1. Introduction

Private equity involvement in long-term care (LTC) has become increasingly important in many countries. In relative terms, it is significant in the United States, moderate in Ireland and negligible in Poland. Those three case studies thus provide contrasting experiences to examine why and how private equity firms invest in LTC and why private equity’s significance may vary from one country to another. The paper includes consideration of both residential (nursing homes) and domiciliary (home care) services. It also pays attention to informal care and investigates its relationship with private equity involvement in a country.

More precisely, this comparative analysis proposes to examine private equity investment (or lack thereof) in LTC along five key criteria: (1) the political debate and discourses about the role and place of private equity in LTC; (2) the empirical extent of private equity investments in LTC; (3) the reasons for private equity involvement (or lack thereof); (4) the business strategies used by private equity firms to enter LTC; (5) the regulations in place relative to private equity that facilitate or limit its involvement. In addition, we assess the degree to which the countries rely on the private formal (market) and informal (family) provision of LTCSS (long-term care services and supports). This framework provides a tool for comparative analysis of the role of private equity in LTC applicable to other countries. Methodologically, we reviewed academic, grey and policy literature relevant to each country’s experience with private equity in LTC. Due to the highly context dependent nature of the evidence gathered, country analysis follows a narrative format for each of the five dimensions describing their private equity experience. No attempt was made to use a formally systematic comparative approach although we emphasise the most significant points of convergence and divergence among our case studies. Our contribution lies largely with our identification of key issues to illuminate private equity involvement in LTC rather than in the nature of our comparative method itself. Finally, the evidence we reviewed is limited by under-reporting of private equity activities, which gives rise to, at times, substantial data gaps.

Before proceeding with our analysis, the remainder of this section outlines the political economy of LTC in each country. In the U.S., LTCSS are delivered and financed through a fragmented system combining public programmes, private insurance, and significant out-of-pocket spendings. Medicaid is the primary public payer, covering approximately 52 per cent of LTC expenditures, but eligibility for Medicaid requires beneficiaries to exhaust most personal assets first. Medicare provides limited coverage, primarily for post-acute care following hospitalisation, but does not cover extended LTC. About 11 per cent of U.S. residents have some form of private LTC insurance (Johnson, Reference Johnson2016).

The delivery system is equally complex, spanning institutional settings (nursing homes) and home- and community-based services (HCBS). Most importantly for this comparative case study, the vast majority of post-acute and LTC services providers in the U.S. are private and for-profit (Sengupta et al., Reference Sengupta, Lendon, Caffrey, Melekin and Singh2022). While nursing homes remain crucial for intensive care needs, there has been a significant shift toward HCBS, which now represents over 50 per cent of Medicaid LTCSS spending in most states (Miller et al., Reference Miller and Thunell2024). The workforce delivering these services faces challenges including high turnover, low wages, and insufficient training. Family caregivers provide substantial unpaid care, estimated at $600 billion annually in economic value in 2021 (Reinhard et al., Reference Reinhard, Caldera, Houser and Choula2023), highlighting the significant gaps in the formal care system.

In Ireland, the formal LTC system comprises residential (nursing homes) and domiciliary (home care) services. LTC is delivered by a mixed system of providers, including public (Health Service Executive, HSE), private for-profit, and non-profit. Over the last two decades, both residential and domiciliary care have been privatised and marketised significantly (Mercille, Reference Mercille2018, 2024; Mercille and O’Neill, Reference Mercille and O’Neill2021; O’Neill and Mercille, Reference O’Neill and Mercille2025) and working conditions remain relatively poor (Mercille et al., Reference Mercille, Edwards and O’Neill2022; O’Neill et al., Reference O’Neill, Mercille and Edwards2023). In 2023, private for-profit nursing homes accounted for 81 per cent of total beds compared to the public sector (16 per cent) and non-profit nursing homes (3 per cent) (HIQA, 2024a). In home care, private for-profit providers (and a small number of non-profits) deliver 61 per cent of home care hours and public provision accounts for 39 per cent (Mercille, Reference Mercille2024). Irish LTC is integrated within the national health and social care system.

The HSE manages the operation and provision of health and social care services at a national level, while also funding and directly providing a significant portion of LTC. Alongside the HSE, there are two other main public bodies involved in the governance of LTC. The Department of Health is responsible for policy and strategic oversight at a national level, while the Health Information and Quality Authority (HIQA) is the independent regulator that monitors the quality and safety of health and social care providers. Since 2009, HIQA regulates and inspects all nursing home care providers in Ireland’s LTC sector. In contrast, home care services remain lightly regulated, fragmented and of uneven quality, with no automatic entitlement to services (Kiersey and Coleman, Reference Kiersey and Coleman2017) – although a major regulatory scheme is in the process of being finalised (HIQA, 2024a). The proposed landmark statutory scheme would transform home care radically by providing entitlements to domiciliary services and implementing tighter regulation.

In Poland formal LTCSS are provided by three sectors: the health care, social assistance and private sector, all of them operating at two levels: home or in-patient facilities (Błędowski and Maciejasz, Reference Błędowski and Maciejasz2013, Wrotek and Kalbarczyk, Reference Wrotek and Kalbarczyk2023). In addition to private retirement homes or professional home caregivers there are also public LTCSS. Specifically, pensioners may use formal care at home or stationary care (Knapik, Reference Knapik2020), which includes: private rest homes, social residential homes – for retirees and pensioners who are in good health (DPS), and health sector facilities – for those who need special medical care (ZOL and ZPO).

LTC is poorly developed in Poland and public spending on LTC, which in 2019 accounted for 0.8 per cent of GDP, is one of the lowest among the EU-27 countries. There is no obligatory LTC insurance in Poland. Hence, informal care is provided by family members. Alternatively, families refer to black market, where unregistered professional home caregivers, frequently utilising migrants as underpaid workforce, are available. The current organisation of the LTC system is unsustainable taking into account the baby boomers entering old age and decreasing acceptance of traditional gender roles. Additionally, low fertility has altered the structure of families deeply towards with fewer children and childlessness. Hence, the room and also need for private providers in LTC is expected to grow rapidly in the near future.

2. Political debate about the role of private equity in LTC

The role of private equity (PE) in health and LTC has been growing in the U.S. and Europe during the last two decades (Tracey et al., Reference Tracey, Schulmann, Tille, Rice, Mercille, Timans, Allin, Dottin, Syrjälä and Sotamaa2025). A number of academic studies have concluded that private equity ownership in LTC leads to poorer quality and higher costs (Gupta et al., Reference Gupta, Howell, Yannelis and Gupta2024; Harrington et al., Reference Harrington, Olney, Carrillo and Kang2012; Stevenson and Grabowski, Reference Stevenson and Grabowski2008), but the evidence is mixed (Braun et al., Reference Braun, Yun, Casalino, Myslinski, Kuwonza, Jung and Unruh2020; Cadigan et al., Reference Cadigan, Stevenson, Caudry and Grabowski2015; Pradhan et al., Reference Pradhan, Weech-Maldonado, Harman, Laberge and Hyer2013). While private equity has received disproportionate attention in the media, from policy makers, and from academics, the quality and cost concerns associated with private equity ownership are similar to those associated with other forms of corporate ownership in LTC. While the debate in the U.S. was centred around ‘private equity [as] the latest manifestation of a long trend toward the corporatization and financialization of medicine’ (Brown and Hall, Reference Brown and Hall2024), in Ireland and Poland media attention focused also on the repercussions for publicly provided LTC.

Similarly to the U.S., the quality of LTC deteriorated also in Poland. However, because the state is the main provider of institutionalised LTC in Poland, the discussion of care quality is centred around the underfunding of the sector, which results in the deterioration of the infrastructure and burnout of the personnel (Nurzyńska, Reference Nurzyńska2022). Multiple publications in influential national journals (Wyborcza, Rzeczpospolita) highlight also scarce monitoring of LTC quality, which leads to malpractices in public nursing homes (NIK, 2024). Against such a backdrop, private equity is described in Polish media as more expensive yet more trustworthy than public LTC (Watoła, Reference Watoła2022), which is in line with the studies documenting that individuals exposed to centrally planned economic regime more often believe that the quality of private services exceeds that of public services in general (Łopaciuk-Gonczaryk and Nicińska, Reference Łopaciuk-Gonczaryk and Nicińska2025).

Regardless, private equity has clearly garnered special attention recently in the U.S. and there may be reasons for this concern. Brown and Hall (Reference Brown and Hall2024) argue that, even if other forms of for-profit ownership are also at risk for poor outcomes, private equity may be uniquely prone to rely on short-term profits, a reliance on debt, ‘and the insulation from professional and ethical norms’ that make them more likely than other investors to emphasise opportunities to maximise profits (Brown and Hall, Reference Brown and Hall2024).

The worry that private equity involves a particularly acute threat to LTC quality has generated attention from some policy makers at the federal and state level in the U.S., but as with attention to nursing homes generally, this attention has been sporadic and policy actions to improve the situation have been limited (Miller et al., Reference Miller, Nadash and Gusmano2020). In 2022, during his second State of the Union address, President Biden highlighted the role of private equity in the nursing home industry. This was not surprising because the poor performance of nursing homes during the Covid-19 pandemic acted as a ‘focusing event’ (Kingdon, Reference Kingdon1995), that generated greater political focus on nursing home quality. In Ireland, large investors, often private-equity backed, have consolidated the nursing home market, leading to the closure of small, family-owned facilities. This generated attention in public discourse, although critical commentary about provate equity involvement has not been overly strong. In Polish political debate, highly dominated by the conflict between two main parties over the rule of law and the war in the Ukraine, the criticism has been voiced mainly by the citizens and activists, leading to minor increase in financial benefits, but no action related to the structure nor organisation of LTC. When private LTC is discussed, it is usually brought up as an alternative to poor quality and limited access to public LTC services. In other words, unlike in the U.S., the issue has not received a large amount of attention in relative terms in Ireland and certainly not in Poland. However, in Poland the regulations concerning the minimum requirements for LTC have been defined in a bill from 2004, while no such legislation exists in the U.S.

One consequence of placing nursing homes in the spotlight was greater attention to ownership differences, with a particular focus on the role of private equity (Atkins, Reference Atkins2021). President Biden gave voice to these concerns when he said, ‘As Wall Street firms take over more nursing homes, the quality in those homes has gone down and costs have gone up. That ends on my watch. Medicare is going to set higher standards for nursing homes and make sure your loved ones get the care they deserve and that they inspect and will get looked at closely’. Most of the subsequent policy efforts proposed by the Biden administration, which included regulations to establish minimum standards for staffing adequacy at nursing homes and additional money for health and safety inspections, were not targeted at private equity, specifically, but were designed to increase ownership transparency requirements.

Transparency has been the focus of the limited policies that have been adopted by the federal and state governments to regulate private equity in health and LTC in the U.S. Transparency is an understandable focus because it is extraordinarily difficult to know when private equity is an owner, or has an ownership stake, in U.S. nursing homes. The ownership structures of many U.S. nursing homes are remarkably complex and without transparent information it is impossible for government regulators or the public to know enough about the implications. Nursing homes often have several layers of ownership. Indeed, as we discuss later, one of the strategies that private equity firms use is to disaggregate a nursing home chain into several different companies. Similarly, private equity often creates auxiliary businesses to syphon money from nursing home operations. For example, when a private equity firm purchases a nursing home, it may create a separate rehabilitation company that provides therapy services to the nursing homes it owns. This may help to mask the ownership of the nursing home because, although the private equity firm may have a substantial ownership interest in these ancillary companies, it may have only a minority ownership stake in the nursing home itself. As a result, they may not meet the ownership threshold that requires reporting to the federal government (GAO, 2023).

As the markets for nursing homes in Ireland and Poland are smaller, similar concerns are absent in the political debate there and most public discussion of nursing home does not include the issue of private equity. For example, a Nexis news search for the two years prior to mid-March 2025 returned 498 articles whose key subject was nursing homes from Ireland’s four main news sources (Irish Times, Irish Independent, Sunday Independent, RTE News); however, only 15 of those mentioned private equity. The bulk of the 498 articles addressed issues like nursing home costs, business transactions, or regulation issues. Normatively, public discourse is both supportive and critical of private for-profit involvement in LTC. For example, public discourse often mentions that public funding to private nursing homes should be increased because the latter face increasing costs, and that private nursing homes manage to operate with lower levels of funding than public nursing homes. An Irish Times editorial is illustrative of the public discourse in general:

‘There is nothing inherently wrong with the provision of residential care by the private sector or indeed the reliance on private equity for financing. But it must be understood that the State and private equity have competing objectives. The State wants high standards of care and value for money. Private equity wants to maximise profits and repay its lenders. In some cases – where the nursing home is owned by a separate, tax-efficient vehicle – the pressure for profit maximisation is intensified and exposure to risks such as interest rate hikes increased.’ (Irish Times, 2024). The anti-competitive risks related to market concentration are also noted: ‘There is also the potential danger that the greater the market dominance of the private equity-funded providers, the greater their power and ability to push up prices and push down standards.’ (Irish Times, 2024).

Beyond the regulatory efforts of the Biden administration, the U.S. Congress has also paid attention to this issue in recent years. The Senate Budget Committee and the Senate Finance Committee have held hearings focused on the role of private equity. Senator Edward Markey (D-MA) introduced the Health Over Wealth Act, which calls for greater reporting by private investor-owned organisations in health care (Scheffler and Blumenthal, Reference Scheffler and Blumenthal2024). Similarly, in 2021, Senators Elizabeth Warren (D-Mass.),Tammy Baldwin (D-Wis.), Jeff Merkley (D-Ore.), Bernie Sanders (I-Vt.), Tina Smith (D-Minn.), and Ed Markey (D-Mass.), along with Representatives Mark Pocan (D-Wis.), Pramila Jayapal (D-Wash.), Raúl Grijalva (D-Ariz.), Rick Larsen (D-Wash.), Barbara Lee (D-Calif.), Delia Ramirez (D-Ill.), Jan Schakowsky (D-Ill.), Alexandria Ocasio-Cortez (D-N.Y.), and Delegate Eleanor Holmes Norton (D-D.C.), reintroduced the Stop Wall Street Looting Act, which would increase transparency requirements, increase liability, and reduce the capacity of private equity to hide assets. The bill does not focus, primarily, on private equity’s involvement in LTC, but the text of the bill justifies the increased regulation by asserting that, ‘private investment funds have also targeted entities that serve low-income or vulnerable populations, including affordable housing developments, for-profit colleges, payday lenders, medical providers, and nursing homes’ (S.5333). The Senate Committee on Banking, Housing, and Urban Affairs held hearings on this bill in September of 2022, but the Congress took no subsequent action on it. Senator Warren reintroduced the bill in 2024. With Republican control of both chambers of Congress following the 2024 election, neither of these legislative efforts are likely to be adopted.

It is also unlikely, in the near future, that the Trump administration will pursue any additional efforts to regulate the nursing home industry or reduce the role of private equity. During the first several months of the second Trump administration, LTC policy has received relatively little attention, but there are good reasons to believe that President Trump may reverse the efforts of the Biden administration. As a presidential candidate leading into the 2024 election, Trump focused on increasing the trend toward shifting LTC from nursing homes to home- and community-based LTCSS. In particular, candidate Trump called for creating tax credits that would offer a greater incentive for family members to care for people in need of LTC at home (Siddiqi, Reference Siddiqi2024). During his first term in office, President Trump reduced nursing home inspections (Siddiqi, Reference Siddiqi2024). Similarly, in 2019 the first Trump administration proposed regulations to reduce the frequency of facility inspections and a variety of workforce requirements. Due to the outbreak of Covid-19, these regulations were never finalised, but it is likely that the current Trump administration will reissue these or similar regulations, and it is not yet clear whether the administration will enforce the Biden era transparency requirements (Kaiser Family Foundation, 2024).

In the absence of new federal efforts to address the role of private equity in LTC, most of the action during the next few years will likely be at the state level. Currently, more than 12 states have enacted laws to regulate private equity in health and LTC (Scheffler and Blumenthal, Reference Scheffler and Blumenthal2024). Nearly all of the states that have either adopted or are considering policies to regulate private equity are controlled by Democrats (Gaivin, Reference Gaivin2024). As with other dimensions of U.S. health policy and politics, there is a growing divide between how Democratic and Republican controlled states, with greater efforts to expand the role of government in Democratically controlled states, and a greater reliance on deregulation and reduced government spending in Republican states (Gusmano and Thompson, Reference Gusmano and Thompson2025).

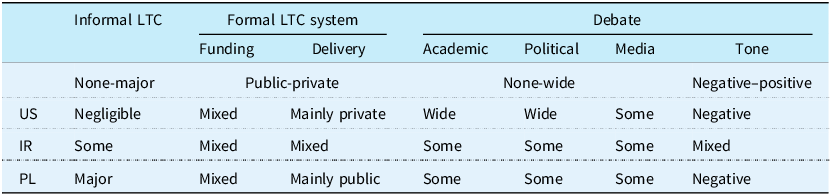

Similarly to Ireland, private equity has been mostly discussed in Poland in relation to residential care (nursing homes). In contrast to the U.S. and also Ireland where home care has become largely dominated by private equity, in Poland the political debate on LTC is focused on family caregivers (Abramowska-Kmon and Szweda-Lewandowska, Reference Abramowska-Kmon, Szweda-Lewandowska and Woycicka2022; Błędowski, 2021). In addition, the debate on formal caregiving considers first, the public financial support to the family (informal) caregivers and second, the public providers of LTC to childless elderly individuals in the form of institutionalised care. The public debate often raises concerns on the caregiving burden especially for female primary caregivers (both mothers of disabled children and wives or daughters caring for their husbands or parents respectively) (Chutnik et al., Reference Chutnik, Szumlewicz and Urbańska2023). Table 1 summarises the comparison of the LTC systems in the examined countries.

Dimensions of the LTC system organisation and political debate on LTC

Similarities and Differences: Our comparison of the political debate on the role of private equity in LTC reveals how cultural, historical, and political contexts shape each country’s approach to this phenomenon. Although an enormous amount of funding for LTC is private, the U.S. relies heavily on the private sector for its delivery and, not surprisingly, it has experienced significant private equity involvement in this sector. Ireland has a mixed public and private system with a growing private equity presence. In contrast, Poland relies primarily on state-provided institutional care with family caregivers as the main support system. The market-driven nature of the LTC system in the U.S. offers fertile ground for PE involvement. After years of perceived poor outcomes, this has resulted in a more sceptical public. Ireland’s ‘mixed’ system and the government’s (tacit) support for PE reflect a kind of fiscal pragmatism. Private equity is viewed as a helpful source of capital investment to expand capacity that the state is unwilling to fund, particularly in an era of constrained public budgets. Conversely, Poland’s historical distrust of state-managed systems has inverted the public reaction, viewing PE as a preferable, albeit expensive, alternative. In the U.S. where private equity has experienced a great deal of negative media attention, there is growing scepticism toward private equity among the public. In Ireland, there are mixed views with some criticism, but also recognition of the private sector’s role in LTC and recent government policies have encouraged the growth of private equity.

Not surprisingly, the political attention this issue has received mirrors the level of involvement of private equity in each country’s LTC system. Given its significant involvement in LTC, private equity has received greater attention from policy makers in the U.S. than either of the other countries, but it would be misleading to suggest that this attention has been significant or sustained. Political attention in Ireland has been moderate, and this issue is a low political priority in Poland, where policy makers are more focused on the rule of law and concerns about the Russian invasion of Ukraine.

3. What is the extent of private equity ownership in LTC?

There is little doubt that private equity has increased its involvement in LTC in the U.S. during the past 25 years, while in Ireland PE funds have entered the Irish nursing home sector and expanded dramatically only in recent years. In 2016, PE funds were largely non-existent in the Irish nursing home sector, which appears to be the current reality in Poland, although the extent of PE involvement is difficult to assess in Poland, similarly to the U.S.

One study found that between 1998 through 2008, there were 77 acquisitions of nursing home chains by private equity in the U.S. (GAO, 2010). Some of these included land and operations, but others focused only on the acquisition of real estate or operations alone. Frequently, nursing homes were bought and sold multiple times by different private equity firms. A study published by the National Bureau of Economic Research in 2021 offered evidence that the percentage of nursing homes owned by private equity firms increased from one percent in 2005 to nine percent in 2015 (Gupta et al., Reference Gupta, Howell, Yannelis and Abhinav2021). A 2010 study published by the U.S. General Accountability Office (GAO), estimated that private equity controlled about 12 per cent of nursing homes in the U.S., but in 2024, the GAO estimated that private equity owned about five percent of nursing homes in the U.S. It is possible that private equity ownership of nursing homes has declined in recent years, but the GAO admitted that the real number was probably higher than five percent, and that the complex ownership structure of nursing homes in the U.S. made it difficult to know (GAO, 2023).

In Ireland, PE funds and real estate investment trusts (REITs) have entered the nursing home market and expanded rapidly. In 2016, investment funds were largely non-existent, but by 2022, 14 out of the top 15 nursing home operators (in terms of beds) were either partially or fully owned by PE funds and/or REITs (O’Neill and Mercille, Reference O’Neill and Mercille2025). Further, the top-10 PE funds and REITs (in terms of beds) held 31 per cent of total nursing home beds in Ireland in their portfolios (O’Neill and Mercille, Reference O’Neill and Mercille2025). Government expenditure is also a useful proxy for the market share of PE- and REIT-owned nursing homes. Between 2017 and 2022, the amount of government funding received by the top-10 nursing home groups (in terms of beds; all of which are PE- and/or REIT-owned) nearly doubled from 14 per cent to 27 per cent of overall government expenditure (O’Neill and Mercille, Reference O’Neill and Mercille2025). In the home care sector, the top-4 private providers in terms of public funding received (Home Instead [now renamed Dovida], Bluebird, Comfort Keepers, and Irish Homecare) are all PE-owned. We can also use government funding as a proxy for their significance and market share. In 2024, the top-4 PE-owned care providers received approximately 30 per cent of overall government spending on the home care sector (authors’ calculations based on Health Service Executive (2024) and Home and Community Care Ireland (2025)).

For Poland, the official Central Statistical Office data document 84,584 beds in social residential homes and 27,068 in private rest homes (GUS, 2024). If we compare the number of beds to the population of elderly people, Poland ranks at one of the last places across European countries. There has been a significant increase in the number of places in private rest homes in recent years (13,500 in 2018), significantly higher than in public facilities (82,800 in 2018). Importantly, private LTC services in Poland are developed in the regions with the presence of markets for such services, that is usually larger cities and their suburbs. Costs of private nursing homes as compared to the median earnings are significant, despite some regional disparity within the country, while the public LTC can be subsidised by the local government. The data on the PE involvement in the Polish LTC sector are scarce, and difficult to proxy with other measures such as REITs, because respective regulations in Poland are at development stage (Bojańczyk, Reference Bojańczyk2025).

The risks associated with the ongoing privatisation of LTC in Poland received most attention in the previous decade in the academic literature (eg. Jurek, Reference Jurek2012; Szukalski, Reference Szukalski2011; Szweda-Lewandowska, Reference Szweda-Lewandowska2014), which had little impact on the decision-makers. Such an approach to health-related policy making has dominated the health care system since the transition (Berman, Reference Berman1998) leaving room for free markets to emerge. Table 2 summarises relevant dimensions of the PE involvement in the examined countries.

Relevant dimensions of PE involvement in LTC sector

Similarities and Differences: All three countries have experienced some degree of privatisation in the LTC sector and in all three, there are challenges in accurately assessing the full extent of private equity ownership due to complex ownership structures. Despite this, the best evidence suggests significant differences in private equity involvement in LTC among these countries. The U.S. has a much longer history of private equity involvement in this sector. Private equity has been active in the U.S. nursing home sector for at least 25 years. In Ireland, private equity involvement has been more recent, but the country has experienced rapid growth in private equity ownership in recent years. Private equity was largely non-existing in 2016, but by 2022, 14 of the top 15 nursing home operators were either partially or fully owned by PE funds and/or REITs, and the top 10 private equity and REITs held 31 per cent of total nursing home beds in Ireland. Beyond nursing homes, the top four private home care providers are private-equity owned. In Poland, private equity is largely non-existent in the nursing home sector as of 2025, but there has been growth in private rest homes, particularly in urban areas.

4. What are the reasons for private equity involvement in LTC (or lack thereof)?

Why has private equity expanded its involvement in LTC in certain countries and in others not? It is important to recognise that about 70 per cent of nursing homes in the U.S. were for-profit organisations before private equity investments in this industry began to grow, so the structure of these corporations were already in line with the goals of private equity, similarly to Ireland but unlike Poland.

Population aging is attractive to PE funds looking to invest in the LTC sector, as it results in more demand for residential and domiciliary services. Ireland is at the beginning of a period of rapid growth in its aging population, and this has attracted PE to the LTC sector because demand translates into a stable stream of income. Data from the Central Statistics Office estimate that by 2051, the population in Ireland aged over 65 will double to 1.6 million (Central Statistics Office, 2022). The biggest increase will be in the over 80 age cohort (predominant users of LTC services), which is expected to dramatically rise from 150,000 in 2016 to 550,000 in 2051 – a 271 per cent increase (Central Statistics Office, 2022).

All examined countries in addition to population aging are characterised by reliable public funding of LTC (traditionally present in European welfare states and in the U.S., through Medicare and Medicaid), which make this sector attractive (Field et al., Reference Field, Furrow, Hoffman, Lownds and Pearsall2023). These two factors helped to reduce the risks associated with investing in nursing homes, while public insurance payment rules and lax quality oversight offered opportunities to increase revenue in the U.S.

Interest by private equity in nursing homes increased significantly during the early 2000s after many of the publicly traded nursing homes in the U.S. had experienced significant financial difficulties. The Balanced Budget Act of 1997 reduced payments for nursing home services and contributed to a growing number of bankruptcies in the industry between the late 1990s and early 2000s (King, Reference King2019; Kitchener et al., Reference Kitchener, O’Meara, Brody, Brody, Lee and Harrington2008). PE firms responded to this opportunity by acquiring nursing home facilities at low prices (Duhigg, Reference Duhigg2007). Similar opportunities exist in Ireland, where PE funds are attracted to fragmented sectors where there is potential for market consolidation and significant expansion – which means growth potential, economies of scale, and large market shares for PE which can take advantage of the situation (O’Neill and Mercille, Reference O’Neill and Mercille2025). Indeed, once a few large global PE funds entered the Irish LTC sector and began to expand, a spotlight was shone on its fragmented composition which is favourable to PE funds looking to consolidate.

Furthermore, PE funds are increasingly drawn to Ireland’s LTC sector as a source of portfolio diversification to minimise investment risk (O’Neill and Mercille, Reference O’Neill and Mercille2025). Diversification is important to PE because it can spread their risk in terms of economic sector and geography. For instance, a PE fund investing in healthcare may be present in cure and care with investments in hospitals, clinics, nursing homes, and home care providers across several different countries globally. This means that if regulations or policies change in a given sector or country, it does not impact all of their assets at once and the potential risk is diversified.

In addition, PE is attracted to the stable government funding flowing to Ireland’s LTC sector because it serves as a state-backed and reliable stream of income to underpin their investment (O’Neill and Mercille, Reference O’Neill and Mercille2025). This is the bottom line when it comes to PE involvement in Irish LTC. There must be returns (usually measured as ‘EBITDAR’ – Earnings Before Interest, Taxes, Depreciation, Amortisation, and Rent) and a secure source of income to ensure the financial viability of their business. EBITDAR is a financial metric used by PE firms when deciding whether to invest in an LTC provider or not.

Finally, regulation is an important factor driving PE involvement in LTC. In the nursing home sector, the regulatory system (through HIQA in Ireland and a respective bill in Poland (Ustawa Nr 64, 2004)) is attractive to PE because it ensures minimum quality standards in the private for-profit providers they own/invest in – which is particularly attractive to transnational PE who are not physically located in the country and do not have in-depth knowledge of the LTC sector (O’Neill and Mercille, Reference O’Neill and Mercille2025). PE funds view the regulation system in a positive light because they perceive it as lowering the risk of investing in the market by ensuring minimum quality standards. Specifically, home care is currently lightly regulated in both countries, and there is no automatic entitlement to services, which remains discretionary.

The highly anticipated statutory regulation scheme in Ireland would transform home care radically by providing entitlements to domiciliary services, which would necessarily involve more state funding to support the sector – which is appealing to PE investors. The scheme would also implement tighter regulation of the sector. At this stage, dominant actors in the market are of the opinion that the market should be more regulated rather than expanded, and this is what the upcoming scheme is expected to do (Mercille and Lolich, Reference Mercille and Lolich2024). Private home care providers are supportive of the scheme for two main reasons (Mercille and Lolich, Reference Mercille and Lolich2024). First, the anticipated increases in stable public funding is key to ensuring profits for investors. Second, tighter regulations are expected to benefit large, established providers with deep resources (financial, staff, IT, organisational) to meet those regulations. A number of small providers are likely to disappear due to their inability to meet those regulatory requirements. In other words, the statutory scheme should benefit large providers and the investors that own and control them.

Despite the opportunities listed above, PE and private LTC in general in certain cultural contexts are limited due to the barriers in social norms and individual preferences. The intergenerational contract in Poland had been shaped by familiaristic relations in the past, but it is subject to a slow yet persistent shift in younger generations. While older generations expect to age at home and receive support from children (especially daughters or daughters-in-law), younger Poles are more and more open to formal care and less willing to provide such care to aging parents (Costa-Font and Nicińska, Reference Costa-Font and Nicińska2023), creating more room for PE in LTC. Despite rapid population aging in Poland, demand for nursing homes remains low due to strong traditional social norms expecting the family member (usually a child) to be a primary caregiver, especially with respect to older parents, which still prevail in selected European countries (Greece, Italy, Poland, Portugal, and Spain,) yet not anymore in Ireland (Verbakel, Reference Verbakel2018). These similarities suggest that cultural norms that place responsibility for LTC in old age in the family and the state, not mainly markets as in the U.S., limit PE expansion. With the expected and ongoing changes in the social norms, one might expect respective shifts in PE involvement in the LTC sector.

Furthermore, current generations of older Poles expect in majority to age in place and be taken care of by a close one (preferably a child) (European Commission, 2007). Some researchers argue that Polish society was trapped by intergenerational solidarity (Krzyżowski, Reference Krzyżowski2011), which is reinforced by the specific post-communist contexts. A strong reliance on state support in the need for care over dependent family members (Costa-Font and Nicińska, Reference Costa-Font and Nicińska2023) and the long-lasting perception of health care available free of charge (Tymowska, Reference Tymowska2001) might lead to relatively low propensity to pay for the formal institutional care. It seems that only when informal care, home-based care services and public nursing homes are unavailable, then the private market is considered as an alternative. Private equity is a new actor in this traditional setting and it is not surprising that market services develop when the risks are minimal and profits substantial, which is not the case in Poland as of now. Summary of the barriers and opportunities for PE developments in LTC sector are summarised in Table 3.

Barriers and opportunities for PE involvement in LTC sector

Similarities and Differences: There are some key policy, market and cultural differences that help to explain why these three countries have experienced such different levels of private equity involvement in their LTC systems to date. The structures of the LTC markets in the three countries before the emergence of private equity’s interest in this sector were strikingly different. Family care plays a major role in all three countries, but the U.S. and Irish systems already relied significantly on private sector delivery and had for-profit structures that were aligned with private equity’s goals. In contrast, Poland’s post-communist context creates a strong reliance on state support and the perception of health and LTC as a good that should be available free of charge. In contrast to Ireland and the U.S., in which pre-existing market structures served as enabling conditions for private equity, Poland’s combination of extensive public systems and the cultural expectation of free care, creates significant structural and political barriers to entry for private equity. These conditions limit the opportunities for PE and help to explain its minimal role in comparison with Ireland and the U.S. As a result, Poland relies predominantly on a public system and places an even greater emphasis on the importance of family care than the other countries, so opportunities for private equity appear to be more limited.

5. What are the business strategies of private equity in LTC?

Private equity uses several techniques to increase the profit margins of the nursing homes they own. One approach in the U.S. is to charge Medicare and Medicaid for more expensive procedures than were actually performed (upcoding) or to charge for services that were never provided or were not needed (Bowers, Reference Bowers2024). Beyond coding, private equity purchases or creates ancillary companies that provide goods or services to nursing homes, offer opportunities to generate additional revenue, limit legal liability, while simultaneously masking the role of private equity. The ancillary companies created by private equity charge high prices to the nursing homes and serve as another source of revenue, while masking the level of private equity ownership in the industry. In addition to creating companies that sell a variety of services to nursing homes, private equity often creates real estate companies that purchase the land on which nursing homes exist. This allows them to generate additional revenue by charging the nursing homes company rent on the land it had previously owned. This strategy is reinforced by the compensation structure used at most private equity firms because they also charge transaction fees, so the firm receives additional payments beyond the ordinary profits associated with the real estate leaseback (Federal Trade Commission, 2024). A consequence of siphoning this additional money from the nursing home is lower investment in staff and reduced quality (Meyer, Reference Meyer2024).

In Ireland, the ‘OpCo/PropCo’ (operating company/property company) business model is the most important strategy that PE funds have used to enter and expand in Ireland’s nursing home sector (O’Neill and Mercille, Reference O’Neill and Mercille2025). The OpCo/PropCo model separates the physical nursing home property (real-estate) from the operations and services provided (operating business). The nursing home property is owned by a PropCo and the nursing home business operations are owned by an OpCo. The OpCo is responsible for the daily operation and management of the nursing home, which involves care provision, staffing, administration, and the overall delivery of services to residents. The PropCo owns the physical property/real-estate of the nursing home and is responsible for the development and maintenance of the facility. Typically, the OpCo is a nursing home group owned (partially or fully) by PE and the PropCo is a real-estate investor such as a REIT. The PropCo leases or rents the nursing home property to the OpCo, similar to the relationship between a tenant and landlord.

A lot of the time, the OpCo/PropCo model is not used to develop new nursing homes but to take over existing ones through mergers and acquisitions (M&As). It is common for the OpCo itself to originally own the nursing home property, prior to selling it to the PropCo, who subsequently leases it back to the OpCo (known as a ‘sale-leaseback’ agreement). In the Irish context, a typical example of how this works is that a PE fund enters the market by acquiring an incumbent Irish-based nursing home group and then sells the underlying property to a REIT. In this instance, the PE fund and the REIT can coordinate the purchase of the operating company and the real estate assets. There are several cases of this happening in recent years, such as Waterland (Dutch PE) buying out Silverstream (large private for-profit nursing home group in Ireland) and in the subsequent years selling the property to Aedifica and Care Property Invest (Belgian REITs). This strategy has proven a quick and effective way for PE to grow their market share and consolidate in the Irish nursing home market.

In the home care sector, PE has entered through two basic processes (O’Neill and Mercille, Reference O’Neill and Mercille2025). First, at the global level, PE has invested in the head companies that have activities in Ireland. For example, Wellspring Capital bought Bluebird Care, Comfort Keepers is owned by Heritage Group, and Home Instead was bought by Honor which is backed by several venture capital and investment bodies. Second, more directly, PE has penetrated the Irish market by acquiring Irish companies and master franchises of global companies. For example, Home Instead’s Irish master franchise (now renamed Dovida) was bought by a group backed by Unigestion, a Swiss PE company (the same process was used to buy Home Instead master franchises in France, the Netherlands, Austria and Switzerland). This has essentially moved the Irish market from one whose master franchises were owned by Irish businessmen to one where the owners are PE funds, a significant ownership change.

To attract clients, private LTC providers position their services in opposition to the public nursing homes, and offer single room, location in green and quiet neighbourhoods of large cities, rehabilitation services, constant nurse presence, regular medical monitoring, and friendly atmosphere where clients can feel ‘at home’. Pricing policy depends on the selection of services offered.

Similarities and Differences: In the U.S. and Ireland, where private equity is already playing a role in the LTC systems, these companies use a host of similar strategies to generate profit. First, in both countries, private equity uses property-related strategies to extract profits from nursing homes. In the U.S., private equity creates real estate companies to charge rent to nursing homes; in Ireland, the ‘OpCo/PropCo’ model similarly separates property ownership from operations. In both countries, there is evidence that private equity creates or uses secondary businesses to generate additional revenue streams from nursing homes. The U.S. LTC financing system offers additional opportunities to generate profit through ‘upcoding’ (charging for more expensive procedures).

6. Regulating private equity

To date, no regulations on specific regulations on PE in LTC are present in any of the examined countries, however in Poland the requirements for the quality of institutionalised care have been regulated for more than two decades.

Policy makers in the U.S. have focused on ownership transparency, but efforts beyond that have been limited. The Biden administration had proposed to increase nursing home workforce requirements and nursing home inspections, but following the 2024 election, these efforts have been abandoned by the Trump administration. Some scholars argue that it may be possible to reduce the role of private equity, and other corporate ownership, if the federal government required greater capital improvements of nursing home buildings (Feder and Schwartz, Reference Feder and Swartz2021). Doing so would make it harder for private equity owners to extract profit from nursing homes because they would have to make substantial investments in the nursing homes they acquire (Feder and Schwartz, Reference Feder and Swartz2021). This, however, would also require increased inspections and enforcement of these requirements. The Biden administration was motivated to make such policy changes, but was limited by Congress. It is highly unlikely that the Trump administration and Republican controlled Congress, which are focused on making enormous reductions to the Medicare and Medicaid programmes, and gutting the capacity of the federal government to enforce regulations, will pursue these ideas during the next four years (Schubel, Reference Schubel2025).

There is a relative absence of existing regulations/legislation that focuses on the involvement of PE and REITs in Irish and Polish LTC. HIQA regulations apply quality and safety standards that monitor care but do not engage with ownership issues, including those relating to PE and REITs (HIQA, 2024b). In general, the Irish state has indirectly facilitated the entry and expansion of PE and REITs due to the significant marketisation of LTC (O’Neill and Mercille, Reference O’Neill and Mercille2025). Indeed, without an established LTC market and private for-profit providers, fewer opportunities exist for PE and REITs to take over (Aveline-Dubach, Reference Aveline-Dubach2022; Hoppania et al., 2022).

In Poland, the bill regulating LTCSS dates back to 2004 (Ustawa Nr 64, 2004). Specifically private providers of LTC are encouraged to reduce the shortages in available formal care by the VAT exemption. In comparison to other entrepreneurial activities, opening a private nursing home is relatively easy with a reasonable amount of paperwork, yet might be time-consuming because the facility must be subject to a study visit by the officials. The permission to operate is given for a defined time period. No specific skills, experience nor formal education of the owner is required for opening a nursing home. Most regulations concern the requirements related to physical infrastructure in the nursing home (no physical barriers in the building and its surrounding; parking places, elevators, doors of a required width, max 3 persons in a room, all beds must be a rehabilitation bed, at least one toilet per 4 persons and one bathroom per 5 persons, showers, bathrooms, and toilets must be adapted to the needs of elderly). As for other requirements, the regulations are less specific. Personnel are required to have nursing qualifications or documented experience in the job of at least 2 years; support in (instrumental) daily life activities must be provided to the clients, and contact with the family and friends must be ensured. Although regular controls of the requirements by the local authorities are allowed, they are not frequent. Table 4 succinctly summarises the regulations relevant to LTC sector.

State regulations of LTC sector

Similarities and Differences: The policy response to private equity has been equally muted in all three countries. Even in the U.S., where private equity has a greater presence, there has been only limited federal regulation with increasing state-level action. Ireland has adopted some regulatory standards affecting smaller facilities and Poland has yet to adopt new policies that would regulate private equity beyond the existing minimum requirements for LTC, which have been in place for more than 20 years.

6. Conclusions

The comparative analysis of private equity involvement in LTC across the United States, Ireland, and Poland reveals significant insights into the interplay between markets, states, and cultural contexts in shaping policy outcomes, along the dimensions identified in the present study. However, it is important to note the significant differences in size, internal diversity, levels of income and spending across the examined countries.

First, these cases highlight the influence of path dependency on market development. Countries with pre-existing privatised care systems (such as the US and Ireland) have seen substantial private equity involvement, while Poland’s state-centred and family-oriented system has created barriers to private market development and institutional instability in recent decades along with a lack of obligatory LTC insurance, might prevent private equity entry due to high risk and low expected gains. This underscores how historical institutional arrangements can both constrain and enable specific policy trajectories.

Second, political attention to private equity in LTC tends to correlate with the degree of market penetration, yet remains remarkably limited across all three countries. Even in the U.S., where private equity has received significant attention and criticism is fiercest, regulatory responses have been minimal, focusing primarily on transparency rather than structural reform. This suggests that the political influence of financial interests plays a significant role in limiting regulatory oversight, regardless of the type of system in place.

Third, these cases underscore how cultural contexts shape market opportunities. Polish caregiving norms, influenced by traditional family roles and post-communist expectations of state-provided care, create a different market environment compared to the more individualistic U.S. context or Ireland’s increasingly privatised system.

Finally, the cross-national comparison reveals how different political economies create varied narratives surrounding PE. In the U.S., PE is increasingly criticised as exploitative, while in Poland, private providers are seen as ‘more expensive yet more trustworthy’ than public alternatives. These divergent perceptions reflect deeper societal attitudes toward state versus market provision, shaped by historical experience. Our case study comparison demonstrates that policy responses to population aging and care needs are deeply political processes, shaped by institutional legacies, cultural contexts, and the power dynamics between states, markets, and civil society.

Acknowledgements

The authors wish to thank two anonymous referees, Peter Berman, David Blumenthal, Rocco Friebel, Alexander Preker, Michael Sparer, Iris Wallenburg and all the participants to the European-Americas EHPG meeting in May 2025 for their valuable comments.

Financial support

No financial support was granted to the present research.

Competing interests

The authors declare none.

Open access

Open access