1. Introduction

During the past several decades, protecting property against catastrophes such as hurricanes, earthquakes, volcanic eruptions, and wildfires has become an increasing concern for insurance companies as well as property owners. Innovative alternatives to conventional reinsurance, such as catastrophe bonds and other insurance-linked securities (ILS), have been the subject of extensive study. A topic receiving less (but an increasing amount of) attention has been that of multi-peril risks, which is the subject of this paper.

To fix ideas, consider a large corporate entity owning a considerable number of globally distributed properties that it wants to ensure against catastrophic events. Although catastrophes rarely occur at any one site during a year, owning multiple sites exposes the company to considerably more risk than owning just one. For example, if catastrophes occur at a site at rate q = 0.01 per year, an owner of a single site can expect one such event every 100 years on average. However, owning n = 10 sites exposes the company to a catastrophe once every 10 years on average. To protect against the substantial losses that catastrophic events induce, the company has put aside sufficient funds to cover  $m-1~( \lt \!n)$ such events during any one year. But it wants to insure all n sites so that if these events occur at m or more of its sites, it will receive a θ dollar payout from the insurer. For conciseness of exposition, we hereafter refer to catastrophes as quakes, regardless of type.

$m-1~( \lt \!n)$ such events during any one year. But it wants to insure all n sites so that if these events occur at m or more of its sites, it will receive a θ dollar payout from the insurer. For conciseness of exposition, we hereafter refer to catastrophes as quakes, regardless of type.

Conceptually, this m-out-of-n insurance policy differs from conventional property insurance that insures each site separately. Although policies that provide less than full coverage of a customer’s losses are common, they usually contain a deductible clause requiring a customer to self-insure the first d dollars, where d is the deductible. But in the context of multi-peril catastrophes spread out over time and space, an m-out-of-n policy offers an alternative option in which the deductible takes the form of a minimal number of sites m incurring losses, rather than a minimal dollar amount, before a customer receives a payout. The challenge for an insurer is to be able to offer the customer an m-out-of-n policy at a competitive premium, but one that properly accounts for the assumed risk.

To offer this m-out-of-n policy, an insurer first needs to determine a premium per dollar of coverage to charge a customer, presumably consistent with the level of risk of loss that the insurer is willing to accept. A conventional way for the insurer to reduce that risk would be to purchase some form of reinsurance and incorporate its cost into the premium. In the context of the present problem, it is reasonable to assume that a market already exists for buying and selling insurance on individual sites, which the insurer can exploit to provide a type of reinsurance.

This study describes and compares three strategies, A, S, and C, for determining both the premium, π, per dollar of customer coverage and the initial reinsurance coverage per site, c. Each strategy pays θ dollars to the customer if at least m sites have quakes during a T-day coverage period. The study also examines the loss/gain probability distribution for each strategy induced by its feasible  $(\pi,c)$ 2-tuples.

$(\pi,c)$ 2-tuples.

Strategy A is static, purchasing reinsurance only at the beginning of the coverage period. Both Strategies S and C are dynamic and adaptive, capable of changing reinsurance coverage as time elapses and/or as quakes occur at individual sites. Because the risk of m out of n sites having quakes during the coverage period changes over time, decreasing as the time remaining decreases and increasing whenever a quake occurs, an adaptive dynamic strategy has a potential advantage over a strategy that is static. Strategy S changes the reinsurance coverage only when a quake occurs, while allowing the new coverage value to depend on the time remaining. Strategy C purchases reinsurance coverage periodically, for example, daily, weekly, or monthly. The coverage lasts only for one period, thus allowing the coverage amount to change (decrease) if no quake occurs in that period, as well as change after a period in which a quake does occur. However, since reinsurers typically demand a higher markup for a given amount of coverage over a shorter as opposed to longer period (see Section 2.1), this added adaptability can come at a cost.

To establish a basis for determining the  $(\pi,c)$ 2-tuples for each strategy and to facilitate comparison among them, the study relies on expected utility theory.Footnote 1 Each strategy determines a collection of 2-tuples for which the insurer is indifferent between offering and not offering the policy because both options have the same expected utility.

$(\pi,c)$ 2-tuples for each strategy and to facilitate comparison among them, the study relies on expected utility theory.Footnote 1 Each strategy determines a collection of 2-tuples for which the insurer is indifferent between offering and not offering the policy because both options have the same expected utility.

Because Strategies A and S generate multiple indifference 2-tuples, additional criteria are needed for evaluating the benefit of each indifference 2-tuple, as well as comparing them for different strategies. For example, price competitiveness and reinsurance coverage both affect loss probability. This paper examines the indifference premiums and loss probabilities of Strategies A, S, and C, for a range of values of the policy parameters, primarily by means of numerical analysis.

Preview of results

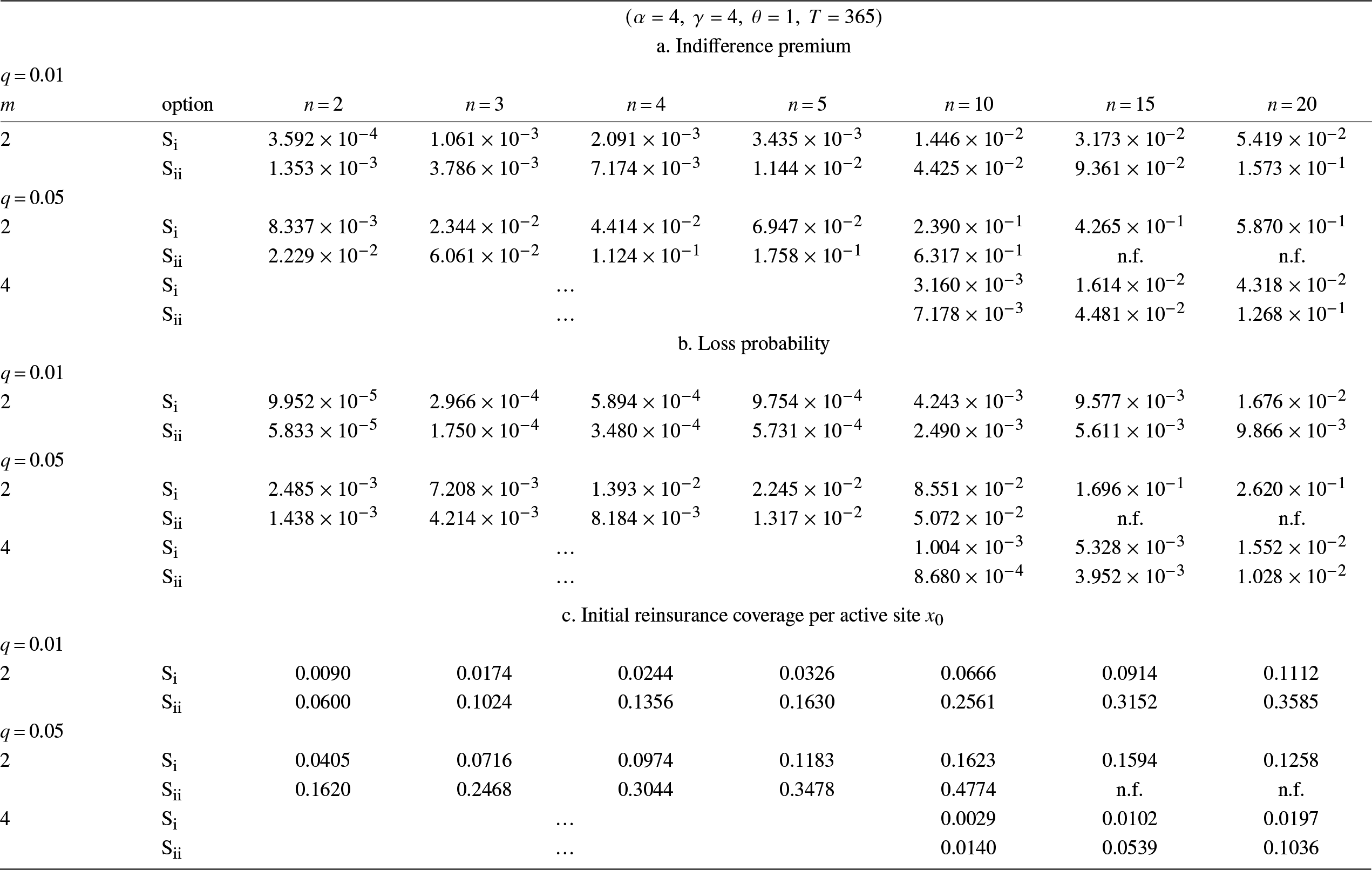

Table 1 provides a preview of the results of this paper, comparing the indifference premiums for Strategies A, S, and C for some representative scenarios for the values of parameters n, m, and q, and the risk-aversion coefficients, α and γ, of the (exponential) utility functions of the insurer and the reinsurer(s), respectively. (The larger the risk-aversion coefficient, the more risk averse is the insurer or reinsurer.) For both Strategies A and S, option i corresponds to the indifference pair with the smallest premium π charged to the customer and option ii to the indifference pair with the largest feasible value of the initial reinsurance coverage c per site. Generally speaking, option i is the most cost competitive and option ii offers the smallest loss probability for the insurer. As mentioned, Strategy C offers only one option, corresponding to the smallest coverage c that guarantees zero probability of loss for all quake histories in which there are no review intervals in which more than one site has a quake.

Indifference premium π.

For all the examples in Table 1, Strategy S generates a smaller indifference premium than Strategy A for option i (minimal premium), but a larger indifference premium for option ii (maximal coverage). By contrast, Strategy C generates a single 2-tuple, usually with a greater premium than those for Strategies A and S.

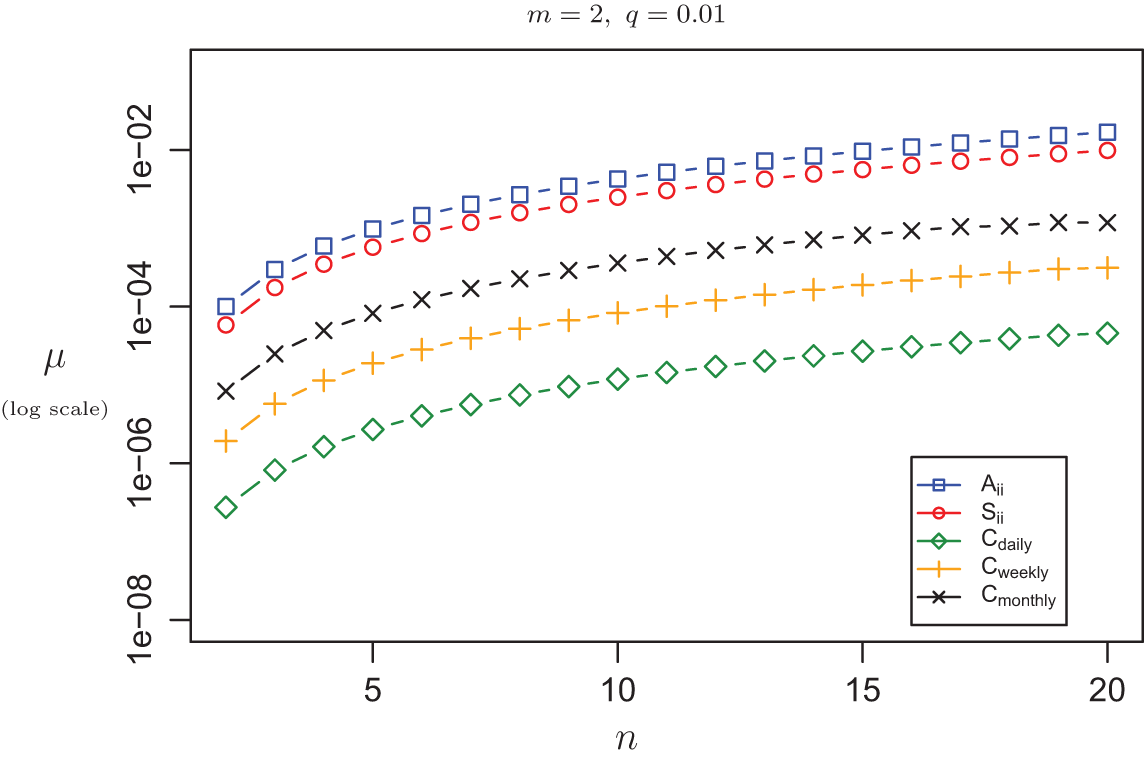

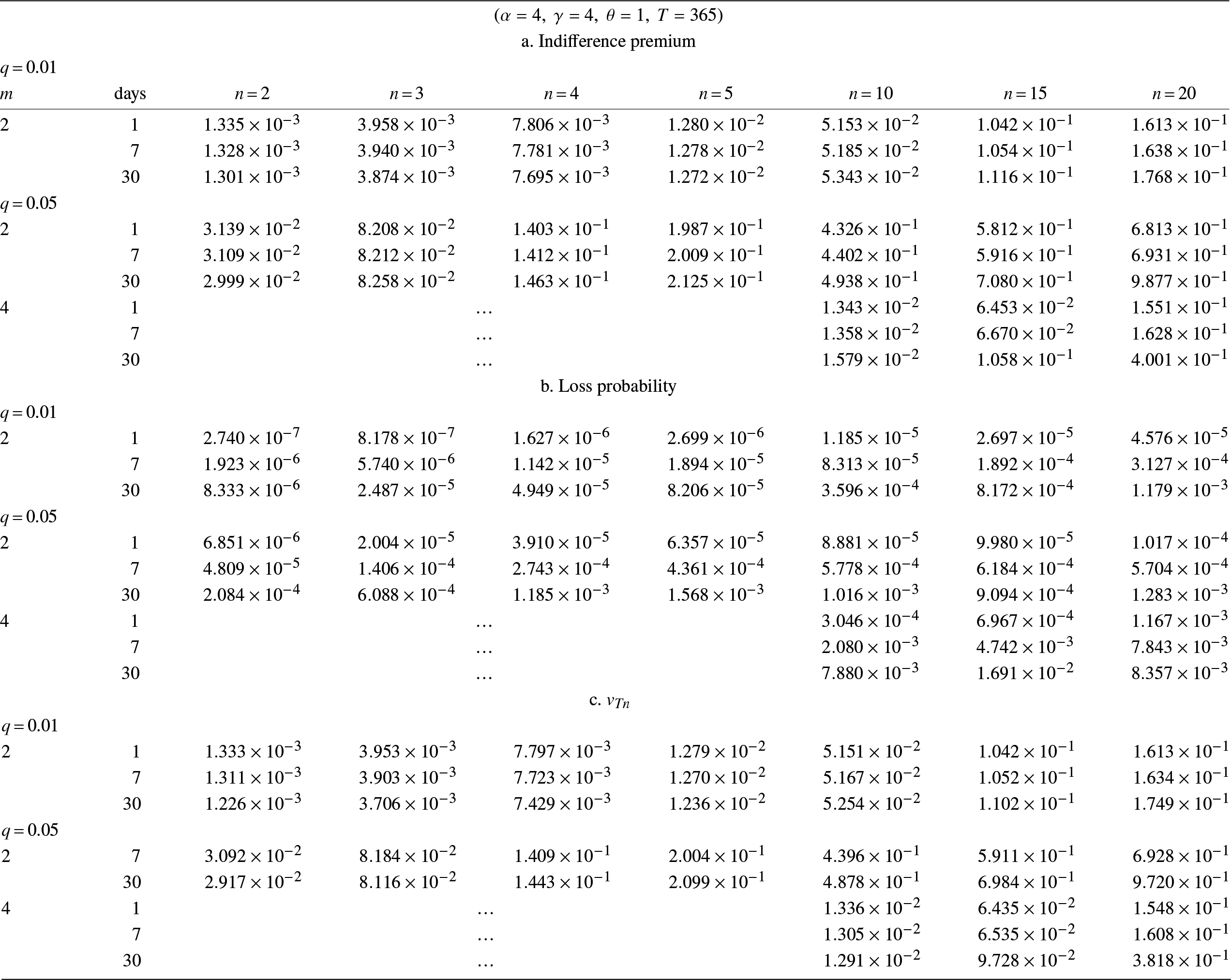

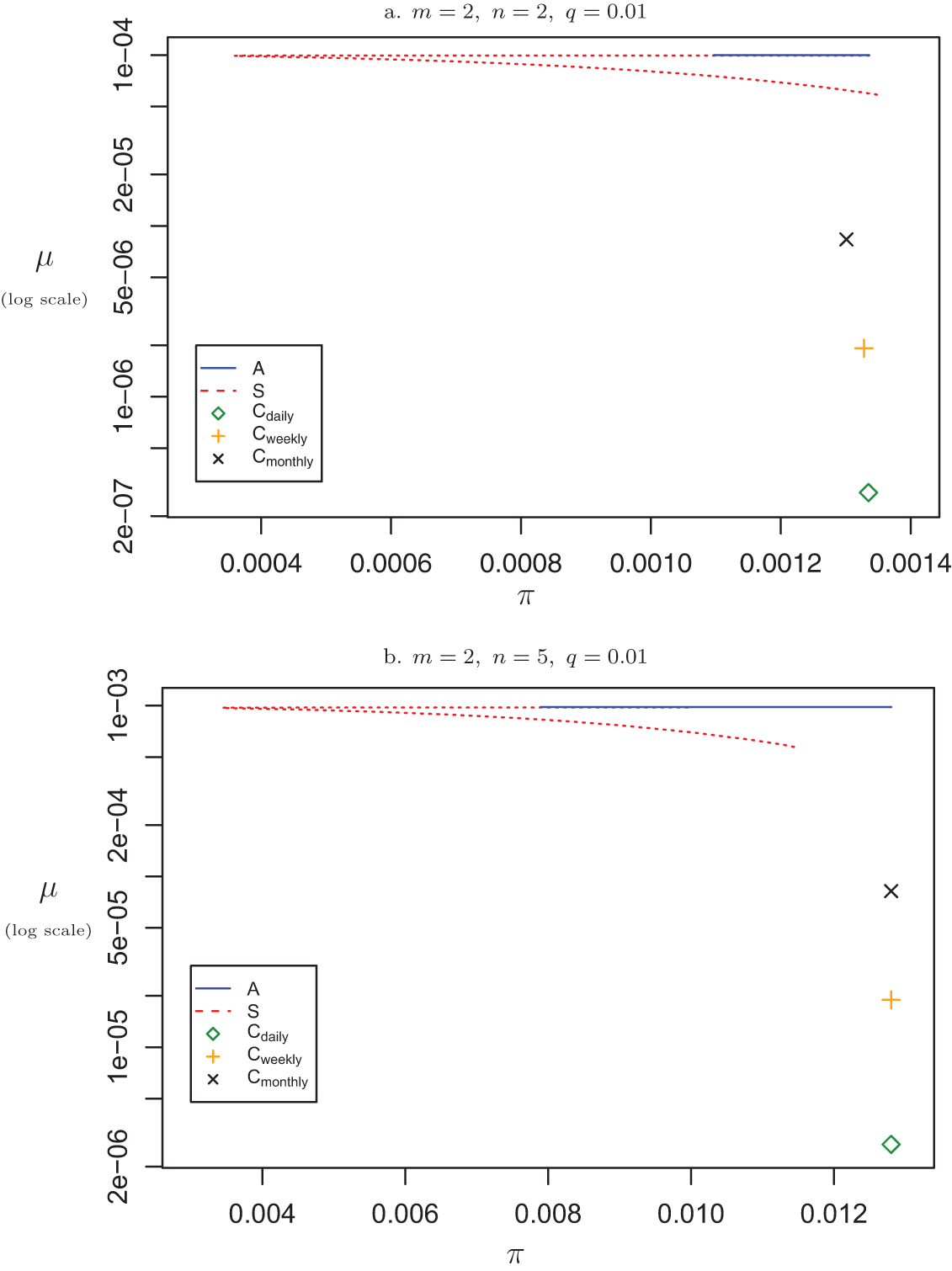

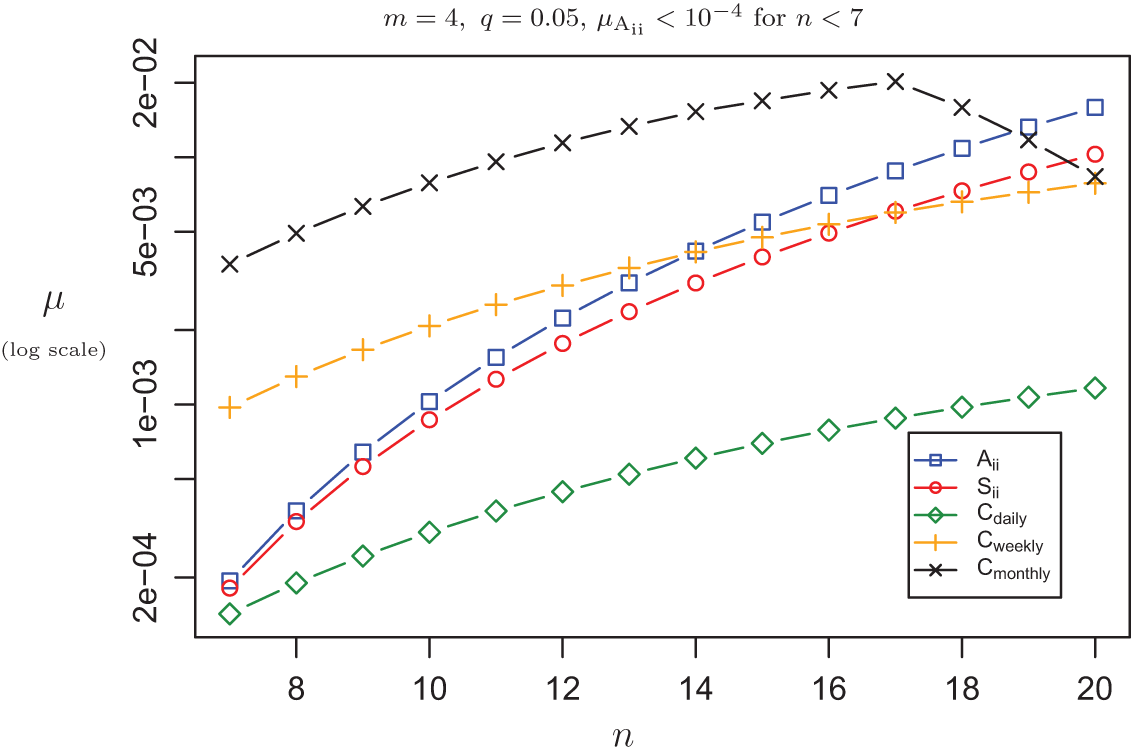

When based on daily review, however, Strategy C induces considerably smaller loss probabilities. It does this by exploiting the rarity of more than one quake over daily intervals. This behavior is illustrated in Figure 1 for a representative example, in which m = 2, q = 0.01, α = 4, and γ = 4, for a range of values of  $n \geq m=2$. The figure plots the loss probability µ (vertical axis) as a function of the number of sites n (horizontal axis) under Strategies A and S (both with option ii) and Strategy C. In this example, loss probabilities are smaller with Strategy C than with A and S for all lengths of the review interval, but the improvement is less dramatic as the review-interval length increases.

$n \geq m=2$. The figure plots the loss probability µ (vertical axis) as a function of the number of sites n (horizontal axis) under Strategies A and S (both with option ii) and Strategy C. In this example, loss probabilities are smaller with Strategy C than with A and S for all lengths of the review interval, but the improvement is less dramatic as the review-interval length increases.

Strategies A, C, and S $_{\rm ii}$: Loss probability µ.

$_{\rm ii}$: Loss probability µ.

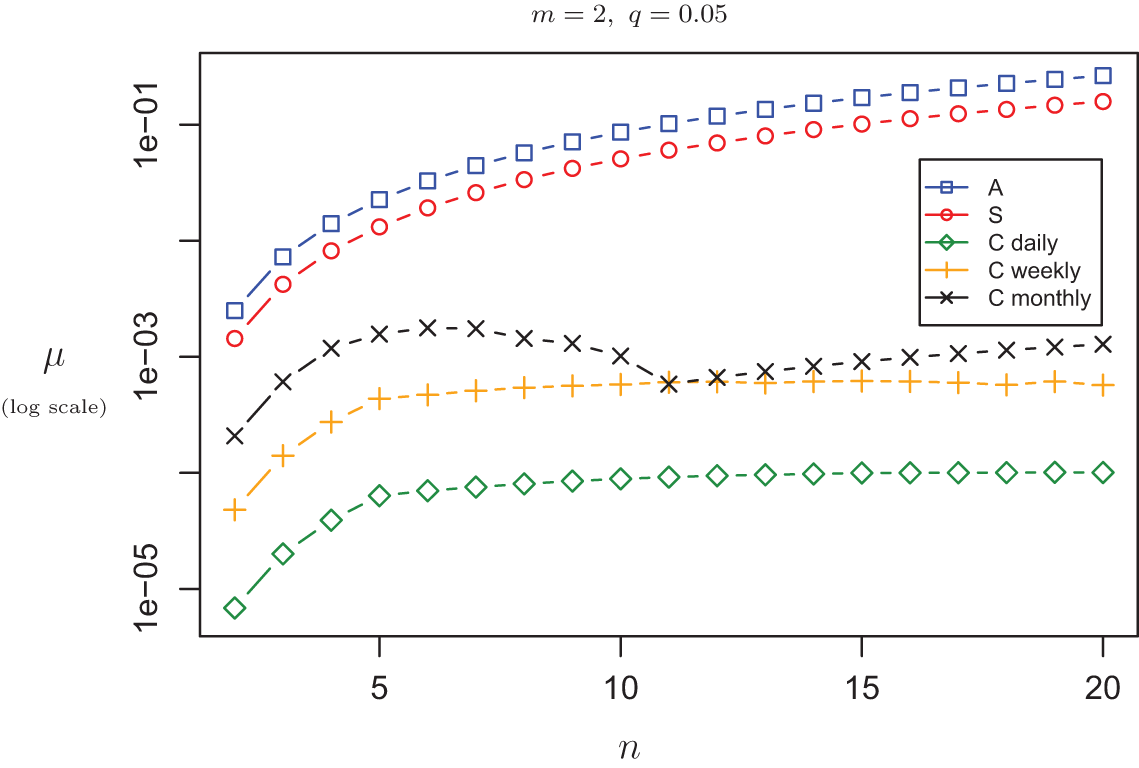

Section 6 contains additional numerical results and comparisons between the strategies. In particular, these results demonstrate that, as the length of the review interval increases, Strategy C continues to induce smaller loss probabilities than A and S for some, but not all,  $(m,n,q)$ scenarios.

$(m,n,q)$ scenarios.

Literature review

While there are relatively few references on multi-peril catastrophic insurance in the peer-reviewed literature, there is indirect evidence of the underwriting of multi-peril risks in practice. In a NY Times article on catastrophic risk, Lewis [Reference Lewis10] cites an example of pricing the premium for coverage of the  $m=n=2$ case by dynamic purchasing of policies on each site. The example is due to John Seo, who founded Fermat Capital Management LLC, a firm specializing in coverage of multi-peril risks by means of catastrophe bonds. Morton Lane (see Lane [Reference Lane9] and the references therein) provides an insightful glimpse of Seo’s techniques, based on a talk Seo gave at the Conference on Risk-Linked Securities in 2003. In the finance literature, Bielecki et al. [Reference Bielecki, Jeanblanc and Rutkowski5] consider the pricing of contingent claims on baskets of credit-default swaps (arguably a form of insurance) under arbitrage-free assumptions, citing the m-out-of-n case as an example.

$m=n=2$ case by dynamic purchasing of policies on each site. The example is due to John Seo, who founded Fermat Capital Management LLC, a firm specializing in coverage of multi-peril risks by means of catastrophe bonds. Morton Lane (see Lane [Reference Lane9] and the references therein) provides an insightful glimpse of Seo’s techniques, based on a talk Seo gave at the Conference on Risk-Linked Securities in 2003. In the finance literature, Bielecki et al. [Reference Bielecki, Jeanblanc and Rutkowski5] consider the pricing of contingent claims on baskets of credit-default swaps (arguably a form of insurance) under arbitrage-free assumptions, citing the m-out-of-n case as an example.

Fishman and Stidham [Reference Fishman and Stidham8] extend Seo’s model and dynamic pricing technique to a general m-out-of-n model. They introduce Strategy C, giving a detailed analysis of its advantages over conventional static reinsurance, with numerical illustrations for a small set of scenarios. The present paper expands this analysis by introducing Strategies A and S, while considering a larger set of scenarios and comparing Strategy C to Strategies A and S with partial as well as full reinsurance.

Strategy C offers two potential benefits over traditional insurance/reinsurance: (1) it exploits the fact that the m-out-of-n risk is a contingent claim, determined by the occurrence of events (quakes at individual sites) for which there exist insurance markets; and (2) it is dynamic and adaptive rather than static, taking advantage of new information at individual sites (quakes) to adjust its actions (reinsurance coverages on sites that have not yet had quakes) over the course of the coverage period.

Our previous paper [Reference Fishman and Stidham8] compared Strategy C to a conventional form of reinsurance: simply ceding to a reinsurer a fraction of the amount the insurer is obliged to pay the customer. That form does not take advantage of either of the two benefits mentioned above. In the present paper, the baseline for comparison is Strategy A, which has the real-world advantage that it is simple, while taking advantage of the contingent-claim benefit by buying reinsurance on individual sites.

One objective of the present paper is to explore further the relative effects of the two potential benefits of Strategy C and address the question: how much do the advantages of Strategy C (lower probability of loss and, in some cases, lower premium) depend on each benefit? In particular, we compare Strategy C to Strategy A, which exploits the contingent-claim benefit (1), but not the dynamic-adaptive benefit (2). We also compare Strategy C to Strategy S, which, although also dynamic and adaptive, does not depend as much as Strategy C does on the availability of reinsurance policies with short coverage periods.

The use of utility theory for the analysis of models for insurance and reinsurance is widespread in the literature, going back at least to the 1960s (see, e.g., [Reference Arrow1, Reference Arrow2, Reference Borch7]). As an alternative to traditional actuarial methods for setting premiums, Bühlmann [Reference Bühlmann3, Reference Bühlmann4] develops an economic model based on an equilibrium solution for prices in a market with utility-maximizing insurers and reinsurers, each with a concave utility function.

Utility theory provides a mechanism for comparing reinsurance strategies for situations in which the insurer is exposed to basis risk, due either to ceding less than the total risk to reinsurers or to using a reinsurance instrument that does not exactly cover the risk being insured, as is the case for example with cat bonds based on risk indices. Both types of basis risk are present in the models of the present paper. Rather than relying completely on utility theory, however, we also compare strategies with respect to the probability of loss or gain, as mentioned previously.

Additional discussion and interpretation of the models and results are in the final section of the paper (Concluding remarks).

2. Preliminaries

The study assumes the existence of a market that dictates a premium, π M, per dollar of coverage for a T day period m-out-of-n policy. An insurer can only be a player in this market if he can offer the policy at a premium π no greater than π M. His ability to do so depends on his attitude toward risk, as embodied in his utility function,  $\{u(w),-\infty \lt w \lt \infty\}$, which we assume is increasing concave in wealth w. Let

$\{u(w),-\infty \lt w \lt \infty\}$, which we assume is increasing concave in wealth w. Let

\begin{equation}

\begin{array}{lrl}

& w_{\mathrm{I}}=&\mbox{insurer's initial wealth or working capital} \\

\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\mbox{and} &&\\

& \kappa=&\mbox{insurer's final wealth or working capital},

\end{array}

\end{equation}

\begin{equation}

\begin{array}{lrl}

& w_{\mathrm{I}}=&\mbox{insurer's initial wealth or working capital} \\

\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\!\mbox{and} &&\\

& \kappa=&\mbox{insurer's final wealth or working capital},

\end{array}

\end{equation} so that  $\kappa-w_{\mathrm{I}}$ denotes the gain or loss that the insurer realizes when coverage ends. For a given strategy,

$\kappa-w_{\mathrm{I}}$ denotes the gain or loss that the insurer realizes when coverage ends. For a given strategy,  $u(w_{\mathrm{I}})$ denotes the insurance company’s utility at the beginning of the coverage period and

$u(w_{\mathrm{I}})$ denotes the insurance company’s utility at the beginning of the coverage period and  $\rm E {\it u}(\kappa)$, his expected utility at its end. Assume the company’s objective is to preserve the expected utility of its initial wealth

$\rm E {\it u}(\kappa)$, his expected utility at its end. Assume the company’s objective is to preserve the expected utility of its initial wealth  $w_{\mathrm{I}}$, so that it is indifferent between offering and not offering the policy at a premium per dollar of coverage satisfying

$w_{\mathrm{I}}$, so that it is indifferent between offering and not offering the policy at a premium per dollar of coverage satisfying

\begin{equation}

\rm E {\it u}(\kappa)={\it u}({\it w}_{\mathrm{I}}).

\end{equation}

\begin{equation}

\rm E {\it u}(\kappa)={\it u}({\it w}_{\mathrm{I}}).

\end{equation}To facilitate comparisons, subsequent sections assume the insurer has the exponential utility function

\begin{equation}

u(w)=-\rm e^{-\alpha {\it w}}\qquad \alpha \gt 0,~\mbox{and }-\infty \lt {\it w} \lt \infty,

\end{equation}

\begin{equation}

u(w)=-\rm e^{-\alpha {\it w}}\qquad \alpha \gt 0,~\mbox{and }-\infty \lt {\it w} \lt \infty,

\end{equation}where α reflects his tolerance for risk. Aversion to risk increases with α. For a utility function given by (3), the indifference equation (2) is equivalent to

\begin{equation}

\rm E {\it u}(\kappa-{\it w}_{\mathrm{I}}) = -1.

\end{equation}

\begin{equation}

\rm E {\it u}(\kappa-{\it w}_{\mathrm{I}}) = -1.

\end{equation}Analogous comparisons can be made using other concave increasing utility functions.

2.1. Reinsurer’s markup

To reduce risk, an insurer purchases individual coverage policies in a reinsurance market on each active site, that is, each site that has not yet had a quake. At the beginning of the coverage period, Strategies A and S purchase an individual reinsurance policy covering the T-day coverage period on each of the n active sites from n reinsurers. During the coverage period Strategy A purchases no additional insurance, but each time a quake occurs, Strategy S purchases additional reinsurance coverage for the remainder of the coverage period. By contrast, at the beginning of each review period, including the first, Strategy C buys reinsurance on each active site covering that period only, the amount of coverage depending on the number of active sites and the time remaining in the coverage period.

Acquiring reinsurance incurs a cost based on the coverage amount, the coverage period, and reinsurers’ markups, which reflect their levels of risk aversion. Let r denote the probability that a quake occurs during the reinsurance interval and b, the reinsurance coverage amount to purchase per active site. A reinsurer charges the insurer  $g(r,b)\times r\times b$ per active site, where

$g(r,b)\times r\times b$ per active site, where  $g(r,b)$ denotes the markup that makes a reinsurer indifferent between offering and not offering reinsurance. To determine

$g(r,b)$ denotes the markup that makes a reinsurer indifferent between offering and not offering reinsurance. To determine  $g(r,b)$, we again rely on expected utility theory.

$g(r,b)$, we again rely on expected utility theory.

Suppose a reinsurer has the concave increasing utility function,  $\{\lambda(w),~-\infty \lt w \lt \infty\}$, where w denotes his wealth. For given initial wealth w, the reinsurer’s final wealth is

$\{\lambda(w),~-\infty \lt w \lt \infty\}$, where w denotes his wealth. For given initial wealth w, the reinsurer’s final wealth is

\begin{equation}

\kappa:= w + g(r,b) r b -

\left\{

\begin{array}{ll}

b&\mbox {if a quake occurs at the reinsured site} \\ \\

0&\mbox{otherwise}.

\end{array}

\right.

\end{equation}

\begin{equation}

\kappa:= w + g(r,b) r b -

\left\{

\begin{array}{ll}

b&\mbox {if a quake occurs at the reinsured site} \\ \\

0&\mbox{otherwise}.

\end{array}

\right.

\end{equation} Then, for given r and b, the reinsurer’s indifference markup  $g(r,b)$ satisfies the expected utility equation,

$g(r,b)$ satisfies the expected utility equation,  ${\rm E} \lambda(\kappa) = \lambda(w)$. In the present context, this equation is equivalent to

${\rm E} \lambda(\kappa) = \lambda(w)$. In the present context, this equation is equivalent to

\begin{equation}

(1-r)\lambda(w+ g(r,b) r b)+r \lambda(w+ g(r,b) r b - b)=\lambda(w).

\end{equation}

\begin{equation}

(1-r)\lambda(w+ g(r,b) r b)+r \lambda(w+ g(r,b) r b - b)=\lambda(w).

\end{equation} Expression (6) has at least two notable properties. First,  $g(r,b)$ is strictly increasing in the coverage for given r. Also,

$g(r,b)$ is strictly increasing in the coverage for given r. Also,  $g(r,b)$ is decreasing in the probability r for given coverage b, provided that the Arrow-Pratt measure of absolute risk aversion,

$g(r,b)$ is decreasing in the probability r for given coverage b, provided that the Arrow-Pratt measure of absolute risk aversion,  $- \frac{\lambda''(w)}{\lambda'(w)}$, is non-increasing in w (equivalently,

$- \frac{\lambda''(w)}{\lambda'(w)}$, is non-increasing in w (equivalently,  $\lambda(w)$ is log-convex).Footnote 2

$\lambda(w)$ is log-convex).Footnote 2

As an illustration of a utility function with these properties, suppose a reinsurer has the exponential utility function

\begin{equation}\lambda(w)=-\mathrm e^{-\lambda w}\;,\;\gamma \gt 0.\end{equation}

\begin{equation}\lambda(w)=-\mathrm e^{-\lambda w}\;,\;\gamma \gt 0.\end{equation} Then, for each active site, his indifference premium for coverage b is  $g(r,b)\times b\times r$, with markup

$g(r,b)\times b\times r$, with markup

\begin{equation}g(r,b)=\frac{\ln\left(1-r+r\mathrm e^{\gamma b}\right)}{\gamma rb}\end{equation}

\begin{equation}g(r,b)=\frac{\ln\left(1-r+r\mathrm e^{\gamma b}\right)}{\gamma rb}\end{equation}with limiting behavior

\begin{equation*}\lim_{r\rightarrow0}g(r,b)=\frac{\mathrm e^{\gamma b}-1}{\gamma b}\leq\frac{\mathrm e^{\mathrm\gamma\mathrm\theta}-1}{\gamma\theta},\;b\in\lbrack0,\theta\rbrack,\end{equation*}

\begin{equation*}\lim_{r\rightarrow0}g(r,b)=\frac{\mathrm e^{\gamma b}-1}{\gamma b}\leq\frac{\mathrm e^{\mathrm\gamma\mathrm\theta}-1}{\gamma\theta},\;b\in\lbrack0,\theta\rbrack,\end{equation*}and

\begin{equation*}

\lim_{b \rightarrow 0} g(r,b) = 1.

\end{equation*}

\begin{equation*}

\lim_{b \rightarrow 0} g(r,b) = 1.

\end{equation*}For convenience of exposition, we hereafter assume that all reinsurers have the same exponential utility function given by (7). Then the insurer’s cost of reinsuring n active sites is

\begin{equation*}ng(r,b)rb=n\gamma^{-1}\ln(1-r+r\mathrm e^{\gamma b}).\end{equation*}

\begin{equation*}ng(r,b)rb=n\gamma^{-1}\ln(1-r+r\mathrm e^{\gamma b}).\end{equation*}All illustrations in this study assume utility functions (3) and (7) for the insurer and reinsurer respectively.

3. Strategy A

Strategy A is a relatively conventional procedure. For coverage of θ dollars, an insurer with initial wealth  $w_{\mathrm{I}}$ offers a customer an m-out-of-n policy at premium π per coverage dollar for a total premium πθ. After receiving this premium, the insurer has working capital equal to

$w_{\mathrm{I}}$ offers a customer an m-out-of-n policy at premium π per coverage dollar for a total premium πθ. After receiving this premium, the insurer has working capital equal to  $w_{\mathrm{I}} + \pi \theta$. At the beginning of the coverage period, the insurer uses funds from this working capital to make a one-time purchase of reinsurance with coverage ϕ on each of the n sites at a total cost

$w_{\mathrm{I}} + \pi \theta$. At the beginning of the coverage period, the insurer uses funds from this working capital to make a one-time purchase of reinsurance with coverage ϕ on each of the n sites at a total cost  $n\times g(q,\phi)\times \phi\times q$, where the reinsurer’s indifference markup per dollar of coverage is

$n\times g(q,\phi)\times \phi\times q$, where the reinsurer’s indifference markup per dollar of coverage is

\begin{equation*}

g(q,\phi)=\frac{\ln(1-q+q\rm e^{\gamma \phi})}{\gamma \phi q}.

\end{equation*}

\begin{equation*}

g(q,\phi)=\frac{\ln(1-q+q\rm e^{\gamma \phi})}{\gamma \phi q}.

\end{equation*}If m or more quakes occur during the coverage period T, the insurer pays the customer θ dollars. If j quakes occur during the coverage period, then the insurer’s final working capital is

\begin{equation}

\kappa_{\mathrm{A}}=w_{\mathrm{I}} +\pi \theta-n \gamma^{-1}\ln(1-q+q\rm e^{\gamma \phi}) - {\it Y}(\phi,j),

\end{equation}

\begin{equation}

\kappa_{\mathrm{A}}=w_{\mathrm{I}} +\pi \theta-n \gamma^{-1}\ln(1-q+q\rm e^{\gamma \phi}) - {\it Y}(\phi,j),

\end{equation}where

\begin{equation}

Y(\phi,j):= - j \phi + (1-I_{j \lt m})\theta, \; j \in \{0,1,\ldots,n \},

\end{equation}

\begin{equation}

Y(\phi,j):= - j \phi + (1-I_{j \lt m})\theta, \; j \in \{0,1,\ldots,n \},

\end{equation} where  $I_{a \lt b} = 1$ if a < b and 0 otherwise. In words,

$I_{a \lt b} = 1$ if a < b and 0 otherwise. In words,  $Y(\phi,j)$ is the portion of the insurer’s obligation to the customer that reinsurance does not cover—the amount that he self-insures—given that j sites have quakes in the coverage period. Note that

$Y(\phi,j)$ is the portion of the insurer’s obligation to the customer that reinsurance does not cover—the amount that he self-insures—given that j sites have quakes in the coverage period. Note that  $Y(\phi,j) \lt 0$ for j > 0 and sufficiently large ϕ, in which case the insurer retains a surplus from reinsurance after paying his obligation to the customer, thus making a profit. If

$Y(\phi,j) \lt 0$ for j > 0 and sufficiently large ϕ, in which case the insurer retains a surplus from reinsurance after paying his obligation to the customer, thus making a profit. If  $Y(\phi,j) \gt 0$, then he incurs a loss.

$Y(\phi,j) \gt 0$, then he incurs a loss.

This study assumes that quakes at different sites are probabilistically independent. The independence of quakes across sites that are “widely separated geographically” is well established in geophysics, provided, of course, that the separation is wide enough. At one extreme, there is little dispute about independence across sites on different continents. Independence might not apply, however, to sites that are relatively far apart but located near the same fault or near different faults that are close enough that a quake on one fault might result in added strain on the other. (Independence across time at a particular site is arguably more problematic, but our model assumes that only the first quake at a site during the year is relevant, so this is not an issue.)

For k > 0, denote the binomial probability mass function and cumulative distribution function respectively by

\begin{equation}

\begin{array}{rl}

f(j;k,r) =& {{k}\choose {j}}r^j(1-r)^{k-j}\qquad r\in(0,1),~ j\in\{0,1,\ldots,k\}, \\

& \\

F(j;k,r) =&\sum_{j=0}^{j}f(j;k,r)\qquad j\in\{0,1,\ldots,k\}.

\end{array}

\end{equation}

\begin{equation}

\begin{array}{rl}

f(j;k,r) =& {{k}\choose {j}}r^j(1-r)^{k-j}\qquad r\in(0,1),~ j\in\{0,1,\ldots,k\}, \\

& \\

F(j;k,r) =&\sum_{j=0}^{j}f(j;k,r)\qquad j\in\{0,1,\ldots,k\}.

\end{array}

\end{equation} The insurer first identifies solutions  $(\pi,\phi)$ that satisfy the indifference condition (2) for his exponential utility function (3), that is

$(\pi,\phi)$ that satisfy the indifference condition (2) for his exponential utility function (3), that is

\begin{equation*}{\rm E} u(\kappa_{\rm A})=-\sum_{j=0}^{n}{\rm e}^{-\alpha \kappa_{\rm A}}f(j;n,q)=u(w_{\rm I})=-{\rm e}^{-\alpha w_{\rm I}},\end{equation*}

\begin{equation*}{\rm E} u(\kappa_{\rm A})=-\sum_{j=0}^{n}{\rm e}^{-\alpha \kappa_{\rm A}}f(j;n,q)=u(w_{\rm I})=-{\rm e}^{-\alpha w_{\rm I}},\end{equation*}or equivalently, using (4),

\begin{equation}{\rm E} u(\kappa_{\rm A}-w_{\rm I})=-{\rm e}^{-\alpha[\pi\theta-nqg(q,\phi)\phi]}\times

\underbrace{\left[\sum_{j=0}^{m-1}{\rm e}^{-\alpha j \phi}f(j;n,q)+{\rm e}^{\alpha\theta}\sum_{j=m}^{n}{\rm e}^{-\alpha j \phi}f(j;n,q)\right] }_{h(\phi)=}

= -1,\end{equation}

\begin{equation}{\rm E} u(\kappa_{\rm A}-w_{\rm I})=-{\rm e}^{-\alpha[\pi\theta-nqg(q,\phi)\phi]}\times

\underbrace{\left[\sum_{j=0}^{m-1}{\rm e}^{-\alpha j \phi}f(j;n,q)+{\rm e}^{\alpha\theta}\sum_{j=m}^{n}{\rm e}^{-\alpha j \phi}f(j;n,q)\right] }_{h(\phi)=}

= -1,\end{equation}subject to the constraints

\begin{equation}

0 \leq \phi \leq \phi_{\rm max}, \; 0 \leq \pi \leq 1,

\end{equation}

\begin{equation}

0 \leq \phi \leq \phi_{\rm max}, \; 0 \leq \pi \leq 1,

\end{equation} where ϕ max denotes the maximal value of ϕ that is eligible for inclusion in an indifference pair  $(\pi,\phi)$. Note that

$(\pi,\phi)$. Note that  $h(\phi)=\mathrm E\lbrack\mathrm e^{\alpha Y(\phi,J)}\rbrack$, where the random variable

$h(\phi)=\mathrm E\lbrack\mathrm e^{\alpha Y(\phi,J)}\rbrack$, where the random variable  $J:= $ the total number of sites that have quakes in the coverage period, and

$J:= $ the total number of sites that have quakes in the coverage period, and  $Y(\phi,j)$ (defined in (10)) is the portion of the insurer’s obligation that reinsurance does not cover (the amount that he self-insures) given that J = j. In other words,

$Y(\phi,j)$ (defined in (10)) is the portion of the insurer’s obligation that reinsurance does not cover (the amount that he self-insures) given that J = j. In other words,  $h(\phi)$ is the insurer’s expected disutility of the out-of-pocket cost he incurs if he purchases reinsurance coverage ϕ on each of the n sites at the beginning of the year.

$h(\phi)$ is the insurer’s expected disutility of the out-of-pocket cost he incurs if he purchases reinsurance coverage ϕ on each of the n sites at the beginning of the year.

3.1. Indifference premium

Let

\begin{equation*}

\cal A=\mbox{collection of all 2-tuples},\, (\pi,\phi),\, \mbox{that satisfy (12) and (13)}.

\end{equation*}

\begin{equation*}

\cal A=\mbox{collection of all 2-tuples},\, (\pi,\phi),\, \mbox{that satisfy (12) and (13)}.

\end{equation*} That is,  $\cal A$ is the feasible, indifference set of

$\cal A$ is the feasible, indifference set of  $(\pi,\phi)$ solutions for Strategy A each of which satisfies

$(\pi,\phi)$ solutions for Strategy A each of which satisfies

\begin{equation}

\pi \theta = \gamma^{-1} n \ln(1 - q + q \rm e^{\gamma \phi}) + \alpha^{-1} \ln \mathit{h}(\phi),

\end{equation}

\begin{equation}

\pi \theta = \gamma^{-1} n \ln(1 - q + q \rm e^{\gamma \phi}) + \alpha^{-1} \ln \mathit{h}(\phi),

\end{equation} which is equivalent to (12). In words, the 2-tuple  $(\pi,\phi)$ is an indifference solution for the insurer if and only if the total premium πθ received from the customer equals the certainty equivalent of the insurer’s total outlay, that outlay being the sum of the insurer’s total premium paid for reinsurance and the amount of the risk that he self-insures. If the market-determined premium

$(\pi,\phi)$ is an indifference solution for the insurer if and only if the total premium πθ received from the customer equals the certainty equivalent of the insurer’s total outlay, that outlay being the sum of the insurer’s total premium paid for reinsurance and the amount of the risk that he self-insures. If the market-determined premium  $\pi_{\mathrm{M}}$ is no less than the smallest premium π in

$\pi_{\mathrm{M}}$ is no less than the smallest premium π in  $\cal A$, the insurer can be competitive by choosing a 2-tuple

$\cal A$, the insurer can be competitive by choosing a 2-tuple  $(\pi,\phi)\in\cal A$ with π no greater than

$(\pi,\phi)\in\cal A$ with π no greater than  $\pi_{\mathrm{M}}$.

$\pi_{\mathrm{M}}$.

Because the reinsurers’ total premium  $n \gamma^{-1} \ln(1-q+q \rm e^{\gamma\phi})$ is convex, strictly increasing in ϕ and

$n \gamma^{-1} \ln(1-q+q \rm e^{\gamma\phi})$ is convex, strictly increasing in ϕ and  $\ln h(\phi)$ is convex strictly decreasing in ϕ, π is convex in ϕ. Moreover,

$\ln h(\phi)$ is convex strictly decreasing in ϕ, π is convex in ϕ. Moreover,

\begin{equation*}

\left. \frac{\rm d \pi}{\rm d \phi} \right |_{\phi=0} =

nq - \frac{\sum_{j=1}^{m-1} j f(j;n,q) + \it {\textrm{e}}^{\alpha \theta} \sum_{j=m}^n j f(j;n,q)}

{\sum_{j=0}^{m-1} f(j;n,q) + \it {\textrm{e}}^{\alpha\theta} \sum_{j=m}^n f(j;n,q)},

\end{equation*}

\begin{equation*}

\left. \frac{\rm d \pi}{\rm d \phi} \right |_{\phi=0} =

nq - \frac{\sum_{j=1}^{m-1} j f(j;n,q) + \it {\textrm{e}}^{\alpha \theta} \sum_{j=m}^n j f(j;n,q)}

{\sum_{j=0}^{m-1} f(j;n,q) + \it {\textrm{e}}^{\alpha\theta} \sum_{j=m}^n f(j;n,q)},

\end{equation*} so that  $q \lt \frac{1}{n}$ is sufficient for

$q \lt \frac{1}{n}$ is sufficient for  $ \frac{\rm d \pi}{\rm d \phi} |_{\phi=0} \lt 0$. Hereafter we assume this condition is satisfied.

$ \frac{\rm d \pi}{\rm d \phi} |_{\phi=0} \lt 0$. Hereafter we assume this condition is satisfied.

The remainder of this section assumes that the upper bound ϕ max is defined by the equation,

\begin{equation}

\ln h(\phi) = 0,

\end{equation}

\begin{equation}

\ln h(\phi) = 0,

\end{equation} so that ϕ max is the unique value of ϕ for which the certainty equivalent of the self-insured risk, namely,  $\alpha^{-1} \ln \ h(\phi)$, equals zero. Then it follows from (14) that the constraints (13) on

$\alpha^{-1} \ln \ h(\phi)$, equals zero. Then it follows from (14) that the constraints (13) on  $(\pi,\phi)$ are equivalent to

$(\pi,\phi)$ are equivalent to

\begin{equation}

0 \leq \theta^{-1} n g(q,\phi) q \phi \leq \pi \lt 1,

\end{equation}

\begin{equation}

0 \leq \theta^{-1} n g(q,\phi) q \phi \leq \pi \lt 1,

\end{equation} and the indifference 2-tuple  $(\pi,\phi)$ satisfies

$(\pi,\phi)$ satisfies

\begin{equation}

\pi \theta = n g(q,\phi) q \phi = n \gamma^{-1}\ln(1-q+q \rm e^{\gamma\phi}) \;

\end{equation}

\begin{equation}

\pi \theta = n g(q,\phi) q \phi = n \gamma^{-1}\ln(1-q+q \rm e^{\gamma\phi}) \;

\end{equation} if and only if  $\phi = \phi_{\rm max}$, in which case the insurer uses all funds received from the customer (and only these funds) to purchase reinsurance.

$\phi = \phi_{\rm max}$, in which case the insurer uses all funds received from the customer (and only these funds) to purchase reinsurance.

This choice for  $\phi = \phi_{\rm max}$ is intuitively appealing because any larger value of ϕ would require that the insurer pay a portion of the cost for reinsurance out of pocket at the beginning of the coverage period. Conventional wisdom regarding the purchase of reinsurance frowns on this practice.Footnote 3

$\phi = \phi_{\rm max}$ is intuitively appealing because any larger value of ϕ would require that the insurer pay a portion of the cost for reinsurance out of pocket at the beginning of the coverage period. Conventional wisdom regarding the purchase of reinsurance frowns on this practice.Footnote 3

Three premium options of particular interest are:

$\mathrm{A}_{\rm i}$. For a minimal premium, choose π corresponding to the largest

$\phi \in [0,\phi_{\rm max}]$ satisfying

$\frac{\rm d\pi}{\rm d\phi}\leq 0$

$\mathrm{A}_{\rm i}$. For a minimal premium, choose π corresponding to the largest

$\phi \in [0,\phi_{\rm max}]$ satisfying

$\frac{\rm d\pi}{\rm d\phi}\leq 0$-

$\mathrm{A}_{\rm ii}$. For maximal reinsurance coverage

$\phi_{\max}$, choose

$\pi=n(\gamma\theta)^{-1}\ln(1-q+q \rm e^{\gamma \phi_{\max}})$

-

$\mathrm{A}_{\rm{iii}}$. For no reinsurance (ϕ = 0), choose

$\pi=(\alpha\theta)^{-1}\ln h(0)$.

Proposition 3.1. The condition  $q \lt \frac{1}{n}$ and the convexity of π in (14) imply:

$q \lt \frac{1}{n}$ and the convexity of π in (14) imply:

(i) If

$\frac{\rm d\pi}{\rm d\phi}|_{\phi = \phi_{\rm max}} \leq 0$,

$\pi_{\rm A_{\rm i}}=\pi_{\rm A_{\rm ii}}$ and

$\phi_{\rm A_{\rm i}}=\phi_{\rm A_{\rm ii}}=\phi_{\rm max}$.(ii) If

$\frac{\rm d\pi}{\rm d\phi}|_{\phi = \phi_{\rm max}} \gt 0$,

$\pi_{\rm A_{\rm i}} \lt \pi_{\rm A_{\rm ii}}$ and

$\phi_{\rm A_{\rm i}} \lt \phi_{\rm A_{\rm ii}} = \phi_{\rm max} $.(iii) The condition

$q {\rm e}^{\gamma \phi_{\rm max}} \gt \left[h(0)\right]^{\gamma/n \alpha} - (1 - q)$ is sufficient for

$\pi_{\rm A_{\rm i}} \lt \pi_{\rm A_{\rm ii}}$ and

$\phi_{\rm A_{\rm i}} \lt \phi_{\rm A_{\rm ii}} = \phi_{\rm max}$.(iv)

$\pi_{\rm A_{\rm iii}} \gt \max[\pi_{\rm A_{\rm i}},\pi_{\rm A_{\rm ii}}]$.

The proof follows from the convexity of (14). As an illustration, for Proposition 3.1(iii), because we have assumed that  $q \lt 1/n$,

$q \lt 1/n$,  $(d \pi/d \phi) |_{\phi = 0} \lt 0$. Therefore,

$(d \pi/d \phi) |_{\phi = 0} \lt 0$. Therefore,  $\pi_{\rm A_{\rm i}} \lt \pi_{\rm A_{\rm ii}}$ if

$\pi_{\rm A_{\rm i}} \lt \pi_{\rm A_{\rm ii}}$ if  $\pi_{A_{iii}} \lt \pi_{A_{ii}}$. The latter inequality is equivalent to

$\pi_{A_{iii}} \lt \pi_{A_{ii}}$. The latter inequality is equivalent to

\begin{equation}

\left( \frac{\gamma}{n \alpha} \right) \ln (h(0)) \lt \ln( 1 - q + q \rm e^{\gamma \phi_{\rm max}}),

\end{equation}

\begin{equation}

\left( \frac{\gamma}{n \alpha} \right) \ln (h(0)) \lt \ln( 1 - q + q \rm e^{\gamma \phi_{\rm max}}),

\end{equation}which in turn is equivalent to

\begin{equation*}

\left[h(0)\right]^{\gamma/n \alpha} \lt 1 - q + q \rm e^{\gamma \phi_{\rm max}}.

\end{equation*}

\begin{equation*}

\left[h(0)\right]^{\gamma/n \alpha} \lt 1 - q + q \rm e^{\gamma \phi_{\rm max}}.

\end{equation*}3.2. Loss and profit

Each solution in  $\cal A$ has different implications for competitiveness, final working capital, and loss probability. For all

$\cal A$ has different implications for competitiveness, final working capital, and loss probability. For all  $\phi\in[0,\phi_{\max}]$, define

$\phi\in[0,\phi_{\max}]$, define

\begin{equation}

\psi_j(\phi):= \alpha^{-1}\ln h(\phi) - Y(\phi,j), \; j \in \{0,1,\ldots,n\},

\end{equation}

\begin{equation}

\psi_j(\phi):= \alpha^{-1}\ln h(\phi) - Y(\phi,j), \; j \in \{0,1,\ldots,n\},

\end{equation} where  $Y(\phi,j)$ is defined by (10), and define

$Y(\phi,j)$ is defined by (10), and define

\begin{equation}

\mu_{\mathrm{A}}(\phi):= \sum_{j=0}^n I_{\psi_j(\phi) \lt 0}\,f(j;n,q).

\end{equation}

\begin{equation}

\mu_{\mathrm{A}}(\phi):= \sum_{j=0}^n I_{\psi_j(\phi) \lt 0}\,f(j;n,q).

\end{equation} In words,  $\psi_j(\phi)$ is the difference between the insurer’s certainty equivalent of the amount he self-insures and the actual amount of self-insurance when j sites have quakes, and

$\psi_j(\phi)$ is the difference between the insurer’s certainty equivalent of the amount he self-insures and the actual amount of self-insurance when j sites have quakes, and  $\mu_{\mathrm{A}}(\phi)$ is the probability that this difference is negative. Note that these quantities are well defined and economically meaningful regardless of the value of the premium π. For the special case where

$\mu_{\mathrm{A}}(\phi)$ is the probability that this difference is negative. Note that these quantities are well defined and economically meaningful regardless of the value of the premium π. For the special case where  $(\pi,\phi) \in \cal A$ (that is, where π is the indifference premium corresponding to ϕ), it follows from the indifference equation (14) that

$(\pi,\phi) \in \cal A$ (that is, where π is the indifference premium corresponding to ϕ), it follows from the indifference equation (14) that

\begin{equation*}

\psi_j(\phi) = \pi \theta - n g(q,\phi) q \phi - Y(\phi,j), \; j \in \{0,1,\ldots,n\},

\end{equation*}

\begin{equation*}

\psi_j(\phi) = \pi \theta - n g(q,\phi) q \phi - Y(\phi,j), \; j \in \{0,1,\ldots,n\},

\end{equation*} so that in this case,  $\psi_j(\phi)$ can also be interpreted as the net change in working capital when j quakes occur during the coverage period and

$\psi_j(\phi)$ can also be interpreted as the net change in working capital when j quakes occur during the coverage period and  $\mu_{\mathrm{A}}(\phi)$ as the probability that this net change is negative, that is, the probability that the insurer incurs a loss.

$\mu_{\mathrm{A}}(\phi)$ as the probability that this net change is negative, that is, the probability that the insurer incurs a loss.

Proposition 3.2. For options  $\rm A_{\rm i}$ and

$\rm A_{\rm i}$ and  $\rm A_{\rm ii}$, if

$\rm A_{\rm ii}$, if

\begin{equation}

j \gt \frac{\gamma\theta(1-\pi)}{q+(1-q)\rm e^{-\gamma\phi}}\qquad\mbox{for some }j\in\{m,\ldots,n\},

\end{equation}

\begin{equation}

j \gt \frac{\gamma\theta(1-\pi)}{q+(1-q)\rm e^{-\gamma\phi}}\qquad\mbox{for some }j\in\{m,\ldots,n\},

\end{equation} then  $\mu_{\rm A}(\phi) = {\rm pr}( \#\ \mbox{ quakes } \geq m) .$ If

$\mu_{\rm A}(\phi) = {\rm pr}( \#\ \mbox{ quakes } \geq m) .$ If

\begin{equation}

\phi\leq \ln\left[\frac{1-q}{\frac{\gamma\theta}{n}(1-\pi)-q}\right],

\end{equation}

\begin{equation}

\phi\leq \ln\left[\frac{1-q}{\frac{\gamma\theta}{n}(1-\pi)-q}\right],

\end{equation}  $\mu_{\rm A}(\phi)= {\rm pr}( \#\ \mbox{ quakes } \geq m)$. If (22) holds, then the benefit of relying on reinsurance in Strategy A arises from reducing loss while not affecting loss probability.

$\mu_{\rm A}(\phi)= {\rm pr}( \#\ \mbox{ quakes } \geq m)$. If (22) holds, then the benefit of relying on reinsurance in Strategy A arises from reducing loss while not affecting loss probability.

Because  $\pi\leq 1$ for option iii,

$\pi\leq 1$ for option iii,  $\mu_{{\rm A}_{\rm iii}} = {\rm pr}( \#\ \mbox{ quakes } \geq m) = 1 - F(m-1;n,q)$.

$\mu_{{\rm A}_{\rm iii}} = {\rm pr}( \#\ \mbox{ quakes } \geq m) = 1 - F(m-1;n,q)$.

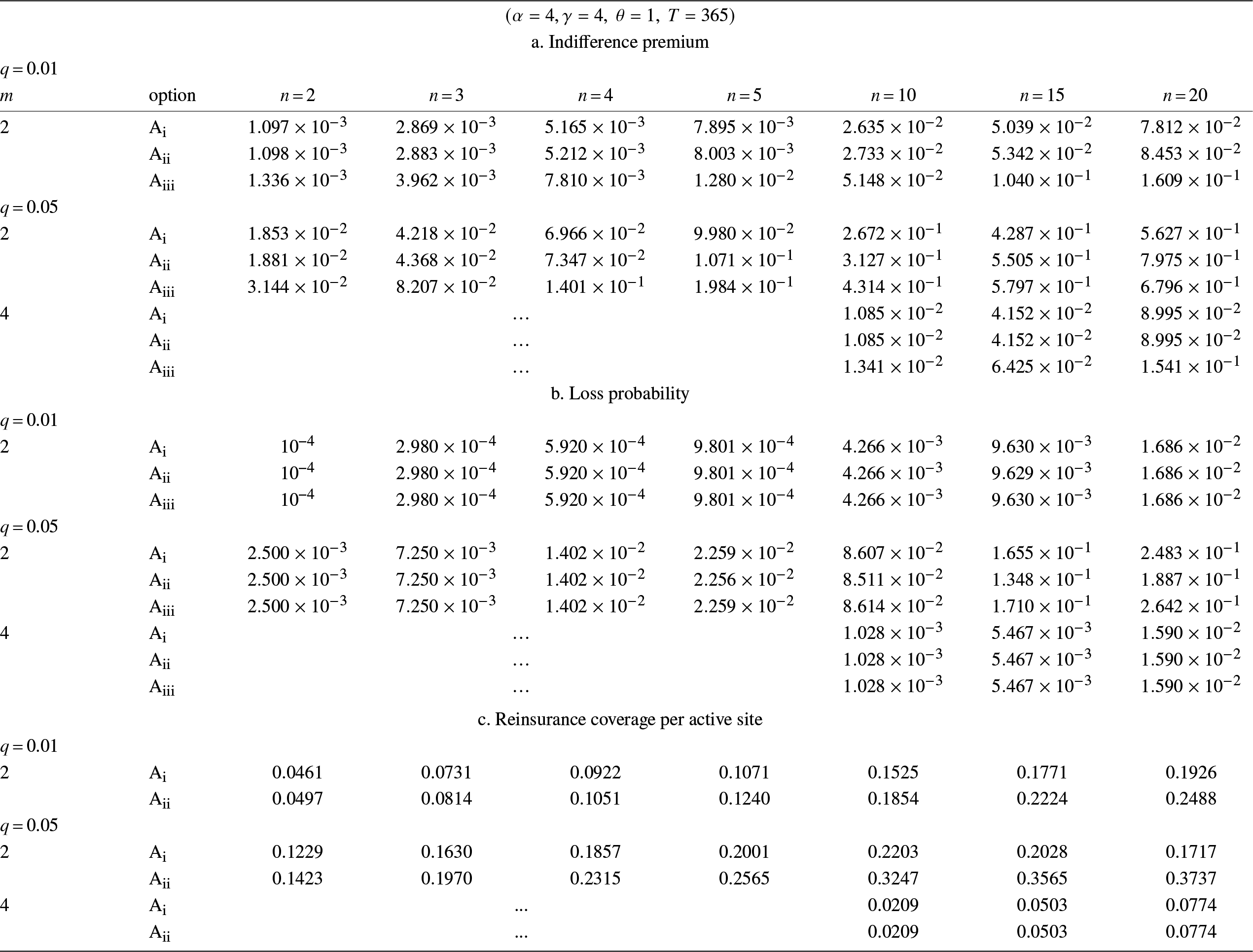

3.3. Comparing options for Strategy A

Table 2 displays indifference premiums, loss probabilities, and reinsurance coverages for options i, ii, and iii for Strategy A based on exponential utility functions for insurer and reinsurers and on variable reinsurance markups as in (8). All entries were numerically computed.

Strategies A: Options  ${\rm i},~{\rm ii},~{\rm iii}$†.

${\rm i},~{\rm ii},~{\rm iii}$†.

† Entries: blank := m > n;  $...:=\mu_{\rm A}(0) \lt 10^{-4}$.

$...:=\mu_{\rm A}(0) \lt 10^{-4}$.

Because reinsurers tend to be less risk averse than insurers, it is not unreasonable to assume levels of risk aversion  $\gamma \leq \alpha$. All comparisons are based on

$\gamma \leq \alpha$. All comparisons are based on  $\alpha=\gamma =4$, allowing us to regard the reinsurer’s markup as an upper bound. The tables show results for

$\alpha=\gamma =4$, allowing us to regard the reinsurer’s markup as an upper bound. The tables show results for  $(m,n,q)$ scenarios for which option A iii (no reinsurance) has loss probabilities

$(m,n,q)$ scenarios for which option A iii (no reinsurance) has loss probabilities  $\mu_{\mathrm{A}}(0)\geq 10^{-4}$. (When

$\mu_{\mathrm{A}}(0)\geq 10^{-4}$. (When  $\mu_{\mathrm{A}}(0) \lt 10^{-4}$, there is arguably no incentive for the insurer to consider reinsurance.)

$\mu_{\mathrm{A}}(0) \lt 10^{-4}$, there is arguably no incentive for the insurer to consider reinsurance.)

The table reveals that:

A1. Option iii (no reinsurance) has the largest premiums. For q = 0.01, option ii premiums exceed those for option i by relatively small amounts. For q = 0.05 and m = 2, option ii again has larger premiums, but here the relative differences increase as n increases. For m = 4, options i and ii have the same premiums for each n.

A2. For

$(m,q)=(2,0.01)$ and

$(4,0.05)$, all options have identical loss probabilities for each n, with one minor exception. For

$(m.q)=(2,0.05)$, they are also identical for

$n=2,\ldots,5$, but

$\mu_{\mathrm{A}}(\phi_{\rm A_{\rm ii}}) \lt \mu_{\mathrm{A}}(\phi_{\rm A_{\rm i}}) \lt \mu_{\mathrm{A}}(\phi_{\rm A_{\rm iii}})$ for

$n=10,15,20$. That is, buying reinsurance for scenarios other than

$(m.q)=(2,0.05)$A3. For

$(m,q)=(2,0.01)$ and

$(4,0.05)$, option ii has smaller reinsurance coverage per active site. For

$(m.q)=(2,0.05)$, options i and ii have the same reinsurance coverages for each n, consistent with having the same premiums in point A1. For this case, option i actually has the smaller loss for any

$j\geq m$.A4. The relatively large premiums for

$m=2,~q=0.05$, and

$n=10,15,20$ make an m-out-of-n policy based on Strategy A unappealing for these scenarios. Later tables show the same is true for Strategies S and C.

As expected for given m and q, option iii (no reinsurance) has the largest premiums and option ii has the smallest in Table 2a. Moreover, premiums for option iii (maximal coverage) differ relatively little from those for option ii, with the difference increasing as n increases.

With the exceptions of m = 2, q = 0.01, and  $n=10,15,20$, the three options have identical loss probabilities to four digits in Table 2b. Clearly the condition of Proposition 3.1(i) is satisfied only for these exceptions. (See Appendix for further discussion of the implications of this condition.) For m = 2 and q = 0.01, option ii’s reinsurance coverage per active site exceeds option i’s by about 8% for n = 2, increasing to about 29% for n = 20. For m = 2 and q = 0.05, option ii’s coverage exceeds that of option i by about 16% for n = 2, increasing to about 118% at n = 20. However, both options have the same coverage for m = 4, consistent with their identical premiums in Table 2a. This occurs because for

$n=10,15,20$, the three options have identical loss probabilities to four digits in Table 2b. Clearly the condition of Proposition 3.1(i) is satisfied only for these exceptions. (See Appendix for further discussion of the implications of this condition.) For m = 2 and q = 0.01, option ii’s reinsurance coverage per active site exceeds option i’s by about 8% for n = 2, increasing to about 29% for n = 20. For m = 2 and q = 0.05, option ii’s coverage exceeds that of option i by about 16% for n = 2, increasing to about 118% at n = 20. However, both options have the same coverage for m = 4, consistent with their identical premiums in Table 2a. This occurs because for  $(m,n,q)=(4,n,0.05)$, π in (14) is strictly decreasing in ϕ over

$(m,n,q)=(4,n,0.05)$, π in (14) is strictly decreasing in ϕ over  $[0,\phi_{\max}]$.

$[0,\phi_{\max}]$.

4. Strategy S

In contrast to Strategy A, which is static, Strategies S and C are adaptive. Each time a quake occurs, Strategy S increases the amount of reinsurance coverage, whereas Strategy C (in the next section) adjusts coverage periodically. Under Strategy S, the insurer offers the customer an m-out-of-n policy for a total premium πθ. After collecting the premium from the customer at the beginning of the coverage period, the insurer with initial wealth w I now has working capital  $w_{\rm I }+ \pi \theta$. As with Strategy A, Strategy S uses funds from working capital to purchase initial reinsurance coverage ϕ on each of the n sites for the entire coverage period. Both π and ϕ are decision variables, the values of which are determined at the beginning of the coverage period. Whereas Strategy A fixes the reinsurance coverage at the beginning of the coverage period, Strategy S uses the proceeds from the reinsurance policies on the sites where quakes have just occurred to purchase additional reinsurance for the remainder of the coverage period on each remaining active site, until either m of the n sites have had quakes or the coverage period ends, whichever occurs first.

$w_{\rm I }+ \pi \theta$. As with Strategy A, Strategy S uses funds from working capital to purchase initial reinsurance coverage ϕ on each of the n sites for the entire coverage period. Both π and ϕ are decision variables, the values of which are determined at the beginning of the coverage period. Whereas Strategy A fixes the reinsurance coverage at the beginning of the coverage period, Strategy S uses the proceeds from the reinsurance policies on the sites where quakes have just occurred to purchase additional reinsurance for the remainder of the coverage period on each remaining active site, until either m of the n sites have had quakes or the coverage period ends, whichever occurs first.

For a given quake history, let

\begin{equation*}\begin{array}{rl}

T=&\mbox{number of days in coverage period} \\ \\ j_i=&\mbox{number of quakes }(\geq 1)\mbox{ on the }i\mbox{-th quake day} \;,\; i \geq 1 \\ \\

k_i=&k_{i-1}-j_i=\mbox{number of active sites at the end of the }i\mbox{-th quake day }\;\;(k_0=n)\;,\;i\geq1 \\ \\

{\mathbf j}_l=&(j_1,\dots,j_l) \;,\; 1\leq l \leq m \;\;({\mathbf j}_0=(0))

\end{array}\end{equation*}

\begin{equation*}\begin{array}{rl}

T=&\mbox{number of days in coverage period} \\ \\ j_i=&\mbox{number of quakes }(\geq 1)\mbox{ on the }i\mbox{-th quake day} \;,\; i \geq 1 \\ \\

k_i=&k_{i-1}-j_i=\mbox{number of active sites at the end of the }i\mbox{-th quake day }\;\;(k_0=n)\;,\;i\geq1 \\ \\

{\mathbf j}_l=&(j_1,\dots,j_l) \;,\; 1\leq l \leq m \;\;({\mathbf j}_0=(0))

\end{array}\end{equation*} \begin{equation*}

\begin{array}{rl}

{\mathcal J}_l= & \{{\mathbf j}_l:\;j_i\geq1\;,\;1\leq i\leq l\;,\;j_1+\cdots+j_l \lt m\}\;,\;1\leq l\leq m-1 \\ \\

{\mathcal J}_l^{\prime}= & \{{\mathbf j}_l:\;j_i\geq1\;,\;1\leq i\leq l\;,\;j_1+\cdots+j_{l-1} \lt m \leq j_1+\cdots+j_l\}\;,\;1\leq l \leq m \\ \\s_i=&\text{day on which the }i\text{-th quake day occurs}\;,\;i\geq1\;\;(s_0=0) \\ \\

{\mathbf s}_l= & (s_0,s_1,\dots,s_l)\;,\;1\leq l\leq m\\ \\

{\mathcal S}_l= & \{{\mathbf s}_l:\;s_0 \lt s_1 \lt \cdots \lt s_l = T\}\;,\;1\leq l \leq m \\ \\

{\mathcal S}_l^{\prime}= & \{{\mathbf s}_l:\;s_0 \lt s_1 \lt \cdots \lt s_l\leq T\}\;,\;1\leq l \leq m \\ \\

{\mathcal S}_l^{\prime\prime}= & \{{\mathbf s}_l:\;s_0 \lt s_1 \lt \cdots \lt s_l \lt T \lt s_{l+1}\},\; 1 \leq l \leq m

\end{array}\qquad \qquad \end{equation*}

\begin{equation*}

\begin{array}{rl}

{\mathcal J}_l= & \{{\mathbf j}_l:\;j_i\geq1\;,\;1\leq i\leq l\;,\;j_1+\cdots+j_l \lt m\}\;,\;1\leq l\leq m-1 \\ \\

{\mathcal J}_l^{\prime}= & \{{\mathbf j}_l:\;j_i\geq1\;,\;1\leq i\leq l\;,\;j_1+\cdots+j_{l-1} \lt m \leq j_1+\cdots+j_l\}\;,\;1\leq l \leq m \\ \\s_i=&\text{day on which the }i\text{-th quake day occurs}\;,\;i\geq1\;\;(s_0=0) \\ \\

{\mathbf s}_l= & (s_0,s_1,\dots,s_l)\;,\;1\leq l\leq m\\ \\

{\mathcal S}_l= & \{{\mathbf s}_l:\;s_0 \lt s_1 \lt \cdots \lt s_l = T\}\;,\;1\leq l \leq m \\ \\

{\mathcal S}_l^{\prime}= & \{{\mathbf s}_l:\;s_0 \lt s_1 \lt \cdots \lt s_l\leq T\}\;,\;1\leq l \leq m \\ \\

{\mathcal S}_l^{\prime\prime}= & \{{\mathbf s}_l:\;s_0 \lt s_1 \lt \cdots \lt s_l \lt T \lt s_{l+1}\},\; 1 \leq l \leq m

\end{array}\qquad \qquad \end{equation*}For each definition, replacing a lower-case letter with a capital letter will denote the corresponding random variable or vector.

Also let

\begin{equation}

\begin{array}{rl}

x_i =& \mbox{coverage per active site at the end of quake day}\ s_i, i \geq 0\, (x_0 = \phi) \\ \\

\xi_i =& x_i-x_{i-1}\qquad x_{-1}=0~~\mbox{and }~~i=0,1,\ldots,l \\ \\

p =&1 - (1-q)^{1/T} \\ \\

=& \left(\begin{array}{c}

\mbox{probability that a quake occurs at an active} \\

\mbox{site on a given coverage day}

\end{array} \right) \\ \\

q_t =&1-(1-p)^t \\ \\

=&\left(\begin{array}{c}

\mbox{probability that a quake occurs at an active} \\

\mbox{site during the remaining}\,t\,\mbox{coverage days}

\end{array} \right) .

\end{array}

\end{equation}

\begin{equation}

\begin{array}{rl}

x_i =& \mbox{coverage per active site at the end of quake day}\ s_i, i \geq 0\, (x_0 = \phi) \\ \\

\xi_i =& x_i-x_{i-1}\qquad x_{-1}=0~~\mbox{and }~~i=0,1,\ldots,l \\ \\

p =&1 - (1-q)^{1/T} \\ \\

=& \left(\begin{array}{c}

\mbox{probability that a quake occurs at an active} \\

\mbox{site on a given coverage day}

\end{array} \right) \\ \\

q_t =&1-(1-p)^t \\ \\

=&\left(\begin{array}{c}

\mbox{probability that a quake occurs at an active} \\

\mbox{site during the remaining}\,t\,\mbox{coverage days}

\end{array} \right) .

\end{array}

\end{equation}Strategy S proceeds as follows:

S1. At the beginning of the coverage period, the insurer buys reinsurance coverage x 0 on each of the n sites for the entire coverage period.

S2. Then, for

$1 \leq i \leq l$, if ji quakes occur on the ith quake day, si, the reinsurer pays

$j_ix_{i-1}$ to the insurer. If

$k_i=k_{i-1}-j_i \leq n-m$, the insurer pays θ dollars to the customer and coverage ends.S3. If

$s_i \lt T$, and

$ k_i=k_{i-1}-j_i \gt n-m$, the insurer uses the ith payment from reinsurance,

$j_i x_{i-1}$, to buy additional reinsurance coverage

$\xi_i=x_i-x_{i-1}$ on each of the ki remaining active sites for the remaining coverage interval

$T-s_i$. That is,

(24)\begin{equation}

j_ix_{i-1} = k_i g(q_{T-s_i},\xi_i) q_{T-s_i} \xi_i, \; 1 \leq i \leq l,

\end{equation}with reinsurer’s markup (see (8))

(25)\begin{equation}

g(q_{T-s_i},\xi_i)=\frac{\ln(1-q_{T-s_i}+q_{T-s_i}\rm e^{\gamma\xi_i})}{\gamma q_{T-s_i} \xi_i}, \; 1 \leq i \leq l.

\end{equation}Thus,

(26)\begin{equation}

j_ix_{i-1} = \gamma^{-1} k_i \ln(1-q_{T-s_i}+q_{T-s_i}\rm e^{\gamma\xi_i}), \; 1 \leq i \leq l.

\end{equation}For given

$x_{i-1}$, ki, ji, and si, this equation has a unique solution for ξi. (Uniqueness follows from the fact that the r.h.s of (26) is strictly increasing in ξi. Equation (29) below exhibits this solution in closed form.) The corresponding value for the reinsurance coverage on each active site on day

$s_i+1$ is

(27)\begin{equation}

x_i = x_{i-1} + \xi_i, \; 1 \leq i \leq l.

\end{equation}S4. If ji sites, each with coverage

$x_{i-1}$, have quakes on quake day si,

$1 \leq i \leq l$, then the insurer’s final working capital is

(28)\begin{equation}

\begin{array}{rl}

\kappa_{\mathrm{S}}=& w_{\mathrm{I}}+\pi-nqg(q,x_0)x_0+

\left\{

\begin{array}{ll}

0 & \mbox{if }l=0\qquad\quad(\mbox{no quakes occur}) \\ \\

0 & \mbox{if } k_l \gt n-m\mbox{ and }s_l \lt T. \\ \\

j_l x_{l-1} & \mbox{if } k_l \gt n-m\mbox{ and }s_l=T \\ \\

j_l x_{l-1} - \theta & \mbox{if } k_{l-1} \gt n-m\mbox{ and }k_l\leq n-m. \\ \\

\end{array}

\right.

\end{array}

\end{equation}

The unique solution to (26) is

\begin{equation}\xi_i = \gamma^{-1}\left\{\ln \left[{\rm e}^{\gamma j_ix_{i-1}/k_i}-(1-q_{T-s_i})\right]-\ln q_{T-s_i}\right\} \; , \; 1 \leq i \leq l ,\end{equation}

\begin{equation}\xi_i = \gamma^{-1}\left\{\ln \left[{\rm e}^{\gamma j_ix_{i-1}/k_i}-(1-q_{T-s_i})\right]-\ln q_{T-s_i}\right\} \; , \; 1 \leq i \leq l ,\end{equation}from which it follows that

\begin{equation}\begin{array}{rll}

x_{i}=&x_{i-1}+\gamma^{-1}\left\{\ln \left[{\rm e}^{\gamma j_ix_{i-1}/k_i}-(1-q_{T-s_i})\right]-\ln q_{T-s_i}\right\} ,& 1 \leq i \leq l, \\

&& \\

x_{l}=&x_0 +\gamma^{-1}\sum_{i=1}^l \ln \left[1+\left({\rm e}^{\gamma j_ix_{i-1}/k_i}-1\right)/q_{T-s_i}\right].\!&

\end{array}\end{equation}

\begin{equation}\begin{array}{rll}

x_{i}=&x_{i-1}+\gamma^{-1}\left\{\ln \left[{\rm e}^{\gamma j_ix_{i-1}/k_i}-(1-q_{T-s_i})\right]-\ln q_{T-s_i}\right\} ,& 1 \leq i \leq l, \\

&& \\

x_{l}=&x_0 +\gamma^{-1}\sum_{i=1}^l \ln \left[1+\left({\rm e}^{\gamma j_ix_{i-1}/k_i}-1\right)/q_{T-s_i}\right].\!&

\end{array}\end{equation}The properties of xl play an essential role in subsequent sections. Clearly for every quake history, xl increases with l. Moreover, because

\begin{equation}\begin{array}{rl}\frac{\mathrm dx_l}{\mathrm dx_0}=&\frac{\mathrm dx_{l-1}}{\mathrm dx_0}\left[1+\frac{j_l}{k_l}\times\frac1{1-(1-q_{T-s_l})\mathrm e^{-\gamma j_lx_{l-1}/k_l}}\right]\\& {}\\=&1+\sum_{i=1}^l\left[\frac{\mathrm dx_{i-1}}{\mathrm dx_0}\times\frac{j_i}{k_i}\times\frac1{1-(1-q_{T-s_i})\mathrm e^{-\gamma j_ix_{i-1}/k_i}}\right]\\& {}\\ \gt &0\end{array} \;\;\; l=1,2,\dots,\end{equation}

\begin{equation}\begin{array}{rl}\frac{\mathrm dx_l}{\mathrm dx_0}=&\frac{\mathrm dx_{l-1}}{\mathrm dx_0}\left[1+\frac{j_l}{k_l}\times\frac1{1-(1-q_{T-s_l})\mathrm e^{-\gamma j_lx_{l-1}/k_l}}\right]\\& {}\\=&1+\sum_{i=1}^l\left[\frac{\mathrm dx_{i-1}}{\mathrm dx_0}\times\frac{j_i}{k_i}\times\frac1{1-(1-q_{T-s_i})\mathrm e^{-\gamma j_ix_{i-1}/k_i}}\right]\\& {}\\ \gt &0\end{array} \;\;\; l=1,2,\dots,\end{equation}and

\begin{equation}\begin{array}{rl}

\frac{{\rm d}^2 x_{l}}{{\rm d} x^2_0}=&\frac{{\rm d}^2 x_{l-1}}{{\rm d} x^2_0}\left[1+\frac{j_{l}}{k_{l}}\times \frac{1}{1-(1-q_{T-s_{l}}){\rm e}^{-\gamma j_{l}x_{l-1}/k_{l}}}\right] \\ \\

&+\left(\frac{{\rm d} x_{l-1}}{{\rm d} x_0}\right)^2\times\frac{ \gamma\left(\frac{j_{l}}{k_{l}}\right)^2\times (1-q_{T-s_{l}}){\rm e}^{-\gamma j_ix_{i-1}/k_i}}{\left[{1-(1-q_{T-s_{l}}){\rm e}^{-\gamma j_{l}x_{l-1}/k_{l}}}\right]^2} \\ \\

\geq& 0,

\end{array} \;\;\; l=1,2,\ldots\end{equation}

\begin{equation}\begin{array}{rl}

\frac{{\rm d}^2 x_{l}}{{\rm d} x^2_0}=&\frac{{\rm d}^2 x_{l-1}}{{\rm d} x^2_0}\left[1+\frac{j_{l}}{k_{l}}\times \frac{1}{1-(1-q_{T-s_{l}}){\rm e}^{-\gamma j_{l}x_{l-1}/k_{l}}}\right] \\ \\

&+\left(\frac{{\rm d} x_{l-1}}{{\rm d} x_0}\right)^2\times\frac{ \gamma\left(\frac{j_{l}}{k_{l}}\right)^2\times (1-q_{T-s_{l}}){\rm e}^{-\gamma j_ix_{i-1}/k_i}}{\left[{1-(1-q_{T-s_{l}}){\rm e}^{-\gamma j_{l}x_{l-1}/k_{l}}}\right]^2} \\ \\

\geq& 0,

\end{array} \;\;\; l=1,2,\ldots\end{equation} each xl is convex increasing in x 0. Also, for given x 0 each quake history,  $({\bf j_l},{\bf s_l})\in({\cal J}_l\cup {\cal J}'_l)\times{\cal S}_l$, determines the locus of increments

$({\bf j_l},{\bf s_l})\in({\cal J}_l\cup {\cal J}'_l)\times{\cal S}_l$, determines the locus of increments  $\{\xi_1,\ldots,\xi_{l-1}\}$.

$\{\xi_1,\ldots,\xi_{l-1}\}$.

4.1. Indifference premium

The challenge now is to determine  $\cal H$, the collection of all

$\cal H$, the collection of all  $(\pi,x_{0})$ 2-tuples that make an insurer indifferent between offering and not offering an m-out-of-n policy. That is, determine

$(\pi,x_{0})$ 2-tuples that make an insurer indifferent between offering and not offering an m-out-of-n policy. That is, determine  $(\pi,x_{0})$ that solves the indifference equation (4), which in this case takes the form,

$(\pi,x_{0})$ that solves the indifference equation (4), which in this case takes the form,

\begin{equation}{\rm E} u\left(\kappa_{\rm S}-w_{\rm I}\right) = - {\rm e}^{-\alpha[\pi\theta - n g(q,x_0) q x_0]}\times\omega(x_0) = -1,\end{equation}

\begin{equation}{\rm E} u\left(\kappa_{\rm S}-w_{\rm I}\right) = - {\rm e}^{-\alpha[\pi\theta - n g(q,x_0) q x_0]}\times\omega(x_0) = -1,\end{equation}or, equivalently,

\begin{equation}

\pi \theta = n g(q,x_0) q x_0 + \alpha^{-1} \ln \omega(x_0),

\end{equation}

\begin{equation}

\pi \theta = n g(q,x_0) q x_0 + \alpha^{-1} \ln \omega(x_0),

\end{equation}subject to

\begin{equation}

0 \leq \theta^{-1}n g(q,x_0) q x_0\leq\pi\leq 1,\; \; \mbox{and } x_0 \geq 0,

\end{equation}

\begin{equation}

0 \leq \theta^{-1}n g(q,x_0) q x_0\leq\pi\leq 1,\; \; \mbox{and } x_0 \geq 0,

\end{equation} where  $\omega(x_0) := $ expected disutility of the insurer’s self-insured share of the difference between final and initial working capital for Strategy S (analogous to the function

$\omega(x_0) := $ expected disutility of the insurer’s self-insured share of the difference between final and initial working capital for Strategy S (analogous to the function  $h(\phi)$ for Strategy A, defined in Eq. (12) in Section 3).

$h(\phi)$ for Strategy A, defined in Eq. (12) in Section 3).

To derive an explicit expression for  $\omega(x_0)$, first note that

$\omega(x_0)$, first note that

\begin{equation}

\kappa_S = w_I + \pi \theta - n g(q,x_0) q x_0 - Y(x_0, (\bf j_l,\bf s_l)),

\end{equation}

\begin{equation}

\kappa_S = w_I + \pi \theta - n g(q,x_0) q x_0 - Y(x_0, (\bf j_l,\bf s_l)),

\end{equation} where  $Y(x_0, (\bf j_l,\bf s_l))$ is the history-dependent component of the final working capital. See the analogous expression (9) for

$Y(x_0, (\bf j_l,\bf s_l))$ is the history-dependent component of the final working capital. See the analogous expression (9) for  $\kappa_{\mathrm{A}}$ for Strategy A in Section 3. Like

$\kappa_{\mathrm{A}}$ for Strategy A in Section 3. Like  $Y(\phi,j)$ for Strategy A,

$Y(\phi,j)$ for Strategy A,  $Y(x_0, (\bf j_l,\bf s_l))$ represents the portion of the insurer’s obligation to the customer that is self-insured under Strategy S and

$Y(x_0, (\bf j_l,\bf s_l))$ represents the portion of the insurer’s obligation to the customer that is self-insured under Strategy S and  $\omega(x_0) = {\rm E}({\rm e}^{\alpha Y(x_0,({\bf J}_l,{\bf S}_l))})$.

$\omega(x_0) = {\rm E}({\rm e}^{\alpha Y(x_0,({\bf J}_l,{\bf S}_l))})$.

Now divide the collection of all histories,  $(\bf j_l,\bf s_l)$,

$(\bf j_l,\bf s_l)$,  $l \geq 1$, into three non-overlapping sets, corresponding to the three different possible expressions (see (28)) for

$l \geq 1$, into three non-overlapping sets, corresponding to the three different possible expressions (see (28)) for  $Y(x_0, (\bf j_l,\bf s_l))$.

$Y(x_0, (\bf j_l,\bf s_l))$.

• for

$1 \leq l \lt m$,

${\cal J}_l \times {\cal S}''_l$ is the set of histories

$(\bf j_l,\bf s_l)$ with fewer than m quakes in the coverage period, the last one occurring on quake day

$s_l \lt T$, in which case

$Y(x_0,(\bf j_l,\bf s_l)) = 0$;• for

$1 \leq l \lt m$,

${\cal J}_l \times {\cal S}'_l$ is the set of histories

$(\bf j_l,\bf s_l)$ with fewer than m quakes in the coverage period, the last one occurring on quake day

$s_l =T$, in which case

$Y(x_0,({\bf j}_l,{\bf s}_l)) =- j_l x_{l-1}$;• for

$1 \leq l \leq m$,

${\cal J}'_l \times {\cal S}_l$ is the set of histories

$(\bf j_l,\bf s_l)$ with m or more quakes in the coverage period, with quake day

$s_l \leq T$ being the last quake day that begins with more than n − m active sites, in which case

$Y(x_0,({\bf j}_l,{\bf s}_l)) = - j_l x_{l-1} + \theta$.

The corresponding probabilities for histories in each of three sets are:

• for

$1 \leq l \lt m$ and

$({\bf j}_l,{\bf s}_l) \in {\cal J}_l \times {\cal S}''_l$,

(37)\begin{equation}{\rm pr} ({\bf J}_l = {\bf j}_l,{\bf S}_l = {\bf s}_l) = \prod_{i=1}^l [ (1-p)^{k_{i-1}(s_i-s_{i-1}-1)} f(j_i;k_{i-1},p) ] (1-p)^{k_l (T-s_l)}\end{equation}• for

$1 \leq l \lt m$ and

$({\bf j}_l,{\bf s}_l) \in {\cal J}_l \times {\cal S}'_l$,

(38)\begin{equation}{\rm pr} ({\bf J}_l = {\bf j}_l,{\bf S}_l = {\bf s}_l) = \prod_{i=1}^{l-1} [ (1-p)^{k_{i-1}(s_i-s_{i-1}-1)}f(j_i;k_{i-1},p)] \times (1-p)^{k_{l-1}(T-s_{l-1}-1)}f(j_l;k_{l-1},p) \end{equation}• for

$1 \leq l \leq m$ and

$({\bf j}_l,{\bf s}_l) \in {\cal J}'_l \times {\cal S}_l$,

(39)\begin{equation}{\rm pr}({\bf J}_l = {\bf j}_l,{\bf S}_l = {\bf s}_l) = \prod_{i=1}^l [ (1-p)^{k_{i-1}(s_i-s_{i-1}-1)} \times f(j_i;k_{i-1},p)]\!.\end{equation}

In all three equations, the quantity in brackets in the product is the conditional joint probability that the ith quake day occurs on day si and that the number of quakes on that day is ji, given that the i − 1st quake day occurs on day  $s_{i-1}$ and ends with

$s_{i-1}$ and ends with  $k_{i-1}$ active sites. In (37) the final expression after the product gives the conditional probability that sl is the last quake day, given the history up to and including quake day sl, since sl is the last quake day if and only if there are no quakes between sl and the end of the coverage period. In (38), the final expression after the product gives the conditional probability that

$k_{i-1}$ active sites. In (37) the final expression after the product gives the conditional probability that sl is the last quake day, given the history up to and including quake day sl, since sl is the last quake day if and only if there are no quakes between sl and the end of the coverage period. In (38), the final expression after the product gives the conditional probability that  $s_l = T$ and that jl quakes occur on that day, given the history up to and including quake day

$s_l = T$ and that jl quakes occur on that day, given the history up to and including quake day  $s_{l-1}$. In both (37) and (38) fewer than m sites have quakes in the coverage period by the definition of

$s_{l-1}$. In both (37) and (38) fewer than m sites have quakes in the coverage period by the definition of  ${\cal J}_l$ and the fact that sl is the last quake day, by the definitions of

${\cal J}_l$ and the fact that sl is the last quake day, by the definitions of  ${\cal S}''_l$ and

${\cal S}''_l$ and  ${\cal S}'_l$. It follows that sl is also the last quake day in the coverage period that begins with more than n − m active sites. In (39) the definition of the set of histories

${\cal S}'_l$. It follows that sl is also the last quake day in the coverage period that begins with more than n − m active sites. In (39) the definition of the set of histories  ${\cal J}'_l\times{\cal S}_l$ itself implies that the number of active sites at the end of quake day sl is less than or equal to n − m and that it is the last quake day in the coverage period that begins with more than n − m active sites. In this case, since m or more sites have had quakes by the end of quake day sl, what happens after that day does not change the final working capital and therefore no additional probability expression is needed. Note that in all three cases, the integer l equals the number of quake days in the coverage period that begin with more than n − m active sites.

${\cal J}'_l\times{\cal S}_l$ itself implies that the number of active sites at the end of quake day sl is less than or equal to n − m and that it is the last quake day in the coverage period that begins with more than n − m active sites. In this case, since m or more sites have had quakes by the end of quake day sl, what happens after that day does not change the final working capital and therefore no additional probability expression is needed. Note that in all three cases, the integer l equals the number of quake days in the coverage period that begin with more than n − m active sites.

It follows from (28) that

\begin{equation}\begin{array}{rl}

\omega(x_0):=& (1-q)^n + \sum_{l=1}^{m-1}

\sum_{({\bf j}_l,{\bf s}_l) \in {\cal J}_l \times {\cal S}''_l}

{\rm pr}({\bf J}_l={\bf j}_l,{\bf S}_l={\bf s}_l)\\ \\

&~~~ + \sum_{l=1}^{m-1}

\sum_{({\bf j}_l,{\bf s}_l) \in {\cal J}_l \times {\cal S}'_l}

{\rm e}^{-\alpha j_lx_{l-1}}

{\rm pr}({\bf J}_l={\bf j}_l,{\bf S}_l={\bf s}_l)\\ \\

&~~~ + {\rm e}^{\alpha\theta} \sum_{l=1}^{m} \sum_{({\bf j}_l,{\bf s}_l) \in {\cal J}'_l \times {\cal S}_l}

{\rm e}^{-\alpha j_l x_{l-1}}

{\rm pr}({\bf J}_l = {\bf j}_l,{\bf S}_l = {\bf s}_l),

\end{array}\end{equation}

\begin{equation}\begin{array}{rl}

\omega(x_0):=& (1-q)^n + \sum_{l=1}^{m-1}

\sum_{({\bf j}_l,{\bf s}_l) \in {\cal J}_l \times {\cal S}''_l}

{\rm pr}({\bf J}_l={\bf j}_l,{\bf S}_l={\bf s}_l)\\ \\

&~~~ + \sum_{l=1}^{m-1}

\sum_{({\bf j}_l,{\bf s}_l) \in {\cal J}_l \times {\cal S}'_l}

{\rm e}^{-\alpha j_lx_{l-1}}

{\rm pr}({\bf J}_l={\bf j}_l,{\bf S}_l={\bf s}_l)\\ \\

&~~~ + {\rm e}^{\alpha\theta} \sum_{l=1}^{m} \sum_{({\bf j}_l,{\bf s}_l) \in {\cal J}'_l \times {\cal S}_l}

{\rm e}^{-\alpha j_l x_{l-1}}

{\rm pr}({\bf J}_l = {\bf j}_l,{\bf S}_l = {\bf s}_l),

\end{array}\end{equation} where the probabilities,  $ \rm pr({\bf{J_l}} = {\bf{j_l}}, {\bf{S_l}} = {\bf{s_l}})$, for the histories in

$ \rm pr({\bf{J_l}} = {\bf{j_l}}, {\bf{S_l}} = {\bf{s_l}})$, for the histories in  ${\cal J}_l \times {\cal S}''_l$ are given by (37), the probabilities for those in

${\cal J}_l \times {\cal S}''_l$ are given by (37), the probabilities for those in  ${\cal J}_l \times {\cal S}'_l$ by (38), and the probabilities for those in

${\cal J}_l \times {\cal S}'_l$ by (38), and the probabilities for those in  ${\cal J}'_l \times {\cal S}_l$ by (39).

${\cal J}'_l \times {\cal S}_l$ by (39).

Every 2-tuple  $(\pi,x_0)$ in

$(\pi,x_0)$ in  $\cal H$ satisfies (33) and (35), implying

$\cal H$ satisfies (33) and (35), implying

\begin{equation}

\begin{array}{rl}

\pi\theta=&n g(q,x_0) q x_0+\alpha^{-1}\ln\omega(x_0) \\ \\

=& \gamma^{-1} n \ln(1-q+q\rm e^{\gamma x_0}) + \alpha^{-1} \ln \omega(x_0)

\end{array}x_0\in[0,x_{0 {\rm max}}],

\end{equation}

\begin{equation}

\begin{array}{rl}

\pi\theta=&n g(q,x_0) q x_0+\alpha^{-1}\ln\omega(x_0) \\ \\

=& \gamma^{-1} n \ln(1-q+q\rm e^{\gamma x_0}) + \alpha^{-1} \ln \omega(x_0)

\end{array}x_0\in[0,x_{0 {\rm max}}],

\end{equation} where  $x_{0 {\rm max}}$ is defined as the unique value of x 0 such that

$x_{0 {\rm max}}$ is defined as the unique value of x 0 such that  $\ln \omega(x_0 )= 0$. The reinsurers’ initial premium,

$\ln \omega(x_0 )= 0$. The reinsurers’ initial premium,  $\gamma^{-1} n \ln(1-q+q\rm e^{\gamma x_0})$, is convex strictly increasing in x 0, and

$\gamma^{-1} n \ln(1-q+q\rm e^{\gamma x_0})$, is convex strictly increasing in x 0, and  $\ln \omega(x_0)$ is convex in x 0, so that πθ is convex in x 0, with derivative

$\ln \omega(x_0)$ is convex in x 0, so that πθ is convex in x 0, with derivative

\begin{equation}\frac{{\rm d} \pi}{{\rm d} x_0}=\frac{nq}{q+(1-q){\rm e}^{-\gamma x_0}}+\frac{1}{\alpha \omega(x_0)}\frac{{\rm d} \omega(x_0)}{{\rm d} x_0}.\end{equation}

\begin{equation}\frac{{\rm d} \pi}{{\rm d} x_0}=\frac{nq}{q+(1-q){\rm e}^{-\gamma x_0}}+\frac{1}{\alpha \omega(x_0)}\frac{{\rm d} \omega(x_0)}{{\rm d} x_0}.\end{equation}Unlike Strategy A, Strategy S uses payments from reinsurers to insurer to increase the amount of coverage for the original m-out-of-n policy. But like Strategy A, it has two options of special interest:

\begin{equation}

\begin{array}{rl}

\mbox{S}_{\rm i} :& \mbox{choose}\,x_0\in[0,x_{0{\rm max}}]\,\mbox{to minimize}\,\pi\,\mbox{in (41)} \\ \\

\mbox{S}_{\rm ii}:& \mbox{choose}\,x_0=x_{0{\rm max}}\,\mbox{to maximize coverage per active site}.

\end{array}

\end{equation}

\begin{equation}

\begin{array}{rl}

\mbox{S}_{\rm i} :& \mbox{choose}\,x_0\in[0,x_{0{\rm max}}]\,\mbox{to minimize}\,\pi\,\mbox{in (41)} \\ \\

\mbox{S}_{\rm ii}:& \mbox{choose}\,x_0=x_{0{\rm max}}\,\mbox{to maximize coverage per active site}.

\end{array}

\end{equation} (Note that the option of choosing  $x_0 = 0$ (no reinsurance) coincides with option A

$x_0 = 0$ (no reinsurance) coincides with option A $_{\rm iii} $, which we already considered in Section 3.)

$_{\rm iii} $, which we already considered in Section 3.)

Consider option S $_{\rm ii}$, for which

$_{\rm ii}$, for which  $\alpha^{-1}\ln\omega(x_0) = 0$. It follows from the indifference equation (41) that the indifference 2-tuple

$\alpha^{-1}\ln\omega(x_0) = 0$. It follows from the indifference equation (41) that the indifference 2-tuple  $(\pi,x_0)$ satisfies the equation

$(\pi,x_0)$ satisfies the equation

\begin{equation*}

\pi \theta = n g(q,x_0) q x_0.

\end{equation*}

\begin{equation*}

\pi \theta = n g(q,x_0) q x_0.

\end{equation*} Now suppose l quake days occur during the coverage period. For an  $l-1~( \lt m)$ day quake history

$l-1~( \lt m)$ day quake history  $(\bf j_{l-1},\bf s_{l-1})$ followed by jl quakes on the lth quake day, it follows from (28) that final working capital is

$(\bf j_{l-1},\bf s_{l-1})$ followed by jl quakes on the lth quake day, it follows from (28) that final working capital is

\begin{equation*}

\kappa_{\mathrm{S}}=w_{\mathrm{I}}+

\left\{

\begin{array}{ll}

0& \mbox{if } k_{l} \gt n-m\mbox{ and }s_l \lt T\\ \\

j_lx_{l-1}& \mbox{if } k_{l} \gt n-m\mbox{ and }s_l=T \\ \\

j_lx_{l-1}-\theta& \mbox{if } k_{l}+j_l \gt n-m\mbox{ and }k_l\leq n-m,

\end{array}

\right.

\end{equation*}

\begin{equation*}

\kappa_{\mathrm{S}}=w_{\mathrm{I}}+

\left\{

\begin{array}{ll}

0& \mbox{if } k_{l} \gt n-m\mbox{ and }s_l \lt T\\ \\

j_lx_{l-1}& \mbox{if } k_{l} \gt n-m\mbox{ and }s_l=T \\ \\

j_lx_{l-1}-\theta& \mbox{if } k_{l}+j_l \gt n-m\mbox{ and }k_l\leq n-m,

\end{array}

\right.

\end{equation*} where (30) defines  $x_{l-1}$. Interestingly, the insurer incurs a profit (that is,

$x_{l-1}$. Interestingly, the insurer incurs a profit (that is,  $\kappa_{\mathrm{S}} - w_{\mathrm{I}} \gt 0$) if at least one quake occurs on the last coverage day T but fewer than m quakes occur during the coverage period.

$\kappa_{\mathrm{S}} - w_{\mathrm{I}} \gt 0$) if at least one quake occurs on the last coverage day T but fewer than m quakes occur during the coverage period.

4.2. Loss and loss probability

Recall that  ${\cal J}'_l\times{\cal S}_l$ denotes the collection of quake histories with

${\cal J}'_l\times{\cal S}_l$ denotes the collection of quake histories with  $l~(\leq m)$ quake days for which reinsurers pay the insurer

$l~(\leq m)$ quake days for which reinsurers pay the insurer  $j_lx_{l-1}$ dollars on the last quake day sl and the insurer pays the customer θ dollars. For all

$j_lx_{l-1}$ dollars on the last quake day sl and the insurer pays the customer θ dollars. For all  $x_0 \in [0,x_{0 \max}]$, define

$x_0 \in [0,x_{0 \max}]$, define

\begin{equation}\eta(x_0,{\bf j}_l,{\bf s}_l):= \alpha^{-1} \ln \omega(x_0) - Y(x_0, ({\bf j}_l,{\bf s}_l)) = \alpha^{-1} \ln \omega(x_0) +

j_l x_{l-1} - \theta \; , \;

({\bf j}_l,{\bf s}_l) \in {\cal J}'_l \times {\cal S}_l \; .\end{equation}

\begin{equation}\eta(x_0,{\bf j}_l,{\bf s}_l):= \alpha^{-1} \ln \omega(x_0) - Y(x_0, ({\bf j}_l,{\bf s}_l)) = \alpha^{-1} \ln \omega(x_0) +

j_l x_{l-1} - \theta \; , \;

({\bf j}_l,{\bf s}_l) \in {\cal J}'_l \times {\cal S}_l \; .\end{equation} In words,  $\eta(x_0,\bf j_l,\bf s_l)$ is the difference between the insurer’s certainty equivalent of the amount he self-insures and the actual amount of self-insurance for a quake history

$\eta(x_0,\bf j_l,\bf s_l)$ is the difference between the insurer’s certainty equivalent of the amount he self-insures and the actual amount of self-insurance for a quake history  $({\bf j_l},{\bf s_l})\in{\cal J}'_l\times{\cal S}_l$ (cf. the function

$({\bf j_l},{\bf s_l})\in{\cal J}'_l\times{\cal S}_l$ (cf. the function  $\psi(\phi,j)$ for Strategy A, defined in Eq. (19) in Section 3). For the special case where

$\psi(\phi,j)$ for Strategy A, defined in Eq. (19) in Section 3). For the special case where  $(\pi,x_0) \in \cal H$ (that is, where π is the indifference premium corresponding to x 0) it follows from the indifference equation (41) that

$(\pi,x_0) \in \cal H$ (that is, where π is the indifference premium corresponding to x 0) it follows from the indifference equation (41) that

\begin{equation}\eta(x_0,{\bf j}_l,{\bf s}_l) = \pi \theta - \gamma^{-1} n \ln (1-q+q {\rm e}^{\gamma x_0}) + j_l x_{l-1} - \theta \; , \;

({\bf j}_{l},{\bf s}_{l}) \in {\cal J}'_l \times {\cal S}_l,\end{equation}

\begin{equation}\eta(x_0,{\bf j}_l,{\bf s}_l) = \pi \theta - \gamma^{-1} n \ln (1-q+q {\rm e}^{\gamma x_0}) + j_l x_{l-1} - \theta \; , \;

({\bf j}_{l},{\bf s}_{l}) \in {\cal J}'_l \times {\cal S}_l,\end{equation} so that in this case  $\eta(x_0,{\bf j}_l,{\bf s}_l)$ can also be interpreted as the net change in working capital for the quake history

$\eta(x_0,{\bf j}_l,{\bf s}_l)$ can also be interpreted as the net change in working capital for the quake history  $(\bf j_{l},\bf s_{l})$. A loss occurs if and only if

$(\bf j_{l},\bf s_{l})$. A loss occurs if and only if  $\eta(x_0,{\bf j}_l,{\bf s}_l) \lt 0$, in which case the amount of the loss equals

$\eta(x_0,{\bf j}_l,{\bf s}_l) \lt 0$, in which case the amount of the loss equals  $ - \eta(x_0, j_l, s_l) \gt 0$.

$ - \eta(x_0, j_l, s_l) \gt 0$.

Define  ${\cal Q}_l:={\cal J}'_l \times {\cal S}_l$ for

${\cal Q}_l:={\cal J}'_l \times {\cal S}_l$ for  $l \in \{1,\ldots,m\}$. The probability of loss is

$l \in \{1,\ldots,m\}$. The probability of loss is

\begin{equation}\mu_{\rm S}(x_0) := \sum_{l=1}^{m }\sum_{({\bf j}_{l},{\bf s}_{l}) \in {\cal Q}_l} I_{ \eta(x_0,{\bf j}_l,{\bf s}_l) \lt 0} \; {\rm pr}({\bf J}_l={\bf j}_l,{\bf S}_l={\bf s}_l),\end{equation}

\begin{equation}\mu_{\rm S}(x_0) := \sum_{l=1}^{m }\sum_{({\bf j}_{l},{\bf s}_{l}) \in {\cal Q}_l} I_{ \eta(x_0,{\bf j}_l,{\bf s}_l) \lt 0} \; {\rm pr}({\bf J}_l={\bf j}_l,{\bf S}_l={\bf s}_l),\end{equation} where  ${\rm pr} ({\bf J}_l = {\bf j}_l, {\bf S}_l = {\bf s}_l)$ is given by (39). Obvious properties are:

${\rm pr} ({\bf J}_l = {\bf j}_l, {\bf S}_l = {\bf s}_l)$ is given by (39). Obvious properties are:

• If

$m x_0\geq\theta$, then

$\mu_{{\rm S}}(x_0) \lt {\rm pr} (\# \mbox{ quakes} \geq m)$.• If there exists a quake history

$({\bf j}_l,{\bf s}_l)\in{\cal J}_l\times{\cal S}_l$ for

$l\in\{1,\ldots,m\}$ such that

$j_lx_{l-1}\geq\theta$, then

$\mu_{{\rm S}}(x_0) \lt {\rm pr}(\# \mbox{ quakes} \geq m)$.• Of special interest is a quake on each of m days, which has

\begin{equation*}\begin{array}{rl}

{\rm pr} \lbrack {\bf J}_m=(\underbrace{1,\dots,1}_m) \rbrack

=& \frac{n!}{(n-m)!} \left( \frac{p}{1-p} \right)^m \times \sum_{1 \leq s_1 \lt \cdots \lt s_m \leq T}

(1-p)^{s_1 + \cdots + s_{m-1} + (n-m+1)s_m}.

\end{array}\end{equation*}

We first focus on loss.

Proposition 4.1. Let

\begin{equation*}

\begin{array}{rl}

Q=& {\cal {Q_1}}\cup\cdots\cup Q_m \\ \\

=&

\left(

\begin{array}{c}

\mbox{collection of all quake histories that end} \\

\mbox{with a payment of}\,\theta\,\mbox{dollars to the customer}

\end{array}\right).

\end{array}

\end{equation*}

\begin{equation*}