I. Introduction

Mergers and acquisitions (M&As) can be an important source of productivity gains in the economy. Although synergies are pointed out as one of the primary drivers behind these gains, the literature examining how synergies materialize is still evolving. Because M&As may also be motivated by factors unrelated to efficiency, such as increases in market power, it is essential to identify the channels through which efficiency gains arise and the conditions under which they are most pronounced. Such evidence is critical for assessing when efficiency considerations prevail over alternative motives.

We add to this literature by focusing on efficiency gains that stem from the substantial expansion of internal labor markets that occurs after these transactions. These gains can be particularly sizeable when the firms involved in the operation are large and possess multiple establishments, such as retail chains. We document how newly formed consolidated firms exploit their expanded pool of human resources to redesign their organization, relocate internal resources, and boost efficiency.

Documenting the role of internal markets in the creation of efficiency gains post-consolidation is challenging. First, it requires matched establishment-employee labor data to trace worker movements within the newly formed firm. Second, it requires metrics of establishment-level productivity before and after the consolidation. Finally, as M&As lead to increases in concentration, it is important to rule out that changes in productivity proxies (such as profitability) derived from revenue and expenditure data are attributable to enhanced market power in both input and output markets (e.g., De Loecker and Syverson (Reference De Loecker and Syverson2021), Arnold (Reference Arnold2020)).

The M&As of large banks in Brazil in the late 2000s provide an ideal setting to overcome these challenges. First, using matched employee-branch data along with branch-level financial information, we are able to track how these firms allocate their inputs across the branch network. Second, we can build branch-level productivity measures before and after consolidations and control for different measures of market power gains. Finally, using pre-M&A ownership information, we classify branches as target or acquirer branches, and, despite establishment identifiers changing after a consolidation, we continue to follow branches using their transaction-invariant address. Therefore, we can document heterogeneous effects on the acquirer and target branches and track employment flows from target to acquirer branches and vice versa.

We focus on consolidations of large private banks that have an extensive branch network and operate in several local markets. An M&A involving institutions with these characteristics has several attractive features. First, a single M&A event leads to different increases in local market shares, depending on the position of the acquirer and target firms before the consolidation. As a result, we can include as controls heterogeneous gains in local market power and reduce concerns that increases in profitability are explained by higher markups in output markets or markdowns in input markets.Footnote 1 This strategy would not be feasible if the firms that participated in the transactions had only a small number of branches. Second, since banks are large and diversified retail banks, it is reasonable to assume they operate in the same market. If banks were small and specialized in serving particular types of clients or in providing particular services (e.g., Blickle, Parlatore, and Saunders (Reference Blickle, Parlatore and Saunders2023), Paravisini, Rappoport, and Schnabl (Reference Paravisini, Rappoport and Schnabl2023)), this assumption would no longer hold, leading to mismeasurement in our metrics of market power gains.

We show that consolidations lead to a substantial internal reallocation of resources. Restructuring generates profitability gains in both target and acquirer branches beyond those resulting from increases in market power. We employ a stacked difference-in-differences empirical strategy using as controls branches of similar institutions (i.e., large private banks) that eventually took part in a consolidation but that operated as separate entities during our sample period. Our approach compares branches within the same municipality, which is our definition of a market. Our within-municipality approach allows us to control for time-varying shocks at the local level, ruling out confounders such as changes in local demand or deterioration of the local economic activity that affects the creditworthiness of borrowers and the performance of existing loans. Moreover, this approach further alleviates concerns that the effects are explained by larger market power, as the local competitors that comprise our control group can act strategically and increase mark-ups in reaction to the M&A.

First, we provide evidence of labor reallocation across the branch network: the number of employees at acquirer branches increases while it decreases at target branches. The increase in employment at acquirer branches is due to internal transfers, not external hiring. Not only does the number of employees increase at acquirer branches, but the skill of the employees also increases, particularly of loan officers, suggesting that banks use M&As to access a scarce source of talent that is crucial to running their activity (Hertzberg, Liberti, and Paravisini (Reference Hertzberg, Liberti and Paravisini2010), Ouimet and Zarutskie (Reference Ouimet and Zarutskie2020), Chen, Gao, and Ma (Reference Chen, Gao and Ma2021)).

Next, we investigate whether this reallocation of internal resources is associated with enhanced operating efficiency. Profits per employee increase at both acquirer and target branches after the consolidation, even after controlling for local increases in market power engendered by the consolidation. The rise in profits per employee in acquirer branches arises from increased lending provision and deposit collection productivity, while in target branches it arises from cost-cutting, as both labor and other costs contract after the consolidation. Furthermore, productivity gains at acquirer and target branches accrue slowly after the M&A, peaking at around 4 years after the event. As restructuring is a lengthy process, while gains from increases in market power can be harvested in a more expedited manner after the M&A, the timing of the effects provides reassuring evidence that the restructuring process plays an essential role in M&A value creation beyond increases in market power.Footnote 2

To shed some light on whether opposite effects on target and acquirer branches offset each other, we create synthetic observations of the consolidated bank prior to the M&A by aggregating target and acquirer branches in a given municipality. We proceed analogously with banks in the control group that eventually merged, but that during our sample period were independent firms. We show that lending and deposits increase post-consolidation in the consolidated bank; that is, the positive effect we observe at acquirer branches dominates the negative effects observed at target branches. At the same time, the number of employees decreases. These two effects generate an increased level of lending and deposits per employee.

Finally, we exploit the fact that internal labor markets are more fluid when branches are geographically proximate, as reassigning an employee within the same municipality is less costly than relocating them to a more distant location (e.g., Cestone, Fumagalli, Kramarz, and Pica (Reference Cestone, Fumagalli, Kramarz and Pica2023)). Consistent with this mechanism, municipalities in which consolidation generates a larger local internal labor market (ILM) realize greater gains from labor reallocation. The nationwide footprint of banks in our sample delivers significant cross-sectional variation in post–M&A ILM size, which we use to test this prediction. We find that lending productivity rises by roughly twice as much in municipalities with sizeable local ILMs relative to those with small ILMs. By contrast, we find only limited evidence that deposit-side productivity increases with local ILM size. This pattern aligns with our earlier result that post-consolidation skill gains concentrate among loan officers rather than other employees, particularly bank tellers who handle deposit-taking and transaction services inside the branches.

Our main results are based on branches that remain open throughout the estimation window and for which we can compute productivity measures. Nonetheless, prior evidence suggests that post-consolidation restructuring often involves branch closures (e.g., Nguyen (Reference Nguyen2019)). Consistent with this evidence, we find that closures play a role in the restructuring process. Target branches are 3.7 percentage points more likely to close than control branches, whereas acquirer branches are 3.9 percentage points less likely to close. We also document that a nontrivial share of internal worker transfers originates from branches that eventually close. Importantly, branch closures are not the only source of efficiency gains, as we observe similar effects even in municipalities without any branch closures.Footnote 3

Our article ties into a literature that inquires into how M&As boost firm value. A branch of the literature focuses on market power gains in output (e.g., Hastings and Gilbert (Reference Hastings and Gilbert2005), Garmaise and Moskowitz (Reference Garmaise and Moskowitz2006), Dafny, Duggan, and Ramanarayanan (Reference Dafny, Duggan and Ramanarayanan2012), and Joaquim, van Doornik, and Ornelas (Reference Joaquim, van Doornik and Ornelas2019)) and input markets, particularly labor markets (e.g., Guanziroli (Reference Guanziroli2023), Arnold (Reference Arnold2020)). The other branch focuses on synergy gains. By focusing on direct measures of branch-level productivity and profitability, our work is related to papers that use plant-level data to uncover the sources of efficiency created by M&As.Footnote 4 While recent papers focus on labor restructuring post-consolidation, which can come from the elimination of duplicated occupations (e.g., Lee, Mauer, and Xu (Reference Lee, Mauer and Xu2018)) and internal reallocation, they do not link directly restructuring and productivity gains (Dessaint, Golubov, and Volpin (Reference Dessaint, Golubov and Volpin2017), Gehrke, Maug, Obernberger, and Schneider (Reference Gehrke, Maug, Obernberger and Schneider2021), Lagaras (Reference Lagaras2021), and Tate and Yang (Reference Tate and Yang2024)). Finally, our results also add to the recent literature on the effects of internal markets on firm performance (Huneeus, Larrain, Larrain, and Prem (Reference Huneeus, Larrain, Larrain and Prem2021), Cestone et al. (Reference Cestone, Fumagalli, Kramarz and Pica2023)). Specifically, we provide evidence that internal markets play an essential role in efficiency gains post-consolidation.

II. Empirical and Institutional Setting

A. The Banking Sector in Brazil and M&A Activity Involving Large Private Banks

We consider M&As of large private banks that took place in the late 2000s. Prior to these M&As, the banking sector in Brazil was already dominated by a small number of private and government-owned banks (Cortes and Marcondes (Reference Cortes, Marcondes, Amann, Azzoni and Baer2018)). In December 2006, the five largest commercial banks accounted for 57.8% of total assets held by financial institutions, 58.6% of total credit, and 63.8% of total deposits.Footnote 5 Government-owned commercial banks were relevant in terms of size. The two largest government-owned commercial banks accounted for 28% of total assets held by financial institutions. The largest banks had an extensive branch network, with most of them having more than 1,000 branches and some of them having more than 4,000 branches.

The banking industry experienced the consolidation of large private banks starting in 2007. Four private commercial banks, which accounted for 30.8% of the total credit granted by financial institutions in 2006, took part in M&A transactions. The share of total credit granted by the target banks alone was 13.5%. The first transaction happened in 2007 and was the result of a consolidation that involved two parent companies headquartered in other countries. The second occurred in 2008 and involved large national banks headquartered in Brazil. The second transaction was a consolidation that had been negotiated for years and was accelerated by the Lehman Brothers collapse in September 2008.Footnote 6 These two M&As sparked increases in concentration measures, which remained stable thereafter (Figure A1 in the Supplementary Material).

The great financial crisis primarily defined the timing of these consolidations. In Brazil, the main effects of the crisis manifested themselves after the Lehman Brothers bankruptcy and were short-lived in comparison to other countries (De Mello and Garcia (Reference De Mello and Garcia2012)). GDP only fell for two quarters (the last quarter of 2008 and the first quarter of 2009) and then started to grow again (Figure A2 in the Supplementary Material). The stock of credit to firms was stable for two quarters and then resumed its growth trajectory. Banks did not fail, in part because of measures taken after the Lehman collapse by the Central Bank to alleviate the lack of liquidity (Mesquita and Torós (Reference Mesquita and Torós2010)). Moreover, large banks—the ones we study—were perceived as too-big-to-fail, and, as a result, the liquidity drought sparked by the crisis was less strict for them (Oliveira, Schiozer, and Barros (Reference Oliveira, Schiozer and C. Barros2015)).

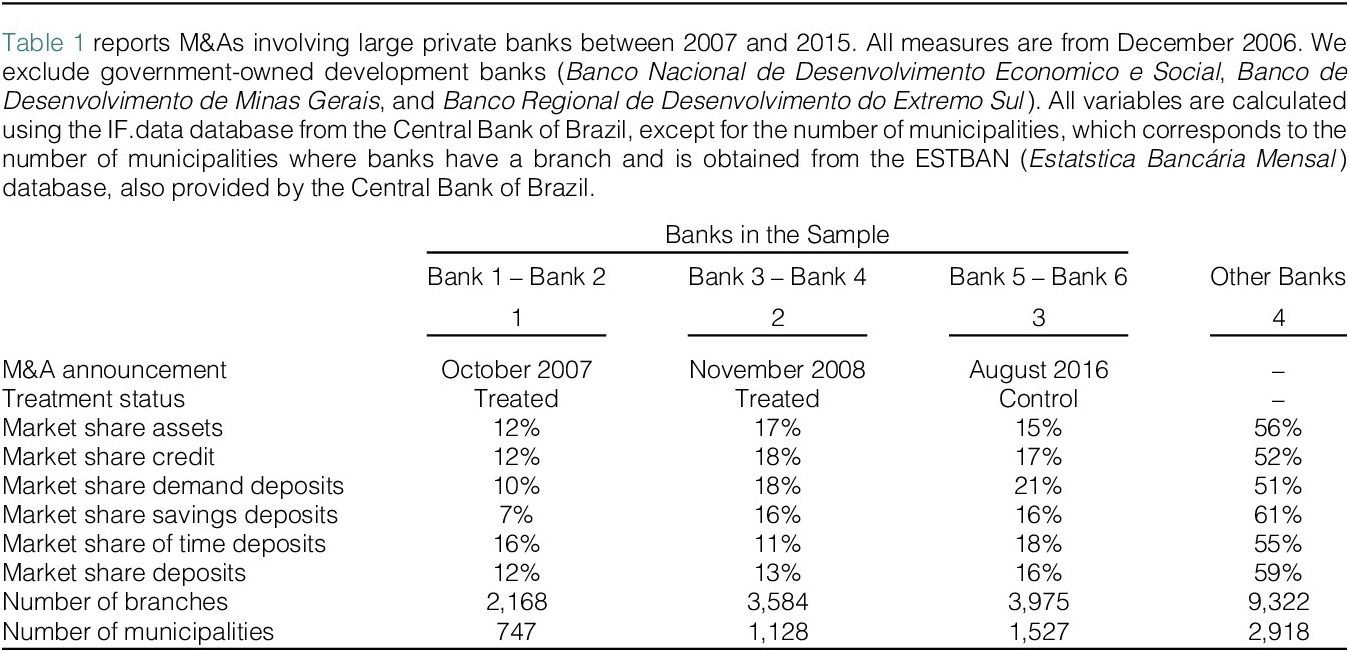

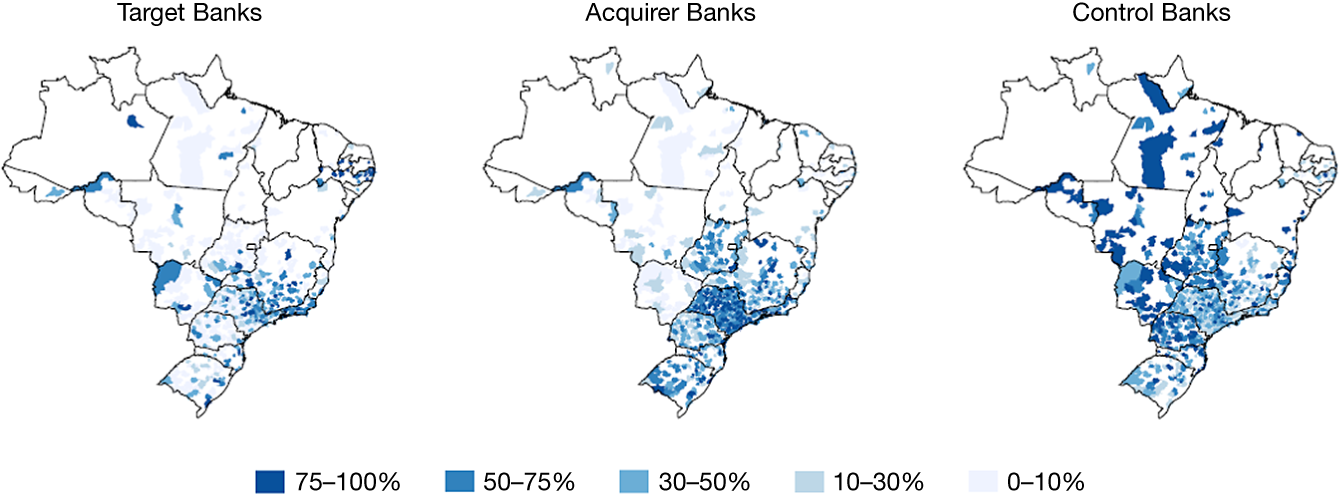

Table 1 shows characteristics of the M&A episodes considered in our analyses.Footnote 7 We focus on large private banks with extensive branch networks and operations in multiple local markets. These characteristics are essential for addressing our research question, as they enable us to account for variations in local market power and study the internal reallocation of resources. To mitigate concerns about selection into consolidation, the control group consists of large private banks that participated in an M&A in 2015—after the period of our analysis, which ranges from 2004 to 2014. We do not include government-owned banks in our sample because there is ample evidence suggesting their objectives differ significantly from those of private banks in Brazil (Coelho, De Mello, and Rezende (Reference Coelho, De Mello and Rezende2013), Coleman and Feler (Reference Coleman and Feler2015), Cortes, Silva, van Doornik et al. (Reference Cortes, Silva and van Doornik2019), Mariani (Reference Mariani2020), and Garber, Mian, Ponticelli, and Sufi (Reference Garber, Mian, Ponticelli and Sufi2021)). The banks in our sample represent 48% of credit, 44% of assets, 45% of deposits, and 51% of bank branches in the financial system. All banks had a presence in hundreds of municipalities, which is our definition of a local market and follows previous research in our setting (Sanches, Silva Junior, and Srisuma (Reference Sanches, Junior and Srisuma2018), Joaquim et al. (Reference Joaquim, van Doornik and Ornelas2019)). Figure 1 depicts the geographical location of the branches. It shows that the banks in our sample had a significant presence in many municipalities throughout the country.

Figure 1 shows the geographical presence of the branches that comprise our sample as of December 2006.

B. Data

Our analysis draws on microdata from several sources. The first is the RAIS (Relação Anual de Informações Sociais), an annual employer–employee matched data set provided by the Brazilian Ministry of Labor. It contains establishment-level labor data for the universe of firms and workers in the formal sector, covering the full population of bank employees. It includes information on job position characteristics, such as salary and occupation, as well as workers’ characteristics, including age, education, gender, and race. The information on the salary and starting and separation dates allows us to compute the total labor costs of each branch. As both branches and employees have a unique taxpayer identifier, we can follow workers across branches.

Branch- and bank-level financial data come from the Central Bank of Brazil. The branch-level yearly information comes from the ESTBAN (Estatística Bancária Mensal) database. We focus on the period between 2004 and 2014.Footnote 8 This data set is derived from a mandatory form that all banks are required to complete, and it includes the branch municipality, the taxpayer identifier, balance sheet information (such as assets, loans, and deposits), and aggregate revenues, costs, and profits. We provide additional details about these data and the variables we construct in Section A3 of the Supplementary Material.

The branch taxpayer identifier is a 14-digit number, out of which the first eight digits are the taxpayer identifier of the bank. This identifier enables us to merge the labor data with branch- and bank-level data. It also allows us to identify the branches that participated in the M&As that occurred in 2007 and 2008 (treated branches) and the ones that participated in the large M&A that occurred in 2015 (control branches). We classify as target branches those that changed their taxpayer number after the M&As.

We obtain detailed branch address information from the Central Bank of Brazil’s Register of Branches, Offices, and Subsidiaries of Consortium Administrators. The data contain the bank branch taxpayer identifier and detailed address information, which is crucial to our article in that it allows us to keep following a branch even when its taxpayer identifier changes because of the M&A. Finally, we utilize bank-level information from IF.data, provided by the Central Bank of Brazil. These data are available on a quarterly frequency and include detailed balance sheet and income statement information. This data set also contains the 8-digit taxpayer identifier of each bank.

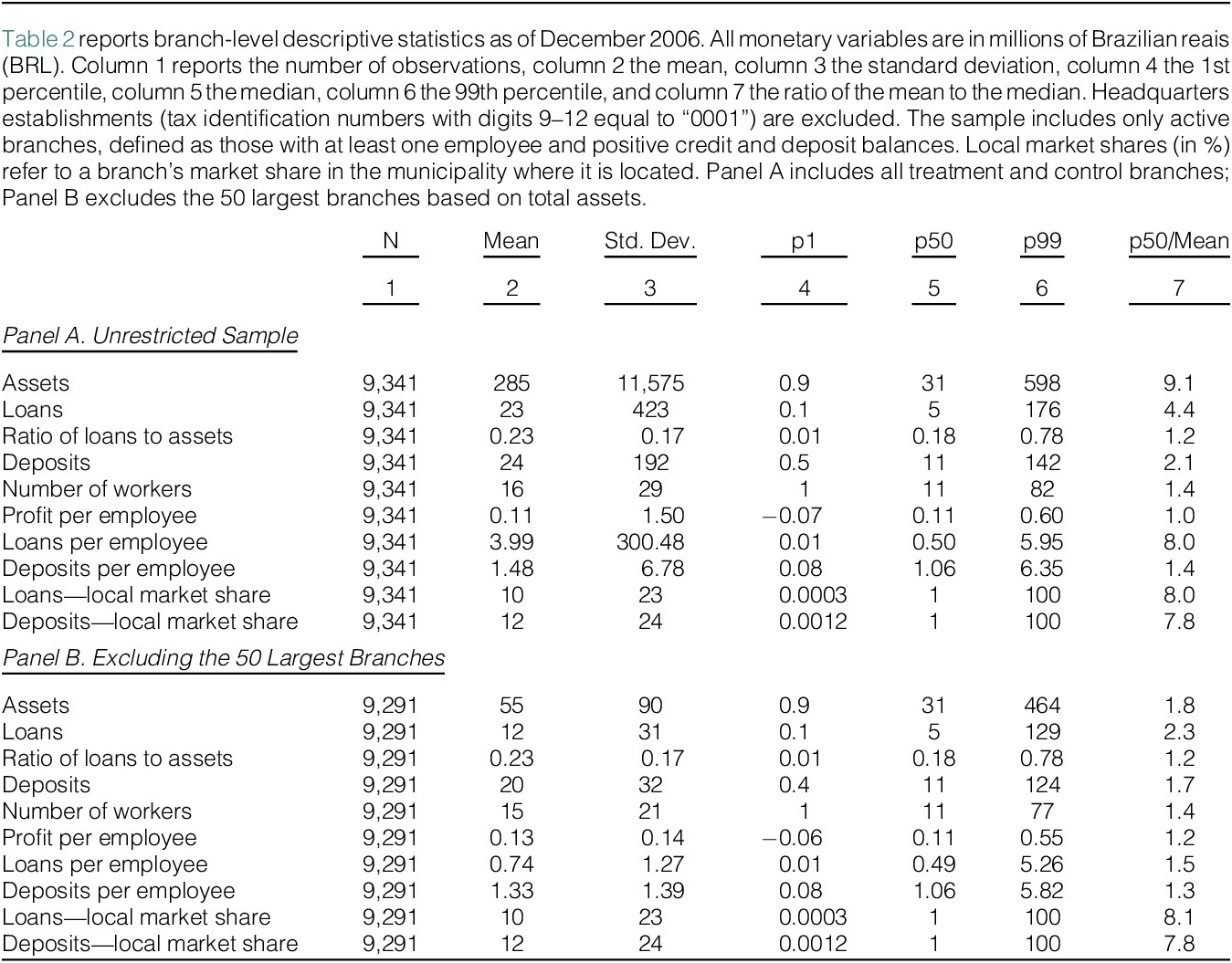

C. Descriptive Statistics

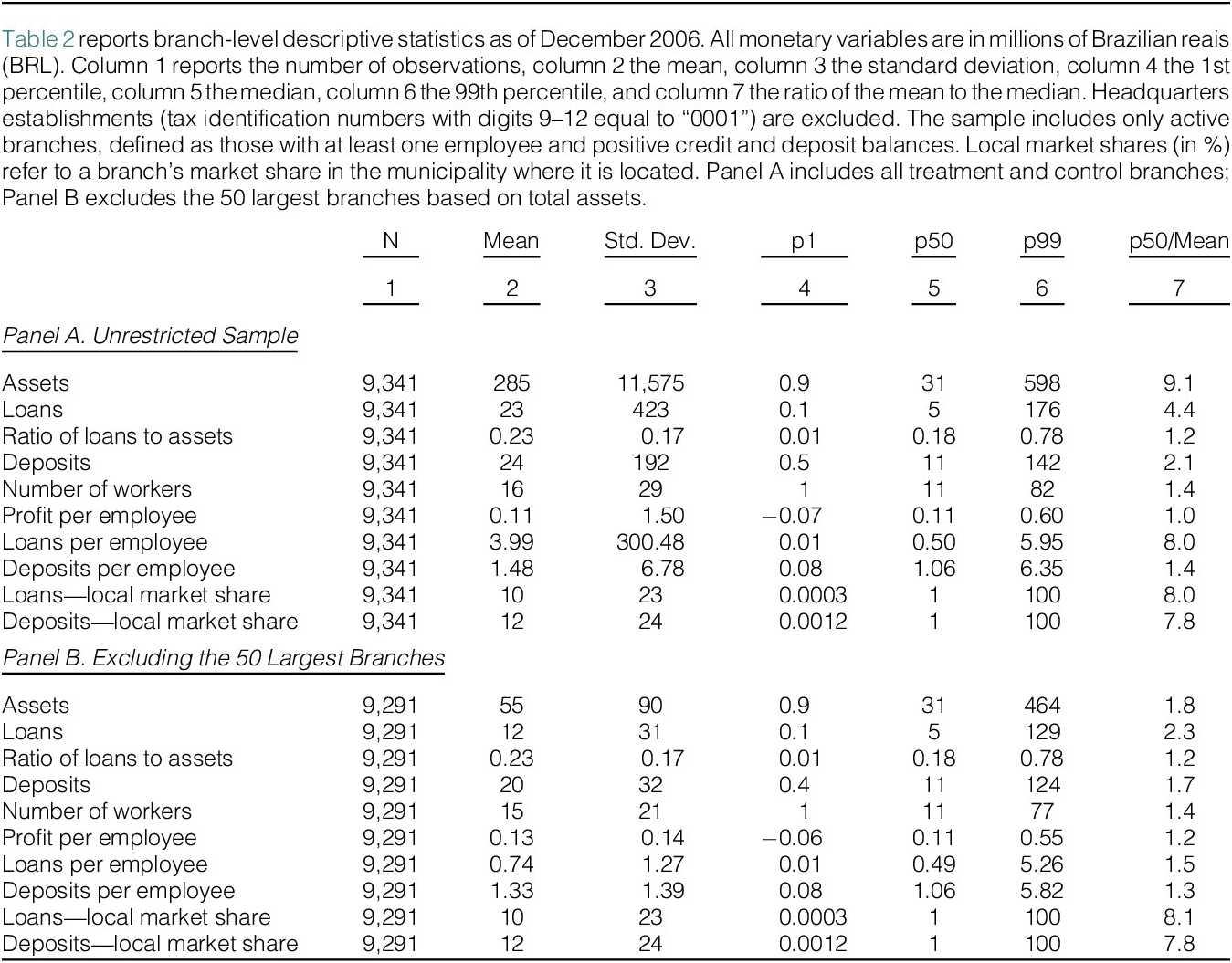

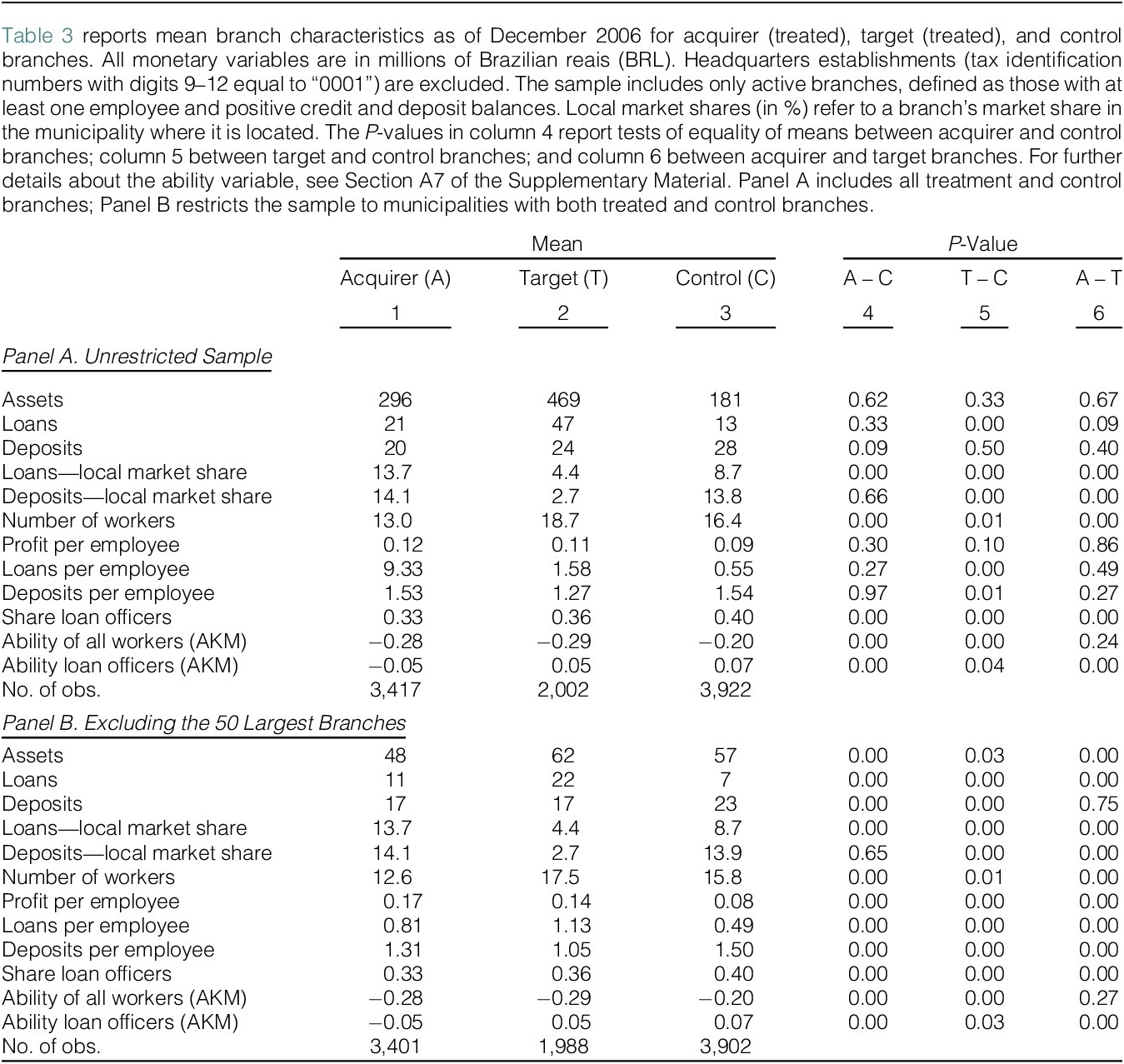

In Table 2, we present descriptive statistics of the branches of banks in the treated and control groups before the M&As.Footnote 9 Control and treated banks had 9,341 active branches in December 2006, which we define as branches that have at least one employee and a positive stock of credit and deposits. The average stock of lending and deposits was 23 million Brazilian reais (BRL) and 24 million BRL in December 2006, respectively. Branches had on average 16 workers (median 11). The average market share of a branch in the lending market is 10% (median 1.2%) and 12% in the deposit market (median 1.5%). The average profit per employee is 0.11 million BRL.

Several variables exhibit substantial right skewness.Footnote 10 In particular, the mean-to-median ratio is 9.1 for assets, 4.4 for the stock of credit, and 2.1 for the stock of deposits. To provide a clearer picture of the average branch, we also report statistics excluding the 50 largest branches (0.5% of the sample) in Panel B of Table 2.Footnote 11 In this restricted sample, the average stock of lending falls to 12 million BRL, the average profit per employee is 0.13 million BRL, the average stock of credit per employee is 0.74 million BRL, and the average stock of deposits per employee is 1.33 million BRL. The average ratio of loans to assets is 0.23.Footnote 12

As we use municipality-by-time fixed effects in our regressions, municipalities that do not contain both treatment and control branches end up being dropped. When we restrict the sample to branches located in municipalities with both control and treatment branches, the characteristics of the branches do not change significantly (Table A1 in the Supplementary Material). Branches are slightly larger in terms of lending, deposits, and the number of employees, and have smaller market shares.

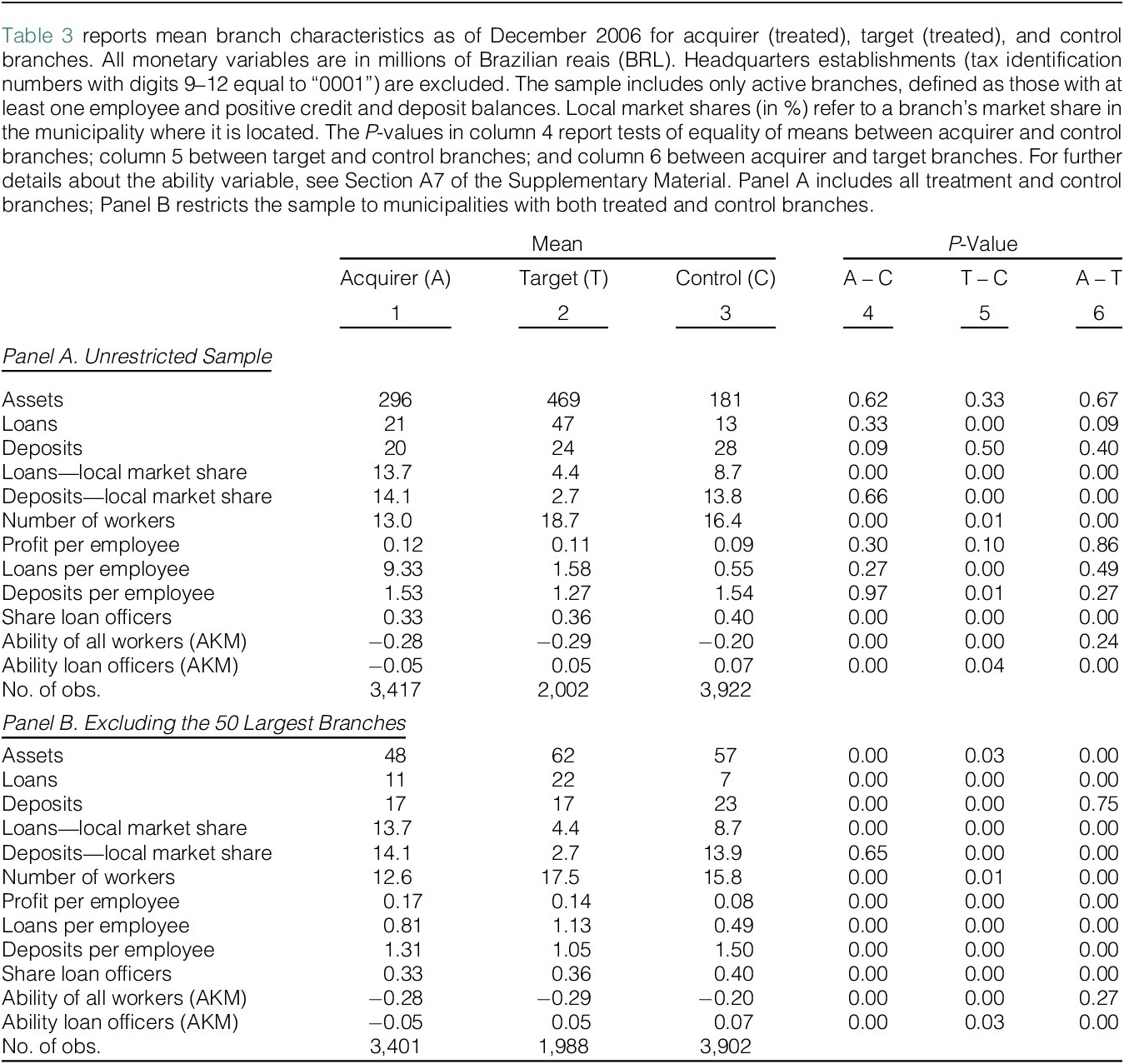

In Table 3, we report summary statistics by branch status—acquirer, target, and control. Although equality of means is rejected for the vast majority of comparisons, the economic magnitudes of many differences remain relatively modest. For example, after excluding the 50 largest branches, acquirer and target branches each hold an average of 17 million BRL in deposits, compared with 23 million BRL in control branches. In this subsample, control branches exhibit lower profits per employee: profit per employee averages 0.17 million BRL in acquirer branches, 0.14 million BRL in target branches, and 0.08 million BRL in control branches. Control branches, however, have larger deposits per employee—1.5 million BRL per worker, compared with 1.05 million BRL in target branches and 1.31 million BRL in acquirer branches. Lending is also larger in target branches relative to control branches.Footnote 13

The fact that characteristics at the bank branch levels are not strikingly different is reassuring. However, to further guarantee that differences in observables do not threaten the plausibility of our identification hypothesis (discussed in Section II.D), that treatment and control branches would follow similar trajectories had the M&As not occurred, we include controls for baseline characteristics interacted with time dummies in our empirical analysis.

D. Empirical Strategy

Our empirical strategy exploits branch-level information and the timing of the M&A events to establish a link between the restructuring that follows a consolidation and branch outcomes. We also exploit variation in branches’ ownership before the consolidation to investigate heterogeneous effects on target and acquirer branches. As our treatment timing is staggered, with events occurring in 2007 and 2008, we implement a stacked regression estimation (Baker, Larcker, and Wang (Reference Baker, Larcker and Wang2022)). We construct two event-specific data sets (one for each M&A) and stack them (Figure A3 in the Supplementary Material). We refer to each event-specific data set as a cohort. For each cohort, the control group consists only of private bank branches that did not participate in a bank M&A during the time window of our estimation, but that participated in these events in the future. We define the control variables for each cohort by interacting them with cohort-specific indicators. We use an estimation window of 10 years: 3 years before and 6 years after the event. We restrict the main analyses to branches that remain open during the window and for which we can measure outcome variables. Using the same stacked approach, we also check the parallel trends assumption and the dynamic treatment effects after the M&A events.

We estimate the following model:

$$ {\displaystyle \begin{array}{l}{y}_{i,g,t}={\delta}_1{Post}_{i,t}\times {Target}_i+{\delta}_2{Post}_{i,t}\times {Acquirer}_i+{\alpha}_{i,g}+{\alpha}_{g,m,t}\\ {}\gamma {MP}_i\times {Post}_{i,t}\times {Treated}_i+{\beta}_{g,t}{X}_i++{\epsilon}_{i,g,t}\end{array}} $$

$$ {\displaystyle \begin{array}{l}{y}_{i,g,t}={\delta}_1{Post}_{i,t}\times {Target}_i+{\delta}_2{Post}_{i,t}\times {Acquirer}_i+{\alpha}_{i,g}+{\alpha}_{g,m,t}\\ {}\gamma {MP}_i\times {Post}_{i,t}\times {Treated}_i+{\beta}_{g,t}{X}_i++{\epsilon}_{i,g,t}\end{array}} $$

in which

$ i $

represents the bank branch,

$ i $

represents the bank branch,

$ g $

the cohort,

$ g $

the cohort,

$ t $

calendar year, and

$ t $

calendar year, and

$ m $

the municipality. The dummy variable

$ m $

the municipality. The dummy variable

$ {Target}_i $

(

$ {Target}_i $

(

$ {Acquirer}_i $

) takes the value 1 when branch

$ {Acquirer}_i $

) takes the value 1 when branch

$ i $

belongs to a bank that was the target (acquirer) party in one of the M&A transactions of our sample. The dummy variable

$ i $

belongs to a bank that was the target (acquirer) party in one of the M&A transactions of our sample. The dummy variable

$ {Treated}_i $

takes the value 1 when branch

$ {Treated}_i $

takes the value 1 when branch

$ i $

is either an acquirer or a target branch. The coefficient

$ i $

is either an acquirer or a target branch. The coefficient

$ {\delta}_1 $

represents the M&A effect on the target branches, and the coefficient

$ {\delta}_1 $

represents the M&A effect on the target branches, and the coefficient

$ {\delta}_2 $

represents the M&A effect on the acquirer branches. We control for any fixed unobserved branch characteristics by using branch fixed effects

$ {\delta}_2 $

represents the M&A effect on the acquirer branches. We control for any fixed unobserved branch characteristics by using branch fixed effects

$ {\alpha}_{i,g} $

(interacted with cohort dummies). To account for time-varying changes at the local level that are common to all branches, such as demand shocks, we include municipality-by-time-by-cohort fixed effects

$ {\alpha}_{i,g} $

(interacted with cohort dummies). To account for time-varying changes at the local level that are common to all branches, such as demand shocks, we include municipality-by-time-by-cohort fixed effects

$ {\alpha}_{g,m,t} $

.Footnote

14 We also control for other possible confounding effects that might be correlated with post-consolidation performance by using branch pre-M&A characteristics (measured in 2006) (

$ {\alpha}_{g,m,t} $

.Footnote

14 We also control for other possible confounding effects that might be correlated with post-consolidation performance by using branch pre-M&A characteristics (measured in 2006) (

$ {X}_i $

) interacted with cohort and time dummies.Footnote

15

$ {X}_i $

) interacted with cohort and time dummies.Footnote

15

We account for the heterogeneous market power gains resulting from the consolidation, which are measured by the sum of the market shares in total lending of the target and acquirer branches in a given municipality prior to the M&A (

$ {MP}_i $

).Footnote

16 Controlling for these gains is essential in our setting since it enables us to isolate the effects of resource restructuring from direct impacts led by changes in local market power. Since both the treated and control banks in our sample are large and diversified retail banks, it is reasonable to assume they operate in the same market. If banks were small and specialized in serving particular types of clients or services (e.g., Blickle et al. (Reference Blickle, Parlatore and Saunders2023), Paravisini et al. (Reference Paravisini, Rappoport and Schnabl2023)), this assumption would no longer hold, leading to mismeasurement in our metrics of market power gains. M&As involving large banks offer the added advantage of creating significant variation in market power gains across municipalities (Figure A4 in the Supplementary Material). Without such variation, controlling for market power gains would be infeasible. Finally, as banks were already large and diversified pre-consolidation, market power gains that are common across all markets (such as those resulting from a large network of branches or concerns about banks being perceived as “too big to fail”) play a smaller role in this context.

$ {MP}_i $

).Footnote

16 Controlling for these gains is essential in our setting since it enables us to isolate the effects of resource restructuring from direct impacts led by changes in local market power. Since both the treated and control banks in our sample are large and diversified retail banks, it is reasonable to assume they operate in the same market. If banks were small and specialized in serving particular types of clients or services (e.g., Blickle et al. (Reference Blickle, Parlatore and Saunders2023), Paravisini et al. (Reference Paravisini, Rappoport and Schnabl2023)), this assumption would no longer hold, leading to mismeasurement in our metrics of market power gains. M&As involving large banks offer the added advantage of creating significant variation in market power gains across municipalities (Figure A4 in the Supplementary Material). Without such variation, controlling for market power gains would be infeasible. Finally, as banks were already large and diversified pre-consolidation, market power gains that are common across all markets (such as those resulting from a large network of branches or concerns about banks being perceived as “too big to fail”) play a smaller role in this context.

Our “within market” approach is convenient because the large M&As we study coincide with the onset of the 2007–2008 financial crisis. As a result, in the absence of the M&A events, different markets could have had distinct performances. For instance, firms in markets with more branches per population could be more leveraged or exposed to disruptions in international markets through trade relationships. Our municipality-by-time-by-cohort fixed effects approach deals with those possibilities.

The main concern with our empirical strategy is that banks participating in consolidations are not randomly selected, which is reflected in some differences in baseline characteristics, as shown in Table 3. Therefore, unobserved factors can cloud the magnitude of our coefficients. For instance, relative to control branches, target and acquirer branches may have experienced changes in productivity even in the absence of the M&A, a possibility that a parallel trends test would not detect. This concern is common to all M&A studies, and no perfect solution has been proposed in the literature. We seek to minimize this issue in several ways. First, our control branches belong to banks that participated in a large M&A after our sample period. Second, we add baseline branch characteristics interacted with time dummies to alleviate concerns that heterogeneity across bank branches affects our results. Third, we implement tests proposed by Rambachan and Roth (Reference Rambachan and Roth2023) to assess the robustness of our results to violations of the parallel trends assumption. Finally, certain features of the M&As we study further mitigate these concerns. One M&A was the result of an operation that involved companies with headquarters in foreign countries. The other had been negotiated for years and was accelerated by the collapse of Lehman Brothers. As a result, its timing was relatively exogenous.

A second confounder could arise from a different reaction of treated and control banks during the financial crisis. However, as explained in Section II.A, the crisis in Brazil was short-lived, mild, and did not spark bank failures. Moreover, our sample comprises large banks only, and these banks experienced an inflow of funding because they were perceived as too-big-to-fail (Oliveira et al. (Reference Oliveira, Schiozer and C. Barros2015)).

Finally, because M&As often lead to branch closures (e.g., Nguyen (Reference Nguyen2019)), our results could be affected by survivorship bias if the branches that remain open are positively selected based on future outcomes. A related concern is that the assets, credit, and deposits of closed branches may be transferred to surviving branches, mechanically inflating these variables in ways unrelated to productivity improvements. We believe these concerns are limited for two reasons. First, branch closures are relatively modest in our setting. Second, our results are robust even when we restrict the sample to markets without branch closures. Lastly, we apply tests following Lee (Reference Lee2009) to account for potential selection bias, and the results further confirm the robustness of our findings.

III. Results

A. Consolidation and Internal Labor Reallocation

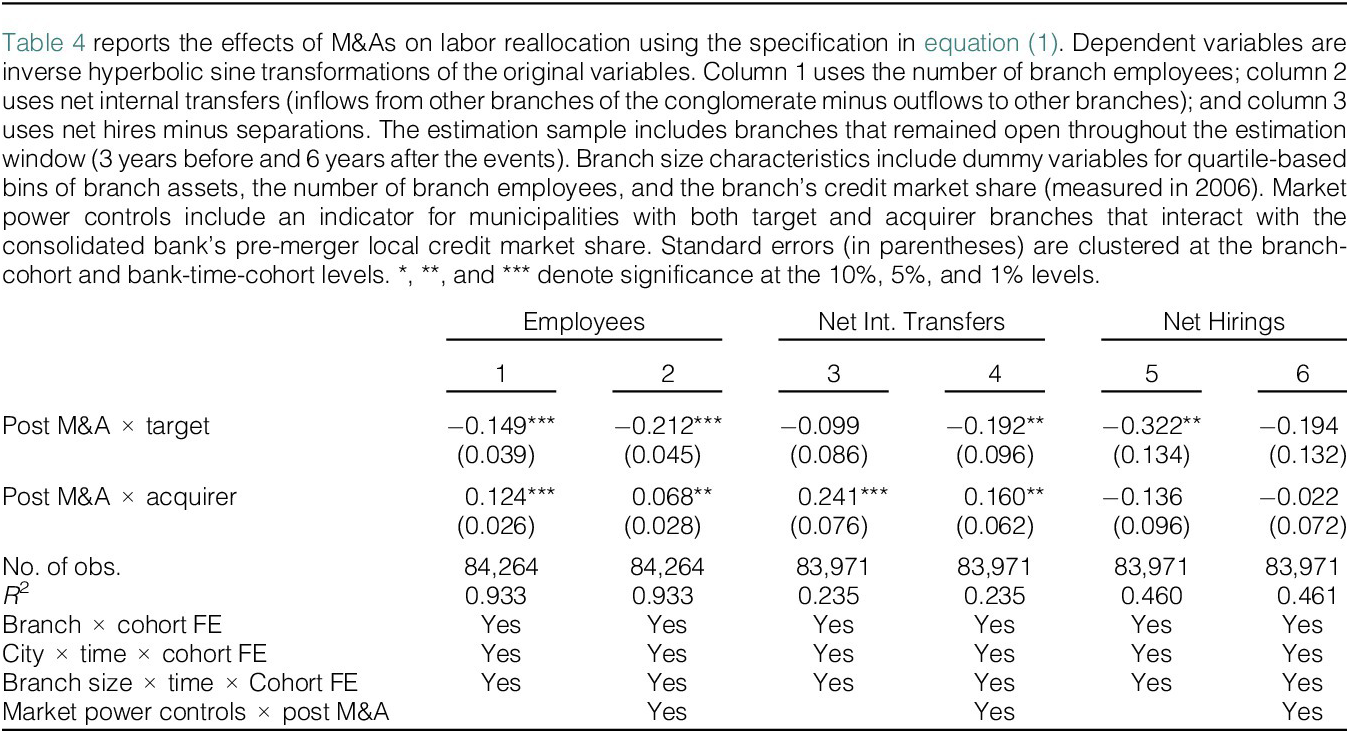

In Table 4, we examine how M&As change the growth in the branches’ number of employees, total external hiring, and the total number of employees internally transferred during the period. Target branches decrease the number of employees by 21.2% in comparison to control branches, while acquirer branches experience an increase of 6.8%.Footnote 17 In target branches, two combined factors seem to explain the large change in the number of employees: the lower number of new net hirings and the increased number of workers transferred to other branches. The increase in the number of employees in acquirer branches comes solely from a large increase in the net number of transfers from other branches (16%). These results point to active internal labor reallocation post-consolidation.

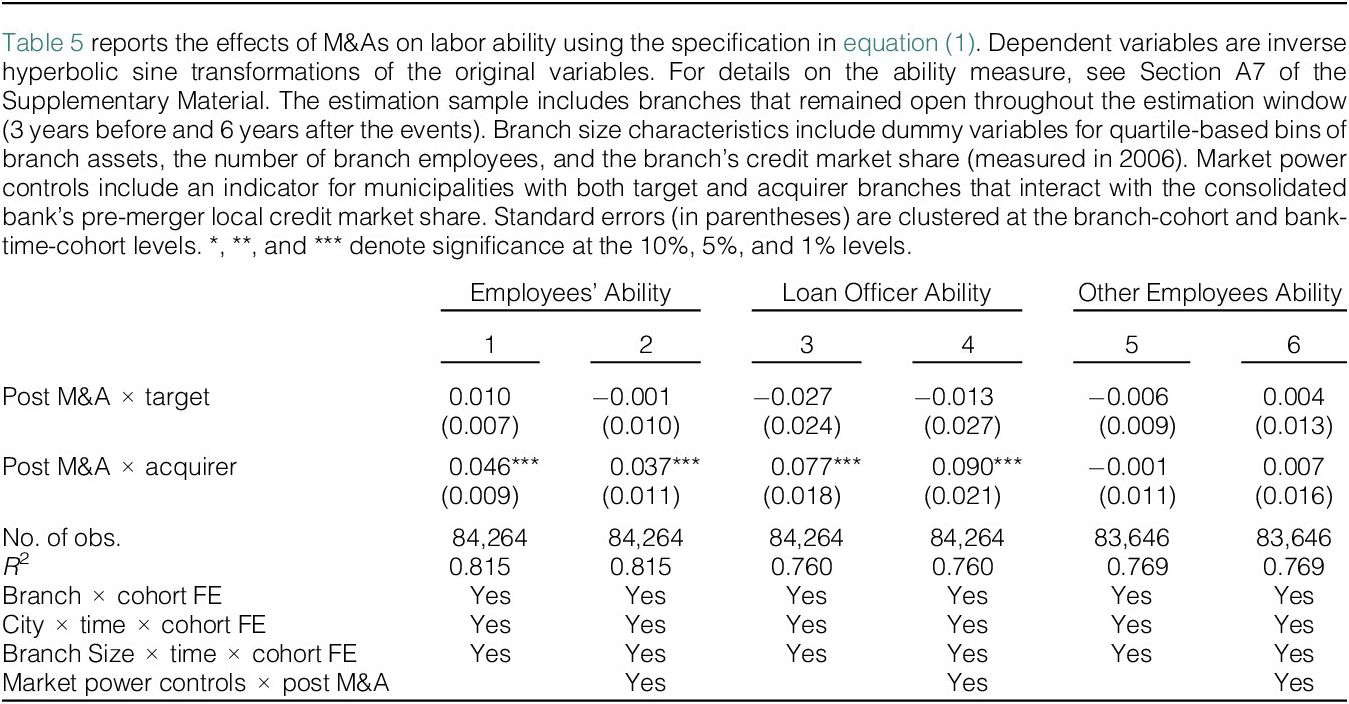

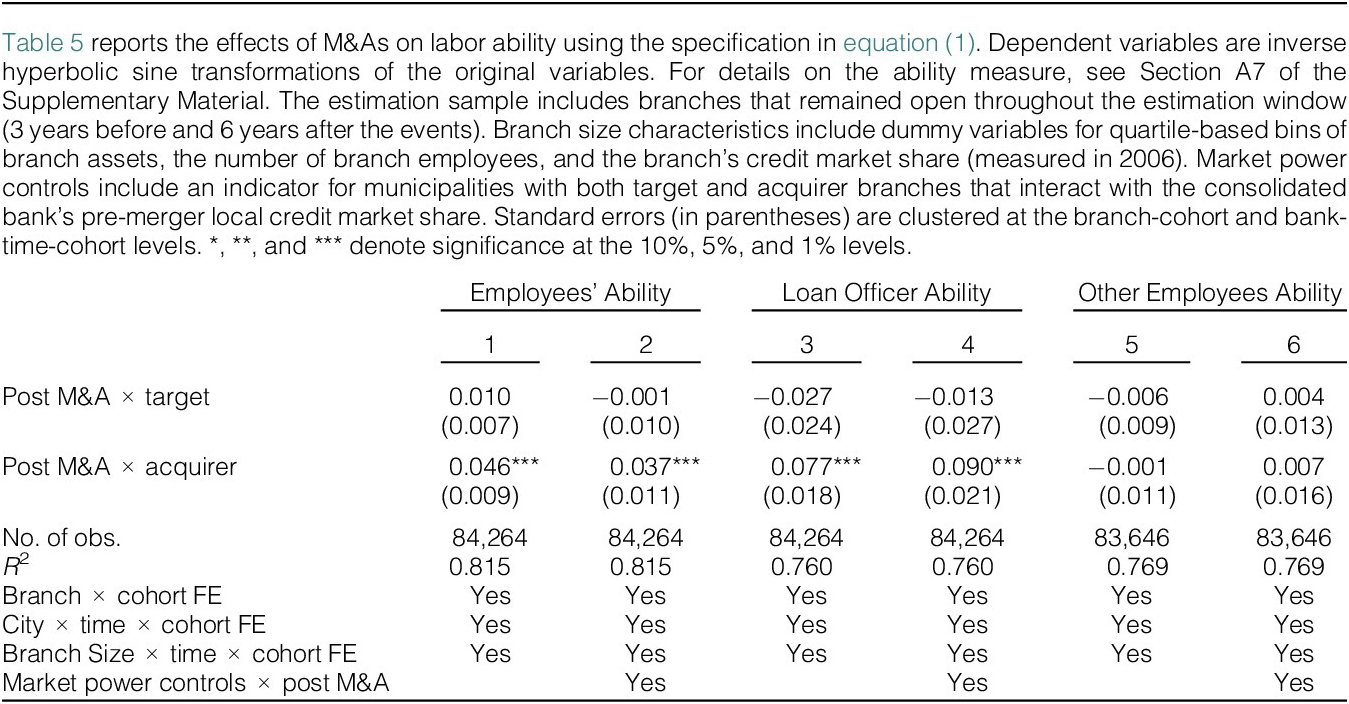

We then analyze how this labor reallocation impacts the average skill of the target and control branches’ employees. We measure ability by employing an approach inspired by the methodology proposed by Abowd, Kramarz, and Margolis (Reference Abowd, Kramarz and Margolis1999).Footnote 18 We use information on the occupation of workers and conduct separate analyses for loan officers and other employees, primarily consisting of bank tellers and administrative staff who do not interact directly with customers. The results in Table 5 show that while there is no significant change in the ability of other employees in target and acquirer branches, the ability of loan officers increases substantially (9%) in acquirer branches. As previous research has shown, this type of bank employee is crucial to running the activity of credit provision (Hertzberg et al. (Reference Hertzberg, Liberti and Paravisini2010), Agarwal and Ben-David (Reference Agarwal and Ben-David2018)).

M&As significantly increase the size of the labor force available to the newly formed bank. Overall, our results in this section suggest that internal labor markets play an essential role post-consolidation. In the next section, we analyze how the restructuring process that we document in this section took place with a concomitant increase in branch activity.

B. M&A Value Creation: Branch Output and Productivity Gains

This section documents the effects of the internal reallocation of workers on branch output and highlights how M&As engender productivity and profitability gains as well as the mechanisms underpinning these improvements, such as cost-cutting or revenue increases.Footnote 19

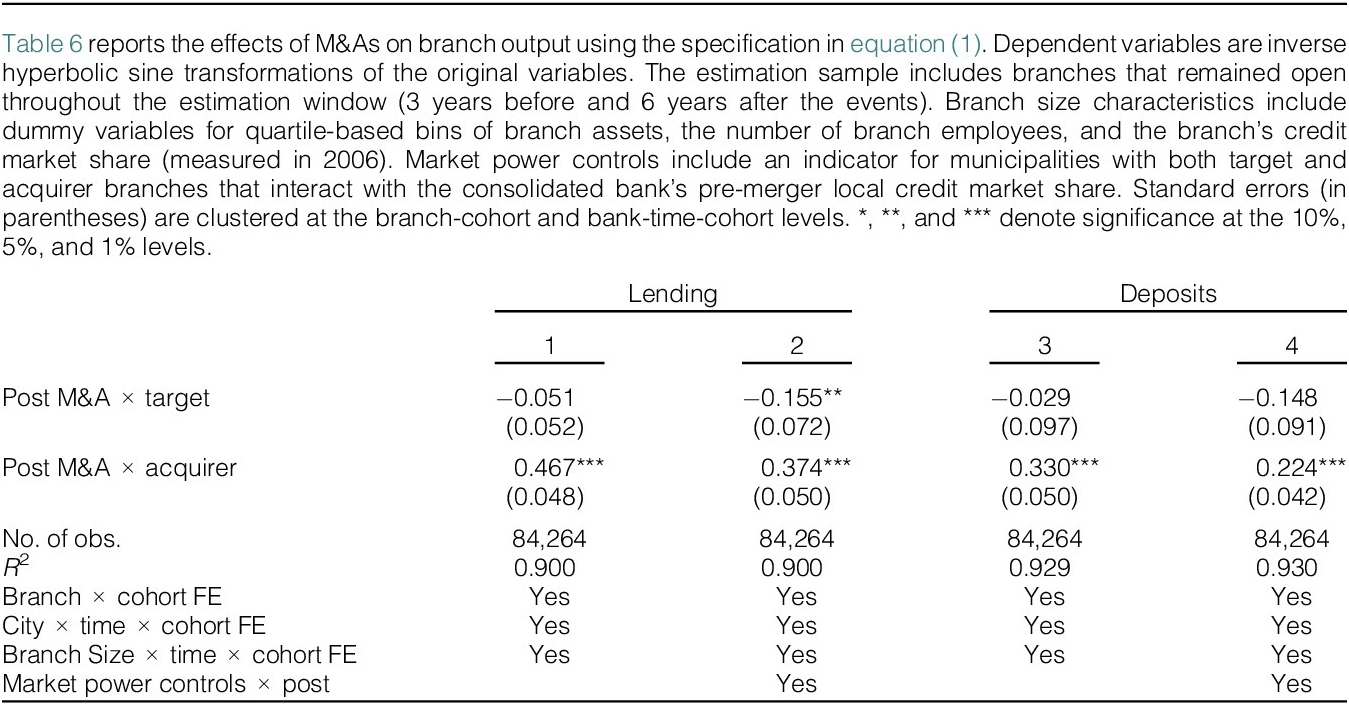

In Table 6, we present the heterogeneous change in lending and deposits across branches of the acquirer and target banks after the consolidation events. On the one hand, lending in acquirer branches increases by 37.4%. On the other hand, lending at target branches contracts by 15.5% in comparison to control branches in the same municipality. Similarly, we find a negative but not statistically significant effect on target branches’ deposits after the consolidations. In line with our previous result on labor reallocation, we show that acquirer branches attract more deposits, with a 22.4% increase. These patterns are consistent with changes in employment and loan officer ability, as well as possible improvements in service quality at acquirer branches post-consolidation. Moreover, they square with a literature that documents a reallocation of credit toward acquirer branches and heterogeneous effects of consolidations on target and acquirer borrowers (e.g., Karceski, Ongena, and Smith (Reference Karceski, Ongena and Smith2005), Di Patti and Gobbi (Reference Di Patti and Gobbi2007), and Degryse, Masschelein, and Mitchell (Reference Degryse, Masschelein and Mitchell2011)).

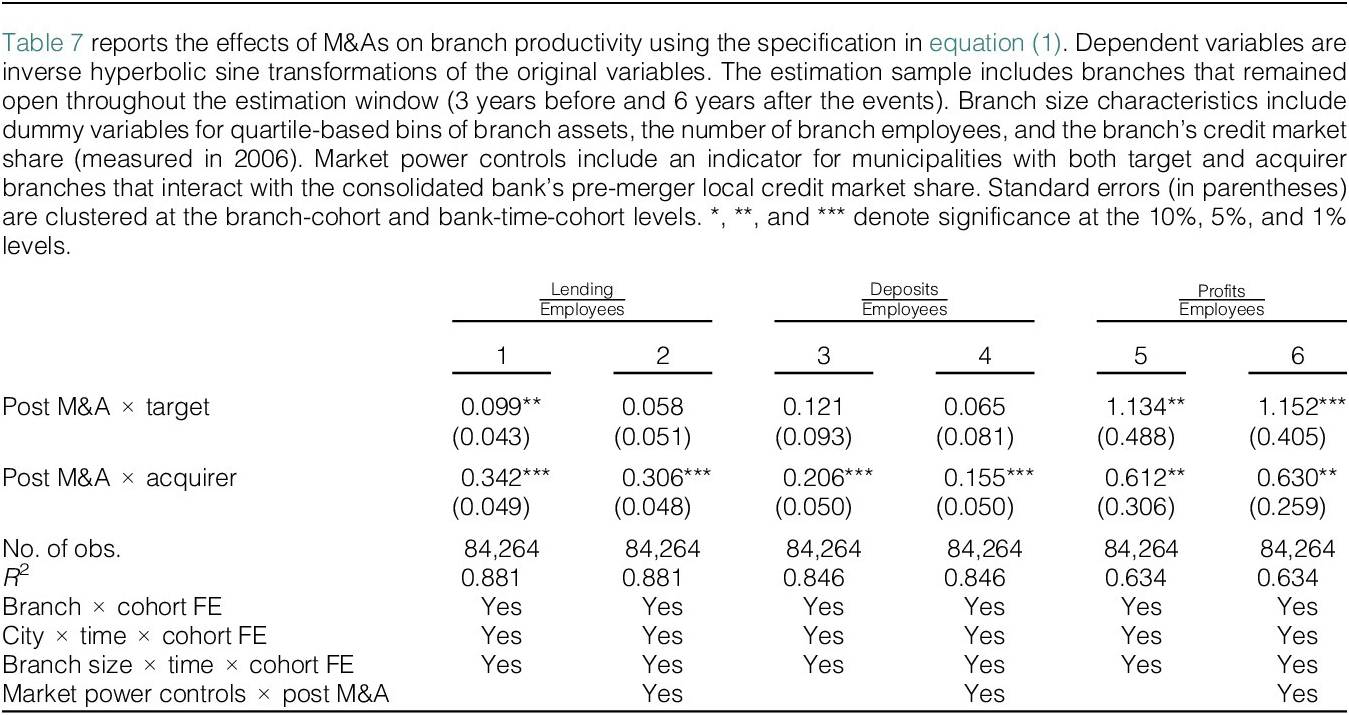

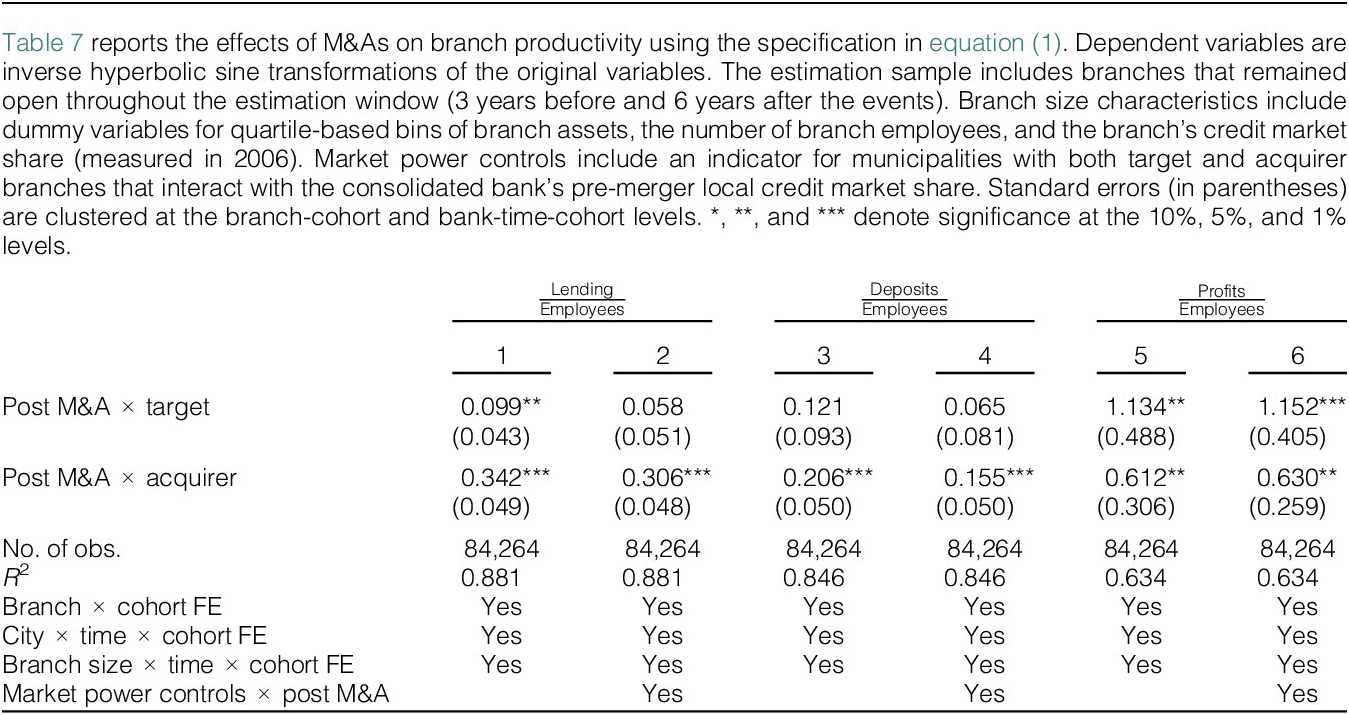

Table 7 documents the effects of M&As on different measures of productivity. We show that, despite an increase in the total number of employees, lending per employee and deposits per employee increase in acquirer branches in comparison to control branches (30.6% and 15.5%, respectively). This result is in line with our results regarding the reallocation of highly skilled workers to acquirer branches. However, we do not observe a statistically significant effect on those variables at target branches after controlling for market power gains.

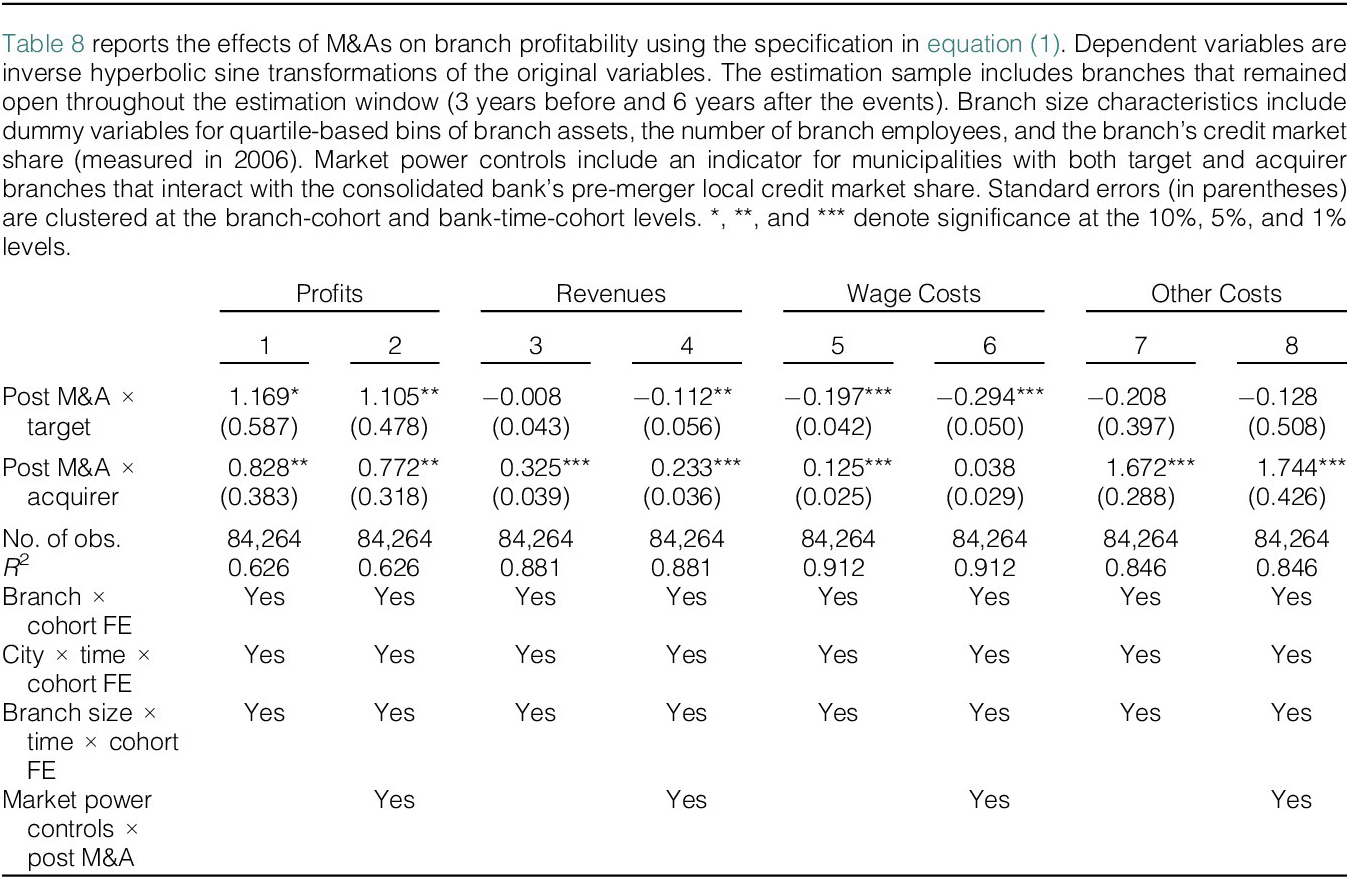

When we examine productivity as measured by profits per employee, we observe that both acquirer and target branches exhibit large and significant gains after the consolidation. To guarantee that these results are not driven by higher markups in lending markets or markdowns in input markets, we explicitly control for the local gain in market power. To identify the drivers of these results, Table 8 decomposes the increase in profits by examining the effects of consolidation on branch-level costs and revenues. Leveraging information on wages, we decompose total costs into labor costs and other costs. We show that increases in profits in acquirer branches are driven by large increases in revenues (23.3%). Despite an increase in other costs, the gain in revenues is such that the net effect on profits is positive. Although revenues in target branches decreased by 11.2%, profits increased due to cost-cutting measures, with wages reduced by 29.4%.

Our results in this section add to the literature on M&A value creation that draws on plant-level data (among others, Braguinsky et al. (Reference Braguinsky, Ohyama, Okazaki and Syverson2015), Blonigen and Pierce (Reference Blonigen and Pierce2016), Macchiavello and Morjaria (Reference Macchiavello and Morjaria2022), and Demirer and Karaduman (Reference Demirer and Karaduman2024)). We document different sources of gains on target and acquirer branches. Moreover, our results on the internal resources reallocation identify a new channel underlying these gains.

C. Branch Closures, Aggregation of Target and Acquirer Branches, and the Role of Internal Labor Markets

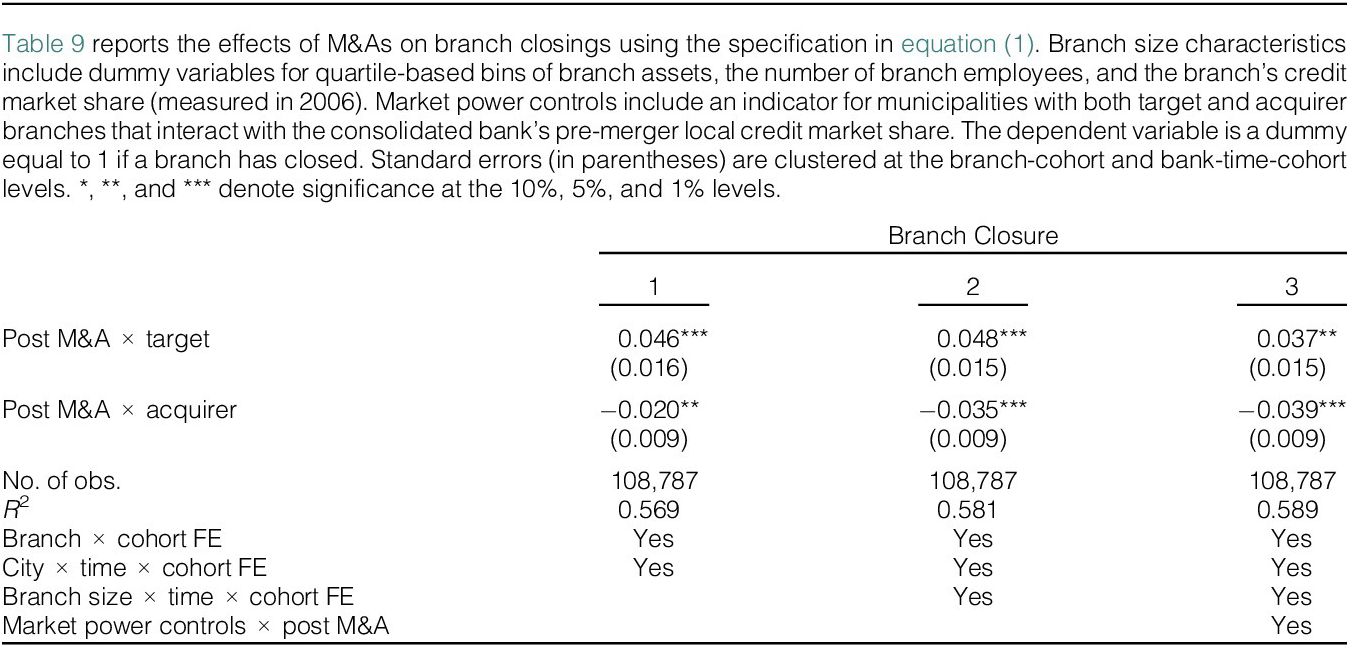

Prior research documents that consolidation leads to branch closures (e.g., Nguyen (Reference Nguyen2019)). We examine whether similar patterns arise in our setting. Target branches close at higher rates, reaching 10% in 2014, compared with 3% for control branches and 4% for acquirer branches. Table 9 reports regression estimates based on equation (1)). After the inclusion of controls, target branch closures increase by 3.7 percentage points following M&As, while acquirer branches are 3.9 percentage points less likely to close relative to control branches.

Given the effects on closures and the contrasting results for targets and acquirers in branch-level lending and deposits documented in Section III.B, we investigate whether M&As result in an overall contraction or expansion of credit and deposits at the local level. To do so, we combine the target and acquirer branches at the municipality level, both before and after the M&As. As before, we form the control group using banks that participated in M&A transactions after our analysis period, treating them as consolidated firms throughout the sample. Consistent with our branch-level specifications, we estimate a stacked difference-in-differences model using data at the bank-municipality-year level:

$$ {y}_{i,g,t}=\delta {Post}_{i,t}\times {Treated}_i+{\alpha}_{i,g}+{\alpha}_{g,m,t}+\gamma {MP}_i\times {Post}_{i,t}\times {Treated}_i+{\beta}_{g,t}{X}_i+{\epsilon}_{i,g,t} $$

$$ {y}_{i,g,t}=\delta {Post}_{i,t}\times {Treated}_i+{\alpha}_{i,g}+{\alpha}_{g,m,t}+\gamma {MP}_i\times {Post}_{i,t}\times {Treated}_i+{\beta}_{g,t}{X}_i+{\epsilon}_{i,g,t} $$

in which

$ i $

represents the bank formed after the M&A (combination of acquirer and target banks or control banks in municipality

$ i $

represents the bank formed after the M&A (combination of acquirer and target banks or control banks in municipality

$ m $

),

$ m $

),

$ g $

the cohort, and

$ g $

the cohort, and

$ t $

calendar year. The dummy variable

$ t $

calendar year. The dummy variable

$ {Treated}_i $

takes the value 1 when bank

$ {Treated}_i $

takes the value 1 when bank

$ i $

belongs to the treatment group. The coefficient

$ i $

belongs to the treatment group. The coefficient

$ \delta $

represents the M&A effect on the newly formed bank. We control for any fixed unobserved bank characteristics by using bank fixed effects

$ \delta $

represents the M&A effect on the newly formed bank. We control for any fixed unobserved bank characteristics by using bank fixed effects

$ {\alpha}_{i,g} $

(interacted with cohort dummies). As in equation (1), we include municipality-by-time-by-cohort fixed effects

$ {\alpha}_{i,g} $

(interacted with cohort dummies). As in equation (1), we include municipality-by-time-by-cohort fixed effects

$ {\alpha}_{g,m,t} $

, bank pre-M&A characteristics (measured in 2006) interacted with cohort and time dummies, and controls for local gains in market power.

$ {\alpha}_{g,m,t} $

, bank pre-M&A characteristics (measured in 2006) interacted with cohort and time dummies, and controls for local gains in market power.

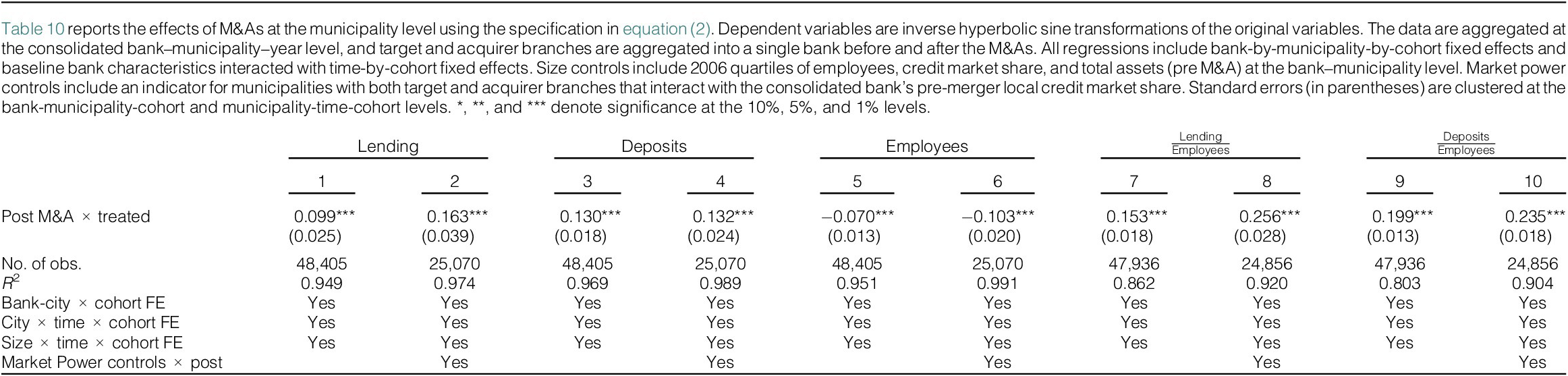

The results in Table 10 show that consolidated banks disproportionately increase their lending and deposits after the M&A compared with other consolidated banks formed just after our period of analysis, indicating that the positive effects on acquirer banks dominate the negative effects on target banks. We also show that consolidated banks reduce employment, leading to an increase in lending and deposits per employee following consolidation.

To highlight the impacts of internal markets on these results, we use an approach similar to Cestone et al. (Reference Cestone, Fumagalli, Kramarz and Pica2023), which analyzes how firms use their local internal labor markets when economic conditions change. Reallocating a worker to a close branch is less costly than reallocating a worker to a distant branch. For instance, workers might demand higher wages to move to a distant location, or it might take time for them to acquire soft information about the customers in the market to which they are moving (Liberti and Petersen (Reference Liberti and Petersen2019)). As a result, internal labor markets are segmented geographically.

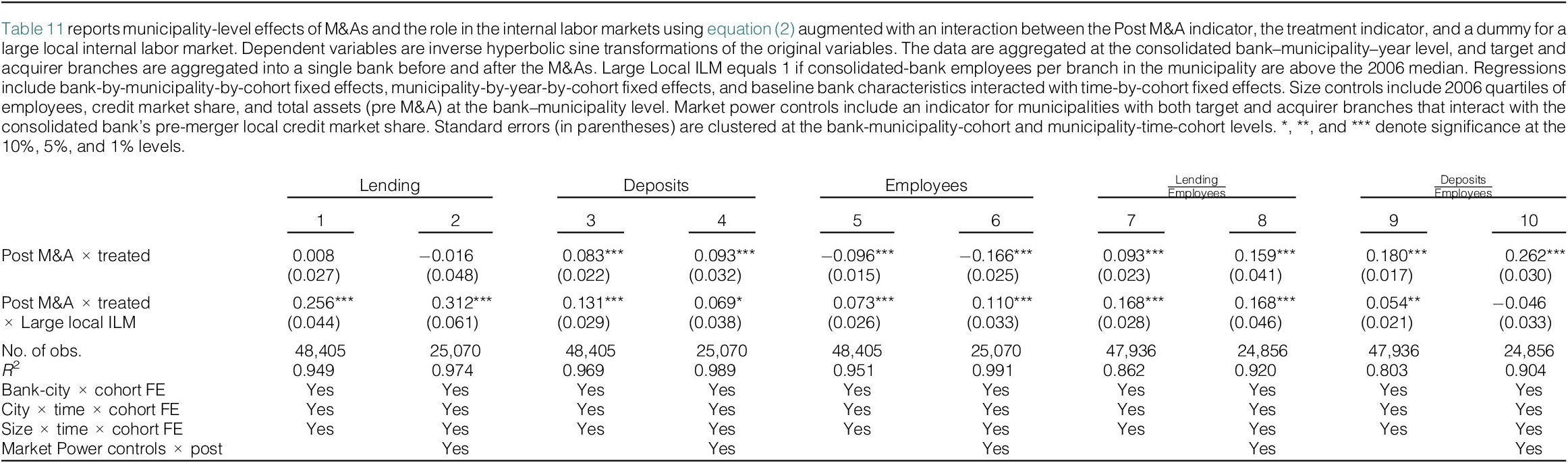

We create measures of the size of local internal labor markets using the boundaries of the municipalities in Brazil. By combining branches that operated independently, M&As lead to instant increases in the size of local internal labor markets. We create the dummy variable Large Local ILM that takes the value 1 if the number of employees per branch of treated branches in a given municipality is above the median. The intuition for this measure is that it is hard to reallocate workers when branches only have a few key employees who perform multiple functions and have a lot of branch-specific knowledge that is hard to transmit.Footnote 20 Treated banks in municipalities where the variable Large Local ILM takes the value 1 have 85 employees and five branches on average, whereas in municipalities where Large Local ILM takes the value 0; they have one branch and five employees on average.

In Table 11, we investigate whether the size of the internal markets affects service provision, labor allocation, and efficiency gains. Our results provide evidence that increases in lending productivity are twice as large in municipalities in which the banks had large internal labor markets (above the median number of employees per branch) (32.7% = 15.9% + 16.8%) compared to places where the consolidated bank had small internal labor markets (15.9%). For deposits, we find limited evidence that banks experience differential gains on deposit productivity on large ILM municipalities: estimates are small in magnitude and become statistically insignificant once we control for city–time fixed effects. This pattern suggests that productivity gains from consolidation associated with internal labor reallocation are concentrated on the lending side, consistent with our evidence that post-consolidation skill gains accrue to loan officers rather than to other employees. These results add to the literature by highlighting how internal local markets play a significant role in generating lending provision productivity gains during the restructuring process that follows M&A episodes.

Taken together, the results from this section show that consolidated banks increase lending and deposits but reduce employment, raising productivity per worker. These gains are concentrated in municipalities with larger local internal labor markets, where lending productivity roughly doubles, indicating that consolidation improves efficiency mainly through local labor reallocation.

IV. Identification, Dynamic Effects, and Robustness Checks

A. Dynamic Effects and Resource Reallocation

In this section, we report estimates from an augmented version of equation (1) that includes leads and lags of the treatment indicator to examine the dynamic effects of M&As on our main variables.Footnote 21 The goals of this exercise are twofold. First, by showing that treated and control branches followed similar trajectories pre-M&A, we alleviate concerns of selection into consolidation. For example, we show that, in comparison to control branches, acquirer branches are not becoming more productive in the years that precede the transaction. Second, even though our estimations take into account local market power gains prompted by the M&A episodes, the results could be driven by increases in market power at a more aggregate level, such as the size of the ATM and branch network, brand reputation, and safety. As these market power gains can be more timely exercised than restructuring gains, a gradual improvement in productivity variables is a further indication that restructuring gains are playing an important part.

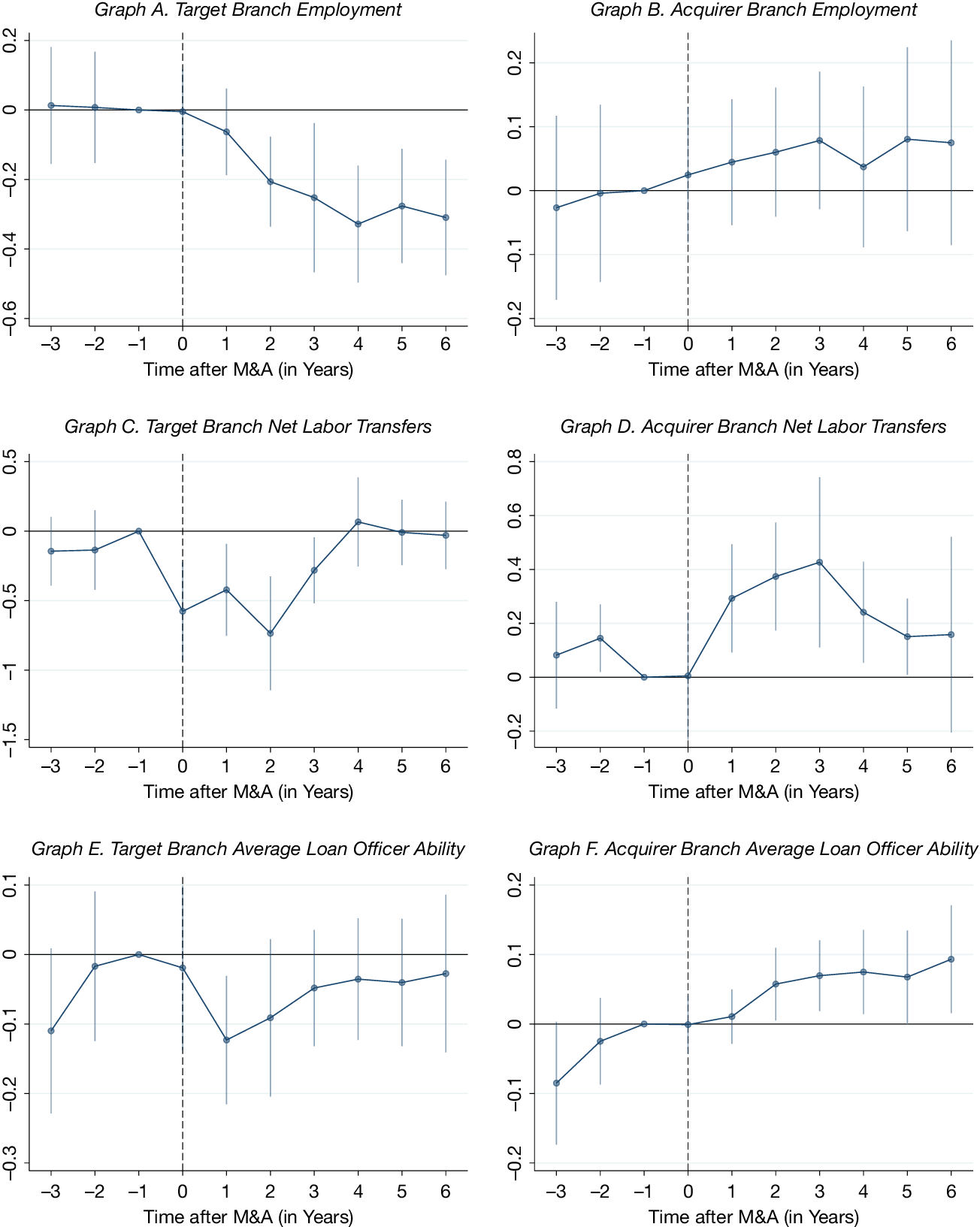

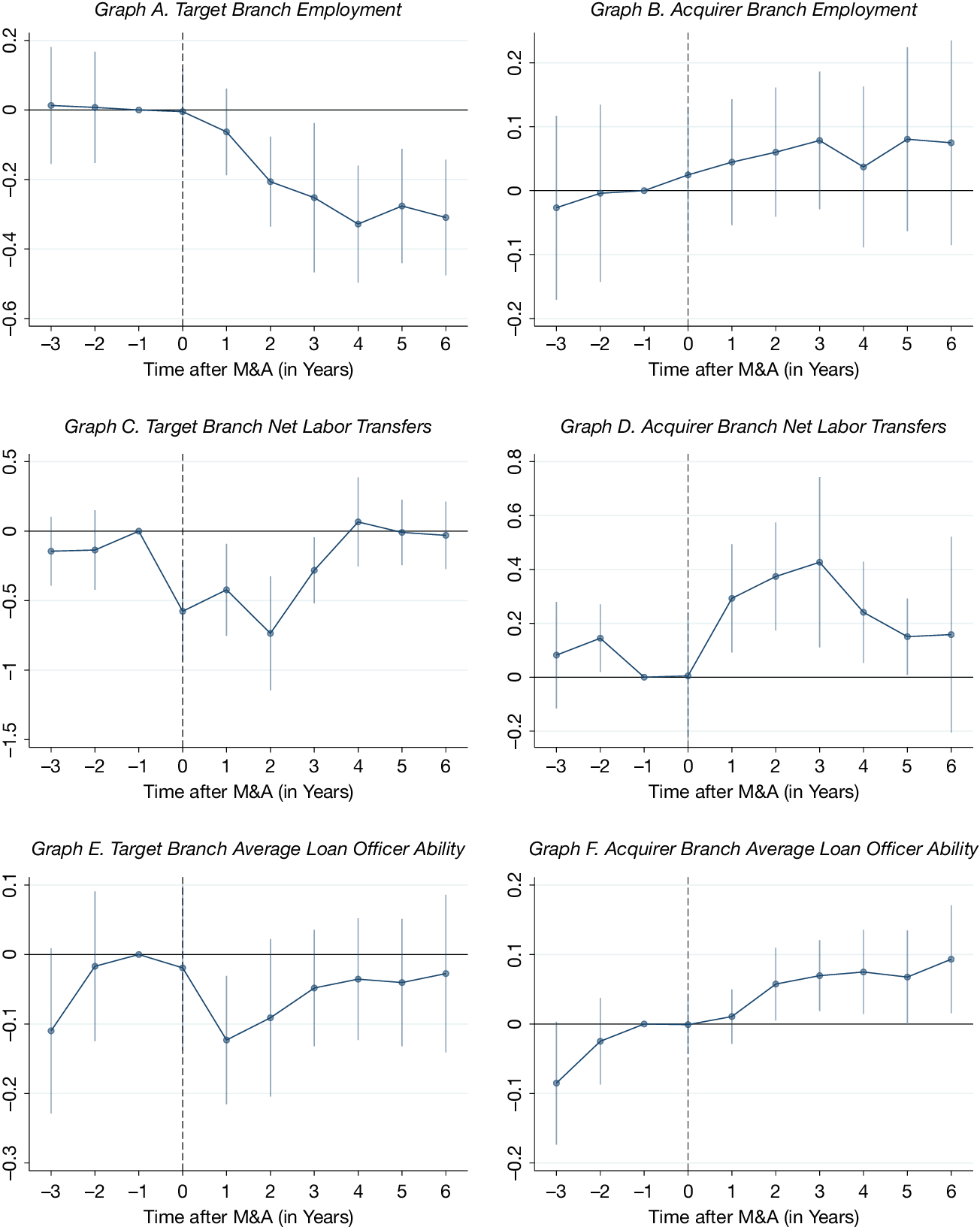

In Figure 2, we analyze the branches’ labor dynamics around the consolidation announcement. We observe that employment decreases slowly over the years in target branches, driven by the increased number of internal transfers of employees, which starts right after the announcement. At the same time, we see an increase in the number of employees in acquirer branches, which is consistent with the transfers from the target branches to acquirer branches. Moreover, we provide evidence that the loan officer’s ability increases in acquirer branches, and the dynamics of this change align with the dynamic effects of internal transfers. Additionally, our dynamic results show that in the long run, the loan officer’s ability in target branches remains unchanged.

Figure 2 reports the dynamic effects of M&As on labor reallocation, estimating an augmented version of equation (1) that includes leads and lags of the treatment indicator. Reported 99% confidence intervals are based on standard errors clustered at the branch-cohort and bank-time-cohort levels. Dependent variables are inverse hyperbolic sine transformations of the original variables. All regressions include branch-by-cohort fixed effects, municipality-by-year-by-cohort fixed effects, baseline branch characteristics interacted with time-by-cohort fixed effects, and market power controls interacted with the Post M&A indicator. The estimation sample includes branches that remained open throughout the estimation window (3 years before and 6 years after the events).

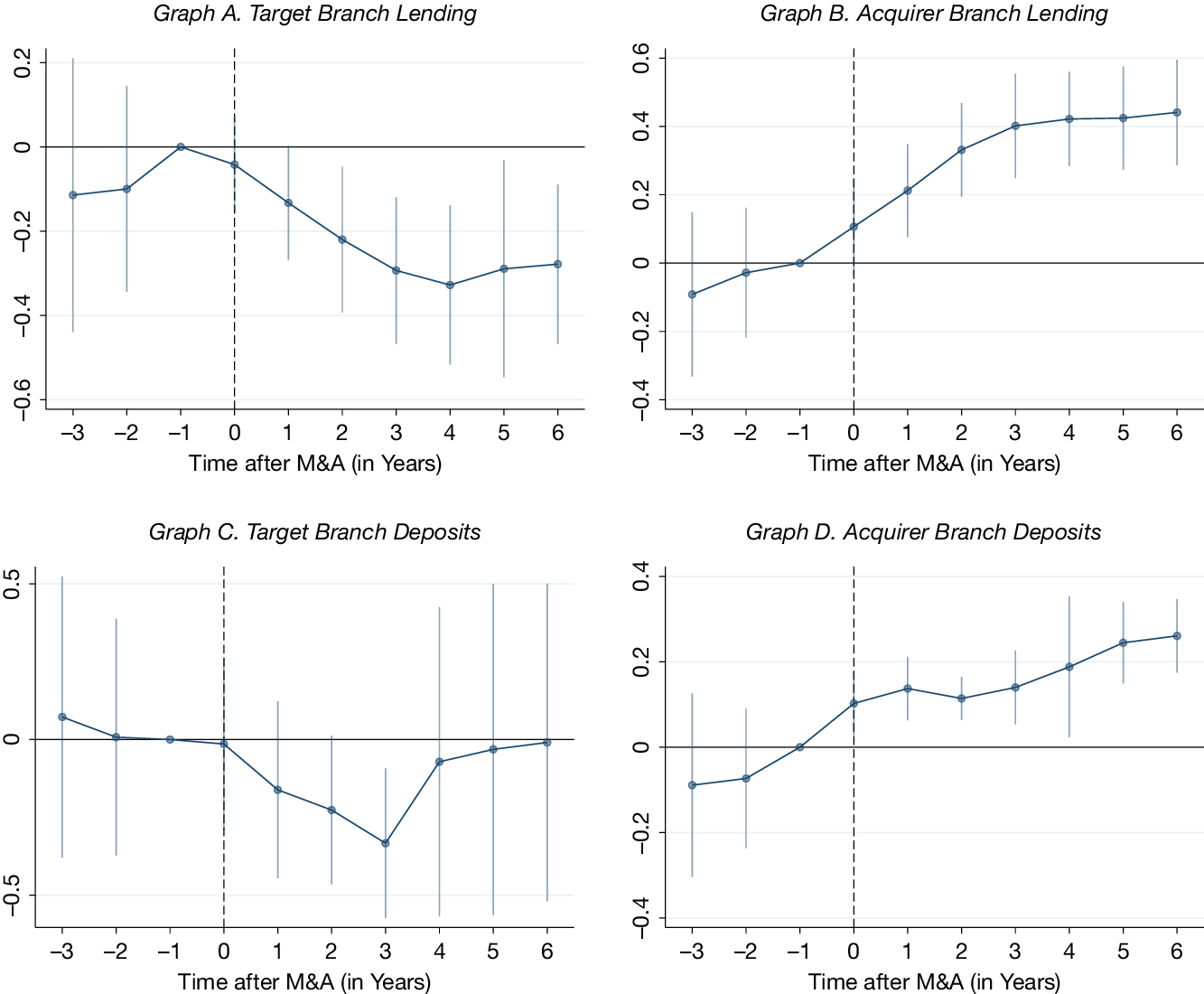

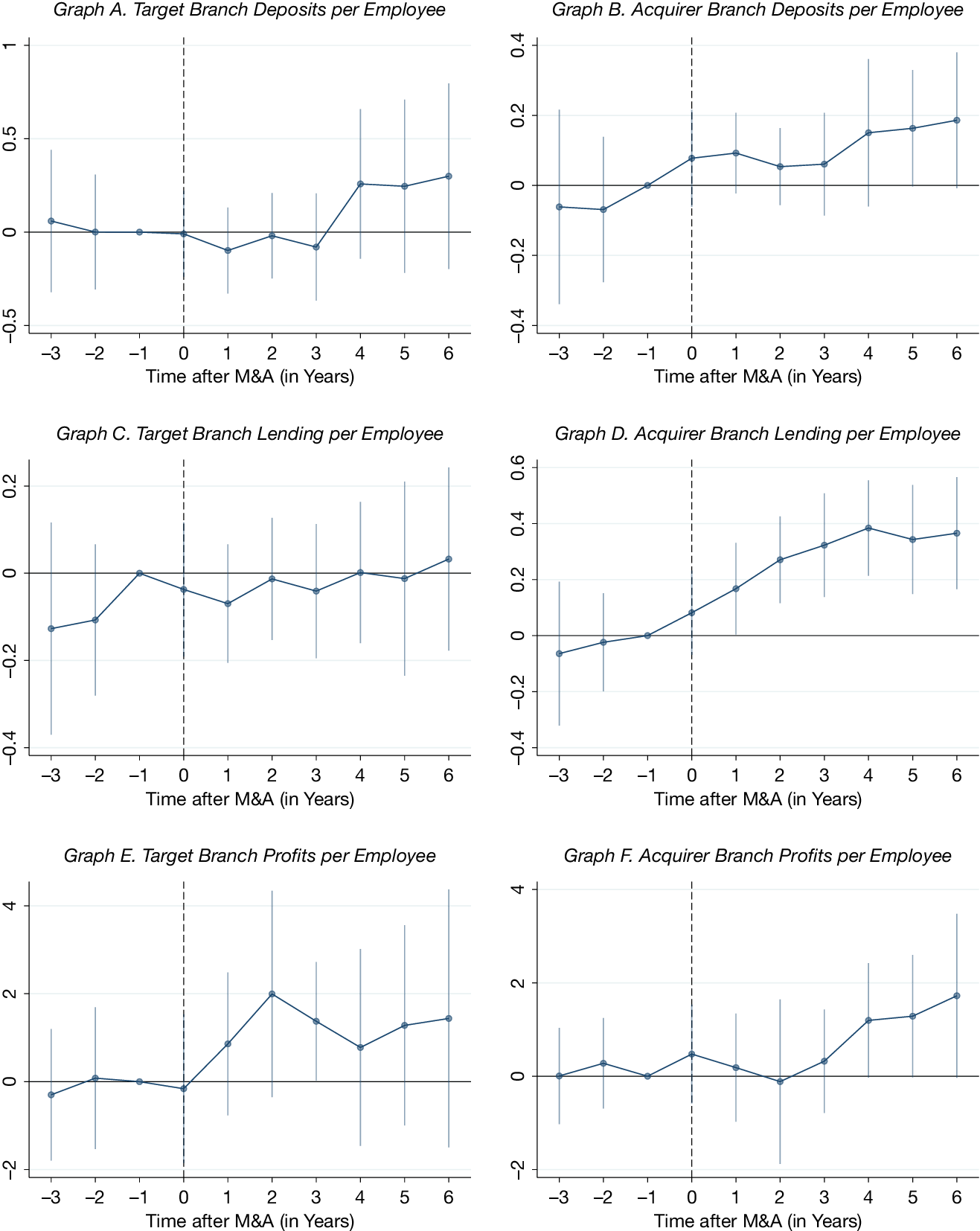

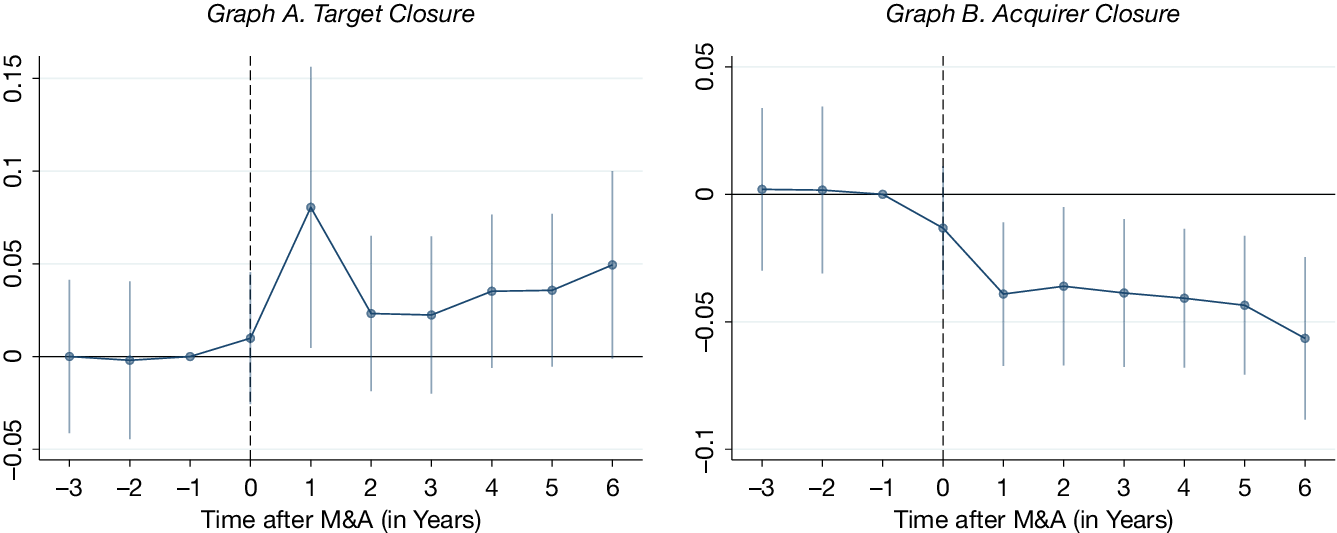

In Figure 3, we show that lending grows gradually after the event in acquirer branches, peaking at around 4 years after the M&A and remaining at this level thereafter. Lending declines gradually at target branches. These dynamic effects on lending supply are consistent with the changes in the labor force. In Figure 4, we show that increases in productivity take some years to materialize, supporting our hypothesis that M&A-driven resource reallocation is a driver of the observed productivity gains. Figure 5 shows the dynamics of the effects on branch closures, which are in line with previous results presented in Section III.C.

Figure 3 reports the dynamic effects of M&As on branch output, estimating an augmented version of equation (1) that includes leads and lags of the treatment indicator. Reported 99% confidence intervals are based on standard errors clustered at the branch-cohort and bank-time-cohort levels. Dependent variables are inverse hyperbolic sine transformations of the original variables. All regressions include branch-by-cohort fixed effects, municipality-by-year-by-cohort fixed effects, baseline branch characteristics interacted with time-by-cohort fixed effects, and market power controls interacted with the Post M&A indicator. The estimation sample includes branches that remained open throughout the estimation window (3 years before and 6 years after the events).

Figure 4 reports the dynamic effects of M&As on productivity, estimating an augmented version of equation (1) that includes leads and lags of the treatment indicator. Reported 99% confidence intervals are based on standard errors clustered at the branch-cohort and bank-time-cohort levels. Dependent variables are inverse hyperbolic sine transformations of the original variables. All regressions include branch-by-cohort fixed effects, municipality-by-year-by-cohort fixed effects, baseline branch characteristics interacted with time-by-cohort fixed effects, and market power controls interacted with the Post M&A indicator. The estimation sample includes branches that remained open throughout the estimation window (3 years before and 6 years after the events).

Figure 5 reports the dynamic effects of M&As on branch closures, estimating an augmented version of equation (1) that includes leads and lags of the treatment indicator. Reported 99% confidence intervals are based on standard errors clustered at the branch-cohort and bank-time-cohort levels. The dependent variable is a dummy equal to 1 if a branch has closed. All regressions include branch-by-cohort fixed effects, municipality-by-year-by-cohort fixed effects, baseline branch characteristics interacted with time-by-cohort fixed effects, and market power controls interacted with the Post M&A indicator.

B. Robustness Checks

We conduct robustness checks to assess the validity of the assumptions underlying our empirical strategy and the sensitivity of our results to alternative specifications.

First, in Table A2 in the Supplementary Material, we re-estimate our baseline specification excluding very large branches, which proxy for regional headquarters.Footnote 22 These establishments perform functions distinct from standard retail branches and may adjust differently following M&As. Moreover, as shown in Table 2, including these observations yields highly skewed distributions and large differences in magnitudes for several key variables, raising concerns that our baseline results may be partly driven by outliers. When we exclude these very large branches, the results remain essentially unchanged, confirming that our findings are not driven by regional headquarters or other exceptionally large establishments.Footnote 23

Second, to address concerns about differential growth paths between treated and control banks, we replicate our main results using alternative control groups and including additional controls. In Table A3 in the Supplementary Material, we include only branches of control banks that acted as acquirers in M&A deals after the period of our analysis, reducing concerns that control banks faced different trends. The estimates remain quantitatively similar to our baseline results.Footnote 24 Additionally, in Tables A4 and A5 in the Supplementary Material, we include baseline productivity measures interacted with cohort and time dummies as controls, with results again consistent with our main findings.

Third, we examine whether our controls for market power adequately account for competitive dynamics in local banking markets. In Table A6 in the Supplementary Material, we include changes in market power in deposit and labor markets, as well as in agricultural loans.Footnote 25 In Table A7 in the Supplementary Material, we control for changes in the Herfindahl–Hirschman Index induced by the M&A events. Across all specifications, our baseline results remain robust.

Fourth, given that the main analyses rely on branches that remain open throughout the estimation window and the abnormal pattern of branch closures that followed the M&As, we test if our results are mechanically driven by the transfer of lending and deposits from closed branches to surviving branches. In Table A8 in the Supplementary Material, we augment our baseline specification with controls for the pre-M&A share of loans and deposits associated with branches that subsequently closed, interacted with the post-M&A indicator. The results remain robust: acquirer branches expand lending, deposits, and profitability, while target branches contract. In Tables A9 and A10 in the Supplementary Material, we further restrict the sample to municipalities with no branch closures. Despite the smaller sample size, the results remain very similar to our baseline. Furthermore, we examine whether workers from closed branches contribute to the labor reallocation documented in Section III.A. Table A11 in the Supplementary Material shows that closed branches account for a nontrivial share of worker inflows at surviving target and acquirer branches. These results indicate that closures might also play a role in the restructuring process by generating fixed-cost savings through the elimination of redundant branches and by contributing to the reallocation of workers to surviving branches.

Fifth, we further probe the role of selective branch exit for our results by implementing tests similar to Lee (Reference Lee2009). As M&As trigger branch closures, one may worry that our estimates based on surviving branches overstate post-M&A improvements if poorly performing units are disproportionately closed. The Lee-bounds approach provides best- and worst-case estimates for treatment effects under monotonic selection by trimming the outcome distribution of surviving control branches so that treated and control groups are comparable. The resulting bounds, shown in Table A12 in the Supplementary Material, remain consistent with the sign and magnitude of our baseline estimates, suggesting that strong selection on branch survival would be required to overturn our main conclusions.

Sixth, we test the impact of alternative transformations of the outcome variables. While our baseline uses the inverse hyperbolic sine transformation to accommodate zero and negative values (Bellemare and Wichman (Reference Bellemare and Wichman2020)), Table A13 in the Supplementary Material replicates the main results using the log of the variable plus one. As this specification excludes negative-valued outcomes, we suppress profit regressions. The estimates remain quantitatively similar.

Seventh, to address potential spillovers in municipalities affected by multiple consolidations, we replicate our analysis excluding all municipalities treated in both the 2007 and 2008 M&A events. Table A14 in the Supplementary Material shows that, although the sample size is reduced by over 90% and confidence intervals widen, point estimates are consistent with the baseline. Notably, we observe insignificant changes in employment at acquirer branches and improvements in target productivity metrics, supporting the interpretation that reallocation of human capital is an important driver of productivity gains.

Eighth, the variable branch assets include certain categories that do not correspond to actual assets and therefore inflate the measure (see Section A3 of the Supplementary Material for details). In Table A15 in the Supplementary Material, we show that our results are robust to controlling for an adjusted measure of pre-consolidation assets. In Table A16 in the Supplementary Material, we further demonstrate that the results remain robust when this control is excluded altogether.

Finally, we evaluate the sensitivity of our results to violations of the parallel trends assumption using the methodology of Rambachan and Roth (Reference Rambachan and Roth2023). Specifically, we allow for differences in linear trends between treated and not-yet-treated units and assess how large such violations would have to be to overturn our conclusions. Figures A6–A8 in the Supplementary Material show that our significant results are robust to both linear and substantial non-linear deviations from parallel trends.Footnote 26

Overall, these robustness checks provide strong evidence that our main conclusions are not sensitive to branch closures, alternative control groups, violations of the parallel trends assumption, outcome transformations, potential spillovers, or market power measures.

V. Conclusion

This article sheds light on the role that resource reallocation plays in post-consolidation efficiency gains. We leverage detailed branch-level data on employees, balance sheets, and income statement items to show that banks reallocate labor across their branch network. We also provide evidence that these reallocations increase productivity and that the restructuring is heterogeneous across acquirer and target branches. While the productivity of acquirer branches increases as a result of higher levels of lending productivity, that of target branches increases due to cost-cutting.

Our results contribute to the buoyant literature that studies the ex post effects of M&As on productivity and consumer welfare. We show that the restructuring process is an essential contributor to productivity increases. As the financial firms in our sample have an extensive, geographically dispersed branch network, there is sizeable cross-sectional variation in increases in market share due to the consolidation. This fact allows us to control directly for increases in local market power, thereby reducing the likelihood that the observed productivity growth is attributed to higher markups or decreases in funding and labor costs. The extensive branch network further allows us to test how internal labor reallocation can enhance efficiency gains.

Overall, our article highlights a mechanism that is often ignored by the literature due to the lack of plant-level information: the effects of labor reallocation during consolidations. We show that this mechanism is essential to operational efficiency improvements after an M&A. Moreover, our results complement recent studies that emphasize the use of internal adjustments in response to changing economic conditions (Cestone and Fumagalli (Reference Cestone and Fumagalli2005), Cestone et al. (Reference Cestone, Fumagalli, Kramarz and Pica2023)). While our analysis focuses on the banking sector, the underlying mechanisms are likely to extend to other industries with multi-establishment firms, such as retail chains. Finally, our article contributes to the policy debate on the potential efficiency gains generated by consolidations in the financial industry and in other industries characterized by multi-establishment firms.

A venue for future research would be to study how technology adoption and changes in management practices during the consolidation process may interact with our reallocation channel and amplify its effects. Understanding these interactions could provide a more comprehensive picture of the factors driving post-M&A performance improvements.

Supplementary Material

To view supplementary material for this article, please visit http://doi.org/10.1017/S0022109026102786.

Open access

Open access