Transparent pricing policy for journals

Transparent pricing policy for journals

We aim to price our journals fairly and transparently. In particular, our subscription prices should reflect the amount of subscription content in a journal.

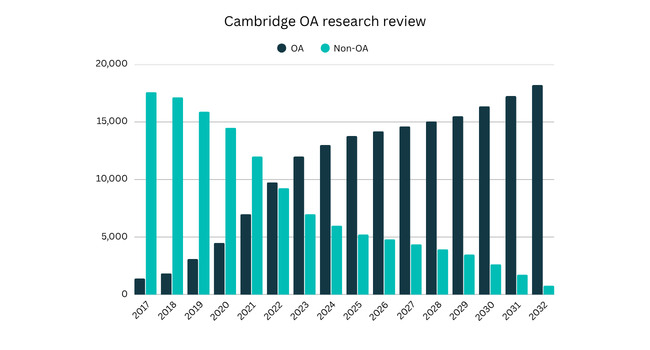

We are undertaking an ambitious transition to open access, with a clear pathway to make the vast majority of our research articles open by the early 2030s. As the proportion of open access content in our journals increases, we reduce subscription (“read”) costs proportionally and fairly to reflect the changing balance of subscription-funded content.

It is unfair to ‘double dip’ by charging subscribers for open access content that has received funding through an institutional open access agreement, an article processing charge (APC), the Cambridge Open Equity Initiative, sponsorship from a third party, or some other mechanism.

Transparent pricing policy for journals

We aim to price our journals fairly and transparently. In particular, our subscription prices should reflect the amount of subscription content in a journal.

We are undertaking an ambitious transition to open access, with a clear pathway to make the vast majority of our research articles open by the early 2030s. As the proportion of open access content in our journals increases, we reduce subscription (“read”) costs proportionally and fairly to reflect the changing balance of subscription-funded content.

It is unfair to ‘double dip’ by charging subscribers for open access content that has received funding through an institutional open access agreement, an article processing charge (APC), the Cambridge Open Equity Initiative, sponsorship from a third party, or some other mechanism.

Our pricing policy includes 3 components:

- An inflationary increase that is applied to all journals to reflect changes to the overall cost base of our journals programme. This increases may vary between print and online formats.

- Occasionally, for exceptional reasons such as a dramatic change in the type of content that a journal publishes, we adjust the price of a specific journal, upward or downward.

- For online-only subscriptions, we then apply a price correction to prevent double-dipping and to reflect changes in content funded by subscription charges (that is, non-open access content and open access articles that were not funded by an APC, an institutional agreement, the Cambridge Open Equity Initiative, or other means). This adjustment is generally limited to a band of –5 % to +5 %.

As we continue to transition our journal research to fully open access, we will be conducting further reviews of our journals pricing policy to ensure we continue to operate a fair and sustainable model.

Worked example

1) Annual inflationary price change: +6 %

2) One-off, exceptional price change: 0 %

3) Subscription content price change (see below): -5 %

Overall change to the journal’s online subscription price: +0.7 %

(This is (106 % x 95 %) - 100 %)

Changes in subscription content

The subscription content component of our pricing policy (item 3 in the above) determines how we reduce the prices for online-only subscriptions during the transition to open access.

The price change is the percentage change in the total amount of subscription content over the two most recent three-year periods. The following two examples show how article data from 2020–2023 journal volumes was used in 2024 to determine the subscription content price change applied to the online-only prices for 2025 journal volumes:

The price change cap and the three-year measurement period help us avoid unnecessary price changes due to transient fluctuations in the amount of subscription content a journal publishes each year.

We will continue to monitor our price caps to ensure they remain appropriate and allow journal subscription prices to be sufficiently reduced over time in line with the transition to open research. In special circumstances we may implement additional journal price decreases.

Example 1: a decrease in subscription articles

Step 1: Total number of subscription articles: 2020-2022 = 475; 2021-2023 = 445

Step 2: Change in total number of subscription articles = -30

Step 3: Percentage change = -6.3 %

Step 4: Cap the price change to between -5 % and +5 % = -5 %

Subscription content price change component for 2025 = -5 %

Example 2: an increase in subscription articles

Step 1: Total number of subscription articles: 2020-2022 = 475; 2021-2023 = 505

Step 2: Change in total number of subscription articles = +30

Step 3: Percentage change = +6.3 %

Step 4: Cap the price change to between -5 % and +5 % = +5 %

Subscription content price change component for 2025 = +5 %

Notes

- Gold OA articles that receive no open access funding are supported by journal subscriptions, and therefore these articles are counted as subscription articles in the pricing calculations.

- A few article types, most notably conference abstracts, are excluded from the calculation.

- The subscription content pricing component is only applied to online-only subscriptions. Subscriptions that include a print copy of a journal are not affected.

- The subscription content pricing component is only applied to online-only subscriptions. Subscriptions that include a print copy of a journal are not affected.

- In rare cases, we have pre-existing agreements with an academic society that affect our ability to fully implement the subscription content pricing component.