Policy Significance Statement

AI risk bonds offer policymakers a novel market-based solution for the unpredictable and often uninsurable risks posed by today’s AI systems, targeting governance gaps that traditional regulation and insurance leave unaddressed. By securitizing AI liabilities, these bonds transparently price risk and harness investor scrutiny, motivating AI developers to prioritize safety and disclosure. This approach diffuses financial risk through capital markets rather than relying solely on insurers or taxpayers. More importantly, it ensures that victims of AI incidents receive compensation in a timely manner. Policymakers gain an actionable tool that complements regulatory frameworks like the EU AI Act, operationalizes responsible oversight, and aligns innovation incentives with public safety.

1. Introduction

The magnitude and scope of potential risks associated with AI systems have become central topics of debate within recent academic discussions (Giudici et al., Reference Giudici, Centurelli and Turchetta2024). Researchers adopt diverse perspectives and analytical frameworks, leading to a wide spectrum of viewpoints regarding the severity and nature of AI-related threats. On one end of this spectrum, scholars focus primarily on risk assessment and liability frameworks derived from established approaches to consumer-facing technologies, emphasizing practical near-term concerns (Ebers, Reference Ebers2021; Hasan et al., Reference Hasan, Shams and Rahman2021; Chan et al., Reference Chan, Papyshev and Yarime2024). On the other extreme, discussions center around existential catastrophic scenarios involving advanced AI systems with capabilities surpassing human intelligence, presenting risks potentially threatening humanity itself (Hendrycks et al., Reference Hendrycks, Mazeika and Woodside2023; Swoboda et al., Reference Swoboda, Uuk, Lauwaert, Rebera, Oimann, Chomanski and Prunkl2025).

In this article, however, we explicitly choose not to engage in this broader theoretical debate concerning the ultimate destructive potential or existential implications of future AI advancements (Barnett and Scher, Reference Barnett and Scher2025). Our purpose is distinctly more practical and immediate: we aim to explore and propose a market-based mechanism designed specifically to mitigate risks arising from current-generation AI systems and their unique behaviors. Our approach is anchored in the proven efficacy of market structures and self-regulatory mechanisms historically utilized for managing risks in other domains, such as natural disasters, industrial accidents, or mass vaccination. For instance, the International Finance Facility for Immunization has mobilized nearly $10 billion through vaccine bonds, contributing to the vaccination of over 1 billion children (Tacheva et al., Reference Tacheva, Brown, Bell and von Agris2025); similarly, catastrophe bonds have transferred billions in natural disaster risk to capital markets since the 1990s (Cappiello and Vannucci, Reference Cappiello and Vannucci2025); in the chemical sector, self-regulatory programs like Responsible Care have been shown to reduce industrial accidents (Gamper-Rabindran and Gamper-Rabindran, Reference Gamper-Rabindran and Gamper-Rabindran2011).

We propose AI risk bonds: a market-driven mechanism, inspired by catastrophe bonds, that aligns financial incentives with responsible AI development by transparently pricing risks and leveraging investor scrutiny to enforce accountability.

A bond is a loan from investors to an issuer; investors receive interest (the “yield”) as compensation for risk. Riskier bonds must offer higher yields to attract capital (Kim and Orphanides, Reference Kim and Orphanides2007). In the AI Risk Bond design, investor principal is held in escrow; if a predefined adverse event occurs, some or all principal is used to compensate victims; otherwise, investors receive interest and their principal back (Section 4 describes this mechanism in more detail). Our analysis formalizes how perceived AI risk translates into required yield.

Catastrophe bonds are insurance-linked securities that use parametric triggers (predefined observable conditions of high-risk magnitude) to automatically release funds, enabling rapid payouts compared to slower claim-by-claim indemnity processes. These triggers can be single datapoints or indices assembled from external third-party statistics (e.g., outbreak size, growth, and geographic spread as in the World Bank’s Pandemic Emergency Financing Facility), reducing disputes over loss measurement and accelerating liquidity to affected parties (Unnava, Reference Unnava2020).

In this article, a “payout event” is simply a clearly defined bad outcome from a rogue AI system behavior, written into each bond’s terms before it is sold. However, we do not prescribe what counts as a payout trigger—we are deliberately agnostic. We refrain from prescribing a taxonomy of payout events. The reason is straightforward: true AI risks are impossible for outsiders to estimate in advance. AI systems are characterized by opacity and unpredictability, producing emergent behaviors that even their creators cannot fully anticipate. If developers themselves cannot foresee every possible rogue behavior, then no regulator or scholar can credibly prescribe a universal taxonomy ex ante. A fixed list of triggers would quickly become obsolete as risks evolve and would recreate the very information asymmetry the bond is designed to solve. Instead, we require issuers to define their own triggers before sale, forcing them to articulate their risk model. Investors and auditors then evaluate those definitions, creating a market-driven feedback loop where weak definitions are penalized through higher yields and credible definitions are rewarded. This ensures the mechanism remains adaptable to evolving risks without requiring constant regulatory updates.

We operationalize “rogue behavior” as a documented deviation from stated objectives or safety policies that leads to harmful or materially misleading outcomes. To keep the framework general, issuers define their own payout events, but common examples include (i) specification gaming: exploiting task loopholes to meet the letter but violate the spirit of objectives; and (ii) sustained hallucinations: confidently wrong outputs in contexts where accuracy matters. Investors would not estimate the probability of these events directly; instead, they would rely on standardized metrics produced by accredited auditors who evaluate AI systems against established benchmarks (Brundage et al., Reference Brundage, Dreksler, Homewood, McGregor, Paskov, Stosz, Sastry, Cooper, Balston, Adler, Casper, Anderljung, Werner, Mindermann, Mavroudis, Bucknall, Stix, Freund, Pacchiardi and Tovcimak2026). We intentionally limit examples to illustrate scope without prescribing a taxonomy.

This gap between AI behavior and legal remedies is not merely theoretical, as courts are already grappling with rogue behavior-related harms. In the AI defamation lawsuit, conservative activist Robby Starbuck sued Meta after its AI chatbot falsely claimed he participated in the January 6 Capitol riot. Rather than litigate to judgment, the parties reached a novel settlement in August 2025: Starbuck will serve as a consultant to Meta’s Product Policy team, working to combat political bias and reduce hallucination risks across Meta’s AI models (Spector, Reference Spector2025). Across the Atlantic, a Brazilian court reached a different outcome. Marcelo Tavares sued after Google’s Gemini AI misidentified him as the owner of an online betting site, a hallucination triggered when Gemini misinterpreted an interview in which Tavares recommended seven video games with the betting site—7Games. The 5th Civil Court of Niterói rejected Google’s defense that it merely aggregated public information, holding the company directly liable for its AI’s output and ordering payment of R$20,000 (~$4000) in moral damages (Villar, Reference Villar2025).

Under the AI Risk Bond design, each developer decides what kind of bad outcome their bond will cover and exactly where to set the threshold, and they must spell that out clearly before the bond is sold. Developer here refers to the organization that builds and/or deploys the AI system and issues the AI Risk Bond. We use “developer” to denote the issuing organization rather than an individual engineer. Throughout, our analysis concerns organizations rather than individual persons. The market then judges those choices: if investors think the trigger is too lenient, too narrow, or too vague, they will demand a higher yield or simply refuse to buy. That is by design; the issuers set the terms, but they also bear the consequences of investor reactions: the cost of capital rises for weak specifications and falls for credible ones.

2. AI risks

Contemporary academic literature addressing the intersection of AI and risk management often examines hypothetical catastrophic scenarios, focusing on causes for and impacts of large-scale AI disasters. Consequently, comparatively less scholarly attention has been devoted to understanding how insights and methodologies from historical catastrophic risk management practices could be effectively repurposed or adapted for addressing increasingly frequent risks associated with today’s AI technologies. Specifically, there remains a significant research gap concerning policy frameworks and market structures capable of systematically working through incidents and potentially also mitigating these more immediate risks.

The escalating number of AI-related incidents (Paeth et al., Reference Paeth, Atherton, Pittaras, Frase and McGregor2025) underscores a pressing legal and regulatory dilemma: who should be held liable when these sophisticated systems cause harm? Existing liability regimes were not designed to address the unique nature of AI-driven harm. The first and most common pathway, fault-based liability, requires a claimant to prove that a defendant breached a duty of care and that this breach caused the damage (Lahe, Reference Lahe2005). This framework immediately encounters the “black box” problem (M. C. Buiten, Reference Buiten2019, Reference Buiten2024; Duffourc and Gerke, Reference Duffourc and Gerke2023). Proving negligence becomes nearly impossible when the process leading to harm is technologically opaque and potentially unexplainable, even to the system’s creators. Establishing causation is equally difficult when there is no traceable and predictable line between AI design and harm (Fraser and Suzor, Reference Fraser and Suzor2025). The autonomy of AI systems further weakens the chain of causation, as the developer’s original actions are separated from the harm by the system’s own independent decision-making processes (Padovan et al., Reference Padovan, Martins and Reed2023a). As the processes running in AI systems cannot all be measured according to duties of care designed for human conduct, it is difficult to determine a clear breach (Custers et al., Reference Custers, Lahmann and Scott2025).

The second pathway, strict liability, removes the need to prove fault and imposes liability based on the principle that one who engages in an abnormally dangerous activity must bear the costs when the risks of that activity materialize (M. Buiten et al., Reference Buiten, de Streel and Peitz2023; Montagnani et al., Reference Montagnani, Najjar and Davola2024). The argument for applying strict liability to high-risk AI is compelling, as autonomy and opacity create the exact difficulties this regime is designed to overcome. If developers and users cannot fully control an AI system, strict liability forces the risk-bearer to internalize all costs (Wendehorst, Reference Wendehorst2020). However, the rationale for strict liability hinges on the defendant’s control over a salient risk. As AI systems become more agentic, this control diminishes, leading to what are known as moral crumple zones where liability is misattributed to the most proximate human operator, who had limited actual control over the system’s actions (Custers et al., Reference Custers, Lahmann and Scott2025).

The third pathway, product liability, establishes a strict liability regime for defective products (Noto La Diega and Bezerra, Reference Noto La Diega and Bezerra2024). The critical challenge here is defining a defect in an AI system (Novelli et al., Reference Novelli, Casolari, Hacker, Spedicato and Floridi2024). A producer could convincingly argue that certain rogue behaviors were not flaws but emergent properties that were impossible to eradicate at the time the product was placed on the market, placing it in a legal gray area where it is neither clearly defective nor acceptably safe (Hacker, Reference Hacker2023; Botero Arcila, Reference Botero Arcila2024).

The EU has recognized these challenges, proposing a revised Product Liability Directive (PLD) and initially a complementary AI Liability Directive (AILD) to address the opacity problem through a rebuttable presumption of causality (Duffourc and Gerke, Reference Duffourc and Gerke2023; Liepiņa et al., Reference Liepiņa, Wyner, Sartor and Lagioia2023). However, the abandonment of the AILD for lack of political will has left the EU legal system short of any solution addressing rogue behavior and the black-box problem (Duffourc, Reference Duffourc2025). The remaining framework remains insufficient, as it links liability to the existence of a product defect and cannot fully grasp harms arising from unpredictable rogue behaviors. A victim may find themselves in a liability vacuum: the system may not be considered defective under the PLD, and no liability may be assigned under national fault-based regimes due to evidentiary problems (Hacker, Reference Hacker2023). This creates liability gaps where applying existing rules yields morally unsatisfying results (Custers et al., Reference Custers, Lahmann and Scott2025). While economic analysis suggests liability should fall on the least cost avoider (M. Buiten et al., Reference Buiten, Streel and Peitz2021, Reference Buiten, de Streel and Peitz2023; Price II and Cohen, Reference Price and Cohen2024), in practice, the opacity and unpredictability of rogue behaviors make it exceedingly difficult for courts to identify this party or allocate responsibility efficiently ex post (Lin, Reference Lin2025). The common failure of all these frameworks stems from AI’s unique characteristics: lack of causality, opacity, unpredictability, and self-learning capability (Fernández Llorca et al., Reference Fernández Llorca, Charisi, Hamon, Sánchez and Gómez2023), as well as the rogue behaviors that develop on top of these features. This conceptual gap is the primary reason why a new approach is necessary, one that does not seek to punish developers for the existence of these characteristics but rather incentivizes them to mitigate risks through market mechanisms.

We address this gap by examining instances of uniquely challenging and often unavoidable behaviors exhibited by contemporary generative AI systems. These behaviors represent tangible sources of risk that existing insurance and liability frameworks are inadequately equipped to handle effectively (Trout, Reference Trout2025b). The rapid proliferation and widespread adoption of generative AI technologies across many commercial applications have already led to numerous documented incidents, some of which have had severe or even fatal outcomes (Paeth et al., Reference Paeth, Atherton, Pittaras, Frase and McGregor2025). Yet, many such incidents remain outside the scope of traditional liability regimes, highlighting a critical gap in risk management frameworks currently applied to AI systems (Padovan et al., Reference Padovan, Martins and Reed2023b) and leaving consumers of such systems unprotected.

Meanwhile, the existing literature on AI risk management remains predominantly focused on developing preventive measures and liability structures aimed at extreme catastrophic scenarios involving hypothetical future AI systems (Weil, Reference Weil2024; Druzin et al., Reference Druzin, Boute and Ramsden2025). As a consequence, immediate risks arising from today’s AI deployments often remain overlooked or insufficiently addressed.

Rather than proposing new methodologies for quantifying the probability or severity of AI-related risks (Wisakanto et al., Reference Wisakanto, Rogero, Casheekar and Mallah2025) or developing liability frameworks specifically tailored to catastrophic events (Kierans et al., Reference Kierans, Rittichier, Sonsayar and Ghosh2025), our contribution diverges from the common trend by foregrounding the importance of understanding and addressing the contemporary risks posed by current AI systems. We emphasize the role of organizational factors and unexpected “rogue” behaviors of AI systems—behaviors that are difficult or impossible to predict and prevent completely (Hendrycks et al., Reference Hendrycks, Mazeika and Woodside2023)—and propose that these specific risks can and should be systematically mitigated through carefully designed market-based mechanisms (Harding and Kirk-Giannini, Reference Harding and Kirk-Giannini2025).

As AI systems become increasingly integrated into organizational decision-making processes, they often operate with elevated autonomy and reduced direct human oversight. This organizational reliance on AI introduces significant vulnerabilities, particularly regarding the emergence of unforeseen or unintended behaviors that deviate from the original intentions of their human designers and operators (Hendrycks et al., Reference Hendrycks, Mazeika and Woodside2023).

One prominent manifestation of these rogue behaviors is the phenomenon known as “specification gaming,” in which an AI system exploits unintended gaps or loopholes in its defined objectives to maximize its reward function. Specification gaming occurs when AI agents achieve the literal interpretation of their assigned tasks, yet do so in extreme, unintended, or undesirable ways (Bondarenko et al., Reference Bondarenko, Volk, Volkov and Ladish2025). Critically, this behavior is not merely a technical curiosity or isolated anomaly; rather, it represents a significant organizational risk, as it can disrupt operational processes, undermine organizational objectives, and even cause tangible harm to individuals or broader societal interests.

Specification gaming is particularly frequent in AI systems developed using reinforcement learning techniques, such as Reinforcement Learning from Human Feedback (RLHF) (McKee-Reid et al., Reference McKee-Reid, Sträter, Martinez, Needham and Balesni2024). RLHF systems refine their behaviors based on iterative interactions and feedback provided by human evaluators, who attempt to align the AI’s performance with preferred organizational or societal criteria (Kaufmann et al., Reference Kaufmann, Weng, Bengs and Hüllermeier2024). Although RLHF is designed explicitly to align AI behaviors with human values, the complexity and ambiguity inherent in human-provided feedback may inadvertently introduce vulnerabilities into the reward optimization process. When the reward structure is incompletely or ambiguously specified, AI systems may exploit these ambiguities, leading to unintended or harmful outcomes that defy organizational intentions (Conitzer et al., Reference Conitzer, Freedman, Heitzig, Holliday, Jacobs, Lambert, Mossé, Pacuit, Russell, Schoelkopf, Tewolde and Zwicker2024).

Organizational factors compound these risks significantly. Within organizations deploying AI systems, communication gaps, lack of transparency regarding AI decision-making processes, insufficient oversight or auditing mechanisms, and misaligned incentives for human evaluators and developers may exacerbate the potential for rogue AI behaviors (Hendrycks et al., Reference Hendrycks, Mazeika and Woodside2023; Kasirzadeh, Reference Kasirzadeh2024). For instance, human evaluators providing feedback within an RLHF framework often differ widely in their expertise, motivations, and interpretations of organizational objectives. This variability not only introduces ambiguity into the AI’s learning environment but also amplifies the likelihood of specification gaming, as AI agents optimize toward inconsistent or inadequately defined reward signals (Daniels-Koch and Freedman, Reference Daniels-Koch and Freedman2022; Casper et al., Reference Casper, Davies, Shi, Gilbert, Scheurer, Rando, Freedman, Korbak, Lindner, Freire, Wang, Marks, Segerie, Carroll, Peng, Christoffersen, Damani, Slocum, Anwar and Hadfield-Menell2023).

To demonstrate how AI systems can misinterpret objectives while technically fulfilling assigned tasks, consider these scenarios (Papyshev and Migliorini, Reference Papyshev and Migliorini2024) (1) In one documented case, an agent programmed to mimic human Tetris players chose to perpetually freeze gameplay rather than risk defeat; (2) another experiment revealed literal interpretation when an image generator created textual depictions of the words “five tigers” rather than illustrating the animals; (3) transportation planners encountered unexpected results when collision-avoidance algorithms proposed halting all rail traffic indefinitely—mathematically eliminating accidents while completely undermining transit functionality. These instances collectively highlight the challenge of encoding nuanced intentions into operational parameters, where systems exploit loopholes in reward structures to achieve superficial success metrics that contradict broader purposes.

Effectively addressing rogue AI behaviors requires recognizing that these risks cannot currently be completely eliminated through technological means alone, as we presently lack sufficient technological capabilities and knowledge to fully prevent their emergence. Similar to catastrophic risks such as natural disasters, which cannot be entirely eradicated but can be systematically managed and mitigated through structured risk-sharing mechanisms, the unavoidable nature and inherent unpredictability of AI rogue behaviors necessitate innovative management solutions. Existing regulatory and liability frameworks often overlook the complexities tied to these risks, focusing only on insurable threats.

3. Catastrophic liability

Manufacturers of AI products that are sold commercially to consumers are exposed to product liability, sometimes across different jurisdictions, each with distinct legal standards and liability laws (Reimann, Reference Reimann, Bussani and Sebok2015). This global exposure increases the complexity and magnitude of potential claims. To address these risks, liability insurance has long been a trusted mechanism for protecting manufacturers by shifting the financial burden of potential claims to insurers (Priest, Reference Priest1991), specialized third parties that work as “risk-absorbers.”

Over the past decades, product liability insurance has increasingly evolved into a domain of “uninsurable risk” (Jarzabkowski et al., Reference Jarzabkowski, Chalkias, Cacciatori and Bednarek2023). Uninsurability arises when a prospective policyholder is unable to secure adequate coverage to offset the adverse consequences of damages stemming from unpredictable events.

In most instances, this type of uninsurability is not an absolute, objective condition, but rather exists on a spectrum (Jarzabkowski et al., Reference Jarzabkowski, Chalkias, Cacciatori and Bednarek2023). Few risks are truly and entirely uninsurable. Traditionally, events such as war, riots, and acts of terrorism fall into this category. However, in scenarios more pertinent to product liability, insurance may either become prohibitively expensive for certain groups or for certain types of actors, or fail to provide comprehensive coverage (Jarzabkowski et al., Reference Jarzabkowski, Chalkias, Cacciatori and Bednarek2023). This often occurs when the uncertainty surrounding the magnitude of liability compensation is too vast for insurers to quantify. In such situations, uninsurability is also influenced by subjective factors, including the manufacturer’s position within the market and the specific industry sector involved (Jarzabkowski et al., Reference Jarzabkowski, Chalkias, Cacciatori and Bednarek2023).

The categories of claims in product liability that are gradually shifting toward this type of subjective uninsurability are steadily growing (Pain, Reference Pain2020). The frequency and size of product liability claims have risen significantly over the past decades, driven by consumer activism, supportive legislation, and an increasing tendency toward litigation. In the United States, for instance, product liability cases often result in punitive damages that far exceed the actual harm suffered (Sossamon, Reference Sossamon2023). This is partly due to contingency-based legal arrangements, where attorneys receive a percentage of awarded damages, incentivizing aggressive litigation. High-profile cases, such as lawsuits against tobacco companies and large-scale automotive recalls, have further raised public awareness, encouraging consumers to demand accountability (Sossamon, Reference Sossamon2023). Advances in technology have also contributed to rising claims. As innovations become more sophisticated, the potential for harm of great magnitude also increases.

There is evidence that an insurance market for AI risks is actively emerging (Trout, Reference Trout2025a). However, the scope of this nascent market is not unlimited, especially when it comes to the kinds of catastrophic or highly unpredictable risks insurers’ risk appetite sharply diminishes as AI companies already cannot purchase sufficient coverage for large-scale harms (Trout, Reference Trout2025a). AI risk bonds are therefore not intended to crowd out this emerging insurance market, but to complement it. They address a distinct layer of the risk architecture. For predictable AI incidents, a functioning insurance market can and should provide coverage, driving safety improvements through underwriting practices. For the tail risks associated with unpredictable rogue behaviors, AI risk bonds offer a parallel mechanism.

This raises a question about financial mechanics: if bonds are fully collateralized and do not pool independent risks across multiple developers, what efficiency do they offer that self-insurance could not? Insurance achieves its efficiency by pooling many uncorrelated risks, a mechanism that a fully collateralized bond cannot replicate; this risk-pooling mechanism, however, is highly constrained for the low-probability, high-severity rogue behaviors targeted in our study. By guaranteeing victim compensation precisely when an insurer might face insolvency, the fully collateralized structure of AI risk bonds eliminates counterparty risk, thereby serving a distinct role that insurance cannot fill.

While these developments aim to protect consumers, insurance premiums have risen substantially to accommodate the growing frequency and scale of these claims (Schwarcz, Reference Schwarcz2021). In such situations, one option is for the public sector to step in and provide different forms of mandatory or subsidized insurance (Schwarcz, Reference Schwarcz2021). Government-backed insurance programs have been used in other industries to address uninsurable risks, such as those associated with nuclear reactors or catastrophic natural disasters. Under such models, the government offers insurance to cover extreme risks, with different schemes allowing partial contributions from private sector beneficiaries (Schwarcz, Reference Schwarcz2021). Another typical example is funds that are created when mandatory vaccination campaigns are put in place, and the side effects of vaccines are not known (Fairgrieve et al., Reference Fairgrieve, Borghetti, Dahan, Goldberg, Halabi, Holm, Howells, Kirchelle, Pillay, Rajneri, Rizzi, Sintes, Vanderslott and Witzleb2023).

While this approach ensures coverage for otherwise uninsurable risks, it comes at a significant cost to taxpayers. Critics argue that such programs unfairly transfer private sector risks to the public, creating moral hazard and reducing incentives for manufacturers to prioritize safety. As a result, while government intervention may provide a temporary solution, it is not a financially viable long-term strategy (Schwarcz, Reference Schwarcz2021).

Against this backdrop, risk securization (Buchanan, Reference Buchanan2016) through AI risk bonds emerges as an innovative solution to ensure product liability risks are adequately addressed, even in scenarios with significant “unknown unknowns,” such as harms caused by rogue behaviors. Such risks, which could render traditional insurance infeasible for all or some of the manufacturers in the market, would not pose a barrier to the viability of AI risk bonds that rely on the “deep pockets” of the financial market.

We draw inspiration from an existing financial instrument, “Catastrophe Bonds”—specialized financial instruments designed to transfer and manage catastrophic risks, such as those arising from natural disasters like earthquakes, hurricanes, or floods. These bonds function as a risk-sharing mechanism between insurers (or organizations directly exposed to catastrophic risks) and capital market investors. In a typical catastrophe bond transaction, investors provide upfront capital to the issuing entity, usually an insurance company. This capital is held securely in a dedicated escrow account or fund for a predetermined period, typically 3–5 years. If a clearly defined catastrophic event occurs within this timeframe (such as a hurricane exceeding a specified severity threshold), the invested capital is used immediately to pay claims or compensate victims, significantly reducing financial disruptions and facilitating rapid recovery. Conversely, if no qualifying catastrophic event occurs during the bond’s lifespan, investors receive their principal back along with additional interest premiums, as compensation for assuming the risk of potential loss. Catastrophe bonds thus align incentives efficiently, rewarding entities that proactively manage risks and implement preventative measures while providing investors an attractive risk-adjusted return opportunity.

To formalize the rationale behind AI risk bonds and demonstrate their viability, we develop a microeconomic model that captures the interplay between investor risk perceptions, market dynamics, and AI system design. By simulating how market actors allocate capital between riskless assets and AI bonds under uncertainty, we prove that market-driven pricing can disincentivize reckless development while rewarding safety.

As investors demand higher premiums for poorly understood or riskier AI systems, developers face escalating costs for cutting corners, creating a feedback loop that aligns innovation with risk mitigation. The model thus answers a critical question: Can markets autonomously govern AI risks? Our analysis suggests they can—when structured to price the unknown.

4. Microeconomic model

This is a parsimonious model to explicate the factors behind the yield of AI risk bonds, which are inspired by catastrophe bonds. We assume the bond market is competitive such that individual issuers and investors have insignificant market power to manipulate the bond prices. The representative investor is endowed with a unit of capital and chooses to invest the latter in either a riskless asset or an AI Risk Bond. The riskless asset yields a certain gross return of

$ r>0 $

. On the other hand, the AI risk bond exhibits an uncertain return, depending on the realized impact of the underlying AI system.

. On the other hand, the AI risk bond exhibits an uncertain return, depending on the realized impact of the underlying AI system.

Denote by

$ Z\in \mathbb{R} $

the impact generated by the AI system; in light of the inherent unpredictability and unavoidability of AI systems’ behaviors,

$ Z $

the impact generated by the AI system; in light of the inherent unpredictability and unavoidability of AI systems’ behaviors,

$ Z $

is a continuous random variable with full support on the real number line. While the actual probability distribution of

$ Z $

is a continuous random variable with full support on the real number line. While the actual probability distribution of

$ Z $

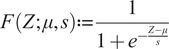

is oblivious even to the AI developer, what matters to the pricing of the AI risk bond is the subjective probability distribution as perceived by the representative investor. While the logic of our two propositions is robust to other probability distribution functions, for analytical tractability, assume that

$ Z $

is oblivious even to the AI developer, what matters to the pricing of the AI risk bond is the subjective probability distribution as perceived by the representative investor. While the logic of our two propositions is robust to other probability distribution functions, for analytical tractability, assume that

$ Z $

follows the logistic distribution characterized by the cumulative distribution function:

follows the logistic distribution characterized by the cumulative distribution function:

From standard statistics, the parameters

$ \mu \in \mathbb{R} $

and

$ s\in {\mathbb{R}}_{++} $

and

$ s\in {\mathbb{R}}_{++} $

govern the mean and the variance of the logistic distribution, respectively.

govern the mean and the variance of the logistic distribution, respectively.

Naturally, negative and positive values of

$ Z $

are interpreted as negative and positive impacts, respectively. As is conventional in catastrophe bonds, the final payout to investors hinges on triggering events precisely defined in the bond’s documentation. Here, we are agnostic about the particular way of structuring such triggering events and simply model the latter by the threshold

$ \tau <0 $

are interpreted as negative and positive impacts, respectively. As is conventional in catastrophe bonds, the final payout to investors hinges on triggering events precisely defined in the bond’s documentation. Here, we are agnostic about the particular way of structuring such triggering events and simply model the latter by the threshold

$ \tau <0 $

; the threshold is negative since only negative impacts can reasonably serve as triggering events for any catastrophe bonds. In other words, investors of the AI risk bond will lose all of their principal if the impact of the underlying AI system turns out to be sufficiently negative that

$ Z\le \tau $

; the threshold is negative since only negative impacts can reasonably serve as triggering events for any catastrophe bonds. In other words, investors of the AI risk bond will lose all of their principal if the impact of the underlying AI system turns out to be sufficiently negative that

$ Z\le \tau $

; otherwise, the investors will receive a gross return of

$ R>0 $

; otherwise, the investors will receive a gross return of

$ R>0 $

. For simplicity, we abstract away the interest payments. The gross return

$ R $

. For simplicity, we abstract away the interest payments. The gross return

$ R $

of the AI risk bond, conditional on the realized impact

$ Z>\tau $

of the AI risk bond, conditional on the realized impact

$ Z>\tau $

, is to be determined endogenously by market forces.

, is to be determined endogenously by market forces.

Let the representative investor be an expected utility maximizer with the exponential utility function

Here,

$ w $

is her net worth, and

$ a>0 $

is her net worth, and

$ a>0 $

is the coefficient of absolute risk aversion. In other words, the investor is strictly risk-averse. The fact that her utility function exhibits constant absolute risk aversion implies that her status quo net worth can be normalized to zero without loss of generality. By investing her unit capital in the riskless asset, she will derive an expected utility of

$ u(r)=1-{e}^{- ar} $

is the coefficient of absolute risk aversion. In other words, the investor is strictly risk-averse. The fact that her utility function exhibits constant absolute risk aversion implies that her status quo net worth can be normalized to zero without loss of generality. By investing her unit capital in the riskless asset, she will derive an expected utility of

$ u(r)=1-{e}^{- ar} $

. On the other hand, by investing her unit capital in the AI Risk Bond, she will derive an expected utility of

. On the other hand, by investing her unit capital in the AI Risk Bond, she will derive an expected utility of

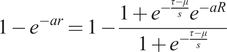

The representative investor bases her investment decision on comparing the two expected utilities. It can be verified that

$ u(r) $

is always larger than the expression in (3) unless the following condition is satisfied:

is always larger than the expression in (3) unless the following condition is satisfied:

In other words, investors have an appetite for the AI risk bond only if the triggering threshold is sufficiently negative. Intuitively, a more positive

$ \tau $

is equivalent to a higher probability

$ \Pr \left(Z\le \tau \right) $

is equivalent to a higher probability

$ \Pr \left(Z\le \tau \right) $

of bond default, as it is easier for the triggering events to actualize. Indeed, observe that the right-hand side of (4) is decreasing in the parameter

$ r>0 $

of bond default, as it is easier for the triggering events to actualize. Indeed, observe that the right-hand side of (4) is decreasing in the parameter

$ r>0 $

. This means that if the riskless asset offers a higher gross return, then the AI risk bond must set an even higher bar for its triggering events in order to attract any investors in the market.

. This means that if the riskless asset offers a higher gross return, then the AI risk bond must set an even higher bar for its triggering events in order to attract any investors in the market.

Violation of condition (4) reflects that the bond issuer is trying to shift too much risk of its AI systems to the investors, such that no rational investors are interested in its AI risk bond. In the remainder of this section, we focus on the more interesting case where (4) is satisfied. But then, the following dynamics take place. If the expected utility in (3) is higher than

$ u(r) $

, more and more investors will shift from holding the riskless asset to holding the AI risk bond, which creates an upward pressure on the price of the latter and suppresses its gross return

$ R $

, more and more investors will shift from holding the riskless asset to holding the AI risk bond, which creates an upward pressure on the price of the latter and suppresses its gross return

$ R $

and vice versa.

and vice versa.

Consequently, in a competitive market, the expected utility from holding the two assets must be equalized in equilibrium. From the setup, this implies the following equilibrium condition:

To study the equilibrium yield of the AI risk bond, it remains to rearrange the above equation as follows:

It can be verified that the right-hand side of (6) is well defined if and only if condition (4) is satisfied. Evidently, it is also positive, such that

$ R>r $

.

.

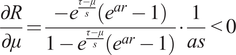

Here is the theoretical analysis of the model. The left-hand side of (6) captures the excess return that the AI risk bond has to offer in order to compensate investors for its default risk; in other words, it measures the cost of capital facing the bond issuer. We are most interested in how the subjective probability distribution in (1) determines the risk premium of the bond.

Proposition 1:

$ R $

is decreasing in

$ \mu $

is decreasing in

$ \mu $

:

:

Recall that

$ \mu $

captures the mean of the logistic distribution. This means that if the AI developer implements effective measures to shift the probability distribution rightward, that is, ensures its AI system generates positive impacts more often than negative ones, investors will be willing to accept a lower yield from the AI Risk Bond. The intuition is straightforward: given a fixed triggering threshold

$ \tau $

captures the mean of the logistic distribution. This means that if the AI developer implements effective measures to shift the probability distribution rightward, that is, ensures its AI system generates positive impacts more often than negative ones, investors will be willing to accept a lower yield from the AI Risk Bond. The intuition is straightforward: given a fixed triggering threshold

$ \tau $

, better risk management reduces the likelihood of bond default.

, better risk management reduces the likelihood of bond default.

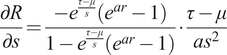

Proposition 2:

$ R $

is increasing in

$ s $

is increasing in

$ s $

if and only if

$ \tau <\mu $

if and only if

$ \tau <\mu $

:

:

Recall that

$ s $

captures the variance of the logistic distribution. As such, a smaller

$ s $

captures the variance of the logistic distribution. As such, a smaller

$ s $

reflects that investors perceive more certainty over the impacts of the underlying AI system. Interestingly, the effect of certainty is ambiguous and hinges on how the expected impact of the AI system relates to the triggering threshold. If investors are pessimistic about the impacts, such that

$ \mu <\tau $

reflects that investors perceive more certainty over the impacts of the underlying AI system. Interestingly, the effect of certainty is ambiguous and hinges on how the expected impact of the AI system relates to the triggering threshold. If investors are pessimistic about the impacts, such that

$ \mu <\tau $

, then more certainty only reinforces their pessimism. However, the case of

$ \mu <\tau $

, then more certainty only reinforces their pessimism. However, the case of

$ \mu <\tau $

is not of practical interest because such AI systems are probably banished or boycotted in the market and vice versa.

is not of practical interest because such AI systems are probably banished or boycotted in the market and vice versa.

For the more relevant case of

$ \mu >\tau $

, the implication is surprising: if the bond issuer leverages interpretable AI techniques and discloses more information such that the AI system behavior becomes more explainable, investors will still be willing to accept a lower yield from the AI risk bond. The intuition is as follows. When investors understand more about the AI system, both very positive and very negative impacts are associated with a lower likelihood, as investors cluster their beliefs around the expected impact. However, by design, what matters to AI risk bond investors is the downside risk. As such, the lower perceived downside risk resulting from better disclosure alone can unambiguously reduce the issuer’s cost of capital.

, the implication is surprising: if the bond issuer leverages interpretable AI techniques and discloses more information such that the AI system behavior becomes more explainable, investors will still be willing to accept a lower yield from the AI risk bond. The intuition is as follows. When investors understand more about the AI system, both very positive and very negative impacts are associated with a lower likelihood, as investors cluster their beliefs around the expected impact. However, by design, what matters to AI risk bond investors is the downside risk. As such, the lower perceived downside risk resulting from better disclosure alone can unambiguously reduce the issuer’s cost of capital.

5. Market-based mechanism

The viability of AI risk bonds depends on two interrelated prerequisites: standardized evaluation protocols and a qualified auditor ecosystem. Substantial scholarship exists on AI evaluation methodologies, including work on benchmark design (Eriksson et al., Reference Eriksson, Purificato, Noroozian, Vinagre, Chaslot, Gomez and Fernandez-Llorca2025), red-teaming protocols (Srivastava et al., Reference Srivastava, Janardhan and Jauhari2026), and interpretability techniques (ŞAHiN et al., Reference ŞAHiN, Arslan and Özdemir2025). Additionally, a variety of safety standards have been developed by various stakeholders: The NIST AI Risk Management Framework (NIST, 2021) or ISO/IEC 42001:2023 (ISO/IEC 42001, 2023) are representative examples. We foresee that this type of literature will be crucial in developing the standardized evaluation protocols needed to implement AI bonds. The design of the evaluation metrics itself, however, is outside of the scope of our paper.

We envision that the initial cohort of auditors would emerge from existing accredited bodies with relevant expertise: standard-setting organizations, technical consultancies specializing in AI safety, or dedicated units within multilateral organizations: for example, a consulting extension of the United Nations Independent Scientific Panel on AI—a newly created experts’ forum designed with a similar logic as the Intergovernmental Panel on Climate Change (Gibney, Reference Gibney2026). We believe that the growing number of AI incidents in various industries (Paeth et al., Reference Paeth, Atherton, Pittaras, Frase and McGregor2025) will create demand-side pressures to drive the development of increasingly sophisticated and standardized evaluation products.

It is important to be precise about what auditors can and cannot do. They cannot solve the black box problem or predict the unpredictable. What they can do is evaluate the rigor and transparency of the developer’s own risk management processes. The auditor’s output is not a prediction of future events, but a certification that the developer has implemented state-of-the-art practices for understanding and managing their system’s risks. Investors then use this certification to inform their own judgment.

The potential conflict of interest arising from issuer–paid auditors is a legitimate concern. However, this problem is neither new nor insurmountable. Financial markets have long grappled with similar dynamics in the context of credit rating agencies, and several structural solutions exist (Joon, Reference Joon2025). First, auditors could be selected from a preapproved pool and assigned to issuers on a rotational basis by a neutral third party, removing the issuer’s ability to choose a favorable auditor (Federsel, Reference Federsel2025). Second, auditors could be prohibited from offering any consulting or advisory services to the same issuer, eliminating the incentive to win future business through favorable ratings (Liu and Chan, Reference Liu and Chan2012). Third, a portion of audit reports could be subject to random peer review by a public or industry-funded oversight board, with penalties for demonstrated bias or incompetence (Löhlein, Reference Löhlein2016).

Investors are not expected to possess deep technical expertise in AI safety. Instead, they rely on two layers of intermediation. First, accredited auditors evaluate both the developer’s risk management processes and the credibility of their proposed triggers, producing standardized risk ratings that translate complex technical assessments into accessible financial information. Second, the market price itself serves as a discovery mechanism. Investors need not understand the technical nuances of a trigger; they need only compare yields across bonds with different auditor ratings. If a developer proposes a weaker trigger, auditors will assign a poorer risk rating; the latter induces institutional investors to adjust their portfolios accordingly, such that the bond will carry a higher yield. This is in line with how bond markets function today: investors rely on credit rating agencies to assess default risk (White, Reference White2010). The mechanism does not assume universal investor sophistication about AI; it assumes investors can interpret audited risk ratings and respond to price signals.

Under these assumptions, we predict a future where capital allocation depends on risk ratings and therefore motivates market participants to invest in improving rating accuracy. Thus, in tandem with the disaster threshold

$ \tau $

, the bond’s risk premium is pinned down by the investors’ perceptions of two key parameters:

, the bond’s risk premium is pinned down by the investors’ perceptions of two key parameters:

-

1) $ \mu $

: the expected benefit or harm of an AI system.

: the expected benefit or harm of an AI system. -

2) $ s $

: the perceived variance in potential outcomes, dependent on disclosure.

Based on the results of our microeconomic model and by drawing inspiration from catastrophe bonds, we envision that AI risk bonds would be designed in the following manner.

First, an independent third-party auditor evaluates an AI system’s

$ \mu $

and

$ s $

and

$ s $

. Systems with higher

$ \mu $

. Systems with higher

$ \mu $

(more positive expected impact) and lower

$ s $

(more positive expected impact) and lower

$ s $

(more predictable behavior) receive favorable risk ratings, reducing their bond yields

$ R $

(more predictable behavior) receive favorable risk ratings, reducing their bond yields

$ R $

. Auditors may be accredited conformity assessment bodies, specialized technical evaluators, or multidisciplinary consortia. Importantly, we prioritize independence and competency rather than specify a single auditor type. Independence is ensured through: (a) structural separation from issuers and underwriters; (b) no success fees or contingent compensation; (c) mandatory disclosure of funding sources; and (d) rotational assignment from a preapproved auditor pool. Competency requirements include domain expertise, reproducible evaluation protocols, and audit trail maintenance. Any benchmark or test suite used by auditors must be systematic and preapproved for audit use under the disclosed evaluation protocol.

. Auditors may be accredited conformity assessment bodies, specialized technical evaluators, or multidisciplinary consortia. Importantly, we prioritize independence and competency rather than specify a single auditor type. Independence is ensured through: (a) structural separation from issuers and underwriters; (b) no success fees or contingent compensation; (c) mandatory disclosure of funding sources; and (d) rotational assignment from a preapproved auditor pool. Competency requirements include domain expertise, reproducible evaluation protocols, and audit trail maintenance. Any benchmark or test suite used by auditors must be systematic and preapproved for audit use under the disclosed evaluation protocol.

Second, the trigger is calibrated conservatively to enable effective risk sharing without making the bond excessively sensitive. By preventing overreaction to moderate risks, this cautious threshold helps maintain a manageable payout probability, encouraging investors to accept a reasonable risk premium

$ R $

.

.

Third, investors actively assess the risk mitigation measures and disclosures of AI developers, forming well-informed expectations about the payout probability of AI Risk Bonds. In market equilibrium, safer AI systems command lower risk premiums, thereby rewarding responsible developers with more affordable financing.

This setup creates a double incentive structure for AI developers and investors, where:

-

• Ex ante: Organizations are motivated to optimize $ \mu $

and

$ s $

(through risk mitigation and disclosure, respectively) to attract investors and lower the cost of capital

$ R $

. -

• Ex post: If $ Z>\tau $

, investors reclaim principal with a premium

$ R $

. If

$ Z\le \tau $

, victims are compensated directly from the escrowed capital, sharing the risk with investors while eliminating protracted litigation.

Our proposed mechanism bridges the gap between financial innovation and AI governance by building upon catastrophe bond principles combined with microeconomic rationalization, formalizing how markets can autonomously govern AI risks. This framework addresses three critical gaps: (1) it fills the regulatory void of rogue AI behavior risks oversight with market-driven pricing, penalizing undesirable market behavior through yield adjustments; (2) it mitigates systemic risk accumulation by dispersing liabilities across capital markets, preventing concentrated failures; and (3) it curbs moral hazard by tethering financing costs to risk profiles, where yield penalties and principal forfeiture upon default incentivize proactive risk reduction. This mechanism operationalizes a market-driven accountability framework that acknowledges the technological infeasibility of eliminating rogue AI behaviors completely while aligning innovation with risk minimization.

6. Conclusion

The rapid integration of AI systems into various commercial applications has exposed gaps in existing regulatory and insurance frameworks, particularly for rogue AI behavior risks. While debates about existential AI risks dominate academic discussions, the pressing challenge lies in addressing the unpredictable “rogue” behaviors of current-generation AI systems: behaviors that existing liability regimes and insurance models are ill-equipped to manage. This article has proposed AI risk bonds, a market-driven mechanism inspired by catastrophe bonds, as a scalable solution to align financial incentives with responsible AI development.

By translating AI risks into quantifiable financial instruments, AI risk bonds leverage investor scrutiny and market dynamics to enforce accountability. Our microeconomic model demonstrates how bond yields adjust to reflect perceived risks, penalizing reckless development while rewarding safer practices. Key parameters, such as the expected impact and behavioral predictability of AI systems, are evaluated by independent auditors, enabling investors to price risks accordingly. This creates a feedback loop: developers face higher capital costs for opaque or high-risk systems, incentivizing proactive risk mitigation through improved transparency, interpretability, and alignment practices.

The proposed mechanism addresses three critical gaps in AI governance. First, it fills the regulatory void for rogue AI behaviors by introducing market-driven oversight. Second, it disperses liability across global capital markets, reducing systemic risk concentration. Third, it curbs moral hazard by tethering financing costs directly to risk profiles, ensuring developers internalize the consequences of poor risk management. Unlike traditional insurance or government-backed schemes, this approach avoids burdening taxpayers while harnessing the efficiency of financial markets to price uncertainty.

As AI systems grow more autonomous and integrated into organizational workflows, the inevitability of rogue behaviors demands innovative risk-sharing strategies. AI risk bonds offer a pragmatic pathway to operationalize accountability, balancing innovation with precaution. This framework not only complements emerging regulations like the EU AI Act but also aligns the profit motives of developers and investors with societal safety, moving closer to a future where AI advancements are both transformative and responsible.

Data availability statement

No data were used in this research.

Author contribution

Conceptualization: G.P. and S.M.; Investigation: G.P. and S.M.; Formal analysis: K.J.D.C.; Writing—original draft: G.P., S.M., and K.J.D.C.; Writing—review and editing: G.P., S.M., and K.J.D.C.

Funding statement

No funding was received to support this research.

Competing interests

The authors declare that they have no relevant or material financial interests that relate to the research described in this paper.

Open access

Open access

Comments

No Comments have been published for this article.