I. Introduction

Money laundering is a key enabling process in profit-motivated crime. It is commonly understood as the conversion or transfer of property to conceal or disguise its illicit origin, or to assist a person involved in a predicate offence to evade the legal consequences of their actions. As such, money laundering provides criminal justice systems with an entry point for disrupting underlying crimes and pursuing illicit proceeds.Footnote 1 Although research has not produced a reliable estimate of the overall scale of criminal proceeds and money laundering,Footnote 2 it is widely accepted that money laundering threatens competitive markets, societal security, and consumer welfare worldwide.Footnote 3

Rather than policing predicate offences alone (such as fraud, bribery, and corruption), national authorities have increasingly sought to disrupt criminals’ ability to legitimise illicit proceeds.Footnote 4 This helps explain why anti-money laundering (AML) instruments have become integral to the wider approach to economic crime and corruption across the world. In particular, the EU’s AML framework places significant responsibility on “gatekeepers” – including banks, gambling firms and crypto-asset service providers – who are obliged under national and EU rules (be they criminal, regulatory or civil) to maintain effective compliance programmes. These programmes can both reduce facilitation opportunities and generate financial intelligence about suspected laundering. Requirements imposed on private-sector actors to implement due diligence, reporting and internal controls therefore sit at the core of AML governance and are also central to tracing corruption-related financial flows.Footnote 5

The EU’s renewed institutional push against money laundering unfolds alongside a sustained scepticism in the academic literature about whether contemporary AML regimes deliver demonstrable reductions in harm.Footnote 6 Critical assessments highlight a mismatch between the scale and intrusiveness of “follow-the-money” controls and the regime’s limited visibility of outcomes: success is typically inferred from observable outputs – new rules, reporting volumes, inspections, fines – that remain weak proxies for reduced laundering, disrupted criminal enterprise or recovered proceeds.Footnote 7 Scholars have therefore repeatedly called for more defensible evaluation strategies and better data infrastructures, warning that – without them – AML risks drifting toward an expensive compliance architecture whose effectiveness claims cannot be tested rigorously.Footnote 8

A parallel strand of scholarship frames AML not simply as a set of technical controls but as a complex multi-level governance regime.Footnote 9 Empirical work on implementation highlights how open-textured “risk-based” duties are operationalised unevenly across supervisors and firms, producing practical gaps between law-on-the-books and law-in-action that can undermine both legitimacy and deterrence.Footnote 10 This matters directly for EU anti-corruption agendas because proceeds-focused controls depend on many actors incurring concentrated costs to produce diffuse, cross-border benefits – conditions that mirror collective-action dynamics identified in the corruption literature.Footnote 11 This article intervenes in these debates by using a collective-action lens to separate meaning-setting from consequence-delivery in EU AML governance, and applying it to AMLA as a hybrid, decentralised design for raising both convergence and cross-border follow-through in corruption-relevant cases.

Against this backdrop, the core question is not only whether AML reduces harm, but also why such a heavily resourced regime so often under-delivers in practice. In this paper, these gaps are interpreted as collective-action problems in providing AML policing as a public good at Union level: many public and private actors are asked to bear concentrated costs, while the benefits of reduced laundering and preserved market integrity are diffuse and cross-border.Footnote 12 First, actors do not share a settled view of what the AML “public good” should consist of – what mix of reduced laundering, recovered assets and safeguarded market integrity counts as success – and relatively low inter-organisational trust among policing, supervisory and private-sector actors undermines cooperation.Footnote 13 Second, roles and accountability are often unclear, partners’ behaviour is hard to monitor, and consequences for weak compliance are uneven or slow across Member States, while coordination across domestic agencies, foreign counterparts and regulated businesses is inconsistent.Footnote 14 Drawing on collective-action and institutional economics approaches to regulation, these problems can be separated into (a) clarity problems – lack of shared, workable expectations about what compliance requires in practice (even where rules are formally clear) – and (b) credibility problems – weak, slow, or uneven consequences when AML obligations are not met.Footnote 15

This paper asks how far the EU’s Anti-Money Laundering Authority (AMLA) is designed to address these collective-action problems – particularly clarity and credibility across the internal market. A collective-action lens is useful because it separates two governance tasks that standard AML accounts often conflate. The first is a classification task: the institutionalised setting and stabilisation of categories, thresholds, templates and supervisory methods that determine how behaviour is sorted into “compliant,” “risky” or “suspicious.” The second is an enforcement task: the organisation of monitoring, escalation, sanctions and follow-through when those benchmarks are not met. In what follows, I use “classification” and “enforcement” as shorthand for these two governance tasks.

I argue that AMLA is best understood as a hybrid decentralised authority that pairs classification functions (a single rulebook, standards, methodologies and shared infrastructures) with selective enforcement (targeted direct supervision and escalation tools) to raise both clarity and credibility across the internal market. This framework also clarifies AMLA’s limits: it can improve convergence and cross-border follow-through even where criminal-law enforcement remains national.

Situating AMLA alongside EU decentralised authorities such as BERECFootnote 16 (the Body of European Regulators for Electronic Communications) and ENISA (European Union Agency for Cybersecurity) highlights that AMLA is part of a wider governance solution – one that relies on agencies to stabilise expectations, build shared infrastructures and manage cross-border interdependence. This creates an opportunity to study how such “classification” institutions operate when the policy domain is economic crime policing, where information is sensitive, incentives to free ride are strong and outcomes are hard to verify. While AMLA is the focal case, the paper’s claims about the role of classification institutions in economic crime policing have broader application beyond this specific authority and the EU and can inform authorities facing complex collective-action problems worldwide.

The remainder of this paper is structured as follows. Section II outlines the collective-action perspective as it applies to AML governance and frames key AML challenges in these terms. Section III analyses AMLA through this lens. Section IV concludes by considering what AMLA’s design suggests about the role of decentralised authorities in addressing collective-action problems, and by highlighting policy implications for economic crime governance.

II. Collective action and EU AML governance

1. Why AML is a collective-action problem

The collective-action perspective is about the provision of public goods.Footnote 17 While both terms – collective action and public goods – are used broadly in policy debates on economic crime and beyond, these terms have precise meanings in institutional economics.Footnote 18 In economic terms, public goods, such as clean water or effective law enforcement, are characterised by non-excludability and non-rivalry in consumption. All members of a relevant group can freely consume such goods without leaving less to others. At the same time those that invest in the provision of public goods cannot exclude others from consuming their benefits.Footnote 19 For example, a large terrorist organisation presents a global threat. If an enforcement agency decides to apply its powers to disrupt financing of such terrorist organisation, many relevant actors, including multiple states, their citizens, and market participants, will enjoy more security without spending any additional resources.Footnote 20

The problem is that relevant actors often have incentives to refrain from bearing the costs of the public goods provision (free riding). In effect, individually rational behaviour can lead to collectively undesirable outcomes, including under-provision of the public good.Footnote 21 From this perspective, failures to mitigate money laundering can be understood as failures to provide a public good: reducing laundering generates broad social and market benefits, but the costs of enforcement, supervision and compliance are concentrated and easy to shift to others.Footnote 22 These collective-action pressures do not concern states alone. They also apply to private actors, whose cooperation – both public–private and private–private – is integral to AML governance.

These collective-action tensions are reflected in the architecture of contemporary AML regulation. A key feature of the global AML system is the delegation of significant preventive and reporting responsibilities to corporations through national laws.Footnote 23 These arrangements have diffused internationally through standard-setting, most prominently the Financial Action Task Force (FATF) Recommendations, and require firms to put in place internal controls and to cooperate with authorities via reporting and information-sharing duties.Footnote 24 Despite the scale of investment that these systems induce, the evidence on whether – and how – AML compliance and enforcement reduce harm from laundering and predicate crimes remains limited.Footnote 25 In the EU, these collective-action pressures can be expressed as clarity and credibility problems in AML governance, defined in the next subsection.

Recent high-profile cases illustrate these collective-action challenges. In the Danske Bank Estonia scandal, approximately €200 billion in suspicious transactions passed through a single branch between 2007 and 2015. Under the pre-2024 EU framework, responsibility for AML supervision of the branch was contested between the Danish and Estonian authorities, with each treating it as primarily the other’s obligation. The costs of this failure were diffuse – spread across jurisdictions – while the burden of preventing it fell on individual supervisors with limited incentives to act.Footnote 26 Cases like the Danske Bank scandal are predictable consequences of a system in which concentrated supervisory costs and diffuse cross-border benefits create persistent incentives for under-delivery of effective AML control.

Operationally, the underlying regulatory architecture works through a three-part chain. First, it imposes preventive obligations on “obliged entities” (customer due diligence, ongoing monitoring and internal controls calibrated through a risk-based approach).Footnote 27 Second, it requires suspicious activity reporting and related information-sharing to financial intelligence units (FIUs) and – where appropriate – law enforcement.Footnote 28 Third, it relies on public supervision and enforcement to check whether firms’ controls and reporting meet legal and supervisory expectations, and to escalate failures through remediation and sanctions.

This architecture helps explain both why AML is expensive and why effectiveness is difficult to demonstrate. Preventive duties are deliberately open-textured (“adequate,” “effective,” “risk-based”), and much of the regime’s output is indirect (alerts, intelligence, deterrence) rather than easily observable crime reduction. As a result, large investments can coexist with uncertainty about impact, and performance often depends less on the existence of rules than on whether actors converge on workable interpretations and then follow through consistently – precisely the terrain of clarity and credibility problems analysed below.Footnote 29

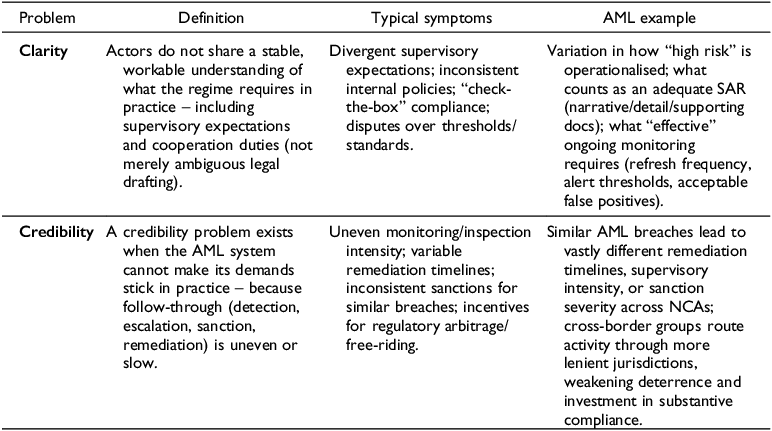

2. Clarity and credibility problems in AML governance

The collective-action perspective is useful for AML because the regime depends on many actors (obliged entities, supervisors, FIUs, law enforcement) and many cross-border interactions – precisely the conditions under which governance challenges accumulate.Footnote 30 In this paper, those challenges are organised around two core problems: clarity and credibility.

Clarity problems arise when actors lack a shared, settled understanding of what they have agreed (or are legally required) to do, how responsibilities are allocated, and where the line between acceptable and unacceptable conduct sits.Footnote 31 They can stem from ambiguity in legal rules and their interpretation, but in AML they often arise even where rules are formally clear because many obligations are deliberately open-textured – for example, requirements to maintain “adequate” controls, apply a “risk-based” approach, or ensure “effective” monitoring and reporting. These standards are recognised in law and regulation but depend on operationalisation through supervisory methodologies, thresholds, evidentiary expectations, and routine practices. Where that operationalisation is incomplete or varies, actors face uncertainty and practices diverge, including over whether a firm’s reporting is “effective” (timely, sufficiently detailed, and usable) or merely formal compliance.

Credibility problems arise when actors broadly know what is required but do not expect meaningful consequences if they fall short.Footnote 32 In AML terms, the regime’s demands fail to “stick” when the likelihood, timing, or severity of supervisory and enforcement responses is low or unpredictable. These problems can reflect gaps in legal powers or sanctioning tools, but in AML they often persist even where rules are formally clear and sanctions exist, because enforcement depends on monitoring capacity, supervisory discretion, institutional priorities and political-economy constraints. Where these constraints bite, detection and escalation become patchy, remedial measures are delayed or negotiated down, and similar breaches attract different supervisory intensity or sanctions across jurisdictions.

3. Governance responses: classification and enforcement institutions

The diagnosis in the previous subsection implies a governance question: what institutional arrangements can improve clarity and credibility in AML governance? For the purposes of this paper, the answer is organised around two institutional logics: classification and enforcement. Classification institutions reduce clarity problems by stabilising meanings and expectations – through the rulebook, technical standards, methodologies, templates and guidance that translate open-textured duties into workable benchmarks.Footnote 33 Enforcement institutions address credibility problems by structuring credible follow-through when deviation occurs – through monitoring, escalation, remedial orders and sanctions, supported by system-level backstops such as peer review, infringement action and judicial review.Footnote 34

In EU AML governance, classification functions are performed by EU and national rule-makers and standard-setters – through legislation, delegated and implementing measures, technical standards, supervisory methodologies and guidance that stabilise “rules-in-use.” Enforcement functions are exercised primarily by national competent authorities – through supervisory investigations, corrective plans, administrative penalties, prosecution and courts – with EU-level backstops where relevant (infringement procedures and judicial review). The question taken up in Section III below is how AMLA is positioned within (and potentially reshapes) this division of labour. Concretely, clarity disputes arise around risk-based compliance and reporting (for example, what “high risk,” “adequate controls” and an “actionable” SAR require), while credibility gaps appear in uneven monitoring, remediation and sanctioning, and in inconsistent cross-border follow-through from SARs to investigations.

In the EU context, these two institutional logics – classification and enforcement – operate within a largely decentralised enforcement landscape, which makes coordination and convergence especially consequential.Footnote 35 In such a system, many practical weaknesses stem not from the content of individual rules or sanctions, but from how classification and enforcement are connected across authorities and borders. Clarity disputes tend to persist where interpretations of risk and controls are developed and applied in isolation, while credibility gaps emerge where follow-up from SARs to investigations and sanctions depends on long and uncertain chains of competent authorities. Mechanisms such as supervisory colleges, shared platforms, common data schemas and case-handoff routines are therefore best understood as basic infrastructure for these institutional logics: they help diffuse common understandings of what compliance requires and support the reliable transfer and escalation of cases across jurisdictions.Footnote 36

Against this governance backdrop, it is notable that AML has historically involved limited centralisation beyond international standard-setting and cooperation bodies, even though cross-border spillovers are pervasive. Supervision and enforcement remain largely national, and uneven follow-through can persist even where standards are shared. The creation of AMLA therefore represents a significant EU institutional innovation: it introduces an EU-level authority intended to strengthen convergence in “rules-in-use” and to improve cross-border supervisory and enforcement outcomes in a system that remains predominantly decentralised. The EU’s wider experience with decentralised agencies – from classification- and coordination-heavy models (e.g., BEREC and ENISA) to bodies with harder supervisory powers (for example, ESMA) – helps to locate AMLA on a spectrum of governance designs.Footnote 37 Section III examines AMLA’s mandate through the classification/enforcement lens developed above.

III. The case of AMLA

Money laundering is not only a criminal-law issue;Footnote 38 from the EU’s perspective it poses a structural threat to the proper functioning of the internal market, creating cross-border blind spots, uneven compliance costs and opportunities for regulatory arbitrage.Footnote 39 In response, the EU Commission moved from incremental, minimum-harmonisation measures to a Union-level architecture that combines harmonised rules with stronger EU-level coordination and – selectively – EU-level supervision.Footnote 40

The 2024 AML package delivers this shift by:

-

creating a single, directly applicable AML rulebook for preventative responsibilities of obliged entities (Regulation (EU) 2024/1624);Footnote 41

-

requiring Member States to build and resource the national “AML machinery” (FIUs, supervisors, powers, cooperation duties, data access) that implements and enforces that AML rulebook (Directive (EU) 2024/1640);Footnote 42

-

establishing AMLA as an EU authority under Article 114 TFEU to drive supervisory convergence, coordinate/support FIUs, and directly supervise a limited set of selected cross-border entities (Regulation (EU) 2024/1620);Footnote 43 and

-

extending the “travel rule” to transfers of funds and certain crypto assets (Regulation (EU) 2023/1113).Footnote 44

Together, these measures recast AML as a market-integrity project. The 2024 package reshapes EU AML governance by combining a directly applicable single rulebook with a new supranational authority that operates both as a standard-setter and, selectively, as a supervisor.

AMLA is the EU’s decentralised authority for AML and counter-terrorist financing (CFT), created by Regulation (EU) 2024/1620 to lift supervisory quality and consistency across the single market and strengthen FIU cooperation. Institutionally, AMLA sits between coordination-heavy agencies (e.g., BEREC/ENISA) and a fully centralised supervisor such as the European Central Bank’s Single Supervisory Mechanism (SSM): it combines convergence-setting (methods, templates, guidance and supervisory approaches that stabilise “rules-in-use”) with risk-based direct supervision of a limited set of selected cross-border obliged entities. That perimeter is designed to be rule-based and dynamic (periodic selection) and includes escalation capacity where national follow-through is inadequate, while day-to-day supervision of the wider market remains primarily national. AMLA became operational on 1 July 2025 and is phasing in capabilities ahead of direct supervision in 2028, including governance set-up, staffing and IT platforms (e.g., EuReCA and the Article 11 central AML/CFT database).Footnote 45

On this basis, the EU shifts from minimum-harmonisation directives to a directly applicable, highly harmonised regime for private-sector preventive duties: the firm-level obligations once scattered across AMLD4/5 are consolidated in Regulation 2024/1624 to reduce national divergence, while AMLD6 focuses on the institutional and cooperation mechanisms through which Member States supervise, enforce and exchange information.Footnote 46

1. AMLA and collective-action problems

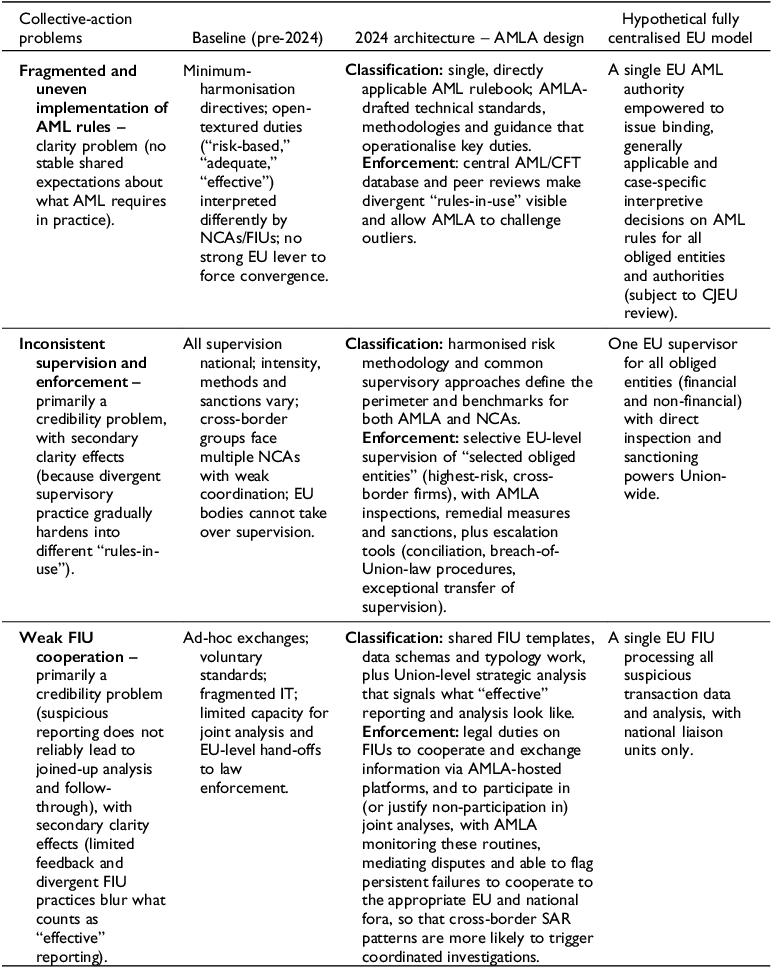

Against this backdrop the Commission’s impact assessmentFootnote 47 frames the case for AMLA around three problems: fragmented and uneven implementation of AML rules, inconsistent supervision across the internal market, and weak cooperation among financial intelligence units (FIUs).Footnote 48 Read through the lens of Table 1, these map onto clarity problems (divergent “rules-in-use” for preventive obligations) and credibility problems (variable supervisory follow-through and sanctions). Table 2 summarises how the 2024 AML package, and AMLA in particular, adjust the governance architecture in response, and contrasts this design with a hypothetical fully centralised model.

Clarity and credibility problems.

AMLA and collective-action problems.

The first problem, regulatory fragmentation, is primarily a clarity deficit. Under the pre-AMLA baseline, minimum-harmonisation directives allowed national add-ons and divergent interpretations of open-textured duties to accumulate.Footnote 49 The AML package shifts to a single, directly applicable rulebook and equips AMLA with standard-setting and convergence tools (technical standards, methodologies, templates and guidance).Footnote 50 These are classification moves that target the clarity deficit. AMLA’s conciliation and mediation functions, and its power to adopt binding decisions between financial supervisors after failed conciliation, operate as enforcement backstops that help ensure common interpretations are followed in practice.Footnote 51

The second problem, inconsistent supervision, is primarily a credibility deficit with a secondary clarity component. The core problem is uneven supervisory enforcement: similar risks do not attract similar remedial action or sanction severity across the EU, and supervisory methods and taxonomies diverge. AMLA addresses both sides by setting common methodologies and risk/sanction matrices (classification) and by exercising selective direct supervision over a defined set of cross-border or high-risk groups,Footnote 52 alongside system-wide oversight of national supervisors and escalation tools, including binding decisions where needed (enforcement).Footnote 53

The third problem, weak FIU cooperation, is likewise a credibility deficit with a clarity component. Ad-hoc exchanges, fragmented IT and variable templates reduce the probability that suspicious activity reports are converted into timely, actionable leads. The AML package responds by hardwiring cooperation through FIU.net as the protected channel for FIU cooperation – managed and hosted by AMLA – and by requiring FIUs to use FIU.net for exchanges and joint analyses. It also mandates standardisation, for instance via technical standards on the format for FIU-to-FIU exchanges and on criteria for forwarding cross-border reports, alongside AMLA providing operational support for joint analyses and benchmarking FIU capabilities.Footnote 54 These mechanisms support clarity (more consistent expectations about “effective” reporting and analysis) and credibility (more reliable follow-through in cross-border cases).

Taken together, these three problems show AMLA as a hybrid response to collective-action problems: it does not centralise all supervision or intelligence work, but it does harden the Union’s capacity to stabilise “rules-in-use” and to escalate where national follow-through is weak. These features frame the discussion of AMLA’s limits and implications in Section IV.

IV. Discussion and conclusion

AMLA should be understood as a hybrid, decentralised authority that pairs classification with enforcement to address the EU AML regime’s core collective-action problems. Through the single rulebook, technical standards and supervisory methodologies it helps stabilise meanings and thresholds (clarity), while selective direct supervision, escalation tools and convergence reviews are meant to improve the likelihood, speed and comparability of consequences (credibility). Coordination infrastructures – joint supervisory teams, colleges, shared data schemas and platforms/databases – help address both clarity and credibility problems, especially in complex cross-border and multi-agency cases.

1. What AMLA can deliver (and what it cannot)

On the EU agency spectrum, AMLA sits between coordination-heavy bodies such as BEREC and ENISA and a fully centralised supervisor like the ECB’s Single Supervisory Mechanism (SSM): it standardises methodologies and data, arbitrates meanings in hard cases, and directly supervises a defined set of cross-border/high-risk groups while overseeing NCAs and supporting FIU cooperation.Footnote 55 The goal is to reduce differences in interpretation and ensure more consistent action across the internal market. However, key risks include concerns about national sovereignty, unequal resources, and the practical challenges of coordinating joint supervision and shared FIU platforms – issues already raised in early discussions.Footnote 56

If the model functions as designed, we should observe tighter convergence in supervisory practice for comparable risks (e.g., more consistent remediation timelines and fewer “outlier” national approaches). For selected cross-border entities, joint supervisory teams and rule-based selection/transfer mechanisms should reduce the coordination failures that may plague multi-NCA supervision.Footnote 57 On the FIU side, the package strengthens EU-level coordination infrastructure.Footnote 58 These are the kinds of clarity and credibility gains the new architecture is intended to enable.

At the same time, the institutional design preserves a nationally led system, and this shapes how far AMLA can act on its own. Direct supervision is confined mainly to large, cross-border financial institutions and certain crypto-asset providers; most obliged entities – especially non-financial gatekeepers – remain under exclusively national supervision, with AMLA influencing them only indirectly through convergence tools and reviews.Footnote 59 FIUs likewise remain national bodies: AMLA can host platforms, coordinate joint analyses and mediate disputes, but it cannot compel an FIU to prioritise a case or to re-allocate domestic resources. The model therefore relies heavily on Member State buy-in, secondments and cultural alignment to turn formal cooperation duties into effective practice.Footnote 60

AMLA is therefore best read as “conductive tissue”: it does not replace national enforcement and intelligence functions, but it can reduce clarity problems by stabilising rules-in-use, mitigate credibility problems by adding selective supervision and escalation where national follow-through is weak, and orchestrate cross-border cooperation among FIUs and NCAs through joint work and shared infrastructures.

2. Public good and effectiveness

Seen through the collective-action lens, the EU AML regime is primarily about the provision of a particular public good: identifying and mitigating money-laundering risks in order, in principle, to prevent such activity from undermining the integrity and stability of the Union’s financial system and the proper functioning of the internal market.Footnote 61 That lens is useful because it makes explicit that this good depends on many actors bearing costs they could rationally try to shift to others, and that clarity and credibility problems shape those incentives. In that sense, the 2024 package and AMLA can be read as an attempt to increase the supply of this public good by stabilising expectations (classification) and by reducing the incentives to under-deliver (selective enforcement and escalation). At the same time, a public-good framing is normatively thin.Footnote 62 It does not, by itself, tell us which laundering risks ought to be prioritised, how to balance AML against privacy or due process, or what mix of administrative and criminal-law responses we should want. Here, the collective-action framework is used in a limited way: to diagnose where the regime is likely to under-provide AML as a public good and how AMLA might change that, not to resolve the deeper distributive and rights-based questions that the wider literature raises.Footnote 63

In this context, effectiveness becomes both more concrete and more demanding. The general empirical debate on whether AML “works” is hampered by the fact that outputs (rules, SARs, inspections, fines) are easy to count, whereas outcomes (disrupted networks, recovered assets, deterred corruption) are diffuse and hard to attribute. The collective-action perspective suggests a more targeted way of asking what effectiveness would look like for AMLA. If AMLA improves the regime, we should see fewer clarity problems (more consistent interpretations of key obligations and FIU expectations) and fewer credibility problems (more timely and comparable remedial action and follow-through), especially in cross-border cases. Indicators should therefore be proximate to these mechanisms: dispersion in supervisory practices for like cases, the quality and timeliness of FIU hand-offs, and the extent to which cross-border schemes trigger coordinated responses, rather than simple counts of guidance, SARs or fines. This does not answer the broader cost–benefit question for AML, but it does sharpen what it would mean for a classification-and-selective-enforcement regime like AMLA to be considered effective.Footnote 64

3. Risk-based AML, legal endogeneity and anti-corruption

The AML system is a paradigmatic form of risk-based governance: it delegates major detection and prevention functions to private “gatekeepers” who must design internal controls, classify customers and transactions, and decide when to report. Over time, socio-legal work on legal endogeneity suggests that such regimes tend to be shaped from within: standards are progressively interpreted and operationalised through compliance programmes, audit practices, supervisory expectations and industry guidance, often drifting towards what is documentable and defensible rather than what most effectively disrupts harmful conduct.Footnote 65 In anti-economic crime areas, including AML, this dynamic is reinforced by the role of professional service firms, RegTech vendors and public–private partnerships in defining risk indicators, transaction-monitoring logic and typology catalogues.Footnote 66 The danger is that the classification side of the regime becomes locked into a managerial vocabulary of “risk appetite,” “mitigation measures” and “control effectiveness” that can travel in internal and external audits, even where its connection to actual laundering disruption is weak.

Whether AMLA’s classification tools discipline or entrench this dynamic will depend on observable institutional choices. If AMLA’s technical standards and peer reviews evaluate supervisory quality primarily through process indicators – numbers of on-site inspections, timeliness of remediation plans, volume and categorisation of SARs – they risk replicating the same output-focused logic this paper identifies as problematic. Conversely, if AMLA develops outcome-sensitive benchmarks – for example, tracking the proportion of cross-border SARs that progress to joint analyses, asset freezes, or prosecutorial referrals – it could begin to push classification toward substantive disruption rather than procedural adequacy.

For anti-corruption, this has two implications. First, the main interface between AML and corruption control is still heavily proceeds-focused: tracing, freezing and confiscating corruption-linked flows through financial intermediaries and cross-border cooperation. AMLA and the single rulebook may strengthen this channel by improving clarity about politically exposed person (PEP) treatment, beneficial ownership, and corruption-related typologies, and by increasing the credibility that cross-border corruption flows detected in one Member State will be pursued elsewhere. This proceeds-centred channel mirrors the emphasis of recent EU anti-corruption reforms on criminalisation and asset recovery.Footnote 67

Secondly, however, a risk-based, compliance-driven AML system can substitute for, or symbolically stand in for, more direct anti-corruption measures.Footnote 68 If “doing AML” becomes a matter of demonstrating sophisticated risk models, extensive training and high volumes of SARs, it can absorb resources and political attention without necessarily increasing the probability that high-level corruption schemes are investigated, prosecuted and stripped of assets. This concern echoes broader assessments of the EU’s expanding anti-corruption toolbox, which stress that new monitoring and legislative instruments will only reduce corruption if they translate into greater investigative capacity and a real track record of high-level cases.Footnote 69 In that sense, AML expansion can be both a support to and a partial trade-off against core anti-corruption enforcement.Footnote 70

AMLA’s role sits at the centre of this tension. On the one hand, by tightening clarity and credibility – through common typologies, templates, supervisory methods and selective enforcement – it could discipline some of the more symbolic aspects of risk-based AML, pressuring firms and authorities to align their practices more closely with corruption-related outcomes (for example, the conversion of corruption-linked SARs into cross-border investigations, asset freezes and confiscation). On the other hand, AMLA might also entrench existing professionalised understandings of “good” AML if its own methodologies, benchmarks and peer reviews lean heavily on the language and metrics of the compliance industry. For anti-corruption, the key question is therefore not only whether AMLA improves formal convergence, but whether its classification and enforcement tools actually raise the probability that corruption-linked financial flows are detected, jointly pursued across jurisdictions, and translated into tangible sanctions and asset recovery, rather than into more sophisticated forms of symbolic compliance.

Competing interests

The author has no competing interests to declare.

AI tools statement

The author used OpenAI’s ChatGPT (GPT-5.1 and 5.2 Thinking, via the ChatGPT interface, January 2026) and Claude Opus 4.6 (February 2026) to assist with language editing and improving the clarity and structure of the manuscript. The author checked and edited all AI-assisted text and is solely responsible for the content.

Open access

Open access