1. Introduction and motivation

A robust disaster risk management plan is crucial for the survival and resilience of any nation. A single catastrophic event has the potential to erase decades, if not centuries, of economic progress and threaten livelihoods. According to MunichRe (2021), global losses from natural catastrophes in 2020 amounted to USD 210 billion, marking a significant increase compared to 2019. In the United States, more than 85% of all natural disasters incur costs exceeding a billion dollars, and the cumulative cost of weather and climate disasters since 1980 has surpassed

$\$$

1.875 trillion (Smith, Reference Smith2021). Furthermore, the ongoing trend of rising temperatures and precipitation driven by climate change is expected to have severe consequences, including the loss of biodiversity, environmental degradation, and increased security and health risks (Linnerooth-Bayer & Hochrainer-Stigler, Reference Linnerooth-Bayer and Hochrainer-Stigler2015; ADB, 2017; Jongman et al., Reference Jongman, Hochrainer-Stigler, Feyen, Aerts, Mechler, Botzen, Bouwer, Pflug, Rojas and Ward2014).

$\$$

1.875 trillion (Smith, Reference Smith2021). Furthermore, the ongoing trend of rising temperatures and precipitation driven by climate change is expected to have severe consequences, including the loss of biodiversity, environmental degradation, and increased security and health risks (Linnerooth-Bayer & Hochrainer-Stigler, Reference Linnerooth-Bayer and Hochrainer-Stigler2015; ADB, 2017; Jongman et al., Reference Jongman, Hochrainer-Stigler, Feyen, Aerts, Mechler, Botzen, Bouwer, Pflug, Rojas and Ward2014).

Disaster Risk Financing (DRF) aims to mitigate the fiscal impacts and economic losses caused by natural hazards, enhancing a country’s financial resilience to such events (WorldBank, 2015). Insufficient protection against disaster risks can result in inadequate funding for rebuilding infrastructure and hinder disaster relief efforts. Conversely, excessive protection may lead to inefficient use of public funds and substantial opportunity costs, limiting a nation’s potential for growth and development. As a result, an increasing number of countries are adopting more proactive and cost-effective approaches to disaster planning to address the extensive human, economic, and fiscal consequences of natural disasters (Mahul et al., Reference Mahul, Signer and Krishna2018). A robust DRF strategy provides governments with rapid access to financial resources during crises, promotes proactive risk management, complements the private insurance sector in transferring catastrophic losses, minimizes humanitarian impacts, and reduces the economic costs of reconstruction (Mahul et al., Reference Mahul, Signer and Krishna2018). However, selecting the appropriate combination and scale of DRF instruments remains a significant challenge. The Global Risk Financing Facility highlights the limited availability of theoretical and empirical studies to guide the effective utilization of risk financing mechanisms (Spencer, Reference Spencer2021).

This paper examines how governments can effectively manage residual financial risksFootnote 1 by employing a combination of DRF instruments, including reserve funds, insurance, contingent credit (CC), and ex-post financing, within the expected utility maximization framework. We incorporate a broad spectrum of real-world considerations commonly used in DRF to derive insights that may not have been previously analyzed or proven. Specifically, we investigate the effects of various factors on the design of a Disaster Fund, including: (i) premium principles, (ii) insurance structures, (iii) risk tolerances and risk horizons, and (iv) the influence of higher-order moments of the loss distribution. The proposed Disaster Fund model is highly adaptable, straightforward to interpret, and accommodates the distinct circumstances of countries with varying degrees of risk aversion, economic and budgetary limitations, and disaster risk profiles.

Our analysis reveals that imposing a Value-at-Risk (VaR) constraint and a Tail VaR (TVaR) constraint yields equivalent outcomes when the quantiles of the VaR and TVaR measures exceed the government’s risk horizon. Under the expected loss premium principle, the Contingent Credit-Insurance (CC-I) layer structure emerges as optimal; however, this may not hold under the standard deviation premium principle. We perform comparative statics to analyze how the optimal mix of DRF instruments adjusts to changes in key inputs, including insurance loadings, interest rates on loans and CC, and risk aversion. Notably, the imposition of a VaR constraint can either increase or decrease the level of insurance coverage, depending on the quantile of the loss distribution relative to the unconstrained optimal parameters. To illustrate the practicality of the Disaster Fund model, we calibrate it using actual flood data from the National Flood Insurance Program (NFIP) in the United States. We explore the optimal mix of DRF instruments and provide visual representations of the parameter space for constructing optimal disaster financing structure under various model specifications.

Given the ambiguity and uncertainty surrounding a government’s true underlying utility function, we avoid deriving closed-form solutions under specific utility functions. While closed-form solutions can often appear elegant and intuitive, they typically require overly restrictive assumptions that omit critical characteristics of real-world scenarios. Instead, the primary contribution of this paper lies in uncovering valuable and previously underexplored insights that are both essential and practical for governments designing DRF funds within an expected utility maximization framework.

1.1 DRF literature review

A review of existing DRF literature reveals an abundance of qualitative studies on DRF adoption but a relative scarcity of quantitative methods and practical guidance for governments on optimally constructing a DRF fund to manage disaster risk (e.g., Kunreuther, Reference Kunreuther1974; Settle, Reference Settle1985; Lewis & Murdock, Reference Lewis and Murdock1996; Harrington, Reference Harrington1997; Weingartner et al., Reference Weingartner, Simonet and Caravani2017; Noy & Edmonds, Reference Noy and Edmonds2019; Oseno & Obiri, Reference Oseno and Obiri2020; Surminski et al., Reference Surminski, Panda and Lambert2019; Ahmed, Reference Ahmed2021). While many studies emphasize the principle of prioritizing risk retention before transferring risk, they often stop short of determining the optimal threshold for retention (Punkdrik, Reference Punkdrik2010; Kashiwagi, Reference Kashiwagi2011; Zelinschi et al., Reference Zelinschi, Domide and Vîrban2013; WorldBank, 2018). These studies frequently rely on arbitrary benchmarks, such as a 1-in-200-year or 1-in-500-year return period, without providing clear justification or assessing the effectiveness and optimality of employing multiple DRF instruments (Vasche & Williams, Reference Vasche and Williams1987; Cornia & Nelson, Reference Cornia and Nelson2003; Barnichon, Reference Barnichon2008; Truong, Reference Truong2021). Moreover, limited research explores the integration of multiple DRF instruments by analyzing diverse insurance structures, real-world constraints, and varied loss profiles to derive optimal strategies for DRF.

The body of quantitative research on the construction of DRF strategies remains limited. In Clarke & Mahul (Reference Clarke and Mahul2011), the authors analyze a range of DRF instruments – savings, loans, CC, and insurance – within a two-period model that maximizes the expected utility of consumption under the expected loss premium principle. They conclude that a layered financing structure is optimal and emphasize the importance of CC. However, their study does not explicitly quantify the optimal allocation of each DRF instrument. Clarke et al. Reference Clarke, Mahul, Poulter and Teh(2017) propose a cost-minimizing strategy for combining disaster risk financial instruments, assuming a risk-neutral government. This framework results in a naturally layered strategy, where DRF instruments are utilized sequentially in order of increasing cost, subject to availability. However, governments are often risk-averse to significant losses, rendering a purely cost-benefit analysis inadequate (Stewart et al., Reference Stewart, Ellingwood and Mueller2011). In contrast to these studies, we advance the literature by determining the optimal allocation of multiple DRF instruments. Our approach incorporates additional practical considerations, including risk aversion, alternative insurance structures, premium principles, VaR and TVaR constraints, risk tolerance, and risk horizon. This comprehensive framework provides a more realistic DRF strategy for addressing the complexities of managing catastrophic risk.

Our paper also connects to the optimal (re)insurance literature. Arrow (Reference Arrow1974) established that the optimal insurance contract under the expected loss premium principle is the excess-of-loss contract, where insurance payouts are triggered only for losses exceeding a specified deductible. The landmark paper by Arrow (Reference Arrow1974) has spurred many extensions such as (1) different risk objective functions and constraints (Huberman et al., Reference Huberman, Mayers and Smith1983; Browne, Reference Browne1995; Huang, Reference Huang2006; Cai and Tan, Reference Cai and Tan2007; Cai et al., Reference Cai, Tan, Weng and Zhang2008; Balbás et al., Reference Balbás, Balbás and Heras2009; Liang & Guo, Reference Liang and Guo2010; Chi & Tan, Reference Chi and Tan2011), (2) different premium principles (Young, Reference Young1999; Chi & Tan, Reference Chi and Tan2013; Liang & Yuen, Reference Liang and Yuen2016a; Chi & Zhou, Reference Chi and Zhou2017; Liang et al., Reference Liang, Wang and Young2022), and (3) different reinsurance structures (Huberman et al., Reference Huberman, Mayers and Smith1983; Zhang et al., Reference Zhang, Zhou and Guo2007; Kaluszka & Okolewski, Reference Kaluszka and Okolewski2008; Liang & Guo, Reference Liang and Guo2011; Ghossoub, Reference Ghossoub2019). Kaluszka & Okolewski (Reference Kaluszka and Okolewski2008) further demonstrated that the excess-of-loss contract remains optimal even when there is an upper bound on insured losses. Our Disaster Fund model can be viewed as a specialized form of the optimal reinsurance problem, where we consider a (1) stepwise increasing cost associated with the use of reserves, (2) proportional and layering insurance structures, (3) expected loss and standard deviation premium principles, (4) VaR and TVaR constraints on terminal fund value, and (5) variable attachment and exhaustion points for both insurance and CC.

We organize the rest of this article as follows. Section 2 introduces the various DRF instruments and key real-world considerations for managing disaster risk, followed by our Disaster Fund methodology and its associated maximization setup. Section 3 presents our theoretical findings and conducts comparative statics. Section 4 provides an empirical study on U.S. flood risk and illustrates the optimal solution to the Disaster Fund model, highlighting the influence of various constraints and assumptions. Finally, Section 5 concludes the paper. Technical details, including proofs and additional figures, are provided in the appendix.

2. Disaster Fund model

2.1 Types of DRF instruments

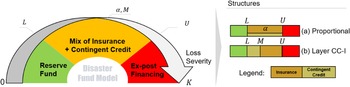

Following the World Bank classification (Mahul et al., Reference Mahul, Signer and Krishna2018) and a substantial body of DRF literature (Kashiwagi, Reference Kashiwagi2011; Zelinschi et al., Reference Zelinschi, Domide and Vîrban2013; WorldBank, 2018), we group DRF instruments into three broad categories.

-

• Budgetary Measures: These measures refer to the allocation of funds by the government for disaster-related expenditures and are typically risk-retention strategies. These funds can be regular injections (e.g., a proportion of GDP) into reserve funds or reallocations from other programs. For ex-ante reserve funds, a sum of money is set aside for disaster relief, allowing the government to react swiftly when disaster strikes. On the other hand, ex-post borrowing and reallocating funds require no preparatory planning but carry high financial and opportunity costs since interest rates will be extremely high after a disaster, and the government must sacrifice otherwise potentially lucrative and valuable development and improvement projects.

-

• Market-based Instruments: These instruments are usually risk-transfer mechanisms, including insurance and insurance-linked securities such as catastrophic bonds and swaps. Adopting such instruments is imperative for a risk-averse decision-maker since they help remove uncertainty. These instruments transfer risk away from the government to third parties, such as the (re)insurance industry or the catastrophe bond capital market.

-

• Contingent Credit: These instruments are specific to DRF and combine elements of risk retention and risk transfer. An external third party, typically a well-established supranational organizationFootnote 2, agrees to lend a pre-agreed amount of funds to the participating countries in the event of a disaster. The loan typically carries a much lower interest rate compared to ex-post financing. However, countries must determine the maximum drawdown amount and pay a small upfront fee, both at the outset and at recurring intervals during the agreement, based on the maximum available drawdown before a disaster occurs.

Lastly, governments can turn to ex-post borrowing (from the public or other nations) and humanitarian aid (relying on donor countries for assistance) as a last resort to finance disaster losses. However, these ex-post financing options are highly uncertain and costly. The Disaster Fund focuses on the most representative and widely used DRF instruments in each category – reserve fund, insurance, CC, and ex-post borrowing.

2.2 Real-world considerations

In this section, we identify several practical constraints and considerations that governments face in managing disaster risk, which will subsequently be incorporated into the construction of the Disaster Fund model.

Observation 1. (Limited reserves) The government can allocate only a limited amount of funds as reserves for disaster financing.

Funds injections into the Disaster Fund have competing uses and opportunity costs, such as investing in development and improvement projects. Hence, it cannot be inexhaustible, making storing huge amounts of money to self-insure against disaster risk practically infeasible. Political opposition and protests are also likely to occur if a disproportionately large amount of cash is locked away for some future probabilistic event instead of improving citizens’ current welfare. For example, Baratz & Moskowitz (Reference Baratz and Moskowitz1978) note that California’s Proposition 13, which limited tax rates on citizens, was partly motivated by public discontent over a

$\$$

5 billion surplus held by the government while taxpayers felt overburdened by excessive taxation. Consequently, the limited reserves that the government can accumulate are often insufficient to cover significant disaster losses, requiring the government to explore other funding sources.

$\$$

5 billion surplus held by the government while taxpayers felt overburdened by excessive taxation. Consequently, the limited reserves that the government can accumulate are often insufficient to cover significant disaster losses, requiring the government to explore other funding sources.

Observation 2. (Limited risk horizon) A government will only protect itself from disaster risk up to a certain threshold.

A government typically does not protect itself from the entire spectrum of disaster risk, particularly when the risk involves exceptionally large losses. For example, within the past 10 years (2010–2020), there have been 8,235 emergency declarations and 14,539 major disaster declarations by U.S. states, which are instances where the individual states face disaster damages beyond their planned capability and resources and, thus, request federal assistance. (FEMA, 2023). Similarly, the National Flood Insurance Program (NFIP) in the U.S. relies on federal borrowings to cover extreme flood losses, as its purchase of public reinsurance and issuance of catastrophe bonds only provide coverage up to a certain threshold (Horn, Reference Horn2024). There are several possible explanations for a government to adopt a limited risk horizon. For enormous losses, governments may consider such disasters too unlikely to occur, or they may believe that securing protection against such remote events is not justified given the associated effort and opportunity costs. Budget constraints (insurance premiums covering the whole disaster loss are impractically high) and a myopic mindset (it is highly unlikely for a disaster to occur within the next few years) are common reasons to forsake planning efforts for such massive losses. The scarcity of market participants willing to absorb high-severity, low-likelihood disaster risk further exacerbates the issue. Additionally, moral hazard may play a role, as governments might expect humanitarian aid from other countries or organizations in the event of catastrophic disasters.

Observation 3. (Risk aversion) For potentially monumental losses, governments exhibit risk aversion behavior.

A critical consideration often overlooked in many DRF papers is the government’s risk aversion. Stewart et al. Reference Stewart, Ellingwood and Mueller(2011) suggest that for non-catastrophic events, governments typically adopt a net present value (NPV) approach to evaluate projects, implying risk neutrality. However, this NPV method fails to account for many of the risk-averse actions governments take regarding catastrophic lossesFootnote 3. Kaufman (Reference Kaufman2014) discusses why many governments tend to overlook the risk-reduction benefits of their actions by failing to account for uncertainties, and strongly recommends that policymakers adjust their decision-making processes to include risk-aversion analysis. Harris (Reference Harris2014) further highlights that governments often exhibit risk-neutrality in response to climate events due to political factors. By framing climate change as “unpredictable, unavoidable, or simply natural,” governments may justify their inaction. However, this mindset can be detrimental, as “by the time climate change impacts are bad enough for policymakers to react effectively, it will probably be too late” (Harris, Reference Harris2014). These examples underscore the importance of adopting a utility-based framework in disaster risk management that accounts for the government’s risk aversion.

Observation 4. (Risk tolerance) Governments seek to limit risk exposure.

Governments typically define acceptable risk levels to ensure they can address essential disaster response requirements while maintaining balanced risk exposure. To achieve this, they establish targets based on preferred risk measures, selected to align with specific objectives such as solvency or capital adequacy requirements (Bernard & Tian, Reference Bernard and Tian2009; Chen et al., Reference Chen, Li and Li2010; Melnikov & Smirnov, Reference Melnikov and Smirnov2012). Among these, VaR and TVaRFootnote 4 are the most commonly employed risk measures.

Under the VaR constraint, the government necessitates that the terminal value of the Disaster Fund remains above a pre-determined threshold after a disaster loss at or below the

$p$

-th percentile if its distribution occurs. For example, insurers under Solvency II must meet a 99.5% VaR requirement (BIS, 2019), while banks under Basel III adhere to a 99.9% VaR standard (EU Commission, 2015). The VaR measure is widely adopted due to its simplicity, interpretability, and ease of communication, making it a popular choice among regulators and financial institutions for quantifying risk.

$p$

-th percentile if its distribution occurs. For example, insurers under Solvency II must meet a 99.5% VaR requirement (BIS, 2019), while banks under Basel III adhere to a 99.9% VaR standard (EU Commission, 2015). The VaR measure is widely adopted due to its simplicity, interpretability, and ease of communication, making it a popular choice among regulators and financial institutions for quantifying risk.

Conversely, a TVaR constraint limits exposure to extreme disaster losses by ensuring that the conditional expected terminal value of the Disaster Fund in the tail of the distribution remains above a specified threshold. The TVaR measure is highly relevant for DRF, given that disaster losses are often characterized by high skewness and fat tails. Unlike VaR, which only considers losses up to a certain quantile, TVaR accounts for the average severity of losses beyond this threshold, addressing the limitations of VaR in ignoring extreme tail risks. In the financial sector, the significance of TVaR has been increasingly recognized. Basel IV, implemented starting in 2023, mandates the use of TVaR at the 97.5% confidence level as a primary risk measure, underscoring its effectiveness in providing a comprehensive assessment of extreme risk scenarios (pwc, 2016; FTSE, 2022).

Observation 5. (Insurance structure) The two primary types of insurance coverage are excess-of-loss and proportional structures.

Under many optimal insurance problems, the excess-of-loss indemnity structure often emerges as the optimal structure (see, e.g., Arrow, Reference Arrow1974; Denuit & Vermandele, Reference Denuit and Vermandele1998; Kaluszka & Okolewski, Reference Kaluszka and Okolewski2008). The superiority of the excess-of-loss structure arises from its flexibility to allow the policyholder to self-insure and avoid paying insurance loading for low-severity risk while removing high-severity risk, which is more volatile and uncertain, especially when the policyholder is highly risk-averse relative to the insurer.

However, practical considerations may render the proportional insurance structure preferable in certain contexts. For example, Huberman et al. Reference Huberman, Mayers and Smith(1983) argue that deductible contracts are suboptimal when there exist economies of scale in cost management. Lampaert & Walhin (Reference Lampaert and Walhin2006) highlight that proportional insurance can reduce moral hazard and is simpler to price. Additionally, Raviv (Reference Raviv1992) shows that co-insurance arrangements are optimal when insurers exhibit risk aversion or when insurance costs are non-linear. Similarly, our study’s inclusion of numerous real-world considerations in designing the DRF fund may suggest that the excess-of-loss structure is not necessarily optimal. These considerations introduce complexities that can alter the balance of costs and benefits associated with each insurance structure, potentially favoring the proportional structure under specific circumstances.

Observation 6. (Insurance premium) Insurers set premium loadings based on both the expectation and the volatility of the claim payments.

Variability-based premium principles have been extensively explored in the actuarial literature (see, e.g., Kaluszka, Reference Kaluszka2001; Chi, Reference Chi2012; Liang and Yuen, Reference Liang and Yuen2016b). Notably, Zeng & Luo (Reference Zeng and Luo2013) demonstrate that under the standard deviation or variance premium principle, the proportional insurance structure emerges as optimal. Furthermore, Landsman & Sherris (Reference Landsman and Sherris2001) critique that the expected value principle does not preserve a consistent risk ordering, as it neglects the variability of risks by assuming that two risks are indifferent as long as their expected payouts are equivalent – an oversight that is particularly significant in catastrophic loss scenarios. Lane & Mahul (Reference Lane and Mahul2008) also provide empirical evidence showing that catastrophe bonds are priced with up to a 44.9% premium loading on the standard deviation of losses, in addition to accounting for expected loss. In this paper, we adopt a hybrid approach that combines both the expected loss and standard deviation premium principles, ensuring a more realistic pricing mechanism. Premium loadings on expected loss help cover claims payouts, administrative charges, and profit margins of the insurer, while loadings on the standard deviation of losses compensate for the high uncertainty and risk borne by the insurer in relation to non-catastrophic risks.

2.3 Disaster Fund

Consider a government seeking to establish a Disaster Fund for effective disaster risk management. The design of the Disaster Fund must incorporate the various instruments discussed in Section 2.1, while also adhering to the constraints and considerations outlined in Section 2.2.

Firstly, since the reserve fund is the most cost-effective form of capital, the government will prioritize its use. Therefore, for low-severity losses up to a certain endogenous threshold

$L$

, the government will opt to use the reserve funds over other instruments. This approach is akin to self-insuring against the first portion of disaster risk from

$L$

, the government will opt to use the reserve funds over other instruments. This approach is akin to self-insuring against the first portion of disaster risk from

$0$

to

$0$

to

$L$

. To integrate Observation1 into the Disaster Fund model, we impose a cap on the availability of the reserve fund, denoted as

$L$

. To integrate Observation1 into the Disaster Fund model, we impose a cap on the availability of the reserve fund, denoted as

$k_L$

, which is exogenously determined. Once the reserve fund is depleted, the government must then rely on alternative methods to finance the remaining lossesFootnote 5.

$k_L$

, which is exogenously determined. Once the reserve fund is depleted, the government must then rely on alternative methods to finance the remaining lossesFootnote 5.

From Observation2, there exists an upper threshold loss amount

$U$

such that losses above

$U$

such that losses above

$U$

beyond which the government does not plan in advance to cover disaster losses, as these losses exceed its defined risk horizon. For losses surpassing

$U$

beyond which the government does not plan in advance to cover disaster losses, as these losses exceed its defined risk horizon. For losses surpassing

$U$

, the government will resort to ex-post financing methods, such as borrowing or reallocating budget from other sources, since ex-post financing generally comes with extremely high interest rates and significant opportunity costs, making it a last resort option after all ex-ante alternatives have been exhausted. Furthermore, we introduce an exogenous upper bound

$U$

, the government will resort to ex-post financing methods, such as borrowing or reallocating budget from other sources, since ex-post financing generally comes with extremely high interest rates and significant opportunity costs, making it a last resort option after all ex-ante alternatives have been exhausted. Furthermore, we introduce an exogenous upper bound

$k_U$

for

$k_U$

for

$U$

where the government will cease arranging additional DRF instruments. This limit could be driven by external factors, such as the unavailability of insurance markets or CC facilities willing to cover extremely severe losses.

$U$

where the government will cease arranging additional DRF instruments. This limit could be driven by external factors, such as the unavailability of insurance markets or CC facilities willing to cover extremely severe losses.

Lastly, for the remaining losses of moderate loss severity between

$L$

and

$L$

and

$U$

, the government will adopt a combination of risk retention and risk transfer strategies – specifically, insurance and CC – to cover disaster losses. This approach aligns with the World Bank’s recommended tiers of risk management: (i) self-retention to finance small but recurrent disasters, (ii) CC mechanisms for less frequent but more severe events, and (iii) disaster risk transfer, such as insurance, to cover major natural disasters (GFDRR, 2015). Our primary focus will be on this layer of risk management. The left diagram of Fig. 1 summarizes the key elements of the model discussed thus far.

$U$

, the government will adopt a combination of risk retention and risk transfer strategies – specifically, insurance and CC – to cover disaster losses. This approach aligns with the World Bank’s recommended tiers of risk management: (i) self-retention to finance small but recurrent disasters, (ii) CC mechanisms for less frequent but more severe events, and (iii) disaster risk transfer, such as insurance, to cover major natural disasters (GFDRR, 2015). Our primary focus will be on this layer of risk management. The left diagram of Fig. 1 summarizes the key elements of the model discussed thus far.

The Disaster Fund model. We consider two strategies, which consist of three distinct layers for losses with various severities, along with the parameters to optimize.

Let

-

•

$R_0 \in \mathbb{R}$

denotes the initial wealth allocated to the fund by the government,

$R_0 \in \mathbb{R}$

denotes the initial wealth allocated to the fund by the government, -

•

$F_{CC},r_{CC},r_e \geq 0$

denote the per-unit upfront administrative charge of CCFootnote 6, rate of interest for CC, and the rate of interest for ex-post borrowing, respectively, -

•

$X$

denotes a continuousFootnote 7, non-negative random variable modeling the disaster loss with a cumulative distribution function

$F_X(x)$

and a density function

$f_X(x)$

, -

•

$Y_I(X),Y_{CC}(X),Y_e(X) \geq 0$

denote the cashflows from insurance claims, CC, and ex-post financing, respectively, and -

•

$C_I, C_{CC} \geq 0$

denote the insurance premium and upfront cost for arranging CC, respectively.

To establish the Disaster Fund, the government determines the allocation of each DRF instrument to adopt across various loss severities, governed by endogenous variables

$L,M,U$

for the CC-I layer structure and

$L,M,U$

for the CC-I layer structure and

$L,\alpha ,U$

for the proportional structure. At the fund’s inception, the government pays the insurance premium

$L,\alpha ,U$

for the proportional structure. At the fund’s inception, the government pays the insurance premium

$C_I$

and the upfront cost of the CC

$C_I$

and the upfront cost of the CC

$C_{CC}$

. Upon the occurrence of a disaster event, the government raises the realized disaster loss amount

$C_{CC}$

. Upon the occurrence of a disaster event, the government raises the realized disaster loss amount

$X$

in full according to the predetermined Disaster Fund strategy. The realized loss will first be raised through the reserve fund

$X$

in full according to the predetermined Disaster Fund strategy. The realized loss will first be raised through the reserve fund

$L$

, followed by a mix of insurance payout

$L$

, followed by a mix of insurance payout

$Y_I(X)$

and CC

$Y_I(X)$

and CC

$Y_{CC}(X)$

if the reserve fund is insufficient to cover the entire disaster loss, and finally, the government resorts to ex-post financing

$Y_{CC}(X)$

if the reserve fund is insufficient to cover the entire disaster loss, and finally, the government resorts to ex-post financing

$Y_{e}(X)$

as a last resort. Subsequently, if CC facilities or ex-post financing are utilized, the government is obligated to repay the loans with interest charged at

$Y_{e}(X)$

as a last resort. Subsequently, if CC facilities or ex-post financing are utilized, the government is obligated to repay the loans with interest charged at

$r_{CC}$

and

$r_{CC}$

and

$r_e$

, respectively. Thus, the terminal Disaster Fund value after disaster occurrence and loan repayments is

$r_e$

, respectively. Thus, the terminal Disaster Fund value after disaster occurrence and loan repayments is

\begin{align} R_1(X) &= R_0 - C_I - C_{CC} \kern7pt\qquad\qquad\qquad\qquad\qquad\qquad \text{(fund initiation)} \\ &\quad -X+Y_I(X)+Y_{CC}(X)+Y_e(X) \qquad \qquad \text{ (disaster occurrence) } \nonumber \\ & \quad - (1+r_{CC})Y_{CC}(X) - (1+r_e)Y_e(X). \qquad \qquad \text{ (loan repayment) }\nonumber \end{align}

\begin{align} R_1(X) &= R_0 - C_I - C_{CC} \kern7pt\qquad\qquad\qquad\qquad\qquad\qquad \text{(fund initiation)} \\ &\quad -X+Y_I(X)+Y_{CC}(X)+Y_e(X) \qquad \qquad \text{ (disaster occurrence) } \nonumber \\ & \quad - (1+r_{CC})Y_{CC}(X) - (1+r_e)Y_e(X). \qquad \qquad \text{ (loan repayment) }\nonumber \end{align}

\begin{align} &= R_0 - C_I - C_{CC} - X + Y_I(X) \\ & \quad - r_{CC} Y_{CC}(X) - r_{e} Y_{e}(X).\nonumber \end{align}

\begin{align} &= R_0 - C_I - C_{CC} - X + Y_I(X) \\ & \quad - r_{CC} Y_{CC}(X) - r_{e} Y_{e}(X).\nonumber \end{align}

Equation (1) groups cashflows occurring at different points in time. In contrast, disregarding the terms

$C_{\text{CC}}$

,

$C_{\text{CC}}$

,

$Y_{\text{CC}}(X)$

, and

$Y_{\text{CC}}(X)$

, and

$Y_{\text{e}}(X)$

, Equation (2) coincides with the utility maximization problem of the renowned Arrow (Reference Arrow1974) model. However, disaster losses are often extraordinarily large, making it impractical for governments to self-retain risk, even when this may be the utility-maximizing solution. Consequently, governments must resort to borrowing to manage retained risk, incurring additional interest payments compared to the zero interest cost associated with using initial wealth. For each DRF instrument, a marginal unit of disaster loss is financed by

$Y_{\text{e}}(X)$

, Equation (2) coincides with the utility maximization problem of the renowned Arrow (Reference Arrow1974) model. However, disaster losses are often extraordinarily large, making it impractical for governments to self-retain risk, even when this may be the utility-maximizing solution. Consequently, governments must resort to borrowing to manage retained risk, incurring additional interest payments compared to the zero interest cost associated with using initial wealth. For each DRF instrument, a marginal unit of disaster loss is financed by

-

(i) one dollar of initial wealth,

-

(ii) one dollar of insurance payoff,

-

(iii)

$(1+r_{CC})$

dollars from a CC loan, or -

(iv)

$(1+r_{e})$

dollars from an ex-post loan.

In an unconstrained scenario, option (i) is the most cost-effective, followed by (iii), with (iv) being the least favorable. Consequently, the government will naturally prioritize funding disaster losses using its own wealth, then CC, and finally ex-post borrowing. To reflect real-world constraints, the limited reserve constraint caps the wealth allocated as a reserve at

$k_L$

, and the limited risk horizon constraint imposes an upper limit

$k_L$

, and the limited risk horizon constraint imposes an upper limit

$k_U$

on the combined use of CC and insurance. Any self-retained risk exceeding

$k_U$

on the combined use of CC and insurance. Any self-retained risk exceeding

$k_L$

must be financed through CC, and losses beyond

$k_L$

must be financed through CC, and losses beyond

$k_U$

necessitate ex-post financing.

$k_U$

necessitate ex-post financing.

In summary, our model is a one-period static framework based on Arrow (Reference Arrow1974)’s setup, with modifications tailored to the context of disaster losses. Specifically, self-retention becomes costly beyond a certain threshold as borrowing is required. The rising cost of capital discourages self-retention and promotes the purchase of insurance.

We assume that initial wealth is not a limiting constraint, meaning the initial fund is sufficiently large to cover at least the reserve fund, the insurance premium, and the CC upfront fee, such that

$R_0 \gt L + C_I + C_{CC}$

. In practice, loan repayments often occur over future periods and may extend across multiple years. However, for analytical convenience, we simplify the model into a single-period framework. Heuristically, the interest rates

$R_0 \gt L + C_I + C_{CC}$

. In practice, loan repayments often occur over future periods and may extend across multiple years. However, for analytical convenience, we simplify the model into a single-period framework. Heuristically, the interest rates

$r_{CC}$

and

$r_{CC}$

and

$r_e$

can be interpreted as adjusted rates, reflecting the net impact of the discounted time value of money and the potential investment returns of the fund over the repayment period.

$r_e$

can be interpreted as adjusted rates, reflecting the net impact of the discounted time value of money and the potential investment returns of the fund over the repayment period.

2.4 Insurance structures and premium principles

Based on Observation5, we consider two distinct structures for combining insurance and CC to address mid-severity losses between

$L$

and

$L$

and

$U$

. Under the excess-of-loss (Layer CC-I) structure, CC is arranged to cover losses within the interval

$U$

. Under the excess-of-loss (Layer CC-I) structure, CC is arranged to cover losses within the interval

$[L,M]$

, while insurance is used to cover the remaining losses within the range

$[L,M]$

, while insurance is used to cover the remaining losses within the range

$[M,U]$

. In contrast, the proportional (prop) structure entails a fixed proportional allocation parameter

$[M,U]$

. In contrast, the proportional (prop) structure entails a fixed proportional allocation parameter

$\alpha \in [0,1]$

, where insurance covers

$\alpha \in [0,1]$

, where insurance covers

$\$\alpha$

of each marginal unit of disaster loss and CC covers the remaining

$\$\alpha$

of each marginal unit of disaster loss and CC covers the remaining

$\$(1-\alpha )$

. As a result, insurance provides protection for up to

$\$(1-\alpha )$

. As a result, insurance provides protection for up to

$\alpha (U-L)$

of the total disaster loss, while CC is responsible for

$\alpha (U-L)$

of the total disaster loss, while CC is responsible for

$(1-\alpha )(U-L)$

.

$(1-\alpha )(U-L)$

.

Furthermore, in line with Observation6, we assume that insurance premiums are loaded by two factors: a multiplier

$\rho _1 \geq 0$

on the expected payout and a multiplier

$\rho _1 \geq 0$

on the expected payout and a multiplier

$\rho _2 \geq 0$

on the standard deviation of the payout. Overall, the terms in Equation (1) are governed by

$\rho _2 \geq 0$

on the standard deviation of the payout. Overall, the terms in Equation (1) are governed by

\begin{align} C_I &= (1+\rho _1)\mathrm{E}(Y_I(X))+\rho _2 \sqrt {\mathrm{Var}(Y_I(X) )},\\[-6pt]\nonumber \end{align}

\begin{align} C_I &= (1+\rho _1)\mathrm{E}(Y_I(X))+\rho _2 \sqrt {\mathrm{Var}(Y_I(X) )},\\[-6pt]\nonumber \end{align}

\begin{align} C_{CC} & = \begin{cases} (1-\alpha ) (U - L) F_{CC} &\mbox{for proportional strategy}\\ (M - L) F_{CC} &\mbox{for layer CC-I strategy} \end{cases} ,\\[-6pt]\nonumber \end{align}

\begin{align} C_{CC} & = \begin{cases} (1-\alpha ) (U - L) F_{CC} &\mbox{for proportional strategy}\\ (M - L) F_{CC} &\mbox{for layer CC-I strategy} \end{cases} ,\\[-6pt]\nonumber \end{align}

\begin{align} Y_I(X) & = \begin{cases} \alpha [(X - L)^+ \wedge (U-L)] &\mbox{for proportional strategy}\\ (X - M)^+ \wedge (U-M) &\mbox{for layer CC-I strategy} \end{cases} ,\\[-6pt]\nonumber \end{align}

\begin{align} Y_I(X) & = \begin{cases} \alpha [(X - L)^+ \wedge (U-L)] &\mbox{for proportional strategy}\\ (X - M)^+ \wedge (U-M) &\mbox{for layer CC-I strategy} \end{cases} ,\\[-6pt]\nonumber \end{align}

\begin{align} Y_{CC}(X) & = \begin{cases} (1-\alpha ) [(X - L)^+ \wedge (U-L)] &\mbox{for proportional strategy}\\ (X - L)^+ \wedge (M-L) &\mbox{for layer CC-I strategy} \end{cases} ,\\[-6pt]\nonumber \end{align}

\begin{align} Y_{CC}(X) & = \begin{cases} (1-\alpha ) [(X - L)^+ \wedge (U-L)] &\mbox{for proportional strategy}\\ (X - L)^+ \wedge (M-L) &\mbox{for layer CC-I strategy} \end{cases} ,\\[-6pt]\nonumber \end{align}

\begin{align} Y_e(X) & = (X - U)^+, \end{align}

\begin{align} Y_e(X) & = (X - U)^+, \end{align}

where

$(x)^+\,:\,x \mapsto \max (0,x)$

,

$(x)^+\,:\,x \mapsto \max (0,x)$

,

$x \wedge y\,:\,(x,y) \mapsto \min (x,y)$

, and the decision variables satisfy

$x \wedge y\,:\,(x,y) \mapsto \min (x,y)$

, and the decision variables satisfy

\begin{eqnarray} \begin{cases} L \leq U, \quad 0 \leq \alpha \leq 1, &\text{for proportional structure} \\ L \leq M \leq U, &\text{for CC-I structure} \end{cases} . \end{eqnarray}

\begin{eqnarray} \begin{cases} L \leq U, \quad 0 \leq \alpha \leq 1, &\text{for proportional structure} \\ L \leq M \leq U, &\text{for CC-I structure} \end{cases} . \end{eqnarray}

2.5 VaR and TVaR constraints

Referring to Observation4, we consider a government that seeks to limit the risk associated with the terminal value of the Disaster Fund by using the VaR and TVaR measures. Let

$p \in (0,1)$

denote the confidence level. We define

$p \in (0,1)$

denote the confidence level. We define

\begin{align} \mathrm{VaR}_p(R_1) &\;:=\;F^{-1}_{R_1}(1-p),\quad \text{and}\\[-6pt]\nonumber\end{align}

\begin{align} \mathrm{VaR}_p(R_1) &\;:=\;F^{-1}_{R_1}(1-p),\quad \text{and}\\[-6pt]\nonumber\end{align}

\begin{align} \mathrm{TVaR}_p(R_1) &\;:=\;\mathrm{E} [R_1 | R_1 \leq \mathrm{VaR}_p(R_1) ], \end{align}

\begin{align} \mathrm{TVaR}_p(R_1) &\;:=\;\mathrm{E} [R_1 | R_1 \leq \mathrm{VaR}_p(R_1) ], \end{align}

where

$F_{R_1}(\cdot )$

is the cumulative distribution function of

$F_{R_1}(\cdot )$

is the cumulative distribution function of

$R_1$

Footnote 8. Therefore, under the VaR and TVaR constraints, the government requires the following conditions to hold

$R_1$

Footnote 8. Therefore, under the VaR and TVaR constraints, the government requires the following conditions to hold

\begin{align} \mathrm{VaR}_p(R_1) & \geq k_{\mathrm{VaR}}, & &\text{ for VaR constraint, and, } \\[-6pt]\nonumber\end{align}

\begin{align} \mathrm{VaR}_p(R_1) & \geq k_{\mathrm{VaR}}, & &\text{ for VaR constraint, and, } \\[-6pt]\nonumber\end{align}

\begin{align} \mathrm{TVaR}_p(R_1)& \geq k_{\mathrm{TVaR}}, & & \text{ for TVaR constraint, } \end{align}

\begin{align} \mathrm{TVaR}_p(R_1)& \geq k_{\mathrm{TVaR}}, & & \text{ for TVaR constraint, } \end{align}

for some

$k_{\mathrm{VaR}} \in \mathbb{R}$

and

$k_{\mathrm{VaR}} \in \mathbb{R}$

and

$k_{\mathrm{TVaR}} \in \mathbb{R}$

exogenously determined by the government.

$k_{\mathrm{TVaR}} \in \mathbb{R}$

exogenously determined by the government.

2.6 Expected utility maximization problem

To simplify notations, let

$\Theta$

denote the feasible parameter space for the decision variables under the various insurance structures. Specifically, we have

$\Theta$

denote the feasible parameter space for the decision variables under the various insurance structures. Specifically, we have

$\theta = (L,\alpha ,U) \in \Theta$

for proportional structure and

$\theta = (L,\alpha ,U) \in \Theta$

for proportional structure and

$\theta = (L,M,U) \in \Theta$

for layer CC-I structure. To address the risk aversion behavior of governments as outlined in Observation3, we assume the existence of a convex utility function

$\theta = (L,M,U) \in \Theta$

for layer CC-I structure. To address the risk aversion behavior of governments as outlined in Observation3, we assume the existence of a convex utility function

$\mathbb{U}(w;\,\gamma )$

that reflects the government’s preferences, where

$\mathbb{U}(w;\,\gamma )$

that reflects the government’s preferences, where

$\gamma \geq 0$

is the risk aversion parameter, and

$\gamma \geq 0$

is the risk aversion parameter, and

$\mathbb{U}'(w) \gt 0$

,

$\mathbb{U}'(w) \gt 0$

,

$\mathbb{U}''(w) \lt 0$

.

$\mathbb{U}''(w) \lt 0$

.

To determine the optimal set of parameter values

$\theta$

, we aim to maximize the expected utility of the terminal Disaster Fund value, as expressed in Equation (1), subject to the constraints discussed in Sections 2.3 and 2.5. Thus, the maximization problem is

$\theta$

, we aim to maximize the expected utility of the terminal Disaster Fund value, as expressed in Equation (1), subject to the constraints discussed in Sections 2.3 and 2.5. Thus, the maximization problem is

\begin{align} \max _{\theta \in \Theta } \mathrm{E} \Big (\mathbb{U}(R_1 (X;\,\theta);\,\gamma )\Big ) \qquad \text{ s.t. } \qquad \begin{array}{cc} L \lt k_L, & \mathrm{VaR}_p(R_1) \geq k_{\mathrm{VaR}}, \\[3pt] U \lt k_U & \mathrm{TVaR}_p(R_1) \geq k_{\mathrm{TVaR}} \end{array} \end{align}

\begin{align} \max _{\theta \in \Theta } \mathrm{E} \Big (\mathbb{U}(R_1 (X;\,\theta);\,\gamma )\Big ) \qquad \text{ s.t. } \qquad \begin{array}{cc} L \lt k_L, & \mathrm{VaR}_p(R_1) \geq k_{\mathrm{VaR}}, \\[3pt] U \lt k_U & \mathrm{TVaR}_p(R_1) \geq k_{\mathrm{TVaR}} \end{array} \end{align}

Intuitively, under utility maximization, the government aims to maximize the terminal value of the Disaster Fund after a disaster event, while simultaneously minimizing the uncertainty associated with that value. The trade-off between these two competing objectives is governed by the risk aversion parameter

$\gamma$

. A higher value of

$\gamma$

. A higher value of

$\gamma$

indicates a stronger preference for minimizing uncertainty, thus prioritizing stability over potential returns.

$\gamma$

indicates a stronger preference for minimizing uncertainty, thus prioritizing stability over potential returns.

3. Analytical results

In this section, we provide a graphical interpretation of the Disaster Fund model, perform comparative statics, and highlight key analytical features of the model.

3.1 Graphical interpretation of Disaster Fund

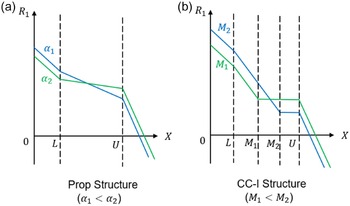

Graphs of terminal Disaster Fund value

$R_1(x)$

as a function of realized disaster losses

$R_1(x)$

as a function of realized disaster losses

$x$

under the (a) proportional and (b) layer CC-I insurance structures. In each graph, the blue curve illustrates the Disaster Fund value with lower insurance coverage and higher contingent credit (CC) arrangements relative to the green curve, which depicts an alternative Disaster Fund with higher insurance and lower CC.

$x$

under the (a) proportional and (b) layer CC-I insurance structures. In each graph, the blue curve illustrates the Disaster Fund value with lower insurance coverage and higher contingent credit (CC) arrangements relative to the green curve, which depicts an alternative Disaster Fund with higher insurance and lower CC.

Fig. 2 illustrates the terminal value of the Disaster Fund across various disaster loss severities. The vertical intercept represents the terminal Disaster Fund value when there are no disaster losses. A larger initial reserve

$R_0$

shifts the entire graph up vertically. A higher level of insurance coverage results in a greater initial premium payment, thereby lowering the vertical intercept. For both insurance structures, the loss magnitude is divided into three distinct regions

$R_0$

shifts the entire graph up vertically. A higher level of insurance coverage results in a greater initial premium payment, thereby lowering the vertical intercept. For both insurance structures, the loss magnitude is divided into three distinct regions

$[0,L)$

,

$[0,L)$

,

$[L,U)$

and

$[L,U)$

and

$[U,\infty )$

, separated by kinks at the attachment point

$[U,\infty )$

, separated by kinks at the attachment point

$L$

and exhaustion point

$L$

and exhaustion point

$U$

of the mid-severity insurance layer. For small losses within the range

$U$

of the mid-severity insurance layer. For small losses within the range

$0$

to

$0$

to

$L$

, the reserve fund fully covers each incremental dollar of disaster loss, producing a linear decline with a gradient of

$L$

, the reserve fund fully covers each incremental dollar of disaster loss, producing a linear decline with a gradient of

$-1$

. For losses exceeding

$-1$

. For losses exceeding

$U$

, the steep gradient reflects the high cost of ex-post financing, characterized by a gradient of

$U$

, the steep gradient reflects the high cost of ex-post financing, characterized by a gradient of

$-(1+r_e)$

.

$-(1+r_e)$

.

The shape of the graph for intermediate losses between

$L$

and

$L$

and

$U$

varies depending on the specific insurance structure employed. Under the proportional structure illustrated in Fig. 2(a), each marginal dollar of loss is split such that a fraction

$U$

varies depending on the specific insurance structure employed. Under the proportional structure illustrated in Fig. 2(a), each marginal dollar of loss is split such that a fraction

$\$$

$\$$

$\alpha$

is funded by the insurer, while the remaining

$\alpha$

is funded by the insurer, while the remaining

$\$$

$\$$

$(1-\alpha )$

is financed through borrowing from the CC facility, resulting in a gradient of

$(1-\alpha )$

is financed through borrowing from the CC facility, resulting in a gradient of

$(1-\alpha )(1+r_{CC})$

for the mid-severity layer, which is generally less steep compared to the gradient for losses between

$(1-\alpha )(1+r_{CC})$

for the mid-severity layer, which is generally less steep compared to the gradient for losses between

$0$

and

$0$

and

$L$

. On the other hand, there are two distinct sub-layers in the CC-I structure in Fig. 2(b). For losses between

$L$

. On the other hand, there are two distinct sub-layers in the CC-I structure in Fig. 2(b). For losses between

$L$

and

$L$

and

$M$

, the gradient

$M$

, the gradient

$1+r_{CC}$

is slightly steeper than

$1+r_{CC}$

is slightly steeper than

$-1$

due to the interest charged by CC. In contrast, since the insurance payout covers the entire disaster losses for losses between

$-1$

due to the interest charged by CC. In contrast, since the insurance payout covers the entire disaster losses for losses between

$M$

and

$M$

and

$U$

, the terminal Disaster Fund value is unaffected, resulting in a horizontal segment with a zero gradient. The point

$U$

, the terminal Disaster Fund value is unaffected, resulting in a horizontal segment with a zero gradient. The point

$M$

marks the boundary between the two sub-layers, delineating the transition from CC financing to full insurance coverage within the intermediate loss range.

$M$

marks the boundary between the two sub-layers, delineating the transition from CC financing to full insurance coverage within the intermediate loss range.

Lastly, we examine how the imposition of various constraints impacts the terminal Disaster Fund value. The constraint

$L\lt k_L$

(respectively,

$L\lt k_L$

(respectively,

$U\lt k_U$

) restricts the attachment point

$U\lt k_U$

) restricts the attachment point

$L$

(respectively, the exhaustion point

$L$

(respectively, the exhaustion point

$U$

) on the horizontal axis to be positioned leftward of the threshold

$U$

) on the horizontal axis to be positioned leftward of the threshold

$k_L$

(respectively,

$k_L$

(respectively,

$K_U$

). In contrast, the VaR constraint asserts that the graph’s height at the

$K_U$

). In contrast, the VaR constraint asserts that the graph’s height at the

$p$

-th quantile of the loss distribution must remain above the threshold

$p$

-th quantile of the loss distribution must remain above the threshold

$k_{\mathrm{VaR}}$

. Similarly, the TVaR constraint can be heuristically interpreted as necessitating that the weighted average height of the graph for losses exceeding the

$k_{\mathrm{VaR}}$

. Similarly, the TVaR constraint can be heuristically interpreted as necessitating that the weighted average height of the graph for losses exceeding the

$p$

-th quantile is greater than the threshold

$p$

-th quantile is greater than the threshold

$k_{\mathrm{TVaR}}$

.

$k_{\mathrm{TVaR}}$

.

Propositions1 and 2 highlight several interesting analytical characteristics of our Disaster Fund model concerning the VaR and TVaR constraints. Let

$p_U = F_X(U)$

.

$p_U = F_X(U)$

.

Proposition 1.

Setting

$\mathrm{VaR}_{p_1}(R_1) \geq k_{\mathrm{VaR}}$

is equivalent to setting

$\mathrm{VaR}_{p_1}(R_1) \geq k_{\mathrm{VaR}}$

is equivalent to setting

$\mathrm{VaR}_{p_2}(R_1) \geq k_{\mathrm{VaR}}^*$

where

$\mathrm{VaR}_{p_2}(R_1) \geq k_{\mathrm{VaR}}^*$

where

$k_{\mathrm{VaR}}^* = k_{\mathrm{VaR}} + (1+r_e)(F^{-1}_X(p_1) - F^{-1}_X(p_2)), \ \forall \ p_1, p_2 \geq p_U$

.

$k_{\mathrm{VaR}}^* = k_{\mathrm{VaR}} + (1+r_e)(F^{-1}_X(p_1) - F^{-1}_X(p_2)), \ \forall \ p_1, p_2 \geq p_U$

.

Proposition1 simplifies the consideration of the VaR constraint for high percentile values

$p\gt p_U$

by allowing it to be re-expressed at a lower percentile. When combined with the constraint

$p\gt p_U$

by allowing it to be re-expressed at a lower percentile. When combined with the constraint

$U \leq k_U$

, it suffices to focus on

$U \leq k_U$

, it suffices to focus on

$p = p_{k_U}=F_X(k_U)$

, as any VaR constraint with a larger

$p = p_{k_U}=F_X(k_U)$

, as any VaR constraint with a larger

$p$

can be equivalently reformulated as a constraint on

$p$

can be equivalently reformulated as a constraint on

$\mathrm{VaR}_{p_{k_U}}(R_1)$

. Intuitively, for losses beyond

$\mathrm{VaR}_{p_{k_U}}(R_1)$

. Intuitively, for losses beyond

$U$

, all strategies converge to relying exclusively on ex-post financing. Consequently, imposing a threshold on the terminal Disaster Fund value for one segment of losses beyond

$U$

, all strategies converge to relying exclusively on ex-post financing. Consequently, imposing a threshold on the terminal Disaster Fund value for one segment of losses beyond

$U$

is not unique; the constraint can effectively be “shifted” anywhere within the range

$U$

is not unique; the constraint can effectively be “shifted” anywhere within the range

$[U,\infty )$

. Graphically,

$[U,\infty )$

. Graphically,

$\mathrm{VaR}_{p_1}(R_1) - \mathrm{VaR}_{p_2}(R_1)$

is the vertical distance in the ex-post financing layer,

$\mathrm{VaR}_{p_1}(R_1) - \mathrm{VaR}_{p_2}(R_1)$

is the vertical distance in the ex-post financing layer,

$1+r_e$

corresponds to the gradient and

$1+r_e$

corresponds to the gradient and

$F^{-1}_X(p_1) - F^{-1}_X(p_2)$

is the horizontal distance of the ex-post financing layer. This relationship highlights the linear dependence of the ex-post financing segment, regardless of the type of insurance structure adopted for lower severity losses.

$F^{-1}_X(p_1) - F^{-1}_X(p_2)$

is the horizontal distance of the ex-post financing layer. This relationship highlights the linear dependence of the ex-post financing segment, regardless of the type of insurance structure adopted for lower severity losses.

Proposition 2.

Setting

$\mathrm{TVaR}_p(R_1) \geq k_{\mathrm{TVaR}}$

is equivalent to setting

$\mathrm{TVaR}_p(R_1) \geq k_{\mathrm{TVaR}}$

is equivalent to setting

$\mathrm{VaR}_p(R_1) \geq k^*_{\mathrm{VaR}}$

where

$\mathrm{VaR}_p(R_1) \geq k^*_{\mathrm{VaR}}$

where

$k^*_{\mathrm{VaR}} = k_{\mathrm{TVaR}} - (1+r_e)F^{-1}_X(p) + (1+r_e) \mathrm{TVaR}_p(X), \ \forall \ p\gt p_U$

.

$k^*_{\mathrm{VaR}} = k_{\mathrm{TVaR}} - (1+r_e)F^{-1}_X(p) + (1+r_e) \mathrm{TVaR}_p(X), \ \forall \ p\gt p_U$

.

Proposition2 establishes that, for a given loss distribution, the VaR and TVaR constraints are equivalent. This equivalence is particularly advantageous since the TVaR threshold is typically more difficult to determine and quantify in practice. Consequently, the government can limit its focus to the VaR measure without losing analytical generality. In conjunction with Proposition1, the TVaR and VaR constraints can jointly be simplified to the form

$ \mathrm{VaR}_{p_{k_U}}(R_1) \geq \bar {k}_{\mathrm{VaR}}$

, where

$ \mathrm{VaR}_{p_{k_U}}(R_1) \geq \bar {k}_{\mathrm{VaR}}$

, where

$ p_{k_U} = F_X(k_U)$

and

$ p_{k_U} = F_X(k_U)$

and

$\bar {k}_{\mathrm{VaR}} = \max \{k_{\mathrm{VaR}}, k^*_{\mathrm{VaR}} \}$

. This simplification significantly reduces the complexity of the maximization problem by eliminating the need to separately consider VaR or TVaR constraints for higher percentiles.

$\bar {k}_{\mathrm{VaR}} = \max \{k_{\mathrm{VaR}}, k^*_{\mathrm{VaR}} \}$

. This simplification significantly reduces the complexity of the maximization problem by eliminating the need to separately consider VaR or TVaR constraints for higher percentiles.

For commonly used parametric loss distributions

$X$

, the analytical expression for the TVaR

$X$

, the analytical expression for the TVaR

$\mathrm{TVaR}_p(X)$

can often be derived explicitly, facilitating the calculation of

$\mathrm{TVaR}_p(X)$

can often be derived explicitly, facilitating the calculation of

$k^*_{\mathrm{VaR}}$

in Proposition2. For instance, when the loss follows an exponential distribution

$k^*_{\mathrm{VaR}}$

in Proposition2. For instance, when the loss follows an exponential distribution

$X \sim \mathrm{Exp}(\lambda )$

,

$X \sim \mathrm{Exp}(\lambda )$

,

$\mathrm{TVaR}_p(X)= \frac {1}{\lambda } (1-\ln (1-p))$

, while for a lognormal distribution

$\mathrm{TVaR}_p(X)= \frac {1}{\lambda } (1-\ln (1-p))$

, while for a lognormal distribution

$X \sim \mathrm{LN}(\mu ,\sigma ^2)$

, we have

$X \sim \mathrm{LN}(\mu ,\sigma ^2)$

, we have

$\mathrm{TVaR}_p(X)= \frac {1}{1-p}e^{\mu +0.5\sigma ^2} \Phi \left ( \sigma - \Phi^{-1} (p) \right )$

, where

$\mathrm{TVaR}_p(X)= \frac {1}{1-p}e^{\mu +0.5\sigma ^2} \Phi \left ( \sigma - \Phi^{-1} (p) \right )$

, where

$\Phi (\cdot )$

is the CDF of the standard normal distribution

$\Phi (\cdot )$

is the CDF of the standard normal distribution

$\mathrm{N}(0,1)$

.

$\mathrm{N}(0,1)$

.

3.2 Premium principles

Building upon the extensive literature on optimal insurance structures, the optimal design for the Disaster Fund’s insurance coverage depends on the pricing methodology of the insurance contract. Consider a simplified scenario in which the VaR and TVaR constraints are not binding, and the upfront cost of CC is negligibleFootnote 9, then Propositions3 and 4 outline the implications of various insurance structures on the Disaster Fund.

Proposition 3.

Under the expected loss premium principle (i.e., when

$\rho _2=0$

), the layer CC-I structure is the optimal insurance structure.

$\rho _2=0$

), the layer CC-I structure is the optimal insurance structure.

Proposition 4.

Under the standard deviation premium principle (i.e., when

$\rho _2\gt 0$

), for sufficiently large losses (specifically for

$\rho _2\gt 0$

), for sufficiently large losses (specifically for

$x \gt \arg _x{\{Y_I(x) = \mathrm{E}(Y_I(X))\}}$

), if the pdf of the loss distribution

$x \gt \arg _x{\{Y_I(x) = \mathrm{E}(Y_I(X))\}}$

), if the pdf of the loss distribution

$f_X(x)$

is decreasing in

$f_X(x)$

is decreasing in

$x$

, CC-I structure is not the optimal insurance structure.

$x$

, CC-I structure is not the optimal insurance structure.

Proposition3 indicates that when the insurance premium principle does not account for the volatility of the payout, it is always preferable to adopt the layered CC-I structure for the Disaster Fund. This is because higher-severity losses lead to a greater reduction in utility for the risk-averse government compared to lower-severity losses. In contrast, Proposition4 suggests that when the premium includes a loading based on the standard deviation of the payout, the proportional structure may be more advantageous than the CC-I structure.

In practice, due to the substantial uncertainty in characterizing disaster losses and the potentially catastrophic magnitudes of the associated payouts, insurers typically impose significant loadings on the variability of disaster risk payouts. Consequently, when

$\rho _2$

is significant, we may observe the proportional structure outperforming the CC-I structure.

$\rho _2$

is significant, we may observe the proportional structure outperforming the CC-I structure.

3.3 Comparative statics

In this section, we perform a comparative static analysis to assess the impact of key external factors on the optimal solution, assuming that all constraints are non-binding, in order to focus on the direction of influence. To facilitate this analysis, we first introduce Lemma1.

Lemma 1.

Suppose

$\theta ^*$

is the maximizer and

$\theta ^*$

is the maximizer and

$\varphi \in \theta$

is one of the decision variables to optimize in Equation

13

. Moreover, assume that

$\varphi \in \theta$

is one of the decision variables to optimize in Equation

13

. Moreover, assume that

$\frac {\partial ^2 \mathrm{E} \mathbb{U} (\theta ^*)}{\partial \varphi ^2} |_{\varphi = \varphi ^*} \lt 0$

. Then, for any exogenous variable

$\frac {\partial ^2 \mathrm{E} \mathbb{U} (\theta ^*)}{\partial \varphi ^2} |_{\varphi = \varphi ^*} \lt 0$

. Then, for any exogenous variable

$\zeta$

(e.g.

$\zeta$

(e.g.

$\rho _1,\rho _2, r_{CC}, F_{CC}$

or

$\rho _1,\rho _2, r_{CC}, F_{CC}$

or

$r_e$

), if an increase (resp. decrease) in

$r_e$

), if an increase (resp. decrease) in

$\zeta$

leads to an increase (resp. decrease) in first-order derivative

$\zeta$

leads to an increase (resp. decrease) in first-order derivative

$\frac {\partial \mathrm{E}\mathbb{U} (\theta ^*)}{\partial \varphi }$

, the optimal

$\frac {\partial \mathrm{E}\mathbb{U} (\theta ^*)}{\partial \varphi }$

, the optimal

$\varphi ^*$

will be increasing (resp. decreasing) in

$\varphi ^*$

will be increasing (resp. decreasing) in

$\zeta$

.

$\zeta$

.

Lemma1 provides insights into how changes in

$\zeta$

affect the optimal solution

$\zeta$

affect the optimal solution

$\varphi ^*$

. It is sufficient to examine the change in

$\varphi ^*$

. It is sufficient to examine the change in

$ \frac {\partial \mathrm{E}\mathbb{U}}{\partial \varphi }$

as

$ \frac {\partial \mathrm{E}\mathbb{U}}{\partial \varphi }$

as

$\zeta$

varies to deduce the impact of

$\zeta$

varies to deduce the impact of

$\zeta$

on

$\zeta$

on

$\varphi ^*$

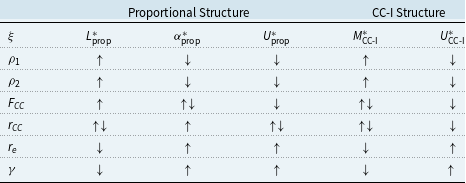

. Table 1 presents the comparative statics for the optimal parameters under both the proportional and CC-I structuresFootnote 10.

$\varphi ^*$

. Table 1 presents the comparative statics for the optimal parameters under both the proportional and CC-I structuresFootnote 10.

Comparative statics for the optimal parameters

$\varphi \in \theta ^*$

under the proportional and CC-I structures in response to changes in exogenous variable

$\varphi \in \theta ^*$

under the proportional and CC-I structures in response to changes in exogenous variable

$\xi$

. As

$\xi$

. As

$\xi$

increases, the optimal parameter

$\xi$

increases, the optimal parameter

$\varphi$

will either increase

$\varphi$

will either increase

$\uparrow$

, decrease

$\uparrow$

, decrease

$\downarrow$

, or the direction of influence is indeterminate

$\downarrow$

, or the direction of influence is indeterminate

$\uparrow \downarrow$

. Since without imposing constraints on

$\uparrow \downarrow$

. Since without imposing constraints on

$L$

,

$L$

,

$L^*_{\text{CC-I}} = M^*_{\text{CC-I}}$

under the layer CC-I structure, the column for

$L^*_{\text{CC-I}} = M^*_{\text{CC-I}}$

under the layer CC-I structure, the column for

$L^*_{\text{CC-I}}$

is excluded

$L^*_{\text{CC-I}}$

is excluded

As insurance premium becomes more expensive (i.e., higher

$\rho _1, \rho _2$

), the government tends to adopt less insurance, reflected in higher values of

$\rho _1, \rho _2$

), the government tends to adopt less insurance, reflected in higher values of

$L^*_{\text{prop}}$

and

$L^*_{\text{prop}}$

and

$M^*_{\text{CC-I}}$

and lower values of

$M^*_{\text{CC-I}}$

and lower values of

$\alpha ^*_{\text{prop}}$

,

$\alpha ^*_{\text{prop}}$

,

$U^*_{\text{prop}}$

and

$U^*_{\text{prop}}$

and

$U^*_{\text{CC-I}}$

. Moreover, when the upfront fee

$U^*_{\text{CC-I}}$

. Moreover, when the upfront fee

$F_{CC}$

for arranging CC is high, the government will generally opt for less CC, leading to a higher

$F_{CC}$

for arranging CC is high, the government will generally opt for less CC, leading to a higher

$L^*_{prop}$

and lower

$L^*_{prop}$

and lower

$U^*_{\text{prop}}$

and

$U^*_{\text{prop}}$

and

$U^*_{\text{CC-I}}$

. However, the effect of

$U^*_{\text{CC-I}}$

. However, the effect of

$F_{CC}$

on

$F_{CC}$

on

$\alpha ^*_{\text{prop}}$

and

$\alpha ^*_{\text{prop}}$

and

$M^*_{\text{CC-I}}$

is inconclusive as higher

$M^*_{\text{CC-I}}$

is inconclusive as higher

$F_{CC}$

can (i) reduce preference for CC due to higher cost, leading to a higher

$F_{CC}$

can (i) reduce preference for CC due to higher cost, leading to a higher

$\alpha ^*_{\text{prop}}$

and lower

$\alpha ^*_{\text{prop}}$

and lower

$M^*_{\text{CC-I}}$

, and (ii) deplete terminal wealth, prompting the government to reduce insurance purchase to lower premium payments and offset the wealth reduction caused by the higher upfront cost causing a lower

$M^*_{\text{CC-I}}$

, and (ii) deplete terminal wealth, prompting the government to reduce insurance purchase to lower premium payments and offset the wealth reduction caused by the higher upfront cost causing a lower

$\alpha ^*_{\text{prop}}$

and higher

$\alpha ^*_{\text{prop}}$

and higher

$M^*_{\text{CC-I}}$

.

$M^*_{\text{CC-I}}$

.

Similarly, the net impact of an increase in

$r_{CC}$

on the optimal

$r_{CC}$

on the optimal

$L^*_{\text{prop}}, U^*_{\text{prop}}$

and

$L^*_{\text{prop}}, U^*_{\text{prop}}$

and

$M^*_{\text{CC-I}}$

is indeterminate since a higher interest rate on CC has two opposing effects: (i) deter the use of CC and propel the government to adopt insurance, which lowers

$M^*_{\text{CC-I}}$

is indeterminate since a higher interest rate on CC has two opposing effects: (i) deter the use of CC and propel the government to adopt insurance, which lowers

$L^*_{\text{prop}}$

and

$L^*_{\text{prop}}$

and

$M^*_{\text{CC-I}}$

and increases

$M^*_{\text{CC-I}}$

and increases

$U^*_{\text{prop}}$

, and (ii) deplete terminal wealth due to higher loan repayment, causing the government to lower insurance purchase to in an effort to stabilize the terminal fund value, which in turn increases

$U^*_{\text{prop}}$

, and (ii) deplete terminal wealth due to higher loan repayment, causing the government to lower insurance purchase to in an effort to stabilize the terminal fund value, which in turn increases

$L^*_{\text{prop}}$

and

$L^*_{\text{prop}}$

and

$M^*_{\text{CC-I}}$

while decreasing

$M^*_{\text{CC-I}}$

while decreasing

$U^*_{\text{prop}}$

.

$U^*_{\text{prop}}$

.

A higher ex-post borrowing interest rate

$r_e$

has an unambiguous effect of increasing insurance uptake to avoid incurring substantial costs to secure additional funding for extremely large losses. Similarly, a higher risk aversion

$r_e$

has an unambiguous effect of increasing insurance uptake to avoid incurring substantial costs to secure additional funding for extremely large losses. Similarly, a higher risk aversion

$\gamma$

motivates the government to rely more on insurance over CC and ex-post borrowing, driven by a preference to minimize volatility in the terminal Disaster Fund value.

$\gamma$

motivates the government to rely more on insurance over CC and ex-post borrowing, driven by a preference to minimize volatility in the terminal Disaster Fund value.

3.4 The VaR constraint

While the constraints

$L \leq k_L$

and

$L \leq k_L$

and

$U \leq k_U$

directly affect the optimal decision variables, the influence of the VaR constraint on these variables is more complex. To facilitate discussion, let

$U \leq k_U$

directly affect the optimal decision variables, the influence of the VaR constraint on these variables is more complex. To facilitate discussion, let

$\varphi \in \{L,M,U \}$

denote a decision variable of interest and let

$\varphi \in \{L,M,U \}$

denote a decision variable of interest and let

$\varphi ^*$

and

$\varphi ^*$

and

$\varphi ^\#$

denote the optimal parameters for our optimization problem in Equation (13) obtained without and with VaR constraint (

$\varphi ^\#$

denote the optimal parameters for our optimization problem in Equation (13) obtained without and with VaR constraint (

$\mathrm{VaR}_p(R_1) \geq k_{\mathrm{VaR}}$

), respectively.

$\mathrm{VaR}_p(R_1) \geq k_{\mathrm{VaR}}$

), respectively.

Proposition 5.

Under a binding VaR constraint,

$\varphi ^\#$

will be either higher (resp. lower) than

$\varphi ^\#$

will be either higher (resp. lower) than

$\varphi ^*$

depending on whether

$\varphi ^*$

depending on whether

$F^{-1}_X(p_{\mathrm{VaR}})$

is higher (resp. lower) than

$F^{-1}_X(p_{\mathrm{VaR}})$

is higher (resp. lower) than

$\varphi ^*$

.

$\varphi ^*$

.

-

• For Proportional Structure:

$F^{-1}_X(p_{\mathrm{VaR}})\lt L^* \Rightarrow L^\#\gt L^*$

, and

$F^{-1}_X(p_{\mathrm{VaR}})\gt L^* \Rightarrow L^\#\lt L^*$

.

$F^{-1}_X(p_{\mathrm{VaR}})\lt U^* \Rightarrow U^\#\lt U^*$

, and

$F^{-1}_X(p_{\mathrm{VaR}})\gt U^* \Rightarrow U^\#\gt U^*$

. -

• For CC-I Structure:

$F^{-1}_X(p_{\mathrm{VaR}})\lt M^* \Rightarrow M^\#\gt M^*$

, and

$F^{-1}_X(p_{\mathrm{VaR}})\gt M^* \Rightarrow M^\#\lt M^*$

.

$F^{-1}_X(p_{\mathrm{VaR}})\lt U^* \Rightarrow U^\#\lt U^*$

, and

$F^{-1}_X(p_{\mathrm{VaR}})\gt U^* \Rightarrow U^\#\gt U^*$

.

Proposition5 outlines the ramifications of enforcing a binding VaR constraint. Intuitively, if the VaR constraint is active and

$p_{\mathrm{VaR}}$

-th quantile loss

$p_{\mathrm{VaR}}$

-th quantile loss

$F^{-1}_X(p_{\mathrm{VaR}})$

is high (resp. low), the optimal strategy involves increasing (resp. decreasing) insurance coverage by reducing (resp. raising)

$F^{-1}_X(p_{\mathrm{VaR}})$

is high (resp. low), the optimal strategy involves increasing (resp. decreasing) insurance coverage by reducing (resp. raising)

$L$

and raising (resp. lowering)

$L$

and raising (resp. lowering)

$U$

.

$U$

.

3.5 The case of CARA utility

The Constant Absolute Risk Aversion (CARA) utility function, widely favored in the literature for its broad adoption and mathematical tractability, is expressed as

\begin{equation*} \mathbb{U}(w;\,\gamma ) = -\mathrm{e}^{-\gamma w}, \text{ for } \gamma \gt 0. \end{equation*}

\begin{equation*} \mathbb{U}(w;\,\gamma ) = -\mathrm{e}^{-\gamma w}, \text{ for } \gamma \gt 0. \end{equation*}

Due to the multiplicative property of exponential utility

$\mathbb{U}(w_1 + w_2) = \mathbb{U}(w_1)\mathbb{U}(w_2)$

, the optimization problem becomes independent of the initial fund injection

$\mathbb{U}(w_1 + w_2) = \mathbb{U}(w_1)\mathbb{U}(w_2)$

, the optimization problem becomes independent of the initial fund injection

$R_0$

when there are no VaR or TVaR constraints. In other words, the magnitude of

$R_0$

when there are no VaR or TVaR constraints. In other words, the magnitude of

$R_0$

does not affect the values of the optimal decision variables

$R_0$

does not affect the values of the optimal decision variables

$\theta ^*$

, and it can be omitted when VaR or TVaR constraints are absent.

$\theta ^*$

, and it can be omitted when VaR or TVaR constraints are absent.

Alternatively, if a government’s preference is governed by a CARA utility function, it is possible to endogenize the initial fund injection

$R_0$

and determine the minimum value of

$R_0$

and determine the minimum value of

$R_0$

necessary to satisfy the government’s risk requirement, as quantified by a VaR constraint with

$R_0$

necessary to satisfy the government’s risk requirement, as quantified by a VaR constraint with

$p_{\mathrm{VaR}}$

above the exhaustion point

$p_{\mathrm{VaR}}$

above the exhaustion point

$U$

. The government can first solve the expected utility maximization problem without the VaR constraint to obtain the optimal decision variables

$U$

. The government can first solve the expected utility maximization problem without the VaR constraint to obtain the optimal decision variables

$\theta ^*$

. Subsequently, the minimum

$\theta ^*$

. Subsequently, the minimum

$R_0$

required to satisfy the VaR requirement is

$R_0$

required to satisfy the VaR requirement is

\begin{align} R_0 & = \inf \Big \{ r_0 \gt 0 \ | \ \mathrm{VaR}_{p_{\mathrm{VaR}}}(R_1(X);\,\theta ^*, r_0) \geq k_{\mathrm{VaR}} \Big \} \nonumber \\ & = \inf \left \{ r_0 \gt 0 \ \Bigg | \ \begin{array}{l} r_0 - C_I - C_{CC} - F^{-1}_{X}(p_{\mathrm{VaR}}) +Y_I\left (F^{-1}_{X}(p_{\mathrm{VaR}})\right ) \\ -r_{CC} Y_{CC}\left (F^{-1}_{X}(p_{\mathrm{VaR}}) \right ) -r_e Y_e\left (F^{-1}_{X}(p_{\mathrm{VaR}})\right ) \end{array} \geq k_{\mathrm{VaR}} \right \} \nonumber \\ & = k_{\mathrm{VaR}} + C_I + C_{CC} + F^{-1}_{X}(p_{\mathrm{VaR}}) - Y_I\left (F^{-1}_{X}(p_{\mathrm{VaR}})\right ) \nonumber \\ & \quad + r_{CC} Y_{CC}\left (F^{-1}_{X}(p_{\mathrm{VaR}})\right ) + r_e Y_e\left (F^{-1}_{X}(p_{\mathrm{VaR}})\right ). \end{align}

\begin{align} R_0 & = \inf \Big \{ r_0 \gt 0 \ | \ \mathrm{VaR}_{p_{\mathrm{VaR}}}(R_1(X);\,\theta ^*, r_0) \geq k_{\mathrm{VaR}} \Big \} \nonumber \\ & = \inf \left \{ r_0 \gt 0 \ \Bigg | \ \begin{array}{l} r_0 - C_I - C_{CC} - F^{-1}_{X}(p_{\mathrm{VaR}}) +Y_I\left (F^{-1}_{X}(p_{\mathrm{VaR}})\right ) \\ -r_{CC} Y_{CC}\left (F^{-1}_{X}(p_{\mathrm{VaR}}) \right ) -r_e Y_e\left (F^{-1}_{X}(p_{\mathrm{VaR}})\right ) \end{array} \geq k_{\mathrm{VaR}} \right \} \nonumber \\ & = k_{\mathrm{VaR}} + C_I + C_{CC} + F^{-1}_{X}(p_{\mathrm{VaR}}) - Y_I\left (F^{-1}_{X}(p_{\mathrm{VaR}})\right ) \nonumber \\ & \quad + r_{CC} Y_{CC}\left (F^{-1}_{X}(p_{\mathrm{VaR}})\right ) + r_e Y_e\left (F^{-1}_{X}(p_{\mathrm{VaR}})\right ). \end{align}

Intuitively,

$R_0$

represents the minimum initial fund injection required to satisfy the VaR constraint

$R_0$

represents the minimum initial fund injection required to satisfy the VaR constraint

$\mathrm{VaR}_{p_{\mathrm{VaR}}}(R_1) \geq k_{\mathrm{VaR}}$

. Graphically, as illustrated in Fig. 2, adjusting

$\mathrm{VaR}_{p_{\mathrm{VaR}}}(R_1) \geq k_{\mathrm{VaR}}$

. Graphically, as illustrated in Fig. 2, adjusting

$R_0$

shifts the entire graph vertically upwards or downwards, while leaving the structure of the different layers (such as the reserve fund, insurance, CC, and ex-post financing) unchanged. In this context,

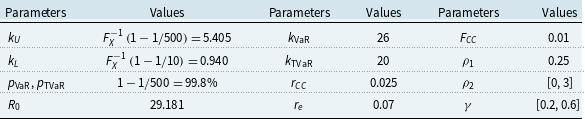

$R_0$