1 INTRODUCTION

There is ample empirical evidence of time-varying parameters in many econometric models (see, e.g., Ghysels and Hall, Reference Ghysels and Hall1990; Inoue and Rossi, Reference Inoue and Rossi2011; Caldara et al., Reference Caldara, Fernández-Villaverde, Rubio-Ramírez and Yao2012; Christoffersen, Jacobs, and Ornthanalai, Reference Christoffersen, Jacobs and Ornthanalai2012; Giacomini and Rossi, Reference Giacomini and Rossi2016). Most studies aiming at accommodating this feature assume a fully parametric model for this time variation; one example of this is structural break models. This has the advantage that the time-varying version of a given model stays parametric and can be estimated using existing methods. The disadvantage is that the researcher runs the risk of choosing a misspecified model for the time variation.

To reduce this risk, methods that treat the problem of time-varying parameters as a structured nonparametric one have been developed: They assume that the sequence of time-varying parameters arise as values of an underlying function which is then estimated nonparametrically; one popular class of estimators that falls in this category are local estimators which includes the so-called rolling-window estimator. However, the existing literature has mostly focused on local constant (Nadaraya–Watson) kernel estimators of the time-varying parameters (see, e.g., Dahlhaus, Richter, and Wu, Reference Dahlhaus, Richter and Wu2019; Bardet, Doukhan, and Wintenberger, Reference Bardet, Doukhan and Wintenberger2022).

We here propose to estimate the time-varying parameters using local polynomial estimators since these are known to have a number of attractive properties compared to the local constant one (see, e.g., Fan, Heckman, and Wand, Reference Fan, Heckman and Wand1995). Under very weak restrictions on the model being estimated and the time-series data being used, we develop an asymptotic theory for the estimators. Specifically, we show that they are normally distributed in large samples and provide a complete characterization of the leading variance and bias components.

The class of estimators includes as special cases the local constant estimator and the local linear estimator. We find that the local constant estimator requires stronger regularity conditions to be well-behaved in large samples and will generally suffer from additional biases in the interior of the domain compared to the local linear estimator. These additional biases involve the so-called time derivative process of the stationary approximation to data which is not present in the biases of the local linear one. Moreover, the local linear estimator enjoys the well-known automatic boundary adjustment property: At the beginning and end of the sample, it will perform better than the local constant one. This feature is important since often the main interest is on the values that the time-varying parameters take at the end of the sample.

The two most closely related papers to ours are Dahlhaus et al. (Reference Dahlhaus, Richter and Wu2019) and Bardet et al. (Reference Bardet, Doukhan and Wintenberger2022) who develop a general theory for local constant estimators of time-varying parameters in Markov models and infinite memory models, respectively. Our general framework encompasses theirs as special cases and we consider a broader class of estimators than they do. Moreover, our proof techniques are different and, when specializing to local constant estimators, allow us to arrive at the same results as they do under weaker conditions: First, our theory imposes minimum requirements on the data-generating process (DGP) with the main assumption being that it is locally stationary. Second, it imposes weaker restrictions on the bandwidth used in the estimation; in particular, we can allow for the bandwidth being chosen using standard bandwidth selection rules, such as cross-validation, which is not the case in Dahlhaus et al. (Reference Dahlhaus, Richter and Wu2019) and Bardet et al. (Reference Bardet, Doukhan and Wintenberger2022). Second, we characterize the leading bias term of the estimators, which is in contrast to Dahlhaus et al. (Reference Dahlhaus, Richter and Wu2019) and Bardet et al. (Reference Bardet, Doukhan and Wintenberger2022). To demonstrate these attractive features of our general theory, we apply it to a class of Markov models with exogenous covariates.

Another important feature of our theory is that it also applies to discrete-valued time-series models, such as Poisson autoregressions. Such models are not covered by the theories of Dahlhaus et al. (Reference Dahlhaus, Richter and Wu2019) and Bardet et al. (Reference Bardet, Doukhan and Wintenberger2022) since these require the DGP to be smooth w.r.t. time which is violated when the time series is discrete-valued. In contrast, our theory for local linear estimators impose very weak smoothness conditions on the DGP due to our new proof techniques and so applies to discrete-valued time-series models without any modifications. For the local constant estimator, we combine the ideas and techniques of Truquet (Reference Truquet2019) with our main result to obtain a complete analysis of this estimator.

We also contribute to the literature on asymptotic analysis of local polynomial estimators of varying-coefficient models by extending existing results (see, e.g., Fan et al., Reference Fan, Heckman and Wand1995; Loader, Reference Loader2006) to cover situations where the objective functions are non-concave. This proves to be a non-trivial extension, but at the same time an important one since the log-likelihood functions of many non-linear models are non-concave.

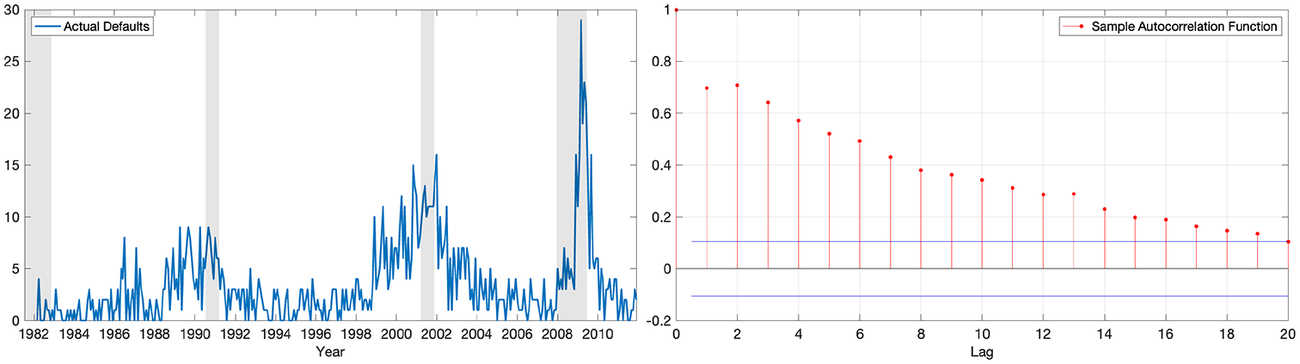

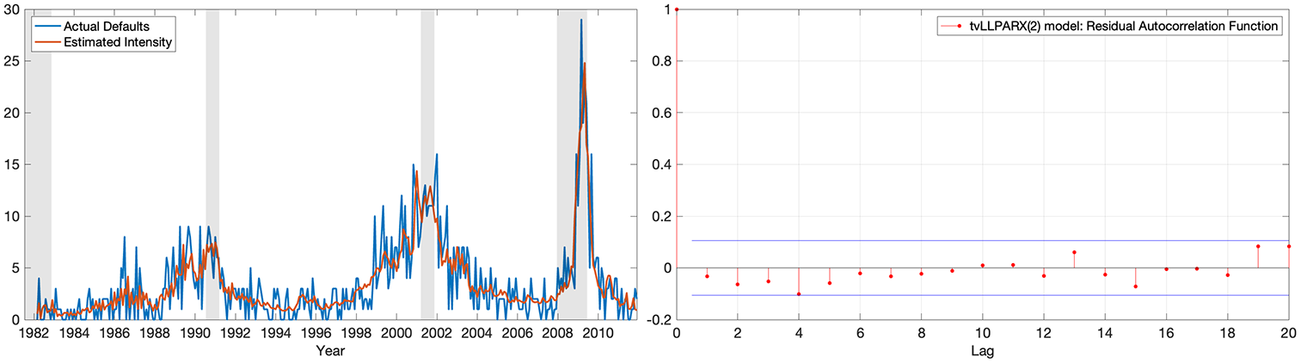

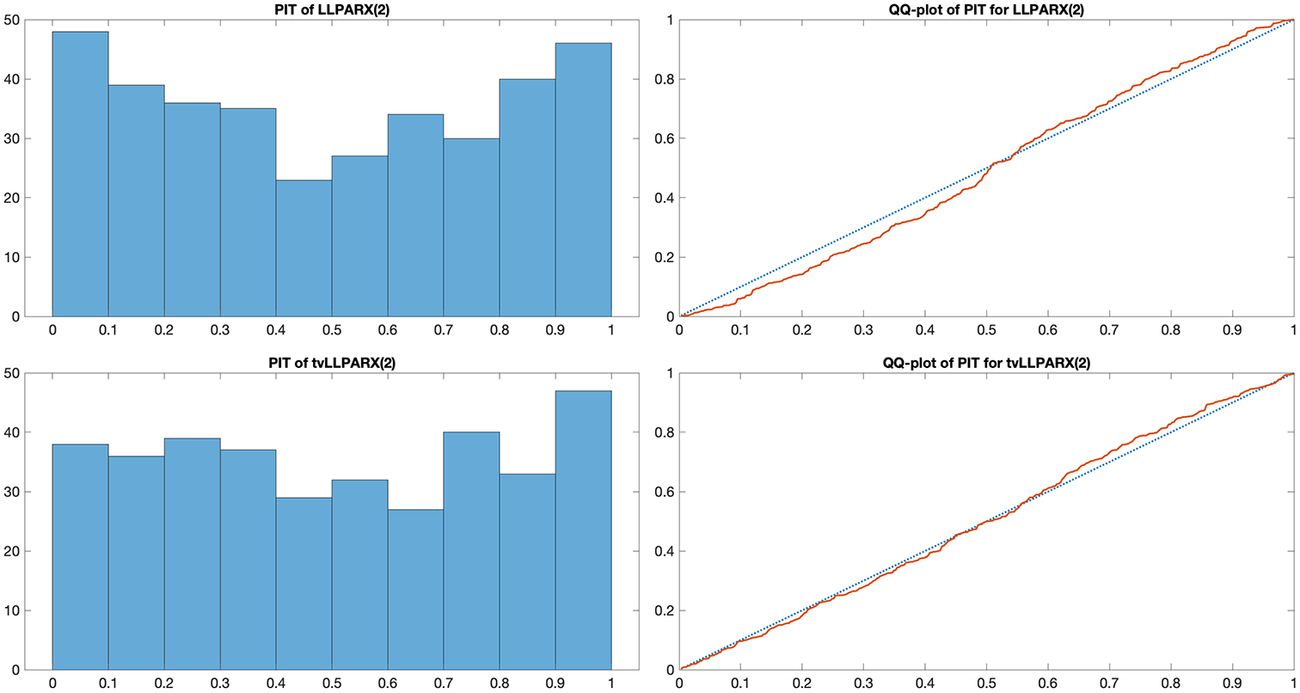

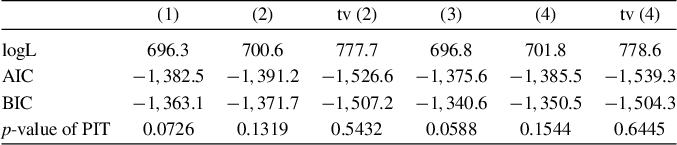

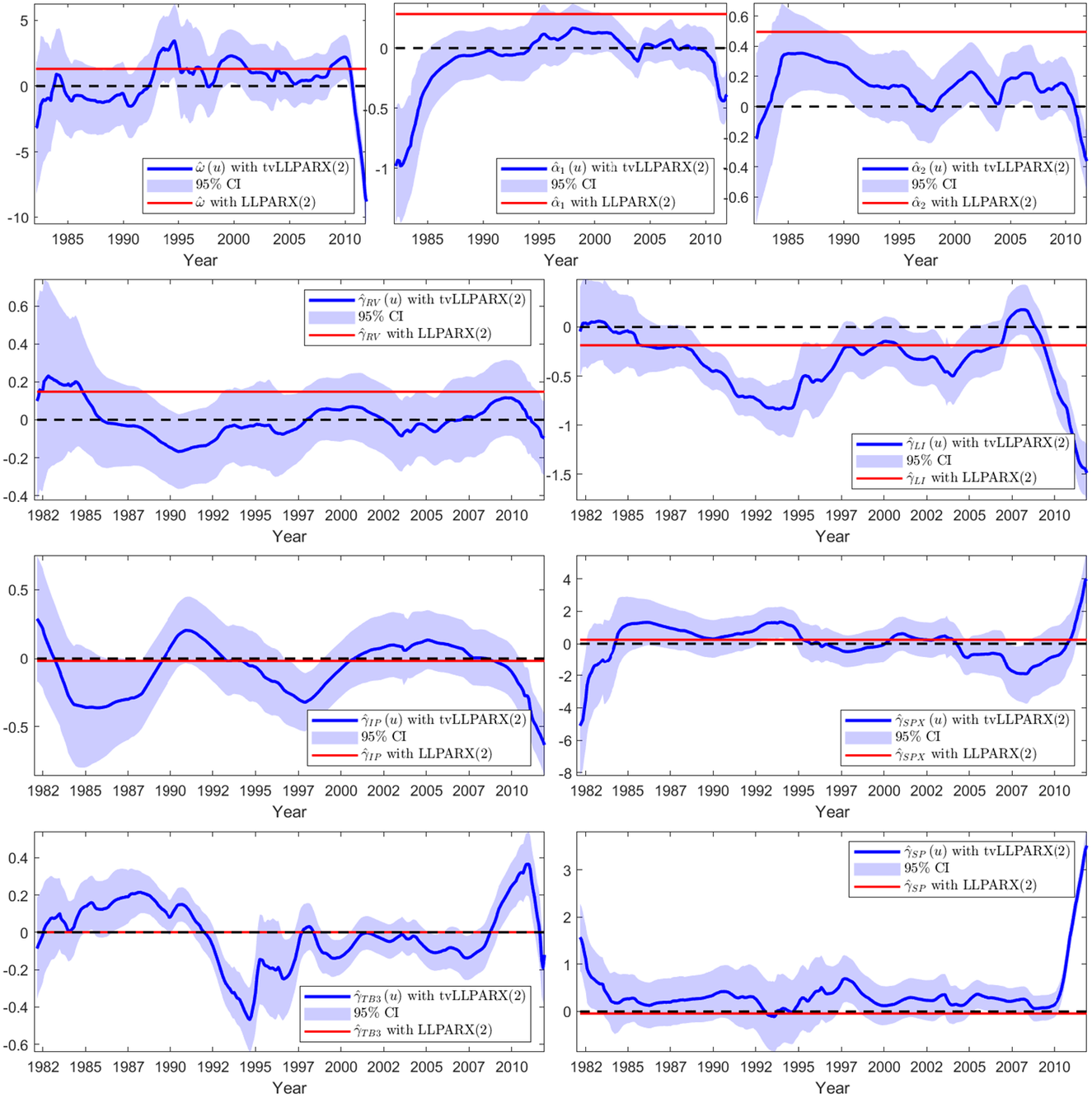

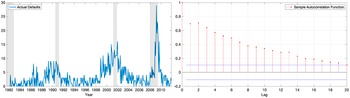

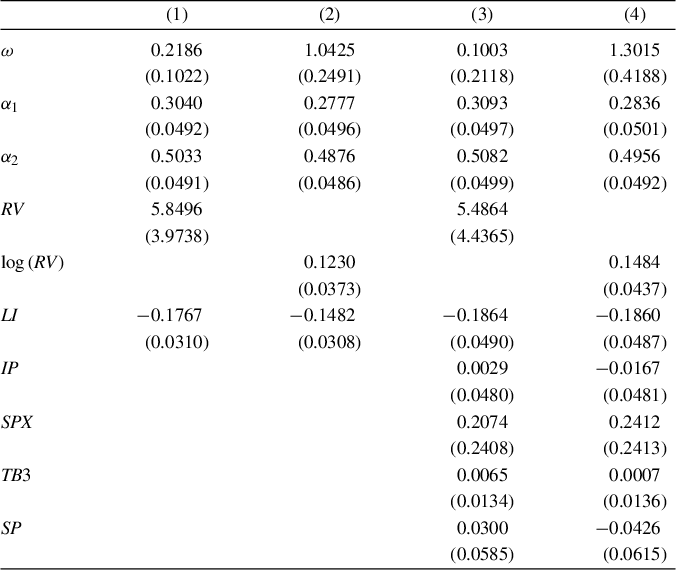

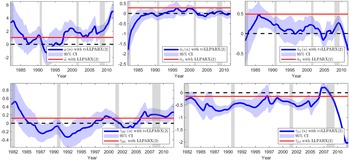

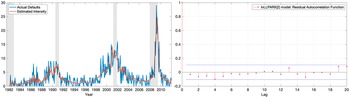

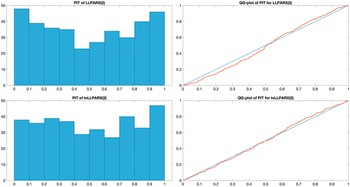

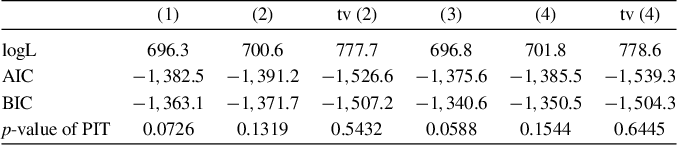

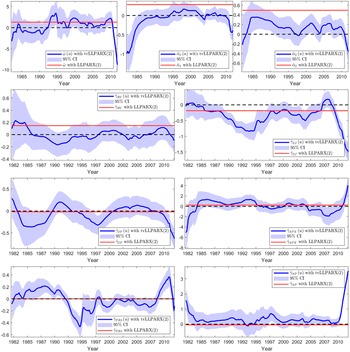

As an empirical application, we revisit the empirical study of Agosto et al. (Reference Agosto, Cavaliere, Kristensen and Rahbek2016), where a Poisson autoregressive model with additional covariates was used to model and analyze U.S. defaults. Using the proposed methodology, we find substantial time variation in the model parameters that the original study was unable to capture. In particular, we find that the ability of macroeconomic and financial variables to predict defaults have varied substantially over time. A battery of informal tests of the time-varying model against the time-invariant version finds strong support for the former.

The remainder of the article is organized as follows. Framework and estimators are introduced in Section 2. Section 3 presents the asymptotic theory of the estimators. Section 4 provides examples of the theory when applied to particular models. We present the results of two simulation studies and the empirical application in Sections 5 and 6, respectively. We conclude in Section 7, where we discuss how our results potentially could be applied to time-varying infinite-memory models. All proofs have been relegated to the Appendix.

2 FRAMEWORK

We are given n observations,

$Z_{n,t}\in \left ( \mathcal {Z},\left \Vert \cdot \right \Vert \right ) $

,

$t=1,\ldots ,n$

,

$t=1,\ldots ,n$

, where

$\left ( \mathcal {Z} ,\left \Vert \cdot \right \Vert \right ) $

, where

$\left ( \mathcal {Z} ,\left \Vert \cdot \right \Vert \right ) $

is a Banach space, from a time-series model characterized by a finite-dimensional vector of unknown parameters

$\theta \in \Theta \subset \mathbb {R}^{d_{\theta }}$

is a Banach space, from a time-series model characterized by a finite-dimensional vector of unknown parameters

$\theta \in \Theta \subset \mathbb {R}^{d_{\theta }}$

to be estimated. In most applications,

$Z_{n,t}$

to be estimated. In most applications,

$Z_{n,t}$

will also be finite-dimensional but our theory allows for, for example, functional data as well. We take as given an objective function

$\ell _{n,t}\left ( \theta \right ) =\ell \left ( \mathcal {Z}_{n,t};\theta \right ) \in \mathbb {R}$

will also be finite-dimensional but our theory allows for, for example, functional data as well. We take as given an objective function

$\ell _{n,t}\left ( \theta \right ) =\ell \left ( \mathcal {Z}_{n,t};\theta \right ) \in \mathbb {R}$

, where

$\mathcal {Z} _{n,t}=\left ( Z_{n,t},\dots Z_{n,0},Z_{n,-1},\dots \right ) $

, where

$\mathcal {Z} _{n,t}=\left ( Z_{n,t},\dots Z_{n,0},Z_{n,-1},\dots \right ) $

. Since we do not observe the process before

$t=1$

. Since we do not observe the process before

$t=1$

, we here initialize the process at deterministic values chosen by us,

$Z_{n,-t}=z_{-t}$

, we here initialize the process at deterministic values chosen by us,

$Z_{n,-t}=z_{-t}$

,

$t\geq 1$

,

$t\geq 1$

. Under regularity conditions stated below, the effect of the initial values will vanish asymptotically.

. Under regularity conditions stated below, the effect of the initial values will vanish asymptotically.

The objective function is assumed to identify the data-generating parameter as its maximizer,

$\theta =\arg \max _{\theta ^{\prime }\in \Theta }\mathbb {E} \left [ \ell _{n,t}\left ( \theta ^{\prime }\right ) \right ] $

, if

$\theta $

, if

$\theta $

indeed was time-invariant, and

$\ell _{n,t}\left ( \theta ^{\prime }\right ) $

indeed was time-invariant, and

$\ell _{n,t}\left ( \theta ^{\prime }\right ) $

was stationary and ergodic. In this case, the natural estimator is to replace population expectations by sample ones and estimate

$\theta $

was stationary and ergodic. In this case, the natural estimator is to replace population expectations by sample ones and estimate

$\theta $

by

$ \hat {\theta }=\arg \max _{\theta ^{\prime }\in \Theta }\frac {1}{n} \sum _{t=1}^{n}\ell _{n,t}\left ( \theta ^{\prime }\right ) $

by

$ \hat {\theta }=\arg \max _{\theta ^{\prime }\in \Theta }\frac {1}{n} \sum _{t=1}^{n}\ell _{n,t}\left ( \theta ^{\prime }\right ) $

.

.

Suppose now that in fact

$\theta $

is varying over time so that

$\mathcal {Z} _{n,t}$

is varying over time so that

$\mathcal {Z} _{n,t}$

is generated by

$\theta _{n,t}=\theta (t/n)$

is generated by

$\theta _{n,t}=\theta (t/n)$

,

$t=1,\ldots ,n$

,

$t=1,\ldots ,n$

, where

$ \theta :\left [ 0,1\right ] \mapsto \Theta $

, where

$ \theta :\left [ 0,1\right ] \mapsto \Theta $

is an unknown function that characterizes the time variation in the parameters.Footnote

1

At the same time, the objective function is still assumed to identify the parameter in the sense that

$\theta \left ( t/n\right ) =\arg \max _{\theta ^{\prime }\in \Theta }\mathbb {E}\left [ \ell _{n,t}\left ( \theta ^{\prime }\right ) \right ] $

is an unknown function that characterizes the time variation in the parameters.Footnote

1

At the same time, the objective function is still assumed to identify the parameter in the sense that

$\theta \left ( t/n\right ) =\arg \max _{\theta ^{\prime }\in \Theta }\mathbb {E}\left [ \ell _{n,t}\left ( \theta ^{\prime }\right ) \right ] $

. We then propose to estimate

$\theta \left ( u\right ) $

. We then propose to estimate

$\theta \left ( u\right ) $

at any given value

$u\in \left [ 0,1\right ] $

at any given value

$u\in \left [ 0,1\right ] $

using local polynomial estimators: First, for

$t/n$

using local polynomial estimators: First, for

$t/n$

in a neighborhood of u, we approximate

$\theta \left ( t/n\right ) $

in a neighborhood of u, we approximate

$\theta \left ( t/n\right ) $

by the following polynomial of order

$m\geq 0$

by the following polynomial of order

$m\geq 0$

:

:

where

$\beta =\left ( \beta _{1}^{\prime },\ldots ,\beta _{m+1}^{\prime }\right ) ^{\prime }\in \mathbb {R}^{\left ( m+1\right ) d_{\theta }}$

with

$\beta _{i+1}=\theta ^{\left ( i\right ) }\left ( u\right ) =\partial ^{i}\theta \left ( u\right ) /\partial u^{i}\in \mathbb {R}^{d_{\theta }}$

with

$\beta _{i+1}=\theta ^{\left ( i\right ) }\left ( u\right ) =\partial ^{i}\theta \left ( u\right ) /\partial u^{i}\in \mathbb {R}^{d_{\theta }}$

and

and

Next, to control the approximation error,

$\theta \left ( t/n\right ) -\theta _{u,\beta }^{\ast }\left ( t/n\right ) $

, we introduce a kernel weighted version of the “global” objective function evaluated at the polynomial approximation:

, we introduce a kernel weighted version of the “global” objective function evaluated at the polynomial approximation:

where

$K_{b}\left ( \cdot \right ) =K\left ( \cdot /b\right ) /b$

,

$K:\mathbb {R} \mapsto \mathbb {R}$

,

$K:\mathbb {R} \mapsto \mathbb {R}$

is a kernel function, and

$b=b_{n}>0$

is a kernel function, and

$b=b_{n}>0$

is a bandwidth. The kernel weights ensure that when

$t/n-u$

is a bandwidth. The kernel weights ensure that when

$t/n-u$

is “large,” the corresponding observations are down weighted in the estimation, thereby controlling for the aforementioned approximation error. We then estimate the polynomial coefficients by

is “large,” the corresponding observations are down weighted in the estimation, thereby controlling for the aforementioned approximation error. We then estimate the polynomial coefficients by

where

The estimated

$\beta $

coefficients are used as estimates of

$\theta \left ( u\right ) $

coefficients are used as estimates of

$\theta \left ( u\right ) $

and its first m derivatives,

$\hat {\theta }^{\left ( i\right ) }\left ( u\right ) =\hat {\beta }_{i+1}\left ( u\right ) $

and its first m derivatives,

$\hat {\theta }^{\left ( i\right ) }\left ( u\right ) =\hat {\beta }_{i+1}\left ( u\right ) $

,

$i=0,\ldots ,m$

,

$i=0,\ldots ,m$

. When

$m=0$

. When

$m=0$

, we recover the standard local-constant estimator. The above class of estimators is similar to the ones considered in Fan et al. (Reference Fan, Heckman and Wand1995) for so-called varying-coefficient models, except that we consider time-series models with the “regressor” that we smooth over being normalized time,

$t/n$

, we recover the standard local-constant estimator. The above class of estimators is similar to the ones considered in Fan et al. (Reference Fan, Heckman and Wand1995) for so-called varying-coefficient models, except that we consider time-series models with the “regressor” that we smooth over being normalized time,

$t/n$

, and do not restrict

$\theta \mapsto \ell _{n,t}\left ( \theta \right ) $

, and do not restrict

$\theta \mapsto \ell _{n,t}\left ( \theta \right ) $

to be convex.

to be convex.

The choice of the order of the polynomial, m, should reflect the degree of smoothness that we are willing to assume

$u\mapsto \theta \left ( u\right ) $

has. If

$\theta \left ( u\right ) $

has. If

$\theta \left ( u\right ) $

is m times differentiable, then we should use this m in the estimation for optimal control of the bias in the nonparametric estimation. On the other hand, increasing the order of the polynomial tends to increase the variability of the resulting estimator, since more local parameters are introduced in the estimation. For a further discussion of this issue, we refer the reader to Section 3.3 of Fan and Gijbels (Reference Fan and Gijbels2018).

is m times differentiable, then we should use this m in the estimation for optimal control of the bias in the nonparametric estimation. On the other hand, increasing the order of the polynomial tends to increase the variability of the resulting estimator, since more local parameters are introduced in the estimation. For a further discussion of this issue, we refer the reader to Section 3.3 of Fan and Gijbels (Reference Fan and Gijbels2018).

Our framework includes Markov processes and stochastic processes with infinite memory (see, e.g., Doukhan and Wintenberger, Reference Doukhan and Wintenberger2008; Bardet et al., Reference Bardet, Doukhan and Wintenberger2022) as special cases. In Section 4, we apply our general theory to the following class of Markov models with exogenous covariates:

where

$G:\mathcal {Y}^{q}\times \mathcal {X}\times \mathcal {E}\times \Theta $

is a known function,

$X_{n,t-1}$

is a known function,

$X_{n,t-1}$

is a Markov process of exogenous covariates, and

$ \varepsilon _{t}$

is a Markov process of exogenous covariates, and

$ \varepsilon _{t}$

is a sequence of errors. For a given specification of G and the distribution of

$\varepsilon _{t}$

is a sequence of errors. For a given specification of G and the distribution of

$\varepsilon _{t}$

, we can then derive the corresponding log-likelihood for the model with time-invariant parameters,

$\ell _{n,t}\left ( \theta \right ) =\ell \left ( Z_{n,t},X_{n,t-1};\theta \right ) $

, we can then derive the corresponding log-likelihood for the model with time-invariant parameters,

$\ell _{n,t}\left ( \theta \right ) =\ell \left ( Z_{n,t},X_{n,t-1};\theta \right ) $

, where

$Z_{n,t}=\left ( Y_{n,t},X_{n,t}\right ) $

, where

$Z_{n,t}=\left ( Y_{n,t},X_{n,t}\right ) $

. Below, we provide three examples of models that our theory applies to.

. Below, we provide three examples of models that our theory applies to.

Example 1. Time-varying threshold autoregressive with exogenous covariates (tv-TAR-X) model with two regimes:

where

$y^{+}:=\max \left \{ y,0\right \} $

and

$y^{-}:=\min \left \{ y,0\right \} $

and

$y^{-}:=\min \left \{ y,0\right \} $

. Here,

$X_{n,t-1}$

. Here,

$X_{n,t-1}$

contains additional predictors, and

$ \varepsilon _{t}$

contains additional predictors, and

$ \varepsilon _{t}$

is i.i.d. with

$\mathbb {E}\left [ \varepsilon _{t}\right ] =0 $

is i.i.d. with

$\mathbb {E}\left [ \varepsilon _{t}\right ] =0 $

and

$\mathbb {E}\left [ \varepsilon _{t}^{2}\right ] <\infty $

and

$\mathbb {E}\left [ \varepsilon _{t}^{2}\right ] <\infty $

. A natural estimator of

$\theta =\left ( \omega ,\alpha _{1}^{\prime },\alpha _{2}^{\prime },\gamma ^{\prime }\right ) ^{\prime }$

. A natural estimator of

$\theta =\left ( \omega ,\alpha _{1}^{\prime },\alpha _{2}^{\prime },\gamma ^{\prime }\right ) ^{\prime }$

is the least-squares one so that

$\ell _{n,t}\left ( \theta \right ) =-\left ( Y_{n,t}-\omega -\sum _{i=1}^{q}\alpha _{1,i}Y_{n,t-1}^{+}-\sum _{i=1}^{q}\alpha _{2,i}Y_{n,t-1}^{-}-\gamma ^{\prime }X_{n,t-1}^{-}\right ) ^{2}$

is the least-squares one so that

$\ell _{n,t}\left ( \theta \right ) =-\left ( Y_{n,t}-\omega -\sum _{i=1}^{q}\alpha _{1,i}Y_{n,t-1}^{+}-\sum _{i=1}^{q}\alpha _{2,i}Y_{n,t-1}^{-}-\gamma ^{\prime }X_{n,t-1}^{-}\right ) ^{2}$

.

.

Example 2. Time-varying ARCH model with covariates (tv-ARCH-X):

where

$\theta =\left ( \omega ,\alpha ^{\prime },\gamma ^{\prime }\right ) ^{\prime }$

,

$\varepsilon _{t}$

,

$\varepsilon _{t}$

is i.i.d. with

$\mathbb {E}\left [ \varepsilon _{t}^{2}\right ] =1,$

is i.i.d. with

$\mathbb {E}\left [ \varepsilon _{t}^{2}\right ] =1,$

and

$X_{n,t-1}$

and

$X_{n,t-1}$

contains additional predictors. The Gaussian log-likelihood function takes the form

$\ell _{n,t}\left ( \theta \right ) =-Y_{n,t}/\lambda _{n,t}\left ( \theta \right ) -\log \left ( \lambda _{n,t}\left ( \theta \right ) \right ) $

contains additional predictors. The Gaussian log-likelihood function takes the form

$\ell _{n,t}\left ( \theta \right ) =-Y_{n,t}/\lambda _{n,t}\left ( \theta \right ) -\log \left ( \lambda _{n,t}\left ( \theta \right ) \right ) $

, where

$\theta =\left ( \omega ,\alpha ^{\prime },\gamma ^{\prime }\right ) ^{\prime }$

, where

$\theta =\left ( \omega ,\alpha ^{\prime },\gamma ^{\prime }\right ) ^{\prime }$

.

.

Example 3. Time-varying Poisson autoregression with exogenous covariates (tv-PARX):

where

$\mathrm {Poisson}\left ( \lambda \right ) $

denotes the Poisson distribution with intensity parameter

$\lambda $

denotes the Poisson distribution with intensity parameter

$\lambda $

,

$\theta =\left ( \omega ,\alpha ^{\prime },\gamma ^{\prime }\right ) ^{\prime }$

,

$\theta =\left ( \omega ,\alpha ^{\prime },\gamma ^{\prime }\right ) ^{\prime }$

, and

$X_{n,t-1}$

, and

$X_{n,t-1}$

contains additional predictors. The log-likelihood function takes the form

$ \ell _{n,t}\left ( \theta \right ) =Y_{n,t}\log \left ( \lambda _{n,t}\left ( \theta \right ) \right ) -\lambda _{n,t}\left ( \theta \right ) $

contains additional predictors. The log-likelihood function takes the form

$ \ell _{n,t}\left ( \theta \right ) =Y_{n,t}\log \left ( \lambda _{n,t}\left ( \theta \right ) \right ) -\lambda _{n,t}\left ( \theta \right ) $

.

.

3 ASYMPTOTIC THEORY

We here provide an asymptotic theory for

$\hat {\beta }$

. One complication of this analysis is that the components of

$\hat {\beta }$

. One complication of this analysis is that the components of

$\hat {\beta }$

converge with different rates. We follow the existing literature and handle this issue by introducing a re-scaled version of

$\hat {\beta }$

converge with different rates. We follow the existing literature and handle this issue by introducing a re-scaled version of

$\hat {\beta }$

(see, e.g., Han and Kristensen, Reference Han and Kristensen2014, for a similar approach): Define

$\hat {\alpha }=U_{n}\hat {\beta }=(\hat {\theta } \left ( u\right ) ^{\prime },b\hat {\theta }^{\left ( 1\right ) }\left ( u\right ) ^{\prime },\ldots ,b^{m}\hat {\theta }^{\left ( m\right ) }\left ( u\right ) ^{\prime })^{\prime }$

(see, e.g., Han and Kristensen, Reference Han and Kristensen2014, for a similar approach): Define

$\hat {\alpha }=U_{n}\hat {\beta }=(\hat {\theta } \left ( u\right ) ^{\prime },b\hat {\theta }^{\left ( 1\right ) }\left ( u\right ) ^{\prime },\ldots ,b^{m}\hat {\theta }^{\left ( m\right ) }\left ( u\right ) ^{\prime })^{\prime }$

, where

, where

is a weighting matrix containing their relative convergence rates, Given that

$U_{n}$

is non-singular, the estimation problem (2) is equivalent to solving

is non-singular, the estimation problem (2) is equivalent to solving

where

$D_{m,b}\left ( u\right ) =D_{m}\left ( u/b\right ) $

and

and

with

$\mathcal {K}$

denoting the support of K. We will then analyze the properties of

$\hat {\alpha }$

denoting the support of K. We will then analyze the properties of

$\hat {\alpha }$

.

.

Due to the time-varying parameters,

$Z_{n,t}$

will generally be non-stationary. To develop an asymptotic theory that allows for this feature, we will rely on the concept of local stationarity as introduced by Dahlhaus (Reference Dahlhaus1997); see also Dahlhaus and Subba Rao (Reference Dahlhaus and Subba Rao2006) and Dahlhaus et al. (Reference Dahlhaus, Richter and Wu2019). We first generalize this concept to sequences of random functions.

will generally be non-stationary. To develop an asymptotic theory that allows for this feature, we will rely on the concept of local stationarity as introduced by Dahlhaus (Reference Dahlhaus1997); see also Dahlhaus and Subba Rao (Reference Dahlhaus and Subba Rao2006) and Dahlhaus et al. (Reference Dahlhaus, Richter and Wu2019). We first generalize this concept to sequences of random functions.

Definition 1. A triangular family of random sequences

$W_{n,t}\left ( \theta \right ) $

,

$\theta \in \Theta $

,

$\theta \in \Theta $

,

$t=1,2,\ldots ,n$

,

$t=1,2,\ldots ,n$

and

$n\geq 1$

and

$n\geq 1$

, is uniformly locally stationary on

$\Theta $

, is uniformly locally stationary on

$\Theta $

(ULS

$\left (p,r,\Theta \right ) $

(ULS

$\left (p,r,\Theta \right ) $

) for some

$ p,r>0$

) for some

$ p,r>0$

if there exists a family of processes

$W_{t}^{\ast }\left ( \theta |u\right ) $

if there exists a family of processes

$W_{t}^{\ast }\left ( \theta |u\right ) $

,

$u\in \left [ 0,1\right ] $

,

$u\in \left [ 0,1\right ] $

, such that: (i) the process

$\left \{ W_{t}^{\ast }\left ( \theta |u\right ) \right \} $

, such that: (i) the process

$\left \{ W_{t}^{\ast }\left ( \theta |u\right ) \right \} $

is stationary and ergodic for all

$\left ( \theta ,u\right ) \in \Theta \times \left [ 0,1\right ] $

is stationary and ergodic for all

$\left ( \theta ,u\right ) \in \Theta \times \left [ 0,1\right ] $

and (ii) for some

$C<\infty $

and (ii) for some

$C<\infty $

and

$\rho <1$

and

$\rho <1$

,

,

If

$W_{n,t}\left ( \theta \right ) =W_{n,t}$

does not depend on any parameters, we write LS

$\left ( p,r\right ) $

does not depend on any parameters, we write LS

$\left ( p,r\right ) $

. The above condition states that

$W_{n,t}\left ( \theta \right ) $

. The above condition states that

$W_{n,t}\left ( \theta \right ) $

may be non-stationary, but it is locally in time well-approximated by a stationary version

$W_{t}^{\ast }\left ( \theta |u\right ) $

may be non-stationary, but it is locally in time well-approximated by a stationary version

$W_{t}^{\ast }\left ( \theta |u\right ) $

. Compared to existing definitions of local stationarity, we allow for an additional term

$\rho ^{t}$

. Compared to existing definitions of local stationarity, we allow for an additional term

$\rho ^{t}$

to appear in the approximation error. This is needed in order to allow for the initial value of

$ W_{n,t}\left ( \theta \right ) $

to appear in the approximation error. This is needed in order to allow for the initial value of

$ W_{n,t}\left ( \theta \right ) $

to be chosen arbitrarily. In contrast, by not including

$\rho ^{t}$

to be chosen arbitrarily. In contrast, by not including

$\rho ^{t}$

in their definitions, most of the existing literature implicitly assumes that

$W_{n,t}\left ( \theta \right ) $

in their definitions, most of the existing literature implicitly assumes that

$W_{n,t}\left ( \theta \right ) $

has been initialized at

$W_{n,0}\left ( \theta \right ) =W_{0}^{\ast }\left ( \theta |u\right ) $

has been initialized at

$W_{n,0}\left ( \theta \right ) =W_{0}^{\ast }\left ( \theta |u\right ) $

. When used in the analysis of local estimators, this latter definition implicitly requires that the DGP changes as the researcher varies u in the local log-likelihood which is a rather peculiar assumption. In contrast, the above definition allows for

$W_{n,0}\left ( \theta \right ) $

. When used in the analysis of local estimators, this latter definition implicitly requires that the DGP changes as the researcher varies u in the local log-likelihood which is a rather peculiar assumption. In contrast, the above definition allows for

$W_{n,0}\left ( \theta \right ) $

to be initialized at a given fixed value—as long as the impact of this dies out with rate

$\rho $

to be initialized at a given fixed value—as long as the impact of this dies out with rate

$\rho $

.

.

For an example of how the additional error term appears in autoregressive models, we refer the reader to the proof of Lemma 3 in Section 4 which allows for arbitrary initialization of the DGP. The additional error term due to different initializations is here assumed to decay geometrically and so our definition rules out long-memory-type processes. This is mostly for simplicity and we expect that most of our results can be generalized to allow for slower decay rates.

We will then require that

$\ell _{n,t}\left ( \theta \right ) $

is ULS

$\left ( p,r,\Theta \right ) $

is ULS

$\left ( p,r,\Theta \right ) $

with stationary approximation

$\ell _{t}^{\ast }\left ( \theta |u\right ) =\ell \left ( \mathcal {Z}_{t}^{\ast }\left ( u\right ) ,\theta \right ) $

with stationary approximation

$\ell _{t}^{\ast }\left ( \theta |u\right ) =\ell \left ( \mathcal {Z}_{t}^{\ast }\left ( u\right ) ,\theta \right ) $

, where

$\mathcal {Z}_{t}^{\ast }\left ( u\right ) =\left ( Z_{t}^{\ast }\left ( u\right ) ,\ Z_{t-1}^{\ast }\left ( u\right ),\dots \right ) $

, where

$\mathcal {Z}_{t}^{\ast }\left ( u\right ) =\left ( Z_{t}^{\ast }\left ( u\right ) ,\ Z_{t-1}^{\ast }\left ( u\right ),\dots \right ) $

is the stationary solution to the model being estimated when

$\theta _{n,t}=\theta \left ( u\right ) $

is the stationary solution to the model being estimated when

$\theta _{n,t}=\theta \left ( u\right ) $

is constant. To illustrate, consider again (3). Under regularity conditions on G and

$\varepsilon _{t}$

is constant. To illustrate, consider again (3). Under regularity conditions on G and

$\varepsilon _{t}$

(see Section 4 for details), the stationary solution will in this case take the form

(see Section 4 for details), the stationary solution will in this case take the form

where we impose the high-level condition that the exogenous covariates are locally stationary. If the DGP is locally stationary, it follows under great generality that the likelihood and its derivatives are also locally stationary (cf. Section 4).

The next step in our proof is to establish a uniform law of large numbers (ULLN) for the stationary approximation of

$Q_{n}\left ( \alpha |u\right ) $

,

$ Q_{n}^{\ast }\left ( \alpha |u\right ) =\frac {1}{n}\sum _{t=1}^{n}K_{b}\left ( t/n-u\right ) \ell _{t}^{\ast }\left ( D_{b}\left ( t/n-u\right ) \alpha |u\right ) $

,

$ Q_{n}^{\ast }\left ( \alpha |u\right ) =\frac {1}{n}\sum _{t=1}^{n}K_{b}\left ( t/n-u\right ) \ell _{t}^{\ast }\left ( D_{b}\left ( t/n-u\right ) \alpha |u\right ) $

. A sufficient condition for a ULLN to hold is that

$\theta \mapsto \ell _{n,t}^{\ast }\left ( \theta |u\right ) $

. A sufficient condition for a ULLN to hold is that

$\theta \mapsto \ell _{n,t}^{\ast }\left ( \theta |u\right ) $

is

$L_{p}$

is

$L_{p}$

-continuous.

-continuous.

Definition 2. A stationary process

$W_{t}^{\ast }\left ( \theta |u\right ) $

is said to be

$L_{p}$

is said to be

$L_{p}$

-continuous w.r.t.

$\theta $

-continuous w.r.t.

$\theta $

if

$ \mathbb {E}\left [ \left \Vert W_{t}^{\ast }\left ( \theta |u\right ) \right \Vert ^{p}\right ] <\infty $

if

$ \mathbb {E}\left [ \left \Vert W_{t}^{\ast }\left ( \theta |u\right ) \right \Vert ^{p}\right ] <\infty $

for all

$\theta \in \Theta $

for all

$\theta \in \Theta $

and

and

Imposing

$L_{p}$

-continuity w.r.t.

$\theta $

-continuity w.r.t.

$\theta $

is weaker than almost surely continuity: If

$\theta \mapsto W_{t}^{\ast }\left ( \theta |u\right ) $

is weaker than almost surely continuity: If

$\theta \mapsto W_{t}^{\ast }\left ( \theta |u\right ) $

is almost surely continuous with

$\mathbb {E}\left [ \sup _{\theta \in \Theta }\left \Vert W_{t}^{\ast }\left ( \theta |u\right ) \right \Vert ^{p}\right ] <\infty , $

is almost surely continuous with

$\mathbb {E}\left [ \sup _{\theta \in \Theta }\left \Vert W_{t}^{\ast }\left ( \theta |u\right ) \right \Vert ^{p}\right ] <\infty , $

the process is also

$L_{p}$

the process is also

$L_{p}$

-continuous since

$DW_{t}(\delta )=\sup _{\Vert \theta -\theta ^{\prime }\Vert \leq \delta }\left \Vert W_{t}^{\ast }\left ( \theta |u\right ) -W_{t}^{\ast }\left ( \theta ^{\prime }|u\right ) \right \Vert ^{p}$

-continuous since

$DW_{t}(\delta )=\sup _{\Vert \theta -\theta ^{\prime }\Vert \leq \delta }\left \Vert W_{t}^{\ast }\left ( \theta |u\right ) -W_{t}^{\ast }\left ( \theta ^{\prime }|u\right ) \right \Vert ^{p}$

,

$\delta>0$

,

$\delta>0$

, will then satisfy

$\lim _{\delta \rightarrow 0}DW_{t}(\delta )=0$

, will then satisfy

$\lim _{\delta \rightarrow 0}DW_{t}(\delta )=0$

almost surely and so, by dominated convergence,

$\lim _{\delta \rightarrow 0}\mathbb {E}[DW_{t}(\delta )]=0$

almost surely and so, by dominated convergence,

$\lim _{\delta \rightarrow 0}\mathbb {E}[DW_{t}(\delta )]=0$

. It is easily verified that

$L_{p}$

. It is easily verified that

$L_{p}$

-continuity w.r.t.

$\theta $

-continuity w.r.t.

$\theta $

implies stochastic equicontinuity of

$Q_{n}^{\ast }\left ( \alpha |u\right ) $

implies stochastic equicontinuity of

$Q_{n}^{\ast }\left ( \alpha |u\right ) $

and so a ULLN holds (cf. Lemma A(i) in Appendix A.1).

and so a ULLN holds (cf. Lemma A(i) in Appendix A.1).

We are now ready to state the regularity conditions used to show consistency.

Assumption 1. (i)

$K\left ( \cdot \right ) \geq 0$

has compact support

$ \mathcal {K}$

has compact support

$ \mathcal {K}$

and

$\int _{-\infty }^{+\infty }K\left ( v\right ) dv=1$

and

$\int _{-\infty }^{+\infty }K\left ( v\right ) dv=1$

; (ii) for some

$\Lambda <\infty $

; (ii) for some

$\Lambda <\infty $

,

$\left \vert K(v)-K(\tilde {v})\right \vert \leq \Lambda \left \vert v-\tilde {v}\right \vert $

,

$\left \vert K(v)-K(\tilde {v})\right \vert \leq \Lambda \left \vert v-\tilde {v}\right \vert $

,

$v,\tilde {v}\in \mathbb {R}$

,

$v,\tilde {v}\in \mathbb {R}$

; and (iii)

$v\mapsto \theta \left ( v\right ) $

; and (iii)

$v\mapsto \theta \left ( v\right ) $

is continuous at u.

is continuous at u.

Assumption 2. (i)

$\Theta $

is compact and the true value

$ \theta \left ( u\right ) \in \Theta $

is compact and the true value

$ \theta \left ( u\right ) \in \Theta $

; (ii)

$\theta \mapsto \ell _{t}^{\ast }\left ( \theta |u\right ) $

; (ii)

$\theta \mapsto \ell _{t}^{\ast }\left ( \theta |u\right ) $

is

$L_{1}$

is

$L_{1}$

-continuous; and (iii)

$\theta \mapsto \mathbb {E}\left [ \ell _{t}^{\ast }\left ( \theta |u\right ) \right ] $

-continuous; and (iii)

$\theta \mapsto \mathbb {E}\left [ \ell _{t}^{\ast }\left ( \theta |u\right ) \right ] $

has a unique maximum at

$\theta \left ( u\right ) \in \Theta $

has a unique maximum at

$\theta \left ( u\right ) \in \Theta $

.

.

Assumption 3.

$\ell _{n,t}\left ( \theta \right ) $

is ULS

$\left ( 1,r,\Theta \right ) $

is ULS

$\left ( 1,r,\Theta \right ) $

for some

$r>0$

for some

$r>0$

with stationary approximation

$\ell _{t}^{\ast }\left ( \theta |u\right ) $

with stationary approximation

$\ell _{t}^{\ast }\left ( \theta |u\right ) $

.

.

Assumption 1(i) imposes stronger than usual assumptions on

$ K$

and excludes, among others, the Gaussian kernel and higher-order kernels. It includes, on the other hand, the Epanechnikov and the triangular kernel. The restriction that

$K\left ( \cdot \right ) \geq 0$

and excludes, among others, the Gaussian kernel and higher-order kernels. It includes, on the other hand, the Epanechnikov and the triangular kernel. The restriction that

$K\left ( \cdot \right ) \geq 0$

is used to ensure the identification of the parameters when

$m>0$

is used to ensure the identification of the parameters when

$m>0$

; without this, identification is not necessarily guaranteed; see below for further discussion. For the analysis of the local constant estimator (

$m=0$

; without this, identification is not necessarily guaranteed; see below for further discussion. For the analysis of the local constant estimator (

$m=0$

), all subsequent results will go through with K having full support and taking negative values.

), all subsequent results will go through with K having full support and taking negative values.

The compact support assumption greatly simplifies our analysis of local polynomial estimation of non-concave models: In order to establish uniform convergence of the likelihood, we require

$\Theta $

to be compact as is standard in the literature. But under this restriction, it is easily checked that

$D_{m,b}\left ( v\right ) \alpha \notin \Theta $

to be compact as is standard in the literature. But under this restriction, it is easily checked that

$D_{m,b}\left ( v\right ) \alpha \notin \Theta $

as

$b\rightarrow 0$

as

$b\rightarrow 0$

for any given

$\alpha =\left ( \alpha _{1},\ldots ,\alpha _{m+1}\right ) $

for any given

$\alpha =\left ( \alpha _{1},\ldots ,\alpha _{m+1}\right ) $

with

$ \alpha _{i}\neq 0$

with

$ \alpha _{i}\neq 0$

for some

$i\geq 1$

for some

$i\geq 1$

and any

$v\neq 0$

and any

$v\neq 0$

. Thus, to allow for kernels with unbounded support, we would generally need the parameter space

$ \mathcal {A}$

. Thus, to allow for kernels with unbounded support, we would generally need the parameter space

$ \mathcal {A}$

, as defined in (8), to collapse at

$\left \{ \left ( \alpha _{1},0,\ldots ,0\right ) :\alpha _{1}\in \Theta \right \} $

, as defined in (8), to collapse at

$\left \{ \left ( \alpha _{1},0,\ldots ,0\right ) :\alpha _{1}\in \Theta \right \} $

as

$ b\rightarrow 0$

as

$ b\rightarrow 0$

. Such shrinking behavior in turn means that a formal Taylor expansion of

$\ell _{n,t}\left ( D_{m,b}\left ( v\right ) \alpha \right ) $

. Such shrinking behavior in turn means that a formal Taylor expansion of

$\ell _{n,t}\left ( D_{m,b}\left ( v\right ) \alpha \right ) $

w.r.t.

$\alpha $

w.r.t.

$\alpha $

is difficult to obtain and so standard arguments to establish asymptotic normality of

$\hat {\alpha }$

is difficult to obtain and so standard arguments to establish asymptotic normality of

$\hat {\alpha }$

cannot be applied. On the other hand, by restricting the support

$\mathcal {K}$

cannot be applied. On the other hand, by restricting the support

$\mathcal {K}$

to be compact,

$ K_{b}\left ( v\right ) \ell _{n,t}\left ( D_{m,b}\left ( v\right ) \alpha \right ) $

to be compact,

$ K_{b}\left ( v\right ) \ell _{n,t}\left ( D_{m,b}\left ( v\right ) \alpha \right ) $

is well-defined for all

$\alpha \in \mathcal {A}$

is well-defined for all

$\alpha \in \mathcal {A}$

and

$v\in \mathbb {R}$

and

$v\in \mathbb {R}$

(where we set

$K_{b}\left ( v\right ) \ell _{n,t}\left ( D_{m,b}\left ( v\right ) \alpha \right ) =0$

(where we set

$K_{b}\left ( v\right ) \ell _{n,t}\left ( D_{m,b}\left ( v\right ) \alpha \right ) =0$

for

$v/b\notin \mathcal {K}$

for

$v/b\notin \mathcal {K}$

). Moreover,

$\left ( \alpha _{1},0,\ldots ,0\right ) $

). Moreover,

$\left ( \alpha _{1},0,\ldots ,0\right ) $

is an interior point of

$\mathcal {A,}$

is an interior point of

$\mathcal {A,}$

and so in our analysis of

$\hat {\alpha ,}$

and so in our analysis of

$\hat {\alpha ,}$

we can employ standard arguments involving a Taylor expansion of the score function around this point.

we can employ standard arguments involving a Taylor expansion of the score function around this point.

Assumption 2 is standard in the analysis of “global” extremum estimators of stationary models on the form

$\tilde {\theta }\left ( u\right ) =\arg \max _{\theta \in \Theta }\sum _{t=1}^{n}\ell _{t}^{\ast }\left ( \theta |u\right ) /n$

. In particular, for a given time-series model, we can import existing results for verification of Assumption 2 (ii) and (iii); see Section 4 for more details. Assumption 2 in conjunction with

$K\left ( \cdot \right ) \geq 0$

. In particular, for a given time-series model, we can import existing results for verification of Assumption 2 (ii) and (iii); see Section 4 for more details. Assumption 2 in conjunction with

$K\left ( \cdot \right ) \geq 0$

ensures that the local polynomial estimator identifies

$\theta \left ( u\right ) $

ensures that the local polynomial estimator identifies

$\theta \left ( u\right ) $

. If we allow for kernels that take negative values, we have to replace Assumption 2(iii) with the following more abstract identification condition: The function

$Q^{\ast }\left ( \alpha |u\right ) =\int K\left ( v\right ) \mathbb {E}\left [ \ell _{t}^{\ast }\left ( D_{m}\left ( v\right ) \alpha |u\right ) \right ] dv$

. If we allow for kernels that take negative values, we have to replace Assumption 2(iii) with the following more abstract identification condition: The function

$Q^{\ast }\left ( \alpha |u\right ) =\int K\left ( v\right ) \mathbb {E}\left [ \ell _{t}^{\ast }\left ( D_{m}\left ( v\right ) \alpha |u\right ) \right ] dv$

satisfies

$Q^{\ast }\left ( \alpha |u\right ) <Q^{\ast }\left ( \left ( \theta \left ( u\right ) ,0,\ldots ,0\right ) |u\right ) $

satisfies

$Q^{\ast }\left ( \alpha |u\right ) <Q^{\ast }\left ( \left ( \theta \left ( u\right ) ,0,\ldots ,0\right ) |u\right ) $

for any

$\alpha \neq \left ( \theta \left ( u\right ) ,0,\ldots ,0\right ) $

for any

$\alpha \neq \left ( \theta \left ( u\right ) ,0,\ldots ,0\right ) $

. We have not been able to provide primitive conditions for this to hold when K can take negative values and so instead impose the positivity constraint on K.

. We have not been able to provide primitive conditions for this to hold when K can take negative values and so instead impose the positivity constraint on K.

If the objective function

$\theta \mapsto \ell _{n,t}\left ( \theta \right ) $

is concave and

$\Theta $

is concave and

$\Theta $

is convex, we can replace Assumption 3 with the following pointwise versions: For any

$\theta \in \Theta $

is convex, we can replace Assumption 3 with the following pointwise versions: For any

$\theta \in \Theta $

,

$\ell _{n,t}\left ( \theta \right ) $

,

$\ell _{n,t}\left ( \theta \right ) $

is locally stationary and

$\mathbb {E}\left [ |\ell _{t}^{\ast }\left ( \theta |u\right ) |\right ] <\infty $

is locally stationary and

$\mathbb {E}\left [ |\ell _{t}^{\ast }\left ( \theta |u\right ) |\right ] <\infty $

(see Theorem 2.7 in Newey and McFadden, Reference Newey and McFadden1994). Under the above assumptions, the following consistency result holds.

(see Theorem 2.7 in Newey and McFadden, Reference Newey and McFadden1994). Under the above assumptions, the following consistency result holds.

Theorem 1. Let Assumptions 1–3 hold. Then, as

$b\rightarrow 0$

and

$nb\rightarrow \infty ,\, \hat {\alpha } \rightarrow ^{p}\left ( \theta \left ( u\right ) ,0,\dots ,0\right ) ^{\prime }$

and

$nb\rightarrow \infty ,\, \hat {\alpha } \rightarrow ^{p}\left ( \theta \left ( u\right ) ,0,\dots ,0\right ) ^{\prime }$

. In particular,

$\hat {\theta }\left ( u\right ) \rightarrow ^{p}\theta \left ( u\right ) $

. In particular,

$\hat {\theta }\left ( u\right ) \rightarrow ^{p}\theta \left ( u\right ) $

.

.

Note that the above theorem only shows the consistency of

$\hat {\theta }\left ( u\right ) $

, and so, at this stage, we cannot make any statements regarding

$ \hat {\theta }^{\left ( i\right ) }\left ( u\right ) $

, and so, at this stage, we cannot make any statements regarding

$ \hat {\theta }^{\left ( i\right ) }\left ( u\right ) $

,

$i=1,\ldots ,m$

,

$i=1,\ldots ,m$

. This is similar to other results for nonlinear extremum estimators that converge with different rates (see, e.g., Theorem 9 in Han and Kristensen, Reference Han and Kristensen2014, where a global consistency result is only provided for the component with the fastest rate).

. This is similar to other results for nonlinear extremum estimators that converge with different rates (see, e.g., Theorem 9 in Han and Kristensen, Reference Han and Kristensen2014, where a global consistency result is only provided for the component with the fastest rate).

However, under additional regularity conditions on the quasi-likelihood function, we can provide a more precise analysis of the estimators, including local consistency of

$\hat {\theta }^{\left ( k\right ) }\left ( u\right ) $

,

$1\leq k\leq m$

,

$1\leq k\leq m$

. With

$s_{n,t}\left ( \theta \right ) =\partial \ell _{n,t}\left ( \theta \right ) /\left ( \partial \theta \right ) \in \mathbb { R}^{d_{\theta }}$

. With

$s_{n,t}\left ( \theta \right ) =\partial \ell _{n,t}\left ( \theta \right ) /\left ( \partial \theta \right ) \in \mathbb { R}^{d_{\theta }}$

and

$h_{n,t}\left ( \theta \right ) =\partial ^{2}\ell _{n,t}\left ( \theta \right ) /(\partial \theta \partial \theta ^{^{\prime }})\in \mathbb {R}^{d_{\theta }\times d_{\theta }}$

and

$h_{n,t}\left ( \theta \right ) =\partial ^{2}\ell _{n,t}\left ( \theta \right ) /(\partial \theta \partial \theta ^{^{\prime }})\in \mathbb {R}^{d_{\theta }\times d_{\theta }}$

,

$D_{n,t}\left ( u\right ) =D_{m,b}\left ( t/n-u\right ) $

,

$D_{n,t}\left ( u\right ) =D_{m,b}\left ( t/n-u\right ) $

and

$K_{n,t}\left ( u\right ) =K_{b}(t/n-u)$

and

$K_{n,t}\left ( u\right ) =K_{b}(t/n-u)$

, the score and Hessian of

$Q_{n}\left ( \alpha |u\right ) $

, the score and Hessian of

$Q_{n}\left ( \alpha |u\right ) $

are given by

are given by

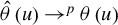

It is easily checked that

$\alpha _{0}:=U_{n}\beta _{0}$

, where

$\beta _{0}=(\theta \left ( u\right ) ^{\prime },\theta ^{\left ( 1\right ) }\left ( u\right ) ^{\prime },\ldots ,\theta ^{\left ( m\right ) }\left ( u\right ) ^{\prime })^{\prime }$

, where

$\beta _{0}=(\theta \left ( u\right ) ^{\prime },\theta ^{\left ( 1\right ) }\left ( u\right ) ^{\prime },\ldots ,\theta ^{\left ( m\right ) }\left ( u\right ) ^{\prime })^{\prime }$

, belongs to the interior of

$\mathcal {A}$

, belongs to the interior of

$\mathcal {A}$

for all n large enough due to Assumption 4(ii) below in conjunction with Assumption 2. Due to the consistency result, so will

$\hat {\alpha }$

for all n large enough due to Assumption 4(ii) below in conjunction with Assumption 2. Due to the consistency result, so will

$\hat {\alpha }$

w.p.a. 1. Thus,

$\hat {\alpha }$

w.p.a. 1. Thus,

$\hat {\alpha }$

will satisfy the first-order condition of (7) which combined with the mean-value theorem yields

will satisfy the first-order condition of (7) which combined with the mean-value theorem yields

where

$\bar {\alpha }$

is situated on the line segment connecting

$\hat {\alpha } $

is situated on the line segment connecting

$\hat {\alpha } $

and

$\alpha _{0}$

and

$\alpha _{0}$

. We then decompose the score function into a bias and variance component,

$S_{n}\left ( \alpha _{0}|u\right ) =B_{n}\left ( u\right ) +S_{n}\left ( u\right ) $

. We then decompose the score function into a bias and variance component,

$S_{n}\left ( \alpha _{0}|u\right ) =B_{n}\left ( u\right ) +S_{n}\left ( u\right ) $

, where

, where

and

$\theta _{u}^{\ast }\left ( t/n\right ) $

was defined in eq. (1). This decomposition is different from the one usually employed in the analysis of kernel estimators of time-varying coefficients, where

$ s_{n,t}$

was defined in eq. (1). This decomposition is different from the one usually employed in the analysis of kernel estimators of time-varying coefficients, where

$ s_{n,t}$

is replaced by the stationary version of the score function evaluated at

$\theta \left ( u\right ) $

is replaced by the stationary version of the score function evaluated at

$\theta \left ( u\right ) $

,

$s_{t}^{\ast }\left ( \theta \left ( u\right ) |u\right ) $

,

$s_{t}^{\ast }\left ( \theta \left ( u\right ) |u\right ) $

(see, e.g., Dahlhaus and Subba Rao, Reference Dahlhaus and Subba Rao2006; Dahlhaus et al., Reference Dahlhaus, Richter and Wu2019). This “usual” choice has the consequence that the corresponding bias term generally involves the time derivative process of the score function and so the resulting analysis tends to impose stronger regularity conditions on the model being estimated. By instead centering the analysis around

$s_{n,t}$

(see, e.g., Dahlhaus and Subba Rao, Reference Dahlhaus and Subba Rao2006; Dahlhaus et al., Reference Dahlhaus, Richter and Wu2019). This “usual” choice has the consequence that the corresponding bias term generally involves the time derivative process of the score function and so the resulting analysis tends to impose stronger regularity conditions on the model being estimated. By instead centering the analysis around

$s_{n,t}$

, we can obtain the leading term of the bias

$ B_{n}\left ( u\right ) $

, we can obtain the leading term of the bias

$ B_{n}\left ( u\right ) $

through a standard Taylor expansion w.r.t.

$\theta $

through a standard Taylor expansion w.r.t.

$\theta $

:

:

Thus, our approach allows for a simpler derivation of the leading bias and variance terms under the following weak regularity conditions.

Assumption 4. (i)

$\theta \mapsto \ell _{n,t}\left ( \theta \right ) $

is twice continuously differentiable; (ii)

$\theta \left ( u\right ) $

is twice continuously differentiable; (ii)

$\theta \left ( u\right ) $

lies in the interior of

$\Theta $

lies in the interior of

$\Theta $

and is

$m+1$

and is

$m+1$

times continuously differentiable; and (iii)

$s_{n,t}$

times continuously differentiable; and (iii)

$s_{n,t}$

is a martingale difference (MGD) array w.r.t.

$\mathcal {F} _{n,t}=\mathcal {F}\left \{ Z_{n,t},Z_{n,t-1},\ldots \right \} $

is a martingale difference (MGD) array w.r.t.

$\mathcal {F} _{n,t}=\mathcal {F}\left \{ Z_{n,t},Z_{n,t-1},\ldots \right \} $

and LS

$\left ( 2,r\right ) $

and LS

$\left ( 2,r\right ) $

with stationary approximation

$s_{t}^{\ast }\left ( \theta \left ( u\right ) |u\right ) $

with stationary approximation

$s_{t}^{\ast }\left ( \theta \left ( u\right ) |u\right ) $

for some

$r>0$

for some

$r>0$

.

.

Assumption 5. (i)

$h_{n,t}\left ( \theta \right ) $

is ULS

$\left ( 1,r, \mathcal {N}\left ( u,\epsilon \right ) \right ) $

is ULS

$\left ( 1,r, \mathcal {N}\left ( u,\epsilon \right ) \right ) $

with continuous stationary approximation

$h_{t}^{\ast }\left ( \theta \left ( u\right ) \right ) $

with continuous stationary approximation

$h_{t}^{\ast }\left ( \theta \left ( u\right ) \right ) $

for some

$r>0$

for some

$r>0$

, where

$\mathcal {N}\left ( u,\epsilon \right ) :=\left \{ \theta\hspace{-0.5pt} \in\hspace{-0.5pt} \Theta :\left \Vert \theta\hspace{-0.5pt} -\hspace{-0.5pt}\theta \left ( u\right ) \right \Vert\hspace{-0.5pt} <\hspace{-0.5pt}\epsilon \right \} $

, where

$\mathcal {N}\left ( u,\epsilon \right ) :=\left \{ \theta\hspace{-0.5pt} \in\hspace{-0.5pt} \Theta :\left \Vert \theta\hspace{-0.5pt} -\hspace{-0.5pt}\theta \left ( u\right ) \right \Vert\hspace{-0.5pt} <\hspace{-0.5pt}\epsilon \right \} $

for some arbitrarily small

$\epsilon>0$

for some arbitrarily small

$\epsilon>0$

and (ii)

$H\left ( u\right ) \equiv \mathbb {E}\left [ h_{t}^{\ast }\left ( \theta (u)|u\right ) \right ] $

and (ii)

$H\left ( u\right ) \equiv \mathbb {E}\left [ h_{t}^{\ast }\left ( \theta (u)|u\right ) \right ] $

is non-singular.

is non-singular.

Similar to Assumption 2, Assumption 4 contains standard regularity conditions used in the analysis of regular parametric estimators on the form

$\tilde {\theta }\left ( u\right ) =\arg \max _{\theta \in \Theta }\sum _{t=1}^{n}\ell _{t}^{\ast }\left ( \theta |u\right ) $

. At the same time, Assumption 4(iii) is non-standard compared to the existing literature (as discussed above) and allows us to apply a novel martingale central limit theorem for locally stationary sequences to

$S_{n}\left ( u\right ) $

. At the same time, Assumption 4(iii) is non-standard compared to the existing literature (as discussed above) and allows us to apply a novel martingale central limit theorem for locally stationary sequences to

$S_{n}\left ( u\right ) $

:

:

(see Lemma A(iii) in Appendix A.1). This result can be seen as a generalization of the standard CLT for stationary and ergodic MGDs that allows for locally stationary processes. The MGD assumption amounts to assuming that the time-varying model is correctly specified and has to be verified on a case-by-case basis (see Section 4.2 for examples of this).

Finally, Assumption 5 together with the expansion in eq. ( 12) is used to derive the limits of

$B_{n}\left ( u\right ) $

and

$H_{n}\left ( \bar {\alpha }|u\right ) $

and

$H_{n}\left ( \bar {\alpha }|u\right ) $

:

:

where

$\mu _{i}=\int _{\mathbb {R}}K\left ( v\right ) v^{m+i}D_{m}\left ( v\right ) dv$

and

$\mathbb {K}_{i}=\int _{\mathbb {R}}K^{i}\left ( v\right ) D_{m}\left ( v\right ) D_{m}\left ( v\right ) ^{\prime }dv$

and

$\mathbb {K}_{i}=\int _{\mathbb {R}}K^{i}\left ( v\right ) D_{m}\left ( v\right ) D_{m}\left ( v\right ) ^{\prime }dv$

,

$i\geq 1$

,

$i\geq 1$

. Combining (9), (13), and (14), we obtain the following theorem.

. Combining (9), (13), and (14), we obtain the following theorem.

Theorem 2. Suppose that Assumptions 1–5 hold. Then, as

$b\rightarrow 0$

and

$nb\rightarrow \infty $

and

$nb\rightarrow \infty $

,

,

where

$R_{n}=diag\left \{ b^{m+1},b^{m},\ldots ,b\right \} \otimes I_{d_{\theta }}$

,

$V(u)=H\left ( u\right ) ^{-1}\Omega \left ( u\right ) H\left ( u\right ) ^{-1}$

,

$V(u)=H\left ( u\right ) ^{-1}\Omega \left ( u\right ) H\left ( u\right ) ^{-1}$

, and

$Bias\left ( u\right ) =\mathbb {K}_{1}^{-1}\mu _{1}\otimes \frac {\theta ^{\left ( m+1\right ) }\left ( u\right ) }{\left ( m+1\right ) !}$

, and

$Bias\left ( u\right ) =\mathbb {K}_{1}^{-1}\mu _{1}\otimes \frac {\theta ^{\left ( m+1\right ) }\left ( u\right ) }{\left ( m+1\right ) !}$

.

.

In particular, for

$i=0,1,\ldots ,m$

,

,

where

$Bias_{i}\left ( u\right ) =\kappa _{1,i}\frac {\theta ^{\left ( m+1\right ) }\left ( u\right ) }{\left ( m+1\right ) !}$

and

$\kappa _{1,i}$

and

$\kappa _{1,i}$

and

$ \kappa _{2,i}$

and

$ \kappa _{2,i}$

denote the ith element of

$\mathbb {K}_{1}^{-1}\mu _{1}$

denote the ith element of

$\mathbb {K}_{1}^{-1}\mu _{1}$

and

$\left ( i,i\right ) $

and

$\left ( i,i\right ) $

th element of

$\mathbb {K}_{1}^{-1}\mathbb {K}_{2}\mathbb {K }_{1}^{-1}$

th element of

$\mathbb {K}_{1}^{-1}\mathbb {K}_{2}\mathbb {K }_{1}^{-1}$

, respectively.

, respectively.

Similar to existing results for local polynomial estimators in a cross-sectional setting, the leading bias term in (15) only depends on

$\theta ^{\left ( m+1\right ) }\left ( u\right ) $

and so the estimators adapt to the curvature of

$\theta \left ( u\right ) $

and so the estimators adapt to the curvature of

$\theta \left ( u\right ) $

. The asymptotic variance in Theorem 2 can be estimated using plug-in methods: It follows from the proof of Theorem 2 that

$ H_{n}\left ( \hat {\alpha }|u\right ) \rightarrow ^{p}\mathbb {K}_{1}\otimes H\left ( u\right ) $

. The asymptotic variance in Theorem 2 can be estimated using plug-in methods: It follows from the proof of Theorem 2 that

$ H_{n}\left ( \hat {\alpha }|u\right ) \rightarrow ^{p}\mathbb {K}_{1}\otimes H\left ( u\right ) $

and

and

Compared to most existing asymptotic results for the local constant estimator, such as Dahlhaus et al. (Reference Dahlhaus, Richter and Wu2019), the above result with

$m\geq 1$

imposes much weaker restrictions on the bandwidth. In particular, standard bandwidth selection rules can be employed here but not under most of the existing theories since their conditions require undersmoothing (i.e.,

$ b\rightarrow 0$

imposes much weaker restrictions on the bandwidth. In particular, standard bandwidth selection rules can be employed here but not under most of the existing theories since their conditions require undersmoothing (i.e.,

$ b\rightarrow 0$

at a faster rate than the optimal one). This is due to the fact that these theories do not provide a complete characterization of the leading bias term. The few papers that do characterize the leading bias term, such as Dahlhaus and Subba Rao (Reference Dahlhaus and Subba Rao2006), require the so-called time derivatives of the stationary score function to exist and be well-behaved since these enter their bias expressions. Our conditions and results, on the other hand, do not require these and are analogous to the ones found in the literature on local polynomial likelihood estimators (see, e.g., Theorem 1b of Fan et al., Reference Fan, Heckman and Wand1995).

at a faster rate than the optimal one). This is due to the fact that these theories do not provide a complete characterization of the leading bias term. The few papers that do characterize the leading bias term, such as Dahlhaus and Subba Rao (Reference Dahlhaus and Subba Rao2006), require the so-called time derivatives of the stationary score function to exist and be well-behaved since these enter their bias expressions. Our conditions and results, on the other hand, do not require these and are analogous to the ones found in the literature on local polynomial likelihood estimators (see, e.g., Theorem 1b of Fan et al., Reference Fan, Heckman and Wand1995).

Equation (15) holds for any value of

$m\geq 0$

and

$ i=0,\ldots ,m$

and

$ i=0,\ldots ,m$

. However, if K is symmetric, then

$\kappa _{1,i}=0$

. However, if K is symmetric, then

$\kappa _{1,i}=0$

when

$m-i$

when

$m-i$

is even. In particular, for the local constant estimator (

$m=i=0$

is even. In particular, for the local constant estimator (

$m=i=0$

), Theorem 2 only informs us that the bias component of

$\hat {\theta } \left ( u\right ) $

), Theorem 2 only informs us that the bias component of

$\hat {\theta } \left ( u\right ) $

is

$o_{p}\left ( b\right ) $

is

$o_{p}\left ( b\right ) $

which is not a sharp rate. To obtain the leading bias term in the cases where

$m-i$

which is not a sharp rate. To obtain the leading bias term in the cases where

$m-i$

is even, a higher-order expansion of

$b_{n,t}$

is even, a higher-order expansion of

$b_{n,t}$

in eq. (10) is necessary. This expansion requires additional assumptions involving aforementioned time derivatives and standard derivatives w.r.t.

$\theta $

in eq. (10) is necessary. This expansion requires additional assumptions involving aforementioned time derivatives and standard derivatives w.r.t.

$\theta $

of

$h_{t}^{\ast }\left ( \theta \left ( u\right ) |u\right ) $

of

$h_{t}^{\ast }\left ( \theta \left ( u\right ) |u\right ) $

. To present these, we need the following additional concept.

. To present these, we need the following additional concept.

Definition 3. A stationary process

$W_{t}^{\ast }\left ( \theta |u\right ) $

is said to be

$ L_{p}$

is said to be

$ L_{p}$

-differentiable w.r.t. u if there exists a stationary and ergodic process

$\partial _{u}W_{t}^{\ast }\left ( \theta |u\right ) $

-differentiable w.r.t. u if there exists a stationary and ergodic process

$\partial _{u}W_{t}^{\ast }\left ( \theta |u\right ) $

with

$ \mathbb {E}\left [ \left \Vert \partial _{u}W_{t}^{\ast }\left ( \theta |u\right ) \right \Vert ^{p}\right ] <\infty $

with

$ \mathbb {E}\left [ \left \Vert \partial _{u}W_{t}^{\ast }\left ( \theta |u\right ) \right \Vert ^{p}\right ] <\infty $

such that

such that

Our definition of time differentiability is slightly weaker compared to the one found in Dahlhaus et al. (Reference Dahlhaus, Richter and Wu2019) and other papers where differentiability w.r.t. u has to hold almost surely. With this definition in hand, we are ready to introduce the following additional regularity conditions in order to derive the leading bias term when

$m-i$

is even.

is even.

Assumption 6.

$\partial h_{n,t}\left ( \theta \right ) /\left ( \partial \theta _{i}\right ) $

exists and is ULS

$\left ( 1,r,\mathcal {N} (u,\epsilon )\right ) $

exists and is ULS

$\left ( 1,r,\mathcal {N} (u,\epsilon )\right ) $

with

$L_{1}$

with

$L_{1}$

-continuous stationary approximation

$ \partial h_{t}^{\ast }\left ( \theta |u\right ) /\left ( \partial \theta _{i}\right ) $

-continuous stationary approximation

$ \partial h_{t}^{\ast }\left ( \theta |u\right ) /\left ( \partial \theta _{i}\right ) $

,

$i=1,\ldots ,d_{\theta }$

,

$i=1,\ldots ,d_{\theta }$

.

.

Assumption 7.

$h_{t}^{\ast }\left ( \theta |u\right ) $

is

$L_{1}$

is

$L_{1}$

-differentiable w.r.t. u at

$\theta =\theta \left ( u\right ) $

-differentiable w.r.t. u at

$\theta =\theta \left ( u\right ) $

with time-derivative

$\partial _{u}h_{t}^{\ast }\left ( \theta \left ( u\right ) |u\right ) =\partial h_{t}^{\ast }\left ( \theta |u\right ) /\left ( \partial u\right ) |_{\theta =\theta \left ( u\right ) }\in \mathbb {R}^{d_{\theta }\times d_{\theta }}$

with time-derivative

$\partial _{u}h_{t}^{\ast }\left ( \theta \left ( u\right ) |u\right ) =\partial h_{t}^{\ast }\left ( \theta |u\right ) /\left ( \partial u\right ) |_{\theta =\theta \left ( u\right ) }\in \mathbb {R}^{d_{\theta }\times d_{\theta }}$

.

.

Assumption 8.

$\sum _{t=1}^{\infty }\left \vert \mathrm {Cov} \left ( h_{ij,0}^{\ast }\left ( \theta \left ( u\right ) |u\right ) ,h_{ij,t}^{\ast }\left ( \theta \left ( u\right ) |u\right ) \right ) \right \vert <\infty $

,

$i,j=1,\ldots ,d_{\theta }.$

,

$i,j=1,\ldots ,d_{\theta }.$

The time-derivative

$\partial _{u}h_{t}^{\ast }\left ( \theta |u\right ) $

will generally involve time derivatives of the underlying stationary approximation of data: If

$h_{t}^{\ast }\left ( \theta |u\right ) =h\left ( \mathcal {Z}_{t}^{\ast }\left ( u\right ) ;\theta \right ) $

will generally involve time derivatives of the underlying stationary approximation of data: If

$h_{t}^{\ast }\left ( \theta |u\right ) =h\left ( \mathcal {Z}_{t}^{\ast }\left ( u\right ) ;\theta \right ) $

for some function

$ h $

for some function

$ h $

which is differentiable w.r.t.

$\mathcal {Z}_{t}^{\ast }\left ( u\right ) $

which is differentiable w.r.t.

$\mathcal {Z}_{t}^{\ast }\left ( u\right ) $

, then it takes the form

$\partial _{u}h_{t}^{\ast }\left ( \theta |u\right ) =\sum _{i=0}^{\infty }\partial h\left ( z_{0},z_{1},z_{2},\dots ;\theta \right ) /\left ( \partial z_{i}\right ) |_{z=\mathcal {Z}_{t}^{\ast }\left ( u\right ) }\times \partial _{u}Z_{t-i}^{\ast }\left ( u\right ) $

, then it takes the form

$\partial _{u}h_{t}^{\ast }\left ( \theta |u\right ) =\sum _{i=0}^{\infty }\partial h\left ( z_{0},z_{1},z_{2},\dots ;\theta \right ) /\left ( \partial z_{i}\right ) |_{z=\mathcal {Z}_{t}^{\ast }\left ( u\right ) }\times \partial _{u}Z_{t-i}^{\ast }\left ( u\right ) $

, where

$\partial _{u}Z_{i,t}^{\ast }\left ( u\right ) $

, where

$\partial _{u}Z_{i,t}^{\ast }\left ( u\right ) $

is the time derivative of

$Z_{t}^{\ast }\left ( u\right ) $

is the time derivative of

$Z_{t}^{\ast }\left ( u\right ) $

. The short memory condition imposed in Assumption 8 is used to control the variance component of the first-order bias term derived in Theorem 2. In Section 4, we use the concept of

$\tau $

. The short memory condition imposed in Assumption 8 is used to control the variance component of the first-order bias term derived in Theorem 2. In Section 4, we use the concept of

$\tau $

—weak dependence (Doukhan and Wintenberger, Reference Doukhan and Wintenberger2008) to verify Assumption 8.

—weak dependence (Doukhan and Wintenberger, Reference Doukhan and Wintenberger2008) to verify Assumption 8.

Under the above additional assumptions, we obtain the following higher-order expansion of the bias component.

Theorem 3. Suppose Assumptions 1–8 hold and

$\theta \left ( \cdot \right ) $

is

$m+2$

is

$m+2$

times continuously differentiable. Then, as

$b\rightarrow 0$

times continuously differentiable. Then, as

$b\rightarrow 0$

and

$nb\rightarrow \infty $

and

$nb\rightarrow \infty $

, the bias

$B_{n}\left ( u\right ) $

, the bias

$B_{n}\left ( u\right ) $

defined in (10) satisfies, with r given in Assumption 6,

defined in (10) satisfies, with r given in Assumption 6,

where, with

$\partial _{u}H\left ( u\right ) =\mathbb {E}\left [ \partial _{u}h_{t}^{\ast }\left ( \theta |u\right ) \right ] _{\theta =\theta \left ( u\right ) }$

and

$\partial _{\theta _{i}}H\left ( u\right ) =\mathbb {E}\left [ \partial h_{t}^{\ast }\left ( \theta |u\right ) /\left ( \partial \theta _{i}\right ) \right ] _{\theta =\theta \left ( u\right ) }$

and

$\partial _{\theta _{i}}H\left ( u\right ) =\mathbb {E}\left [ \partial h_{t}^{\ast }\left ( \theta |u\right ) /\left ( \partial \theta _{i}\right ) \right ] _{\theta =\theta \left ( u\right ) }$

,

,

As a special case, we obtain the following result for the local constant estimator.

Corollary 1. Under the assumptions of Theorem 3 with

$ m=0$

together with

$\int _{\mathbb {R}}K\left ( v\right ) vdv=0$

together with

$\int _{\mathbb {R}}K\left ( v\right ) vdv=0$

, the local constant estimator satisfies, as

$b\rightarrow 0$

, the local constant estimator satisfies, as

$b\rightarrow 0$

,

$nb^{3}\rightarrow \infty , $

,

$nb^{3}\rightarrow \infty , $

and

$n^{\min \left \{ r,1\right \} }b\rightarrow \infty $

and

$n^{\min \left \{ r,1\right \} }b\rightarrow \infty $

,

,

where

$Bias_{0}\left ( u\right ) =H^{-1}\left ( u\right ) \left [ B_{1}(u)+B_{2}\left ( u\right ) \right ] $

and

$B_{1}(u)$

and

$B_{1}(u)$

and

$B_{2}(u)$

and

$B_{2}(u)$

are given in Theorem 3.

are given in Theorem 3.

Two equivalent representations of

$B_{1}(u)+B_{2}\left ( u\right ) $

are, with

$s_{t}^{\ast }\left ( \theta |u\right ) $

are, with

$s_{t}^{\ast }\left ( \theta |u\right ) $

denoting the stationary approximation of

$s_{n,t}\left ( \theta \right ) $

denoting the stationary approximation of

$s_{n,t}\left ( \theta \right ) $

,

,

where the second representation is only well-defined if

$s_{t}^{\ast }\left ( \theta |u\right ) $

is twice

$L_{1}$

is twice

$L_{1}$

-differentiable w.r.t. u.

-differentiable w.r.t. u.

To our knowledge, this is the first complete characterization of the leading bias term of local constant estimators in general time-varying parameter models. The final characterization of the bias,

$B_{1}(u)+B_{2}\left ( u\right ) =-\frac {1}{2}\partial _{u}^{2}\mathbb {E}\left [ s_{t}^{\ast }\left ( \theta \left ( v\right ) |u\right ) \right ] _{v=u}$

, corresponds to the one obtained in Dahlhaus and Subba Rao (Reference Dahlhaus and Subba Rao2006) for the time-varying ARCH model. This characterization, however, requires

$s_{t}^{\ast }\left ( \theta |u\right ) $

, corresponds to the one obtained in Dahlhaus and Subba Rao (Reference Dahlhaus and Subba Rao2006) for the time-varying ARCH model. This characterization, however, requires

$s_{t}^{\ast }\left ( \theta |u\right ) $

to be twice differentiable w.r.t. u, while our characterization only requires

$h_{t}^{\ast }\left ( \theta |u\right ) $

to be twice differentiable w.r.t. u, while our characterization only requires

$h_{t}^{\ast }\left ( \theta |u\right ) $

to be once differentiable w.r.t. u.

to be once differentiable w.r.t. u.

Comparing Theorems 2 and 3, we see that the local linear and local constant estimators share convergence rate and asymptotic variance, but that the latter suffers from additional biases. This is consistent with the theory found for local constant and local linear estimators in a cross-sectional setting (see, e.g., Fan et al., Reference Fan, Heckman and Wand1995).

3.1 Discrete-Valued Time Series

The above theory for the local constant estimator does not cover discrete-valued time-series models. Specifically, Theorem 3 requires

$h_{t}^{\ast }\left ( \theta |u\right ) $

to be differentiable w.r.t. u (cf. Assumption 7). This property rarely holds when

$h_{t}^{\ast }\left ( \theta |u\right ) $

to be differentiable w.r.t. u (cf. Assumption 7). This property rarely holds when

$h_{t}^{\ast }\left ( \theta |u\right ) $

is a function of discrete-valued random variables since these are generally not smooth functions of the underlying parameters of the model (see Truquet, Reference Truquet2019 for more details). Thus, Theorem 3 does not apply to, for example, the Poisson autoregressive model.

is a function of discrete-valued random variables since these are generally not smooth functions of the underlying parameters of the model (see Truquet, Reference Truquet2019 for more details). Thus, Theorem 3 does not apply to, for example, the Poisson autoregressive model.

But Theorem 2 still applies. We therefore combine the ideas of Truquet (Reference Truquet2019, Reference Truquet2020) with Theorem 2 to obtain a theory for the local constant estimator that also covers models with discrete-valued outcomes. This is achieved by replacing Assumptions 7 and 8 with the following ones.

Assumption 9.

$v\mapsto \mathbb {E}\left [ h_{t}^{\ast }\left ( \theta \left ( u\right ) |v\right ) \right ] $

is continuously differentiable at u.

is continuously differentiable at u.

Assumption 10. (i)

$\bar {V}_{ijkl}\left ( v_{1},v_{2}\right ) :=\sum _{t=1}^{\infty }\mathrm {Cov}\left ( h_{ij,0}^{\ast }\left ( \theta \left ( u\right ) |v_{1}\right ) ,h_{kl,t}^{\ast }\left ( \theta \left ( u\right ) |v_{2}\right ) \right ) $

exists for all

$\left ( v_{1},v_{2}\right ) $

exists for all

$\left ( v_{1},v_{2}\right ) $

in a neighborhood of

$\left ( u,u\right ) $

in a neighborhood of

$\left ( u,u\right ) $

and all

$ \left ( i,j,k,l\right ) $

and all

$ \left ( i,j,k,l\right ) $

and (ii)

$\bar {V}_{ijkl}\left ( v_{1},v_{2}\right ) $

and (ii)

$\bar {V}_{ijkl}\left ( v_{1},v_{2}\right ) $

is continuously differentiable at

$\left ( v_{1},v_{2}\right ) =\left ( u,u\right ) $

is continuously differentiable at

$\left ( v_{1},v_{2}\right ) =\left ( u,u\right ) $

.

.

If

$v\mapsto h_{t}^{\ast }\left ( \theta \left ( u\right ) |v\right ) $

is

$ L_{1} $

is

$ L_{1} $

-differentiable w.r.t. v at u, then

$\partial _{v}\mathbb {E}\left [ h_{t}^{\ast }\left ( \theta \left ( u\right ) |v\right ) \right ] _{v=u}=\mathbb {E }\left [ \partial _{v}h_{t}^{\ast }\left ( \theta \left ( u\right ) |v\right ) \right ] _{v=u}$

-differentiable w.r.t. v at u, then

$\partial _{v}\mathbb {E}\left [ h_{t}^{\ast }\left ( \theta \left ( u\right ) |v\right ) \right ] _{v=u}=\mathbb {E }\left [ \partial _{v}h_{t}^{\ast }\left ( \theta \left ( u\right ) |v\right ) \right ] _{v=u}$

. Thus, Assumption 9 is weaker than Assumption 7 and is satisfied as long as the cumulative distribution function of

$h_{t}^{\ast }\left ( \theta \left ( u\right ) |v\right ) $

. Thus, Assumption 9 is weaker than Assumption 7 and is satisfied as long as the cumulative distribution function of

$h_{t}^{\ast }\left ( \theta \left ( u\right ) |v\right ) $

is differentiable w.r.t. v (cf. Lemma 2 below). This property holds for many discrete-valued models, including Poisson autoregressions and dynamic discrete choice models (cf. Truquet, Reference Truquet2019, Reference Truquet2020).

is differentiable w.r.t. v (cf. Lemma 2 below). This property holds for many discrete-valued models, including Poisson autoregressions and dynamic discrete choice models (cf. Truquet, Reference Truquet2019, Reference Truquet2020).

Assumption 10, on the other hand, is stronger than Assumption 8. However, similar to Assumption 8, part (i) is satisfied if

$h_{t}^{\ast }\left ( \theta \left ( u\right ) |v\right ) $

is

$\tau $

is

$\tau $

-weakly dependent for v in a neighborhood of u since this in turn implies that the joint process

$ \left ( h_{t}^{\ast }\left ( \theta \left ( u\right ) |v_{1}\right ) ,h_{t}^{\ast }\left ( \theta \left ( u\right ) |v_{2}\right ) \right ) $

-weakly dependent for v in a neighborhood of u since this in turn implies that the joint process

$ \left ( h_{t}^{\ast }\left ( \theta \left ( u\right ) |v_{1}\right ) ,h_{t}^{\ast }\left ( \theta \left ( u\right ) |v_{2}\right ) \right ) $

is weakly dependent for

$\left ( v_{1},v_{2}\right ) $

is weakly dependent for

$\left ( v_{1},v_{2}\right ) $

in a neighborhood of

$\left ( u,u\right ) $

in a neighborhood of

$\left ( u,u\right ) $

. Moreover, part (ii) will hold under the same conditions that ensure Assumption 9 holds, namely, that the joint distribution function of

$\left ( h_{0}^{\ast }\left ( \theta \left ( u\right ) |v_{1}\right ) ,h_{t}^{\ast }\left ( \theta \left ( u\right ) |v_{2}\right ) \right ) $

. Moreover, part (ii) will hold under the same conditions that ensure Assumption 9 holds, namely, that the joint distribution function of

$\left ( h_{0}^{\ast }\left ( \theta \left ( u\right ) |v_{1}\right ) ,h_{t}^{\ast }\left ( \theta \left ( u\right ) |v_{2}\right ) \right ) $

is differentiable.

is differentiable.

The following result shows that the results for the local constant estimator remain essentially the same under Assumptions 9 and 10 in place of Assumptions 7 and 8.

Theorem 4. Suppose Assumptions 1–6, 9, and 10 hold and

$ \theta \left ( \cdot \right ) $

is

$m+2$

is

$m+2$

times continuously differentiable. Then the conclusions of Theorem 3 and Corollary 1 still hold, except that

$\partial _{u}H\left ( u\right ) $

times continuously differentiable. Then the conclusions of Theorem 3 and Corollary 1 still hold, except that

$\partial _{u}H\left ( u\right ) $

in the expression of

$B_{1}\left ( u\right ) $

in the expression of

$B_{1}\left ( u\right ) $

is now defined as

$\partial _{u}H\left ( u\right ) =\partial _{v}E\left [ h_{t}^{\ast }\left ( \theta \left ( u\right ) |v\right ) \right ] _{v=u}$

is now defined as

$\partial _{u}H\left ( u\right ) =\partial _{v}E\left [ h_{t}^{\ast }\left ( \theta \left ( u\right ) |v\right ) \right ] _{v=u}$

.

.

3.2 Behavior at Boundary

We have already seen that the local linear estimator has smaller biases than the local constant one in the interior of its domain,

$u\in \left ( 0,1\right ) $

. Another well-known advantage of the local linear estimators in a cross-sectional setting is that they exhibit automatic boundary carpentering. This property also holds in our setting where the boundaries are

$u=0$

. Another well-known advantage of the local linear estimators in a cross-sectional setting is that they exhibit automatic boundary carpentering. This property also holds in our setting where the boundaries are

$u=0$

and

$u=1$

and

$u=1$

. Since the results for

$u=1$

. Since the results for