1. Introduction

NHS funded cataract surgery in England has seen a rapid and largely unplanned expansion of provision by private, largely for-profit hospitals and clinics (termed independent sector providers or ISPs in this paper). Since 2019, a combination of factors including ‘any qualified provider’ (AQP) rules promoting competition and patient choice, growing demand, long NHS waiting lists, capacity constraints, and low barriers to market entry, have contributed to a dramatic rise in cataract surgery delivered by independent sector providers (ISPs). Between 2018/19 and 2023/24, the total number of NHS-funded cataract surgeries rose from almost 417,000 to about 650,000 annually and the ISP share increased from 22 per cent to 57 per cent. During this period ISP-delivered procedures quadrupled while NHS provision declined.

The rapid growth of NHS-funded cataract surgery performed in the independent sector offers a valuable opportunity to examine the processes, impacts, and consequences of increased independent sector involvement in publicly funded healthcare. The objective of this study is to examine the growth of ISPs delivering NHS-funded cataract surgery in England, and to explore its causes and consequences. The study contributes to the literature by providing insights into how healthcare commissioning and market-based reforms influence independent sector and NHS provision within publicly funded health systems, with implications for policy in the UK and internationally. The paper is structured around four core areas: the nature and causes of changes in the cataract surgery market; arrangements for commissioning, contracting and clinical coding; effects on patient choice, waiting times and referral pathways; and issues of quality, productivity, and productivity. These findings are considered in light of existing literature, with policy implications drawn for other specialties, as well as for international health systems facing similar pressures.

2. Background

For at least three decades, successive governments in England (and the other countries of the UK) have sought to address continuing problems with access to and waiting lists for elective surgery (Kreindler, Reference Kreindler2010; Sheard, Reference Sheard2018; Siciliani and Hurst, Reference Siciliani and Hurst2005). Long waiting lists and waiting times have been a perennial source of political and electoral pressure for healthcare reform, and a key determinant of overall public satisfaction with the National Health Service (NHS). During the 2000s, the then Labour government succeeded in driving down waiting times to a point where median waits for elective care were below five weeks and over 90 per cent of non-urgent patients waited less than 18 weeks from referral to start of treatment (Pope, Reference Pope2023). But waiting lists for elective surgery grew steadily during the 2010s in a period of sustained financial austerity for public services, with several successive years of low growth in NHS spending, and then accelerated during and after the disruption to elective care caused by the COVID19 pandemic in 2020–21 (Blythe and Ross, Reference Blythe and Ross2022; Warner and Zarenko, Reference Warner and Zarenko2024). Currently, there are a record 7.4 million cases on NHS waiting lists in England, the median wait time is 14 weeks, and around 3 million of these cases have been waiting longer than 18 weeks (BMA, 2025).

Governments have used two main policy approaches to seek to reducing waiting times and waiting lists: strategies aimed at increasing activity and productivity in traditional, NHS providers (NHS trusts); and approaches designed to encourage the growth of capacity and activity by non-NHS providers (private, mostly for-profit providers, which we refer to as ISPs) (Bachelet et al., Reference Bachelet, Goyenechea and Carrasco2019; Blythe and Ross, Reference Blythe and Ross2022; Kreindler, Reference Kreindler2010). In both the NHS and the independent sector, governments have sought to use markets, competition and financial incentives to drive provider behaviours (Gaynor et al., Reference Gaynor, Moreno-Serra and Propper2012; Gilbert et al., Reference Gilbert, Clarke and Leaver2014). For example, governments in England have introduced activity-based funding for elective care and extended it to both the NHS and the independent sector (Sussex and Farrar, Reference Sussex and Farrar2009); funded a succession of waiting list initiatives and dedicated funding streams for increased elective activity (Blythe and Ross, Reference Blythe and Ross2022); set demanding waiting list and waiting time targets (Dimakou et al., Reference Dimakou, Parkin, Devlin and Appleby2009); funded the creation of new independent sector treatment centres (Turner et al., Reference Turner, Allen, Bartlett and Pérotin2011) and NHS high volume low complexity surgical hubs (Scantlebury et al., Reference Scantlebury, Sivey, Anteneh, Ayres, Bloor, Castelli, Castro-Avila, Davies, Davies, Glerum-Brooks, Gutacker, Lampard, Rangan, Saad, Street, Wen and Adamson2024); introduced statutory rights for patients to exercise choice and to use non-NHS providers when waiting times are exceeded (Appleby and Dixon, Reference Appleby and Dixon2004); promoted increased productivity through various collaboratives and national improvement teams (Atkins et al., Reference Atkins, Birmpili, Glidewell, Li, Johal, Waton, Boyle, Pherwani, Chetter and Cromwell2023); and made it easier for new providers to enter the NHS market through ‘any qualified provider’ contracting rules (Blythe and Ross, Reference Blythe and Ross2022).

These policies remain highly contested. Supporters argue they have increased access, activity, and productivity, while critics raise concerns about overprovision, equity, and quality. Critics argue that greater ISP involvement can undermine the sustainability of NHS services, encourage patient selection by providers (cream-skimming), and prioritise profit over public interest (Holmes, Reference Holmes2023). Some object to for-profit provision in principle, seeing it as part of a broader agenda to privatise the NHS (Roderick and Pollock, Reference Roderick and Pollock2022).

2.1. Institutional background

Cataracts are usually identified during routine sight tests in community optometry, with patients now referred directly to ophthalmology following the national introduction of direct referral pathways in England (NHS England, 2023a). Previously, community optometrists referred patients to their GP, who then referred them to a local NHS ophthalmology department. The updated pathway enables optometrists to refer straight to ophthalmology providers, offering patients a choice of providers at the point of referral (NHS England, 2023c). National and professional guidance emphasises that access to cataract surgery should be based on clinical need and patient-reported visual function rather than fixed visual acuity thresholds, with a focus on the impact of cataracts on quality of life (NICE, 2017; The Royal College of Ophthalmologists, 2007). After assessment, eligible patients are listed for surgery, which is typically delivered as a high-volume elective procedure in NHS or ISPs.

Commissioning responsibility in England sits with 42 Integrated Care Boards (ICBs), which are the statutory bodies responsible for commissioning and contracting for most NHS-funded healthcare services, although some specialised services are still dealt with directly by NHS England (NHS England, 2023b). Cataract surgery has traditionally been funded through national tariff–based activity payments, though block and blended contracts are also used in response to financial pressures and waiting list management (Bell, Reference Bell, Charlesworth and Lewis2021). In recent years, NHS England has funded several ICBs to establish optometry-led single points of access (SPoA) for ophthalmology referrals (NHS England and NHS Improvement, 2022). While models vary locally, SPoAs are intended to route all referrals through a central triage service, from which patients may be referred to hospital care, redirected to primary eye care, or returned with clinical advice.

3. Methods

This was a mixed methods study combining semi-structured interviews conducted with key informants in England with the analysis of routinely collected administrative hospital data. Mixed methods combine findings from qualitative and quantitative fieldwork to provide a more robust and explanatory account of the subject of the research (O’Cathain et al., Reference O’Cathain, Murphy and Nicholl2007).

3.1. Qualitative interviews with key leaders in the NHS and independent sector

We developed an interview schedule informed by a review of relevant policy documents and preliminary discussions with key leaders in the NHS and independent sector, and it evolved through an iterative process as interviews progressed. The schedule covered the growth and impact of the independent sector in delivering ophthalmology services, commissioning arrangements and the referral pathway, and the impact that the growth of independently delivered ophthalmology services has on patients. Interview participants were identified through a combination of purposive and snowball sampling.

Data collection occurred between July 2024 and February 2025. Two authors (GS/KW) carried out 12 interviews with individuals with responsibilities relevant to ophthalmology, including 3 senior leaders in NHS organisations and 3 senior leaders in ISPs, 3 optometrists and 3 consultant ophthalmologists. The mean age of the participants was 50 (SD = 10.6) and there were 6 women and 6 men, 8 were white English, one was white Irish, one was white Scottish and one was Asian Pakistani. All data was collected using video conferencing software at a time convenient to the participant. Interviews averaged 51 minutes, were audio-recorded and transcribed verbatim by a professional transcription service. NVivo was used to organise interview transcripts into codes, and reflexive thematic analysis was conducted following Braun and Clarke’s approach (Braun and Clarke, Reference Braun, Clarke and Maggino2020; Braun and Clarke, Reference Braun and Clarke2021). This inductive method allowed for flexible exploration of patterns within the data. Themes were developed through iterative coding, reflexive engagement, and interpretation, with researcher subjectivity acknowledged as a resource in the analytic process (Braun and Clarke, Reference Braun and Clarke2024). The interviews encompassed a broad range of stakeholders and organisations, capturing diverse perspectives and experiences. To strengthen the interpretation, findings were triangulated with accounts from participants as well as input from broader stakeholders, including those involved in commissioning ophthalmology services, consultant organisations, and health policy leaders (Carter, Reference Carter2014; Morgan, Reference Morgan2024; Patton, Reference Patton1999). These strategies were designed to enhance reflexivity and ensure an authentic and balanced representation of the data.

3.2. Quantitative analysis of routine data on admitted patient care

We analysed the quantitative data descriptively, summarising patterns and differences in activity and waiting times without testing causal relationships. We used patient-level data from Hospital Episode Statistics (HES) for all patients undergoing cataract surgery from 2013/14 to 2023/24 – a total of 4,681,157 admissions (2,958,074 patients). HES captures information on all NHS-funded admissions (whether to NHS hospitals or independent hospitals) and on privately-funded (self-pay or insurance) admissions to NHS hospitals. It does not capture information on privately-funded admissions to independent hospitals. It contains detailed information including patient demographics, admission details, diagnoses, procedures, and discharge details. Patients were classified by provider type (NHS or independent sector provider) using provider codes available within HES. We used Healthcare Resource Groups (HRGs), which group patients with similar resource use, to explore patient complexity for admissions from 2017/18 onwards (when the current HRG classification was introduced). Three HRGs for cataract surgery cover over 85 per cent of cases – HRG BZ34A (most complex), BZ34B (intermediate), and BZ34C (least complex). In England, HRGs are used to reimburse healthcare providers and more complex HRGs attract a higher payment to the provider. We also used NHS Emergency Care Data Set (ECDS) to examine rates of emergency department admissions within seven days of the date of cataract surgery within NHS and ISPs by linking HES and ECDS using unique patient identifiers.

We also used aggregate hospital admission data for privately funded and privately provided cataract activity sourced from the Private Healthcare Information Network (PHIN) (PHIN, 2025). These PHIN data were only available in aggregated form without details on patient demographics and complexity, and only for the period 2019/20–2023/24. We were unable to analyse emergency department admissions for privately funded and privately provided cataract surgery as we did not have access to patient-level PHIN data.

All analyses focused on finished consultant episodes (FCEs), each representing a continuous period of admitted patient care under a single consultant. Annual hospital activity – for both NHS providers and ISPs – was calculated by summing the total number of FCEs per financial year. All analyses were performed in Stata 18.

4. Results

4.1. Changes in the market for cataract surgery: scale and causes

The annual total number of NHS-funded cataract surgery admissions in England increased from 416,691 cases in 2018/19 to 649,886 in 2023/24 (a 56 per cent rise). This overall rise was accompanied by a major shift in service provision: while the NHS performed over three quarters of these surgeries in 2018/19, by 2023/24 ISPs were responsible for 56.8 per cent of NHS-funded cataract surgeries, up from 22.4 per cent just five years earlier (see Figure 1).

Cataract admissions by NHS providers and ISPs, 2013–14 to 2023–24.

Note: PHIN data only available from 2019/20.

The number of ISP sites undertaking cataract surgery increased from 116 in 2018/19 to 183 in 2023/24. There was a growing concentration of cataract activity within a few specialised ISPs, for example one provider increased from 1 site in 2015 to 52 by 2023 and another went from 5 sites in 2017 to 25 in 2023.

In our interviews, respondents noted that these new, specialised independent ophthalmology providers had entered the market alongside traditional independent hospitals which undertake a wide range of elective surgery, and they had expanded very rapidly. They pointed to pressures from growing waiting lists and times for cataract surgery (especially during and after the COVID pandemic). But they also noted that high volume, low complexity cataract surgery was potentially very remunerative for the new providers, especially when they operated from new, purpose-designed facilities, and that patient choice regulations and changing referral pathways from optometrists had made it easier to enter this market.

It was suggested that the transformation of the market for cataract surgery had not been a matter of national policy or planned intent, and that NHS England and commissioning bodies had been essentially passive actors at best in the changes that occurred, as one interviewee observed:

…I think there’s, kind of, a danger of thinking that there is intelligent design within NHS England in relation to the operation of markets. There is no conscious thought about the operation of markets within NHS England. There is no team that has any responsibility for that. …We’re only really coming to the realisation that there are a series of markets that are failing and we have no means to address them… Ophthalmology is a growing one… (Interview B, NHS)

In contrast, respondents from the independent sector highlighted that they had recognised the commercial potential of cataract surgery and adapted their business models accordingly. One ISP interviewee explained that the pause in elective surgeries during the COVID-19 pandemic in 2020 provided a valuable opportunity to reflect and plan for the future:

… we moved to be what we are now, which is about 80 per cent NHS work and about 20 per cent private self-pay, so a real big shift in what we did. We did that by reducing dramatically the number of service lines that we offered on the private side and by re-doubling our efforts to become a high-volume NHS cataract provider. Unbeknown to us, we were about to walk into a COVID pandemic, which did a number of things. It probably meant that providers like us became more in demand … it gave us an opportunity to really stop the business, reset, restructure and go again. (Interview G, Independent)

4.2. Commissioning, contracting and clinical coding for cataract surgery

There was broad agreement among respondents that ICBs faced significant challenges in commissioning and contracting cataract services. These difficulties were attributed to limited capacity, expertise, and experience, as well as commissioning processes often constrained by tight financial and time pressures. Respondents also highlighted a power imbalance between ICBs and large ISPs, particularly evident when contractual disputes arose. In such cases, the legal resources available to major ISP chains often placed ICBs at a disadvantage.

I think commissioners, in theory, have a lot of powers, they just don’t necessarily realise it. And we’ve made no investment in commissioners since pre-2008… Basically, there’s no training, there’s no development … and we have such wide variation in standards because people learn from whoever they sit next to. So, I think a really simple thing to do would be to upskill commissioners everywhere. I just don’t think that would be a particularly complicated thing to do and I think that would be incredibly valuable with massive spillover effect in other areas. (Interview B, NHS)

Respondents also described inefficiencies in the way services were commissioned. The current structure of ICBs meant there was variation in commissioning approaches across regions. Differences in local priorities and decision-making processes meant that similar services were commissioned separately across multiple areas.

Also, I do think that we should be commissioning on much larger footprints for services that are essentially the same. There’s absolutely no point commissioning 42 times for [private provider name], it just doesn’t make sense to me. We could do that seven times or one time. (Interview B, NHS)

Respondents also described inconsistencies in access across different parts of the country due to variation in commissioning policies which could affect patient eligibility criteria for cataract surgery.

…there had been quite strict rules put in some regions about what level of vision you had to achieve in order to be allowed a cataract operation… that all was taken away. So, anyone who went to the independent sector, none of those requirements were required…. So suddenly, you have a complete postcode lottery. So, if you were in one place with NHS provision and a visual requirement, you would not be able to be referred. And yet you could go somewhere with no visual requirement, and in fact very little visual problems, and be referred. (Interview D, Independent Sector)

But in addition, the policy environment for commissioning and contracting meant that ICBs had quite limited powers to influence or control service provision. ICBs faced limitations in restricting ISPs, particularly regarding what was termed ‘non-contracted activity’. Under ‘any qualified provider’ (AQP) rules, a provider with a contract in one ICB in England could operate elsewhere without a local contract. This meant a provider could deliver services, accept referrals and invoice for services in areas where the local ICB had neither commissioned the service nor set quality standards, while the commissioning ICB was not in a position to evaluate or inspect the provider’s site for quality and safety. Respondents noted that this arrangement sometimes led to overprovision of cataract services in certain areas. As one NHS interviewee explained, even when commissioners had concerns about providers operating locally, their ability to intervene was limited:

I think the choice agenda’s sensible but I think it’s gone a bit too far. I think we need to rein it in a bit because we just can’t have any provider coming along. They do work for us in non-contractual activity and we want them to have a contract, at least we’ve got control. But if we’ve got concerns about the provider, we can’t stop them delivering, we still have to allow them to deliver but they don’t have to do what we ask them to do. So, it’s a very difficult balance. (Interview E, NHS)

A lack of commissioning control was linked to a perceived oversupply of providers in some areas, where multiple providers could establish services despite relatively short waiting times:

I can’t believe that they have been allowed to allow seven providers in a relatively small area. I feel as though the area that I work in is flooded with cataract providers, absolutely flooded, there are a lot… I have got a friend who’s an optometrist who’s in one of the commissioning boards… I had a chat with her and I said, why have you allowed these two new premises to open when there’s only a … two week wait for cataract surgery, it’s nothing, and she said they had to. (Interview J, Independent sector)

Whether ISPs had a contract with an ICB or not, the processes for documenting activity, checking clinical coding, raising and paying invoices were also called into question by respondents, who felt that the monitoring of activity and expenditure was often quite limited.

And one of the ICBs has spent an enormous amount of time pulling apart all these invoices and tracking them and found that actually there’s high levels of duplication between them. They break patient pathways across multiple invoices, so it’s really hard to track them. There’s been all sorts of slightly odd payments and things like this. And so, I think, yeah, there’s very odd behaviour going on in this market in relation to this. (Interview B, NHS)

A respondent from an ISP made the point that such behaviours were not universal and emphasised the efforts they made to maintain positive relationships with ICBs and to adhere to established contracts and agreements, but noted that ICBs were not necessarily monitoring or auditing their performance:

We only do ophthalmology; we’re not owned by an optometry practice like I think a couple of the providers… But no, we certainly make sure…our relationship with ICBs is we’re contracted at all of our ICBs… but also, we follow the rules. So that’s…you know, and we lose referrals because optometrists get frustrated if we reject patients. But that is the rule for that local ICB. Whether you like it or not, that is the local commissioning guidance and we follow it. So, it is there, it’s just whether or not it’s being audited, that’s a separate issue. (Interview D, Independent sector)

It was also suggested by a number of respondents that some ISPs’ clinical coding practices sought to maximise their income and were questionable, and that ICBs were not well placed to check or challenge them. One respondent suggested that providers were pushing the boundaries of existing rules, illustrating how NHS contracting may be ineffective or insufficient in regulating private provision:

I think this is them being imaginative within the existing rules… they are maximising the value they get from the codes that are available. And there’s some ongoing conversations around patient lives at home alone, so you should only code that where the patient stays longer. Some of the providers argue that the extra 10 minutes they spend to talk to the patient means the patient is staying longer, therefore, they should be able to code to it. So, this kind of thing. So, there’s a few of these, kind of, which are really dubious and the guidance is really quite fluid. And it comes back to that, kind of, regulation thing. NHS policy is written with a good person in mind, not someone who’s trying to make a profit. (Interview B, NHS)

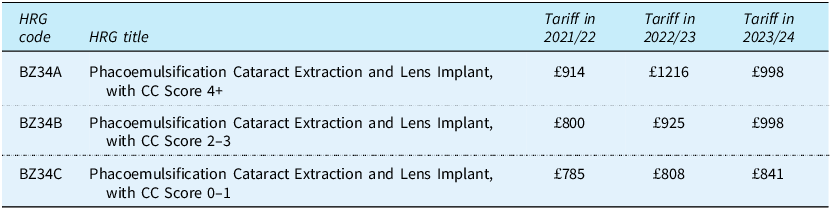

These views are supported by our quantitative analysis. The diagnosis and procedure codes recorded for each cataract surgery admission by the provider are used to assign the patient admission to a HRG. Each HRG has a fixed tariff or payment associated with it, set by NHS England and based on NHS hospital cost returns for previous years, with some adjustments. While there are 10 HRGs which related to cataract surgery, about 80 per cent of cases fall into the three HRGs set out in Table 1 below. The differentiator between the three HRGs is the ‘CC score’ which is derived from secondary diagnoses codes recorded by the provider for comorbid conditions which may increase the case complexity. Tariff rates have varied substantially over the three years as shown in Table 1 but in 2023/24 the most complex HRG (BZ34A) attracted a tariff of £998 that was higher than that for the least complex HRG (BZ34C) which attracted a tariff of £841.

HRGs and tariffs for cataract surgery 2021–22 to 2023–24

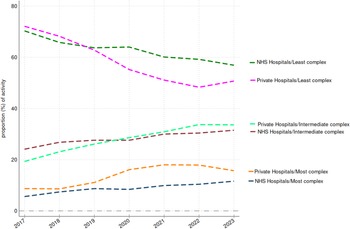

Respondents suggested that ISPs generally handled fewer complex cases either because they did not have the facilities to deal with some patients (eg. those requiring a general anaesthetic) or because they operated referral criteria which excluded patients whose care might be more complex (such as those with mobility problems, severe obesity, or some comorbidities). We explored the distribution of patient admissions to NHS and ISPs in HRG BZ34 between the three levels of complexity (A, B and C) and how they have changed over time, with the results shown in Figure 2. It can be seen that ISPs report a higher share of the most complex cases (BZ34A) and a lower share of the least complex cases (BZ34C) than NHS providers, and that the reported complexity of the patients treated by ISPs has increased over time faster than that of NHS providers. It seems very unlikely, given the differences in facilities and referral criteria, that ISPs are actually treating more complex patients than NHS providers and so it seems likely that this does result from systemic differences in clinical coding practices.

Proportions of NHS funded cataract admissions in HRG BZ34 (least to most complex) by NHS and ISPs 2017–18 to 2023–24.

4.3. Waiting times, patient choice and referrals

Many respondents thought that the greatest benefit to patients from the expansion of cataract surgery provision over recent years had been improved access and reduced waiting times for surgery, both for those treated in the NHS and in the independent sector.

So, I think for patients, it’s provided extra capacity, often at a short time, and by and large, the service is good. So, I think for patients that’s great and it’s got the waiting list right down. If you look at the waiting time for cataract surgery compared to, I don’t know, hip surgery or some similar high-volume procedure in ENT, because it’s been done out of the hospital in the community, the waiting list has plummeted. And that’s fantastic for patients. (Interview C NHS)

Figure 3 shows the median waiting times for patients treated in NHS providers and ISPs over time. Waiting times in ISPs have been consistently lower than those in NHS providers throughout the period, but the gap has widened over recent years because ISPs’ waiting times have fallen, while NHS provider waiting times have remained constant or risen slightly.

Median waiting times (days) for cataract surgery for NHS providers and ISPs, 2013–14 to 2023–24.

Respondents were often sceptical about how well these arrangements supported patient choice. Respondents observed that patients typically deferred to the community optometrist for a recommendation. They reported that some ISPs offered transport to and from their clinics, which could encourage some patients to select them. Overall respondents felt that these changes had put considerable influence in the hands of community optometrists.

One ISP respondent clarified that optometrists are paid modestly for delivering aftercare, ensuring continuity, and entering patient data, but stressed that this is not a core business model or incentive-driven arrangement. However, several respondents suggested that some ISPs may offer financial incentives to optometrists for referrals, particularly through contracts for post-cataract follow-up care. Respondents described ways in which this could affect patient choice and referrals.

Introducing the choices of the private sector in, meant that optometrists were a group of people who could maybe be influenced more by the private sector selling what they had to offer, so that when the optometrist was delivering that choice conversation to a patient about where they want to go, that choice conversation had really been influenced by the commercial marketing from the private sector… And I think some patients are much more or less informed about the fact that they do have choice when it comes to their NHS care. (Interview K, NHS)

… optometrists weren’t giving choice but they are paid by [private provider name], [private provider name] to refer to them. So, what’s happened is that they’re paid, they get the money and they refer there, even if the patient doesn’t want to go there. And the patient’s saying, well, I don’t want to go here, what am I doing here, I want to go to the NHS? (Interview E, NHS)

Respondents also observed that ISPs were much more adept than NHS providers at fostering relationships with optometrists. One NHS respondent described how ISPs invested in relationship building activities that NHS trusts generally did not:

The other thing that the independent sector do… is they spend a lot more time and effort, or they recognise where their source of referral is and they build a relationship. And with all respect to the NHS trusts, they have treated optometrists with contempt for a very long time. And they still continue to do it. Whereas the independent sector will…they run CPD events, they take the time to show them round their clinics, they take the time to…they have customer relationship managers who go into every practice. So, there is a really good, kind of, relationship building. (Interview B, NHS)

Some respondents raised concerns that efforts by ISPs to build and maintain relationships with referring professionals occasionally extended into offering free continuing professional development (CPD) and other incentives, raising questions about the appropriateness of such practices. As one NHS respondent explained, early accreditation and CPD events could be persuasive, but recent standardisation by commissioners had helped to formalise pathways:

So, that in the early days was a really big pull, and they would run their own accreditation service – so come along to an education evening and we’ll accredit you to do our post-cat follow-ups, we’ll give you access to this website where you can see all the information. Oh, and while you’re here, we’ll give you a nice meal or we’ll get some pizzas in and some cakes in and we’ll do a bit of education on top and we’ll give you some CPD points for doing that too. But I think in recent years the commissioners have really got on top of this, because it just got a little bit murky, so there’s really now a good standardised pathway for pre-cataract and post-cataract. (Interview K, NHS)

However, ISPs argued that CPD events and related marketing strategies served as legitimate opportunities to build relationships, share information, and respond to queries about their services, ultimately aiming to be considered as a referral option. One ISP respondent described relationship building in practical terms, explaining the information that they provided to support patient referrals:

We also have a team of…I suppose, you might call them a sales team. So, we call them account development managers and they will go and visit optometrists in the community to explain what our offering is and answer any questions that the referrers might have. And they might be well where are your sites and what are your referral to clinic times, what are your referral to treatment times, what are the outcomes that you achieve. So, that when patients do come in, we’ve at least empowered the optometrist by supporting them with the answers to questions that might come up. Because if we don’t do that, we can’t expect them to consider us when they’re deciding where best to send the patients. (Interview H, Independent sector)

A few respondents raised concerns about what happened when there was an organisational relationship (such as shared or linked ownership) between a community optometrist provider and an independent ophthalmology provider, and whether this would lead to referrals being directed to the linked provider:

So, my concern and what absolutely seems to be happening in [area name], but this is obviously anecdotal, is that [optometrist name] refer purely into [ISP name], bypassing other hospitals that are much closer for a patient to go to. (Interview J, Independent sector)

4.4. Quality of care, complications and outcomes

We sought to understand what differences might exist in the quality of cataract surgery between NHS and ISPs. We explored differences in casemix (which have already been discussed earlier in the section on commissioning and contracting), perceptions of quality, the doctors undertaking cataract surgery, the lenses used by providers, and some post-surgery complications and outcomes.

There were some clear concerns from respondents about the quality, safety, and overall integrity of some specific ISPs. Respondents clearly identified differences in practice and performance among ISPs and expressed some frustration that there were insufficient mechanisms to deal with poor practice and performance. As one NHS respondent explained, providers varied widely:

So [private provider name] are the ones who operate most cleanly. [private provider name] are slightly…there’s some grey areas around some of their practice. Then you’ve got [private provider name], who are in the much more cutthroat end of the market where they are…there have been regular conversations between them and the NHS branding people about misuse of their branding… There’s been, kind of, a lot of really difficult conversations. …so yeah, they’re at the really shady end. (Interview B, NHS)

Respondents from the independent sector also had concerns about the quality and safety of certain providers in their own sector. An ISP respondent described specific concerns about providers not following pathways and how governance structures influenced where surgeons preferred to work:

It‘s people who don’t follow the pathways. It‘s people that aren’t rejecting people it should be rejecting. Its people are cutting corners in terms of quality and safety. There’s one provider, and I won’t name it, but some of my surgeons have worked there. They get paid more if they work there but they say it’s danger money and actually they’d sooner work for a provider like ourselves. And actually, we pay the lowest of all the independent providers but they’d sooner work for us because they feel more comfortable with our governance structure, they feel safe the way we’re indemnified. (Interview D, Independent sector)

Most respondents believed that ISPs predominantly handled straightforward cases, an approach seen by some as appropriate given their capacity, but by others as ‘cherry-picking’ easier, more profitable patients. This raised concerns about the comparability of outcomes, quality, and complication rates across sectors, though some ISP respondents argued that they did deal with more complex cases too:

So, I’d love to say all our cataracts are really clear and easy ones. If you asked my surgeons … our cataracts are pretty dense. [city name], in particular, we have some pretty horrific cataracts, to the point where we actually have a complex list where we have specialist surgeons who do our more complex cataracts. Because we don’t want these going back to the NHS, we’re happy to take them on and deal with our own complications. (Interview D, Independent sector)

Several respondents suggested that ISPs were more likely to perform additional diagnostics, see patients earlier than clinically necessary, schedule unnecessary follow-up appointments, or carry out cataract surgeries that were not clinically required, often motivated by financial incentives. As one NHS respondent explained this could include repeated imaging:

…your cataract surgery, we could give you a better lens. So, once they’re in the door, the other thing we’ve seen is a real increase in OCT [optical coherence tomography], which probably doesn’t have that much of a place except for the initial, kind of, assessment of the patient. But we’re seeing lots and lots of follow-ups with OCT after OCT after OCT. You don’t see that in the NHS. (Interview E, NHS)

One respondent reported concerns about financial incentives to ‘upsell’ products not covered by the NHS, suggesting that commercial pressures affected how treatment options were presented to patients:

So, the upsell… basically, you can put a lens in the eye, it lets you see in the distance, and then you have to wear reading glasses. But there are really fancy lenses now that allow you to not wear glasses, called high-spec lenses. They are not covered by the NHS. But if you go to an independent sector provider, they will say things like, oh, but you’ve got astigmatism, so if you actually pay for, they don’t have to treat them as NHS. They can get paid for their NHS consultation and then the patient will up-pay. So, they’ll pay the £3500 to get the lenses. (Interview A, NHS)

ISPs operate under a consultant-delivered model, which typically involves surgery performed by a consultant ophthalmologist who may or may not also work in the NHS. In contrast, the NHS operates under a consultant-supervised model, where ophthalmology trainees perform some cataract surgeries under the guidance of a consultant, integral to the development of future specialists. The NHS, must balance patient care with professional training and workforce sustainability. ISPs, by contrast, emphasise productivity and consistent outcomes. Respondents noted that it would not be in the interests of ISPs to employ consultants with high complication rates:

… you get into the situation where you’re looking at corporate difficulties versus individual difficulties. So, I have no doubt…I have no doubt that if there was a surgeon performing badly, with complications, they would not be kept in the independent sector. Because it’s of no…interest to them, because they do high volume, high efficiency. So, they don’t want somebody who’s making mistakes all the time. And in fact, if you look at all their sign-on requirements… they don’t want people with high complication rates. (Interview A, NHS)

The focus on maintaining low complication rates and delivering predictable surgical outcomes also appeared in the way ISPs use surgeons who perform high-volume cataract surgery, which respondents associated as contributing to lower PCR rates:

…the PCR rates across the independent sector versus NHS, they are better. Maybe it’s better because we have less doctors, junior doctors to train. Even if you remove those anomalies, I think you still find that the adjusted PCR rate for independent sector is as good, if not better than the NHS. And it absolutely should be. We have consultants that do nothing but high-volume cataract surgery. Our lead NHS consultant, [consultant name], has done over 40,000 cataract procedures in his lifetime. You’re going to get pretty bloody good at a cataract after doing 40,000. (Interview G, Independent sector)

Some expressed concerns about the lenses used by certain ISPs and the potential impact on outcomes, particularly higher rates of post-cataract opacification (PCO), which may require subsequent YAG laser capsulotomy. One NHS respondent suggested that some ISPs knowingly used cheaper lenses associated with higher PCO risk, thereby generating additional demand for YAG laser procedures for which providers were then remunerated:

One thing I did hear that was very, very worrying and I can’t remember which ISP it was, they said to the patient, yes, we’ll get you in for your cataract’s surgery but within twelve months you’ll have to have a laser capsulotomy… Since the advancement of intraocular lens implants and the change of the lens edge designs in the last five to ten years, the instance of PCO has dropped dramatically. What that says to me is that ISP is using cheap, nasty implants, they know that the patients are going to need a replacement laser capsulotomy very soon. (Interview I, NHS and Independent sector)

By contrast, one ISP respondent emphasised that lens choice is a critical part of quality care, and that investing in higher-quality lenses reduces complications:

The lens that we use is so critical to the outcomes that the patient achieves… we’ve chosen to use a hydrophobic acrylic lens because it’s got lower PCO rates which, you know, you may be aware that might require a secondary procedure from patients… So, we believe that we’ve chosen a quality lens, it’s not the cheapest lens in the market but it’s a quality lens and that’s such an important part of our cataract offering that you feel it’s worth that investment. (Interview H, Independent sector)

Our quantitative analyses provide corroborative evidence of potential quality differences between NHS hospitals and ISPs in the rates of post-cataract YAG laser capsulotomy (Figure 4). The proportion of patients requiring YAG laser treatment within two years of cataract surgery varied substantially between NHS and ISPs and this difference has widened substantially over time.

Proportion of cataract surgeries that were followed by a YAG laser capsulotomy within 2 years for NHS providers and ISPs 2013–14 to 2023–24.

Respondents expressed conflicting views on how ISPs manage and record complications. One ISP respondent emphasised their organisations thorough data submission processes and how they use outcome data to monitor surgeon performance:

So, we were one of the people that advocated for it in the new national specification, any provider, whether it’s independent sector or NHS must be submitting their data because we must be, you know, benchmarking individual surgeons but also sites. So obviously I do that as well, I benchmark by surgeon, I benchmark by sight. But then I also use some of the European data and the European benchmarks. Because the UK’s great but I also like to think of it more international when I’m looking at safety, et cetera. (Interview D, Independent sector)

However, it was frequently suggested that complications were inconsistently recorded in data submitted to the National Ophthalmology Database (NOD), with some patients returning to NHS providers for treatment instead of the ISPs. As one respondent explained, this means complications managed outside the independent sector are not reflected in their reported complication rates:

…there were independent providers not managing their complications. So, they’ve got a serious acute complication which they should be picking up and dealing with and looking after the patient and they end up in the eye emergency clinic of the Trust. So, it’s flagged as a post-cat eye complication emergency but they didn’t do the surgery, so it distorts their figures and that’s wrong. I raise with the commissioners in a meeting, I said, well surely isn’t it in their contract that they have to deal with these complications and look after the patient, look after the cases. Oh yes, it is, well they’re not, so why aren’t they having their contracts pulled for a breach. Oh no, we can’t do that, why not, what’s the point of having a contract if you can’t make it continue to work properly (Interview I, NHS and Independent sector)

We examined the rates of intraoperative posterior capsule rupture (PCR) recorded in HES from 2013/14 onwards for both NHS and ISPs and the results are shown in Figure 5. Rates have risen over time and have been generally higher for cataract surgeries in NHS providers than in ISPs, although that gap has narrowed over time. We are cautious about the interpretation of these findings, because the recording of PCR is dependent on good quality clinical coding and is a relatively rare outcome.

Rates (%) of cataract surgery with an intraoperative posterior capsule rupture (PCR) complication recorded for NHS and ISPs, 2013/14 to 2023/24.

We used HES data linked by pseudonymised patient identifiers to the NHS ECDS to explore the rate at which patients admitted for cataract surgery then attended an NHS accident and emergency (A&E) department within the following seven days. ECDS is not available before 2021/22 so we were only able to do this for three years. The results are shown in Figure 6. Overall, less than 1 per cent of patients undergoing cataract surgery have an A&E visit within seven days, and rates are slightly higher for patients at NHS providers than they are for patients at ISPs. Of course, it should be noted that some patients of ISPs requiring unscheduled post-operative care may be returning to the ISP rather than going to an NHS A&E department, so the rates are probably not directly comparable.

Proportion (%) of cataract surgery admissions with an NHS A&E department visit within seven days post-admission, 2021–22 to 2023–24.

5. Discussion

We set out to explore the rapid growth of private, for-profit provision by ISPs of cataract surgery in England in recent years; to understand its causes and consequences; and to consider what lessons could be drawn for health policy on healthcare commissioning, markets and competition in the UK and internationally.

We find that the rapid growth of independent sector cataract surgery in England since 2019 was largely unplanned by NHS England and ICBs. This expansion appears to have been associated with the entry of new specialised ISPs responding to high demand, NHS tariffs structures, relatively low entry barriers, and direct referrals from community optometrists, often supported by private equity investment (Centre for Health and the Public Interest, 2024). ICBs struggled to manage this growth due to national policies like the AQP rules and patient choice guidance, combined with limited commissioning capacity. ISPs have leveraged these rules to operate widely, sometimes delivering care without a contract in place, which ICBs must still reimburse. Patient choice requirements have increased referrals to ISPs, sometimes incentivised through optometrists’ involvement in follow-up care. Efforts to manage the referral pathway have had mixed success and face conflicts with choice policies. Contractual oversight by ICBs has been weak, allowing some providers to use clinical coding to secure higher tariff payments. ISPs can achieve higher productivity through specialised facilities and financial incentives, contributing to increased surgery volumes and reduced waiting times, while NHS providers’ productivity has lagged (Warner, Reference Warner and Zarenko2023) despite significant investment through NHS England’s eyecare transformation programme and the GIRFT (Getting it Right First Time) initiative aimed at improving productivity in ophthalmology (NHS England, 2019). However, concerns remain about quality and outcomes in the independent sector, including higher rates of post-cataract complications like YAG laser capsulotomy.

There is much to be learned from this unplanned experiment in the large-scale delivery of NHS funded elective care by for-profit ISPs. First, it demonstrates the importance of effective service commissioning, monitoring and control, and somewhat paradoxically the difficulties that can arise from government policies designed to promote patient choice, markets and competition. Contract specifications need to be clear about things like referral criteria and thresholds, facilities, procedures and lenses used, data reporting, and outcomes. Much of that may have been taken largely on trust in past contracts with NHS providers.

Second, it shows that the NHS tariff system, which is based on calculations of costs from NHS provider cost returns, is a poor tool for contracting with ISPs who do not participate in those returns and have a very different cost structure. A generous activity-based tariff creates very powerful incentives for all providers to undertake more activity where there is unused capacity available and while that can be positive in helping to tackle waiting times and access problems, it also raises potential risks of overprovision and variable quality, highlighting the need for careful design of referral processes and pathways and robust contractual management to ensure appropriate volumes and standards of care. The NHS could learn from experiences in other countries which have moved away from fee for service tariffs to reimbursement models based around care pathways, care outcomes, or blended models incorporating capitation and encouraging risk sharing between the purchaser and the provider.

Third, it illustrates the need to think less transactionally about a single type of condition or procedure and more broadly about service commissioning at a specialty or multispecialty level. The developments in cataract surgery which this paper has outlined have led to large increases in activity and funding, but that is at a cost to other ophthalmology services and indeed perhaps to other acute care services.

We note some limitations to this paper. We have focused on cataract surgery but not addressed wider service provision for other common eye conditions, or changes in the whole pathway of care in both the community and in hospital for cataract patients. Without linked data on outpatient and community clinic activity or clinical data on pre- and post-cataract patient characteristics it has not been possible to explore the appropriateness of referrals and patient management or differences in clinical outcomes. Also, the lack of routine data on referral pathways prevents us from quantitatively assessing whether changes such as direct optometrist referrals contributed to the growth of independent provision. In addition, the conditions which have led to the dramatic changes in service provision in cataract surgery have not been replicated to a similar degree in other surgical specialties where ISP provision is significant (such as orthopaedics, general surgery, gynaecology, urology or ENT) and so we should be cautious about generalising from these important findings in ophthalmology. An important consideration raised in the interviews is that if a growing share of care is delivered in settings that provide limited training for junior doctors, this may have implications for workforce development and the sustainability of quality across the wider health system, and merits further investigation in future work.

6. Conclusions

Increased independent sector provision of cataract surgery in England over recent years has provided much greater access to cataract surgery and lower waiting times for patients which clearly has positive consequences for their health and wider life, but at some considerable financial cost to the NHS. This paper highlights the importance, when moving from a monopolistic, publicly provided healthcare system to one in which there is a greater diversity of private and public provision, of paying careful attention to the design and implementation of commissioning arrangements, contracting, and service monitoring to maximise the potential benefits of greater choice and competition while avoiding or mitigating some potential disbenefits.

Data availability statement

The data that support the findings of this study are available on request from the corresponding author, Gemma Stringer. The qualitative data are not publicly available due to their containing information that could compromise the privacy of research participants.

Acknowledgements

We are grateful to the participants from both the NHS and the independent sector who shared their time and perspectives.

Financial support

This paper was produced as part of a research project undertaken by researchers at the University of Manchester, the University of York and the University of Birmingham and funded by the National Institute for Health Research (NIHR – grant no NIHR135108). The views expressed are those of the author(s) and not necessarily those of the NIHR or the Department of Health and Social Care.

Competing interests

The author(s) declare none.

Open access

Open access