I

The relationship between financial globalization and peripheral integration has emerged as one of the most discussed issues in contemporary political economy (Schularick Reference SCHULARICK2006; Nesvetailova Reference NESVETAILOVA and Robinson2019; Oliveira et al. Reference OLIVEIRA and DE CONTI2025). As the world moves from unipolar to multipolar financial architectures, with emerging economies developing alternative institutional frameworks that challenge traditional Western dominance (Bordo and Flandreau Reference BORDO and FLANDREAU2001), fundamental questions persist about how peripheral regions integrate into global financial networks while remaining systematically subordinate to them. The persistence of these asymmetric relationships has drawn increasing scrutiny from scholars examining the role of contemporary financial elites in perpetuating core–periphery dependencies (Mohan and Tan-Mullins Reference MOHAN and TAN-MULLINS2019).

Recent research on financialized capitalism shows how global financial elites continue to shape peripheral integration through mechanisms that mirror historical patterns – from sovereign wealth fund investments to the development of a range of financing models – while maintaining decisive control over capital allocation and risk assessment (Bonizzi et al. Reference BONIZZI, KALTENBRUNNER and POWELL2022). Developing countries still experience subordinate and dependent integration patterns that reproduce core–periphery dependencies rather than fostering autonomous development, highlighting that the influence of transnational financial elites remains as crucial today as it was during capitalism’s formative period (Oliveira and De Conti Reference OLIVEIRA and DE CONTI2025).

The persistence of unequal financial relationships points to deeper structural continuities in how financial power has historically shaped global integration. The apparent spontaneity of market expansion often concealed the deliberate orchestration of powerful financial interests that shaped institutional arrangements to serve their particular ends (Polanyi Reference POLANYI1944). The first wave of financial globalization is especially revealing. The first global century (1820–1913) (Williamson Reference WILLIAMSON2006) emerged with the consolidation of transnational networks linking distant actors through social ties (kinship, religion, politics, friendship) and shared business and financial interests (Cassis Reference CASSIS1997; Jones Reference JONES2002; Hausmann et al. Reference HAUSMAN, HERTNER and WILKINS2008). In this context, leading financial and business figures forged the connections through which core financial centres penetrated peripheral regions, laying the foundations of global capitalism (Cameron Reference CAMERON1961; Cassis and Cottrell Reference CASSIS and COTTRELL2009). During this formative period, transnational business groups (BGs) – formed by legally independent firms interconnected through economic and social ties and operating across different regions (Khanna and Yafeh Reference KHANNA and YAFEH2007; Jones and Colpan Reference JONES, COLPAN, Colpan, Hikino and Lincoln2010) – were key conduits in the process, projecting the influence of core centres and extending their reach into the peripheries (Colpan et al. Reference COLPAN, HIKINO and LINCOLN2010). From the 1850s, and more markedly from the 1860s, foreign direct investments (FDI) redirected capital from European cores to peripheral economies, supporting industrialization, technology transfer and infrastructure development beyond traditional trade and sovereign bonds’ channels (Gille Reference GILLE1968; Twomey Reference TWOMEY2000).

However, while much of the existing literature on nineteenth-century financial capitalism has largely focused on core financial centres, relatively little attention has been paid to understanding these dynamics from the perspective of peripheral regions themselves (Khanna and Yafeh Reference KHANNA and YAFEH2007). Indeed, there is a body of evidence both from economic history (Feis Reference FEIS1965; Woodruff Reference WOODRUFF1966; Cassis Reference CASSIS2010) and economics (Schularick and Steger Reference SCHULARICK and STEGER2006) documenting the role of European capital in the economic development of peripheral economies prior to 1914. However, many questions remain open. How did peripheral economies navigate their integration into global financial circuits? What role did local elites play in shaping the terms of this integration? What can these historical processes reveal about the persistent tension between institutional learning and structural dependency that continues to characterize contemporary development debates (Prasad et al. Reference PRASAD, ROGOFF, WEI, KOSE and Harrison2007)?

To address these questions, this article examines the case of Southern Italy, specifically Naples, during its integration into nineteenth-century globalization. Naples offers a particularly revealing case study for several reasons (Schisani et al. Reference SCHISANI, RAGOZINI, VITALE and Corazza2018). As the capital of the Kingdom of the Two Sicilies and later a major city in unified Italy, it possessed sufficient economic significance to attract sustained international investment, while remaining structurally peripheral to the dominant financial centres of Northern Europe and the rest of Italy. This intermediate position allows us to observe the full complexity of peripheral integration processes that might be less visible in either completely marginal regions or emerging core centres.

Drawing on an original micro-level data and applying advanced SNA techniques, we investigate the nature and implications of the networks through which Naples was integrated into global capitalism. We focus particularly on how foreign actors – bankers, industrialists and entrepreneurs – formed transnational BGs that connected local firms and institutions to wider circuits of capital, technology and influence. These groups did not merely operate as conduits of investments; rather, they functioned as intermediaries, brokers and at times gatekeepers, shaping the terms of local engagement with global finance through what we conceptualize as ‘relational infrastructures’.

Our approach problematizes linear and deterministic narratives of modernization that continue to influence development economics today. Rather than assuming that financial globalization necessarily produces convergence and development, this analysis considers whether these groups facilitated genuine financial modernization in peripheral economies or instead entrenched new forms of dependency and asymmetric integration. We explore whether transnational BGs acted as paragons, bringing knowledge and institutional innovation, or as parasites, exploiting local structural weaknesses for rent-seeking purposes. A dichotomy that remains relevant for understanding contemporary foreign investment patterns in emerging markets (Khanna and Yafeh Reference KHANNA and YAFEH2007).

The historical trajectory we trace suggests that peripheral integration into global capital flows was neither automatic nor uniform but occurred through gradual and negotiated processes marked by institutional constraints, political alliances and relational infrastructures. By analysing how these transnational groups emerged, evolved and interacted with local elites and institutions, we show the mechanisms through which peripheral regions were embedded into global networks. Importantly, we demonstrate that these processes were not purely exogenous but involved significant agency and strategic adaptation on the part of local actors, a finding with implications for contemporary debates about peripheral participation in global capitalism (Bruszt and Vukov Reference BRUSZT and VUKOV2018).

Methodologically, our use of social network analysis to map BGs’ evolution and relational infrastructures positions this study within a growing recognition among international business scholars that understanding global capitalism requires attention to densely structured networks of trust, influence and institutional proximity rather than pure market forces (Jones and Zeitz Reference JONES and ZEITZ2019). The analytical techniques we employ – including betweenness centrality analysis, community detection and modularity measures – offer a replicable framework for analysing both historical and contemporary cases of peripheral integration.

The article unfolds across four pivotal historical periods (1820–39, 1840–61, 1861–80 and 1880–1903), each marking distinct phases of financial integration and institutional transformation. For each period, we reconstruct the structure and dynamics of the Naples business network, by identifying prominent communities of actors and firms where foreign financiers and entrepreneurs were active, and by examining the role played by financial interlocks, kinship ties and sectoral diversification.

The rest of the article is organized as follows. Section II introduces the historical framework while Section III presents the data and the analytic strategy within the SNA approach, accompanied by a glossary of network terms in the Appendix. In Section IV the main network results are described. We then discuss period by period in the following sections (V to VII) the evolving topology of the networks, aiming to interpret how globalization mechanisms unfolded from the core to the periphery through the evolution and dynamics of connections between international and local actors. Section VIII concludes with some final remarks.

II

The process of globalization represents complex and uneven patterns of economic integration driven by the interconnection of markets, monetary and financial systems, and technological networks (Bordo and Flandreau Reference BORDO and FLANDREAU2001; Williamson Reference WILLIAMSON2006). At its core lies the construction of network-related infrastructures – from railways, canals, ports, utilities to modern ICT systems – that provide the physical and institutional foundations for global connectivity (Bretagnolle and Mimeur Reference BRETAGNOLLE, MIMEUR and Frétigny2025). These infrastructures are not merely technical artefacts; they embody the spatial and financial architectures through which global capitalism expands, linking distant territories and enabling the circulation of capital, goods and information, connecting valuable interests, while disconnecting valueless ones (Castells Reference CASTELLS1999).

From the nineteenth century onward, the creation of infrastructure networks required vast financial resources and sophisticated organizational structures, often exceeding the capacities of individual states or local entrepreneurs. Consequently, public authorities and private investors collaborated through hybrid arrangements – ranging from concessions to complex financial partnerships – that prefigured contemporary forms of project financing and public–private partnerships (Dupuy and Tarr Reference DUPUY and TARR1988; Schisani and Caiazzo Reference SCHISANI and CAIAZZO2016). In this sense, the nineteenth-century globalization of infrastructures anticipated modern investment practices such as build–operate–transfer (BOT) schemes, through which capital from the industrialized core sought profitable opportunities in emerging or peripheral regions (Bonizzi et al. Reference BONIZZI, LASKARIDIS and TOPOROWSKI2019; Hoppe and Schmitz Reference HOPPE and SCHMITZ2021; Castelblanco et al. Reference CASTELBLANCO, MANGANO, ZENEZINI and DE MARCO2025).

Such arrangements revealed a structural asymmetry inherent in global economic integration (Frank Reference FRANK1966; Wallerstein Reference WALLERSTEIN1974). While core regions supplied capital, technology and institutional models, peripheral areas provided markets, raw materials and strategic locations but remained dependent on external financing and expertise. This imbalance – between those who controlled investment and those who depended on it – became one of globalization’s most debated features, raising questions about whether global integration promotes convergence and shared development or reinforces dependency and hierarchy between core and peripheral economies (Frank Reference FRANK1998, Reference FRANK2002).

During the first globalization of the late nineteenth century, this ambivalence was already central to intellectual and political debates. The formation of a world economy was intended by many observers as both a mechanism of integration and an instrument of imperial expansion (Hobson Reference HOBSON1902; Hilferding Reference HILFERDING1910). Classical theorists interpreted global economic expansion primarily from the vantage point of the industrial and financial metropolises, while scholars from peripheral contexts offered more nuanced readings emphasizing how peripheral regions internalized, resisted or reinterpreted global forces (Manoilescu Reference MANOILESCU1929).

In this broader historical framework, the Mediterranean space – and particularly Southern Italy – offers an illuminating example of how infrastructural and financial globalization materialized in concrete form. Situated at the crossroads of maritime routes, connecting Western Europe, North Africa and the Near East, the region functioned as both a conduit and a testing ground for the circulation of capital, technology and expertise (Salvemini Reference SALVEMINI2009; Drolet Reference DROLET2015). Italy’s unification in 1861 marked a decisive turning point that transformed the former Bourbon periphery into a liberalized frontier of investment within a newly unified national market. The dismantling of protectionist barriers, together with the liberal government’s openness to foreign capital, created conditions for intensified integration into European financial circuits (de Majo Reference DE MAJO, Assante, De Luca and Muto2006a; Schisani and Caiazzo Reference SCHISANI and CAIAZZO2016). The opening of the Suez Canal (1869) represented the culmination of this process, as it symbolically recentred the sea within global routes while materially contributing to a rehierarchization of ports and routes that privileged those better integrated into Atlantic-facing and Northern European commercial networks over Mediterranean ports (Cristina Reference CRISTINA and Curli2022).

Naples, as the principal city of Southern Italy, occupied a pivotal position within this process. Its geographic centrality and maritime vocation made it a strategic node in the emerging Système de la Méditerranée envisioned by the Saint-Simonian economist Michel Chevalier (Reference CHEVALIER1832), a transnational project of infrastructural integration linking the ports of the Mediterranean to Europe’s political and financial capital cities (Crispo Reference CRISPO1940; Drolet Reference DROLET2015). Within this vision, railways, shipping lines, canals and public utilities were conceived not only as instruments of modernization but as vehicles for geopolitical influence, mirroring the present processes of globalization of the Global South (Mohan and Tan-Mullins Reference MOHAN and TAN-MULLINS2019). The Mediterranean was imagined as a French lake, a space of economic and political coordination underpinned by the principles of free trade, monetary uniformity and technical interconnectivity that culminated in the 1865 Latin Monetary Union (LMU) (Cameron Reference CAMERON1961; Gille Reference GILLE1968). In this view, it was essential to integrate the South into the physical infrastructure networks that connected territories, seas and markets, since – unlike other pre-unification states (above all Piedmont) – it had remained isolated from this process, eventually becoming a breeding ground for FDI after unification (Schisani and Caiazzo Reference SCHISANI and CAIAZZO2016). This was especially true given that Southern Italy and Naples in particular were not primary beneficiaries of the Suez Canal (Curli Reference CURLI and Curli2022).

The evolution of Naples during the nineteenth century must therefore be read within these global currents. Foreign merchants, bankers and engineers established durable footholds in the city, operating through transnational BGs that connected it to core financial centres, Paris, Geneva, Brussels and London (Davis Reference DAVIS1979; Caglioti Reference CAGLIOTI, Doria and Petri2007). These actors imported capital, institutional models and legal instruments such as the concession à la française, a system that intertwined political authority, financial capital and entrepreneurial initiative (Schisani and Caiazzo Reference SCHISANI and CAIAZZO2016). Through such arrangements, international investors became central participants in the creation of infrastructures and utilities (railways, ports, gas lighting and other public utilities), embedding the southern periphery within a network of financial and technological dependencies that were both enabling and constraining (de Majo Reference DE MAJO2006b; Schisani Reference SCHISANI2010a).

Without anticipating later analyses, it is enough to note that these dynamics – linking infrastructure, finance and geography – form the essential context for understanding how peripheral regions such as Naples were incorporated into the early architectures of global financial and economic integration.

III

To investigate how transnational BGs shaped the integration of Southern Italy into global financial networks, we draw on original archival data organized in the IFESMez database (Imprese, Finanza, Economia e Società nel Mezzogiorno). IFESMez is a multi-source relational database that captures the economic, financial and socio-political connections among individual and collective actors operating in Southern Italy (and abroad) between 1808 and 1913. It documents how firms and financiers were linked through ownership, management, kinship and other enduring relationships – thereby providing the empirical foundation to reconstruct the relational infrastructures of early globalization.

Data were collected primarily from the State and Notarial Archives of Naples, the Italian State Archive in Rome, and foreign repositories such as CARAN, CAEF and CAMT in Paris, as well as municipal archives and national libraries in Naples, Paris and Geneva. Additional evidence from newspapers, genealogical records and secondary literature complements the archival sources. Thanks to the complexity and richness of the database, it can be used to quantitatively address a range of social, economic and financial issues of nineteenth-century Southern Italy. The data have been used for several different studies, considering different periods and time spans, such as the analysis of gas infrastructures in Southern Italy (Schisani and Caiazzo Reference SCHISANI and CAIAZZO2016), for modelling the mechanisms of formation and persistence of economic elites (Schisani, Balletta and Ragozini Reference SCHISANI, BALLETTA and RAGOZINI2021) also in relation to the persistence of familism in Southern Italy (Rondinelli et al. Reference RONDINELLI, SCHISANI and RAGOZINI2025), and for examining the transition from insurance to banking in the local financial local system (Schisani and Ragozini Reference RONDINELLI, SCHISANI and RAGOZINI2025). In the present article, the data have been specifically employed to investigate relational mechanisms associated with international BGs that enabled Naples to enter the first globalization.

Given our focus on a networked mechanism of peripheral integration, we employ Social Network Analysis (SNA)Footnote 1 not merely as a visualization device, but as a form of argumentative evidence to test how transnational capital penetrated and restructured the Neapolitan business environment. SNA allows us to trace who connected to whom, how durable those connections were, and which actors mediated between foreign financial cores and local institutions. A glossary of the network terms and measures used in the article can be found in the Appendix, where both formal definitions and their substantive meaning are illustrated with references to our analysis.

From IFESMez, we extract a bipartite (actor–firm) dataset linking each individual to the firms where they served as shareholders, directors or managers.Footnote 2 Given the large number of actors and firms involved in the networks, a comprehensive prosopographical account would result in extremely extensive descriptions and narratives spanning an entire century of Naples’s economic history. For this reason, we have chosen to include tables summarizing only the most relevant information on the key actors and firms identified through network measures, as these details help to illuminate the macro-processes underlying globalization. Note that some actors are present in more than one table referring to different periods, as they change the position and role in the network depending on their changing connections.

Restricting the timeframe to 1820–1903, the dataset contains approximately 40,000 ties among 2,947 firms and 24,625 actors. To analyse historical change, we divide the sample into four periods – 1820–39, 1840–61, 1861–80 and 1881–1903. Twenty-year periods were chosen for both practical and historical reasons. Statistically, twenty years provide a stable basis for analysis. Indeed, shorter spans would produce too many fluctuations, while longer ones would blur together companies that operated in very different times. Historically, each period is marked by turning points. The first period ends with the establishment of the Pouchain gas company (1838), the first foreign-led public utility in Southern Italy, the birth of the first foreign BG. In 1861, Italian unification brought a crucial institutional shift. The early 1880s, with the 1882 Commercial Code, opened a new phase by liberalizing the creation of joint-stock companies. This final period closes with a key moment for the southern electricity sector with the founding of the Société Financière Italo-Suisse (1902), which brought Swiss finance to the core of Naples’ business network as French finance withdrew, in line with the new financial and technological know-how.

We focus on the largest connected component, or giant component – the largest subgraph where all nodes are mutually reachable (Cartwright and Harary Reference CARTWRIGHT and HARARY1956) – and identify BGs as clusters of at least three firms operating in distinct sectors, connected by persistent and non-occasional ties such as interlocking directorates or cross-shareholdings (Khanna and Yafeh Reference KHANNA and YAFEH2007). Communities are detected using the Louvain modularity optimization algorithm, which identifies cohesive structures based on tie density (Blondel et al. Reference BLONDEL, GUILLAUME, LAMBIOTTE and LEFEBVRE2008). In the field of corporate network studies, the modularity maximization algorithms, such as the edge-betweenness algorithm (Newman and Girvan Reference NEWMAN and GIRVAN2004), the Louvain, the Leiden (Traag et al. Reference TRAAG, WALTMAN and VAN ECK2019) can be considered a sort of standard tools to analyse interlocking directorates, business groups, corporate elite networks and financial networks (see e.g. Elouaer-Mrizak & Chastand Reference ELOUAER-MRIZAK and CHASTAND2013; Heemskerk et al. Reference HEEMSKERK, DAOLIO and TOMASSINI2013; Drago & Ricciuti Reference DRAGO and RICCIUTI2017; Heemskerk et al. Reference HEEMSKERK, TAKES, GARCIA-BERNARDO and HUIJZER2016; Takes & Heemskerk Reference TAKES and HEEMSKERK2021; Yassine et al. Reference YASSINE, KADRY and SICILIA2022; Mastrandrea et al. Reference MASTANDREA, AMATO and PATUELLI2025; Schisani and Ragozini Reference SCHISANI, RAGOZINI, Schisani, De Luca, Ragozini and Cimadomoforthcoming and references therein). However, their explicit application to historical economic networks (pre-twentieth century) remains limited. Most applications focus on contemporary data rather than long-term historical evolution. Generally, economic history papers use network visualization (Grandjean Reference GRANDJEAN2021) and statistical analysis of components without formal community detection methodology.

Methods for community detection predominantly focus on one-mode networks (Yassine et al. Reference YASSINE, KADRY and SICILIA2022). In our case, however, the network under study is a two-mode interlocking directorates network. In this context, researchers typically either apply community detection approaches to projections onto one of the two modes, or – less frequently – propose adaptations of one-mode network algorithms that operate alternately on the two modes (for a discussion of this issue, see Zhou et al. Reference ZHOU, FENG and ZHAO2018). All these approaches treat the two modes of the network asymmetrically, privileging one mode over the other (e.g. assigning greater importance to inter-firm ties rather than to ties among actors). Our objective, instead, is to highlight how actors and firms form cohesive groups, namely, how prominent actors cluster around relevant firms and, at the same time, how prominent actors connect groups of firms through their roles. Modularity, which identifies communities of nodes that exhibit denser internal connections than connections to the rest of the network (Newman and Girvan Reference NEWMAN and GIRVAN2004), is well suited to capturing this criterion. Moreover, among the algorithms that maximize modularity in networks, the Louvain algorithm operates first at a local level – creating a form of super-node – and subsequently at a global level, making it, despite some limitations, particularly effective for very large and complex networks (Lancichinetti and Fortunato Reference LANCICHINETTI and FORTUNATO2011). In our case, the functioning of this algorithm first aggregates actors who locally participate in the same firm and then – when actors strongly connect firms through interlocking directorates – aggregates firms themselves. When these constellations of actors and firms exhibit the characteristics described above, we identify these communities as BGs. As will become clear in the following sections, the algorithm highlights, for example, large communities consisting of a single firm and all the actors associated with it (the super-nodes created in the first step), which are only weakly connected to the rest of the network and therefore remain, to some extent, isolated. At the same time, it clearly identifies BGs at the global level of the network. This methodology is novel insofar as it represents an adaptation that turns potential limitations of the method into an advantage for our analysis. The Louvain algorithm was not originally designed for two-mode networks and tends to isolate peripheral actors and firms, especially when applied to the largest connected component. By contrast, using the traditional approach of projecting the two-mode network onto firms and performing community detection on the resulting one-mode firm network would force all firms into communities, even in the presence of very weak ties, thereby generating excessively broad or even spurious BGs (Elouaer-Mrizak and Chastand Reference ELOUAER-MRIZAK and CHASTAND2013). A particularly telling example is that of cooperative firms and/or cooperative banks, which may have a very large number of members, only a few of whom connected to other firms. Under our approach, these organizations remain separate and form individual communities, as is analytically appropriate. In contrast, more traditional approaches that operate alternately on the two modes risk assigning them to communities together with other firms, thereby distorting the interlocking logic that is central to our analysis.

Each detected BG is characterized by sectoral classification (NACE Rev. 2) (Schisani and Ragozini Reference RONDINELLI, SCHISANI and RAGOZINI2025) and actor prominence. To quantify brokerage and connectivity, among the network centrality measures (betweenness, degree, closeness, eigenvector centrality, etc) we focus on degree and betweenness. Specifically, actors with high betweenness are interpreted as brokers or hinge nodes bridging foreign and local clusters, thus operationalizing the core–periphery linkage central to our argument (David and Westerhuis Reference DAVID and WESTERHUIS2014).

To move beyond static description, we systematically compare network properties across time-periods. This dynamic analysis assesses how integration intensified or fragmented over the century by tracking:

• average degree and changes in modularity (overall connectivity, cohesion and degree of community segmentation);

• community persistence and reconfiguration (which BGs endured, merged, or dissolved); and

• the shifting position of brokerage actors (e.g. Rothschild vs Meuricoffre vs Parent, etc.).

Visualizations generated through a force-directed layout (ForceAtlas2) (Jacomy et al. Reference JACOMY, VENTURINI, HEYMANN and BASTIAN2014) are used to represent these transformations consistently across periods, enabling comparative interpretation. We decided to represent the networks through this force-directed layout, which optimizes the forces of attraction and repulsion among nodes, as it is very effective in highlighting dense areas of the network revealing communities incorporating also the idea of the presence of multigravity centres (as in our case). As closely connected nodes cluster near each other while non-connected nodes repel, the distances among the communities can be interpreted in terms of strength and closeness of their relations (Jacomy et al. Reference JACOMY, VENTURINI, HEYMANN and BASTIAN2014).

In all graphs, communities mainly composed of local economic/financial actors and firms are represented by light colours, while international BGs are characterized by dark colours. The size of the nodes is proportional to their betweenness centrality. Through this approach, we can visually and quantitatively trace the entry, exit and reorganization of BGs, capturing the evolving architecture of financial globalization in Naples.

IV

Table 1 and Figure A1a–d (in the Appendix) display the evolution of the four two-mode networks (actors-by-firms) and their projections (over actors and the firms). Recall that the networks include both firms that are legally registered in Naples and firms that are registered elsewhere but operate in Naples, or firms that are linked to actors and firms in Naples through actors who are common shareholders/directors/managers, as well as the public administration and the political institutions they belong to. Over time, the number of economic actors and firms increases, in particular after unification thanks to the liberal turn and new interests in the development of the South, bringing about an increase in the number of potential links. The number of actors over the 80 years increased by more than 10 times, while the number of companies increased by about four times, growing from 1,590 to 17,680, and from 265 to 1,094, respectively. However, the density of the network decreased since the average degree remains quite constant, suggesting a sort of structural feature of the business network, i.e. each actor can manage a limited number of participations in companies, apart from the big interlockers that belong to the local and international business and financial elites. Also, the share of both isolated and marginal firms in the interlocking networks remains quite constant, being stable at around 72 per cent for the first three time spans, decreasing to around 60 per cent in the last period. On the other hand, despite the growing number of actors, the share of both isolated and marginal ones decreases dramatically over time from 15 to 0.05 per cent. This is particularly true in the last 20 years, when we observe a significant increase in the number of actors associated with a small decrease in the number of firms. This can be explained by two factors: (i) the effects of the twin crises (1889 and 1894) that yielded several bankruptcies and company mergers (Cova Reference COVA2014); (ii) the boost given by the 1882 Code of Commerce to the foundation of large special interest insurance-type firms (the so-called Mutue) and large local cooperative banks in limited liability form (Schisani et al. Reference SCHISANI, BALLETTA and RAGOZINI2021). These large institutions mechanically create links among all members of the institution itself, regardless of whether they are linked to actors in other institutions,Footnote 3 and without generating meaningful interlocks.

Descriptive measures for temporal two-mode and one-mode networks

Table 1 Long description

The table reports descriptive statistics for temporal networks across four periods from 1820–39 to 1881–1903, including an actors-by-firms network (whole network and largest component) and derived one-mode networks. In the two-mode whole network, the number of actors grows from 1,590 to 17,680 and links from 2,225 to 21,934, while firms rise from 265 to 1,439 by 1861–80 then fall to 1,094 in 1881–1903; public administrations increase from 7 to 63 then drop to 34. Density is very low throughout, listed as 0.001 in the first two periods and 0.000 in the last two, while average degree stays fairly stable around the low twos. Fragmentation changes over time: components increase from 129 to 734 by 1861–80, then decrease to 382 in 1881–1903. In the largest component, actors expand from 1,288 to 16,639 and firms from 108 to 712, with density again near zero and average degree around the mid twos. Community structure in the largest component becomes more segmented over time, with communities rising from 21 to 48 and modularity increasing from 0.738 to about 0.865 by the last two periods; relevant business groups with foreign actors peak at 11 in 1861–80. In the firm-by-firm network, isolated firms and marginal firms increase through 1861–80 (634 isolated, 458 marginal) then decline in 1881–1903 (356 isolated, 304 marginal). In the actor-by-actor network, isolated actors remain relatively low (34 to 80) while marginal actors rise strongly to 1,458 in 1861–80 before falling to 808. Values are descriptive and period-specific, and the density rounding to three decimals can mask small differences in sparsity.

Thanks to the progressive integration of the business environment, we observe a changing network topology with an increase in the shares of actors and firms in the largest connected component of the networks (from 81 to 94 per cent, and from 40 to 63 per cent, respectively), suggesting that firms tended to create a more closely linked network structure. Overall, a large number of nodes and the low density in all time-periods, and in general the complexity of the network structure, mainly after 1861, justify the extraction of the largest connected components and the Louvaine community detection method (Blondel et al. Reference BLONDEL, GUILLAUME, LAMBIOTTE and LEFEBVRE2008) to uncover the relevant and hierarchically dominant BGs. Over time, both the modularity (i.e. the strength of division of the network into modules or communities) and the number of communities increase: many of them cannot be considered BGs, while others are local ones. The number of international BGs is quite stable, even though, as will be clearly described in the following, their composition and strength in terms of economic power evolve a lot over time. To analyse them in each period, we take a closer look at the networks highlighting the international BGs, identified as described in the previous section, by representing them in dark colours, in contrast to local BGs represented by light colours, and to other scattered firms present in the network (grey).

In the following, on the basis of the results, we found four interesting patterns related to the four time spans:

i. Network formation and financial brokerage (1820–39)

ii. The role of business groups in asymmetric integration (1840–61)

iii. Institutional learning and endogenous modernization (passive modernization hypothesis) (1861–80)

iv. Crisis, transformation and changing alliances (1881–1903)

The next three sections, one for pre-unification periods (Section V) and two for post-unification (Sections VI and VII), discuss the analysis of the communities in the largest component. The results show the central position of financial and related services firms (not only banks but also big transport and public utilities companies with a strong financial component) in the structuring of transnational BGs linked to core financial centres. Networks highlight a stable core of foreign agents, generally members of the European financial and political milieu, clustered in cohesive groups with local actors (merchant bankers, private bankers, financiers, politicians) with the highest centrality. The pervasiveness of the international BGs in the Neapolitan business environment is testified by their presence in the core of the network and by their ability to preserve the connectedness.

V

The integration of Naples and Southern Italy into nineteenth-century global finance unfolded through a fundamental transformation in network architecture, yet one that progressively consolidated rather than dismantled peripheral status.

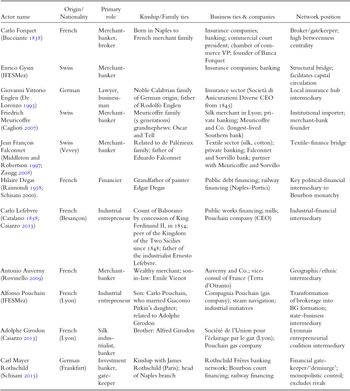

This process began with a dual-architecture network (1820–39) (Figure 1) that includes: (i) a local-core clustering around insurance and local industrial and banking companies (cyan and light green community) at the very core of the largest component; (ii) small, tight foreign cliques (dark blue, dark green, dark red and purple) operating as modular gateways to international BGs, surrounding the core of the largest component. In this first configuration, foreign resident capitalists functioned as structural bridges rather than replacements for local actors. Merchant-bankers like Carlo Forquet, Friedrich Meuricoffre, Hilaire Degas, Jean François Falconnet, Enrico Gysin and Giovanni Englen, who had high betweenness centrality inside their communities (Table 2), enabled the circulation of capital, knowledge and institutional practices between Naples and major European markets, while maintaining tight ethnic, religious and kinship cohesion among themselves (Davis Reference DAVIS1979; Caglioti Reference CAGLIOTI2006).

Largest component of the Naples business network, 1820–39

Figure 1 Long description

A thematic network map showing a labeled business network for Naples, 1820–39. The layout is a node-and-link diagram: many small labeled nodes are connected by straight line segments, forming one large connected component with several dense clusters and many peripheral nodes. Text labels visible near the central area include: “Assicurazioni generali del Sebeto”, “Società Tontina”, “Commerciale di Assicurazioni”, “Compagnia privilegiata Napoletana di Assicurazioni” and “Rassicurazione dei rischi del mare”. Additional labeled nodes appear around the outer parts of the network, including “Sebezià” and “Banca”. The diagram uses different visual groupings to separate clusters of nodes. A legend or key explaining the meaning of these groupings, node sizes, or line styles is not readable at this resolution, so only the presence of multiple distinct clusters, labeled nodes and connecting lines is visually verifiable. No compass, scale bar, or geographic base map is shown; the arrangement appears relational rather than geographic.

Network formation and financial brokerage, 1820–39

Table 2 Long description

The table lists 11 actors and summarizes their origin or nationality, primary role, family ties, business affiliations, and described position in a financial and commercial network. Most actors are French or Swiss merchant-bankers or industrial entrepreneurs, with a smaller German presence. Carlo Forquet is characterized as a broker and gatekeeper with high betweenness, while Carl Mayer Rothschild is described as a dominant financial gatekeeper who controls access and excludes rivals. Several figures act as bridges across sectors: Gysin facilitates capital circulation, Falconnet links textiles and finance, and Englen serves as an insurance-sector intermediary. State-facing intermediation appears in Degas, Lefebvre, and Pouchain through public debt, railways, public works, and gas and navigation ventures. Family and kinship ties recur as a mechanism of continuity and alliance, including multi-generation banking families and marriages connecting business groups. Network-position labels are qualitative rather than numeric, so comparisons reflect the authors’ characterizations rather than measured centrality values for every actor.

Critically, these foreign actors operated as modular gateways (i.e. gateways to their local module or community), preserving internal group solidarity while connecting outwards to fragmented local partners (merchants, private bankers, industrial entrepreneurs). This architecture reveals that network centrality stemmed from positional advantage in cross-border capital coordination rather than from nationality. The Rothschilds exemplified this logic most powerfully, with Carl Mayer Rothschild operating as a ‘financial demiurge’ (Schisani Reference SCHISANI2010a). His role as a monopolistic gatekeeper allowed him to control information distribution (Díez-Vial and Montoro-Sánchez Reference DÍEZ-VIAL and MONTORO-SÁNCHEZ2020), selectively opening Naples to the French haute banque – through kinship ties with James Rothschild in Paris – and excluding rivals like the Belgian-founded Banca del TavoliereFootnote 4 (orange community on the left side).

Yet the first network also displayed an incipient modularity that foreshadowed deeper structural changes. Aligned with European modernization logics, foreign-led cliques functioned as institutional importers transmitting modern organizational forms, such as private merchant-banks, industrial partnerships, limited-liability utilities. The community brokers German-Swiss cotton entrepreneurs (Vonwiller, Zublin, Escher, Schlaepfer, Wenner)Footnote 5 (communities shown in purple at the bottom right of the network) and other manufacturing clusters represent examples of long-term anchoring of their communities in the local production system (Balletta Reference BALLETTA, De Luca, Lorenzini and Romani2018). Notably, the Lyonnais Compagnia di Illuminazione a Gas Della Città di Napoli better known as Compagnia Pouchain (1839) (dark blue community on the right) emerges as pivotal. Figures like Alfonso Pouchain and Adolphe Girodon (Table 2) – also thanks to established relationships with the foreign resident industrialist Carlo Lefebvre and the merchant-banker Antonio Auverny – transformed brokerage into an embryonic transnational BG formation. They show how multi-market interlocks could link the rising French financial/entrepreneurial coalitions to Bourbon infrastructural ventures while creating state-business entanglement through royal shareholding (King Ferdinand II’s siblings Leopold Count of Syracuse and Caroline Bourbon).

This initial configuration laid the structural foundations for deeper transnationalization, which led to a decisive hierarchization of the network during the subsequent period from 1840 to Italian Unification. This transformation resulted in a consolidation of asymmetric interdependence. What distinguished this hierarchized configuration from earlier brokerage-based forms was a shift in the locus of power within the network. During the first period, foreign brokers mediated between relatively autonomous local clusters and European markets: their centrality derived from bridging disconnected worlds. By mid-century, foreign capital had consolidated into cohesive transnational BGs with internal decision-making structures, strategic portfolios spanning multiple sectors and countries, and the capacity to impose hegemonic conditions on peripheral integration. Naples connected densely to global capital markets, yet exclusively on terms that still reproduced its peripheral positionality within the European financial hierarchy. The largest component of the network shifted towards a tripartite architecture (Figure 2): (i) the local core was still dominated by maritime insurance and traditional mercantile finance (communities depicted in cyan), and it remained structurally subordinate to (ii) large transnational BGs clustered around international railways, public utilities and investment banking (shown in dark red, dark blue, and dark green); (iii) hybrid intermediary clusters (dark red and light green) connected the previous two.

Largest component of the Naples business network, 1840–61

Figure 2 Long description

The image displays a network diagram with numerous interconnected nodes and links. The nodes are distributed across the image, forming clusters of varying densities. Different colors are used to represent distinct groups or categories within the network. Lines connect the nodes, indicating relationships or interactions between them. The layout suggests a complex structure with multiple interconnections, highlighting the intricate nature of the network.

Three major transnational BGs dominated this new configuration: (i) the Rothschilds/Réunion Financière (dark red starting from upper left side to lower left side), leveraging Auguste Dassier’s Swiss financial milieu; (ii) the Pereire/Crédit Mobilier (dark green lower part of the network); and (iii) the Basile Parent’s Franco-Belgian coalition (dark green lower right side) (Table 3). These groups competed through fundamentally conflicting models of financial capitalism (Cameron Reference CAMERON1961) – the Pereire brothers’ new bank (Crédit Mobilier) challenged Rothschild’s old haute banque order (Landes Reference LANDES1956). At the international level, this rivalry paradoxically reinforced structural integration rather than fracturing it. Big interlockers (Table 3) like Auguste Dassier, Edward Blount, Basile Parent and Gustave DelahanteFootnote 6 maintained transversal connectivity across competing networks, ensuring that conflict preserved structural cooperation. It was rather at the peripheral level that this competition revealed its limits: in the Neapolitan battleground, the attempt to found a Mobilier-type institution through the takeover of the Banca Fruttuaria del Regno delle Due SicilieFootnote 7 (dark green community in the lower area) failed. Indeed, integration occurred only under hegemonic conditions, with Rothschild’s gatekeeping power determining which financial models could be imported and which excluded in the peripheral market. The attempted Mobilier takeover and the Rothschilds’ gatekeeping role exemplified this dynamic. Integration was no longer negotiated between equals but governed by core actors determining peripheral incorporation on asymmetrical terms. Brokers became administrators of dependence.

Role of business groups in asymmetric integration, 1840–61

Table 3 Long description

The table lists key actors and business groups active in European finance and infrastructure from 1840 to 1861, describing each one’s origin, primary role, family ties, sectors, and integration strategy. Major investment-banking poles include the Rothschild network as a dominant gatekeeper in railways and sovereign finance, and the Pereire brothers’ Crédit Mobilier as a rival model that pursued expansion but faced setbacks. Several figures act as connectors across countries and sectors: Basile Parent and Gustave Delahante link construction, metallurgy, banking foundations, and railway companies, while Edward Blount bridges Franco-British finance through rail and water-works projects. Swiss haute banque appears through Auguste Dassier and Oscar Meuricoffre, emphasizing partnership-based investing and multi-generational continuity in private banking and insurance ties. Lyon-based industrial-financial actors Alfonso Pouchain and Adolphe Girodon concentrate on gas, steam navigation, and metallurgy, using marriage and family links to build coalitions and state–business partnerships. A local consolidation pattern is represented by Rodolfo Englen, who leads insurance networks tied to a Calabrian noble family. Across entries, kinship and interlocking partnerships repeatedly support asymmetric integration strategies, but the table summarizes roles and relationships rather than measuring outcomes or performance.

The critical innovation of this second period lies in the emergence of a subset of foreign actors who achieved positional centrality as hinge nodes, anchoring themselves in the local business as a mechanism of control. Foreign intermediaries like Alfonso Pouchain, Oscar Meuricoffre (Frederich’s grandnephew), Rodolfo Englen (son of Giovanni), Adolphe Girodon and Carl Rothschild achieved positional centrality not through wholesale displacement of local actors but through strategic embedding in local governance, insurance firms and banking enterprises. Rothschild’s institutionalized relationship with Bourbon sovereignty, mediated through kinship ties and financial services, prefigured a model in which foreign capital operated through local elite collaboration rather than external imposition (Schisani Reference SCHISANI and Balletta2010b). Simultaneously, political/institutional entities – the Bourbon monarchy, the Municipality of Naples and later the Kingdom of Italy – occupied structurally invariant positions as mandatory passage points, mediating all flows between global investors and provincial infrastructures (Schisani and Caiazzo Reference SCHISANI and CAIAZZO2016).

This configuration implied that international capital required embedded intermediaries to access local markets and institutional privileges. Foreign actors could not simply impose their presence but had to negotiate with sovereign institutions and local notables. The result was not convergence towards a uniform European capitalist model but rather codification of a core–periphery hierarchy within a single connected system. Naples, indeed, was simultaneously indispensable (as a market, revenue source and geopolitical asset) and subordinated (constrained to secondary roles in financial innovation, capital accumulation and decision-making).

Thus, the network topology evolution reveals a configuration in which foreign actors served as links between separate worlds into one in which Naples became a subordinate node within a pre-existing European financial–industrial order. Peripherality was not simply geographic or economic. It was structurally encoded in network architecture build of a tripartite division between local core, transnational clusters and hybrid intermediaries, in the mandatory passage point role of the state, and in the gatekeeping prerogatives of core financial actors.

VI

After Italian unification, and particularly with the acceleration of the first wave of globalization in the 1870s, Naples experienced a structural shift in its mode of international financial integration. The period marks the definitive consolidation of the Southern Italian periphery into a densely connected European financial–industrial network in which transnational BGs fully permeated the local corporate landscape, forming international clusters that connected the entire Neapolitan structure. The persisting cohesion of the network, even when restricting the graph to major foreign players only, scattered all around (Figure 3), demonstrates that in this reconfiguration foreign BGs became indispensable integrators, connecting Naples to the European core. The Rothschilds’ strategic withdrawal from Southern Italy (1863) (Schisani Reference SCHISANI2015), after their progressive peripheralization in the network (dark red community on the peripheral upper right side), marked a decisive structural pivot towards an infrastructure-based convergence. This reorientation reflected both strategic repositioning by core European finance and adaptive reconfiguration by Neapolitan elites (Schisani et al. Reference SCHISANI, BALLETTA and RAGOZINI2021). Rather than representing decline, this shift exemplified how peripheral actors repositioned within transnational networks of utilities, railways and finance, where network position and institutional arrangements – rather than geographic location alone – determined economic viability.

Largest component of the Naples business network, 1861–80

Figure 3 Long description

The diagram is a complex network visualization representing the Naples business network from 1861 to 1880. It features numerous nodes and connecting lines, indicating various entities and their relationships. The nodes are color-coded, with clusters of different colors spread throughout the diagram, suggesting different communities or groups within the network. Lines connect these nodes, illustrating the interactions or connections between them. The layout is dense, with some areas more concentrated, indicating a higher number of connections. Text labels are present, identifying specific nodes or groups, but are not legible in this view. The overall structure suggests a web of interconnected entities, reflecting the integration of Naples into a broader European financial-industrial network during this period.

The opening of the Suez Canal in 1869 (dark blue community on the upper right side) crystallized the strategic logic of this reorientation by restructuring Mediterranean hierarchies and privileging Northern European shipping routes (Tang Reference TANG and Curli2022). Suez exposed the over-optimism about Naples’ traditional strategic maritime position (Giuntini Reference GIUNTINI and Curli2022). Local and international interests were forced to experiment with alternative pathways to global integration, which relied more on the control of infrastructural networks and financial intermediation as key assets than on commerce-based brokerage.

This shift towards an infrastructure-based convergence, still serving the realization of the Système de la Méditerranée, is clearly exemplified by the Compagnie Napolitaine d’Éclairage et de Chauffage par le Gaz (CNG) (dark blue community in central position) that emerged as the central hub through which multiple transnational BGs converged (Figure 3). Public utilities became the institutional interface of globalization, concentrating flows of capital, technology and managerial practices. This transformation was deeply rooted in the model of nineteenth-century large-scale infrastructure financing that required vast resources and sophisticated organizational forms exceeding individual states’ capacities. The legal instrument of concession à la française mediated technology transfer while establishing public–private governance arrangements (Bezançon Reference BEZANÇON1995; Barjot and Berneron-Couvenhes Reference BARJOT and BERNERON-COUVENHES2005; Guglielmi Reference GUGLIELMI2006). These concessions (resembling systems still nowadays adopted in Europe) functioned as financial instruments, allowing private concessionaires to recover advanced capital and amortize it through user fees, tolls, or loans guaranteed by contract (Veeser Reference VEESER2013), this way generating hierarchies of dependency through ostensibly contractual arrangements.Footnote 8

The new infrastructure-centred logic was embodied by the CNG’s founding BGs: Basile Parent’s Franco-Belgian BG and the Swiss high-finance group coordinated by Auguste Dassier (dark red community in the upper area). After unification, Parent entered Naples and founded the CNG by absorbing the Compagnia Pouchain, also mobilizing kinship-based coalitions – Adrien Louis Lebeuf de Montgermont, Eugène Blin, François Lavaurs and Henry Borguet (see Table 4) – clustered around the Parent and Schaken partnership and the Compagnie de Five-Lille (dark red community in the uppermost area),Footnote 9 a diversification platform spanning France, Spain, South America, Africa and Russia.Footnote 10 Crucially, kinship governance enabled survival across leadership transitions. When Parent died in 1866 and Schaken in 1870, the business group maintained structural centrality through lineage-based authority rather than collapsing (Schisani and Caiazzo Reference SCHISANI, CAIAZZO, Coffman, Lorandini and Lorenzini2018). Parallel to this, Auguste Dassier – through his nephews, the engineer Jean Daniel Colladon, and in the following period the banker Gustave Ador – extended Swiss influence in the CNG, reinforcing the BG continuity. The same mechanism of lineage-based institutional authority represented a recurrent mechanism of long-term financial coordination (Stoskopf Reference STOSKOPF2002). This kinship-structured governance was a fundamentally different mechanism of network persistence from the earlier brokerage model. Rather than relying on individual positional centrality, transnational BGs now embedded themselves through family strategies that ensured multi-generational control of critical infrastructure nodes.

Institutional learning and endogenous modernization, 1861–80

Table 4 Long description

The table lists 17 named actors and families, giving their origin or nationality, primary role, kinship ties, key companies or sectors, and stated contribution to modernization. Most figures are bankers, investors, or entrepreneurs, with a smaller set of engineers, architects, and politicians, showing finance-led modernization supported by technical specialists. Cross-border networks are prominent: Belgian, Swiss (Geneva), French, English, German-Jewish, and Neapolitan elites connect through marriage and extended family ties. Repeated organizations indicate hubs, especially the Naples gas utility company (CNG) and Société Générale, alongside Paribas, Crédit Mobilier, Naples Water Works, and Banca Napoletana. Several entries emphasize kinship governance and continuity, such as Parent linked to Lebeuf de Montgermont and Blin, and the Cahen d’Anvers and Bischoffsheim banking dynasties. Neapolitan actors (Persico, Gallotti, Cilento, Arlotta) are portrayed as adapting external models by founding or leading local banks and integrating political connections. Infrastructure sectors recur across entries—gas, water, rail, and public works—framed as channels for technology transfer and globalization interfaces. Interpretive labels like “bridge,” “hub,” and “modernization supporter” summarize authors’ assessments rather than providing quantified outcomes.

Stemming from Parent’s BG branching within the French and Swiss financial milieu, with its role in infrastructure financing, a second important network dynamic emerges leading to Naples’ full integration into international financial circuits and its subsequent banking modernization. Parent’s broader diversification strategy anchored Naples in the financial networks of Paris and Geneva through ties with the Cahen d’Anvers and Hentsch banking dynasties. These connections linked Naples to the Société Générale, Crédit Lyonnais and Paribas. Parent’s strategic roles – as shareholder and director in the Société Générale (1864) (Bonin Reference BONIN2006) alongside Meyer Joseph Cahen d’Anvers, father of Edouard (both located midway between their dark red community and the local dark blue and green communities), Edward Blount, Edouard Hentsch and Louis Bischoffsheim (all located in the upper part of the dark red community around their firms) – generated four major relational branches, each extending different forms of globalization across Naples and constituting distinct institutional pathways for capital circulation.

First, Paribas (1872) (dark red community in the upper right area) formed the core of a dense universal banking cluster with global colonial reach, spanning from Europe to the Middle East through the Banque Franco-Égyptienne and Banque Impériale Ottomane, and Asia including Banque de l’Indochine. Second, the Crédit Lyonnais (1863) emerged as the critical bridge to Geneva and Swiss finance, connecting to Compagnie Genevoise de l’Industrie du Gaz and directly to the Neapolitan gas industry through CNG (dark blue community in the central right area). This connection anchored Naples within Swiss financial circuits that would prove increasingly important as electricity challenged gas in the subsequent decades. Third, the CGE (1853)/CGEE (1879) (Compagnie Générale des Eaux and Compagnie Générale des Eaux pour l’Etranger) expanded the technical globalization of water infrastructure through Edward Blount’s Naples Water Works (1878), establishing Naples as a node within a distinct utility infrastructure network. Fourth, the Banca Napoletana (1871) (dark green in the lower central area) provided the local institutional translation of international banking models, creating an endogenous financial intermediary that replicated transnational BGs logics within the peripheral context. These four branches did not operate independently; rather, they formed an integrated portfolio through a complex system of cross-cutting interlocks in which Parent and his associates managed Naples’ insertion into multiple circuits of global capital simultaneously, that is financial speculation (Paribas colonial ventures), regional finance (Crédit Lyonnais), infrastructure development (water and gas) and local banking modernization.

International actors, strictly interplaying with local elites, moved fluidly across these relational branches, carrying capital, knowledge and organizational practices. This portfolio diversification resembling Chinese boxes enabled capital accumulation in one sector to finance ventures in another (Schisani and Caiazzo Reference SCHISANI and CAIAZZO2016), and represented a distinct evolution from the earlier phases where foreign brokers typically maintained separate roles in insurance, banking or commerce. In this period, the same actors embodied multiple sectoral positions, functioning as multilevel intermediaries who could mobilize capital across infrastructure domains. Within this process local elites progressively acquired positions across the network, transforming peripheral participants into co-managers of this multilayered structure. The institutional learning and adaptive capacity materialized as Neapolitan elites – families and agents such as Oscar Meuricoffre (dark red community in the centre of the graph), Leopoldo Persico, Antonio Cilento and his brothers Francesco and Federico, Domenico Gallotti (dark blue community), Eduardo Falconnet, Mariano and Enrico Arlotta (dark blue and dark green communities in the lower central area) (see Table 4) – gradually internalized BG models, shifting from maritime insurance towards investment banking and infrastructure finance (Schisani and Ragozini Reference SCHISANI and RAGOZINI2025). The Banca Napoletana became the operational hub of hybrid holding structures financing industrial construction (Impresa Industriale Italiana di Costruzioni metalliche IIICM), maritime credit (Cassa Marittima di Napoli), and storage logistics and utilities (Magazzini Generali), while simultaneously interlocking with northern Italian institutions like the Turinese Credito Mobiliare Italiano and with foreign BGs linked to the CNG.

Crucially, the modernization Naples’ banking did not appear as passive foreign imposition. By the 1870s, after a decade of political liberalization, Neapolitan elites did not simply receive capital and technology but actively participated in their adaptation to local conditions, their growing political roles both at local and national level, negotiating the terms of infrastructure concessions, and positioned themselves strategically within transnational networks. A small group of elite connectors through their positions in key state institutions (orange community in the upper left area) operated as obligatory passage points for transnational capital. In this setting, modernization unfolded through political intermediation, rather than bypassing it. Thus, Naples institutionalized long-term capital intermediation not through purely endogenous innovation, but under strong external influence, transforming its peripheral status into a strategic asset within transnational financial networks centred on infrastructure and investment banking.

VII

The period from the mid 1880s to the turn of the century marked the most acute phase of structural stress in the Italian financial system. The twin crises (1889–94) and collapse of Italian Crédit Mobilier-type institutions (Credito Mobiliare Italiano and Banca Generale) revealed the fragility of a speculative banking model dependent on weak monetary governance (De Luca et al. Reference DE LUCA, DI MARTINO and SCHISANI2025). Yet rather than indicating a slowdown in the integration process, the Naples network underwent a systemic transformation from external brokerage to internalized intermediation. In this period, changes in the network’s topology mirror broader geopolitical reconfiguration (Figure 4). The dissolution of the Latin Monetary Union (1878), the Triple Alliance with Germany and Austria–Hungary (1882), and the rupture of trade relations with France (1887) progressively pulled Italy, including Naples, away from its traditional French matrix of capital, realigning it towards the German industrial-finance model (Confalonieri Reference CONFALONIERI1974). As evident in Figure 4, the entrance of the Milan-based COMIT (Banca Commerciale Italiana, 1894) (dark red community in the lower area) and CREDIT (Credito Italiano, 1895) (dark blue community in the lower area), the first Italian German-type universal banks, fundamentally transformed the Naples network. Their dense interlocking directorates with Deutsche Bank, Berliner Handels-Gesellschaft, Wiener Bankverein, Credit-Anstalt, Credit Suisse (dark red community in the lower area) and Dresdner Bank (dark blue community in the lower area) established a northeastern vector of financial influence, replacing the earlier Paris–Brussels axis and reflecting Italy’s reorientation towards Central European finance.

Largest component of the Naples business network, 1881–1903

Figure 4 Long description

The scatter plot represents the largest component of the Naples business network from 1881 to 1903. The axes are not labeled with measured variables; instead, node positions reflect network layout, where proximity indicates relational closeness between entities. The network contains one dominant central cluster where nodes are densely packed, indicating a high degree of interconnection among a core group of entities. Several smaller clusters are distributed around this central mass, each appearing as a distinct grouping of nodes with visible spacing between them. Beyond these clusters, a large number of nodes are positioned at the periphery, sparsely connected to the main structure, indicating weaker or fewer ties to the core network. Node labels are present throughout the plot. Visible text labels include names such as Banco Nazionale nel Regno d′Italia, Banca Nazionale Toscana, Banca Toscana di Credito, Banco di Napoli, Societa Bancaria Italiana, Credito Meridionale, Banca Commerciale Italiana, Credito Italiano and several others, though many labels are small and partially legible at this resolution. Multiple distinct communities are visible within the network, each differentiated by a separate visual grouping. These communities are present across the central and lower portions of the plot. A legend identifying community categories by name is not visible in the image. The overall structure shows one large, tightly connected core, multiple mid-sized peripheral communities and many isolated or loosely connected nodes at the outer edges of the layout, indicating a network with a concentrated core and dispersed peripheral entities.

The most consequential structural shift occurred at the interface between global capital and local power, marking a clear reorientation of the local relational axis towards a political-financial elite, southern actors who held high-level institutional roles in both local and national politics (members of Parliament, senators of the Kingdom of Italy, ministers, and high-ranking officials of the central bank Banca Nazionale/Banca d’Italia, mayors, etc.). Figures such as Davide Consiglio (orange community) and Ignazio Florio, both in the COMIT’s Board, together with Fedele De Siervo, Leopoldo Persico, Gaetano Pavoncelli and Maurizio Capuano (all in the dark blue community) (see Table 5), became domestic gatekeepers. These members of the local elite had internalized brokerage functions previously completely monopolized by foreign interlockers. Foreign BGs still dominated the central hubs, but local elites occupied positions of genuine strategic coordination. Their betweenness centrality peaks capture a transition in brokerage that became institutionally embedded.

Crisis, transformation, and changing alliances, 1881–1903

Table 5 Long description

The table lists key people and institutions, giving their origin, primary role, family or elite ties, major company positions, and their strategic function in financial and utility networks. Neapolitan actors such as Davide Consiglio, Fedele De Siervo, Leopoldo Persico, Gaetano Pavoncelli, and Maurizio Capuano appear as domestic gatekeepers and brokers connecting local politics, banks, and utilities. Milan-based universal banks COMIT and CREDIT are presented as systemic hubs that restructure and modernize finance after crisis, with strong German and Austro-Hungarian interlocks. Swiss Geneva figures and vehicles, including Ernest Hentsch, Gustave Ador, Jean Daniel Colladon, and the Société Financière Italo-Suisse, provide cross-border capital and coordination, especially around utility consolidation and crisis resolution. Utility companies SGI and SME act as junction points linking shipping and finance to infrastructure, highlighting a transition from gas lighting toward electrification led by SME. Other Italian financiers from Turin, Trieste, and Florence are shown as temporary or bridging presences that extend northern and international models into the south. Strategic labels such as “gatekeeper,” “connector,” and “hub” are interpretive summaries rather than quantified measures, and the table emphasizes relationships and roles over exact dates or amounts.

This dynamic unfolded in the energy-utilities sectors, where the second industrial revolution had introduced electricity in competition to gas (Schisani and Caiazzo Reference SCHISANI and CAIAZZO2016). The reconfiguration of technological know-how and capital requirements elevated the significance of Swiss financiers and engineers. The Parent-Montgermont-Lavaurs coalition (clustered around the Fives-Lille) moved to the network periphery (dark blue in the peripheral lower right area), while the Swiss banker Ernest Hentsch’s Swiss BG emerged as the new technological and financial fulcrum (Paquier Reference PAQUIER2001), articulating Naples’ public utilities with electrical expertise from Geneva and Zurich (Schisani and Caiazzo Reference SCHISANI and CAIAZZO2016). The progressive takeover of the CNG by Ernest Hentsch positioned him as a strategic crossroads between local and Swiss gas and electricity companies (dark blue community in the lower area). His BG linked the newly founded Società Meridionale di Elettricità (SME) (1899), the CNG (both in the dark blue community) and the Società Generale per l’Illuminazione (SGI) (1875) (purple community in the central right area) with the Société Franco-Suisse pour l’Industrie Electrique (1898) (dark red community in the lower area close to COMIT) and the Société Financière Italo-Suisse (1902) (dark blue community in the lower right area), as well as the traditional Geneva gas companies. The formation of this enlarged BG relied on key non-occasional interlockers. Beyond prominent Swiss financiers, such as Gustave Ador and Jean Daniel Colladon, several members of Southern Italy’s elite played pivotal roles due to their institutional positions. Significantly, actors such as De Siervo, Persico, Pavoncelli and Capuano became major linkers across clusters, sitting on the boards of CNG, SME and SGI, brokering between international and local financial interests in gas–electricity competition. During this phase, these local actors reproduced the multiplex role of foreign actors described in the previous period. Their simultaneous participation in utilities, infrastructure and finance demonstrates how domestic gatekeepers achieved structural centrality not through monopolizing single positions but through critical roles spanning multiple clusters.

This period also witnessed the maturation of local corporate holding structures, enabled by the 1882 Commercial Code. The Società di Credito Meridionale (1885), evolving from the Banca Napoletana, became the very core of the Naples network (dark blue cluster in the core area), coordinating the city’s infrastructural modernization (maritime warehouses, harbour expansion, the Risanamento projectFootnote 11 and complementary rail networks). Its speculative activities finally triggered the 1889–94 crisis in the Neapolitan banking system that ultimately led to its liquidation in the early years of the twentieth century (Marmo Reference MARMO1976). Northern Italian entrepreneurs and bankers, such as Ludovico Arduin and Emilio Weiss (dark blue cluster), Ulrich Geisser and Giuseppe Morpurgo (dark red cluster close to CREDIT), had temporarily infiltrated this BG since the time of the Banca Napoletana, which explains the apparent reduction of foreign dominance, not by disengagement, but through diffusion of alliance structures.

Nevertheless, transnational finance did not retreat despite diplomatic realignment and banking crises. The enduring presence of the Blount-led Anglo-French group (NWW, CGEE) (dark blue cluster at the bottom) and Belgian groups linked to tramway construction (Société Anonyme des Tramways Napolitains – SATN) (dark red cluster on the lower left) (Dumoulin Reference DUMOULIN1990) demonstrates that financial globalization follows network logics, not national loyalties. Capital, once embedded in institutional arrangements and territorial relationships, persists and adapts across geopolitical ruptures.

The Naples network between 1880 and 1903 embodies a systemic transformation from external brokerage (from the core to periphery) to internalized intermediation (from periphery to the core). Integration persists, but the locus of strategic control shifted. Foreign capital remains structurally indispensable; yet domestic actors come to govern the interfaces where capital, technology and political authority converged. Path dependence persists through the enduring logic of BGs and the internalization of dependence on the core’s technical and financial culture. In this process, Naples ceases to be merely a peripheral node of international finance and becomes a selective producer of its own modernity. This transformation occurred just as Italy was approaching its economic take-off.

VIII

The evidence presented in the article suggests that the integration of peripheral economies into global capitalism of the nineteenth century can be better understood as a transformation in their relational architecture rather than as a simple inflow of foreign capital or adoption of modern institutions. The network perspective reveals that globalization operated through the emergence of structurally cohesive constellations of financial and entrepreneurial actors whose power lay in their capacity to reorganize the channels through which information, credit, control and political power circulated. In this configuration, finance had a foundational role. It was the domain in which cross-border coordination was first institutionalized, where brokerage positions acquired systemic relevance, and where asymmetries in access and influence became most visible.

The case study analysed shows how the globalization of a peripheral economy unfolded through a dynamic interplay between external financial logics and local mechanisms of absorption, translation and negotiation. What proved decisive was not the mere presence of foreign capital, but the construction of relational networks able to stabilize expectations, organize risk-sharing, and align local decision-making with the constraints and opportunities of international financial centres. Once financial interlocks and BG structures crystallized as the dominant mode of coordination, they generated a distinctive form of path dependence, shaping how technologies, institutions and political arrangements were subsequently incorporated into the peripheral context. Thus, this process of peripheral modernization was neither purely exogenous nor mechanically imposed; rather, it entailed institutional learning, strategic adaptation and the reconfiguration of local financial structures within enduring asymmetric power relations.

By foregrounding these dynamics, the findings suggest a conceptual reframing of peripherality as a historically situated reconfiguration of social and financial ties. A region becomes peripheral not because it lacks connections, but because the structure of its connections embeds it in asymmetric networks of financial intermediation. The persistence of brokerage positions concentrated in a limited set of actors – local and/or foreign – suggests that peripheral integration tends to reproduce hierarchical forms of globalization even as it facilitates modernization. In this sense, financial globalization is neither inherently emancipatory nor inherently exploitative. It can be intended as a dynamic process that acts through multiplex relational mechanisms, selectively empowering those positioned at the intersections of multiple circuits of capital and information. This conceptual perspective may extend beyond the specific case study, offering a framework for interpreting how other peripheral regions have been captured into global financial systems in the past, and why such insertions continue to generate both opportunities for development and enduring structural dependencies.

Appendix

Glossary of network terms and measures

Table A1 Long description