Congo’s Minerals or Rwanda’s Resource Nationalism?

This chapter describes the evolution of the minerals sector in Rwanda, both its domestic mining sector and the trade of minerals from the neighbouring DRC. Rwanda’s domestic minerals sector has received little attention when compared to the minerals sector in the DRC. Both Rwanda and the DRC are located on the same Central African Kibara orogenic belt. This belt extends from Katanga in the south to southern Uganda in the north. Most of Rwanda’s mineral production comprises the 3T minerals: cassiterite (or tin), wolframite (or tungsten), and columbite-tantalite (coltan or tantalum). Other minerals include gold, beryl and gemstones, including sapphire. The overarching ambition of the RPF’s domestic minerals strategy is to maximise revenues from its domestic mining sector through ensuring exploration precedes extraction and promoting large-scale sustainable mining.

Trading minerals from mineral-rich Eastern DRC has benefited Rwanda’s domestic economy through providing access to foreign exchange revenues. However, Rwanda’s involvement in the DRC since the 1990s has numerous motivations aside from trading ‘conflict minerals’ (Stearns Reference Stearns2023; Vogel Reference Vogel2022; Vogel & Raeymaekers Reference Vogel and Raeymaekers2016). Yet international press, as well as multilateral agencies, donors and humanitarian agencies, all focus on a single cause of conflict: control over minerals. This resonates with the popular arguments of Collier and Hoeffler (Reference Collier and Hoeffler2004), who tested whether civil wars were caused by ‘greed’ or ‘grievance’. Collier’s work relied on the logic that if individuals were driven by self-interest and rational choice, they might be driven to violence (Cramer Reference Cramer2006).

Both ‘greed’ and ‘grievance’ are important drivers of conflict. However, rather than viewing them independently, motives of conflict must be examined in the context of historical social relations and how the greedy manipulate the grievances of others (Keen Reference Keen2012). The conflict in the Kivus is rooted in local tensions that originate from the colonial era. Motivations of Rwandan elites have transformed since the Congo Wars began. Groups of elites maintain different loyalties and interests. Operating within the same military commercial networks may force loyalty to a centralised authority but also contribute to friction among elites within the political hierarchy. In addition, commodities other than ‘conflict minerals’ are traded in the Kivus. Actors in the region have also profited from trading coffee, timber, food and fuel.

The RPF’s own defensive narrative clashes with the narrative in the international press. The RPF accuses the international press of neglecting the long history of interaction among communities in the Kivus, the need to protect the Banyarwanda population in the Kivus and the presence of Hutu militias (FDLR). In recent years, RPF officials have argued that the government deserves credit for the revitalisation of the domestic minerals sector.Footnote 1

Think about this in terms of our history. There is a long history of interaction of our communities. You could even say that parts of Eastern DRC are actually part of Rwanda … For us, security is the number one issue. When it comes to FDLR in DRC, that government is incapable of doing anything. We have lost one million people in three months because of those people and they continue to kill others in DRC. Others are so arrogant that they have forgotten this event. But in Rwanda, we have to counter any genocide … After the Dodd-Frank Act, others thought that Rwanda is finished now. But it has actually made Rwanda more stable. They have helped us send the message that Rwanda does not depend on the illegal exploitation of minerals. Now, investors can no longer blackmail us that they would rather trade minerals than invest in the domestic minerals sector. Soon, we hope that we will no longer have to export raw minerals to Malaysia and we can export finished products here.Footnote 2

The Rwandan government has been repeatedly criticised for its interference in the DRC, primarily for its support of rebel groups in the DRC. Since the early 2000s, donors have periodically suspended or cancelled aid. In late 2012, fighting broke out between the M23 (a rebel group linked to the Rwandan government) and the Armed Forces of the Democratic Republic of Congo (FARDC). Donors accepted the arguments put forward by civil society organisations, particularly arguments related to the trading of minerals being the key motivation for conflict. With the passing of Section 1502 of the Wall Street Reform and Consumer Protection Act (Dodd–Frank 1502), global civil society groups succeeded in introducing legal obligations for firms registered with the Securities and Exchange Commission to disclose supply chains for certain minerals to verify if they originated from the DRC, and if so, whether they are financing conflict. Later, the EU introduced a voluntary conflict mineral regulations scheme and the UN and OECD developed due diligence guidelines on sourcing natural resources in high-risk areas such as the DRC (Radley & Vogel Reference Radley and Vogel2015). The Dodd–Frank Act was widely criticised in the years that followed. One major concern was that it restricted its definitions of conflict financing to the activities of non-state armed groups (Vogel & Raeymaekers Reference Vogel and Raeymaekers2016). Such definitions absolved the FARDC, the DRC’s army, of any responsibility in the violence. The FARDC was also guilty of financing conflict through trading minerals, as well as the extreme levels of sexual conflict that Dodd–Frank sought to reduce (Baaz & Verweijen Reference Baaz and Verweijen2013).

The previous phase of aid cuts and the Dodd–Frank Act had a limited effect in resolving the conflict (Vogel Reference Vogel2022). However, they did contribute to political and military re-shuffles within Rwanda, as well as increased public confrontation with prominent domestic capitalists (like Rujugiro). The period after aid cuts was a ‘critical juncture’ in Rwandan politics that contributed to elite frictions and significant political upheaval. It showcased the increased reliance on Congolese minerals as a source of foreign exchange. It also highlighted how the RPF feared reprisal from within its military, especially mobilisation among military officers who lost benefits from trading networks in the DRC. Some military officials also gained substantial holding power through past military involvement or the power they enjoyed through their position in trading networks. The chapter describes how Rwanda’s reliance on DRC’s minerals and its broader involvement in the DRC is a double-edged sword. Rwanda’s involvement in the DRC has the benefit of providing immense and much-needed revenues. Yet Rwanda’s involvement is also a threat to the RPF ruling coalition as other elites stand to accumulate personal wealth outside centralised control, as well as gain power and loyalty through their enhanced importance in military and commercial networks.

Though many harbour doubts about the existence of Rwanda’s domestic minerals sector, the chapter shows that the RPF has made some progress in transforming the sector (though clearly, its imports from the DRC far exceed domestic mineral extraction). The RPF government has focused on increasing domestic production and adding value by processing minerals (beneficiation). However, the government (with insufficient expertise, funding and skills) faces challenges in ensuring that policies are geared in line with long-term objectives because it has experienced difficulties in disciplining and monitoring private companies.

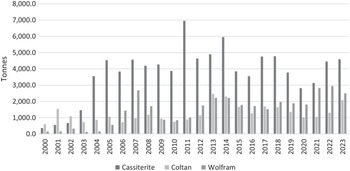

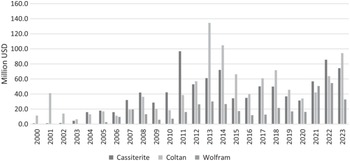

Figures 7.1 and 7.2 detail the evolution of Rwanda’s key domestic minerals, which are often referred to as 3T – tin (cassiterite), tantalum (coltan) and tungsten (wolfram). In the early 2010s, there was a surge in volume and value of traditional 3T minerals exports. However, more recently, new minerals have appeared in official export statistics, raising the total value of minerals exported in 2022 to 772 million USD and over a billion USD in 2023. Gold has been the most significant contributor to Rwanda’s mineral exports since 2019, amounting to more than 500 million USD in 2022 and 2023 (Twum Reference Twum2022). Nearly all gold is exported to the UAE, and some is processed at a new gold refinery in Rwanda. Zirconium, niobium and vanadium have also contributed significantly to Rwanda’s minerals exports in recent years. Observers, including the United Nations Security Council Group of Experts (UNSCGoE) have questioned the source of these minerals, highlighting that Rwanda is yet to extract most of its gold reserves domestically. Additionally, the UNSCGoE has suggested that gold exports have been underestimated, with the UAE reporting a much higher amount of gold imported from Rwanda than Rwanda reported to have exported to the UAE (UNSC 2019).

Volume of Rwanda’s cassiterite, coltan and wolfram exports: 2000–2023.

Value of Rwanda’s exports of cassiterite, coltan and wolfram: 2000–2023.

Rwanda’s trade deficit means that the foreign exchange provided by re-exporting minerals from the DRC has been invaluable for the national economy. However, at the same time, dependence on DRC’s minerals (and particularly the negative publicity it provides) threatens Rwanda’s goals of presenting itself as a Pan-African services hub on the continent.

The Political Economy of Mining in Pre-1994 Rwanda

Rwanda has historically been a conduit for trading minerals that originated from the Eastern DRC (MINIRENA 2010). Since the colonial era, minerals from the Eastern DRC were usually transported to Dar es Salaam or Mombasa for export. As a result, some minerals had to pass through Rwanda. However, there was always some domestic mineral extraction during the Kayibanda and Habyarimana governments. The first geological investigations were conducted in 1909 during German colonial rule (MINIRENA 2010). Investments by the colonial administration were motivated by the success of Union Minière du Haut Katanga in present-day DRC, which had begun to prosper after initial difficulties (Buelens & Marysse Reference Buelens and Marysse2009). In 1925, cassiterite was discovered in Rwanda. Concessions were opened for prospecting only in 1927 after delays in establishing mining legislation (Hillman Reference Hillman1997). Unlike in Katanga in the DRC, there was no dominant charter company. Concessions were allocated competitively in Rwanda. This meant that it was difficult to mobilise capital to invest in geological investigations. The largest concession in Rwanda was allocated to a commercial house, which was owned by Belgian settlers, Compagnie du Kivu, which later became Société Minière de Muhinga et de Kigali (SOMUKI). Other initial concessionaries consolidated their holdings to establish Société des Mines d’Etain du Rwanda-Urundi.Footnote 3

Minerals were first exported out of Rwanda in 1928. The first mining code was established in 1938, which detailed the provision of concessions, as well as allocated licenses for research, exploration and extraction. Cassiterite was the most widely extracted mineral in Rwanda, dominating exports. Many mining sites were developed during this time. However, very few of these mines were large-scale industrial mines.

The relationship of mining and development is ‘contentious and ambiguous’ (Bebbington et al. Reference Bebbington, Hinojosa, Bebbington, Burneo and Warnaars2008). The sector is associated with positive attributes such as the potential to generate large profits. However, it is also tainted with a reputation for appalling labour conditions, environmental degradation and spectacularly unequal distributions of income between companies and their miners. The establishment of mines in Rwanda and in neighbouring countries provided benefits for mining companies, opportunities for peasants as well as new forms of exploitation. Through opportunities in the mining sector, many peasants escaped forms of forced labour. However, SOMUKI’s low wages and appalling working conditions were likened to ‘the mining methods of the Pharaohs’ (Hillman Reference Hillman1997, p. 163). Yet compared to the coffee sector, mining provided an opportunity ‘at independence’ (Bezy Reference Bezy1990, p. 22). Many leaders of early Hutu protest activity in the 1950s were former contract wageworkers in the mining sector (Newbury Reference Newbury1988).

After independence, Kayibanda’s government attempted to secure some control over the domestic minerals sector. In 1963, he repealed the colonial mining code. The colonial mining code gave companies sole ownership of mining operations within their concessions. Repealing the code was part of the government’s strategy to make artisanal and small-scale mining (ASM) the core of mining operations. In line with his ‘peasant-focused’ ideology, Kayibanda gave ‘small’ miners free access to concessions and tried to bring all unexploited concessions under government control. Total annual production remained low at around 2,000 tonnes during Kayibanda’s reign (Uwizeyimana Reference Uwizeyimana1988). During this time, mining firms did not make any new investments. However, firms established basic infrastructure for workers such as footpaths around mining sites, which are still intact today.Footnote 4

Habyarimana’s government advanced further than Kayibanda in gaining control of mining concessions. Habyarimana worked with Jean-Louis Van Den Brande, the new president of Géomines (which owned SOMUKI and GEORWANDA), to transform the domestic minerals sector. Their leadership led to a ‘spectacular change’ for the future direction of the minerals sector (UNECA 1984, p. 50). Concessions and resources of various mineral operators were amalgamated (Uwizeyimana Reference Uwizeyimana1988). Concessions were bought from other operators and merged under a single company – SOMIRWA. Belgian-owned Géomines owned 51 per cent of the company’s share capital and provided management expertise. The government retained 49 per cent of shares.

SOMIRWA became the dominant firm in the mining sector, processing the ore produced in its own mines, as well as buying ore from small miners. SOMIRWA initiated ‘subcontracting’ labour arrangements, which persist as the dominant labour arrangement in the sector today. Under these ‘subcontracting’ arrangements, SOMIRWA organised rural labour by providing miners with access to concessions and controlling commercialisation (trade and export). Local entrepreneurs and landowners (exploitants) organised artisanal miners into working teams and paid them according to their production (Perks Reference Perks2013). However, permit holders and national operators were financially constrained and could not develop their mineral deposits. Miners suffered due to low wages under a backdrop of unenforced mine and labour standards, fluctuating international prices and ineffective government regulation (Perks Reference Perks2013). Theft and smuggling persisted. Middlemen took advantage of sporadic and inconsistent governance, aware that miners would sell their products to the highest bidder.

SOMIRWA was the largest employer in Rwanda. It directly employed over 2,500 miners and over 7,500 wageworkers (Bezy Reference Bezy1990). During most of the 1970s, SOMIRWA maintained direct employment on its large concessions, while using the subcontracting model on smaller deposits. However, as prices fell in the 1980s, SOMIRWA favoured the subcontracting model rather than directly employing miners.

Like Rwandex in the coffee sector, SOMIRWA held monopolistic control over trade and export operations in the mining sector. The differences between prices offered at the London Metal Exchange (LME) and the prices SOMIRWA offered to miners domestically were shared as profits between the government and Géomines. However, there were several groups further down the chain that distorted the market, that is, informal comptoirs (exporters) or negociants (traders). These groups encouraged the creation of ‘informal’ mineral networks outside the formalised chain. Most artisanal miners suffered during the commodity crises that followed in the 1980s. SOMIRWA reacted to the fall in tin prices by reducing the prices at which they bought minerals through subcontracting arrangements.

Minerals were a valuable source of foreign exchange during the 1970s and 1980s. The minerals sector was second only to coffee, representing approximately 20 per cent of total exports. Export receipts were buoyed by high international tin prices, with the tin price at $8.2/ton in 1974, $10.7/ton in 1977, and $17.2/ton in 1980 – in comparison to $6.9/ton in 1989 (Bezy Reference Bezy1990).

In 1977, the government introduced plans to build a smelter to process cassiterite ore produced in Rwanda. Such attempts at value addition were relatively rare across African countries. Though it showed signs of a long-term ‘developmental’ ambition, others argued that the construction of the smelter was undertaken primarily to take advantage of rising global tin prices.Footnote 5 Since Belgian owners showed little interest in the investment, the government retained sole ownership of the smelter (UNECA 1984). The smelter was built in 1981 in Kabuye (15 km from Kigali) at a total cost of 8.9 million USD. The construction of the smelter was financed by a loan from the European Investment Bank (2.7 million USD) and SOMIRWA’s own cash reserves (6.2 million USD) (World Bank 1985). Despite the impressive infrastructure that was built, the smelter never yielded profits.Footnote 6 The supply of minerals never matched the 3,000-ton capacity of the smelter (only 25 per cent in 1983).Footnote 7 Heavy losses hit SOMIRWA in the early 1980s. Losses amounted to 2.2 billion RwF in 1984 before the company finally went bankrupt in 1985 (Bezy Reference Bezy1990).

Géomines closed operations in Rwanda in 1985. After that, the government acted as a caretaker for concessions. After the European Economic Community expressed concerns about Rwanda’s subcontracting model, particularly regarding smuggling and poor working conditions, the government organised the establishment of a cooperatives federation, Union National des Coopératives Artisanales Minières et Rwandaises (COPIMAR), in 1988. COPIMAR generated profits almost immediately through buying and selling the production of its members (Perks Reference Perks2013).Footnote 8

The Habyarimana government struggled to reduce the trade deficit and find new sectors for the accumulation of rents in the 1980s. The mining sector’s inactive concessions presented an opportunity to solve these problems. In January 1989, Régie d’Exploitation et de Développement des Mines (REDEMI) was formed to operate the former SOMIRWA concessions. REDEMI operated in a total area of 104,000 ha with a capital of 97 million RwF (GoR 2010). Habyarimana reactivated the defunct concessions ‘from the ashes’ (UNCTAD 2006, p. 61), ignoring donor advice to ditch the old subcontracting model. Habyarimana’s government reacted by increasing the unit price for minerals produced through subcontracting arrangements, maintaining a state monopoly of in-country buying and limiting export contracts to one or two international buyers (Perks Reference Perks2013).

The Habyarimana government’s structural vulnerabilities motivated increased investments in mining, with REDEMI and COPIMAR increasing production substantially in 1989 before production waned in the following years. Elites retained control of revenues in the minerals sector. Trusted government official Jean Bosco Bicamumpaka, who served as REDEMI’s first director, and other Gisenyi elites served as directors at mines. Jean Mburanumwe, the president of COPIMAR, worked closely with Protais Zigiranyirazo (a lead figure in the akazu) during the genocide (ICTR 2008).

Habyarimana invested in the construction of a tin smelter and negotiated some national control of the domestic minerals sector. However, policies were focused on the short term, with the goal of extracting profits for elites. There was no long-term strategy of maximising production and exports from domestic mines. He installed loyal government officials at SOMIRWA to ensure he retained full control over mining revenues. Investments in REDEMI in 1989 may have provided some respite for Habyarimana. However, by 1993, REDEMI was on the verge of bankruptcy, losing 50 million RwF a year (EIU 1993). The RPF government’s policies are strikingly different when compared to those of its predecessors, departing from a short-term focus (but also less directly focused on empowering ‘small’ miners) and more focused on maximising long-term mineral revenues.

Rwandan Mining in the Shadow of the Eastern DRC

The Congo Wars

There is a popular view among segments of the international press, transnational NGOs and critics of the Rwandan government that the RPF remains involved in the DRC purely out of economic interest and that the FDLR’s presence is minimal and does not represent a salient threat. For example, some prominent scholars (Reyntjens Reference Reyntjens2009, p. 226/227) argue that RPF presence in the Kivus is motivated by the ‘need (of the Rwandan elite) to maintain a lavish lifestyle and possess a large and efficient army’. The RPF often argues that the Rwandan government has no connection to armed groups in the DRC. When they do admit their presence, they argue that they are there for their own national security or to protect Banyarwanda groups in the Kivus, which are threatened by the FARDC and rebel groups like the FDLR. For example, one RDF official argued:

None of this is about minerals. There is a history here. The boundaries themselves have been artificially drawn and why don’t you talk about the FDLR and the way it kills people in the DRC?Footnote 9

This section highlights that the RPF’s involvement in the Kivus is not purely motivated by economic interests. The RPF’s ideological foundations, as well as its elite cohesion, is maintained through a public commitment to protecting Tutsis in neighbouring countries and through tackling the external threat posed by the FDLR and its allies. Even though the Rwandan military is far better resourced than the FDLR, an alliance between the FDLR and the FARDC presents a significant danger, especially if there is external support from other countries. For the Rwandan government, the strengthening of FDLR-allied groups represents an existential threat to its ideological goals and its own security.

The RPF’s initial involvement in the Congo Wars was mostly motivated by national security interests and the need to counter the power of its enemies (including ex-FAR soldiers). The RPF highlighted the strengthening of Hutu militias in refugee camps outside Rwanda and the funding received by camps from donors.Footnote 10 Former Interahamwe and ex-FAR soldiers controlled these camps and launched infiltrations into Rwanda almost immediately after 1994 (Prunier Reference Prunier2009). RPF cadres rebuilt national identity and elite cohesion through highlighting a clear enemy: the retreating Interahamwe (and its allies). Mobutu’s decision to harbour genocidaires made the Congolese government an enemy of the RPF. Kagame led a coalition with Uganda, Burundi and Angola to fight Mobutu’s forces, the retreating Interahamwe and their allies. When the First Congo War began in September 1996, extracting mineral revenues was not the primary motivation.

In 1997, the forces led by the Alliance of Democratic Forces for the Liberation of Congo-Zaire (AFDL), supported by Angolan, Rwandan and Ugandan troops, installed Laurent Kabila as the new president of the DRC. In 1998, Kabila reacted against Rwandan control by sending many of his Rwandan supporters home. Rwandan military general James Kabarebe was fired from his post as Kabila’s first Chief of Defence Staff. Kabarebe retaliated by launching a military effort against the Congolese government and took control of the Kivus in forty-eight hours (Prunier Reference Prunier2009).Footnote 11 From then on, neighbouring countries and the rebel groups they supported fought over control of the Kivus. Commercial networks developed around the trade of minerals such as coltan, tin, diamonds and gold; agricultural goods such as coffee and timber; and the control of land. Initially, these commercial networks were developed to pay for continued military efforts. Kagame himself described it as a ‘self-financing war’ (Jackson Reference Jackson2002, p. 528).

Rwandan interests were slowly transformed to what Jackson (Reference Jackson2002) called an ‘economisation of conflict’ where actors reoriented their goals to create profitable opportunities. However, in line with the RPF’s ideological paradigmatic goals of self-reliance, profits obtained from commercial networks were highlighted as being reinvested in line with national priorities, rather than to make elites rich. United Nations Security Council (UNSC 2001) reports and Vlassenroot and Romkema (Reference Vlassenroot and Romkema2002) observed that Rwandan commercial networks were disciplined with strict centralised control from Kigali.Footnote 12 Even the most disciplined ‘ideological’ project, as Stearns (Reference Stearns2011, p. 301) calls Rwanda’s incursion into the DRC, had contradictions. Discipline was never applied universally. Individual military and commercial elites made profits, and many were punished for doing so. Some military figures even argue that anyone in the military who confronted RPF senior leadership was later falsely accused of benefiting illegally from DRC.

Ultimately, it is a war and many people made money. You only get punished if the President gets angry or someone close to him wants to make problems for you.Footnote 13

Alliances constantly shifted in the Kivus. However, Rwandan-supported groups were often opposed by groups that mobilised on anti-Tutsi sentiment. Reyntjens (Reference Reyntjens2005) describes how mai-mai militias (who had previously fought Kabila) later aligned with the FARDC to form an ‘anti-Tutsi’ coalition. Anti-Tutsi rhetoric also assisted Rwandan-supported groups to enlist support, since ‘every anti-Tutsi slur or assault was a reminder of past violence’ (Stearns Reference Stearns, Marysse, Reyntjens and Vandeginste2008, p. 263). Commercial networks trading various goods funded military efforts on both sides. Such networks extracted revenues from mining in the Kivus in different ways. Military and rebel groups engaged in mineral extraction themselves. Military networks invested in shares in mining companies. Militaries and rebel groups provided protection for companies and imposed taxes on local and international actors. Many companies were established primarily in response to the rising mineral prices (particularly coltan). Coltan prices increased about tenfold during the 2000s before a dramatic fall. These companies linked traders, politicians and military officers on the Rwandan side of the border with those on the Congolese side of the border. Rwandan-linked companies included Société Minière des Grands Lacs (SOMIGL),Footnote 14 Rwanda Metals (RM)Footnote 15 and Grand Lacs Metals (GLM). UNSC (2001) indicates thirty-five companies (from several countries) traded minerals through Rwanda in 2001. There are large variations in the estimates of the value of Congolese mineral exports travelling through Rwanda, estimated at between $17 million and $250 million a month (Jackson Reference Jackson2002; UNSC 2001). In 1997, Rwanda’s official coltan exports increased despite very little mining taking place domestically (ibid). Diamonds were officially listed as an export although Rwanda held no diamond deposits (ibid).

Mineral trading networks included international mining companies and prominent regional traders, some of whom were also arms dealers (Cuvelier & Raeymaekers Reference Cuvelier and Raeymaekers2002). The Congo Desk (CD) has been highlighted as the infamous network through which centralised control of the commercial networks of trading minerals and other goods was organised. The CD included many senior military officials who ran military and economic operations in the DRC. In the early 2000s, the CD forced all local diamond traders to sell to a single principal comptoir (trading firm) to establish centralised control over trading networks (UNSC 2002).Footnote 16 This was after a battle in Kisangani between RPA-supported forces and the Uganda People’s Defence Force–supported groups. In this battle, Rwandan General Patrick Nyamvumba led forces that beat veteran Ugandan officer James Kazini. After such military victories, the CD reorganised military and commercial networks with the goal of centralising control over political and economic decision-making. The literature refers to the CD’s control as La Systeme, referring to an ‘informal economy’ consolidated through Rwandan-owned companies or by Rwandan- or RCD-protected companies. La Systeme was organised through providing firms with incentives to join the network, which included reduced business costs, less taxation and limited political interference (Stearns Reference Stearns2013).

Working together in the war effort forged alliances and loyalties among military elites. Many military officials forged relationships through kinship, personal and historical loyalties, with their Tutsi brethren across the border (Longman Reference Longman and Clark2002). Such alliances and loyalties did not necessarily correspond with loyalty to Kagame’s leadership.Footnote 17 Several military officials, including NyamwasaFootnote 18 and Kabarebe, developed significant holding power of their own, with military officials in their charge owing loyalty to them.Footnote 19 Through the war, many RDF officers thus became capable of mobilising support both for and against Kagame, which made their loyalty crucial to maintaining elite cohesion but also meant that they were a potential threat. The prominence of military officials involved in the DRC increased at the time. Kagame was reluctant to cede control of those commercial networks. In some cases, Kagame’s own relatives became directly involved in the DRC. For example, Kagame’s brother-in-law, Alfred Rwigema, was on one company’s payroll. The company in question later briefly began exploration for coltan in Rwanda (Cuvelier & Marysse Reference Cuvelier and Marysse2003).

In 2003, a power-sharing agreement was reached between Rwandan-supported rebel groups and the Congolese government. Rwandan-supported RCD-G was one of several groups that ceased fighting the Congolese government. The agreement required belligerents of the Second Congo War (1998–2003) to be merged into a new national army. The new national army promised to geographically spread military officers and ensure a ‘balanced’ composition within the military ranks (Baaz & Verweijen Reference Baaz and Verweijen2013). The RCD-G dodged attempts at integration and operated autonomously in the Kivus. The RCD-G justified its resistance by stressing the need to protect the Tutsi population in the Kivus. After the agreement, Eugene Serufuli was appointed governor of North Kivu. Serufuli was an RCD member and the former vice president of the Tous Pour la paix et le Developpement NGO, established in 1998. The move to elevate Serufuli, a Hutu, was helpful for the RPF, since the RPF feared the isolation of the Tutsi community in the Kivus. Serufuli promoted himself as a ‘Rwandophone’ leader, organising marches and public rallies protesting the threats Kinshasa directed against both Hutus and Tutsis (Stearns Reference Stearns, Marysse, Reyntjens and Vandeginste2008).

Laurent Nkunda, a former RPA soldier who had fought in the liberation effort, refused to join the Congolese army in 2003. Profiting from the continued support of the Rwandan government and Serufuli, Nkunda reacted to the deal by organising several rebel militias, with the support of other RCD-G dissidents. Nkunda enjoyed popularity among Tutsis in the region for his stance on protecting Tutsi rights (Lemarchand Reference Lemarchand2009). In 2006, Nkunda formed the CNDP on the premise of protecting Tutsis from genocide. Serufuli also switched sides. He began working closely with Kabila while highlighting Tutsis as enemies (Stearns Reference Stearns2013). Rwandan commercial networks were gradually reorganised, since the RPF chose to support Nkunda against Serufuli (Stearns Reference Stearns, Marysse, Reyntjens and Vandeginste2008). Within a few months of its formation, the CNDP became one of the most powerful groups in the DRC in military, political and economic terms (Baaz & Verweijen Reference Baaz and Verweijen2013).

Elements within the CNDP resisted Kigali’s control. Some within the CNDP had ‘uncomfortable and distrustful relations with Kigali’ (Baaz & Verweijen Reference Baaz and Verweijen2013, p. 580). Kigali countered Nkunda’s rise in power in the region by installing Bosco Ntaganda as the new leader of the CNDP in March 2009. Nkunda was then placed under house arrest in Rwanda.Footnote 20 Twelve days after being announced as the new leader of the CNDP, Ntaganda announced joint operations with the Congolese army to fight the FDLR. Ntaganda’s increased wealth and prominence fostered discord within CNDP ranks.Footnote 21 Some even joined other rebel groups. Sultani Makenga, a prominent Nkunda loyalist, was a rival to Ntaganda’s power within the CNDP.

With the reorganised CNDP and through Kigali’s support, Ntaganda’s influence strengthened. Ntaganda worked closely with the RPF, removing Nkunda loyalists and placing his own officers and those chosen by the RPF in positions of responsibility (Stearns Reference Stearns2013). However, tensions continued to grow within the CNDP, as Ntaganda favoured empowering soldiers within his own patronage network above other powerful officers. The Congolese government also countered Ntaganda’s power with increased attempts at reintegrating the CNDP into the army, appeals to Kigali and the mobilisation of the Congolese population on ‘us–them’ rhetoric against Tutsis (Stearns Reference Stearns2012).

In April 2012, the M23 was formed. The M23 officially mutinied because Kinshasa did not respect the 23 March 2009 peace agreement. The mutiny was a reaction from former CNDP officials to the Congolese government’s attempts to constrain its power. After Rwanda was accused of providing support to the M23, many donors withdrew aid. The Rwandan government eventually reacted by withdrawing support for the M23. Though the M23 relied on the RPF for support, the M23 had a tense relationship with the RPF (Stearns Reference Stearns2012). The M23 was not unified. Tensions persisted, with the Makenga and Ntaganda wings even fighting against each other (Vogel Reference Vogel2014).

Supporting rebel groups in the DRC conflicted with the RPF’s long-term goals of becoming an externally dependent services hub. The RPF government was forced to make a choice: continue supporting rebel groups in the DRC and lose the support of Western donors or withdraw support for the M23 and antagonise powerful RPF elites who benefited from commercial networks. Businesspeople, including Rujugiro, had individual interests in the Kivus that were protected by Ntaganda’s forces. Rujugiro’s own decision to exit the dominant coalition can be ascribed to RPF decisions, which threatened his individual property rights. Other businesses, including RPF-owned firms, were engaged in selling goods in the Kivus (Behuria Reference Behuria2015a). Rebel leaders, including Ntaganda, owned cattle ranches in Masisi (Stearns Reference Stearns2012). However, Rwandan and M23 involvement in the DRC was also motivated by the need to protect the Tutsi population in the Kivus. Individual RPF elites held a variety of loyalties and interests in the DRC. Some elites had pushed to withdraw support for M23 much earlier.Footnote 22 Others pushed to continue support for the M23.Footnote 23 The choice to withdraw support from the M23 caused tensions within Kigali.

Of course. These are difficult decisions. We fought alongside some of these people. But it is simple for us. We debate about it and then we reach a decision. Then everyone agrees to that. Once decisions are made, there is no disagreement anymore.Footnote 24

Any analysis that develops the image of a homogeneous predatory elite (Reyntjens Reference Reyntjens2004, Reference Reyntjens2013) or an RPF elite that operates through consensus (Booth & Golooba-Mutebi Reference Golooba-Mutebi2013) is a simplistic characterisation of Rwandan politics. The withdrawal of aid and the RPF’s decision to withdraw support for the M23 had significant consequences, with frictions emerging within the RPF and its key supporters. Several military elites lost profits because of this decision. Rujugiro, who had interests in the Kivus who were protected by Ntaganda’s forces, lost millions of dollars (Stearns Reference Stearns2012). As Chapter 4 documents, the aid cuts also resulted in major political and military reshuffles, as inter-elite rivalry surfaced repeatedly.

Post–Dodd–Frank and the Reorganisation of Rwanda’s Kivu Trading Networks

After legislations such as the Dodd–Frank Act were signed into law, there was a long delay in introducing traceability schemes through iTSCi, the bagging-and-tagging system for minerals. iTSCi is managed by the International Tin Association (ITA), formerly the International Tin Research Institute (ITRI), the body of the international tin industry, which is responsible for legal trade in tin, tantalum and tungsten (3T) minerals. In the early 2010s, only those mining states that were certified by iTSCi could export 3T minerals. By 2014, only a small proportion (about 40 out of more 900 in South Kivu alone) of mining sites retained legal access to global markets (Radley & Vogel Reference Radley and Vogel2015). iTSCi was accused of consolidating a monopoly in the traceability market, working against the growth of rival schemes such as Better Sourcing (Huggins Reference Huggins2023). Local producers and traders were confronted with a choice of either paying a fee to iTSCi or operating illegally by bypassing the traceability schemes (Cuvelier et al. Reference Cuvelier, Van Backstael, Vlassenroot and Iguma2014). iTSCi effectively operated as a ‘closed pipeline’, controlling and determining the legality of 3T production in space and time while controlling who participated in the value chain (Huggins Reference Huggins2023). Scholars (Deberdt Reference Deberdt2022) have reported that the region’s black market in minerals was bolstered, inadvertently boosting the system against which it was installed to fight. During that time, there was also a significant increase in Rwanda’s minerals exports. There were varied explanations of this. Some argued that Rwanda-based comptoirs had stockpiled minerals beforehand.Footnote 25 Others argued that the tagging system was beset with corruption and mismanagement, with minerals from the DRC being smuggled into Rwanda, where they were tagged and exported as Rwandan production (UNGOE 2020).Footnote 26 Most district officials and individuals responsible for tagging minerals were alleged to be complicit in smuggling.Footnote 27 Others highlighted that Rwanda-based comptoirs were willing to pay higher prices to Congolese miners who would sell their products to them (Atanasijevic Reference Atanasijevic2016). A systematic analysis of iTSCi’s tagging system highlighted the difficulties of enforcing conflict-free certification in the region (Postma et al. Reference Postma, Geenen and Partzsch2021). Several companies were blacklisted, and the Rwandan government also often acted against firms that were blacklisted. Yet a large share of DRC minerals still gets exported as conflict-free certified through Rwanda.

In 2013, Ntaganda voluntarily surrendered by presenting himself to the US Embassy in Kigali. After military defeat in December 2013, the M23 signed a peace agreement with the DRC government, with M23 leadership fleeing to Rwanda and Uganda. M23 demands were the same as the demands of previous Rwanda-affiliated groups: guarantee a safe return to DRC for M23 membership, end discrimination against Congolese Tutsi and encourage the return of Congolese Tutsi who have been displaced to neighbouring countries (Verweijen & Vogel Reference Verweijen and Vogel2023). For the next few years, there was an apparent thawing of relations between the DRC and Rwanda (although occasionally tensions did flare up). When Felix Tshisikedi became the president of the DRC in 2019, he initially collaborated with Rwanda, with the two countries working together in anti-FDLR operations (Verweijen & Vogel Reference Verweijen and Vogel2023). While Makenga returned from Uganda in 2017, his forces did not go beyond controlling a small area between DRC’s volcanoes.

During this time, Rwanda had begun to make inroads in its broader strategy of becoming a ‘hub’ for trading activities in the Kivus. As has been discussed, a major part of this strategy was to become a major exporter of agricultural and other products to the Kivus, with significant success in the trade of cereals, horticulture and other agricultural items. The Rwandan government had successfully managed to consolidate its position as the hub through which minerals (from the DRC) were traded (amid continued competition with Uganda), with significant increases in gold exports in the late 2010s. Politically, however, the Rwandan government continued to have difficult relationships with its neighbours. While its relationship with the DRC had thawed, Rwanda–Uganda relations had soured significantly, and there were tense relations with Burundi (Bareebe & Khisa Reference Bareebe and Khisa2023).

In late 2021, tensions between the re-mobilised M23 and the Congolese army flared up again. As Vogel (Reference Vogel2024) writes:

Private security companies and neighbouring states have joined the fray, and the diffuse range of belligerents has galvanized along two clear fronts: one aligned with the Congolese government, the other with the M23.

Rwanda was widely accused of being responsible for the M23’s resurgence. The Congolese government argued that the Rwandan government transferred arms and ammunition to the M23, facilitated recruitment and was even involved in direct combat. Congolese leadership also accused Rwandan elites of continuing to destabilise the Kivus to extract minerals worth billions of dollars annually (Chatelot Reference Chatelot2024; Wilson & Schipani Reference Wilson and Schipani2023). The M23 argued that the DRC government failed to deliver on their 2013 agreements. The Rwandan government denied involvement but argued that the DRC was supporting a terrorist group (FDLR) and was endangering the lives of the Congolese Tutsi community in the Kivus. While some observers recognise the FDLR as ‘a genuine security threat’ (Verweijen & Vogel Reference Verweijen and Vogel2023), there are also deeper concerns within the DRC that the Rwandan government sees the Kivus as part of a ‘Greater Rwanda’. The ‘Greater Rwanda’ version of history aims to legitimise Rwandan claims to parts of the Kivus. The ‘Greater Rwanda’ version of history presents the pre-colonial Rwandan kingdom as extending into parts of present-day DRC, including where Kinyarwanda-speaking populations lived (Mathys Reference Mathys2017).

The DRC government has complained about how Rwanda’s economy has benefited from its broader ‘hub’ strategy, using the DRC both as a market and for trading DRC minerals through Rwanda. To counter this, the DRC government has signed direct sales agreements with Emirati buyers to sell gold directly to them and reduce the minerals traded through Rwanda-based traders (Wilson & Schipani Reference Wilson and Schipani2023). The DRC became the newest member of the EAC, supported by regional allies. However, there are dangers that this will increase smuggling because of the lack of tax harmonisation across the region (Byiers et al. Reference Byiers, Kakare, Golooba-Mutebi, Nkuba and Karuta2023; Verweijen & Vogel Reference Verweijen and Vogel2023). The DRC government criticised the EAC Regional Force, which was employed to stabilise the Kivus. It was replaced by the Southern African Development Community (SADC) Forces, which the Rwandan government distrusted. As of December 2024, the United States had gone further than other external observers in suspending all military aid to Rwanda and attempting to broker a ceasefire in December 2023 (Stearns & Walker Reference Stearns and Walker2024). The United States also sanctioned RDF Brigadier General Andrew Nyamvumba (the former CEO of Ngali and brother of former CDS Patrick Nyamvumba) for collaborating with M23 to attack FARDC locations.Footnote 28 At the time, the United States was Rwanda’s largest donor, providing almost a third of Rwanda’s aid budget. The United Kingdom was more tentative in pressuring Rwanda, especially since it struck a controversial asylum deal in 2022. The European Union, meanwhile, signed a $22 million deal with Rwanda to support RDF deployments in Mozambique and signed a Memorandum of Understanding to support exploration of lithium mining in Rwanda (Stearns & Walker Reference Stearns and Walker2024).

Dependence on minerals from the DRC was a double-edged sword. While providing significant revenues and being central to national security interests, increased reliance on the DRC contributes to the empowerment of certain business and military elites that may prove to be threats in the future. According to some retired RDF officials, recent events forced Kagame to recall several earlier ‘retired’ generals to more prominent positions within the government apparatus – with Kabarebe now back in a more prominent position and former RDF generals being appointed high commissioners abroad.Footnote 29 Thus, domestic mineral investments remains a strategic priority and is central to achieving more economic autonomy, less reliance on domestic military elites and on minerals from the DRC.

But We Have Minerals Too

The RPF government has invested in revitalising its own minerals sector. Chapter 4 describes the evolution of elite frictions within the political settlement. These frictions partially related to Rwanda’s engagement in the DRC and the benefits derived from it. Dynamics within Rwanda’s domestic minerals sector mirrored broader changes within the political settlement. As the RPF sought to centralise control over political and economic decision-making in the first decade of the twenty-first century, actions began to be taken against individuals who had gained power within the RPF and control over rents from the DRC’s commercial trading networks. This included several businesspeople and dissidents, including Nyamwasa and Karegeya (who would later form the RNC). The increased power of certain individuals within the RPF presented a threat to the centralisation of control over political and economic decision-making, which was organised around President Kagame. In the 2010s, after aid cuts, actions were taken against certain elites, highlighting a struggle to centralise control over DRC’s commercial networks and military command. As compared to other sectors, the RPF relied more on foreign investors during the first phase of privatisation and liberalisation of mining assets. However, in recent years, there has been an attempt to use more government-owned or closely affiliated investment groups (particularly Ngali) both in taking over new mining concessions and in investing in beneficiation.

Within Rwanda, domestic mining is largely organised around ASM though the government’s strategic goals are to encourage large-scale mining and to organise artisanal miners into federations, with production organised through the federation. The government has ambitious goals of becoming a processing and beneficiation hub. Investments in processing and beneficiation remain inadequate across African countries despite many announcements across the continent of the need to prioritise gaining more revenues out of African-produced minerals. In line with other experiences elsewhere on the continent, in Rwanda, though new smelters have been built, limited supply continues to hinder beneficiation possibilities.

The minerals sector only recovered to 1970 production levels in 2004. Annual cassiterite exports did not reach the 2,000-ton mark (consistently achieved in the 1970s) till 2004. Gradually, the RPF government has begun to exceed the production levels of preceding governments. Between 2004 and 2012, annual cassiterite exports were between 3,000 and 5,000 tonnes. Since 2006, wolfram exports have exceeded 1970s levels (except for 2008). Coltan exports are at their highest levels in Rwandan history. During the first Congo war, there were surges in cassiterite and coltan exports from Rwanda in some months in 1997 and 1998. Most spikes in exports before 2004 are explained by an increase in minerals traded from the DRC and as a response to global prices. During the coltan rush that started in late 2000, prices rose exponentially from 20 USD/kg in January to about 200 USD/kg in December. Most of the coltan that entered Rwanda originated in the DRC. Government officials recognised that a large share of these exports (in the early 2000s) comprised minerals that originated from the DRC.Footnote 30

Until the early 2000s, the domestic minerals sector was not prioritised. State-owned REDEMI retained ownership of domestic concessions through the 1990s and early 2000s. Very few new mining sites were developed. Labour was organised around two inherited methods – the earlier subcontracting arrangement and local cooperatives. In the 1990s, COPIMAR was relatively active in organising small-scale miners, although many small-scale miners operated independently from it. Government departments were hindered by a lack of expertise. Very few geologists and officials from the previous regime stayed on.Footnote 31 Informal comptoirs operated and their networks were established through security guarantees. Smuggling within Rwanda was likely to have occurred with help from government officials.Footnote 32 As one senior government official put it:

Everything was a mess. We didn’t have any geologists. We still don’t. We didn’t know what minerals were there. There was no governance of the mining sector and in the last few years, we have just been trying to rebuild our governance.Footnote 33

In the late 1990s, in line with broader privatisation reforms pushed by IFIs, the government liberalised mining trade and export, allowing additional firms to operate. The government also began initiating the sales of REDEMI’s mineral concessions. In 2004, REDEMI exported about 60 per cent of Rwanda’s cassiterite. Some of these exports came from the REDEMI-operated cassiterite-processing facility in Rutongo. COPIMAR and Metal Processing Association (MPA), among other companies, were also involved in the production and export of cassiterite (Pourtier Reference Pourtier2004). REDEMI exported most of the wolfram in Rwanda (approximately 65 per cent in 2004). Most wolfram was produced in the REDEMI-owned concession in Nyakabingo. COPIMAR and other companies exported the remaining wolfram (Yager Reference Yager2004). REDEMI operated processing facilities in Gatumba for coltan production. Artisanal miners produced most domestic coltan. Two other comptoirs operated officially, while others operated informally. Aside from Rwanda-produced minerals, all comptoirs, including REDEMI and COPIMAR, re-exported minerals (including smuggled minerals) from the DRC.Footnote 34

In 2004, REDEMI operated eight concessions and received a small amount of production from independent traders who purchased minerals from small-scale miners (Garrett Reference Garrett2008). In total, REDEMI owned twenty concessions, although twelve were not in operation. By the end of 2005, only two concessions that were previously under operation remained under REDEMI control. Investments and joint ventures in the early 2000s were ways for Kagame to reward loyalists. For example, Simba Manasseh owned a local company named Pyramides.Footnote 35 Manasseh’s company was assisted in developing a joint-venture partnership with a Chinese company to build a coltan refinery in Western Rwanda. Manasseh became a representative for Rwandan mining companies and a member of the Value Addition Committee, which was established in 2006.

Initial liberalisation and privatisation were relatively unregulated, with companies invited to bid for concessions on a first-come, first-served basis. A flood of new mining companies was registered in the mid-2000s. The Rwanda National Innovation and Competitiveness Report listed fifty-five private sector companies in the sector in 2005. Companies in the minerals sector comprised 23 per cent of all companies operating in Rwanda (Temesgen et al. Reference Temesgen, Ezemenari and Munyakazi2006). Most of these companies were minor comptoirs that exported small quantities of minerals after buying them from artisanal miners. Licenses for REDEMI’s concessions were also given out on a first-come, first-served basis ahead of the establishment of a mining law in 2009.Footnote 36

REDEMI had no capacity to mine and couldn’t exploit all key concessions. Privatising was the right thing in terms of getting finance but we didn’t get the best of investors. It was difficult because the mining sector was not known in Rwanda.Footnote 37

By 2010, thirty-eight large-scale mining licenses were granted to (almost entirely) foreign investors. These investors were from countries including South Africa, the United States, Germany, Botswana, China and Russia. Most investors obtained vast concessions at low prices. The government struggled to force most private companies to comply with the mining law. Most companies based their business plans on trading first and investing in exploration thereafter. Others were simply there to raise the value of their company by hoping for promising survey reports, and some were waiting for ‘a big discovery’.Footnote 38 The government complained that many large companies did not respect the mining law, giving the example of Natural Resources Development (NRD). NRD operated five concessions and had 110 regular employees, with 1,100 artisanal miners selling their production to the company (Garrett Reference Garrett2008).Footnote 39 NRD was accused of wasting their land and being more interested in trading than extracting minerals from their own concessions.Footnote 40 The government cancelled some concession licenses in 2016. Two American companies filed an international arbitration suit at the International Centre for Settlement of Investment Disputes (ICSID). ICSID ruled in favour of the Rwandan government in 2022, marking a rare case of victory in the dispute settlements court for a developing country against a foreign investor.

We didn’t know the value of our minerals. We gave them on a first-come, first-serve basis. Then we realised we didn’t want to just give away concessions without knowing the value of our mines.Footnote 41

After initial sales resulted in few investments in domestic mineral exploration and extraction, the government chose to alter its mining regulations. Since the 2009 Mining Law, there has been a long-horizon oriented strategy in place for the mining sector. Priority is placed on companies investing in exploration before extraction of minerals and ensuring investors work in line with government priorities of long-term sustainable mining and beneficiation.

Aid cuts in 2012 represented an opportunity to transform the sector. The Rwanda Mines, Petroleum and Gas Board (RMB) has regularly claimed that Rwanda only mines about 30 per cent of its full potential (Sabiiti Reference Sabiiti2023b). To address these challenges, donors and foreign geological survey companies were approached to fund exploration. Between 2012 and 2016, Canadian, German and Australian companies studied and mapped several potential target areas (PTAs). The UK government also funded the Sustainable Development of Mining Project in Rwanda, which interpreted airborne geographical survey data in 2017 that had been conducted by South African, Indian and Russian companies previously. After these surveys were conducted, twenty-three PTAs were then identified, and the RDB worked to find investors for each PTA.

A new mining law was established in 2014, which demarcated access to land at 400 ha each, rather than the immense areas of land earlier designated to companies.Footnote 42 The new mining law also departed from the previous rigid time spans that accompanied the granting of licenses. The previous law only allowed the government to grant five-year licenses or thirty-year licenses. As part of the new law, the government provided more flexible licenses. Both because of increased elite vulnerability and because initial privatisation did not achieve its targets, the government has begun to invest directly (through providing concessions to Ngali, a government-owned firm).

A significant entrant into the mining sector is government-owned investment group, Ngali, which has taken over some concessions – particularly those with significant potential in gold. Another significant initiative has been the establishment of Trinity Mines, which is under the collective ownership of Ngali and foreign investors. Trinity includes three major concessions (Rutongo, Myusha and Nyabakingo mines). It is now one of Rwanda’s largest private employers, employing over 6,300 Rwandans. In the last two years, however, after more exploration was carried out, the government has further redistributed the twenty-three PTAs into fifty-two PTAs and continues to seek investment from foreign investors. Some major headlines have included an announcement in 2023 that Rio Tinto, the world’s second-largest mining company, signed a joint venture with UK-based Aterian and a Rwandan company (Kinunga Mining) to explore lithium in Rwanda.

Yet there continue to be difficulties in disciplining companies to invest in exploration and make use of their concessions. In January 2024, the RMB cancelled seven licenses, including one that belonged to Ngali (a gemstones concession) (Sabiiti Reference Sabiiti2024c). Funding gaps have plagued the sector. As a Rwandan geologist said, ‘In government documents, mining is always lost while it is always first in exports.’Footnote 43 The government has often cited a shortage in mining technicians and geologists as a major impediment. Many private companies also hired the few geologists who were working for the government, leaving the government with fewer geologists. Recognising the void in domestic mining expertise, the government gradually attempted to address skills gaps. The government has invested in developing Rwandan mining expertise. Around fifty students were sent to study geology in the United Kingdom, India, Nigeria and other countries. They returned in 2015. The School of Mining and Geology was established in 2015, and the first cohort of students graduated in 2019.

Almost the entire surface area of the country is covered by licenses. It is a challenge to know if people are actually working. Those ones are the ‘guessers’ – by chance, if something erupts, then they’ll get advantages. We didn’t have clear standards at the time. Earlier, we were managing 40. Then we had 400 so quickly. But we adapted our system.Footnote 44

Though most of Rwanda’s mineral exports can be assumed to be re-exports of Congolese minerals, the RPF has significantly transformed its domestic mining sector. Investments in geological surveys and the prioritisation of exploration before extraction have coincided with increasing government involvement in the sector (through Ngali) and attempts at strategically attracting leading global mining companies (like Rio Tinto). Like in Rwanda’s agriculture sector (Ansoms Reference Ansoms2009), there is a ‘large-scale’ bias in Rwanda’s mining sector, which is also common in other African countries (Hilson Reference Hilson2019). However, most domestic mining continues to be artisanal and small scale. The government’s reorganisation of ASM is discussed next.

ASM Dependence amid Formalisation

Rwandan domestic mining is dominated by ASM. Small-scale miners are a diverse group, with concessions ranging from less than one hectare to over 500 hectares.Footnote 45 Many small-scale miners hold multiple permits. For the last decade, the RPF government has aimed to formalise the mining sector to coordinate domestic production to maximise value through ensuring the processing and beneficiation of minerals domestically.

Our motto is ‘professional mining’. How can we transition from a sector that was dominated by guessing where some people try and see if they can gain something quickly by getting a license? Now, we want people to have plans, have estimates about reserves and then develop the mine … In the future, I don’t see Rwanda having 700 mining companies and 700 sites. We want to merge the smaller sites. Right now, there are five companies on one hill. We want them to make a consortium and produce more. Then we can collect royalty or they can easily send minerals to the smelter.Footnote 46

FECOMIRWA is the key organisation through which the Rwandan government aims to organise ASM. FECOMIRWA was established in 2009, taking over from COPIMAR. It acted as a federation of five regional mining cooperatives. In 2018, FECOMIRWA included twenty-nine registered cooperatives as members. These 29 cooperatives had 749 members, with 4,419 persons hired as either permanent or casual labour. The government encourages all small-scale miners to sell their minerals to FECOMIRWA (but they are not forced to do so and few do). However, FECOMIRWA has found it difficult to compete with comptoirs over the last five years.Footnote 47 Because of the liberalised trade-and-export segment of Rwanda’s domestic minerals sector, miners have retained some freedom to sell their production to rival comptoirs (other than FECOMIRWA). FECOMIRWA representatives also recognised that miners were reluctant to join cooperatives and the federation because they were seen as dominated by ‘big men’.Footnote 48 Fees were perceived to be ‘not worth it’ given that FECOMIRWA often faced financial challenges and could not provide the loans they promised.Footnote 49

FECOMIRWA’s role was to export the production of its members, give loans to its members and provide technical assistance. FECOMIRWA only buys minerals from cooperatives. Individual cooperatives are free to sell their products to other comptoirs, and this has often resulted in competitive pricing between comptoirs. FECOMIRWA officials claim they struggled to compete with other comptoirs in some years because of other social responsibilities, including giving loans to members. They complained of added difficulties, such as the increase in taxes and payments because of recent transparency initiatives.Footnote 50

From the time we started, we have had a decline in production. We give mining cooperatives technical advice and even invested in mining cooperatives. Once the traceability system came and with added taxes, they found situations where if they supplied minerals to us, we deducted our initial investments. Now, other comptoirs compete with us and our miners sell their minerals to them. Our production should be increasing but the environment has meant it has decreased.Footnote 51

The government’s initial model aimed to mimic global extractives policy ‘best practice’, which places emphasis on empowering small-scale miners through encouraging cooperative formation. The government prioritised formalising the subcontracting model used by companies, while also formalising ASM practices through strengthening cooperatives and ensuring official employment contracts, health insurance and payroll taxes. Formalisation provided an opportunity for the government to increase its tax base and reduce ‘informality’, which was perceived as regressive and a threat to efficiency.Footnote 52

The government initially modelled its approach on a romanticised reading of the success of Ghanaian artisanal gold mining and, in particular, the Precious Minerals Marketing Corporation (PMMC). The PMMC oversaw tenfold gold production increases between 1989 and 1997. PMMC acted as a centralised comptoir, facilitating trade out of Ghana. A total of 750 licensed agents purchased from artisans and sold local gold production to the PMMC. COPIMAR (and later FECOMIRWA) was envisioned to have a similar role in Rwanda’s mineral sector. In Rwanda, Perks (Reference Perks2013, p. 733) lauded ‘the spirit of the cooperative, whereby members invest in the operations through contributions and redistribute annual profits’. Despite Perks’ optimism regarding cooperatives in Rwanda, the distribution of profits was unequal between members of cooperatives and wageworkers who were employed by small-scale miners. Joining cooperatives required an initial investment from miners.Footnote 53 Some miners were often forced out of the sector, while others operated informally.

FECOMIRWA had a long-standing arrangement with a Thai investor and sold all its tin exports directly to this investor in Thailand and all its coltan to another investor in Hong Kong. However, these relationships later faced difficulties. FECOMIRWA’s former executive secretary Augustin Ruhigira was jailed in 2017 because he allegedly embezzled 1 billion Rwandan francs. It was difficult to assess the veracity of these claims, as Ruhigira claims that the allegations were made by disgruntled employees within FECOMIRWA who desired his removal (and wanted his job).Footnote 54

Mineral smuggling, which is outside the RPF’s direct control, represents a threat to goals of centralising revenues within the mining sector. Government officials often highlight the ‘smuggling threat’ and the ‘waste’ associated with ASM.Footnote 55 The tagging system also contributed to additional challenges, with cooperatives often criticised and miners then opting to sell their minerals to other comptoirs. COMIKAGI is a member of FECOMIRWA and is one of Rwanda’s biggest cooperatives. COMIKAGI consists of thirty-nine members, each of whom owns a share in the cooperative. There are also seventy active subcontractors working under COMIKAGI (including ten women), who oversee five to twenty workers each. However, like almost every other mining cooperative, it has been criticised by PACT and Responsible Mines for its inadequate management of tagging procedures. One report also criticizes COMIKAGI for its lack of attention to environmental concerns.Footnote 56

While the government has sought to formalise ASM and manage domestic production through a federation of ASM cooperatives alongside large-scale mining, miners have not fallen in line. Since comptoirs operate in a competitive environment and the tagging systems have benefited better-resourced and connected comptoirs, this has also contributed to incentivising smuggling outside formalised procedures. The RPF’s attempts at centralising control over the sector are countered by competing commercial networks within and outside Rwanda. Tagging systems and the Dodd–Frank Act have only encouraged more smuggling. As a result, the RMB has, instead, placed more efforts on large-scale mining as the only route through which there can be more order within the domestic mining sector.

The Promise of Beneficiation

The RPF government’s most ambitious goal in the sector is to become a hub for minerals processing and beneficiation within the region. In 2006, consultants estimated that if Rwanda smelted all exported cassiterite, revenues would increase exponentially. Yet Rwanda did not have enough domestic production to make a smelting facility feasible for foreign investors. In 2006, a Mining Industry Value Addition Committee was established to develop a strategy to process minerals. The committee included industry experts, the government and the private sector. The committee highlighted the need for increased production of quality minerals and the importance of ensuring all minerals production is sent to processors. However, they warned that a focus on processing would limit attraction to invest in Rwanda’s minerals sector and would face resistance from foreign mining companies (both from domestic comptoirs with links to foreign smelters and foreign smelters themselves).Footnote 57

In the late 2010s/early 2020s, there was progress in constructing new smelters: the Gasabo Gold Refinery and the Power X Tantalum Refinery. Additionally, the tin smelter, which was built by SOMIRWA in the 1980s, became operational again. The government also sought investment in new processing facilities. Smelter owners consistently cited how limited production meant they usually operated at much less than half their capacity. Over the years, prospective investors and former smelting company owners have also highlighted how competitors and foreign buyers ‘sabotage their operations’.Footnote 58 High energy costs and inconsistent energy supply was another significant issue. After the tagging systems were introduced, the additional regulations that needed to be passed were an impediment. Smelters complained of cumbersome paperwork and delays in getting approvals.

The government’s prioritisation of beneficiation is evident through the experiences of its old Karurama smelter, which was built during Habyarimana’s reign in the 1980s. In 2001, the government decided to put the smelter up for sale ahead of other REDEMI assets. European-based NMC Metallurgie (who later changed their name to Phoenix Metals) was granted ownership of the smelter. Though Phoenix initially invested in Rwanda to operate the smelter, the company later operated as a comptoir. The smelter rarely operated during Phoenix’s ownership. Phoenix representatives complained about the limited availability of minerals, the high cost and unreliable supply of electricity and the difficulty in finding foreign buyers for processed minerals. In 2013, in the wake of aid cuts, discussions gathered pace in government circles to guarantee an assured supply (and a lower price) of electricity to Phoenix Metals (which was initially promised in 2006).

While transnational mining companies lobby against the construction of smelters within Africa, significant resistance comes from domestic comptoirs who export mineral production through direct relationships with foreign processing companies. The government’s decision to guarantee the supply of production to one processing facility was thus extremely political and was part of an attempt to centralise control over domestic mineral production and minerals trading networks. However, it has not succeeded. With senior RPF cadres and military officials also involved in the trading of minerals, the government’s limited progress in guaranteeing domestic supply to smelters shows how elite vulnerability thwarts goals of self-reliance.

Officially, there are more than fifty comptoirs exporting Rwandan minerals. Between 2010 and 2015, Minerals Supply Africa (MSA), which had links to the Malaysia Smelting company, exported around 60 per cent of Rwanda’s minerals.Footnote 59 MSA was the dominant Rwanda-based comptoir from 2008 until the mid-2010s. In 2016, David Bensusan – the former CEO of the company (2008–2016) – left to set up his own comptoir (with other shareholders). He, along with Deputy CEO Fabrice Kayihura and Yves Godelet (also formerly of MSA), set up TAMS. TAMS quickly made gains in the market. MSA – which is owned by Cronimet Central Africa – continues to operate in Rwanda.

In 2023, some of the most prominent Rwanda-based comptoirs were Gisandi Trading, Boss Mining and African Panther. Gisandi Trading is a partnership between a Rwandan citizen and Advanced Metal Japan. Gisandi captured significant shares of the market in the late 2010s. Advanced Metal Japan pre-financed the Rwandan partner to buy minerals in-country and the Japanese investor then transported materials out of the country. Most local comptoirs had partnerships with larger buyers outside the country, but it is usually the responsibility of the local comptoir to ensure the minerals reach the ship. Thus, Gisandi’s investment gives them an edge in terms of providing greater space for its Rwandan partner to manoeuvre and capture more of the market. Boss Mining is owned by Eurasian Resources Group. It has a partner company in the DRC. Boss Mining was a comparatively late entrant in Rwanda but they quickly ranked among the top two leading cassiterite exporters in the country (along with African Panther Resources).

The speed with which a comptoir can enter Rwanda’s market and capture significant shares highlights two key challenges to beneficiation in the face of limited government capacity to guarantee supply to smelters. As one comptoir mentioned, ‘cash is king in the mining sector’.Footnote 60 Since miners often prefer to have cash immediately, and since comptoirs operate in a very competitive market, there is significant demand for minerals (especially minerals that are tagged and certified by iTSCi). Second, while elsewhere in the economy, the RPF have successfully centralised and coordinated production, managing resistance from farmers, this has not been the case in the mining sector. The government has not been willing or capable of managing the powerful vested interests in minerals trading. Thus, the government has failed to organise production to support beneficiation, showing how elite vulnerability has hindered RPF goals of becoming a hub for minerals processing.

All smelters must pass Conflict-Free Smelter tests before they can export processed minerals through their facility. Phoenix complained that foreign-based smelters like Malaysia Smelting Company did not have to go through the same audits as Rwanda-based smelters.Footnote 61 After Phoenix left Rwanda in 2018, the government transferred ownership of the Karurama tin smelter to Luna Smelter, a joint venture between Polish-owned Luma Holding Group and Ngali. The Luna Smelter became an iTSCi member in 2018 and was certified as the only conflict-free tin smelter by the Responsible Minerals Initiative in 2020. These achievements highlighted the first major signs of significant progress in beneficiation for the Rwandan government. However, familiar problems remained for the smelter. In 2023, Luna received only 100–120 tons of cassiterite out of the 400 tons generally exported out of Rwanda every month, resulting in the processing facility operating at well below capacity (Sabiiti Reference Sabiiti2023d).

Ngali’s investments in mining were part of a broader strategy for the RPF across the economy. For its most ambitious upgrading and diversification attempts, the government has been directly involved, sometimes in partnership with foreign investors or through its party- or military-owned investment groups or closely affiliated businesspeople. Ngali, which also has been involved in exploration and has been awarded several mining licenses, has been the RPF’s trusted initial investor in beneficiation. For RMB officials, Ngali was supposed to provide ‘a demonstration effect’, with foreign investors later establishing other smelters.Footnote 62 A European-owned firm (but headquartered in the United Kingdom), Power Resources Group, established the Power X Tantalum factory in 2022, working with Rwandan partners.

However, an attempt at establishing a gold refinery faced significant challenges. Alain Goetz, a Belgian minerals trader who owned a gold refinery in Uganda, entered a joint venture through his company, Aldango, with Ngali to establish a gold refinery in 2019. In 2020/2021, the Rwandan government made several arrests at the refinery and revoked Aldango’s export license. With gold not part of the iTSCi tagging system, gold processing was argued to present a significant opportunity to Rwandan goals of beneficiation. Goetz accused the Rwandan government of unfair treatment, while the Rwandan government claimed that Aldango was guilty of tax evasion (Rio Times 2023). Since then, the gold refinery has resumed operations.

Though there are signs of promise, the Rwandan government has faced significant hurdles in beneficiation. First, it has failed to develop effective partnerships with foreign investors. Second, the RMB has faced difficulties in organising domestic minerals production to be sent to processors, highlighting how elite vulnerability continues to thwart the RPF’s attempts to centralise rents in the sector.

Conclusion

Rwanda’s mining sector has become more central to the domestic economy than it has ever been. However, most of Rwanda’s mineral exports originate from the DRC. There are also significant challenges to centralise control over domestic mineral value chains. The chapter shows how the RPF has struggled to centralise control over the distribution of rents in the sector. After market-led reforms reaped limited success in the 2000s, the government revised its policies to prioritise exploration before extraction and increasingly encourage ASM formalisation and large-scale mining. The RPF and some Rwandan elites accrued massive revenues from trading minerals. However, the Rwandan economy’s increased dependence on commercial networks around Congolese trade represents a potential threat to RPF rule. Evidence of this is the increased inter-elite rivalry that surfaced in the 2000s and again in the 2010s.

Dynamics in the domestic minerals sector mirror the elite vulnerability that characterises other sectors. Though RPF elites initially benefited from privatisation efforts alongside foreign investors, there is increased reliance on government-owned firms (like Ngali) for its most ambitious upgrading strategies. Yet the government’s implementation capabilities of coordinating domestic production to serve its ambitions in the sector (like encouraging supply to smelters) have fallen short as compared to the agriculture sector. This highlights the significant power of Rwanda-based comptoirs (with links to powerful global mineral-processing companies) and the elite vulnerability of the RPF itself, with senior RPF leadership unable (or unwilling) to redirect commercial trade to meet the goals of increasing supply to smelters and refineries.