I. INTRODUCTION

The last essay that Frank Knight completed before his death on April 15, 1972, was published in the Dictionary of the History of Ideas at the start of the next year (Knight Reference Knight and Wiener1973). The Dictionary (Wiener Reference Wiener1973) was the offspring of the Journal of the History of Ideas, founded in 1940. The goal was to provide a guide to the study of “pivotal ideas” within and across disciplinary boundaries. The preface tells us that historians of ideas respect those boundaries but make their own contributions to knowledge “by tracing the cultural roots and historical ramifications of the major and minor specialized concerns of the mind” wherever that may take them (Wiener Reference Wiener1973, p. vii). The historian of biology Jane Oppenheimer (Reference Oppenheimer1974, p. 243) remarked that the Dictionary was “a nonlexicographical compendium of original and free-wheeling essays about the history of a number of seemingly disparate ideas” that somehow fit “together into a multidimensional web.” Francis E. L. Priestley (Reference Priestley1974, p. 532), a Canadian English professor who was the general editor of the Collected Works of J. S. Mill (Robson Reference Robson1963–1991), was less generous to the economics entries, saying that the editorial choice to select fewer entries reflected the fact that “purely economic ideas tend to be particular in concern, and often technical, without the broad overtones and interrelations so fascinating to the historian of ideas (Mill Reference Mill and Robson1963–1991).” Today, we might well ask questions regarding who selected the topics and authors and by what criteria some ideas were judged pivotal and others not. But in the 1970s the Dictionary was generally praised for its breadth and depth, despite the contributed essays focusing primarily on the historical importance of major texts written and studied by mostly American male scholars, like Knight.

His contribution to the Dictionary provided Knight the opportunity to condense the message of the history of economics course he had taught at the universities of Iowa and Chicago between the early 1920s and mid-1950s. But the audience here was a general academic readership. Thus, he chose to start his essay with a short introduction to the intellectual background prior to Adam Smith’s Wealth of Nations and then identify and discuss briefly thirty-two pivotal moments that had shaped economic theory over the 200 years since Smith. Only at the end of the essay did he focus on “Movements Opposed to Analytical Economics,” discussing briefly Carlylean idealism, various forms of socialism, and the linkages between the German historical school and American Institutionalists. He concluded with a reminder to readers of the “parallelism of economic theory with the science of mechanics” (Knight Reference Knight and Wiener1973, p. 61). He began work on the essay at the beginning of April 1964; his last dated edits are from the middle of June 1968.Footnote 1

Knight’s submitted essay bore the title “Pivotal Ideas in the History of Economic Thought.” However, because all the essays in the Dictionary discussed pivotal ideas, the editorial team retitled Knight’s essay simply as “Economic History.” It’s unfortunate that, before his death, Knight did not have the opportunity to convince the editors to use “Economic Thought,” or even just “Economics,” as the title. While the title they used standardized Knight’s essay to the Dictionary’s usage of terms like “intellectual history,” “political history,” or “religious history,” I expect Knight might have been able to convince them that by the early 1970s economic history had become its own discipline, separable from economics (Goldin Reference Goldin1995). Unfortunately, the title has probably contributed to the small number of citations Knight’s essay received over the past fifty years.

Don Patinkin (Reference Patinkin1973, p. 789) once remarked that Knight’s classroom lectures were like “a general-equilibrium system—which could not be solved until the students were familiar with the set of Knight’s articles that specified the relationships between the various parts of the lectures, and thus converted their unknowns into knowns.” Fortunately, in the latter half of his career, Knight spoke regularly to public audiences: he gave over 100 such talks at universities, student groups, professional associations, and even churches. The plan he followed in the essay was similar to the outlines of his public addresses: he created a list of ideas in generally chronological order and provided his assessment of whether any given idea contributed to the progress of economic knowledge or not as he went along. His organization made the essay accessible, despite the condensed presentation. And of course, his judgments of the ideas addressed were emphatic.

II. WHY WAS KNIGHT CHOSEN TO WRITE THE ENTRY?

In a letter written to his mentor Frederick D. Kershner in March 1925, Knight mentioned that he was teaching history of economics to both graduate and undergraduate students at the University of Iowa for the first time, and felt like he was “bluffing” his way through because he did not have time to “make even a beginning at a study of the sources” (Emmett Reference Emmett and Emmett2013, p. 210). But Knight caught up quickly, teaching our subject regularly at the University of Iowa from 1919 to 1928 (Samuels Reference Samuels2006; Samuels et al. Reference Samuels, Johnson and Johnson2008; Tavlas Reference Tavlas2023, p. 167), and then at Chicago, where the course became a regular part of the economics graduate curriculum until after his retirement in 1951. Knight’s contributions during his career emerged from his frequent reframing of past theories in the context of new theorists he engaged with, especially Arthur Cecil Pigou (Reference Pigou1924) in the mid-1920s, and Friedrich A. Hayek (Reference Hayek1935) and John Maynard Keynes (1936) in the 1930s.

Knight’s own economic theory evolved enough over the years that both critics and supporters of various theoretical stances can find things to praise as well as criticize. Risk, Uncertainty and Profit (Reference Knight1921a) became famous for “uncertainty,” and also provided the foundation for the price theory courses he taught at both Iowa and Chicago. As well, a portion of the material he had prepared for classes at Iowa was published as The Economic Organization (Knight Reference Knight1933); and reprinted copies of his articles circulated across the United States and Great Britain from the 1920s until at least the 1940s. His students at Chicago produced three collections of Knight’s articles, each chronicling a decade’s worth of his work: The Ethics of Competition and Other Essays (Reference Knight1935), Freedom and Reform (Reference Knight1947), and On the History and Method of Economics (Reference Knight1956).

But Knight was not the only noteworthy mid-twentieth-century American economist who taught and wrote about the history of economic ideas, so why was he chosen, and not someone else, to represent economics in the Dictionary? Two potential alternatives come to mind. The first is Columbia’s Joseph Dorfman, who published more than Knight on the history of American economic thought, especially his three-volume The Economic Mind in American Civilization (Reference Dorfman1946, Reference Dorfman1949, Reference Dorfman1959), as well as Thorstein Veblen and His America (Reference Dorfman1934) and Institutional Economics: Veblen, Commons and Mitchell Reconsidered (Reference Dorfman1963). Dorfman was also active in scholarly societies, winning the Veblen-Commons Award for his contributions to the Association for Evolutionary Economics in 1974 (Samuels Reference Samuels1975), being named a Distinguished Fellow of the History of Economics Society in 1982, and having the History of Economics Society put his name on its Best Dissertation Prize, which was initiated in 1990. Another contemporary scholar who might have been selected to write the entry was Jacob Viner, Knight’s colleague at Chicago. Both Viner and Knight were honored by the American Economic Association with the Walker Medal—Knight in 1957 and Viner in 1962. And although Viner did not teach the history of economics during his tenure at Chicago (first in 1916–17, and then again from 1919 to 1946), many of the essays that ended up in his Essays on the Intellectual History of Economics (1991) were published while he was at Chicago.

Dorfman, Viner, and Knight were, therefore, all eminently qualified to write an entry on economics for the Dictionary. Perhaps the reason why Dorfman and Viner were not asked was the narrowness of their interests. Dorfman was a historian of American Institutionalism, while Viner’s historical work focused initially on the evolution of international trade theory, and only later, after the publication of the Dictionary, on religion and economics (see Viner Reference Viner1972, Reference Viner1978, Reference Viner and Irwin1991). Knight was seen as reaching a broader audience because he was a leading economic theorist who also published articles on classical liberalism and social philosophy throughout his career. Also, Knight was one of the four founders of the Committee on Social Thought at Chicago in the early 1940s, returning to the committee during the decade of Hayek’s presence. But perhaps what ultimately tilted the Dictionary’s editorial decision in Knight’s favor were the writings and talks he addressed to public audiences. The Economic Order and Religion was a dialogue between Knight and Thornton Merriam on “the practical dualism” of modern morality, with “the traditional Christian ethic at one pole and the variegated … practices and precepts of our secular life at the other” (Knight and Merriam Reference Knight and Merriam1945, p. vii). The book coupled well with Knight’s approximately 100 public lectures or talks to audiences at universities, churches, and social clubs in Chicago, and across the United States and Canada, seeking to revive “in a more sophisticated, modern form, the ancient, long widely rejected, ‘moral sciences’ conception of … economics” (Taylor Reference Taylor1957, p. 343; see also Knight Reference Knight1960). Knight’s public audience was exactly the people whom the Dictionary’s editorial team wanted to reach.

III. ECONOMICS: PRINCIPLES OF FREE SOCIETY APPLIED TO ECONOMIC ORGANIZATION

Economics, Knight tells us at the start, deals with “the general and hence abstract principles of ‘economic’ conduct and of the free ‘economic’ social order, based on exchange” (1973, p. 44). However, Knight also puts into play another principle relevant to the Dictionary’s interest, one that he called the “central and distinctive feature” of Western civilization—that is, liberty. Liberty is seldom naturally free because we all face limiting conditions. But the political priority would be to limit “arbitrary interference by other persons” as we go about our lives (1973, p. 44). To highlight the priority he gave to liberty within economics, Knight briefly outlined the evolution of Western economic thought in four stages (see Table 1). The differences between the stages are based on what objectives each society considered to be the “proper ends of social policy” (1973, p. 44).

Epochs in the Evolution of Economic Thought

Source: Created from Knight (Reference Knight and Wiener1973, p. 44).

To the best of my knowledge, Knight never started a discussion of economic organization by referring to scarcity. What he took from Greek thought was not Hesiod’s (Medema Reference Medema2019) acknowledgment of scarcity but rather the fundamental contrast between modern individualism and the social/spiritual idealism of the Greeks. Given that Knight was the first to translate Max Weber’s work into English (see the “Translator’s Preface” in Weber Reference Weber and Knight1927), it was nice to see him mention Weber’s identification of the Greek spirit with that of comrades in arms (Knight Reference Knight and Wiener1973, p. 44), providing a contrast to the methodological individualism of modern economics.

From ancient Greece, Knight moves quickly toward religious liberty, the establishment of the rule of law, and political struggles that tipped the balance toward elements of what he calls the “modern cultural revolution”—the combination of “progress through freedom and freedom for progress, directed by intelligence” (Knight Reference Knight1960, p. 45). Personal freedom in one’s economic activity was, to Knight, “the central and distinctive feature” of liberalism, implying “absence of arbitrary interference” by others, with the “primary function of coercive law and government” being the assurance of “maximal freedom for all” (Knight Reference Knight1960, p. 44).

Knight believed three pivotal moments set the stage for the birth of economics. The first moment is highlighted by a story George Stigler (Reference Stigler1985, p. 11) once told. During the outbound ocean journey to the inaugural meeting of the Mont Pélerin Society, there was a lot of turbulence, forcing passengers off the open deck. One day while Stigler was walking the passageways to get some exercise, he saw Knight in his cabin, reading a new collection of Jacob Burckhardt’s writings (Reference Burckhardt and Haugaard1943). Stigler remembered thinking (i) how could Knight be reading while the seas are roiling? and (ii) how appropriate that Knight would be reading Burckhardt. Many years later, in the Dictionary, Knight confirmed Stigler’s second observation, identifying the Italian Renaissance, Burckhardt’s (Reference Burckhardt and Middlemore1878) most famous object of study, as the moment when the word economy took on its modern meaning—the effective use of available means to achieve a pursued goal. The Renaissance was the pivotal moment when the door to economic freedom was cracked opened (Knight Reference Knight and Wiener1973, pp. 44–45).

Knight’s second pivotal moment recognized that even before the Renaissance, in early Greek and Roman thought, the notion that government should be constrained by the consent of the governed had already taken root. But after Knight notes Xenophon’s consideration of the management of a householder’s estate (Knight Reference Knight and Wiener1973, p. 45), he then jumps to the Middle Ages, when “economy” came to refer to seeking effective uses of the means available to achieve the goals that rulers and their advisors established. Until the mid-nineteenth century, after cameralism’s decline, the application of political economy to societal management still retained the notion of a state ruler as the owner of an estate. The ruler could encourage efficient management of production, provide a stable currency facilitating trade that benefited both rulers and citizens, and create infrastructure that allowed peaceful commerce, all the while enriching the kingdom.Footnote 2

But while the Renaissance encouraged the application of reason to social order, that order’s justification remained anchored in medieval Catholicism until the Reformation, which Knight marks as the moment when State functions in the social and religious realms were separated from their functions in the political and economic order. What the Renaissance began, classical political economy reconfigured. Absent institutions endowed with supernatural powers to constrain freedom, personal thought and conduct could, slowly, but then tumultuously, become free.

Knight’s third moment, then, reconstructed the link between politics and economics via the coincidence of the 119-day interval between the publication of Adam Smith’s Wealth of Nations (Smith Reference Smith1776) on March 9, 1776, and the proclamation of the American Declaration of Independence on July 4 of the same year. The third moment, however, differs from the others by the recognition that the governed are now owed the opportunity to choose who will govern them. Knight uses this connection to tie the emergence of the concept of “economic liberty” to (i) the minimizing of compulsory control over individuals’ lives by custom and law, (ii) the expansion of opportunities to exchange through experimentation and invention, (iii) the push-and-pull of public discourse regarding compulsory control, and (iv) the outcomes of legal debates and resulting precedents. It was thus important for Knight to use the confluence of the two separate events in 1776 to connect economic and political freedom. The pivotal idea, perhaps still under dispute, is whether our political and economic freedom can be maintained by consent of the governed.

Thus, during the seventeenth and eighteenth centuries, political economy emerged to assist rulers in addressing key monetary and trade-related issues. The ruler could be seen as encouraging the development of efficient management of production, stable currencies to facilitate trade benefiting rulers and citizens, and infrastructure that allowed peaceful commerce. Despite the ongoing presence of unconstrained governments, the emergence of freedom of thought and democracy helped set the stage for the emergence of a liberalism in which economic activity would flourish.

All this market and democratic talk, of course, required what Knight called the“archetypal human institution”—language, evolving imperceptibly through use. He first made the point that talk undergirded not only democratic discussion but also market interaction while he was an undergraduate at Milligan College. It was later reinforced by his friendship with the linguist Edward Sapir at Chicago. Unlike the American Institutionalists, who trusted institutions encoded in written law, Knight saw language, social customs and mores, consumer choices, and business practices as evolving through use more than edict, and hence being essential to progress. Trade is interchange; democracy is discussion—that is Knight in a nutshell. Unlike the American Institutionalists who preferred rules rather than discretion, Knight emphasized the benefits for both sides of any exchange, even while recognizing that self-love, pride, and even error could always tip the advantage to one side of an exchange or the other (see Knight Reference Knight1935). He concludes his opening discussion of the origins of economics by saying: “A major lesson to be learned from the history of ideas is to realize [our]’glacial’ tardiness … in seeing what it later seems should have been obvious at the first look. This is strikingly illustrated by the concept of economy. People have always … ‘economized,’ … but have been unaware of the principle” (Knight Reference Knight and Wiener1973, p. 46).

IV. TRUTH AND ERROR: PIVOTAL IDEAS IN CLASSICAL ECONOMICS

Knight recognized that ideas he considered fallacious were nevertheless pivotal to the history of economics. This was especially true in his evaluation of classical political economy. The labor theory of value was, for Knight, “the fountainhead of analytical fallacy” (Knight Reference Knight and Wiener1973, p. 47). A second pivotal error was the classical idea that the price of any good equals the sum of the wages, profit, and rent, each of which the classical economists considered to be determined independently of the others. Instead, Knight argued, the current price of a good in any market is simply what is required to reconcile current demand to the existing supply. If the classical economists used a term like “natural price,” Knight suggested it referred to the reconciliation of prices over the longer term through the movement of goods and resources between firms in response to current prices (Knight Reference Knight and Wiener1973, p. 48).

Two implications of Knight’s definition of economics should be addressed. The first is that the discipline of economics as a scientific enterprise must always deal with the distance created by “arbitrary interference” on the part of government between a society’s economic organization today and how it might exist in a laissez-faire state (Knight Reference Knight and Wiener1973, p. 44). The second is that it may be impossible to know for sure whether any aspect of our current social organization meets the ideal. Together, these implications suggest humility by economists regarding any predictions based on economic models, no matter how sophisticated.

The largest number of pivotal ideas in Knight’s essay emerge from classical economics (Knight Reference Knight and Wiener1973, pp. 47–50). Not surprising, because his own theoretical apparatus was a merger of (i) what he appreciated from Smith despite his errors, (ii) corrections provided by late classical economists (especially Nassau Senior), and (iii) early marginalism (especially Philip Wicksteed), coupled with (iv) a rejection of Cambridge economics, especially the work of Pigou and Keynes. Of the eight pivotal ideas Knight associated with the classical economists, five were identified as errors (see Table 2).

Pivotal Ideas in Classical Economics that Knight Identified as Errors

Source: Created from Knight (Reference Knight and Wiener1973, pp. 47–50)

Knight’s first pivotal error in classical economics is the use of “natural price.” Smith’s discussion is not very clear because he left open several meanings of the term. But Smith does understand that changes will come about through short-term price adjustments, with the natural price acting as an anchor that fluctuating markets will eventually settle upon. However, the remainder of classical price theory, in Knight’s estimation, is mistaken (see Knight Reference Knight1935, pp. 37–88). The labor theory of value was, for Knight, “the fountainhead of analytical fallacy” (Knight Reference Knight and Wiener1973, p. 47). Smith and David Ricardo saw wages, profits, and land rents being determined separately, in part because wages and land rents were believed to be primarily determined outside of markets and therefore slow to respond to economic fluctuations.

While the coincidental equation of the sum of the factors’ returns with the market price is possible, Knight’s price theory judged market price to be simply the short-term reconciliation of demand to existing supply, because resources may have a multitude of alternative uses at any point in time (Knight Reference Knight and Wiener1973, p. 48). The potential for mismatches to occur, Knight argued, was part of “the meaning of the irksomeness of work” (Knight Reference Knight and Wiener1973, p. 48)—what one expected was not necessarily what one received, neither in the workplace nor in the pocket. A related issue for Knight was the “pivotal absurdity” of the classical economists’ idea that monopolies can always charge the highest possible price (Knight Reference Knight and Wiener1973, p. 48). The basic point, of course, is that classical economists primarily looked at markets from a perspective dominated by their British social context, while twentieth-century economists had generalized beyond those constraints.

Second, Knight judged Malthusian population theory to be in error, despite how pivotal it was to classical theory (Knight Reference Knight and Wiener1973, pp. 49–50). Knight’s key issue with Thomas Robert Malthus was the way he assumed population increases functioned to keep wages level with a fixed living requirement, because that allowed classical economists to argue that “a given amount of capital in any form can maintain a definite amount of labor or industry” (Knight Reference Knight and Wiener1973, p. 49). The population principle implies that “their numerical increase keeps wages at this level, regardless of the amount assigned to their support” (Knight Reference Knight and Wiener1973, p. 49). Knight also suggests that Malthus is responsible for the assumption that labor and capital were subject to diminishing returns (the third classical economics error); an assumption that Knight points out is valid only if technological advance is ignored. Knight concludes with a sentence one perhaps has to read twice to catch his understated irony: “The historical fact has, of course, been a vast rise of wages, in spite of redoubling of numbers of workers” (Knight Reference Knight and Wiener1973, p. 49). Perhaps Knight did listen to the economics historians who were his colleagues in the Chicago department after all.

The fourth error Knight identified among classical political economists was their “apparent mental fixation on labor as alone really productive”; adding that the idea comes from Genesis 3:19, which he identifies as “folklore” (Knight Reference Knight and Wiener1973, p. 47). The fundamental classical error was, in Knight’s view, their treatment of labor: in a short paragraph, made long by a host of parenthetical insertions, Knight lays out the argument against this classical fixation and the miscues it gave later classical theorists. For them, the productivity of labor was primarily determined by the proportion of those who perform what the classical economists considered to be labor that was useful. Smith himself attributed the “greatest improvement” in productivity to come from “specialization” (Knight’s word for Smith’s idea) and “the division of labor” (Knight now quoting Smith to link specialization to the subdivision of work). Knight goes on to say that specialization “works in three ways” for the classical economists: it increases the skill level of workers generally, saves on time by reducing each worker’s task, and increases “the application of proper machinery.” Knight adds to his description of Smith’s notion of “capital” that much of the world continues to view “property” as the “means for exploiting workers” and that even free nations “commonly impute all ‘productivity’ to labor,” and define capital as “support for laborers, chiefly food, ‘advanced’ by persons who have a surplus beyond their own needs for consumption” (Knight Reference Knight and Wiener1973, p. 47).

The fifth, and final, error of classical political economy is perhaps one of those examples of not knowing that we are breathing air. Smith’s “three great constituent orders”—land, labor, and capital (Knight Reference Knight and Wiener1973, p. 49)—were knit into the fabric of European and British societies long before Adam Smith; for example, the statement “money is the sinews of war” was first used almost 2,000 years before The Wealth of Nations in Cicero’s fifth oration against Mark Antony. Thus, perhaps we should not expect to be surprised that the classical economists followed the French Physiocrats in thinking of society as having three great orders, identified with land, labor, and capital. The problem with that view, Knight says, is that “as with water and diamonds, land, labor and capital are not marketed as categories, but by bits and discrete items which differ vastly within each class” (Knight Reference Knight and Wiener1973, pp. 49–50).

All these criticisms of classical economics highlight the point from which Knight will move forward—what he calls the “glacial tardiness” in economists’ consideration of “the concept of an economy” (Knight Reference Knight and Wiener1973, p. 46). The correct approach was to be a refashioning of economics via the tools provided by the Marginal Revolution. Marginalism emerged out of classical economics with the recognition that the “economic value of a good reflects the use-value of an increment (acquired or given up), not that of the commodity in the abstract” (Knight Reference Knight and Wiener1973, p. 50). Furthermore, the value of an additional increment decreases as more of the commodity is used or transferred. “That is, wants are satiable” (Knight Reference Knight and Wiener1973, p. 50), which was part of his objection to classical theory. Marginalism is also applicable to the “yield of productive services.” As production of a good or service increases, the “increments of physical yield decline, and the value product still more” (Knight Reference Knight and Wiener1973, p. 50). The incremental principle was also applied by John Bates Clark and Wicksteed to the distribution among the three traditional factors.

Knight concludes the section of the paper on marginalism by noting that “[t]he most important defect in the traditional theory is that its factors are unreal.” Productive “persons” as well as “natural agents” qualify as “capital goods” because they are “produced at a cost and require maintenance and replacement.” And “original and indestructible” land is “unknown on the market.” All three productive factors must be produced, maintained, and replaced; and all are mutually complementary in use. None exist independent of the others. Yet, in a free society, we must recognize that people are “in human and social terms, a category distinct from ‘property’” (Knight Reference Knight and Wiener1973, p. 51).

V. ENTREPRENEURS, ENTERPRISES, AND THE ECONOMY

Knight surprises the reader at this point with a move that has two aspects. The first looks familiar —a move toward a system of multiple markets rather than just one, with a degree of simultaneity comprising a general equilibrium system or, perhaps more accurately in terms of what Knight is doing, a macroeconomy. The second is uniquely Knight’s—a focus on entrepreneurs and enterprises in that macroeconomy. Of course, as soon as I say “entrepreneur” in any connection to Knight, everyone is going to immediately think of the entrepreneur of Knight’s Risk, Uncertainty and Profit (1921a)—who is often portrayed as a Crusoe-like character—the very definition of a solo entrepreneur. Knowing that Knight wrote Risk, however, does not really help us here. Rather than casting the entrepreneur onto a deserted island to fashion things himself, Knight surrounds the entrepreneur with an enterprise: production will be “carried on by an organization of persons and equipment, with much internal specialization of roles” (Knight Reference Knight and Wiener1973, p. 54). Such an enterprise will require money and a decision-maker—the entrepreneur. Entrepreneurs become the central figures of the “enterprise economy,” but the firm and the economy in which they are situated form a “complex system, rooted in a higher order of specialization” (see Emmett Reference Emmett2011). I see him thinking about high-tech sectors and Start-up Nation (Senor and Singer Reference Senor and Singer2009), but certainly not The Entrepreneurial State (Mazzucato Reference Mazzucato2013). Entrepreneurs buy “most of the labor power and property services” (Knight Reference Knight and Wiener1973, p. 54) required from outside owners. Entrepreneurs make most of the economic decisions for their enterprises, based on interactions in product, labor, and services markets; profit, therefore, is the return to bearing responsibility for the enterprise’s success. Of course, Knight points out that profit is separable from payment for the entrepreneur’s own contribution of services or property.

But as soon as we join Knight in this move, we encounter an economic error that goes back to the “empty boxes” debate of the 1920s over increasing and decreasing returns (Clapham Reference Clapham1922; Pigou Reference Pigou1924; Pigou and Robertson Reference Pigou and Robertson1924). The error lies in seeing increasing returns as an increasing ratio of output to inputs with an expanding scale of units in organizations, that is itself made possible by increased specialization. As Knight puts it in the essay:

The principle of “decreasing returns” is related to any kind of productive agent applied in increasing proportions to any combination of kinds. And all “means” are means of production. There is no corresponding law of “increasing returns” except, rigorously speaking, for a short threshold on a minimal dosing of one kind of means onto others. The expression “increasing returns” is confusingly used for an increasing ratio of output to input with an expanding scale of units in organizations, due to increasing specialization so made possible. The “unit” in production has various meanings. The subject calls for mention because the two expressions falsely suggest antithesis; but more especially because of the tendency of many people, and some economists, to think that increasing returns with larger scale is also a general law. It holds for an early stage in a hypothetical expansion of a ‘unit,’ beginning at zero. The gains from more minute specialization are soon offset by increased difficulty of coordination, unwieldiness, and costs of management. (Knight Reference Knight and Wiener1973, p. 51)

Of course, what can expand an enterprise’s activity and size simultaneously is new technology, emerging from the enterprise’s research and product development activities. Invention is a type of investment—“a creative act, perceiving and solving a problem” without knowing in advance what the solution will be. Because “the end cannot possibly be known in advance,” the activity is not “economic in the strict meaning.” Failure occurs often, which is also the case for exploration of natural resources. Thus, “progress is no definable equilibrium position” (Knight Reference Knight and Wiener1973, p. 51).

Knight points out that selling goods is the same thing as leasing those goods, under ideal conditions. When a sales agreement is made, the seller could agree to take a “note” for the price and receive interest instead of rent for the term of the agreement. Under conditions of perfect knowledge and economic rationality, the combination of sale price and interest rate should make the payment equivalent to that of a lease. The same principle allows for various combinations of purchase, rent, and lease (Knight Reference Knight and Wiener1973, pp. 55–56). To press the point home, Knight reminds his audience that neither our system nor the entrepreneurs who are lauded by it can take credit for success. Profit is the consequence of imperfections in the competitive market system, which are, in turn, the result of uncertainty and limited entrepreneurial foresight (Knight Reference Knight and Wiener1973, p. 55). Uncertainty and limited foresight can be reduced but never eliminated.

Thinking of enterprise activity in terms of the price system, a common error is to believe that humans prefer recent goods to future goods of like kind and amount. But Knight insists that this ignores three facts: i) I do not want to postpone today’s consumption, ii) neither do I want to consume tomorrow’s provisions today, and iii) I cannot postpone consumption perpetually. Alfred Marshall’s (Reference Marshall1890, p. 120) “homely illustration” makes the point well: when eating a plum pie, “some will pick out the plums and eat them first, some will save them to the last, and others eat them as they come to them.” No abstract principle of current versus future consumption will hold for everyone. For consumption, it will depend upon people’s tastes; and for investment, rational conduct dictates making an investment that is judged to return “above the going rate” (Knight Reference Knight and Wiener1973, p. 56).

Knight closes the section on enterprise economies with the introduction of “the concept of a general equilibrium relation among all the main variables—prices and quantities—treated in economic analysis” (Knight Reference Knight and Wiener1973, p. 51). If economic conditions were stable enough for all effects to work out, a general equilibrium across an economy could be realized; that is,

simultaneously all consumer expenditures would buy at the margin equal increments of satisfaction and all productive resources would yield (marginally) equal increments of value product, all prices being equal to costs…. This conclusion should be qualified by the fact that the system pictured embodies ‘feedback’ principles, and … these typically produce oscillations, where responses are not instantaneous. (Knight Reference Knight and Wiener1973, p. 55; emphasis in the original)

Knight (Reference Knight and Wiener1973, p. 52) rightly attributes “the idea of a … crude system of equations” to Leon Walras (1874/Reference Walras1877).

Thus, it is likely that the enterprise form of economic organization is inevitable. Lending money may not be inevitable, because a loan can always be replaced with a sale or a lease, but with enough economic activity, all forms of exchange will become well developed. Major decisions for enterprises will be “made formally by entrepreneurs, interacting with their opposite numbers in markets, and acting directly or through agents whom they hire.” But entrepreneurs are, in the end, “responsible to consumers and owners of productive agents … and ‘at equilibrium’ have no power at all,” because, as Knight said in “Cost of Production and Price Over Long and Short Periods,” entrepreneurs in the long run “are forced to use the most efficient methods or give place to others who do” (Knight Reference Knight1921b, p. 318).

To analyze economic conduct, it is necessary to abstract away from “all social interests and relations” (Knight Reference Knight and Wiener1973, p. 52). Imagine, then, an isolated individual who is responsible for making all decisions regarding her production and consumption under a given set of conditions. Apportioning her “productive capacity”—whatever that may be—for “maximum want-satisfaction” will be guided by two principles: a) diminishing marginal utility, and b) the equi-marginal principle, which is that, given her income, when she is done apportioning it among the various uses she values, the result will yield equal satisfaction at the margin for all units in all uses.

In the Crusoean context, all risks and uncertainties are borne by the single individual. But decisions regarding the postponement of consumption are not uniform among human beings. Even if abstract rationality “would surely call for something near uniformity over time,” there is no principle embedded in human nature that determines our choice between goods today versus goods tomorrow. The function of interest rates is to mediate today’s, tomorrow’s, and the future’s consumption without necessitating the theorist or a central planner to make a social/political decision regarding our consumption preferences. The decision is a matter of individual taste, and, in that regard, de gustibus non est disputandum.

Knight concludes discussion of an enterprise economy with two other issues that classical economics did not handle well, probably with good reason. The first is the progressive satiability of human want, and the second is the link, perhaps unavailable to the classical economists, between exploration/discovery of new resources and innovation. With respect to the first issue, classical political economy held “utility” to be “a condition of value, but not a cause—or measure”—of value. Thus, they missed the pivotal idea that the satisfying power of any good is progressively satiable, which finally entered economics “nearly a century after Smith” with adoption of the expression “diminishing marginal utility.” For Knight, diminishing marginal utility marked the change from political economy to economics. Diminishing marginal productivity was a “parallel principle” not recognized until later (Knight Reference Knight and Wiener1973, p. 48).

Invention is an even greater challenge for economics—“a creative act,” Knight calls it, “perceiving and solving a problem” (Knight Reference Knight and Wiener1973, p. 51). Because the result cannot be predicted or known ahead of time, invention is only partially “economic” in the strict sense of the word. Progress does not have a “definable equilibrium position” and, as much as we expect inventions to pay off, they often fail to find useful applications, at least initially. Much the same can be said about exploration for natural resources (Knight Reference Knight and Wiener1973, p. 48).

VI. MONOPOLY, STABILIZATION, THE BUSINESS CYCLE, AND SYSTEMIC FEEDBACK ADJUSTMENTS

Knight then turns to issues that don’t really fit elsewhere. The first is the problem of monopoly. Classical political economists wrote “nonsense” about monopoly pricing, because it is less important than most people think. The evils of monopoly power are exaggerated, often because it can be “natural, even inevitable,” and more may be beneficial. Governments grant patent and copyright privileges “to encourage useful innovations, and a large share of those privately set up work in the same way” (Knight Reference Knight and Wiener1973, p. 57). Monopolies in labor, agriculture, and foreign trade are costly, but often the public wants more of them. A common mistake on both sides of the debate is to claim that tariff barriers will support existing monopolies and allow the establishment of new ones; however, protective trade barriers do not necessarily establish monopolies.

His remarks regarding monopolies harken back to his late teens, when he once started a patent application for a stenograph machine, although there is no evidence he submitted it. At that time (the late 1890s), he also worked as a nighttime telephone operator for his uncle’s Lexington (IL) Home Telephone Company. His uncle owned and operated the business for the next thirty years, selling only in 1928 to the Illinois Commercial Telephone Company, which became part of General Telephone and Electronics Corporation. GTE merged with Bell Atlantic in 2000 to form Verizon (Emmett Reference Emmett2024, p. 10).

Knight’s comments on the business cycle start with the feedback mechanisms he had already mentioned as producing oscillations of supply and demand—something normal price theory should account for. But classical economists mostly failed to get behind the veil of money. David Hume was an exception, recognizing that an increase in the quantity of money would raise selling prices faster than cost prices, which would enable business profits to increase, while also causing misery and unemployment. The influx of New World silver and gold favored debtors at the expense of creditors; Smith mentioned the losses incurred by feudal landlords whose feudal rents were payable in cash. As well, when a boom begins to reverse, remediation “through monetary and fiscal action” can be undertaken. “But no one knows just when to act or how much action to take, while the public opposes ‘killing prosperity’” (Knight Reference Knight and Wiener1973, p. 58). In the other direction, it is not clear why economic declines stop and with what speed the upswing will proceed. Sometimes people see the bottom of the cycle as a “stable equilibrium along with extensive idleness of labor and other resources” (Knight Reference Knight and Wiener1973, p. 58), which is self-contradictory. Given that Knight began his career at Chicago just before the Great Depression, he describes both the bottom of the cycle as well as the beginnings of any economic upswing in terms that reflect personal experience. And the result may be surprising, “first, that money, and circulating credit, must be ‘managed’—a policy of laissez-faire here has ‘intolerable results’”; but second, that the management cannot be very effective, consistent with social freedom. New Deal policies, he believed, had been “ineffective.” Only the outbreak of war in Europe had “finally cured” the Great Depression (Knight Reference Knight and Wiener1973, p. 58). And I should probably mention that Keynes gets one nod (but only one!) for his stress on “interest as a rent on cash” (Knight Reference Knight and Wiener1973, p. 58).

VII. KNIGHT’S DIVISIONS OF MODERN ECONOMIC SCIENCE

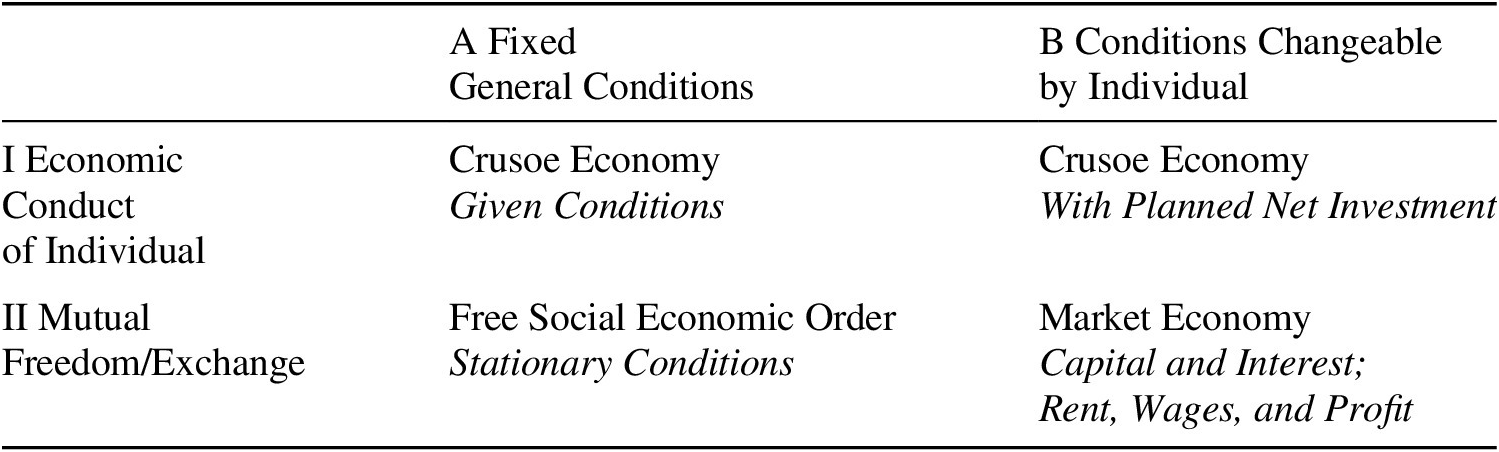

Turning from classical economics to what was, for Knight, modern economics required the development of a simple model with embedded assumptions that, when weakened or removed, allowed more of our economic activities to be explained (see Table 3). Knight chose to use the “Crusoe” economic model as his starting point because it involved initially a single person operating under mostly fixed general conditions, both to utilize resources the person could find to satisfy needs, and to fashion tools that would make it easier either to satisfy needs or to create even better tools and processes that could expand the resources Crusoe had available. But we are already ahead of ourselves, because the Crusoe whom Knight introduces in this model is concerned only with dividing what is immediately available to uses that Crusoe knows will contribute to want-satisfaction. Thus, the Crusoe Economy initially features merely the general principles of diminishing marginal utility and apportionment among options available (food, shelter, clothing, etc.) on the principle that “equal units (of negligible size) make equal additions to total satisfaction in all uses” (Knight Reference Knight and Wiener1973, p. 52).

Divisions of Modern Economic Science

But “consumption is by no means the whole end” of life (Knight Reference Knight and Wiener1973, p. 53), and if a Crusoe could add some security by maintaining a constant income through saving and investing, personal welfare could be increased. Capital accumulation requires creating value more than cost, and investing requires time, thus a rate of growth is needed in light of Crusoe’s target income, which, when reached, would allow Crusoe to focus on maintaining the net income desired. Knight tells us that these concepts are “pivotal for our understanding of economic analysis.” But he also points out that investment theory is abstract, in the sense “that an investor could never have the knowledge required for accurate calculation.” He closes the section by saying the “main reason for considering the Crusoe economy” is “to analyze the growth rate of investment apart from lending and interest” (Knight Reference Knight and Wiener1973, p. 53).

Knight’s use of the expression “free Social-Economic Order” comes from John Bates Clark’s The Distribution of Wealth (Reference Clark1899, p. 53), but he appears to have preferred Alfred Marshall’s (Reference Marshall1890) “more realistic, though less systematic, treatment” of price over both the short run and the long run, despite Marshall’s maintenance of John Stuart Mill’s commitment to a future stationary state (Knight Reference Knight and Wiener1973, pp. 53–54). By Knight’s account, the most serious errors in Marshall are: a) his failure to note that new technology is chiefly produced by investment, which increases the yield of and demand for all kinds of productive services; and b) the fact that new technologies “constantly open the way to more progress, with no assignable limit” (Knight Reference Knight and Wiener1973, p. 54). Thus, because technology progresses, other things will never continue to be equal and the stationary economy, beloved of Marshall and Clark, is an illusion. What emerges is an “enterprise economy” (Knight Reference Knight and Wiener1973, p. 54), where profits are the result of perpetual market imperfections (caused by uncertainty and limited foresight) and the agency relation dominates business and political life.

VIII. KNIGHT’S LIST OF MOVEMENTS OPPOSED TO ANALYTICAL ECONOMICS

Knight was well known for acerbic dismissals of scholars with whom he disagreed—his comment in the essay about Edward Chamberlin giving “inconvenient Greek names” to “a group of vague monopoloid situations” (Knight Reference Knight and Wiener1973, p. 51) being a mild example compared to some of his attacks on other scholars. The four objections to the findings of analytical economics that he does address at the end of his essay raise foundational issues that perennially get asked of economists by their students and the public. The first of these is the objection to economic reasoning raised by Thomas Carlyle, the dismalness of which Knight identified with “the need to give up one good to get another” (Knight Reference Knight and Wiener1973, p. 26). Why do we have to face trade-offs? Knight suggests that idealists of all sorts have problems with scarcity, and it can only be mitigated, not overcome. But he adds that we could point to the work of entrepreneurs, who continually bring us new goods and services.

A second objection that Knight addressed was John Charles Léonard Simonde de Sismondi’s issues with Smith’s defense of the notion of “natural liberty.” Knight states his agreement with Sismondi’s remark that The Wealth of Nations is “one-sided propaganda” for economic freedom—the one side being a political argument based on utilitarianism, which Knight (Reference Knight and Wiener1973, p. 59) says “has nothing to do with economics as a science.” But Knight added that, without a clear identification of what Smith meant by the “invisible hand,” criticisms could be leveled at the classical tradition for not recognizing anything that would qualify as a “real social interest” (Knight Reference Knight and Wiener1973, p. 59). Would Smith have accepted a definition of society that made it merely an organization of individuals for the purpose of mutually beneficial economic advantage? Deirdre McCloskey’s “Bourgeois Era” trilogy (McCloskey Reference McCloskey2006, Reference McCloskey2010, Reference McCloskey2016) suggests that Smith would not accept a “merely” economic response, and Knight would not have accepted it either. In that regard, I’ve often wondered about the interesting two-sidedness of Knight’s household. On one side is Frank, whom we think of as the epitome of the “dismal scientist,” while his wife, Ethel—who was called “Miss Verry”—was the executive director of the Chicago Child Care Society. Miss Verry placed over 10,000 children in new homes and worked nationally to establish standards for child-care agencies (see McCausland Reference McCausland1976).

The third objection that Knight addressed was the opposition that the economics profession faced because of its laissez-faire orientation, an argument he traces back to Sismondi (Reference de Sismondi and Léonard1819). Sismondi’s argument emerged from his own time, when laissez-faire had been converted into an ethical stance and even a political doctrine (Manchester liberalism), both of which Knight views as mistakes. The science of economics assumes, he says, only the analytical, hence partial, “descriptive truth of its principles, not their ethical rightness” (Knight Reference Knight and Wiener1973, p. 59), just as friction is ignored in physics. Given his undergraduate physics background, Knight often remarked that theoretical economics is as valid as theoretical mechanics.

And lastly, Knight objects to the identification of laissez-faire with anarchism. Smith and Knight provide arguments that point out the benefits of market freedom and the measures available in a democratic society to address or mitigate the market failures that remain. Yet for some, laissez-faire means anything goes, the effects of which must be ameliorated or countered by societal and governmental action. Knight argues that Smith and other economists identified three qualifications often ignored by capitalism’s critics. The first is that specific “evils” or “ills” of market freedom must be identified and considered in terms of our ability to offset them. For example, the fact that market participants must make choices among differing outcomes ought not to be mislabeled immoral. And might well-meaning policymakers worsen the situation by inhibiting individual actions that could ameliorate the ills? Or might the measures proposed require actions a democratic polity cannot undertake? Finally, in a liberal society, we must demonstrate that the measures proposed can maintain maximal freedom for everyone in society. All this, Knight concedes, requires a “fair degree of legal order” (Knight Reference Knight and Wiener1973, p. 59).

Based on these arguments, Knight concluded by saying the various movements opposed to analytical economics are not really in conflict with economic orthodoxy, because “price theory yields laws more useful for guiding action than any other comparably simple view of social phenomena” (Knight Reference Knight and Wiener1973, p. 61).

COMPETING INTEREST

The author declares no competing interests exist.

Open access

Open access