This first empirical section examines the contradictory impulses involved in managing hype. Across two chapters, it explores the dual role that industry analysts play in moderating hype. On one hand, analysts scrutinise exaggerated claims to curb unrealistic expectations; on the other, they amplify the claims they deem most promising. Chapter 4 – The Second Most Important Pitch – focuses on entrepreneurial storytelling (Lounsbury & Glynn, Reference Lounsbury and Glynn2001, Reference Lounsbury, Gehman and Glynn2019). Entrepreneurship research adopts a ‘strategic perspective on hype as a form of storytelling’ (Wadhwani & Lubinski, Reference Wadhwani and Lubinski2025, p. 2). It demonstrates how entrepreneurs secure stakeholder support for their ventures through ‘projective’ narratives (Kalvapalle et al., Reference Kalvapalle, Phillips and Cornelissen2024). O’Connor (Reference O’Connor, Hjorth and Steyaert2004, p. 120) encapsulates this idea: ‘Before a company exists, it is a story about an imagined future.’

However, as start-ups transition from pitching to investors to engaging with industry analysts, we demonstrate that their narratives must evolve. Entrepreneurs, therefore, undergo a strategic reorientation – shifting from imaginative, aspirational pitches to grounded, detail-rich accounts that meet analysts’ evidentiary expectations. Our findings show that analyst briefings can be emotionally charged encounters that expose start-ups to a steep learning curve. Many ventures struggle to satisfy analysts’ stringent evaluation criteria; these gatekeepers routinely probe, problematise, and deconstruct founders’ narratives. When a story appears overly imaginative or lacks operational detail, analysts demand substance, precise timelines, and credible implementation plans.

Chapter 5 – Cool Vendors – investigates how industry analysts identify and amplify the narratives of select disruptive start-ups by bestowing labels such as ‘Cool Vendor’, ‘Innovator’, or ‘Market Disruptor’. These designations endorse ventures that challenge traditional assumptions and have the potential to transform market practices, thereby boosting their visibility and legitimacy. The chapter addresses a paradox: analysts are typically critical gatekeepers, yet they actively promote the very ventures they evaluate. Drawing on the French sociologist François Vatin (Reference Vatin2013), we distinguish between evaluation (assessing value) and valorisation (creating value) to explain this behaviour. By amplifying credible narratives while curbing unsustainable ones, analysts operate in both capacities – gatekeeping and promoting. This dual role illustrates a new model of how hype functions as a legitimising mechanism.

An entrepreneur starts a venture. It’s a software firm. It has been relatively successful. It’s a growing venture in the space and challenging the incumbents. The next crucial step is to win coverage from industry analysts. The entrepreneur approaches the industry analyst briefing like the investor pitch to ‘sell the vision’ of the venture. However, the briefing did not go as planned; the analysts seemed unconvinced by what they heard. The meeting becomes antagonistic. The entrepreneur starts with: ‘Hey, how are you? I am glad I have the chance to talk to you’, and quickly says, ‘I do not understand why you do not see this’. According to an analyst relations (AR) expert who advises entrepreneurs on how to brief industry analysts, it typically ‘takes less than 30 minutes’ for these initial meetings to break down, and this is not a one-off but ‘happens every single time’. This scenario illustrates how entrepreneurs encounter industry analysts who now serve as critical gatekeepers in the digital economy. These gatekeepers represent the new business of hype – professional evaluators who commodify the interpretation of emerging technologies for clients.Footnote 1

Crafting an appealing story is crucial when creating a new venture (Zilber, Reference Zilber2007; Bartel & Garud, Reference Bartel and Garud2009; Wry et al., Reference Wry, Lounsbury and Glynn2011; Garud & Giuliani, Reference Garud and Giuliani2013). Stakeholders can be unfamiliar with ventures (Lounsbury & Glynn, Reference Lounsbury and Glynn2001), especially technology ventures, where products are often complex and the opportunity difficult to grasp (Martens et al., Reference Martens, Jennings and Jennings2007). The task for the entrepreneur is to construct a narrative that frames the venture to build understanding and mobilise support (Davidsson, Reference Davidsson2015). Studies to date have provided rich insights into the storytelling that entrepreneurs carry out with initial audience groups, such as investors (Lounsbury & Glynn, Reference Lounsbury, Gehman and Glynn2019).

Less frequently considered is how these storytelling processes are extended to a later-stage audience (Lounsbury & Glynn, Reference Lounsbury, Gehman and Glynn2019). It is recognised that if the venture is to continue surviving and growing, it will need the support of a range of stakeholders (Fisher et al., Reference Fisher, Kotha and Lahiri2016). Yet, the storytelling that builds comprehension in an early-audience group may be less compelling in enrolling a future audience. As our discussion above of the entrepreneur attempting to brief an industry analyst shows, there are potential obstacles inherent in attracting a new audience. The ‘pitch’ that worked well with the investor does not seem to work as well with this audience group. Nor does the entrepreneur appear to understand what this new stakeholder is looking for and how to go about the ‘briefing’ (Überbacher et al., Reference Überbacher, Jacobs and Cornelissen2015; O’Neil & Ucbasaran, Reference O’Neil and Ucbasaran2016).

There is a clear gap in the existing literature regarding how entrepreneurs extend storytelling processes beyond an early-stage audience to a new, later-stage audience group (Überbacher, Reference Überbacher2014; Fisher, Reference Fisher2020). Research has suggested that different audiences will have different expectations of narrative, and different ways of assessing them (Fisher et al., Reference Fisher, Kuratko, Bloodgood and Hornsby2017). However, it is unclear how entrepreneurs go about meeting the demands of new audience groups. To explore this important phenomenon, we ask: How do entrepreneurs revise processes of storytelling to meet the expectations of a later-stage audience, and how does this audience group probe and challenge the storytelling processes put forward such that they require revision?

We examine this issue through qualitative, inductive research of the way entrepreneurs brief industry analysts. Industry analyst briefings have become a mandatory stepping stone for emerging ventures in the digital sector (Petkova et al., Reference Petkova, Rindova and Gupta2013). As discussed in Chapter 1, these analysts function as new gatekeepers in the hype ecosystem, shaping which ventures gain visibility. Based on this research, we develop a model of how entrepreneurial storytelling processes are extended to this new audience. Our analysis suggests that entrepreneurs struggle to move beyond the initial investor pitch and understand what is expected in industry analyst briefings. However, they can still repair the connection with this group by revising their narratives. We also demonstrate that, while entrepreneurs benefit from garnering a new audience’s support, this audience group can subject storytelling to greater scrutiny and additional probing, which in turn influences how ventures evolve.

4.1 Entrepreneurial Storytelling

Early studies have laid the groundwork for a perspective that views stories as playing a vital role in processes that enable new ventures to develop and survive (Hjorth & Steyaert, Reference Hjorth and Steyaert2004). As such, storytelling could be considered central to entrepreneurship (Lounsbury & Glynn, Reference Lounsbury and Glynn2001, Reference Lounsbury and Glynn2019; Bartel & Garud, Reference Bartel and Garud2009; Wry et al., Reference Wry, Lounsbury and Glynn2011; Garud & Giuliani, Reference Garud and Giuliani2013). Entrepreneurial storytelling has been defined as ‘accounts that legitimate individual entrepreneurs to networks of investors, competitors, and visionaries, who make resource decisions and take strategic actions based upon what the stories mean to them’ (Lounsbury & Glynn, Reference Lounsbury and Glynn2001, p. 545). Storytelling endeavours to make the ‘unfamiliar familiar’ by conceptualising the new venture in a way that is more readily ‘understandable and thus legitimate’ (Lounsbury & Glynn, Reference Lounsbury and Glynn2001, p. 549). This focus on future-oriented narrative echoes our analytical framework for hype (Chapter 2), where we described how entrepreneurs’ promissory stories help create and organise emerging technology fields. Storytelling can include the spontaneous accounts that form part of ‘everyday conversations’ through to the more ‘scripted narratives’ familiar to formal business presentations (Martens et al., Reference Martens, Jennings and Jennings2007, p. 1109).

Storytelling is seen as particularly relevant in the case of technology entrepreneurship (Martens et al., Reference Martens, Jennings and Jennings2007), which, because it is often ‘knowledge-intensive’, is more difficult for stakeholders to understand (Doganova & Eyquem-Renault, Reference Doganova and Eyquem-Renault2009, p. 1567). Scholars acknowledge that future-oriented and more promissory narratives are particularly crucial, as they highlight the possibilities surrounding a technology (Zilber, Reference Zilber2007). As Gartner (Reference Gartner2007) writes, to construct an entrepreneurial narrative is to generate ‘hypotheses about how the future might look and act’ (p. 614). Similarly, Chiles et al. (Reference Chiles, Bluedorn and Gupta2007) explain how stories ‘create opportunities through expectations of an imagined future’ (p. 467). Through writing the story, the entrepreneur comes to ‘imagine the opportunity for novel ventures’ (Cornelissen & Clarke, Reference Cornelissen and Clarke2010, p. 539). As we argued in Chapter 2, such future-oriented, promissory storytelling is a core mechanism of technology hype, performing and shaping expectations in nascent markets.

4.1.1 Adjusting Storytelling for Later-Stage Audiences

There are calls to broaden entrepreneurial storytelling research (Lounsbury & Glynn, Reference Lounsbury and Glynn2019). So far, the literature has primarily focused on how narratives are developed to engage early-stage audience groups, such as investors (Überbacher, Reference Überbacher2014). However, as ventures move beyond the initial birth and growth stages, it is recognised that they require the support of further resource providers (Navis & Glynn, Reference Navis and Glynn2011). Lounsbury and Glynn (Reference Lounsbury, Gehman and Glynn2019) argue that it is essential to distinguish between the early stages, where entrepreneurs craft stories to build ‘the legitimate distinctiveness of the new venture’ (p. 18) and later stages, where storytelling can appeal to resource providers who endow them with broader ‘assets’ (p. 23). Similarly, Fischer et al. (Reference Fischer, Kotha and Lahiri2016) point to the importance of researching how a venture transitions through ‘different stages of development’ (p. 401) as the dynamics surrounding its interactions with audiences will change at each growth phase. Building on Chapter 3’s discussion of how ventures navigate uncertainty, we see here that entrepreneurs must adapt their narrative logics to different stakeholder expectations.

Given the importance of enrolling further stakeholders, scholars have begun to enquire whether a story that interests one audience will appeal to others (Überbacher, Reference Überbacher2014; Fischer et al., Reference Fischer, Kotha and Lahiri2016, Reference Fisher, Kuratko, Bloodgood and Hornsby2017). Implicit in early research was the assumption that stakeholders would have the same or similar expectations of the entrepreneurial story (Überbacher, Reference Überbacher2014). More recently, however, it has been posited that, as audiences change, expectations will likely change as well. For instance, Fischer et al. (Reference Fisher, Kuratko, Bloodgood and Hornsby2017) point to how different audiences will likely apply other evaluative criteria, or ‘logics’, when assessing ventures (p. 68). Such logics are non-trivial as they will encourage audiences to emphasise different things when judging ventures. As a result, there have been calls for research to study the evaluation of ventures by other audience groups to shed further light on this crucial issue (Überbacher, Reference Überbacher2014).

Alongside changing audience expectations, existing research identifies the importance of studying how entrepreneurs learn to satisfy new audiences when storytelling. Understanding how entrepreneurs revise their narratives is significant because, as Lounsbury and Glynn (Reference Lounsbury and Glynn2001) point out, storytelling must ‘align with audience interests’ (p. 550). As emphasised in Chapter 2’s actor-centred view of hype, entrepreneurs must tailor their narratives to each audience’s logic; if not, audience interest wanes. Alternatively, if a story fails to resonate with key audiences, it will decrease their ‘interest and commitment’ (Navis & Glynn, Reference Navis and Glynn2011, p. 490; see also Giorgi, Reference Giorgi2017). Fischer et al. (Reference Fischer, Kotha and Lahiri2016) discuss the demise of a promising digital venture that became ‘distracted and confused’ (p. 395) by the different expectations of a later audience, which, they argue, ultimately led to its downfall.

Yet, despite its evident importance, we know little about how entrepreneurs carry out storytelling processes with a new audience. We cannot assume they will possess the necessary competencies to gain the attention of a new audience group. As Überbacher et al. (Reference Überbacher, Jacobs and Cornelissen2015) write, it may be that they would have to learn and gain the ‘requisite cultural awareness and skills’ (p. 945). However, it is unclear how entrepreneurs learn to meet the expectations of new audiences. Understanding how cultural competences are developed remains ‘empirically underexplored and conceptually under-theorised’ (Überbacher et al., Reference Überbacher, Jacobs and Cornelissen2015, p. 945).

We also lack an understanding of how a later-stage audience responds to storytelling, which perhaps reflects the emphasis in the current literature on ‘black-boxing’ the interactions between entrepreneurs and audiences (Lounsbury et al., Reference Lounsbury, Gehman and Glynn2019). This gap reflects a broader need, identified in Chapter 1, to understand how new gatekeepers (beyond early investors) influence entrepreneurial narratives. Previous studies have focused on the entrepreneurs’ role, characterising them as ‘skilled cultural operatives, able to influence how their audience understands the promise of their new venture, (Lounsbury & Glynn, Reference Lounsbury and Glynn2001, p. 559). As Gegenhuber and Naderer (Reference Gegenhuber and Naderer2019) argue, however, this implicitly portrays the audience as ‘passive recipients of the entrepreneurial story’ (p. 154), which means we lack insights into the specific demands an audience might have of processes of storytelling (Gehman & Soubliere, Reference Gehman and Soublière2017).

Although little explicit focus has been on how entrepreneurs extend storytelling processes to a later-stage audience, two studies describing ‘revised’ storytelling offer potential insights. O’Connor (Reference O’Connor, Hjorth and Steyaert2004, p. 120) presents the case of an internet start-up that ended up with a ‘transitional story’ after it was required to recraft its ‘visionary’ narrative to a more conventional ‘marketplace’ story. Garud et al. (Reference Garud, Schildt and Lant2014b) recount how a group of internet entrepreneurs engaged in storytelling to enrol the support of funders, but these stakeholders raised questions about story ‘plausibility’ (p. 1485).

Crucially, both studies emphasise how stories can be ‘challenged’. O’Connor (Reference O’Connor, Hjorth and Steyaert2004, p. 120) reveals how a new investor considered a venture’s story to offer little more than an ‘armchair perspective’ and suggested an alternative. In Garud et al.’s (Reference Garud, Schildt and Lant2014b) case, whilst seemingly there had been little initial evaluation of the storytelling process, it was when entrepreneurs missed critical milestones that stakeholders held them ‘accountable’, which required ‘revised storytelling’ (p. 1485). These examples of narrative revision echo the idea from Chapter 3 that entrepreneurs face dilemmas as producers of hype; they must learn when to pivot or tighten their pitch. Though there has been progress in the literature, it remains unclear how entrepreneurs revise storytelling processes to meet new audience expectations or how a further audience group might probe and challenge storytelling processes to the extent that they require revision. These topics merit further investigation.

4.1.2 A Note on Analyst Briefings

This chapter is based on a study at the analyst relations (AR) agency in North America we will call ‘Sunshine’. We negotiated permission to conduct a four-week-long observation at Sunshine, which typically facilitated three or four briefings each week between entrepreneurs and industry analysts. We were able to observe ten such briefings. Also, we were given access to a further seven previously recorded briefings stored in an online repository. All briefings were conducted online, and each one lasted around 60 minutes. Participating ventures were between four and ten years old. While no longer in the early stages of formation, they were still very much constructing their stories through addressing such questions as ‘who we are’ and ‘what we do’ (Navis & Glynn, Reference Navis and Glynn2011, p. 479).

Alongside briefings, we could witness and participate in the various ‘prep’ sessions, which would go into a detailed discussion of how entrepreneurs could improve their story’s telling. Moreover, when briefings finished, it was common practice for the entrepreneur and AR expert to stay on the line to perform a short ‘debrief’ of what could be changed or improved next time. These observations produced insights that we followed up in informal conversations and more formal interviews, which we describe below. For instance, one critical insight that emerged from observations was that entrepreneurs had little or no understanding of what industry analysts were looking for in these briefings, creating numerous challenges and problems.

Throughout the book, we refer to interviewees using the following codes: A1, A2, A3, etc. for analysts; AR1, AR2, AR3, etc. for AR professionals; and V1, V2, V3, etc. for venture representatives. Each chapter is designed to be read as a standalone study, so an identifier such as A1 in Chapter 4 does not necessarily refer to the same individual as A1 in Chapter 5.

4.2 Entrepreneur Presents an Initial Story

For entrepreneurs, industry analyst briefings are not an easy task. For instance, there is nowhere near the same level of guidance one can find for investor pitches (Clarke et al., Reference Clarke, Cornelissen and Healey2019). Winning the attention of an industry analyst firm is a challenging and lengthy endeavour? Such firms are inundated with briefing requests from up-and-coming enterprises. For instance, Gartner reports that its analysts sit through 12,000 briefings yearly (Hare, Reference Hare2020). Moreover, if the venture wants to maintain analyst interest, it must brief them every few months and then continue to engage regularly with them, year after year. Our empirical data demonstrate that briefings would start with entrepreneurs selling their vision, but interactions would quickly turn sour as they found opposition to their story.

4.2.1 Selling the Vision

During briefings, entrepreneurs would attempt to ‘come out strong’, capture the analyst’s attention, and ‘try to keep it’ (V1, prep). During these moments, analysts often seemed distracted by other tasks, such as checking email (V1, prep). As a result, entrepreneurs would attempt to capture the analyst’s attention by starting with projections of how their technology would be developed, for example, by discussing roadmaps, forecasts of the potential market size, and estimates of competition.

One venture, for instance, evangelised around its vision to revolutionise lending in developing countries: ‘We’re doing this to start establishing the creditworthiness of … populations that are highly off … the grid in terms of the traditional credit bureaux and data sources’ (V12, briefing).

Another entrepreneur was excited to showcase his new image-recognition technology demo: ‘We have a proof of concept, and we’ll have to reinforce that we are showing a future at this point and roadmap stuff, but actually, we have a demo that I first got to see last week which I have been excitedly showing people’ (V1, prep). Products were always ‘next generation’ (V1, prep) or ‘next frontier’ (V2, prep) and deliberate analogies with high-profile digital giants were typical: ‘Our product is Google on top of social media’ (V1, prep).

Throughout briefings, there was an inevitable discussion of displacement and disruption. Characteristically, entrepreneurs were confident about how their products measured up against competitors. The following, though bullish, was not rare: ‘We really feel like we are far ahead of where [large rival 1 and 2], or even [very large rival 3] are, and we know we are already displacing those vendors in many, many cases’ (V4, briefing). On hearing how a venture that had only been in existence a few years was displacing much larger rivals, the AR expert working with this venture leaned over to our fieldworker and whispered, ‘That is a big claim!’ (V4, briefing).

Briefings, almost always, made mention of ‘strategic partnerships’. Reference to a partnership would encourage the analysts to probe further: ‘What’s … the name of the partner you’re working with?’ (V1, briefing). Entrepreneurs would then take the opportunity to expand. One venture, for instance, advertised its growing partnership with ‘BigTech’: ‘We’re doing a lot with [BigTech] on a strategic nature, to make sure that we are treated as their most strategic partner level … that we have alignment within their R&D team as well as within the various product teams’ (V4, briefing).

4.2.2 Finding Opposition from the Analyst

Our informants described how it was customary for entrepreneurs to start with ‘passion’ and to be ‘aggressive when it’s about telling the story’ (AR3, interview), but these meetings could become antagonistic. Expecting briefings to be similar to investor pitches, entrepreneurs were enthusiastic and animated about what they were saying. An AR expert gives his perspective on what typically went wrong:

These up-and-coming entrepreneurs, they’re … quoting about ‘changing the world’, and ‘offering something totally new’. They believe that’s so true to the core of their heart. And to have an analyst show scepticism about either their strategy or their market, it is to call their baby ugly! When [analysts] make these claims and make these judgements, it is not just talking about facts, it is striking at the very heart of how [the entrepreneurs] define themselves.

Another AR expert described how entrepreneurs approached briefings with the idea that they had to ‘win the meeting’ (AR3, interview). This informant describes how:

[Entrepreneurs] are very used to being leaders within these firms. They are salespeople… They sell their ideas. They sell their firm. They sell their concept. They sell themselves to investors… So, their obsession with trying to win the meeting creates bad behaviour.

A further AR expert points to how ‘there is a huge difference between pitching your business and briefing an analyst’ (AR4, interview). She talked about how briefings could become ‘salesy’ where ‘the speaker is not speaking to the analyst’ (AR4, interview). Instead, ‘they’re broad-brushing as though they’re trying to pitch their business’ (AR4, interview).

However, analysts did not appreciate ‘being sold to’ (AR4, interview). According to informants, it was common for entrepreneurs to pitch their business and for analysts, in turn, to respond negatively. The AR expert goes on:

An analyst is going to get really annoyed with this, because usually when you’re selling, you’re pitching, you’re talking about how ‘you’re the best’, ‘you’re the only one’, ‘you’re the greatest’. And so, analysts’ red flags will go up. They’ll start being super-sceptical. They’ll stop believing what you’re saying.

Another AR expert talked us through what he described as a typical first-briefing scenario, where an entrepreneur, having received a critical response from an analyst, begins to question directly, and even disparage, the analyst: ‘So at once, [the entrepreneur will] assault [the analyst’s] judgement, assault their wisdom and assault their integrity’ (AR3, interview). Such emotional and conflict-filled displays were far from isolated examples. According to the AR expert, ‘this happens every single time’ (AR3, interview). A further AR expert tells us how ‘[Y]ou would not believe the number of conversations we start where …we’re repairing relationships’ (AR6, interview).

The above exemplifies the struggle around what we call ‘selling the vision’. The entrepreneurs, who think they have a strong story to tell, act out their vision of the venture, but this audience does not appear to share their passion and enthusiasm. After these initial episodes, entrepreneurs are often persuaded to change their approach. An AR expert will ‘prep’ the entrepreneur, which includes telling them what the analyst is looking for and how to respond. Recollecting his difficulty in prepping one particular entrepreneur, an AR expert discusses how he tries persuading entrepreneurs to keep passion and aggression in the background:

I think that the assertive, aggressive technique, it’s really interesting. What [entrepreneurs] want to do is [be] aggressive and assertive about arguing the theme of the story. So, [they] are storytellers. When somebody says, ‘I will force [entrepreneurs] to be aggressive when it’s about telling the story’, like ‘No, no, no, no, no Ted stop there’.

The AR expert encourages entrepreneurs to be open to the analyst’s perspective and to modify behaviour and expectations through the course of the meeting:

I don’t let them be aggressive [as] we play on this idea that [analysts] don’t change their mind very often. So, there’s this idea that if you come in with black when they’re white, they’re probably not going to come half your way. But if you come in with pink or light blue, that’s closer to the white.

We have demonstrated a gap between the entrepreneur’s story and that expected by the analyst. The ensuing repair work – an iterative negotiation between entrepreneurs and market gatekeepers – is part of the broader ‘taming hype’ process explored in this book, through which exaggerated claims are managed and recalibrated. We now consider what analysts look for by examining how they evaluate the story.

4.3 Gatekeeper Probes and Problematises the Story

In theory, what analysts attempt, namely verifying the future potential and survivability of a new venture, including the plausibility of its technology and market projections, is difficult or even impossible (Navis & Glynn, Reference Navis and Glynn2011). The initial challenge is to identify the most promising opportunities in the rapidly changing innovation landscape, which involves a relatively high degree of uncertainty and ambiguity. Will the venture be ‘disruptive’? Alternatively, could it be a flop? How are analysts to make sense, so they can advise clients? It appears that they have well-established methods and techniques for conducting what is commonly referred to in the investor pitch as due diligence (Huang & Pearce, Reference Huang and Pearce2015). Below, we show that briefings are organised as an escalating process whereby analysts often lie in wait for entrepreneurs before getting to the truth.

4.3.1 Analysts Lie in Wait for Entrepreneurs

Attending briefings is a routine part of the analyst day. They listen to several in a single sitting, and it is common for them to come off one call, pause for a few seconds and scan through a new set of PowerPoint slides, before entering a further briefing. Here, an analyst describes his reasons for attending briefings: ‘I want to learn what [ventures] do, so we have one-hour briefings. I had one yesterday… I had one this morning, where we are trying to understand more about their business’ (A1, interview). During briefings, analysts will sit, listen, and take notes to understand what they are being told. It could be that later they will be required to relay this information to their clients: ‘I have to do the research. I have to do the vetting of that vendor. And I have to be somewhat confident that they’re going to deliver, because you’re going to get [my clients] reading my stuff and buying IT, based on my recommendations’ (A2, interview).

Briefings are organised in a temporal arrangement to produce an ever-increasing process of evaluation. As indicated, these are not one-off events. The entrepreneur will potentially build a long-term relationship with the analyst, meaning that they could be briefing them many times over the next few years. Therefore, during the initial stages, many analysts are relaxed and restrained, knowing they can return to scrutinise the story later.

An analyst describes how ‘[W]e are quite easy-going in the first one or two. We let people flow their own way. But usually, by the time we have a second or third one … you go: “Wait a minute. Let’s just cut to it now…”’ (A1, interview).

When listening to a venture outline its vision and offering, analysts restrict themselves to questions of understanding. After this initial courtship period, the analyst begins ratcheting up the process. They will go through the story ‘with a fine-tooth comb’ (A1, interview). An analyst describes how:

I am trying to bet on who is going to survive to some degree ─ viability becomes important. I am trying to bet on who has commitment from the service providers and systems integrators. I am trying to look at the management team. I am trying to look at the product itself.

Analysts were highly skilled at holding stories up to the light and talked of how easy it was to spot when a venture was inflating its position. Vendor exaggeration could be counterproductive since it only invites the analyst to ‘poke around’. Here, an analyst talks about how ventures should approach briefings:

Don’t overstate your competitive position … [it] turns into again another opportunity just to poke around on that, because, if it doesn’t seem believable, the analytic brain says, ‘let me go figure out where that’s wrong, because it doesn’t seem right what I’m hearing’.

Another analyst talked of how they could quickly ‘cross-check’ because the venture’s customers were also often their customers:

There was a vendor briefing and they tell me they have 500 customers and there is 50 people in the company. Who are you kidding with that? What they don’t know is that most of their clients are our clients too. So, for us, it is very easy to cross-check.

The robustness and veracity of a story are developed over a staged process. Each progressive stage places the ventures under more scrutiny, thus forming an escalating process. Entrepreneurs have much to gain and indeed lose from briefings. Hence, as the analysts themselves recognised, the situation could induce ‘overstating’ and ‘misrepresentation’, raising the question of how they dealt with stories that seemed implausible.

4.4 Getting to the Truth

Analysts described how they placed great importance on building good relationships with entrepreneurs but that these interactions could, at times, become practically and morally fraught. Their experience told them entrepreneurs would dress things up: ‘They always want to give you an impression that they do much more than they really do’ (analyst 6, interview). The analyst role, by contrast, was ‘to get to the truth’: ‘Some of the vendors are telling the truth; some of the vendors are exaggerating’ (A7, interview).

An analyst describes how: ‘We are quite cynical, and the reason we are quite cynical is that most people are lying to us … so the question is, how do you get behind the lies to find out what is really going on?’ (A1, interview).

Therefore, during briefings, analysts will mobilise mechanisms to evaluate claims, which include acting out moral frames to get behind ‘the façade’ as they see it. Similarly, ‘proof’ was also a standard part of their lexicon. An analyst describes how: ‘[O]ne kind of value is not just being different but being able to prove it… Prove your differentiation… If we’re going to say that, let’s have some proof to it, let’s have some metrics, let’s have some facts’ (A3, webinar). However, this raises the question of what counts as proof in these situations.

Upon hearing a questionable claim, an analyst may not immediately challenge the entrepreneur but instead go away and verify the information before returning to it in a later briefing. To see through stories, analysts performed something akin to ‘proxy ethnographies’ (Knorr Cetina, Reference Knorr Cetina2010). When entrepreneurs began mentioning a prestigious ‘partner’ or ‘customer’, the analyst would ask for names so that those cited could be contacted.

Customers and partners are seen to offer some validity to the emerging story, but it is not that analysts have blind faith in them, as they expect ‘prepping’ and ‘staging’. To get around this, analysts are on the lookout for impromptu or unsupervised gatherings. An analyst discusses how, when a venture invited him to a conference event, he took the opportunity to meet informally with its partners and customers. Such casual exchanges, known as ‘personal briefings’, were rich in information:

I just went around talking to customers and partners… I organised some of the meetings in advance, some I did on the sly, but it was like a series of one [to one] personal briefings on channel partners which I don’t think was quite what [the venture] intended. I think they were hoping to have me sit in front of [the CEO] and be bored.

The analyst portrays their role as one where they take pride in not being taken in by entrepreneurs. Thus, they will listen with interest during briefings and later hold the venture accountable for the claims made. We describe below one such episode involving a venture (V4), where analysts had uncovered what they believed was a potentially misrepresented claim, which was then relayed to the venture’s CEO, prompting him to undertake corrective action.

An AR expert recounts how V4 had claimed to have established a ‘strategic partnership’ with [BigTech], and this helped it not only win analyst attention but make it onto a high-profile ranking: ‘[V4] shouldn’t have made the [ranking]. They made the [ranking] because [the analysts] saw them as a disruptive technology, [but] what they’re doing is they are piggybacking off a lot of [BigTech] initiatives’ (V4, prep). However, the analysts were now beginning to pour water on V4’s claim that it had indeed established a strategic partnership with BigTech. When the analysts approached BigTech for confirmation of this partnership, they received a surprising response. An AR expert recounts the words of the analyst: ‘You know, I asked people at [BigTech] about you, because I wanted some of that third-party validation that you do what you say you do, and no one’s even heard of you!’ (V4, prep). BigTech’s failure to corroborate V4’s claim of a strategic partnership caught the CEO off guard. The AR expert recounts the conversation:

[V4’s CEO] was like: ‘Well, who are you talking to, because [BigTech] is so big?’ And [the analysts] poked holes in [V4’s] market strategy because they said, ‘[BigTech] is not selling you … so why is [BigTech] not going to market with you in their back pocket?’ and ‘why are you not doing … joint pitches?’ And so that’s where [the CEO] was like, ‘Erm’. … (V4, prep)

A few months later, in a subsequent briefing, the analysts would return to this issue. The analyst asks: ‘[T]he thing I’m kind of curious about is this relationship that you’ve formed with [BigTech], more detail about that would be good’ (V4, briefing). In the preceding months, the venture had spent considerable time working to improve and repair this part of the story, which required significant effort to establish the strategic partnership discussed. The AR expert describes: ‘[S]o, [V4’s] been working really hard on beefing their [BigTech] support so that they have that ecosystem that’s helping to sell, and then [the analysts] will see that, so this is going to hopefully impress [them]’ (V4, prep). During the briefing, the CEO tells the analysts how: ‘We weren’t necessarily that well-known within the [BigTech] ecosystem … so we spent really the last three or four months working closely … on the [BigTech] side … [so] that we could get to the [BigTech] executive team and talk to them’ (V4, briefing). The V4 CEO points to how they will be doing joint pitches with BigTech at a forthcoming event: ‘[W]e are now going to be in keynote presentations and other highly-visible spots within the [BigTech] event where [BigTech] are highlighting the nature of our relationship’ (V4, briefing). The repair work satisfies the analyst, and the matter is dropped.

4.5 Entrepreneur and AR Expert Adjust and Reconcile the Story

We found that, over time, the briefing process can become a source of frustration for entrepreneurs. The disappointment is that, while the evaluation is being ratcheted up, they can often be in the dark about how the analyst perceives them, which prompts them to attempt to elicit feedback from the analyst. Moreover, fear of attracting disapproval or losing analyst interest could tempt the entrepreneur to engage in revised storytelling.

4.5.1 Drawing Out Feedback from the Analyst

The briefing was a highly asymmetric process. While it was common for the analyst to probe and quiz the entrepreneur continually, this was not a two-way interaction: the analysts limited the amount of comment and feedback.

Feedback and advice are sold as part of a service called ‘client enquiry’. An analyst describes this service but also how it plays out in practice: ‘Briefings are not a forum for analysts to provide feedback. True, we are told not to. Most analysts, I think, will buckle towards the end, I usually do, and give a little bit of feedback, though we’re not going to give very much’ (analyst 5, webinar).

The lack of feedback could create problems for entrepreneurs and advisors because it meant there were few indicators, from one briefing to the next, as to how things were progressing. Did the analyst believe they were onto something? Might they be losing interest or, worse still, unconvinced by what they were hearing? For instance, after one such briefing, an AR expert admits how: ‘I did not get anything, and I do not know what to talk about next’ (V1, debriefing).

What should entrepreneurs do when feedback is in such short supply? Some worked this into briefing routines. For instance, those advising made clear to first-timers their one-directional nature. A neophyte is told how: ‘If you hear silence on the other end of the line, it’s a good thing. [The analyst] takes a lot of notes and he doesn’t feel the need to say, uhuh, uhuh, uhuh…. But if he doesn’t seem extremely engaged, it’s actually the opposite’ (V1, prep). Advisors would also coach entrepreneurs on the importance of drawing the analyst out, to solicit clues to understand whether they liked what they were hearing:

We take her time, go slow, ask for her feedback throughout. This will be a good sense of her priorities moving forward to, so there are things that she wants to see that we … can’t show. Those will probably be important in the next [ranking] moving forward, so we can inform the product team or at least build a story around those things we can’t do yet.

Some entrepreneurs and their advisors took this further by attempting to disrupt the standard briefing practice. In an example that shows that storytelling is a material phenomenon enacted by material practices as much as by narratives, we saw that some had developed methods for drawing the analyst out. An analyst informant describes the ‘card-trick’, where entrepreneurs go through their PowerPoint slide-deck at a rapid pace, hoping the analyst will ask them to return to a slide that catches their attention:

I’ve seen multiple companies do that where they literally have 20 slides and go shuffle, shuffle really fast, and they’re pretending they’re going to get to slide 20 and spend an hour on slide 20, but actually, what’s really going on is they’re going: ‘Which one is it you want?’ And then you go: ‘That one’. It’s laying out a menu, and you go ‘that one’.

The card trick’s materiality is crucial because it upsets the analyst’s usual reticence and provokes a visible display of interest that can then be used to adjust stories.

4.5.2 Revising Storytelling

The importance of shifting towards the analyst was a common theme throughout fieldwork. An AR expert explains to an entrepreneur during a prep session how ‘[t]he number-one objective, when you are introducing yourself to analysts, is to get yourself in a box as quickly as possible’ (V1, prep). A further AR expert describes how the goal is to ‘create alignment with [the analyst]’ (V2, prep). Advisors will gather ‘intel’ to understand a specific analyst’s ‘POV – point of view’ (AR4, interview). They will then ‘talk about how that [POV] either aligns or doesn’t align with the [entrepreneur’s] perspective and … try to find a point of commonality [to] start the briefing with’ (AR4, interview). Some tell the entrepreneur to put themselves in the shoes of the analyst:

Imagine you are an analyst with a [ranking] coming up, and you’ve got your [category], you’re trying to do a find and fill like you’re playing bingo. Do you think they are structuring the information in a way that’s gonna be – obviously, it’s a very easy way for them to tell their story – but is it an easy way for the analyst to consume?

During fieldwork, we observed numerous instances where ventures were encouraged to reframe their narratives to better align with audience expectations and address areas of concern. There appeared to be not one but an array of potential adjustments. One venture ‘pivoted’, for instance, after receiving decisive feedback from analysts. Relations with the analyst had got off to a bad start as a venture informant recounts: ‘When we started talking to [analyst firm], it was like we were Martians. It would be like, ‘Oh, that’s interesting. It never occurred to me that somebody could do it that way. How nice of the Martians. Let us know what you think of our world”’ (V16, interview). The informant goes on to recount how the analyst’s feedback became a ‘turning point’, where he suggested they reframe entirely how they think of themselves.

Another venture maintained ‘a façade’ where it spoke differently to different audiences. An informant describes how they differentiated between the analyst community and the ‘broader world’:

How it works is that we have a concept which aligned very tightly with one of [the analyst firm’s] concepts… So what we do is, when we are pitching and briefing and talking to those analysts that work in that area, we alter our language to match what they are saying, even though the concept is the same, we change our language to match theirs. But we don’t necessarily do that to the sort of broader world.

Because it was being passed from one analyst to another, another venture reverted to ‘dressing up’ (AR-G, interview) (e.g. trying out different versions of its story) to attract interest. Developing an ambitious artificial intelligence (AI) solution for the ‘underbanked’ (V12, briefing), its product crossed ‘four or five different [analyst] categories’ (AR7, interview), which meant whenever it approached an industry analyst firm, their request for a briefing was rejected. This led them to ‘rewrite’ their story:

We submitted it [to the analyst firm]…. And it went to AI people, and they turned it down. So, then we rewrote it, resubmitted it, and it went to financial services people, and they turned it down. And then we rewrote it and resubmitted it, and it went to … communications providers, and then it went through there.

Such rewrites required producing a credible account of their product, together with their understanding of the analyst categories. This AR expert recounts the process of adjustment necessary: ‘So, rewriting the story as if you’re a completely different company. In a certain sense, you have to look at the [categories] that they’ve declared…. And so, it’s that dressing up’ (AR7, interview).Footnote 2

4.6 Discussion: Extending Storytelling to Industry Analysts

While Cultural Entrepreneurship scholarship has offered rich insights into how storytelling can persuade and enrol an early-stage audience, such as investors, there has been less focus on how entrepreneurs extend processes of storytelling to a later-stage audience group, like industry analysts (Fischer et al., Reference Fischer, Kotha and Lahiri2016; Lounsbury & Glynn, Reference Lounsbury and Glynn2019). Based on this, our chapter offers a model that maps and theorises how entrepreneurs revise storytelling processes to meet this new audience’s demands and expectations.

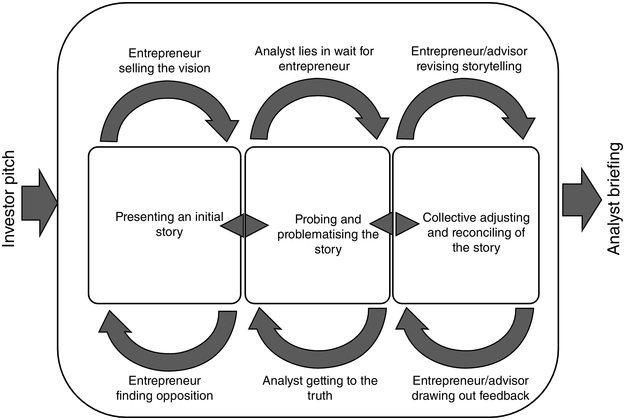

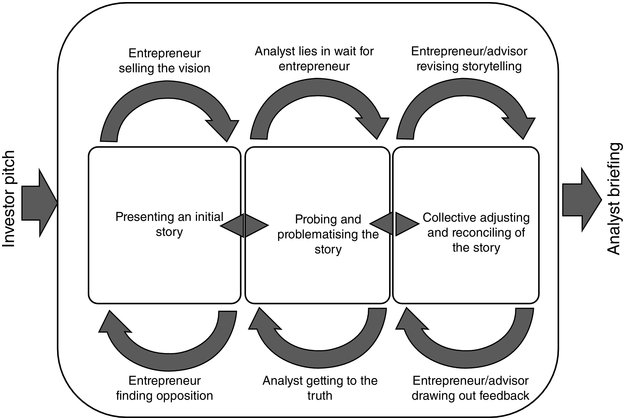

We found that entrepreneurs struggle to move beyond the initial investor pitch and understand what is expected in industry analyst briefings. But they can still repair the connection with this audience through revised storytelling. Our main contribution to research on entrepreneurial storytelling is to reveal and theorise the stages through which entrepreneurs brief a later-stage audience through presenting an initial story that had worked well with a previous group, how industry analysts then engage in probing and problematising the story, which led to collective adjusting and reconciling of the story to meet new audience demands. Below, we describe the key stages and their various steps that lead entrepreneurs to extend and translate storytelling processes to garner the attention of a new audience group (see Figure 4.1).

Figure 4.1 Long description

The model presents a feedback loop with three main components between the investor pitch and analyst briefing. It begins with presenting the initial story, where the entrepreneur sells the vision and is met with opposition. Probing and problematising the story follows where the analyst gets to the truth and lies in wait for the entrepreneur. The entrepreneur or advisor draws out feedback and revises the storytelling whereby it is collectively adjusted and reconciled.

We show that entrepreneurs attempt to enrol this new audience by extending the same or similar storytelling processes that had worked well with previous investor audiences, which comprised selling the vision. However, we found that interactions with this new audience often turned sour, theorised as finding opposition (see also Zilber, Reference Zilber2007). Driven by different goals and concerns, we identify that analysts probe and problematise stories through an escalating evaluation process that consists of two steps. Initially, they lie in wait for entrepreneurs, knowing that allowing them space and freedom to sell the vision would provide an opening for further interrogation. Then they carry out a second step where they expose story weaknesses and limitations, which we theorise as getting to the truth.

During the briefing process, the entrepreneur learns (O’Neil & Ucbasaran, Reference O’Neil and Ucbasaran2016) or is counselled by advisors that it is not just a matter of selling the vision but aligning with the audience’s interests (Lounsbury & Glynn, Reference Lounsbury and Glynn2001). As a result, entrepreneurs attempt what we theorise as adjusting and reconciling to consider (and perhaps even adapt to) the analysts’ prevailing view (Zuckerman, Reference Zuckerman1999). Specifically, adjusting and reconciling involves ‘drawing out feedback’ from the analyst and engaging in revised storytelling based on the entrepreneur and AR expert scrutinising and making sense of (the often limited) reaction received.

We observed how revised storytelling could take numerous forms that included: (1) ‘repair work’ (Bachmann et al., Reference Bachmann, Gillespie and Priem2015), where an entrepreneur carried out transformative changes to reverse growing analyst distrust of a potentially misrepresented claim; (2) ‘pivoting’ (Grimes, Reference Grimes2018), where a venture radically changed direction after receiving analyst feedback; (3) ‘dressing up’, where an entrepreneur drew on a range of similar but slightly modified stories to capture analyst attention (Giorgi & Weber, Reference Giorgi and Weber2015); and (4) ‘maintaining a façade of conformity’ (Hewlin, Reference Hewlin2003), where an entrepreneur told one story to analysts and a different one to other audiences.

Our interpretation of events is that while the investor pitch and industry analyst briefing appeared similar enough for the entrepreneur, the industry analyst had, in Fisher et al.’s (Reference Fisher, Kuratko, Bloodgood and Hornsby2017) terms, different ‘expectations’. This audience seemed less accepting of the more future-oriented and promissory narratives favoured by the entrepreneur (O’Connor, Reference O’Connor, Hjorth and Steyaert2004). Our chapter captures and theorises the ‘critical moment’ (Boltanski & Thevenot, Reference Boltanski and Thévenot1999) when the audiences’ different expectations become evident and explains why entrepreneurs find themselves in difficulty and discord. There was initially what Boltanski and Thevenot (Reference Boltanski and Thévenot1999) might describe as a ‘shift’ of expectations as the entrepreneurs’ ported stories honed for one audience to another group. It follows that because the investor pitch and analyst briefing expectations were mostly incompatible with one another, the entrepreneur was then required to shift between different expectations to attempt to garner the support of this new audience.

Despite the importance of extending entrepreneurial storytelling processes to a new audience (Überbacher, Reference Überbacher2014; Fischer et al., Reference Fischer, Kotha and Lahiri2016, Reference Fisher, Kuratko, Bloodgood and Hornsby2017), we know relatively little about how an entrepreneur can enrol a further audience group (Fischer et al., Reference Fischer, Kotha and Lahiri2016; Lounsbury & Glynn, Reference Lounsbury, Gehman and Glynn2019). Our chapter thus directly responds to calls for further research into the processes by which an entrepreneur might modify storytelling processes for a later-stage audience (Überbacher, Reference Überbacher2014; Fisher et al., Reference Fisher, Kotha and Lahiri2016, Reference Fisher, Kuratko, Bloodgood and Hornsby2017). Even though the transfer of a story to a new audience group has been labelled a critical entrepreneurial ‘competence’ (Überbacher et al., Reference Überbacher, Jacobs and Cornelissen2015, p. 946), research to date has not yet provided a detailed examination and theorisation of how this extension process ‘actually occurs’ (Überbacher, Reference Überbacher2014, p. 684). Nor has it examined how entrepreneurs meet the different expectations of their audiences. Some suggest that audiences apply different ‘logics’ when assessing ventures (Fischer et al., 2017, p. 68). However, studies have not thoroughly explored the complex, evolving considerations and oppositions that govern interactions between entrepreneurs and a new audience (Gegenhuber & Naderer, Reference Gegenhuber and Naderer2019; Lounsbury et al., Reference Lounsbury, Gehman and Glynn2019), as we have done here.

4.7 Struggling to Transcend the Initial Vendor Pitch

A key contribution is that we demonstrate how entrepreneurs struggle to transcend the initial investor pitch. Whereas Fisher et al. (Reference Fisher, Kuratko, Bloodgood and Hornsby2017) suggest that entrepreneurs can ‘reframe’ stories to meet different audience expectations, our findings lead us to question their assumption that frames are ‘easily adjusted’ (p. 66). In our study, it was not always the case that entrepreneurs could ‘quickly and easily change their frames’ to attract and appeal to new audiences (p. 66). Instead, our evidence hints at the presence of ‘path-dependent’ processes (Garud et al., Reference Garud, Kumaraswamy and Karnøe2010). Some entrepreneurs based their storytelling to this new audience on techniques seen as successful with earlier groups (namely, investors). Our argument echoes Mauer and Ebers’ (Reference Maurer and Ebers2006) analysis, which suggests that entrepreneurs can suffer from ‘lock-in’ (p. 277) due to their limited ability and competence to relate to later groups. Yet, we extend their focus by showing how these same path-dependency processes can apply not just to forming new audience relationships but also during storytelling processes.

4.8 Audiences of Storytelling Far from Inactive

A second contribution is demonstrating the audience’s role in shaping storytelling, which contrasts with the assumption implicit in research that audiences are ‘passive recipients of the entrepreneurial story’ (Gegenhuber & Naderer, Reference Gegenhuber and Naderer2019, p. 154). However, a unique aspect of our study is that we could study both entrepreneurs and audience simultaneously, which provided us with evidence that market gatekeeper audiences are far from inactive. Specifically, we found that by probing and problematising narratives and moving entrepreneurs through an escalating evaluation process, where the story is placed under an increasing amount of scrutiny, this audience could bring to the surface discrepancies for which the entrepreneurs would ultimately be held accountable, leading to revised storytelling.

We are not alone in highlighting these critical audience evaluations. Some studies do give importance to how audiences ‘challenge’ entrepreneurs (O’Connor, Reference O’Connor, Hjorth and Steyaert2004). Scholars (Garud et al., Reference Garud, Schildt and Lant2014b, p. 1485) point to how, as ‘milestones are missed repeatedly’, entrepreneurs can be held accountable. However, whereas previous studies have focused on how audiences become critical after entrepreneurs encounter difficulties and setbacks – what Garud et al. (Reference Garud, Schildt and Lant2014b, p. 1483) characterise as ‘commitment rather than critical evaluation’ – we demonstrate how audiences probe and problematise entrepreneurs before forming their assessment. This finding is important because it challenges the tacit assumption of previous studies (Garud et al., Reference Garud, Schildt and Lant2014b) that entrepreneurial storytelling is only episodically or exceptionally exposed to audience evaluation. We instead shift attention to an ongoing evaluation process surrounding storytelling, where audiences are active and bring significant influence to bear from the outset.

4.9 How Entrepreneurs Modify Storytelling for Later-Stage Audiences

A final contribution is to develop our understanding of how entrepreneurs adapt storytelling processes for later audiences. While it is increasingly recognised that an audience will probe an entrepreneur, especially when they transition from an early-stage to a later-stage audience, the processes of ‘replotting’ (O’Connor, Reference O’Connor, Hjorth and Steyaert2004; Garud et al., Reference Garud, Schildt and Lant2014b) have not been extensively studied and theorised. Our chapter contributes here by opening the ‘black box’ of replotting to identify the repertoire of potential revisions deployed by entrepreneurs (e.g. repair work, pivoting, dressing up, and maintaining a façade). Unpacking the replotting process is essential because it reveals the various ways an entrepreneur can modify and revise a story to manage relationships with an audience that may struggle to understand and place them within their own frames and categories.

Moreover, once we open the black box, we can demonstrate that revised storytelling can result from a direct audience challenge to a potentially misrepresented narrative. For instance, V4 revised its story following the questioning of its strategic partnership. This makes it different to entrepreneurs identified in prior work, who revised storytelling either to attract a new audience group (Fisher et al., Reference Fisher, Kuratko, Bloodgood and Hornsby2017) or because they had failed to maintain earlier promises (O’Connor, Reference O’Connor, Hjorth and Steyaert2004; Garud et al., Reference Garud, Schildt and Lant2014b). Importantly, while there was potential for this misrepresentation to be treated more seriously than mere ‘legitimacy lies’ (Rutherford et al., Reference Rutherford, Buller and Stebbins2009), we also observed that it was possible to remedy the situation.

On this occasion, where censure was anticipated, we observed that the venture in question devoted considerable effort to revising its storytelling processes. Our chapter, in this respect, responds to recent calls for further research on how a new venture might ‘mitigate’ audience threats (Fisher, Reference Fisher2020, p. 19). It also moves us beyond a dualistic view that depicts entrepreneurs as either winning audience backing or not to a more dynamic perspective that shows, for instance, how they could gain initial support but then have their story problematised and be required to reverse growing audience scepticism through revised storytelling.

4.10 Research Opportunities for Studying Briefings

We join with those reconsidering the prevailing understanding of entrepreneurs as ‘skilled cultural operatives’ (Lounsbury & Glynn, Reference Lounsbury and Glynn2001, p. 559), where it is argued that one cannot assume entrepreneurs have from ‘the outset’ (Überbacher et al., Reference Überbacher, Jacobs and Cornelissen2015, p. 945) the necessary competences to gain the support of a new audience group (see also Lounsbury et al., Reference Lounsbury, Gehman and Glynn2019). Instead, as our chapter begins to explore, entrepreneurs often start with little knowledge of a new audience and must acquire the skills and competencies to win their backing. However, more studies are required, particularly those that explore the internal dynamics within ventures as they seek to understand and meet new audience expectations. Moreover, we shed light on a case where interactions were mediated by an AR agency that guided entrepreneurs on approaching industry analysts. However, it would be helpful to study situations where no such mediation and support were available to understand whether similar or different responses would occur.

Chapter 5 extends the above analysis by shifting focus from the act of storytelling and narrative refinement to the downstream consequences of a successful briefing. Specifically, it explores how some ventures, having passed through these evaluative filters, are elevated by analysts as ‘disruptors’ through designations such as Cool Vendor, Market Disrupter, Hot Vendor, etc.

‘ABC’, a software start-up from Estonia, was selected as the preferred supplier in a procurement contest in the UK for delivering a customer relationship management (CRM) system. However, it suddenly found itself ejected from the process after the adopting organisation approached an industry analyst firm for more information about the venture. An analyst reported back that they had ‘a list of some 500 vendors of CRM, many of which [the analyst] meets regularly to track the development of their products, but [ABC] is not on the list’. The analyst suggested that if the adopting organisation bought from an ‘unknown venture’, it would be ‘taking a risk’, which led one procurement team member to ask, ‘who would sign up to a company that no one has heard of?’ (Pollock & Williams, Reference Pollock and Williams2011). This interaction underscores that industry analysts act as brokers in a market of hype – their endorsements (or omissions) effectively commodify credibility, determining which innovations gain traction in the economy of expectations.

The above example reflects a pressing problem. All ventures face the difficulty that they are unknown quantities at the outset (Fisher et al., Reference Fisher, Neubert and Burnell2021). However, they can seemingly rectify this problem in part through drawing support from ‘key resource holders’ (Lounsbury et al., Reference Lounsbury, Gehman and Glynn2019, p. 1229), such as a market gatekeeper (Plummer et al., Reference Plummer, Allison and Connelly2016; Soublière & Gehman, Reference Soublière and Gehman2020). An evaluation or endorsement from an influential gatekeeper, like an industry analyst, is critical because it is ‘linked to the likelihood of firm survival and growth’ (Navis & Glynn, Reference Navis and Glynn2011, p. 479). Scholars have noted that market gatekeeper coverage can reassure audiences about investing in or purchasing from a venture lacking a proven track record (Fischer et al., Reference Fischer, Kotha and Lahiri2016). Others have provided evidence that when gatekeeper backing is not forthcoming, it can become a block or impediment to progress (Petkova et al., Reference Petkova, Rindova and Gupta2013). For instance, if a venture does not appear on a ‘recommended vendor list’, as the example of ABC above shows, the gatekeeper will caution against it (Coslor et al., Reference Coslor, Crawford and Leyshon2020). As noted in Chapter 3, digital start-ups often turn hype into a strategic asset by targeting key audiences; here, that means utilising analyst coverage to overcome being perceived as an ‘unknown quantity’.

However, the process through which ventures gain the support of a market gatekeeper has not been fully addressed (Überbacher, Reference Überbacher2014). The literature suggests a ‘screening process’ (Petkova et al., Reference Petkova, Rindova and Gupta2008, p. 327) involving abstract ‘filtering’ and ‘selecting’ mechanisms (Petkova et al., Reference Petkova, Rindova and Gupta2013, p. 866). Still, the specific evaluative processes used by gatekeepers remain poorly understood (Überbacher, Reference Überbacher2014), which highlights the need for further investigation into how, in ‘crowded locations’ (Petkova, Reference Petkova, Barnett and Pollock2012, p. 396) with numerous ventures competing for gatekeeper attention, certain ones garner support.

The challenge of drawing gatekeeper coverage appears especially acute in the context of digital entrepreneurship. There has been a recent surge in the number of new digital ventures (Nambisan, Reference Nambisan2017; Nambisan et al., Reference Nambisan, Wright and Feldman2019), defined as ventures that have ‘digital artefacts at the core of their business model for value creation and capture’ (Lin & Maruping, 2021, p. 1). How do new digital ventures engage and benefit from market gatekeeper support? Answering this research question is crucial. It is argued that the uncertainties surrounding digital ventures differ from those of non-digital enterprises (Ingram Bogusz et al., Reference Ingram Bogusz, Teigland and Vaast2018), rendering them especially reliant on gatekeeper coverage (Von Briel et al., Reference Von Briel, Recker and Davidsson2018; Elia et al., Reference Elia, Margherita and Passiante2020).

5.1 Liability of Newness

A core insight of the new venture literature is that young enterprises suffer from the ‘liability of newness’ (Stinchcombe, Reference Stinchcombe and March1965; Bruederl & Schuessler, Reference Bruederl and Schuessler1990). Scholars have given significant attention to identifying how potential customers and others, because new ventures lack a track record, could be sceptical towards their performance and whether they can deliver the required quality in a timely manner (Fischer & Reuber, Reference Fischer and Reuber2007; Fischer et al., Reference Fischer, Kotha and Lahiri2016). Recently, it has been noted that this liability is more prominent in new technology areas or what Überbacher (Reference Überbacher2014) calls ‘high velocity environments’ as there can be a ‘rapid transformation’ (p. 685) of many different aspects, including what venture performance and quality mean. We focus below on digital ventures, as the liabilities surrounding these enterprise types are especially pronounced.

5.1.1 New Digital Ventures

In the emerging field of digital entrepreneurship, attention has recently turned to differences between digital and non-digital enterprises (Nambisan, Reference Nambisan2017). An early insight of this embryonic literature is that the liability of newness may be ‘manifested differently’ in these contexts (Ingram Bogusz et al., Reference Ingram Bogusz, Teigland and Vaast2018, p. 318; see also Srinivasan & Venkatraman, Reference Srinivasan and Venkatraman2017). It is argued that digital ventures have a ‘high propensity for radical transformation’ (Von Briel et al., Reference Von Briel, Recker and Davidsson2018, p. 284) because their products can be taken in new directions by, for instance, user innovation (Nambisan et al., Reference Nambisan, Wright and Feldman2019). Other studies suggest that ‘pivoting’, where digital technologies enable a radical change in focus, goals, or strategy, is a distinguishing characteristic of digital entrepreneurship (Ghezzi & Cavallo, Reference Ghezzi and Cavallo2020; Wagner & Som, Reference Wagner, Som and Fayolle2021). Despite progress, an important issue left unaddressed concerns how digital ventures make themselves visible and understandable to potential audiences.

Scholars have drawn attention to how digital ventures uniquely rely on gatekeeper support for building market acceptance (Elia et al., Reference Elia, Margherita and Passiante2020; Von Briel et al., Reference Von Briel, Selander, Hukal, Lehmann, Rothe, Fürstenau and Wurm2021). It has been suggested that we are witnessing the emergence of ‘an increasing number of intermediaries’ who ‘play the role of brokers’ and help digital ventures ‘reach key goals’ (Von Briel et al., Reference Von Briel, Selander, Hukal, Lehmann, Rothe, Fürstenau and Wurm2021, p. 13). Some argue that winning the support of a gatekeeper will become increasingly decisive as digital entrepreneurship continues to grow (Nambisan et al., Reference Nambisan, Wright and Feldman2019). Others point out that, as the number of new digital ventures increases (Hull et al., Reference Hull, Hung, Hair, Perotti and DeMartino2007; Hair et al., Reference Hair, Wetsch, Hull, Perotti and Hung2013), competition for gatekeeper attention will become more challenging (Nambisan et al., Reference Nambisan, Wright and Feldman2019). Others still suggest that ventures failing to win gatekeeper support will become marginalised or that hierarchies could emerge between those receiving endorsement and those ignored (Dy et al., Reference Dy, Marlow and Martin2016). However, notwithstanding calls for more research on the ‘nature of intermediaries and their impact on digital entrepreneurship’ (Von Briel et al., Reference Von Briel, Selander, Hukal, Lehmann, Rothe, Fürstenau and Wurm2021, p. 13), scholars have stopped short of examining the process gatekeepers play in the formation of new digital ventures and what a venture can do to win and harness their support.

5.2 Gatekeeper Screening Processes

Mainstream scholarship has made much progress in showing how new ventures attempt to remedy the liability of newness through ‘being selected for coverage by influential institutional intermediaries’ (Petkova et al., Reference Petkova, Rindova and Gupta2013, p. 866). Gatekeeper coverage provides valuable assurances because it is assumed that the gatekeeper has conducted some evaluation and made a favourable judgement about venture qualities and viability (Hsu, Reference Hsu2004). Gatekeepers are defined as neutral ‘third parties’ (Beckert & Aspers, Reference Beckert and Aspers2011) or ‘intermediaries’ (Bessy & Chauvin, Reference Bessy and Chauvin2013; Coslor et al., Reference Coslor, Crawford and Leyshon2020) who evaluate phenomena in which they have no stake or interest (Beckert & Musselin, Reference Beckert and Musselin2013; Khaire, Reference Khaire, Durrand, Granqvist and Tyllström2017). The most well-known gatekeepers include industry analysts (Pontikes & Kim, Reference Pontikes and Barnett2017), industry media (Vasterman, Reference Vasterman2005; Kennedy, Reference Kennedy2008; Byrne & Giuliani, Reference Byrne and Giuliani2025; Magalhães & Smit, Reference Magalhães and Smit2025), and critics (Coslor et al., Reference Coslor, Crawford and Leyshon2020). Research shows that the gatekeeper performs essential functions such as ‘enhancing the visibility’ of ventures and ‘mediat[ing] information flows’ between it and other stakeholders (Pollock & Gulati, Reference Pollock and Gulati2007, p. 347). Ventures that win gatekeeper attention fare better as they channel market attention to those covered (Petkova et al., Reference Petkova, Rindova and Gupta2013). Failing to attract coverage will mean ventures will ‘not only be perceived as of lower quality’, but they could also be ‘less visible’ (Pollock & Gulati, Reference Pollock and Gulati2007, p. 347) since they are not part of industry discussions. However, the fact that gatekeepers have become an important staging post for new ventures echoes the puzzle we highlighted in the previous chapter. In Chapter 4, we showed that analyst briefings are a crucial site where start-ups repair their narratives to meet analysts’ criteria. Here we pick up on that by asking how, in practice, an analyst chooses one venture over another.

Studies have noted how gatekeepers have an internal ‘screening process’ (Petkova et al., Reference Petkova, Rindova and Gupta2008, p. 327) where they figure out ‘which firms merit their attention, for what reasons and to what extent’ (Rindova et al., Reference Rindova, Petkova and Kotha2007, p. 34). Others similarly describe how gatekeepers ‘filter information about new developments’ and ‘select a relatively small subset of issues, events, and organisations to focus public attention on’ (Petkova et al., Reference Petkova, Rindova and Gupta2013, p. 866). However, beyond these abstract screening processes, the actual mechanisms and evaluation processes remain poorly understood (Überbacher, Reference Überbacher2014). How, in situations where there are hundreds or, as with digital entrepreneurship, thousands of ventures vying for attention, does the gatekeeper decide to cover one venture and not another?

5.3 Valuation Studies

To help specify the gatekeeper evaluation process, we turn to recent Valuation Studies, a body of work that has shifted conceptions of evaluation from simple outcomes based on filtering and selection to more ‘processual’ understandings (see Millo et al., Reference Millo, Power, Robson and Vollmer2021). Two key insights are relevant from this literature. First, it acknowledges that venture performance or qualities are not given. Instead, they must be enacted as part of an evaluation. This is not an abstract or cognitive evaluation but rather one that involves distinctive socio-technical evaluation processes (Helgesson & Muniesa, Reference Helgesson and Muniesa2013, p. 23). Here, we will focus on the briefings provided by new digital ventures to industry analysts and the latter’s efforts to comprehend venture viability and distinctiveness.

Second, this research also highlights how evaluation can be transformative (Antal et al., Reference Antal, Hutter, Stark, Antal, Hutter and Stark2015; Kornberger et al., Reference Kornberger, Justesen, Madsen and Mouritsen2015). In tracing the etymology of the concept of ‘value’, for instance, the French sociologist Vatin (Reference Vatin2013) distinguished between ‘evaluating’ and the more generative notion of ‘valorising’, where the latter conception captured how the work of evaluation is not merely about appraisal but can also be additive towards the phenomenon under review. To evaluate ‘corresponds with a static judgement attributing a value to a good, a thing, a person’, whereas to valorise ‘has a dynamic meaning – increasing a value, adding an increment to it, a surplus value’ (Vatin, Reference Vatin2013, p. 33). The view of evaluation as concerned with identifying and creating value has begun having currency within management scholarship and broader social sciences (Karpik, Reference Karpik2010). For instance, in their study of the evaluation of art, Plante and colleagues (Reference Plante, Free and Andon2020, p. 3) discuss how art evaluators do more than identify the value of a particular artistic asset. In defending and rationalising their assessment to others, they actively enhance its value (see also Barman, Reference Barman2015; Bidet, Reference Bidet2020; Frenzel & Frisch, Reference Frenzel and Frisch2020).

When considering how gatekeepers screen new ventures, existing scholarship describes the first conception, appraisal (Pollock & Gulati, Reference Pollock and Gulati2007; Petkova et al., Reference Petkova, Rindova and Gupta2013), but not the second, valorising. Inspired by the idea that digging further into gatekeeper screening processes reveals potentially more profound value-creating mechanisms, we highlight the role of valuation and valorisation in screening processes as new ventures brief gatekeepers to win their backing.

5.4 New Ventures: An Unknown Quantity

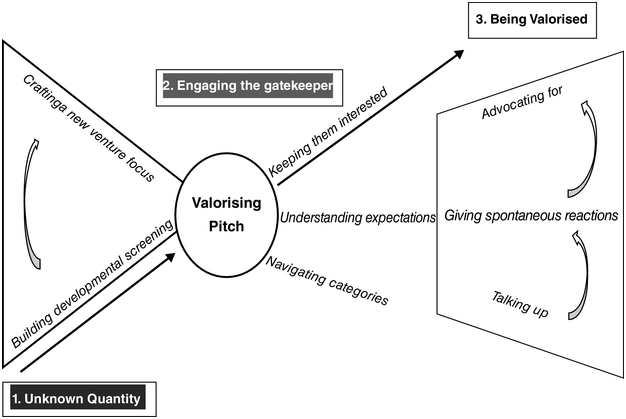

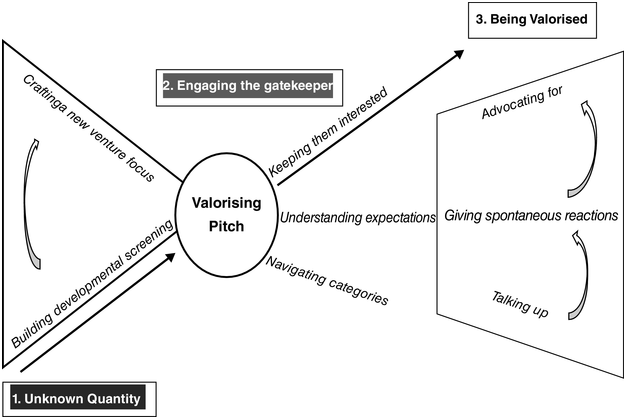

To understand how new digital ventures engaged with and benefited from gatekeeper support, we surfaced three processes that enabled ventures to move from being an unknown quantity in the eyes of the gatekeeper to engaging the gatekeeper, to being valorised by it.

We found that analyst firms are expanding their coverage as they attempt to map and categorise the start-up community. This is a significant departure point. Previously, they only focused on the more prominent and significant/established players. This shift, we found, involved them in crafting a new venture focus and building developmental screening.

5.4.1 Crafting a New Venture Focus

The interest in creating specific categories and processes for identifying new ventures started when Gartner launched its ‘Cool Vendor’ reports. Each year, this firm chooses several hundred ventures from various technology areas for coverage. An analyst specialising in the customer relationship management (CRM) area describes this focus:

We do a Cool Vendor report across the whole of Gartner where we look at Content Management, Web Analytics, and all sorts of different subjects, and we look for Cool Vendors in that area. It could be networking technologies, or mobile technologies or broadband or whatever; it doesn’t really matter. But in the area of CRM, we’ll routinely find 30 to 40 vendors easily, and we pick about 15 to write up and say that is quite cool or even different.

The analyst defines what is different about new ventures compared to the more established players usually covered:

Our Cool Vendor reports are really vendors that have been trading for three or four years, maybe five, unlisted. Most people haven’t got a clue who they are, but we know that they have got some really good customers. The customers say they are good, and that is what we think is cool about them. They have got something unique, and they got real customers.

From the earliest stages of industry analyst formation, Gartner often leads the way in developing new types of promissory products (Pollock & Williams, Reference Pollock and Williams2016). Thus, other industry analyst firms have followed suit, in many cases, borrowing and remaking the Cool Vendor appellation. For instance, the CEO of Analyst Firm B describes the provenance of his ‘Hot Vendor’ designation: ‘I was at Gartner for a long time. So, I started [Analyst Firm B] seven years ago. We said it’s not cool to be Cool, it’s cool to be “Hot”! We just took that phrasebook and reinvented it’ (A2, interview). The new venture focus was further augmented recently when another major analyst firm launched its ‘Innovators’ label. An informant from Analyst Firm C explains what they are doing to build a focus on new ventures:

We’re investing in the market around the ‘Innovators’, around the emerging vendors. We’ve got the analyst teams now supporting emerging vendors a lot more than what we’ve done in the past. We’re wanting to write about them a lot more. We want to get them visibility a lot more.

Two reasons were given for this expansion of coverage. The first point to shifts in digital innovation: ‘Most of the really innovative technologies are not coming from the big companies that always occupied [analyst research], it’s coming from the small vendors. They’re very innovative…. [And] seem to account for most of the innovation’ (A4, interview). Another cited reason was the changing interests of technology adopters, the main clients of industry analyst firms. Recent technological developments, such as Software-as-a-Service (SaaS) and cloud-based services, meant new ventures could offer attractive solutions to technology adopters:

The thing that we notice…. in SaaS software and in a lot of cloud-based applications, is you wonder if the product works and if [buyers] can sign up and they can cancel. A lot of business buyers say: ‘Look that [start-up] looks pretty good to me. I think I’m going to sign up for that’.

Analyst informants specified how clients no longer avoided new ventures. Seemingly, the buyer’s assessment is, ‘If it works, and it will help my business, then I’m going to take a chance, and I’m going to go for it’ (A2, interview). Since ensuring clients maintain subscriptions is an immediate priority, this means analyst firms are increasingly focusing on new ventures.

5.4.2. Building Developmental Screening