1. Introduction

Over the past few decades, there has been a global trend toward financial globalization, which despite being driven by the intention to direct resources to their most productive destinations, has led to higher volatility in financial markets, global imbalances, and a global financial cycle that disproportionately affects emerging economies (Rey, Reference Rey2015; Miranda-Agrippino and Rey, Reference Miranda-Agrippino and Rey2020). To address these issues, policymakers have implemented new macroprudential regulations such as those in the Basel Accords, and established new institutions, including the Financial Stability Board. The effectiveness of these regulations has been extensively evaluated, along with their broader effects, leakages, and externalities.Footnote 1 However, although observed empirically, these leakages are less understood in terms of their functioning and driving mechanisms (Forbes, Reference Forbes2021); for example, it would be relevant to understand their nature or what generates them, and whether they create additional unaccounted vulnerabilities or, perhaps, the space for welfare improving policy adjustments.

In this study, we develop a macroeconomic framework to explore these regulatory leakages and related questions. We focus on an open economy environment where several emerging economies interact with a common financial center in global markets.Footnote 2 For these economies, the international consequences of nationally implemented regulations are particularly relevant, given their increased fragility to the shocks of global markets (Chang and Velasco, Reference Chang and Velasco2001; Reinhart and Rogoff, Reference Reinhart and Rogoff2009). As policymakers recognize the borderless effects of their implementation, regulations in different locations may become interdependent, prompting policymakers to react with their own toolkit in response. As a result, policy frameworks that internalize such cross-border linkages could be better poised for managing the fluctuations dictated by global financial while better balancing the costs and trade-offs of regulation.Footnote 3

We investigate the nature of international policy spillovers and how they are shaped by the presence of financial frictions and the direction of the policy leakages. Our study is innovative in that we explore a framework with multiple peripheries that jointly can become a relevant entity for their common financial center but that still depend financially on the latter economy given it acts—through their banking sector—as a global creditor. In this setup, the regulators trade-off their incentives to mitigate their financial frictions with those of boosting financial intermediation, and their resulting actions will potentially impact the economic conditions in other locations.

We consider the presence of the banking sector explicitly in our framework along the lines of Gertler and Kiyotaki (Reference Gertler, Kiyotaki, Gertler and Kiyotaki2010), Gertler and Karadi (Reference Gertler and Karadi2011), Adrian and Shin (Reference Adrian, Shin, Adrian and Shin2010), but extended to an open economy environment as in Céspedes et al. (Reference Céspedes, Chang and Velasco2017), with the difference that we allow for a multiperipheral economic structure.Footnote 4 Therefore, this work is related to the studies exploring whether changing financial conditions increase the extent of policy interdependency (e.g., in Fujiwara and Teranishi, Reference Fujiwara and Teranishi2017; Banerjee et al. Reference Banerjee, Devereux and Lombardo2016; Agénor et al. Reference Agénor, Jackson, Kharroubi, Gambacorta, Lombardo and Silva2021).Footnote 5 We build on these studies with a focus on macroprudential interventions and potential cross-border linkages between different types of financially integrated economies.

To introduce a meaningful role for prudential policies, we consider a setup with financial frictions caused by a limited enforcement agency distortion as described by Gertler and Karadi (Reference Gertler and Karadi2011) and Mendoza (Reference Mendoza2010), which will be more prevalent in emerging markets and leads to a default premium on interbank lending relationships, amplifying the scale of financial intermediation, and potentially shaping the international financial spillovers. We examine the existence and nature of cross-border policy spillovers and evaluate the effectiveness of several policy regimes in mitigating this distortion and smoothing the credit spreads. Specifically, we consider a macroprudential instrument that taxes banking sector revenues, similar to Agénor et al. (Reference Agénor, Jackson, Kharroubi, Gambacorta, Lombardo and Silva2021). It is worth noting that this policy tool may impact capital flows across borders and could be seen as a form of capital control. However, we argue that it is better described as a macroprudential tool with potential capital flows implications. To see this, we first demonstrate that it is equivalent to a leverage-ratio requirement, and secondly, we note that it primarily regulates the scale of financial intermediation, which could be international or domestic, without significant effects on capital flows.Footnote 6

Our framework is set as a large open economy model similar to Banerjee et al. (Reference Banerjee, Devereux and Lombardo2016), or Agénor et al. (Reference Agénor, Jackson, Kharroubi, Gambacorta, Lombardo and Silva2021), but with the abstraction from monetary policy concerns. This simplification enables us to extend the environment to that of a multiperipheral financially integrated economy, facilitating the examination of strategic interactions between macroprudential regulators in different types of economies. The consideration of a large open economy is relevant when studying potential prudential leakages; even under the standard assumption that financial centers’ regulators are not concerned with the policy actions of smaller countries (e.g., as in Jin and Shen, Reference Jin and Shen2020), as it may be the case that emerging countries decide to synchronize their policies at the regional level and generate non-trivial policy leakages in both directions—financial center to peripheral block and vice versa—that planners in each location would want to internalize. Having mentioned this, it should be noticed that the financial center still plays a prevalent role in the global market we consider. Hence, by accounting for such international spillovers dictated by financial centers, our study is also related to the global financial cycle literature (Rey, Reference Rey2015, Reference Rey2016) and to studies on the stabilizing role of financial regulations for emerging economies (Nuguer, Reference Nuguer2016; Cuadra and Nuguer, Reference Cuadra and Nuguer2018).

International policy externalities manifest through several channels. First, the profits of exiting bankers are directly affected by domestic and foreign policy tools, and these changes enter the households’ budgets due to ownership. Second, firms fund their input acquisitions with banking loans, and the costs of these loans depend on the policy instruments. Moreover, there is another relevant externality mechanism that implies an interlink between financial distortions at different locations. This mechanism consists of the general equilibrium effects of implementing a policy action. For example, if a center regulator implements a tightening to decrease the external finance premium locally, she inadvertently decreases the cost of debt in other locations since its creditor banks must be indifferent between funding local and foreign projects in equilibrium; this has the unintended effect of increasing the implied financial frictions, credit spread, and external finance premia abroad, prompting foreign regulators—in debtor countries—to make additional policy adjustments.Footnote 7

Additionally, we find that the impact of policy measures increases with the extent of financial distortions, an outcome that aligns with the conventional wisdom that these policies are more useful in emerging markets (Alam et al. Reference Alam, Alter, Eiseman, Gelos, Kang, Narita, Nier and Wang2025 ; Boz et al. Reference Boz, Unsal, Roch, Basu and Gopinath2020). Other factors influencing these effects include the net foreign asset positions, the price and demand changes in the interbank sector, and the disruption in real production activities, which is a prevalent concern in regulation circles and recent empirical studies (e.g., Richter et al. Reference Richter, Schularick and Shim2019; Kim and Mehrotra, Reference Kim and Mehrotra2022). Importantly, all of these features reflect a policy trade-off faced by the financial regulators—they must balance their intention to mitigate the financial frictions with the impact of more stringent policies on financial regulation. Moreover, the open economy setup allows us to see that such trade-off extends beyond the border of the planner’s jurisdiction. For example, a tighter regulation on an emerging country that curtails intermediation domestically will affect negatively the center economy whose banks’ act as a creditor of the former economy.

To inquire further into the nature of these leakages, we apply another extension where repeated financial intermediation with profits retaining is incorporated into the framework to allow for richer—and more empirically plausible—policy dynamics. In this case, the policy decisions become dynamic in the sense that current policy changes have effects on future balance sheets (and profits) of the banking sector. In this context, the policy effects—direct and leaked across borders—can be magnified, increasing the interdependency of policy across economies.

Finally, we explore the implications of our framework for policy design. We find that optimal policy configurations prompt emerging economies to prioritize mitigating their frictions, while the center reacts by attempting to steer higher intermediation flows toward the peripheries through tighter domestic policies (which in relative terms implies looser lending conditions toward other lenders abroad). These nationally oriented policies imply strong interventions that can be socially costly, which we illustrate by reporting optimal policies for alternative regimes where regulators internalize their effect on the rest of the world’s welfare. In such centralized cases, planners can afford to minimize regulatory wasteful actions by enacting the same effects with more conservative interventions. Importantly, we verify that policies are impactful enough to mitigate the financial friction in all regimes, an outcome that hinges heavily in the flexibility of the policy toolkit in each regime as illustrated by Korinek (Reference Korinek2016). However, when regulation costs potentially affect the toolkit flexibility, the decentralized (nationally oriented) policies, requiring more interventionism, become less capable of achieving a constrained efficient outcome, opening the scope for welfare-inducing coordinated policy frameworks.

There are several strands of literature related to our work. First, our study intends to provide a framework consistent with the empirical findings on macroprudential linkages across borders; these consider the studies on how financial regulation can affect foreign agents and markets (Buch and Goldberg, Reference Buch and Goldberg2017; Forbes et al. Reference Forbes, Reinhardt and Wieladek2017; Forbes, Reference Forbes2021), as well to how prudential policies implementations can leak financial (in)stability to other economies (Aiyar et al. Reference Aiyar, Calomiris and Wieladek2014; Tripathy, Reference Tripathy2020). On the other hand, related literature has produced two-country large open economy frameworks to explore the interdependency of macroprudential regulators, for example, for interactions between regulators in a monetary union (e.g., Rubio and Carrasco-Gallego, Reference Rubio and Carrasco-Gallego2016; Agénor et al. Reference Agénor, Jackson and Jia2021; Dennis and Ilbas, Reference Dennis and Ilbas2023) or for interactions between emerging and advanced economies (e.g., Nuguer, Reference Nuguer2016; Cuadra and Nuguer, Reference Cuadra and Nuguer2018); our framework is similar in exploring regulatory interactions but differs in that it considers a multiperipheral structure that permits us to see which effects arise between seemingly disconnected (emerging) countries that share a common financial center.Footnote 8

On the other hand, to study the implications of the leakages, we explore potential policy design implications for interconnected countries that in principle may choose to coordinate their policy decisions. In that sense, although performing a comprehensive welfare accounting exercise is beyond the scope of our setup, some implications are similar to studies on macroprudential policy cooperation (e.g., Davis and Devereux, Reference Davis and Devereux2022; Korinek, Reference Korinek2016; Bengui, Reference Bengui2014; Jin and Shen, Reference Jin and Shen2020; Kara, Reference Kara2016, among others).Footnote 9 , Footnote 10

The rest of the paper is organized as follows: Section 2 explains the baseline model, Sections 3 and 5 explore the model analytically, initially in our baseline setup and then in an extended version, respectively. Then in Section 4, we describe the numerical solution of the model, and in Section 6, we discuss the policy implications. Finally, we conclude.

2. The model

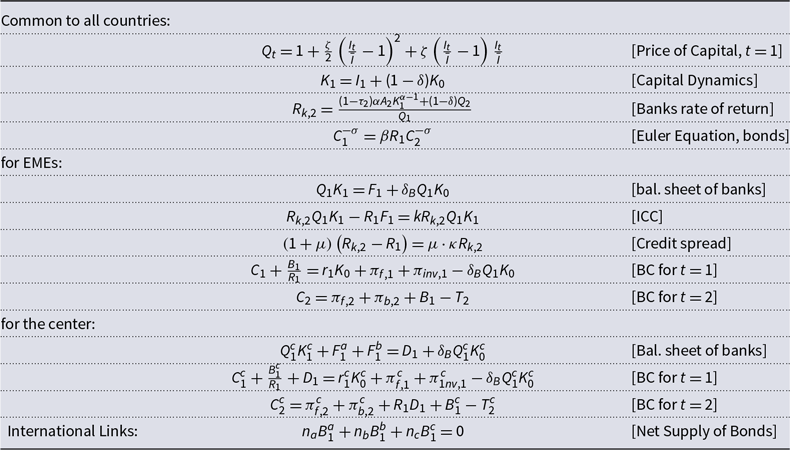

Our framework is based on Banerjee et al. (Reference Banerjee, Devereux and Lombardo2016), meaning that it essentially follows the banking sector modelation of Gertler and Karadi (Reference Gertler and Karadi2011) applied to an open economy setup. In this paper, however, we introduce a multiperipheral environment, where the peripheric block of the economy is allowed to have several emerging economies that interact with one financial center. At the same time, we include a macroprudential policy in the form of a tax to the return on capital as in Agénor et al. (Reference Agénor, Jackson, Kharroubi, Gambacorta, Lombardo and Silva2021) and Aoki et al. (Reference Aoki, Benigno and Kiyotaki2016), among others. The advantage of this formulation is that the policy instrument will be attached directly to the credit spreads that are augmented by the friction and drive the capital flows at the cross-country level. On the other hand, to keep the model simple, our initial formulation will only consider a simple financial intermediation period, but this is extended in the later sections.Footnote 11

2.1 Economic environment

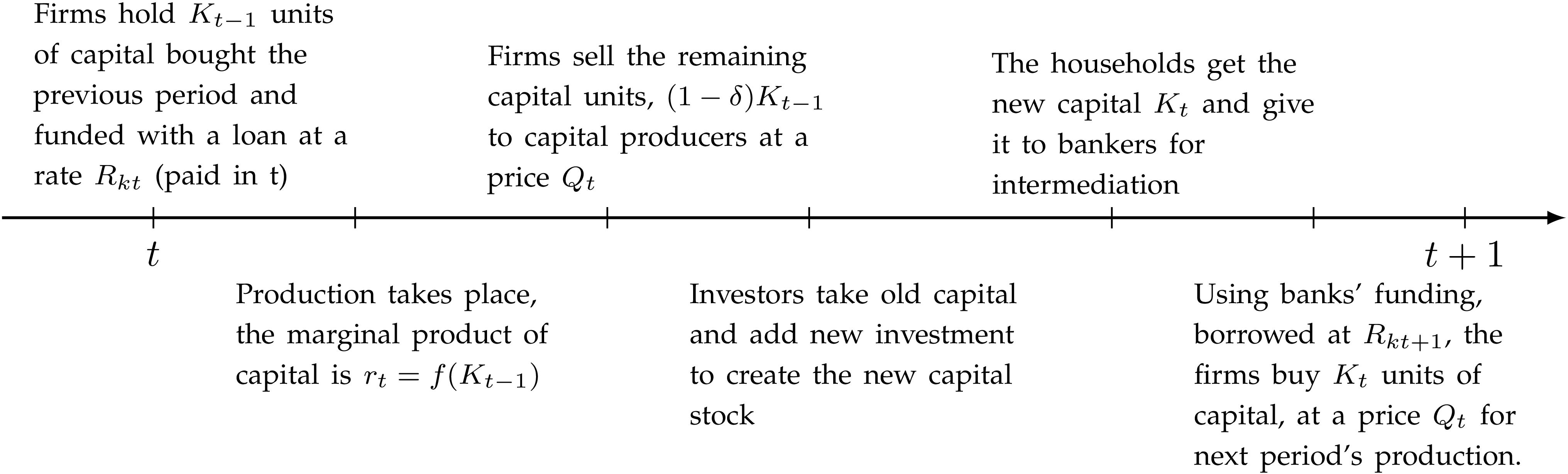

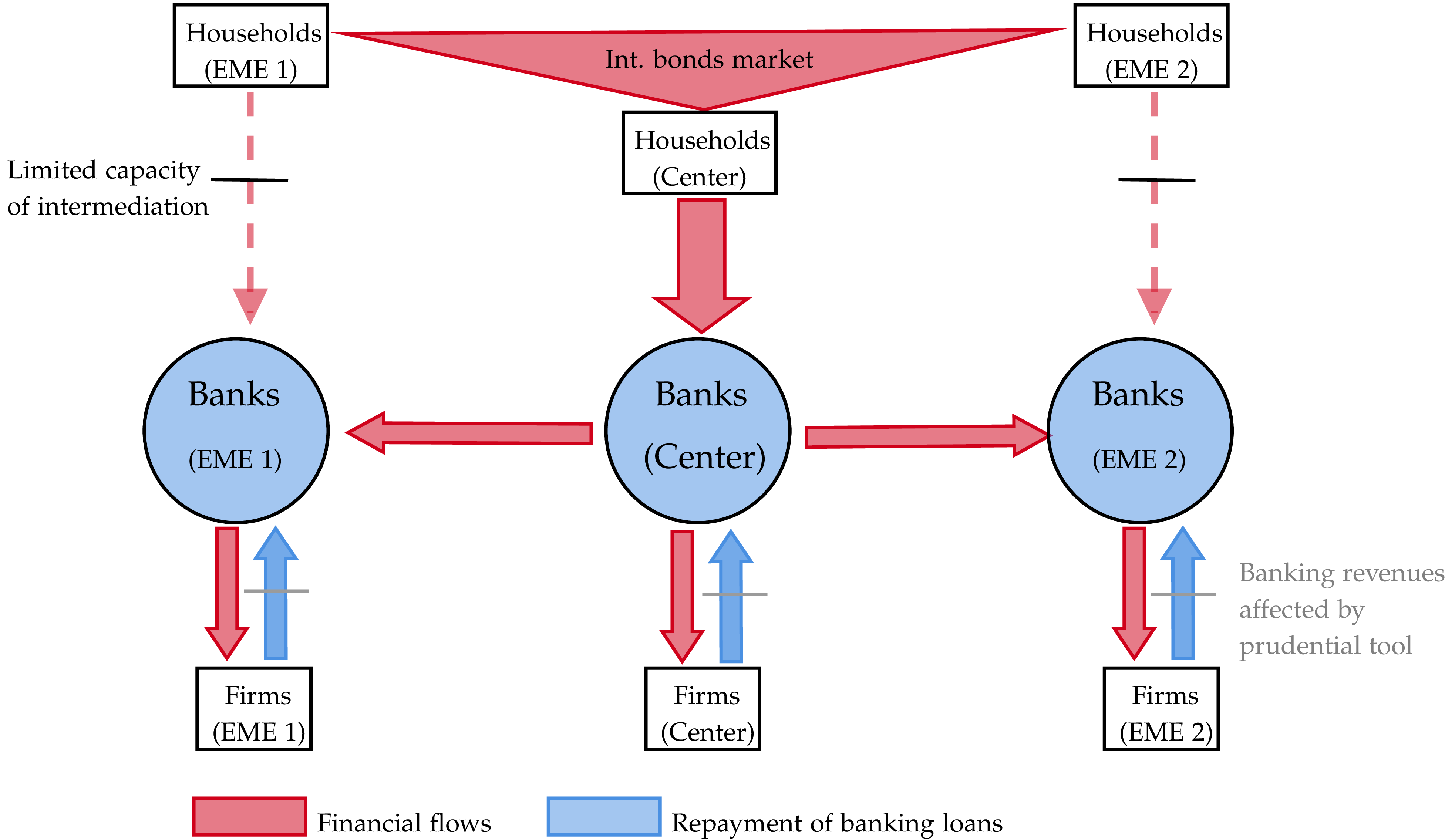

The main feature defining whether a country is an emerging economy is that its financial sector has a limited intermediation capacity, meaning it is unable to issue deposit claims for their households to some extent. As a consequence, it will have to resort to the international financial banking sector to make up for the difference and being able to meet their firms’ funding needs. This environment is depicted in Figure 1, where the red arrows represent financial flows.

Financial flows environment in the model.

Note: All arrows denote financial flows. The blue arrows, in addition, refer to flows that are paid to the banks by their borrowers. This latter type of flow—or specifically the associated rate of return perceived by financial intermediaries—is the one affected by the prudential regulations in the model.

Such structure implies that the emerging economies are financially dependent on the funding from center banks, and in an environment of imperfect information in the lending contracts, this could imply a double layer of agency frictions in the economy: that between center households and banks and another one between global banks and emerging country banks. We also assume the friction is more accentuated in the peripheries.Footnote 12

For simplicity, the real sector will consist only of one consumption good, and there will be no deviations from the law of one price. Preferences are identical between agents, implying the parity or purchasing power holds, and the real exchange rate will be constant (equal to one), playing no role in this version of the model. Additionally, the households will have access to an international market of non-contingent bonds. This is relevant as it implies that, despite the limited capacity to hold deposits, the saving decisions of emerging economies’ households are not curtailed in any way once they trade these assets.

Finally, the lending relationships are subject to a limited enforceability friction which induces an external finance premium and augments the scale of intermediation and credit cycles. The external premium takes the form of an increased return rate for the banks which raises their—expected and eventual—revenues. Such revenues will be targeted by the macroprudential regulation, meaning it will attack the financial friction at its origin.

2.2 Timing and countries setup

The world consists of three economies that live for two periods

$t=1,2$

. The economies are indexed by

$t=1,2$

. The economies are indexed by

$i={a,b,c}$

, where the first two will be emerging countries (

$i={a,b,c}$

, where the first two will be emerging countries (

$a$

and

$a$

and

$b$

) and the third one is a developed economy that acts as financial center (c). The relative population sizes of the economies are

$b$

) and the third one is a developed economy that acts as financial center (c). The relative population sizes of the economies are

$n_i$

with

$n_i$

with

$1-(n_a+n_b) \geq \tfrac {1}{2}$

. Each economy has five types of agents: households, final consumption good producers, capital producers, banks, and a government sector.

$1-(n_a+n_b) \geq \tfrac {1}{2}$

. Each economy has five types of agents: households, final consumption good producers, capital producers, banks, and a government sector.

As mentioned before, preferences across countries’ households are identical, and there is only one final consumption good worldwide that is freely traded and produced in all locations. In terms of notation, superindexes denote the country, while subindexes refer to other features such as the sector of the economy and time periods. Additionally, if a superindex is omitted, it normally means that the variable or equation applies to the three countries.

2.3 Investors

For simplicity, the investment decision is separated from the other household decisions and will be subject to adjustment costs. Physical capital is produced in a competitive market by using old capital and investment. The investment will be subject to convex adjustment costs, with the total cost of investing

$I_1$

being:

$I_1$

being:

\begin{equation*} C(I_1) = I_1\left (1 + \frac {\zeta }{2} \left (\frac {I_1}{\bar I}-1\right )^2 \right ), \end{equation*}

\begin{equation*} C(I_1) = I_1\left (1 + \frac {\zeta }{2} \left (\frac {I_1}{\bar I}-1\right )^2 \right ), \end{equation*}

where

$\bar I$

represents the reference level for defining the adjustment cost; The reference level is usually set at the steady state, the previous level of investment, or a combination. In any case, it must hold that

$\bar I$

represents the reference level for defining the adjustment cost; The reference level is usually set at the steady state, the previous level of investment, or a combination. In any case, it must hold that

$C(0) = 0, \ C''(\! \cdot \!) \gt 0$

. The capital-producing firms (investors) buy back the old capital stock from the firms at price

$C(0) = 0, \ C''(\! \cdot \!) \gt 0$

. The capital-producing firms (investors) buy back the old capital stock from the firms at price

$Q_1$

and produce new capital subject to the adjustment costs (proportional to the parameter

$Q_1$

and produce new capital subject to the adjustment costs (proportional to the parameter

$\zeta$

).

$\zeta$

).

The investor solves:Footnote 13

\begin{equation*} \max _{I_1} \ Q_1 I_1 - I_1\left (1 + \frac {\zeta }{2} \left (\frac {I_1}{\bar I}-1\right )^2 \right )\!, \end{equation*}

\begin{equation*} \max _{I_1} \ Q_1 I_1 - I_1\left (1 + \frac {\zeta }{2} \left (\frac {I_1}{\bar I}-1\right )^2 \right )\!, \end{equation*}

the optimality condition (F.O.N.C.) is,

\begin{equation} [I_1] \, : \qquad Q_1 = 1 + \frac {\zeta }{2} \left (\frac {I_1}{\bar I}-1\right )^2 + \zeta \left (\frac {I_1}{\bar I}-1\right ) \frac {I_1}{\bar I}, \end{equation}

\begin{equation} [I_1] \, : \qquad Q_1 = 1 + \frac {\zeta }{2} \left (\frac {I_1}{\bar I}-1\right )^2 + \zeta \left (\frac {I_1}{\bar I}-1\right ) \frac {I_1}{\bar I}, \end{equation}

2.4 Firms

Each period, the firms will operate with a Cobb–Douglas technology that aggregates capital predetermined at the end of the period before. This technology of aggregation is given by

$Y_t = A_t(\xi _tK_{t-1})^\alpha$

, where

$Y_t = A_t(\xi _tK_{t-1})^\alpha$

, where

$A_t$

is the aggregate productivity and

$A_t$

is the aggregate productivity and

$\xi$

is a capital-specific productivity or quality term. The capital in

$\xi$

is a capital-specific productivity or quality term. The capital in

$t=1$

follows standard dynamics with depreciation as,

$t=1$

follows standard dynamics with depreciation as,

\begin{equation} K_1 = I_1 + (1-\delta ) \xi _1 K_0. \end{equation}

\begin{equation} K_1 = I_1 + (1-\delta ) \xi _1 K_0. \end{equation}

The capital in the initial period will be provided directly by the households in the quantity

$K_0$

. However, after that, the firm funds physical capital acquisitions for future production (

$K_0$

. However, after that, the firm funds physical capital acquisitions for future production (

$K_1$

) using lending from the banking sector. Given the model’s timing, there is only one period of intermediation (

$K_1$

) using lending from the banking sector. Given the model’s timing, there is only one period of intermediation (

$t=1$

) when lending is extended to acquire capital for production in the final period (

$t=1$

) when lending is extended to acquire capital for production in the final period (

$t=2$

).

$t=2$

).

In this setup, the firms solve a slightly different problem each period. First, they decide how much capital to rent from households:

\begin{align*} \max _{K_{0}} \ \pi _{f,1} &= Y_1 - r_1 K_{0}, \\[2pt] s.t. \quad & Y_1 = A_1(\xi _1 K_{0})^\alpha , \end{align*}

\begin{align*} \max _{K_{0}} \ \pi _{f,1} &= Y_1 - r_1 K_{0}, \\[2pt] s.t. \quad & Y_1 = A_1(\xi _1 K_{0})^\alpha , \end{align*}

where

$r_1$

is the rental rate of capital, which, from the optimality condition, is

$r_1$

is the rental rate of capital, which, from the optimality condition, is

$r_1 = \alpha A_1\xi _1^\alpha K_{0}^{\alpha -1}$

. For the second period, the firms take into account the cost of funding and the revenue of selling the remaining capital stock to capital good producers that carry out the necessary investment to build the capital stock for the next period. Thus, in the second period, the firm will solve:

$r_1 = \alpha A_1\xi _1^\alpha K_{0}^{\alpha -1}$

. For the second period, the firms take into account the cost of funding and the revenue of selling the remaining capital stock to capital good producers that carry out the necessary investment to build the capital stock for the next period. Thus, in the second period, the firm will solve:

\begin{align*} \max _{K_{1}} \ \pi _{f,2} &= Y_2 + Q_2 (1-\delta ) \xi _2 K_1 - R_{k,2} Q_1 K_1, \\[2pt] s.t. \quad & Y_2 = A_2(\xi _2 K_{1})^\alpha . \end{align*}

\begin{align*} \max _{K_{1}} \ \pi _{f,2} &= Y_2 + Q_2 (1-\delta ) \xi _2 K_1 - R_{k,2} Q_1 K_1, \\[2pt] s.t. \quad & Y_2 = A_2(\xi _2 K_{1})^\alpha . \end{align*}

With F.O.N.C.,

\begin{equation*} [K_{1}]\,: \qquad \alpha A_2 \xi _2^\alpha K_1^{\alpha -1} + (1-\delta ) \xi _2 Q_2 = R_{k,2} Q_1. \end{equation*}

\begin{equation*} [K_{1}]\,: \qquad \alpha A_2 \xi _2^\alpha K_1^{\alpha -1} + (1-\delta ) \xi _2 Q_2 = R_{k,2} Q_1. \end{equation*}

To facilitate the model notation, we follow the same definition for

$r_2$

, that is,

$r_2$

, that is,

$r_2 = \alpha A_2 \xi _2^\alpha K_{1}^{\alpha -1}$

.

$r_2 = \alpha A_2 \xi _2^\alpha K_{1}^{\alpha -1}$

.

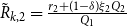

Substituting in the optimality condition for

$K_1$

, we obtain that the rate paid to the banks by the firms is given by

$K_1$

, we obtain that the rate paid to the banks by the firms is given by

$\tilde R_{k,2} = \tfrac {r_2 + (1-\delta )\xi _2Q_2}{Q_1}$

. Moreover, by taking into account the possibility of a macroprudential tax on the marginal return on capital, such as in Agénor et al. (Reference Agénor, Jackson, Kharroubi, Gambacorta, Lombardo and Silva2021), we have that the effective rate obtained by the banks, that is, after paying the macroprudential taxes (

$\tilde R_{k,2} = \tfrac {r_2 + (1-\delta )\xi _2Q_2}{Q_1}$

. Moreover, by taking into account the possibility of a macroprudential tax on the marginal return on capital, such as in Agénor et al. (Reference Agénor, Jackson, Kharroubi, Gambacorta, Lombardo and Silva2021), we have that the effective rate obtained by the banks, that is, after paying the macroprudential taxes (

$ \tau r_2 K_1$

) to the government is given by:

$ \tau r_2 K_1$

) to the government is given by:

\begin{equation} R_{k,2} = \frac {(1-\tau )r_2 + (1-\delta ) \xi _2 Q_2}{Q_1}. \end{equation}

\begin{equation} R_{k,2} = \frac {(1-\tau )r_2 + (1-\delta ) \xi _2 Q_2}{Q_1}. \end{equation}

For the sake of clarity, it is important to notice that the firms will pay the pre-taxes banking rate. Only afterward, the banks will consider the effect of the taxes in their profits.Footnote 14 We elaborate on the policy tool and the role of this return rate in later subsections.Footnote 15

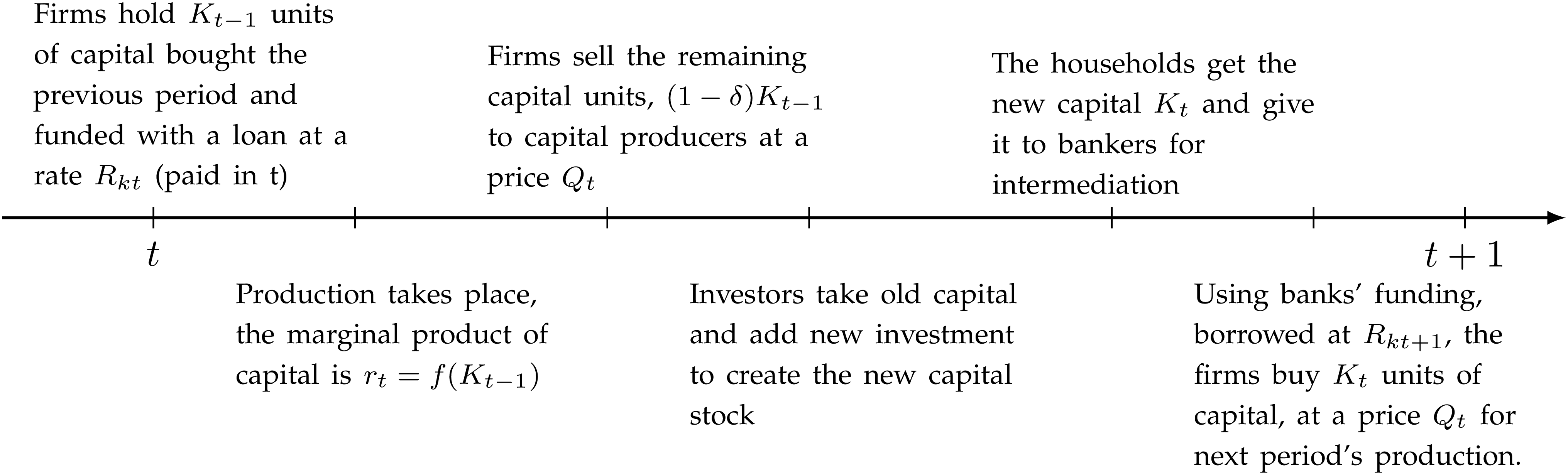

2.4.1 Capital dynamics and ownership

The dynamics of the model will be driven (within and cross-country) by the capital flows. For that reason, it is relevant to clarify how capital is held, and profited from, by several types of agents in a single period.

Capital ownership within a period.

Note: This figure describes the ownership of capital across the agents of the model for a generic period

$t$

. In terms of our baseline model

$t$

. In terms of our baseline model

$t = 1$

; similarly,

$t = 1$

; similarly,

$t={1,2}$

for the second setup with two periods of intermediation.

$t={1,2}$

for the second setup with two periods of intermediation.

There is only one period of capital accumulation (

$t = 1$

). The initial capital will be given for that period as

$t = 1$

). The initial capital will be given for that period as

$K_0$

. Then, by the end of the accumulation period, the capital in the economy will be given by

$K_0$

. Then, by the end of the accumulation period, the capital in the economy will be given by

$K_1$

. That capital will be used for the following period’s production. The capital ownership between agents throughout each period is shown in Figure 2, which explains a typical period with intermediation.

$K_1$

. That capital will be used for the following period’s production. The capital ownership between agents throughout each period is shown in Figure 2, which explains a typical period with intermediation.

It should be noticed that the capital used for production in the period

$t = 1$

cannot be subject to intermediation since there are no banks before the rest of the agents exist (the banks themselves are owned household agents). Therefore, the pre-existing capital stock (

$t = 1$

cannot be subject to intermediation since there are no banks before the rest of the agents exist (the banks themselves are owned household agents). Therefore, the pre-existing capital stock (

$K_0$

) will be provided directly from households to firms without explicit financial intermediation.Footnote

16

$K_0$

) will be provided directly from households to firms without explicit financial intermediation.Footnote

16

2.5 Banks

This is the target sector of the macroprudential policies. The set up is largely based on Gertler and Karadi (Reference Gertler and Karadi2011). There is a financial intermediation sector in the first period that facilitates funding for firms at the local level. In addition, the bank at the center is also a global creditor and extends loans to banks in other locations. In terms of its functioning, the bank receives a start-up capital by their owner household and will try to maximize the value of the banking activities, given by the present value of its profits. Finally, at the end of its life, the bank will give back their net worth to the households as profits.

There will be a costly enforcement agency friction where it is possible for the banks to divert a portion of the assets they intermediate. The eventual implication of this is the imposition of an external finance premium to the banking revenue rates, which is imposed to prevent the banks from absconding assets and to align their incentives with those of the assets’ owners. This is the financial friction in this environment that augments the credit cycles.

Starting from this section, it will be useful in some cases to use a super index

$e$

for denoting variables from emerging economies (

$e$

for denoting variables from emerging economies (

$e=\{a,b\}$

), whereas as before, variables that apply for all countries are either left without a superindex or labeled with an index

$e=\{a,b\}$

), whereas as before, variables that apply for all countries are either left without a superindex or labeled with an index

$i$

when necessary (e.g., when the same expression involves variables from various locations).

$i$

when necessary (e.g., when the same expression involves variables from various locations).

2.5.1 Emerging countries

The financial system of the emerging countries will have a limited capacity of intermediation of deposits from local households. For simplicity, we assume that there are not any local deposits in these economies, implying that they rely almost entirely on foreign lending from the center banks for providing funding to firms for production. Therefore, the balance sheet of the bank includes, on the asset side, the lending provided to firms, and on the liability and equity side, the foreign lending from center banks and a start-up capital they receive from local households.

The lending relationship between foreign and local banks will be subject to agency frictions, arising from the fact that creditor banks could default on their debt repayment and divert a portion

$\kappa$

of their intermediated assets.Footnote

17

In either case (default or not), the gross return from intermediation for the bank is

$\kappa$

of their intermediated assets.Footnote

17

In either case (default or not), the gross return from intermediation for the bank is

$R_{k,2}$

as defined in equation (3).

$R_{k,2}$

as defined in equation (3).

The emerging market bank maximizes its franchise value in the period 1 (

$J_1$

):

$J_1$

):

\begin{align} \max _{F_1^e,L_1^e} J_1^e \,= \, \mathbb{E}_1\Lambda _{1,2}^e\pi _{b,2}^e &= \mathbb{E}_1\Lambda _{1,2}^e\big(R_{k,2}^e L_1^e - R_{b,1}^eF_1^e\big), \nonumber \\[4pt] s.t. \quad L_1^e &= F_1^e + \delta _bQ_1^eK_0^e, \\[-2pt] \nonumber \end{align}

\begin{align} \max _{F_1^e,L_1^e} J_1^e \,= \, \mathbb{E}_1\Lambda _{1,2}^e\pi _{b,2}^e &= \mathbb{E}_1\Lambda _{1,2}^e\big(R_{k,2}^e L_1^e - R_{b,1}^eF_1^e\big), \nonumber \\[4pt] s.t. \quad L_1^e &= F_1^e + \delta _bQ_1^eK_0^e, \\[-2pt] \nonumber \end{align}

\begin{align} J_1^e &\geq \kappa \mathbb{E}_1\Lambda _{1,2}^e R_{k,2}^eL_1^e, \\[-10pt] \nonumber \end{align}

\begin{align} J_1^e &\geq \kappa \mathbb{E}_1\Lambda _{1,2}^e R_{k,2}^eL_1^e, \\[-10pt] \nonumber \end{align}

where

$L_1^e = Q_1^eK_1^e$

is the total intermediated lending,

$L_1^e = Q_1^eK_1^e$

is the total intermediated lending,

$F_1^e$

is the foreign interbank lending borrowed from the center bank at a gross rate

$F_1^e$

is the foreign interbank lending borrowed from the center bank at a gross rate

$R^e_{b,1}$

,

$R^e_{b,1}$

,

$\delta _bQ_1^eK_0^e$

is the start-up capital received from households, and

$\delta _bQ_1^eK_0^e$

is the start-up capital received from households, and

$\Lambda _{1,2}^i = \beta u'(C_2^i)/u'(C_1^i)$

is the stochastic discount factor for a household in country

$\Lambda _{1,2}^i = \beta u'(C_2^i)/u'(C_1^i)$

is the stochastic discount factor for a household in country

$i$

. At the same time, the constraints correspond to the balance sheet of the bank and an incentive compatibility constraint (ICC) imposing that the value of the bank equals or exceeds the value from defaulting.

$i$

. At the same time, the constraints correspond to the balance sheet of the bank and an incentive compatibility constraint (ICC) imposing that the value of the bank equals or exceeds the value from defaulting.

The F.O.N.C. with respect to the foreign debt is:

\begin{align} [F_{1}]\,: \qquad (1+\mu ^e)\mathbb{E}_1\Lambda _{1,2}^e\big(R_{k,2}^e-R_{b,1}^e\big) = \mu ^e\mathbb{E}_1 \kappa \Lambda _{1,2}^e R_{k,2}^e, \end{align}

\begin{align} [F_{1}]\,: \qquad (1+\mu ^e)\mathbb{E}_1\Lambda _{1,2}^e\big(R_{k,2}^e-R_{b,1}^e\big) = \mu ^e\mathbb{E}_1 \kappa \Lambda _{1,2}^e R_{k,2}^e, \end{align}

where

$\mu ^e$

is the Lagrange multiplier of the ICC. This expression is already informative about some implications of the frictions that we explore in propositions at the end of this section.Footnote

18

$\mu ^e$

is the Lagrange multiplier of the ICC. This expression is already informative about some implications of the frictions that we explore in propositions at the end of this section.Footnote

18

2.5.2 Advanced economy

To simplify, we assume there is no agency problems at the center.Footnote 19 Then, the center bank solves:

\begin{align} \max _{F_1,L_1,D_1} J_1 = \mathbb{E}_1\Lambda _{1,2} \pi _{b,2}^c &= \mathbb{E}_1\Lambda _{1,2}\big(R_{b,1}^aF_1^a + R_{b,1}^bF_1^b +R_{k,2}^c L_1^c - R_{D,1}D_1\big), \notag \\[2pt] s.t. \quad &F_1^a + F_1^b + L_1 = D_1 + \delta _bQ_1^cK_0^c. \end{align}

\begin{align} \max _{F_1,L_1,D_1} J_1 = \mathbb{E}_1\Lambda _{1,2} \pi _{b,2}^c &= \mathbb{E}_1\Lambda _{1,2}\big(R_{b,1}^aF_1^a + R_{b,1}^bF_1^b +R_{k,2}^c L_1^c - R_{D,1}D_1\big), \notag \\[2pt] s.t. \quad &F_1^a + F_1^b + L_1 = D_1 + \delta _bQ_1^cK_0^c. \end{align}

The only restriction will be the balance sheet of the bank that now counts with the foreign interbank flows on the asset side and the local center deposits on the liability side (

$D_1$

). Additionally, the deposits from households are subject to a gross rate

$D_1$

). Additionally, the deposits from households are subject to a gross rate

$R_{D,1}$

.

$R_{D,1}$

.

The associated F.O.N.C.s are:

\begin{align*} \big[F_1^a\big]\,: \quad \mathbb{E}_1\big(R_{b,1}^a - R_{D,1}\big) = 0, \qquad \big[F_1^b\big]\,: \quad \mathbb{E}_1\big(R_{b,1}^b - R_{D,1}\big) = 0,\qquad \big[L_1^c\big]\,: \quad \mathbb{E}_1\big(R_{k,2}^c - R_{D,1}\big) = 0. \end{align*}

\begin{align*} \big[F_1^a\big]\,: \quad \mathbb{E}_1\big(R_{b,1}^a - R_{D,1}\big) = 0, \qquad \big[F_1^b\big]\,: \quad \mathbb{E}_1\big(R_{b,1}^b - R_{D,1}\big) = 0,\qquad \big[L_1^c\big]\,: \quad \mathbb{E}_1\big(R_{k,2}^c - R_{D,1}\big) = 0. \end{align*}

An important consequence of these optimality conditions is that a policy that affects the revenue rate

$R_{k,2}^c$

will have general equilibrium effects and inadvertently lower the cost of debt for debtor economies (

$R_{k,2}^c$

will have general equilibrium effects and inadvertently lower the cost of debt for debtor economies (

$R_{b,1}^a, R_{b,1}^b$

). This implies an interaction between the credit spreads and financial frictions between countries that is overlooked by nationally oriented planners.Footnote

20

$R_{b,1}^a, R_{b,1}^b$

). This implies an interaction between the credit spreads and financial frictions between countries that is overlooked by nationally oriented planners.Footnote

20

2.6 Macroprudential policy and public budget

Among the number of possible prudential policiesFootnote

21

(VaR regulations, leverage caps, loan/value ratios, etc.) we consider a general type of policy that, as explained by Agénor et al. (Reference Agénor, Jackson, Kharroubi, Gambacorta, Lombardo and Silva2021), encompasses a broad set of macroprudential regulations: a tax (

$\tau$

) on the return to capital (

$\tau$

) on the return to capital (

$R_{k2} = [(1-\tau ^i)r_t+(1-\delta )\xi _2Q_2]/Q_1$

). This will be a tax levied on the banking sector, as shown in Equation (3).

$R_{k2} = [(1-\tau ^i)r_t+(1-\delta )\xi _2Q_2]/Q_1$

). This will be a tax levied on the banking sector, as shown in Equation (3).

Although prudential in nature—as it is implemented on the intermediation sector—the policy tool can also be thought in practice as a device to impose controls on capital flows. This is the case because the tax has the advantage of affecting directly the wedge between the return on capital and borrowing rate (cost of funds for the bank), that is, the credit spread, which in turn drives financial flows at the interbank level. Thus, we are taxing the source of inefficiencies directly.Footnote 22

On the public budget level, this is reflected as a distortionary tax funded with lump sum taxes (

$T$

) in each period; that is, we assume a balanced fiscal budget,

$T$

) in each period; that is, we assume a balanced fiscal budget,

\begin{equation*} \tau ^i r_2 K_{1} + T = 0. \end{equation*}

\begin{equation*} \tau ^i r_2 K_{1} + T = 0. \end{equation*}

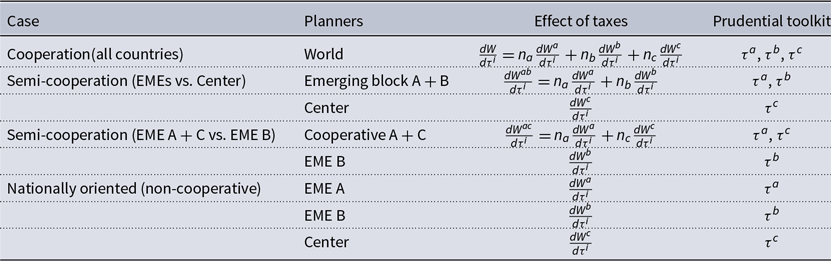

When setting the taxes optimally, each social planner might consider whether to maximize her national welfare or to join cooperative arrangements which would dictate policy centrally.Footnote 23 We explore these cases as an additional exercise in Section 6.

2.7 Households

The households derive utility from consumption and its lifetime utility is given by

$U = u(C_1) + \beta u(C_2)$

with

$U = u(C_1) + \beta u(C_2)$

with

$u(C) = \tfrac {C^{1-\sigma }}{1-\sigma }$

. The budget constraints in each period are the following:

$u(C) = \tfrac {C^{1-\sigma }}{1-\sigma }$

. The budget constraints in each period are the following:

Emerging markets:

\begin{align} C_1^e + \frac {B_1^{e}}{R_1^e} &= r_1^e K_0^e + \pi _{f,1}^e + \pi _{inv,1}^e - \delta _b Q_1^e K_0^e, \\[-10pt]\nonumber \end{align}

\begin{align} C_1^e + \frac {B_1^{e}}{R_1^e} &= r_1^e K_0^e + \pi _{f,1}^e + \pi _{inv,1}^e - \delta _b Q_1^e K_0^e, \\[-10pt]\nonumber \end{align}

\begin{align} C_2^e &= \pi _{f,2}^e + \pi _{b,2}^e + B_1^e - T^e, \quad for \ e=\{a,b\}, \\[-2pt] \nonumber \end{align}

\begin{align} C_2^e &= \pi _{f,2}^e + \pi _{b,2}^e + B_1^e - T^e, \quad for \ e=\{a,b\}, \\[-2pt] \nonumber \end{align}

where

$C$

is the final consumption good,

$C$

is the final consumption good,

$B$

a non-contingent internationally traded bond,

$B$

a non-contingent internationally traded bond,

$r_1$

the rental rate of capital,

$r_1$

the rental rate of capital,

$Q$

the relative price of capital,

$Q$

the relative price of capital,

$K$

the capital stock, and

$K$

the capital stock, and

$T$

is a lump sum tax. Additionally,

$T$

is a lump sum tax. Additionally,

$\pi$

stands for profits which can come from production activities in final goods (

$\pi$

stands for profits which can come from production activities in final goods (

$f$

), capital goods (

$f$

), capital goods (

$inv$

), or banking services (

$inv$

), or banking services (

$b$

).

$b$

).

Advanced Economy:

\begin{align} C_1^c + \frac {B_1^{c}}{R_1^c} + D_1 &= r_1^c K_0^c + \pi _{f,1}^c + \pi _{inv,1}^c - \delta _b Q_1^c K_0^c, \\[-10pt] \nonumber \end{align}

\begin{align} C_1^c + \frac {B_1^{c}}{R_1^c} + D_1 &= r_1^c K_0^c + \pi _{f,1}^c + \pi _{inv,1}^c - \delta _b Q_1^c K_0^c, \\[-10pt] \nonumber \end{align}

\begin{align} C_2^c &= \pi _{f,2}^c + \pi _{b,2}^c + B_1^c + R_{D,1}D_1 - T^c, \\[12pt] \nonumber \end{align}

\begin{align} C_2^c &= \pi _{f,2}^c + \pi _{b,2}^c + B_1^c + R_{D,1}D_1 - T^c, \\[12pt] \nonumber \end{align}

where the advanced economy also includes local deposits

$D$

in the budget constraint as these are intermediated by their banks. Additionally, the profits are given by:Footnote

24

$D$

in the budget constraint as these are intermediated by their banks. Additionally, the profits are given by:Footnote

24

\begin{align*} \pi _{f,1} &= A_1 \xi _1^\alpha K_0^{\alpha } - r_1 K_{0}\\[2pt] \pi _{f,2} &= A_2 \xi _2^\alpha K_1^{\alpha } + Q_2 (1-\delta )\xi _2 K_1 - R_{k,2} Q_1 K_1\\[2pt] \pi _{inv,1} &= Q_1 I_1 - I_1 \left (1+\frac {\zeta }{2} \left ( \frac {I_1}{\bar I} -1 \right )^2 \right )\\[2pt] \pi _{b,2}^e &= R_{k,2}^e Q_1^e K_1^e - R_{b,1}^e F_1^e, \quad for \ e=\{a,b\} \\[2pt] \pi _{b,2}^c &= R_{b,1}^a F_1^a + R_{b,1}^b F_1^b + R_{k,2}^c Q_1^c K_1^c - R_{D,1} D_1 \end{align*}

\begin{align*} \pi _{f,1} &= A_1 \xi _1^\alpha K_0^{\alpha } - r_1 K_{0}\\[2pt] \pi _{f,2} &= A_2 \xi _2^\alpha K_1^{\alpha } + Q_2 (1-\delta )\xi _2 K_1 - R_{k,2} Q_1 K_1\\[2pt] \pi _{inv,1} &= Q_1 I_1 - I_1 \left (1+\frac {\zeta }{2} \left ( \frac {I_1}{\bar I} -1 \right )^2 \right )\\[2pt] \pi _{b,2}^e &= R_{k,2}^e Q_1^e K_1^e - R_{b,1}^e F_1^e, \quad for \ e=\{a,b\} \\[2pt] \pi _{b,2}^c &= R_{b,1}^a F_1^a + R_{b,1}^b F_1^b + R_{k,2}^c Q_1^c K_1^c - R_{D,1} D_1 \end{align*}

In the first period, households maximize their lifetime utility stream subject to the budget constraints for the first and second periods. The F.O.N.C. for the three countries’ households is:

\begin{align} u'(C_1) \,=\, \beta R_1 \mathbb{E}_1 [u'(C_2)], \qquad u'\big(C_1^c\big) \,=\, \beta R_{D,1} \mathbb{E}_1 \big[u'\big(C_2^c \big)\big], \end{align}

\begin{align} u'(C_1) \,=\, \beta R_1 \mathbb{E}_1 [u'(C_2)], \qquad u'\big(C_1^c\big) \,=\, \beta R_{D,1} \mathbb{E}_1 \big[u'\big(C_2^c \big)\big], \end{align}

where the first equation is the Euler equation for bonds and applies to the three economies, while the second is the Euler equation for local deposits and holds only for country

$c$

.

$c$

.

2.8 Market clearing

At the world level, bonds are characterized by zero-net-supply,

\begin{equation} n_a B_1^a + n_b B_1^b + n_c B_1^c = 0. \end{equation}

\begin{equation} n_a B_1^a + n_b B_1^b + n_c B_1^c = 0. \end{equation}

The goods market clearing conditions for each period are

\begin{align*} n_a \left ( C_1^a + I_1^a \left (1+\frac {\zeta }{2} \left ( \frac {I_1^a}{\bar I} -1 \right ) \right ) \right ) + n_b \left ( C_1^b + I_1^b \left (1+\frac {\zeta }{2} \left ( \frac {I_1^b}{\bar I} -1 \right ) \right ) \right )& \\[2pt] + n_c \left ( C_1^c+ I_1^c \left (1+\frac {\zeta }{2} \left ( \frac {I_1^c}{\bar I} -1 \right ) \right ) \right ) = n_a Y_1^a &+ n_b Y_1^b + n_c Y_1^c,\\[2pt] n_a C_2^a + n_b C_2^b + n_c C_2^c = n_a Y_2^a + n_b Y_2^b + n_c Y_2^c \end{align*}

\begin{align*} n_a \left ( C_1^a + I_1^a \left (1+\frac {\zeta }{2} \left ( \frac {I_1^a}{\bar I} -1 \right ) \right ) \right ) + n_b \left ( C_1^b + I_1^b \left (1+\frac {\zeta }{2} \left ( \frac {I_1^b}{\bar I} -1 \right ) \right ) \right )& \\[2pt] + n_c \left ( C_1^c+ I_1^c \left (1+\frac {\zeta }{2} \left ( \frac {I_1^c}{\bar I} -1 \right ) \right ) \right ) = n_a Y_1^a &+ n_b Y_1^b + n_c Y_1^c,\\[2pt] n_a C_2^a + n_b C_2^b + n_c C_2^c = n_a Y_2^a + n_b Y_2^b + n_c Y_2^c \end{align*}

Finally, given that there is only one final good and the law of one price holds (so that the real exchange rate in all cases is one), we have by an uncovered interest rate parity argument that:

$R_1^a = R_1^b = R_1^c = R_1$

, where

$R_1^a = R_1^b = R_1^c = R_1$

, where

$R_1$

denotes the world interest rate on bonds in period

$R_1$

denotes the world interest rate on bonds in period

$1$

.Footnote

25

$1$

.Footnote

25

2.9 Equilibrium

Given the policies

$\{\tau ^a, \tau ^b, \tau ^c\}$

, the equilibrium consists of prices

$\{\tau ^a, \tau ^b, \tau ^c\}$

, the equilibrium consists of prices

$\{Q_t^i\}$

, rates

$\{Q_t^i\}$

, rates

$\{R_1, R_{k,2}^e\}$

and quantities

$\{R_1, R_{k,2}^e\}$

and quantities

$\{B_1^i, K_1^i, F_1^e, D, C_t^i, I_t^i\}$

for

$\{B_1^i, K_1^i, F_1^e, D, C_t^i, I_t^i\}$

for

$t=\{1,2\}$

, with

$t=\{1,2\}$

, with

$i=\{a,b,c\}$

,

$i=\{a,b,c\}$

,

$e=\{a,b\}$

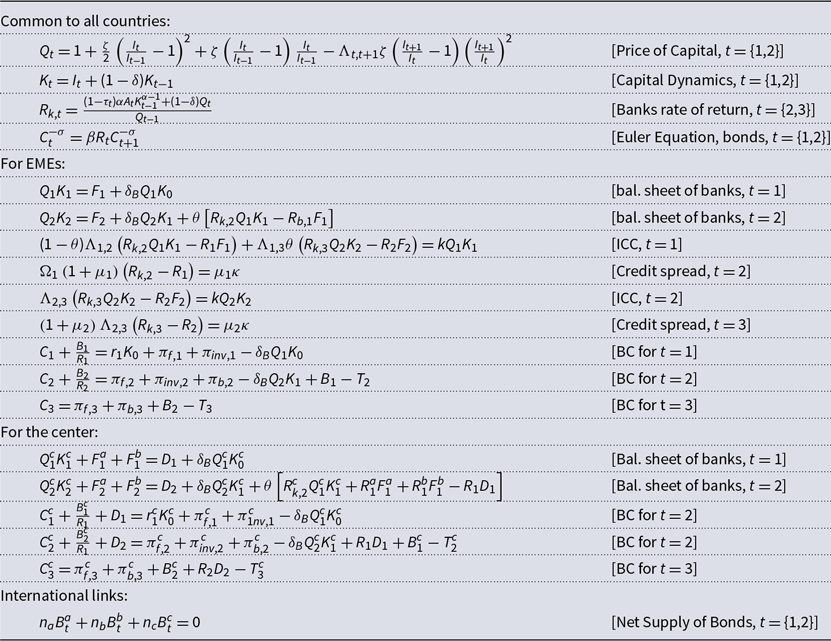

, such that the households solve their utility maximization problem, the firms solve their profits maximization problems, banks maximize their franchise value, and the goods and bonds markets clear. This allocation is characterized by the solution to the system of equations (1)–(13) where some equations apply for the three economies, other show up by country type, and the clearing condition is considered once (26 equations and variables in total). The simplified system of equations we use to solve the model is summarized in Table A1 in Appendix A.

$e=\{a,b\}$

, such that the households solve their utility maximization problem, the firms solve their profits maximization problems, banks maximize their franchise value, and the goods and bonds markets clear. This allocation is characterized by the solution to the system of equations (1)–(13) where some equations apply for the three economies, other show up by country type, and the clearing condition is considered once (26 equations and variables in total). The simplified system of equations we use to solve the model is summarized in Table A1 in Appendix A.

2.10 Some relevant implications of the model

From this setup, we can already derive a number of important results that can be helpful in understanding the policy implications of the model. First, we can link the extent of the inefficiency—captured by the credit spread—and financial friction to a specific parameter (

$\kappa$

):

$\kappa$

):

Proposition 1.

If the ICC binds the credit spread is positive and increases in

$\kappa$

$\kappa$

Proof. W.L.O.G. we will work in a perfect foresight setup, otherwise the same result applies to the expected credit spread. From the F.O.N.C. in equation (6), we can obtain:

\begin{equation*} R_{k,2}^e = \underset {\Phi }{\underbrace {\frac {1+\mu ^e}{1+(1-\kappa )\mu ^e}} }R_{b,1}. \end{equation*}

\begin{equation*} R_{k,2}^e = \underset {\Phi }{\underbrace {\frac {1+\mu ^e}{1+(1-\kappa )\mu ^e}} }R_{b,1}. \end{equation*}

$\Phi \gt 1$

represents the proportionality scale between

$\Phi \gt 1$

represents the proportionality scale between

$R_{k,2}$

and

$R_{k,2}$

and

$R_{b,1}$

and guarantees the credit spread is positive in the model. The larger

$R_{b,1}$

and guarantees the credit spread is positive in the model. The larger

$\Phi$

, the greater the spread. At the same time,

$\Phi$

, the greater the spread. At the same time,

$\mu \gt 0$

by definition of the ICC (and the fact that it binds). Hence, it follows that,

$\mu \gt 0$

by definition of the ICC (and the fact that it binds). Hence, it follows that,

\begin{align*} \frac { \partial \Phi }{\partial \kappa } = \frac {\mu (1+\mu )}{(1-(1-\kappa )\mu )^2}\gt 0 \\[-30pt] \end{align*}

\begin{align*} \frac { \partial \Phi }{\partial \kappa } = \frac {\mu (1+\mu )}{(1-(1-\kappa )\mu )^2}\gt 0 \\[-30pt] \end{align*}

The results and exercises in later sections will exploit extensively this result to draw lessons on the role of the extent of financial frictions in shaping the policy leakages of prudential regulations.Footnote 26

On the other hand, we can derive another result to elaborate on how general is our framework in representing the prudential toolkit in real life:

Proposition 2. An increase in the macroprudential tax decreases the leverage ratio of banks

Proof. W.L.O.G. we will work in a perfect foresight setup, otherwise the same result applies to the expected value of the leverage. In the ICC (binding) we substitute the total foreign lending

$F_1^e = Q_1^eK_1^e - \delta _B Q_1^eK_0^e$

for any emerging economy

$F_1^e = Q_1^eK_1^e - \delta _B Q_1^eK_0^e$

for any emerging economy

$e = \{a,b\}$

and solve for the total assets

$e = \{a,b\}$

and solve for the total assets

$L_1^e = Q_1^eK_1^e$

in terms of the initial net worth of banks:

$L_1^e = Q_1^eK_1^e$

in terms of the initial net worth of banks:

\begin{equation*} L_1 \, = \, \underset {\phi _L: \ \text{leverage ratio}}{\underbrace {\frac {R_{b,1}^e}{R_{b_1}^e-(1-\kappa ^e)R_{k,2}}}}\delta _BQ_1^eK_0^e, \end{equation*}

\begin{equation*} L_1 \, = \, \underset {\phi _L: \ \text{leverage ratio}}{\underbrace {\frac {R_{b,1}^e}{R_{b_1}^e-(1-\kappa ^e)R_{k,2}}}}\delta _BQ_1^eK_0^e, \end{equation*}

We can substitute

$R_{k,2}^e = [(1-\tau ^e)r_2^e - (1-\delta )\xi ^e_2 Q_2]/Q_1$

and differentiate with respect to

$R_{k,2}^e = [(1-\tau ^e)r_2^e - (1-\delta )\xi ^e_2 Q_2]/Q_1$

and differentiate with respect to

$\tau ^e$

:

$\tau ^e$

:

\begin{equation*} \frac {\partial \phi _L}{\partial \tau ^e} \, = \, -\frac {(1-\kappa ^e)R_{b,1}^e(r_2^e)}{\big(R_{b,1}^e-(1-\kappa ^e)R_{k,2}^e\big)^2Q_1^e} \lt 0 \end{equation*}

\begin{equation*} \frac {\partial \phi _L}{\partial \tau ^e} \, = \, -\frac {(1-\kappa ^e)R_{b,1}^e(r_2^e)}{\big(R_{b,1}^e-(1-\kappa ^e)R_{k,2}^e\big)^2Q_1^e} \lt 0 \end{equation*}

This result takes into account that the denominator is never zero given the ICC is binding and the credit spread is positive.

A direct implication of this result is that, as mentioned above, the tool we assume has analogous implications in terms of the standard macroprudential policy toolkit (e.g., leverage ratios).Footnote 27

3. Policy welfare effects between economies

As a first approximation, we can verify analytically the welfare spillover effects between economies from prudential policy actions. We set the welfare based on a social planner problem along the lines of Davis and Devereux (Reference Davis and Devereux2022) in order to find the equilibrium welfare effects of a change in the policy tools: Let the welfare of country

$i$

be expressed as

$i$

be expressed as

$W^i = U^i + \lambda _1^i BC_1^i + \beta \lambda _2^i BC_2^i$

:

$W^i = U^i + \lambda _1^i BC_1^i + \beta \lambda _2^i BC_2^i$

:

\begin{align*} W^e = U^e &+ \lambda _1^e \left ( r_1^e K_0^e + \pi _{f,1}^e + \pi _{inv,1}^e - \delta _b Q_1^e K_0^e - C_1^e - \frac {B_1^{e}}{R_1^e} \right )\\[2pt] &+ \beta \lambda _2^e \big( \pi _{f,2}^e + \pi _{b,2}^e + B_1^e - T^e - C_2^e \big), \qquad \text{for } e=\{a,b\}\\[2pt] W^c = U^c &+ \lambda _1^c \left ( r_1^c K_0^c + \pi _{f,1}^c + \pi _{inv,1}^c - \delta _b Q_1^c K_0^c - C_1^c - \frac {B_1^{c}}{R_1^c} - D_1 \right ) \\[2pt] &+ \beta \lambda _2^c \big( \pi _{f,2}^c + \pi _{b,2}^c + B_1^c + R_{D,1}D_1 - T^c - C_2^c \big). \end{align*}

\begin{align*} W^e = U^e &+ \lambda _1^e \left ( r_1^e K_0^e + \pi _{f,1}^e + \pi _{inv,1}^e - \delta _b Q_1^e K_0^e - C_1^e - \frac {B_1^{e}}{R_1^e} \right )\\[2pt] &+ \beta \lambda _2^e \big( \pi _{f,2}^e + \pi _{b,2}^e + B_1^e - T^e - C_2^e \big), \qquad \text{for } e=\{a,b\}\\[2pt] W^c = U^c &+ \lambda _1^c \left ( r_1^c K_0^c + \pi _{f,1}^c + \pi _{inv,1}^c - \delta _b Q_1^c K_0^c - C_1^c - \frac {B_1^{c}}{R_1^c} - D_1 \right ) \\[2pt] &+ \beta \lambda _2^c \big( \pi _{f,2}^c + \pi _{b,2}^c + B_1^c + R_{D,1}D_1 - T^c - C_2^c \big). \end{align*}

where all variables are defined as before, and

$\lambda ^i_t$

is the Lagrange multiplier associated to the budget constraint of each period. This problem is analogous to a standard planner problem. Nonetheless, the optimality conditions (equilibrium allocations) for other agents are accounted for by the planner. We substitute the profits for banks and firms in accordance with the private equilibrium (ICCs included), the tax rebates, and some of the interest rates (equalized in equilibrium):

$\lambda ^i_t$

is the Lagrange multiplier associated to the budget constraint of each period. This problem is analogous to a standard planner problem. Nonetheless, the optimality conditions (equilibrium allocations) for other agents are accounted for by the planner. We substitute the profits for banks and firms in accordance with the private equilibrium (ICCs included), the tax rebates, and some of the interest rates (equalized in equilibrium):

with

$\phi (\tau ^e) = 1 + (\kappa ^e - 1)(1 - \tau ^e)\alpha . \quad \text{for } e=\{a,b\}$

.

$\phi (\tau ^e) = 1 + (\kappa ^e - 1)(1 - \tau ^e)\alpha . \quad \text{for } e=\{a,b\}$

.

We can see that, for the emerging markets, the direct effect of the regulation tax is not immediately eliminated from the welfare, even from the perspective of the planner. This occurs due to the effect of accounting for a binding ICC in the profits. Conversely, in the advanced economy and in absence of financial frictions, the rebate cancels out with the taxed revenue in the second period.

From these welfare expressions, we will obtain the effects of taxes, via implicit differentiation, and will simplify our resulting expressions by substituting additional optimality conditions from the private equilibrium. It is also worth noting that the convenience of this method relies on the decrease in the number of variables that we must consider as we can ignore the effects on decision variables of the households. For the latter, the optimality conditions (that are equal to zero) will always be a factor of the tax effect on each variable and hence will be canceled out.

3.1 Domestic effects of policy

The direct—or domestic—welfare effect of the tax for the emerging economies is given by,

\begin{align*} \frac {dW^a}{d\tau ^a} = \beta \lambda _2^a \left \{ R_1 I_1^a \frac {dQ^a_1}{d\tau ^a} + \frac {B^a_1}{R_1} \frac {dR_1}{d\tau ^a} + \left ( \phi (\tau ^a) r_2^a + \kappa ^a(1-\delta )\xi _2^a Q_2^a \right ) \frac {dK^a_1}{d\tau ^a} + \alpha (1-\kappa ^a) Y_2 \right \}, \end{align*}

\begin{align*} \frac {dW^a}{d\tau ^a} = \beta \lambda _2^a \left \{ R_1 I_1^a \frac {dQ^a_1}{d\tau ^a} + \frac {B^a_1}{R_1} \frac {dR_1}{d\tau ^a} + \left ( \phi (\tau ^a) r_2^a + \kappa ^a(1-\delta )\xi _2^a Q_2^a \right ) \frac {dK^a_1}{d\tau ^a} + \alpha (1-\kappa ^a) Y_2 \right \}, \end{align*}

where the

$d$

is the total derivative operator. The same functional form applies for country

$d$

is the total derivative operator. The same functional form applies for country

$b$

. Each term in this expression is associated with a source of variations on welfare:Footnote

28

$b$

. Each term in this expression is associated with a source of variations on welfare:Footnote

28

Changes in investment profits: The first term corresponds to changes in the investment profits, and its sign depends on whether the country is investing above or below the reference level in the adjustment cost function. For our parameters and initial state values, the sign is positive.

Changes in external assets position: The second term reflects the welfare effects from changes in the international debt position.

$\tfrac {dR_1}{d\tau ^a}$

is negative as there is a lower demand for funds by the levied banks. The sign of the whole term, however, depends on the sign of

$\tfrac {dR_1}{d\tau ^a}$

is negative as there is a lower demand for funds by the levied banks. The sign of the whole term, however, depends on the sign of

$\tfrac {B_1^a}{R_1}$

(net foreign assets) which is positive for emerging markets (and negative for the center).

$\tfrac {B_1^a}{R_1}$

(net foreign assets) which is positive for emerging markets (and negative for the center).

Change in welfare by distorting capital accumulation: The third term reflects the change in welfare after hindering capital accumulation; hence, it will be proportional to the change in physical capital holdings and to the sources of profit from holding capital, that is, the marginal product of capital as well as its after-depreciation resale value. The sign of this term is negative as capital accumulation lowers with a tax raise.

Finally, the last term reflects the direct effect of the policy tool on welfare. Even from a planners’ perspective, this effect will not cancel out for the emerging markets (as in the center) because of the presence of a binding ICC for these economies. Its sign is positive. Importantly, we can see there are offsetting welfare effects in the entire expression, and at the same time, the signs and magnitudes depend on the reference point and scale of the policy change that each country planner would plan to implement.Footnote 29

For the center economy, the effect is:

\begin{align*} \frac {dW^c}{d\tau ^c} = \beta \lambda _2^c \left \{ R_1 I_1^c \frac {dQ^c_1}{d\tau ^c} + {\frac {B^c_1}{R_1} \frac {dR_1}{d\tau ^c} }+{ \left ( r_2^c + (1-\delta )\xi _2^{c}Q_2^c \right )}\frac {dK_1^c}{d\tau ^c} + R_{b,1}^{e} {\left ( \frac {dF_1^a}{d\tau ^c} + \frac {dF_1^b}{d\tau ^c}\right ) }+ \frac {dR_{b,1}^{e}}{d\tau ^{c}} F_1^{ab} \right \}, \end{align*}

\begin{align*} \frac {dW^c}{d\tau ^c} = \beta \lambda _2^c \left \{ R_1 I_1^c \frac {dQ^c_1}{d\tau ^c} + {\frac {B^c_1}{R_1} \frac {dR_1}{d\tau ^c} }+{ \left ( r_2^c + (1-\delta )\xi _2^{c}Q_2^c \right )}\frac {dK_1^c}{d\tau ^c} + R_{b,1}^{e} {\left ( \frac {dF_1^a}{d\tau ^c} + \frac {dF_1^b}{d\tau ^c}\right ) }+ \frac {dR_{b,1}^{e}}{d\tau ^{c}} F_1^{ab} \right \}, \end{align*}

where

$F_1^{ab} = F_1^a + F_1^b$

is the total intermediation to emerging economies, and

$F_1^{ab} = F_1^a + F_1^b$

is the total intermediation to emerging economies, and

$R_{b,1}^e$

is the interest rate paid by emerging banks (these equalize in equilibrium). The interpretations for the first three terms are analogous to those of the emerging country mentioned above. The final two terms correspond to:

$R_{b,1}^e$

is the interest rate paid by emerging banks (these equalize in equilibrium). The interpretations for the first three terms are analogous to those of the emerging country mentioned above. The final two terms correspond to:

Welfare effect from changes in intermediation profits: this is an effect coming from the change of the tax on the funding quantities or gross rates related to cross-border lending. In the context of the model, this is also related to the scale of aggregate intermediation. This scale affects the centers, as the latter contains the creditor banks for global markets. Notice the emerging markets can also be affected by the dynamics of financial intermediation, but mostly through their implications for their capacity to fund physical capital.

To the risk of being repetitive, it is still important to reiterate that the signs of these effects are not trivial and may lead to varied—and potentially conflicting— welfare effects. For example, depending on the debt position, the country may benefit from higher taxes, which in itself may provide incentives to national policymakers to alter their policy setup to induce changes in the interest rate that improve the financial position of their economy. This in itself may lead to an increased regulatory activity that may disrupt financial stability.

3.2 Cross-border policy effects

The welfare effect between emerging countries is,

\begin{align*} \frac {dW^a}{d\tau ^b} = \beta \lambda _2^a \left \{ R_1 I_1^a \frac {dQ^a_1}{d\tau ^b} + \frac {B^a_1}{R_1} \frac {dR_1}{d\tau ^b} + \left ( \phi (\tau ^a) r_2^a + \kappa ^a(1-\delta )\xi _2^{a}Q_2^a \right ) \frac {dK^a_1}{d\tau ^b} \right \}\!, \end{align*}

\begin{align*} \frac {dW^a}{d\tau ^b} = \beta \lambda _2^a \left \{ R_1 I_1^a \frac {dQ^a_1}{d\tau ^b} + \frac {B^a_1}{R_1} \frac {dR_1}{d\tau ^b} + \left ( \phi (\tau ^a) r_2^a + \kappa ^a(1-\delta )\xi _2^{a}Q_2^a \right ) \frac {dK^a_1}{d\tau ^b} \right \}\!, \end{align*}

with an analogous counterpart following for the effect in

$W^b$

when

$W^b$

when

$\tau ^a$

is changed. Notice this expression is similar to the within-country effect of their own tax. Although, in contrast, the last term is absent given there is not a direct welfare effect from a tax at the cross-country level.

$\tau ^a$

is changed. Notice this expression is similar to the within-country effect of their own tax. Although, in contrast, the last term is absent given there is not a direct welfare effect from a tax at the cross-country level.

The emerging country welfare effect from a change in the center country tax is,

\begin{align*} \frac {dW^a}{d\tau ^c} = \beta \lambda _2^a \left \{R_1 I_1^a \frac {dQ^a_1}{d\tau ^c} + \frac {B^a_1}{R_1} \frac {dR_1}{d\tau ^c} + \left ( \phi (\tau ^a) r_2^a + \kappa ^a(1-\delta )\xi _2^{a}Q_2^a \right ) \frac {dK^a_1}{d\tau ^c} \right \}\!. \end{align*}

\begin{align*} \frac {dW^a}{d\tau ^c} = \beta \lambda _2^a \left \{R_1 I_1^a \frac {dQ^a_1}{d\tau ^c} + \frac {B^a_1}{R_1} \frac {dR_1}{d\tau ^c} + \left ( \phi (\tau ^a) r_2^a + \kappa ^a(1-\delta )\xi _2^{a}Q_2^a \right ) \frac {dK^a_1}{d\tau ^c} \right \}\!. \end{align*}

On the other hand, the effect of a change in an emerging tax in the welfare of the center is,

\begin{align*} \frac {dW^c}{d\tau ^e} = {\beta}{ \lambda} _2^c \left \{R_1 I_1^c \frac {dQ^c_1}{d\tau ^e} + \frac {B^c_1}{R_1} \frac {dR_1}{d\tau ^e} + \left (r_2^c + (1-\delta ){\xi _2^{c}}Q_2^c \right )\frac {dK_1^c}{d\tau ^e} + {R_{b,1}^{e}} \left ( \frac {dF_1^a}{d\tau ^e} + \frac {dF_1^b}{d\tau ^e}\right ) +{ \frac {dR_{b,1}^{e}}{d\tau ^a}} {F_1^{ab} }\right \}\!, \end{align*}

\begin{align*} \frac {dW^c}{d\tau ^e} = {\beta}{ \lambda} _2^c \left \{R_1 I_1^c \frac {dQ^c_1}{d\tau ^e} + \frac {B^c_1}{R_1} \frac {dR_1}{d\tau ^e} + \left (r_2^c + (1-\delta ){\xi _2^{c}}Q_2^c \right )\frac {dK_1^c}{d\tau ^e} + {R_{b,1}^{e}} \left ( \frac {dF_1^a}{d\tau ^e} + \frac {dF_1^b}{d\tau ^e}\right ) +{ \frac {dR_{b,1}^{e}}{d\tau ^a}} {F_1^{ab} }\right \}\!, \end{align*}

where as before

$F^{ab}_1$

is the total intermediation to the emerging economies, and

$F^{ab}_1$

is the total intermediation to the emerging economies, and

$R_{b,1}^e = R_{b,1}^a = R_{b,1}^b$

is the interest rate paid by emerging banks to the center intermediary. The interpretations of each term follow analogous intuitions to those explained in Subsection 3.1.

$R_{b,1}^e = R_{b,1}^a = R_{b,1}^b$

is the interest rate paid by emerging banks to the center intermediary. The interpretations of each term follow analogous intuitions to those explained in Subsection 3.1.

3.2.1 Optimal toolkit and its drivers

We can use these effects expressions as first-order conditions for national planners and derive the optimal taxes (i.e., setting

$dW^i/d\tau ^i = 0$

and solve for

$dW^i/d\tau ^i = 0$

and solve for

$\tau ^i$

). The optimal emerging tax would be:

$\tau ^i$

). The optimal emerging tax would be:

\begin{equation*} \tau ^{e \ *} {=}{\frac {-1}{\alpha ({1} - {\kappa}^{e})}} \left \{ \frac {1}{r_2^e} \left [ \left ( R_1 I^e_1 {\frac {dQ^e_1}{dK^e_1} }+ {\frac {B^e_1}{R_1}} {\frac {dR_1}{dK^e_1}} \right ) + {\kappa ^a} (1-\delta){\xi _2^{e}}Q_2 \right ]\! + {1} {+} {\alpha} {(\kappa ^e - 1)} \right \}\!, \,\,\, {\text{for }} e= \{a,b\}. \end{equation*}

\begin{equation*} \tau ^{e \ *} {=}{\frac {-1}{\alpha ({1} - {\kappa}^{e})}} \left \{ \frac {1}{r_2^e} \left [ \left ( R_1 I^e_1 {\frac {dQ^e_1}{dK^e_1} }+ {\frac {B^e_1}{R_1}} {\frac {dR_1}{dK^e_1}} \right ) + {\kappa ^a} (1-\delta){\xi _2^{e}}Q_2 \right ]\! + {1} {+} {\alpha} {(\kappa ^e - 1)} \right \}\!, \,\,\, {\text{for }} e= \{a,b\}. \end{equation*}

Similarly, for the financial center (

$c$

):

$c$

):

\begin{align*} \tau ^{c \ *} {=} \frac {Q_1^c}{r_2^c} \left \{ R_1 I_1^c \frac {dQ_1^c}{dF^{ab}_1} {+} \frac {B_1^c}{R_1} \frac {dR_1}{dF^{ab}_1} {+} \big (r_2^c {+} (1-\delta )\xi _2^{c}Q_2\big)\frac {dK^c_1}{dF^{ab}_1} +\big(F_1^a + F_1^b\big) \frac {dR_{b,1}^{e}}{dF^{ab}_1} + (1 - \delta )\xi _2^{c}\frac {Q_2}{Q_1^c} \right \} {+} 1, \end{align*}

\begin{align*} \tau ^{c \ *} {=} \frac {Q_1^c}{r_2^c} \left \{ R_1 I_1^c \frac {dQ_1^c}{dF^{ab}_1} {+} \frac {B_1^c}{R_1} \frac {dR_1}{dF^{ab}_1} {+} \big (r_2^c {+} (1-\delta )\xi _2^{c}Q_2\big)\frac {dK^c_1}{dF^{ab}_1} +\big(F_1^a + F_1^b\big) \frac {dR_{b,1}^{e}}{dF^{ab}_1} + (1 - \delta )\xi _2^{c}\frac {Q_2}{Q_1^c} \right \} {+} 1, \end{align*}

with

$dF^{ab}_1 = dF_1^a + dF_1^b$

.

$dF^{ab}_1 = dF_1^a + dF_1^b$

.

From these expressions, we get an idea about the effects driving the optimal taxes. The peripheral tax depends on the effect on prices and interest rates from changes in the capital stock, which is proportional to the investment and foreign bonds position. Other relevant features are the resale price of capital and the marginal product of capital whose increases lead to lower tax values. The intuition here is that, if capital becomes more productive, it is better to distort the economy by less. We will see in later sections that this is a feature distinguishing policy regimes with different levels of decentralization: The more internationally centralized—or coordinated—policies can achieve the same effects with lower interventionism.

Here is useful to remember that, in equilibrium the marginal product of capital is directly taxed by the tool. As a result, we could interpret that in order to have a meaningful effect, the tax (or subsidy) will have to be set more strongly in countries with lower marginal product of capital. Finally, it is noticeable that the extent of the financial distortion (

$\kappa ^e$

) plays an amplifying role—for a stronger financial friction, a more stringent policy stance would have to be implemented.

$\kappa ^e$

) plays an amplifying role—for a stronger financial friction, a more stringent policy stance would have to be implemented.

On the other hand, the financial center optimal tool is driven by the effect of the changed aggregate international intermediation (

$F_1^{ab}$

) on both the sources of revenue for the banking sector (prices and revenue rate), and on domestic capital intermediation. (

$F_1^{ab}$

) on both the sources of revenue for the banking sector (prices and revenue rate), and on domestic capital intermediation. (

$K^c$

). Both features reflect the global creditor role of the center; on one side the former—international lending volume effect—leads to direct changes in profits, but the latter effects reflect a substitution of local for global intermediation as more resources that would go to domestic firms are instead flowing to other locations. In either case, notice how the effects of policy, both at center and peripheries, are pinned down at first by the effect on interbank intermediation and later by how this affects each banks’ profitability.Footnote

30

$K^c$

). Both features reflect the global creditor role of the center; on one side the former—international lending volume effect—leads to direct changes in profits, but the latter effects reflect a substitution of local for global intermediation as more resources that would go to domestic firms are instead flowing to other locations. In either case, notice how the effects of policy, both at center and peripheries, are pinned down at first by the effect on interbank intermediation and later by how this affects each banks’ profitability.Footnote

30

4. Numerical exploration of the policy effects in the model

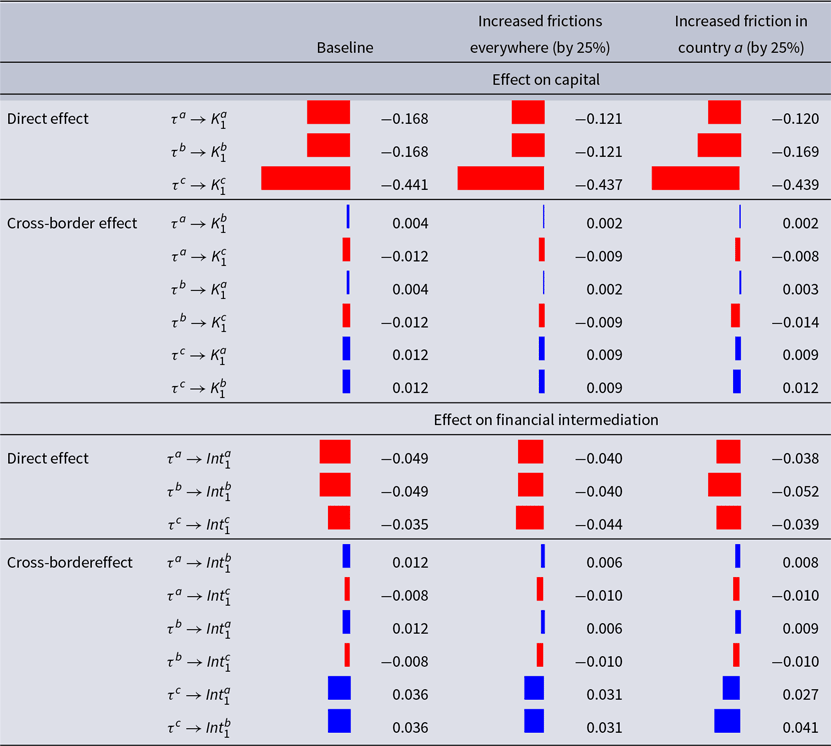

We also can approximate the effects of policy (domestic and cross-border) numerically for the baseline setup. Numerical solutions can be useful to complement the insights indicated in the expressions in the previous section and to gauge the impact of the policy instrument in other variables in the model. Here, for example, we show the effects on capital accumulation and banking intermediation. The results are reported in Table 1.Footnote 31

Policy effects in the model

Note: The effects shown in the table correspond to the numerical approximate to the derivative of each variable with respect to the prudential instrument (

$\tau$

) in each location. The measure is obtained by solving the model with an increased tax (from the location indicated in the row), with no taxes, and then computing the change in the variable between the tax-distorted allocation and the no-taxes equilibrium (

$\tau$

) in each location. The measure is obtained by solving the model with an increased tax (from the location indicated in the row), with no taxes, and then computing the change in the variable between the tax-distorted allocation and the no-taxes equilibrium (

$\tau =0$

). The resulting number is divided by the change in the tax (

$\tau =0$

). The resulting number is divided by the change in the tax (

$\frac {\Delta Variable}{\Delta \tau }$

). The solution in each case is obtained with a nonlinear solver applied to the equations system in Table A1. The superindexes refer to the countries with

$\frac {\Delta Variable}{\Delta \tau }$

). The solution in each case is obtained with a nonlinear solver applied to the equations system in Table A1. The superindexes refer to the countries with

$a$

: EME-A,

$a$

: EME-A,

$b$

: EME-B and

$b$

: EME-B and

$c$

: center. Banking intermediation is measured based on the left-hand side of the balance sheet of the banks, that is,

$c$

: center. Banking intermediation is measured based on the left-hand side of the balance sheet of the banks, that is,

$L_1^e = Q_1K_1^e$

for EM countries (

$L_1^e = Q_1K_1^e$

for EM countries (

$e=\{a,b\}$

) and

$e=\{a,b\}$

) and

$F_1^a + F_1^b + L_1$

for the center. The first column reports the effects for the baseline parameters (Table A2), the second for all frictions parameters increased by 25%, and the third for a parameter for

$F_1^a + F_1^b + L_1$

for the center. The first column reports the effects for the baseline parameters (Table A2), the second for all frictions parameters increased by 25%, and the third for a parameter for

$a$

increased by 25%.

$a$

increased by 25%.

To obtain the numerical solutions, we solve nonlinearly (with a standard numerical search routines) the system of equations characterizing the private equilibrium of the model (shown in Table A1) using the parameters from Table A2. This solution will not activate the shocks at particular levels and also requires the provision of values for the taxes as these are taken as given by the agents. We proceed by solving for the equilibrium with no taxes, and then by applying an increase in each tax instrument by different amounts. Then, we approximate the change in the economic variables by their numerical derivative, that is, by the change in the variable after the tax increase divided by the applied change in the tax.

The results are consistent with the notion that tighter macroprudential regulations are, in their effects, similar to capital controls. We can see, for example, that the local effects of the instrument always lead to a lower capital accumulation which can be rationalized from the negative effect of the tax on the banking returns (and credit spread). At the same time, we can see that the effect of the policy on capital is stronger at the center which can be attributed to substitution effects in intermediation where a lower return in local intermediation activities stimulates a substitution toward foreign lending.

At the same time, we see that the cross-border effect for capital is rather small relative to the direct one which may lead to underestimating the cross-border effects of policy. However, if we focus on the effects on banking intermediation, we can see that a policymaker that cools down intermediation locally is de facto increasing the lending to other economies. This substitution is also consistent with the fact that the financial frictions are potentially interdependent in general equilibrium, and thus, lowering the credit spread at the center (if any) can inadvertently lead to an increased spread and intermediation in other (financially) interconnected economies. Finally, similar results follow for the case of welfare spillovers, even if a quantitative gauge of such variable is less accurate in a simplified setup as the one we exploit here analytically than in a stochastic infinite time environment. We still show some welfare effects in Appendix A that reflect that the cross-border leakages are stronger when stemming from center policies and in environment with stronger financial frictions.

5. The role of dynamic policymaking: An extended model

The baseline framework so far introduces a number of interesting features that, together with a number of simplifications, allow us to explore the drivers of the policy effects analytically. However, once we understand some of these drivers, it is natural to think how would the insights of the model be shaped in other plausible environments. In particular, it can be relevant to understand how the lessons from a setup with static policy decisions extrapolate to the context of dynamic decision-making by regulators.

For this, the most natural extension is to consider a framework where intermediation occurs more than once. In that setup, the policy outlook may change substantially, for if we allow the policies to have a long-lasting effect on the banking profits, and the agents are aware of it, then the policymakers become forward-looking agents. We apply such change to see how relevant—for the presence and nature of the policy spillovers—it is to consider a dynamic decision-making by regulators. We do this by increasing the horizon of the model by one period and by including two new properties common in the literature: retained profits and an entry–exit setup for banks (e.g., Gertler and Karadi, Reference Gertler and Karadi2011; Aoki et al., Reference Aoki, Benigno and Kiyotaki2016, among others).

In the rest of this section, we highlight the most salient changes relative to the baseline model—the banking sector and policies—and leave the (mostly analogous) explanations on the setup for each agent in Appendix E.

General economic environment. The setup is analogous to the previous one, but now there are three periods

$t = \{1,2,3\}$

. The world consists of three countries, two emerging countries and one center, and each economy is populated by five types of agents: households, final goods firms, investors, the government, and a representative bank. As before, the initial capital endowments are given (

$t = \{1,2,3\}$

. The world consists of three countries, two emerging countries and one center, and each economy is populated by five types of agents: households, final goods firms, investors, the government, and a representative bank. As before, the initial capital endowments are given (

$K_0$

), and afterward, physical capital is acquired by firms for production with banking funding. In that sense, there are now two periods of intermediation: the first at the end of the first period and one more a period later. Importantly, as long as there are intermediation activities in the future, the banks may continue in business and in that case retain profits; thus, the banking decisions are dynamic or forward-looking in

$K_0$

), and afterward, physical capital is acquired by firms for production with banking funding. In that sense, there are now two periods of intermediation: the first at the end of the first period and one more a period later. Importantly, as long as there are intermediation activities in the future, the banks may continue in business and in that case retain profits; thus, the banking decisions are dynamic or forward-looking in

$t=1$

, while in

$t=1$

, while in

$t=2$

, the banking problem is static. In what follows, we emphasize on the differences in the decision-making of the bankers and policymakers between these two periods.

$t=2$

, the banking problem is static. In what follows, we emphasize on the differences in the decision-making of the bankers and policymakers between these two periods.

5.1 Banks

EME-Banks. The problem of the bank is extended to account for the probability of continuation in the intermediation activities. This is also reflected in the constraints that now include the balance sheet period of future periods, which is affected by the net worth of the bank that now includes the profits from previous periods.Footnote 32

In the first period of intermediation (end of t = 1), the bank aims to maximize its expected franchise value, given by

$J_1$

, and solves:

$J_1$

, and solves: