1. Introduction

In the early 1990s, the Spanish government ended its strategy of creating “national champions” to deter potential European competition. The newly formed Banco de Bilbao Vizcaya (BBV) and Banco Santander remained relatively small, regional, and retail-focused intermediaries, with a limited presence in the wider European and global banking landscape. However, between 1994 and 2007, both institutions underwent a profound transformation, becoming global, universal banks through a series of strategic amalgamations, particularly in Latin America. In 1995, Santander ranked 55th and BBV 47th in the world by total assets. By 2005, Santander had risen to 10th place and Banco de Bilbao Vizcaya Argentaria (BBVA) to 31st (Guillén and Tschoegl, Reference Guillén and Tschoegl2008, pp. 68–69).Footnote 1 The acquisitions in Latin America proved instrumental in helping both banks withstand the global financial crisis of 2007.

The pace of amalgamations lost momentum after 2012. Yet, by 2024, Spanish banks were market leaders across the most significant Latin American economies, with only the Brazilian giant, Itaú, surpassing them in terms of asset size. This unprecedented development has attracted much scholarly attention as various authors have sought to explain the emergence of a multinational retail banking model, a phenomenon previously unseen.

The contributions of Pablo Martín-Aceña have been central to understanding the internationalization of Spanish banks in Latin America (Martín-Aceña, Reference Martín-Aceña2007; Martin-Aceña, Reference Martin-Aceña2008; Cuevas et al., Reference Cuevas, Martín-Aceña and Pons2018, Reference Cuevas, Martín-Aceña and Pons2020, Reference Cuevas, Martín-Aceña and Pons2021). Martín-Aceña’s work complemented that of other Spanish and international scholars, as well as corporate histories commissioned to mark the anniversaries of banks (González et al., Reference González, Anes and Mendoza2007; Martín-Aceña, Reference Martín-Aceña2007; Guillén and Tschoegl, Reference Guillén and Tschoegl2008).Footnote 2 Other contributions explored the specific advantages Spanish banks held in Latin America (Batiz-Lazo et al., Reference Batiz-Lazo, Mendialdua and Zabalandikoetxea2007; Minda, Reference Minda2009; Jiménez and Narbona, Reference Jiménez, Narbona, García Delgado, Alonso and Jiménez2010).

This article revisits and reinterprets the literature on Spanish banks in Latin America, foregrounding the contributions of Martín-Aceña. Our empirical base includes 41 first-round interviews (each lasting 1–2 hours) and 2 follow-up interviews with senior executives, media personnel, IT and systems managers, and regulatory officials in Spain, Argentina, Brazil, Chile, Peru, and Mexico. These oral sources offer unique insights absent from corporate records or standard archives (Hood, Reference Hood, Barber and Peniston-Bird2009; Austin et al., Reference Austin, Dávila and Jones2017; Jones and Comunale, Reference Jones and Comunale2019). These were combined with publicly available sources such as annual reports and newspaper items. See further the methodological appendix.

This research deepens previous contributions around six dimensions: the rationale behind investment decisions; the processes of acquisition and divestment; divergent integration strategies and their consequences; human resources and managerial practices (including retail bank branch restructuring, digital product development, and local leadership appointments); and strategic planning in both new and mature markets.

On the one hand, both Santander and BBVA achieved success in securing significant market share while pivoting across those six dimensions, while others, with longer regional histories, failed to develop comparable operational or technological capabilities. This was particularly evident in the cases of major American, British, and German banks such as Citi, HSBC, Lloyds, and Deutsche Bank. On the other hand, Spanish banks’ superior deployment of digital infrastructure was transformative, providing a clear advantage over both global and local competitors (Avendaño Ayestarán and Moreno, Reference Avendaño Ayestarán and Moreno2005; Kase and Jacopin, Reference Kase, Jacopin and Molyneux2007).Footnote 3

In addition to becoming a source of comparative advantage, technological innovation was central to integrating Latin American acquisitions, particularly through branch expansion and systems interoperability. A key driver of this integration was the creation and deployment of robust, flexible core banking platform (Weill et al., Reference Weill, Ross and Robertson2006; Walker and Morris, Reference Walker and Morris2021). While there is no single agreed definition of core banking, we adopt the definition provided by interviewees as “a granular system of record of all data necessary to comply with regulations for all operations of a bank.”Footnote 4

The remainder of this article examines the strategic, technological, and organizational factors behind the transformation of Santander and BBVA from domestic institutions into global leaders in retail banking. Drawing on Martín Aceña’s work, alongside the framework of Guillén (Reference Guillén2005) and Guillén and García Canal (Reference Guillén and García Canal2010) of intangible assets, we argue that it was not financial strength or technological invention, but organizational capabilities that became the true differentiators, particularly in contrast to local competitors and retreating European and North American banks.

We begin by revisiting the domestic and international banking context of the 1990s and 2000s, which spurred the overseas expansion of Spanish banks. Particular attention is paid to intangible assets such as managerial expertise and systemic integration, which created unexpected and durable competitive advantages. The third section explores three underexamined dimensions: the adoption of interoperable IT systems and common core banking platforms, human capital strategies that combined local insight with Spanish managerial models, and organizational architectures that supported both cohesion and adaptability across markets. In a fourth section, we seek to contrast the trajectories of both banks after the crisis of 2007 and during the 2010s, documenting the continued influence of earlier strategic and technological choices. The distinction between technological adoption and transformative deployment constitutes our key theoretical contribution, advancing both the framework of intangible assets by Guillén (Reference Guillén2005) and Guillén and García Canal (Reference Guillén and García Canal2010) together with Martín Aceña’s institutional perspective.

2. Revisiting banking consolidation in Latin America

2.1. The technological footprint of the expansion saga

Contributions exploring the globalization of retail banking span nearly three and a half decades, beginning with the pioneering study of Tschoegl (Reference Tschoegl1987). Studies documenting the rise of Spanish banking multinationals highlight three key aspects. First, Spain had no recognized comparative advantage in banking, information technology, or wholesale finance. Second, their expansion formed part of a broader transformation in foreign direct investment (FDI), whereby firms from non-core economies began to achieve global prominence (Guillén and García Canal, Reference Guillén and García Canal2010, Reference Guillén and García Canal2013). Third, it marked the first large-scale globalization of retail banking (Tschoegl, Reference Tschoegl1988, Reference Tschoegl2002a, Reference Tschoegl2002b).Footnote 5

Yet, most contributions looking at the growth of Spanish banks were published between 2007 and 2012, coinciding with the global financial crisis. This concentration left the post-crisis period underexplored, particularly the consolidation of Spanish banking multinationals during the 2010s. Moreover, the transformative impact of information and communication technologies (ICTs), including core banking systems, mobile banking, and digital applications, has been insufficiently examined.

These omissions are significant, as technological change constitutes a fundamental component of globalization. ICTs, as the backbone of modern global interconnectedness, have drastically reduced physical and operational distances and enabled the emergence of integrated financial systems. While earlier studies focused on identifying the principal drivers of retail banking globalization and assessing its geographical and developmental impacts, our study takes a different approach. We explore the role that information technology played in this process. More fundamentally, we questioned whether technology enabled the global expansion of Spanish banks or whether their strategic vision shaped the adoption and development of new technologies.

The trajectory of Spanish banks’ outward FDI reflects many of the distinctive features associated with what Guillén and García Canal (Reference Guillén and García Canal2010) describe as the “new multinationals.” Spanish firms, including banks, did not internationalize based on proprietary technological innovations alone. Instead, they relied heavily on other intangible assets, such as organizational and managerial capabilities, political and network-related skills, and project-execution know-how. This strategic emphasis is reflected in several characteristics of their internationalization: a strong regional concentration of investment, particularly in Latin America; a preference for joint ventures and alliances in the initial phases; and an eventual transition toward full acquisitions and wholly owned greenfield investments as they consolidated their presence abroad. These patterns suggest that, rather than being passive recipients of technological diffusion, Spanish banks actively shaped the deployment of ICTs to support their broader strategic objectives and expand their international footprint.

2.2. The rise of the Spanish banking leviathans

The expansion of Spanish banks in Latin America, beginning in the mid-1990s, must be seen against a backdrop of unique circumstances. These included the internal transformation of Spain’s banking system during the 1980s and 1990s, Spain’s accession to the European Economic Community in 1986, and the forthcoming implementation of the Second Banking Coordination Directive (89/646/EEC) (Cuervo, Reference Cuervo1988; García Ruíz, Reference García Ruíz, Vargas-Machucha Salido and Martín2024). All these led to the creation of two banking leviathans.

The creation ex nihilo moment took place after decades of stability among Spain’s seven largest financial institutions. Banco de Bilbao and Banco de Vizcaya initiated change by merging in 1988 to form BBV (Arroyo et al., Reference Arroyo, Larrinaga and Matéz2012; García Ruiz, Reference García Ruiz2017; Vargas-Machuca Salido and Arroyo Martín, Reference Vargas-Machuca Salido and Arroyo Martín2024). The domestic concentration of the Spanish banking sector culminated in 1999 with the formation of two giants. On the one hand, Banco Santander merged with Banco Central Hispano (BCH) to create Banco Santander Central Hispano (BSCH), a conglomerate with total assets of €239 billion, 8,681 branches, and 106,519 employees (García Ruiz, Reference García Ruiz2007).Footnote 6 Co-chaired by Emilio Botín (1934-2014) and José María Amusátegui, BSCH reverted to the Santander name in 2007, reaffirming the primacy of the Botín legacy.Footnote 7

On the other hand, as part of its struggle to regain leadership in the Spanish banking sector, the BBV, in late 1999, merged with Corporación Argentaria, which had just completed the process of amalgamation of several government-owned banks and subsequent privatization. In principle, the union was presented as a merger of equals. Emilio Ybarra (1936-2019) and Francisco González assumed the co-chairmanship of the new entity, with Pedro Luís Uriarte as CEO, and a board of directors comprising all the BBV and Argentaria board members. However, the process of taking control differed from that of Santander. The most experienced BBV directors were finally excluded in early 2002, when a case of alleged corruption saw Ybarra step down, along with many members of the board from the Basque group. From December 2001, Francisco Gonzalez, formerly at Argentaria, became the sole president of BBVA.

Following these mergers, Santander and BBVA commanded around 90% of domestic banking operations. Both had gained critical expertise in managing internal mergers (Calderón Hoffmann and Casilda Béjar, Reference Calderón Hoffmann and Casilda Béjar2000; Toral Cuetos, Reference Toral Cuetos2004). This knowledge and experience would prove essential for overseas expansion.Footnote 8

Spanish retail banking was, however, a fully mature market tending to saturation (Calderón Hoffmann and Casilda Béjar, Reference Calderón Hoffmann and Casilda Béjar2000). According to Sierra Fernández (Reference Sierra Fernández2007), at the beginning of the 1990s, only 40% of the adult population in Latin America held a bank account. In Spain, the figure stood at 99%. This suggests that while the business opportunities for retail banking in Latin America in the early 1990s were considerable, so too were the risks.

At the time, opportunities opened within the region after decades of financial regulation that had severely limited foreign capital inflows and excluded fully owned foreign participants in most markets (Cuevas et al., Reference Cuevas, Martín-Aceña and Pons2021). Things changed radically in Latin America following two major economic crises, both initiated in Mexico in 1982 and 1994, respectively (Del Ángel et al., Reference Del Ángel, Bazdresch Parada and Suárez Dávila2005; Tschoegl, Reference Tschoegl, Honohan and Laeven2005). These crises compromised the financial viability of several local players. They also resulted in other broad-scope changes following the liberalization winds of the Reagan/Thatcher era, the implicit agreements of the so-called Washington Consensus, and the demands for openness of some international treaties, such as the North American Free Trade Agreement between the US, Canada, and Mexico, signed in 1992. It was within this context that a drive for international expansion took place for the Spanish banks.

2.3. Main factors underpinning international expansion

Several interpretations have been proposed to explain the timing and geography of Spanish bank expansion. Some propose that the international expansion of Spanish banks was dominated by the rationale of “following the client” (Berges et al., Reference Berges, Ontiveros, Valero, Malo de Molina and Martin-Aceña2012; Pons, Reference Pons2020; Cuevas et al., Reference Cuevas, Martín-Aceña and Pons2021; Martín-Aceña, Reference Martín-Aceña2009), whereby banks follow their corporate clients abroad, particularly in sectors like telecommunications (Calvo, Reference Calvo2017) or construction (Torres 2009). Originally proposed by Grubel (Reference Grubel1977), this explanation does not hold for Spanish banks in Latin America. First, empirical studies document that foreign investments by Spanish banks did not mirror the trajectories of their corporate clients (Batiz-Lazo et al., Reference Batiz-Lazo, Mendialdua and Zabalandikoetxea2007). Second, archival evidence shows that banks like Santander and BBVA had already established representative offices in the region as early as the 1940s and 1950s. Santander’s early acquisitions in Argentina (1963), Panama (1967), and Chile (1979), among others, together with BBVA’s antecedents in Banco Exterior de España and Banco de Vizcaya, suggest longstanding regional engagement (Santander Annual Report, 1989; González et al., Reference González, Anes and Mendoza2007; Martín-Aceña, Reference Martín-Aceña2007; Arroyo et al., Reference Arroyo, Larrinaga and Matéz2012).

These early activities were peripheral to the subsequent mergers and expansions, and interviewees during our research confirmed that the strategic focus lay in serving local markets rather than supporting Spanish multinationals.Footnote 9 While executives like Marcial Portela (vice president and CEO of Telefónica, 1996–1997) brought valuable experience from corporate roles abroad, the primary objective was always to engage domestic customers in Latin America.

Extant contributions to the growth of Spanish banks in Latin America also highlight the importance of cultural and linguistic ties for the development of Spanish investment in the region (Uriarte, Reference Uriarte2000; García Delgado et al., Reference García Delgado, Alonso and Jiménez2008; Jiménez and Narbona, Reference Jiménez, Narbona, García Delgado, Alonso and Jiménez2010). This was unanimously stressed by all interviewees. In relation to the environment, one interviewee outlined that for Emilio Botín, Latin America was “our natural place of space because of historical affinities, language, and understanding of (their) financial needs.”Footnote 10

2.4. Kick-starting the amalgamation process in Latin America

Santander and BBVA pursued different paths in executing their international strategies. In 1995, Emilio Botín committed $5 billion to Santander’s cross-border expansion, commissioning Goldman Sachs to identify acquisition targets. This sum is equivalent to BBVA’s inaugural investments in Latin America, yet sufficient for scarcely a dozen such banks and amounting to merely one-fifth of Barclays’ prevailing share valuation.

The process at Santander was led by Santander Investment, under Ana Patricia Botín, with José María Yubero overseeing operational integration and Ignacio Rasero managing commercial assimilation.Footnote 11

Following the 1999 merger with BCH, Santander reviewed and selectively integrated BCH’s Latin American holdings, although these were generally smaller and less profitable than Santander’s own targets and were often divested.

BBVA’s strategy, as devised by Uriarte’s team, reflected its precarious position in 1994, marked by executive departures and falling share prices. Instead of compiling a list of targets, BBVA launched the “Programme of the Thousand Days,” focusing on partial stakes in key markets including Colombia, Peru, Argentina, Chile, and Brazil. This plan, presented to the Board in October 1994, involved a strategy of partial investments in prominent financial institutions, with the objective of gradually increasing its shareholdings to achieve control.Footnote 12

One key event involved Probursa in Mexico. BBVA, having acquired a 20% stake during its privatization in 1992, faced losses following the peso crisis. While divestment was considered, Uriarte and Ybarra opted to increase BBVA’s stake and sought regulatory approval from the Zedillo administration.Footnote 13

In parallel, BBVA was invited by the Brescia Group to jointly acquire Banco Continental in Peru. Despite initial hesitations, BBVA outbid Santander and secured the acquisition in June 1995. In the same month, BBVA also finalized its majority stake in Probursa. This strategy marked the beginning of BBVA’s transformative expansion in the region.

Figure 1 summarizes BBVA’s regional investments, which intensified from the mid-1990s. In Mexico, BBVA acquired Banco de Oriente and Banca Cremi in 1996, forming BBVA-Probursa under Vitalino Nafría. In Peru, BBVA and the Brescia Group took 60% of Banco Continental, increasing to 75.14% by 1996 and launching BBVA Banco Continental in 1998. In Colombia, BBVA raised its stake in Banco Ganadero from 40% in 1995 to 55% by 1998 (Arroyo et al., Reference Arroyo, Larrinaga and Matéz2012; Vargas-Machuca Salido and Arroyo Martín, Reference Vargas-Machuca Salido and Arroyo Martín2024).

BBVA in Latin America, 1960–2024.

Figure 1 Long description

The timeline illustrates BBVA's acquisitions and sales in Latin America from 1960 to 2024. It begins with Financiera de Comercio Exterior in Uruguay in 1954, followed by Banco Exterior in Paraguay and Panama in 1967. Banco Exterior in Nicaragua was acquired in 1977 and Financiera Inmobiliaria in Ecuador in 1978. Banco Exterior in Argentina was acquired in 1980 and Banco Bilbao-Panamá in 1983. The timeline shows Banco Ganadero in Colombia acquired in 1996, Banco Provincial in Venezuela in 1996 and Banco Francés del Río de la Plata in Argentina in 1996. BBVA Brasil was sold in 2003 and BBVA Chile was sold in 2018. BBVA Bancomer in Mexico was formed in 2000, with Hipotecaria Nacional acquired in 2004. The timeline ends with BBVA's presence in Peru, Uruguay, Paraguay, Colombia, Argentina, Venezuela, Chile and Mexico in 2024.

BBVA’s largest investment came in Argentina with Banco Francés, which was acquired in 1996 and expanded through mergers in 1997 and 1999. In Venezuela, BBVA became the main shareholder of Banco Provincial in 1997. It also acquired banks in Puerto Rico and entered Brazil by purchasing Banco Excel Económico for $853 million in 1998. In Chile, BBVA bought 44% of Banco Hipotecario, forming BBV Chile.Footnote 14 By the end of 1998, BBVA had invested $5.4 billion, with 19.8% of its assets in Latin America. The turning point came in 2000 when BBVA’s $1.4 billion acquisition of Bancomer merged with BBVA-Probursa and Banca Promex to form BBVA-Bancomer, commanding a 30% market share of the domestic market (González et al., Reference González, Anes and Mendoza2007; Del Angel, Reference Del Angel2007; Del Ángel, Reference Del Ángel2012).

Expansion was not without friction. After BBV’s 1999 merger with Corporación Argentaria, the new chairman, Francisco González, initially skeptical of Latin America, halted new acquisition projects and sold Banco Excel at a loss. Nevertheless, he failed to block the Bancomer deal, which proved to be BBVA’s most profitable investment in the long-run.Footnote 15 External pressures also arose, for instance, in 2001, the Argentine Corralito crisis curtailed operations, and BBVA later divested from Brazil, Puerto Rico, Panama, and Paraguay between 2003 and 2019. It also exited pension fund businesses in four countries in 2012.

Figure 2 outlines Santander’s expansion, which contrasts with BBVA’s. Santander favored full ownership over partnerships. In 1995, it acquired Banco Interandino and Banco Mercantil in Peru, merging them in 1996 to form Banco Santander Peru. In the same year, it began buying into Banco Osorno y La Unión in Chile, eventually securing 70% ownership.

Santander in Latin America, 1960–2024.

Figure 2 Long description

The timeline illustrates Santander's expansion in Latin America from 1960 to 2024. Key events include the acquisition of Banco El Hogar Argentino in 1963, Banco Santander y Panamá in 1967 and Banco Condal Dominicano in 1976. In 1995, Banco Mercantil and Banco Interandino in Peru were acquired and merged to form Banco Santander Peru. The timeline also shows the acquisition of Banco Rio de la Plata in 1997, Banco Comercial Antioqueño in 1997 and Banco de Venezuela in 1997. Santander's presence in Brazil is marked by the acquisition of Banco Bozano/Meridional in 2000 and Banco Real in 2007. The timeline continues with the establishment of Santander Uruguay in 2007 and Santander México in 1997. The expansion strategy includes full ownership and mergers, with significant developments in Argentina, Brazil, Mexico and Chile.

Figure 2 shows how Santander’s pivotal year was 1997, when it finalized the acquisition of Banco de Venezuela and purchased Banco Mexicano, rebranding as Banco Santander Mexicano. In Colombia, it took 55% of Banco Comercial Antioqueño and acquired Invercrédito. In Argentina, Santander secured 35% of Banco Río de la Plata, later raising its stake to 51% to form Santander Río. In the same year, it entered Brazil by acquiring Banco Geral do Comércio. At this point, Santander was positioned as Latin America’s leading bank, with a 24% market share, surpassing all other Spanish banks combined (Martín-Aceña, Reference Martín-Aceña2009).

BCH, which merged with Santander in 1999, had taken a more conservative approach. Through O’Higgins Central Hispano (OHCH), formed with Chile’s Luksic Group, BCH focused on shareholding investment rather than management control (Sierra Fernández, Reference Sierra Fernández2007). OHCH acquired banks in Chile, Paraguay, Uruguay, Argentina, Mexico, and Bolivia between 1995 and 1998 (Martín-Aceña, Reference Martín-Aceña2009). Most were later divested or absorbed, except for those in Chile, Argentina, and Mexico.

Santander’s strategy in Brazil intensified in 2000 with the acquisitions of Banco Bozano Simonsen, Banco Meridional, and Banespa, the latter purchased for €5.018 billion. In 2007, the acquisition of Banco Real, through the ABN AMRO consortium, doubled Santander’s market presence, making it the third-largest bank in deposits and second in loans (Santander Annual Report, 2000 and 2007).

Elsewhere, Santander increased its stake in Banco Río to 80%, merged with Banco Tornquist, and expanded its Argentine network by acquiring 482 Citibank branches. In Venezuela, it acquired Banco de Caracas in 2000. In Mexico, it bought Grupo Financiero Serfin, and in Chile, it increased its holding in Banco Santiago to 79%, enabling its merger with Banco Santander Chile.

Santander’s expansion was not without internal tensions. After merging with BCH, divisions emerged between the newly acquired “Ana Banks,” led by Ana Patricia Botín and Ignacio Rasero, and “Matías Banks,” managed by Matías Rodríguez Inciarte. Power struggles followed, prompting Ana Patricia Botín’s temporary departure. Emilio Botín ensured continuity by establishing the America Division under Francisco Luzón (1948-2021) and Marciel Portela. Luzón, operating autonomously, led the division until his departure in 2012.Footnote 16

Table 1 illustrates two major growth stages for both Santander and BBVA, improving their rankings across Latin America between 1999 and 2024.

Ranking of commercial banks by assets (1999, 2006, 2012, and 2024)

Table 1 Long description

The table ranks commercial banks Santander and BBVA by assets in various Latin American countries for the years 1999, 2006, 2012, and 2024. Santander consistently ranks high, maintaining the 1st position in Chile from 1999 to 2012 and 3rd in Brazil from 2012 to 2024. BBVA shows strong performance in Mexico, holding the 1st position from 2012 to 2024. In Argentina, Santander and BBVA have fluctuating ranks, with Santander reaching 1st in 2012 and BBVA peaking at 3rd in 2012. Peru sees BBVA consistently in 2nd place from 2006 to 2024, while Santander's presence is less consistent. The data highlights the dominance of these banks in specific regions, with some fluctuations over the years, particularly in Argentina and Venezuela.

Sources: Martín-Aceña (Reference Martín-Aceña2007), p. 290; BBVA 2006 and 2015 RSC reports; Calderón Hoffmann and Casilda Béjar (Reference Calderón Hoffmann and Casilda Béjar2000), pp. 78, 81; Santander and BBVA Annual Reports; Americaeconomía.com; Eleconomista.es; Sincomillas.com; Lainformación.com, mx.investing.com; rankia.com.ar; rankia.cl; and spglobal.com. Notes: *Loans/deposits. Santander (S) and BBVA (B) in Latin America.

A first phase, from 1994 to 2006, saw Spanish banks acquiring banking assets across the region. Santander quickly secured a dominant regional position, surpassing the influence of longstanding US banks by 1999, with major operations in Chile, Argentina, Mexico, and Brazil. BBVA established itself as the leader in Mexico and gained a strong foothold in Peru, Venezuela, Uruguay, and Argentina.

A second phase, beginning in 2008 and continuing to the present, has been defined by strategic consolidation. Both banks expanded points of contact with retail customers through bank branches, ATMs, telephone, and digital platforms in high-potential markets while exiting countries and business areas lacking strategic relevance or operational stability. Despite divestments, Santander tripled its regional size over three decades, reaching 100.5 million customers by 2024, twice that of BBVA. The latter experienced significant growth in Mexico, serving approximately 50 million customers by 2023 (see Figure 3).

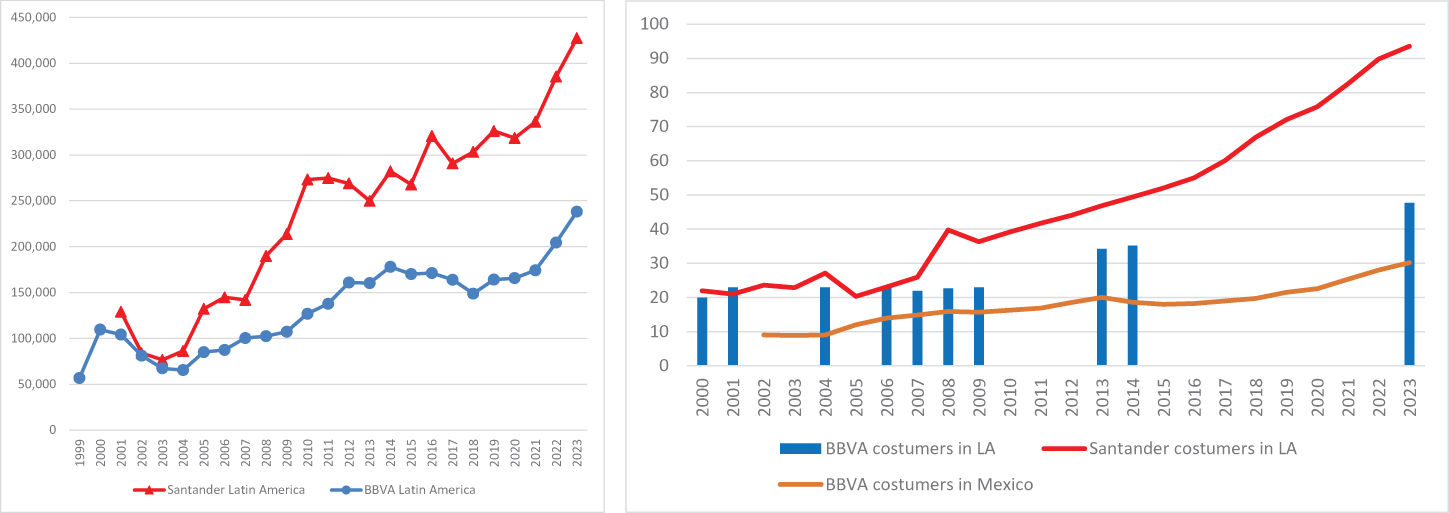

Santander and BBVA assets and clients in Latin America M€ and millions, 1999–2023.

Figure 3 Long description

The image contains two line graphs. The first graph on the left shows the assets of Santander and BBVA in Latin America from 1999 to 2023. The x-axis represents the years from 1999 to 2023 and the y-axis represents the assets in millions. Santander's assets show a steady increase, peaking in 2023, while BBVA's assets also increase but at a slower rate. The second graph on the right shows the number of customers for BBVA and Santander in Latin America and BBVA in Mexico from 2000 to 2023. The x-axis represents the years from 2000 to 2023 and the y-axis represents the number of customers in millions. Santander's customer base in Latin America shows a significant rise, especially after 2010, while BBVA's customers in Latin America and Mexico show a more gradual increase.

The left-hand panel of Figure 3 shows how, following the 1999 mergers in Spain, Santander and BBVA focused on Latin America, diversifying across countries, lines of business, and customer groups (including establishing the largest retail bank branch networks in the region), backed by $10 billion in investments. The right-hand panel suggests how both banks strengthened their positions in key markets like Mexico and Brazil, achieving significant growth in assets and customer bases across the region. These financial institutions thrived in underbanked economies, where Spanish banks outperformed international competitors. Santander became the leading foreign bank in Argentina, Chile, and Peru, while BBVA dominated in Colombia, Mexico, and Venezuela.

3. Technological integration and governance in banking

3.1. The role of technology in bank integration

The interplay between historical practices, information management, globalization, and technological innovation sheds light on the operational and organizational transformation of Spanish banks (Cortada, Reference Cortada2005, Reference Cortada2006, Reference Cortada2011, Reference Cortada2025; Walker and Morris, Reference Walker and Morris2021; Weill et al., Reference Weill, Ross and Robertson2006; Yates, Reference Yates1989, Reference Yates2005). Central to this shift was the role of information technologies in helping retail banks assess customer profitability in environments with limited data. Successfully integrating acquisitions required reconciling legacy systems with the banks’ own infrastructures while ensuring alignment with strategic priorities such as customer satisfaction, efficiency, and regulatory compliance.Footnote 17

These concerns mirrored historical patterns noted by Yates (Reference Yates1989, Reference Yates2005), while the frameworks of Weill et al. (Reference Weill, Ross and Robertson2006) underscored the importance of aligning IT architecture with organizational strategy. The transformation occurred amid a broader digital transition in banking, as institutions worldwide grappled with adapting to emerging technologies (Batiz-Lazo et al., Reference Batiz-Lazo, Maixe-Altes and Thomes2011). Yet the transition proved complex (Cortada, Reference Cortada2005, Reference Cortada2025).Footnote 18 A particularly difficult first challenge was dismantling “silo” informational and organizational architectures that fragmented customer data and obstructed integration. Similarly, the rise of “spaghetti architectures” built on top of legacy applications complicated operations through an uncoordinated patchwork of interconnected systems.

The solution was a unified core banking architecture and a centralized customer database. The Spanish were not pioneers in this domain (Walker and Morris, Reference Walker and Morris2021).Footnote 19 Santander and BBVA succeeded in deploying these systems across diverse markets. Their approaches, however, diverged markedly. Santander pursued a centralized model through its Altair platform, investing in uniform system deployment supported by IBM-backed scalability tests in Montpellier. BBVA, instead, adopted a decentralized approach known as “tropicalization,” integrating local systems through tailored interfaces that accommodated regulatory and operational specificities.

The core banking platform of these banks have the same historical roots. They both evolved from a system called Altamira. This application was designed in 1983–1984 by Juan Carlos Martín Guirado, a young Spanish engineer at Arthur Andersen, originally conceived to solve accounting-related issues for pension management in New York state. In 1986, Martín Guirado, still at Arthur Andersen, returned to Spain and went on to adapt that system for banking purposes by developing accounting and banking-specific modules. The chief advantage of a core banking platform was that it centralized banking operations around the client, consolidating all functions and products into a single database, while streamlining programming through unified, standardized applications and allowing key legacy applications (such as payment clearing) to continue running undisturbed. Its subsequent adoption by Spanish banks underscores how legacy technologies can be repurposed to meet new challenges.Footnote 20 This iterative process of technological adaptation, as described by Cortada (Reference Cortada2006), highlights the nonlinear and path-dependent nature of innovation in financial institutions.

It is noteworthy that both Spanish banks leveraged their technological platforms to achieve significant synergies and operational efficiencies. Santander’s Altair facilitated a rapid and efficient integration process, culminating in the successful assimilation of Banco Real in Brazil, despite its scale. BBVA’s Regional Computing Center in Monterrey, Mexico, and Santander’s regional call center in Queretaro, Mexico, exemplify the potential for centralized infrastructures to achieve cost savings and streamline operations.Footnote 21 These initiatives not only enhanced the banks’ competitiveness in the region but also imposed a standardized management framework on their subsidiaries, curbing the autonomy of local managers and aligning operations with corporate strategies.

These successes were not without limitations. Both banks encountered significant challenges in achieving complete technological integration. In April 1998, Santander initiated the development of Altair, supported by a dedicated technical unit and a $10 million investment.Footnote 22 Meanwhile, BBVA deployed teams from Spain to collaborate with local technical teams (supported by scores of engineering consultants), analyzing system integration with the group’s architecture while addressing national legal and operational requirements.Footnote 23 These short 2-week visits resulted in detailed integration and investment plans, culminating in a complete system migration over 2–3 years.Footnote 24

Santander’s Altair, while effective in Latin America, remained incompatible with its European platform, Partenón.Footnote 25 Similarly, BBVA’s attempts to centralize operations across Latin America through additional regional centers were only partially successful.Footnote 26 The failure of early internet-only banking ventures, such as Santander’s Patagón and BBVA’s Uno-e, further illustrates the difficulties of navigating emerging technologies in a rapidly evolving digital landscape.Footnote 27

These limitations underscore the inherent complexities of technological integration in multinational banking. The “spaghetti structure” of legacy systems, characterized by disconnected and inefficient applications, presented significant barriers to achieving a unified architecture. Santander and BBVA’s strategies highlight the trade-offs between standardization and adaptability, as well as the importance of aligning technological investments with organizational objectives and market realities. However, they also underscore the critical reliance on extensive technical support from firms such as Arthur Andersen, Everis, and IBM during the integration of acquired banks.Footnote 28 Additionally, their strategic importance is highlighted by the involvement of top management in these technological initiatives. For instance, Santander’s Technology, Productivity, and Quality Committee was led by Emilio Botín, chairman, and Alfredo Sáenz, the Group’s CEO. This exemplifies how technological decisions were elevated to the highest levels of corporate governance.Footnote 29 BBVA’s delegation of technological autonomy to its Latin American subsidiaries highlights a contrasting approach, reflecting a more decentralized philosophy.Footnote 30

3.2. Hierarchical governance vs centralization

Technological integration in banking does not inherently lead to improvement unless accompanied by the development of robust banking practices, corporate cultures, and governance structures. Both BBVA and Santander, with their long-standing traditions in commercial banking, exemplify this principle through their strategic approaches in Latin America. Their governance models, though distinct, highlight the importance of organizational structure, cultural integration, and leadership in achieving successful technological and operational outcomes.

Both BBVA and Santander, albeit with different philosophies, reserved key positions for their new Latin American subsidiaries in the organizational charts. An example of the relative importance of these new businesses is depicted in the organization chart presented immediately after the 1999 merger between BBV and Argentaria in Figure 4.

Organization chart of BBVA in Latin America, 1999.

Figure 4 Long description

The organisation chart displays the structure of BBVA in Latin America in 1999. At the top is the position 'Vicepresidente y Consejero Delegado'. Below it is 'Banca en América' led by José I. Goirigolzarri Tellechea. The chart lists several BBVA branches: BBV Puerto Rico with Jaime Guerribalde Romojaro, BBV México with Teófilo Nájera Gómez, BBV Banco Continental with José Antonio Colomer, BBV Banco Francés with Antonio Merino-España Llorente, BBV Banco Ganadero with José María Ayala Vargas, BBV Banco Provincial with Juan Carlos Zorrilla Bravo, BBV Banco Francés with Vicente Benedito Perea, BBV Banco BHIF with Carlos Serrat Sales, BBV Panamá with Félix Vega and BBV Banco Provincial with Luis Yagüe. Additional divisions include 'Desarrollo de Negocio Internacional' with Ignacio Sánchez-Asiaín Sanz, 'Identidad Corporativa y Comunicación' with José Ignacio Goirigolzarri, 'Desarrollo Corporativo y Estrategias de Expansión' with Antonio de la Torre López de Arana and 'Estrategia y Finanzas' with José Sevilla Álvarez.

Figure 4 illustrates how, following the 1999 merger between BBV and Argentaria, BBVA implemented a hierarchical governance structure in its Latin American subsidiaries. Key positions, including CEO, CFO, media director, commercial director, and risk director, were reserved for senior executives from BBVA’s Spanish head office (many of whom had first-hand experience managing retail bank branches as branch managers, and later, as regional directors). This ensured a transfer of expertise and alignment with the parent company’s corporate culture. For instance, José Ignacio Goirigolzarri oversaw four coordination units and the CEOs of each Latin American subsidiary, all of whom were experienced BBVA executives. Local non-executive presidents, often prominent individuals from acquired banks, were retained to maintain regional ties.Footnote 31 Over time, BBVA successfully integrated local talent into these roles, including national CEOs, while maintaining a cohesive corporate culture.Footnote 32

Santander’s approach between 1999 and 2012 revolved around a centralized Americas Division under Francisco Luzón (1948–2021).Footnote 33 This division operated with significant autonomy, reporting directly to Chairman Emilio Botín. The philosophy emphasized:

… a small, very powerful management structure, with very strong people, that covers and manages to make the banks in the Americas a single bank from the point of view of management principles, commercial orientation, technology and management control methods, [we aimed to build] a single bank, but with reasonable autonomy from the country heads.Footnote 34

Interpreted through the lens of the intangible assets framework (Guillén, Reference Guillén2005; Guillén and García Canal, Reference Guillén and García Canal2010, Reference Guillén and García Canal2013), this statement underscores the centrality of organizational and managerial capabilities in the internationalization of Spanish multinationals. Rather than relying on proprietary technology or product innovation, the quoted approach reflects a deliberate strategy to leverage a compact, yet highly capable management structure as a key intangible asset. The emphasis on unified management principles, commercial orientation, technological coherence, and standardized control methods across diverse national operations illustrates the deployment of codified managerial know-how to create a cohesive corporate identity and operational model. At the same time, the provision of “reasonable autonomy” to local heads suggests a nuanced application of this framework, in which centralized strategic vision is balanced with local responsiveness. This combination aligns closely with Guillén and García Canal (Reference Guillén and García Canal2010; Reference Guillén and García Canal2013) argument that Spanish multinationals expanded internationally not through the transfer of technology per se but through the replication and adaptation of sophisticated organizational routines and managerial systems across culturally and institutionally diverse contexts.

Santander’s strategy relied heavily on strong leadership, with key individuals such as Luzón, Marcial Portela, and Jesús María Zabalza driving the division’s operations. The division’s independence was evident in its decision to discard Goldman Sachs’ expansion plan and instead collaborate with McKinsey to implement growth strategies throughout the region.Footnote 35

As noted, the acquisition of Banco Real in Brazil in 2007 marked a turning point. The sheer scale of the Brazilian market led Santander to separate it from the Americas Division, with Portela appointed as president of Santander Brazil, reporting directly to Alfredo Sáez, the group’s CEO, while Luzón was left in charge of the rest of the Latin American subsidiaries and reported directly to Emilio Botín, the Chairman.

Following Luzón’s resignation in 2012, Santander shifted from centralization to a more decentralized model, granting greater independence to country managers to adapt to local market conditions. Thus, between 2013 and 2021, Santander changed course in its strategy in Latin America (and throughout the group), following an arrangement that one executive defined as “a confederation of banks.”Footnote 36 This rather decentralized approach allowed for differentiated commercial and technological strategies, while maintaining the Santander brand and leveraging shared platforms, such as call centers in Mexico.

In 2022, Santander reverted again to a centralized structure, creating regional divisions (e.g., Mexico and the US, South America, and Europe) to simplify governance and enhance decision-making efficiency. This restructuring aimed to accelerate transformations and improve coordination among territories with shared characteristics.Footnote 37

A nuance often overlooked in comparative analyses of the expansion of Spanish banks is how management policies at BBVA and Santander distinguished them from Anglo-American competitors in the region, such as Citibank and HSBC. Central to this distinction were practices that underpinned their competitive edge in Latin America. These practices emphasized long-term executive assignments, cultural and linguistic affinity, and the deliberate integration of corporate culture,Footnote 38 elements that not only facilitated deeper regional embeddedness, overseeing expansion efforts and coordinating operations, but also enabled bidirectional knowledge flows.

At the core of the Spanish banks’ approach lay extended deployments of executives, which cultivated profound expertise and operational continuity. BBVA and Santander routinely stationed senior Spanish leaders in the region for multi-year tenures, allowing them to navigate complex local dynamics with nuance and foresight. By contrast, Anglo-American banks often rotated executives on shorter assignments, typically 18–36 months, which, while promoting global exposure, often constrained executives’ capacity to forge authentic ties or internalize regional subtleties.Footnote 39

Alongside the rotation of staff through different regions, global banks with British or North American headquarters offer regular talent and executive development programs. Likewise, Spanish banks created bilateral mobility through several programs, in which people from different countries were selected based on their development potential to work in Madrid.Footnote 40 They were posted across departments at Head Office, progressing from entry-level to mid-level while they acquired a different mindset, ethical outlook, and working methods. The aim was that, after these executives had spent some years in Spain, they would spread this learning back home. Since the late 1990s, therefore, expatriate appointments in both directions have been a constant feature of BBVA and Santander.

Spanish executives’ cultural and linguistic familiarity with Latin America made them adept at deciphering local practices, from relational negotiation styles to regulatory intricacies, thereby accelerating trust-building with stakeholders, enhancing organizational cohesion and innovation across borders. Many Anglo-American executives, by contrast, often failed to learn the local language or adapt to regional idiosyncrasies, such as the primacy of personal networks (“redes personales”) over formal hierarchies, while giving preference to work practices developed at head office.Footnote 41

Integration into a new corporate culture further amplified these advantages, with both banks implementing mechanisms to align global vision with local realities. Santander held regular executive meetings in Madrid, with Emilio Botín playing a central role in reinforcing corporate values. BBVA, on the other hand, integrated local executives who had successfully led or managed a major project in Latin America into global management structures, ensuring alignment with the bank’s overarching culture while promoting local talent.Footnote 42

The experiences of BBVA and Santander in Latin America underscore the critical role of governance structures, cultural integration, leveraged human capital mobility, and leadership in leveraging technological advancements to sustain a culturally attuned, resilient presence in Latin America. While their approaches differed—BBVA’s hierarchical model vs Santander’s centralized-then-decentralized strategy—both banks demonstrated the importance of aligning organizational practices with regional realities. Their success contrasts sharply with the challenges faced by Anglo-American banks, such as Citi and HSBC, highlighting the value of long-term commitment, cultural adaptability, and cohesive corporate cultures in international retail banking. BBVA’s emphasis on hierarchical control and gradual localization of leadership, alongside Santander’s dynamic shift between centralization and decentralization, reflect the nuanced strategies required to navigate complex and diverse markets such as Latin America.

3.3. Harmonizing efficiency and strategic commercial policies

Spanish banks in Latin America developed a series of business initiatives to consolidate and make their investments profitable. These initiatives primarily focused on reorganizing operations and professionalizing activities, as noted by prominent local observers.Footnote 43 The most significant measures can be broadly categorized into two groups: on the one hand, the adaptation and rationalization of the workforce and the retail bank branch office network, and, on the other hand, the implementation of specific commercial policies.

Regarding workforce and office network rationalization, both BBVA and Santander undertook substantial restructuring to achieve acceptable levels of efficiency and cost savings while improving management procedures. Interviewees considered that most newly acquired subsidiaries were overstaffed by 20–25%, prompting immediate workforce reductions and the introduction of objective, centralized hiring criteria.Footnote 44 Investments in technological solutions, digitalization, and improved internal procedures to manage cash further enhanced retail bank branch efficiency.Footnote 45 For instance, Santander invested $3.4 billion between 1999 and 2006 in restructuring and modernizing human resources, physical assets, and technological infrastructure across its Latin American subsidiaries (Luzón, Reference Luzón2007). Both banks also developed coherent retail bank branch distribution models designed to ensure operational cost coverage (break-even point), incorporating regional zoning criteria for branch openings. Incentive models for employees were introduced, based on objective productivity metrics, to eliminate discretionary decision-making by managers at various levels. Additionally, standardized loan approval systems were implemented to streamline credit processes.Footnote 46

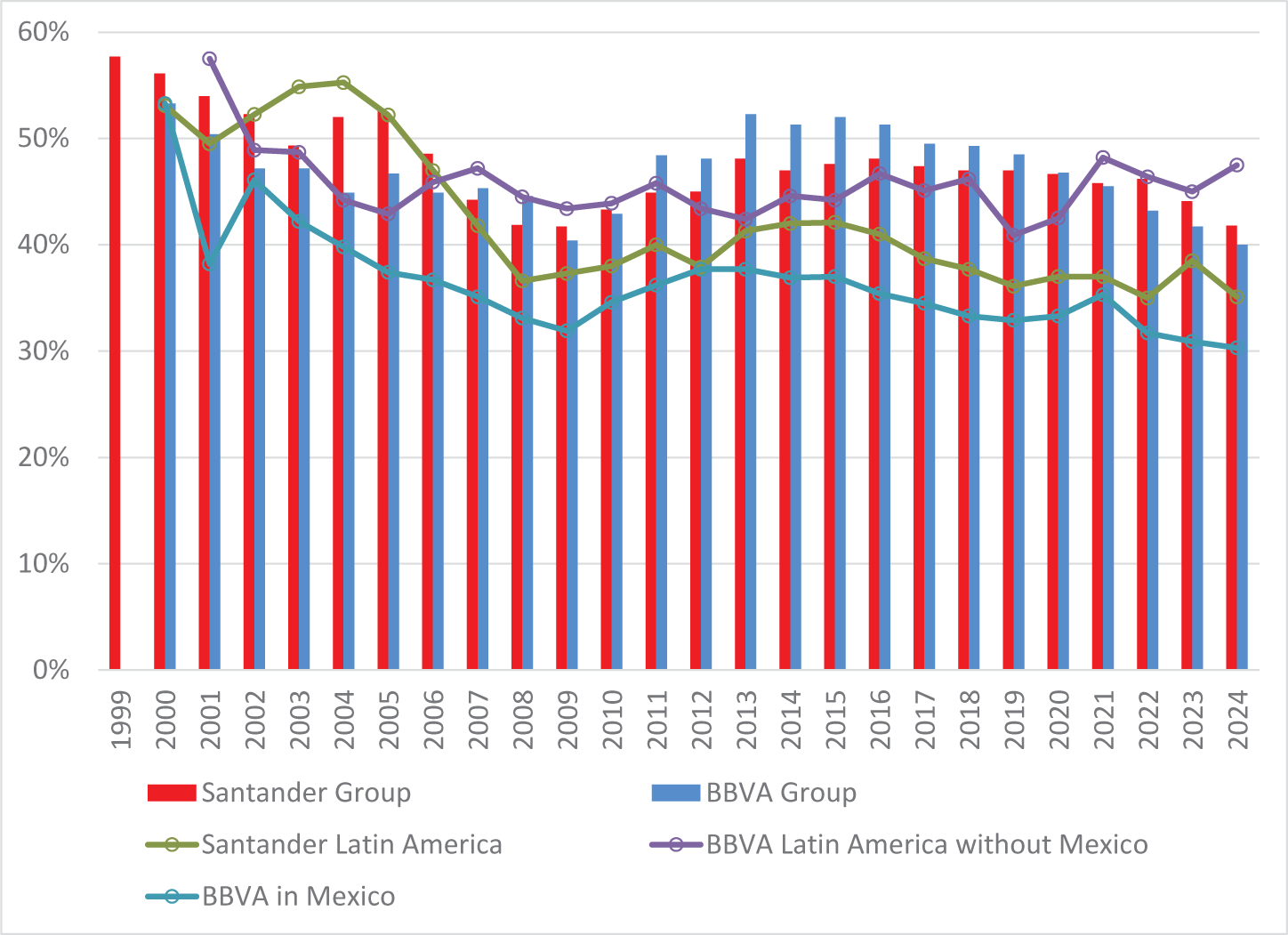

Figure 5 depicts how the combination of these reforms led to a significant and sustained improvement in the efficiency levels of the Latin American subsidiaries, surpassing the average performance of their parent groups.

Santander and BBVA efficiency ratios, Parent vs Latin America, 1999–2024.

Figure 5 Long description

The graph shows efficiency ratios from 1999 to 2024 for Santander Group, BBVA Group, Santander Latin America, BBVA Latin America without Mexico and BBVA in Mexico. The x-axis represents years from 1999 to 2024, while the y-axis shows efficiency ratios in percentage from 0 percent to 60 percent. Santander Group and BBVA Group are represented by dark and light bars, respectively. Lines represent Santander Latin America, BBVA Latin America without Mexico and BBVA in Mexico. The graph illustrates trends and comparisons among these groups over the years.

Risk management, particularly in credit, also saw substantial change. Bad debt ratios improved markedly until the onset of the financial crisis of 2007–2008, bringing the subsidiaries closer to the group averages (see Figure 6).

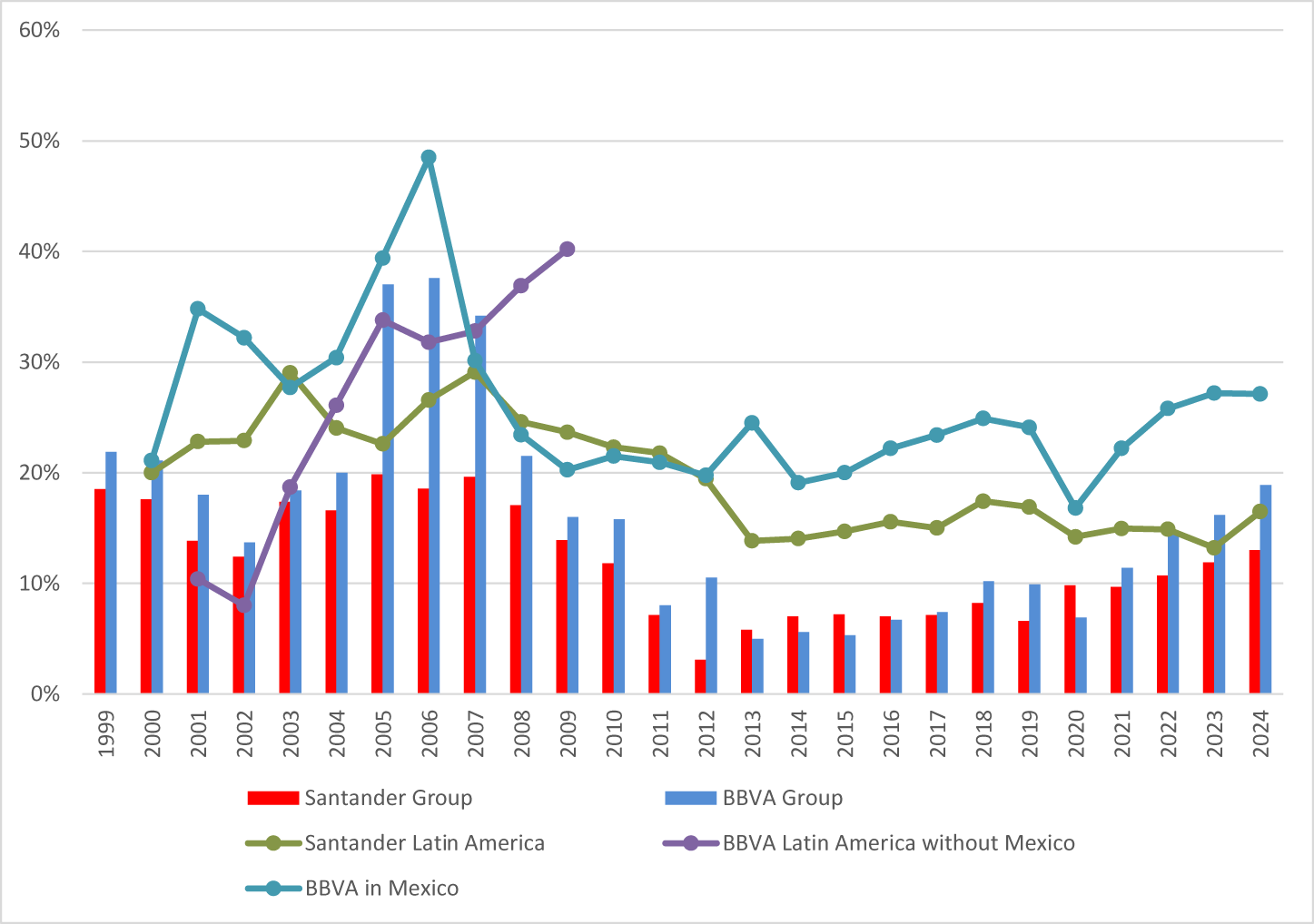

Santander and BBVA non-performing loan to assets ratio, Parent vs Latin America, 1999–2024.

Figure 6 Long description

A graph with both line and bar elements displays the non-performing loan to assets ratio for Santander and BBVA from 1999 to 2024. The x-axis represents the years from 1999 to 2024, while the y-axis shows the percentage from 0 percent to 8 percent. Four lines represent different data: Santander Group, Santander Latin America, BBVA in Mexico and BBVA Latin America without Mexico. The graph shows fluctuations in the ratios over the years, with notable peaks and troughs. The Santander Group and BBVA Group are represented by bars, while the other categories are shown with lines. The data indicates changes in the non-performing loan ratios over time, reflecting economic and financial trends in the regions mentioned.

Figure 6 depicts the 2007–2008 crisis, causing a general deterioration in performance. BBVA, on account of its Mexican subsidiary, managed to weather the downturn more effectively than other international banks. Santander, after absorbing its Brazilian subsidiary, demonstrated a clear recovery from 2010 onward. These outcomes underscore the effectiveness of the restructuring and professionalization strategies employed by BBVA and Santander, highlighting their ability to adapt to regional challenges while maintaining operational and financial resilience.

On the other hand, in terms of commercial policies, both banks pursued a similar strategy, transforming all subsidiaries into universal banks capable of offering corporate banking, investment banking, business banking, small and medium-sized enterprise (SME) banking, retail banking, and private banking across their branches. The overarching message both banks communicated to employees was to convert branches into “points of sale” rather than mere “points of service or administration.”Footnote 47

This approach did not preclude the banks from implementing a studied segmentation of customers and regions to tailor their services effectively.Footnote 48 Order was also established in product distribution, with Spanish banks introducing products that had proven successful in Spain. For example, BBVA’s “El Libretón,” created in 1990 during Spain’s competitive “Supercuentas” era, was successfully replicated in Latin America, with the Mexican subsidiary attracting 8 million “Libretón” accounts by 2002.Footnote 49 Similarly, Santander exported successful products such as Brazil’s “Crédito Nómina,” Mexico’s “Light” (i.e., no-frills, no-fee) payment card, Chile’s consumer credit through Banefe, Argentina’s community banking, and Venezuela’s microcredits through Bancrecer (Luzón, Reference Luzón2007, p. 130). However, Spanish executives also had to adapt to local financial practices to which they were not accustomed. This was the case of the extensive practice of financing the consumer credit of families through rollover credit in payment cards in Mexico, a stark contrast to their role as mere payment instruments in Europe.Footnote 50

Technological investments played a pivotal role in expanding sales channels beyond retail bank branches, enabling growth through call centers and digital banking applications. These platforms, which started from scratch post-merger, experienced exponential growth. For instance, in Mexico, Spanish banks led the charge in digital banking adoption, with BBVA boasting 21 million digital customers by 2023, followed by Citibanamex with 10.4 million and Santander with 6.4 million.Footnote 51

More recently, both banks unified their corporate images, logos, offices, advertising, and social networks across subsidiaries, albeit at different paces. Santander completed this process by 2004, phasing out acquired bank names like Banespa in Brazil and Serfin in Mexico. BBVA followed suit in 2019, coinciding with the transition from Francisco González to Carlos Torres (CEO since 2015) as Chairman. That year also coincided with the elimination of the remaining local designations, such as Francés in Argentina, Bancomer in Mexico, and Continental in Peru, for all subsidiaries to trade under the single BBVA and Santander brands. These efforts underscored the banks’ commitment to creating a cohesive brand identity while leveraging local adaptations to drive growth and customer engagement.Footnote 52

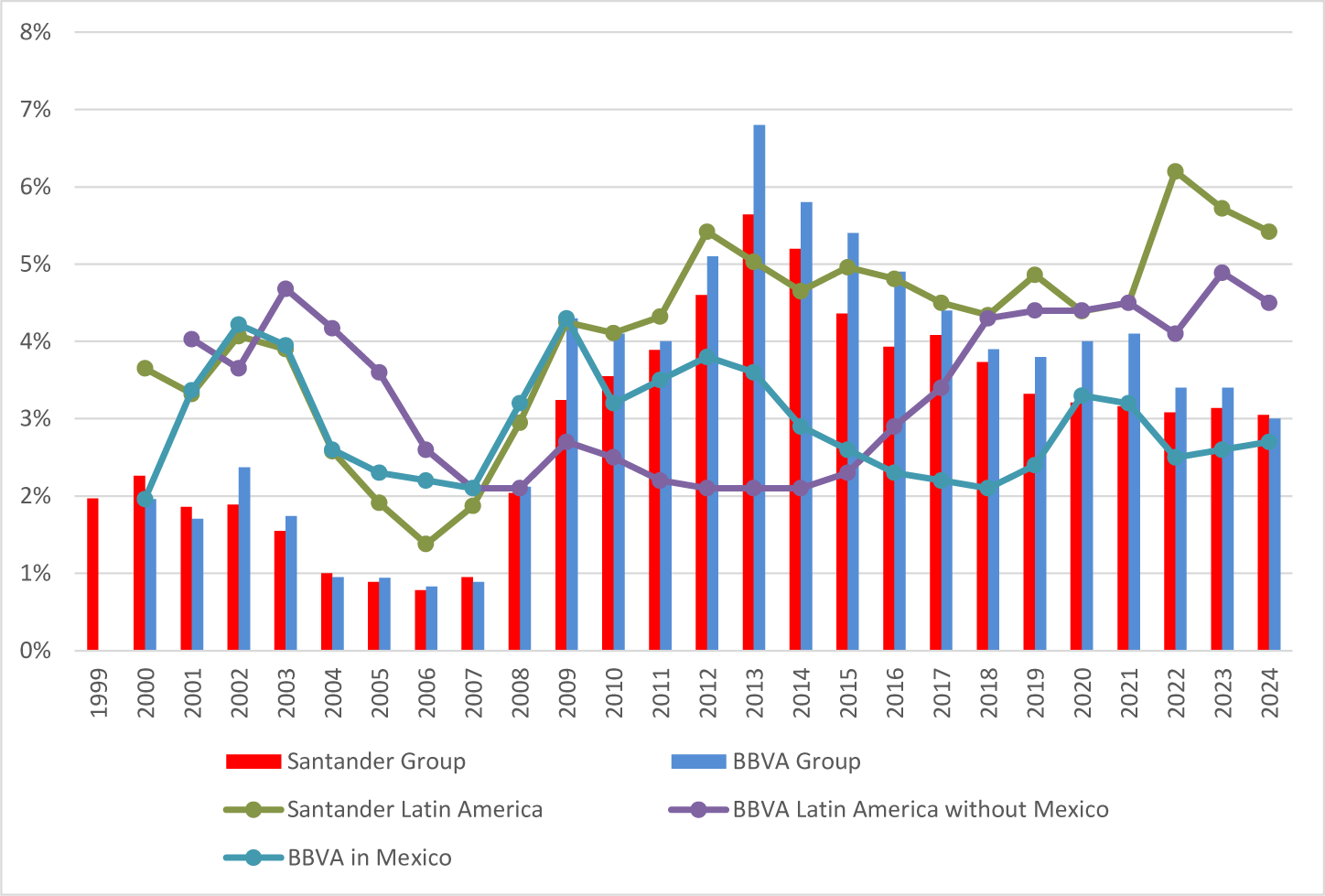

Figure 7 shows the outcome of the Latin American expansion in terms of profitability between 1999 and 2019. This is remarkable by way of the fact that the Latin American subsidiaries of BBVA and Santander consistently outperformed the profitability (as measured by Return on Equity) of both their respective parent companies.

Return on equity (ROE) of Santander and BBVA, Parent vs Latin America, 1999–2024.

Figure 7 Long description

The x-axis represents years from 1999 to 2024 and the y-axis represents percentage from 0 percent to 60 percent. Four lines are plotted: Santander Group, BBVA Group, Santander Latin America and BBVA Latin America without Mexico. Santander Latin America peaks around 2005, exceeding 40 percent. BBVA in Mexico shows a similar peak. Both parent companies have lower percentages, generally below 20 percent. The graph highlights the higher profitability of Latin American subsidiaries compared to parent companies over the period.

Figure 7 shows how, once again, from 2008 onward, Latin America played a pivotal role in supporting the overall financial results of both banking groups, more than offsetting the decline in profitability of their parent companies and the adverse economic conditions in Europe, including collapsing economic activity and falling interest rates over more than a decade. This trend has been increasingly pronounced, with Santander’s Latin American operations contributing 34.4% of the group’s profits in 1999, rising to 50.7% by 2022. For BBVA, the shift was even more striking, with Latin America’s share of total profits increasing from 13.1% in 1999 to 76.5% in 2022, as evidenced by the annual reports of both institutions. This growing contribution underscores the region’s strategic importance and the success of the banks’ localized strategies in driving sustained profitability and resilience.

In summary, the trends outlined in Figure 7 show the result of the digital conquest of Latin America, with regional operations observing superior performance to their Conquistador parent company, underscoring the long-term success of the strategic initiatives of the Spanish leviathans, including workforce rationalization, technological investments, and the implementation of universal banking models tailored to local markets. The sustained profitability of these subsidiaries highlights the effectiveness of the adaptive strategies of the parent company and their ability to leverage regional opportunities while maintaining operational efficiency and robust governance structures. This achievement not only reinforced the parent companies’ global competitiveness but also demonstrated the viability of their long-term commitment to the Latin American market.

4. Tentative conclusions and future research

While Spanish banks maintained a limited presence in Latin America before 1994, these early operations (in the form of representative offices), though not constituting full market entry, provided indispensable institutional knowledge that facilitated their dramatic expansion. This process was characterized by major acquisitions, their consolidation, and the divestiture of underperforming or strategically unrelated business activities. The process marked the emergence of truly multinational retail banking groups. The subsequent 30 years witnessed what Guillén (Reference Guillén2005) and Guillén and García Canal (Reference Guillén and García Canal2010) framework would identify as an unparalleled case of intangible asset deployment, transforming regional banks into the cornerstone of financial globalization.

The foundational work of Pablo Martín-Aceña remains essential to understanding how Spanish banks built a strong presence in individual economies while evolving into globally significant institutions. Neither banking nor information technology were sectors in which Spain held a global competitive advantage, yet, as this article documents, Spanish banks clearly outperformed domestic and foreign counterparts in retail banking across the region.

The success of Spanish banks in Latin America was shaped by a unique confluence of political, economic, and institutional factors. In Europe, Spain’s mature, integrated, and crowded financial system faced limited growth opportunities, prompting banks to seek expansion abroad. In Latin America, democratic transitions, market liberalization, and scores of unbanked populations presented fertile ground for investment, particularly as the region grappled with deep financial crises that necessitated the privatization of state-owned banks and the restructuring of financially impaired institutions. The preparedness of a generation of Spanish bankers, combined with the willingness of Latin American elites and government officials to welcome foreign banks with retail banking expertise, further facilitated this process. These conditions created a distinctive and unique environment that enabled Spanish banks to establish a dominant regional presence, which other foreign banks were either unwilling or unable to capture.

The historical context of Spanish banks’ growth in Latin America has often been presented as isolated institutional narratives. This article, instead, offers a comparative analysis of the international expansion strategies of Santander and BBVA. While both institutions competed directly (most notably in bank auctions in Peru) and indirectly (for instance, in Mexico during the early acquisitions), they also pursued distinct approaches to market entry and consolidation. Santander tended to favor immediate takeovers and full ownership, whereas BBVA often opted for local partnerships to navigate political and business environments. Despite intense competition, both domestically and abroad, our study complements the existing literature by examining not only the motivations behind investment decisions but also the technological and organizational innovations that enabled both banks to secure leading positions in Latin America. By tracing the similarities and differences, we show how each bank forged a path to regional dominance while outperforming domestic rivals and traditional foreign competitors alike. This is not to underestimate the fact that they remain fierce competitors in the Spanish domestic market and across the region today (notably in Argentina, Chile, and Mexico). While one bank may temporarily enjoy a stronger presence in a given market while the other scales up its operations, their rivalry is perhaps most evident in the increasingly contested domain of digital banking.

We reject the hypothesis known as “follow the client,” which proposes that the presence of other Spanish multinationals sparked banks’ growth abroad. We acknowledge this departs from prior contributions (Berges et al., Reference Berges, Ontiveros, Valero, Malo de Molina and Martin-Aceña2012; Cuevas et al., Reference Cuevas, Martín-Aceña and Pons2020). Our conclusion is based on three interlocking considerations. First, the origin of the hypothesis in the context of Anglo-American investment banking renders it inapplicable to retail-oriented expansions, where physical infrastructure trumps client-specific services (Zaheer, Reference Zaheer1995). Indeed, Spanish banks eschewed the pursuit of merchant or investment banking in Latin America. Instead, Spanish banks scaled up as universal banking institutions anchored in retail operations, which, prior to 2010, necessitated extensive networks of retail bank branches and ATMs as primary distribution channels. This strategy is highly capital-intensive and deemed ill-suited and too risky for client-following dynamics in nascent markets (Ghemawat and Khanna, Reference Ghemawat and Khanna1998).

Second, with the partial exceptions of Telefónica and Iberia, large Spanish non-financial multinationals such as Endesa, Iberdrola, and Repsol entered Latin America contemporaneously with the banks rather than prior to them (Rosas Xicota and Casanova Domenech, Reference Rosas Xicota and Casanova Domenech2022). Between 1990 and 2004, Spanish outward FDI was dominated (both in value and number of transactions) by SMEs lacking the multinational footprint to generate a “client pull” effect (Batiz-Lazo et al., Reference Batiz-Lazo, Mendialdua and Zabalandikoetxea2007). Third, both quantitative data on asset allocation (such as growth in total assets or the proliferation of retail bank branch networks) and qualitative insights from executive interviews affirm that Santander and BBVA operated as retail multinationals, prioritizing mass-market penetration over corporate or wholesale banking, thereby forging independent trajectories unencumbered by predecessor firms. In short, in our view, the empirical evidence in this paper unequivocally refutes the “follow the client” hypothesis.

It is worth noting the differences in the leadership styles and entry strategies of Santander and BBVA. On the one hand, Santander’s top-down leadership favored direct acquisitions and immediate takeovers of financial intermediaries with clear financial return targets. On the other hand, BBVA’s collegiate decision-making often sought local partners to navigate relationships with industrial elites and government officials, while preferring a combination of strategic and financial rewards. Yet, as most instances that observe long-term growth, we record a combination of apparent contradictions: intent and learning; foresight vs trial & error; strong personalities vs institutions and governance; commitment and vision vs chance and opportunity; and matching or outbidding competitors vs cooperation and support. Growth is, therefore, paradoxically shown as messy, nonlinear, and nuanced.

We further document how both Santander and BBVA shared a sustained commitment to technological investment and operational modernization. Technology and the dynamics of technological change play a central role in our analysis: at times enabling strategic initiatives, at other times introducing constraints that had to be carefully managed. The orientation toward innovation was shaped partly by global developments, such as the advent of the Internet, the proliferation of cashless payments, and the widespread adoption of mobile banking applications. These developments fundamentally altered the nature of customer interaction. At the same time, the expansion into Latin America required a response to structural deficiencies, particularly chronic underinvestment, and the urgent need for financial modernization as signaled by the introduction of core banking platforms.

In this respect, our study foregrounds the role of intangible assets, precisely the element that Guillén (Reference Guillén2005) and Guillén and García Canal (Reference Guillén and García Canal2010) identify as central to the international success of Spanish multinationals. Crucially, Spain’s comparative strength lay not in the invention of new technologies but in the distinctive organizational capacity to deploy and optimize existing technological solutions. This subtle yet significant distinction underscores the originality of our contribution.

The scale of the challenge that involved managing tens of thousands of employees and serving millions of customers, across geographically and institutionally diverse territories, required the development of new informational and organizational architectures. A notable marker of these innovations is that, in 1994, Banesto’s technological platform—later adopted by Santander—was recognized as the best in the world, a clear testament to its acknowledged excellence in this field.

As noted, a defining element of this transformation was the implementation of integrated core banking systems and the dismantling of legacy information silos. These reforms necessitated significant investment, decisive leadership, and sustained organizational commitment. Additionally, cadres of local knowledge, such as consultants (particularly IT engineers) and new staff at bank branches, could be called upon to support the transformation. The successful execution of transformative adoption demonstrated that Spanish banks were able to combine robust managerial structures with flexible, cutting-edge technology to achieve high levels of operational efficiency and strategic effectiveness.

These technological and organizational advances facilitated more effective governance across large, complex institutions, enhanced day-to-day operations, and enabled a broader and more coherent range of products and services. Moreover, the establishment of shared technical and commercial frameworks further supported these developments by reducing costs and promoting consistency across regional subsidiaries.

A critical component of the Spanish banks’ success in the region was the transfer of managerial expertise and corporate culture from headquarters to their Latin American affiliates. Knowledge transfer and amalgamation were largely achieved through the deployment of a small cadre of experienced executives from Spain, who occupied strategic positions and developed long-term careers in the region. The cultural and linguistic affinity between Spanish executives and local populations was important, but much more so was the long-term commitment of “ex pats” to the project, which provided a comparative advantage over other foreign and domestic banks, facilitating smoother integration and stronger relationships with local stakeholders.

The medium- and long-term outcomes of this expansion were remarkable. Both banks achieved outstanding financial success, with Latin American subsidiaries consistently outperforming the financial performance of parent companies and activities elsewhere in the world. Santander’s investments were larger in scale, doubling its asset base, while BBVA’s profitability was driven by its highly successful Mexican subsidiary. This diversification proved crucial during the 2007–2008 global financial crisis, as profits from Latin America offset losses in developed markets, underscoring the strategic importance of the region.

Despite these achievements, several areas remain underexplored and warrant further investigation. First, a comparative analysis of the influence of Spanish banks on Latin American economies is needed, examining their impact on operational efficiency, management practices, product offerings, and customer service across diverse ethnic, socioeconomic, and geographic contexts. Second, their interaction with government-owned banks, fintechs, and credit cooperatives in shaping the region’s financial systems requires deeper scrutiny, particularly in light of regulatory innovations, governance changes, the challenges for gender equality, and the influence of illicit financial flows. Third, the next technological threshold—marked by the migration of banking systems to the cloud and the digitization of operations—presents a critical area for future research. This includes examining the evolving role of physical bank branches and the potential of emerging technologies, like blockchain and artificial intelligence, to enhance financial inclusion and transform the region’s financial landscape. Fourth, the uneven progress of digital payment systems across Latin America, from Brazil’s trailblazing initiatives to the stagnation in countries like Mexico and Venezuela, highlights the need for a comparative analysis of the factors driving success and the challenges hindering technological adoption. By addressing these gaps, future research can provide valuable insights into the ongoing transformation of Latin America’s financial systems and the role of Spanish banks in shaping this evolution.

Supplementary material

The supplementary material for this article can be found at https://doi.org/10.1017/S0212610926101037.

Acknowledgements

Authors appreciate contributions from interviewees. They also appreciate Juan Luis Cárdenas, César Castillo, James Cortada, Francisco Gil Díaz, and Matilde Masso for their helpful comments, as well as participants at the Business History Conference (Mexico City), EBHA (Madrid), ABH-EBSH (York), AEHE International (Las Palmas, Gran Canaria), and Canning House Latin Academic Forum (London). The authors are also grateful to Victoria Siddaway for her editorial assistance in improving the readability of the manuscript. The usual disclaimers apply.

Sources

BBVA Annual Report (1989 to 2024), Banco Bilbao Vizcaya Argentaria, Madrid.

Santander Annual Report (1989 to 2024), Banco Santander, Santander.

Open access

Open access