1 Introduction

The use of economic sanctions has become increasingly common as a tool of foreign policy. While the motives behind the enactment of sanctions are often political, a substantive portion of debates regarding sanctions has to do with their economic consequences and developmental side effects on the population. Estimates about their effectiveness are hotly contested (Pape, Reference Pape1997; Elliott, Reference Elliott1998; Pape, Reference Pape1998; Hufbauer et al., Reference Hufbauer, Schott, Elliott and Oegg2007), with recent estimates pointing to a 35% success or partial success rate between 2000 and 2016, with variation depending on the stated political objectives (Felbermayr et al., Reference Felbermayr, Morgan, Syropoulos and Yotov2021).Footnote 1 Similarly contested is the literature regarding the economic effects on sanctioned countries: While there are studies favoring the view that sanctions induce a reduction in GDP growth rates and development outcomes (Neuenkirch and Neumeier, Reference Neuenkirch and Neumeier2015, Reference Neuenkirch and Neumeier2016, Reference Neuenkirch and Neumeier2023), the endogenous nature of sanctions has been highlighted as a potential limitation to the validity of estimates in this literature (Kaempfer and Lowenberg, Reference Kaempfer and Lowenberg2007; Kwon et al., Reference Kwon2020; Gutmann et al., Reference Gutmann, Neuenkirch and Neumeier2020; Felbermayr et al., Reference Felbermayr, Morgan, Syropoulos and Yotov2021).

Debates about cross-country average effects of sanctions are mirrored when discussing specific case studies. In this Element, we focus on the case of Venezuela, which was subject to financial sanctions and to oil sanctions from the United States in late 2017 and early 2019, respectively. On the one hand, sanctions have failed to deliver regime change and democratization, which was their stated objective. On the other hand, negotiations among the Maduro regime, the Venezuelan opposition, and the United States led to an election with a modicum of electoral conditions, in which the opposition was able to prove massive electoral fraud (Corrales and Kronick, Reference Corrales and Kronick2025). Throughout these negotiations, the regime repeatedly demanded relief from economic sanctions as conditions for electoral concessions (Anadolu Agency, 2021; Itriago Acosta, Reference Itriago Acosta2022; Buitrago et al., Reference Buitrago, Sequera and Spetalnick2023a, Reference Buitrago, Sequera and Spetalnick2023b), suggesting that they were an effective negotiation tool. Whether these moderate and short concessions from the regime were worth it depends on a subjective assessment against the potential economic side effects that sanctions may have imposed on Venezuelans.

On this latter front, there is a sizable literature led by development economists arguing that sanctions worked as a “collective punishment” on Venezuelans. Jeffrey Sachs argued that the 2017 financial sanctions led to the death of 40,000 Venezuelans (Sachs and Weisbrot, Reference Sachs and Weisbrot2019). Francisco Rodríguez recently asserted that sanctions led to more than half of Venezuela’s economic contraction and corresponding refugee crisis (Rodríguez, Reference Rodríguez2025a). The main purpose of this Element is to assess the merits of these claims. Our central finding is that the evidence does not support the “collective punishment” narrative. Using newly assembled datasets and a range of rigorous empirical methods, we show that the bulk of Venezuela’s economic contraction and deterioration in welfare indicators took place prior to the imposition of sanctions, with no indication of incremental harm attributable to them thereafter.

To ground this assessment, we begin with a broad view of Venezuela’s economic and developmental outcomes between 2013 and 2023.

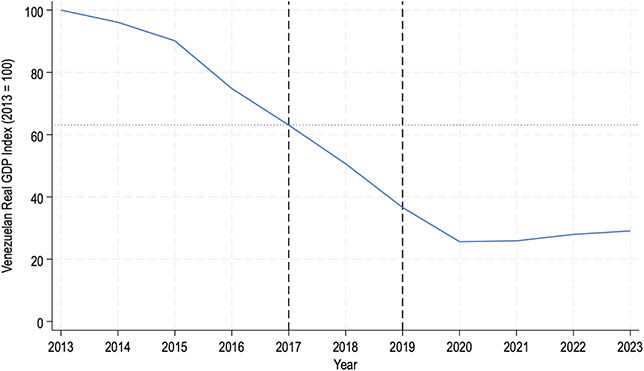

In the following figures, we show the broad evolution of economic and developmental indicators for Venezuela around economic sanctions. In all these figures, the vertical dashed lines mark the August 2017 sanctions, these sanctions had a relatively limited scope, which we will refer to as “financial” sanctions and the January 2019 sanctions, which were much more stringent and we refer to as “oil” sanctions. The horizontal dotted lines mark the 2017 values of the variable being considered, which helps assess the share of the variation that occurred before economic sanctions.

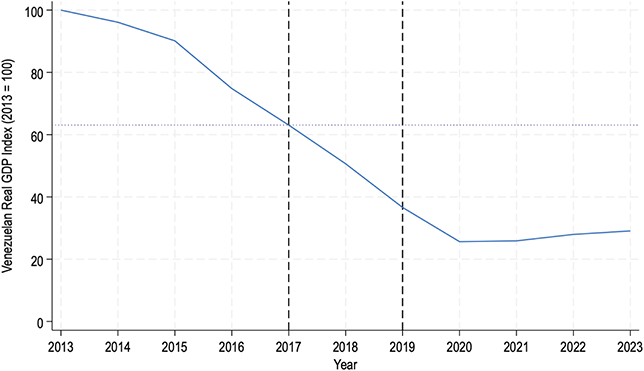

Panel A of Figure 1 shows the evolution of Venezuela’s yearly gross domestic product between 2013 and 2023. By 2017, real GDP had fallen by 37%, which represented 52% of the GDP loss between 2013 and 2023. We observe no acceleration in rate of collapse then, but a continuation of pre-sanctions trends - that is, had the Venezuelan economy continued to evolve as it was before sanctions were first enacted, we would observe very similar outcomes by 2020. Interestingly, the Venezuelan economic collapse comes to a halt in 2020–2021, right after the enactment of oil sanctions in 2019, and despite the COVID-19 pandemic.

Venezuelan real GDP index and total imports, 2013–2023

Note: Panel A shows Venezuela’s real GDP index (2013 = 100) from 2013 to 2023. Panel B shows total imports in billions of USD over the same period. Vertical dashed lines indicate the imposition of US financial sanctions (August 2017) and oil sanctions (January 2019). Horizontal dotted lines mark 2017 values.

Real GDP Index

Imports

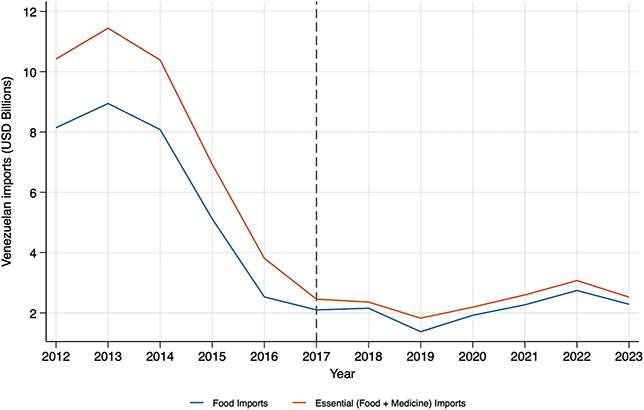

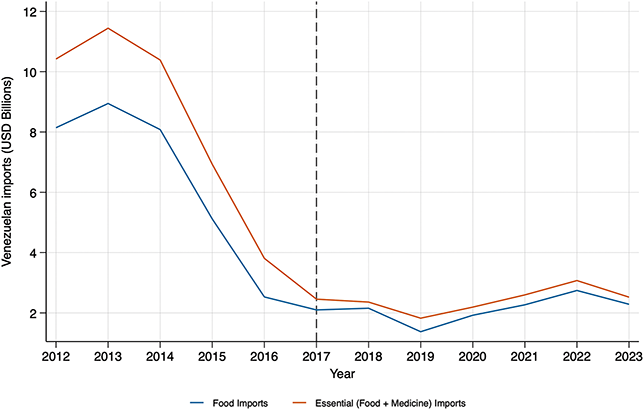

Imports are a key link in the causal logic behind the argument that sanctions were a collective punishment on Venezuelans: By reducing Venezuela’s oil exports, sanctions constrained the capacity for the country to sustain essential imports, in turn leading to the collapse of the economy, the death of thousands, and the migration of millions. Panel B of Figure 1 focuses on Venezuelan imports between 2013 and 2023. By 2017, imports had fallen by 77% when compared to 2013, constituting 98.5% of the import losses between 2013 and 2023. Notably, the rate of collapse in Venezuelan imports starts to attenuate in 2017, and imports start to grow in 2020, right after the 2019 sanctions and despite the COVID-19 pandemic.

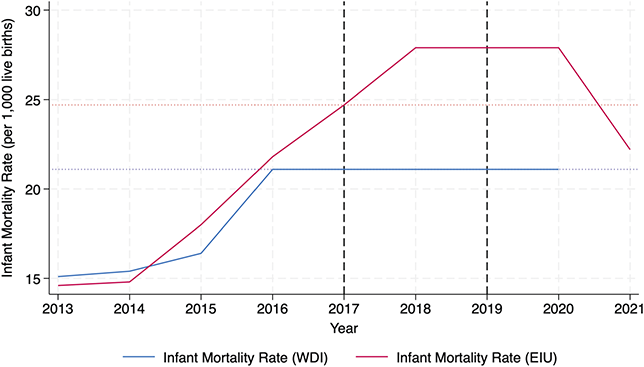

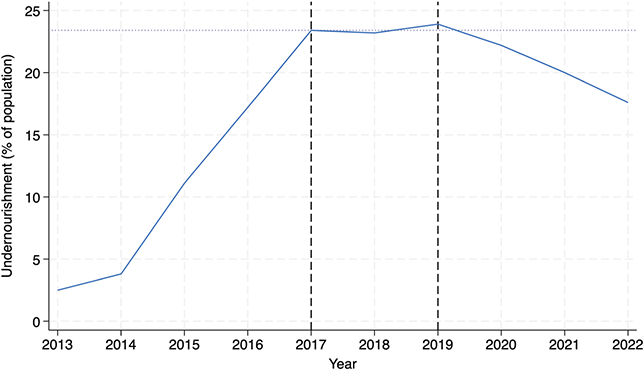

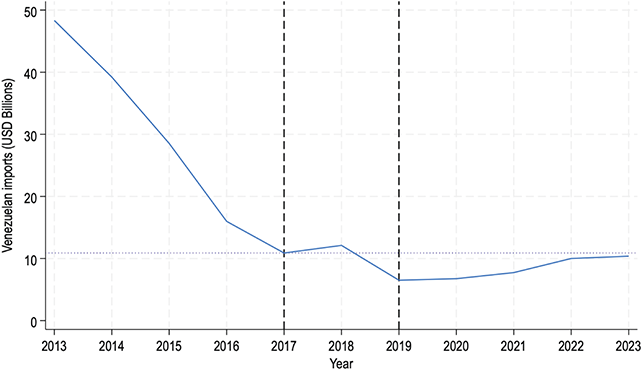

Beyond economic outcomes, the argument of sanctions as a collective punishment on Venezuelans focuses on how they led to the massive collapse of Venezuelans’ living standards. We now focus on fundamental health and nutrition indicators capturing the evolution of such standards.Footnote 2 Panel A of Figure 2 shows the evolution of infant mortality rates as published by the World Bank’s World Development Indicators (WDI) and the Economist Intelligence Unit (EIU). Infant mortality rates grew 40%–70% between 2013 and 2017, depending on the source. Fundamentally, both sources suggest that infant mortality rates stabilized in 2017–2018, and the EIU reference suggests they started to decrease between 2020 and 2021, after the 2019 sanctions and despite the COVID-19 pandemic. Panel B focuses on undernourishment rates as published by the WDI. This is a key variable to consider in the context of the collective-punishment logic, as it should be driven by worsening access to food imports. Undernourishment rates grew from 2.5% to 23.5% of the population -a more than eightfold increase- between 2013 and 2017, remaining stable after sanctions during 2018–2019, and starting to decrease between 2020 and 2022.

Venezuelan infant mortality and undernourishment rates, 2013–2022

Note: Panel A shows infant mortality rates (deaths per 1,000 live births) from 2013 to 2021, with two data series from different sources. Panel B shows the prevalence of undernourishment as a percentage of the total population from 2013 to 2022. Vertical dashed lines indicate the imposition of US financial sanctions (August 2017) and oil sanctions (January 2019). Horizontal dotted lines mark 2017 values.

Infant mortality rates

Undernourishment rate

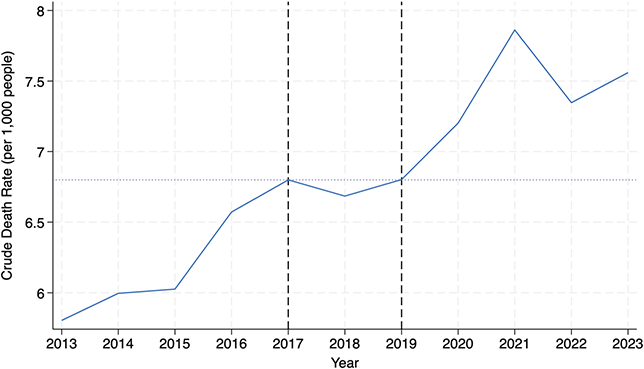

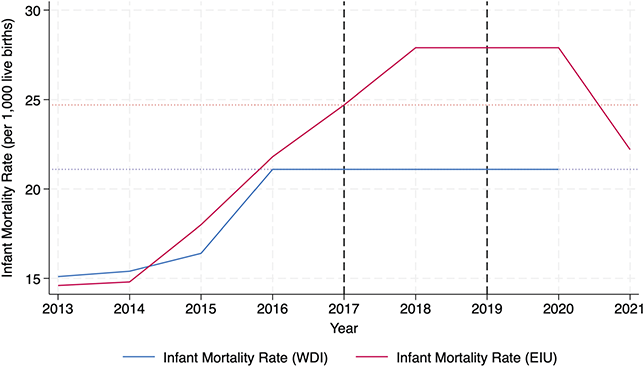

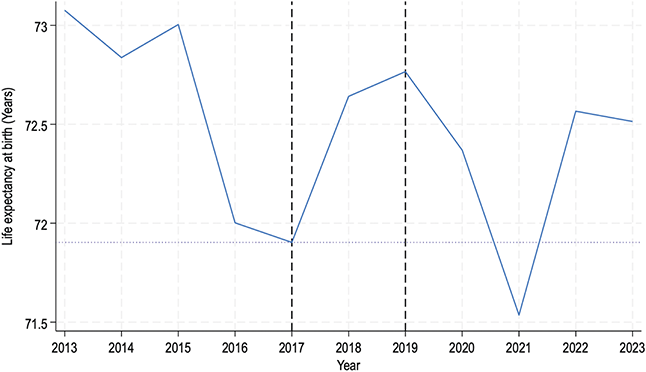

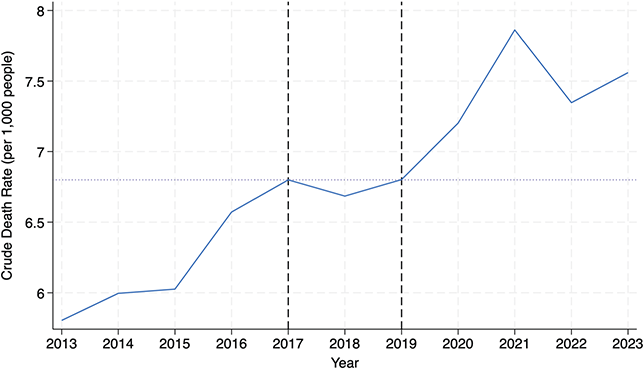

We now turn to indicators that reflect the capacity of sustaining life in Venezuela. Panel A of Figure 3 shows the evolution of Venezuelans’ life expectancy at birth between 2013 and 2023, which dropped by 1.25 years between 2013 and 2017 and improved after financial sanctions, between 2017 and 2019. Life expectancy started to drop again between 2020 and 2021, as expected by the onset of the COVID-19 pandemic, but as the emergency ended, it quickly recovered to near-2015 levels. Panel B shows the country’s crude death rates between 2013 and 2023, which grew by 18% between 2013 and 2017, and stabilized between 2017 and 2019. Again, as in previous indicators, crude death rates started to increase in 2020, stabilizing in 2022 once the COVID-19 pandemic ended.

Venezuelan life expectancy and crude death rates, 2013–2023

Note: Panel A shows life expectancy at birth in years from 2013 to 2023. Panel B shows crude death rates (deaths per 1,000 population) over the same period. Vertical dashed lines indicate the imposition of US financial sanctions (August 2017) and oil sanctions (January 2019). Horizontal dotted lines mark 2017 values.

Life expectancy

Crude death rates

Taken together, this broad view of Venezuelan economic and development indicators suggests that, with the exception of variables directly affected by the COVID-19 pandemic, the downward spiral of living standards that the country was experiencing before sanctions stabilized and started to improve in the aftermath of sanctions. It is true that we cannot observe what would have happened to these same outcomes had sanctions not been enacted, and the point could be made that they might have improved even further. But the argument that the country’s demise was “deliberately caused by the United States, by what I [J. Sachs] would say are illegal sanctions” (Democracy Now!, 2019) is inconsistent with the data. If the lion’s share of economic and developmental collapses had occurred by the time sanctions were enacted, and if their worsening trends attenuated and started improving after sanctions, then it is extremely hard to justify statements that impute “52% of the Venezuelan economic collapse” and four out of the eight million Venezuelan refugees as a consequence of sanctions (Ruiz, Reference Ruiz2025).

The next step is to move beyond this descriptive overview and evaluate the causal claims about the effects of sanctions on Venezuela.

If such statements are in opposition to this broadest view of the Venezuelan data, then what is the analytic substance behind them? In this Element, we first present a thorough timeline of political and economic events in Venezuela around sanctions, between 2013 and 2025. Building on this background, we then engage on a critical review of the quantitative causal literature about the effects of the financial and oil sanctions on the Venezuelan economy, considering contributions both in favor and against the view that they worked as a collective punishment on Venezuelans. Our conclusion is that the literature favoring that view does not overcome three fundamental concerns: 1)It does not engage with key intermediary economic indicators and developmental outcomes behind the “causal chain” logic of the argument; 2)it does not differentiate effects of sanctions from the continuation of pre-sanctions trends; and 3)it does not properly identify effects of either the 2017 financial or the 2019 oil sanctions from the effects of several concurrent treatments.

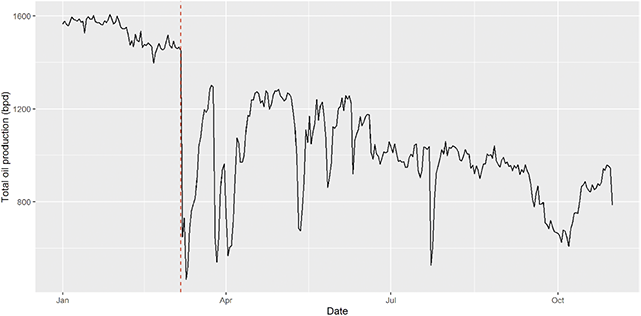

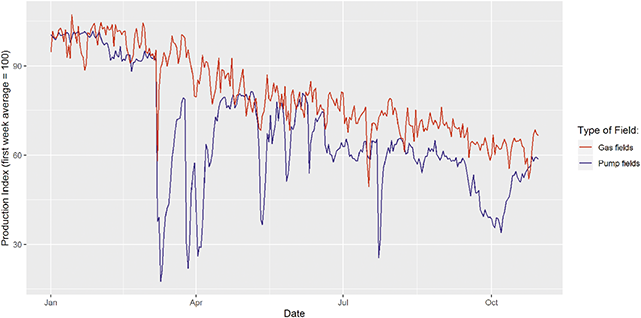

In response to this literature, this Element provides three pieces of novel independent analyses to overcome these concerns. First, we evaluate whether economic and migration patterns in oil-producing regions worsened disproportionately after sanctions were first enacted. We find that they did not. We then look at daily and field-specific oil production data on the days before and after the 2019 blackouts, which occurred about a month after the oil sanctions were enacted. We find massive negative effects of the blackouts, highlighting how concluding that worsening oil production after sanctions is a consequence of sanctions relies on confounding the effects of concurrent treatments and methodologically problematic identification strategies. Finally, we pursue a synthetic control methodology to evaluate whether Venezuelan essential imports dropped disproportionately after the enactment of sanctions. Once again, we find that they did not.

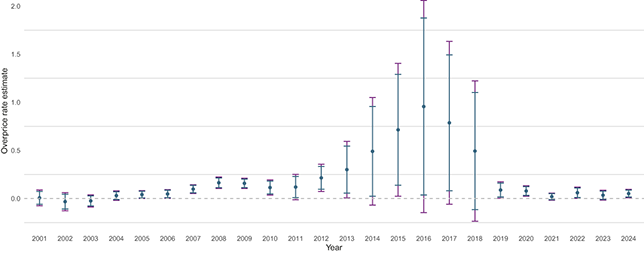

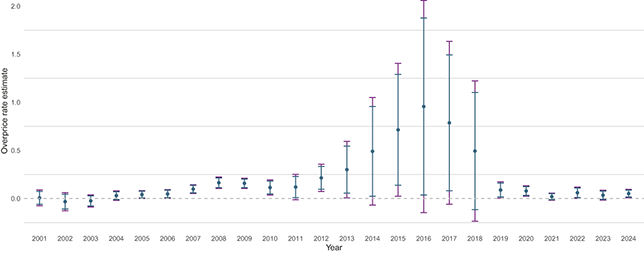

We then narrow our focus to Venezuela’s foreign exchange controls and their decoupling around the enactment of sanctions. After describing their structure and profoundly negative effects on the country’s economy and institutionality, we outline the different post-sanctions steps taken by the Maduro regime to progressively remove exchange controls. We then measure and describe overpricing in Venezuelan imports, one of the key corrosive consequences of exchange controls. We document that overpricing starts after exchange controls were first enacted in 2003, grows greatly with the start of the economic crisis, and peaks, in 2016. Then, they start to dwindle after 2017, and completely disappear after the 2019 oil sanctions.

It may be that exchange and price controls would have been removed in the absence of sanctions.Footnote 3 In that case, the stabilization and mild recovery that followed should not be considered a consequence of sanctions. However, analysts have argued and there is substantive anecdotal evidence indicating that such economic reforms were part of the regime’s response to the increased economic pressure brought about by sanctions. If this was the case, then not only would have sanctions not induced the collapse of the economy, but instead they may have functioned as external constraints on the regime’s discretionary authority, indirectly prompting welfare-enhancing policy adjustments. While the evidence for this second claim is more tentative and should be interpreted with caution, it highlights a mechanism that has not been explored on the literature on sanctions and merits further research. This theory would also be consistent with regime demands for sanction relief despite the stabilization of economic outcomes after sanctions: By constraining discretionary authority and rents, sanctions cornered the regime into an uncomfortable and unstable position, forcing it to implement welfare-enhancing policy reforms while bargaining electoral conditions for relaxed constraints.

The implications of the analysis and conclusions reached by this Element are consequential for the debate over sanctions on Venezuela. While sanctions may have failed to deliver regime change, neither did they precipitate the collapse of the economy or further deterioration of Venezuelans’ living standards. On the contrary, by constraining the regime’s room for maneuver, sanctions may have compelled limited reforms that yielded modest welfare gains. The Maduro government’s consistent demand for sanction relief in every negotiation over electoral conditions further underscores their relevance: While democratization remains elusive, sanctions appear to have functioned as leverage for incremental democratic concessions, and - perhaps unintendedly - as a catalyst for some material relief.

2 Timeline of Economic Events

Venezuela’s economic collapse began by mid 2013, when shortages of basic goods such as food and household staples became widespread and living standards deteriorated sharply. By early 2014, the country was already facing a deepening macroeconomic crisis–marked by worsening food scarcity and mounting political repression – which was later compounded by a sharp decline in global oil prices that would halve Venezuela’s export revenues by 2015 (IMF, 2015; Santos, Reference Santos2017, Reference Ángel Santos2021). By every comparative measure, Venezuela went on to experience the largest economic collapse in modern history outside of war or natural disaster. Writing about the GDP loss recorded just between 2014 and 2016, a cumulative contraction of 25.2%, Barrios and Santos (Reference Barrios and Santos2017) conclude:

In the last twenty years, only four three-year periods worldwide have recorded greater economic devastation: Libya (

60.5% between 2009–2011), South Sudan (

60.5% between 2009–2011), South Sudan (

45.9% between 2010–2012), Iraq (

45.9% between 2010–2012), Iraq (

36.2% between 2001–2003), and the Central African Republic (

36.2% between 2001–2003), and the Central African Republic (

35.5% between 2012–2014). In all these cases, the collapse coincided with armed conflicts of various kinds, which makes the Venezuelan episode a truly exceptional case of economic ruin.Footnote 4

35.5% between 2012–2014). In all these cases, the collapse coincided with armed conflicts of various kinds, which makes the Venezuelan episode a truly exceptional case of economic ruin.Footnote 4

Policy decisions under Maduro’s government further deepened the crisis, pushing the country into a prolonged cycle of hyperinflation and contraction. Venezuela suffered an additional 15.7% loss of economic activity in 2017, and hyperinflation officially began in December of that year when monthly inflation surpassed the 50% threshold (55.6%).

In total, the country lost 74% of its GDP between 2013 and 2020. Half of that contraction occurred between 2013 and 2017, and two-thirds took place before the imposition of sanctions on the state-owned oil company Petroleos de Venezuela (PDVSA) in January 2019. The oil industry mirrored the evolution of GDP, losing 79% of its output between 2013 and 2020. A quarter of that loss occurred between 2013 and 2017, and more than half was recorded before the January 2019 sanctions. By 2016 Venezuela’s debt had surpassed the $120 billion mark and its ratio to exports (4.37) was the highest among all the countries covered in the World Development Indicators database of the World Bank that year. As documented by Bahar et al. (2019), Venezuela’s sovereign risk averaged 2,364 basis points (or 23.64%) from January to August 2017 and did not significantly depart from those levels once financial sanctions were imposed later that month. Spreads skyrocketed more than a month later, once the Venezuelan debt entered in outright default in November of that year after a failed meeting convened by the Venezuelan government with creditors in Caracas.

As reported by Hernández and Monaldi (Reference Hernández and Monaldi2016), the Venezuelan oil industry was already in a state of profound financial and operational fragility in 2016. Net cash-generating exports had eroded to nearly half of reported production, once the subsidized domestic market, and in-kind debt repayments to China were discounted. At the same time, PDVSA faced a crushing fiscal burden, as resources were systematically diverted to social programs and extra-budgetary funds, while debt service costs escalated amid restricted access to credit markets. Mounting arrears to service contractors led major international firms to curtail operations, exacerbating technical bottlenecks, while chronic power outages, refinery accidents, and shortages of inputs undermined reliability across the supply chain. Inflation, exchange-rate distortions, and the bloated payroll further inflated costs, pushing the company’s cash flow into persistent deficit.

By 2020, Venezuela’s level of economic activity had fallen back to that of 1964, with income per capita levels not seen since the 1940s (World Bank, 2021). The Venezuelan exodus had reached, by mid 2019, approximately 3.9 million people or 14% of its total populationFootnote 5. It has been estimated at 7.9 million people or 24% of its population by 2024.Footnote 6 Thus, it has become the largest population displacement recorded in Latin America, and among the largest in the world together with Syria, Afghanistan, and, more recently, Ukraine.Footnote 7

Financial Sanctions and Democratic Backsliding

On March 8, 2015, President Barack Obama signed Executive Order 13692, imposing targeted sanctions on eleven senior current or former Venezuelan officials, citing corruption and human rights violations (White House, 2015). Later that year, the opposition coalition won a decisive victory in the parliamentary elections of December 6, 2015, securing a two-thirds supermajority in the National Assembly for the first time since Hugo Chávez came to power seventeen years earlier. However, the pro-government Supreme Court of Justice (TSJ) swiftly blocked four opposition deputies from Amazonas state from taking office, citing alleged irregularities in the electoral process that it claimed affected the validity of the vote in that region (TSJ, 2015, 2016a). By excluding these deputies, the ruling deprived the opposition of the qualified majority needed to override presidential vetoes, appoint or remove key officials, and pass constitutional reforms independently. In April 2016, the TSJ formally declared the National Assembly in contempt and nullified its legislative powers (TSJ, 2016b). Later that year, when the opposition launched a recall referendum effort to remove Maduro, the TSJ and National Electoral Council (CNE) suspended the process (BBC News, 2016).

By March 2017, the TSJ escalated its attack on the legislature, dissolving the National Assembly entirely (TSJ, 2017). This decision triggered a massive wave of protests throughout the country. Heavy repression from security forces left 157 people dead, 2000 people injured and more than 5000 imprisoned (Llorens, Reference Llorens, país and venezuela2018). Moreover, President Maduro called elections for a parallel Constitutional Assembly (ANC), tasked with drafting a new constitution. The ANC election, which was called for without meeting the necessary constitutional requirements, was held on July 30, 2017, amid nationwide protests and international condemnation (TalCual Digital, 2019).

In response, the Trump administration issued Executive Order 13808 on August 25, 2017, imposing financial sanctions that barred the Venezuelan government and its state-owned oil company (PDVSA) from issuing new bonds in United States’ markets or trading existing bonds there, effectively preventing both entities from refinancing their external debt (U.S. Treasury, 2017). These were financial sanctions and did not prohibit oil trade between the United States and Venezuela. Soon after, the European Union imposed its own targeted sanctions (EU Council Decision, 2017). Another significant development was the formation of the Grupo de Lima, a multilateral coalition of Latin American countries and Canada, established in August 2017 in response to the ANC with the explicit purpose of coordinating diplomatic pressure to restore democratic order in Venezuela. Following this, later in November 2017, Nicolas Maduro appointed Manuel Quevedo, a high-ranking official of the National Guard to head PDVSA, effectively militarizing the oil company. He was president of PDVSA and Minister of Oil until 2020.

Constitutional Crisis and “Oil” Sanctions

Despite widespread international rejection, the Maduro regime proceeded with presidential elections on May 20, 2018, which were broadly denounced as fraudulent due to bans on opposition candidates, electoral manipulation, and widespread irregularities. The elections had the lowest turnout for a presidential election in the history of Venezuela, regardless of the source: 46.1% according to the Venezuelan Electoral Council (Venezuelan Electoral Council, 2021), 25.1% according to the Mesa de la Unidad Democrática,Footnote 8 17.3% according to independent pollsters (HuffPost, 2018). Considering that the essential tenets of credible, transparent, and inclusive elections were violated in the electoral process, the international democratic community rejected the process and did not recognize its results, including the European Union (Parliament, 2018), the Organization of American States (Organization of American States, 2021), the Grupo de Lima (Grupo de Lima, 2018), as well as the United States (Reuters, 2018). Only a handful of countries – including China, Cuba, Iran, Russia, Syria, and Turkey – recognized the election result (Infobae, 2018).

When Maduro’s second term formally expired on January 10, 2019, the opposition-led National Assembly, pursuant to its authority under the Venezuelan constitution to fill a vacancy in the presidency, appointed the President of the legislative body, Juan Guaidó, as the Interim President of Venezuela. On February 5 the National Assembly passed the Statute Governing the Transition to Democracy to reestablish the Validity of the Constitution of the Bolivarian Republic of Venezuela, a bill that “governs the installation of a provisional Government and the call to free elections,” and “establishes the election of new rectors of the National Electoral Council, new magistrates of the Supreme Tribunal of Justice and new representatives of the Citizen Power” (Asamblea Nacional, 2019).

On January 23, the United States recognized Juan Guaidó as Interim President of Venezuela (U.S. Department of State, 2019). Canada followed shortly (Global Affairs Canada, 2019) as well as more than half of the twenty-eight European Union countries, including Germany, France, Spain, and the United Kingdom (BBC News, 2019a).

On January 28 2019, the US Treasury’s Office of Foreign Assets Control (OFAC) designated PDVSA under Executive Order 13850, freezing its assets under the US jurisdiction and prohibiting its citizens from engaging in transactions with PDVSA. The measure effectively banned imports of Venezuelan crude into the United States and restricted the export of refined products and diluents critical for processing heavy crude (U.S. Department of the Treasury).

In parallel, OFAC issued General License 8, which allowed Chevron, Halliburton, Schlumberger, Baker Hughes, and Weatherford International to continue “ordinary and necessary” activities with PDVSA to preserve assets and maintain operations. This authorization, repeatedly renewed through 2019, essentially permitted United States’ firms to sustain the status quo of existing contracts but not to expand or modify them (Hernández, Reference Ignacio Hernández2022).

By the end of February 2019, thirty-six countries had recognized Juan Guaidó as Interim President, a figure that grew to more than fifty by the end of that year (Foreign Policy, 2019). That same month, Venezuela suffered a series of nationwide blackouts, including the longest power outage in the country’s history, which left most of the population without electricity for nearly a week and caused persistent supply disruptions for months afterward (Reuters, 2019; BBC News, 2019b).Footnote 9

Amid worsening conditions, Juan Guaidó and other opposition leaders attempted to rally military support for a transition of power on April 30, 2019, but the effort failed and forced many opposition figures into exile (BBC News, 2019c). Later that year, on August 5, 2019, the Trump administration issued Executive Order 13884, imposing a comprehensive embargo that effectively froze all Venezuelan government assets under US jurisdiction, blocked the Central Bank of Venezuela’s access to dollars, and prohibited nearly all transactions with officials of the Maduro regime (White House, 2019).

COVID and Relief of Sanctions

The onset of the COVID-19 pandemic in 2020 further deepened Venezuela’s economic crisis. From 2020 onward, sanctions expanded to include third-country intermediaries that helped market Venezuelan crude. In April 2020, with the issuance of General License 8F, permissions previously granted to maintain the status quo were significantly curtailed: Chevron and others were restricted to the limited rights of minority shareholders in joint ventures, barred from financing PDVSA’s share of investments, distributing dividends (even in crude), or receiving oil in payment of debt. Companies could still cover basic costs such as local taxes, utilities, and salaries, but new investment and debt arrangements were prohibited. These restrictions shifted the burden of financing entirely to PDVSA, which lacked the capacity to sustain capital expenditures, and were subsequently reiterated in renewed licenses through 2022 (BBC News, 2019c).

In April, the United States’ Department of Justice indicted Nicolás Maduro and senior officials on charges of narco-terrorism and corruption, offering a reward of up to $15 million for information leading to Maduro’s arrest (U.S. DOJ, 2020). In June, the Treasury imposed additional sanctions designating four shipping companies for operating vessels that transported Iranian oil products to Venezuela in violation of sanctions and embargoes, attempting to cut off critical gasoline imports essential to the country’s economy (U.S. Treasury, 2020). These measures marked the final phase of the Trump administration’s “maximum pressure” strategy: Imposing sanctions on nearly every economic sector in the expectation that mounting constraints would either force a democratic transition or provide leverage for negotiations.

Amid tightening sanctions and worsening economic conditions, the Venezuelan government organized elections for a new National Assembly on December 6, 2020. Major opposition parties and leaders boycotted the vote, denouncing it as illegitimate due to restrictions on political participation, lack of electoral guarantees, and manipulation by the pro-government National Electoral Council (CNE). In its final report, the European External Action Service (EEAS) concluded that the process failed to meet international democratic standards and reaffirmed that the 2015-elected National Assembly remained the only legitimate parliamentary body (European Council, 2020). Following the vote, the United States also rejected the results and reaffirmed its support for the opposition-led Assembly (U.S. Department of State, 2020). In 2021, Venezuela continued to face severe humanitarian hardship and renewed political tensions. Early that year, the European Union announced that it would no longer formally recognize opposition leader Juan Guaidó as Venezuela’s interim president, though it reiterated that Nicolás Maduro’s 2018 reelection remained illegitimate (Euronews, 2021). In November, regional elections were held, marking the opposition’s return to electoral participation after years of boycotts. Despite this reengagement, independent observers and opposition figures reported widespread irregularities and structural advantages for pro-government candidates (European Union Election Observation Mission, 2021). The year closed with initial steps toward renewed negotiations between the opposition and the government, first mediated by Norway and later culminating in the Barbados Agreement framework.

In October 2022, the Biden administration offered a limited relaxation of sanctions by granting Chevron Corporation a specific license to resume restricted oil production and export operations in Venezuela, under clear conditions tied to political concessions. This was the first significant easing of sanctions since they were imposed in 2017 and 2019. Through General License No.41, Chevron was authorized to produce oil but not to pay taxes or royalties directly to the Maduro government, aiming to ensure funds were ring-fenced for debt repayment and humanitarian uses (U.S. Treasury, 2022). In return, the Maduro administration agreed to allow the opposition to hold primary elections to select its leadership and ultimately enable the candidacy of María Corina Machado for the 2024 presidential election.

Throughout 2023, diplomatic tensions continued, marked by a cycle of temporary concessions and renewed repression. In October, the United States temporarily lifted key sanctions on Venezuela’s oil, gas, and gold sectors after the signing of the Barbados Agreement, making this relief conditional on Nicolás Maduro’s commitments to release political prisoners and allow internationally monitored free and fair elections. This easing took the form of General License No.44, which authorized to resume certain transactions with PDVSA and the Venezuelan mining sector for a limited period (U.S. Treasury, 2023). However, by November Maduro’s government backtracked on these commitments when security forces arrested multiple members of opposition leader María Corina Machado’s campaign team, drawing condemnation from the United States and the European Union for undermining the agreed electoral guarantees.

In December 2023, the United States warned that it would reimpose sanctions if the Maduro regime failed to fulfill its commitments under the Barbados Agreement, highlighting the fragility of the diplomatic framework and Maduro’s ongoing reluctance to implement meaningful democratic reforms. Ultimately, General License No.44 expired in April 2024 after the regime failed to meet its core conditions, which included allowing free and fair elections and respecting opposition candidates’ right to run. Instead, authorities upheld a ban preventing María Corina Machado from standing as a presidential candidate, and subsequently barred her chosen substitute, Corina Yoris, from registering as well (U.S. Department of State, 2024). Under mounting domestic and international pressure, Maduro eventually conceded by permitting opposition figure Edmundo González Urrutia to stand as a unity candidate – but this sequence of obstructions triggered the wind-down and nonrenewal of the license (U.S. Treasury, 2024).

Presidential Elections and Return of Sanctions

The political situation deteriorated significantly in 2024. After Nicolás Maduro failed to fulfill his commitments under the Barbados Agreement, the United States reinstated sanctions on Venezuela’s vital oil and gas sector in April 2024, restoring financial pressure on PDVSA and associated state revenues (U.S. Treasury, 2024). In July, the presidential election was marred by widespread allegations of fraud, voter intimidation, and ballot manipulation. Despite independently corroborated evidence indicating that opposition candidate Edmundo González Urrutia won by a significant margin – with estimates suggesting he secured around 70% of the vote – Maduro refused to acknowledge defeat and declared himself the winner (U.S. Mission to the OAS, 2024; U.S. Department of State, 2024). The outcome was swiftly rejected by international election observers, the European Union, the United States, and multiple Latin American governments, all of whom cited severe irregularities and the absence of democratic guarantees (European External Action Service, 2024).

3 Critical Literature Review

As discussed in the introduction, the evolution of key economic and developmental outcomes around sanctions seems to contradict the punitive narrative that sanctions acted as collective punishment on Venezuelans. Given this contradiction, it is important to critically assess how such a narrative has been both substantiated and rebutted. In this section, we now discuss the literature assessing the developmental effects of United States’ sanctions on Venezuela. First, we outline the scope of our review and present the list of contributions covered – both supportive and critical of the view that sanctions collectively punished Venezuelans. We then discuss the literature chronologically, showing how different contributions address each other. Finally, we conclude this section outlining the three key gaps in the literature favoring the notion of sanctions-as-collective-punishment.

Scope of This Literature Review

The scope of this review is deliberately focused on contributions that meet two specific criteria. First, we concentrate on studies analyzing the impact of sanctions on Venezuela following their implementation in 2017. While the broader sanctions literature includes numerous cross-country analyses and studies of other sanctioned regimes, we consider only those that advance Venezuela-specific analyses. This targeted approach allows us to assess the evidence base regarding this particular case, which has been the subject of scholarly and policy debate.

Second, we limit our focus to quantitative contributions that employ methodological frameworks to estimate the causal effects of these sanctions. These studies share a common feature: They attempt to construct “counterfactual” benchmarks – estimates of what would have happened to economic and development outcomes in the absence of sanctions – to isolate the sanctions’ impact from other factors affecting Venezuela’s economy. This approach distinguishes the literature we review from a broader set of policy notes, legal analyses, and opinion pieces that discuss Venezuela sanctions from normative or descriptive perspectives without attempting to estimate causal effects through quantitative, causal approximations.

It should be noted that the literature that meets these criteria varies in terms of methodological rigor and publication status. As of the writing of this Element, only one paper in this list has undergone peer review in an academic journal. Other contributions exist as academic working papers, policy analyses, or opinion pieces released by think tanks, media outlets, or individual researchers. This variation in publication status requires careful consideration when assessing the robustness and reliability of findings across the literature. Finally, while several other articles and books quote or reintroduce the arguments and findings presented in the contributions discussed next, we limit our focus to the main sources of the analytic findings used to weigh on the debate of Venezuelan sanctions as collective punishment.Footnote 10

Summary of the Literature

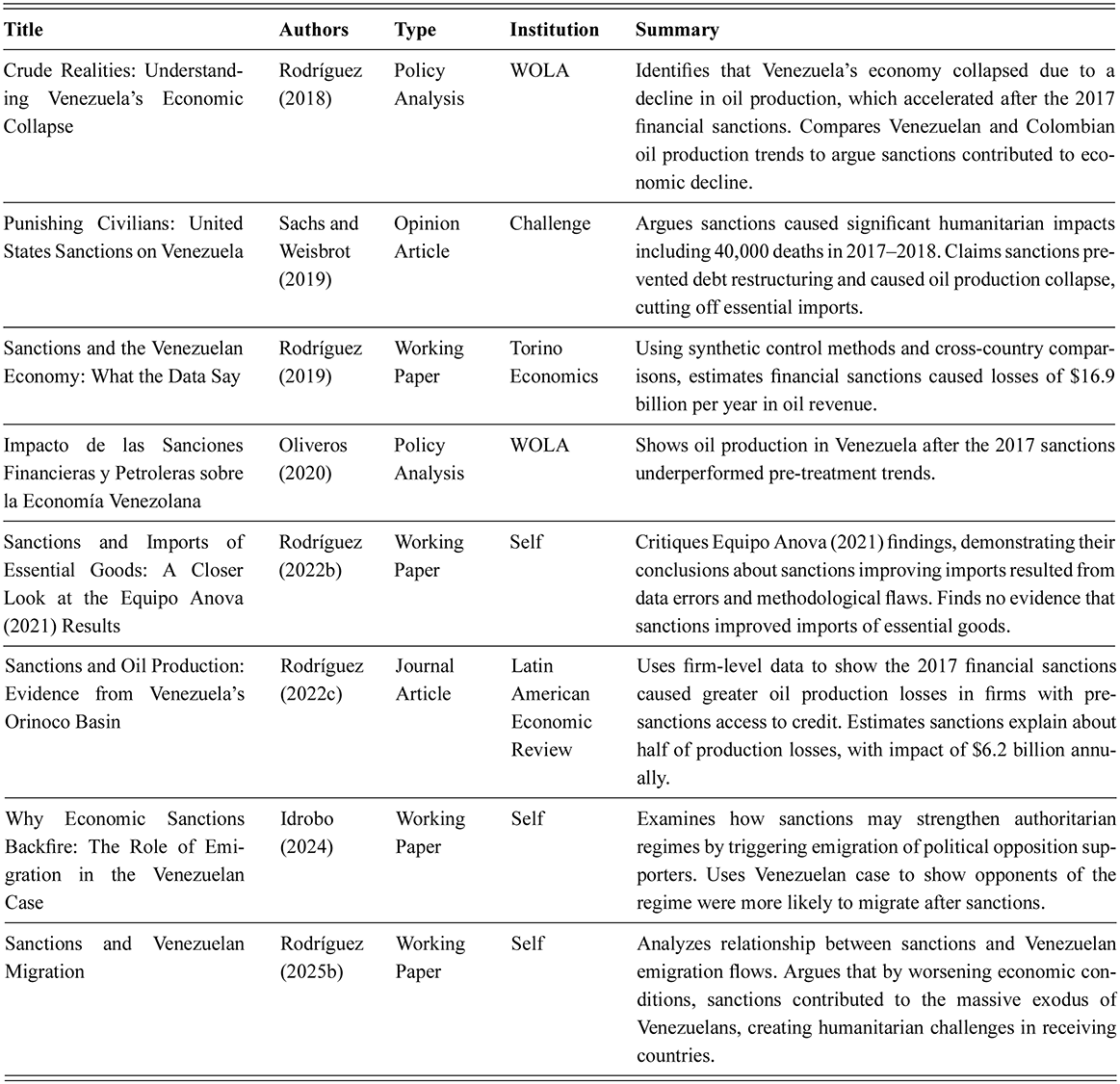

Table 1 outlines the contributions providing quantitative evidence in favor of the view that US sanctions on Venezuela worked as a tool for collective punishment, while Table 2 outlines contributions providing evidence rejecting that view.

Table 1 Long description

The table has five columns. Across the entries, the works are mostly policy analyses and working papers, with one journal article and one opinion article. The studies generally argue that sanctions, especially the 2017 financial sanctions and later sanctions, contributed to oil production losses, reduced public revenue, economic contraction, import shortages, humanitarian harm, and increased migration. Specific claims in the summaries include those sanctions accelerated Venezuela’s collapse after oil production fell, caused large annual oil-revenue losses, were associated with major humanitarian costs, including an estimate of 40,000 deaths in 2017 to 2018, and contributed to mass emigration by worsening living conditions and potentially strengthening authoritarian rule. The table presents works the authors classify as supporting the position that sanctions on Venezuela functioned as a form of collective punishment by imposing broad harms on the population. The table contains eight entries.

Row 1. Crude Realities: Understanding Venezuela’s Economic Collapse.

The summary says that the study identifies Venezuela’s economic collapse as resulting from a decline in oil production, and that this decline accelerated after the 2017 financial sanctions. It compares Venezuelan and Colombian oil production trends and argues that sanctions contributed to Venezuela’s economic deterioration.

Row 2. Punishing Civilians: United States Sanctions on Venezuela.

The summary says that the piece argues sanctions caused major humanitarian effects, including a claim of 40,000 deaths in 2017 to 2018. It also says sanctions prevented debt restructuring and contributed to the collapse of oil production, thereby cutting off imports of essential goods.

Row 3. Sanctions and the Venezuelan Economy: What the Data Say.

The summary states that the study uses synthetic control methods and cross-country comparisons to estimate that the financial sanctions caused losses of $16.9 billion per year in oil revenue.

Row 4. Impacto de las Sanciones Financieras y Petroleras sobre la Economía Venezolana.

The summary says that oil production in Venezuela after the 2017 sanctions performed worse than projected pre-treatment trends. The emphasis here is on underperformance in oil output after sanctions were imposed.

Row 5. Sanctions and Imports of Essential Goods: A Closer Look at the Equipo Anova (2021) Results.

The summary says that this work critiques the findings of Equipo Anova (2021). According to the summary, it argues that Equipo Anova’s conclusion that sanctions improved imports was driven by data errors and methodological flaws. The row concludes that the paper finds no evidence that sanctions improved imports of essential goods.

Row 6. Sanctions and Oil Production: Evidence from Venezuela’s Orinoco Basin.

The summary says the article uses firm-level data to show that the 2017 financial sanctions caused larger oil production losses among firms that had access to credit before sanctions were imposed. It estimates that sanctions explain about half of the production losses, with an economic impact of $6.2 billion annually.

Row 7. Why Economic Sanctions Backfire: The Role of Emigration in the Venezuelan Case.

The summary says the paper examines how sanctions may strengthen authoritarian regimes by encouraging emigration among political opposition supporters. Using the Venezuelan case, it argues that opponents of the regime were more likely to migrate after sanctions were imposed.

Row 8. Sanctions and Venezuelan Migration.

The summary says the paper analyzes the relationship between sanctions and Venezuelan emigration flows. It argues that by worsening economic conditions, sanctions contributed to the mass exodus of Venezuelans, which in turn created humanitarian and policy challenges in receiving countries. Overall, the table presents a body of literature that links sanctions to multiple categories of negative impacts.

| Title | Authors | Type | Institution | Summary |

|---|---|---|---|---|

| Don’t Blame Washington for Venezuela’s Oil Woes: A Rebuttal | Hausmann and Muci (Reference Hausmann and Muci2019) | Opinion Article | Americas Quarterly | Argues Venezuela’s economic crisis predated sanctions, and that the 2019 oil output decline was caused by electrical blackouts, not sanctions. Questions whether Colombia is an appropriate counterfactual for Venezuela’s oil production trends. |

| Sanciones: ¿causa o consecuencia de la crisis? | Morales-Arilla (Reference Morales-Arilla2019) | Opinion Article | Prodavinci | Contends Venezuela’s oil production decline was primarily caused by militarization of the oil industry and corruption investigations, not sanctions. Notes production was declining before sanctions due to mismanagement and investment cuts. |

| Impact of the 2017 Sanctions on Venezuela: Revisiting the Evidence | Bahar et al. (Reference Bahar, Bustos, Morales-Arilla and Santos2019) | Policy Analysis | Brookings Institution | Challenges the causal link between sanctions and humanitarian crisis, showing social indicators were declining before sanctions. Argues Venezuela had already lost access to capital markets prior to sanctions, making financial sanctions redundant. |

| Impacto de las Sanciones Financieras Internacionales contra Venezuela: Nueva Evidencia | Zambrano et al. (Reference Zambrano, Hernández and Escalante2021) | Policy Analysis | ANOVA | Claims financial sanctions were associated with improvements in imports of food and medicines, while acknowledging negative effects on oil production. Suggests sanctions may have forced positive policy changes including economic liberalization by the government. |

| Sanctions on Venezuela Are Not Driving Migration to the US Southwest Border: An Empirical Assessment | Bahar and Hausmann (Reference Bahar and Hausmann2025) | Working Paper | Center for Global Development | Finds higher oil income and prices correlate with more Venezuelan migration to the United States, not less. Argues sanctions actually reduce migration flows by constraining economic activity, contradicting claims that sanctions worsen the migration crisis. |

The “Causal Chain”: 2017 Sanctions, Oil Production, and Venezuela’s Collapse

The first contribution formally studying the effects of Venezuelan sanctions was Rodríguez (Reference Rodríguez2018). In this study, released by the Washington Office on Latin America (WOLA), Rodríguez argues that the 2017 financial sanctions caused a reduction in Venezuelan oil production. Rodríguez argues that changes in oil production observed in Colombia provide an adequate counterfactual of what would have happened to Venezuelan oil production had the 2017 financial sanctions not been enacted. Chiefly, both Venezuela and Colombia saw a decline in production after oil prices fell under the $30 per barrel threshold -which the author argues would be expected in both countries given their reliance on costly extraction of extra-heavy oils. However, Venezuelan oil production collapsed after financial sanctions were enacted in August 2017, while Colombian production remained steady.

Rodríguez (Reference Rodríguez2018) first introduced what we call the “causal chain” behind the argument that sanctions induced the collapse of the Venezuelan economy. By eroding oil production, sanctions limited Venezuela’s oil export revenues, which constrained the country’s import capabilities, producing the collapse of the economy: “I argue that Venezuela’s economy has imploded because it can’t import, and it can’t import because its export revenue has collapsed.” This argument is most drastically presented in Sachs and Weisbrot (Reference Sachs and Weisbrot2019). After reasserting the findings in Rodríguez (Reference Rodríguez2018), Sachs and Weisbrot extend the implications of the causal chain to argue that by “ending much of the country’s access to these essential imports including medicine and food,” the 2017 financial sanctions induced the death of 40,000 Venezuelans. Chiefly, the way the authors estimate such effects is by assuming that the increase in mortality rates in Venezuela between 2017 and 2018 was fully a consequence of the 2017 sanctions: “there was a 31 percent increase in general mortality from 2017 to 2018. This would imply an increase of more than 40,000 deaths.” While this and other similarly calculated estimates would be extensively cited in policy and political debates regarding the effects of sanctions (Fox News, 2019; RealClearPolitics, 2019), Sachs would later say that “I don’t want anyone to think that there is precision in these numbers” (Democracy Now!, 2019).

At least three other contributions introduced further evidence in favor of the view that the 2017 sanctions eroded Venezuela’s oil production - and extrapolated these findings to argue that sanctions were the key culprit behind the collapse of the Venezuelan economy. Rodríguez (Reference Rodríguez2019), released by Torino Economics, leveraged the synthetic control methodology to produce a data-driven counterfactual of what the Venezuelan oil production would have been had the 2017 sanctions not been enacted. The paper argues that sanctions led to a decrease in oil production of 797,000 barrels of oil per day, adding to lost oil export revenue of $16.9 billion per year. Chiefly, the paper underscores the “causal chain” argument:

If one assumes that large variations in mortality (particularly increases, which are rare) are driven by changes in income and one assumes that Venezuelan GDP would have stabilized in the absence of the decline in production caused by the 2017 sanctions, then one can conclude that the main cause of the increase in mortality that year was the adoption of sanctions.

Similarly, Oliveros (Reference Oliveros2020) argues that there was an acceleration in the collapse of oil production after the enactment of the 2017 financial sanctions. The analysis uses monthly drops in pre-sanctions productions levels between 1% and 2% as a counterfactual range to calculate the effect of sanctions on oil export revenues, estimating a drop in revenues of $31 billion to $17.5 billion between August 2017 and July 2020. Now again, the analysis advances the “causal chain” discussed earlier: “With the fall of oil production in Venezuela, the Venezuelan government’s foreign exchange revenues also drop, producing an import contraction that, ultimately, affects the poorest Venezuelans.”

Finally, Rodríguez (Reference Rodríguez2022c) presents the only piece of independently peer-reviewed evidence that the 2017 sanctions affected oil production. Published in the Latin American Economic Review,Footnote 11 the paper uses production data from different firms within Venezuela’s Orinoco Oil Basin. Leveraging a difference-in-differences framework, the paper finds that oil production dropped faster for firms with better pre-sanctions access to financing after the 2017 financial sanctions, which limited PDVSA’s access to US financial markets.Footnote 12 Despite being peer-reviewed, the paper has been criticized on methodological grounds. Among other criticisms, Bahar (Reference Bahar2024) discusses the paper’s main figure to make the point that firms with and without PDVSA financing agreements were clearly in different production trends before sanctions were first enacted, rendering the fundamental assumption of difference-in-difference designs (parallel trends between treatment and control units) implausible to estimate causal effects in this setting. In any event, as the paper concludes Rodríguez (Reference Rodríguez2022c) reemphasizes the “causal chain” of the collective punishment argument: “the evidence suggests that financial sanctions can and did act as an economic surgical strike capable of replicating the effects of a full-fledged trade embargo.”

Initial Rebuttals: Did These Papers Prove That Sanctions Eroded Oil Production?

The release of Rodríguez (Reference Rodríguez2018) and Sachs and Weisbrot (Reference Sachs and Weisbrot2019) produced an initial set of rebuttals on whether these findings proved that the 2017 financial sanctions eroded oil production and overall living standards in Venezuela. First, Hausmann and Muci (Reference Hausmann and Muci2019) questioned the validity of using Colombian oil production as a counterfactual for what would have happened to Venezuelan oil production in the absence of sanctions. The authors argue that Venezuela and Colombia were on diverging production trends before sanctions. Moreover, they argue that oil production drops in Venezuela between January 2016 and August 2017 were concentrated in oil fields with light and medium oils, so oil production in Venezuela did not fall during that period because of oil price drops - as was the case in Colombia. The authors argue that Venezuela’s share of oil production from OPEC countries had been falling at similar rates since 1999.

Morales-Arilla (Reference Morales-Arilla2019) seconds the argument that Colombia provides an inadequate counterfactual, underscoring that oil prices quickly recovered and were already above the $30 per barrel benchmark by May 2016, so they cannot explain the pre-sanctions drops in oil production in Venezuela. Citing Bloomberg (2016), the article references consulting firms in the Venezuelan oil sector arguing that pre-sanctions production drops extended to lighter oils whose production should not remain commercially viable at lower oil prices. Consultants argued that the key reasons for pre-sanctions production declines were “drilling challenges, natural gas compression issues and well maintenance difficulties due to restriction of field services and theft,” not lower oil prices. The author argues that 76% of all Venezuelan oil production losses between 2015 and 2018 either occurred before the August 2017 sanctions or could be explained by extrapolating pre-sanctions production trends.Footnote 13

Morales-Arilla (Reference Morales-Arilla2019) also makes the point that assuming that worsening post-sanctions trends are a consequence of sanctions would be confounding concurrent treatments. This would be especially so given how sanctions were triggered by the enactment of the Constitutional Assembly of 2017, a massive institutional shock that could have induced further production drops regardless of sanctions. Moreover, the author argues that the imposition of military control over the oil industry, which followed shortly after the enactment of the 2017 financial sanctions, could have explained further disruptions to oil production, as shown anecdotally in Reuters (2018a). The author argues that the multiplicity of relevant treatments occurring in Venezuela during this narrow period of time makes the use of synthetic control specifications inadequate for the study of the potential effects of sanctions on oil production, preemptively rebutting the validity of later findings presented in Rodríguez (Reference Rodríguez2019).

Perhaps most important in the list of initial rebuttals, Bahar et al. (Reference Bahar, Bustos, Morales-Arilla and Santos2019) extend the scope of criticisms beyond events in the oil sector. Released by the Brookings Institution, the authors first make the point that the financial nature of the 2017 sanctions did not erode Venezuela’s access to international financial markets, because such access was already closed to Venezuela due to the country’s insolvency - a point also raised by Hausmann and Muci (Reference Hausmann and Muci2019). One way to see this is through the fact that the imposition of sanctions was not followed by an increase in the country’s sovereign risk, which by that point was already 9.5 times the risk premium paid on average by emerging markets. The article then provides further evidence against the view that pre-sanctions drops in oil production were driven by low oil prices in 2016, but due to managerial factors that continued -or possibly worsened- once sanctions were enacted. That is, it is impossible to disentangle pre-sanctions trends from the effects of sanctions. Chiefly, the article extends this logic to key socioeconomic development outcomes to challenge Sachs and Weisbrot’s (Reference Sachs and Weisbrot2019) claim that sanctions “inflicted

more than 40,000 deaths from 2017–2018.” As mentioned earlier, this estimate is based on the assumption that mortality increases in this period were strictly a consequence of the 2017 financial sanctions. However, the paper shows that imports of food and medicines, infant mortality rates, and the caloric purchasing power of the country’s minimum wage were all in deep negative and worsening trends by the time that sanctions were first enacted. According to the authors, this means both that post-sanctions events cannot be plausibly disentangled from pre-sanctions trends, and that the bulk of the deterioration in living standards discussed in Sachs and Weisbrot (Reference Sachs and Weisbrot2019) preceded -and hence cannot be attributed to- the 2017 financial sanctions.

more than 40,000 deaths from 2017–2018.” As mentioned earlier, this estimate is based on the assumption that mortality increases in this period were strictly a consequence of the 2017 financial sanctions. However, the paper shows that imports of food and medicines, infant mortality rates, and the caloric purchasing power of the country’s minimum wage were all in deep negative and worsening trends by the time that sanctions were first enacted. According to the authors, this means both that post-sanctions events cannot be plausibly disentangled from pre-sanctions trends, and that the bulk of the deterioration in living standards discussed in Sachs and Weisbrot (Reference Sachs and Weisbrot2019) preceded -and hence cannot be attributed to- the 2017 financial sanctions.

Critiques on the Causal Chain: Effects of Sanctions on Essential Imports.

By this point, studies had focused on the potential effects of sanctions on oil production, or lack thereof. However, the argument extending contested evidence on oil production to the collapse of the Venezuelan economy and of Venezuelans’ living standards is implicitly based on a separate logic. As mentioned earlier, the logical “causal chain” underlying the reasoning of Venezuelan sanctions as collective punishment travels through alleged restrictions to the country’s current account: Dwindling oil production leads to a reduction in oil export revenues, which in turn limits the country’s capabilities of importing essential goods -especially food and medicines. Sanctions-induced scarcity of these imported basic staples is the main culprit behind the collapse in the country’s living standards, the argument goes.

While Bahar et al. (Reference Bahar, Bustos, Morales-Arilla and Santos2019) emphasized the drastic collapse in imports and living standards before financial sanctions were first enacted, it did not discuss how these variables evolved after the sanctions. The first paper to explicitly consider the question of whether sanctions induced a collapse in the country’s import capabilities through quantitative causal methodologies was Zambrano et al. (Reference Zambrano, Hernández and Escalante2021). Released by Anova Policy Research, the article used a regression discontinuity design to evaluate whether monthly food and medicine imports dropped discretely at the time of sanctions. Interestingly, despite estimating a negative effect of sanctions on oil production through this methodology, the authors find a positive effect of sanctions on these essential imports.

How could imports increase if oil production/exports decreased? Zambrano et al. (Reference Zambrano, Hernández and Escalante2021) presented the first iteration of the hypothesis that we outline later in this Element. Sanctions coincided with the government’s first steps towards de facto liberalize internal prices and foreign exchange rates. While this might have been a coincidence, the authors say that “it is possible to argue that the change in the government’s policy orientation, which ultimately led to the relaxation of the framework of controls, was also an immediate consequence of the tightening of financial sanctions against PDVSA. In this case, the greater external availability of food and medicine would be a consequence of the sanctions policy, at least indirectly.”

The specific statistical results of this analysis’ regression discontinuity specifications would be contested on technical grounds. Specifically, in a self-released working paper, Rodríguez (Reference Rodríguez2022b) argues that the conclusions in Zambrano et al. (Reference Zambrano, Hernández and Escalante2021) are contingent on coding errors, specific regression specification and outcome variable transformation choices, and a narrow definition for the set of product codes to be considered food. Interestingly, both papers seem to concur on the finding that there was a positive change in the “slope,” that the import collapse stopped (or came to a halt) after sanctions. This makes sense from the perspective of Bahar et al. (Reference Bahar, Bustos, Morales-Arilla and Santos2019): Once imports had collapsed so aggressively before sanctions, it was essentially impossible for them to continue falling at similar rates. This key fact is often absent from the literature: Most of the economic collapse preceded the sanctions.

This is something that Zambrano (Reference Zambrano2023) reconsiders in the context of the 2019 oil sanctions, in a “thread” only released on Twitter/X. While the aforementioned papers show that imports of food and medicines stabilized after the 2017 financial sanctions, these essential imports started to increase after the 2019 oil sanctions. While it could be argued that such improvements could have been bigger in the absence of sanctions, it is hard to look at these facts and argue that both the 2017 and 2019 sanctions led to a collapse in the availability of imported essential goods - a key step in the “causal chain” logic that sanctions worked as a collective punishment on Venezuelans. Most importantly, Zambrano (Reference Zambrano2023) argues that these changing trends, which have to do with the de facto liberalization and dollarization of the economy, warrant the question of whether the government would have pursued such drastic economic policy reforms in the absence of sanctions. If the relevant economic policy changes were triggered by sanctions, then the corresponding stabilization and improvement in living standards would be a consequence of sanctions.

Did Sanctions Cause the Venezuelan Refugee Shock?

One of the main consequences of Venezuela’s economic collapse was the resulting refugee shock that saw 25% of Venezuela’s population leave the country, mainly to neighboring countries in South, Central, and North America. A more recent strain of the literature on Venezuelan sanctions has started to focus on whether sanctions were the main culprit behind the Venezuelan exodus.

A first paper in this literature is Idrobo (Reference Idrobo2024), who argues that sanctions inadvertently weakened domestic opposition against the Maduro regime because opponents are most likely to choose to “exit” in response to worsening economic conditions (Hirschman, Reference Hirschman1970). The paper takes data from Venezuelans’ social security records capturing the year when individuals stop participating in the system. Arguing that this metric is a proxy for individuals’ migration choices, the author shows that migration after 2017 was strongest in areas with higher baseline opposition support.Footnote 14

A second paper in this literature is Rodríguez (Reference Rodríguez2025b). While not presenting original results based on quantitative causal inference methods, this article reaffirms the “causal chain” logic described earlier and leverages prior evidence on the alleged effects of sanctions on oil production to assert that sanctions explain “approximately half of the decline in living standards observed since 2012.” Based on this claim and on cross-country analysis of the connection between growth and migration, the author builds migration estimates for different sanction “scenarios” under the new Trump administration. Despite not studying the effects of prior sanctions on the Venezuelan refugee shock, the article estimates that a return to a “Maximum Pressure” sanctions strategy by the Trump administration would lead to an additional one million Venezuelan migrants.

Released by the Center for Global Development (CGD), Bahar and Hausmann (Reference Bahar and Hausmann2025) respond to Rodríguez (Reference Rodríguez2025b) arguing that the latter’s approach “fails to account for confounding variables that could influence both economic performance and migration simultaneously, such as political repression and institutional deterioration,” and “ignores the fact that much of Venezuela’s economic decline proceeded the 2017 sanctions.” Leveraging methods for time-series analyses, the authors study the association between Venezuelans’ outmigration trends and potential Venezuelan oil revenues as an inverse proxy for the imposition of sanctions. Interestingly, the authors find that higher oil prices and income are associated with an increase in the number of Venezuelans crossing illegally into the United States. The authors argue that this at first counterintuitive finding can be explained by oil revenues allowing Venezuelans to accumulate resources to face the fixed cost of migration, and by oil revenues helping the Maduro regime stabilize its ruling coalition, eroding Venezuelans’ hopes for regime change.Footnote 15

Are Claims of Sanctions as “Collective Punishment” on Venezuelans Warranted by This Evidence?

The papers discussed earlier account for the causal quantitative literature on the effects of sanctions on the Venezuelan economy. We first described an initial set of studies documenting effects of sanctions on oil production, and how those studies were contested on different grounds. We then discussed how there is a dearth of evidence that sanctions worsened access to imported essential goods and developmental outcomes, including mortality and migration. Interestingly, there is evidence in favor of the view that the collapse in imports stopped after the 2017 sanctions, and started to recover after the 2019 sanctions. We believe this point is key: Even if oil production was indeed affected by sanctions, the lack of evidence that sanctions led to a collapse in essential imports, and the evidence that import access actually improved after sanctions, constitutes a fundamental and logical breakdown of the “causal chain” of the sanctions-as-collective-punishment argument.

An important challenge in the literature studying the effects of sanctions on oil production, imports, and other developmental outcomes is the difficulty of disentangling the continuation and worsening of pre-sanctions dynamics eroding the relevant outcomes from the potential effects of sanctions. As discussed in Hausmann and Muci (Reference Hausmann and Muci2019), Morales-Arilla (Reference Morales-Arilla2019), and Bahar et al. (Reference Bahar, Bustos, Morales-Arilla and Santos2019), oil production, essential imports, and developmental outcomes were all in accelerating downward trends before the imposition of financial sanctions in 2017. As these articles argue, it is extremely difficult to conceive a sensible counterfactual for any of the relevant outcomes because no country other than Venezuela has experienced a comparable collapse. In the absence of a plausible counterfactual for what would have happened to Venezuela in any of these outcomes had sanctions not been enacted, plausible causal effects of sanctions cannot be estimated.

Perhaps most importantly, economic sanctions do not occur in a vacuum, but they are often triggered by meaningful political events and are surrounded by consequential economic events and policy choices. The financial sanctions of 2017 and the oil sanctions of 2019 are no exception. As discussed in the timeline of events, the 2017 sanctions were preceded by the curtailing of legislative prerogatives, the prohibition of a recall referendum in 2016, and by the brutal repression of massive protests and the usurpation of legislative authorities by the Asamblea Nacional Constituyente (ANC). Indeed, it was the unconstitutional creation of the ANC which triggered the 2017 sanctions, along with other diplomatic interventions like the Grupo de Lima. Finally, they were soon followed by the government’s decision to cede managerial control of the oil industry to the Armed Forces, a decision that has been discussed as greatly disruptive for operations in the sector.

Following the imposition of the 2017 financial sanctions, the executive board of PDVSA was restructured and replaced by high-ranking military officials. Reuters (2018a) documents the rise of Manuel Quevedo, a Major General in the Venezuelan National Guard, as president of PDVSA, and his appointment as the Oil Minister of the country. This report from Reuters shows how, a year after his appointment, Quevedo had- from the perspective of industry experts- implemented corrosive reforms which were expected to cause erosions in production. In light of financial sanctions, the constitutional shocks experienced in the country, and the military takeover of the oil industry, all events which may have had an important effects on the oil industry, it is difficult to parse out their specific effects in order to establish causal claims.

This problem of multiple concurrent treatments also plagued the rollout of the 2019 oil sanctions, which were triggered by the start of the constitutional crisis in late January, and were soon followed by the massive blackouts of early March. Independently, each of these concurrent treatments could have plausibly had consequential negative effects on Venezuelan economic and development outcomes in the absence of others. How do we know that the synthetic control findings in Rodríguez (Reference Rodríguez2019) were not a consequence of worsening of pre-sanctions dynamics, or of any of these concurrent events? In Rodríguez (Reference Rodríguez2022c), beyond the lack of parallel pre-treatment trends, which already renders the methodological assumptions of the paper implausible, how do we know that firms with pre-sanctions credit access were not disproportionately exposed to the institutional and operational effects of the Constitutional Assembly and of military control shocks over the oil sector? The fact that all these consequential events occurred in such proximity makes it hard to identify independent causal effects on outcomes that could plausibly be eroded by any of them.

This criticism is even more relevant for Idrobo (Reference Idrobo2024), who argues that sanctions helped stabilize the Maduro regime by inducing regime opponents to migrate. As a matter of fact, the finding that opposition individuals were more likely to migrate after the start of the Venezuelan economic crisis has been identified in other recent contributions to the migration literature (Cabra-Ruiz et al., Reference Cabra-Ruiz, Rozo and Sviatschi2024; Morales-Arilla et al., Reference Morales-Arilla, Martin and Morales2025). Idrobo (Reference Idrobo2024) uses individual records and local aggregates of formal labor force participation at a yearly level to proxy for migration. This first methodological decision is already problematic, as people may drop from the formal labor force for economic reasons other than migration. Most importantly, other papers in the literature on migration are careful not to conclude that opponents’ exit was driven by a particular separate component of the complex and intertwined political and economic events that plagued Venezuela after 2014.

The reason is that the result could be explained by any of all the meaningful concurrent events. For example, the last year of Idrobo’s (Reference Idrobo2024) pre-treatment period is 2016, a year when the opposition-led legislature was prevented from enacting any laws, and when the opposition was not allowed to pursue a constitutionally enshrined recall referendum on Nicolás Maduro. Moreover, 2017 started with an effort to illegalize the opposition-controlled legislature, which triggered massive opposition protests that were heavily repressed, and which induced the creation of the Asamblea Nacional Constituyente, which took over supraconstitutional powers in the hand of the regime. Even if economic events like sanctions, and changing living conditions had no effect on migration outcomes, these strictly political factors could plausibly explain the observed political gradient in migration.

Moreover, it is the evolution of these political events which “triggered” the imposition of sanctions, and these political events could have their own effects of the economy, along with those of other concurrent events within the same year (i.e. sanctions), the military takeover of the oil sector, among others. Moreover, as migration choices are often planned months ahead, it is perfectly possible that the flows observed in 2017 were the result of choices induced by pre-sanctions economic erosion, which accounts for the bulk of the collapse of the Venezuelan economy. It is expected for regime opponents to choose to “exit” in response to the same degree of economic duress (Hirschman, Reference Hirschman1970), but even if the results in Idrobo (Reference Idrobo2024) were driven by the worsening economic conditions and not by the targeted political discrimination and repression that they were being subjected to, claiming that the outmigration of opponents beginning in 2017 is a causal effect of sanctions relies on the implausible assumption that the prior economic trends had no effect on post-2017 migration, and that consequential concurrent events had no economic impacts.

That opponents may have chosen to leave as a response to the same pre-sanctions economic shock or to the economic effects of consequential concurrent events is compounded by the possibility of favoritism in the policy responses to said shocks and events. For instance, if Maduro’s response to the economic crisis was to discriminate in favor of its supporters and against opponents (Morales-Arilla, Reference Morales-Arilla2022; Morales-Arilla and Abbott, Reference Morales-Arilla and Abbott2024, Morales-Arilla and Traettino, Reference Morales-Arilla and Traettino2024), then the pre-sanctions macroeconomic collapse might have had a disproportionately harsh effect on the living standards of regime opponents. This adds the possibility of favoritism to the set of potential explanations for opponent migration that are not related to sanctions.

The assumptions that Idrobo (Reference Idrobo2024) needs to make to conclude that his findings are a consequence of the 2017 sanctions are not only implausible, but also untestable, given the low (yearly) frequency in his data. It is especially hard to interpret the 2017 increases in outmigration in opposition-leaning areas as a result of sanctions because the data does not allow us to observe migration choices in the narrow window between sanctions and other consequential treatments. This concern is also relevant for Zambrano et al. (Reference Zambrano, Hernández and Escalante2021), who try to estimate effects of the 2017 sanctions on oil production and essential imports by performing a regression discontinuity specification on monthly data. In our view, the most interesting result of that article is not to show a discontinuous increase in imports at the time that sanctions were first enacted, but to show that the import collapse that the country was experiencing stopped with the 2017 financial sanctions.

Finally, as discussed in Bahar et al. (Reference Bahar, Bustos, Morales-Arilla and Santos2019), there are no reasons to expect for financial sanctions to trigger immediate effects on oil production or other economic outcomes, as financial markets were effectively closed to the government and PDVSA by the time that sanctions were approved. Indeed, Idrobo (Reference Idrobo2024) claims that “sanctions and general economic decay effectively exported a significant part of the political opposition,” and that the Venezuelan refugee wave “was partly a consequence of the economic sanctions.” Unfortunately, the paper does not separate the specific effects of sanctions from those of the “general economic decay” - the majority of which preceded sanctions - from the concurrent harassment of the political opposition, from the potential favoritism in regime responses to the economic crisis, and from the economic effects of consequential concurrent shocks to the economy. Without adequately addressing these, we cannot reject the null hypothesis that the part of the effect that is determined specifically by sanctions is zero without relying on implausible assumptions.

In sum, there are three key critiques on the empirical literature arguing that sanctions worked as a “collective punishment” on Venezuelans. First, the literature fails to identify negative causal effects on imports and on development outcomes. Second, the literature does not separately identify the effects of sanctions from worsening pre-sanctions economic trends. Finally, the literature does not identify the effects of sanctions from those of meaningful concurrent treatments. Having failed to overcome these critiques, we believe the claim that sanctions eroded Venezuelans’ living standards is not warranted by the causal quantitative literature. In the following four sections, we introduce original evidence warranting further skepticism on that view.

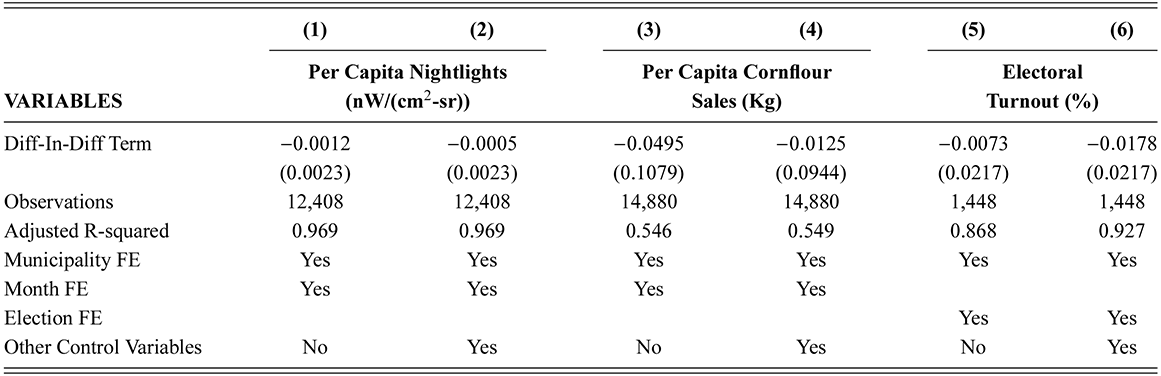

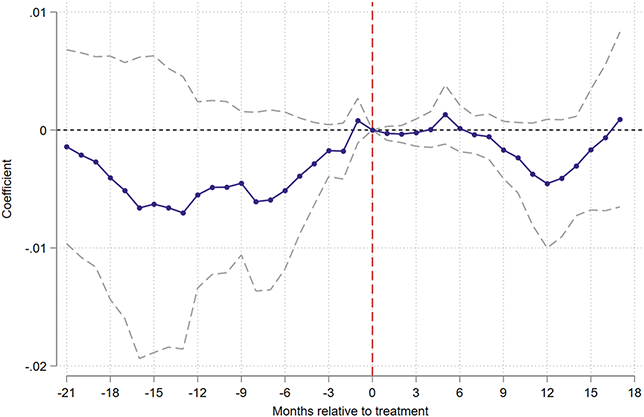

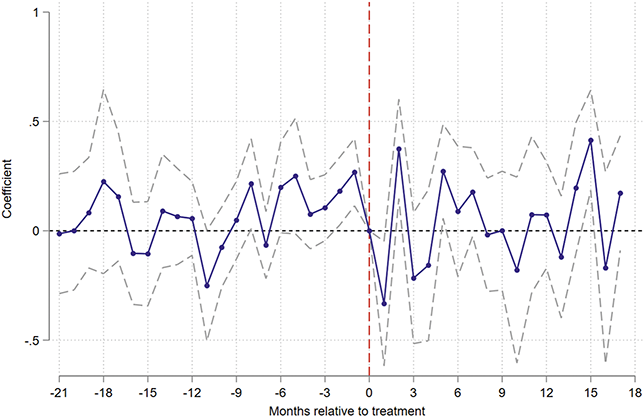

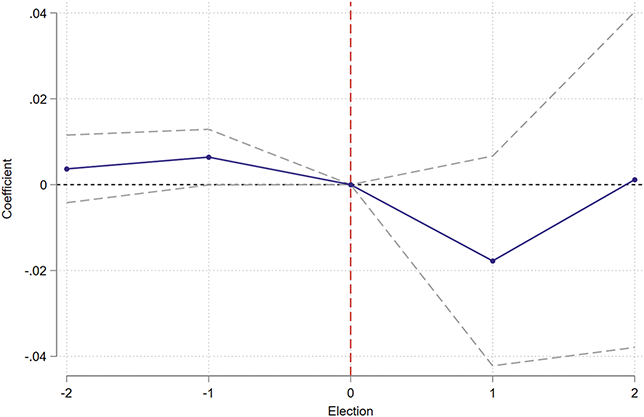

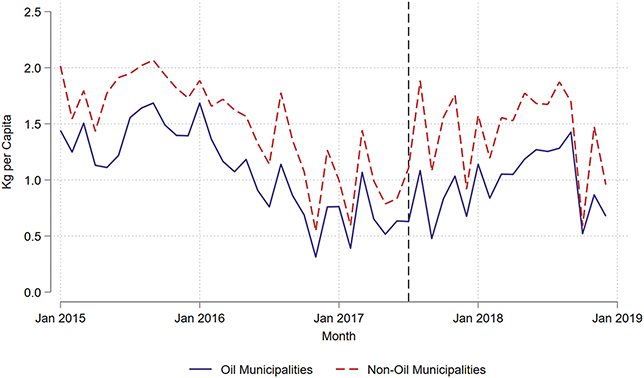

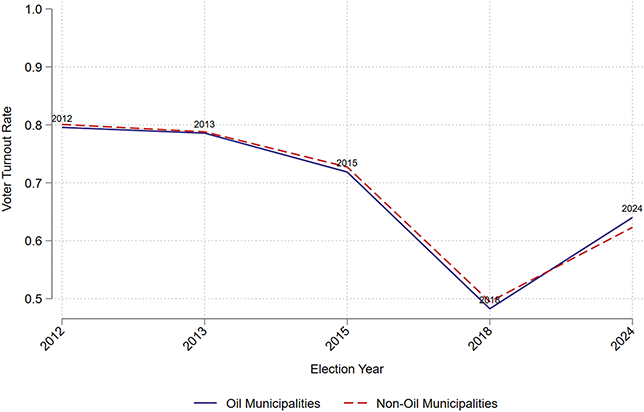

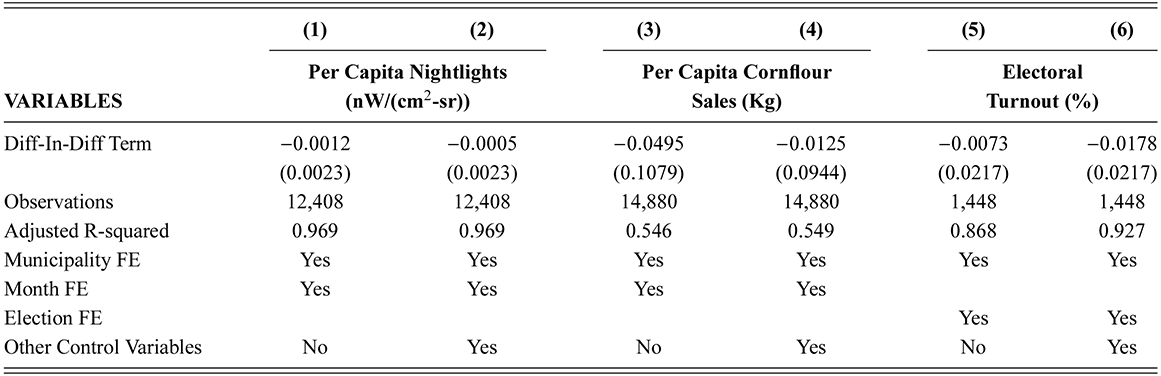

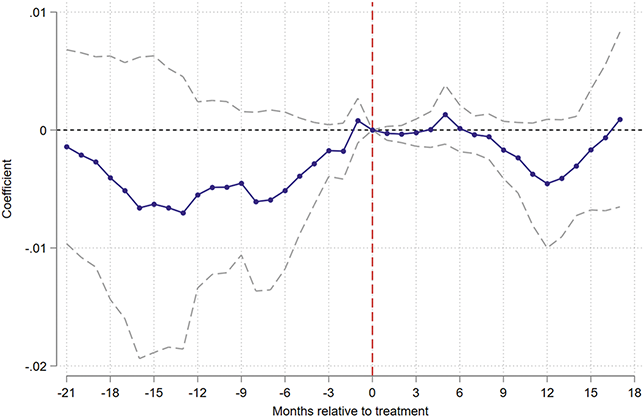

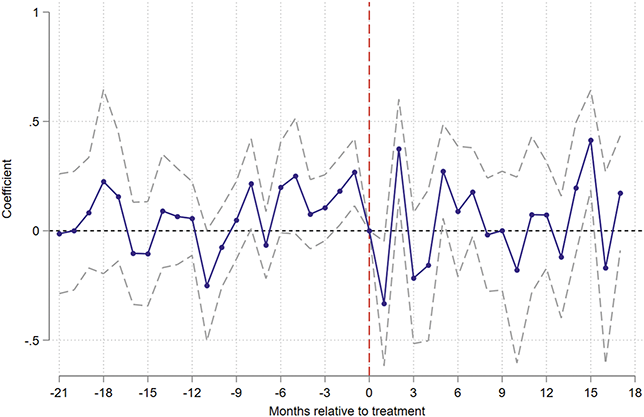

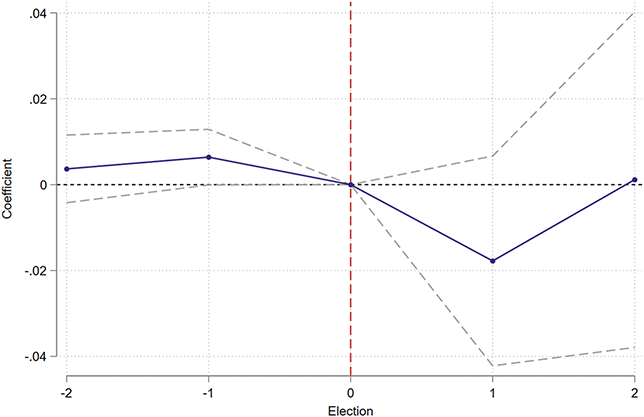

4 Case Study 1: Did the 2017 Financial Sanctions Affect Local Economic Outcomes in Oil-Producing Areas?

The Venezuelan economy is heavily dependent on its oil sector (Organization of the Petroleum Exporting Countries (OPEC), 2024; World Bank, 2025), which has long been centrally controlled by the country’s government -mainly through PDVSA, Venezuela’s National Oil Company. For this reason, it could be expected that constraints imposed on PDVSA by the 2017 financial sanctions could have had massive effects on the country’s economy. At the same time, as discussed earlier, Bahar et al. (Reference Bahar, Bustos, Morales-Arilla and Santos2019) show that financial markets were essentially already closed to new debt issuance by PDVSA, making access to fresh financing limited under the no-sanctions counterfactual. Given these contradicting expectations, and since the bulk of the literature discussed earlier has focused on how sanctions affected the Venezuelan economy starting in 2017, how can we assess if the 2017 financial sanctions affected the Venezuelan economy?

The causal chain for sanctions as collective punishment suggests that, beginning in August 2017, they eroded the Venezuelan economy by restricting access to oil export revenues, with the resulting foreign-exchange shortage triggering a collapse in imports of essential goods. This is indeed a “macroeconomic” argument that should affect the economy as a whole. However, different from the 2019 oil sanctions, the 2017 financial sanctions did not affect PDVSA’s capacity to market Venezuelan oil in the United States or elsewhere. That is, if the 2017 financial sanctions affected oil export revenues, it is not due to their effect on PDVSA’s export prices, but because of a reduction in the amount of oil it was able to produce. The 2017 financial sanctions could produce that effect if the oil sector became unable to sustain its working capital and engage in the necessary investments for maintaining its infrastructure and productive capabilities.

If this was indeed happening, the resulting macroeconomic effect should be accompanied by a disproportionate erosion of local economic outcomes in oil-producing areas of the country, as it is their main local economic activity that could be affected by sanction-induced financial constraints on PDVSA. Certainly, observing such an outcome could also be driven by the concurrent institutional and operational treatments experienced in Venezuela during the second half of 2017. However, as all these treatments should in principle affect the oil sector negatively, it would be harder to argue that the 2017 financial sanctions were especially corrosive if economic outcomes in oil-producing areas collapsed at the same rate as those of non-oil-producing areas.