Stunted Industrial Policies in Rwanda

Since the 2008 financial crisis, industrial policy discussions have become increasingly common among policymakers, donors, multilateral institutions and even many neoclassical economists. World Bank chief economists, including Justin Lin and Pinelopi Goldberg, have advocated for market-conforming industrial policy for over a decade (Goldberg & Reed Reference Goldberg and Reed2023; Lin Reference Lin2011). Yet Lin’s New Structural Economics, as well as the kinds of industrial policy advocated by the World Bank, still retains an aversion to state-induced rents. Most mainstream industrial policy only justifies ‘very limited forms of policy correcting market failures rather than creating new markets’ (Cramer et al. Reference Cramer, Sender and Oqubay2020, p. 101).Footnote 1 There is very little recognition that industrial policy is always difficult and has historically always been characterised by some failure. What sets successful industrial policy apart is the capacity of governments to provide ‘rents for learning’ and encourage latecomer firms to invest in technological capability acquisition so they can be competitive in export markets (Khan & Sundaram Reference Khan and Sundaram2000; Whitfield et al. Reference Whitfield, Therkildsen, Buur and Kjaer2015).

Though not always publicly, African governments implemented different forms of industrial policy for decades, albeit with variable outcomes (Rodrik Reference Rodrik2008a). For example, industrial hubs and SEZs were established in Mauritius, Senegal, Uganda, Liberia, Kenya and other African countries (Oqubay & Lin Reference Oqubay and Lin2020). Yet African economies have been reshaped by decades of market-led reforms, including financial liberalisation, reductions in capital and exchange controls, privatisation and trade liberalisation. Accessing finance to invest in industrial policy is also particularly difficult under contemporary globalisation. As discussed in Chapter 5, typical ‘functional substitutes’ (Gerschenkron Reference Gerschenkron1962) – like development banks or state-owned banks – used by previous successful late developers are not widely employed in African countries.

In the twenty-first century, most African countries contend with ideological, political, economic and geographical constraints associated with decades of market-led reforms. In terms of ideological constraints, within African governments, power has shifted to austerity ministries like the Ministry of Finance, which are primarily concerned with providing the right market signals to donors, IFIs and financial markets. On the political side, politicians have found it difficult to build a consensus for the need for industrial policy and targeting specific industries (Whitfield & Buur Reference Whitfield and Buur2014). Trade liberalisation has contributed to empowering importers and transnational companies at the cost of domestic manufacturers (Boone Reference Boone1994). On the economic front, there is still limited policy space – though much of this is in the form of bilateral pressure rather than because of tariff rates prescribed by the WTO (Behuria Reference Behuria and Goodfellow2019; Khan 2007b). On the geographical side, most of the African continent still has inadequate transport infrastructure (road, rail and airfreight). African governments tend to face high transport costs (and a competitive disadvantage) when exporting their goods both within the region and outside it.

While African firms have clearly grown and diversified throughout the continent, this has not been because of conscious industrial policy. Where industrial policy has been strategically employed as part of a national strategy, governments have tended to follow the fashionable advice of GVC/GPN scholarship to partner or ‘strategically couple’ with lead foreign firms to access international export markets (Gereffi et al. Reference Gereffi, Humphrey, Kaplinsky and Sturgeon2011; Yeung Reference Yeung2016). Scholars make arguments, focusing on the experiences of successful East Asian industrialisers, that the most dynamic latecomer firms emerged through strategic engagement with foreign investors (Mathews & Ch Reference Mathews and Cho2000). Most industrial policy proposals for African countries are biased towards encouraging firms to export to European/North American markets. This is understandable because these markets have traditionally been the largest sources of demand for most industrial products. Just as exporting different products increases economic and political autonomy, exporting to different destinations leaves countries less vulnerable when relationships become strained. The Rwandan government has focused on supporting Rwanda-based firms to export to a variety of markets to find ways to break into niches and diversify its sources of foreign exchange. Where it has struggled is in creating effective domestic state–business relationships to promote technological capability acquisition. It could be argued that the Rwandan government should have done more to encourage foreign investors to transfer technology to domestic firms. However, convincing foreign firms to part with their knowledge is no easy feat. Yet even where there may have been some possibility of firms being willing to share knowledge (e.g. in symbolic efforts to engage with lead firms such as Volkswagen and BioNTech), the government has not supported domestic firms to be ready to take advantage of such opportunities.

The Rwandan government did not prioritise manufacturing growth until very recently (since the mid-2010s). There has been some industrial policy success. But this success has been largely within agriculture (processing primary commodities and finding new agriculture exports). In agriculture, in particular, exports have not only aimed at European or North American markets but also targeted regional and Asian markets. As Chapters 1–8 show, diversification has been a central agenda for the Rwandan government.

Investments in manufacturing have lagged despite the focus on diversification. This chapter argues that this is primarily because of the government’s elite vulnerability, as characterised by fractious relationships with domestic capitalists. The RPF initially failed to build effective relationships within the manufacturing sector because many former industrial firms were perceived to have had close relationships with previous governments. Later, several RPF-allied capitalists who owned industrial firms fell out with RPF leadership, with some leaving the country in exile or being jailed. These domestic capitalists have been perceived as threats because of their potential to finance rival coalitions against the RPF. This fear was evident in the early 2000s but has characterised RPF rule more generally, as few capitalists have emerged that are not closely affiliated with the government. The government justifies the limited attention to manufacturing in relation to its broader strategy of transforming its landlocked disadvantages into becoming a land-linked services hub. Part of the RPF’s vision was to focus on manufacturing once enough access to regional and continental markets had been achieved and the cost disadvantages associated with high transport costs had been reduced. However, since 2015, because of increasing high under- and unemployment, the government has begun to prioritise manufacturing. Rwanda’s attempts to revive manufacturing have attracted high-profile investments, including from BioNTech and Volkswagen. There has been some limited success in exporting to regional markets (in construction materials), with government-affiliated companies leading the way.

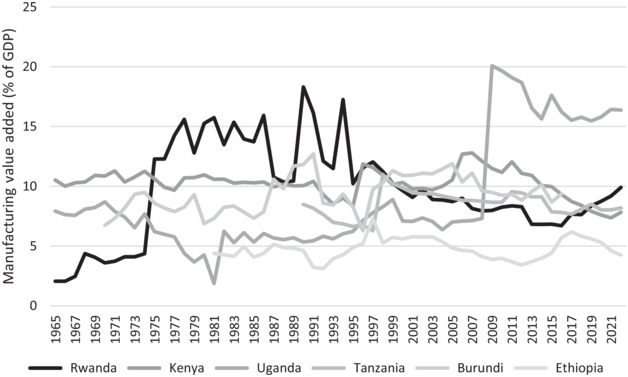

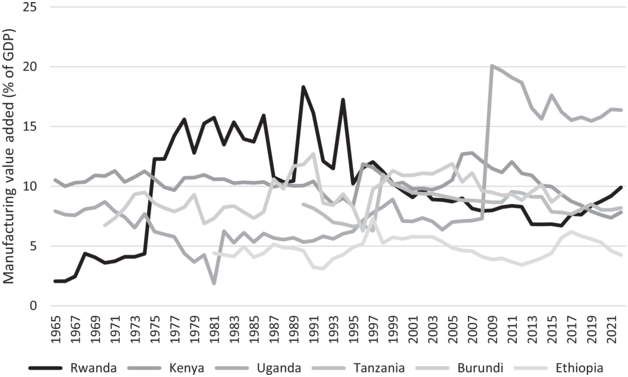

Several government strategy documents (GoR 2017; MINECOFIN 2013, 2020; MINICOM 2011a, 2011b, 2015, 2017) have paid lip service to the industrial sector, but support for manufacturing-focused policies has been slow. As Figure 9.1 shows, manufacturing value added (MVA) as a percentage of GDP, while performing relatively similarly to other East African countries, is much lower than it was in the 1980s. In 2011, Rwanda’s real manufacturing output per capita was $20.4 (about half of what it was in the 1980s). Observers (Gathani & Stoelinga Reference Gathani and Stoelinga2013) argued that Rwanda would only achieve its pre-genocide maximum real manufacturing output per capita by 2025. Yet, as Figure 9.1 shows, Rwanda is still far behind the MVA levels of the 1970s/1980s.

Manufacturing value added (percentage of GDP) for selected East African countries: 1965–2021.

This chapter begins with a discussion of the evolution of industrial policy in Rwanda. It then describes Rwanda’s industrial record. The remainder of the chapter describes how domestic capital has been marginalised in favour of supporting RPF-affiliated firms or relying on foreign investors, particularly for symbolic investments. It does this by providing detailed examples of the construction materials, apparels (textiles and garments) and pharmaceuticals sectors. In line with all other chapters, it shows how elite vulnerability has contributed to the government failing to provide rents for learning to domestic firms, giving them little opportunity to invest in technological capabilities. Thus, like many other African countries, Rwanda’s hopes for structural transformation fall at a key domestic hurdle: building effective state–business relationships aimed at technological capability acquisition for latecomer firms.

Contemporary Industrial Policy in Rwanda: Landlocked or Land-Linked?

When asked why MVA was not at the levels of the 1970s and 1980s, Rwandan government officials argued that in the 1990s, ‘we considered our natural constraints. Because of high transport costs, manufacturing just wasn’t an option’.Footnote 2 Regularly, government officials cited landlocked geographical disadvantages as the reason why a services-oriented development trajectory was preferred. One report suggested that Rwanda’s transport costs represent as high as 40 per cent of export and import values (MINICOM 2011a). One senior government official argued:

Most would say being landlocked is a disadvantage. But we wanted to turn it into an opportunity. Rather than being landlocked, our philosophy was to be land-linked. Our strategy is to become a hub for services. For sports. For tourism. For finance. For airports. When people think of Africa, we want them to think Rwanda is the centre of it.Footnote 3

Rwanda’s development strategy – VISION 2020 – initially outlined the goal of becoming a ‘knowledge-based economy’. The manufacturing sector is barely mentioned in the strategy, with the reasoning that ‘industrial development cannot be realized without a competitive stock of skills, infrastructure and financial services’ (GoR 2000, p. 11). Government officials and businesspeople complained about high transport costs, the limited availability of raw materials, inadequate and inconsistent supplies of energy and limited skills and local training initiatives.

The hub-based strategy quickly became characterised by inadequate employment opportunities for the youth. The EDPRS 2 (MINECOFIN 2013) highlighted the urgent need to create jobs. After the 2008 financial crisis, there was also increasing space to openly discuss industrial policy. Partially also inspired by Ethiopian manufacturing successes, the Rwandan government then made a concerted attempt to publicly highlight the need for industrialisation.Footnote 4 For some government officials, the choice to refocus on industrialisation was part of a broader strategy: to build infrastructure to become a regional hub and then use trade agreements to build competitive advantages in certain manufacturing sectors.

The Rwandan government has been a champion of regional (like the EAC) and continent-wide integration (AfCFTA) efforts, with President Kagame and other senior government officials playing a leading role in calling for the reduction of trade barriers within the continent. Regional industrialisation strategies were integral to Pan-Africanist ambitions in the 1960s and 1970s. Led by UNECA and several national governments, regional integration efforts had a focus on regional industrialisation from the onset. Yet within the AfCFTA and even in regional organisations like the EAC, specialised industrialisation strategies have rarely been prioritised. There have been some initiatives. The AfCFTA Guided Trade Initiative was launched in 2022. Eight countries (including Rwanda) exported goods to each other using the AfCFTA Rules of Origin Certificate, which certifies that a product has been manufactured using materials sourced from Africa, making it eligible for lower customs duties.

There remains a long-standing fear that countries with existing advantages in industrial capabilities (like Kenya in East Africa or South Africa in Southern Africa and Nigeria within West Africa) would benefit more than other members (Odijie Reference Odijie2019). When the old East African Common Market was established in the 1970s, Kenya cemented its position as the region’s industrial hub. Kenya produced more than 70 per cent of the region’s manufactured goods before the Common Market collapsed in 1977 because of tensions within the EAC (Mugomba Reference Mugomba1978; Ravenhill Reference Ravenhill1979). Rwandan officials, while cognisant of this history, remain hopeful of the opportunities that may accompany regional integration. Some academics share the hopeful view that the AfCFTA’s establishment would enhance access to large markets, reduce the burden of distance to the coast for landlocked countries and raise competitiveness against foreign (and particularly Chinese) imports (Naude & Tregenna Reference Naude and Tregenna2023).

Within the Rwandan government, there continues to be a debate about the viability of industrial growth becoming an engine of diversification in the future. The focus of industrial policy, whether it should be directed at capturing domestic and regional markets or whether more priority should be placed on exports to markets outside Africa, has also been debated. IFIs and donors have often criticised the Rwandan government’s initiatives aimed at capturing domestic markets, arguing for ‘export promotion in areas aligned with the country’s comparative advantages’ (World Bank 2019, p. xvi). While commitment to manufacturing has been low, there were some attempts at industrial policy from the mid-2000s. One example is the Kigali SEZ.

SEZs have been associated with varied outcomes across Africa (Farole Reference Farole2011). SEZs are often associated with increases in exports and foreign exchange earnings, as well as increases in employment generation, which depend on large increases in foreign investment. Governments attract foreign investment through providing ‘fiscal incentives, better physical and bureaucratic infrastructure and often also differential labour and environmental regulations’ (Whitfield & Staritz Reference Whitfield, Staritz, Oqubay and Lin2020, p. 931). Too often, however, SEZs have been associated with limited structural transformation because there is not enough focus on backward, forward and horizontal linkages with firms outside the zones, as well as technology transfer from foreign to domestic firms. In many African countries (including Rwanda), attracting investment to such zones simply leads to ‘thin industrialization’ and wastefully provides rents to foreign firms (Whitfield & Staritz Reference Whitfield, Staritz, Oqubay and Lin2020).

In 2006, the Kigali SEZ programme was initially announced. The process in setting up the Kigali SEZ did not follow a systematic analysis of what could be learned from the experiences of establishing SEZs elsewhere. In comparison, prior to constructing its much-celebrated SEZ, the Ethiopian government learnt from experiences elsewhere to prioritise (1) promoting cluster and agglomeration benefits; (2) producing something more than basic products (such as Cut-Make-Trim in apparel) to ensure footloose firms do not leave once labour costs rise and (3) making parks environmentally sustainable and compliant with international standards (Staritz & Whitfield Reference Staritz, Whitfield, Cheru, Cramer and Oqubay2019). The Kigali SEZ was fully operational only in the mid-2010s. Since then, the government has offered incentives to investors, including building factories, providing low rents and waiving taxes on machinery imports. While most of the industrial park’s plots are now on rent, many have long been used as warehouses by factories that had relocated from other premises in Kigali (Behuria Reference Behuria and Goodfellow2019). As of 2024, the government claimed that 155 firms have made investments of over $2 billion in the Kigali SEZ.Footnote 5 So far, there are few signs that Rwanda has done enough to avert the ‘thin industrialization’ trap that many low-income countries have repeatedly fallen into when establishing SEZs.

The government also has plans to establish one additional special economic zone (Bugesera) and seven industrial parks across the country. The construction of these additional facilities was done in haste, with several difficulties coming to the fore. Environmental Impact Assessments were not conducted. This was an obvious mistake given that factories needed to meet the environmental standards necessary to export to European and North American markets. There is also no basic infrastructure (regarding water and electricity), while feasibility studies regarding relocating landowners who have been expropriated had not been carried out (Sabiiti Reference Sabiiti2024e).

The second SEZ is planned close to the new international airport in Bugesera, which is a forty-minute drive from Kigali. ARISE Integrated Industrial Platforms, managed by Indian national Gagan Gupta but funded by the Africa Finance Corporation and Africa Transformation and Industrialization Fund, has been given 40 per cent ownership of the Bugesera Industrial Park (with 60 per cent retained by the government) and is charged with developing the 330 ha facility.Footnote 6 The Bugesera SEZ has eleven industries in operation worth around $95 million of investments.

The 2006 SEZ policy was augmented by a National Industrial Policy in 2011, which highlighted the ‘unsustainable position of the trade deficit’ (MINICOM 2011a, p. 11) and encouraged employing a ‘cluster progression ladder’ to identify which manufacturing sectors to prioritise. The EDPRS 2 (MINECOFIN 2013) mentioned the need to focus on manufacturing and agro-processing exports to create employment. After 2015, industrial policy was pursued more vigorously. The Domestic Market Recapturing Strategy (DMRS) (MINCOM 2015), a strategy to reduce imports in specific sectors and thereby address the widening trade deficit, was announced. Cement, textiles and garments were highlighted as priority sectors. Alongside the DMRS, the Made in Rwanda (MINICOM 2017) policy was launched, which focused on five pillars, including reducing production costs, sector-specific strategies, improving quality, promoting backward linkages and encouraging consumers to buy Rwandan products. Public procurement, which accounted for 12 per cent of GDP (MINICOM 2017), was highlighted as one possible route to boost industrial production, with the bonus that the policy did not violate WTO rules, as Rwanda is not a signatory to the WTO Agreement on Government Procurement.

As industrial policy discussions were gaining traction in 2016, a new Investment Promotion and Facilitation Law was established in 2015 to provide significant incentives to investors. Already by 2019, government officials were receiving complaints that many benefits promised in the previous code were not provided. In 2021, the old law was repealed. A new law was passed that expanded the list of eligible investors to different sectors (with manufacturing as a central focus) and increased incentives available to registered investors. Strategies were revised to focus on three different markets (domestic, regional and Asian/European/North American markets):

We’re learning. Manufacturing is a bit new for us. Since 2015, the domestic market has been important. We need to reduce the import bill. We are also trying to keep our strategic partnerships for high-value products in Western markets. But the biggest opportunity is the Congo. The Congo is a good market for us. That’s our advantage. Otherwise Kenya and Tanzania – maybe Uganda, they have bigger manufacturing companies.Footnote 7

While the increased prioritisation of the industrial sector remains a secondary priority in comparison to services, there is a growing shift in the RPF leadership’s rhetoric and the position of industry within national policy documents. There has been a growing consensus about the urgency to industrialise in Africa Heads of State meetings, as well as in Pan-African organisations such as the AU and the AfDB. To keep in line with this focus on the African continent, the RPF’s goals to present itself as a regional and continental hub have also necessitated a focus on the industrial sector.

The truth is that the government is always trying to be all things to everyone. One moment, it will focus on services. The other on industry. Sometimes, it praises markets and in other times, it will be all about how state intervention is important.Footnote 8

In the last few years, there have been significant incentives provided to key investors with which the government has sought to develop partnerships with lead firms to ‘strategically couple’ in GVCs (Yeung Reference Yeung2016). Volkswagen’s car assembly plant was launched in Rwanda in 2018. Also, after the pandemic, the Rwandan government has been at the centre of diplomatic initiatives to increase manufacturing and facilitate access to vaccines, medicines and health technologies in Africa. With the European Union’s financial support, BioNTech has committed to begin testing mRNA production for process validation. In 2024, the African Union signed an agreement to establish the headquarters of the AMA in Kigali. These high-profile investments bolster Rwanda’s symbolic position as a hub for Pan-African economic progress. In particular, BioNTech’s investments after the Covid-19 pandemic, which highlighted the African deficit in pharmaceutical manufacturing, attracted positive publicity for Rwanda. However, significant industrial production is not visible. There are few signs that domestic firms are being nurtured to leverage technology transfer from BioNTech. The most significant industrial progress has been through firms that have captured the domestic market or are exporting to regional markets. The evolution of Rwanda’s industrial record will be discussed next.

Rwanda’s Industrial Record

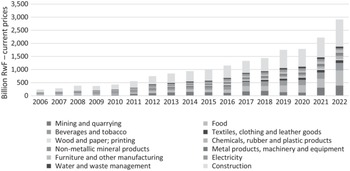

Figure 9.2 shows that in nearly every industrial sector, there has been some growth between 2006 and 2022 (although in official industrial sector statistics, mining and some agricultural sectors, including some agriculture products, are included within ‘industry’). However, this growth is not a reason to celebrate industrial progress, since it was growing from such a low base. Production and utilisation of construction materials has remained the most significant contributor to industrial GDP. This is also directly linked to Rwanda’s hub strategy, rather than being a product of a significant focus on manufacturing alone. The goal of transforming Kigali into a hub has provided the RPF with an opportunity to prioritise the manufacturing of cement and other building materials. At times, some construction materials were significant contributors to imports, which led to an increasing trade deficit. Some of the initial motivations to invest in construction materials were thus simply to reduce imports rather than build technological capabilities among local firms to make them internationally competitive. Figure 9.2 highlights growth in the food and beverages sectors. There has also been some growth in the textiles, clothing and leather goods sector, though these sectors remain a small contributor to GDP.

GDP within industry by activity: 2006–2022.

The RPF aims to use industrial policy while also embracing regional integration, with the goal of taking advantage of specialising in producing certain goods. To gain tariff-free access to foreign markets, the government has signed up to trade agreements through the Common Market for Eastern and Southern Africa (COMESA), EAC and the AfCFTA. Rwanda is also part of an additional tripartite agreement, including the EAC, COMESA and SADC. Rwanda also benefits from access to the European Union’s Everything but Arms treaty and bilateral treaties with large Asian markets (including China, India, Korea and Japan).

Government-commissioned historical industrial surveys have highlighted that domestic and foreign firms had established a significant industrial base by the 1970s (Gathani & Stoelinga Reference Gathani and Stoelinga2013). Most of these firms produced for domestic or regional markets. Many of these firms were Rwandan-owned or Asian-African-owned but were closely linked to previous governments. In the 1980s/1990s, the owners of some of these firms, especially those who were Tutsi, were targeted by the government. Many of these Tutsi industrialists (and even some Hutu ones like Silas Majyambere) funded the RPA’s military effort in the 1990s. However, many firm owners (including foreign owners) did not fund the RPA’s military effort and, as such, the RPF did not trust them when they assumed power in 1994. As a manager of an Asian-African industrial firm said:

It was natural for the government to not trust us. But no matter what we did to win their trust, we never got a fair deal from them.Footnote 9

Industrialists in Rwanda highlighted the ‘environment of distrust’ in the private sector.Footnote 10 During the 1980s, many industries that were focused on the domestic market relied on the government for procurement contracts. Even some owners, many of whom were Asian-African, admit that ‘it is understandable why they don’t want to support us. Our booming years were the 1980s. But then that was when industrial workers also did well in Rwanda’.Footnote 11

The environment of elite vulnerability in the manufacturing sector mirrors the evolution of the political settlement. Initially, closely allied private businesspeople like Rujugiro, Kajeguhakwa, Rwigara and others were entrusted with ownership of manufacturing companies and industrial facilities, some of which were privatised and sold to them in the late 1990s. As Golooba-Mutebi and Booth (Reference Golooba-Mutebi and Booth2018) argue, in some cases, Rwandans were encouraged to pool their wealth together to invest in strategic projects. However, as attempts were made to centralise control over political decision-making and the distribution of rents, the government reduced its reliance on private businesspeople. Other domestic businesspeople who invested in manufacturing included Valens Kajeguhakwa, Robert Bayigamba and Denis Karera. These three prominent capitalists have also either fled the country or been regularly arrested (and later released). Another example of the distrust in the domestic manufacturing sector is the plight of the Rwanda Association of Manufacturers (RAM) chairpersons. RAM is the organisation that represents manufacturing interests and is generally headed by the most prominent manufacturers. Rujugiro was a former chairperson. However, his successors as RAM chairpersons owned less prominent firms or had less diversified investments. There has been a rapid turnover in RAM’s chairpersons, with some of its former chairpersons now in exile abroad. Currently, RAM is headed by Felicien Mutalikanwa, who owns ProDev Foods, and is directly in partnership with the government in his investments (Chapter 6). One former RAM chairman highlighted the challenging environment for local manufacturers:

There is always a fear of arrest if you are a successful businessman in Rwanda. They keep watching. If you don’t fall in line or show too much independence, they will let you know who is boss.Footnote 12

When domestic capital has contributed to industrial growth, it has largely been driven by the government or government-affiliated firms. The following sections describe three examples of manufacturing investments in recent years: construction materials, apparels and pharmaceuticals.

The Trajectories of Industrial Policy Evolution in Rwanda

Both the EDPRS 2 and NST 1 have had clear job targets, with an increasing emphasis on industrial growth as an avenue for employment creation. A recent World Bank (2019) country diagnostic highlighted the potential of the manufacturing sector in creating more jobs, especially since services did not increase its share in total employment between 2011 and 2017. The highest share of jobs was created in agriculture between 2011 and 2019. The diagnostic exercise highlighted how agriculture and industry had outperformed services in terms of job creation between 2016 and 2019. Though industrial growth lagged behind services, the industrial sector was still creating more jobs prior to the pandemic. The employment potential of manufacturing sectors has contributed to shifting the government’s tone regarding industry.

Being landlocked, it’s very difficult to see how industrial growth can succeed. All Rwandans only see money in Kigali in real estate. Our biggest challenge, as MINICOM, is to convince them not to build a hotel but to instead take a chance and build a factory.Footnote 13

In Rwanda, industrial policy has evolved through a process of trial-and-error and has been impeded by difficult relations with business elites. Domestic elite vulnerability has obstructed possibilities for ambitious investments, as have competing priorities in service sectors and the occasional requirement of adhering to IFI concerns and presenting the economy as a leading reformer (to provide the right signals to financial markets).

Rather than relying on partnerships with domestic firms, the government has recently sought partnerships with lead firms in GVCs (such as Volkswagen). As part of a push to become a hub for electric vehicles (cars, tractors and motorbikes) and thereby present itself as an environmental leader on the continent, the Rwandan government provided significant incentives to Volkswagen to build an assembly plant for electric cars. Officially, government officials highlight that it was through President Kagame’s relationships that this deal was achieved.Footnote 14 However, others argue that this was in coordination with the German embassy, while some mention that it was driven by Volkswagen, which was looking to establish plants in Africa and found Rwanda to be a suitable destination because of the incentives on offer.Footnote 15 Martina Biene, the managing director of Volkswagen South Africa, said one of the reasons they chose Rwanda was that ‘they’ve removed import duties and VAT from electric vehicles because they want to encourage importers to bring in electric vehicles and that is why we are keen on partnering with them’ (Nyabor Reference Nyabor2023).

Incentives included being exempt from taxes and excise duties on electric cars, their spare parts, batteries and charging station equipment. However, the government did not require any parts to be sourced within Rwanda, highlighting how investing in domestic linkages was ignored. Volkswagen initially launched the e-Golf model in 2019 in Rwanda, importing cars with the intention of establishing a local ride-hailing service. Though the initial goal was to develop a service of fifty cars and fifteen charging stations, very few of the cars remain on the road, and charging infrastructure has not been developed (Djikstra Reference Djikstra2022). In 2022, only twenty of the cars were on the road, and very few charging stations were being used. The cars were primarily being used to ferry customers between high-end hotels, the airport and other tourist attractions (Djikstra Reference Djikstra2022). There were challenges in investing in charging stations outside Kigali, given the lack of demand, as well as what would have been inconsistent usage. Additionally, Volkswagen recognised that ‘the unevenness in road infrastructure and the height of speed-bumps turned out to be too challenging for the e-Golf, which has relatively low ground clearance’ (Djikstra Reference Djikstra2022).

The Volkswagen experience showed that the government had not clearly thought through whether continuing to provide incentives to support this experiment was feasible. Though Volkswagen remains in partnership with the government to establish electric tractors and import new electric cars, there is little evidence that the experiment has done anything other than further establish Rwanda’s green credentials.

Often, manufacturing remains a secondary priority compared to service-oriented or environmental priorities. MINICOM’s activities have received very little donor support or government budgetary support, and there have also been consistent personnel changes in the ministry. Through the examples of construction materials, apparels and pharmaceuticals, the remainder of this chapter describes how (1) the government has navigated domestic elite vulnerability to find partners for industrial policy; (2) used industrial policy amid goals of regional and continental integration, thereby attempting to industrialise while reducing trade barriers and (3) presented itself as adhering to Pan-African goals to contribute to its hub-based development strategy.

Construction Materials

Rwanda’s services-oriented development strategy has been centred on transforming Kigali into a regional and continental hub for finance, tourism, sports and air travel. Since the 2000s, the RPF’s party- and military-owned firms, as well as closely affiliated businesspeople, including Hatari Sekoko and Denis Karera, have led investments in malls, skyscrapers and residential housing (Goodfellow Reference Goodfellow2014). Karera was the co-owner of Kigali Heights, a showpiece mall in Kigali. He also owned several other high-profile residential properties in Kigali. He has been arrested several times over the last decade, after being investigated over questionable business deals and his close relationships with dissidents.Footnote 16 Sekoko was one of the lead investors in the Marriott Hotel, a flagship commercial property (Kigali City Tower) and several residential properties. Sekoko was involved in metals trading in the DRC. He was one of two Rwandans named in the Panama Papers. The Rwandan government denies that Sekoko and former Intelligence Chief Emmanuel Ndahiro, who were named as directors of the offshore company named in the Panama Papers, used the funds for private gain (The East African 2016). Sekoko primarily invests in real estate and is not a prominent investor in diversification (aside from some investments in CWSs in the 2000s). This highlights that some of Rwanda’s richest businesspeople choose to invest in real estate rather than in productive sectors. Karera remains in a difficult relationship with the government primarily because of his close relationship with former RPF elites who have now become dissidents.Footnote 17 The ruling coalition’s treatment of him shows their anxiety that he could use his wealth to finance the efforts of dissidents to mobilise popular grievances.

In the 2000s, there was a construction boom, which led to a rapid increase in construction material imports, including cement, ceramic tiles and granite (Behuria Reference Behuria2018a). In the 2010s, the government highlighted the construction materials sector as a priority sector to reduce the trade deficit, create jobs and capture the domestic market (with the eventual goal of competing within regional markets). Two companies – CIMERWA Cement Limited and East African Graphite Industries (EAGI) – have led government initiatives. Both have been funded by a combination of the RSSB, CVL, military-owned firms and foreign investors at different stages. In both cases, there has been significant progress (though both companies experienced obstacles along the way). CIMERWA’s success has acted as a demonstration effect to other investors in Rwanda’s cement sector. However, CIMERWA’s recent sale also highlights continued elite vulnerability, with the weakening of RIG. RIG investments depended on private investors pooling resources together, but many of the initial investors in RIG fell out with the government and are currently in exile. With the weakening of RIG, the government has struggled to find alternative investors.

Cement production in Rwanda began with the discovery of limestone, quartz and clay deposits in the 1970s. The government then established a joint venture with a Chinese company in 1976, and a cement plant, CIMERWA, was constructed with a loan from the Chinese government (Gathani & Stoelinga Reference Gathani and Stoelinga2013). In 1984, CBMC, a Chinese company, managed the plant. In 2001, the plant’s production capacity was doubled to 100,000 tons per year. When the Chinese government’s loan expired in 2006, the firm was privatised and sold to RIG. However, RIG did not invest much primarily because RPF senior leadership fell out with RIG’s leading investor, Tribert Rujugiro, and his assets were seized. In 2011, the RSSB and the government took majority control of CIMERWA, but RIG still retained some shares. In 2013, South Africa’s largest cement producer, PPC Ltd., bought 51 per cent of CIMERWA and invested in increasing the production capacity to 600,000 tons per year (Behuria Reference Behuria and Goodfellow2019). Under PPC’s ownership, CIMERWA began to take increasing control of the domestic market. At that time, Rwanda was heavily reliant on cement imports from the region, especially Ugandan companies. The government supported CIMERWA by providing guaranteed contracts for strategic projects like the construction of the Kigali Convention Centre and the Kigali Heights shopping complex. Rwanda had another smaller cement plant, Kigali Cement Company, which was owned by Kenya’s ARM Cement. ARM Cement was involved in legal wrangles until it was liquidated in 2021. A local government-affiliated firm (PRIME Cement) has also constructed a smaller cement plant. Chinese investor West China Cement, through its subsidiary, Anjia Prefabricated Construction, established a $100 million cement plant in Muhanga, with the goal of achieving an annual output of 1 million tonnes.

The government’s partnership with Anjia represents a significant shift in its decades-long attempt to capture the domestic cement market and compete with Ugandan cement exporters in the DRC market. The government’s choice to rely on foreign investors rather than use its own closely affiliated firms or work with private domestic investors highlights both elite vulnerability and the failure of Rwandan-owned companies to invest in the required technological capabilities. For most of the 2010s, despite public procurement deals being provided to CIMERWA, Rwandan domestic cement companies have rarely captured more than 50–60 per cent of the domestic market. Given that no duties were charged on imports from neighbouring countries, Rwandan companies were unable to compete with the lower prices charged by Ugandan firms (aside from when the Uganda–Rwanda border was closed because of political tensions). One of the main challenges has been that Rwandan firms need to import clinker from abroad, and this has raised the production costs of domestically produced cement. Anjia quickly began to produce the cheapest cement domestically because it received clinker from the DRC and managed to lower transportation costs through transporting it via Burundi (Gahigi Reference Gahigi2024). Anjia’s investments in a new plant means that if CIMERWA and Anjia were both to run near capacity, they would easily meet domestic cement demands and export to the region.

The difficulties experienced by South African investor PPC eventually contributed to them selling their majority ownership of CIMERWA to Kenya’s Devki Cement in 2023. The government – through RSSB and other institutional investors – retains 49 per cent of CIMERWA. While in the last decade, significant progress has been made in building cement factories, increasing domestic cement production and becoming more competitive with regional firms, the government has still struggled to dominate the domestic market, let alone compete with Ugandan or Tanzanian firms in the region. The government has eventually chosen to rely on foreign investors, showing how the failure to support domestic capitalists is impeding structural transformation. While foreign investors have established expertise and technological capabilities in cement production, the government will find it difficult to discipline investors in line with strategic goals (like increasing employment, value addition) and incentivise learning.

EAGI, on the other hand, is an example of an investment group that is still majority-owned by government-affiliated investment group, CVL. Unlike in the cement sector, EAGI retains full ownership of the domestic production of the dimensional stones it produces (primarily granite) – from quarry to factory. Centralising control over the value chain has enabled EAGI to reduce coordination problems. The firm has learned after failing, with policies becoming more responsive to the market. EAGI’s ownership has gone through several different formulations, with the military (through Horizon), RPF (through CVL) and the government (through RSSB) owning shares at different times. Currently, CVL and RSSB retain joint ownership of EAGI. In 2012, EAGI established a $15 million granite-processing factory with a production capacity of 200,000 square metres per year, making EAGI’s factory the largest in the region. Initially, EAGI had a partnership with Beijing Union Stones to train employees in mining skills and provide assistance with technology and expertise for project implementation. However, the imported machines from China did not meet their needs, and ‘the first four years were a learning curve’, with EAGI officials nearly ‘giving up on the project after two years’.Footnote 18 They were forced to look elsewhere to seek technological expertise. EAGI officials emphasised the importance of finding new opportunities to learn and experiment. Firm representatives visited Italy, Turkey and Germany in 2015 to find new partners and to invest in technology.

EAGI then made new investments and installed European machines, which were better suited to Rwanda-produced granite. In 2017, EAGI had begun producing 200–300 square metres of granite per day, and representatives said that with new investments, this could increase to 1,000 square metres of granite per day. EAGI also exports small volumes to Kenya, Tanzania, Uganda and Burundi. Yet the company faces challenges in finding investment to acquire the required technological capabilities and in accessing reliable electric supply. There are difficulties with blackouts and ‘voltage issues’ while also having to pay ‘high power costs’.Footnote 19 Though EAGI’s case highlights some positives associated with the centralised control that came with close affiliation to the government, EAGI officials also complained about inefficient government officials and conflicting priorities.

Both the cement and granite cases show signs of progress. However, the government has fallen short in building effective domestic state–business relationships that encourage learning and technology acquisition among local firms. In the cement sector, elite vulnerability obstructed possibilities to acquire technological capabilities and manage the impediments associated with being ‘landlocked’, including high transport costs. However, even where there is centralised control, the government’s limited attention to the needs of its own closely affiliated firms have meant that there have not been adequate investments to make EAGI a regional leader in construction materials.

Apparels (Textiles and Garments)

Rwanda’s apparels strategy has received global attention, sparking international press coverage when the sector became an arena for a trade conflict with the United States. Spearheaded by Rwandan efforts, in early 2016, East African leaders decided to roll out a ban on the import of second-hand clothing and shoes by 2019, once EAC countries had agreed on a common industrialisation policy. As a first step to an eventual ban, in June 2016, the Rwandan government increased import duties on used clothes from US $0.2/kg to US $2.5/kg. Duties were also raised on used shoes, from US $0.5/kg to US $5/kg (Behuria Reference Behuria and Goodfellow2019).

Second-hand clothes have been imported to Rwanda from Europe and Asia for more than a century (Haggblade Reference Haggblade1990). However, as the trade deficit widened in the mid-2010s, government officials were increasingly concerned by the estimated $100 million spent on importing second-hand clothes.Footnote 20 MINICOM estimated that banning second-hand clothes would not only help recapture the domestic market (with a 37 per cent decline in apparel imports) but also could increase apparel exports by $17 million (Behuria Reference Behuria and Goodfellow2019). In response, the US-based Secondary Materials and Recycled Textiles Association petitioned the United States Trade Representative, arguing that the ban would negatively affect 40,000 American jobs. Gradually, every EAC member except Rwanda backed down from banning the import of used clothing and leather products. In July 2018, US president Donald Trump took the decision to withdraw Rwanda’s right to export apparel duty free to the United States under the African Growth and Opportunity Act (AGOA). An immediate ban seemed to be poorly planned given that few domestic firms existed that could immediately compete with other imports (from China) or meet domestic demand. Crucially, there was also limited discussion of where new firms would source inputs (like fibre).

Rwanda continues to retain its ban on second-hand clothes despite the United States’ withdrawal of access to AGOA benefits. The RPF’s defiant position was in line with both the government’s own paradigmatic ideological goal of self-reliance and its attempt to position President Kagame as a leader, following anti-colonial and Pan-Africanist principles. Since then, the Rwandan government has lobbied to ensure African trade ministers adopt rules of origin in the apparels industry that prevent trading in second-hand clothes across the continent under the AfCFTA (Kagina Reference Kagina2023b). Though the Rwandan government has made some progress in increasing apparels exports (through accessing European markets and exporting to neighbouring countries), there is little evidence of wider redistributive benefits (with prices of clothes increasing). Aside from providing publicity to luxury Rwandan fashion brands, growth in apparels is inhibited by the inability to strategically direct and coordinate policies aimed at technological capability acquisition among local firms.

Until 1984, there were no large factories producing textiles or garments in Rwanda. In 1984, Kishor Jobanputra, whose family had lived in Rwanda for over a century, although they were of South Asian descent, was encouraged by President Habyarimana to establish an integrated textile company – L’Usine Textile du Rwanda (UTEXRWA). UTEXRWA’s production benefited from winning public procurements to supply the army and public institutions in Rwanda and in neighbouring DRC. UTEXRWA benefited from Habyarimana’s close relationship with Mobutu. The DRC contracts alone were worth $20 million in 1993 but ended when the RPF took power in 1994.Footnote 21

Jobanputra left Rwanda to move to Uganda shortly after the 1994 genocide and later purchased the struggling Ugandan parastatal, Nyanza Textile Industries Limited, in 1996. Like with other industrial firms, the RPF’s relationship with UTEXRWA management remained ‘difficult and uncertain for the last 20 years’.Footnote 22 UTEXRWA management admit that Jobanputra focused its investments in Uganda given the low domestic demand in Rwanda and the loss of trained workers during the genocide.Footnote 23 In the early 2000s, UTEXRWA began working with the government to diversify textile production. To provide UTEXRWA with a guaranteed income, the government provided them with a lucrative contract to supply uniforms to the military, police and some local industries. However, government officials claim that UTEXRWA did not deliver what they had promised, while UTEXRWA officials blame the government for obstructing their progress, highlighting the emergence of a military-owned firm producing silk as an example of unfair competition (Behuria Reference Behuria and Goodfellow2019). UTEXRWA also lost some of its uniform contracts towards the end of the 2000s, with the military choosing the cheaper option of importing uniforms from China.

The government failed to build an effective relationship prioritising learning and diversification with its local firm. Instead, it chose to focus on attracting Chinese investors when it began refocusing on industrial policy in the mid-2010s. In 2014, a Chinese firm, C&H Garments, which had already established firms in Ethiopia, Lesotho and Kenya, was the first company to be given EPZ status in Rwanda. As part of the EPZ status, the government provided tax and duty exemptions on imports, constructed the company’s factory and charged ‘almost zero rent’.Footnote 24 C&H committed to exporting 80 per cent of its garments, which were mostly uniforms, to China and the United States with the intention of diversifying to European markets. In addition, the government granted several public procurement contracts to C&H. In hindsight, partnering with C&H proved to be a poor bet for the government, with the firm developing a poor reputation within the region for leaving once incentives dried up.

C&H Management was clear that if AGOA trade privileges stopped, they would shut the factory, as production costs made it difficult to compete against firms in other neighbouring countries (Gambino Reference Gambino2017). In 2020, despite the government supporting them with additional procurement contracts, C&H shut its factory.

Instead, the government has chosen to focus most of its attention on attracting new investors, with established relationships in European markets, as Rwanda still benefits from preferential access to Europe through the Everything but Arms agreement. In 2019, Hong Kong–based firm Pink Mango C&D took over C&H’s factory in the Kigali SEZ in a joint venture with Rwandan entrepreneur Maryse Mbonyumutwa. C&D produces a range of garments, including jackets, casual wear, T-shirts and sportswear. As of 2022, Pink Mango employed over 4,300 workers and had begun exporting to Europe (MINICOM 2022b). Additionally, smaller textile producers like the Kigali Garments Centre (KGC) were established. The KGC is jointly owned by eighty-three Rwandan tailors and is part of a government initiative to organise the textiles and garments value chain.

The government claims that between 2018 and 2020, textile exports increased from $5.9 million to $34.6 million. Exports to the DRC represented most of this increase, with the KGC and the approximately thirty to forty smaller firms that now operate in Rwanda able to tap into the DRC market for fabrics. While exports to the United States had reduced significantly during this period, exports to Europe (through C&D) increased. Though C&D’s investments have been positive, there are two reasons to be concerned about the direction of the apparels sector strategy. First, the literature on SEZs tells us that industrial agglomeration is what matters (Farole Reference Farole2011; Whitfield & Staritz Reference Whitfield, Staritz, Oqubay and Lin2020) in contributing to making latecomer firms competitive in global markets, and relying on one firm will have its limits. Second, there are very few latecomer firms that are being supported to leverage technology acquisition from foreign firms such as C&D.

MINICOM has instead focused on portraying many of its textile designers and entrepreneurs as leaders in high fashion. MINICOM (2022b, p. 32) has expressed a desire to use the AfCFTA to ‘position itself at the high end of the value chain’ of African high fashion and export to East and West African countries. Plans have also included establishing a Rwandan Institute of Design and Clothing since 2016. This has not materialised yet, although such plans were mentioned again in the 2022 strategy documents (MINICOM 2022b). Mbonyumutwa’s luxury fashion brand, Asantii, which is produced out of Pink Mango C&D’s factory, has been featured in Vogue Africa and has been sold in retail stores in Kigali, Abidjan, Accra, New York, Brussels and London (Benissan Reference Benissan2022). Moses Turahirwa’s Moshions was also featured in Vogue and was worn by President Paul Kagame and members of the Kagame family at high-profile events in Rwanda and abroad. However, Turahirwa is in jail after being accused of forgery and possession of drugs. The government has also organised several fashion events. Kigali Fashion Week and the Rwanda Cultural Fashion show are events that showcase Rwandan-owned high-fashion brands. The Rwandan government also organised an advertising campaign, as part of the #VisitRwanda campaign, with Arsenal football players wearing Rwandan luxury fashion brands such as Haute Baso, House of Tayo, Inzuki Designs, K’tsobe, Moshions, Rwanda Clothing and Uzi Collections.

In hindsight, the ban on used clothing has yielded mixed results. Domestically produced garments have not been able to compete with the prices of imported garments. Though imports of used clothes may have stopped from North America and Europe, they have simply been replaced by imports from China.Footnote 25 Numerous small- and medium-sized firms have been established, which target exports to the DRC (and are focused on exporting low-value woven cotton fabrics, pile fabrics and quilted textiles). The government’s revitalisation of the apparels sector was focused primarily on encouraging more vertical integration, as well as exports to high-value markets. So far, little has changed in this regard. A Chinese company that was exporting to the United States has been replaced by another Chinese company that now exports primarily to Europe. At the same time, UTEXRWA continues to rely mostly on government procurement contracts as it did earlier. Though the government hoped UTEXRWA could produce high-quality affordable fabrics, the company’s production capacity has halved (MINICOM 2022b).

The textiles and apparels sector accounts for almost 15 per cent of manufacturing employment. Employment in the sector increased from 41,963 in 2017 to 57,527 (after peaking before the pandemic in 2019 at 71,212). Increases in employment are a positive outcome. In terms of support for firms, however, the most emphasis seems to be placed in positioning Rwanda as a high-fashion destination. However, this strategy is much more in alignment with Kigali being portrayed as a services hub rather than having a significant positive impact on manufacturing in terms of exports. Very limited employment is also provided by manufacturing these niche brands. Presenting Rwanda as a hub for high-end fashion also aligns more with the goals of positioning Rwandan elite youth at the forefront of African fashion. Such investments position President Kagame as a Pan-African leader, wearing African-made brands that are accompanied by slogans of Africans wearing African-made products rather than foreign fashion brands. However, there are hardly any signs that industrial policies have supported domestic firms in acquiring technological capabilities to export to foreign markets.

Pharmaceuticals: Symbolic Industrial Policy

Producing medicines so that populations can access them at an affordable price should be an important priority for any country. By the 1970s, the Non-Aligned Movement and some multilateral organisations like the United Nations Industrial Development Organisation (UNIDO 1978) were highlighting the urgent need for developing countries to establish their own domestic pharmaceutical industries (Balasubramanian Reference Balasubramanian1983). Lall (Reference Lall1975) was among those who highlighted how multinational companies represented a major obstacle to poorer countries gaining access to affordable pharmaceuticals. In the 1980s, World Bank publications dissuaded developing countries from investing in domestic pharmaceutical production, focusing on the limited feasibility of such industrial policies (Kaplan & Laing Reference Kaplan and Laing2005). The WTO’s Trade-Related Aspects of Intellectual Property Rights Agreements was finalised in 1994, with all WTO members required to sign up to standard minimum patent protection, with developing countries given a ten-year transition period and least developed countries a longer extension. Since many new drugs can be copied easily once invented, patents debates have been a central issue in the pharmaceuticals sector. Firms and organisations based in North America and Europe own most patents. This has led to a concentration of technological capabilities in North America and Europe with a concomitant concentration of pharmaceutical profits among firms based in those regions (Shadlen Reference Shadlen2007).

In 2005, a survey found that thirty-seven African countries had some manufacturing capabilities, but it was largely restricted to producing generic medicines (Berger et al. Reference Berger, Murugi, Buch, Ijsselmuiden, Kennedy, Moran, Guzman, Devlin and Kubata2009). Soon after, the AU (2007) took leadership in addressing the pharmaceutical manufacturing deficit on the continent, adopting a Pharmaceutical Manufacturing Plan for Africa. The African Medicines Regulatory Harmonization initiative was established in 2009, with the intention of harmonising the regulation of pharmaceuticals across the continent. Before the pandemic, in 2019, the AU adopted the Treaty for the Establishment of the AMA. More than a year into the pandemic, in November 2021, it was estimated that Africa imported 99 per cent of its vaccines, and only 10 per cent of Africans were fully or partially immunised against Covid-19 (Ekström et al. Reference Ekström, Tomson, Wanyenze, Bhutta, Kyobutungi, Binagwaho and Ottersen2021). During this time, Kagame lobbied for strengthening African pharmaceutical production. He also called for making Kigali a pharmaceutical hub for the continent. Despite having negligible domestic pharmaceutical production, Rwanda won the bid to host the AMA and the APTF. Winning these bids was accompanied by significant funding from multilateral organisations like the AU, AfDB, bilateral donors, including the European Union and philanthropic investors like the Bill and Melinda Gates Foundation. In doing so, a transnational array of actors, including philanthropists and multilateral organisations provided legitimacy and funding for the RPF’s development project.

Within Rwanda, the government has developed partnerships with firms that receive significant incentives and are part of the SEZ. Rwanda has attracted investments from a leading global pharmaceutical manufacturing firm, BioNTech, to be part of a Pan-African end-to-end manufacturing network for mRNA-based vaccines. BioNTech has committed to an investment of $150 million, as well as employment for 100 Rwandans. Attracting BioNTech provided legitimacy for Rwanda’s goal of becoming a hub and for solidifying its ideological commitment to self-reliance and Pan-Africanist goals. As part of the agreement, BioNTech will retain intellectual property, but Rwanda, as host country, will have control over distribution and export (Farmer Reference Farmer2023). BioNTech has stated that investment in Rwanda will be a ‘lighthouse project’ ahead of further investments in Senegal and South Africa. There are reasons to doubt whether the partnership with BioNTech will result in Rwanda becoming a pharmaceutical production leader on the continent, especially since there is very little existing expertise in pharmaceutical manufacturing and few skilled employees. David Himbara (Reference Himbara2023b), one of the RPF government’s most vociferous critics, has likened BioNTech’s investments to Volkswagen’s unmet promises. He, along with other dissidents abroad, regularly contests the ‘developmental’ significance of such projects in the foreign press, as well as in social media (to reach Rwandan audiences).

In 2020, Apex Biotech Limited, co-owned by Bangladeshi and Rwandan investors, established Rwanda’s first pharmaceutical manufacturing plant in the Kigali SEZ. Though Apex was the first factory to be licensed by the Rwanda Food and Drug Authority, it is yet to begin operations. Government-owned Akagera Medicines, which is majority owned by the RSSB, is incorporated in Delaware and has two laboratories in the United States. It has opened a subsidiary in Kigali to begin manufacturing and to undertake clinical trials. Michael Fairbanks, former advisor to the Rwandan president and chairman of Akagera Medicines Board of Directors, stated that Akagera Medicines already invested $16 million in the last four years and would soon produce affordable medication for tuberculosis, HIV and Lassa fever (Sabiiti Reference Sabiiti2023f). However, it is too early to say whether this government-owned company will fulfil its promises.

Rwanda’s pharmaceutical goals are the most ambitious of its manufacturing priorities. There is little evidence so far to show that Rwanda has the necessary infrastructure, expertise or technological capabilities to become a pharmaceutical production hub in the future. BioNTech’s investments have sparked widespread hope that Kigali could fill the pharmaceutical manufacturing void on the continent. Kigali was successful in gaining the confidence of an array of stakeholders. Yet challenges within the country’s political settlement (failure to develop effective domestic state–business relationships with private investors) and skills gaps are reasons to doubt that future goals will be met.

Conclusion

Government officials initially justified their limited attention to manufacturing sector growth on the grounds that Rwanda faced severe geographical and infrastructural challenges in comparison to neighbouring East African countries. Comparatively, Rwandan firms faced much higher transportation costs, and there were inadequate and inconsistent supplies of affordable energy. There were also other challenges. Most significantly, politically, the Rwandan government had a difficult relationship with older manufacturing firms, which were perceived to have close relationships to pre-1994 governments. Additionally, the choice to prioritise services and later to present the country as leaders of environmental policy (including banning of packaging materials) resulted in conflicting policy priorities, which made industrial development much more difficult.

Gradually, since the 2010s and especially since 2015, the government has reversed track in response to the urgent need to address high levels of unemployment and underemployment. There is growing emphasis on industrial policy, with reference to agro-processing and even manufacturing sectors. Industrial policy takes different forms. In line with GVC-inspired IFI advice, the government has attempted to entice global lead firms in various sectors ranging from automobiles to pharmaceuticals to textiles. For its most ambitious experiments, the government continues to lean on its own closely affiliated investment groups, with limited evidence of emerging private industrial capitalists.

The RPF’s industrial strategies have had symbolic success. They have not achieved significant advances in increasing industrial employment, production and exports. Partnerships with foreign lead firms in automobiles and pharmaceuticals have advanced the RPF’s goals of becoming a continental leader in environmental policy (in electric cars), as well as contributing to ideological goals of self-reliance and presenting Kagame as a Pan-African leader (through pharmaceutical investments). Even in the apparels sector, the government has prioritised positioning Rwanda at the helm of African fashion through supporting domestic brands in luxury fashion. Such investments contribute more to building Rwanda’s ‘national brand’ than reducing the trade deficit or increasing exports.

While the government now recognises that services may not be able to create the same number of jobs as manufacturing, there continues to be difficulty in steering domestic capital to invest in industrial sectors.

I think we’ve seen some progress in jobs. It’s good that the government is prioritising industry again but I do not see enough investors interested in industry – foreign or Rwandans. That’s a major problem.Footnote 26

In Rwanda, there are few signs of significant industrial growth. Structural transformation in the country has not advanced in a classic late-development trajectory. Post-war development economics (Hirschman Reference Hirschman1958; Lewis Reference Lewis1954) argued that structural transformation has classically taken the form of transforming economies from low to high productivity activities. More recently, prominent economists (McMillan et al. Reference Mcmillan, Rodrik and Verduzco-Gallo2014) have argued that contemporary economic transformation (in most African countries) has generally been from low-productivity agriculture to low-productivity services. The concluding chapter summarises how analysing Rwanda’s development trajectory can contribute to our understanding of how multi-scalar pressures are shaping the challenges of late development under contemporary globalisation.

Open access

Open access