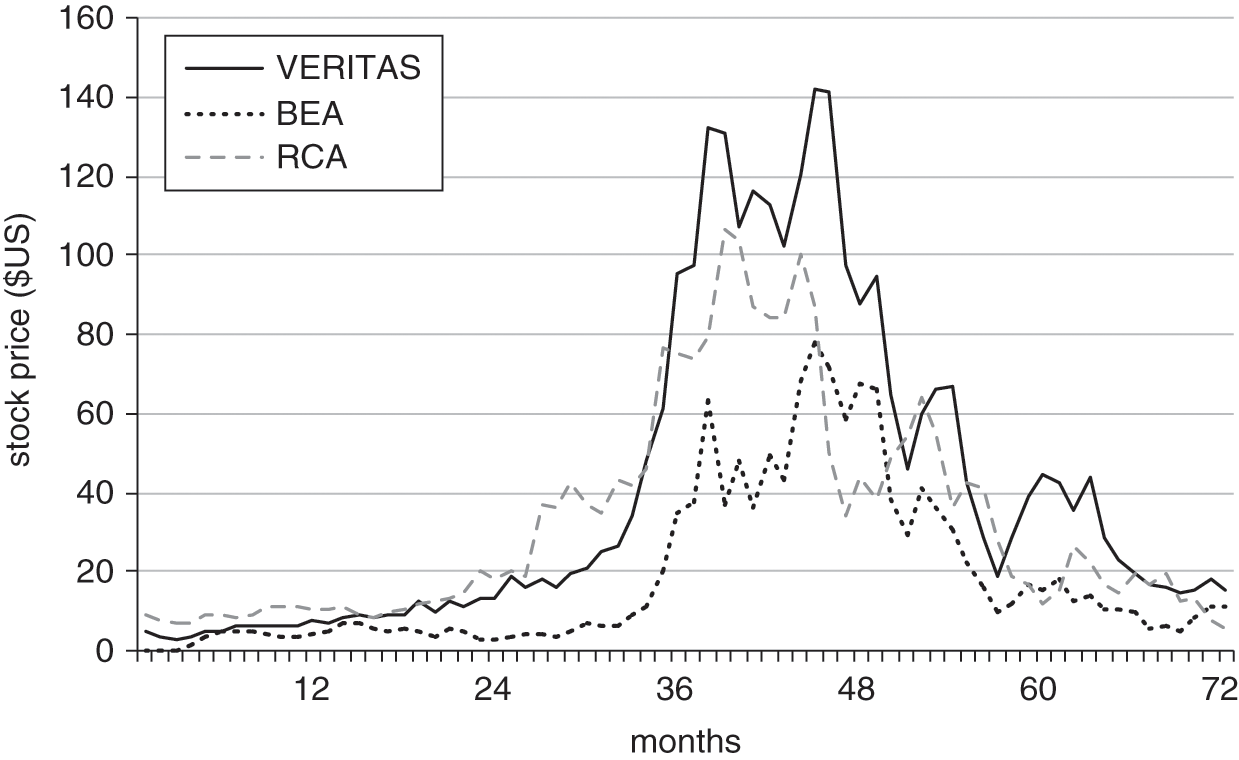

The bubble into which Warburg Pincus liquidated the bulk of its investment in BEA Systems was extreme, but it was not unique. My awareness of the prelude to the Crash of 1929 had persisted some thirty years after my scholarly engagement with economic policy in response to the financial crisis and economic contraction of 1929–1931. At that time the Radio Corporation of America (RCA) had been an emblem of the “new economy”: broadcasting represented the revolutionary application of scientific innovation to a commercial medium of boundless potential. An image of the RCA stock price from the mid-1920s through its apogee and beyond served me as a momento mori for speculative excess, especially as VERITAS Software and BEA Systems were swept up by the 1998–2000 version.

Figure 7.1 sets out the development of the stock price for RCA, VERITAS and BEA over the six years, denominated in months, beginning with January 1926 in the case of RCA and with January 1997 in the case of VERITAS and BEA. Because I had once studied the trajectory of RCA’s stock after it rose by a factor of ten in less than two years, it was easy to foresee what awaited the shares of VERITAS and BEA when they rose by broadly comparable multiples over an even shorter period of time.

Figure 7.1 Stock prices for RCA, 1926–1932, VERITAS Software, 1997–2003, and BEA Systems, 1997–2003

The persistent recurrence of speculative excess is a defining feature of financial capitalism wherever and whenever bankers are flush with cash to invest in liquid secondary markets in financial assets. Three canonical personifications of financial capitalism can be abstracted from the historical record. In Fernand Braudel’s version, financial capitalism is heroic. It is as if “the characteristic advantage of standing at the commanding heights of the economy … consisted precisely of not having to confine oneself to a single choice, of being able, as today’s businessman would put it, to keep one’s options open.”Footnote 1

From within the Clinton White House, beaten into putting a balanced budget before all other policy priorities, James Carville called out financial capitalism as the ultimate bully: “I used to think that if there was reincarnation, I wanted to come back as the president or the pope or a .400 baseball hitter. But now I want to come back as the bond market. You can intimidate everybody.”Footnote 2

A less flattering portrait of financial capitalism captures the recurrent waves of speculative boom and bust that express the essential behavior of financial institutions and markets, whose participants are compelled to make commitments today in the face of inescapable uncertainty about the world in which the consequences of those com- mitments will be realized. Nicholas Sibley, once the public face of the leading investment firm in Hong Kong, characterizes financial capitalism as a lush: “Giving capital to a bank … is like giving a gallon of beer to a drunk: you know what will come of it, but you can’t know which wall he will choose.”Footnote 3

It is Sibley’s version that concerns us now.

Early Bubbles in France and England

Historically, the appearance of bubbles transcends both political regimes and market structures. Comprehending this is the first and critical step to grasping how capitalism works. The second step is to understand that the phenomenon of bubbles challenges received doctrines of neoclassical economics: the dual hypotheses of efficient markets and rational expectations. The third step cuts against the bulk of the literature on the wastefulness of bubbles and the inevitable crashes that follow; it is to recognize the role that financial speculation has played in funding the episodic deployment of revolutionary technology at systemic scale. Thus, I am concerned to illustrate how boringly repetitive – how banal – the emergence of speculative excess is, precisely because it has played a historic role as the engine of transformation, driving growth in economic productivity and living standards for the 250 years of the modern era.

This rhyming of financial history reaches back far beyond the 1920s. In modern memory, the phenomenon dates back to the Dutch tulip mania of 1636–1637.Footnote 4 Sixty years later, as London emerged to rival Amsterdam, the mid-1690s witnessed the launch of some 100 new joint stock companies, enterprises whose ownership was represented by more or less freely transferable equity securities. Their shares offered outlets for speculative investment to those who could not gain access to the shares of the few established monopolies, first among which was the East India Company, dating from the reign of England’s James I. The purposes of the stock promotions ranged from the recovery of shipwrecks in search of treasure to the seemingly more mundane manufacture of linen. In the former instance, a “projector” absconded with the funds provided by Daniel Defoe and others; in the latter, the incompetence of its founders forced the Linen Company to purchase for resale at a loss goods it did not itself know how to produce.Footnote 5

The London stock market boom of the mid-1690s was accompanied by a proliferation of equity derivatives, notably put and call options, which respectively carried the right – but not the obligation – to sell or buy shares at an agreed price for an agreed period of time. This was not the first and would not be the last time that a speculative wave was accompanied by financial innovations: tulip bulb futures had been traded in Amsterdam in the 1630s. As at other times, the derivatives could be employed to leverage opportunity for gain as readily as to manage risk of loss.Footnote 6

“The close association between gambling and investment was constantly reinforced at this time,” due in good part to the proliferation of lotteries, sponsored both by private promoters and by the state, which gradually evolved a structure of public finance to fund Britain’s participation in Europe’s perennial dynastic wars of the period.Footnote 7 Most of the new joint stock companies disappeared without a trace, with the notable exception of the Bank of England, but the lotteries left a rich legacy in the form of probability theory. Samuel Pepys wrote to Isaac Newton that the lotteries had

almost extinguished for some time at all places of publick conversation in this towne, especially among men of numbers, every other talk but what relates to the doctrine of determining between the true proportions of the hazards incident to this or that given chance or lot.Footnote 8

Cultural memory of that first English stock market boom has been overshadowed by the canonical South Sea Bubble, which swept London in 1720. At the time and since, the South Sea Bubble was linked to the contemporaneous Mississippi Bubble in Paris: John Blunt in London and John Law in Paris each saw the potential for harnessing the speculative spirit of the nascent stock exchange to meet the endless need for finance by states perpetually at war, most often with each other. An incentive to speculation in each case was the prospect of monopoly profits on trade with the New World.Footnote 9 In each case, the offer of private gain was meant to serve a public purpose: an extraordinarily imaginative, bold exercise in state finance.Footnote 10 Here was a creative, collaborative game to be played between financial capitalism and the state. And, given the inherent instability of the former, it was a game that was doomed at birth in both locales. This is a fact worth recalling whenever a politician, driven by opportunism or ideology, proposes the privatization of the social safety net.

A private company would fund the haphazardly accumulated debt of the state by issuing its shares to the public, this at a time when organized markets in long-term government debt were hardly known. For those charged with managing the public debt, the offer was administratively appealing: they could eliminate the high transaction costs of dealing with individual creditors by transferring responsibility to a single entity that would function like a giant investment trust, a sort of Berkshire Hathaway whose asset would be government debt.Footnote 11 The Bank of England had been established fifteen years earlier for a similar purpose.

In Paris, manic buying was limited to Law’s Mississippi Company, which merged with the Banque Royale and in parallel secured a monopoly on all of France’s international trade. The shares in Law’s new vehicle, the Compagnie des Indes, rose by a factor of twenty during the second half of 1719, fueled by Law’s issuance of paper currency far in excess of the Bank’s holdings of specie. In London, the shares of Blunt’s South Sea Company rose from less than £100 to £1,000 during the first six months of 1720. Realized gains spilled over into the markets for other assets, financial and real. London’s far more mature machinery for manufacturing products to meet the speculative appetites of investors went into high gear.Footnote 12 In each case, the inevitable collapse generated an orgy of political recriminations, legal proceedings and personal tragedies.

The long-term consequences of the twin bubbles were radically different in the two countries. In France, Law’s catastrophic failure was followed by deepening disarray in the state’s finances and ever more corrupt and oppressive efforts to raise needed funds. In Britain, the South Sea scheme counterintuitively served to continue the extended process of consolidating government debt and stabilizing public finances.Footnote 13 Various attempts to regulate the stock exchange and to limit the potential for speculation did not preclude the gradually accelerating deployment of liquid capital into agricultural improvements. Even the notorious Bubble Act of 1720, which prohibited the creation of new joint stock companies, is now read as special-interest legislation intended to bar competitors from bidding for investors against the South Sea Company; it was barely enforced in the years that followed.Footnote 14 It certainly did not prevent the emergence of speculative investment in new transportation networks – turnpikes and canals – in the early 1770s, or the full-blown Canal Mania of the 1790s.Footnote 15

For my immediate purpose, the most significant attribute of the South Sea Bubble was the extraordinarily wide range of projects that served as the objects of speculation, amplifying the phenomenon of the 1690s. Writing from hearsay some 120 years later, Charles Mackay compiled a list of eighty-six “bubble companies” that were declared illegal in 1720, ranging from straightforward proposals for “the importation of Swedish iron” and for “making glass bottles” to more grand, even grandiose, schemes for “paving the streets of London” and “furnishing funerals to any part of Great Britain.” Of course, Mackay includes the iconic – and now generally deemed apocryphal – project: “For carrying on an undertaking of great advantage, but nobody to know what it is.”Footnote 16 To my mind, this enormous range of speculative projects carries the most important historical lesson and analytical challenge: anything, it appears, can be the object of speculation, whether that speculation is expressed through the lending of capital for projects with minimal likelihood of generating cash sufficient for repayment or through the purchase of shares at valuations impossible to relate to the cash flow fundamentals of the economic assets they represent.

Following the end of the Napoleonic Wars, London was clearly established as the leading international financial center. As such, it was the locus for repeated outbreaks of speculative fever. David Kynaston’s history The City of London documents the phenomenon. The first two (of four) volumes cover the century from 1815 to 1914: across this span, Kynaston identifies no fewer than ten waves of speculative fever on the floor of the London Stock Exchange. The first speculative boom of the nineteenth century became visible at the start of 1825. The Duke of Wellington himself anticipated the inevitable outcome, as reported by a close friend: “He thinks the greatest national calamities will be the consequence of this speculative mania, that all the companies are bubbles invented for stockjobbing purposes & that there will be a general crash.”Footnote 17

The boom was compounded of investments in foreign loans, especially those issued by the newly liberated Latin American republics; foreign mines, particularly the silver mines (real and fanciful) of Latin America; and domestic promotion of canals and less tangible projects initiated by the unregulated provincial banks. Deposits that had been placed with these “country banks” and typically devoted to financing local commerce were diverted to pursue the far higher nominal returns offered by issuers about whom the country banks knew nothing.Footnote 18

The Bubble of 1825 was significant not only because it was the first of the new century, as Europe – with America in tow – emerged from a generation-long world war, with its accompanying restrictions on trade and payments, into an epoch of commercial expansion, industrial investment and, at least aspirationally, political liberalization. As was the case 100 years earlier, speculation spread from a plausible core narrative – some canal companies had proven themselves commercially, and the final collapse of the decrepit Spanish empire in America did open new markets to Britain – to the far-fetched and outright outlandish. Moreover, it was the occasion for the first forced intervention of a central bank as lender of last resort to the money market and the banking system, as documented and dramatized by Walter Bagehot two generations later in Lombard Street.

The necessity and the effectiveness of the Bank’s initiative were both hard won. Bagehot summarized the experience in language that has become foundational for evaluating all the many subsequent such episodes, those that failed as well as those that succeeded:

The success of the Bank on this occasion was owing to its complete adoption of right principles. The Bank adopted these principles very late; but when it adopted them, it adopted them completely. According to the official statement, “we,” that is, the Bank directors, “lent money by every possible means and in modes which we had never adopted before; we took in stock on security, we purchased Exchequer Bills, we made advances on Exchequer Bills, we not only discounted outright, but we made advances on deposit of Bills of Exchange to an immense amount in short, by every possible means consistent with the safety of the Bank.” And for the complete and courageous adoption of this policy at the last moment the directors of the Bank of England at that time deserve great praise, for the subject was then less well understood than it is now; but the directors of the Bank deserve also severe censure for previously choosing a contrary policy, for being reluctant to adopt the new one; and for at last adopting it only at the request, and upon a joint responsibility with the Executive Government.Footnote 19

The Bank had been compelled to learn the most basic law of crises: when each player attempts to self-insure retrospectively – that is, when each player seeks Cash and Control in response to the unanticipated – only the open offer of collective insurance by a credible counterparty can prevent catastrophe. From the seminal events of 1825, the fine balance is evident between the leave-it-alone liquidationism that dominated policy during the slide into the Great Depression in 1931–1933 and the intervention à outrance that marked central bank policies during the autumn and winter of 2008–2009. In 1825, the Bank’s initial delay and manifest reluctance exhibits the inevitable tension generated, on the one hand, by the need for the authorities of the state to protect both financial capitalists and the market economy that depends upon them and, on the other hand, by the certainty that any extension of such protection will only encourage them to provoke such a crisis again – propagating what has come to be called moral hazard.Footnote 20

In his analysis of the role of the central bank, in Stabilizing an Unstable Economy, Hyman Minsky summarizes the core challenge that the dynamics of financial capitalism create for the authorities:

In as much as the successful execution of lender-of-last-resort functions extends the domain of [central bank] guaranties to new markets and new instruments, there is an inherent inflationary bias to these operations; by validating the past use of an instrument, an implicit guaranty of its future value is extended. Unless the regulatory apparatus is extended to control, constrain and perhaps even forbid the financing practices that caused the need for lender-of-last-resort activity, the success enjoyed by this intervention in preventing a deep depression will be transitory; with a lag, another situation requiring intervention will occur.Footnote 21

Decennial Dramas before 1914

The pattern of a financial bubble that funds investment in all sorts of speculative projects followed predictably by panic and crash and then, often, by more or less effective appeal for state relief has repeated itself throughout the history of commercial and industrial capitalism. During the long century preceding 1914, there was not a decade without such a drama. Focusing on London as the global financial capital, in 1835 the first, “little” Railway Mania – one in which realizations actually managed to match expectations – was followed the next decade by the “great” Railway Mania of 1845, which culminated in the Crisis of 1847 and the suspension of the Bank of England’s spanking new charter, enacted only three years earlier.Footnote 22

In the mid-1850s, London contributed financially to the enormous railway boom in the United States and suffered accordingly in the Crash of 1857.Footnote 23 In 1863, even as the American Civil War was forcing contraction on Britain’s textile industry, a financial innovation from France – the joint stock investment bank, modeled on the Crédit Mobilier, to direct liquid capital into physical investments – became a signal object of “a major bull market, in which almost 700 new companies were registered and the City was awash with speculative froth.”Footnote 24 Kynaston proceeds:

The new finance houses were not helped by the fact that during the year after their launch there took place … a wave of company promotions so relentlessly opportunistic as to darken the name of any new financial concern. “Most unblushing have been the appropriations made for services in the establishment of banks,” declared Morier Evans in his aptly named Speculative Notes (1864), asserting that “the amount of transparent jobbery almost recognized in the light of day, has exceeded that known to have existed in the great bubble period of 1824–25, or the later railway mania of 1845.”Footnote 25

Only seven years later, one of the financial entrepreneurs of 1863–1864 led another feverish bull market. Albert Grant (formerly Albert Gottheimer), whom Kynaston identifies as “the real-life Melmotte” of Trollope’s The Way We Live Now – that definitive rendering of the culture of speculative excess – himself summarized the spectacle. The year 1871, he wrote,

was a year and an era when everyone was seeking what he could make on the Stock Exchange. There is a peculiar fascination to some people in making money on the Stock Exchange. I know hundreds who would rather make £50 on the Stock Exchange than £250 by the exercise of their profession; there is a nameless fascination, and in the year 1871 the favorite form of making money on the Stock Exchange was by applying for shares, selling them at whatever premium they were at, and the money was considered made – I say considered honourably made.Footnote 26

Note, above all, the obvious irrelevance of the real assets nominally represented by the shares. More than a century later, at the peak of the IPO mini-bubble of 1983, Eberstadt participated in underwriting the first venture-backed company ever to go public with a market valuation of $1 billion. I well recall the dialogue between two traders, quoted in the Wall Street Journal on the day following the offering: “What’s a Diasonics?” “I don’t know, but we have to buy some!”

Domestic company promotions were not the only objects of speculation in the early 1870s. London saw yet another “craze for foreign loans” at the time. Paraguay, Costa Rica, San Domingo and Honduras became notorious for borrowing, according to The Economist:

immense sums which they could never have paid, and which they never meant to pay … and what is more extraordinary than all that, in several cases, they, the borrowing states, obtained scarcely any of the money because it was intercepted by the persons who framed the devices. Those who cheated the English public cheated also – and that upon the largest scale – those in whose names they borrowed.Footnote 27

The third Honduras loan in 1872 stretched the willing disbelief of the greedy herd beyond the breaking point. Its purpose was to fund “A ‘ship railway,’ by which ocean-going ships would be raised from the sea by hydraulic lifts, transported across the Isthmus on fifteen parallel tracks that would carry a giant cradle, and slid onto the water on the other side.”Footnote 28

A decade later, the“Brush Boom” ignited the London Stock Exchange with “a wave of popular enthusiasm for anything to do with the pioneering world of electricity, electric lighting and the manufacture of electrical equipment.”Footnote 29 It is worth lingering on this event, because of its significance – entirely negative – for long-term, strategic interaction between the financial capitalism of London and Britain’s version of the Innovation Economy. Certainly, it began with a bang. The Brush Electric Light Company was the target:

There was such a rush for the shares as had never been seen before in Lombard Street, the whole street being blocked by the crowd pressing to get to the bank to pay in their applications … The capital was enormously oversubscribed, all the well known City names amongst the list of subscribers, and the shares, which on allotment were to be £3 paid, were on the day of the prospectus dealt on the London Stock Exchange at £7 per share, or £4 premium.Footnote 30

The 133 percent pop would have been worthy of a dotcom IPO in 1999.

Brush proceeded to franchise its patents to subsidiary companies under the Electric Lighting Act of 1882. But its fundamental technological and legal position was challenged by “a handful of powerful bears” on the Stock Exchange even as its subsidiaries failed to develop their concessions. Thomas P. Hughes, author of the magisterial Networks of Power: Electrification in Western Society, 1880–1930, reports the denouement:

A year after the bright promise of the spring of ’82, the Anglo-American Brush Company stood revealed as a patent-holding and manufacturing company which had been founded on an arc-lighting system that was no longer outstanding in its field and on an incandescent-lamp patent of doubtful value.Footnote 31

A dozen years later, Alexander Siemens pronounced the epitaph on the Brush Boom, offering a homily on the problematic relationship between financial speculation and innovative enterprise:

However much other causes may have contributed to delay the development of electrical engineering, it is clear that the principal one must be looked for in the exaggerated expectations that were raised, either by ignorance or by design, when the general public first seriously thought of regarding electricity as a commodity for everyday use.

At that time the promoters of electric companies preached to the public that electricity was in its infancy, that the laws of science were totally unknown, and that wonders could be confidently expected from it. There was a short time of excitement to the public and of profit to the promoters; then the confidence of the public in electricity was almost destroyed and could only be regained by years of patient work.Footnote 32

That exact consequence – a premature bubble delays investment in a fundamental technology – was demonstrated a century later when the end of the first AI hype cycle in the 1980s ushered in an “AI winter” that persisted into the twenty-first century until the development of novel techniques of machine learning, as discussed in Chapter 2.

Kynaston suggests that the consequences of the Brush Boom had even more general significance, setting London firmly against financing those new industries – “above all electrical engineering, chemicals and in due course motor cars … high tech and capital intensive” – where America and Germany were establishing leadership.Footnote 33 The Brush Boom is a signal example of how financial speculation can discredit innovative technology. As we shall see, it stands out against the decisive moments, before and since, when it was precisely speculative bubbles in financial assets that enabled fundamental innovation to be funded before it was possible to assess the economic returns therefrom in any rigorous way. Again and again, it has been the opportunity for financial investors to sell shares into a rising market that has motivated investment by entrepreneurs in real assets that embody frontier technology.

If Schumpeter’s entrepreneur in principle loses other people’s money, historically financiers who have recognized the critical importance of liquidity have been able to win from speculation even when the projects they fund ultimately fail, and it is the entrepreneur and the purchasers of the original investors’ shares who lose.

In 1882, the City of London and its clients took a figurative bath in the most economically significant technological innovation of the time – and fled. Four years later, they collectively plunged into the most traditional of speculative assets in pursuit of auri sacra fames. The discovery of gold on the Witwatersrand in South Africa generated the first wave of the “Kaffir Circus” on the floor of the London Stock Exchange, as brokers fought with each other for access. Kynaston takes note of “an adage, beloved of the Stock Exchange [that] dates from about this time: ‘a mine is a hole in the ground owned by a liar.’”Footnote 34

In reality, the great South African gold boom had legs, although it had to wait for convincing evidence that innovative mining technology could open up the deep mines and that cyanide could be used to extract gold from pyretic ore. When the market did become convinced in late 1894, the boom that followed “became one of those phases of City history that almost ranked with the South Sea Bubble in terms of mythological status.”Footnote 35 The value of annual production on the Rand rose 50 percent, from £5.18 million to £7.84 million, and the net British purchase of shares to fund the increase is estimated at some £40 million. So great was the volume of trading that it spilled out from the floor of the Stock Exchange and continued after hours. When in March 1895 the police attempted to clear the area, the Battle of Throgmorton Street erupted as the brokers refused to suspend their dealing and move on.

Anticipation of the Boer War, which was to break out in 1898, finally closed down the Kaffir Circus, although Westralian promotions continued haphazardly to attract speculative interest. Under their shadow, a notorious promoter named Harry Lawson attempted to incite his own bubble in the prospective investment returns from the nascent automobile industry. Following the spectacular success of the IPO of the Dunlop Rubber Company, whose pneumatic tires enabled the cycling craze of the mid-1890s which generated its own “bicycle bubble,”Footnote 36 Lawson acquired British rights from Daimler and established the British Motor Syndicate (BMS), with the customary array of peers of the realm as directors. Its initial offering of £100,000 was followed by the launch of the Great Horseless Carriage Company by way of a £750,000 flotation. Less than a year from its IPO, the BMS was back with a proposed £3 million offering, no less than £2.7 million of which was to go to the selling shareholders, led, of course, by Lawson. This finally was too much. Kynaston muses:

Did it matter that by far the most important financial intermediary in the early history of the British motor-car industry was a crook? The answer is surely yes, for quite apart from the specific matter of the shortages of working capital adversely affecting pioneer producers such as Daimler, the Lawson saga marked the beginning of what would be an uneasy, mutually mistrustful relationship between that industry and the City. The industry, not unnaturally, feared being ripped off again; the City, just as naturally, perceived the industry was full of unprofitable “lemons” and was reluctant to subscribe or encourage the subscription of further capital. The analogy with the electrical industry, following the catastrophic “Brush Boom” of the early 1880s, is painfully obvious.Footnote 37

In May 1910, London saw the last explosion of speculation before the First World War. “Rubber Fever” was the occasion, as the prospects of cheap rubber from the plantations of the east seized the city’s imagination. On the floor of the Stock Exchange, “the scenes were even more frantic than those experienced during the Kaffir Boom fifteen years earlier,” but in a matter of months it was over.Footnote 38

The Great American Trust Bubble

As the London Stock Exchange was immunizing itself against the funding of innovative technology, New York demonstrated an even more extreme reaction to the economic consequences of that great wave of transformational technology, the railroads. Throughout the industrializing world, the radical reduction in manufacturing and transportation costs occasioned by the railroad construction boom reflected parallel revolutions in the scale of production and the extent of markets. While real incomes rose as never before, everywhere the response of “the dealers … in any branch of trade and manufactures” was exactly as Smith had reported more than 100 years before: “to widen the market and to narrow the competition.”Footnote 39 In Europe, cartels predominated. In the United States,

the Sherman Act, which passed as a protest against the massive number of combinations that occurred during the 1870s and 1880s, clearly discouraged the construction of loose horizontal federations of small manufacturing enterprises formed to control price and production.Footnote 40

In place of cartels, the trust movement was born, dramatizing a classic crux in the Three-Player Game: the state moves to enable competition in the market economy, and financial capital counters to freeze it in place. In order to pursue its goal, the trust movement required active, liquid markets in the securities of the industrial companies and franchised utilities that were its stock in trade. In this it was served by the regulatory reforms that the NYSE had enacted in response to the long deflation of the same “first Great Depression,” from 1873 to 1893, that had motivated the architects of the trusts. Reduced returns from the railroad securities that had utterly dominated trading induced a search for new instruments. The reforms in New York, which tightened listing requirements and fostered collaboration with the less regulated New York Curb Exchange, enabled the NYSE to establish itself as “the blue chip market, creating an imprimatur of quality … [that] greatly advanced the education of unsophisticated American investors of the late nineteenth century.”Footnote 41

In my hands is a remarkable document from that time, a thick volume whose pages have begun to crumble: John Moody’s The Truth about the Trusts: A Description and Analysis of the American Trust Movement, a first edition of which I found in my father’s library some twenty years ago. On his way to establishing his firm as an authority on the financial status of American business, Moody provided detailed analyses of the formation of the 7 “Great Industrial Trusts” and summary information on no fewer than 298 “Lesser Industrial Trusts,” plus 13 “Important Industrial Trusts in process of Reorganization or Readjustment,” 8 “Telephone and Telegraph Consolidations,” the 103 “Leading Gas, Electric Light and Street Railway Consolidations,” the 6 “Great Steam Railroad Groups,” and 10 “Allied Independent Steam Railroad Systems.”Footnote 42 From this exhaustive and exhausting exercise emerges a robust, meta-economic defense of “the modern Trust” as “the natural outcome or evolution of the societal conditions and ethical standards which are recognized and established among men to-day as being necessary elements in the development of civilization.”Footnote 43

To those schooled in the doctrine of free and efficient markets, Moody’s rhetoric must seem alien, even pernicious. But writing at the intersection of the market economy and financial capitalism as each reached its first full maturity on the back of 100 years of globalizing industrialization, Moody correctly read the trust movement as a natural, even necessary, response to the competitive forces that had been unleashed at a scale and with a ferocity never before experienced. The trust movement represented an effort to control the market economy in order to ensure sufficient cash flows to validate the financial obligations of market participants.Footnote 44 In doing so, it leveraged a genuine innovation in financial engineering that linked the combinations of industrial assets with the value of the financial assets that represented them. For the value of the newly created trusts was to be based not on the historic rate of dividends paid by their constituents but on the prospective dividend-paying capacity of the combination. Of course, in all previous bubbles – whether or not they proved to have funded productive assets – prices had decoupled from backward-looking measures of value by definition. But in the case of the trusts, forward-looking benchmarks of value were explicitly defined at the outset.

Moody rationalized the much-criticized phenomenon of “watered” capital – shares issued in excess of the book value of an enterprise’s hard assets:

In forming combinations of all kinds, a certain amount of the securities are usually issued for good-will, patent rights, franchises and so forth. Very often stock is issued without its specific purpose being explained beyond the statement that the amount issued is based upon the earning power of the property … The “good-will” or “watered” stock usually anticipates the value of the monopoly element, and, of course, if this feature does not turn out to be as important as expected, there frequently is no other asset back of the “good-will” or watered stock, and a general collapse follows.Footnote 45

This conceptual innovation has survived to define the process of investment analysis ever since.

Chandler notes that access to the liquid (whether watered or not) shares of the trusts proved powerfully attractive:

The manufacturers who organized trusts were surprised by Wall Street’s interest in obtaining their trust certificates … Manufacturers soon realized that they could use the growing market as a source of funds for working and investment capital. They were also quick to appreciate that the demand for industrial securities enhanced the values of their own companies. Expanded demand for industrial securities permitted manufacturers to obtain a handsome rate of exchange when they completed a merger by turning over the stock of their little known small enterprises for that of a nationally known holding company.Footnote 46

A sure indication that the speculation would end in tears was the fact that “financiers began to take sizable blocks of stock as payment for arranging and carrying out a merger.”Footnote 47 The same signal was evident at the peak of the credit bubble of 2004–2007, when the banks that originated complex derivatives chose to hold their products as if the AAA credit ratings they had participated in fabricating had substantive meaning.

Chandler cites sources that count 212 combinations in the years 1898–1902 and the contemporaneous disappearance of 2,634 firms through merger. But by 1903 the trust bubble had burst. The Wall Street Journal compiled a table, reproduced in Moody’s work, to show that from peak to trough the aggregate market value of the leading 100 industrial stocks had declined by 43.4 percent.Footnote 48 “No sympathy,” Moody asserted, “needs to be wasted on the many noisy speculators who are now loudly condemning all Trusts because they themselves happened to be caught in a speculative crash.”Footnote 49

In a broader sense, no sympathy need be expended regarding the trust bubble itself, as investors had sought to capitalize on prospective monopoly profits that were apparently accessible at one moment of time, as if the dynamics of competition – driven ultimately by technological innovation – could be captured and frozen. And yet, even as it failed, this doomed effort to invoke Cash and Control in the face of the economic and financial uncertainty occasioned by technological innovation demonstrates the historical relevance of the strategy I discovered eighty years later.

The Spirit of Speculation

Ten unsustainable bull market runs on the London Stock Exchange in ten decades and the trust bubble in New York: such a review must dispel any notion that speculative excess is a distinctive feature of more recent times. On the contrary, the spirit of speculation is ever present. One of the pleasures of writing this book has been the discovery of previously unknown fellow travelers. One such is the once-prominent, now forgotten, Wall Street legend Philip Carret, who published a how-to book provocatively titled The Art of Speculation in 1927, just when his generation’s maximum opportunity was at hand. Much of Carret’s book is a sensible tutorial on the typology of financial instruments, on the structure of balance sheets and income statements, and on the more or less treacherous strategies for attempting to win easy money from the market. But he goes deeper, as when he identifies the stock market speculator’s economic role as a provider of liquidity – “increased marketability” is Carret’s term – for “long-pull” investors.Footnote 50 Carret specifies that “the road to success in speculation is the study of values” but goes on to observe, after paying due heed to management’s discretionary authority to run a business in disregard of the interests of the stockholders, that there is “no logical basis for any assumption regarding the relation between book and market values.”Footnote 51

In line with the theme of this chapter, Carret offers a splendid prospect to his novice reader: “Limitless horizons stretch before the would-be speculator. All the commodities of commerce are possible subjects for his trafficking.”Footnote 52 Carret is most compelling when he describes the challenge to the studious speculator represented by the “ripples and waves” of price movements driven by mere gamblers:

To attempt to trade on such movements is mere gambling with the odds against the trader by a considerable margin. It is astounding that thousands of otherwise intelligent persons persist in trying to make money in this way. Commonly accepted figures of somewhat dubious origin are frequently cited to show that 90% to 95% of all margin players lose money in the stock market. The deep-seated gambling instinct, the well-founded belief that in widely fluctuating markets there must be opportunities for profit nevertheless bring fresh recruits to the brokerage offices in constant streams.Footnote 53

Carret’s gamblers were rediscovered two generations later by theorists who have attributed the emergence of bubbles to the activity of mindless “noise traders.” Writing as the bull market that would peak in October 1929 gathered force, Carret had truly seen nothing yet.

The Super-bubble

For almost all of the two generations that followed the Crash of 1929, the financial markets were “repressed,” as Carmen Reinhart and Kenneth Rogoff put it.Footnote 54 Banking regulation, foreign exchange controls and generalized risk aversion constrained systemic speculation for almost half of the twentieth century. In the United States, the first stirrings of postwar exuberance could be discerned in the “-onics” boom beginning in the early 1960s, so named for the electronics companies sponsored by the Defense Department and NASA, and in the “Money Game” – the go-go stock market of the late 1960s. The stagflation years of the 1970s deferred the recovery of exuberance, a recovery that I observed first-hand in the reawakening of the market for IPOs in 1983. To us, those few months seemed like a peak of frenzy, but they amounted to mere foothills relative to the spectacular excess of the dotcom/telecom bubble.

The mini-bubble in the IPO market of 1983 marked the onset of an unprecedented global phenomenon, a generation-long “super-bubble,” to use George Soros’s term. During the course of twenty-five years, contemporary financial institutions and markets proved themselves as prone to speculative excess as those of the laissez-faire nineteenth-century regime of small-state capitalism, when, across the industrializing world, public sectors were on the order of 10 percent of national economies or less. In the modern case, however, the breaking of each wave of speculation generated only modest recession in the real economy. As reflected in the reduced volatility of the time series that register economic fluctuations, this came to be known as the Great Moderation.

Behind the seeming stabilization, the world economy entered a leverage cycle that reached historically unprecedented levels.Footnote 55 It was punctuated by a sequence of bubbles in relatively discrete categories of financial assets: the junk bonds in the late 1980s that fueled a takeover boom in the United States; emerging market debt in the mid-1990s; the dotcom/telecom bubble in the stock market in 1998–2000. After that bubble burst at the turn of the millennium, the focus became residential property, not only in the United States but also across Europe and in key emerging markets, from Central Europe to China. Over the whole period, from 1981, the debt of the US private sector rose from 123 percent of GDP to 290 percent, household debt doubled to 100 percent of GDP, and the ratio of household debt to disposable income increased from 65 percent to the unsustainable level of 135 percent.Footnote 56

The parallel transformation of Wall Street in the course of a generation can also be quantified. In 1970, the aggregate financial assets of the nation’s security brokers and dealers were $16 billion. During the first half of the 1980s, as the new business model took hold, total financial assets surged from $33 billion in 1979 to $185 billion in 1986. Following a brief pause, growth exploded in the 1990s as balance sheets increased by more than 5 times to almost $1.5 trillion in the eleven years from 1990 to 2001. From there they doubled in the next five years, reaching $3 trillion in 2007.Footnote 57

Taking an even longer view, Hyun Shin shows that the growth in the assets of the financial sector – commercial banks and securities broker-dealers – moved in step with the assets of the nonfinancial corporate and household sectors from the early 1950s to 1980, each rising by a factor of ten. Then came an enormous divergence. The balance sheets of the commercial banks remained aligned with those of nonfinancial corporates and households, all rising to the 2007 peak by slightly less than ten times. But as the investment banks – the broker-dealers – transformed themselves from agents into principals, they grew their increasingly leveraged assets by no less than a factor of 100.Footnote 58

The succession of bubbles in different classes of financial assets that collectively constituted the super-bubble confirmed the banality of the phenomenon in general terms. But, cumulatively, as their consequences were repeatedly contained by the effective interventions of governments and regulators, they transcended the banal and set the stage for a phenomenon that truly was different: the first global crisis of big-state capitalism.