Introduction

Despite decades of land reforms in many developing countries, land institutions remain characterised by inefficiency, opacity, and fraudulent activities (Bujko et al., Reference Bujko, Fischer, Krieger and Meierrieks2016). In Ghana, for example, almost US$50 million has been spent on the Land Administration Project phase two to improve land administration, yet tenure insecurity and administrative inefficiencies persist (Alhola and Gwaindepi, Reference Alhola and Gwaindepi2024). Opaque land administration and transaction systems have created opportunities for fraudulent and illegal transactions, contributing to conflicts, particularly in rapidly urbanising areas (Kasanga and Kotey, Reference Kasanga and Kotey2001; Ouma et al., Reference Ouma, Musya and Weru2022). What institutional forms could effectively secure property rights in these countries where formalisation efforts have repeatedly fallen short?

Blockchain technology is a promising solution that provides a secure record-keeping system and enables the enforcement of property rights independent of third-party mechanisms (Allen et al., Reference Allen, Lane and Poblet2019; Allen et al., Reference Allen, Berg, Markey-Towler, Novak and Potts2020). However, its institutional dimensions in land transactions and administration as an institutional technology that reduces transaction costs (TCs) and facilitates efficient economic exchanges (Davidson et al., Reference Davidson, De Filippi and Potts2018; Ishmaev, Reference Ishmaev2017) remain underexplored. The dominant technological view of blockchain has contributed to its narrow application (Olbrecht, Reference Olbrecht2023), as most pilot projects in the land sector have not scaled (Owusu et al., Reference Owusu Ansah, Voss, Asiama and Wuni2023). Understanding its institutional dynamics is crucial to guide policy and private-sector interventions (Owusu et al., Reference Owusu Ansah, Voss, Asiama and Wuni2023).

This paper examines the extent to which blockchain addresses opportunism in urban land transactions, compared with existing institutions for transacting in urban land in Ghana. As an institutional technology, it meets the requirements of property without legal recourse and third-party enforcement and ensures that transaction records and system protocols are transparent and discoverable (Ishmaev, Reference Ishmaev2017). Consequently, we treat blockchain adoption as a comparative decision: which institutions best secure exchange partners’ property rights at the least cost? Drawing on Williamson’s (Reference Williamson1985) discriminant alignment hypothesis, we assess blockchain’s efficacy in minimising potential transaction-related hazards and safeguarding the interests of transacting parties relative to Ghana’s existing institutions for governing land transactions and isolate the nature of ex ante and ex post behavioural uncertainties in blockchain-based institutions across institutional types.

Ghana is well-suited for this study because it shares many features of developing economies: dual land-tenure systems, uneven administrative capacity across regions, rapidly growing urban centres, and persistent challenges with land tenure formalisation. Our findings could inform comparable contexts.

Institutions of Ghana’s urban land market

This section provides a brief institutional context for a blockchain-based land governance system to operate and compete. Detailed accounts of the urban land market and land reforms are available elsewhere (see, e.g., Alhola and Gwaindepi, Reference Alhola and Gwaindepi2024; Kasanga and Kotey, Reference Kasanga and Kotey2001; Mireku et al., Reference Mireku, Kuusaana and Kidido2016).

About 80–90% of Ghana’s undeveloped land is customary, historically owned and managed according to indigenous traditions and unwritten rules, with allodial title vested in families, first settlers or chieftaincies (Kasanga and Kotey, Reference Kasanga and Kotey2001).Footnote 1 Customary rights often involve multiple, overlapping claims to the same parcel, leading to multiple disputes and tensions (e.g., Lund, Reference Lund2004, for details). In the Greater Accra region, there are over 3,000 land litigation cases.Footnote 2 Persistent contested allodial authority among chiefs, first settlers and landholding families is a recurring source of conflict. Most land conflicts are intra-family (Kline et al., Reference Kline, Moore, Ramey, Hernandez, Ehrhardt, Reed, Parker, Henson, Winn and Wood2019). Customary institutions, their interpretation and implementation vary widely across the country, with no version necessarily representative of a particular community or ethnolinguistic group (Lentz, Reference Lentz2000).

Decades of land reforms favouring registration and the privatisation of land rights aimed at improving tenure security have yielded institutions with uneven effectiveness (Alhola and Gwaindepi, Reference Alhola and Gwaindepi2024). Broadly, land transactions either occur entirely within customary systems or are supplemented by statutory institutions through formal registration. Land registration is not compulsory because the Land Act 1036 (2020) recognises customary tenure and management. However, the customary land secretariats (CLSs) intended to support it have been largely dysfunctional: 62 of the 108 established CLSs are currently inactive. Customary enforcement mechanisms, including personal networks and reputation, are increasingly ineffective at safeguarding against ex post hazards. It is common for land title/deed holders to employ extra-legal contract-enforcement mechanisms, such as fencing the parcel to prevent encroachment and re-entry by the landlord. In major urban areas like Accra, landguardism (the use of thugs to protect land) has emerged to safeguard land rights.

Title registration under Torrens principles remains confined to registration districts in Accra, Tema and Kumasi, with no new registration districts declared. Within the statutory system, the processes for title/deed registration and property title transfer remain unclear, lengthy, cumbersome, and prone to record manipulation and corruption (Owusu and Boapeah, Reference Owusu and Boapeah2003).

Blockchain-based land transactions as a governance structure

Blockchain institutions (Davidson et al., Reference Davidson, De Filippi and Potts2018) offer an alternative to traditional transaction governance by reducing opportunism, uncertainty, information asymmetry, and inequality. As a digital technology for transactions and record-keeping, blockchain operates a decentralised algorithm, allowing transacting parties to transparently conclude transactions without a mediating trust party. It also eliminates the possibility of double payment for a single digital asset when the transaction is exclusively on-chain.

Blockchain, with its distributed architecture, consensus verification, immutable record hashing, timestamped transactions, enhanced transparency, and smart contract capabilities, offers useful affordances for land transactions (Ameyaw and de Vries, Reference Ameyaw and de Vries2020). These affordances provide a means to check opportunistic behaviours among land-transacting parties. The land attribute data (incl. location, owner’s name, and associated documents) is recorded, timestamped, and cryptographically hashed to other records for immutability. Parcels can be tokenised as non-fungible tokens (NFTs) on Ethereum and traded or exchanged via blockchain interfaces (Agbesi and Tahiru, Reference Agbesi and Tahiru2020). These NFTs enable interested parties to trade parcels. Prior to the addition of any record to this system, however, the initiation of the addition process sends the transaction in a decentralised way such that the parties to the transaction can verify its authenticity against the record on the ground (Figure 1). While off-chain data is still susceptible to misrepresentation, the transparency and traceability of blockchain records reduce opportunities for data manipulation once information is recorded on-chain. The consensus mechanism helps correct errors or oversights, preventing present and future land disputes. See Agbesi and Tahiru (Reference Agbesi and Tahiru2020) for the process of development of the system.

A generic blockchain working architecture/governance structure. Source: Lastovetska (Reference Lastovetska2021).

Figure 1. Long description

A flowchart illustrating the stages of a blockchain transaction process. The process begins with a transaction request initiated from a device. A block representing the transaction is then created. This block is sent to every node in the network. Nodes validate the transaction, and upon validation, they receive a reward for the proof of work. The validated block is added to the existing blockchain, completing the transaction.

Blockchain governance for land transactions has limitations. A major one is that the system is not self-aware of data authenticity. Because it cannot self-verify the authenticity of land information, Ameyaw and de Vries (Reference Ameyaw and de Vries2021) suggest using an off-chain oracle that involves an independent team of land-sector stakeholders, including public land-sector officials, private land-sector representatives, and representatives from all relevant stakeholder bodies, to verify data off-chain before onboarding.

Theoretical framework

Transaction cost economics (TCE) recognises that economic transactions occur in dynamic, uncertain environments characterised by technological change, knowledge imperfections, market fluctuations, and regulatory shifts (Laarabi and Chegri, Reference Laarabi and Chegri2022; Langlois and Robertson, Reference Langlois and Robertson1995). However, without opportunism, where parties tend to exploit the information asymmetries or manipulate transactions for personal gain, uncertainty will not create governance problems (Williamson, Reference Williamson1985). Contracts could be renegotiated as new information emerges.

Ex post incentive misalignment can increase monitoring, contract enforcement, and dispute resolution costs. The threat that one party may act deceptively forces the other party to incur additional TCs to protect against such behaviour. TCs are ex ante (e.g., due diligence, negotiating and drafting contracts) and ex post expenses (e.g., costs of contract policing and resolving disputes).

To reduce opportunism and its effects, actors choose specific governance structures – institutions and organisational arrangements – suited to the characteristics of each transaction (Williamson, Reference Williamson1985). In the land sector, governance structures determine how property rights are defined, exchanged and enforced (Deininger et al., Reference Deininger, Selod and Burns2012). Conventional land governance structures comprise formal institutions. In this paper, we classify Ghana’s predominant land governance institutions into two categories: customary (C) and customary-statutory hybrid (CS) (details in section Institutions of Ghana’s urban land market).

According to Williamson’s (Reference Williamson1985) discriminant alignment principle, transactions are matched with institutional arrangements that minimise total TCs. In land markets, simple trust-based exchanges could be adequately governed by customary institutions. Transactions involving high uncertainty or enforcement risks favour hybrid, statutory, or blockchain-based mechanisms. Blockchain adoption is thus a comparative governance choice and not a technical one.

Blockchain is not a socially neutral governance mechanism. Following Frolov (Reference Frolov2021), it is better understood as an assemblage of sometimes conflicting logics – technical protocols, economic incentives, ideological commitments to decentralisation, and ambient legal norms. Its ability to reduce opportunism and safeguard transactions depends on how these internal logics align or compete with existing governance arrangements.

The central premise of TCE is that governance structures and institutions are chosen discriminately – based on their cost and efficacy (Williamson, Reference Williamson1981). Thus, we assume that the adoption or use of specific mechanisms, blockchain-based or otherwise, is contingent on their efficacy in minimising TCs. For example, in ‘simple’ transactions, such as those between an indigene of a landholding family and the holding unit in rural areas, customary institutions (e.g., personal trust) could adequately safeguard one’s interests. There is no need for more complex structures or registration, unlike in urban areas with weak social and customary ties. A transaction involving non-indigenes often requires elaborate governance structures (statutory measures or, in addition, extralegal mechanisms such as land guards, i.e., thugs).

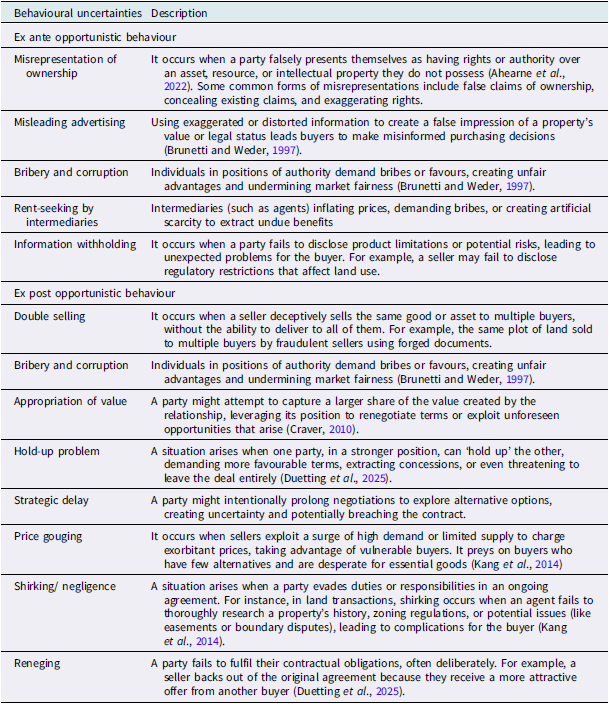

Table 1 summarises the common behavioural uncertainties relevant to land transactions, which form the basis for our comparative analysis.

Methodology

In examining opportunism, what people perceive is what they account for in their transaction governance decisions (Penrose, Reference Penrose2009). ‘If one is concerned with the effect of uncertainty on a firm’s behaviour, one is concerned with “subjective” uncertainty – with the entrepreneur’s state of mind – and subjective estimates of the risk of disappointment’ (Penrose, Reference Penrose2009: 52). This implies that a qualitative approach is suitable for our research. The scale of behavioural uncertainties (opportunism) is measured based on the authors’ experiences and supported by existing literature. The relative ranking of TCs across different contractual choices or governance modes is what matters for understanding governance choices (Wang, Reference Wang2003).

Specifically, we employed an analytical autoethnographic research design given the research objectives and the phenomenon studied. Analytical autoethnography enables us to fully explore the authors’ experiences of land transactions in informal contexts and the institutional mechanisms for safeguarding property rights. In analytical autoethnographic studies, ‘authors use their own experiences in cultural reflexivity to bend back on self and look more deeply at self-other interactions’ (Ellis, Reference Ellis2004: 46). The authors’ experiences, their interactions, feelings and thoughts, and what they see and hear as engaged members of the social group and context constitute the research data (Adams et al., Reference Adams, Ellis and Jones2017). Because the researcher’s experience is the data, they can tell their stories in ways unavailable to those without direct experience (Adams et al., Reference Adams, Ellis and Jones2017).

For our purposes, analytical autoethnography is particularly useful because people are not expected to say in an interview, ‘I delayed signing a deed to extract a bribe’. Analytical autoethnography has three tenets. The researcher must be a full member of the research setting, visible as such in published texts, and committed to developing theoretical understandings of broader social phenomena (Anderson, Reference Anderson2006).

Data collection spanned 2019–2020 and 2023 across Accra, Kumasi, Sunyani, and Wa. These were the cities where researchers acquired land, covering two of Ghana’s largest and two mid-sized cities, providing extensive coverage of the country’s urban land landscape. As part of their acquisition process, each researcher collected field notes, site observations, and notes from interactions with stakeholders, from engaging with customary landowners to deed registration and observing others’ transactions. This process yielded four independent sets of observations and experiences, enabling triangulation across sites, thereby reducing the risk of oversights or omissions. All acquisitions were family lands. All authors are also active researchers in land governance in the country.

The identified behavioural uncertainties (outlined in the theoretical framework and Table 1) were individually ranked by the authors. The subjective ranking relied on the researchers’ academic knowledge, targeted literature review and notes from their firsthand experiences. The results were then discussed among the authors and aggregated in Tables 2 and 3 and supported by evidence from the literature. The ranking is classified as ‘++’, ‘+’ and ‘0’.

Common opportunistic behaviours in land transactions

Table 1. Long description

A table with two columns, behavioral uncertainties and descriptions, detailing various opportunistic behaviors in land transactions in developing markets. The table includes behaviors such as misrepresentation of ownership, misleading advertising, bribery and corruption, rent-seeking by intermediaries, information withholding, double selling, appropriation of value, hold-up problem, strategic delay, price gouging, shrinking/negligence, and reneging. Each behavior is described in detail, explaining how it occurs and its impact on land transactions.

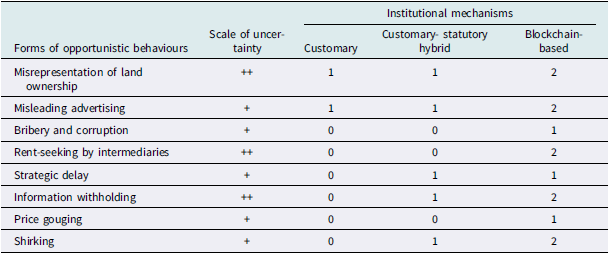

Ex ante opportunistic tendencies buyers face in urban land transactions and governance efficacy

Table 2. Long description

A table with 8 rows and 5 columns compares various forms of opportunistic behaviors faced by buyers in urban land transactions. The columns include Forms of opportunistic behaviors, Scale of uncertainty, Customary, Customary-statutory hybrid, and Blockchain-based. Each row lists a specific behavior such as Misrepresentation of land ownership, Misleading advertising, Bribery and corruption, Rent-seeking by intermediaries, Strategic delay, Information withholding, Price gouging, and Shrinking. The scale of uncertainty is marked with plus signs indicating low or high uncertainty. The institutional mechanisms columns show rankings of 0, 1, or 2, indicating the effectiveness of each mechanism in mitigating the behaviors. Notable trends include higher rankings for Blockchain-based mechanisms in addressing Misrepresentation of land ownership, Misleading advertising, and Rent-seeking by intermediaries.

Note: Uncertainty key: Present to a substantial degree ++; Present +; 0 presumed to be absent.

Efficacy scale: 2 = effective, 1 = somewhat effective, 0 = ineffective.

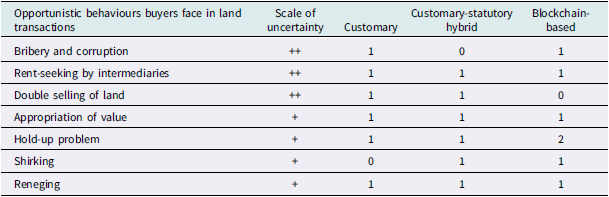

Ex post opportunistic behaviours buyers face in urban land transactions and governance efficacy

Table 3. Long description

The table compares opportunistic behaviors buyers face in land transactions across different systems, including customary, customary-statutory hybrid, and blockchain-based systems. It has seven rows and five columns. The columns are labeled ‘Opportunistic behaviours buyers face in land transactions’, ‘Scale of uncertainty’, ‘Customary’, ‘Customary-statutory hybrid’, and ‘Blockchain-based’. The rows list specific behaviors such as ‘Bribery and corruption’, ‘Rent-seeking by intermediaries’, ‘Double selling of land’, ‘Appropriation of value’, ‘Hold-up problem’, ‘Shirking’, and ‘Reneging’. Each behavior is ranked according to the scale of uncertainty and the presence or absence of the behavior in each system. Notable trends include the presence of bribery and corruption in all systems except the customary-statutory hybrid, and the absence of double selling of land in the blockchain-based system.

Uncertainty key: Present to a substantial degree ++: Present, +: 0 presumed to be absent.

Efficacy scale: 2 = effective, 1 = somewhat effective, 0 = ineffective.

Ranking scale:

‘++’ indicates strong consensus – both among the authors and within existing studies – that this behavioural uncertainty is pervasive.

‘+’ denotes clear evidence of its presence, though with less unanimity or depth of impact.

‘0’ implies that the uncertainty is presumed absent or negligible, either because it rarely manifests or is unsupported by literature.

To illustrate, in Wa, the lands acquired and registered were later threatened with loss because other family members from whom the lands were initially acquired sold the plots to another person, who immediately began developing the site. This situation required police intervention at a cost (non-market TCs) to reclaim the land, despite a deed being in place. To reduce police costs, the other family members were paid off (an amount equivalent to half the land’s initial purchase price), thereby closing the matter. Authors commonly observed the threat of ex post disposition in their respective areas. The lands in Kumasi and Accra were immediately developed after acquisition to prevent disposition risks. Our experiences also align with published research reports, as detailed in Analysis and findings. The scale of uncertainty about ‘multiple land sales’ at the ex post stage is thus rated ‘++’.

This subjective – but systematically applied – classification highlights which opportunistic risks are ingrained in Ghana’s multi-stakeholder land system, where overlapping claims and informal practices dominate. A similar approach was used to evaluate the institutional competencies of the various governance structures.

Analysis and findings

Ex ante behavioural uncertainties buyers face in land transactions

This section presents a comparative analysis of the efficacy of the three governance structures relative to the identified opportunistic tendencies of actors in land transactions. Table 2 presents the extent of ex ante (pre-sale) uncertainties that buyers face. For each score on the uncertainty scale, we provide the detailed justification. The scores in Tables 2 and 3 are to be interpreted comparatively with respect to the other governance structures. The efficacy scores are not absolute or indicative that any governance structure eliminates opportunistic behaviour but relative to other structures.

Ownership misrepresentation and information withholding in the urban land market typically manifest as boundary and family disputes and as fraud by agents, vendors, and subsequent owners (Appiah, Reference Appiah2012). Title fraud is common in the Greater Accra Metropolitan Area, where some vendors reportedly forge property titles and sell land or ‘ghost properties’. The Ghana Police Service warns, ‘Don’t rely on the document you are given by the Landlord’,Footnote 3 highlighting the propensity for property title forgery. The 70 property-related fraud cases reported weekly by the Property Fraud Section of the Ghana Police ServiceFootnote 4 are likely an underestimate, as many cases go unreported. From October 2001 to March 2005, multiple sales or sales by a person/agency without title to the land constituted about 13% of the land dispute cases filed in the country’s courts (cited from Kline et al., Reference Kline, Moore, Ramey, Hernandez, Ehrhardt, Reed, Parker, Henson, Winn and Wood2019).

Similarly, family ownership is nuanced. People can strengthen their claims to family lands by supporting other family members, through inheritance or by acting as if they are the owners (Berry, Reference Berry2023). Thus, one may be dealing with the rightful family but not the right person within the family unit to allocate land because that right is often internally contested (Evans et al., Reference Evans, Mariwah and Barima Antwi2015). In the Wa case, for instance, different factions of the same family later claimed the right to dispose of the family land. Gyapong (Reference Gyapong2021) similarly illustrates how, in the Eastern region, increased land commodification has led to power grabs by a select few family members, often disadvantaging other members. An example is the Boateng Vrs Mckeown Investment Ltd. [2020] GHASC 3 (5 February 2020) case. The plaintiff (Dora Boateng) acquired and registered the land from Kwame Kissiedu Kwaasi, who claimed to be the family head and lawful representative of the Kissiedu Kwaasi Family. McKeown also claimed to have acquired the land from Naggesten Farms, which had initially purchased it from a family at Larteh, to which Mr Kwaasi (the plaintiff’s grantor) belongs and is its secretary. The dispute reached the Supreme Court. In delivering the judgement in favour of Boateng, the Supreme Court’s decision noted, ‘innocent purchasers . . . no matter how diligent their inquiries, are always susceptible to falling victim to unscrupulous members of families . . . who indulge in multiple sales of land’ (Boateng Vrs Mckeown Investment Ltd. [2020] GHASC 3 (5 February 2020), 2020: 19). Thus, ownership misrepresentation is scored ‘++’ (Table 2).

Land-related disputes are common, especially in urban areas. While lands vested in chiefs are less prone to vendor fraud, intercommunity boundary contestations are on the rise (Kansanga et al., Reference Kasanga, Cochrane, King and Roth1996). About 3,744 new land cases were filed in the country’s high courts in the 2022/2023 legal year, of which only 16.23% were resolved, with an overall total of 14,000 cases still pending (Ghana Judicial Service, 2024). There are instances in which courts have been misled by falsified information provided by families seeking to assert ownership.Footnote 5

Price gouging and strategic delay in practice are less common, albeit related. If there are multiple buyer interests in a parcel of land, the landowner tends to delay the transaction as they ‘sniff’ for higher price offers. This practice is partly due to the unreliable and inadequate comparable market data available. One instance observed by researchers involved a buyer who was shown a plot but later told by the seller that he had mistaken it for his own, even though it belonged to his sister, who had already sold it. The buyer was offered a less desirable replacement. Apparently, a subsequent buyer had offered more for the original parcel because it was sandwiched between two plots, which will reduce the cost of building a fence wall, as the other owners will build theirs. In this situation, price gouging was not about increasing the price but about giving the land to a subsequent high bidder, contrary to the initial verbal agreements, and replacing it with something else.

Misleading advertising is not common. However, unlicensed real estate agents are prevalent, contributing to scams and fraudulent real estate transactions (Obeng-Odoom, Reference Obeng-Odoom2009).

Efficacy of governance institutions at the ex ante transaction stage

We assess how well the governance structures could address opportunistic behaviours if they were to arise. Could they effectively minimise escalation risks and resolve hazards?

For 50% (4 of the 8) of the itemised opportunistic behaviours a land buyer faces in transacting land, the blockchain system arguably has a superior capacity to address them compared to existing institutional mechanisms (Table 2). For example, blockchain requires that ownership issues be resolved before a parcel can be listed for sale. Utilising a blockchain system requires parties to clarify any ambiguities regarding ownership before the land is on-chain, safeguarding potential buyers from information asymmetries and misleading advertising. Any encumbrances on the land can be easily obtained, even if the seller wishes them to be concealed, because they are easily traceable on a digital system that incorporates live land-related data, including pending court cases. This advantage is not readily available with customary or statutory transactions. While transacting state-owned lands is relatively safe (albeit disproportionately benefiting the rich and politically connected (Gillespie, Reference Gillespie2016), a title/deed check at the Lands Commission only applies to registered land transactions. As such, a ‘negative’ search result means that a parcel is unregistered, not that it is unsold. In such instances, there is no single source of truth. There is also evidence that a deed/title search at the Lands Commission can return different owners. In the Boateng v. McKeown Investment Ltd. [2020] case,Footnote 6 two official searches to establish the genuine owners of the land returned fourteen different sellers’ names who sold the land between 1984 and 2014. This weakness increases the scale of due diligence a buyer must undertake to transact land safely. However, none of the authors encountered a land search involving multiple owners.

Where the land has never been registered, one must rely on the seller’s word of mouth as evidence of their legitimacy as the owner or representative. Chiefs have been reported to sell communal land without regard for the communal interest, leading to confrontations (Okeyere and Bedu, Reference Okyere and Bedu2024; Lanz et al., Reference Lanz, Gerber and Haller2018). This situation undermines the effectiveness of customary institutions in safeguarding the rights to transacted land. It also necessitates the use of multiple institutional mechanisms to safeguard one’s interests. Such mechanisms include personal relations, networks, and statutory institutions. Buyers often rely on customary and statutory mechanisms in urban areas to access statutory enforcement and formal-sector institutions such as banks (Edwin et al., 2020).

Similarly, a blockchain system is better able to minimise rent-seeking behaviour by enabling direct exchanges between the seller and buyer. These include informal and formal intermediaries involved in the land acquisition process. Each stage of the buying process is thus susceptible to rent-seeking. Indeed, one cannot customarily access the chief palace without an intermediary.

We contend that the current customary and customary-statutory institutional mechanisms have limited effectiveness in addressing ex ante opportunism without substantial additional TCs. Fundamentally, these trust mechanisms can generate private benefits from misalignment. Gyapong (2021) and Kasanga and Kotey (Reference Kasanga and Kotey2001) argue that the commodification of land and the land reforms have reduced the capacity of customary land institutions to adequately resolve challenges in the land market. However, as Table 2 shows, blockchain has limitations. Even smart contracts cannot address strategic delay more effectively than CL. There is a risk of off-chain bribery and corruption, especially within public institutions that must complete specific tasks in the land registration process (e.g., preparing cadastral plans and registering titles and deeds). While smart contracts ensure that contracts are self-enforcing, the possibility that actors want to be ‘facilitated’ to act exists, and it is not different from the existing title and deed search and registration processes at the Lands Commission. As UNODC (2022) shows, the commonest reason for paying bribes (44.4%) is to expedite or finalise an administrative procedure. There is no reason to suggest that a blockchain system can address this risk unless an act is deemed completed after a specified period has elapsed. Even then, individuals can request additional time or initiate preliminary steps to circumvent the trigger clause, thereby prolonging the process.

Importantly, the advantages of blockchain require off-chain institutional reforms to clean up land data and resolve boundary and ownership issues, among others, before a blockchain system can be implemented. Such off-chain investments will also help reduce the weaknesses of existing land governance structures. When existing land governance structures are weak, the benefits of blockchain as a trust institution are reduced.

Ex post opportunistic behaviours in land transactions and the efficacy of governance institutions at addressing them

Table 3 indicates opportunistic behaviours are prevalent post-transaction, particularly double sales and reneging. These behaviours are mainly associated with land sellers, intermediaries and land professionals involved in post-transaction processing, although buyers are not exempted.

In our experiences, obtaining a deed took 1-2 years to register. Bribery, corruption, and rent-seeking in land acquisition are rated ’present to a substantial degree’ (Table 3) because ‘facilitation’ was noted across the deed registration process in the form of ‘take this for water, lunch or fuel’. Several studies (Kasanga and Kotey, Reference Kasanga and Kotey2001; Sittie, Reference Sittie2006) have reported inefficiencies in the land registration process and ‘facilitation fees’ (dressed-up bribes). The Lands Commission is the fourth-most-corrupt public institution in the country (UNODC, 2022), with an average bribe size of GH¢1,669 per individual officer (UNODC, 2022). The officials, directly or indirectly, requested 75% of all bribes paid to public officials. This finding suggests that power imbalances and weak institutions enable public officials to solicit extra-legal payments before providing services. Edwin et al., (Reference Edwin, Glover and Glover2020) report that creating cadastral plans and maps for land conveyancing is a key stage for corruption in securing land titles/deeds, often involving officials and their associates. It should be noted that personal relationships with staff seem to mediate the need for ‘facilitation’. ‘If you know someone at the Survey department, they can help you get things done quickly’, one co-author observed.

The lengthy and sluggish land registration process has led to increased broker involvement, increasing inefficiency and rent-seeking. However, rent-seeking and corruption are not limited to state institutions. Acquiring stool land often involves several stages and intermediaries. In the Ashanti Region, for example, there are two chiefs (sub and divisional chiefs) involved in the process before registration with the Otumfuo’s (overlord of the Ashanti) customary land secretariat. While the transacted price is supposed to be shared equally (1/3 each), lower levels have been known to charge exorbitant fees and re-enter sold lands (Mintah et al., Reference Mintah, Boateng, Baako, Gaisie and Otchere2021; Nyabor, Reference Nyabor2023). Four subchiefs were destooled in 2023 for involvement in various land fraud, including selling the same land to multiple buyers in the Ashanti Region (Nyabor, Reference Nyabor2023). Chiefs have been reported to sell communally owned land without consulting existing users, leading to community members’ dissatisfaction and confrontation (Okeyere and Bedu, Reference Okyere and Bedu2024). Among 286 land purchasers in Accra, only 1 completed the titling process because the actual cost of titling was significantly higher than official fees, owing to intermediaries’ rent-seeking behaviour (Antwi and Adam, Reference Antwi and Adams2003).

A blockchain system, on the other hand, presents some opportunities. While it cannot eliminate bribery incentives, blockchain digitises land processing using smart contracts. Blockchain’s consensus mechanism enables various forms of procedural oversight. However, off-chain activities fall outside the scope of blockchain. Thus, complementary to blockchain’s on-chain potential to address bribery and corruption, there is a need for off-chain efforts to curb corrupt activities that may occur off-chain.

Rent-seeking by intermediaries and the appropriation of value are somewhat addressed more effectively through blockchain governance than through statutory and customary governance structures in principle. However, due to the low levels of literacy and technological awareness of landowners, we posit the emergence of new intermediaries because of blockchain (Table 3). In one of the acquisitions (author’s experiences), the real estate agent who facilitated the transaction later demanded additional fees after the purchase was completed. When the researcher declined to pay, the agent used thugs to prevent access to the land or to carry out any developments. To avoid further conflicts and to access the land that had already been paid for, the researcher paid the additional amount demanded (totalling approx. 15% of the land’s price). However, it was not part of the original agreement in engaging the agent and exceeded the negotiable 10% commission that agents charge.

Blockchain limits intermediaries by directly connecting landowners with buyers and official stakeholders. The efficacy of blockchain in this regard depends on stakeholders’ commitment to processing land within the blockchain governance framework. When stakeholders boycott the system to engage off-chain, the system cannot address bribery and corruption, value appropriation, and rent-seeking behaviours. The full potential and efficacy of blockchain in resolving these ex post transaction opportunistic behaviours thus depend on stakeholders’ acceptance and commitment to transact within the decentralised system’s governance and on their acknowledgement of the risks of transacting off-chain, which can be misaligned with their self-interest.

Multiple selling is more common in Accra and Kumasi, the prime urban centres, but was also experienced in Wa. The situation is pronounced in that many prospective land buyers now resolve to develop the land immediately after concluding transactions with customary authorities, before registering the deed or obtaining development permits (Eshun and Asibey, Reference Eshun and Asibey2024). It is often during the lengthy land registration process that dishonest customary land sellers conspire to resell the same piece of land to other purchasers. To address this, however, results from Table 3 show promises from both the customary and statutory governance structures, as well as from the blockchain governance structures.

By adopting diverse verification approaches, prospective buyers reduce the risk of being victims of double sales within customary and statutory governance structures. For instance, in a customary sale, prospective buyers may privately enquire about the status of the land from other members of the family or the stool purporting to sell the land. Additionally, in both statutory and customary contexts, prospective buyers could visit the land to enquire from neighbouring landowners whether they had seen the sellers visit the land with other people they suspected were potential buyers. Information from these means and sources can assist due diligence and further probe whether the land has already been sold to another buyer. Accordingly, both systems, through their social embeddedness, provide some protection against double sales, although they do not eliminate the possibility. In our experience, social embeddedness was crucial to due diligence in minimising opportunism.

A complete on-chain governance structure can eliminate double sales by redirecting any subsequent actions on a parcel to the original transaction, making ownership, encumbrances, and required consents immediately visible. This reduces the need for costly pre-transaction due diligence and enables more informed buyer decisions. This is an advantage over both customary and statutory structures. However, this advantage holds only when all dealings are on-chain, with no parallel off-chain processes. That notwithstanding, current leases and deeds with access to thirdparty enforcements often inadequately secure property rights, which significantly weaken the promises of blockchain. An example is the Wa experience.

Reneging occurs when a seller (or buyer) withdraws from the initial transaction and then refunds the money received from the first buyer because they have taken, or seek to take, a higher sum from the supposed second purchaser. One of the researchers observed this in Sunyani.

For both hold-up and reneging issues, all governance mechanisms have similar efficacy. Although blockchain is superior in dealing with hold up, this is conditional only on on-chain transactions. Because blockchain governance systems are effective at preventing dishonest and crafty behaviour, such sellers are unlikely to be interested in transacting through them. As previously mentioned, in customary urban areas, land sellers are aware of the potential for better deals owing to the high demand for their land. However, when transacting such deals under statutory or customary frameworks, these systems offer actors the opportunity to seek social interventions, such as seeking a court order for specific performance. Moreover, alternative solutions, such as customary arbitration, could also be considered to resolve hold-up and reneging problems.

For shirking challenges, both the statutory system and blockchain are identified as being partially effective. Lessees can conduct an official search of the land with the Lands Commission, rely on information supplied by sellers and their social networks, or do both. Although not always reliable, title/deed searches offer a sound basis for due diligence. Dishonest sellers may also withhold significant information from prospective buyers, leading to post-transaction challenges. Conversely, the blockchain governance structure enables tracking all historical transactions related to a piece of land, clarifying ownership and delineating the rights associated with it. This functionality helps eliminate information hoarding on these matters and mitigates the potential for challenges.

Discussions and conclusion

The study examined the efficacy of blockchain as an institutional technology for safeguarding land transactions compared with customary and statutory institutions in Ghana. The study offers at least three essential insights and contributions to the literature. The first is that, at the ex ante stage in land transactions, blockchain institutions were generally better at addressing opportunism than existing mechanisms, which are vulnerable to manipulation, as seen in Boateng V McKeown Investment Ltd. [2020] GHASC 3 (5 February 2020). Customary institutions were the least effective at addressing behavioural uncertainties in urban land transactions. With the challenges of land registration, the prevalence of lessees facilitating the title/deed registration of their urban land provides sufficient evidence of the additional benefits of distributed ledger technology (DLT). Blockchain land governance is less susceptible to incentive misalignment, offering a safer alternative in urban land markets.

However, blockchain’s ex ante effectiveness depends on resolving fundamental off-chain issues, such as boundary disputes, before the land is digitised and on-chain. These challenges also affect existing institutions. The difference is that once these issues are resolved, the opportunities for ex ante incentive misalignment are relatively minimised for DLT. In the case of existing structures, the opportunities persist due to weaknesses in third-party structures and openness to selfish personal exploitation (Ameyaw and de Vries, Reference Ameyaw and de Vries2020).

The second is that blockchain is weak at the ex post stage. After the land is acquired, the risks of resale, family disputes, rent-seeking, and litigation are often high. Blockchain’s decentralised contract enforcement becomes a liability in resolving such disputes. Requiring third-party enforcement defeats a core advantage of blockchain, reducing it to an immutable record-keeping technology that can be easily abandoned by beneficiaries of opportunism. Customary and statutory institutions, albeit with varied weaknesses, offer social and legal recourse (e.g., customary arbitration), which blockchain lacks. The risk of losing your land or engaging in protracted land litigation is a significant concern for any lessee.

Thirdly, our findings do not support existing studies such as Mintah et al., (Reference Mintah, Baako, Kavaarpuo and Otchere2020), Mintah et al., Reference Mintah, Boateng, Baako, Gaisie and Otchere2021, and Agbesi and Tahiru (Reference Agbesi and Tahiru2020) proposed blockchain governance as a solution to land challenges in developing countries. At best, it is a partial solution, as the opportunistic risks buyers face persist. Frolov’s (Reference Frolov2021) arguments are, however, supported because to be fully effective, especially at the ex post stage, blockchain institutions would require hybrid or conflicting institutional logics.

Despite the inefficiencies associated with statutory and customary systems, there is a crucial distinction that influences buyers’ choices in governing their land transactions. The inefficiencies in public institutions are predominantly procedural, e.g., delays and administrative discretion, which give rise to expensive TCs as noted in our experience and the broader literature (see sections Institutions of Ghana’s urban land market and Analysis and Findings). However, registration gives the lessee access to statutory enforcement. In the Wa case, the police intervened in the researcher’s favour because they had a deed.

Customary enforcement, especially at the family level, differs because it embeds a conflicting incentive. Secure land transactions reduce opportunities for opportunistic rent extraction for an asset in fixed supply. Reselling or reallocating the same plot is financially attractive and allows multiple family members to extract gains from the same parcel, rather than once every 99 or 50 years, depending on whether the lease is for residential or commercial use. Every prospective buyer anticipates these risks and therefore prioritises prompt land registration; quickly developing the land (e.g., building a fence wall), as used by the researchers in Accra and Kumasi; or using extra-legal mechanisms for additional protection. The choice of governance structure is predicated on anticipated transaction risks and the ability to safeguard the buyer’s interests.

In terms of research contribution, this study is among the first to move beyond the dominant technological lens through which blockchain has been examined in the literature. Land governance is fundamentally an institutional challenge that requires an institutional lens, a call that Owusu et al. (Reference Owusu Ansah, Voss, Asiama and Wuni2023) reiterated. The study operationalises recent theoretical and conceptual research (Allen et al., Reference Allen, Lane and Poblet2019; Davidson et al., Reference Davidson, De Filippi and Potts2018) on the potential of blockchain as an institutional technology that offers new ways to coordinate economic activities. By doing so, we provide evidence of blockchain’s limits, which illuminate why many pilot projects might have failed. Our findings provide contributory evidence for failure and admonish that the institutional limitations of blockchain must be addressed to improve adoption success and secure property rights. By taking a comparative approach, our findings challenge the notion that blockchain is a superior governance mechanism to existing ones. The study also provides a realistic framework for understanding blockchain, treating transacting actor behaviour explicitly as potentially opportunistic, challenging the techno-rationalist assumptions prevalent in existing research that adoption follows from technical efficiency. It extends Williamson’s (Reference Williamson1985) TCE by demonstrating how blockchain can serve as an alternative governance mechanism that reduces TCs but varies in its efficacy at mitigating opportunistic behaviour in land transactions.

Is blockchain as land governance dead?

Studies such as those by Mintah et al., Reference Mintah, Baako, Kavaarpuo and Otchere2020 portray blockchain as a ‘panacea’ to the problems in Ghana’s land market. Our findings challenge this view. If buyers with land titles/deeds still face litigation and rent-seeking, there is no reason to think that a digital token would safeguard them from these issues. Blockchain has superior capabilities to mitigate some ex ante opportunism, as we showed. However, even at this stage, blockchain requires off-chain resolution (e.g., resolving boundary disputes, ownership documentation and verification) before on-chain transactions can be reliably executed. Suppose customary and statutory governance systems enjoy the same pre-transaction resolutions; the need and comparative advantage for blockchain would reduce to enhancing transaction speed.

Blockchain’s core value proposition is ‘trustless’ automation – smart contracts that self-execute without third-party enforcement. However, in land transactions, occasional disputes are inevitable due to inheritance, encroachment, and fraud, requiring human adjudication and third-party enforcement, which trustless automation cannot address or enforce for physical assets.

Conclusion

This study is among the first to examine, comparatively, the institutional dynamics of blockchain in land transactions. At the ex ante stage, blockchain has advantages over customary and statutory systems. However, realising them requires off-chain institutional solutions first before blockchain can be effective. Fixing existing institutional weaknesses requires institutional policy reforms such as harmonising customary and statutory land administration, developing a national land information infrastructure, strengthening customary land secretariats, and streamlining land registration procedures. Yet, if these reforms were successfully implemented, the case for blockchain governance would be significantly reduced. After the exchange, blockchain faces severe limitations and outperforms existing mechanisms in only one of the seven risk areas examined. Despite its technological superiority, blockchain as an institutional technology is weaker than it is often portrayed for land transactions.

Our findings illuminate why tokenised land projects have struggled to scale despite blockchains’ advantages. Our findings suggest that much of the enthusiasm for blockchain-based land governance rests on a category error: extrapolation from purely digital assets, where property rights can be secured cryptographically. Land is a physical, rival asset, and post-transfer rights are vulnerable to encroachment or contestation regardless of how transparent or tamper-resistant the registry is. Thus, blockchain requires complementary third-party institutions, especially contract enforcement institutions, to be effective. This finding exposes a core tension. Blockchain seeks to remove third-party enforcement, but without it, blockchain becomes substantially less effective than existing institutions in safeguarding property rights. If opportunism persists when actors are cognisant of legal and customary enforcement mechanisms, what would they do without these institutions, as DLT proposes? Despite the deficiencies of statutory and customary land governance, access to third-party enforcement capabilities remains attractive to anyone transacting land in urban areas. As researchers, we would be reluctant to transact without access to third-party enforcements.

Blockchain adoption decisions should be comparative, weighing its benefits, efficiencies, and costs against those of existing institutions, especially in jurisdictions where costs, scalability, technology infrastructure, network effects, and inadequate technical expertise are key constraints. While a hybrid approach leveraging blockchain’s ex ante capabilities and addressing its ex post weaknesses is reasonable, ‘hybridity’ should be a comparative decision. Future studies should quantify the benefits and costs of a hybrid approach relative to improving existing institutions and the specific components of an effective institutional hybrid. Our position is that immutability, improved transaction speed and reduced TCs are insufficient to justify adoption for conventional land transactions in developing markets. Another recommendation is to examine blockchain from a property rights theory lens – how land rights are defined, encoded, and transferred on a DLT and how they interact with existing tenure.

Our findings are context-specific and may not generalise beyond Ghana, although the TCE framework and the value of an institutional lens for examining new institutional technologies are replicable in other contexts. The autoethnographic method carries a risk of confirmation bias and selective recall, and the researcher’s experiences may be less representative of the population. Our tripartite approach partly mitigates these weaknesses by grounding personal experiences in existing literature and theory.

Open access

Open access