Introduction

What does it mean to assess a new government on its early tax policies? A fair assessment will want to take into consideration the ambitions of the new government, the constraints it faces, and the options and opportunities it enjoys. From a specifically social policy point of view, any assessment will want to consider how tax policies contribute to meeting social need, to tackling poverty or reducing inequality, and how fully tax is being used as an instrument to achieve such social policy goals in and of itself, or as part of other policy tools at the government’s disposal.

This article examines the tax policies adopted in the UK Labour government’s first year in office in the context of a challenging fiscal and economic backdrop. We develop a critique of these policies and attempt to explain the government’s approach. The analysis draws on Budget documents, other policy materials, and expert commentary.

The Labour Party came into office in July 2024 with an overarching promise – to bring change to the country (Labour Manifesto, 2024). It promised to initiate a decade of renewal and to rebuild the country so that it serves the interest of working people. This would be achieved in four main ways. First, economic growth would be a driving impetus, underpinned by a partnership with business, with an emphasis on long-term investment in economic and social infrastructure such as prisons, transport, and hospitals. Economic growth would offer more and better jobs and provide the revenues for public spending on the social wage. Second, a transition to green energy would be put into effect through public and crowded-in private investment, constituting an important pillar of economic growth, strengthening future ecological sustainability, and improving lives through green jobs, cleaner air, better insulated homes, and lower energy bills. Third, quality of life would be improved through better public services, with thousands more teachers, millions of extra appointments in the National Health Service (NHS), and free breakfast clubs in primary schools. Finally, people would feel more secure through action on crime reduction and anti-social behaviour at a community level and stronger control over borders, and action on defence and counter terrorism at national and international levels. These goals gave Labour the challenge of securing tax revenues for public spending without damaging growth and, where possible, using tax policy to promote growth and support the expansion of green energy (Labour Manifesto, 2024).

With regard to social policy concerns of social need, inequality, and poverty, the Labour Party said little prior to the election. Inequality was barely mentioned in the Manifesto, and poverty was to be tackled primary through work: for example, making work pay, helping people into jobs and reforming employment support, and through a variety of social measures such as free breakfast clubs, protecting renters from arbitrary eviction, and reducing fuel poverty. This suggested fiscal policy might be used to reduce the tax liabilities of those on low pay and raise revenues to fund breakfast clubs or reduce fuel costs.

A consideration of the economic and fiscal backdrop to Labour’s election in 2024 demonstrates the challenges faced by the new government in devising a fiscal policy to fulfil its policy ambitions. After establishing this context, Labour’s tax stance on the eve of the 2024 General Election is described followed by the main tax measures taken in Labour’s first year. The article then turns to a critique of Labour’s tax policies and finishes by proposing some tentative explanations for the approach it has adopted.

Challenging fiscal and economic context

The UK economy has suffered four major shocks over the past fifteen to twenty years: the global financial crash, the decision to leave the European Union, the coronavirus pandemic, and the economic consequences of the Russian invasion of Ukraine. During this time the country has experienced a prolonged period of low economic growth – just 6 per cent per capita growth over a fifteen-year period (Emmerson et al., Reference Emmerson, Johnson, Ridpath, Seldon and Egerton2024). The economy has suffered disruptions in trade and supply chains (including labour supply) and low levels of business investment, largely arising from uncertainty. The long-term effect of Brexit has been estimated to be a loss of around 5 per cent of GDP (Springford, Reference Springford2022).

The UK has also seen the slowest period of wage growth in 200 years, with wages in 2023 having around the same value as they did in 2013 (Emmerson et al., Reference Emmerson, Johnson, Ridpath, Seldon and Egerton2024). A prolonged period of austerity, undertaken to reduce the deficit, which took nine years instead of the anticipated five, resulted in reduced-quality public services, which were then further weakened by the pandemic.

The combined effects of these fiscal and economic pressures required significant additional levels of government spending and with it, additional government borrowing. This, plus the economic contraction, especially in 2020–21, has resulted in increased public debt-to-GDP ratio which was 25 per cent in 2001 and is now 95 per cent (OBR, 2025a). Servicing the debt interest costs over £100bn p.a., some 3.5 to 4 per cent of GDP (OBR, 2025b). Labour also inherited a number of constraining tax policies from its Conservative predecessors, including the freezing of the personal allowance and rate thresholds in income tax and national insurance (NI), the abolition of a new health and social care levy designed to channel more resources into health and social care, and the (unfunded) reduction by 4 percentage points of employee national insurance contributions (NICs). Moreover, the experience of the Truss government showed what instability can follow when a government loses its fiscal credibility.

So, the Labour government came into office with a poorly functioning economy, a relatively high deficit (5.7 per cent rather than the 2 per cent pre-Covid), high public debt interest costs, and a high tax-to-GDP ratio in historical context (although not in a comparative context). At the same time, the public were eager to see their standards of living rise, requiring attention to the economy, wages, and the quality of public services. All of this was taking place in the midst of a worsening climate crisis and in the context of political turbulence with the rise of populist right and challenges to the survival of the two-party electoral system.

Labour’s stance on tax at the time of the 2024 general election

Some of the tax policies Labour promoted in the run-up to the General Election had a populist feel to them: for example, they promised a crackdown on tax avoidance; they announced they would impose VAT on private school fees; they promised a harsher tax regime for ‘non-doms’ (the non-domiciled, who reside in the UK but maintain that their permanent residence is outside the UK so pay less tax on their worldwide incomes and assets); they would close ‘loopholes’ including those around the inappropriate use of capital gains tax (CGT) instead of income tax for performance-related pay and end the use of offshore trusts to avoid inheritance tax; and they promised more revenues from a windfall tax on gas and oil companies (Labour Manifesto, 2024). Importantly, and some argued perhaps unnecessarily (e.g. Tetlow, Reference Tetlow2024; IfG & IFS, 2025), Labour also promised that they would not raise taxes on working people – specifically ruling out raises in income tax, national insurance, and value-added tax (VAT). They also pledged to build His Majesty’s Revenue and Customs (HMRC)’s capability. The Manifesto framed much of this as addressing unfairness in the tax system.

Generally, though, Labour was reluctant to be drawn into detailed discussion about their plans for specific taxes. The Manifesto said they would safeguard taxpayers’ money, spend responsibly, address unfairness in the tax system, and keep taxes as low as possible.

What was fully emphasised was Labour’s intention to base decisions on ‘sound money’ principles and on economic stability, especially through adherence to strong fiscal rules. This was framed such that policy developments should be moving towards fiscal balance, and net financial debt should be falling by the end of the parliament.

Tax policies in Labour’s first year

In this section we consider a selection of both explicit new policies and implicit policies where significant pre-existing tax arrangements were retained.

‘Repairing public finances’

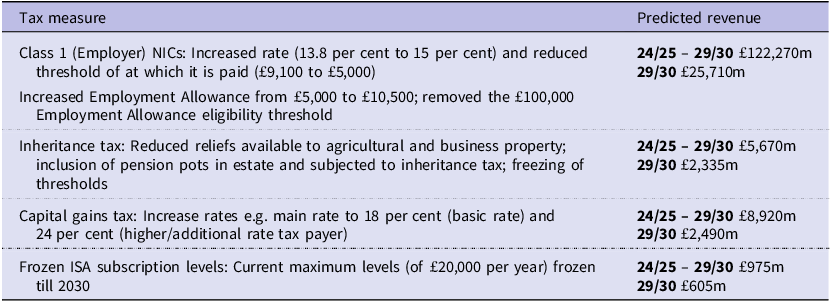

The first set of policies we will consider was badged in the Budget Policy document as ‘repairing public finances’ through ‘raising revenue fairly’ (HMT, 2024). These changes are outlined in Table 1.

Selected Autumn 2024 Budget policies to ‘repairing public finances’ plus associated revenue predicted in the Budget for 2024/25-2029/30 inclusive and for 2029/30 alone

Table 1 Long description

The table presents selected Autumn 2024 Budget policies aimed at repairing public finances through raising revenue fairly. It includes four main tax measures: Class 1 Employer National Insurance Contributions with increased rates and reduced thresholds, increased Employment Allowance with removed eligibility threshold, changes to Inheritance Tax including reduced reliefs and inclusion of pension pots, and increased Capital Gains Tax rates. Additionally, it mentions frozen ISA subscription levels. The table has two columns: Tax measure and Predicted revenue, with the latter further divided into revenue for the periods 2024/25 to 2029/30 and 2029/30 alone. The predicted revenue values are listed in millions of pounds for each policy and period.

‘Delivering on our promises’

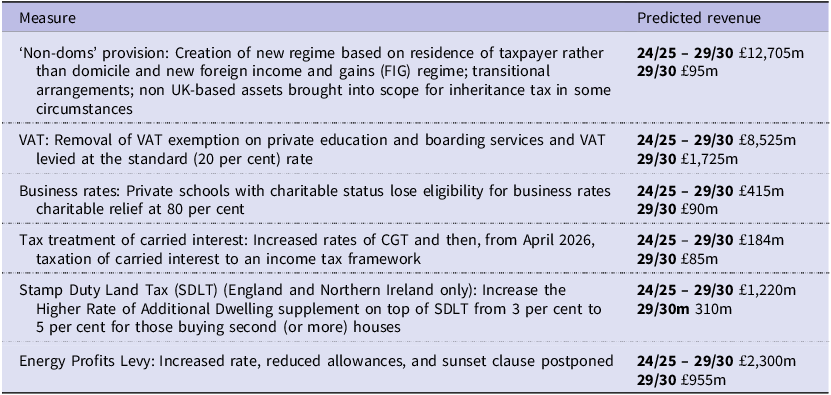

Second, some tax changes were trailed well before the July 2024 general election and were presented in the Budget as ‘delivering on our promises’. These are summarised in Table 2, along with the revenue predicted by the Treasury to be raised.

Selected Autumn 2024 Budget policies to ‘deliver promises’ and associated revenue predicted in the Budget for 2024/25-2029/30 inclusive and for 2029/30 alone

Table 2 Long description

A table detailing selected Autumn 2024 Budget policies and their associated predicted revenue. The table has two main columns: Measure and Predicted revenue. The Measure column lists various tax and policy changes, such as the creation of a new regime for non-doms, removal of VAT exemption on private education, changes in business rates for private schools, increased rates of capital gains tax, changes in stamp duty land tax, and adjustments to the energy profits levy. The Predicted revenue column provides the expected revenue for each measure for the periods 2024/25-2029/30 and 2029/30 alone. The table includes specific financial figures for each policy change, indicating the expected financial impact over the specified periods.

‘Closing the tax gap’

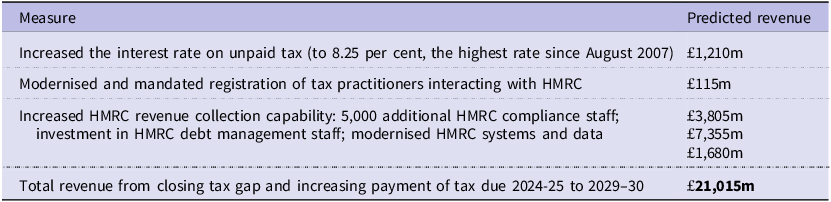

A third set of tax policies related to the enforcement of tax rules and to enhance compliance and payment, thereby reducing the tax gap: that is, the difference between the amount of tax that should in theory be paid to HMRC and the amount that is actually paid. Selected policies are shown in Table 3.

Selected Autumn 2024 Budget measures to close the tax gap and increase payment of taxes due and associated expected revenues

Table 3 Long description

The table presents various tax measures implemented in the UK Autumn 2024 Budget aimed at closing the tax gap and increasing the payment of taxes due. It includes four measures: increasing the interest rate on unpaid tax, modernizing and mandating registration of tax practitioners, enhancing HMRC revenue collection capability, and additional investments in HMRC systems and staff. The table has two columns: Measure and Predicted revenue, with four rows detailing each measure and its associated predicted revenue in millions of pounds. The total revenue from these measures is expected to be 21,015 million pounds.

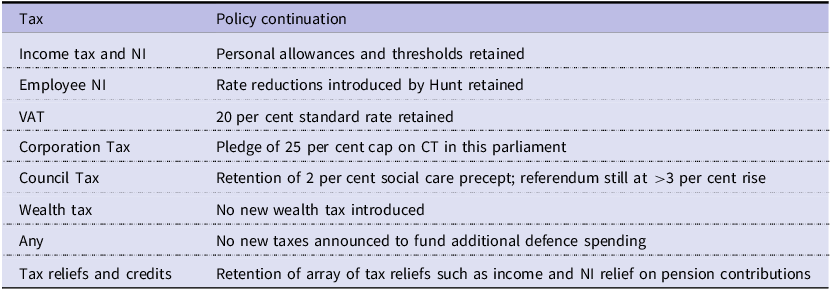

Finally, some significant tax policies adopted by the Labour government comprised not new tax measures per se, but the purposeful retention of certain tax policies from previous governments. Table 4 shows some of the most noteworthy ones.

Selected Autumn 2024 Budget policies based on the continuation of the policies of prior governments

Table 4 Long description

The table presents a summary of key tax policies that the Labour government has chosen to retain from previous administrations. It includes seven rows and two columns. The first column lists different types of taxes such as income tax, employee national insurance, value-added tax, corporation tax, council tax, wealth tax, and tax reliefs and credits. The second column describes the specific policies retained for each tax type. For instance, personal allowances and thresholds are retained for income tax and national insurance, rate reductions introduced by Hunt are retained for employee national insurance, and a twenty percent standard rate is retained for value-added tax. The table also notes the pledge of a twenty-five percent cap on corporation tax, the retention of a two percent social care precept for council tax, and the retention of various tax reliefs such as income and national insurance relief on pension contributions.

Making sense of Labour’s tax policies

We now turn to a discussion of the implications of Labour’s first year tax policies and consider how best to interpret them.

Raising revenue to fund policy ambitions

One of the main objectives of the Budget was to raise revenues to address spending requirements. Labour’s first Budget can be seen as a ‘tax and spend’ Budget entailing an annual average of almost £70bn of additional spending and £36bn additional tax revenues (OBR, 2024). Total departmental spending was set to rise by 2.3 per cent annually on average over the lifetime of the parliament but with significantly bigger rises in spending by March 2026 (3.4 per cent) and lower spending rises after that (1.5 per cent) (Boileau, Reference Boileau2025). As a result of the Budget, government spending was set at around 4.9 percentage points higher than pre-pandemic levels (OBR, 2024).

However, despite some significant rises in the 2025–26 financial year, spending increases across the parliament looked unlikely to address pre-existing funding shortfalls and improve services, let alone address the many problems driven by climate crises, growing poverty, and inequality that had received little recognition by the previous government. For example, despite receiving a comparatively generous settlement, the NHS was awarded well below the 4 per cent believed necessary (Charlesworth et al., Reference Charlesworth, Anderson, Donaldson, Johnson, Knapp, McGuire, McKee, Mossialos, Smith, Street and Woods2021), and there was little respite for local authorities facing bankruptcy. The judgement of Paul Johnson, (then) director of the Institute for Fiscal Studies, was that the very tight spending provisions for the later years of the parliament meant there was a good chance of further tax rises in later Budgets, particularly if the additional spending, including additional capital spending, did not have sufficient impact on economic growth (Johnson, Reference Johnson2024).

Tackling privilege, reducing inequality, and the use of tax as an instrument of social policy

In making sense of Labour’s tax policies, it is worth exploring the possibility that Labour were attempting to tackle privilege and reduce inequality. Some tax measures were trailed well in advance of the General Election and could be seen as signalling a populist, anti-privilege stance. These included the increased taxation of private schools and new policies tightening up the tax treatment of non-doms. In both cases, relatively small groups of taxpayers were affected: there were an estimated 83,000 non-dom taxpayers in the tax year ending 2023 (HMRC, 2024a) and just 6 per cent of school pupils were in private schools (HMRC, 2024b). Additionally, the crackdown on tax avoidance was well publicised and could be seen as populist. It was the second largest revenue raiser in the Budget (£21bn over the parliament and rising), increased tax efficiency and effectiveness and would appeal to those who perceive themselves to be making a fair contribution while others avoid doing so.

A higher rate for the Energy Price Levy, one of the windfall taxes on oil and gas companies and which raises around £2.5–3bn a year, could also be seen as a populist measure that targeted beneficiaries of high energy prices, although this received much less attention in the media. The capping of relief for business and agricultural property might be seen as an anti-privilege stance although the exclusion of inheritance tax reform from the Party Manifesto suggests a desire to contain discussion of it before the election (perhaps wisely, from a Labour Party point of view, given the sustained political furore following its announcement in the 2024 autumn Budget and the persistent unpopularity of the tax). The decision to transfer carried interest, a form of performance-related pay for those managing investment/savings funds, from CGT to an income tax framework, also stands to increase taxes on those with higher incomes, in this case on those working in the finance sector.

However, looking at the tax measures overall, we cannot see the Budget as targeting the rich and better off more generally. The Chancellor of the Exchequer, Rachel Reeves, did not equalise CGT rates with income tax rates (albeit moving them in that direction), nor restructure council tax to ensure the ratio of property value to tax levied created a progressive tax, nor reintroduce NICs on investment income, or remove the upper earnings threshold, thereby levying the same NI rate on all income above the lower earnings threshold, nor any number of other tax policies that could have directly targeted financial inequalities present in the UK. And Reeves did not introduce a new specific wealth tax or more significant changes to taxes affecting wealth, although this has been advocated by many (e.g. Rowlingson, Reference Rowlingson, Lymer, May and Sinfield2023).

The limited consideration of the stubbornly persistent high levels of inequality and their costs in the thinking of the Chancellor and HM Treasury continue the low priority given to this in the Manifesto. Inequality is scarcely mentioned in the Budget, and measures in the Budget were not framed around the principle of reducing inequality. This suggests that either the reduction of inequalities is not a major Labour goal at present or, if it is, it must be tackled stealthily.

Despite some increased taxes on the better off, tax is not being used more widely by Labour as an instrument to redistribute in its own right. Almost all of a vast array of tax reliefs remain in place. Some tax reliefs are policy motivated: for example, to incentivise certain kinds of behaviour (e.g. pension saving is encouraged by giving income tax and NI relief on the portion of salary that is paid into an occupational pension). They are best thought of as tax expenditures in the sense that they reflect decisions about the allocation of resources through our tax arrangements: that is, by not collecting revenues which otherwise would have been raised by the normal operation of the tax system (Sinfield, Reference Sinfield, Lymer, May and Sinfield2023).

The government has stated that there are 344 such non-structural, or policy-motivated, tax reliefs and that 107 of these policy-motivated reliefs have been costed at £207bn in foregone revenue in 2023–24 (HMRC, 2024). This was the equivalent of 25 per cent of the total revenues raised in tax that year so it represents a significant amount of revenue foregone. However, many of these reliefs (e.g. pensions relief and private residence relief) benefit the better off much more than the less well off (Gregory et al., Reference Gregory, Lymer and Rowlingson2021; Sinfield, Reference Sinfield, Lymer, May and Sinfield2023). In other words, many tax reliefs increase inequality. For instance, tax reliefs in income tax and NI allocated to individuals through registered pension schemes cost well over £50bn annually, with higher reliefs allocated to those on higher incomes. Income tax relief alone on private pensions is very regressive: the top tenth of taxpayers receive half, the bottom half a tenth (Sinfield, Reference Sinfield, Lymer, May and Sinfield2023). However, there was limited action on these reliefs in the Autumn 2024 Budget, and there was no systematic analysis of the suitability of the menu of reliefs currently in place.

So, there have been some moves to raise taxes from the better off and these might be the first steps in an incremental programme of reducing inequality through redistribution. However, it is not yet clear that Labour has a coherent strategy in relation to tax at all, and there is certainly no coherent narrative on tax. Instead, it might be more accurate to perceive the government as having adopted a ‘magpie strategy’ – that is, taking revenues wherever they could find them (and within the self-imposed fiscal constraints they have set themselves) – rather than a strategy to tackle income and wealth inequality systematically. For example, the government continued to take taxes from those on very low incomes by retaining the frozen income tax and NI personal allowances; by failing to take action on council tax; and by retaining the increased rate of VAT introduced during the Coalition government-imposed austerity despite ongoing debates about proportionality of VAT and its role in pushing households into poverty (Thomas, Reference Thomas2020). The bitter reference in the February 2025 resignation letter of Anneliese Dodds, the then Minister for Development, to her expectation that the need to increase defence spending would be addressed through a discussion about tax rather than simply taking £6bn from the overseas aid budget also pointed to a lack of coherence in the government’s policy on tax (Dodds, Reference Dodds2025).

All of this together suggests that Labour is not fully realising the opportunities posed by taxes as instruments of social policy to reduce inequality and poverty. For example, there is near universal expert view that council tax should be reformed or replaced to (a) deal with the use of out-of-date property values (around half of all properties are now thought to be in the ‘wrong band’ (Phillips, Reference Phillip2025) and (b) reduce or remove the regressivity that is currently built into the tax design. However, the Labour government, like others before it, steered away, in its first year, from making any changes, which would be politically costly while raising arguably limited additional revenue (Prabhakar, Reference Prabhakar2016; see also Orton’s (Reference Orton2023) more wide-ranging discussion).

Establishing reputation for economic and fiscal credibility

If we cannot (yet) be certain we see an incremental approach to inequality reduction in the Labour government’s tax policies, there is one principle that does appear to be a major driver of Chancellor Reeves’ policies. The Chancellor is keen to ensure the government is perceived to be one of economic and fiscal credibility. This is seen by government as essential to maintaining a sustainable fiscal position, engender confidence among international investors, and avoid market reactions that could push up borrowing costs (Economics Observatory, 2024). Labour is attempting to achieve this through a commitment to economic growth and improved productivity while bringing about a reduction in the UK’s deficit and national debt.

As part of a strategy to achieve a reputation as fiscally trustworthy, UK Chancellors of the Exchequer have, since 1997, created ‘fiscal rules’. It is against these rules that others can then assess government’s fiscal prudence and fiscal discipline. Fiscal rules are restrictions on fiscal policy the government sets itself to constrain its own decisions on spending and taxes. More recently, the Office for Budget Responsibility (OBR), established by Conservative Chancellor Osborne in 2010, has become the arbiter of whether these ‘rules’ are being met (Pope et al., Reference Pope, Hourston and Sangha2024). Chancellor Reeves has stipulated three fiscal rules.

The first rule – the stability rule – is that the current budget should be on course to be in balance or surplus by 2029/30. This means that day-to-day costs are met by revenues by 2029/30 to within 0.5 per cent of the gross domestic product (GDP). At that stage, the government should be borrowing only to invest.

The second rule – the investment rule – is that net financial debt should fall as a share of the economy in 2029/30. This means that public debt should be lower in 2029/30 than 2028/29 as a share of the economy. Although investment rules are not new, the Chancellor has changed the way net financial debt is defined to make it a more comprehensive measure of all state liabilities and the assets available to cover these. Public sector net financial liabilities (PSNFL) include all the debt and assets counted within public sector net debt (PSND) and funded pension obligations (like local government schemes), as well as illiquid financial assets such as equity stakes in private companies and loans (including student loans).

The third rule – the welfare (sic) cap – stipulates that some types of social security spending must remain below a pre-specified level. This puts in place additional constraints on spending on social security payments and includes roughly half of social security spending. This rule is omitted from the Manifesto and often absent in the Chancellor’s speeches. In practice, it limits the extent to which any policy changes can increase social security spending. Payments to pensions and payments ‘most sensitive to the economic cycle’, such as Jobseekers’ Allowance and associated housing benefit, are excluded (Pope et al., Reference Pope, Hourston and Sangha2024).

The gap between the Budget’s annual average increase of £36bn in tax revenues and almost £70bn in spending gave rise to extra average annual borrowing of around £32bn (OBR, 2024). Changing the way public debt is measured made possible tens of billions of pounds of additional borrowing for capital investment.

Despite well-documented criticisms of the fiscal rules (see below), the current Labour Government has consistently reaffirmed its commitment to them. The Charter for Budget Responsibility, approved by Parliament in January 2025, formally entrenches these ‘non-negotiable’ fiscal rules in legislation. Several public spending decisions (e.g. on the two-child benefit cap and proposed cuts to social security payments to disabled people) have also drawn attention to the privileging of these rules.

Labour has also promoted a strong narrative on the centrality of good economic growth and has pursued policies of reducing regulation (e.g. changes to the Competition and Markets Authority and in planning), muting criticism of foreign leaders in pursuit of trade deals, improving the minimum wage and wages in the public sector, boosting public capital investment and back-to-work initiatives. Even if we set aside the question of the desirability of growth per se rather than ‘equitable and inclusive growth’ or ‘sustainable growth’, we should note that tax measures in Labour’s first year were not used to increase growth other than by raising revenue to fund public expenditure. This is expected to have a positive long-term impact on GDP, though leaving GDP largely unchanged at the end of the parliament (OBR, 2024). Public investment multipliers tend to be larger than tax multipliers and thus larger than private investment, suggesting the near status quo ante policy on tax reliefs might have weakened Labour’s impact on economic growth (Espinoza et al., Reference Espinoza, Gamboa-Arbelaez and Sy2020; Tovar Jalles et al., Reference Tovar Jalles, Park and Qureshi2024).

The large increase in employer NICs is also likely to temper growth since it increases the cost of employment. and the OBR has estimated the measure to reduce potential output by 0.1 per cent by 2029/30 (OBR, 2024). This ‘tax on jobs’ primarily affects workers, and the cost of employer NICs is traditionally viewed as ultimately borne by employees (Iraizoz, Reference Iraizoz2024), the argument being that increased employer NICs create pressures on employers to hold wages down, reduce the hours worked, or recruit fewer staff than would otherwise have been the case.

Narrowness in tax making policy

The use of fiscal rules as currently conceived has been subjected to sustained criticisms. Critics argue (e.g. Kumar, Reference Kumar2024; Tetlow et al., Reference Tetlow, Bartrum and Pope2024) they are based on simplistic and arbitrary targets and ignore the broader macroeconomic context. In one sense they are too short-termist, with investment and spending decisions offering long-term paybacks, such as investment on climate adaptation, being stymied by a focus on immediate fiscal metrics. On the other hand, they prevent spending today because of speculative forecasts about what will be happening in four or five years’ time. They have been used repeatedly to justify constrained spending on public services regardless of the wider political-, economic-, and equity-related effects arising from the consequent damage to public services.

Alternatives to the fiscal rules have been proposed, including widening the indicators considered. The New Economics Foundation (NEF), for example, advocates an independent new Fiscal Policy Committee overseeing policy by providing guidelines to the government including optimal ranges for the primary balance, taking into consideration a wider range of factors such as private sector activity, inflation, and resource constraints (van Lerven et al., Reference Van Lerven, Stirling and Prieg2021).

Some have gone beyond criticism of the fiscal rules as part of a longer-term push to challenge the whole process of tax policy making. The Institute for Government, Chartered Institute of Taxation, and Institute for Fiscal Studies produced a report in 2017 entitled Better Budgets: Making Tax Policy Better (Rutter et al., Reference Rutter, Dodwell, Johnson, Crozier, Cullinane, Lilly and McCarthy2017). The report observed that, in contrast to much public expenditure decisions, tax policy making was characterised by secrecy, insufficient challenge, and limited scrutiny. Consultations, which are typically tightly drawn and poorly advertised, should start earlier and cast the net wider, involving evidence from, and the views of, a wider range of people and groups around a wider range of options, the report argued. The report emphasised the importance of much more public engagement, with a government proactively securing it.

As Labour’s first Budget took place a few months after a general election, many of Reeves’ tax policies had received more public attention than usual. However, Labour introduced no change in Budget process itself. The opportunity offered to reframe both the country’s contemporary problems and the approach to addressing them in the context of a fresh start was not grasped. Tetlow, of the Institute for Government, observed that, in the face of a unique combination of policy challenges, an opportunity to implement major radical reform, rather than multiple minor reforms, was missed but would have allowed a more compelling narrative telling a bigger story (IfG and IFS, 2025).

The decisions made on tax to date suggest little appetite from Labour to shift the narrative on taxation – whether, for example, by devolving more taxes to the local level to strengthen the link between tax decisions and the services they fund (as in Sweden), or by challenging the prevailing view of taxation as a ‘burden’ to be minimised rather than a means of collective investment. The focus on economic growth, rather than other measures of societal wellbeing and development, has arguably detracted from giving due consideration to the importance of informal caring, social security, and the activities of public services in enhancing wellbeing and social cohesion and thereby an investment in economic growth; rather these are often seen as costs. As recent analysis has shown, the history of economic thought has long neglected caring activities as contributors to economic growth (Holten, Reference Holten2025).

What is clear is that, embarking on a new start and promising transformative change in the context of an enormous parliamentary majority, a unique opportunity to present a big and bold agenda was lost although ongoing fiscal challenges suggest the crisis may not yet have been wasted.

As Lymer and colleagues point out (Reference Lymer, May and Sinfield2023), tax-policy-making-as-usual leads to ‘outsider’ engagement only with those who are working for a reduction in inequalities and stronger policies on social inclusion such as tax reform campaign groups (e.g. Tax Justice UK, Just Money), charitable organisations such as the Child Poverty Action Group, as well as social policy scholars. Meanwhile, the views of business representatives and tax consultancy firms are seen as indispensable to achieve policies that are effective in raising revenue while avoiding the destabilisation of the economy.

Concluding remarks: What do we learn about Labour from the tax policies of its first year in office?

This paper has sought to assess, from a social policy perspective, the tax policies adopted by the Labour government between July 2024 and June 2025, in the context of its economic and fiscal inheritance.

On a positive note, the increased focus on closing the tax gap, with increased spending on HMRC’s debt management staff and commitment to hiring an additional 5,000 compliance staff, may, by increasing the capability of HMRC, signal an incremental shift in some of the cultural dimensions of our tax arrangements. The NAO report on taxing wealthy individuals (NAO, 2025) might also contribute to a shift in the debate on the need for greater taxation of wealth generally in the UK’s tax system. The popular and elite perception of aggressive tax avoidance and even evasion as inevitable, rational, and in some cases justifiable, with the corresponding lack of outrage and urgency for reform, is part of a cultural dimension of the tax arrangements in our society and as important as the rate of any tax (Byrne and Ruane, Reference Byrne and Ruane2017). Elite tolerance of aggressive avoidance is seen in the routine inclusion as insiders in the tax policy-making process of companies that sell aggressive tax avoidance schemes. Popular tolerance is seen in fraudulent claims for tax reliefs and activities in the ‘hidden economy’ (where around 10 per cent of all economic activities are hidden from the view of HMRC) (HMRC, 2023).

On the negative side, the Chancellor has, as yet, made limited use of taxation to achieve improvements in social policies. Taking first year tax measures overall, it is difficult to avoid the perception that the overwhelming driver of Rachel Reeves’ approach has been the raising of revenue combined with a concern to stamp Labour’s approach as one of fiscal credibility and prudence. We should note something which might seem too obvious to state which is the fact that Reeves chose to raise revenues to fund government spending rather than use tax measures to lower tax receipts to facilitate private spending (or saving). Not only does this approach enable greater government influence to shape society, but public spending generally has a higher fiscal multiplier than private spending. This is through increasing aggregate demand as well as by expanding the productive capacity of the economy by crowding in private investment (Espinoza et al., Reference Espinoza, Gamboa-Arbelaez and Sy2020; Belmer et al., Reference Bermel, Cummings, Deese, Delgado, English, Garcia, Hess, Houser, Pasnau and Tavarez2024; Jung, Reference Jung2024).

Despite a ‘tax and spend’ Budget, Labour has not yet succeeded in demonstrating itself to be markedly different from its predecessor government. The overall effect of its fiscal policy revealed to date, alongside a stuttering economy, is to convey sameness and continuity rather than significant change. This is partly because it is too early to feel the effects of extra spending, much less of proposed capital investment, but also because the extra spending is not sufficient to address the under-investment in, and poor state of, public services. The government may well have underestimated the bill left by the long period of a series of governments working to weaken the welfare state. It might also be partly to do with Labour’s choice of a very conventional approach.

Thus, the choice of a conservative approach to fiscal policy – the use of fiscal rules despite their hindering impact, the retention of the ‘welfare cap’ introduced by a Conservative Chancellor as part of a programme of austerity, the devolution of ‘approval’ or ‘disapproval’ of Budget policies to the Office for Budget Responsibility, and the orthodoxy practiced by an over-powerful Treasury – all prevent, or at least make it much more difficult to embark upon, transformative policies. The pre-election pledge to not increase the rates of the main revenue-raising taxes also straightjacketed the government by removing important policy options and arguably make further cuts to social security and public services more likely as the June 2025 Spending Review illustrated.

The failure to reform the tax policy-making process can be seen not only as a missed opportunity but as a badge of orthodoxy, a sign of determination not to be different, not to open the process of policy making up, and to continue to confine real influence over tax policy to a narrow range of interests. Ironically, in choosing to keep one election promise – fiscal credibility – in the way they did, Labour may make it almost impossible to keep another – bringing about transformative change, with potentially severe consequences for Labour at the ballot box.

How might we explain Labour’s approach to tax in its first year in office? The answer may lie in a mix of economics, the structural power of capital, and calculations surrounding an electoral strategy in a first-past-the-post system.

The Labour government inherited very weak public finances and does not share the advantages enjoyed by Gordon Brown at the turn of the century in terms either of a balanced budget and comparatively low public debt or of the breadth of UK assets available for public sale. The Labour leadership’s orthodoxy is in part a response to the structural power of investors and the fear of startling investors in ways which move the financial markets towards higher borrowing costs. The debacle of the short-lived Truss government is too recent to ignore. Chancellor Kwarteng’s ‘mini-budget’ in September 2022, with its unfunded tax cuts and additional spending, raised borrowing costs for government and householders and is thought to have cost the government £30bn in lost revenues and higher borrowing costs (Helm and Inman, Reference Helm and Inman2022).

In putting together an electoral strategy to appeal to a broad enough swathe of the population to win seats from both Conservative and Scottish Nationalist parties, Labour promoted the ideas of both change and trustworthiness. The ‘red wall’ seats of deindustrialised districts may have been perceived by Labour, on the basis of polling, to be characterised by voters more likely to lean to the right than to the left and towards conservative values rather than progressive ones. While we might see the pre-election pledge not to increase income tax, employee NI or VAT as consistent with a commitment to prioritising economic growth, it is better understood as primarily a political decision. Although the choice to retain frozen personal allowances and thresholds pulls in the opposite direction, it is politically easier to raise revenues in ways that do not attract high levels of media generated criticism: fiscal drag is a much harder concept to explain to the layperson than an increased rate of tax.

Raising employer NICs also contradicts the growth strategy, but revenues must be raised somehow and this approach does – not completely but to some extent – protect the earnings of workers (the OBR (2024) estimates that 61 per cent of employer NIC raises will be borne by workers). So, to some extent, we must understand Labour’s first year tax policies, and what might be seen as their internal contradictions, through the lens of the public scrutiny attendant upon a general election, both in terms of populist announcements and in terms of caution. This is against the memory of the 1992 election, which was thought to have been lost by Labour in part through a combination of a tax-raising ‘shadow budget’ and complacency about the Labour vote (Broxton, Reference Broxton2022).

The Chancellor has used taxation as a tool of social policy to reduce inequality to a limited extent: removing the tax protection conferred upon private schools by their charitable status, capping the tax relief enjoyed by those using land to reduce tax liabilities, and changing the non-dom taxation are limited steps towards re-setting relationships. It will only be in the coming years that we can see whether or not tax is being seen systematically by this Labour government as a means of redistribution from the wealthy and better off to others. Although closing ‘loopholes’ and closing the tax gap measures constitute the second largest revenue raising intervention of the Budget, at £21bn, they yield less only a modest proportion of the potential tax gap expected during this parliament (which was almost £47bn in 2022/23 alone (HMRC, 2025a). This could be seen as limited ambition, drawing attention to the ongoing influence of the tax avoidance industry in what remains a conservative tax policy-making process, although subsequent Budgets might take the policy further.

There is no attempt to reshape attitudes by criticising UK levels of inequality or presenting taxation and social security in positive terms. Having nailed its fiscal credibility colours to the mast, the government may have become boxed in, finding it difficult to address politically consequential criticism arising from its fiscal policy. A slightly different approach to tax might become evident in the remainder of the parliament, one which is designed to address the perceived threat from Reform UK. The government seeks to promote economic growth, partially address global heating, improve the public finances, and satisfy the electorate it is best placed to bring about change and improve living standards. This is a tough and contradictory agenda.

Acknowledgement

We are grateful to Adrian Sinfield for his insightful comments on an earlier draft of this article.

Funding statement

No funding has been received for the work involved in this article.

Competing interests

Sally Ruane and Andy Lymer confirm there are no competing interests. Emma Congreve has family links to agriculture, which may be affected by policies relating to agricultural and business property relief.