I am of the opinion that department and bureau chiefs, who can make decisions, should have the opportunity to offer their visitors a cigarette. This is to prevent them from having to refuse an offered cigarette by their visitors, which would not benefit the meeting. However, if an offered cigarette does get accepted without anything presented in return, business will surely say: “Just bring some of the good cigarettes, then you will get your way.”Footnote 1

Circular Personnel Affairs, Department of Industry and Trade, Ministry of Economic Affairs, the Netherlands. n.d. between 1945–1947.

According to the quote, Dutch government officials were both aware of and concerned about the influence of business on policymakers. This concern relates to a longstanding debate among historians and social scientists, who have examined the interactions between business and politics and the extent to which these dynamics shape the policy process. Specifically, scholars of business power have addressed this issue through two theoretical approaches: instrumental and structural power. Instrumental power highlights a dynamic similar to that suggested by the quote and suggests that business exerts power through direct interaction with political actors. This can include activities such as lobbying, maintaining close political relationships, or participating in the policy process as experts.Footnote 2 Conversely, the structural approach stresses the indirect nature of business power. From this perspective, the importance of business in the economy constrains policymakers, who may avoid opposing business interests for fear of capital flight or declining economic activity.Footnote 3 In the Dutch postwar context, stimulating economic activity and growth was a key concern of policymakers, and business was considered a central actor in postwar economic reconstruction.Footnote 4 From a structural power perspective, such a setting invites consideration of the dependency between business and government, and the extent to which this shaped policymaking.

Historians and business historians are increasingly adopting the concept of business power to analyze business-government relations. Recent publications by Rollings (2021) and Wuokko and Fellman (2024) specifically call for greater engagement with business power within business history.Footnote 5 Alongside these contributions, other historians have explored closely related themes over the past decade. For instance, Decker (2011) explored corporate political activity in Ghana; Douglas (2018) and Bower and Higgins (2023) studied lobbying activities in the banking and alcohol industries, respectively; and Bucheli and DeBerge (2023) focused on firms’ non-market strategies.Footnote 6 Moreover, Spognardi (2024) used instrumentalism and structuralism to analyze the power of Argentinian Credit Unions in the 1960s.Footnote 7 Although historical scholarship on business power is certainly advancing, there remains significant scope for further assessment across different policy areas and historical settings. Notably, the issue of taxation remains largely unexplored in this respect.

This is surprising given that taxation is a key arena of contention between government and business, where interests easily collide. Business historians are increasingly examining taxation through themes such as corporate tax planning and the rise of tax havens. Studies on tax havens, both in colonial contexts and in Europe, demonstrate how corporate actors helped to promote and facilitate favorable tax regimes.Footnote 8 Specifically, in the case of Luxembourg, Calabrese and Giacomin (2025) show how close business-government ties in small-state environments contributed to the development of specific tax regulations.Footnote 9 While this literature recognizes the involvement of business in fiscal regimes, it remains less clear how these outcomes should be understood in terms of power dynamics. Social and political scientists address this by examining business power in fiscal policymaking. Several studies make theoretical contributions by, for example, highlighting the importance of ideas and subjectivity in structural power, the role of business organizations and state-business ties, and the intersection of instrumental and structural power.Footnote 10 These theoretical insights, and the empirical tools they offer, can usefully inform business-historical research on taxation.

This study builds on the theoretical insights of business power to examine the role of corporate actors in the tax policy process in the Netherlands. It specifically focuses on the case study of the Tax Revision 1950 ( Belastingherziening 1950, hereafter TR1950). The study covers the period from 1945 to 1950, a time of transition in both fiscal policy and business-government relations. World War II contributed to rising fiscal burdens on corporate profits in the Netherlands. After the war, the government pursued reconstruction through industrialization policies to stimulate economic activity and recovery. These policies framed the business sector as a vital actor in reconstruction and sought to encourage industrial investment through facilitative measures. As a result, tensions emerged between the existing fiscal pressures and broader economic policy objectives. The TR1950 functioned as the fiscal component of these industrialization policies and aimed to stimulate investments, thereby linking fiscal and economic policymaking. Given this connection and the heavy postwar tax burdens, the revision was high on the corporate agenda. Consequently, business interest associations (BIAs) and business representatives became heavily involved in the policy process.

The central aim of the study is to analyze how business engaged with the TR1950 policy process, the mechanisms and strategies they employed, and the extent to which this shaped the outcome. The case study is embedded within the literature on postwar business-government relations, corporatism, and industrial policy to clarify the broader role of business in society at the time. By drawing on business power frameworks and addressing corporate interests at the intersection of economic and fiscal policy, the study aims to make the following contributions. Firstly, the case illustrates that the government cannot be considered a monolithic entity. The tensions between fiscal and economic policy aims produced not only divergences between business and government interests, but also intra-governmental differences. Existing scholarship notes variation in interests and degrees of influence within the broader business sector, depending on factors such as firm size, industry, or national versus international operations.Footnote 11 This study extends that insight to the state: differing departmental mandates and intra-governmental tensions produced uneven corporate access and influence across governmental factions.

Secondly, and relatedly, corporate actors actively exploited these governmental differences. Business was able to reframe fiscal relief as conducive to industrial policy, aligning itself closely with the reconstruction objectives of specific governmental factions. This strategy rested on the construction of narratives and arguments that drew simultaneously on structural and discursive dimensions of business power. Business actors did not merely express preferences; they shaped the framework of the policy debates, embedding their interests within a broader narrative of economic reconstruction that proved difficult for policymakers to resist.

Finally, the case study is situated within broader histories linking corporate interests to fiscal and economic policy. Efforts to minimize fiscal burdens intersect directly with the administrative and political capacity of the state in relation to capital; a tension that has been exacerbated over the course of the twentieth century by corporate tax minimization strategies and tax havens. Since the late twentieth century, the Netherlands has been increasingly recognized as an international hub for tax avoidance, although relatively little is known about the early role of corporate actors in shaping its fiscal regime.Footnote 12 Existing scholarship suggests that this position has increasingly developed since World War II, partly through efforts to establish an attractive investment climate.Footnote 13 Simultaneously, scholars note that despite the decreasing tax burdens during the postwar period, governments also came to view taxation and fiscal incentives as tools for economic management, which in some cases contributed to a more national orientation of business.Footnote 14 While this study does not directly engage with the development of the contemporary Dutch role in international tax avoidance, it aims to show how corporate actors engaged with the tax policy process and the creation of fiscal alleviations in the early postwar period. Crucially, it demonstrates how business actors appropriated the postwar reconstruction context to advance their interests by presenting fiscal relief as a crucial element of industrial policy and economic recovery.

The study is structured as follows. The following section discusses business power scholarship, focusing on the different corporate strategies, mechanisms of power, and how different forms of power can be recognized. Following this, literature on business-government relations during the postwar period in Western Europe and the Netherlands will be discussed, alongside the case study and the fiscal-historical context. The subsequent section clarifies the methodology and source selection. This is followed by an examination of the business-government networks and the committees of the TR1950 policy process. The penultimate section will provide a discussion and analysis of the policy process using the business power framework, after which the study is concluded.

Business Power

Structural and instrumental power can interact; as such, it may prove difficult to clearly distinguish between the two forms. The business sector’s heavy involvement in the TR1950 policy process, both through BIAs and individual business representatives in policy committees, illustrates this ambiguity well. Although such participation may appear to reflect instrumental power, their involvement—or seat at the table—can equally signal their structural importance in the economy.Footnote 15 In turn, lobbying may strengthen structural power when policies that enhance capital mobility are advocated, for instance.Footnote 16 Babic et al. (2022) propose a unifying framework that integrates both forms alongside broader societal factors.Footnote 17 Both direct activities, such as lobbying, and structural mechanisms, such as the threat of disinvestment, can coexist and be driven by material or ideational premises. Business actors may, for example, mobilize media, expertise, and research organizations to influence prevailing ideas on policy issues. Politicians, meanwhile, face pressure from voters. Policies that cause disinvestment can lead to layoffs, impacting constituents and potentially reducing political support and loss of votes, deterring them from making certain decisions.Footnote 18 These factors collectively shape the conditions under which business may exert influence over policy outcomes.

A central concern in the literature is therefore the question of when and how such dynamics amount to regulatory capture, the shaping of policy outcomes in line with business interests. Culpepper (2010) argues that the involvement of business in policymaking, for instance as experts, varies according to the political salience of policy issues. For low-salience issues, typically complex and of little interest to voters, policymakers are more likely to rely on business expertise and are less constrained by public scrutiny, creating favorable conditions for business influence.Footnote 19 Although taxation is typically of public concern, the technical nature of fiscal policy complicates its salience. As the complexity of issues increases, policymakers may be more inclined to defer to business expertise, granting corporate actors greater discretion in shaping outcomes. In the Dutch context specifically, Culpepper further highlights how a small-country environment fosters close networks between political and business elites, reinforcing corporate involvement in policymaking.Footnote 20

Alternatively, Bell and Hindmoor (2014) challenge Culpepper’s view by emphasizing how business can actively shape the public perception of certain issues in its favor. In their study, business actors swayed public debate and political ideas by leveraging their structurally important position in the economy, thereby influencing subsequent political action. Structural power, from this perspective, is “inter-subjectively” constructed rather than a given.Footnote 21 This involves discursive practices through which actors shape ideas, interests, and beliefs around desirable courses of action.Footnote 22 The idea that structural power is not just “automatic” but actively used by corporate actors is also argued by Culpepper and Reinke (2014), who emphasize its strategic form. They show how corporate actors deliberately draw on their structural position in political activities, for example, by threatening disinvestment and relocation elsewhere.Footnote 23 While this involves direct interaction with policymakers, it differs from instrumental power, which consists of activities external to firms’ core economic role. Instead, actors rely on their structural importance in the economy.Footnote 24 Because of its focus on explicit bargaining and action, the strategic perspective is particularly valuable for historical research, as such behavior may leave traceable evidence in policy documents and correspondence.

While understanding the presence and nature of actions and strategies is important, identifying the effects of those activities is also key for determining whether business power and regulatory capture actually materialized. The impact of such actions can vary, as policymakers may resist corporate demands because of conflicting political aims or other pressures. Therefore, Bell and Hindmoor (2024) differentiate between power and influence to illustrate how corporate actors may act when their power is restrained. They define the latter as follows:

For our purposes, the key points are these. Power rests on the use of threats and offers (and throffers) to change the relative costs and benefits of particular courses of actions. Power, in this way, can be distinguished from non-coercive persuasion, what we are calling influence, where an actor genuinely believes and seeks to persuade another actor that there are good reasons why they ought to revise their understanding of a situation in the absence of any threats or offers. Such forms of non-coercive persuasion are a form of “cooperative exercise” in which one actor seeks to change how another person thinks and with this to “understand some aspect of the world or come to some agreement.”Footnote 25

The authors argue that, in some cases, corporate actors and policymakers recognize their mutual dependence and seek to maintain long-term relationships. Under such conditions, corporate actors may prefer “persuasive influence,” aligning their policy preferences with governmental goals, for example.Footnote 26 Where credible threats or strong leverage are unavailable to actors, softer tools of persuasion become more important.

Taken together, the theoretical framework has focused on identifying tools to empirically disentangle mechanisms of corporate power and influence. It has thus emphasized several approaches that account for business actively engaging with the policy process, either through instrumental, structural, or discursive capacities, to facilitate analysis of the TR1950 policy process. Process tracing provides the methodological tools for reconstructing and examining business-government interactions at different stages. Qualitative analysis of the process will allow for a nuanced assessment that treats business involvement not as an all-or-nothing phenomenon and accounts for a broader view of corporate political activity.

Postwar Business-Government Relations and Industrialization

Across Western Europe, the postwar period saw substantial changes in political and economic organization. Specifically, the role of the state within the economy expanded considerably.Footnote 27 This affected not only economic, but also fiscal policy. Tax rates, which had risen during the war, remained relatively high. Steinmo (2003) argues this coincided with the prevalence of Keynesian ideas, as tax was increasingly considered as a tool for economic management and steering investments.Footnote 28 As will be illustrated in the Dutch case, the postwar goals of economic reconstruction and industrialization clashed with the fiscal pressures on the private sector in several countries. Consequently, France, Italy, Belgium, Austria, Germany and the Netherlands all introduced some form of fiscal relief for business.Footnote 29 Daunton (2007) shows that, in Britain, organized industrial interests actively advocated for such measures.Footnote 30 While the state played a significant economic and fiscal role during postwar reconstruction, the business sector was by no means absent as a political actor.

Scholars frequently employ the framework of corporatism to understand business-government relationships and politics in postwar Europe. There exists a large body of political science scholarship debating the meaning of corporatism.Footnote 31 However, it is generally considered a form of interest representation, in which both capital and labor participate.Footnote 32 Schmitter (1974), in an effort to identify the patterns of political economic organization in post-war Western Europe,Footnote 33 defines it as follows:

Corporatism can be defined as a system of interest representation in which the constituent units are organised into a limited number of singular, compulsory, noncompetitive, hierarchically ordered and functionally differentiated categories, recognised or licensed (if not created) by the state and granted a deliberative representational monopoly within their respective categories in exchange for observing certain control on their selection of leaders and articulation of demands and supports.Footnote 34

Corporatism can be understood as a response to the expanding responsibilities of the state, as governments sought to integrate external interests and actors to enhance legitimacy and access information and expertise.Footnote 35 Scholars have also critically assessed the role of labor in these systems by emphasizing underlying class relations. Cawson and Saunders (2010) state that in corporatist-capitalist societies: “The state intervenes to safeguard and protect capital accumulation, but it must legitimate its intervention to both capital and labour.”Footnote 36 Additionally, Panitch (1980) finds that it is exactly the (capitalist) state’s predisposition to ensure capital accumulation which facilitates an unequal system of representation, favoring business and employer interests over labor.Footnote 37 As a result, the formal positions of interest groups may diverge from their actual roles in the system, which in turn may depend on national contexts.

Scholars have mapped the differences in postwar corporatist arrangements across different states. Katzenstein (1985) describes the Netherlands, Belgium, and Switzerland as liberal corporatist, reflecting their internationally oriented economies and a politically prominent business sector.Footnote 38 In the Netherlands, postwar corporatism (also known as neo-corporatism) evolved from wartime corporatist arrangements established during the Nazi occupation, which were subsequently adapted to the new political context. Heemskerk et al. (2021) show that, within this corporatist context, a dense network of business-government relationships emerged during the first two postwar decades and that business executives were extensively involved in policymaking through governmental committees, for example. The ties gradually weakened with the neoliberal transformation of the economy in the late twentieth century.Footnote 39 While these accounts provide valuable long-term and general insights into the close relationships between business and government within the context of corporatism, they offer less clarity on the effects of these ties on policy processes and outcomes.

More broadly, scholars link corporatist institutions to industrial and economic reconstruction policies, and even to economic growth.Footnote 40 Business historians have similarly studied post-war industrialization and growth, often through case studies, such as the automobile or steel industries, emphasizing factors including US aid and the relation to fascist economic organization.Footnote 41 Moving beyond sectoral explanations, Foreman-Peck (2014) analyzes national variety in post-war industrial policy and economic planning. Different trends can be detected among, for example, Germany, well-known for its steep postwar economic growth and generally considered more planning-averse and an advocate of free competition and markets, and countries such as the Netherlands, Belgium, and several Nordic countries, where industrial planning took an “indicative” form.Footnote 42 In turn, scholars associate indicative economic planning with corporatist organization, in which general or sectoral yet non-binding policy plans are formulated, reflecting the future economic aims or targets agreed upon by different interest groups.Footnote 43

In the Dutch context, recent studies illustrate how corporatist ideals, the orientation of industrial policy, and political ideology intersected in the immediate postwar years. The period from 1945 to 1950 was marked by three cabinet changes and competing economic ideas. Initially, economic policy was shaped by a Labour Party (PvdA) minister who favored extensive government intervention. From 1946 onwards, however, Catholic party (KVP) ministers chaired the Ministry of Economic Affairs and promoted a much more liberal outlook, thereby shifting the orientation of industrial policy planning.Footnote 44 Mellink (2021) explains how the Ministry’s Industrialisation Notes ( Industrialisatie Nota’s ), the leading policy agenda for industrialization, while part of a planned program, reflected this liberal orientation. These notes emphasized the central role of the private sector in industrial development and framed the government’s role primarily as facilitating favorable conditions for business activity. Key policy measures focused on deregulation, fostering investment, and international competitiveness of Dutch firms. Profit-restricting measures, including fiscal burdens, were considered detrimental to private initiative.Footnote 45 Mellink argues that by connecting these liberal aims to Christian and corporatist ideals, particularly through their emphasis on employment levels, these ideas aligned with ordo-liberal ideology.Footnote 46

Taken together, previous scholarship on postwar business-government relations and industrialization reveals the complexities of political environments and policies. On the one hand, the Netherlands had a system of interest representation involving labor, a growing economic role of the state, rising tax rates, and industrial plans. Conversely, business was tied to policymakers, and economic policies both emphasized and favored the role of business in industrialization. The TR1950 can be situated within these broader developments, illustrating how different ideals and governmental objectives were not always easily reconciled.

Historical Context and Case Study: TR1950

The TR1950 illustrates the intersection of fiscal and industrial policy in two main ways. Firstly, the industrialization policies emphasized that tax policies should foster a profitable and attractive investment climate.Footnote 47 Secondly, after the war, businesses struggled with capital scarcity. During the 1940s and 1950s, Dutch industry primarily relied on internal financing and struggled to attract external investors. This was further strained by fiscal burdens, and industrialists argued this impeded further industrial investments.Footnote 48 Meanwhile, the postwar expansion of the welfare state spurred the growth of institutional investors, such as pension and social funds and (life) insurance companies, prompting debate over their potential role in private sector financing. However, these institutions remained reluctant to invest, and their participation would only flourish decades later.Footnote 49 Thus, the fiscal burdens possibly limiting investments became a key issue for businesses and industrial development.

The taxes considered restrictive to internal financing primarily affected private income and profit. This was a relatively recent issue. Before World War II, the Netherlands did not have a corporate income tax; only a tax on dividends existed. Just before the 1940 invasion, parliament approved a new Profit Tax, which the German occupier later converted into a Corporate Tax ( vennootschapsbelasting ) in 1942 (but applicable retrospectively from 1941). In addition, a Corporate Wealth Tax ( vermogensbelasting ) and a Trade Tax ( ondernemingsbelasting ) were introduced.Footnote 50 The wartime tax system was not immediately reversed or modified after the war, leading to a significantly heavier tax burden on Dutch businesses.

Under Minister of Finance P. Lieftinck (1945–1952), the immediate postwar years saw attempts to rectify the monetary imbalances and outstanding tax payments through various intervening monetary procedures and two “special reconstruction taxes” on wealth.Footnote 51 These interventions, however, clashed with the necessary economic growth. Consequently, the Ministry introduced the Tax Revision 1947 (TR1947) to address the heavy fiscal pressures on a short-term basis. The TR1947 intended to foster economic activity, stimulate the business sector, and encourage savings. This revision, and the Minister’s emphasis on the benefits for business and investors, sided him with the more moderate branch of his party, which favored increasing liberalization.Footnote 52 However, the business sector was still not completely satisfied, and complained about the persisting fiscal burdens, emphasizing how these conflicted with the policy goals of industrialization and reconstruction.Footnote 53 These critiques fueled the debates leading up to the Tax Revision 1950.

Key components of the 1950 Tax Revision were the revised concept of profit (for taxable income), the accelerated depreciation and revaluation of assets, and new untaxed reserves, accompanied by the repeal of the Trade Tax.Footnote 54 The Trade Tax would be phased out gradually, compensated for by an increase in the Corporate Tax from 36 percent in 1949, when part of the Trade Tax was still in place, to 40 percent.Footnote 55 Although the final rate of this tax did increase, the revision included several fiscal alleviations for the tax on corporate profits. This was the result of a debate surrounding the current cost method ( Vervangingswaarde ) for fiscal reporting, which concerned the principles of tax deduction and depreciation for calculating taxable profit.Footnote 56 For business-economic and fiscal purposes, businesses were allowed to deduct certain costs, such as the costs or depreciation of material assets, resources and supplies, from their profits to create reserves for re-investment. The costs had always been calculated on the basis of historical costs, the price at which an asset had been purchased. However, in times of inflation, this method created a gap between the formed reserves and the contemporary prices of new assets. The current cost method proposed that material assets and supplies would be valued at current price levels. With rising prices, this would result in a larger depreciation, and thus lower taxable profits. The method would increase corporate reserves for reinvestment, protect against an inflated estimation of corporate profits, and result in fiscal advantages for taxpayers. After World War II, this debate was revived due to steep levels of inflation.Footnote 57

Ultimately, the proposal was shelved due to the conflicting perspectives on the implementation of the current cost method. Instead, other fiscal measures to support businesses and industrial development were adopted.Footnote 58 Nonetheless, the current cost debate was central to the development and outcome of the TR1950. In the end, the TR1950 included: accelerated depreciation, asset revaluation, a new type of tax-exempt reserve, and a broader definition of profit.Footnote 59 Furthermore, the Trade Tax was phased out and repealed. While not entirely adopted in the final revision, the current cost method was a key issue for the business representatives involved and did shape the TR1950 policy process.

Methodology and Sources

Establishing the influence of an actor on specific policy outcomes is a well-known methodological challenge. In response, scholars have developed various methodologies. Process-tracing (PT) is used by social and political scientists to identify influence and causal relationships. It analyzes the sequence of events in a policy process, the interventions of different actors, and how these factors shape the outcome, by drawing on qualitative analysis of empirical data.Footnote 60 While PT can serve various analytical purposes, it is often applied through in-depth case studies, thick description, and a sequential reconstruction of events that organize processes and intervening factors leading to a specific outcome.Footnote 61 It thus resembles the methodology often already used by historians.Footnote 62 Yet, PT allows for integrating theoretical explanations and systematic observations with case-specific elements, aiming to conclude “beyond the single case.”Footnote 63

In this study, PT methodology has inspired data collection and presentation. Firstly, to reconstruct the TR1950 policy process, archival data was collected, partly by working backwards from the revision outcome and piecing together empirical records of events and interactions that led to it.Footnote 64 The method also guided the selection of the business organizations and governmental agencies included in the analysis, by identifying those actors that were prominently involved in the policy process, whose archives could then be consulted in turn. The majority of documents on the TR1950 were located in the archives of the Ministries of Finance and Economic Affairs, complemented by the archives of business organizations, such as the Chambers of Commerce and corporatist groups. Sources from the Ministry of Finance primarily documented the fiscal policy process itself and debates on specific fiscal measures and revision drafts. Given the connection between the TR1950 and industrialization, these documents also involved correspondence with the Ministry of Economic Affairs and business organizations, which led me to these archives. The Ministry of Economic Affairs sources concerned the revision and fiscal measures in relation to industrial development, industrial policy more broadly, and included frequent contact with business associations. In addition, (historical) newspapers and government websites have been used to learn more about individuals, such as their affiliations and organizations.Footnote 65

The BIAs in this study were primarily larger sectoral organizations (industrial interest groups), employers’ organizations, and the regional Chambers of Commerce. These archives were consulted because of the BIA’s repeated involvement in the TR1950 policy process. Key documents included meeting minutes, in which government officials sometimes participated, drafts of policy advice, and correspondence with other BIAs or governmental agencies. These organizations usually framed their demands in the interests of business more generally or a specific industry or sector.Footnote 66 However, while these organizations aimed to represent beyond big business, it is unlikely that all types of firms were equally represented. It may well be that the interests of prominent companies and representatives, or large contributors, for example, were weighted more heavily or better represented on boards and councils. Similarly, the individual business representatives were employed by larger and more prominent Dutch businesses and industries, and there was no direct representation of small and local firms. The term business thus likely does not represent all types of businesses in the case of the policy process. While certain fiscal measures, such as lower fiscal burdens, may expect broader support in the corporate community, organizations and participants often did not directly represent specific sectors or small firms. In short, representation among firms and industries in the policy process was uneven.

PT also informed the structure and presentation of the empirical analysis. The policy process is structured sequentially by outlining key stages, the actors involved, their preferences, and the actions undertaken. When determining whether certain actors impacted policies or subsequent steps in the policy process, evidence is drawn directly from archival material.Footnote 67 Thus, I am staying close to the content of the sources when identifying impact. Dür (2008) states that PT and strong reliance on available data may cause an underestimation of the influence of specific groups (when not referred to in the sources or due to behind-closed-doors activities), and relies on the statements of policymakers themselves, who (sub)consciously may be circumventing specific factors.Footnote 68 While this risk exists, especially in archivally driven historical research, I have aimed to limit it by combining documentation from different governmental agencies and external organizations to incorporate a variety of perspectives. Also, the theoretical framework provides tools for critically assessing the interactions in the process. In doing so, this study aims to provide a comprehensive account of the TR1950 policy process and the intervening actors and factors that contributed to its outcome.

TR1950: Business-Government Networks

The TR1950 policy process demonstrated the close ties between politics and business in the Netherlands. Business was involved in the process in three main ways: through corporatist organizations, individual business representative-government contact, and as experts in government or business committees. Between 1945 and 1950, the corporatist organizations were remnants of those created under wartime Nazi occupation. During the war, business and industry had been hierarchically organized (also known as Organisatie Woltersom). Six Main Groups (or Hoofdgroepen )—industry, trade, transport, craft, insurance, and banking—oversaw and represented sector-specific corporate subgroups.Footnote 69 The wartime organization remained active until 1950, when the government revised the system.Footnote 70 Within the TR1950 policy process, especially the Main Group Industry ( Hoofdgroep Industrie , hereafter HI) played an active role.Footnote 71

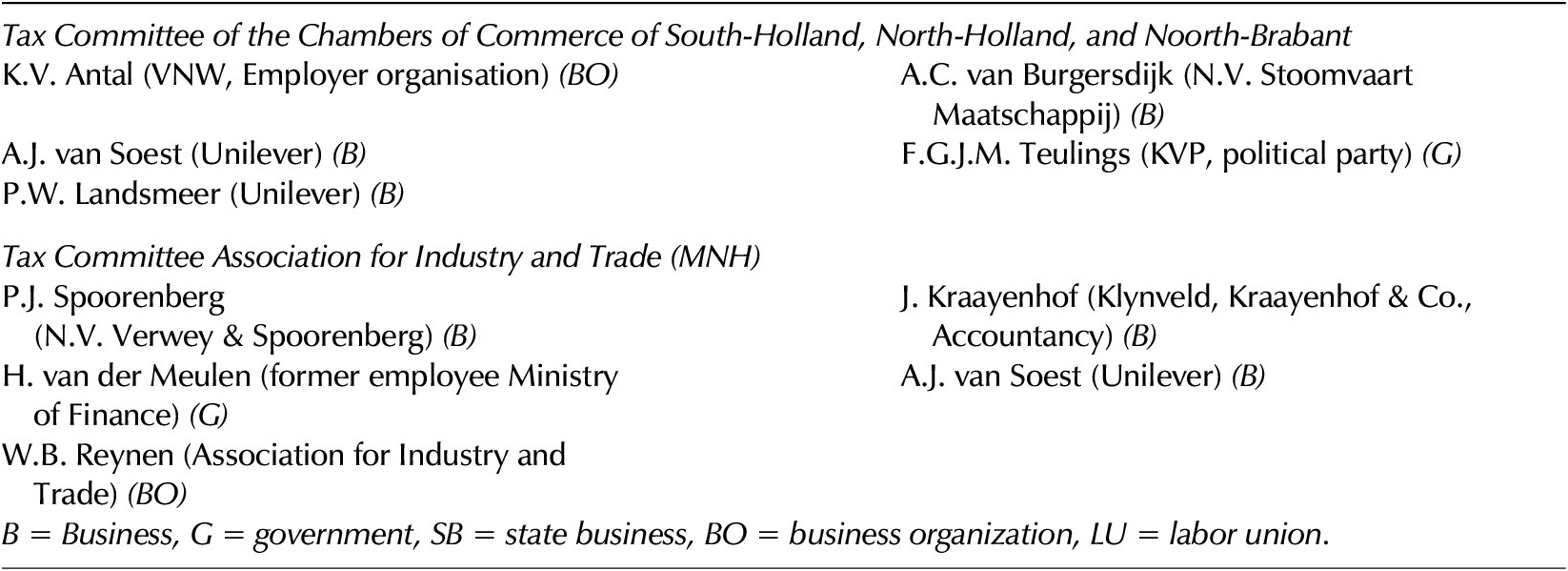

Business representatives participated in the TR1950 policy process by serving on BIA fiscal committees (Table 1). In the Netherlands, business interests were also represented through Chambers of Commerce. The Chambers represented local and provincial commercial interests and were well-connected to businesses in their respective regions. The provincial Chambers of Commerce (CoC) of North-Holland, South-Holland, and North-Brabant established a combined fiscal committee and published various reports expressing their recommendations and critiques of tax policy proposals.Footnote 72 While the Chambers also represented regional and smaller businesses, members included larger and international businesses located in the area, such as Unilever N.V. in Rotterdam (South-Holland), as well. Additionally, the Association for Industry and Trade ( Maatschappij voor Nijverheid en Handel , MNH) established a committee. The MNH was an economic research organization, but also represented and lobbied for business interests.Footnote 73 This committee was created at the request of Minister Lieftinck, who asked the MNH to study the current cost method.

Business organization committees engaged with the Tax Revision 1950 a

Table 1. Long description

The table is divided into two main sections based on committee names.

Section 1: Tax Committee of the Chambers of Commerce of South-Holland, North-Holland, and North-Brabant.

* K. V. Antal (V N W, Employer organisation) (B O)

* A. C. van Burgersdijk (N. V. Stoomvaart Maatschappij) (B)

* A. J. van Soest (Unilever) (B)

* F. G. J. M. Teulings (K V P, political party) (G)

* P. W. Landsmeer (Unilever) (B)

Section 2: Tax Committee Association for Industry and Trade (M N H).

* P. J. Spoorenberg (N. V. Verwey and Spoorenberg) (B)

* J. Kraayenhof (Klynveld, Kraayenhof and Co., Accountancy) (B)

* H. van der Meulen (former employee Ministry of Finance) (G)

* A. J. van Soest (Unilever) (B)

* W. B. Reynen (Association for Industry and Trade) (B O)

A legend at the bottom defines the abbreviations: B equals Business, G equals government, S B equals state business, B O equals business organization, and L U equals labor union.

a Documents pertaining to participants and their employment: Letter MNH to Minister of Finance, 1948, NL-HaNA, Finance / Taxes, 2.08.69, inv.no. 290; CoC list of AFCA participants and correspondence, 1950, NL-HaNA, CoC Rotterdam / Secretariat, 3.17.17.04, inv.no. 1536; CoC Fiscal Committee, Correspondence and meetings, 1948, NL-HaNA, CoC Rotterdam / Secretariat, 3.17.17.04, inv.no. 1554; Additional literature used for identifying employment of participants: Van Beurden and Jonker, “A Perfect Symbiosis,” 74; Bogaarts, De periode van het Kabinet-Beel, Band B, 830; Boer, “NTFR 2014/1954 - 50 jaar Belastingrecht in Leiden!”.

In both committees, business representatives accounted for nearly all participants. The only non-business member was the politician F.G.J.M. Teulings (KVP). He was a member of the Senate and later became Minister of Domestic Affairs (1949–1952).Footnote 74 Teulings left the committee upon becoming minister but rejoined after his term.Footnote 75 He worked closely with A.J. Van Soest (Unilever) in establishing the CoC committee and outlining its goals. Van Soest also served on the MNH committee, thereby connecting the two committees.Footnote 76 These BIAs mainly held an advisory role in the policy process, by communicating and lobbying for their preferred outcomes. They occupied a less central role in the policy process than the government committees.

Yet, business representatives also served on these government committees as experts. As Table 2 illustrates, the majority of these participants were government employees and state business representatives. In the Netherlands, state businesses did not necessarily function as an extension of the government and were typically managed as private companies with relatively little government interference.Footnote 77 In each of the three governmentally issued committees, several business representatives participated. Again, either an individual or an organisation was represented in multiple committees, strengthening the interconnectedness of the TR1950 network.

Governmentally initiated committees engaged with the Tax Revision 1950 a

Table 2. Long description

The table is divided into three sections based on committee name.

1. The Advisory Committee for Fiscal Affairs (A F C A), Ministry of Finance:

- P.J. Oud (V V D, liberal political party) (G) and H.J. Hofstra (S D A P / P V D A, social-democratic political party) (G).

- H. Albarda (Nederlandse Handelsmaatschappij, bank) (B) and W.H. van den Berge (Ministry of Finance) (G).

- M.W. Holtrop (The Dutch National Bank) (S B) and W.F. Lichtenauer (Chamber of Commerce Rotterdam) (B O).

- C.A. Takken (Ministry of Finance) (G) and E. Tekenbroek (Accountant) (B).

- M.J.H. Smeets (Ministry of Finance) (G) and P. Kuin (Unilever) (B).

- E.D.M. Koning (Van Doorne’s Aanhangwagenfabriek) (B) and M.J. Prinsen (Ministry of Domestic Affairs) (G).

- B. Schendstok (Ministry of Finance) (G) and Tj. S. Visser (Ministry of Finance) (G).

- J. Takken (Ministry of Finance) (G) and D.J. Muller (Ministry of Finance) (G).

2. Committee Mey (dedicated to studying the topic for state businesses), Ministry of Economic Affairs:

- A. Mey (Ministry of Finance) (G) and P. Schierbeek (Ministry of Economic Affairs) (G).

- H. Reinoud (P. T. T. National Postal, Telegraph, and Telephone Service) (S B) and P.J. van Acker (Ministry of Domestic Affairs) (G).

- J.G. de Weger (Ministry of Finance) (G) and L.G. Wansink (Ministry of Economic Affairs) (G).

- A. Hugas (P. T. T. National Postal, Telegraph, and Telephone Service) (S B) and B.P.A. Schregel (Ministry of Domestic Affairs) (G).

3. Committee Financial Affairs, Department of Industrialisation, Ministry of Economic Affairs:

- B. Schendstok (Ministry of Finance) (G) and J. Tinbergen (Central Planning Bureau) (G).

- E. Gorter (H. ten Cate Hzn. and Co.) (B) and J.A. Middelhuis (Catholic Labour Movement) (L U).

- J.F. Posthuma (Herstelbank) (G) and H.L. Woltersom (Bank of Rotterdam) (B).

A legend at the bottom defines the codes: B equals Business, G equals Government, S B equals state business, B O equals business organization, and L U equals labor union.

a Some of these committees, such as the Committee Financial Affairs (DGI), would exist for a longer period of time, also after the TR1950, and therefore its membership would change over the years. The committee mentioned is based on its earliest 1949 memberlist. Membership as displayed in Tables 1 and 2 shows membership as before the creation of the TR1950. AFCA members and employment: AFCA memberlist, 1948/1949, NL-HaNA, CoC Rotterdam / Secretariat, 3.17.17.04, inv.no. 1534; NL-HaNA, DNB: archief van president Dr. Marius Wilhelm Holtrop, 2.25.69.13, inv.nr. 18382; DGI committee: Ministry of Economic Affairs, Appointment, November 1949, NL-HaNA, EA / Central Archive, 2.06.087, inv.no. 872; Committee Mey: Ministries of Finance, Economic Affairs, Transport, and Domestic Affairs, Appointment, 7.10.1948, NL-HaNA, BiZa / Gen. Secretariat and Compatibility, 2.04.50, inv.no. 420; Parlement.com, “Mr. P.J. (Pieter) Oud,”; “Mr E. D. M. Koning overleden,” NRC.

The Ministry of Finance tasked two committees with the study of the current cost method. The Ministry was finally responsible for fiscal policy and thus the decisive department regarding the TR1950. However, it continuously cooperated with and was advised by other governmental departments (the Ministry of Economic Affairs) and external interest groups, such as the MNH. Firstly, the Committee Mey studied state business financing and, more specifically, the current cost method for financial reporting. The committee’s members came from the Ministries of Finance, Economics, and Domestic Affairs, as well as state companies, such as the state postal company P.T.T. and the Dutch State Mines (DSM).Footnote 78 The committee’s stance toward current cost depreciation for financial reporting was rather positive, but it was not much engaged with the fiscal aspect of the question.Footnote 79 As such, it did not end up having a major role in the TR1950 policy process.

Secondly, the Advisory Committee for Fiscal Affairs (AFCA) played a key role in the actual formulation of the TR1950. This committee was housed in the Ministry of Finance, specifically tasked with studying fiscal issues and current cost depreciation. While most members of this committee were employees of the Ministry or politicians, some members originated from the business sector. P.J. Oud, co-founder of the liberal party (VVD) and former Minister of Finance (1933–1937), chaired the committee, and Labour Party’s H.J. Hofstra was its secretary.Footnote 80 Business sector representatives included W.F. Lichtenauer, secretary of the Chamber of Commerce in Rotterdam (South-Holland) and in frequent contact with the CoC Tax Committee, and P. Kuin, who as Secretary-General at the Department of Industry and Trade (Ministry of Economic Affairs) had cooperated frequently with the HI, but was subsequently employed as economic advisor at Unilever.Footnote 81 Several participants were fiscal experts and scholars, such as B. Schendstok, M.J.H. Smeets, who were also government employees, and E. Tekenbroek. These experts often held individual perspectives on economic and fiscal issues and occupied different positions in these debates. Generally, these scholars considered the fiscal pressures facing industrialization problematic but also held a critical stance toward current costs.Footnote 82 Several Ministry of Finance officials (Tj. S. Visser, J. Takken, and D.J. Muller) were not part of the standard committee but offered additional insights on the question of fiscal alleviations.Footnote 83 The committee integrated the interests of the business sector, but combined this with Ministry of Finance perspectives and policy aims. Its position within the Ministry and fiscal focus made it a key component of the policy process.

The Ministry of Economic Affairs took part in the development of the TR1950 and became involved in the process because of the repercussions for the economy and industrial development. It was thus involved with, but not directly responsible for, fiscal policymaking. The department participated in Ministry of Finance debates and committees, provided information on the topic, and advocated certain policy routes. Its stance was often very close to that of the business sector, with which the department cultivated a strong relationship. Hen (1980) even argues that it operated as “a department of business” from the interwar period onwards.Footnote 84 After the war, government officials were recruited from the business sector, and business representatives were involved in industrial policymaking. The Ministry’s Directorate General for Industrialisation (DGI) established industrial advisory committees in which the business sector, employer organizations, and labor unions were represented.Footnote 85 One of the DGI committees focused on financial and fiscal issues: the Committee for Financial Affairs. Business representatives participated in this committee, and through its participants, it was also connected to the Ministry of Finance and the AFCA. The committee was only created in 1949, rather late in the TR1950 policy process.Footnote 86

Most of the business-government interactions concerning the TR1950 happened within the Ministries of Economic Affairs and Finance. BIAs approached both departments but often found stronger support within the former. While the Ministry of Finance was the leading authority on fiscal and financial issues, Economic Affairs officials tended to support and communicate BIA views to the Ministry of Finance, providing an additional source of pressure. In turn, business representatives claimed various formal positions in the policy process. Additionally, as individuals participated in multiple committees or shared affiliations, an integrated network of interest groups and representatives was established. However, these “formal” roles may not illustrate the entirety of the network. Informal networks spanned much further, through social engagements or former employment. Individuals would more often alternate between private and public sectors or take on roles at multiple organizations simultaneously. While an account of these formal roles provides no indication of the content of the interactions or impact, the extensive involvement of business representatives illustrated the governmental preference for cooperation and close ties with the business community.

The Tax Revision Policy Process

The TR1950 policy process had its roots in the earlier tax debates and the TR1947. The TR1947 had been intended as a short-term measure offering temporary relief rather than permanent solutions. Further revisions were thus anticipated, though their content remained a matter of debate and would be partly shaped by business sector involvement. It had also become clear that postwar fiscal burdens weighed heavily on the business sector. Business representatives built on these premises in the initial phase of the TR1950 policy process.

BIAs played a central role in the early stage of the policy process by redirecting the policy debate and introducing the issue of current costs. The HI emerged as a particularly important actor, voicing strong criticism of the TR1947 and postwar wealth taxes.Footnote 87 It addressed the combined politics of price controls, imposed to prevent inflation, and high fiscal pressures, which were considered to undermine investment and industrial expansion. Consequently, member industrialists had proposed the current cost method as the solution.Footnote 88 To disseminate this idea, officials from the Ministry of Economic Affairs were invited to HI meetings, where the current cost method was discussed as a fiscal instrument for industrial development.Footnote 89 These discussions also moved internal ministerial debates. In 1947, after discussing the topic with the HI, the Director-General of Prices (Ministry of Economic Affairs) wrote to the Minister of Finance: “Perhaps it would be possible to meet the fiscal wishes of the business sector, by basing the depreciations for profit determination on current costs.”Footnote 90 In this early phase, BIAs relied on their corporatist connections and close governmental ties to diffuse ideas and alter policy debates.

To further increase political pressure, the HI coordinated with several employers’ organizations (VNW, AKWV, and VPCW).Footnote 91 In May 1948, these BIAs jointly addressed a letter to the Ministries of Finance and Economic Affairs, arguing that the economic climate and tax system restricted private investments and hindered business development. The letter presented the current cost method as an economic necessity and a tool for industrial development. In addition, the address strategically used a comparison with Belgian fiscal measures. The tax revision process unfolded as the first steps toward European integration were being taken, particularly among the Benelux countries (Belgium, the Netherlands, and Luxembourg). According to the BIAs, Belgium had introduced fiscal alleviations for businesses, raising concerns about the international competitiveness of Dutch firms.Footnote 92 The context of European integration was thus used as leverage. The BIAs’ address was further supported by another inflation-focused lobby group ( Stichting tot Daadwerkelijke Bestrijding van het Inflatiegevaar ), which also emphasized the detrimental effects of fiscal burdens on business and the economy.Footnote 93 This organization had been established by representatives of employer organizations, industry, banks, and institutional investors to address inflation and financial policies.Footnote 94 Cooperatively and separately, BIAs linked the current cost method to key economic concerns, generating extensive debates among policymakers.

The BIAs were particularly impactful within the Ministry of Economic Affairs. Their address became a key point of reference, frequently cited by officials and various TR1950 committees. The link with industrial development, as well as the issue of Belgian alleviations and international competitiveness, resonated with ministerial priorities. As a result, current costs became a central topic within the Ministry, which actively asserted its position and communicated its views to the Ministry of Finance. The Directorate General of Industry and Trade (Ministry of Economic Affairs) even stated “that the request of the industry deserves support.”Footnote 95 The significance of these BIAs in the policy process is further confirmed by a 1982 Ministry of Economic Affairs report on post-war industrialization. It acknowledged the involvement of the BIAs and their push for the current cost method in deciding the direction of the policy process, leading to governmental studies on the method.Footnote 96 These interactions illustrate two important modes of intervention by corporate actors. First, while another tax revision was anticipated, BIAs were important in embedding the issue of current cost within the TR1950 policy process and aligning it strategically to ministerial goals. This intervention relied on reframing and constructing a specific argument: fiscal relief was presented not just as a corporate interest, but as a condition for economic recovery and industrial expansion. This constituted a turning point in the policy process, as it shaped governmental discourse and the premises of subsequent proposals and policy actions. Second, by aligning the narrative with concerns of the Ministry of Economic Affairs, BIAs effectively mobilized the department as an additional factor of pressure, turning it into an ally of business interests.

The impact of the BIAs on the Ministry of Economic Affairs illustrated corporate strategic-structural and discursive capacity. The Ministry’s policy goals centered around industrialization and economic reconstruction, and BIAs capitalized on this by framing the current cost method as essential to expanding industrial activity. Rather than relying solely on their access and connections, their argument drew on the structurally important role of industry and business in the economy, specifically during reconstruction. In doing so, they contributed to the “inter-subjective construction” of ministerial beliefs by emphasizing the detrimental effects of fiscal burdens and the positive impact of current costs on industrialization.Footnote 97 By framing fiscal relief as a necessity for industrial development and recovery, BIAs made it difficult for policymakers to ignore their position. This is reflected in the frequent references to their addresses in subsequent policy debates and proposals, not only within the Ministry of Economic Affairs but also within the Ministry of Finance.

The Ministry of Finance’s responses to the issue varied. Officials had raised budgetary and practical concerns about the current cost depreciation.Footnote 98 At the same time, correspondence between the minister and a vice-chairman of Unilever N.V. (the Dutch parent company) suggested the Minister had privately expressed support for the method, considering it important for industrial development.Footnote 99 BIA activities also had tangible effects within the Ministry. Following the BIAs’ addresses, the Minister tasked the AFCA committee and the MNH, an external BIA, with studying current cost depreciation.Footnote 100 Overall, the BIAs thus exerted varying degrees of impact across different governmental departments, reflecting differences in how successfully their arguments aligned with departmental policy goals. While attitudes within the Ministry of Finance remained more reserved than the enthusiasm and collaborative spirit of the Ministry of Economic Affairs, current cost nonetheless became a central theme following BIA engagement.

Subsequently, various committees published their proposals for the revision. Several of these proposals reflected the Ministry of Finance’s hesitancy regarding current cost depreciation, seeking to accommodate this. Firstly, the Chambers of Commerce, in earlier critiques of postwar tax burdens, had raised the matter of current costs.Footnote

101 However, as the TR1950 approached, the CoC’s Fiscal Committee also acknowledged the practical challenges of this method as outlined by the Minister of Finance.Footnote

102 Secondly, the AFCA’s proposals were formulated in direct response to the earlier BIA addresses, and it agreed with the need for fiscal alleviations for depreciation. However, it addressed that the current cost method could not be applied in its entirety, due to practical issues and theoretical disagreement. Instead, it proposed a moderated method of depreciation, and in doing so, aligned with the views of Ministry of Finance officials.Footnote

103 It suggested the revaluation of pre-1940 assets at 1

$ \frac{2}{3} $

times their value, and an accelerated depreciation of assets acquired post-1946, enabling the depreciation of larger sums over a shorter period of time. Lastly, the MNH expressed the urgency of “the problem of fiscal depreciation of fixed assets due to increased prices for business,” yet recognized that far-reaching changes like the current cost method were not feasible in the short term. Therefore, it proposed revaluing fixed assets for fiscal depreciation by a factor of two to counteract the “abnormal” inflation resulting from the war. The Ministry’s final proposals incorporated elements of both the ACFA and MNH.Footnote

104

$ \frac{2}{3} $

times their value, and an accelerated depreciation of assets acquired post-1946, enabling the depreciation of larger sums over a shorter period of time. Lastly, the MNH expressed the urgency of “the problem of fiscal depreciation of fixed assets due to increased prices for business,” yet recognized that far-reaching changes like the current cost method were not feasible in the short term. Therefore, it proposed revaluing fixed assets for fiscal depreciation by a factor of two to counteract the “abnormal” inflation resulting from the war. The Ministry’s final proposals incorporated elements of both the ACFA and MNH.Footnote

104

Finally, the Ministry of Finance TR1950 plans adopted several aspects of these mediated proposals, particularly regarding accelerated depreciation and revaluation. The accelerated depreciation of recently acquired assets was acknowledged as a “notable alleviation in terms of profit” in the short term, but also as a future postponement rather than elimination of fiscal burdens.Footnote 105 This measure, first limited to 1952, would be extended to the late 1950s.Footnote 106 Secondly, the revaluation of assets was considered “a real loss for the fiscal administration.”Footnote 107 Following the MNH proposal, the revision included a revaluation by a factor of two for assets acquired before 1942, though certain fixed assets, such as buildings, were excluded from the measure.Footnote 108 While current cost depreciation was not adopted, these measures were grounded in similar concerns and principles. The committees’ suggestions comprised less invasive measures than the methods earlier advocated for by the BIAs. Instead, they accommodated policymakers’ concerns and hesitations while still achieving a degree of fiscal relief. These efforts correspond with Bell and Hindmoor’s idea of persuasive influence: where actors resort to softer methods of persuasion, taking into account governmental aims, responsibilities, and public interests to convey certain ideas, rather than relying on offers or threats.Footnote 109 Similarly, the BIAs’ early-stage push for current costs relied on similar mechanisms of persuasion. By aligning their narrative with policy aims, business was able to redirect policy debates.

Furthermore, the revision introduced a broader concept of profit through the principle of good merchant’s practice ( goed koopmansgebruik , GKG). Although the term had a longer fiscal history, the TR1950 formerly anchored profit determination in GKG, allowing greater flexibility in determining profit, provided consistent principles were applied in line with the law.Footnote 110 The narrative surrounding GKG also emphasized its role in facilitating investment and business activity. The Ministry of Economic Affairs discussed it as favorable for business activity shortly after the war.Footnote 111 Additionally, the Committee for Financial Affairs (DGI) also recommended GKG for industrial development.Footnote 112 This measure aimed to give businesses greater freedom and the ability to adapt to economic and societal challenges.Footnote 113 This illustrates how deeply the link between fiscal accommodation and industrialization was embedded in the TR1950.

Nevertheless, the final TR1950 formulation left business organizations and government employees (particularly those in the Ministry of Economic Affairs) dissatisfied, as their demands had not been fully adopted. Therefore, attention was shifted to another component of the tax system: the Trade Tax. The tax, and its German and wartime origins, had been critiqued by the business community as well as several politicians. Labour Party’s Hofstra (member of the ACFA) had infamously argued in 1946: “in today’s Dutch tax system, there is no place for the Trade Tax.”Footnote 114 Although Hofstra later defended the tax during the TR1950 process, BIAs had strategically used this statement in their arguments against the tax. Again, they were supported by officials in the Ministry of Economic Affairs, who drafted various proposals suggesting the repeal of the Trade Tax, and even the Corporate Tax entirely—a more radical proposal than any of the business organizations and representatives had made.Footnote 115 Yet, eventually, the departments, in cooperation with the Ministry of Finance, created a much less radical plan that included phasing out the Trade Tax.Footnote 116

This issue became a matter of political conflict. Several Liberal and Catholic politicians who had opposed the tax were praised by the Chamber of Commerce.Footnote 117 One of its critics had been Teulings, a politician and a previous member of the CoCs Tax Committee.Footnote 118 The matter was also supported by Minister Lieftinck, though opposed by fellow party members, such as Hofstra. The Minister’s decision-making was also driven by the role of fiscal policy in fostering investments and industrialization and, subsequently, employment. Ultimately, the Trade Tax was repealed.Footnote 119

One of the key industrial plans would acknowledge the TR1950 as: “a step in the direction of encouraging the in this moment necessary private investment activity.”Footnote 120 While determining the full extent of corporate influence on a policy outcome may be difficult, the following can be established. Business was directly involved in the policy process through committee participation and BIA advocacy, promoting fiscal alleviations and disseminating information and ideas. This engagement steered government debates, prompted the commissioning of studies, and introduced a narrative linking fiscal relief and current cost depreciation to industrial development, which ultimately determined the course of the TR1950 policy process.

Conclusion

This study has analyzed the involvement of corporate actors in tax policymaking by drawing on perspectives from business power scholarship. Historians have not yet widely applied theories of business power to study tax policy. These frameworks offer a valuable lens for examining the relationship between the state and business in fiscal bargaining, which can be tied to broader tensions over the state’s fiscal base and its ability to engage in economic management during reconstruction and over time. The core focus of the study, however, has been to clarify the different roles of actors in tax policymaking and the effects of their activities and interactions through a detailed reconstruction of the TR1950 policy process. Dissecting the policy process in this way demonstrates the value of engaging with the intricacies of tax policy, and of looking beyond aggregate outcomes such as the final tax rate. Corporate actors concerned themselves with detailed and technical aspects of tax policy. Similar debates over these intricacies and the alignment of economic and tax policy did not just happen in the Netherlands. Throughout Europe, policymakers and the business community faced similar struggles.

The case study examined here is not an illustration of the absolute power of business. Rather, it demonstrates the nuances of business-government interactions when direct exertion of power is constrained. By combining perspectives on business power with historical insights, the key contributions of this study lie in identifying the mechanisms and strategies used by business actors to intervene in the policy process, with particular attention to the intersection of fiscal and economic policy.

Business intervened in the TR1950 policy process in several distinct ways. Corporate actors in the Netherlands were able to draw on their close ties to policymakers and corporatist institutions and were integrated into the policy process through participation on committees. The importance of such close-knit business-government environments has been identified by scholars of European tax havens, albeit on even smaller-country scales (e.g. Luxembourg). Consequently, as an interest group, the corporate sector was strongly represented in the TR1950 policy process. Such extensive participation can reflect instrumental capacity but may equally arise from the business’s perceived structural importance in the economy and society. Moreover, involvement across different stages of the policy process also resulted in business actors assuming different roles at different moments. Early BIA addresses advocated for more ambitious and far-reaching measures, notably the current cost method, than the mediated proposals subsequently put forward by public-private committees operating within or closer to government departments. The more extreme positions staked out early in the process established the outer boundaries of the debate, while the more moderate actors worked within those boundaries to secure what was achievable.

The most consequential mode of intervention, however, involved the embedding of fiscal demands within broader economic concerns, thereby constructing a convincing narrative. Early in the policy process, corporate actors promoted fiscal relief as an economic necessity for industrial development. Tying together fiscal and economic policy in the context of postwar reconstruction made their efforts difficult to ignore. As a result, they shaped subsequent policy debates and determined their terms. This went beyond the expression of corporate interests. It contributed to the construction of an argument that became deeply embedded in the policy process, influenced courses of action, and was adopted and reproduced by government officials themselves. The narrative created relied on the structurally important position of business in the economy and for industrial development, but through the incorporation of governmental concerns and responsibilities also reflected dynamics of influence and persuasion.

Crucially, it also exposed intra-governmental tensions over the relationship between fiscal and economic policy. This produced an unevenness in terms of business-government relations, as corporate efforts proved more effective within the Ministry of Economic Affairs, whose reconstruction aims aligned with the narrative of the BIAs, than within the more cautious Ministry of Finance. This finding underlines a broader point: just as the business community is not a monolithic actor, neither is the state. Corporate power and influence may vary across government departments, further complicating ideas about business-government interactions.

Open access

Open access