Introduction

In the late twentieth century, the combination of technological innovation and increasing competition transformed telecommunications markets worldwide. Because the sector had developed during the twentieth century within nationally constructed monopolies, especially in Europe, privatization became one of the most visible expressions of this broader transformation. In Italy, this trajectory culminated in October 1997, when the government sold most of its stake in Telecom Italia, the state-owned enterprise (SOE) that had emerged from a decade-long process of reorganization. As the first major national SOE to be divested, the outcome of privatization was widely expected to shape subsequent transactions, earning it the label of the “mother of all privatizations.”Footnote 1 The sale generated 22,883 billion lire, roughly €12 billion,Footnote 2 equivalent to about one quarter of Italy’s 1996 budget deficit,Footnote 3 and stood as the largest single privatization in Europe to that date.Footnote 4 Despite a decade of successful public restructuring, the privatized company soon entered a period of financial instability and contraction, raising questions about the necessity and rationale of the divestment. The Italian experience unfolded within a European framework in which the European Economic Community (EEC), later the European Union, increasingly influenced member states’ decisions. By placing telecommunications at the center of its agenda—first through industrial policy initiatives and later through liberalization—European institutions helped set the stage for the privatization of the incumbent monopolists.Footnote 5 Thus, drawing on archival sources from Italy’s principal state-owned holding company, alongside material from European and national institutions and contemporary media, this article questions the inevitability of Telecom Italia’s full privatization by examining the regulatory framework in which it unfolded, the restructuring that preceded it and the corporate trajectory that followed. Rather than presenting public ownership and the liberalization of telecommunications markets as incompatible, it shows how a state-owned conglomerate could adapt to competition and deliver industrial and technological modernization.

The privatization of Italian public telecommunications formed part of a broader restructuring that began in the early 1980s, when the sector faced low productivity, organizational inefficiencies, and technological backwardness.Footnote 6 The industry was vertically integrated under STET.Footnote 7 Each branch remained fragmented along geographic lines inherited from earlier phases of public ownership, undermining effectiveness. Shifts in international markets and regulatory frameworks prompted government action. The digital revolution, the breakup of the American Telephone and Telegraph Company (AT&T), and the privatization of British Telecom (BT) in the early 1980s placed deregulation at the center of public debate.Footnote 8 While in the EEC, the European Commission progressively became a driver of market liberalization, promoting competition and the dismantling of national monopolies.Footnote 9 In response, the Italian government reorganized the state-owned telecommunications industry to strengthen it and prepare it for a competitive environment. Was privatization required by, or functional to, these changing international and supranational frameworks? Historians have discussed the European influences on Italian privatization, and this research builds on analyses that have underscored the homegrown dimension of market adjustment.Footnote 10 In the article, I argue that the restructuring launched in the 1980s had already produced an efficient, financially sound, and technologically competitive corporation, demonstrating that modernization in a high-tech sector did not require a change in ownership. Continued public ownership remained compatible with European telecom regulation, provided full compliance with market liberalization and competition requirements. A process initially driven by industrial modernization ultimately yielded to fiscal priorities, redirecting corporate transformation toward revenue extraction rather than long-term strategic consolidation.

This article intervenes in two main strands of scholarship. First, it engages with debates about the late-twentieth-century transformation of the telecommunications industry. Scholars have shown how technological innovation and regulatory reform, particularly at the supranational level in Europe, reshaped industries long embedded in national political economies.Footnote 11 Business actors actively participated in this shift,Footnote 12 and the digital revolution generated new user demands within an emerging information and communication technology ecosystem in which innovation and digital capabilities increasingly displaced physical infrastructure as the primary source of value.Footnote 13 Indeed, across many European countries from the 1980s onwards, these structural transformations drove a process of corporatization and marketization of telecommunications monopolies: a transition from public agencies into state-owned firms increasingly governed by commercial logic.Footnote 14 Nevertheless, this article builds on scholarship that emphasizes the importance of national specificities to the analysis of these changes. Mark Thatcher has shown that restructuring did not lead to linear convergence toward a single neoliberal model, as national institutional and political configurations mediated reform and produced divergent outcomes.Footnote 15 Reconstructing the Italian case from within shows that domestic actors did not merely adapt to structural trends favoring homogenization but actively shaped the trajectory of the telecommunications sector and its main protagonist.

Second, the article contributes to debates on the assessment of privatization. Since the 1970s, market-oriented logic has reshaped the relationship between the state and SOEs, framing public intervention as obsolete and presenting efficiency gains and revenue generation as primary justifications for divestment.Footnote 16 Yet, some scholars have undertaken a historical reassessment of privatization by reconsidering the role of state presence in the economy and emphasizing the continued relevance of public intervention.Footnote 17 Others have highlighted the persistence of “economic patriotism” within liberalized markets.Footnote 18 By showing that restructuring had already achieved corporate efficiency before privatization occurred, along a convergent European pattern of corporatization, this article complicates functionalist accounts. It clarifies how politics and fiscal objectives gradually displaced industrial strategy as the primary framework for divestment. Historicizing privatization also requires evaluating the firm’s pre- and post-privatization performance, a topic largely dominated by economists who equate success with financial results.Footnote 19 This article adopts a broader conception of performance, moving beyond financial returns to include innovation, scale, and competitiveness. Such an approach is essential for a strategic actor like public telecommunications operators, which not only provide public utility services but also sustain a national technological manufacturing base in a sector crucial to the twenty-first-century economy.Footnote 20 This research joins this debate by analyzing and problematizing the evolution of the Italian Telecom SOE during its long-term transformation from public to private ownership.

Hence, the article is structured as follows. Section I examines how and why technological innovation and European regulation promoted the liberalization of telecommunications markets. It analyzes how the European Commission combined industrial policy and market instruments to address the challenges posed by the convergence of telecommunications and computing, the rise of American and Japanese competitors, and the need to strengthen Europe’s technological base. Section II explores Italy’s domestic response through the Piano Europa , an ambitious public reorganization plan aimed at modernizing and consolidating the state-owned telecom conglomerate. It foregrounds the numerous outcomes achieved amid persistent political obstacles and ultimately examines how national authorities decided to privatize the public telecommunications industry, prioritizing government revenues over industrial strategy. The final section examines the company’s post-privatization trajectory, using its subsequent instability to reassess whether divestment represented an inevitable outcome of structural change.

New Market, New Rules

The transformation of Italian telecommunications unfolded within a rapidly evolving technological and European regulatory framework. The convergence of computing and communications, together with intensifying international competition, prompted the European Community to redefine the rules governing the sector through a combination of industrial policy initiatives, standardization, and gradual market liberalization. To assess whether the privatization of Telecom Italia was inevitable, it is therefore necessary to clarify how European regulation reshaped national telecommunications systems and, crucially, what it did—and did not—require from member states. Only by distinguishing between regulatory constraints and political choice can we determine whether divestment of the telecommunications industry represented a structural necessity or a domestically constructed response.

During the 1980s, the relationship between national monopolies, technology, and equipment suppliers in the telecommunications industry entered a period of profound change. For decades, Public Telecommunications Operators (PTOs) had controlled networks and major research centers. At the same time, a few domestic manufacturers supplied equipment under stable conditions, often tied by “cozy” patent-sharing agreements or protected frameworks.Footnote 21 Over time, this productive structure had supported key innovations such as digital switching and fiber optics. But microelectronics and information technology lowered the entry barriers and demanded faster innovation and greater flexibility than vertically integrated monopolies could deliver. Manufacturers like Siemens, Alcatel, and Ericsson expanded their own research and development (R&D) capacity, reducing their dependence on laboratories embedded within publicly owned telecommunications companies. US and British regulators dismantled the AT&T and BT monopolies, reinforcing this shift by breaking long-standing vertically integrated productive patterns and promoting competition across both services and manufacturing. Reformers argued that innovation could flourish outside vertically integrated systems, a claim that encouraged other industrialized countries to reconsider the balance between state control and market forces. Together, these transformations reflected a shift away from the older model of state-controlled telecommunications toward what policymakers envisioned as a more open and technologically dynamic global industry.Footnote 22

In those years, US manufacturers in the technology and telecommunications sectors leveraged accelerating innovation to expand their global reach and challenge European players. As telecommunications and computing converged technologically, firms that had previously operated in distinct sectors began expanding across both, reshaping competitive dynamics in network services. The increasingly software-driven nature of digital switching equipment lowered the technical barriers that had previously kept computer manufacturers out of the telecommunications equipment market. At the same time, the Iran-Iraq conflict and the debt crisis in developing countries weakened global demand, particularly for American exports, prompting the US to turn toward Europe as a key market.Footnote 23 Motivated by Cold War rivalry, Washington reignited its technological ambitions through initiatives such as the Strategic Defense Initiative—a symbol of its broader drive for high-tech leadership with indirect effects on Europe’s advanced industrial sectors. The 1982 deregulation of the US telecommunications industry, which dismantled AT&T’s domestic monopoly, freed American firms to compete internationally and intensified pressure on European players.Footnote 24 US companies sought footholds in Europe, moving to compete mainly in manufacturing, which was more open to foreign entry, rather than in services, still protected by national monopolies.Footnote 25

Japan also presented formidable challenges to the EEC. By the early 1980s, Japan’s dominance in mature and advanced technological sectors such as steel, automotive manufacturing, and shipbuilding exacerbated Europe’s trade deficit.Footnote 26 Japanese companies leveraged their technological advantages to strengthen their international position, whereas European firms faced significant obstacles in entering the Japanese market, including restrictive distribution networks and broader socio-economic resistance. These asymmetries highlighted the need for Europe to reassess and modernize its industrial strategies and regulatory structures to sustain its competitiveness in the evolving global economy.Footnote 27 Japanese electronics and telecommunications firms—NEC, Fujitsu, Hitachi, Oki Electric, and Toshiba—rapidly expanded their export capacity in the late 1970s and 1980s. They combined advanced semiconductor technology, government support through the Ministry of International Trade and Industry (MITI), and aggressive investment in R&D. By the early 1980s, they had become major competitors in switching systems, fiber optics, and emerging mobile communications.

After trying protectionist measures,Footnote 28 the European Commission responded to these developments with positive industrial policy initiatives to support the EEC’s industrial competitiveness. The European Round Table of Industrialists (ERT) was a high-level lobbying group founded in 1983 that brought together leaders of major European multinational corporations to influence EEC policies on industrial competitiveness, infrastructure, and market integration. It originated from a joint initiative by European Commissioner for industrial affairs Etienne Davignon, a strong advocate for EEC industrial policy, and multinational CEOs with a long-standing commitment to European integration. The ERT’s early orientation reflected a neomercantilist logic, advocating industrial support measures—R&D investment, infrastructure development, and protection of emerging technology sectors—to strengthen European firms against American and Japanese competition.Footnote 29

Accordingly, the Commission justified the new measures by recognizing the urgent need to directly and explicitly support technological innovation, thereby addressing a key weakness in European industry.Footnote 30 The Commission developed industrial policy R&D programs to support innovation further and help European manufacturing firms keep pace with technological and financial advances. Among the cooperative efforts undertaken by European countries,Footnote 31 the landmark ESPRIT (the European Strategic Program for Research in Information Technology) initiative targeted advances in microelectronics, software technologies, and automation applications. Launched in 1984, ESPRIT invested approximately 5,250 million ECUFootnote 32 over the 1984–1991 period, with half of the funding provided by the EEC. Complementing ESPRIT, the RACE (Research and Development in Advanced Communications Technologies in Europe) program focused on user-terminal scenarios and preliminary technological analysis. These programs also supported SOEs: Italy’s STET played a pivotal role in ESPRIT’s development starting in 1981, with its subsidiaries demonstrating remarkable success in securing funding. By 1984, STET ranked fourth among European industries, securing 56 billion lire in financing for 38 projects.Footnote 33

By the middle of the decade, EEC institutions decided to complement these industrial policy initiatives, which they described as insufficient to strengthen the global competitiveness of Europe’s technological industry, with stronger measures to promote market integration. In 1984, the Dutch Commissioner for Competition, Frans Andriessen, lamented the negative consequences of the delay in market integration. From a technological innovation perspective, the slow dismantling of market barriers did not bode well for Europe’s ability to respond to rising foreign competition. Although the EEC represented 18 percent of the global telecommunications market (compared to 42 percent for the United States and 11 percent for Japan), the largest national market among its member states did not exceed 4 percent. Any delay in adopting Community-wide standards reduced the potential market size and, in turn, limited European manufacturers’ learning opportunities.Footnote 34

Community governance first turned to standardization to deepen market integration. The ERT, which had previously supported neomercantilist approaches, began to advocate for market integration through common technical standards to harmonize regulations and help European firms face foreign competition. Responding to these demands, the EEC introduced several measures to remove technical barriers to trade, including the 1983 Mutual Information Directive, which aligned national legislation with regional initiatives, and the 1985 “New Approach to Technical Harmonization and Standards,” which replaced detailed product specifications with essential conformity requirements.Footnote 35 The challenge proved especially acute in telecommunications manufacturing, from consumer terminals to switching and transmission systems, where fragmented standards raised costs and limited export potential. The advent of digital technology made these new harmonization initiatives both possible and necessary to transmit more programs and data over the same infrastructure.Footnote 36 In 1984, Commissioner Davignon coordinated efforts within the European Conference of Postal and Telecommunications Administrations (CEPT)Footnote 37 to address the issue. Italian representatives from IRI Services warned that, if coordination failed, the Community should create an EEC body with regulatory powers, drawing on the more centralized models of the US and Japan.Footnote 38 Eventually, in 1988, CEPT created the European Telecommunications Standards Institute, an independent body responsible for adopting technical specifications and standards through consensus among its members.Footnote 39

By 1985, the European Commission, under the leadership of its new dynamic president, Jacques Delors, accelerated market integration to drive technical innovation and industrial modernization. The White Paper drafted by Lord Arthur Cockfield set the Single Market objective, and the Single European Act (1986) gave the Commission the tools to achieve it. In 1987, the Green Paper on Telecommunications outlined a strategy to transform the sector through the gradual liberalization of equipment manufacturing and value-added services,Footnote 40 the harmonization of technical standards, and the phased reform of core infrastructure and basic telephony, which were still under the control of national monopolies. The plan aimed to create a single European telecommunications market by removing regulatory and technical barriers, encouraging competition and innovation, strengthening industrial competitiveness, and investing in modern infrastructure.Footnote 41 The European Commission’s forecasts suggested that, by the late twentieth century, telecommunications and related industries could account for as much as 7 percent of the European Community’s GDP, a significant increase from just 2 percent. Moreover, it expected that over 60 percent of employment would depend heavily on telecommunications technologies. The Commission’s document stressed that realizing this economic potential and creating new jobs required a more open and competitive market environment that encouraged innovation, experimentation, and flexibility.Footnote 42

The liberalization of European telecommunications advanced in stages, beginning with manufacturing and only later extending to services. The European Commission sought to open the market gradually, starting where competitive entry was most feasible. Directive 88/301/EEC aimed to liberalize terminal equipment, ending the preferential rights that national PTOs held over the import, marketing, and maintenance of devices connected to public networks. This reform sought to break long-standing monopolies and open competition within the integrated structures linking service provision, infrastructure, and manufacturing. The 1990 Services Directive (90/388/EEC) built on this foundation by promoting functional separation between network operation, service provision, and regulation. Rather than mandating full vertical disintegration, the Commission required member states to distinguish between monopoly and competitive activities and to prevent public operators from using their control of infrastructure to block new entrants. This sequencing demonstrates that European intervention targeted market structure and competitive conduct rather than ownership status. This regulatory architecture, therefore, left room for different institutional configurations. What mattered for the Commission was transparency, functional separation, and non-discriminatory access. Corporatized public enterprises could comply with liberalization provided they adapted their governance structures and accounting practices to the new competitive environment. The issue was not whether public ownership could coexist with European market integration, but whether domestic authorities were willing to reorganize it accordingly.Footnote 43

In addition, European law maintained formal neutrality on ownership. Article 222 of the EEC Treaty affirmed that the Community would not prejudice national systems of property ownership, meaning that public enterprises remained legally compatible with the emerging regulatory framework. While the Commission promoted competition and functional separation, it did not—and could not—require privatization, leaving divestment a matter of domestic political choice.Footnote 44 The experience of other member states that maintained significant public ownership during the early stages of liberalization confirms that adherence to European competition rules did not automatically entail full divestment or loss of control. Both the French and German governments would gradually, and most importantly, partially reduce their stakes in France Télécom and Deutsche Telekom below the 50 percent threshold between the late 1990s and early 2000s, in parallel with the companies’ stock market listings. Yet, they would remain the largest shareholders in both firms and continue to exercise significant influence over their strategic direction. In the Italian case, European liberalization defined the regulatory environment in which the government reorganized STET and, later, Telecom Italia. The shift from public restructuring to full, and not partial, divestment resulted from domestic fiscal and political priorities.

A Contested but Successful Public Restructuring

Beyond European developments, the Italian government and the SOEs’ leadership also responded to shifting technological and economic conditions with a domestic industrial adjustment strategy, reflecting the “corporatization” of the state-owned telecom monopolists in the 1980s and 1990s.Footnote 45 To bridge the gap between the state-owned conglomerate STET and its main competitors, the government and IRI launched the Piano Europa (“Plan for European Alignment,” or Europe Plan), which was approved by the cabinet in May 1987 and officially implemented in March 1988.Footnote 46 IRI and STET leadership designed the plan to revitalize the national telecom industry through two core pillars: a broad investment program and, above all, a corporate reorganization to improve performance and rationality. Italian politicians and the SOEs’ governance complemented the plan by attempting to participate in the ongoing process of industrial integration. This section illustrates how these strategies sought to reconcile the quest for efficiency and adaptation to liberalized markets with public ownership. The prospect of privatization ultimately facilitated the consolidation of Telecom Italia into a large, innovative, and financially sound international firm. However, the section also shows that the main barriers to restructuring stemmed not from market pressures or conflicting industrial visions, but from entrenched political power struggles between those who favored market adjustment and those who sought to sustain public prerogatives and continued party influence.

Launching the Plan

The investments outlined in the Europe Plan were designed to address several long-standing challenges. The national public telecom industry lagged in the manufacturing sector, where Italian state-owned corporations failed to secure a significant share in global markets. Meanwhile, the domestic market appeared substantially dominated by the national industry. From a comparative perspective, Italy’s public telecommunications sector lagged in service quality and infrastructure modernization, requiring substantial financial commitments to bridge the gap. The Plan estimated investments in telecommunications networks for 1988–1997 at 82,400 billion lire, at 1987 prices. Including private corporations, total investments were expected to range between 104,000 and 116,000 billion lire.Footnote 47

The government and the SOEs’ leadership directed these investments toward infrastructure modernization and R&D. In 1987, IRI allocated 5,700 billion lire to plant development, with 90 percent of the funds directed toward telecommunications, focusing primarily on SIP’sFootnote 48 switching centers, network infrastructure, and user terminals. The STET group planned to invest 30,400 billion lire between 1988 and 1992, dedicating 92 percent of the resources to SIP to modernize telecommunications networks and services, with an emphasis on service quality. Investments in the manufacturing and industrial plant sectors totaled 970 billion lire, with a focus on defense systems and switching equipment. Then, STET projected an increase in its R&D workforce to 6,630 employees by 1992, representing a gain of 700 employees compared to 1988. Approximately 65 percent of R&D staff would focus on electronics and industrial plant sectors, while the remainder would work on telecommunications services. Total R&D costs over five years were projected at 3,650 billion lire, with 23 percent of the funding covered by planned divestments and 8 percent by non-repayable public financing. The burden of these investments fell primarily on Italtel and Selenia-Elsagg,Footnote 49 which together accounted for approximately 80 percent of R&D expenditures. Their focus areas included advanced telecommunications systems, transmission technologies, new telematic products, and defense and space systems.Footnote 50 It is important to note that at this stage, the state-owned conglomerate was already operating profitably. In 1986, it recorded profits of 414 billion lire, a 24 percent increase over the previous year, and benefited from abundant liquidity, which allowed it to self-finance 82 percent of its planned investments.Footnote 51 Profitability continued to rise steadily through the second half of the decade, reaching 735 billion lire in 1989, confirming the group’s financial strength on the eve of liberalization and before any privatization pressures emerged.Footnote 52

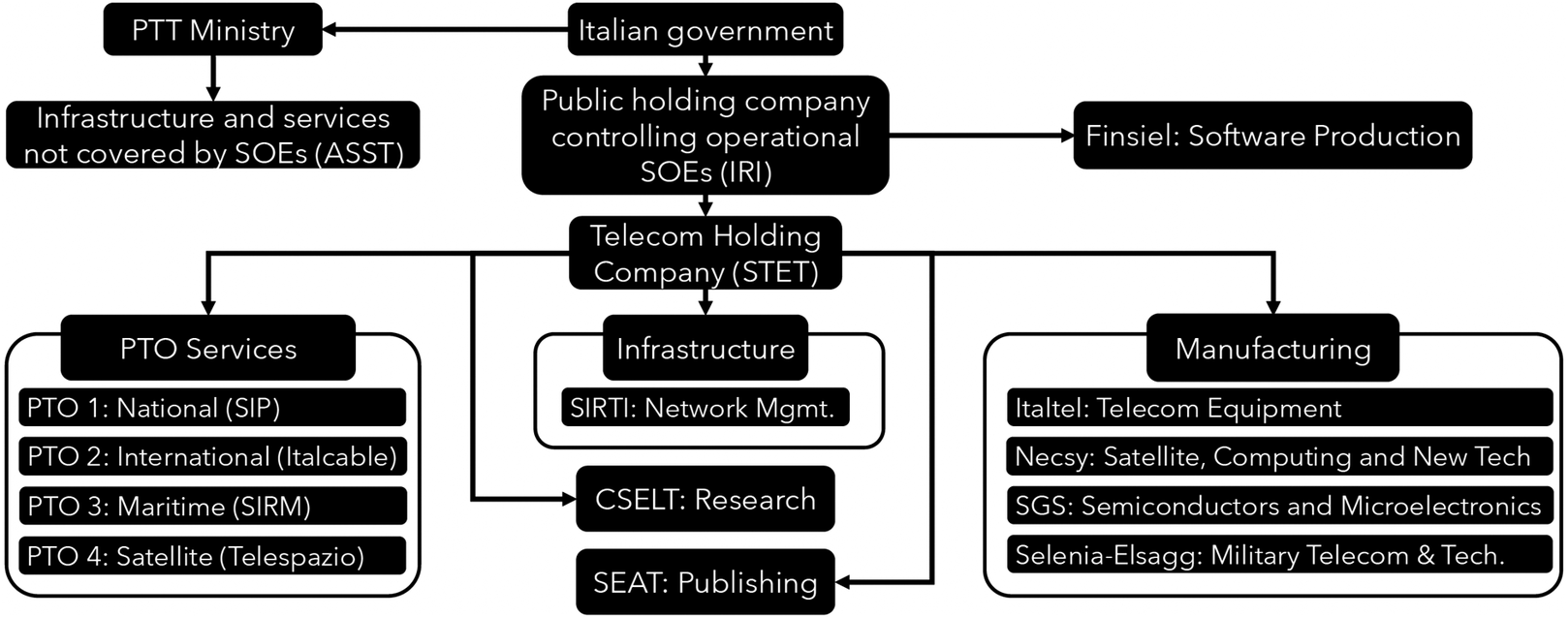

But the most critical aspect of Piano Europa was the corporate reorganization, which aimed at improving the efficiency of the public telecom sector while preserving its size and scope. As shown in Figure 1, a complex and inefficient structure, which reflected the historical evolution of SOEs that often grouped companies with overlapping functions by sector, burdened the state-owned telecommunications industry. The firms that composed the public telecom galaxy ranged from telecommunications services and infrastructure management to manufacturing, research, and, interestingly, publishing, with SEAT, which printed telephone directories. The involvement of multiple bureaucracies, making coordination challenging, compounded this inefficiency. To address these issues, the Europe Plan initiated a structural reorganization to restore efficiency and cohesion and prepare the sector for global competition. However, the process, dependent on administrative and legislative decisions, became far lengthier and more contentious than anticipated due to the significant political and economic stakes. Political parties effectively held the reorganization hostage, prioritizing the preservation of their power over corporate efficiency and undermining the plan’s transformative potential.

Public telecom industry in 1987.

Source: Elaborations on documents from the IRI fund at the Central State Archives (ACS).

Figure 1. Long description

The flowchart begins at the top center with the Italian government. An arrow points left to the P T T Ministry, which oversees Infrastructure and services not covered by S O E s (A S S T). A central arrow from the government points down to the Public holding company controlling operational S O E s (I R I). From I R I, an arrow points right to Finsiel: Software Production, and another points down to the Telecom Holding Company (S T E T).

S T E T branches into three main sectors:

1. P T O Services (left): Includes P T O 1: National (S I P), P T O 2: International (Italcable), P T O 3: Maritime (S I R M), and P T O 4: Satellite (Telespazio).

2. Infrastructure and Research (center): Includes Infrastructure (S I R T I: Network Mgmt.), C S E L T: Research, and S E A T: Publishing.

3. Manufacturing (right): Includes Italtel: Telecom Equipment, Necsy: Satellite, Computing and New Tech, S G S: Semiconductors and Microelectronics, and Selenia-Elsagg: Military Telecom & Tech.

Through the reorganization, the government and IRI leadership intended to address the fragmentation of decision-making centers, which they identified as the primary weakness of the public telecommunications system and which had caused inefficient investment and poor service quality. To resolve this, Italian authorties sought to consolidate the corporate structure and create a single PTO to optimize investments, enhance service quality, and guarantee the corporation’s long-term development.Footnote 53 The national program for telecommunications also sought to align Italy’s telecommunications system with those of the most advanced industrial nations by consolidating STET’s manufacturing sector and separating companies of broader strategic value that were not fully aligned with the core business, thereby streamlining operations. A study by IRI consultants highlighted that leading global industries in the sector had already adopted the proposed solution.Footnote 54 The reorganization transferred several manufacturing subsidiaries with high-tech and defense profiles, including Selenia-Elsagg and SGS, from STET to Finmeccanica, IRI’s aerospace and defense conglomerate, where they could be integrated into existing military and civilian operations.Footnote 55 A national security rationale also underpinned the transfers to Finmeccanica, shielding these entities from European liberalization. In turn, STET integrated FinsielFootnote 56 into its structure in 1992 to consolidate its manufacturing capacity in the information technology sector.Footnote 57

Most importantly, the core of the reorganization regarded the PTOs. The IRI board that launched the Piano Europa in March 1988, under the leadership of its president Romano Prodi, designed the so-called Super STET: a merger of all STET’s operational PTOs (SIP, SIRM, Italcable, and Telespazio) and the service duties carried out by ASST, the agency of the Post, Telegraph and Telephone (PTT) ministry. Proponents presented the operation’s advantages as self-evident, arguing that it would create a single corporation with an 18,000 billion lire turnover and sufficient critical mass to hold a solid position in the market and not “fall short” in Europe.Footnote 58 The new company (single PTO) would remain within the STET conglomerate, maintaining ties with associated companies such as Italtel, Necsy, and Sirti, as well as the infrastructure and manufacturing capabilities controlled by Azienda di Stato per i Servizi Telefonici (ASST), which the newly formed SOE would incorporate. Prodi, the plan’s primary sponsor, described the integration in a letter to PT Minister Oscar Mammì, tasked with initiating the necessary legislative process, as a crucial step toward creating a coherent and efficient telecommunications sector capable of addressing future challenges and opportunities.Footnote 59

Political Challenges

Yet, it was clear from the start that the process would not be immune from political intervention. The difficulties were of two types: first, there was the hurdle of parliament, which had to pass legislation promptly to greenlight the reorganization and formalize the transfer of ASST to STET. Then there were the political obstacles, such as those that had previously caused the failure of the merger between Italtel and Telettra, the primary private manufacturer of telecom equipment owned by Fiat.Footnote 60 Additionally, significant corporate consolidation within the state holdings system would reduce the number of positions to be filled by politicians on the boards of various SOEs, thereby reducing their economic and political leverage.Footnote 61 The government took one year to issue a bill to implement the reorganization. On 3 March 1989, Minister Mammì, who belonged to the Italian Republican Party (PRI) (a political faction supporting the reinforcement of market mechanisms and the reorganization designed by Prodi), won over the resistance in the cabinet.Footnote 62 It would take parliament until January 1992, almost three years, to approve the reorganization bill. The legislation authorized the transfer of ASST to STET. Still, it also triggered a new complex bureaucratic process: it required IRI to indicate to the ministries of PTT and SOEs the criteria it foresaw for the restructuring by 20 May 1992. The relevant ministers would then meet in the Interministerial Committee for Economic Policy (CIPE) to set the guidelines, further delaying the operational decisions.Footnote 63

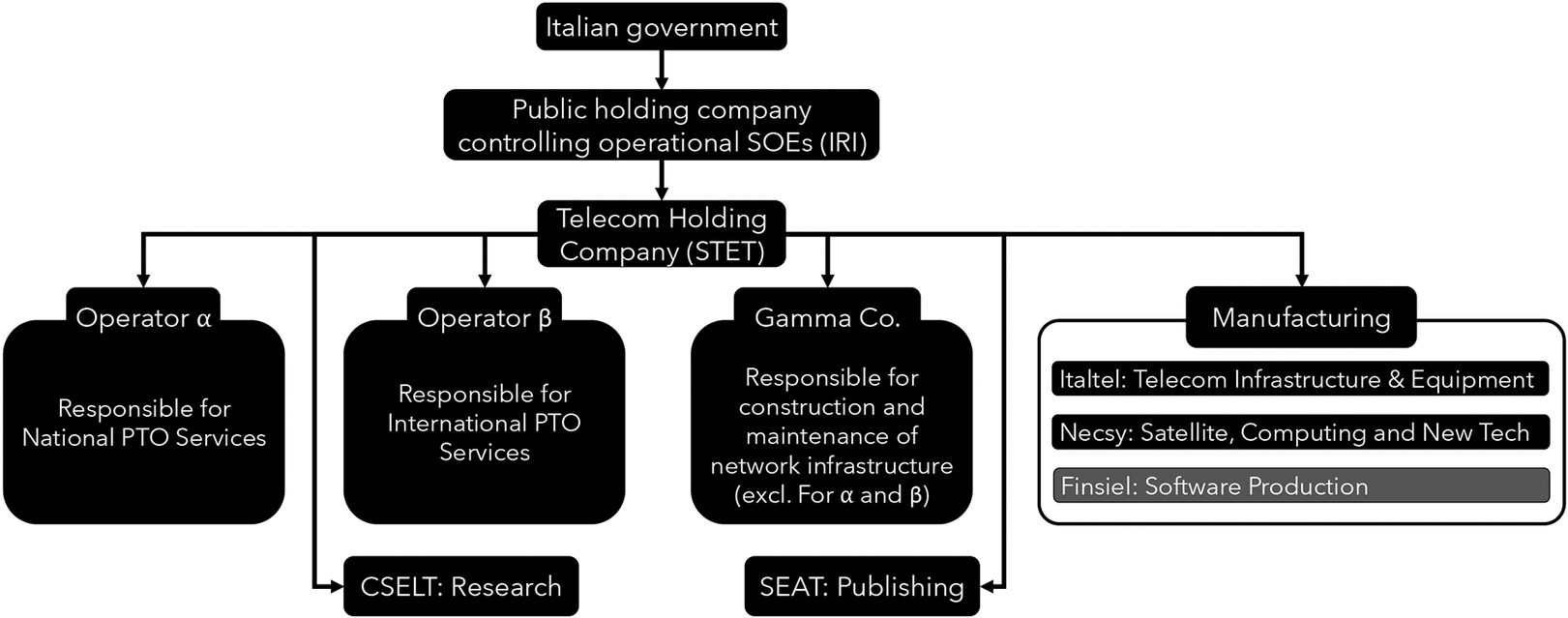

Between the launch of the reorganization process and the developments in spring 1992, the world changed within the universe of Italian SOEs. In the fall of 1989, Romano Prodi resigned from the presidency of IRI in protest against political obstructionism to industrial adjustment. Franco Nobili, who was much more attentive to political exigencies and inclined to preserve the SOEs’ structures and rationale as well as public ownership, succeeded him.Footnote 64 By 1992, politicians replaced Prodi’s plan with a new one, crystallizing the Italian political class’s temptation to return to a more articulated structure, which did not prioritize rationality and efficiency: the establishment of three distinct operational companies under STET’s coordination—the so-called bipolar structure, illustrated in Figure 2. Operator Alpha was designated to manage national telecommunications services, including SIP, Iritel,Footnote 65 and SIRM, with the option to spin off certain services, such as mobile telecommunications, into independent entities. Operator Beta would focus on international and intercontinental services, handling Italcable and Iritel’s international operations with an emphasis on long-distance infrastructure. The Gamma company would oversee long-distance networks, satellite connections, and undersea cables by integrating the infrastructures of Telespazio, SIP, and Italcable while also fostering synergies with radio broadcasting services. Its capital would be open to other shareholders, notably institutional users of the Gamma company’s network, in proportion to their contributions to revenue. Its proponents claimed that the proposed restructuring aimed to enhance operational efficiency, unify services, and align with European telecommunications standards.Footnote 66

The “bipolar” reorganization proposal of 1992.

Source: Direzione pianificazione e controllo, “Nota per il comitato di presidenza: riassetto del settore telecomunicazioni,” May 1992, IRI, numerazione nera, serie 4, sottoserie 4, sotto-sottoserie 2, fascicolo 41, AG/990, ACS.

Figure 2. Long description

The flowchart begins at the top with the Italian government, which points down to the Public holding company controlling operational S O E s (I R I). This entity points down to the Telecom Holding Company (S T E T).

From S T E T, the structure branches into four main vertical columns from left to right.

* The first column contains Operator alpha, responsible for National P T O Services. Below this is a branch to C S E L T: Research.

* The second column contains Operator beta, responsible for International P T O Services.

* The third column contains Gamma Co., responsible for construction and maintenance of network infrastructure (excl. For alpha and beta). Below this is a branch to S E A T: Publishing.

* The fourth column is labeled Manufacturing and contains three sub-entities: Italtel: Telecom Infrastructure and Equipment; Necsy: Satellite, Computing and New Tech; and Finsiel: Software Production.

However, the proposed bipolar solution would likely have failed to deliver on its promises: coordination among the three newly created companies, solidly under public ownership, except for partial privatization opportunities of the gamma company, would have lacked the unified and flexible structure necessary to achieve the critical mass required for international competitiveness. Moreover, the model remained rooted in a monopolistic logic that separated national and international communications and maintained close ties between service provision and network management. As such, it would have been difficult to reconcile with the European Commission’s liberalization framework.

The bipolar solution never saw the light of day, but the reorganization accelerated due to a radical change in scenery. By the summer of 1992, the situation had shifted again due to mounting budgetary constraints. First, the Maastricht Treaty, which established the Economic and Monetary Union (EMU) and set strict entry conditions (2 percent inflation, 60 percent public debt, and a 3 percent budget deficit), required Italy—running a 10 percent deficit and 100 percent debt in 1991—to undertake substantial fiscal adjustments to qualify for full participation. Then, in the spring and summer of 1992, Italy faced a financial crisis, forcing the government to reassure financial markets, international financial institutions, and foreign governments of its commitment to fiscal reforms and public debt sustainability.Footnote 67 These pressures, combined with a political legitimacy crisis stemming from widespread corruption scandals, reshaped the public stance on SOEs, facilitating the launch of privatization as a strategy to reduce debt and restore market confidence.Footnote 68 The telecom sector, one of the most viable and attractive, became central to this privatization drive. As a result, the government and the SOEs’ leadership suspended the reorganization process until April 1993, when an interministerial committee mandated the Treasury Ministry to develop a final operational plan. From that point on, the restructuring of the telecom sector became closely tied to the acceleration of Italy’s privatization program.

Toward Privatization

The Italian government decided to privatize the public telecom company in the spring of 1993, driven not by a broader industrial strategy but by the urgency of fiscal adjustment within an accelerating wave of public divestments. However, the full divestment of the telecom sector was not a foregone conclusion. STET was not explicitly included in Treasury Minister Piero Barucci’s November 1992 list of SOEs slated for privatization and was defined as “non-divestible.”Footnote 69 Yet, pressure intensified over the spring. The Christian Democrat economist Beniamino Andreatta, a strong advocate of privatization, was appointed foreign minister in late April 1993 and assumed responsibility for negotiating the fate of SOEs with the European Commission. Among those who had been disappointed by the Barucci plan, he had argued, in March, that STET should also be privatized, insisting that “there is nothing strategic in it.”Footnote 70 Eventually, although the Andreatta-Van Miert Agreement—which set the procedures according to which Italy should privatize—left some margin of maneuver regarding the state-owned telecommunications conglomerate.Footnote 71 The setting changed on 30 June 1993, when the government, chaired by Carlo Azeglio Ciampi,Footnote 72 issued a decree mandating the initiation of procedures to sell the state’s direct and indirect stakes in ENEL (Electricity), INA (Insurances), Banca Commerciale Italiana, Credito Italiano, IMI (Bank), STET, and ENI (Oil and gas) within thirty days. STET was included primarily for its market value and attractiveness, and because its sale could significantly contribute to the reduction of IRI’s debt.Footnote 73

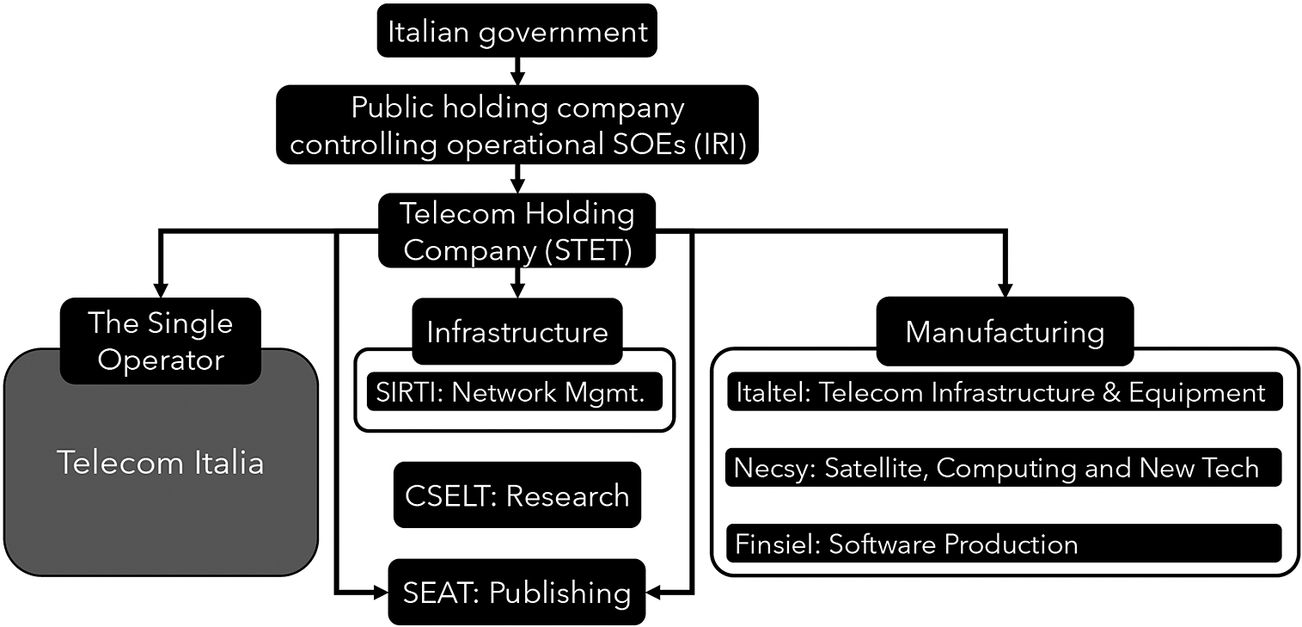

This decision also influenced corporate reordering. On the same day, 30 June, the Treasury accelerated the reorganization of the telecom sector. SIP, Italcable, Telespazio, and Iritel—which had absorbed the PT Ministry’s transferred assets—were to merge into a single company, Telecom Italia. STET would remain the controlling holding company, overseeing manufacturing firms and infrastructure management, as shown in Figure 3. “The reconsideration of the state’s presence in the economy and the launch of SOEs’ privatization increased the need to enhance corporate value, making it more attractive for potential share sales,” stated the official documents launching the process. The government set the deadline for finalizing the reorganization for 30 September 1994.Footnote 74 The government and IRI completed the merger of the PTOs on 27 July 1994, creating Telecom Italia.

The state-owned telecom industry after the reorganization of 1994.

Source: Elaborations on documents from the IRI fund at ACS.

Figure 3. Long description

A vertical flowchart begins at the top with the Italian government. An arrow points down to a box labeled Public holding company controlling operational S O E s I R I. This box points down to Telecom Holding Company S T E T.

From S T E T, the structure branches into three main columns from left to right.

1. The Single Operator: A box labeled The Single Operator sits above a larger grey box containing the text Telecom Italia.

2. Infrastructure and Research: A central column contains three vertical components. At the top is Infrastructure, which includes S I R T I: Network Mgmt. Below this is C S E L T: Research. At the bottom is S E A T: Publishing, which receives arrows from both the central and right-hand columns.

3. Manufacturing: The right column is headed by Manufacturing. It contains a large white box with three internal black bars: Italtel: Telecom Infrastructure and Equipment, Necsy: Satellite, Computing and New Tech, and Finsiel: Software Production.

Nevertheless, many details remained unresolved as reorganization was only a prerequisite for privatization. The government had to manage the transition toward the final privatization deadline set for 1997. It was caught between two difficult-to-reconcile objectives: maximizing state revenue and preserving a strategic national industrial actor. From the outset, the successive governments sought to implement protective measures. In May 1994, the conservative government, led by Silvio Berlusconi, introduced the so-called golden share, a mechanism first introduced in the United Kingdom during the privatization of British Aerospace and British Telecom. This special governmental prerogative was a legal safeguard against takeovers of strategically significant privatized companies.Footnote 75

The Italian government also took a protective stance in framing the company’s new private ownership. Progressive Prime Minister Romano Prodi, who succeeded Berlusconi, and Treasury Minister Ciampi designed the privatization process to combine widespread ownership with a “hard core” of “blockholders,” bringing together prominent Italian capitalist “families” of the time to ensure stability in the company’s governance.Footnote 76 The group included the dynasties controlling the major private companies of the time: Agnelli (Fiat), Colanninno (Olivetti), Tronchetti Provera (Pirelli), and the major banking groups (Mediobanca, Generali, and Intesa Sanpaolo).Footnote 77 Prodi and Ciampi believed that the alignment between private and national industrial interests could guarantee the strength of the privatized company. The Italian idea was not new, as the French government had implemented it in the 1986–1988 privatization. French privatization differed fundamentally from the British model in its emphasis on controlled ownership transfer. Rather than floating shares broadly on the open market, the Ministry of Finance orchestrated the process centrally, designating a noyau dur of stable investors that typically held between 15 and 30 percent of shares, while allocating portions to employees and limiting foreign institutional access. The overriding priority was governance stability and protection from hostile acquisitions.Footnote 78

On the road to privatization, Telecom Italia’s public ownership and management successfully navigated the changing competitive landscape and sustained the company’s market position. First, it took advantage of the international opening of markets, internationalizing the company, and making it a leading player in the Mediterranean region and South America.Footnote 79 In addition, it successfully entered the rapidly expanding mobile telecommunications segment. In 1993, the government launched the first tenders for mobile network licenses, ahead of full market liberalization in 1995. In the meantime, following its earlier focus on fixed telephony under the Europe Plan, Telecom Italia redirected resources toward mobile telephony and the internet, investing in innovations such as prepaid mobile cards and in ambitious, large-scale network and infrastructure expansion, including the Socrate and Fido-Dect projects.Footnote 80 Mobile telephony proved a remarkable commercial success, and by 2000, Italy had become a global leader in mobile penetration. In 1995, Telecom Italia created Telecom Italia Mobile (TIM) to face the impending liberalization of the market.Footnote 81 TIM leveraged Telecom Italia’s infrastructure and expertise to meet rising demand in a liberalizing market. Its expansion strengthened the group’s competitive position just as new entrants began challenging its dominance. In partnership with Bell Atlantic, Olivetti obtained the first private mobile license and launched Omnitel in December 1995. Competition intensified in the late 1990s with the entry of ENEL’s Wind Telecomunicazioni, followed by Blu and the Hong Kong-based “3 (Hutchinson),” marking the full opening of the Italian market, including to foreign capital.Footnote 82

Public ownership initially sought to preserve the vertically integrated structure of the Italian conglomerate, whose leadership considered a strength. Some players, such as British Telecom, attempted to develop their own manufacturing capacity in the 1990s but failed due to the scale of the required investment.Footnote 83 From this perspective, STET—later Telecom Italia—retained a comparative advantage because it had already integrated manufacturing, infrastructure, and services. Nevertheless, IRI’s leadership initially considered enhancing STET’s manufacturing divisions a cornerstone of its corporate strategy. In September 1996, at a hearing before the Telecommunications Committee of the Italian Chamber of Deputies, IRI President Michele Tedeschi stated:

Among the strategic priorities identified by STET, particular relevance should be given to the one concerning the development of the manufacturing (Italtel), plant and network engineering (Sirti), and information technology (Finsiel) sectors, whose growth is expected to complement the objectives of expanding the core business offering. Beyond the strengthening of market position in traditional products and services, these sectors are expected to enrich their offering by following, and where possible anticipating, emerging needs, including through the contribution of potential partners external to the group. This will allow STET to seize the new opportunities offered by the market, including within the framework of the numerous ongoing consolidation processes among actors belonging to the various converging sectors. Within this context, Italtel and Sirti will be able, where possible, to act in a complementary manner, leveraging the existing synergies between manufacturing and plant engineering activities.Footnote 84

The defense of vertical integration reflected more than institutional inertia. In a technology-intensive industry marked by rapid innovation cycles and effective economies of scale, integrating services and manufacturing secured control over research trajectories, technical standards, and supply chains. Public ownership enabled coordination across these segments and aligned network development with domestic industrial capacity. Dismantling this structure would therefore not amount to a mere organizational adjustment, but to a redefinition of industrial strategy. In most major European countries, monopolistic PTOs managed services and networks, while specialized private manufacturers, such as Alcatel in France,Footnote 85 Plessey in Britain, and Siemens in Germany, supplied equipment within an already-competitive industrial logic. Italy differed structurally. It concentrated both functions within the state-owned conglomerate STET, as private telecommunications and equipment manufacturing remained comparatively weak. The manufacturing divisions of the public group thus constituted the core of the national telecommunications industrial base.

Nevertheless, driven by its interest in maximizing revenue, the government ultimately imposed a valuation logic in preparation for privatization. In the same hearing in which he had defined manufacturing and network as strategic segments, Tedeschi acknowledged that, upon the government’s request, IRI would undertake studies on the “divestibility” of Sirti and Italtel, which appeared to be a reluctant concession.Footnote 86 To ensure such a course would be pursued, the government appointed new leadership at STET with an explicit mandate for privatization: Tommaso Tommasi di Vignano as CEO and Guido Rossi as chairman. Appearing before the same parliamentary committee six months later, the newly appointed “ticket” argued that the European Commission viewed structural separation as conducive to full market liberalization and that competitors were increasingly adopting disintegrated organizational models.Footnote 87 Although no European legislation required such disaggregation, the prospect of future asset divestments enhanced the company’s appeal to private investors, who could anticipate higher returns from a leaner and more flexible corporate structure.

The drive to boost valuation also triggered a final corporate reorganization. In December 1996, IRI sold its 54.5 percent stake in STET to the Treasury—with the remaining shares already publicly traded—to reduce its debt exposure.Footnote 88 Most importantly, to maximize revenues, in April 1997, the government decided to merge STET and Telecom Italia into a single entity, which retained the name Telecom Italia. The new structure consolidated three core functions of the former monopolist conglomerate: service provision, network infrastructure management, and manufacturing, encompassing software production through Finsiel and equipment production through Italtel.Footnote 89 Eventually, between October and November 1997, the government divested almost its entire stake, rather than retaining a relative majority, generating record revenues ahead of the European Commission’s 1998 liberalization deadline. That year also marked the final window to consolidate fiscal adjustment sufficiently for Italy to qualify for entry into the third stage of EMU in January 1999.Footnote 90 What initially appeared to be the culmination of a linear reform process soon became entangled in political and financial power struggles, with significant long-term consequences for the company’s governance and strategic coherence.

An Unstable Privatized Life

Did a change in ownership enhance the company’s strategic capacity and competitiveness in a liberalized market? The pursuit of efficiency has long served as a central justification for reducing the state’s role in the economy. While the previous sections traced the political and institutional path to privatization, evaluating whether divestment was truly necessary requires examining how the company evolved afterward. The post-privatization trajectory provides a concrete test of the claim that ownership change was essential to enhance competitiveness. At the time of its sale, Telecom Italia ranked among Europe’s strongest state-owned enterprises: large, profitable, and technologically advanced. In 1997, it reported €21.7 billion in revenues, €1.3 billion in net profit, and an operating margin of 45.4 percent.Footnote 91 It was Europe’s leading mobile operator by subscriber count, held significant stakes across Europe, Latin America, and Asia, and channeled 61 percent of its internally generated resources into productive investments. With 127,000 employees, €10 billion in debt, and €16.8 billion in tangible net equity, Telecom Italia embodied a vertically integrated model that combined services, infrastructure, and manufacturing, sustaining control over technology and production.Footnote 92 Still, the subsequent trajectory reveals a paradox: although profitability initially increased, governance became unstable, and the industrial base weakened as vertical disintegration progressed. In pursuit of efficiency and financial returns, unstable private ownership dismantled the integrated structure that had underpinned Telecom Italia’s technological capacity and economic strength. The instability that followed did not derive mechanically from market liberalization. Instead, it stemmed from the specific governance architecture adopted at privatization: dispersed ownership, a weak core group, and limited effective use of the state’s residual powers.

Despite its efforts, the government failed to establish a governance structure capable of ensuring the company’s long-term stability and growth. The “hard core” group designed to anchor private ownership proved largely symbolic, as it controlled only 6.7 percent of Telecom Italia’s shares. IFIL, the Agnelli family’s holding company and the leading member of the core, held just 10 percent of that stake, amounting to a mere 0.6 percent of total equity.Footnote 93 The new ownership structure also lacked a strategic outlook. Among the first decisions made by the post-privatization management was the suspension of investments in the Socrate and Fido-DECT programs—projects that, despite their short-term lack of profitability, might have positioned Italy at the forefront of advanced telecommunications infrastructure.Footnote 94 Moreover, the lack of clear leadership and competing visions for the company’s future did not facilitate the emergence of stable corporate governance. The “core” shareholders reappointed Guido Rossi, the outgoing president who had overseen the privatization, as president of the newly privatized Telecom Italia. However, recognizing the unfavorable environment, he resigned a few months later. Gian Mario Rossignolo succeeded him in January 1998; appointed by the Agnelli family, he nonetheless found his tenure undermined by the quarrelsome “core,” leading to his resignation within a few months. Eventually, in November 1998, Franco Bernabè, a former ENI executive, took over as CEO.Footnote 95

This weak structure was vulnerable to predatory acquisitions. Just months after taking charge, Bernabè faced a takeover attempt by Roberto Colaninno’s Olivetti. Colaninno began planning the operation in late 1998, securing financial backing from several major banks, including Chase Manhattan Bank, Donaldson Lufkin & Jenrette, Lehman Brothers, and Mediobanca. He also received political support from Prime Minister Massimo D’Alema, the first head of government with roots in the former Communist Party, which had by then transitioned to social democracy. D’Alema saw the move as evidence of a vibrant Italian financial market and an opportunity to confirm his commitment to capitalist practices.Footnote 96 He also viewed Colaninno as a representative of a new generation of entrepreneurial leaders capable of replacing the old guard, symbolized by figures like the Agnelli family, and with whom he could foster a productive working relationship to reform the Italian economy.Footnote 97 Olivetti formally launched its takeover bid on 20 February 1999. Just weeks earlier, on 27 January, D’Alema had hinted at the potential for such a move, stating: “There is the issue of strengthening the core group of shareholders who hold control […] it is a matter under review.” Then, observing the market activity leading up to the bid, he expressed, on 19 February, “appreciation for the courage of a group of individuals, entrepreneurs, and managers who want to acquire and manage a large company like Telecom.”Footnote 98

Political considerations hindered the pursuit of viable alternative options despite the tools available to counter Olivetti’s bid and widespread doubts about the buyer’s industrial strategy. Telecom Italia’s CEO Franco Bernabè fervently opposed the takeover, arguing that the buyers’ strategic industrial plans remained unclear. Moreover, the proposed leveraged buyout would significantly weaken the company’s financial position by increasing its debt burden and undermining its capacity for investment and innovation.Footnote 99 Olivetti lacked the financial resources to acquire Telecom Italia outright and relied on substantial bank financing, further increasing the corporation’s indebtedness, and the leveraged buyout would transfer the debt burden to ordinary shareholders. Moreover, Bernabè advocated for an alternative strategy, proposing a merger with Deutsche Telekom.Footnote 100 This plan, which also drew interest from France Télécom, aimed to establish a European telecommunications hub, advancing a unified European approach in this strategic sector. Foreseeably, the government did not use the golden share to stop the takeover. In addition, it prohibited the Treasury Chief, Mario Draghi, who, together with Ciampi, had opted for the “hard core,” from evaluating alternatives that would be more favorable for the shareholders.Footnote 101 Despite the instruments available, the government, often pursuing inconsistent or conflicting approaches and lacking a cohesive industrial strategy, failed to safeguard Telecom Italia’s position within the national economic and industrial landscape. The failure to activate available protective instruments underscores that the erosion of Telecom Italia’s industrial coherence was not an unavoidable consequence of privatization, but the result of discretionary political choices within a privatized ownership framework.

The successive owners and corporate operational choices maximized returns while eroding Telecom Italia’s overall strength and performance. When Olivetti and the so-called capitani coraggiosi (brave captains) led by Roberto Colaninno acquired control through a highly leveraged buyout, Telecom inherited around 29 trillion lire (€15 billion) in debt. The new owners pursued aggressive financial maneuvers, such as the repurchase of the publishing firm SEAT Pagine Gialle for a much higher price, only three years after its divestment.Footnote 102 These operations pushed the company’s debt from 8 to 22 billion euros, in addition to the 15 billion euros incurred for the takeover.Footnote 103 By 2001, Colaninno and his partners sold their entire stake, collecting a €1.5 billion capital gain and transferring the real estate assets, leaving Telecom and its subsidiaries burdened with €43 billion in debt.Footnote 104 That same year, Marco Tronchetti Provera, CEO of Pirelli, backed by major Italian banks and industrial groups, launched a second leveraged buyout to take control of the company. Tronchetti Provera’s management focused on reducing liabilities, but debt levels nearly doubled the company’s equity, constraining investment and innovation. The mergers of Olivetti and Telecom Italia (2003) and the costly full acquisition of TIM (2005), which had been partially demerged in 1995, worth €14.5 billion, further increased liabilities to €44 billion. The combination of financial mismanagement and the government’s laissez-faire approach produced chronic instability in ownership, leaving Telecom Italia uniquely exposed—one of the few privatized firms in the world to undergo two leveraged buyouts and four ownership changes in less than a decade.Footnote 105

This cycle of speculative management accelerated the divestment of Telecom Italia’s manufacturing capabilities and its withdrawal from international markets, dismantling the industrial and global structure inherited from STET. The state-owned conglomerate had combined vertical integration with an extensive international network through Italcable and Telespazio, and through participation in Latin America, including Telecom Argentina and Entel Chile. The 1994 merger that created Telecom Italia aimed to rationalize this structure while preserving vertical integration, but priorities shifted after privatization. The new private ownership began selling them to raise liquidity and service debt. Telecom Italia sold Sirti to Albacom shortly after privatization; it sold Italtel—Telecom Italia’s flagship manufacturing subsidiary—to Cisco Systems and Clayton, Dubilier & Rice in 2000, and Finsiel followed soon after to an Italian IT company.Footnote 106 In parallel, Telecom began a gradual retreat from foreign markets, selling major stakes in its Latin American holdings in the early 2000s and completing its final exit from Telecom Argentina in 2016, closing a cycle that had begun with STET’s ambitious global expansion in the 1980s.Footnote 107 By the mid-2000s, Telecom Italia had abandoned its manufacturing base and most of its international presence. What remained was a much leaner service provider, heavily indebted, and focused on the domestic market. By 2010, Telecom Italia had become a very different company. Revenues reached €27 billion, and net profit grew to €3.1 billion, but these figures masked structural resizing. The financial debt had surged to €38.6 billion, and tangible net equity had dropped to €11.3 billion. Investments, which had fallen to 30 percent under Tronchetti Provera’s management in 2006, later recovered to 40 percent, still far from the 61 percent pre-privatization level.Footnote 108

If privatization had been required to secure competitiveness, one would expect the company’s performance to converge with that of comparable European incumbents. The opposite pattern emerged. The widening gap suggests that the shift in ownership neither ensured stronger long-term capabilities nor necessarily strengthened them. The evolution of Telecom Italia as a telecommunications operator illustrates this divergence. In 1997, its revenues reached €22.1 billion, a figure broadly comparable to those of British Telecom (€21.7 billion) and France Télécom (€23.9 billion). They were higher than Telefónica’s (€14.2 billion) but remained well below Deutsche Telekom’s (€34.5 billion). By 2009, however, Telecom Italia’s revenues were comparable only to those of British Telecom, which had by then separated from its mobile operations. They corresponded to roughly 42 percent, 59 percent, and 48 percent of the revenues recorded by Deutsche Telekom, France Télécom, and Telefónica. Employment figures reveal a similar trend. Between 1997 and 2009, Telecom Italia reduced its workforce by 41.6 percent. Over the same period, Telefónica expanded markedly, increasing its employee count from 92,151 to 257,426. Taken together, these developments point to a clear divergence in strategic expansion and organizational outcomes among Europe’s major telecommunications incumbents.Footnote 109 Before its privatization, Telecom Italia had been one of the most advanced European companies in introducing new switching technologies, mobile telephony, and data compression systems. It ranked among the best globally regarding self-financing capacity, lines per employee, profitability, and investment in upstream research and innovation within its supply system. The comparison with Telecom Italia’s privatized life appears strikingly unfavorable.Footnote 110

Conclusion

Asking whether the full privatization of Italy’s telecommunications SOE was inevitable is intentionally provocative. The point is not to deny that fiscal constraints and political incentives made divestment likely in the 1990s, but to underscore the stakes hidden in the process’s details and question the assumption that technological modernization and European liberalization of a strategic high-tech industrial segment structurally required a change in ownership. This research has thus explored the capacity of public ownership to drive industrial and technological modernization in a critical sector of contemporary economies.

This article has advanced our understanding of the late-twentieth-century transformation of the telecommunications industry by showing that the shift from public monopoly to private, liberalized ownership was not structurally determined by regulatory, technological, and economic changes. Across Europe, structural pressures drove the corporatization of state-owned telecommunications monopolies, yet the Italian case confirms that domestic agency and institutional specificities produced divergent paths even within a shared regulatory environment. National actors actively shaped a trajectory that was distinctly Italian: through marketization, consolidation, and sustained investment, the public conglomerate had become a large, vertically-integrated, profitable, and technologically competitive enterprise capable of operating within the emerging European regulatory framework, showing that public ownership and market competition were not inherently incompatible. It also contributes to the historical reassessment of privatization by complicating the efficiency narrative that has long served as its primary justification. Telecom Italia did not emerge from private ownership as a stronger Italian corporate actor. Chronic instability, rising indebtedness, and the erosion of manufacturing capabilities followed, a trajectory that stands in stark contrast to the large, innovative, and internationally projected firm that public ownership had produced, and that only becomes fully visible when performance is evaluated beyond financial returns to encompass innovation capacity, industrial scale, and international competitiveness.

Eventually, the historical reassessment of Telecom Italia’s privatization retains more than scholarly interest, as suggested by recent developments: in March 2026, the Italian government launched a bid for state-owned Poste Italiane to acquire control of TIM (the new name of Telecom Italia, after rebranding). If completed, the operation would symbolically close a circle nearly three decades in the making, returning the national telecommunications operator to effective public control through a market-based mechanism, a process still unresolved at the time of writing.Footnote 111 Whether or not the transaction succeeds, its very possibility underscores the argument advanced in this article: privatization, that way, was not an irreversible structural necessity, but one political choice among others, and one whose consequences continue to shape the strategic dilemmas of Italian industrial policy.

Acknowledgements

I would like to Antonio Bonatesta, Giuliano Garavini, and Grace Ballor for the opportunity to collaborate within the PRIVIT project, in the framework of which this research was carried out. I also wish to thank the participants in the workshop “La ritirata dello Stato? Le privatizzazioni italiane nel contesto internazionale” (University of Roma Tre, February 2025) and the March 2025 Business History Conference for the valuable discussions. I am especially grateful to Grace Ballor and Shane Hamilton for their thoughtful feedback on earlier drafts, as well as to the journal’s anonymous reviewers for their constructive comments. All errors remain my own.

Funding statement

Research for this article was supported by Italian Ministry of University and Research (MUR) through the National PRIN 2022 Project: “The Politics of Privatisations: State, Energy and Social Transformations in the International Context (PRIVIT)” [Prot. 2022B39PAK, CUP: J53D23000120001], co-directed by Antonio Bonatesta, Giuliano Garavini and Grace Ballor.

Open access

Open access