this must be taken in context or else their enthusiasm does not make sense: eighty-four thousand contracts still only represented 6% of living beef cattle in the country at a time when speculation in paper wheat regularly exceeded the volume of all real wheat.Footnote 107 But everyone already knew you could trade paper wheat.

Economists and exchange leaders rejoiced. Reflecting on the success of cattle, Bakken said futures in “animated products” should rank equal with “the coinage of money, the abolition of slavery, private property ownership, the negotiable contract, the bill of exchange, and the corporate organization” in the history of “milestones” of modern capitalist development.Footnote 108 Palme waxed even more eloquent that cattle futures “may readily be compared to some of the early voyages on uncharted seas, exploration of new lands or manned flights into outer space.”Footnote 109 Both emphasized that this historical event settled the theoretical debate on material constraints. “Physical delivery,” concluded Bakken, “is an imaginary illusion that need never be real; it is a vestigial concept of an age-old custom that may be relegated to oblivion whenever the enlightened enterpriser chooses to cast it into discard.”Footnote 110 Of course, cattle futures also opened a litany of new questions. There was no doubt that the CME had proved that the untradeable was tradeable, but it was unclear why it worked, who was using it, how they were using it, or what it all meant. The academic futures conversation pivoted swiftly from the CBOT to the CME, with the younger exchange hosting spirited cattle futures seminars in 1965, 1966 (twice), 1967, and 1979.

As Bakken suggested in 1959, the real victim was hedging. Gray seemed a bit dumbstruck, admitting that “Harris appeared to be one of the most snake bitten individuals in the world” for talking “mostly to himself about such unlikely prospects as […], of all things, live animals.”Footnote 111 Gray insisted that “all the evidence” pointed to the need for hedging and hedgers, but doubt accumulated at the seminars.Footnote 112 Though still convinced of its importance, Working proposed placing “‘hedging’ in quotation marks” because “the word means different things to different people and in different contexts.”Footnote 113 The economists produced numerous empirical studies of livestock futures that suggested older hedging models did not work. Marvin Skadberg and Gene Futrell proposed that live cattle futures were “basically different” from all previous storable commodities, and they suggested that economists knew next to nothing about how or why they functioned.Footnote 114 Lester Telser eventually argued in 1979 that hedging theory was a historical–rhetorical justification for futures, barely different from moral accusations about gambling and that it was not fundamental to futures markets’ success.Footnote 115 Bakken queried his field smugly, “Is the classical concept of hedging entirely passé?”Footnote 116

The CME did not ultimately need to understand cattle futures to profit from them. As more and more people called in to buy and sell cattle, the value of membership in the CME swelled. The CME swiftly sold all its vacant seats to cattle producers for $4000 and by 1969 a membership was worth $50,000.Footnote 117 Also in 1969, the CME surpassed the CBOT in trading volume, something no other exchange had done in over ninety years.Footnote 118 CME leaders noticed that speculators migrated from the New York securities exchanges to their commodity pits. Journalist Emily Lambert described how “the meat pits were full of men in their thirties suddenly making money.”Footnote 119 One of them was Leo Melamed, who later became the architect of the CME’s first currency futures and a close collaborator with monetary economists. Melamed has mostly downplayed the importance of cattle futures, which preceded his innovations in financial derivatives, but his biography made clear that before 1964 he was struggling to make an income as a trader at the CME.Footnote 120 Without cattle futures, it is hard to imagine either the person or the organization being in a place to launch financial derivatives once Bretton Woods ended. But cattle futures did happen, and they were ready.

The CME’s success with live cattle spawned imitators. The CBOT began work in 1964 and launched a competing market in 1966.Footnote 121 Winnipeg Grain Exchange executives toured the CME cattle pit in 1966 and launched their contract in 1967.Footnote 122 The Kansas City Board of Trade (1970), Pacific Commodities Exchange (1974), New York Mercantile Exchange (c.1981), and MidAmerica Commodity Exchange twice (c.1981, c.1996) followed, but none lasted. Variations such as carcass beef futures and the CME’s own feeder cattle futures also failed to match live cattle’s success. However, the CME launched a successful live hogs contract in 1966 making it the greatly-envied world leader in livestock futures. By 1980, live cattle futures were the largest single contract offered by the CME. However, the real legacy of cattle futures was not in other livestock contracts; it was in the suddenly explosive realm of “non-storables,” especially financial futures.

Live cattle did not directly inform the design of financial futures, but they did mold the culture of innovation at the CME. As Palme recalled, Friedman of the University of Chicago, first reached out to him with “the idea of the currency futures” because Friedman “became aware of the fact that I had worked on the live cattle and had ties with the [CME].”Footnote 123 Palme referred Freidman to Melamed, who urged the CME to form the International Monetary Mart (IMM) and launch the first futures contracts on currencies in 1972. The CBOT immediately contracted economist Richard Sandor, and by 1975, they launched the first futures on interest rates (Government National Mortgage Association Mortgage-Backed Securities). Andersen proposed hiring a permanent research economist at the CME following his committee’s experience conducting extensive research on the cattle contract, and the economist they hired came up with the idea to launch the first futures on Treasury Bills in 1976.Footnote 124 The CBOT followed up with the first Treasury Bonds (T-Bonds) in 1977 and Treasury Notes in 1982. Also in 1982, the IMM introduced index futures (S&P 500), and the CME began launching options on everything.Footnote 125 Sandor described the novelty of the T-Bond, for example: “To the uninitiated, the design of the contract appeared almost surreal. We had created a fictional bond as a proxy for the long-term bond market.”Footnote 126 Miller, another of Melamed’s academic collaborators, concluded in 1986 that “the mind boggles.”Footnote 127 By 1985, storable agricultural commodities accounted for less than a quarter of American derivatives trading, and the innovations in nonstorables have only continued with derivatives on cryptocurrencies and weather patterns launching in recent decades. In retrospect, refrigerators were more like wheat than many of the things that ended up trading on derivatives markets after Goldschmidt posed his question.

For those most closely involved, this all linked back to live cattle as much as Bretton Woods. Melamed believed that “agriculture was never going to be the future” but he observed a “dramatic step” with the first nonstorable in, “wonder of wonders, […] a product that was alive and kicking.”Footnote 128 Cattle “broke the genetic code of futures” leading to Melamed’s innovations in financial derivatives. Sandor also called out livestock futures, writing, “At the start of the twentieth century, the definition of a commodity from which a spot market could evolve into a futures market was widely accepted as one comprised of standardized, bulk, and storable commodities. […] In the mid-1960s, futures markets in live cattle and hogs eliminated the necessity for storability.”Footnote 129 Economist Barry Goss reiterated, “until recently it was customary to distinguish storability and deliverability as feasibility conditions” for “futures trading to be possible,” but “recent experiences such as trading in […] finished live beef cattle […] have shown these two conditions to be unnecessary.”Footnote 130 Finally, Commodity Futures Trading Commission Chairman Philip Johnson, stated most explicitly, “Well within my memory the futures industry considered the creation of a futures contract on any perishable commodity impossible. […] The advent of financial futures can be credited in no small measure to the success of seemingly impossible commodity futures, which led the industry to believe that anything might be possible.”Footnote 131

Counterperformativity helps decipher the financial revolution of 1964 and the impacts of live cattle futures on financial derivatives and other nonstorables. Common sense suggests that cattle are more like grains than mortgage-backed indices because they are agricultural, but in the way derivatives experts imagined it, cattle were more like abstract debt instruments because they were nonstorable. Rather than a shift away from agriculture, the explosion of abstract derivatives after 1972 might better be described as a shift towards things more like living livestock. Without hedging models that insisted on storability as a necessary condition for derivatives markets, there would be no reason to make such a conceptual leap. Widespread acceptance of hedging models led eventually to the creation of markets that undermined the postulates of those models. The failure of the model was itself heavily scripted. Economists and exchange leaders constructed cattle futures as a theoretical test that depoliticized longstanding social boundaries on commodity speculation. Skadberg and Futrell revealed that empirical data on live cattle futures remained ambiguous, but experts swiftly interpreted the results as broadly as possible. The silliness of past belief in material constraints, as demonstrated by cattle futures, became central to economists’ and exchange leaders’ “legitimizing narratives” about new and increasingly abstract markets.Footnote 132 Following Austin, economists and exchange leaders said cattle futures made nonstorables of any kind possible, and then they made that true in practice. However, for cattle producers material reality remained somewhat distinct from speech acts.

The Texas Hedge

At the 1979 CME cattle futures seminar, producer Bruce Ginn suggested, “I think there is, to a certain extent, a difference between what the people at the [CME] call a successful contract, and what cattlemen call a successful contract.”Footnote 133 Cattle producers also treated cattle futures as a test, but not of theory. Producers wanted to know if futures would be helpful in the context of their cattle businesses, and that was a material concern. Producers’ opinions on cattle futures took longer to develop than the financial derivatives revolution, and they were more ambiguous. Cattle producers were the principal audience for economists’ hedging models, and they applied them to a futures market in nonstorable commodities for the first time. In contrast to storable hedging models, cattle hedging models failed miserably and had a minimal impact on the paper cattle market in practice. Instead, producers constructed their own alternative vision of the market based on unchecked speculation, which would eventually become known as the “Texas hedge.” Ultimately, cattle producers would count as the greatest proponents and the greatest opponents of cattle futures, and in both cases, it was because they could see things best.

By 1964, American cattle producers had ample experience with finance and markets. Urban investment capital from the Eastern United States, England, and Scotland spurred growth and collapse in the western cattle industry since the late nineteenth century. By the mid-twentieth century, cattle producers financed their land, cattle, feed, vehicles, buildings, and machines with local and national lenders. Cooperative selling was negligible in the industry, and every producer accounted for their own marketing within a dizzying array of options. The development of a complex carcass grading system since 1905 and the proliferation of sale points meant producers were already always measuring real cattle against imagined ones with different potential values. After the 1940s, cattle production cleaved into feeder raising (cow–calf ranching) and feedlot finishing (feeding), which doubled the pricing categories and forced producers to imagine their animals’ value across their lifecycle (i.e., time in the future). Waldner visited the CME “beef pit” in 1965 and reported, “The cattleman particularly, should feel at home […]. The action there is similar, in many respects, to the activity of the livestock auction arena.”Footnote 134 Although farmers had previously had reactionary responses to derivatives in grains and vegetables, cattle producers were well-conditioned to consider a radical new financial tool in their industry by the time the derivatives business finally caught up with them.

More than any other party involved, cattle producers took a practical approach to futures, and the issues of fungibility, storability, and deliverability did not concern them deeply. Waldner and other boosters always insisted producers should act like delivery was possible for their calculations but never actually did it. What mattered for producers was whether those partially-imagined calculations would prove profitable or not. Cattle producers were interested in hedging because their lived experience of cattle prices was chaos. Taken over the long term, the late 1950s and 1960s were one of the best growth periods with the best prices American cattle producers would ever get, but the annual and daily variability still made them feel like the worst. Cattle futures were particularly attractive to cattle feeders, who had the greatest investment in animals and industrial technology, and who had the least flexibility in the timing of sales. “Cattle feeding is risky business,” noted the CBOT, and it “is becoming increasingly riskier.”Footnote 135 The CME learned that “the profit that a feeder makes is more likely to be determined by the time the animals are for sale and the market level at that point, than the efficiency with which the cattle are fed.”Footnote 136 The derivatives industry realized that economists might not be quite ready for cattle futures, but cattle producers were.

There was scant empirical evidence that producers drove the first years of growth in cattle futures, but few experts disputed it. When asked about “the nature of [the CME’s] clientele” at a seminar in 1966, Harris answered “in a somewhat subjective manner” that cattle feeders were “very active.”Footnote 137 A survey of everyone holding a cattle contract on July 28, 1967, found that cattle producers and other livestock industry people held over two-thirds of open interest.Footnote 138 Mostly, economists simply inferred that producers had to be there since the market worked.Footnote 139 It is reasonable to believe that a significant number of producers participated because the CME worked so hard to recruit them, but again this was relative since a huge number of cattle producers for the CME was still a small fraction of that industry. In 1973, another survey of 599 Illinois livestock feeders found that only 5.8% of them had used a livestock futures contract in any way.Footnote 140 This means that a small minority of American cattle producers played an outsized role in proving derivatives markets functioned for nonstorable commodities.

Waldner offered a rare glimpse into the origins of cattle futures. Waldner enthusiastically made the first sale in November 1964, and then he tracked and reported on the new market for other cattle producers through its first year. By April, Waldner and most other sellers had dutifully closed out their contracts in cash, but Lloyd Ewald and Cliff Haden of Rochelle, Illinois (just 80 miles from Chicago) decided to deliver living animals instead. Unlike elevator receipts for grains, there was no system of stockyard receipts to simplify the delivery clause that still existed on the contract despite the alleged nondeliverability of the underlying asset. Waldner was at the Union Stockyards in Chicago at 6 a.m. on April 27, 1965, to observe the “final test” of cattle futures. He waited four hours until two USDA graders appeared and spent 5 minutes per pen assessing the animals against specifications. Waldner declared the result “an unqualified success,” but that was a matter of perspective. Unsurprisingly, Ewald and Haden did not actually deliver lots of twenty-five identical animals. The USDA graders orchestrated a bovine hokey-pokey between the pens and left the sellers with cash penalties and surplus cattle to sell elsewhere.Footnote 141 According to Waldner, Ewald and Haden’s misfortune followed their decision to ignore the modeled assumption that delivery never takes place.

Producers’ tests of the delivery clause revealed that delivery of material goods, which used to punish speculators into accepting wholesale prices, now punished hedgers into accepting futures prices. As reported at a CME futures seminar, Kenneth Monfort, a cattle feeder from Greeley, Colorado, believed “live cattle futures would not work” and decided to test the market explicitly. First, Monfort bought cattle futures and insisted on taking delivery, but the animals “did not yield or grade anywhere near what they were supposed to,” and he “raised hell” like a “nut.”Footnote 142 Second, Monfort sold cattle futures with the plan of delivering comparably scrappy animals but then found the CME “revamp[ed] the whole thing” to prevent it after his complaint. Monfort lost money on both sides of the transaction, but he concluded from the test that futures worked. Monfort had tried and failed to speculate on the basis, specifically the subtle difference between real cows and calculated ones. Delivery was evidently possible, but it was so impractical and unpleasant for the producer that cattle’s poor adherence to the fungibility, deliverability, and storability principles probably helped the futures market train behavior. In the first two years of trading, only “13 contracts in every 10,000 transactions were terminated by the delivery of live cattle.”Footnote 143 That meant cattle hedgers delivered on 0.001% of contracts compared to 2% for all previous storables. The converted Monfort concluded that “it would be silly for us […] to figure out how much it would cost to market steers in Chicago, since we never ship them there. We use as a basis the historical average difference between the Chicago and Greeley market.”Footnote 144 In other words, Monfort advocated for following the model and pretending delivery was a calculable abstraction that would never happen in reality.

Despite his keenness to sell the first paper cattle, Waldner soon became worried that cattle producers were rushing into the market too quickly. By June of 1965, enthusiasm for futures had driven cattle prices up two dollars per hundred pounds. Despite being “financially refreshing” for producers, who were now rushing to join the market, Waldner called it “abnormal” and “dangerous!” “The descent from a rapidly achieved peak position” for cattle producers, who did not fully understand the market, would be “treacherous.”Footnote 145 It was made worse by the fact that many producers complained that they were being pushed unwillingly into futures to secure credit. It was widely reported to cattle producers that banks would be “more willing to advance credit against hedged inventories than against those that are not protected by hedging,” but lenders’ interest in futures was uneven.Footnote 146 “To my amazement,” Waldner found after months of research, “no bank had a defined loan policy nor was any bank prepared to alter its customary loan policy to accommodate ‘hedged’ cattle.”Footnote 147 Nonetheless, individual lenders were experimenting. In the 1960s and 1970s, larger national banks were moving increasingly into rural lending, and they, in particular, encouraged futures. An executive of the Bank of America said, for example, “we enthusiastically endorse the idea of price insurance as it is evolved by producers’ [sic] through live cattle futures contracts.”Footnote 148 This was despite the bank’s recent “financially disastrous” experience of “poor advice, inadequate timing, incomplete counseling, and certainly, indecisive action” for its borrowers using futures.Footnote 149 Nancy Espy, a Montana producer and Chairman of Women in Farm Economics (WIFE), surveyed bankers in the early 1980s and found many had abandoned their support of futures. One banker “said he was scared to death every time he read accounts of manipulations in the futures because he felt a great deal of responsibility for those clients that he had encouraged to go ahead and […] hedge their cattle.”Footnote 150

Whether drawn in by the pull of high prices or the push of cheaper debt, producers began to sour on futures. A poll in Livestock Weekly in April 1981 found that 96% of respondents believed futures trading was harmful to the cattle industry.Footnote 151 A more representative ANCA survey of its membership in 1980 revealed a roughly clean split between those who saw futures as useful or abhorrent.Footnote 152 The US Congress held heated hearings on cattle futures in 1979 and 1982. Iowa Representative Neal Smith provoked the latter hearings after submitting his findings that small traders (mainly hedgers) lost $115.5 million to large traders (speculators and firms) over 16 months. In Smith’s analysis, “the cattle futures contracts still fail to meet minimum requirements necessary to make them a justifiable economic tool and as presently constituted, they do more harm than good to farmer-feeders as a whole.”Footnote 153 A vocal share of producers agreed, foremost Espy. Espy surveyed producers broadly and found only regret: “One of them said he had used them one time and lost his shorts and that was it; he was through.” Another told her “the psychological affects [of futures losses] on himself and his family were more than he would care to go through again.”Footnote 154 Some producers claimed that they attended CME seminars and tried to learn the models and do it properly. “After amassing this evidence and studies and experience of others,” Victor Tomka remembered, “I began in earnest to hedge cattle futures,” but only a small handful of the hundreds of contracts he sold allowed him to “break-even” on his animal investment.Footnote 155 The most damning accusation was that cattle futures prices were leading wholesale prices and producing a “systematic downward bias” against hedgers, which was the exact opposite of how they ought to work in the models.Footnote 156

Cattle futures survived these challenges because an equally forceful minority of producers spoke on their behalf. Paradoxically, these producers mostly did not conform to model hedging.Footnote 157 Early in the contract’s history, Luverne producer Howard Schmidt spoke positively of futures after his experience having “played it on the long side.”Footnote 158 That meant Schmidt bought cattle futures in anticipation of rising wholesale prices probably at the same time that he invested in feeder cattle leading to a double payout. Early hedging models were designed for feedlot operators, but in 1966, Harris observed that “cow-calf people” were also active in the market, and they, in particular, participated “sometimes speculatively.”Footnote 159 The CME’s 1967 survey found that cattle producers held 46% of long contracts and 53% of producers elected to register as speculators instead of hedgers.Footnote 160 The propensity for cattle producers to go double-long in direct contradiction with model hedging became known to CME insiders as the “Texas hedge.”Footnote 161 Eventually, it also emerged that meatpackers were selling futures, which was double-shorting, or a reverse Texas hedge.Footnote 162 The CME and other exchanges learned that producers and other commodity handlers wanted to speculate and were capable of collectively agreeing on prices without the strict need for delivery to work materially.

Waldner certainly hedged at least a few contracts because he had an intricate understanding of the model and he aimed to test it, but he admitted that speculation attracted him more. Waldner believed cattle feeding was inherently speculative, but feeders could only benefit if prices were rising and they had capital to invest in cattle. Speculating on futures meant they could deal huge volumes on margin, and even bet against the price of cattle if they wanted. The futures speculator dreamt Waldner, “need hire no labor; ameliorize no equipment; repair no fences; have no ‘vet’ bill; wade through no mud; undergo no death loss; suffer no ‘cost of gain’ squeeze; mend no broken water lines in the sub-zero winter;” or “be constantly plagued by ‘something else’ going wrong; ad infinitum.” The speculator “need only remain warm, dry, and comfortable, and astutely cognizant of market conditions.”Footnote 163 Speculation would have appealed to cattle producers because they had reason to believe they knew cattle prices better than anyone, and cowboys like to gamble. The old populist narrative argued that urban speculators were grifting farmers, and the Smith report rehashed that, but the successful minority of producers were likely joining with the CME locals to exploit an expanding population of dupes.

The perspective of cattle producers offers several important qualifications about the financial revolution of 1964 and the performativity of derivatives markets. First, living cattle were not quite like grains, but neither were they nonfungible, nonstorable, and nondeliverable in the absolute sense portrayed by economists and exchange leaders. Nonstorability became a practical reality enacted in the material world of stockyards and fines. Anticipating Sandor’s T-Bond, producers treated Chicago cattle futures like a “fictional proxy” for their own local markets, which helped cattle futures function as if truly nondeliverable. Second, hedging models in producers’ hands had performative and counterperformative effects. They molded the market in their image of nonstorability, or rather exclusively calculable storage and delivery, but they failed to produce a market in which true hedging was sufficiently profitable. Texas hedging emerged as the exact contradiction of model hedging. In a broader sense, agricultural producers registering as hedgers for the purposes of clandestine speculation and exploitation of general-public traders represented the total repudiation of the modeled vision for socially justifiable derivatives trading. Hedging is still important to derivatives markets, but cattle producers helped make it strictly voluntary.

Conclusion